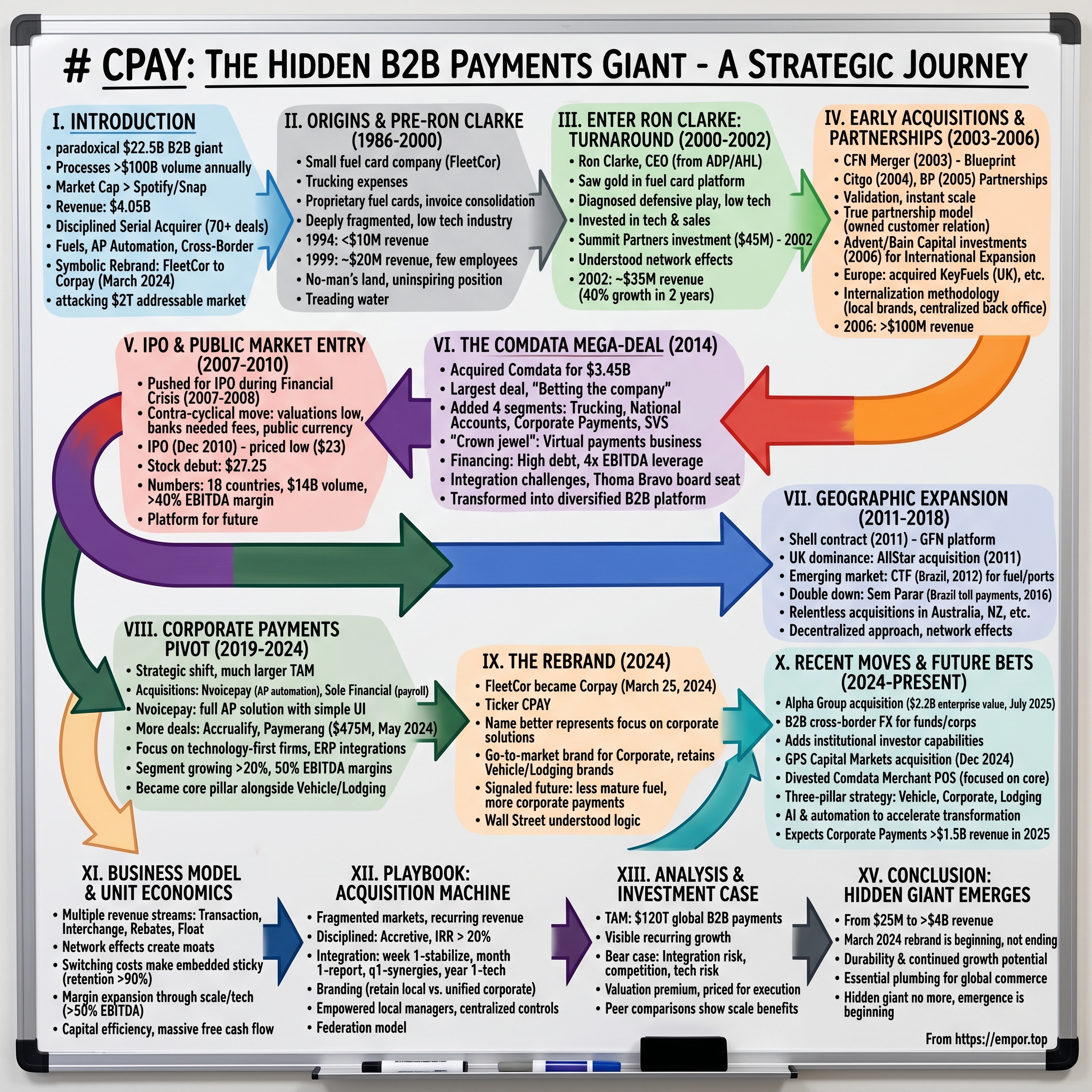

Corpay: The Hidden B2B Payments Giant

I. Introduction & Episode Roadmap

Picture this: A company processing over $100 billion in annual payment volume, operating in 170 countries, with a market capitalization larger than Spotify or Snap. Yet if you asked ten people on the street—even ten reasonably informed investors—to explain what Corpay does, you'd likely get ten blank stares.

This is the paradox of Corpay, the $22.5 billion B2B payments behemoth that most people have never heard of. With $4.05 billion in revenue and commanding positions in multiple payment verticals, it's one of the most successful serial acquirers in fintech history. But unlike flashy consumer brands or crypto unicorns, Corpay has built its empire in the unsexy trenches of corporate fuel cards, accounts payable automation, and cross-border B2B payments.

The question that should fascinate any student of business is this: How did a struggling fuel card processor with just $25 million in revenue in 2000 transform into a global payments powerhouse? The answer involves one of the most disciplined acquisition machines ever built, a CEO who saw gold where others saw rust, and the patience to compound returns in markets everyone else ignored.

In March 2024, the company made a symbolic break with its past, rebranding from FleetCor Technologies to Corpay. The name change wasn't just cosmetic—it reflected a fundamental transformation. What started as a fleet fuel card company had evolved into something much bigger: a comprehensive B2B payments platform attacking a $2 trillion addressable market.

This is the story of how Ron Clarke and his team built a fintech roll-up machine that would make even the most aggressive private equity firms jealous. It's about finding inefficiencies in fragmented markets, the power of network effects in B2B payments, and why the most boring businesses often make the best investments. Along the way, we'll explore over 70 acquisitions, multiple near-death experiences, and the counterintuitive strategies that turned a niche processor into a global giant.

What you're about to learn isn't just the Corpay story—it's a masterclass in building through acquisitions, creating value in mature markets, and why B2B payments might be the greatest business model nobody talks about.

II. Origins & The Pre-Ron Clarke Era (1986–2000)

In 1986, while Michael Milken was revolutionizing junk bonds and Microsoft was going public, a small company called FleetCor was founded with a decidedly less glamorous mission: helping trucking companies manage their fuel expenses. The founders weren't Silicon Valley visionaries or Wall Street wonderkinds—they were operations people who saw a specific pain point in commercial transportation and built a narrow solution.

The original business model was almost quaint by today's standards. FleetCor issued proprietary fuel cards to commercial fleet operators—trucking companies, delivery services, local governments. Drivers would use these cards at participating gas stations, and FleetCor would handle the back-office headache: consolidating invoices, applying negotiated discounts, providing spending reports. In an era of paper receipts and manual expense reports, it was a genuine improvement. But it was also a business with natural limitations.

For fourteen years, FleetCor operated in this sleepy niche, growing at a pace that would make a utility company yawn. The industry context explains why: fleet management in the 1990s was deeply fragmented, relationship-driven, and resistant to change. Fleet managers—often grizzled operations veterans—trusted their local fuel suppliers and saw little reason to adopt new payment systems. Technology adoption was glacial. Many companies still reconciled fuel expenses by having drivers submit paper logs.

The numbers tell the story of stagnation. By 1994, eight years after founding, FleetCor had barely crossed $10 million in revenue. Growth came in dribs and drabs—winning a municipal fleet here, adding a trucking company there. The company's technology infrastructure was basic at best, essentially a glorified database with some reporting capabilities. Marketing consisted of cold-calling fleet managers and attending regional trucking conferences. The company's competitive position was equally uninspiring. Regional fuel card providers dominated local markets through personal relationships. National players like Wright Express (later WEX) had superior technology and scale. Oil companies issued their own proprietary cards. FleetCor was stuck in no-man's land—too small to compete on scale, too generalist to win on specialization.

By 1999, revenue had crawled to approximately $20 million. The company employed fewer than 100 people, mostly in back-office processing roles. Technology investment was minimal—the core platform was aging, customer interfaces were primitive, and data analytics capabilities were essentially non-existent. The board, composed mainly of early investors and industry veterans, seemed content with modest returns and limited ambitions.

The turn of the millennium found FleetCor at $25 million in revenue—a 15-year-old company that had grown at roughly 10% annually since inception. It wasn't failing, but it wasn't thriving either. It was the corporate equivalent of treading water: generating enough cash to survive but lacking the vision or resources to transform. The fuel card industry itself seemed destined to remain a backwater of B2B payments, dominated by oil companies and regional players, with limited innovation and glacial consolidation.

What nobody could have predicted was that this sleepy processor was about to become the foundation for one of the most successful serial acquisition strategies in fintech history. The raw materials were there—a fragmented market, recurring revenue streams, network effects potential—but it would take new leadership to see the opportunity hiding in plain sight.

III. Enter Ron Clarke: The Turnaround Begins (2000–2002)

In August 2000, a 42-year-old executive named Ron Clarke walked into FleetCor's modest offices for his first day as CEO. The board had hired him after an exhaustive search, desperate for someone who could breathe life into their stagnant business. What they got was something more: a leader who would orchestrate one of the most successful transformations in B2B payments history.

Clarke came from AHL Services, where he served as chief operating officer of the staffing and marketing services outsourcer. But his real education had come earlier, during eight years at Automatic Data Processing (ADP) from 1990 to 1998, where he rose from Chief Marketing Officer to Division President. At ADP, he'd learned the power of recurring revenue, the importance of scale in processing businesses, and most critically, how to spot inefficiencies in fragmented markets.

His background also included time as a Principal at Booz Allen Hamilton and as a marketing manager at General Electric—a classic corporate pedigree that suggested competence but not necessarily vision. Yet Clarke saw something in FleetCor that others had missed. Where the board saw a struggling fuel card processor, Clarke saw a platform for consolidating one of the most fragmented markets in business payments.

The early days were about diagnosis, not treatment. Clarke spent his first months talking to customers, analyzing competitors, and most importantly, understanding why FleetCor had stagnated. The answers were revealing: the company had been playing defense for years, focused on retaining existing customers rather than winning new ones. Technology investment had been minimal. The sales force was undersized and undertrained. Most damaging, there was no coherent growth strategy beyond hoping for incremental market share gains.

Clarke's initial strategic shifts were subtle but fundamental. First, he began investing in technology—not bleeding-edge innovation, but basic infrastructure that would allow FleetCor to process transactions more efficiently and provide better data to customers. Second, he rebuilt the sales organization, hiring experienced B2B salespeople and implementing disciplined sales processes borrowed from his ADP days. Third, and most importantly, he began developing what would become the FleetCor acquisition playbook.

The validation came in 2002 when Summit Partners, the Boston-based venture capital firm, invested $45 million in FleetCor to expand and recruit major regional and national convenience stores into the fleet program. This wasn't just capital—it was a vote of confidence from sophisticated investors who saw the same opportunity Clarke did. Summit's involvement brought more than money; it brought discipline around financial reporting, board governance, and most critically, a framework for evaluating acquisitions.

What made Clarke different from his predecessors wasn't just ambition—it was his understanding that the fuel card business was fundamentally a network effects business disguised as a payment processor. Every new customer made the network more valuable to merchants. Every new merchant made the network more valuable to customers. The key was reaching critical mass, and in a fragmented market, that meant consolidation.

By the end of 2002, FleetCor's revenue had grown to approximately $35 million—a 40% increase in just two years. More importantly, the foundation was in place for what would come next: a systematic rollup of the fuel card industry that would transform FleetCor from a bit player into the dominant force. The sleepy processor was waking up, and Ron Clarke was just getting started.

IV. Building the Foundation: Early Acquisitions & Partnerships (2003–2006)

The merger with Commercial Fueling Network (CFN) in 2003 marked FleetCor's transformation from organic grower to serial acquirer. CFN brought a complementary network of cardlock fueling locations—unmanned commercial fueling sites primarily used by truckers. But more importantly, it proved that Clarke could execute on his consolidation thesis. The integration went smoothly, synergies materialized faster than expected, and suddenly FleetCor had a blueprint for growth. In 2004, the company partnered with Citgo to process Citgo Petroleum Corp.'s commercial fleet card, the CITGOFleet card. In 2005, Fleetcor began a relationship with BP, a contract that has since been extended several times. These weren't just vendor agreements—they were transformative partnerships that validated FleetCor's business model and provided instant scale.

The Citgo deal came first, a hard-fought victory stolen from a competitor. Bill Schmit, president of FleetCor's Private Label Division, would later recall the intensity of that pursuit. Since winning the CITGO business from a competitor in 2004, FleetCor has worked hard to earn the respect of CITGO, its branded marketers and the end customers of its branded fleet-card program. The partnership gave FleetCor processing rights for thousands of Citgo-branded cards, dramatically expanding its transaction volume overnight.

The BP relationship that began in 2005 would prove even more significant. BP has been a FLEETCOR partner since 2005, offering flexible, customized fueling options through the BP Business Solutions fleet program. Unlike traditional processor relationships where the oil company maintains control, FleetCor negotiated a true partnership structure. They would jointly develop products, share economics, and most importantly, FleetCor would own the customer relationships. This model would become the template for every major oil partnership that followed.

What Clarke understood—and what his predecessors had missed—was the power of network effects in the fuel card business. Every new merchant location made the card more valuable to fleet customers. Every new fleet customer made the network more attractive to merchants. The partnerships with Citgo and BP didn't just add volume; they added thousands of accepting locations, creating a virtuous cycle of growth.

In 2006, the company attracted its next major institutional investor. With the addition of an investment of $46 million in equity from Advent in 2006 for European expansion, Fleetcor launched British Petroleum (BP) Mastercard, a North American major oil co-branded fleet card, and introduced FleetCardsUsa.com, a fleet card web portal. But the real story was Bain Capital's $75 million investment that same year, providing the firepower for international expansion. The European expansion began with FleetCor acquiring United Kingdom company KeyFuels in 2006, processing over 500,000 business fleets. KeyFuels wasn't just another fuel card company—it was the UK's leading provider of fuel management solutions for larger commercial vehicle fleet operators, with a network spanning the United Kingdom, Ireland, Belgium, Luxembourg, Netherlands and Benelux. The acquisition gave FleetCor instant scale in Europe and a platform for further expansion.

Other European acquisitions from 2006 to 2009 included Abbey Fuelcards, CCS, ICP Smart Concepts, Petrol Plus Region (the largest independent fuel card company in Russia), and The Fuelcard Company (a United Kingdom commercial fuel card reseller). Each acquisition followed the same playbook: identify fragmented markets, acquire the leading independent player, integrate the back office while maintaining the local brand, then use the platform to consolidate smaller competitors.

The integration methodology Clarke developed during this period would become FleetCor's secret weapon. Rather than forcing acquired companies into a single operating model, FleetCor maintained local brands and relationships while centralizing only what mattered: technology infrastructure, credit underwriting, and financial reporting. This allowed them to preserve the entrepreneurial culture and customer relationships that made these businesses successful while capturing significant cost synergies.

By the end of 2006, FleetCor's revenue had crossed $100 million—a four-fold increase in just six years under Clarke's leadership. The company was processing billions in payment volume across multiple countries. More importantly, they had proven that the fuel card consolidation thesis worked not just in the United States but globally. The foundation was set for what would come next: taking the company public and using the capital markets to fund even more aggressive expansion.

V. The IPO & Public Market Entry (2007–2010)

The timing seemed almost perverse. In 2007, as credit markets began showing the first cracks of what would become the global financial crisis, FleetCor was preparing to go public. By 2008, with Lehman Brothers collapsing and credit frozen worldwide, most companies were battening down the hatches. FleetCor was filing S-1 documents.

Ron Clarke's decision to push forward with the IPO during the worst financial crisis since the Great Depression revealed something fundamental about his approach to building businesses: when others retreat, attack. The logic was counterintuitive but compelling. Valuations for acquisition targets were plummeting. Competitors were pulling back. Banks needed fee income and would support a rare IPO from a profitable company. Most importantly, being public would give FleetCor a currency—its stock—to make acquisitions when sellers were desperate. In 2010, Fleetcor went public, debuting a $335 million initial public offering. The company priced its initial public offering of 12,675,000 shares of its common stock at a price to the public of $23 per share. The pricing came at the low end of the expected range—a reflection of market skepticism about a business model most investors didn't understand.

The IPO structure was telling. 12,244,039 shares of common stock were being offered by certain of FleetCor's stockholders and only 430,961 shares were being offered by FleetCor itself. The selling stockholders—Summit Partners, Bain Capital, and Advent International—were taking chips off the table after generating extraordinary returns. But Clarke and management retained significant ownership, signaling their confidence in the future.

The roadshow had been brutal. Fund managers questioned everything: the sustainability of fuel cards in an increasingly digital world, competition from credit card companies, the integration risk from multiple acquisitions. One particularly memorable exchange saw a portfolio manager ask Clarke why anyone would invest in "a glorified middleman in a dying industry." Clarke's response was characteristic: "Because we're going to use your money to buy more middlemen and build a network no one can replicate."

The first day of trading on December 15, 2010, provided vindication. The stock opened at $27.25 and closed at $28.31, up 23% from the IPO price. It was a strong debut in a market still recovering from the financial crisis. More importantly, it gave FleetCor the currency and credibility to execute on its ambitious growth plans.

The numbers at IPO told the story of transformation. From $25 million in revenue when Clarke took over in 2000, FleetCor had grown to approximately $400 million in 2010. The company was processing $14 billion in payment volume across 18 countries. It had 530,000 commercial accounts and 2.5 million cards in circulation. EBITDA margins had expanded to over 40%, proving that scale and operational improvements could drive extraordinary profitability in this business.

But the real value of being public wasn't the $10 million in net proceeds FleetCor received—it was the platform for what came next. As a public company, FleetCor could use its stock as acquisition currency, access debt markets more efficiently, and most importantly, tell its story to a broader audience. The fuel card processor from Georgia was about to go shopping, and the Comdata acquisition four years later would prove that going public was just the beginning.

VI. The Comdata Mega-Deal: Betting the Company (2014)

On August 12, 2014, Ron Clarke walked into a conference room to announce the deal that would define FleetCor's future. The company had signed a definitive agreement to acquire Comdata Inc. from Ceridian LLC, a portfolio company of funds affiliated with Thomas H. Lee Partners, L.P. and Fidelity National Financial Inc., for $3.45 billion. It was a transaction so large that FleetCor's own market cap at the time was only marginally higher. Clarke was essentially betting the entire company on a single acquisition.

Comdata was a leading business-to-business provider of innovative electronic payment solutions. As an issuer and a processor, Comdata provided fleet, and corporate payment solutions to over 20,000 customers. In 2013, Comdata managed over 625 million cards and processed over 1.4 billion transactions from over 48 countries and in 37 currencies. Founded in 1969 and headquartered in Brentwood, Tennessee with approximately 1,300 employees globally, Comdata enabled over $54 billion in payment volume annually.

The strategic rationale was compelling but complex. Comdata added four new segments where Fleetcor previously didn't operate: an on-the-road trucking business, where Comdata was the market leader with its proprietary fuel card and cash-disbursement services; a national accounts business, where Comdata provided a universal MasterCard to its clients; corporate payments, where Comdata had established a health care vertical and a virtual MasterCard payment program designed to help businesses simplify their payables-payment process; and SVS (Stored Value Systems), which specialized in global gift card processing and program management.

But it was the virtual payments business that really caught Clarke's attention. During the acquisition call, he could barely contain his enthusiasm: "Another motivation is the deal helps Fleetcor gain entry into the 'attractive virtual card space, which is quite large and growing fast,' Clarke said. 'Comdata's got a great position, great proprietary technology, a pretty unique vendor-enrollment model, and some great reseller relationships,' he said. 'Comdata's well positioned, and our view is this could mature into a very big—I mean very big—business over time. So in some ways for us, this line of business is really the crown jewel of the company.'"

The financing structure revealed just how audacious the bet was. Under terms of the deal, FleetCor would pay $2.4 billion in cash and $1 billion in common stock to Comdata's parent company Ceridian LLC. To raise the cash, FleetCor had to tap every available source of capital: a new term loan, senior notes, and drawing on revolving credit facilities. The company's leverage ratio would spike to over 4x EBITDA, levels that made conservative investors nervous.

The integration challenges were immense. Comdata wasn't just bigger than any previous FleetCor acquisition—it was bigger than all previous acquisitions combined. The company had its own entrenched culture, legacy technology systems, and complex customer relationships. Moreover, Comdata operated in segments FleetCor had never touched, requiring new expertise and operational capabilities.

Yet Clarke approached the integration with characteristic confidence. "We have followed Comdata's growth and development for many years, and are excited today to be bringing the companies together," said Ron Clarke, chairman and chief executive officer of FleetCor Technologies, Inc. "Comdata's virtual payments business will add a completely new growth leg to FleetCor. We believe that the combination will result in significant synergies as we implement our operating disciplines to their portfolio of businesses."

The deal closed on November 17, 2014, with Thomas M. Hagerty, a representative from THL, joining FleetCor's board of directors. This wasn't just a financial transaction—it was a strategic partnership that brought sophisticated private equity expertise to FleetCor's board.

The market's initial reaction was mixed. Some investors worried about integration risk and leverage. Others saw the transformative potential. What nobody disputed was that FleetCor had just made the boldest move in its history. The fuel card company from Georgia had evolved into something much bigger—a diversified B2B payments platform with ambitions to reshape how businesses handle their expenses. The Comdata acquisition wasn't just about getting bigger; it was about fundamentally reimagining what FleetCor could become.

VII. Geographic Expansion & International Growth (2011–2018)

The year 2011 marked a watershed moment in FleetCor's international ambitions. In February, the company announced a game-changing partnership: Logica, partnering with FleetCor Technologies Inc., had won a 10-year, EUR 300 million contract to support Shell's Commercial Fleet fuel cards programme in Europe and Asia. Business-to-business fuel cards offer firms that operate fleets of commercial vehicles a convenient, cost-effective and secure way to pay and account for fuel and other on-road services. Logica has teamed up with FleetCor to deliver the service to Shell. Logica, as the prime contractor to Shell, will join FleetCor to provide the technology platform and underlying business processes to run Shell's fuel card portfolio. FleetCor's Global FleetNet (GFN) card processing platform will be used to develop Shell's customer offering.

Shell is one of the world's leading fuel card issuers. The project will run across 35 countries in Europe and Asia and will lead to better service and faster time to market of innovation and system enhancements. Shell's award of the contract follows an extensive selection and procurement process. Ron Clarke's reaction captured the significance: "We are delighted Shell has chosen us and we will work closely with Logica to help improve the performance of the Shell fuel card portfolio. This win validates our ambition to provide the world's oil companies with a fuel card industry platform. The benefits of scale and global learning will accrue to early adopters of the system."

Just months later, in December 2011, FleetCor made another bold move, acquiring AllStar Business Solutions (fuel card provider in the UK market) for $304 million. AllStar wasn't just any acquisition—it was the UK's market leader with approximately 40,000 customers and about one million cardholders. The company's fuel cards were accepted at all major UK fuel brands, giving FleetCor instant dominance in one of Europe's most sophisticated fleet markets. The Brazil expansion in 2012 revealed FleetCor's growing appetite for emerging markets. FleetCor continued its global expansion in 2012 by acquiring a leading fuel card systems company in Russia and CTF, a fuel payment processing services provider in Brazil, for $180 million. CTF provides fuel payment processing services for over-the-road fleets, ships, mining equipment, and railroads in Brazil. CTF's payment platform links together fleet operators, two of the largest Brazilian banks, Bradesco and Itau, and the two largest Brazilian oil companies, Petrobras and Ipiranga.

Clarke explained the strategic logic with characteristic clarity during the acquisition call: "We were attracted to CTF for four reasons: 1) its leading position in the fuel payments market in Brazil, one of the most attractive emerging markets in the world, 2) its strong relationships with Petrobras and Ipiranga, which combined have more than 60% market share of fuel retailing in Brazil, 3) the potential to take the CTF solution to our oil partners around the world, particularly in emerging markets where fuel theft is a significant problem, and 4) the fee based business model, whereby CTF takes virtually no credit risk."

The Brazilian market would prove to be a goldmine. In 2016, FleetCor doubled down with the acquisition of Sem Parar, an electronic toll payments company in Brazil, for over $1 billion. Sem Parar wasn't just about tolls—it was about creating a ubiquitous payment network. The company's RFID tags could be used for parking, drive-thrus, and eventually even McDonald's restaurants. It was a glimpse of FleetCor's future: moving beyond fuel into any B2B payment scenario.

The pace of international expansion was relentless. In 2013, Fleetcor acquired the following: Australia's FleetCard, New Zealand's Cardlink, VB Serviços (a provider of transportation cards and vouchers in Brazil), DB Trans (also in Brazil), Epyx (a SaaS system and a network of vehicle repair garages serving fleet operators in the UK), and NexTraq, a US-based provider of telematics solutions. Each acquisition followed the same playbook but adapted to local conditions.

The cultural challenges of international M&A were significant. Brazilian business culture differed dramatically from Australian, which differed from Russian. Local regulations varied wildly—what worked in the UK might be illegal in Brazil. Currency fluctuations could turn a profitable acquisition into a loss overnight. Yet FleetCor navigated these challenges with a decentralized approach: maintain local management, preserve local brands, but centralize technology and financial controls.

By 2018, FleetCor's geographic diversity had become a major competitive advantage. When oil prices crashed in one region, tolls might boom in another. When European economies struggled, Latin America might thrive. The company had built a portfolio of businesses that, while all related to B2B payments, were diversified enough to weather almost any storm. International operations now contributed over 40% of revenue, up from essentially zero when Clarke took over.

The compound effect of geographic expansion was more than just risk mitigation—it was about learning transfer. A product innovation in Brazil might work in Mexico. A sales technique from Australia could transform the UK business. The global platform allowed FleetCor to be both local and global simultaneously, a rare achievement in B2B payments. As the company approached the next phase of its evolution, this international foundation would prove invaluable in the pivot toward corporate payments.

VIII. The Corporate Payments Pivot (2019–2024)

The year 2019 marked a strategic inflection point for FleetCor. While the company had built its empire on fuel cards and fleet management, Clarke saw a much larger opportunity in the broader corporate payments space. In 2019, Fleetcor led three major acquisitions: Nvoicepay (an Account Payables automation for businesses company), Sole Financial (a payroll card provider), and Travelliance (airline lodging programs). But it was Nvoicepay that signaled the company's true ambitions.

FLEETCOR Technologies, Inc. announced that it has signed a definitive agreement to acquire Nvoicepay, Inc., a leader in full AP automation for businesses. Nvoicepay delivers automated accounts payable solutions to over 400 business clients, providing a simple UI that allows customers to electronically pay all of their suppliers. Clarke's enthusiasm was palpable: "Nvoicepay presents an exciting opportunity to accelerate growth of our Corporate Payments business by offering customers a simple way to pay all their accounts payable with one vendor. Through the combination of Comdata, Cambridge and soon Nvoicepay, we believe FLEETCOR will offer one of the most comprehensive domestic and international AP payments solutions available to businesses."

The strategic logic went beyond just adding another product. Kurt Adams, Group President of Corporate Payments at FLEETCOR, explained the broader vision: "Combined with our industry-leading virtual card and corporate card solutions, we believe FLEETCOR Corporate Payments is now the best choice for businesses looking to modernize their AP processes." This wasn't about fuel cards anymore—it was about becoming the operating system for all B2B payments. The momentum in corporate payments continued to accelerate. In August 2022, Fleetcor acquired Accrualify, an accounts payable software firm. Then in May 2024, the newly rebranded Corpay acquired Paymerang, a Richmond, Virginia headquartered accounts payable automation company for $475 million. The acquisition expands Corpay's presence in four attractive vertical markets: education, healthcare, hospitality and manufacturing.

Clarke's enthusiasm for the Paymerang deal reflected the strategic importance of the corporate payments pivot: "This acquisition is right in our wheelhouse and exactly the kind of transaction we find most attractive. It's a business growing over 20%, within Corporate Payments, where we can accelerate growth and profitability. It will help us sell more in several large verticals where Paymerang has a strong position with satisfied customers, ERPs and partners."

The numbers told the story of transformation. Paymerang adds over 250,000 merchants to Corpay's existing merchant network of over 1 million vendors, and together the businesses will process $120 billion in annual spend. More importantly, with the addition of Paymerang and GPS Capital Markets (acquired in December 2024), Corpay expected its Corporate Payments business to exceed $1.5 billion in revenue in 2025.

What made the corporate payments pivot so compelling was the addressable market. While fuel cards were a $10 billion global market, B2B payments represented a $120 trillion opportunity. Only about 50% of B2B payments were electronic, compared to over 90% in consumer payments. The inefficiency was staggering: businesses still processed billions of paper checks annually, each costing $5-10 to process versus pennies for electronic payments.

The acquisition strategy in corporate payments differed from the fuel card rollup. These were technology-first companies with sophisticated software platforms, not just payment processors. Integration was more complex, requiring careful attention to APIs, workflow automation, and ERP integrations. But the payoff was higher margins, stickier customers, and massive cross-sell opportunities.

By 2024, Corporate Payments had become one of Corpay's three core pillars alongside Vehicle and Lodging. The segment was growing at over 20% annually, with EBITDA margins approaching 50%. More importantly, it positioned Corpay as a comprehensive B2B payments platform rather than just a fuel card company. The transformation that began with the Comdata acquisition in 2014 was now complete: Corpay had successfully pivoted from a narrow vertical payments provider to a broad-based B2B payments powerhouse.

IX. The Rebrand: From FleetCor to Corpay (2024)

On March 8, 2024, FLEETCOR Technologies announced it would become Corpay. The rebrand took effect on March 25, 2024 when the Company's stock began trading on the New York Stock Exchange under the new ticker symbol CPAY.

The announcement came with characteristic Clarke directness: "The Corpay name better represents what we do now, which is provide corporate payment solutions. We will use Corpay as the go-to-market brand for our Corporate Payments segment, and retain our existing popular go-to-market brands in our Vehicle Payments and Lodging Payments segments".

The timing wasn't coincidental. The rebranding came a year after FLEETCOR announced a board refresh and a strategic review that would encompass both the company's portfolio and its business configuration. The company had evolved far beyond its fuel card roots. Corporate Payments was becoming the growth engine, Vehicle Payments remained the cash cow, and Lodging Payments provided diversification. The FleetCor name, while historically significant, no longer captured the breadth of what the company had become.

The market positioning was carefully orchestrated. Corpay served more than 800,000 business customers globally and was the No. 1 B2B commercial Mastercard issuer in North America. In 2023, its revenues totaled $3.75 billion. The rebrand signaled to investors, customers, and acquisition targets that this was no longer a niche fuel card processor but a comprehensive B2B payments platform.

The retention of legacy brands in specific segments revealed sophisticated market segmentation. In fuel cards, brands like Fuelman, Comdata, and FLEETCOR had decades of equity and customer loyalty. In lodging, brands like CLC Lodging maintained their specialized market positions. But for the corporate payments push—where Corpay competed against companies like Bill.com and AvidXchange—a unified, modern brand was essential.

Wall Street's reception was telling. Rather than the confusion that often accompanies major rebrands, the market understood the strategic logic. The company was telegraphing its future: less emphasis on the mature fuel card business, aggressive expansion in corporate payments, and a vision of becoming the operating system for all B2B payments. The stock responded positively, continuing its upward trajectory as investors bought into the transformation story.

X. Recent Moves & Future Bets (2024–Present)

The July 2025 announcement of the Alpha Group acquisition sent shockwaves through the B2B payments industry. Corpay had reached agreement on the terms of a recommended cash acquisition of Alpha Group International plc for an enterprise valuation of approximately $2.2 billion. Under the terms of the offer, Alpha shareholders would receive £42.50 per share, representing a 55% premium to Alpha's undisturbed closing share price on May 1, 2025.

Ron Clarke's enthusiasm was unmistakable: "We couldn't be happier to acquire Alpha. This transaction meaningfully expands our relationships with investment managers and results in four Cross Border customer segments: corporates, financial institutions, investment funds and digital currency providers".

Alpha was a leading provider of B2B cross border FX solutions to corporations and investment funds in the UK and Europe. Alpha pioneered alternative bank accounts as a simpler, faster way for investment managers to fund their investments and pay expenses anywhere in Europe. Today, Alpha holds approximately $3 billion of deposits in over 7,000 client accounts.

The strategic rationale went beyond just adding scale. Alpha brought capabilities Corpay lacked—particularly in serving institutional investors and private equity firms. The acquisition would accelerate Corpay's expansion into new customer segments while providing Alpha with the resources to expand globally. Corpay expected that the Acquisition would deliver meaningful revenue and expense synergies, be accretive to revenue growth, and be at least $0.50 accretive to Corpay's cash EPS in the 2026 financial year.

Six months earlier, in December 2024, Corpay had completed another strategic acquisition. Corpay completed the acquisition of GPS Capital Markets, LLC, a business-to-business cross-border solutions provider to upper middle market companies. The GPS deal had been announced in June 2024, with Clarke calling it "our third largest deal ever".

The GPS acquisition brought critical capabilities in FX netting technology and a blue-chip client roster. Combined with the earlier Paymerang acquisition, these deals positioned Corporate Payments for explosive growth. "With the addition of Paymerang and now GPS, we expect our Corporate Payments business to exceed $1.5 billion in revenue in 2025", Clarke announced.

But Corpay wasn't just buying—it was also selling. Corpay announced the completion of the divestiture of Comdata Merchant POS Solutions, a point-of-sale hardware and software solution for truck stop merchants, to a private equity-backed company PDI Technologies. The divestiture reflected a disciplined approach to portfolio management: focus on core B2B payments, divest non-strategic assets, and redeploy capital into higher-growth opportunities.

The three-pillar strategy was now crystal clear. Vehicle Payments would remain the profit engine, generating steady cash flows from a mature but essential market. Corporate Payments would drive growth, targeting the massive and still largely manual B2B payments market. Lodging Payments would provide diversification and cross-sell opportunities. Everything else was expendable.

The funding strategy for these acquisitions revealed financial sophistication. The Alpha acquisition would be funded through a combination of cash, debt, bank capital optimization and non-core divestitures. Rather than diluting shareholders with equity raises, Corpay was using its strong cash generation, modest leverage capacity, and strategic divestitures to fund transformative deals.

Looking forward, the integration of AI and automation promised to accelerate the transformation. Every acquisition brought not just customers and revenue but also technology and data. The combined entity would process hundreds of billions in payment volume annually, creating a data moat that could power AI-driven insights, fraud detection, and workflow automation.

XI. Business Model & Unit Economics

The beauty of Corpay's business model lies in its multiple revenue streams, each with different economic characteristics but all contributing to a powerful financial engine. Transaction fees form the foundation—every swipe of a fuel card, every cross-border payment, every AP automation transaction generates revenue. But the real magic happens in the layers beyond simple processing.

Interchange revenue, the fees paid by merchants to accept card payments, flows directly to Corpay's bottom line. In fuel cards, where Corpay often has exclusive relationships with merchants, these rates can be particularly attractive. The company also captures rebates from oil companies and merchants—volume-based payments that increase with scale. The more volume Corpay processes, the better terms it can negotiate, creating a virtuous cycle of improving economics.

Float income, often overlooked by analysts, provides a significant profit stream. When a corporation loads funds onto Corpay cards or when money sits in Corpay accounts between collection and disbursement, the company earns interest on these balances. In a rising rate environment, this "free" revenue stream can contribute hundreds of millions to the bottom line.

The network effects in Corpay's business create formidable competitive moats. In fuel cards, every new accepting location makes the network more valuable to fleet customers. Every new fleet customer makes the network more attractive to fuel merchants. This two-sided network effect makes it increasingly difficult for competitors to challenge Corpay's position once it achieves critical mass in a market.

Switching costs provide another layer of protection. Integrating Corpay's systems with a corporation's ERP, training employees on new payment workflows, and establishing spend controls represent significant investments of time and resources. Once embedded in a customer's operations, Corpay becomes extremely sticky. Customer retention rates consistently exceed 90%, and customer lifetime values can stretch into decades.

The customer acquisition strategy brilliantly balances organic growth with M&A. Acquisitions bring immediate scale and eliminate competitors, while organic sales efforts focus on cross-selling into the expanded customer base. A fuel card customer becomes an AP automation prospect. An AP automation customer might need cross-border payments. The expanded product portfolio creates multiple touchpoints and revenue opportunities within each customer relationship.

Margin expansion through scale and technology has been relentless. When Clarke took over in 2000, EBITDA margins were in the low teens. Today, they approach 50% in mature segments. This expansion comes from three sources: operating leverage as fixed costs spread over larger volumes, technology investments that automate manual processes, and pricing power from superior products and network effects.

The capital efficiency of the model is remarkable. Unlike traditional financial services companies that need significant capital to support lending, Corpay primarily facilitates payments rather than extending credit. The business generates massive free cash flow—typically 70-80% of EBITDA converts to free cash flow—providing the fuel for acquisitions and shareholder returns.

The diversification across payment types, geographies, and customer segments provides resilience. When oil prices crash, reducing fuel card volumes, cross-border payments might surge as companies seek better FX rates. When economic uncertainty hits corporate spending, government and education customers provide stability. This portfolio approach smooths out the inevitable cycles in any single market.

XII. Playbook: The Corpay Acquisition Machine

Over two decades and 70-plus acquisitions, Corpay has refined a repeateable playbook that turns M&A from an art into a science. The approach begins with target identification: fragmented markets with multiple subscale players, recurring revenue models, and clear network effects potential. Clarke and his team aren't looking for turnarounds or transformations—they want good businesses they can make great through scale and operational excellence.

The evaluation process is ruthlessly disciplined. Every acquisition must meet specific financial hurdles: accretive to earnings within 12 months, IRR exceeding 20%, and clear path to margin expansion. Cultural fit matters too—entrepreneurial management teams that will thrive in Corpay's decentralized model are preferred over corporate bureaucracies that need wholesale replacement.

The integration methodology has evolved into a precise choreography. Week one: stabilize the business, reassure customers, retain key employees. Month one: integrate financial reporting, implement Corpay's credit policies, begin technology assessment. Quarter one: identify quick wins in cross-selling and cost synergies. Year one: complete technology integration while maintaining customer-facing continuity.

The decision on branding reveals sophisticated market understanding. In fuel cards, local brands often have decades of customer relationships—Fuelman in the US, AllStar in the UK, CTF in Brazil. These brands are preserved and even invested in. But in corporate payments, where Corpay is building a global platform, acquisitions are quickly rebranded to build unified market presence.

International expansion through acquisition requires additional complexity. Local management teams are retained and empowered—they understand regulatory requirements, cultural nuances, and market dynamics that would take years for outsiders to learn. But financial controls, risk management, and technology platforms are centralized to capture economies of scale.

The financing approach has evolved with Corpay's size and sophistication. Early acquisitions were funded with venture capital and private equity. Post-IPO deals used a mix of cash and stock. Today's mega-deals tap debt markets, utilizing Corpay's investment-grade credit rating to access cheap capital. The company maintains disciplined leverage targets—typically 2.5-3.5x EBITDA—ensuring financial flexibility for opportunistic deals.

Post-merger value creation follows predictable patterns. Cost synergies come first: eliminating duplicate functions, negotiating better vendor terms, optimizing real estate. Revenue synergies follow: cross-selling products, expanding geographic reach, leveraging technology investments. The final phase is transformation: using Corpay's scale and capabilities to fundamentally reimagine the acquired business's potential.

The decentralized operating model is perhaps the most counterintuitive aspect of Corpay's approach. Rather than forcing all acquisitions into a single operating model, the company maintains a "federation" of businesses. Each unit has its own P&L, management team, and go-to-market strategy. Corporate provides capital allocation, strategic direction, and shared services, but operational decisions remain local.

Risk management in serial acquisition requires constant vigilance. Integration teams have learned to identify early warning signs: customer defection rates, employee turnover, technology incompatibilities. When problems emerge, resources are surged to address them before they metastasize. Not every acquisition succeeds, but failures are rare and contained.

The human capital strategy recognizes that acquisitions are ultimately about people. Key executives from acquired companies often receive retention packages and expanded responsibilities. Many of Corpay's current division presidents came through acquisitions. This creates a deep bench of talent and institutional knowledge about successful integration.

XIII. Analysis & Investment Case

The bull case for Corpay rests on multiple pillars, each compelling in isolation but powerful in combination. The TAM opportunity is massive and growing—B2B payments represent a $120 trillion market globally, with only 50% currently electronic. Even capturing a tiny incremental share of this transition from paper to electronic payments could double Corpay's revenue. The company's proven execution over 20+ years provides confidence that management can capitalize on this opportunity.

The recurring revenue model with 90%+ retention rates creates exceptional visibility and compound growth. Unlike transactional businesses that must resell customers constantly, Corpay's embedded position in customer workflows generates predictable, growing revenue streams. The network effects and switching costs make the business increasingly defensive as it scales.

The margin expansion story remains compelling despite already impressive profitability. As payment volumes grow, incremental margins can exceed 70%. Technology investments continue to automate manual processes. Pricing power remains strong in many segments. The path to 50%+ EBITDA margins across all segments appears achievable.

The bear case cannot be dismissed lightly. Integration risk looms large with the pace and scale of recent acquisitions. The Alpha Group deal alone represents 10% of Corpay's market cap—a failed integration could destroy billions in shareholder value. The company is attempting to integrate multiple large acquisitions simultaneously while entering new customer segments and geographies.

Competition from both traditional players and fintech disruptors is intensifying. Companies like Bill.com and AvidXchange are attacking corporate payments with modern, cloud-native solutions. Traditional banks are finally investing in their B2B payments capabilities. Big Tech companies like Apple and Amazon are eyeing B2B payments as their next frontier.

Valuation concerns are legitimate. At current levels, Corpay trades at premium multiples to both historical averages and peers. The market is pricing in flawless execution on integration, continued high growth rates, and successful expansion into new segments. Any disappointment could trigger multiple compression and significant stock price decline.

Technology risk represents another concern. While Corpay has successfully modernized through acquisitions, much of its core infrastructure remains legacy. Competing against venture-backed fintechs with modern tech stacks and no technical debt could become increasingly challenging. The cost and complexity of technology transformation while maintaining business continuity is enormous.

The comparison to peers reveals both strengths and vulnerabilities. With revenue expected to exceed $1.5 billion in Corporate Payments alone in 2025, Corpay is achieving scale that smaller competitors cannot match. But pure-play specialists like WEX in fleet or Bill.com in AP automation can focus resources more narrowly and potentially out-innovate in specific verticals.

The financial metrics tell a story of exceptional performance but also high expectations. Trading at approximately 16x forward EBITDA and 25x forward earnings, the stock prices in continued strong execution. Free cash flow yield of roughly 4% provides some valuation support, but any stumble in growth or margins could trigger a sharp re-rating.

XIV. Lessons & Takeaways

The Corpay story offers profound lessons about building enduring value in seemingly commoditized markets. First and foremost: boring businesses can generate extraordinary returns. While Silicon Valley chased consumer apps and crypto speculation, Corpay quietly built a $22 billion enterprise processing fuel purchases and paying invoices. The lesson is clear—solving real business problems with superior execution beats chasing buzzwords.

The power of focus in fragmented markets cannot be overstated. When Clarke arrived in 2000, the fuel card industry had hundreds of small players, each serving local markets with similar offerings. By rolling up these subscale competitors, Corpay achieved economies of scale that created a sustainable competitive advantage. Fragmentation is an opportunity, not an obstacle.

Building through M&A is a legitimate strategy when executed with discipline. Too often, serial acquirers destroy value through overpayment, poor integration, or strategic drift. Corpay demonstrates that with clear acquisition criteria, proven integration playbooks, and patient capital, M&A can be a powerful value creation engine. The key is discipline—walking away from deals that don't meet hurdle rates, even when pressure to grow is intense.

The importance of patient capital deserves emphasis. Corpay's transformation took over two decades. Early investors who held through the journey generated life-changing returns, but it required tolerating years of integration challenges, market skepticism, and economic cycles. In an era of quarterly capitalism, Corpay's long-term approach stands out.

Creating value through operational improvements remains underappreciated. Corpay rarely bought great businesses—it bought decent businesses with untapped potential. Through technology investment, process improvement, and scale economies, the company consistently expanded margins and accelerated growth in acquired properties. Operational excellence, not financial engineering, drove returns.

The compound effect of strategic consistency is remarkable. While competitors pivoted with market fashions—blockchain, buy-now-pay-later, cryptocurrency—Corpay remained focused on B2B payments. This consistency allowed cumulative learning, relationship building, and capability development that created insurmountable advantages.

Why B2B payments represents one of the great business models becomes clear through Corpay's example. High switching costs, network effects, recurring revenues, and capital-light operations create a nearly perfect business. While consumer payments get attention, B2B payments generate superior economics with less competition for investor attention.

The final lesson is about leadership and vision. Ron Clarke saw potential in a $25 million fuel card processor that others missed. But vision without execution is hallucination. Clarke built a team, developed a strategy, and executed relentlessly for over two decades. The combination of strategic vision and operational excellence is rare and valuable.

XV. Conclusion: The Hidden Giant Emerges

Twenty-four years after Ron Clarke walked into a struggling fuel card processor, Corpay stands as testament to the power of compound growth, strategic focus, and relentless execution. From $25 million to over $4 billion in revenue, from a single country to global presence, from fuel cards to comprehensive B2B payments—the transformation is complete, yet the journey continues.

The March 2024 rebrand from FleetCor to Corpay marked not an ending but a beginning. With the Alpha Group acquisition set to close, GPS Capital Markets integrated, and Corporate Payments approaching $2 billion in revenue, the company is positioned for its next phase of growth. The vision is ambitious but achievable: becoming the operating system for global B2B payments.

What makes Corpay's story remarkable isn't just the financial success—it's the method. In an era of blitzscaling and growth-at-all-costs, Corpay grew profitably. While others chased headlines, Corpay focused on customers. When competitors pursued transformational pivots, Corpay deepened its core competencies. The result is a business with remarkable durability and continued growth potential.

The challenges ahead are real. Integration complexity is rising with deal size and scope. Competition is intensifying as the B2B payments opportunity becomes obvious. Technology transformation requires massive investment while maintaining operational stability. Geographic expansion brings regulatory and cultural complexity. Success is not guaranteed.

Yet betting against Corpay seems unwise. The company has navigated the dot-com crash, global financial crisis, COVID-19 pandemic, and countless smaller challenges. Each time, it emerged stronger. The playbook is proven, the team is experienced, and the opportunity remains massive.

For investors, Corpay offers a unique proposition: exposure to the secular shift from paper to electronic B2B payments, delivered through a proven operator with demonstrated acquisition expertise. While valuation requires careful consideration, the long-term opportunity appears compelling for patient capital.

For competitors, Corpay represents a formidable challenge. Its scale advantages in network effects, data, and economics are difficult to replicate. The breadth of its product portfolio creates multiple defensive moats. The geographic diversity provides resilience. The M&A machine can quickly eliminate emerging threats through acquisition.

For the broader business community, Corpay demonstrates that transformation is possible at any stage. A 14-year-old struggling business became a global leader through vision, strategy, and execution. The path wasn't smooth or quick, but it was achievable. In a world obsessed with overnight success, Corpay's two-decade journey offers a different model—one built on patience, discipline, and compound growth.

As we look toward the future, Corpay's hidden giant status is ending. The company is increasingly recognized as a major force in global payments. The question is no longer whether Corpay will succeed—it already has. The question is how much bigger it can become. With B2B payments still in the early innings of digitization, the answer might surprise even the optimists.

The story that began with a simple fuel card in 1986 has evolved into something far greater: a global payments infrastructure powering the world's economy. From the trucks delivering goods to the corporations paying suppliers to the investment funds moving capital globally, Corpay has quietly become essential plumbing for global commerce. The hidden giant is hidden no more, and its emergence is just beginning.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube