Circle Internet Group: The Rise of the Digital Dollar

I. Introduction & Episode Roadmap

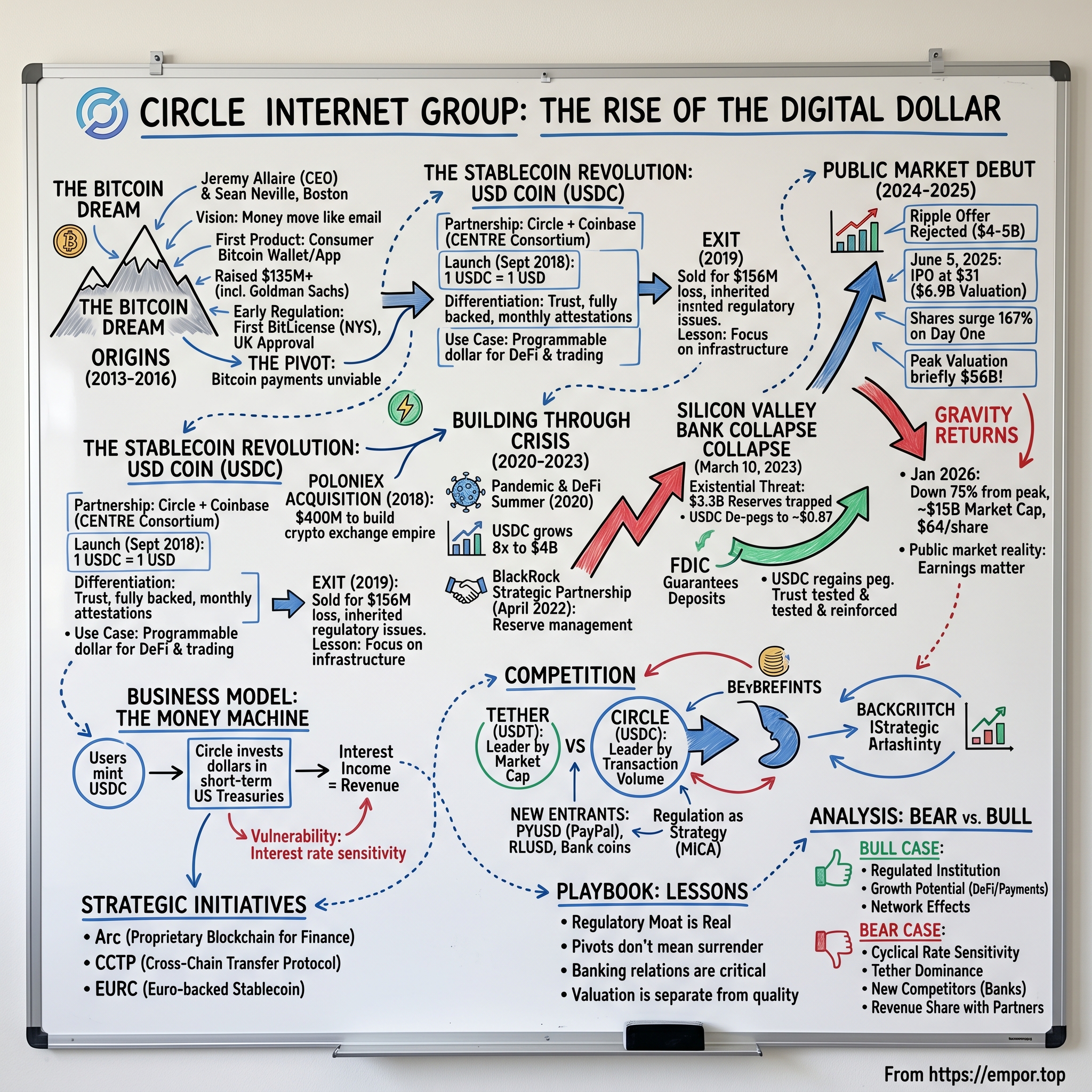

Picture this: it’s March 10, 2023. Jeremy Allaire, Circle’s CEO, is staring at the kind of problem that can kill a financial company in a weekend. Silicon Valley Bank has just collapsed, and Circle has $3.3 billion of USDC’s reserves sitting there. In crypto, where confidence is everything, that’s not just a banking headline—it’s an existential threat.

The panic hits fast. USDC, the “safe” stablecoin at the heart of huge swaths of crypto trading and DeFi, slips off its dollar peg. At the worst point it trades down into the high 80-cent range. Across Boston and San Francisco, Circle’s leadership goes into crisis mode—on the phone with regulators, investors, partners, and customers who all want the same thing: certainty that one USDC is still worth one dollar.

Now jump ahead just over two years. In June 2025, Circle finally makes it to the public markets at roughly a $6.9 billion valuation—and then the stock goes vertical. Shares surge 167% on day one. Within weeks, the market is briefly valuing Circle at $56 billion, one of the wildest post-IPO runs in recent memory.

And then gravity returns. By early 2026, the stock is down more than 75% from its peak, hovering around $64 a share and roughly a $15 billion market cap. A reminder that even in crypto—maybe especially in crypto—public markets ultimately care about earnings, interest rates, and what you’re paying for growth.

So how did a company that once bet on Bitcoin payments become crypto’s most trusted institution? How did Circle build what is, in practice, a stablecoin toll road—earning $1.68 billion in revenue in 2024 largely by investing the dollars behind USDC? And why did investors briefly decide that business was worth $56 billion… before snapping back to reality?

This is the story of Circle Internet Group: a company born from the dream of making money move like email, forced through multiple reinventions by crypto’s chaos, and ultimately forged into the infrastructure layer for the digital dollar. It’s a story about trust in a system designed to be trustless, about regulatory strategy as a competitive moat, and about building financial rails for the internet age. Along the way, Circle morphs from a consumer Bitcoin wallet into institutional plumbing, learns expensive lessons from a $400 million crypto exchange acquisition, and turns the unsexy business of managing reserves into a machine that can generate real, scalable profit—then has to learn what it means to live under the unforgiving spotlight of the public markets.

II. Origins & The Bitcoin Dream (2013–2016)

It was 2013, and Bitcoin was having its first real moment in the mainstream. The price rocketed from the teens to over $1,000, then cracked back down—an early preview of the boom-bust rhythm that would come to define crypto. But in Boston, two founders weren’t looking at Bitcoin as a trade. They were looking at it as a new set of rails.

The question they cared about wasn’t “How high can this go?” It was: what if money could move like the internet—instant, global, and always on?

Jeremy Allaire came to crypto from a very different world than the stereotypical cypherpunk scene. He was a seasoned entrepreneur who’d built and sold Brightcove, a video software company, for hundreds of millions of dollars. He understood how to build products that normal people actually use, how to win institutional trust, and how to operate in heavily regulated environments. His co-founder, Sean Neville, brought deep technical chops from their prior work together. When they founded Circle in October 2013, they put the ambition in plain English: “make money as easy to move and use as email, transcending borders and banking hours with the efficiency of the internet.”

Circle’s first product took aim at the obvious wedge: a consumer Bitcoin wallet and payment app—Venmo-like in spirit, but powered by cryptocurrency. The idea was simple: let users send money to friends or pay for things, while Circle quietly handled the ugly parts behind the curtain, like converting between dollars and Bitcoin. To investors, the story was compelling: Circle would be the friendly on-ramp that made Bitcoin usable for everyone else.

The money followed. From 2013 through 2016, Circle raised over $135 million across four rounds, including a $50 million round led by Goldman Sachs. That Goldman check mattered far beyond the dollars. As New York Times reporter Nathaniel Popper wrote at the time, it “should help solidify Bitcoin’s reputation as a technology that serious financial firms can work with.” In other words: this wasn’t a hobby anymore. Wall Street had shown up.

Circle also did something that, in crypto, is both rare and expensive: it leaned into regulation early. In 2015, it became the first company to receive a BitLicense from the New York State Department of Financial Services. By April 2016, it was also the first to gain approval for virtual currency operations from the British government. While others sprinted through gray zones, Circle was building a compliance-first identity—like it was preparing for a future where rules would be the barrier to entry.

But even with top-tier investors and a growing stack of licenses, the consumer dream wasn’t clicking. Bitcoin’s volatility made everyday payments feel absurd—buy something in the morning and it might cost “more” or “less” by lunch. Running anything that looked like an exchange in the U.S. came with crushing complexity. And maybe most importantly, Circle wasn’t just competing with banks. It was competing with beautifully simple payment apps like Venmo, where users didn’t have to learn anything new, let alone think about blockchains.

The pivot came in stages. Circle repositioned as a “social payments” company, trying to beat Venmo at its own game while keeping crypto rails in the background. But by December 2016, the Circle app stopped supporting Bitcoin exchange entirely, even though it still allowed money transfers. The original Bitcoin payments thesis—at least in its pure form—was effectively over.

And yet, what looked like a retreat was really a hard-earned insight. The issue wasn’t that digital money was a bad idea. The issue was the asset. For payments to work, value has to stay put.

Circle didn’t need a better Bitcoin wallet. It needed a digital dollar.

III. The Stablecoin Revolution: Birth of USDC (2017–2019)

By 2017, Circle was cornered—in the productive way. The consumer payments pivot hadn’t broken through. Venmo and the banks still owned the default experience. And Circle had to answer a brutal question: if it wasn’t going to win by being the prettiest app on someone’s home screen, what was it uniquely built to do?

The company’s real assets weren’t viral growth tricks. They were the things most crypto startups avoided: licenses, credibility with institutions like Goldman Sachs, and working relationships with regulators. Circle didn’t need a product that dodged the system. It needed a product that used the system—and made it work at internet speed.

The market was already screaming for it. Crypto was volatile, regulation was tightening, and Bitcoin simply wasn’t a practical unit of account. Traders needed somewhere to park value without leaving the ecosystem. Early DeFi builders needed a stable building block. Global businesses wanted dollars that could move as easily as data, without waiting for banking hours or wire cutoffs. In other words: everyone needed a digital dollar. They just didn’t have one they could trust.

That’s what a stablecoin is supposed to be. A token that moves on blockchains, but holds steady value because it’s backed by real dollars in reserve. If you mint one unit, one dollar goes into the reserve. If you redeem it, you get your dollar back and the token is destroyed. The point isn’t that it’s flashy—it’s that it’s useful: dollars that can move globally, quickly, and around the clock, without bank holidays, without multi-day settlement delays, and without the friction of traditional rails.

Circle’s big move was to turn that concept into a product people could actually adopt—and to do it with the right partner. On May 15, 2018, Circle raised $110 million in venture funding to create USD Coin. But USDC wasn’t built as a Circle-only project. It was developed with Coinbase, with both companies as partners and co-founders of the CENTRE Consortium. Coinbase brought what Circle didn’t have: instant distribution. A regulated exchange with millions of users meant USDC could launch into real liquidity and real use cases from day one.

And USDC’s real differentiation wasn’t that it was the first stablecoin. Tether had dominated the category since 2014. The difference was trust—and the strategy behind it. Where Tether lived in the gray, with opaque reserves and perpetually messy banking relationships, Circle and Coinbase aimed for the opposite: the “clean” stablecoin. USDC was designed to be fully backed, with reserves subject to regular public reporting. Monthly attestations from an independent accounting firm were meant to answer the only question that matters in a stablecoin: are the dollars really there?

Circle launched USDC in September 2018, and it caught fast. Within weeks, more than 40 companies—wallets, exchanges, custodians, and decentralized applications—had signed on to support it. The timing helped. DeFi was starting to take shape, and developers needed a stable unit of account to build lending markets, decentralized exchanges, and the early experiments that would later explode into “DeFi summer.” A programmable, blockchain-native dollar was simply easier to wire into applications than traditional bank dollars.

The CENTRE structure mattered, too. By wrapping USDC in a consortium with Coinbase, Circle made it feel less like one company’s product and more like emerging infrastructure. Builders are more willing to commit when they believe the rails won’t be yanked out from under them—or controlled by a single entity acting purely in its own interest. It’s the same intuition that made open standards like HTTP so powerful.

By 2019, USDC had established itself as the second-largest stablecoin, going from zero to billions in circulation in under a year. Circle wasn’t trying to out-Venmo Venmo anymore. It had found the higher ground: become the dollar layer inside crypto—plumbing you don’t think about until it breaks, and once it works, you can’t imagine the system without it.

IV. The Poloniex Acquisition & Exit (2018–2019)

February 26, 2018 started like any other Monday in crypto—until Circle dropped a headline that made the industry do a double-take: it had bought the Poloniex cryptocurrency exchange for $400 million. In crypto terms, it felt like a blue-chip finance player buying a major stock exchange overnight. Poloniex wasn’t just another venue; it was one of the early giants, an exchange that helped define the first wave of altcoin trading and, famously, gave Ethereum some of its earliest meaningful liquidity.

On paper, the logic was clean. Circle was trying to assemble a full-stack crypto financial services company: Circle Pay on the consumer side, Circle Trade for institutional liquidity, USDC for stable value, and now Poloniex as the global marketplace where all those assets would trade. Allaire and Neville framed it as another foundational layer—“an open global token marketplace”—plugged directly into the rest of Circle’s growing product suite.

And the timing made it look like a masterstroke. Crypto had just come off a historic run, with the overall market swelling dramatically over the prior year. Circle Trade was already doing billions in monthly transactions and had put up eye-catching revenue in a short span. Add a major exchange, and suddenly Circle didn’t just look like infrastructure—it looked like it could rival Coinbase in scale and breadth.

But almost immediately, reality started leaking through the deal announcement.

Poloniex had grown fast—too fast. Circle’s founders described it as “rocket ship velocity,” and the metaphor was apt: astonishing acceleration, plus the whiplash that comes when you try to turn that into a mature, regulated business. Customer support struggled to keep up. The technical foundation was fragile. And the compliance posture that might pass in the early, anything-goes era of crypto didn’t hold up once Circle, a U.S.-regulated, license-heavy company, owned the keys.

Then came the part Circle couldn’t refactor with engineers: the baggage. Poloniex arrived with regulatory risk that Circle hadn’t fully appreciated at the time of purchase. The SEC had filed a complaint tied to activity from 2017 involving trading that “may be characterized as securities.” There were also potential sanctions issues, with the exchange allegedly allowing users from restricted countries to trade. Circle hadn’t just bought an exchange. It had bought someone else’s unresolved liabilities.

Still, Circle initially pressed forward with the broader vision. In October 2018, it announced the acquisition of SeedInvest, a crowdfunding platform aimed at enabling security tokens—another signal that Circle was leaning into the idea of building a comprehensive crypto capital markets platform.

But inside the company, the Poloniex integration was turning into a grind. The codebase was brittle. The compliance systems weren’t ready for U.S. expectations. And as Circle wrestled with all of that, the market turned. The bull run faded into a punishing bear market that crushed volumes, shattered token prices, and made exchange economics far less forgiving.

By October 2019, Circle pulled the plug. It and Poloniex split, with Poloniex spinning out as a new entity called “Polo Digital Asset.” Financially, it was a painful eighteen-month round trip. Circle lost $156 million between the acquisition and the eventual sale. And the aftershocks lingered: Circle set aside more than $10.4 million to settle the SEC matter it had inherited, plus another $1.1 million to $2.8 million to OFAC tied to sanctions violations.

The lesson was as expensive as it was clarifying. In crypto, “empire building” looks brilliant right up until the moment you inherit someone else’s shortcuts—and discover that the real liabilities aren’t on the balance sheet, they’re in the regulators’ inbox.

As 2019 closed, Circle made the decision that shaped everything that came next: focus. It stopped trying to be every kind of crypto company at once. Consumer products would wind down. Exchange ambitions would be abandoned. Circle would double down on what was working—USDC and the infrastructure around it—and commit to being the plumbing, not the faucet.

V. Building Through Crisis: DeFi Summer to Banking Turmoil (2020–2023)

The pandemic rewired the world’s relationship with money—and Circle happened to be holding the right piece of infrastructure at the right time. As lockdowns began in March 2020, the traditional system showed its seams: international transfers slowed, settlement timelines felt archaic, and “banking hours” looked increasingly ridiculous in an always-on economy. The pitch Circle had been making for years—instant, borderless movement of dollars—suddenly felt less like a crypto slogan and more like a practical need.

Then, in the summer of 2020, crypto found its own accelerant: DeFi. In a single year, the value locked in decentralized finance exploded from about $800 million to more than $23 billion. USDC rode that wave hard, growing roughly eightfold and finishing the year around $4 billion in circulation. Protocols like Uniswap, Compound, Aave, and Maker weren’t just trading playgrounds anymore—they were becoming the core apps of a new financial stack. And they needed a stable, programmable dollar to run on.

USDC fit perfectly. It stopped being just a place to park value between trades and became the default building block for everything DeFi wanted to do: lending, borrowing, liquidity pools, on-chain settlement. The more developers embedded USDC, the more it showed up everywhere, because it was simply the easiest way to denominate crypto finance in something the real world understood.

Circle made the defining strategic move of this era: it stopped chasing consumers and leaned into infrastructure. Instead of trying to win on the home screen, Circle focused on the behind-the-scenes work—APIs for payments, treasury management, and global money movement built for institutions and developers. It wasn’t flashy. No viral loops, no consumer branding battles. Just documentation, integrations, and enterprise sales. But it scaled in a way consumer products rarely do—more like selling the tools the entire ecosystem uses than trying to run the ecosystem’s most popular storefront.

Investors followed the shift. In May 2021, with USDC’s market cap above $20 billion, Circle announced a $440 million funding round backed by a who’s who of crypto and traditional finance—Fidelity, FTX, Digital Currency Group, and others. Less than a year later, in April 2022, Circle raised another $400 million from BlackRock, Fidelity, Marshall Wace, and Fin Capital.

The BlackRock piece was the tell. This wasn’t just capital. It was institutional validation. BlackRock entered a broader strategic partnership with Circle, including exploring capital markets applications for USDC and serving as the primary asset manager of USDC’s cash reserves. The Circle Reserve Fund would be custodied at The Bank of New York Mellon and managed by BlackRock. In other words, the dollars behind USDC were now being handled by the same names that sit at the center of global finance.

With that momentum, Circle tried to do what every fast-growing fintech wanted to do in 2021: go public. It announced plans for a SPAC merger with Concord Acquisition Corp, valuing the company at $4.5 billion. Management talked up continued growth. But the SPAC market collapsed under its own hype, and Circle’s deal ultimately fell apart amid volatility and regulatory uncertainty. At the time it looked like a setback. In hindsight, it may have spared Circle from being publicly judged at exactly the wrong moment in the cycle.

Because the moment that followed nearly broke the company.

On March 10, 2023, Circle disclosed that $3.3 billion of USDC’s roughly $40 billion in reserves were held at Silicon Valley Bank when the bank collapsed. The market didn’t wait for nuance. USDC started slipping—and then it fell hard. By 2 a.m. on March 11, it traded as low as $0.87. The stablecoin built to be the safest dollar in crypto was suddenly down 13%, and panic ripped through the system as traders rushed to exit.

The irony was brutal. Circle had spent years building a “clean” stablecoin story: transparent reserves, regulatory compliance, blue-chip partnerships. And yet the threat didn’t come from some shadowy offshore entity. It came from a very normal-looking U.S. bank—exactly the traditional financial system Circle was supposed to make more reliable.

What saved USDC wasn’t crypto. It was the government. The FDIC made an exceptional decision to guarantee all deposits at SVB beyond the standard $250,000 insurance limit. By Monday morning, Allaire could tell the market, “100% of deposits from SVB are secure and will be available at banking open tomorrow.” USDC snapped back to its peg.

But the episode left a mark. USDC and Tether had nearly reached parity in market share in 2022, and then USDC’s position weakened after the SVB shock—because in stablecoins, trust isn’t a tagline. It’s the product. Circle responded by tightening the entire risk posture: it moved cash reserves to The Bank of New York Mellon and, by late 2023, announced a $1 billion cash cushion intended to help the company withstand future stress.

Circle had survived its near-death weekend. But it came out with a clearer understanding of what it was really building. Not just software. Not just crypto rails. Financial infrastructure—where the hardest problems aren’t always technological, and where the failures that matter most can still come from the old world.

VI. The IPO Spectacle & Public Market Debut (2024–2025)

In January 2024, Circle filed a confidential S-1 with the Securities and Exchange Commission. After years of almosts—the SPAC that evaporated, the SVB weekend that nearly shattered trust—the company was finally choosing the hardest path: letting public markets judge the business, in real time, every day.

Then April 2025 delivered a curveball. Ripple Labs offered to buy Circle for $4 to $5 billion. Circle said no. And that “no” was revealing: a company that had watched its flagship product briefly break the buck just two years earlier was now turning down a multi-billion-dollar exit because it believed it was worth more in the open market. With USDC circulation above $60 billion and 2024 revenue of $1.68 billion, Ripple’s offer implied a valuation of only a few times revenue—cheap, if you believed stablecoins were becoming permanent infrastructure.

On June 5, 2025, Circle stepped onto the stage. The IPO priced at $31 per share—well above the expected $24 to $26 range—valuing the company at about $6.9 billion and raising $1.1 billion. And then the market did what the market does at the peak of excitement: it re-priced Circle in public, instantly, and violently upward. The stock opened into a frenzy, hit $95 on day one, and closed at $82.84—up 167%. By the end of the next trading day, shares had reached $107.50.

That kind of first-week surge makes headlines, but it also creates a different kind of story: who got the upside. The gap between the IPO price and where the stock traded almost immediately became an emblem of “money left on the table.” The $1.76 billion shortfall between the IPO price and the first-day close ranked as the seventh largest for any IPO since 1980, according to University of Florida professor Jay Ritter. In plain terms, a huge chunk of the early gains flowed not to Circle, but to the underwriters’ institutional clients—one of the oldest rituals in public markets, and a sharp reminder that even sophisticated fintechs don’t control the IPO machine.

By late June 2025, the exuberance peaked. Circle’s market cap briefly touched $56 billion—roughly a 700% move from the IPO price. Investors weren’t just buying a company; they were buying the idea that stablecoins were the next major financial primitive, and that Circle was the regulated, institution-friendly winner.

But the spell broke. In the second half of 2025 and into early 2026, the stock corrected hard. From a peak near $299 per share, CRCL fell to around $64 by late January 2026—down more than 75%—and the market cap reset to roughly $15 billion. The drivers were familiar: weaker crypto sentiment, worries that potential interest rate cuts would reduce the reserve income that powers Circle’s earnings, and the simple fact that even strong businesses don’t live forever at valuations that imply perfection.

Circle’s public debut ended up capturing the entire emotional cycle of modern markets: euphoria first, spreadsheets later. The early surge was the market’s excitement about owning a pure-play stablecoin company. The drawdown was the market rediscovering that Circle’s fortunes are tightly linked to earnings, competition, and the Federal Reserve. For long-term investors, the debate shifted to a tougher question: at roughly a $15 billion valuation—about 91 times trailing earnings—was Circle finally reasonably priced for its next chapter, or still too expensive for a business whose core economics move with interest rates?

VII. Business Model & The Stablecoin Money Machine

The genius of Circle’s business model is its simplicity. While much of crypto chases complex yield strategies and grand infrastructure visions, Circle mostly makes money the old-fashioned way: it holds dollars and earns interest on them.

The machine works like this. When someone turns a dollar into USDC, Circle takes that dollar and places it into low-risk, interest-bearing assets—mostly short-term U.S. Treasuries and government money market funds. Circle earns the interest while the USDC stays in circulation, and when the token is redeemed, the dollar goes back out. It looks a lot like a bank’s deposit business, except Circle doesn’t make loans. That cuts out credit risk, but it also caps how aggressive returns can be.

For most of 2020 and 2021, that wasn’t a great business. Interest rates were near zero, so there wasn’t much to earn. Then the Federal Reserve started hiking aggressively in 2022 to fight inflation, and suddenly every dollar of USDC in circulation became a meaningful income-producing asset. At scale—tens of billions of dollars—small changes in rates turn into very large swings in revenue.

By Q3 2025, the model’s power was hard to miss. Total revenue and reserve income reached $740 million, up 66% year-over-year. Net income rose 202% to $214 million. USDC circulation was up 108% year-over-year to $73.7 billion, and on-chain USDC transaction volume jumped 580% to $9.6 trillion for the quarter.

Circle has tried to make the reserves as boring as possible—and that’s the point. The portfolio is custodied at The Bank of New York Mellon and managed by BlackRock, invested primarily through the Circle Reserve Fund, an SEC-registered government money market fund. No commercial paper. No corporate bonds. No reaching for yield. Mostly U.S. government securities and cash. That conservatism is a feature, not a constraint: monthly attestations from Grant Thornton, daily reporting from BlackRock, and a compliance-first posture are how Circle sells trust at internet scale.

Distribution is the other flywheel. Circle doesn’t need to win every end customer directly. Through exchanges, wallets, and payment platforms, USDC gets embedded across the ecosystem and becomes accessible to hundreds of millions of end users. Each integration is a channel, and each channel makes the stablecoin more useful—without Circle having to run a consumer acquisition machine.

Then there’s the moat that’s harder to copy: regulation. Circle holds licenses in 46 U.S. states, has the New York BitLicense, and became the first global stablecoin issuer to achieve MiCA compliance in Europe. Replicating that footprint isn’t just paperwork—it’s years of work and real money.

But Circle pays for distribution—especially Coinbase. Coinbase receives 50% of the “residual payment base,” a portion of the revenue generated from reserves backing USDC. Total distribution costs reached $448 million in Q3 2025, up 74% year-over-year. That hits margins, but it also keeps incentives aligned with one of the most powerful distribution engines in crypto.

In theory, the model scales incredibly well: another billion in USDC circulation doesn’t require anything like a billion dollars of additional operating expense. The big vulnerability is also obvious: interest rate sensitivity. If rates fall back toward zero, reserve income shrinks fast even as many costs stick around. Circle has been working to diversify, guiding to $90 to $100 million of “Other Revenue” in 2025 from products like the Cross-Chain Transfer Protocol and platform services, but reserve income still drives the story.

If you’re trying to understand Circle’s business in a handful of metrics, two matter most. First: average USDC in circulation—the deposit base—and it grew 97% year-over-year to $67.8 billion in Q3 2025. Second: the RLDC margin, or Reserve Less Distribution Costs as a percentage of revenue, which management guided to about 38% for 2025. Together, those two numbers capture the core reality: how big the base is, and how much of the interest Circle keeps after paying for distribution.

VIII. Competition & Market Dynamics

In the stablecoin wars, there is Tether, there is Circle, and then there is everyone else fighting for scraps. But the real competition isn’t as simple as a leaderboard. It’s about where each coin is used, who trusts it, and what tradeoffs each issuer is willing to make.

Tether (USDT) is still the heavyweight. With a market cap around $160 billion—more than 60% of the stablecoin market—its dominance can feel inevitable. USDC, at roughly 29% as of Q3 2025 (up from 23% a year earlier), is gaining share, but it’s been chasing from behind since day one. Tether launched in 2014—four years before USDC—and that head start compounded into something real: default trading pairs, deeper exchange liquidity, and habits that are brutally hard to unwind.

But the more interesting signal isn’t market cap. It’s movement. According to data compiled by Visa, USDC overtook Tether in stablecoin transaction volume in April 2024. In other words: even if USDT is bigger, USDC is increasingly the one doing the work—especially in the U.S. and with institutions. Circle’s own Q3 2025 figures echoed that shift: USDC on-chain transaction volume hit $9.6 trillion for the quarter, up 580% year-over-year.

Under the hood, this is a story about regulation as strategy. Circle positioned USDC as the stablecoin built to survive scrutiny, and in July 2024 it became the first global stablecoin issuer to receive approval under Europe’s MiCA framework. Tether took the opposite posture, criticizing MiCA’s requirements and refusing to comply. That split creates a clean trade: Tether keeps its growth and reach by staying flexible in gray zones, while Circle gives up some speed in exchange for a form of credibility that regulated institutions require.

Geography makes the divide even clearer. USDC tends to dominate in the U.S. where compliance-heavy use cases matter. USDT tends to dominate outside the U.S. as a practical dollar proxy—especially in emerging markets where access to dollars is constrained and availability often matters more than regulatory pedigree. And despite the “payments” narrative around stablecoins, USDC is still largely crypto plumbing: more than 75% of supply is used in DeFi or on exchanges, at least for now.

Meanwhile, the pack behind them is getting more crowded. PayPal’s PYUSD, issued in partnership with Paxos, brings a different kind of threat: instant consumer distribution. Ripple’s RLUSD reached $600 million in market cap. Banks are exploring their own stablecoins and “deposit coins.” And by January 2026, Compass Point analysts were calling out a new wave—names like USDH and CASH—as early examples of smaller stablecoins beginning to nibble at share.

Then there’s MakerDAO’s DAI, which competes on ideology as much as function. It’s a decentralized stablecoin designed to minimize reliance on any single company. For users who worry that issuer-backed stablecoins are one government order away from frozen funds, DAI’s censorship resistance is the point—even if it comes with its own complexities.

Profitability comparisons between USDT and USDC are revealing, but they’re also incomplete. Tether’s larger reserve base and potentially higher-yielding—and riskier—approach likely produces more absolute profit. Circle’s advantage is that investors can actually see the math. That transparency gap matters: for regulated entities and institutions, “trust me” is not an investment thesis. Verified reserves are table stakes.

And hovering over everyone is the CBDC question: what happens if governments issue their own digital currencies? A true Fed-issued digital dollar could make parts of the private stablecoin market feel redundant. Europe’s digital euro effort and China’s digital yuan continue to advance. But in the U.S., political appetite for a CBDC has looked limited, and most observers expect a messy coexistence—government rails in some places, private stablecoins in others—rather than a clean replacement.

For now, the market is big enough for multiple models. But the fight is getting sharper. Circle’s next chapter will be defined by a single challenge: growing USDC against Tether’s liquidity machine while holding off the new entrants trying to copy the playbook—or reinvent it.

IX. Strategic Initiatives & Future Bets

Circle’s future isn’t just about defending USDC’s market share. The company’s roadmap reads like a bid to become the default infrastructure layer for moving value online—stablecoins today, and broader financial rails tomorrow.

One of the biggest swings is Arc, a proprietary blockchain Circle has been building for stablecoin payments, foreign exchange, and capital markets use cases. The positioning is deliberate: Arc isn’t trying to be the next general-purpose chain fighting for DeFi users and NFT activity. It’s meant to be boring in the way banks want—built for moving money with sub-second finality, negligible transaction costs, and compliance features baked in. The pitch is simple: institutions want blockchain efficiency, but they can’t live with blockchain chaos. Arc is Circle’s attempt to give them the former without the latter.

Another pillar is Circle Gateway, which aims to make USDC feel truly “one” asset across a fragmented, multi-chain world. Today, USDC exists on Ethereum, Solana, Avalanche, and a long list of other networks. Moving it between those chains can be slow, expensive, and—because bridging is a common attack surface—genuinely risky. Gateway’s promise is that a user can deposit USDC on one chain and withdraw on another, while Circle handles the complexity behind the scenes.

This is the same core idea behind Circle’s Cross-Chain Transfer Protocol (CCTP), which is already live and getting real usage. By Q3 2025, CCTP had facilitated more than $31.3 billion in USDC transfers, with volume up 7.4x year-over-year. That matters because it subtly changes what Circle is. If USDC is the product, CCTP is the network—and networks can charge tolls.

Geographic expansion is the other big lever. Circle’s euro-backed stablecoin, EURC, had become the largest euro-backed stablecoin by circulation and surpassed $1 billion in weekly transfer volume. With MiCA compliance secured, Circle entered Europe with the same playbook it used in the U.S.: win by being early, compliant, and institution-friendly. And if EURC works, the obvious next question is whether Circle can replicate the model with other currencies and build an interoperable portfolio of regulated digital cash.

Then there are emerging markets, where the demand signal can be even stronger. In places with volatile local currencies or weak banking access, USDC can function as a stable store of value and a bridge to the global economy. But this is where Circle’s challenge stops being technical. Reaching those users depends on partnerships—mobile money operators, remittance providers, local fintechs. The technology may be global, but distribution is still painfully local.

And perhaps Circle’s most important product decision is philosophical: make crypto disappear. Circle’s APIs and developer tools are built to hide blockchain complexity so businesses can add “digital dollars” without needing to understand smart contracts or manage private keys. The bet is that stablecoins go mainstream the same way the internet did—not because people learned the underlying protocols, but because those protocols became invisible.

All of this is starting to show up in the numbers at the margins. Management raised its 2025 “Other Revenue” guidance to $90 to $100 million, suggesting these non-reserve-income businesses are beginning to matter. But the reality remains: reserve income is still the engine, and these initiatives are still, in large part, bets. The investor question is straightforward—and existential. Can Circle turn itself from a one-product earnings story into a broader financial infrastructure platform before interest rate cuts compress the economics that made the last chapter so lucrative?

X. Playbook: Business & Investing Lessons

Circle’s path—from a Bitcoin wallet to a publicly traded company building digital-dollar infrastructure—reads like a case study in how to pivot without losing the plot. Strip away the crypto buzzwords, and the lessons are surprisingly universal: strategy matters, trust matters more, and the “boring” choices can end up being the most valuable ones.

Start with regulatory arbitrage. Circle’s biggest edge wasn’t some secret algorithm or breakthrough protocol. It was a decision about where to play. While much of crypto chased growth in the gray, Circle chose the slower, more expensive route: compliance. For years, that looked like self-sabotage—especially with Tether racing ahead. But as institutions arrived and scrutiny intensified, Circle’s licenses, policies, and reporting standards turned into something that’s hard to buy and slow to build. In markets that eventually get regulated, being early to the rules can be a stronger moat than being early to the product.

Circle’s reinventions tell a second lesson: pivots don’t have to mean surrender. Circle moved from Bitcoin wallet to payments app to exchange operator to stablecoin infrastructure. From the outside, it could look like a company that kept giving up on its last idea. But the throughline never changed. The mission was always the same—make money move like information. What changed was the vehicle. The difference between thrashing and true iteration is whether the core insight stays intact while the implementation evolves.

Then there’s the most uncomfortable truth Circle learned the hard way: in crypto, you’re only as safe as your banking relationships. The SVB weekend wasn’t a failure of smart contracts or cybersecurity. It was a traditional bank run. Circle’s product may live on blockchains, but its credibility still rests on the legacy system that holds the reserves. When you build a bridge between old finance and new finance, the old system’s failures become your failures. That’s why the move to shift reserves to The Bank of New York Mellon and build a $1 billion cash cushion wasn’t a nice-to-have—it was survival strategy.

The Poloniex saga is the capital allocation lesson. Buying an exchange for $400 million sounded like “full-stack crypto” ambition. In practice, it meant integration pain, inherited liabilities, and an expensive exit that left Circle with a $156 million loss. Compare that with the BlackRock relationship: a partnership that strengthened Circle’s credibility and reserve management without importing a new set of operational and regulatory problems. In platform markets, being essential plumbing often beats owning everything connected to the pipes.

For investors, Circle is also a reminder that a great business and a great stock are not the same thing. Circle’s shares went from a $31 IPO price to a peak near $299, then fell to around $64 by early 2026. The underlying business didn’t whip back and forth that dramatically. What changed was the market’s appetite to pay for growth, and its assumptions about interest rates—the key driver of Circle’s reserve income. The lesson isn’t “don’t buy growth.” It’s that valuation is a separate decision from quality, and markets can swing from euphoria to discipline faster than fundamentals move.

And finally: winning a technology transition is often about delivering what people actually need, not what they think they want. Circle didn’t win by making Bitcoin easier. It won by making dollars usable on the internet. In the end, Circle’s most important innovation wasn’t inventing a new kind of money. It was turning the most familiar kind—cash—into software.

XI. Analysis & Bear vs. Bull Case

The Bull Case

The optimistic view is that Circle is becoming a real financial institution—just one that runs on internet rails. Not a crypto app, not an exchange, but the issuer and operator of what could become a standard layer for moving dollars globally.

The first pillar is regulation, which is finally moving from “looming risk” to “clear rules.” In the U.S., proposals like the CLARITY Act point toward a framework that looks a lot like what Circle has already been doing: full reserves, regular attestations, and regulatory oversight. If the law ends up rewarding that approach, Circle isn’t adapting to a new world—it’s already built for it. And that matters because compliance isn’t something you bolt on at the end. It’s years of licensing, controls, audits, bank relationships, and behavior.

The second pillar is growth. Management has talked about a 40% compound annual growth rate for USDC circulation. Against recent performance, bulls argue that doesn’t sound wildly aggressive. USDC circulation grew 108% year-over-year to $73.7 billion in Q3 2025, and meaningful wallet addresses increased 77% to 6.3 million. If stablecoins expand beyond crypto trading and DeFi into treasury management, cross-border payments, and mainstream fintech workflows, the ceiling stops looking like “tens of billions” and starts looking like “hundreds of billions.”

Third is the institutional wave. Circle’s partners aren’t fringe crypto entities; they include names like BlackRock, Fidelity, and BNY Mellon. Bulls see that as a strategic position that’s hard to replicate. If banks, payment processors, and large enterprises adopt stablecoins in a serious way, Circle is already sitting in the meetings—and, in many cases, already integrated.

Finally, there are the network effects. USDC runs across more than twenty blockchain networks. Circle’s Cross-Chain Transfer Protocol is scaling fast, with volume up 7.4 times year-over-year. Each additional chain, wallet, exchange, and payment platform makes USDC more useful, and usefulness drives more integration. It’s the same flywheel that made card networks so durable: once the rails are everywhere, the default becomes very hard to displace.

Put through Hamilton Helmer’s 7 Powers lens, bulls see multiple defensible advantages: network economies (more USDC in circulation creates more liquidity and utility), switching costs (it’s painful for applications to migrate their core settlement asset), and counter-positioning (competitors like Tether can’t easily copy Circle’s compliance-first strategy without fundamentally changing how they operate).

The Bear Case

The skeptical view starts with a simple point: Circle’s story may be “the digital dollar,” but its earnings are still heavily tied to interest rates.

Reserve income is the engine. When the Fed holds rates high, the model throws off cash. When rates fall, the machine slows down—fast. If rates ever move back toward zero, reserve income compresses dramatically. And Circle’s costs don’t all flex down with it. In Q3 2025, distribution costs alone were $448 million, and a meaningful portion of those payments—especially to partners like Coinbase—doesn’t automatically shrink just because the yield on Treasuries does. In a low-rate environment, bears argue Circle could end up closer to breakeven, even if USDC remains widely used.

Then there’s the uncomfortable durability of Tether. Despite years of controversy, USDT still holds more than 60% market share. It has the deepest liquidity, entrenched trading pairs, and strong penetration in emerging markets where availability often beats pedigree. Bears worry this becomes a familiar tech outcome: the “better” product loses to the “good enough” incumbent because inertia is a feature, not a bug.

Competition is also coming from every angle. PayPal has PYUSD. Ripple has RLUSD. Smaller challengers like USDH and CASH are emerging. And the looming question is what happens when major banks launch their own stablecoins. If JPMorgan or Bank of America offers a stablecoin-native cash product, do corporate clients stick with USDC, or default to the coin issued by the bank they already use?

Step back and the structure looks like a tough industry. Using Porter’s Five Forces: supplier power is concentrated (BlackRock manages reserves, BNY Mellon provides custody, Coinbase captures 50% of residual revenue), buyer power rises as alternatives increase, substitutes are everywhere (bank stablecoins, CBDCs, competing tokens), and even the regulatory moat may shrink once rules crystallize and new licensed entrants can follow the playbook.

That Coinbase revenue share is its own bear case. Handing a distribution partner half the residual revenue can be rational when you’re buying scale and liquidity. But it’s also a dependency that puts a ceiling on margin expansion, and it raises an obvious strategic risk: if Coinbase ever shifts incentives toward a different stablecoin, Circle feels it immediately.

Finally, valuation risk hasn’t disappeared just because the stock corrected. At roughly a $15 billion market cap and around 91 times trailing earnings, the stock still assumes meaningful growth and a favorable rate environment. Any combination of slower USDC expansion, rate cuts, or regulatory friction could force another repricing. The 75% decline from peak into early 2026 suggests expectations already came down sharply—but the question is whether they came down enough.

The Synthesis

The most realistic outcome is probably in the middle. Stablecoins look like they’re here to stay, and Circle is arguably the best-positioned regulated issuer. But “best-positioned” doesn’t guarantee that USDC becomes the default everywhere, and Circle’s sensitivity to interest rates makes it more cyclical than many investors want to admit.

If you want the story in two metrics, watch these. First: average USDC in circulation, the “deposit base” that creates reserve income, which grew 97% year-over-year in Q3 2025. Second: RLDC margin, management-guided to about 38% for 2025, which captures how much Circle keeps after paying distribution partners. Together, they tell you whether Circle is winning on both fronts that matter: scale, and economics.

XII. Epilogue & Reflections on the Digital Dollar's Future

If you were sitting in Jeremy Allaire’s chair in early 2026, it would feel less like victory laps and more like flying through turbulence after the adrenaline wears off. Circle’s stock had done the full round trip: from a $31 IPO price, up to a peak near $299, and back down to roughly $64. Crypto was recalibrating. Public markets were, too. The analyst narrative that once sounded like a chorus had split into camps. In late January 2026, firms like Mizuho and Compass Point moved to neutral—essentially saying, “we see the promise, but we also see the fragility,” especially around crypto correlation and interest rate risk. And with the next earnings report set for February 25, 2026, investors were going to ask the obvious question: did Q3’s momentum carry into Q4, or was it the high-water mark?

The next chapter hinges on a challenge that’s both simple and hard: Circle needs to become less dependent on interest income before interest rates potentially compress it. Arc, CCTP, Gateway, and EURC are the right kinds of bets, but none has yet grown large enough to cushion a real decline in reserve income. Management’s target of $90 to $100 million in “Other Revenue” for 2025 is meaningful progress. But next to the kind of quarterly revenue Circle was producing at the peak, it’s still small—more proof of direction than a replacement engine.

If Circle wants to keep expanding, the smartest geographic strategy may be to stop fighting only for the center of the map. The U.S. and Europe are crowded battlefields—heavily regulated, highly competitive, and packed with incumbents. The sharper edge is at the periphery: Southeast Asia, Africa, and Latin America, where stablecoins aren’t a future use case but a present-day tool. In places like Lagos or Manila, holding USDC instead of a volatile local currency isn’t about “web3.” It’s about stability. Those are users and flows that Tether serves today—and that PayPal and potential bank stablecoins may be less naturally positioned to reach.

Capital allocation has its own lesson written in permanent ink: no more Poloniex-style empire building. If Circle does M&A, it has to be surgical—small acquisitions that buy specific missing pieces, not sprawling ambitions. Think targeted capabilities: a European e-money license, an Asian payment network, or a DeFi protocol with technology Circle can actually integrate and productize.

And then there’s the most counterintuitive option: instead of trying to “win” stablecoins the way social networks win attention, Circle could try to win by making itself useful to everyone—including competitors. If USDC becomes the interoperability layer, the universal translator that routes liquidity between chains, wallets, and even other stablecoin ecosystems, Circle can win even when market share ebbs and flows. When every stablecoin needs USDC to move safely and efficiently across platforms, Circle stops looking like a coin issuer and starts looking like infrastructure.

That’s the real arc of the story. The internet took information—something physical, slow, and local—and turned it into something digital, instant, global, and programmable. Circle is trying to do the same for value. It has already proven that the transformation is possible. Whether Circle is the company that finishes the job, or the pioneer that clears the path for others, is still an open question.

What isn’t open is the direction of travel. Money is becoming digital. Digital money needs stable infrastructure. And Circle—whatever the stock chart says in any given month—has built a version of that infrastructure that a large part of the market trusts. The question now isn’t whether it matters. It’s how much it’s worth, and who ultimately gets to control the rails.

XIII. Recent News

The first weeks of 2026 brought a reset in how Wall Street talked about Circle. On January 28, Mizuho moved CRCL up to neutral from underperform, pointing to a surge in activity on Polymarket—the crypto prediction platform—as an underappreciated driver of USDC demand. The analyst also raised forecasts for average USDC in circulation for 2026 and 2027 by roughly 7% and 21%, respectively. The next day, Compass Point analyst Ed Engel followed with his own upgrade to neutral, while cutting his price target to $60 and arguing that Circle had started trading less like a standalone fintech and more like a proxy for the broader crypto cycle.

There were also early signs of cooling. USDC supply fell about 9% from its December 2025 peak—nothing catastrophic, but the kind of data point that gets watched closely when a company’s earnings engine depends on how much USDC is out in the world. At the same time, newer stablecoins kept nibbling at the edges of the market, and the pending CLARITY Act in Congress loomed as a potential inflection point—either reinforcing Circle’s compliance advantage or clearing the runway for well-capitalized bank competitors.

Some insider activity added to the chatter. Director and co-founder Patrick Sean Neville sold 35,000 shares of Class A common stock in January. It drew attention, but it was still only a small fraction of his overall stake. The next real gut-check was on the calendar: Circle’s Q4 2025 earnings report, expected February 25, 2026, which would show whether the second-half growth story held up as crypto markets cooled.

Meanwhile, Cathie Wood’s ARK Invest kept buying CRCL during the selloff—a visible vote of confidence from one of crypto’s most prominent institutional believers. And the stock’s 52-week range, from $31 to $299, told the whole emotional story in one line: conservative IPO pricing, a burst of euphoria, and then the long walk back to reality.

XIV. Links & Resources

SEC filings: Circle’s S-1 registration statement, plus ongoing quarterly and annual reports (10-Q and 10-K), are available through the SEC’s EDGAR database. They’re the most direct source for the company’s financials, risk factors, and how USDC reserves are structured.

Circle pressroom: Circle posts quarterly results and major announcements at circle.com/pressroom, including the Q3 2025 release that reported $740 million in revenue and $214 million in net income.

USDC reserve reports: Monthly attestation reports from Grant Thornton are published on Circle’s transparency page. If you want to understand whether USDC’s backing is as solid as advertised, start here.

Key interviews: Jeremy Allaire has done a long run of interviews on Bloomberg, CNBC, and crypto podcasts, where he lays out Circle’s strategy, regulatory posture, and the broader “digital dollars” thesis in his own words.

Industry research: Visa’s stablecoin transaction-volume data, DeFiLlama’s dashboards on USDC usage across protocols, and Chainalysis reports on stablecoin flows provide independent lenses on what’s happening beyond Circle’s own reporting.

Regulatory frameworks: Europe’s MiCA regime—where Circle received the first stablecoin approval in July 2024—proposed U.S. legislation such as the CLARITY Act, and state-by-state money transmitter rules all shape Circle’s competitive landscape.

Academic context: Research on stablecoin economics from institutions like the Bank for International Settlements and the Federal Reserve helps frame the bigger question: how private “digital dollars” interact with monetary policy, banking, and financial stability.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube