Brookfield Corporation: From Canadian Roots to Global Infrastructure Giant

Origins: The Brascan Story

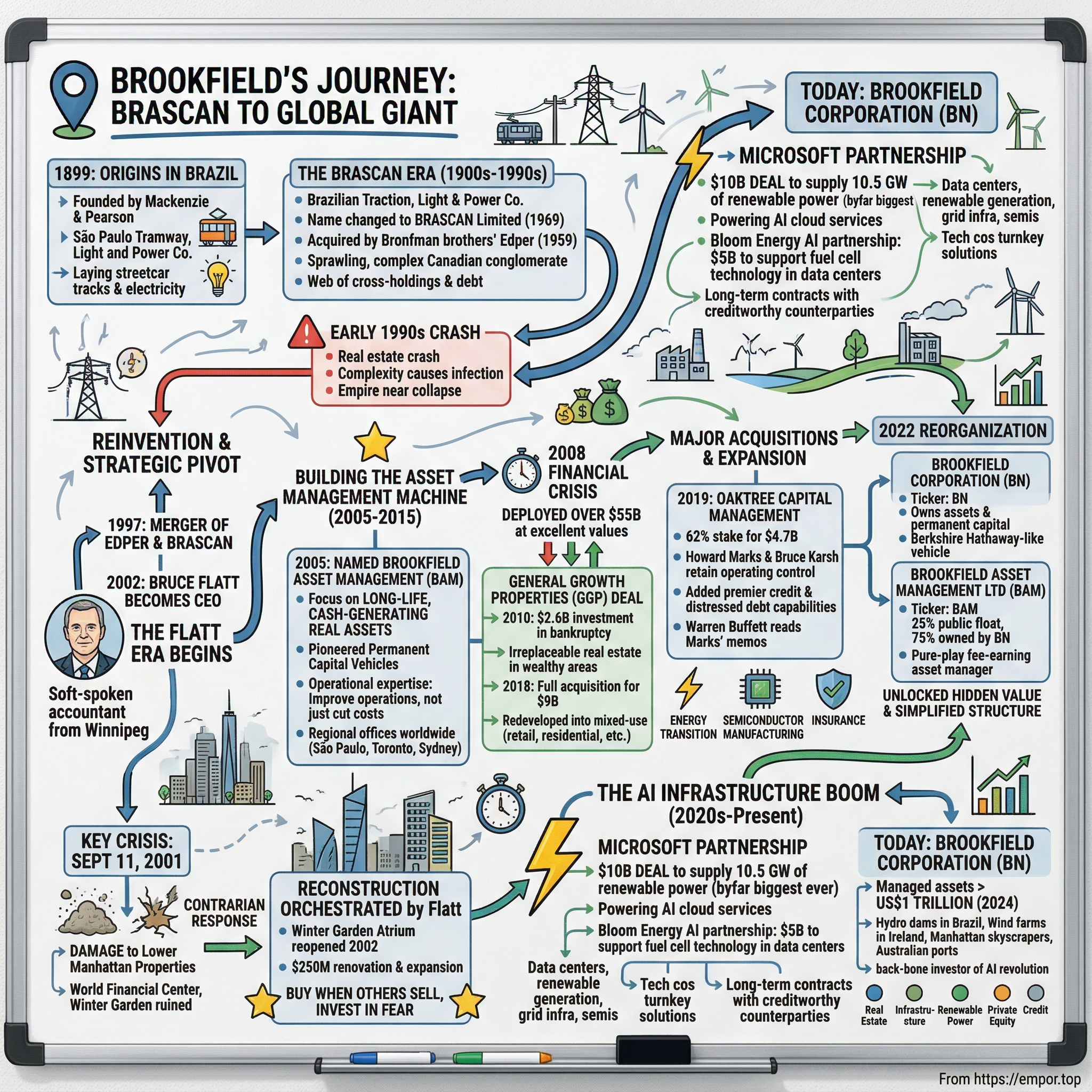

The muddy streets of São Paulo at the dawn of the 20th century seemed an unlikely birthplace for what would become a trillion-dollar investment empire. Yet it was here, in Brazil's burgeoning commercial capital, that the seeds of Brookfield Corporation were first planted. The company was founded in 1899 as the São Paulo Tramway, Light and Power Company by William Mackenzie and Frederick Stark Pearson. It operated in the construction and management of electricity and transport infrastructure in Brazil.

William Mackenzie wasn't your typical Victorian-era entrepreneur. A Scottish-Canadian railway contractor who had already made his fortune building Canada's transcontinental railroad, Mackenzie saw opportunity where others saw impossibility. Brazil in 1899 was a newly minted republic, having abolished its monarchy just a decade earlier. São Paulo, though growing rapidly on coffee wealth, still relied on mule-drawn trolleys for public transportation. The city's elite traveled in private carriages while the working class trudged through unpaved streets that turned to rivers of mud during the rainy season.

Alexander Mackenzie, a Toronto lawyer, and Frederick Pearson, an engineer with the Metropolitan Street Railway in New York, formed the São Paulo Railway, Light & Power Company in Toronto on 7 April 1899. When Mackenzie and Pearson began laying rails in the streets of São Paulo on 5 July 1899, a bitter dispute arose with the Companhia Viação Paulista. Souza and Gualco finally sold their electrification rights to the Canadians, but legal battles and street fights continued until SPTL&P bought the mulecar company on 17 July 1901. The early days were marked by literal street fights between workers of competing companies, with local newspapers documenting pitched battles over who had the right to lay tracks on particular streets.

The transformation was swift and dramatic. The first six Brill cars arrived in December and the first electric streetcar line in São Paulo, between Largo São Bento and Barra Funda, was inaugurated on 7 May 1900. Suddenly, journeys that took an hour by mule car could be completed in fifteen minutes. The electric lights that powered the overhead wires turned São Paulo's main thoroughfares into beacons of modernity. Within five years, the company had expanded beyond streetcars to provide electric power to factories, reshaping São Paulo's industrial landscape.

In 1904, the Rio de Janeiro Tramway, Light and Power Company was founded by Mackenzie's group. In 1912, Brazilian Traction, Light and Power Company was incorporated in Toronto as a public company to develop hydro-electric power operations and other utility services in Brazil, becoming a holding company for São Paulo Tramway Co. and Rio de Janeiro Tramway Co. This consolidation created one of the largest foreign-owned utilities in Latin America, controlling everything from streetcars to telephone lines in Brazil's two largest cities.

The company's Brazilian operations thrived for decades, becoming so integral to daily life that Brazilians simply referred to it as "Light" – the English word becoming part of Portuguese vernacular. By the 1960s, the company provided electricity to millions of Brazilians and operated one of the world's largest urban transit systems. However, political winds were shifting. Brazil's military government, which had taken power in 1964, increasingly viewed foreign control of essential utilities as a threat to national sovereignty.

In 1966, Brazilian Traction, Light and Power Company changed its name to Brazilian Light and Power Company, and again in 1969, changed its name to Brascan Limited. Brascan is a portmanteau of "Brasil" and "Canada". During the 1970s, the company began to sell its Brazilian interests, and invested more heavily in industries such as real estate, timber and mining. The name change to Brascan represented more than cosmetic rebranding – it signaled a fundamental strategic pivot away from Latin American utilities toward North American real assets.

Enter the Bronfman brothers. In 1959, Edper Investments, founded by brothers Peter and Edward Bronfman, acquired Brazilian Traction, Light and Power Company for $15 million. Peter and Edward were the "other" Bronfmans – cousins to Samuel Bronfman who built the Seagram liquor empire. While their cousins dominated Montreal's social scene with their whiskey fortune, Peter and Edward quietly built their own empire through Edper Investments, named after their combined first names.

The Bronfman era at Brascan was characterized by aggressive expansion and increasing complexity. Through the 1970s and 1980s, Edper-Brascan became the center of a sprawling web of Canadian companies. They acquired everything from trust companies to mining operations, from real estate to consumer products. The structure became Byzantine in its complexity – companies owned pieces of other companies that owned pieces of the first companies, creating circular ownership patterns that even seasoned analysts struggled to untangle.

By the early 1990s, the Edper-Brascan empire encompassed over 550 companies with combined revenues exceeding $30 billion. The corporate structure resembled a plate of spaghetti more than an organizational chart. Companies like Trilon Financial, Hees International, and Carena Developments formed an intricate web of cross-holdings. This complexity served a purpose – it allowed the Bronfmans to control vast assets with relatively small equity stakes, using multiple layers of holding companies to maintain voting control while raising external capital.

But complexity became the empire's Achilles heel. When real estate markets crashed in the early 1990s, the interconnected structure meant problems in one company quickly infected others. Banks that had happily lent against inflated real estate values suddenly wanted their money back. The same leverage that had amplified returns during good times now threatened to destroy the entire structure.

The current Brookfield Corporation is the creation of the 1997 merger of Edper and Brascan. At its inception, the company was known as EdperBrascan, then changed its name to Brascan in 2000, and Brookfield Asset Management in 2005. The merger represented both an ending and a beginning – the end of the Bronfman era and the start of something entirely new. The company that emerged from this crucible would be shaped by the hard lessons of the 1990s: the dangers of excessive complexity, the importance of transparent structures, and above all, the value of patient, contrarian capital.

Standing in the wreckage of the Edper empire was a young executive who had joined Brascan in 1990, just as the troubles were beginning. Bruce Flatt joined Brookfield in 1990 and became CEO in 2002. Few could have predicted that this soft-spoken accountant from Winnipeg would transform the company into one of the world's most powerful investment firms. But first, he would have to navigate the company through its darkest hour – and in doing so, discover the investment philosophy that would define Brookfield's future.

The Bruce Flatt Era Begins

Bruce Flatt never intended to become one of the most powerful people in global finance. Flatt, whose father was an executive at a Manitoba mutual fund company, was born in Canada in 1965. Following university, Flatt worked as a chartered accountant at Clarkson Gordon. Growing up in Winnipeg, Manitoba – a prairie city known more for harsh winters than high finance – Flatt embodied the understated Canadian style that would later become his trademark. He was educated at Grant Park High School and studied at the University of Manitoba, earning his accounting designation before age 25.

The young accountant's career might have followed a predictable path through Canada's corporate establishment, but fate intervened when he joined Brascan in 1990, just as the company's elaborate structure was beginning to unravel. Flatt was 25 years old, ambitious but unproven, thrust into a company facing existential crisis. Real estate values were collapsing, credit was evaporating, and the Edper-Brascan empire – once the pride of Canadian business – was crumbling.

What Flatt witnessed during those early years would shape his entire investment philosophy. He watched as highly leveraged companies failed not because their underlying assets were worthless, but because they couldn't survive the liquidity crisis. He saw how complexity bred confusion, how financial engineering could obscure fundamental value, and how market psychology could swing from irrational exuberance to paralyzing fear in a matter of months. These lessons would prove invaluable when, a decade later, he would face his first major test as a leader.

The morning of September 11, 2001, started like any other for Brookfield Properties, where Flatt had recently been appointed CEO. The company owned several premier office buildings in Lower Manhattan through its World Financial Center complex. Then American Airlines Flight 11 struck the North Tower at 8:46 AM, followed seventeen minutes later by United Airlines Flight 175 hitting the South Tower. The world changed in an instant, and with it, the fate of Brookfield's Manhattan properties.

The devastation to Brookfield's holdings was severe. During the September 11 attacks, debris severely damaged the lobby and lower floors' granite cladding and glass. It has since been fully restored and significant repairs were made to the other buildings in the complex. The Winter Garden, Brookfield's crown jewel – a soaring glass pavilion that served as a public space and cultural venue – was effectively destroyed. Debris from the collapsing towers had torn through the structure like shrapnel, leaving twisted metal and shattered glass where once stood one of Manhattan's most elegant spaces.

Flatt's response to the crisis revealed the leadership style that would define his tenure. Rather than managing from Toronto, he immediately flew to New York and established a command center in temporary offices. He personally walked through the damaged buildings, met with shell-shocked employees, and began planning not just recovery but renewal. While other landlords were questioning whether anyone would ever want to work in Lower Manhattan again, Flatt was already envisioning how to rebuild better than before.

The contrarian instincts that would become Brookfield's hallmark were on full display. As competitors fled Lower Manhattan and property values plummeted, Flatt saw opportunity. He pushed forward with the $250 million renovation while simultaneously looking for distressed properties to acquire. His reasoning was simple but powerful: Manhattan had survived worse, quality assets in prime locations would always have value, and the best time to invest was when others were too frightened to act.

Often dubbed "Canada's Warren Buffett" in the media for his value-investing approach, Flatt transformed Brookfield from a somewhat opaque conglomerate into a focused, global asset manager. The Buffett comparison wasn't just about investment philosophy – it extended to personal style. Like the Oracle of Omaha, Flatt eschewed Wall Street flash for substance. He lived modestly despite his growing wealth, flew commercial rather than private, and was known for reading annual reports on weekends rather than attending society galas.

But there were key differences that would define Flatt's unique approach. While Buffett typically bought minority stakes in public companies, Flatt preferred control positions in real assets. Where Buffett avoided turnarounds, Flatt actively sought distressed situations where Brookfield's operational expertise could create value. And while Buffett's Berkshire Hathaway remained essentially an American company, Flatt harbored global ambitions from the start.

In 2002, Bruce Flatt was appointed CEO of Brascan. His appointment came at a crucial juncture. The company had survived the 1990s crisis but remained a complex amalgamation of assets ranging from mining to financial services. Flatt's first priority was simplification. He began methodically selling non-core assets, using the proceeds to reduce debt and invest in the sectors where Brookfield had genuine competitive advantages: real estate, infrastructure, and renewable power.

The strategy was deceptively simple but revolutionary for a company with Brascan's conglomerate history. Instead of trying to be everything to everyone, Brookfield would focus on long-life, cash-generating real assets. These assets – office buildings, power plants, toll roads – had several attractive characteristics: they generated stable cash flows, their values generally kept pace with inflation, and most importantly, they required operational expertise to manage effectively.

This operational focus became Brookfield's secret weapon. While financial buyers could lever up assets and cut costs, Brookfield could actually improve operations. They could make power plants run more efficiently, increase occupancy in office buildings, optimize toll road pricing. This operational value-add meant Brookfield could pay more for assets than pure financial buyers while still generating superior returns.

Bruce Flatt was named CEO of the Year by The Globe and Mail in 2017, 60th in a list of the top 100 best-performing CEOs published by Harvard Business Review in 2018, and one of Bloomberg's 50 people who defined global business in 2019. These accolades reflected not just financial success but a fundamental reimagining of what an asset manager could be. Under Flatt's leadership, Brookfield was pioneering a new model – part private equity firm, part infrastructure operator, part permanent capital vehicle.

The transformation wasn't without skeptics. Traditional private equity firms questioned whether Brookfield could generate adequate returns without high leverage. Public market investors struggled to value a company that was part asset manager, part owner-operator. Rating agencies worried about the complexity of Brookfield's structure, even after the simplification efforts. But Flatt remained focused on a simple metric: long-term compound returns.

Brookfield is a value investor with a track record of delivering 15%+ annualized returns to shareholders for over 30 years, supported by deep investment and operational expertise. This track record wasn't built on any single brilliant trade or lucky timing, but rather on consistent application of contrarian principles: buy when others are selling, improve operations rather than just financial engineering, and hold for the long term rather than flipping quickly.

The philosophy crystallized into what Brookfield employees call the "herd off the cliff" mentality. Every Brookfield office around the world displays the same image: a photograph of sheep blindly following each other off a cliff. It's a daily reminder that the best opportunities arise when conventional wisdom is wrong, when the market's consensus view creates mispricings, when fear or greed pushes valuations to extremes.

Flatt is married to art collector Lonti Ebers, who is the founder of a non-profit organization, Amant, and a trustee and patron of New York City's Museum of Modern Art. This connection to the art world provided another lens through which Flatt viewed investing. Like acquiring art, building a real asset portfolio required patience, taste, and the ability to see value that others might miss. It also required the confidence to hold positions for years or decades, allowing their true worth to be realized over time.

Flatt lives in London and New York City, splitting his time between Brookfield's major offices. This global perspective became increasingly important as Brookfield expanded beyond North America. Flatt could see firsthand how infrastructure needs in Europe differed from those in Asia, how renewable energy policies in Australia created different opportunities than those in Brazil. This global outlook would prove crucial as Brookfield built one of the world's first truly international infrastructure platforms.

By the mid-2000s, the transformation was gaining momentum. The renamed Brookfield Asset Management was shedding its conglomerate past and emerging as a focused alternative asset manager. But Flatt's ambitions extended far beyond simply cleaning up the company's structure. He envisioned Brookfield as something unprecedented: a permanent capital vehicle that could invest like a private equity firm but hold like Berkshire Hathaway, that could operate assets like an industrial company but allocate capital like an investment firm.

Achieving this vision would require building something the investment world had never seen before – an asset management machine that could raise capital from the world's largest institutions while maintaining the patience and contrarian discipline of a value investor. The next decade would test whether this audacious model could work at scale.

Building the Asset Management Machine (2005-2015)

In September 2005, after 37 years, Brascan Corp. was renamed to Brookfield Asset Management Inc. The name change was more than cosmetic rebranding – it signaled a fundamental transformation in how the company would create value. No longer would Brookfield simply be an owner of assets; it would become a manager of capital for the world's largest institutions, pioneering a model that would reshape the entire alternative investment industry.

The timing of this transformation was no accident. The mid-2000s represented a unique moment in financial history. Pension funds worldwide were struggling with underfunded liabilities as people lived longer and traditional fixed-income investments yielded less. These institutions desperately needed higher returns but couldn't stomach the volatility of public equities. Infrastructure and real assets offered a solution: stable, inflation-linked cash flows with equity-like returns. The only problem was that most pension funds lacked the expertise to invest directly in power plants or ports.

Flatt recognized this gap and positioned Brookfield to fill it. But rather than following the traditional private equity model of raising closed-end funds with 10-year lives, Brookfield pioneered something different: permanent capital vehicles. These listed partnerships – Brookfield Infrastructure Partners, Brookfield Renewable Partners, Brookfield Property Partners – would trade on public exchanges but invest like private funds. They offered institutions liquidity when needed but encouraged long-term holding through stable, growing distributions.

The structure was brilliant in its simplicity. Brookfield Asset Management would serve as the general partner, earning management fees on the capital while maintaining control with a minority economic interest. The limited partners – both institutional and retail investors – would receive most of the cash flows but rely on Brookfield's operational expertise. This alignment of interests meant Brookfield only prospered when its investors did, creating a powerful incentive for long-term value creation.

Then came 2008, and with it, the greatest test of Flatt's contrarian philosophy. As Lehman Brothers collapsed and credit markets froze, the conventional wisdom was to hoard cash and wait for the storm to pass. Brookfield did the opposite. The company had maintained a strong balance sheet precisely for moments like this, and now Flatt deployed capital with conviction. In total, we invested over $55 billion at excellent values in 2023, and we expect to reap the rewards of these contrarian investments for years to come – but it was during the 2008-2009 crisis that this contrarian approach was truly forged.

The shopping list was extraordinary. Brookfield acquired distressed real estate from overleveraged developers, purchased infrastructure assets from governments desperate for cash, and bought renewable power facilities from utilities under financial pressure. Each acquisition followed the same pattern: high-quality assets available at distressed prices because their owners couldn't survive the liquidity crisis. Brookfield's permanent capital advantage meant it could be patient while others were forced sellers.

One particularly illustrative deal involved General Growth Properties, then the second-largest mall owner in America. As the financial crisis deepened, GGP faced a brutal combination of plummeting property values and maturing debt it couldn't refinance. Despite owning some of America's premier shopping centers – properties generating substantial cash flow – the company was forced into bankruptcy in April 2009. It was the largest real estate bankruptcy in American history.

In February 2010, Brookfield Asset Management made a $2.625 billion equity investment in the company during bankruptcy. While others saw a dying mall company, Brookfield saw irreplaceable real estate in America's wealthiest suburbs. The investment thesis was straightforward: the properties were worth far more than the distressed price, the bankruptcy would allow for debt restructuring, and Brookfield's operational expertise could improve performance. Over the next eight years, as GGP recovered and retail real estate values normalized, Brookfield's investment generated exceptional returns, setting the stage for the full acquisition in 2018.

But Brookfield's evolution during this period went beyond opportunistic acquisitions. The company was systematically building capabilities that would differentiate it from traditional asset managers. While BlackRock managed paper assets and Blackstone focused on leveraged buyouts, Brookfield was creating something unique: an operational platform that could actually run the assets it acquired.

This meant hiring differently. Instead of just financial analysts and deal-makers, Brookfield recruited power plant operators, construction managers, and property developers. The company built regional offices not just in financial centers but in operating locations – São Paulo for Brazilian hydroelectric facilities, Toronto for Canadian infrastructure, Sydney for Australian utilities. This operational depth meant Brookfield could underwrite investments others couldn't, seeing value creation opportunities that pure financial buyers would miss.

The infrastructure platform exemplified this approach. While other investors saw toll roads as simple bond substitutes – stable cash flows with modest growth – Brookfield recognized they were operating businesses that could be optimized. By implementing dynamic pricing, improving traffic flow, adding electronic tolling, and developing adjacent land, Brookfield could dramatically increase cash flows from mature assets. This operational value-add justified paying premium prices in competitive auctions while still generating superior returns.

Similarly, in renewable power, Brookfield didn't just buy wind farms and solar panels. The company assembled one of the world's largest renewable development platforms, with expertise spanning site selection, permitting, construction management, and power marketing. This integrated capability meant Brookfield could develop projects from greenfield to operation, capturing value at each stage rather than simply buying completed assets.

The financial crisis also taught Brookfield about the importance of multiple funding sources. While competitors relied heavily on bank debt that could disappear in a crisis, Brookfield cultivated diverse funding channels. The company issued long-term corporate bonds, created asset-backed securities, partnered with sovereign wealth funds, and maintained strong banking relationships globally. This funding diversity would prove crucial during future volatility.

By 2010, the transformation was evident in the numbers. Assets under management had grown from $50 billion in 2002 to over $100 billion. More importantly, the quality of these assets had improved dramatically. Instead of a confused collection of legacy holdings, Brookfield now owned premier infrastructure, top-tier office buildings, and large-scale renewable power facilities. The company had also proven its contrarian investment philosophy worked at scale, generating exceptional returns by investing when others retreated.

The institutionalization of Brookfield's investment process was another crucial development during this period. The company created a rigorous investment committee structure, with multiple layers of review for major decisions. Every investment had to meet strict criteria: it had to be a high-quality asset, available at a value price, within Brookfield's operational expertise, and capable of generating stable cash flows. This disciplined approach meant Brookfield walked away from far more deals than it pursued, maintaining selectivity even as capital available for deployment grew.

The human capital strategy was equally important. Flatt instituted a partnership culture where senior employees were required to invest meaningful personal capital alongside institutional investors. This skin-in-the-game approach aligned interests and attracted entrepreneurs who thought like owners rather than employees. The company also emphasized long-term career development, rotating high-potential employees through different platforms to build broad expertise.

Technology, often overlooked in real asset investing, became another differentiator. Brookfield invested heavily in systems to monitor and optimize asset performance. Smart meters in buildings tracked energy usage in real-time. Predictive analytics identified maintenance needs before equipment failed. Digital platforms streamlined property management across global portfolios. These technological capabilities improved operations while reducing costs, creating value invisible to traditional financial statements.

The cultural transformation was perhaps most significant. The old Brascan had been a top-down conglomerate where division heads protected their turf. The new Brookfield emphasized collaboration across platforms, with infrastructure executives sharing insights with real estate teams, renewable power experts advising on property energy efficiency. This cross-pollination created synergies that pure-play competitors couldn't match.

By 2015, Brookfield had achieved something remarkable: it had built an asset management franchise generating billions in fee revenue while maintaining operational excellence across diverse global platforms. The company managed over $200 billion for hundreds of institutional investors while operating thousands of real assets employing hundreds of thousands of people. It was a scale and scope unprecedented in alternative asset management.

But success brought new challenges. Institutional investors increasingly demanded larger check sizes, forcing Brookfield to pursue ever-bigger deals. Competition intensified as other firms recognized the attractiveness of real assets. And most fundamentally, Brookfield's complex structure – part asset manager, part operator, with multiple listed vehicles – confused public market investors who struggled to value the company appropriately.

These challenges would drive the next phase of Brookfield's evolution: massive acquisitions that would test its operational capabilities, expansion into new asset classes that would broaden its platform, and ultimately, a corporate restructuring that would attempt to unlock hidden value. The contrarian philosophy that had served Brookfield well during the financial crisis would soon be tested again, this time in the retail apocalypse.

Major Acquisitions: GGP - The Mall Gamble (2018)

The American mall in 2017 was supposedly dying. Amazon was devouring retail, department stores were declaring bankruptcy monthly, and analysts predicted that hundreds of malls would close within five years. The phrase "retail apocalypse" dominated headlines, and mall REITs traded at massive discounts to asset value. It was, in other words, exactly the kind of situation that attracted Bruce Flatt's attention.

General Growth Properties owned 125 malls across 40 states, including some of America's most productive retail properties: Ala Moana Center in Honolulu, Water Tower Place in Chicago, and The Grand Canal Shoppes in Las Vegas. But GGP's stock price reflected none of this quality. Years of retail pessimism had pushed shares down to levels implying the company's malls were worth less than replacement cost – in many cases, less than the land alone was worth.

Brookfield's history with GGP stretched back to the financial crisis. In February 2010, Brookfield Asset Management made a $2.625 billion equity investment in the company during bankruptcy, helping rescue GGP from the largest real estate bankruptcy in American history. That investment had generated exceptional returns as GGP recovered, giving Brookfield intimate knowledge of the portfolio. By 2017, Brookfield owned approximately 34% of GGP and saw an opportunity to acquire the rest at a compelling valuation.

The first approach came in November 2017. Brookfield offered $23 per share, valuing GGP at approximately $14.8 billion. The proposal was elegant in its structure: GGP shareholders could choose cash or units in Brookfield Property Partners, allowing them to exit or maintain exposure to retail real estate. But GGP's independent directors, advised by Goldman Sachs, rejected the offer as inadequate. They believed Brookfield was trying to steal the company at the bottom of the retail cycle.

What followed was a masterclass in patient, disciplined acquisition strategy. Rather than launching a hostile takeover or walking away in frustration, Brookfield spent months refining its proposal. Flatt personally engaged with GGP's special committee, explaining Brookfield's vision for the properties. The message was consistent: while others saw dying malls, Brookfield saw irreplaceable real estate in wealthy communities that could be transformed for the digital age.

Brookfield Property Partners announced Monday it finally reached a deal to buy mall operator General Growth Properties for $9.25 billion in cash. Brookfield already owns roughly one third of GGP. The final agreement, announced in March 2018, valued GGP at $23.50 per share – only slightly higher than the original offer, but structured to provide more cash to shareholders who wanted immediate liquidity.

The acquisition thesis revealed Brookfield's contrarian thinking at its finest. While conventional wisdom focused on declining mall traffic and store closures, Brookfield saw several factors others missed. First, the best malls – those in affluent areas with experiential offerings – were actually thriving. These "A-class" properties saw increasing sales per square foot as they became social destinations rather than just shopping venues.

Second, the real estate itself had enormous alternative use potential. Many GGP malls sat on dozens of acres in prime suburban locations, often near transit and surrounded by wealthy residential neighborhoods. These sites could be partially redeveloped into mixed-use properties combining retail, residential, office, and entertainment. The land value alone often exceeded the market's valuation of the operating mall.

Third, the retail transformation created opportunities for active management. As traditional department stores closed, Brookfield could reclaim that space for more productive uses: fitness centers, restaurants, entertainment venues, medical offices, or even fulfillment centers for the same e-commerce companies supposedly killing malls. This flexibility to reimagine space was exactly the kind of operational value-add that distinguished Brookfield from passive landlords.

On August 28, 2018, GGP was acquired by Brookfield Property Partners and management of its former portfolio was transferred to its Brookfield Properties subsidiary for $9 billion in cash. Brookfield Property Partners L.P. announced today that it has completed its acquisition of GGP Inc.. The closing represented one of the largest retail property transactions in history, executed at a time when most investors were fleeing the sector.

The integration strategy was methodical and focused. Rather than dramatic restructuring, Brookfield emphasized operational improvements. Property management was consolidated to achieve economies of scale. Leasing was centralized to negotiate better terms with national tenants. Capital allocation was optimized, investing heavily in the best properties while selling or redeveloping weaker assets.

The transformation of specific properties illustrated Brookfield's approach. At Stonestown Galleria in San Francisco, Brookfield partnered with developers to add 3,500 residential units, transforming a traditional mall into a mixed-use community. At Fashion Show in Las Vegas, investments in luxury retail and dining created a destination that competed with casino properties. At Ala Moana in Honolulu, expansion into experiential retail and entertainment made it Hawaii's gathering place.

Upon closing the acquisition, Brookfield immediately sold a 49% interest in each of three former GGP super-regional malls to CBRE Group, and a 49% interest in three other former GGP malls to TIAA subsidiary Nuveen, seeking additional joint ventures for its newly-acquired malls. These partnerships validated Brookfield's thesis – sophisticated institutional investors saw value in quality retail properties at the right price. The joint ventures also provided immediate capital recovery, reducing Brookfield's net investment while maintaining control and management fees.

But the GGP acquisition wasn't without challenges. The retail environment continued deteriorating, with store closures accelerating through 2018 and 2019. Some analysts accused Brookfield of catching a falling knife, buying into a structurally declining sector. The COVID-19 pandemic in 2020 seemed to validate these concerns, forcing temporary mall closures and accelerating e-commerce adoption.

Yet Brookfield's patient capital approach and operational expertise proved their worth. The company had underwritten conservative scenarios assuming continued store closures and declining rents. The balance sheet was structured to weather downturns without forced asset sales. Most importantly, Brookfield had the capital and expertise to reimagine properties for post-pandemic uses, accelerating mixed-use development and alternative tenant strategies.

By 2021, the wisdom of the contrarian bet was becoming apparent. The best malls saw traffic rebound sharply as consumers returned to physical retail for experiences e-commerce couldn't provide. Retail sales at Brookfield's premier properties exceeded pre-pandemic levels. Development projects launched during the downturn began generating returns. And perhaps most importantly, the acquisition had given Brookfield control of irreplaceable real estate in America's wealthiest communities – assets whose value would only appreciate over time.

The GGP acquisition exemplified everything that made Brookfield unique: the patience to pursue complex transactions over months or years, the capital to act when others couldn't, the operational expertise to improve assets rather than just own them, and most importantly, the contrarian conviction to invest when conventional wisdom said flee. It was value investing applied to real assets at massive scale.

The success of the GGP acquisition also demonstrated Brookfield's evolution from opportunistic investor to strategic consolidator. The company wasn't just buying distressed assets anymore; it was acquiring and transforming entire platforms. This platform approach – buying large portfolios and operating companies rather than individual assets – would become increasingly important as Brookfield pursued scale in other sectors.

Moreover, the GGP deal highlighted Brookfield's unique position in the investment ecosystem. Private equity firms typically couldn't pursue such transactions because their fund lives were too short for long-term transformation. REITs lacked the operational expertise and patient capital for major redevelopment. Only Brookfield, with its permanent capital vehicles and operational platform, could execute such a complex, long-term value creation strategy.

The lessons from GGP would inform Brookfield's next major platform acquisition. But this time, instead of buying hard assets like malls, Brookfield would acquire something seemingly antithetical to its real asset focus: a pure investment manager focused on credit and distressed debt. The acquisition of Oaktree Capital would test whether Brookfield's operational model could extend beyond physical assets into financial services.

Major Acquisitions: Oaktree - The Credit Platform (2019)

Howard Marks was holding court in his Los Angeles office, regaling visitors with stories about market cycles and investor psychology, when Bruce Flatt first approached him about a combination. The two men seemed an unlikely pair – Marks, the philosopher-investor who wrote widely-read memos about risk and market dynamics; Flatt, the operations-focused builder who preferred action to articulation. Yet their investment philosophies were remarkably aligned: both were contrarians, both were value investors, and both believed in the power of patient capital.

Howard Stanley Marks is an American investor and writer. He is the co-founder and co-chairman of Oaktree Capital Management, the largest investor in distressed securities worldwide. Founded in 1995, Oaktree had built one of the world's premier credit franchises by consistently investing when others retreated. The firm's motto, "if we avoid the losers, the winners will take care of themselves," reflected a risk-focused approach that resonated with Brookfield's philosophy.

The strategic rationale for combination was compelling. Brookfield had built dominant positions in real assets but lacked meaningful credit capabilities. As interest rates remained low and institutional investors searched for yield, credit strategies offered attractive returns with different risk characteristics than real estate or infrastructure. Moreover, credit markets were massive – multiples larger than real asset markets – providing enormous growth potential.

In March 2019, Canada's Brookfield Asset Management announced that it had agreed to buy 62% of Oaktree Capital Management for approximately $4.7 billion. The structure of the transaction was carefully crafted to preserve what made Oaktree special while providing the benefits of combination. Howard Marks would continue as Co-Chairman of Oaktree, Bruce Karsh as Co‑Chairman and Chief Investment Officer, and Jay Wintrob as Chief Executive Officer. Howard Marks and Bruce Karsh would continue to have operating control of Oaktree as an independent entity for the foreseeable future.

The negotiation process revealed both firms' sophisticated approach to value creation. Rather than a simple takeover, this was structured as a partnership. Oaktree would maintain its brand, culture, and investment autonomy. Brookfield would provide permanent capital, global distribution, and operational support. Both firms' clients would benefit from expanded capabilities – Brookfield investors gaining access to credit strategies, Oaktree investors to real asset expertise.

Howard Marks would join Brookfield's board of directors, bringing his strategic insights to Brookfield's governance. This wasn't just symbolic – Marks's presence would help Brookfield navigate credit cycles and identify distressed opportunities across all asset classes. His intellectual framework for understanding market psychology complemented Flatt's operational focus, creating a more complete investment perspective.

According to Warren Buffett, "When I see memos from Howard Marks in my mail, they're the first thing I open and read. I always learn something, and that goes double for his book". This endorsement from the Oracle of Omaha validated what Brookfield was acquiring: not just a credit platform, but an investment culture and intellectual framework that had consistently generated alpha through multiple cycles.

The integration process was deliberately gradual and respectful. Unlike typical private equity acquisitions that immediately impose new systems and processes, Brookfield took a hands-off approach to Oaktree's investment operations. The focus instead was on areas where combination created genuine value: coordinating fundraising efforts, sharing due diligence resources, and identifying crossover opportunities where credit and real asset expertise intersected.

On September 30, 2019, completion of the acquisition of a majority stake by Brookfield Asset Management was announced. The closing came at an interesting moment in credit markets. Years of low interest rates had compressed spreads, making traditional credit investing challenging. But Marks and Flatt saw opportunity in this challenge – their combined platform could pursue more complex, larger-scale transactions that pure credit or real asset investors couldn't execute alone.

The synergies became apparent quickly. When distressed situations emerged in real estate or infrastructure, Oaktree's credit expertise helped Brookfield structure complex rescue financings that provided both debt and equity returns. When Oaktree evaluated distressed companies, Brookfield's operational expertise helped assess whether underlying assets could be improved. This combination of financial and operational perspectives created a competitive advantage in complex situations.

One illustrative example was the collaboration around retail real estate distress during COVID-19. As retailers faced bankruptcy, Oaktree could provide rescue financing while Brookfield could acquire the real estate. This integrated approach allowed both firms to capture value across the capital structure – Oaktree earning high yields on rescue loans, Brookfield acquiring properties at distressed prices.

The cultural integration proved surprisingly smooth despite the firms' different histories. Both organizations attracted professionals who thought like investors rather than agents. Both emphasized long-term value creation over short-term gains. Both maintained partnership cultures where senior professionals invested meaningful personal capital alongside clients. These shared values eased integration challenges that often derail mergers.

The financial impact was substantial and immediate. The addition of Oaktree's $120 billion in assets under management brought Brookfield's total AUM to over $500 billion, achieving scale that provided operating leverage across the platform. Fee-related earnings grew as costs were spread across a larger base. Fundraising accelerated as institutional investors appreciated the convenience of accessing multiple strategies through a single manager.

Perhaps more importantly, the Oaktree acquisition positioned Brookfield for the next evolution in alternative investing: the convergence of traditional asset classes. As institutional investors sought solutions rather than products, the ability to provide integrated offerings across equity, credit, and real assets became increasingly valuable. A pension fund looking to finance infrastructure could access both equity and credit strategies. A sovereign wealth fund seeking yield could combine real estate equity with structured credit.

The success of the Oaktree integration also validated Brookfield's platform acquisition strategy. Rather than building credit capabilities organically over decades, Brookfield acquired a premier franchise with established track record and relationships. This buy-versus-build approach would inform future expansion into insurance and other adjacent sectors.

Brookfield paid $4.8B in cash and stock in 2019 to acquire a majority interest in Oaktree, and then it rapidly expanded the business. By 2024, the partnership had exceeded all expectations. Oaktree's assets under management had grown substantially, benefiting from Brookfield's global distribution network. New credit strategies were launched leveraging Brookfield's sector expertise. Most importantly, the cultural integration had preserved what made both firms special while creating something greater than the sum of parts.

The Oaktree acquisition also marked Brookfield's evolution from a real asset manager to a true alternative asset manager. With leading positions in real estate, infrastructure, renewable power, private equity, and now credit, Brookfield could offer institutional investors complete alternative investment solutions. This breadth would prove crucial as the firm pursued its next transformation: creating distinct vehicles for its asset management and investment operations.

The 2022 Reorganization: Creating BN and BAM

For years, Bruce Flatt had faced the same question from investors: "What exactly is Brookfield?" The company owned and operated assets like an industrial firm, managed money like BlackRock, invested permanent capital like Berkshire Hathaway, and raised funds like Blackstone. This complexity created a valuation puzzle – public markets struggled to properly value a hybrid that didn't fit neatly into any category. The solution, announced in 2022, would be one of the most significant corporate reorganizations in Canadian business history.

The conglomerate discount was real and persistent. Analysts estimated that Brookfield traded at 30-40% below its sum-of-parts value. The asset management business alone, generating billions in stable fee revenue, should have commanded a premium multiple similar to pure-play alternative managers. The owned assets – prime real estate, infrastructure, renewable power – were worth far more than their carrying values. Yet the market valued the combined entity at less than either piece would command separately.

Shares are expected to commence trading December 12, 2022. The Spinco will assume the ticker BAM and name Brookfield Asset Management. SPDJI will treat this as a zero price spinoff. The restructuring plan was elegant in its simplicity: split Brookfield into two distinct public companies. Brookfield Corporation (BN) would own the assets and permanent capital, investing alongside funds and generating returns from operations. Brookfield Asset Management (BAM) would be a pure-play manager, earning fees from managing money for others.

The Corporation has changed its name from Brookfield Asset Management Inc. to Brookfield Corporation, with effect from today and at the open of markets on December 12, 2022, its shares will trade under the new ticker "BN" on both stock exchanges. The Manager takes the name Brookfield Asset Management Ltd. and has been successfully listed on the New York Stock Exchange and the Toronto Stock Exchange. At the open of markets on December 12, 2022, its shares will trade under the ticker "BAM" on both stock exchanges.

The mechanics of the split required careful structuring to preserve value and maintain alignment. Brookfield Corporation would retain approximately 75% ownership of the asset manager, ensuring the two entities remained strategically aligned. Public shareholders would receive shares in both entities, allowing them to maintain exposure to both strategies or sell one to concentrate their investment. The structure was tax-efficient for most shareholders, avoiding triggering capital gains on the reorganization.

The benefits were immediately apparent to different stakeholder groups. For asset management investors, BAM offered a pure-play exposure to one of the world's fastest-growing alternative managers. The company's fee-related earnings were highly predictable, growing steadily with AUM. Without the complexity of owned assets and development projects, BAM could be valued using simple multiples of fee revenue, similar to other public asset managers.

For value investors, BN represented a Berkshire Hathaway-like vehicle owning high-quality real assets plus a controlling stake in a premier asset manager. The company would continue investing permanent capital opportunistically, generating returns from both asset appreciation and operational improvements. With the asset management stake clearly delineated, investors could better appreciate the value of the owned assets.

The timing of the reorganization was strategic. Alternative asset management was experiencing unprecedented growth as institutional investors increased allocations from traditional stocks and bonds. Pure-play managers traded at premium valuations, with markets finally appreciating the stability of fee revenue and the scalability of the model. By separating the asset management business, Brookfield could capture this valuation uplift while maintaining control through its majority stake.

The organizational challenges were significant. Thousands of employees needed clarity on their reporting lines and compensation structures. Systems had to be separated while maintaining operational continuity. Transfer pricing between the entities required careful structuring to ensure both companies were economically viable. The entire reorganization had to be executed while continuing to manage over $700 billion in assets across multiple strategies and geographies.

Cultural considerations were equally important. Brookfield's success had been built on alignment – everyone rowing in the same direction. The split risked creating competing interests or rival camps. To prevent this, leadership emphasized that the two companies were partners, not competitors. BN would be BAM's largest client and strategic partner. BAM would provide BN with fee revenue and investment opportunities. Senior executives would serve both companies, ensuring strategic alignment.

The market reaction validated the strategy. Upon separation, both stocks performed well, with the combined value exceeding the pre-split price. BAM attracted new institutional investors who previously avoided Brookfield due to its complexity. BN appealed to value investors who could now clearly see the asset base and investment strategy. The separation unlocked billions in value that had been hidden by structural complexity.

On December 9, 2022, the company's name was changed from Brookfield Asset Management Inc. to Brookfield Corporation. Brookfield Corporation then spun-off 25% interest in their asset management business into the new publicly listed Brookfield Asset Management Ltd. This 25% public float provided BAM with its own currency for acquisitions and employee compensation while maintaining BN's control through its 75% stake.

The reorganization also positioned both companies for future growth. BAM could pursue acquisitions of other asset managers, using its publicly traded stock as currency. The company could also more easily access debt markets as a pure-play manager with predictable cash flows. Employee retention and recruitment improved with clearer equity compensation tied directly to the asset management business.

For BN, the reorganization clarified its investment proposition. The company could pursue larger, more complex investments without worrying about confusing asset management investors. The permanent capital model was now clear – BN would invest patient capital in real assets, generating returns over decades rather than quarters. This clarity attracted a new class of long-term investors who appreciated the Berkshire Hathaway-like model.

The strategic implications extended beyond valuation. The separation allowed each company to optimize its capital structure independently. BAM could maintain minimal debt, appropriate for a fee-based business. BN could use leverage strategically at the asset level, enhancing returns while maintaining conservative corporate borrowing. This financial flexibility would prove valuable as interest rates rose and capital markets evolved.

The reorganization also facilitated cleaner reporting and enhanced transparency. Investors could now see exactly how each business performed without complex consolidation adjustments. Fee-related earnings at BAM were clearly separated from investment returns at BN. This transparency built trust with investors and reduced the skepticism that often accompanies complex conglomerates.

By early 2024, the benefits of the reorganization were undeniable. BAM had been included in major indices, attracting passive investment flows. The company's multiple had expanded to match peer asset managers. BN had successfully raised permanent capital from new sources, including sovereign wealth funds that appreciated the clarity of the investment model. The combined market capitalization of both entities substantially exceeded the pre-split valuation.

The 2022 reorganization would prove to be perfectly timed for what came next. As artificial intelligence drove unprecedented demand for infrastructure, both companies were optimally positioned to capitalize. BAM could raise massive funds focused on AI infrastructure. BN could invest its permanent capital in transformative projects. The structural clarity achieved through reorganization would prove essential as Brookfield embarked on its most ambitious chapter yet.

The AI Infrastructure Boom (2020s-Present)

The meeting at Microsoft's Redmond headquarters in early 2024 was supposed to be routine – a discussion about renewable energy procurement for data centers. But as Bruce Flatt and his team sat across from Microsoft's infrastructure executives, it became clear that something much bigger was at stake. The AI revolution wasn't just changing software; it was fundamentally reshaping global infrastructure needs. The power requirements were staggering – Microsoft alone projected needing as much electricity as entire small countries. And they needed partners who could deliver at unprecedented scale.

Microsoft announced a $10 billion deal with asset manager Brookfield to supply Microsoft with a whopping 10.5 gigawatts of renewable power capacity between 2026 and 2030. That's by far the biggest such deal ever signed, roughly equivalent to the amount of electricity required to power 4 million homes. The agreement represented more than just a power purchase – it was a strategic partnership to build the infrastructure backbone of the AI age.

The convergence of Brookfield's capabilities with AI's infrastructure needs was almost poetic. For decades, Brookfield had been assembling exactly the assets and expertise that AI development required: massive renewable power generation, data center development capabilities, grid infrastructure expertise, and most importantly, the capital and operational skill to deploy at scale. While competitors scrambled to understand AI's implications, Brookfield was already positioned to capitalize.

The numbers were mind-boggling. Data center power consumption, stable for years, was projected to triple by 2030. Each new AI training cluster required as much power as tens of thousands of homes. The largest AI factories being planned would consume gigawatts – equivalent to entire nuclear power plants. Traditional utilities, already stretched by renewable transition and grid modernization needs, simply couldn't keep pace.

In May 2024, Brookfield signed an agreement with Microsoft Corp. to deliver more than 10.5 gigawatts of additional renewable energy capacity over a five-year period to power its AI cloud services business. But this was just the beginning. Behind the scenes, Brookfield was orchestrating a comprehensive AI infrastructure strategy that would touch every aspect of the computational revolution.

The renewable power platform became the cornerstone. Brookfield's existing portfolio of hydroelectric, wind, and solar facilities provided immediate capacity. But more importantly, the company's development pipeline – one of the world's largest – could be oriented toward AI power needs. Sites previously considered marginal became valuable when located near data center clusters. Grid connections reserved for future projects could be repurposed for AI facilities.

Then came the Bloom Energy partnership, announced in October 2024. US fuel cell developer Bloom Energy has signed a $5 billion AI infrastructure partnership with global investment firm Brookfield. The partnership will see Brookfield invest up to $5bn to support the deployment of Bloom's Solid Oxide Fuel Cell (SOFC) technology in AI data centers worldwide. This wasn't just about backup power – it was about creating independent energy solutions for AI facilities that couldn't wait for grid expansion.

The Bloom partnership exemplified Brookfield's operational approach to AI infrastructure. Rather than simply financing data centers and hoping for the best, Brookfield was actively solving the bottlenecks constraining AI development. Bloom's fuel cells could provide reliable, on-site power generation, allowing AI facilities to operate independently of constrained grids. The technology was particularly valuable in markets where renewable power was intermittent or grid connections were years away.

KR Sridhar, founder, chairman, and CEO of Bloom Energy, said: "Unlike traditional factories, AI factories demand massive power, rapid deployment, and real-time load responsiveness that legacy grids cannot support. The lean AI factory is achieved with power, infrastructure, and compute designed in sync from day one. That principle guides our collaboration with Brookfield to reimagine the data center of the future".

Brookfield's AI infrastructure strategy extended beyond just power generation. The company was assembling a complete ecosystem: land near fiber routes for data centers, cooling solutions for heat management, grid infrastructure for power distribution, and even semiconductor manufacturing facilities for chip production. This integrated approach meant Brookfield could offer tech companies turnkey solutions rather than piecemeal components.

The financial opportunity was unprecedented. Investment firm Brookfield Asset Management, one of the largest investors in the AI value chain globally with more than €150bn (US$157bn) invested across digital infrastructure, renewable power and semiconductor manufacturing globally, has emerged as a leading investor. The company plans to invest €20bn (US$20.9bn) over the next five years to develop data centres and AI infrastructure in France. Brookfield has allocated €15bn (US$15.7bn) to data centres, which will be led by its portfolio company Data4.

The competitive advantages Brookfield brought to AI infrastructure were difficult to replicate. First, the company's permanent capital structure meant it could commit to decade-long development programs while others worried about fund expiration. Second, its operational expertise across power, real estate, and infrastructure allowed integrated solution development. Third, its global presence meant it could support AI development wherever computational needs arose.

The partnerships being formed revealed the strategic nature of AI infrastructure. Unlike traditional data centers that simply housed servers, AI factories required tight integration between compute, power, and cooling. Brookfield's operational expertise meant it could optimize these systems holistically rather than treating them as separate components. This systems-level thinking created efficiencies that pure financial investors couldn't achieve.

Geographic strategy became crucial as AI infrastructure needs varied by region. In Europe, where renewable power was plentiful but grid connections were constrained, Brookfield focused on behind-the-meter solutions connecting renewable generation directly to data centers. In Asia, where land was scarce, the emphasis was on efficiency and density. In America, where power demand was exploding, Brookfield pursued large-scale integrated facilities combining generation, transmission, and computation.

The risk management approach to AI infrastructure was distinctly Brookfieldian. While others rushed to build speculative data centers hoping to attract AI tenants, Brookfield focused on contracted, long-term arrangements with creditworthy counterparties. The Microsoft agreement exemplified this – a decade-long partnership with one of the world's strongest technology companies. This approach provided stable, predictable returns while others gambled on AI's uncertain trajectory.

The second-order effects of AI infrastructure investment were equally important. As Brookfield built power generation for AI facilities, excess capacity could serve local grids, improving renewable penetration. Data center developments catalyzed fiber network expansion, benefiting broader digital infrastructure. The economic activity generated by AI facilities – from construction jobs to ongoing operations – revitalized communities that hosted them.

By late 2024, Brookfield's AI infrastructure investments were generating substantial returns. The Microsoft partnership was ahead of schedule. The Bloom Energy collaboration was deploying fuel cells globally. New partnerships with other hyperscalers were being negotiated. Most importantly, Brookfield was establishing itself as the indispensable infrastructure partner for the AI age – a position that would generate value for decades.

The AI infrastructure boom also validated Brookfield's long-term strategy of controlling real assets. While software companies captured headlines, the physical infrastructure enabling AI – power plants, data centers, fiber networks – generated steady, growing cash flows. These assets, once built, became essential and irreplaceable, creating exactly the kind of competitive moats Brookfield had always sought.

Looking ahead, the AI infrastructure opportunity was still in its infancy. Artificial general intelligence, quantum computing, and other emerging technologies would require even more sophisticated infrastructure. Brookfield's early positioning, operational expertise, and patient capital positioned it to capture disproportionate value from these trends. The company that had started laying tramway tracks in São Paulo was now laying the foundation for humanity's computational future.

Financial Performance & Capital Allocation

The numbers tell a story that few companies can match. Brookfield is a value investor with a track record of delivering 15%+ annualized returns to shareholders for over 30 years. To put this in perspective, $10,000 invested in Brookfield thirty years ago would be worth over $660,000 today – a testament to the power of compound growth and disciplined capital allocation. But raw returns only tell part of the story; the consistency and methodology behind these results reveal why Brookfield has become a model for long-term value creation.

In the third quarter of 2024, BAM collected $21 billion in capital, which put its assets over the $1 trillion mark. This milestone wasn't just symbolic – it represented a scale that provides enormous competitive advantages. At this size, Brookfield can pursue transactions no one else can finance, negotiate better terms through bulk purchasing power, and spread fixed costs across a massive base. The journey from $5 billion in assets under management when Flatt became CEO to over $1 trillion today represents a 200-fold increase in just over two decades.

The capital allocation framework that produced these results is deceptively simple but ruthlessly disciplined. Every investment must meet four criteria: it must be a high-quality asset with sustainable competitive advantages, available at a price below intrinsic value, within Brookfield's operational expertise, and capable of generating stable, growing cash flows. This framework means Brookfield walks away from the vast majority of opportunities, maintaining discipline even when capital is plentiful.

The permanent capital advantage cannot be overstated. While traditional private equity firms must return capital within 10 years, forcing sales regardless of market conditions, Brookfield can hold assets indefinitely. This patient approach has profound implications. The company can invest in long-term value creation that won't pay off for years. It can hold through cycles, buying when others must sell and selling when others desperately need to buy. Most importantly, it can compound returns over decades rather than constantly restarting with new funds.

The fee-related earnings model provides remarkable stability. Unlike traditional asset managers whose performance fees are volatile and unpredictable, Brookfield's base management fees on $1 trillion of assets generate billions in predictable annual revenue. These fees are typically locked in for years through long-term fund commitments, providing visibility and stability that few businesses enjoy. This stable cash flow funds operations, supports the dividend, and provides dry powder for opportunistic investments.

Capital recycling has become a core competency that multiplies returns. Brookfield doesn't just buy and hold forever; it constantly optimizes its portfolio, selling mature assets at premium valuations and redeploying capital into higher-return opportunities. A typical asset might be acquired at a distressed valuation, improved operationally over 5-7 years, then sold to a core investor at a much lower required return. The capital is then redeployed into the next distressed opportunity, repeating the cycle.

The leverage philosophy differentiates Brookfield from both conservative corporations and aggressive private equity firms. Debt is used strategically at the asset level – non-recourse to the parent company and matched to asset cash flows. Corporate leverage remains conservative, ensuring Brookfield can survive any downturn. This approach provides enhanced returns during good times while protecting against catastrophic loss during crises. The weighted average debt maturity exceeds seven years, providing protection against refinancing risk.

Geographic diversification provides both opportunity and stability. With operations in over 30 countries, Brookfield can pursue the best opportunities globally while reducing exposure to any single market. When North American real estate was overvalued, Brookfield invested in Europe. When developed markets were saturated, it pursued emerging market infrastructure. This global flexibility means Brookfield is never forced to invest in overheated markets but can always find attractive opportunities somewhere.

The power of operational improvement often exceeds financial engineering. A typical Brookfield investment might generate 5-7% returns from financial structure, but 10-15% from operational improvements. This might mean increasing occupancy in office buildings, improving efficiency at power plants, or optimizing pricing at toll roads. These operational gains are more sustainable than leverage-driven returns and less vulnerable to market cycles. They also create real value rather than simply transferring it from one stakeholder to another.

Skin in the game aligns interests throughout the organization. Senior executives are required to invest meaningful personal capital alongside institutional investors – often millions of dollars of their own money. This requirement ensures that decision-makers feel the pain of losses personally and share in the upside of success. It also attracts a different type of professional: entrepreneurs who think like owners rather than agents collecting paychecks regardless of performance.

The distribution strategy balances growth and current income. Brookfield targets paying out 60-70% of operating cash flow as distributions, retaining the remainder for growth investments. This balance appeals to both income-seeking investors who need current cash and growth investors who want capital appreciation. The distribution has grown at approximately 7% annually for decades, well above inflation, while retaining sufficient capital to fund growth.

In the first quarter of 2025, the company raised $25 billion of new capital and deployed $16 billion across its various business segments. Over the last twelve months, Brookfield has raised an impressive $142 billion and deployed $53 billion, demonstrating its ability to attract investor capital and identify attractive investment opportunities globally. This massive scale of activity – raising and deploying more capital than most firms' entire AUM – demonstrates the institutional trust Brookfield has earned.

The margin expansion story is compelling. As assets under management have grown, fee-related earnings margins have expanded from the low 40s to nearly 60%. This operating leverage is inherent to asset management – the cost of managing $1 trillion isn't significantly higher than managing $500 billion, but the fees are double. This margin expansion drops directly to the bottom line, driving earnings growth faster than AUM growth.

Performance fees, while volatile, provide significant upside. When Brookfield's funds exceed hurdle rates – typically 8-9% annually – the company earns 20% of excess returns. Given the scale of funds under management, these performance fees can amount to billions in high-return years. Unlike management fees which are steady but modest, performance fees provide the upside that drives exceptional returns during strong markets.

The insurance strategy represents the next evolution in permanent capital. Through Brookfield Reinsurance and acquisitions of insurance companies, Brookfield is accessing the float of insurance premiums – money that can be invested for years before claims are paid. This insurance float, similar to what powered Berkshire Hathaway's growth, provides another source of permanent capital that can be deployed into high-return investments while earning spread income.

Tax efficiency has been carefully engineered into the structure. Many of Brookfield's investments are structured as partnerships, allowing tax-efficient cash distributions to investors. Depreciation and other non-cash charges shelter much of the cash flow from immediate taxation. The global structure allows optimization of tax rates across jurisdictions. While complex, these structures meaningfully enhance after-tax returns for investors.

The acquisition integration track record demonstrates execution excellence. Major acquisitions like GGP and Oaktree have been successfully integrated, generating returns well above initial projections. This success stems from Brookfield's patient approach – taking time to understand businesses before acquiring them, maintaining management teams and culture post-acquisition, and focusing on long-term value creation rather than quick flips.

Looking at sector performance reveals the power of diversification. When office real estate struggled during COVID-19, infrastructure and renewable power thrived. When interest rates rose, hitting real estate values, infrastructure assets with inflation-linked revenues prospered. This diversification isn't just about risk reduction – it's about having capital deployed across multiple themes, ensuring some portion of the portfolio is always positioned to benefit from current trends.

The technology investments, often overlooked, are transforming operations. Artificial intelligence optimizes building energy usage. Machine learning predicts maintenance needs before equipment fails. Digital platforms streamline property management across global portfolios. These investments don't appear as separate line items but manifest as improving margins and operational metrics across all platforms.

By any measure – total return, consistency, scale, or durability – Brookfield's financial performance ranks among the best in the investment industry. The company has delivered these results not through leverage or speculation, but through patient capital allocation, operational excellence, and contrarian thinking. As the company enters its next phase, with AI infrastructure and energy transition providing massive investment opportunities, the financial foundation built over three decades positions it to continue delivering exceptional returns for decades to come.

Strategic Analysis: Porter's 5 Forces

Threat of New Entrants (Low)

The barriers to competing with Brookfield at scale are nearly insurmountable. Consider what a new entrant would need: tens of billions in committed capital, relationships with hundreds of institutional investors, operational expertise across multiple complex sectors, a decades-long track record to earn trust, and the patience to invest through multiple cycles. The industry has seen numerous attempts to replicate Brookfield's model, but none have achieved similar scale and scope.

The capital requirements alone are staggering. While anyone can start an asset management firm with modest capital, competing for the transactions Brookfield pursues requires billions in equity and access to tens of billions in debt financing. The recent Microsoft renewable energy deal, requiring $10+ billion in development capital, exemplifies the scale needed. Few organizations globally can write checks of this size, and even fewer can then operate the assets effectively.

Track record represents an even higher barrier. Institutional investors entrusting billions in pension assets demand decades of proven returns through multiple cycles. Brookfield's 30-year history of 15%+ returns cannot be replicated quickly. New entrants face a catch-22: they need capital to build track record, but investors won't provide capital without track record. This dynamic strongly favors incumbent firms with established histories.

Operational expertise cannot be hired overnight. Brookfield employs thousands of operating professionals – power plant engineers, property managers, infrastructure operators – who understand the nuances of running complex assets. This expertise, built over decades, allows Brookfield to underwrite risks others can't evaluate and create value others can't capture. A financial buyer might acquire a hydroelectric facility, but only Brookfield can optimize its operations across a global fleet.

Bargaining Power of Suppliers (Medium)

In Brookfield's context, "suppliers" are primarily sellers of assets – from individual property owners to governments privatizing infrastructure. These sellers have options but face constraints that limit their bargaining power. For large, complex transactions, the universe of potential buyers shrinks dramatically. Only a handful of firms globally can execute multi-billion dollar infrastructure acquisitions or complicated corporate carve-outs.

Brookfield's reputation as a reliable closer enhances its position. Sellers know that a deal with Brookfield will likely close without re-trading or financing contingencies. This certainty has value, especially for governments facing political pressure or corporations needing to hit quarterly targets. The premium for certainty often means Brookfield can win competitive auctions without being the highest bidder.

However, sellers retain meaningful power in hot markets. When multiple strategic buyers compete for trophy assets, prices can become irrationally high. Brookfield's discipline means it often walks away from such auctions, limiting its access to certain assets. The company's contrarian philosophy works best when sellers are distressed or markets are dislocated, conditions that don't always exist.

Bargaining Power of Customers (Low-Medium)

Brookfield's "customers" are primarily limited partners investing in its funds – pension funds, sovereign wealth funds, insurance companies. These institutions have alternatives but face their own constraints. They need scale that only the largest managers can provide, expertise in complex sectors like infrastructure, and track records that justify fiduciary decisions. The universe of managers meeting these criteria is small and shrinking through consolidation.

Switching costs are substantial. An institution invested in a Brookfield fund has typically committed capital for 10+ years. Exiting requires selling in secondary markets at significant discounts. Moreover, the relationship-specific knowledge developed over years – understanding Brookfield's strategy, trusting its team, knowing its processes – creates soft switching costs. The reputation risk of abandoning a successful manager for an unproven alternative further increases customer stickiness.

Fee pressure exists but is manageable. While institutions constantly push for lower fees, Brookfield's performance justifies its charges. The company's 2-and-20 fee structure (2% management fee, 20% performance fee) remains intact despite industry pressure. Investors ultimately care more about net returns than gross fees, and Brookfield's track record supports premium pricing.

Threat of Substitutes (Medium)

The primary substitutes for Brookfield's services are direct investing by institutions, public market investments, and other alternative strategies. Each substitute has limitations that preserve Brookfield's position. Direct investing requires massive internal teams and operational expertise that most institutions lack. Public markets offer liquidity but not the control and operational improvement opportunities Brookfield provides. Other alternatives like hedge funds or venture capital serve different risk-return profiles.

The most serious substitution threat comes from institutions building internal direct investment capabilities. Large pension funds like Canada's CPPIB and OTPP have developed sophisticated internal teams that compete with Brookfield for assets. However, even these sophisticated investors often partner with Brookfield on complex transactions, recognizing the value of its operational platform and global reach.

Technology poses a longer-term substitution risk. As data analytics and artificial intelligence improve, some investment decisions could be automated or democratized. However, the operational complexity of real asset investing – negotiating with governments, managing union workforces, navigating environmental regulations – requires human judgment and relationships that technology cannot easily replace.

Competitive Rivalry (Medium-High)

The competitive landscape has intensified as alternative assets have become mainstream. Blackstone, with over $1 trillion AUM, competes directly in real estate and infrastructure. KKR has built substantial infrastructure and real estate platforms. Apollo has expanded beyond credit into real assets. Even traditional asset managers like BlackRock have launched alternative strategies. This proliferation of competitors has made asset acquisition more competitive and fee pressure more intense.