The Carlyle Group: From Washington Boutique to Global Private Equity Powerhouse

I. Introduction & Episode Roadmap

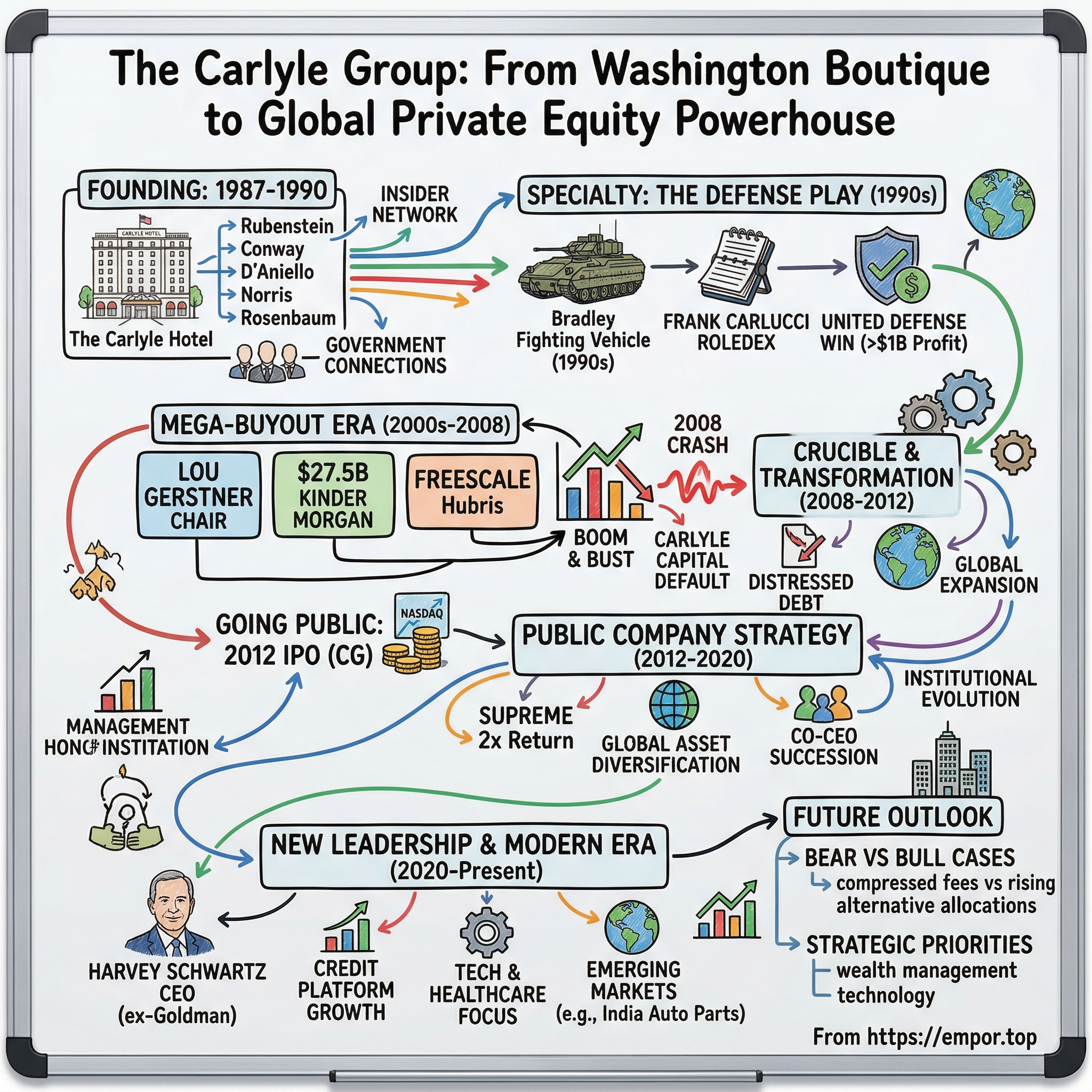

Picture this: A mahogany-paneled conference room in Washington D.C., 1987. Five men gather around a table at the Carlyle Hotel in New York City—the very hotel that would lend its name to their venture. They're not Silicon Valley entrepreneurs or Wall Street titans. They're Washington insiders, government alumni, and corporate executives who see an opportunity that others have missed: marrying political connectivity with private capital in ways the financial world had never quite seen before.

Today, that meeting has evolved into The Carlyle Group—a $426 billion behemoth managing assets across the globe from 28 offices on four continents. With nearly 2,200 employees orchestrating deals from São Paulo to Seoul, Carlyle stands as one of the "Big Four" private equity firms alongside Blackstone, KKR, and Apollo. But here's what makes their story compelling: unlike their New York rivals who built empires on pure financial engineering, Carlyle constructed theirs on a foundation of Beltway relationships and defense industry expertise.

The question that drives this narrative isn't just how five guys in suits built one of the world's largest alternative asset managers—it's how a boutique investment bank that started by advising Middle Eastern royalty on American investments transformed into a global financial powerhouse that would eventually take companies like Dunkin' Donuts, Hertz, and Supreme from private to public and back again.

This is a story of three distinct acts: First, the Washington years, when political connections were currency and defense deals were the bread and butter. Second, the mega-buyout era, when Carlyle shed its D.C. boutique image to compete toe-to-toe with the New York giants. And third, the public company evolution, where the firm grappled with transparency, leadership transitions, and the eternal tension between generating returns for limited partners while satisfying public shareholders.

What listeners—and readers—can expect is not just a corporate history, but a masterclass in how regulatory expertise, sector specialization, and global ambition can build an empire. We'll explore the controversies (yes, we're going to talk about that September 11th investor meeting), the massive wins (turning $850 million into billions with United Defense), and the spectacular failures (Hawaiian Telcom, anyone?).

Most importantly, we'll decode the Carlyle playbook: how they've consistently turned government connections into competitive advantages, why they chose to go public when they did, and what their journey teaches us about the evolution of private equity itself. Because understanding Carlyle isn't just about understanding one firm—it's about understanding how power, money, and influence intersect in modern capitalism.

II. The Founding Story: Washington Insiders Build a Boutique (1987–1990)

The origin story begins not in the glass towers of Manhattan but in the power corridors of Washington D.C., where David Rubenstein, a 37-year-old lawyer who'd cut his teeth as deputy domestic policy advisor in the Carter Administration, was watching his peers make fortunes on Wall Street while he practiced law. Rubenstein had that particular brand of Washington ambition—the kind that measures success not just in dollars but in access and influence.

He wasn't alone in feeling the pull of private capital. Stephen Norris and Daniel D'Aniello, colleagues at Marriott Corporation, were wrestling with similar aspirations. Norris, a Harvard MBA with Alaska roots, handled Marriott's mergers and acquisitions. D'Aniello, a Syracuse graduate from working-class Pennsylvania, managed finance and development. Both understood corporate America from the inside—how deals got done, where value hid, which executives you could trust.

Then there was William Conway Jr., the numbers guy from MCI Communications who understood telecommunications when it was still the future, not the present. Conway brought something the others lacked: operational experience in a high-growth industry and the analytical rigor of someone who'd managed actual P&Ls, not just advised on them.

The fifth founder, Greg Rosenbaum, ran a small investment company and would last barely a year—a footnote in Carlyle lore but important for what his departure revealed about the firm's DNA. This wasn't going to be a democracy; it would be ruled by those willing to grind through the early years of rejection and near-misses.

They named their firm after the Carlyle Hotel on Manhattan's Upper East Side—an establishment known for discretion, where the Kennedys kept an apartment and where powerful people made private deals. The name itself was a statement of intent: we're not another aggressive Wall Street shop; we're something more refined, more connected, more Washington.

The early years were brutal in that specific way that tests whether founders have chosen the right partners. They operated deal-by-deal, essentially running a merchant bank without the bank. The Chi-Chi's debacle exemplified their struggles—an attempted takeover of the Mexican restaurant chain that collapsed spectacularly, leaving them with nothing but legal bills and bruised egos. Rubenstein later called it "humiliating," but it taught them a crucial lesson: enthusiasm without expertise equals expensive education.

Their breakthrough came not from buying companies but from facilitating one of the most significant foreign investments in American banking history. In 1991, Prince Al-Waleed bin Talal wanted to invest $500 million in Citigroup, then Citicorp, which was reeling from real estate losses. The Saudis needed someone who understood both Washington's regulatory maze and Wall Street's sensibilities. Carlyle navigated the Committee on Foreign Investment, the Federal Reserve's blessing, and the delicate politics of Arab money rescuing an American icon. The deal established their reputation as fixers—the guys you called when the transaction was as much about politics as profits.

By 1990, they'd raised their first dedicated buyout fund: $100 million. In the context of today's mega-funds, it's a rounding error. But it represented transformation from advisory boutique to principal investor. They weren't just advising on deals anymore; they were doing them.

The founding team had coalesced around a thesis that would define Carlyle for the next decade: Washington wasn't just America's political capital; it was an untapped source of investment intelligence. Every federal budget, every regulatory shift, every defense appropriation created winners and losers. If you understood the process—really understood it, not just read about it in the Journal—you could see value where others saw bureaucracy.

Norris would depart in 1995, cashing out after helping establish the firm's early culture but before the real money started flowing. The remaining triumvirate—Rubenstein, Conway, and D'Aniello—would form one of private equity's most enduring partnerships, their complementary skills creating a balance that would survive booms, busts, and billions. As they entered the 1990s, they were about to discover their killer app: buying and selling the companies that supplied America's military-industrial complex.

III. The Defense Industry Play: Carlyle's Early Specialty (1990s)

The Berlin Wall had fallen, the Soviet Union was crumbling, and defense contractors across America were staring at what industry insiders called the "peace dividend"—Washington-speak for budget cuts that would vaporize billions in military spending. While others saw a dying industry, Carlyle saw a generational opportunity. They understood something fundamental: America might be cutting defense spending, but it wasn't abandoning defense. The industry would consolidate, modernize, and the survivors would thrive.

In 1992, Carlyle made its first major defense play, acquiring the electronics division of General Dynamics. This wasn't a glamorous business—it made electronic countermeasures and submarine communications systems, the kind of technology that never makes headlines but keeps American submarines hidden and fighter jets alive. They renamed it GDE Systems and brought in Frank Carlucci, Ronald Reagan's former Secretary of Defense, as chairman. The signal was unmistakable: Carlyle wasn't just another financial buyer; they were defense industry insiders.

The Carlucci hire represented a new model in private equity. Where KKR had Henry Kravis's dealmaking prowess and Blackstone had Steve Schwarzman's Wall Street relationships, Carlyle would have the Rolodex of Republican Washington. Carlucci didn't just bring credibility; he brought intelligence—knowing which programs would survive budget cuts, which generals were rising stars, which technologies the Pentagon would prioritize in a post-Cold War world.

The GDE flip to Tracor in 1994 validated the strategy, but the 1993 acquisition of Magnavox Electronic Systems from Philips Electronics showed their growing sophistication. Magnavox made electronic warfare systems—the boxes that detect incoming missiles and confuse enemy radar. Boring? Perhaps. Critical to every American military aircraft? Absolutely. They held it for just two years before selling to Hughes Aircraft for $370 million, nearly doubling their investment.

But October 1997 marked Carlyle's transformation from boutique player to serious force: the $850 million acquisition of United Defense Industries. This wasn't some small division of a larger conglomerate—this was a crown jewel of American defense manufacturing. United Defense made the Bradley Fighting Vehicle, the Paladin self-propelled howitzer, and was developing what would become the Crusader artillery system. The price tag was massive for Carlyle at the time, but they saw what others missed: the Pentagon was about to modernize its entire ground combat fleet.

Then came the meeting that would haunt Carlyle for years. On September 11, 2001, Carlyle was hosting its annual investor conference at the Ritz-Carlton in Washington. The guest of honor? Shafiq bin Laden, Osama's half-brother and a Carlyle investor. As the planes hit the towers, the world's most awkward business meeting was underway. The optics were devastating—the bin Laden family invested in a firm profiting from America's defense buildup while Osama orchestrated the attacks that would trigger that buildup.

The conspiracy theorists had a field day, but the reality was more mundane and perhaps more damning: Carlyle had gotten so comfortable mixing money, defense, and politics that they'd lost sight of how it looked from the outside. They quickly severed ties with the bin Laden family, but the damage to their reputation lingered.

Ironically, 9/11 and the subsequent War on Terror would make United Defense one of the most profitable investments in private equity history. They took the company public in December 2001, just three months after the attacks, raising $200 million. By April 2004, when they sold their remaining stake, the investment had returned over $1 billion in profits. The Bradley Fighting Vehicles were rolling through Iraq, the Paladins were pounding Taliban positions in Afghanistan, and Carlyle was counting money.

The defense years established Carlyle's playbook: find industries where government and business intersect, hire former officials who understand both sides, and profit from the inefficiencies that this intersection creates. It was lucrative, legal, and ethically complicated. Critics called it crony capitalism; Carlyle called it specialized expertise.

By the late 1990s, they were already diversifying beyond defense—into telecommunications, healthcare, and real estate. The defense portfolio had given them capital, credibility, and scale. But as the new millennium approached, Carlyle faced a choice: remain a specialized, politically connected fund or compete with the mega-buyout firms on their own turf. They chose competition, setting the stage for a dramatic expansion that would test whether their Washington DNA could survive transplantation to the global stage.

IV. Scaling Up: The Mega-Buyout Era (2000s–2008)

By 2002, Carlyle wasn't playing defense anymore—they were playing offense with the best of them. The firm had accumulated $13.9 billion of assets under management and had generated annualized returns for investors of 36%—numbers that would make any investor salivate. But in the clubby world of mega-buyouts, Carlyle was still the Washington outsider trying to break into the New York establishment.

The hiring of Lou Gerstner as chairman in January 2003 was their declaration of independence from the defense contractor image. Here was the man who'd saved IBM, who'd run Nabisco, whose corporate credentials were unimpeachable. Gerstner replaced Frank Carlucci as chairman, with the hiring intended to reduce the perception of Carlyle as a politically dominated firm. The message was clear: we're not just the Pentagon's banker anymore; we're players in the real economy.

The deals started getting bigger, more ambitious, and occasionally more reckless. Carlyle, together with Welsh, Carson, Anderson & Stowe, led a $7.5 billion buyout of QwestDex, with the purchase occurring in two stages: a $2.75 billion acquisition of assets known as Dex Media East in November 2002 and a $4.30 billion acquisition of assets known as Dex Media West in 2003. This wasn't defense contracting; this was yellow pages and phone directories—boring, cash-flowing, and perfectly suited for the leverage machine that private equity had become.

In May 2004, Carlyle announced the $1.6 billion acquisition of Hawaiian Telcom from Verizon. On paper, it looked brilliant: buy the monopoly telecom provider for Hawaii, load it with debt, extract dividends, and ride the cash flows. What could go wrong in paradise? Everything, as it turned out. Competition from wireless carriers, a brutal regulatory environment, and too much debt would drive Hawaiian Telcom into bankruptcy by 2008, burning $425 million of Carlyle's money—their most spectacular failure to date.

But the mid-2000s weren't about caution; they were about scale. August 2006 saw Carlyle team up with Goldman Sachs for the $27.5 billion acquisition of Kinder Morgan, including debt. This was pipeline infrastructure on a continental scale—the kind of deal that only the biggest players could even contemplate. A month later, they led a consortium for Freescale Semiconductor at $17.6 billion, the largest technology leveraged buyout ever at that point.

The Freescale deal epitomized the era's hubris. Here was a semiconductor company being bought at the peak of the market, loaded with debt just as the industry was about to crater. The consortium paid 17.5 times earnings—a valuation that assumed perfection in an industry famous for brutal cycles. Within two years, Freescale would be struggling to service its debt as semiconductor demand collapsed.

What's fascinating about this period is how Carlyle transformed from a specialized, politically connected fund into a global dealmaking machine. They opened offices from Seoul to São Paulo, raised funds denominated in euros and yen, and competed for deals that had nothing to do with government contracts. The three founders—Rubenstein, Conway, and D'Aniello—had successfully repositioned their firm from Washington boutique to global powerhouse.

But they'd also lost something in translation. The deep sector expertise that characterized their defense investments was replaced by financial engineering and momentum investing. They were buying companies because they could, not because they understood them better than anyone else. The abundance of cheap debt made everyone look smart—until it didn't.

The warning signs were there by 2007. Debt markets were showing stress, portfolio companies were missing projections, and the IPO window was slamming shut. But like everyone else in private equity, Carlyle was too busy closing deals to notice the foundation cracking beneath them. They'd built a machine optimized for one environment—abundant credit, rising valuations, easy exits—and that environment was about to disappear overnight.

V. Crisis & Transformation: 2008 Financial Meltdown to IPO (2008–2012)

March 12, 2008. The headlines screamed disaster: Carlyle Capital Corporation defaulted on about $16.6 billion of debt as the global credit crunch brought about by the subprime mortgage crisis worsened. The fund, established in August 2006 to invest in AAA-rated residential mortgage-backed securities, had been leveraged up to 32 times—borrowing $32 for every dollar of equity to buy what were supposed to be the safest bonds in America.

The mathematics of leverage are brutal in reverse. CCC, which led to the loss of all of its US$1 billion of capital, had seemed bulletproof just weeks earlier. The portfolio consisted entirely of agency mortgage-backed securities—bonds guaranteed by Fannie Mae and Freddie Mac, essentially backed by the U.S. government. What could possibly go wrong? Everything, when your leverage ratio means a 3% decline wipes you out.

In March 2008 an unexpected and unforeseen liquidity crisis hit the financial markets, worse than the August 2007 crisis. A consequence of this crisis was a sharp contraction in the availability of repo financing. CCC's repo lenders marked the value of its RMBS down substantially, and as a result made extremely large margin calls which CCC was unable to meet.

The irony was excruciating. Here was Carlyle—masters of leverage in private equity—brought down by leverage in public markets. The same firm that had loaded portfolio companies with debt for decades couldn't manage its own borrowing when markets seized up. The losses to the Carlyle Group due to the collapse of Carlyle Capital are reported to be "minimal from a financial standpoint", but the reputational damage was immense.

While Carlyle Capital was melting down, the entire private equity industry was discovering that the music had stopped. The mega-deals of 2006 and 2007—Freescale, Hawaiian Telcom, and others—were underwater. Banks that had committed to finance buyouts were refusing to fund them or demanding massive discounts. The "denominator effect" was crushing institutional investors: as public equity portfolios collapsed, their private equity allocations suddenly exceeded target percentages, forcing them to stop new commitments. But survival required transformation. The years between 2008 and 2012 became Carlyle's crucible, forging a different kind of firm. They raised distressed debt funds to buy the loans banks were desperate to shed. They expanded internationally, particularly in Asia where growth continued despite Western malaise. Most importantly, they began contemplating what had been unthinkable for a private equity firm: going public.

The decision to IPO wasn't just about raising capital; it was about permanence. The founders—Rubenstein, Conway, and D'Aniello—were all approaching 60. Without a public listing, Carlyle risked the fate of many partnerships: gradual dissolution as founders retired and junior partners fought over the spoils. Going public would create a permanent capital base, a currency for acquisitions, and liquidity for the hundreds of Carlyle professionals who owned stakes in the firm.

As of December 31, 2011, Carlyle had approximately $147 billion of assets under management across 89 active funds and 52 fund of fund vehicles. The recovery from the crisis had been remarkable—not just in AUM but in positioning. They'd evolved from a U.S.-focused buyout shop to a global alternative asset manager with four distinct segments: Corporate Private Equity, Real Assets, Global Market Strategies, and Fund of Funds Solutions.

On May 3, 2012, Carlyle priced the initial public offering of 30.5 million common units at $22 per unit, raising $671 million, with the units trading on the NASDAQ Global Select Market under the symbol "CG". It was the fourth-largest IPO for a private equity company on record.

The IPO transformed the three founders into instant billionaires on paper, with each taking home $138 million in 2011. Together, they retained 51% ownership, ensuring control while gaining liquidity. But the public markets were skeptical. Blackstone was trading around 56 percent below its IPO price, and Apollo Global Management was around 32 percent below its offering. Investors struggled to value firms whose earnings came in unpredictable bursts from carried interest rather than steady management fees.

What the IPO really represented was Carlyle's transition from partnership to institution. The days of five guys making deals around a conference table were definitively over. In their place stood a global platform with 1,300 employees across 33 offices, managing everything from Asian growth equity to European real estate. The crisis had nearly killed them, but like the best private equity deals, they'd emerged from restructuring stronger and more valuable than before.

VI. Public Company Evolution: Leadership Changes & Strategic Shifts (2012–2020)

Life as a public company initially seemed to validate Carlyle's transformation. They expanded aggressively into new asset classes—credit, infrastructure, real estate—becoming less dependent on the boom-bust cycle of leveraged buyouts. The AUM climbed steadily, reaching new records quarter after quarter. But beneath the surface, tensions were building about succession, strategy, and whether the founding trio could ever truly let go.

The October 2017 investment in Supreme perfectly captured Carlyle's evolution. In October 2017, the Carlyle Group made a $500 million investment in the brand Supreme valuing the company at $1 billion. Here was a streetwear brand built on exclusivity and counterculture—the antithesis of private equity's corporate image. Yet Carlyle saw what others missed: a digitally native brand with 60% e-commerce sales, fanatical customer loyalty, and massive untapped international potential.

The Carlyle Group paid USD 500 million in 2017 for a roughly 50% stake in the fashion brand, an investment that could double in value based on the latest transaction. When In 2020, the investment was acquired by VF Corporation, which owns The North Face, Timberland, and Vans for $2.1 billion. In three years, Carlyle had doubled their money on a brand that many thought they'd ruin with corporate interference. The secret? They left founder James Jebbia alone to run his business while providing operational support and international expansion expertise.

But the real drama was happening in Carlyle's C-suite. After three decades of control, the founders finally acknowledged what everyone else could see: succession planning couldn't wait forever. In October 2017—the same month as the Supreme investment—they announced that Glenn Youngkin and Kewsong Lee would become co-CEOs, with the founders stepping back from day-to-day operations. Youngkin lasted just two years before leaving to successfully run for governor of Virginia, leaving Lee as sole CEO. Meanwhile, the portfolio continued to evolve dramatically. In 2021, Carlyle teamed with Blackstone and Hellman & Friedman to acquire Medline Industries for $34 billion—the largest healthcare leveraged buyout ever. The deal showcased how Carlyle had evolved: from doing billion-dollar deals alone to partnering on transactions so massive that even they needed help financing them.

January 2021 saw Carlyle take a majority stake in Jagex, the developer of RuneScape, showing their willingness to invest in digital entertainment. March 2022 brought the acquisition of Dainese, the Italian motorcycle gear manufacturer, for an undisclosed sum. May 2022 saw the $3.9 billion purchase of ManTech International, returning Carlyle to its defense industry roots but at a scale unimaginable in the 1990s.

Throughout this period, the firm grappled with a fundamental tension: how to be both a public company satisfying quarterly earnings expectations and a long-term investor managing decade-long fund cycles. The stock price reflected this struggle, consistently trading at a discount to both book value and competitors. Public investors couldn't quite figure out how to value a business where the real money—carried interest—came in unpredictable lumps years after investments were made.

The decade from 2012 to 2020 proved that Carlyle could survive as a public company, but questions remained about whether it could thrive. The founders had successfully navigated the IPO, expanded globally, and diversified beyond traditional buyouts. But as 2020 ended, a new challenge emerged: could Carlyle transition to the next generation of leadership while maintaining the culture and relationships that had built the firm? The answer would come sooner—and more dramatically—than anyone expected.

VII. Modern Era: New Leadership & Global Expansion (2020–Present)

The boardroom drama that erupted in 2022 would have made compelling television. Kewsong Lee, who'd been sole CEO since Glenn Youngkin left to become Virginia's governor, was locked in a power struggle with the founders over compensation and control. Lee wanted the autonomy and pay package of a true CEO; the founders, particularly Conway and Rubenstein, weren't ready to fully let go. The tension became untenable, and in August 2022, Lee abruptly resigned, leaving Bill Conway as interim CEO at age 73.

The search for a new leader became existential. Carlyle needed someone with the stature to command respect from the founders, the operational expertise to run a public company, and the vision to chart a path forward. On February 15, 2023, they found their answer: Harvey M. Schwartz was appointed as Chief Executive Officer and a member of the Board.

Schwartz, born in 1964, is currently CEO of The Carlyle Group, the world's sixth-largest private equity firm. He previously worked at Goldman Sachs from 1997 to 2018, rising through the position of chief financial officer to that of president and co-chief operating officer. His Goldman pedigree was impeccable—he'd helped navigate the firm through the 2008 crisis as CFO, then served as president during its resurgence. More importantly, he understood both the public markets that valued Carlyle and the private markets where it invested.

At Carlyle, Mr. Schwartz would be responsible for setting and executing a strategy that advances and accelerates the diversification plan the firm has successfully pursued, as well as identifying new investment opportunities to further grow and scale the firm, drive sustained performance for fund investors, and create significant shareholder value.

The appointment signaled a new era. For the first time in Carlyle's history, someone outside the founding circle held ultimate authority. Schwartz moved quickly to modernize operations, streamline decision-making, and most importantly, articulate a vision for Carlyle that went beyond the founders' legacy. Under Schwartz's leadership, Carlyle has accelerated its global expansion and sector diversification. In February 2025, The Carlyle Group entered India's auto components market by acquiring a controlling stake in an entity formed through the merger of Indian auto parts companies Highway Industries and Roop Automotives. The deal, reportedly worth $400 million with Carlyle taking a 65-70% stake, exemplifies the firm's push into emerging markets and advanced manufacturing.

Amit Jain, Managing Director and Head of Carlyle India Advisors, articulated the strategy: "We believe India offers a tremendous opportunity in the advanced manufacturing sector, particularly in the auto components supply chain for both domestic and export markets."

The modern Carlyle manages $465 billion of assets under management, operating from 29 offices across four continents with over 2,300 employees. The portfolio spans everything from Mediterranean oil and gas ventures to RuneScape video games, from Italian motorcycle gear to Indian auto parts. It's a far cry from the boutique defense contractor investor of the 1990s.

Yet challenges remain. The stock still trades at a discount to peers, reflecting investor skepticism about private equity's public market prospects. Competition has intensified from all angles—sovereign wealth funds with patient capital, family offices with direct investment capabilities, and new players with innovative models. The carried interest tax treatment that has enriched private equity partners faces political pressure globally.

More fundamentally, Carlyle must answer whether its model—raising successive funds, charging management fees, earning carried interest—remains relevant in a world of permanent capital vehicles and direct investing. Schwartz has begun addressing these questions, pushing into credit, expanding wealth management channels, and building more recurring fee streams.

The firm's recent performance suggests momentum is building. Record fee-related earnings, successful fund raises, and strategic acquisitions indicate that Carlyle has successfully navigated its leadership transition. But the real test lies ahead: can a firm built on political connections and defense expertise thrive in an era of technological disruption, ESG mandates, and democratized access to alternatives?

What's certain is that Carlyle's journey from Washington boutique to global powerhouse represents more than one firm's evolution—it mirrors the transformation of private equity itself from a niche financial technique to a dominant force in global capitalism. The next chapter, under Schwartz's pen, will determine whether Carlyle can transcend its origins to become something greater: not just a private equity firm that went public, but a permanent capital allocator for the 21st century.

VIII. Business Model & Investment Strategy

The architecture of Carlyle's business model reads like a masterclass in financial engineering layered with relationship capital. At its core, the firm operates through three distinct but interconnected segments that generate multiple revenue streams from the same underlying activity: investing other people's money.

Global Private Equity remains the flagship, managing leveraged buyout and growth capital funds across geographic and sector-specific vehicles. The economics are straightforward yet lucrative: charge 1.5-2% annual management fees on committed capital during the investment period, then on invested capital thereafter. But the real money comes from carried interest—typically 20% of profits above an 8% preferred return. A $10 billion fund generating a 2x return creates $2 billion in carried interest for Carlyle. Multiply that across dozens of funds, and you understand why the founders became billionaires.

The beauty of the model lies in its scalability. Once you've built the infrastructure—deal teams, operating partners, back-office support—adding another billion in AUM costs relatively little. The marginal economics are extraordinary: that next billion generates $20 million in annual management fees with minimal incremental expense.

Global Credit represents Carlyle's evolution beyond traditional buyouts. Global Credit pursues investment opportunities across various segments of private credit managing $194 billion in AUM as of December 31, 2024. This includes collateralized loan obligations (CLOs), direct lending to private equity-owned companies, opportunistic credit, and distressed debt. The shift to credit reflects a fundamental insight: in a world of perpetually low interest rates and yield-starved investors, being a sophisticated lender generates attractive risk-adjusted returns with more predictable cash flows than equity investments.

Global Investment Solutions, anchored by the AlpInvest acquisition, offers fund-of-funds, co-investment opportunities, and secondary purchases of existing private equity stakes. This segment serves investors who want private equity exposure but lack the scale or expertise to build their own portfolios. It's lower margin than direct investing but provides steady fees and deep market intelligence about what other firms are doing.

The geographic footprint tells its own story of ambition. Invested in 40 U.S. states and 39 countries, with offices from Tokyo to São Paulo, Carlyle has built a truly global platform. But unlike investment banks that plant flags everywhere, each Carlyle office represents deep local relationships and on-the-ground investment capabilities. The Mumbai office doesn't just source Indian deals for U.S. funds; it manages India-dedicated vehicles with local LPs.

Sector focus has evolved dramatically from the defense concentration of the 1990s. Today's portfolio spans technology, healthcare, consumer, financial services, energy, infrastructure, and real estate. Yet within each sector, Carlyle maintains specialized teams with genuine operating expertise. The healthcare team includes former hospital executives; the technology team features former software CEOs. This isn't just window dressing—these operating partners help identify targets, conduct due diligence, and drive post-acquisition value creation.

The LP (limited partner) base represents perhaps Carlyle's most valuable asset. These aren't just investors; they're a carefully cultivated network of pension funds, sovereign wealth funds, endowments, and insurance companies that commit capital fund after fund. CalPERS, the Canadian pension plans, Middle Eastern sovereign funds—these institutions don't just provide capital; they provide credibility. When Carlyle raises a new $15 billion buyout fund, half might come from existing LPs rolling over their commitments.

Fund structure has become increasingly sophisticated. Beyond traditional 10-year closed-end funds, Carlyle now offers longer-duration vehicles, perpetual capital structures, and separately managed accounts for large investors. The firm has also pushed into the retail market through vehicles accessible to individual investors, democratizing access to private equity while creating new fee streams.

The value creation playbook has evolved far beyond financial engineering. While leverage remains important—typically 50-65% debt financing on buyouts—operational improvements drive most returns. Carlyle's portfolio operations team, numbering in the hundreds, works with management teams on everything from procurement savings to digital transformation to international expansion. They'll bring in experts to optimize supply chains, restructure sales organizations, or accelerate R&D.

Risk management has become increasingly sophisticated, particularly after the 2008 crisis. The firm now models multiple scenarios for each investment, stress-tests portfolio companies regularly, and maintains strict diversity limits by sector and geography. The days of betting everything on defense contractors are long gone.

What makes Carlyle's model distinctive isn't any single element—competitors have similar fund structures, comparable return targets, and overlapping LP bases. It's the integration of political intelligence, operational expertise, and global reach. A Carlyle deal might originate from a government relations insight, get financed through Middle Eastern relationships, add value through operational improvements, and exit via an Asian strategic buyer. Few firms can orchestrate such complex value creation across multiple dimensions.

The model's sustainability faces real questions. Fee pressure continues as LPs demand better terms. The denominator effect limits new commitments when public markets decline. Competition from strategic buyers with permanent capital advantages challenges return expectations. Yet Carlyle's business model has proven remarkably adaptable, evolving from boutique advisory to defense investing to mega-buyouts to diversified alternatives. That adaptability, more than any specific strategy, may be its greatest strength.

IX. Competitive Analysis: Carlyle vs. The PE Giants

The private equity league tables read like a sports championship where Carlyle perpetually finishes in the medals but rarely takes gold. In June 2024, it ranked sixth in Private Equity International's PEI 300 ranking among the world's largest private equity firms, with The Carlyle Group Washington DC raising $60,178 million over the trailing five years. Ahead sit the usual suspects: Blackstone at $123,993 million, KKR at $103,241 million, EQT at $99,123 million, CVC at $77,570 million, and TPG at $61,934 million.

But raw fundraising numbers tell only part of the story. Carlyle's competitive position is more nuanced than rankings suggest. While Blackstone has become the everything store of alternatives—managing over $1 trillion including credit, real estate, and hedge funds—Carlyle has maintained a more focused approach. This isn't necessarily a weakness; it's a strategic choice about where to compete and how to win.

Blackstone represents the apex predator of private equity, roughly double Carlyle's size with superior public market valuation. Where Carlyle originated from Washington connections, Blackstone emerged from Wall Street royalty—Stephen Schwarzman and Pete Peterson literally wrote the playbook for modern private equity. Blackstone's advantages are scale (allowing them to do deals others can't), breadth (they're in everything), and brand (they're the Goldman Sachs of alternatives). Yet their very size creates challenges: finding enough large deals to deploy capital, managing complexity across disparate businesses, and maintaining returns as the law of large numbers kicks in.

KKR, Carlyle's closest historical peer, shares similar DNA—founded within a decade of each other, similar AUM, both public. But KKR's New York heritage gave it different advantages: deeper Wall Street relationships, earlier access to leverage innovations, and a more aggressive culture epitomized by the RJR Nabisco deal. Where Carlyle built on government connections, KKR built on financial engineering. Today, KKR has arguably adapted better to the modern era, with stronger technology investments and more innovative fund structures.

Apollo represents the credit-first model that Carlyle is trying to emulate. Leon Black built Apollo with a distressed debt mentality—buy cheap, restructure aggressively, maximize cash extraction. Apollo's massive credit business, managing over $400 billion, generates steadier fees than traditional buyouts. Carlyle's credit platform, while growing, hasn't achieved similar scale or margins. Apollo proves that being excellent at one thing (credit) can trump being good at many things.

TPG, founded by David Bonderman and Jim Coulter, mirrors Carlyle in many ways—similar size, diversified strategies, global presence. But TPG's West Coast roots gave it different sector expertise: technology, media, and consumer rather than defense and government. TPG went public after Carlyle, learning from others' mistakes, and achieved a better initial valuation. The firms often compete for the same deals, with success depending more on relationships and timing than fundamental advantages.

The European giants—CVC, EQT, Permira—represent different competitive dynamics. They dominate their home markets in ways American firms can't, given Europe's fragmented regulatory environment and relationship-driven business culture. Carlyle competes effectively in Europe but lacks the home-field advantage these firms enjoy. Conversely, European firms struggle to crack the U.S. market at scale.

Specialized players pose increasingly serious competition. Thoma Bravo in software, Vista Equity in enterprise technology, Silver Lake in technology growth—these firms' deep sector expertise allows them to win deals through operational value creation rather than financial engineering. Carlyle's generalist approach, while providing diversification, can't match their specialized knowledge.

The sovereign wealth funds and family offices represent competition of a different sort. They're not raising outside capital but investing directly, often willing to accept lower returns for strategic benefits. Singapore's GIC, Abu Dhabi's Mubadala, Canada's pension plans—these institutions increasingly bypass private equity firms entirely, hiring their own teams and doing direct deals.

Performance comparison reveals mixed results. Carlyle's returns have historically been strong—high teens to low twenties across most vintage years—but not exceptional. Top-quartile but rarely top-decile. The firm's diversification helps smooth returns but prevents the spectacular outcomes that focused firms sometimes achieve. A software-focused fund might generate 3x returns in a good vintage; Carlyle's diversified funds more typically deliver 1.8-2.2x.

Public market valuation tells a harsh truth: investors don't fully value Carlyle's franchise. The stock trades at roughly 10-12x earnings versus 15-20x for traditional asset managers, reflecting uncertainty about carried interest timing and sustainability. Blackstone trades at a premium to Carlyle despite similar business models, suggesting either superior execution or better investor relations.

Carlyle's competitive advantages remain real but increasingly replicable. The government connections that once opened unique doors matter less in a world of competitive auctions. The global platform that took decades to build can now be assembled quickly with enough capital. The sector expertise, while valuable, faces challenge from specialized firms with deeper knowledge.

What distinguishes Carlyle today isn't any single dominant advantage but rather the combination of capabilities: credible at mega-deals but also in mid-market, strong in buyouts but growing in credit, American roots but global presence, sector expertise but diversified exposure. It's the Swiss Army knife of private equity—not the best at any single function but useful across many situations.

The question facing Carlyle isn't whether it can compete—clearly it can—but whether being sixth-largest is a stable position. In an industry increasingly dominated by scale advantages, can Carlyle thrive as a strong second-tier player? Or must it either grow dramatically or specialize more narrowly? The answer will determine whether Carlyle remains a permanent fixture in the top ten or gradually slides toward irrelevance.

X. Playbook: Lessons from Carlyle's Journey

The Carlyle story offers a masterclass in building a financial empire from an unlikely starting point. While competitors emerged from Wall Street trading floors or Harvard Business School classrooms, Carlyle grew from Washington conference rooms and Georgetown dinner parties. The lessons from their journey apply far beyond private equity.

The Power of Regulatory Arbitrage: Carlyle's founding insight—that understanding government creates investment alpha—remains profoundly relevant. Every major Carlyle success, from defense consolidation to healthcare roll-ups, originated from regulatory intelligence. They understood that in highly regulated industries, knowing what rules would change mattered more than traditional financial analysis. The lesson: in any complex system, those who understand the rules best can exploit inefficiencies others miss.

Building Sector Specialization Through Pattern Recognition: Carlyle didn't randomly become defense experts; they recognized that their Washington DNA gave them unique advantages in government-adjacent industries. They then systematically built expertise through hiring, deals, and relationships. Each successful defense deal made the next one easier—portfolio companies could share contracts, executives could move between firms, knowledge accumulated. The pattern: identify your unfair advantage, systematically deepen it, then expand to adjacent areas where that advantage translates.

The Double-Edged Sword of Political Connections: Carlyle's government relationships opened doors but also created vulnerabilities. The bin Laden controversy, the perception as a "Republican" firm, the scrutiny during defense deals—political connections brought both opportunity and liability. The broader lesson: any competitive advantage that depends on relationships or perception requires careful management and can quickly become a disadvantage if public sentiment shifts.

Timing Public Markets—The Cost of Being Early: Carlyle's 2012 IPO came at a challenging time for private equity public listings. Earlier movers like Blackstone had disappointed public investors; the model of lumpy carried interest didn't fit neatly into quarterly earnings expectations. Yet waiting longer might have meant missing the window entirely. The lesson: in timing strategic moves, being early and suffering initial pain may be better than being perfect but late.

Managing Through Crisis by Returning to Core Strengths: The 2008 financial crisis nearly destroyed Carlyle Capital and severely damaged the firm's reputation. Yet Carlyle survived by returning to what it knew best—disciplined buyouts in sectors they understood. They didn't chase exotic structures or unfamiliar markets. Crisis revealed that their core competency wasn't leverage or financial engineering but sector expertise and operational improvement.

Leadership Succession as Existential Challenge: The transition from founder control to professional management nearly tore Carlyle apart. The Kewsong Lee departure showed how difficult it is for founders to truly cede control. Yet bringing in Harvey Schwartz—an outsider with gravitas—finally broke the pattern. The lesson: successful succession requires founders to accept real loss of control, not just titular change.

Global Expansion Through Local Presence: Unlike investment banks that parachute into countries for specific deals, Carlyle built genuine local presence with native teams. The Tokyo office isn't Americans doing Japanese deals; it's Japanese professionals with deep local relationships. This required patience, capital, and accepting lower initial returns, but created sustainable competitive advantages.

The Platform Evolution—From Deals to Asset Management: Carlyle's transformation from deal-by-deal merchant bank to diversified asset manager required fundamental changes in mindset, systems, and people. They had to build repeatable processes, institutional memory, and scalable infrastructure. The playbook: start opportunistic, systematize what works, then scale aggressively.

Operational Value Creation as Sustainable Advantage: As financial engineering advantages eroded—everyone could access leverage, competition bid up prices—Carlyle invested heavily in operational capabilities. Portfolio operations teams, sector expertise, digital transformation capabilities—these became the new sources of alpha. The lesson: when financial arbitrage disappears, operational excellence becomes the differentiator.

The Diversification Paradox: Carlyle's expansion into credit, real estate, and infrastructure provided stability but diluted focus. Each new area required different skills, relationships, and investment approaches. Some worked (credit), others struggled (hedge funds). The teaching: diversification reduces risk but also reduces excellence; knowing when to stop expanding is as important as knowing when to start.

Managing Public Market Expectations While Running Private Market Strategies: As a public company, Carlyle faces quarterly earnings pressure while managing funds with 10-year horizons. They've addressed this through increased disclosure, regular distributions, and educating investors about the model. Yet the stock still trades at a discount, suggesting incomplete success. The challenge: aligning short-term market expectations with long-term value creation remains unsolved.

The Network Effect in Professional Services: Carlyle's true asset isn't its funds or portfolio companies but its network—thousands of executives, advisors, and limited partners who provide deals, expertise, and capital. Each successful exit creates executives who might run the next portfolio company; each satisfied LP might increase their commitment. Networks compound exponentially but require constant cultivation.

Adapting to Technological Disruption: Carlyle's recent investments in software, gaming, and digital infrastructure show adaptation to technological change. Yet they're following, not leading—Vista and Thoma Bravo understood software first. The lesson: established firms can adapt to disruption but rarely lead it; success comes from fast following rather than innovation.

The Importance of Controversy Management: From bin Laden to bankruptcy, Carlyle has weathered numerous controversies. Their approach—acknowledge quickly, change if necessary, move forward—has generally worked. They severed the bin Laden connection immediately, replaced leadership when needed, and maintained institutional continuity. Crisis management isn't about avoiding controversy but managing it when it inevitably arrives.

The Carlyle playbook ultimately teaches that building a global investment firm requires more than capital and connections. It demands the ability to evolve continuously—from boutique to institution, from specialist to generalist, from private to public—while maintaining core disciplines of risk management, relationship cultivation, and value creation. The firms that survive aren't necessarily the largest or most profitable, but those most capable of adaptation.

XI. Bear vs. Bull Case & Future Outlook

The Bull Case: Platform Power in a Growing Industry

The optimistic view of Carlyle rests on structural advantages that compound over time. Start with scale: at $465 billion AUM, Carlyle has achieved escape velocity where size begets size. Large LPs need to deploy billions efficiently; they can write $500 million checks to Carlyle but not $50 million to emerging managers. This concentration of capital among mega-firms accelerates as smaller investors struggle to raise funds.

The diversification across strategies provides multiple engines of growth. When buyout markets slow, credit thrives. When U.S. deals become too expensive, Asia offers opportunities. This isn't just risk management—it's optionality. Carlyle can pivot capital and talent to whatever strategy offers the best risk-adjusted returns. Smaller, focused firms lack this flexibility.

Harvey Schwartz's leadership represents a genuine reset. Unlike previous internal promotions, Schwartz brings Goldman Sachs operational excellence and public market credibility. Early indicators—record fee-related earnings, successful fund raises, strategic acquisitions—suggest he's executing effectively. The founder overhang that plagued previous leaders has finally lifted.

The secular trend toward alternatives remains powerful. As public markets become more efficient and bonds yield nothing, institutional investors must increase alternative allocations to meet return targets. McKinsey projects alternative AUM growing from $13 trillion to $24 trillion by 2030. Even maintaining market share means massive growth for Carlyle.

Technological transformation creates unprecedented investment opportunities. Every company needs digital transformation, cybersecurity, and data analytics. Carlyle's operational resources can help portfolio companies navigate these transitions, creating value beyond financial engineering. Their recent tech investments show they're learning to compete in the innovation economy.

Geographic expansion offers decades of growth. Carlyle's February 2025 entry into India's auto components market exemplifies the opportunity: massive markets, growing middle classes, and underdeveloped private capital markets. As these economies mature, local private equity becomes essential for growth capital and corporate development.

The credit platform provides ballast and growth. Credit generates steadier fees than buyouts, appeals to different investors, and faces less competition from strategic buyers. As banks retreat from lending due to regulation, private credit fills the gap. Carlyle's $194 billion credit AUM could double while maintaining attractive returns.

The Bear Case: Structural Headwinds and Competitive Erosion

The pessimistic view sees Carlyle trapped between larger players with scale advantages and smaller firms with specialization benefits. At sixth-largest, Carlyle lacks Blackstone's gravitational pull or boutique firms' nimbleness. This "stuck in the middle" position typically erodes over time.

Fee pressure continues inexorably. LPs increasingly demand lower management fees, reduced carried interest, and better terms. The 2-and-20 model that built Carlyle's fortune is becoming 1.5-and-15, or worse. As fees compress, only massive scale or spectacular returns maintain margins. Carlyle has neither Blackstone's scale nor top-decile performance.

Competition intensifies from every angle. Strategic buyers with permanent capital can pay higher prices. Sovereign wealth funds do direct deals, bypassing private equity entirely. Family offices hire ex-PE professionals to build internal capabilities. The proliferation of capital reduces returns for everyone.

The public market discount appears permanent. Despite years as a public company, Carlyle trades at valuations implying the market doesn't believe the model. Either investors fundamentally misunderstand the business—unlikely after a decade—or they correctly perceive structural challenges. The discount limits Carlyle's ability to use stock for acquisitions or retention.

Technological disruption threatens traditional private equity. Software can now perform due diligence, AI can identify targets, and platforms can syndicate deals. The human relationships and expertise that justified huge fees are being automated. Younger firms born digital have advantages Carlyle can't replicate.

Political and regulatory risks are mounting globally. Carried interest tax treatment faces pressure in the U.S. and Europe. Antitrust authorities increasingly scrutinize PE roll-ups. ESG requirements add costs and limit investment options. The regulatory arbitrage that Carlyle mastered is reversing.

Leadership stability remains uncertain. While Schwartz has started well, Carlyle's history of leadership drama creates uncertainty. The founders still own significant stakes and board seats. Will they truly let Schwartz transform the firm, or will they intervene if changes threaten their legacy?

Future Strategic Priorities

Carlyle's path forward requires decisive choices about identity and ambition. Several strategic imperatives emerge:

Wealth Management Penetration: The retail market represents trillions in untapped capital. Carlyle must create products accessible to individual investors while maintaining institutional quality. This requires new distribution, different fee structures, and simplified communications—challenging transformations for an institutional firm.

Technology Platform Investment: Beyond investing in tech companies, Carlyle must become a technology company. This means AI-powered due diligence, automated portfolio monitoring, and digital LP interfaces. The firms that successfully digitize will have massive advantages in efficiency and scale.

Emerging Markets Expansion: Developed markets are saturated with capital. The real growth lies in India, Southeast Asia, Africa, and Latin America. But succeeding requires more than opening offices—it demands local talent, cultural understanding, and patience with different return profiles.

Credit and Permanent Capital: The future of alternatives may look more like lending than buyouts. Building massive credit platforms with permanent capital vehicles provides steady fees and reduces fundraising burden. Carlyle must decide whether to build, buy, or partner to achieve critical scale.

Sector Verticalization: Generalist investing increasingly loses to specialized expertise. Carlyle might need to reorganize around sectors—healthcare, technology, energy—with dedicated teams, strategies, and brands. This conflicts with the "One Carlyle" culture but may be necessary for competitiveness.

The Verdict: Gradual Decline or Transformation?

The most likely scenario sees Carlyle remaining a significant but gradually less relevant player—profitable, stable, but not transformative. The firm has too much momentum to fail quickly but lacks the bold vision to reinvent the industry. They'll continue raising funds, doing deals, and generating acceptable returns, but the electricity of the early years is gone.

Unless Schwartz can execute a genuine transformation—not just operational improvements but fundamental model innovation—Carlyle risks becoming the IBM of private equity: respected, profitable, but no longer defining the future. The next five years will determine whether Carlyle writes a new chapter or becomes a case study in institutional senescence.

XII. Recent News

The recent news flow from Carlyle reflects a firm in full execution mode under Harvey Schwartz's leadership. Our quarterly results reflect focused execution against our long-term strategy, evidenced by record Fee Related Earnings, FRE margin, and assets under management, Schwartz noted in the Q1 2025 earnings call.

For the fourth quarter and full-year ended December 31, 2024, U.S. GAAP results included income before provision for income taxes of $265 million and $1.4 billion, respectively. Carlyle delivered a strong 2024, meeting every financial target we set, including record Fee Related Earnings and FRE margin, and robust inflows.

The firm's assets under management reached $453 billion as of March 31, 2025, continuing its steady growth trajectory. The Board of Directors has declared a quarterly dividend of $0.35 per common share. For full-year 2024, the Board of Directors declared $1.40 in aggregate distributions to common shareholders, demonstrating confidence in cash generation capabilities.

Strategic transactions continue to demonstrate Carlyle's diversification. Trucordia today announced it will receive a $1.3 billion strategic investment from global investment firm Carlyle's Global Credit platform. The transaction will reduce Trucordia's leverage and simplify its governance structure by repurchasing units from existing minority investors.

In the life sciences space, Carlyle and SK Capital announced the tender offer to acquire all of the outstanding common stock of bluebird bio, Inc. for either $3.00 per share in cash and a contingent value right per share, entitling the holder to a payment of $6.84 in cash per contingent value right.

The entertainment sector saw Carlyle expand with Entertainment 360, one of the world's premier talent management companies, announced today that it would be receiving an investment from global investment firm Carlyle. The transaction marks the first time in Entertainment 360's 22-year history that the company has received outside funding.

Carlyle Announces Senior Leadership Appointments in July 2025, continuing to strengthen its management bench as it scales operations globally.

Looking ahead, The firm remains 'very, very focused' on the performance of Fund VIII, which closed below target in 2023, and is eyeing Q4 2025 launch for next private equity flagship, suggesting continued fundraising momentum despite market challenges.

XIII. Links & Resources

Official Carlyle Resources: - Corporate Website: www.carlyle.com - Investor Relations: ir.carlyle.com - LinkedIn: The Carlyle Group - X (Twitter): @OneCarlyle

Regulatory Filings: - SEC EDGAR Database: Search "The Carlyle Group Inc." (CG) - Annual Reports (10-K) and Quarterly Reports (10-Q) - Proxy Statements (DEF 14A)

Industry Analysis & Rankings: - Private Equity International PEI 300 Annual Rankings - Preqin Global Private Equity Report - McKinsey Private Markets Annual Review - Bain & Company Global Private Equity Report

Historical Resources: - "The Carlyle Group: The Iron Triangle" (Documentary) - "King of Capital" by David Carey and John Morris (on Blackstone, but covers Carlyle extensively) - Michael Moore's "Fahrenheit 9/11" (controversial portrayal) - Harvard Business School Case Studies on Carlyle

Academic Research: - "The Economics of Private Equity Funds" - Andrew Metrick & Ayako Yasuda - "Private Equity Performance: What Do We Know?" - Harris, Jenkinson & Kaplan - INSEAD and Wharton papers on private equity governance

Industry Publications: - Private Equity International - Buyouts Magazine - PE Hub - Alternative Investment Management Association (AIMA)

Competitor Resources: - Blackstone (BX): blackstone.com - KKR (KKR): kkr.com - Apollo Global (APO): apollo.com - TPG (TPG): tpg.com

Portfolio Company Examples: - Medline Industries - Supreme (sold to VF Corp) - ManTech International - Jagex (RuneScape)

Professional Networks: - Institutional Limited Partners Association (ILPA) - American Investment Council - Emerging Markets Private Equity Association (EMPEA)

Data Providers: - PitchBook - Preqin - S&P Capital IQ - Refinitiv

Podcast & Media Coverage: - "Masters in Business" episodes featuring PE leaders - "The Deal" podcast coverage - Bloomberg Deals coverage - Financial Times Due Diligence newsletter

Note: This analysis is based on publicly available information and should not be considered investment advice. Readers should conduct their own due diligence and consult with qualified financial advisors before making investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube