CDW Corporation: From Garage Startup to IT Services Giant

I. Introduction & Episode Roadmap

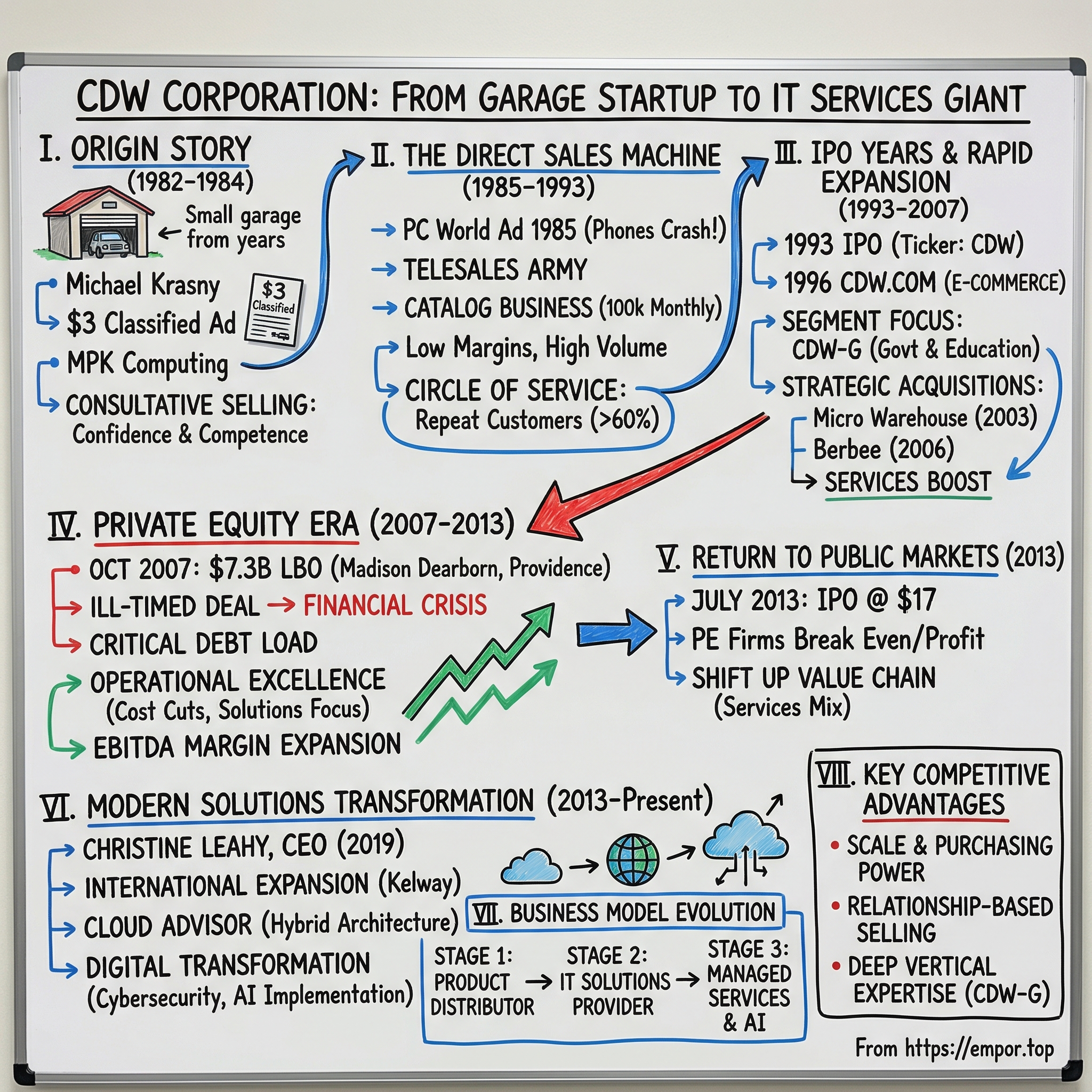

Picture this: A computer salesman in Chicago, recently laid off, places a three-line classified ad in a free newspaper for $3. He's just trying to unload his used computer. Instead, the phone rings off the hook with buyers wanting not just computers, but someone to explain this mysterious new technology called the "personal computer." That salesman was Michael Krasny, and that $3 ad in 1982 would spawn CDW Corporation—today a Fortune 500 company generating $21 billion in annual net sales, employing over 15,000 professionals, and serving a quarter million organizations worldwide.

The CDW story reads like a business school case study in perfect market timing meets relentless execution. From a garage startup riding the PC revolution to becoming North America's largest technology solutions provider, CDW has navigated every major computing transition: PCs to client-server, internet explosion, cloud migration, and now AI transformation. Along the way, it survived a spectacularly ill-timed $7.3 billion private equity buyout just before the 2008 financial crisis, reinvented itself from a box-mover to a solutions architect, and built one of the most loyal customer bases in B2B technology.

This is fundamentally a story about three transformations. First, how a direct sales pioneer disrupted traditional computer retail by obsessing over customer service when everyone else obsessed over inventory. Second, how private equity ownership during the worst financial crisis since the Depression forced operational excellence that competitors couldn't match. And third, how a products distributor successfully climbed the value chain to become a trusted technology advisor—a transition most distributors attempt but few achieve.

We'll trace CDW's evolution through distinct eras: the scrappy startup years when Krasny's "Circle of Service" philosophy created fanatic customer loyalty; the go-go public company years of geographic and segment expansion; the bruising but transformative private equity period; and the modern era of strategic acquisitions and services transformation. Each phase reveals timeless lessons about building competitive moats, navigating technology disruptions, and the compounding power of customer relationships.

The key themes that emerge: How direct sales and relationship-based selling created durable advantages in a commoditized industry. Why customer service obsession matters more than price in B2B markets. How to successfully transition from selling products to selling outcomes. And perhaps most importantly, how a company selling commodity hardware built a services business with recurring revenue streams and expanding margins.

II. The Michael Krasny Origin Story (1982–1984)

The mythology of Silicon Valley celebrates the college dropout in a garage. CDW's origin story is distinctly Midwestern: a laid-off computer salesman, a free newspaper, and a relentless focus on helping confused customers navigate an intimidating new technology. In 1982, Michael Krasny found himself unemployed when his employer, a struggling computer retailer, went under. With a mortgage to pay and minimal savings, he decided to sell his personal computer—an expensive luxury he could no longer afford.

The ad was simple: three lines in the Advertiser, a free-circulation Chicago newspaper. Cost: $3. But something unexpected happened. The phone started ringing with buyers, and it didn't stop. More intriguingly, these callers didn't just want to buy a computer—they wanted someone to explain what a computer was, what it could do, and most importantly, how to make it work. Personal computers in 1982 were alien technology to most Americans. The IBM PC had launched just a year earlier. Most small businesses still used typewriters and filing cabinets. The callers reaching Krasny were pioneers, but nervous ones.

Rather than simply selling his computer to the highest bidder, Krasny developed what would become CDW's foundational insight. He created a consultative sales pitch: Let me not just sell you a computer, but set up your entire system, teach you how to use it, and be your ongoing technology advisor. When prospects agreed—and many did—the venture that would become Computer Discount Warehouse was born. Krasny incorporated the business in 1984 as "MPK Computing" (his initials), operating initially from his home in Chicago.

The early business model was beautifully simple and perfectly timed. Personal computers were expensive, complicated, and intimidating. Buyers—especially small businesses—desperately needed someone who could demystify the technology. Krasny became that trusted advisor, spending hours on the phone with customers, often walking them through basic operations like installing software or connecting printers. He wasn't just selling boxes; he was selling confidence and competence in the digital age.

By 1985, a fascinating pattern emerged. Krasny noticed he was selling multiple computer systems to a single buyer—a Chicago entrepreneur who was reselling them by mail. This customer was marking up each machine by $300, nearly doubling the profit margin. The revelation was profound: there was massive demand for computers sold directly to end users, bypassing traditional retail channels. But Krasny saw an even bigger opportunity. While his competitor marked up machines by $300, Krasny decided to add just $25. Volume over margin—a decision that would define CDW's strategy for decades.

This pricing philosophy wasn't just about undercutting competition. Krasny understood something fundamental about the direct sales model: customer acquisition cost is high, but customer lifetime value is even higher if you deliver exceptional service. By keeping margins razor-thin, he could capture market share rapidly. By providing fanatical customer service, he could turn one-time buyers into repeat customers. In an industry where most players focused on the transaction, Krasny focused on the relationship.

The numbers from this period are modest but revealing. CDW generated roughly $2 million in sales in 1984, its first full year of operations. But more importantly, over 60% of revenue came from repeat customers—an astronomical figure in the early PC industry where most sales were one-time transactions. Krasny's "Circle of Service" philosophy was already taking shape: treat every customer interaction as the beginning of a relationship, not the end of a sale.

III. Building the Direct Sales Machine (1985–1993)

In November 1985, Krasny made a bet that would transform CDW from a local operation to a national player. He spent $3,000—a significant sum for the young company—on a full-page advertisement in PC World magazine. The ad was deliberately understated: no flashy graphics, just product listings with prices that were 15-30% below typical retail. The phone system crashed within hours of the magazine hitting newsstands. CDW had to hire five new salespeople within a week just to handle the call volume.

This moment crystallized CDW's core strategy: combine aggressive pricing with obsessive customer service, and distribute through direct channels to maintain margins despite low markups. While competitors like CompUSA and Computer City were building expensive retail footprints, CDW was building a telesales army. Each salesperson was trained not just to take orders but to become a technology consultant. The average CDW sales call in 1987 lasted 18 minutes—an eternity in transactional sales but perfectly reasonable for consultative selling.

The catalog business launched in 1986, initially just a photocopied price list that looked like it was produced in someone's basement—because it was. But customers didn't care about production values; they cared about selection and price. By 1988, CDW was mailing 100,000 catalogs monthly, each one thicker than the last. The 1989 catalog ran 248 pages and featured over 3,000 products. For comparison, the Sears catalog—the gold standard of mail-order retail—dedicated just 12 pages to computers.

Krasny made a curious decision in 1989: he opened a retail showroom in Chicago. This seemed to contradict CDW's direct-sales model, but Krasny understood something subtle about B2B technology sales. Corporate buyers wanted to touch and test products before making large purchases. The showroom wasn't meant to generate retail sales; it was a proof point that CDW was a "real" company. Revenue from the showroom never exceeded 2% of total sales, but it served its purpose as a credibility builder.

The financial trajectory during this period was extraordinary. Sales grew from $2 million in 1984 to $58 million in 1989, then exploded to $176 million in 1991 and $271 million in 1992. Net margins were thin—averaging just 2.3%—but the return on equity was spectacular because CDW required minimal capital. The company was essentially a logistics and sales operation, carrying little inventory and collecting payment from customers before paying vendors. The competition during this period reveals CDW's strategic genius. While the PC industry consolidated into retail giants—CompUSA, Computer City, MicroAge—CDW stayed focused on direct sales. The personal computer business suffered an ugly downturn in 1991 that squelched sales by most retailers. In contrast, the direct marketing channel continued to grow. As overall personal computer shipments plummeted 14 percent in 1991, traditional retailers watched from the sidelines as direct marketers increased PC sales by a whopping 76 percent. CDW's timing was perfect: they were riding the direct sales wave just as traditional retail was getting crushed.

But here's what separated CDW from other direct marketers: the "Circle of Service" wasn't just marketing fluff. Krasny implemented a radical compensation structure for the era. He paid CDW's employees with stock options and vacations, among other perks, and many of the company's salespeople earned well over $100,000 annually. In 1992, when the median household income was $30,000, CDW salespeople were earning triple that. This wasn't generosity—it was strategy. Well-compensated salespeople stayed longer, knew their customers better, and generated more repeat business.

The operational innovations during this period were equally impressive. CDW had been processing 200 orders daily with 12 people in its billing department in the 1980s. By the early 1990s, after implementing new information systems, the same department was churning out 5,000 orders each day with only four workers. This 75x improvement in productivity per employee funded the aggressive pricing strategy. CDW could afford to be the low-price leader because their operational efficiency was unmatched.

By 1993, CDW had become one of the top two computer direct marketers in the United States, neck-and-neck with Micro Warehouse. The company was processing over 5,000 orders daily, shipping from a 450,000-square-foot distribution center in Vernon Hills, and maintaining a customer retention rate exceeding 80%—extraordinary in an industry where most purchases were transactional. The stage was set for the next phase: going public and using capital markets to fuel geographic and segment expansion.

IV. The IPO Years and Rapid Expansion (1993–2007)

The IPO roadshow in May 1993 was a disaster—at least initially. Institutional investors couldn't understand CDW's model. How could a company with 2% net margins be worth a premium valuation? Why would customers pay CDW when they could buy directly from manufacturers? The bankers priced the offering at $6.25 per share, the low end of the range. But something remarkable happened: the stock opened at $8.50 and closed the first day at $10.25, a 64% pop. Within a year, shares traded above $25. The market had figured out what the roadshow investors missed: CDW wasn't selling computers; it was selling expertise and trust at scale.

Krasny took the company public in 1993 after changing the name from Computer Discount Warehouse to CDW Computer Centers. The initial public offering of stock brought expansion capital into CDW's war chest and provided Krasny just compensation for his efforts. His profits from stock sales combined with his 43 percent ownership share gave the 40-plus-year-old entrepreneur a net worth of some $350 million by the mid-1990s.

The public capital unleashed a growth explosion. In 1995, CDW surpassed $1 billion in annual sales. But the real innovation came with the internet revolution. In 1996, CDW launched CDW.com—not just a website, but a fully integrated e-commerce platform. Customers could check real-time inventory, configure systems, track shipments, and access their purchase history. This seems obvious now, but in 1996, most B2B companies treated websites as digital brochures. CDW spent $10 million building the platform—a massive bet for a company with $50 million in annual profits.

The internet strategy paid off spectacularly, but not how you'd expect. By 2000, online sales accounted for just 12% of total revenue. The real value was operational: online customers required 70% less sales support, ordered 40% more frequently, and had 25% higher average order values. The website didn't replace salespeople; it made them more productive by handling routine transactions so they could focus on complex, high-value engagements. Segment specialization became CDW's next growth vector. CDW-G was founded to focus exclusively on providing IT solutions to U.S. governmental entities, including K-12 schools, universities, non-profit healthcare organizations, and local, state, and federal governments. This wasn't just creating a sales division—it was building entirely different operational capabilities. Government contracts required specific certifications, complex procurement processes, and the ability to navigate federal acquisition regulations. CDW hired former government IT officials, built specialized contract vehicles, and developed deep expertise in education technology requirements.

The geographic expansion accelerated through strategic acquisitions. The watershed moment came in September 2003 when CDW acquired the assets of Micro Warehouse, its longtime rival that had filed for bankruptcy. The deal, valued at $22 million, was a steal—Micro Warehouse had generated over $1 billion in revenue just two years earlier. CDW cherry-picked the best salespeople, absorbed the customer relationships, and essentially eliminated its largest direct competitor overnight. But the real strategic coup came in October 2006 with the Berbee acquisition. CDW completed the acquisition for a total purchase price of $184 million, including an adjustment for working capital. Berbee was founded in 1993 by James G. Berbee and grew to over 300 million USD in revenue and more than 800 employees. This wasn't just buying revenue—it was acquiring capabilities CDW desperately needed. Berbee provided world-class solutions and engineering capabilities in advanced technologies primarily across the Cisco, IBM and Microsoft platforms. Areas of expertise included network infrastructure and unified communications, systems and storage, security, productivity applications and managed services.

The Berbee deal revealed CDW's strategic evolution. They weren't content being a box-mover; they wanted to climb the value chain into services and solutions. For the trailing 12 months ended July 31, 2006, Berbee's revenue was $390 million and earnings before interest, taxes, depreciation and amortization was $22 million. The price paid—roughly 8x EBITDA—was aggressive for a distribution business but reasonable for a services company. CDW was betting they could leverage Berbee's expertise across their entire customer base.

By 2007, CDW had transformed from a mail-order catalog company into a multi-channel IT solutions provider. Sales exceeded $8 billion. The company employed over 6,000 people, including 760 advanced technology specialists and engineers. They operated from two massive distribution centers totaling nearly one million square feet. The government and education division (CDW-G) had become a powerhouse, generating over $2 billion in annual sales. Everything was clicking. Which made the timing of what happened next particularly painful.

V. The Private Equity Era: Madison Dearborn & Providence (2007–2013)

October 12, 2007. The Dow Jones Industrial Average closed at 14,093—an all-time high. Lehman Brothers stock traded at $61. And in Vernon Hills, Illinois, CDW's board approved a $7.3 billion buyout by private equity firms Madison Dearborn Partners and Providence Equity Partners. The timing could not have been worse. Within twelve months, Lehman would be bankrupt, the Dow would lose half its value, and IT spending would crater as businesses slashed budgets. Madison Dearborn and Providence had just executed one of the most spectacularly ill-timed leveraged buyouts in private equity history. The numbers tell the story of private equity hubris. Madison Dearborn led the $7.3 billion buyout, putting up $1.1 billion in equity alongside Providence Equity Partners, which contributed $1.0 billion. The rest—over $5 billion—was debt. CDW shareholders received $87.75 in cash per share, representing a 16% premium to the last trading day and a 31% premium to the 90-day average. Everyone celebrated. John Edwardson, CDW's CEO who orchestrated the deal from the company side, stood to make $118 million. The bankers—J.P. Morgan, Lehman Brothers, Morgan Stanley—collected tens of millions in fees. It was the peak of the credit bubble, and everyone was drunk on leverage.

Then reality hit like a sledgehammer. By March 2009, the S&P 500 had fallen 57% from its peak. Corporate IT spending—CDW's lifeblood—collapsed as companies froze budgets and delayed upgrades. CDW's revenue fell from $8.1 billion in 2007 to $7.2 billion in 2009. EBITDA margins compressed. The company was burning cash to service its massive debt load. Madison Dearborn and Providence watched their $2.1 billion equity investment get marked down to virtually nothing. Industry observers started using CDW as a cautionary tale about the dangers of excessive leverage.

But here's where the story gets interesting. Rather than panic or try to flip the company quickly, the private equity owners did something unexpected: they got operationally excellent. Tom Richards joined as president and COO in 2009, then became CEO in 2011. Richards, a former executive at Qwest and US West, understood technology transformation and had experience managing through downturns. He implemented a three-pronged strategy: cut costs ruthlessly, invest in solutions capabilities, and prepare for the eventual recovery.

The cost cutting was surgical rather than slash-and-burn. CDW reduced headcount by 8% but protected the sales force and engineers. They renegotiated vendor agreements, optimized the distribution network, and automated back-office functions. The company saved over $200 million annually without damaging customer relationships. More importantly, they used the crisis to accelerate the transformation from products to solutions. While competitors retreated, CDW hired solution architects and acquired specialized capabilities in cloud, security, and managed services.

The operational improvements showed up in the numbers. Despite flat revenue, CDW's EBITDA margins expanded from 5.8% in 2009 to 7.2% in 2012. The company generated over $400 million in free cash flow annually, paying down debt and reducing leverage ratios. By 2012, CDW's net income had rebounded to $119 million, up from just $17 million in 2011. The company that looked like a disaster in 2009 had become a lean, efficient, solutions-focused machine.

Madison Dearborn and Providence learned an expensive lesson about market timing, but they also demonstrated the value of patient capital and operational discipline. The gains have been a long time coming for Madison Dearborn, which engineered the LBO in 2007, just before financial markets collapsed. The deep recession hurt CDW's business, forcing Madison Dearborn to wait six years before bringing the company back to public markets. That's much longer than private-equity firms like to wait for a cash-out. But the wait would prove worthwhile, as CDW emerged from private equity ownership stronger than it entered.

VI. The Return to Public Markets (2013)

June 27, 2013. The NASDAQ opening bell rang, and CDW Corporation began trading under the ticker "CDW" for the second time in its history. The IPO priced at $17 per share—well below the $87.75 that Madison Dearborn and Providence paid six years earlier. But adjusted for the operational improvements and debt paydown, the private equity firms were about to break even on what many considered a catastrophic investment. Sometimes in private equity, not losing money is its own victory. The IPO market drama was intense. CDW blazed back into the public markets on July 2, 2013, at an IPO offer price of $17 per share, and quickly ran up to $18.37 by close of trading—a one-day, 8.1% gain. Gross proceeds from the IPO, at $17 a share, worked out to about $454 million raised for CDW. Of this amount, the company said it intended to spend about $331 million paying down debt. The offering was smaller than originally planned—Madison Dearborn and Providence had hoped to sell shares in the IPO but pulled back when investors balked at what looked like a private equity exit rather than a growth story.

But here's what the market initially missed: CDW wasn't the same company that went private in 2007. The operational improvements during the private equity years had fundamentally transformed the business. Revenue per employee had increased by 22%. EBITDA margins had expanded by 140 basis points. The company had reduced its debt-to-EBITDA ratio from over 7x to under 5x. Most importantly, the services and solutions mix had increased from 8% to 15% of gross profit—a critical shift up the value chain.

The stock performance vindicated the transformation. Within a year, shares traded above $25, and by December 2014, they reached $34—double the IPO price. Madison Dearborn, Chicago's largest private-equity firm, sold 40 million CDW shares at prices ranging from $20.50 to $33.28, for total proceeds of $1.1 billion, roughly the amount of its original equity investment in the 2007 buyout. Its remaining 26.7 million CDW shares were worth $910.7 million. The combined value represented a gain of approximately 83 percent—not spectacular by private equity standards, but remarkable given the timing of the original investment.

Providence Equity followed a similar playbook, gradually selling down its position as the stock appreciated. By 2015, both private equity firms had fully exited, having turned what looked like a catastrophic investment into a modest success. But more importantly for CDW, the company emerged from private equity ownership with a clear strategic direction: become the trusted technology advisor for mid-market and enterprise customers navigating digital transformation.

The post-IPO performance demonstrated the durability of CDW's model. Revenue grew from $10.8 billion in 2013 to $13.0 billion in 2015. The company expanded internationally, acquiring Kelway in the UK for strategic entry into European markets. CDW ranked #253 on the Fortune 500, employed nearly 1,400 technology specialists and engineers, and had transformed from a product distributor into a solutions provider. The foundation was set for the next phase of growth.

VII. The Modern Transformation: From Products to Solutions (2013–Present)

Christine Leahy stood before CDW's sales team in early 2019 with a provocative question: "What business are we really in?" The answer used to be simple—selling computers and software. But as Leahy, who had joined as Chief Revenue Officer in 2017 and would become CEO in 2019, surveyed the technology landscape, she saw a fundamental shift. Customers didn't want to buy products; they wanted to buy outcomes. They didn't need vendors; they needed partners who could help them navigate cloud migration, cybersecurity threats, and digital transformation. CDW's future, Leahy argued, wasn't in moving boxes but in solving complex technology challenges. The international expansion through Kelway marked CDW's first major move beyond North America. On 3 August 2015 the company announced that it had acquired the remaining 65% of Kelway Ltd., a London based multinational business with significant presence in the IT sector. Eight months earlier, CDW had bought a 35 percent stake in Kelway. The total investment of approximately $510 million gave CDW instant access to 4,500 UK customers and established supply chain relationships in over 100 countries. But more importantly, it provided a blueprint for international expansion without the risks of greenfield operations.

The real transformation, however, was happening in CDW's service offerings. Cloud adoption was accelerating, and CDW positioned itself as the trusted advisor helping companies navigate the complexity. Rather than viewing cloud providers like AWS and Microsoft Azure as threats, CDW became their channel partner, helping enterprises architect hybrid solutions that combined on-premise infrastructure with cloud services. By 2018, CDW was generating over $3 billion in cloud-related sales—not just reselling licenses, but providing migration services, security assessments, and ongoing management.

The numbers validated the strategy. Services and solutions grew from 15% of gross profit in 2013 to over 25% by 2020. These weren't just higher-margin revenues; they were stickier. A customer buying hardware might switch vendors for a 2% discount. A customer relying on CDW to manage their Azure environment and secure their cloud infrastructure was essentially locked in. The lifetime value of these relationships was multiples higher than traditional product sales.

Digital transformation became CDW's rallying cry, but it wasn't just marketing speak. The company invested heavily in building specialized practices around emerging technologies. They hired former CIOs and CTOs as solution architects. They developed deep expertise in vertical markets—healthcare providers navigating HIPAA compliance, school districts implementing one-to-one device programs, government agencies modernizing legacy systems. This wasn't the CDW of the 1990s selling computers from a catalog; this was a strategic technology partner embedded in customers' digital transformation journeys. The modern CDW has fully embraced the AI revolution, but not in the way you might expect. Rather than just reselling AI tools, CDW has become an AI implementation partner. When CDW embarked on an ambitious digital transformation in 2020, AI was a cornerstone of the company's strategy. CDW adopted a three-pronged approach: integrating off-the-shelf capabilities, developing custom solutions for specific workflows, and creating in-house tools and customer experiences using deep learning and large language models. With the rise of generative AI in 2023, CDW expanded its efforts by identifying new use cases, establishing policies and procedures to ensure coworkers use AI responsibly, and helping coworkers increase their AI fluency.

The internal AI adoption reveals CDW's strategy: become the expert first, then help customers navigate the same journey. CDW has achieved significant success with HAROLD, an IT support chatbot launched in 2021. Housed in Microsoft Teams, the bot resolved more than 42,000 issues for nearly 13,000 coworkers in 2023—essentially managing 40% of support tickets. This isn't just efficiency improvement; it's proof-of-concept that CDW can deliver for enterprise customers.

Cybersecurity has become CDW's fastest-growing practice area, and the numbers tell the story. CDW surveyed more than 950 IT and security professionals from across industries in the U.S. to understand key issues: What stresses them out about cybersecurity? What tools do they rely on to provide a clear picture of their cybersecurity landscape? The research isn't just market intelligence—it positions CDW as a thought leader helping customers navigate an increasingly complex threat landscape.

CDW helps customers navigate the complexities of an increasingly digital world, addressing challenges such as AI (artificial intelligence), cloud security, data storage, and cybersecurity. This isn't the language of a box-mover; it's the positioning of a strategic technology partner. The transformation from products to solutions is complete, setting the stage for CDW's biggest bet yet.

VIII. The Sirius Acquisition: Doubling Down on Services (2021)

October 18, 2021. CDW announced its largest acquisition ever: $2.5 billion in cash for Sirius Computer Solutions, a leading managed services provider. The price tag raised eyebrows—it represented nearly 15% of CDW's market cap at the time. But for CEO Christine Leahy and her team, this wasn't just an acquisition; it was a declaration of intent. CDW was going all-in on services transformation, and Sirius was the accelerator. Founded in 1980, Sirius is a leading provider of secure, mission-critical technology-based solutions for approximately 3,900 large and mid-sized customers. One of the largest IT solutions integrators in the United States, Sirius generated 2020 net sales of $2.04 billion. With over 2,600 employees, multiple offices across the U.S., and a team of experts with more than 5,500 professional and technical certifications, the Sirius team specializes in Digital Infrastructure, Security, Cloud, Managed Services, and Business Innovation (Digital and Data).

The strategic rationale was compelling. The transaction is expected to accelerate and enhance CDW's services and solutions capabilities in key growth areas, including Hybrid Infrastructure, Security, Digital and Data Innovation, and Cloud and Managed Services. Combining with Sirius would expand CDW's services portfolio by about 45%, from about $900 million in annual net sales in 2020 to about $1.3 billion in combined annual net sales. This wasn't just buying revenue; it was acquiring capabilities that would take years to build organically.

But the real genius was in the customer synergies. Sirius brought 3,900 enterprise customers, most of whom weren't CDW customers. These were complex, large organizations requiring sophisticated IT services—exactly the market CDW wanted to penetrate. Meanwhile, CDW could cross-sell Sirius's advanced services to its 250,000 customers. The revenue synergy potential was enormous.

The integration strategy was deliberate and careful. Rather than immediately merging operations, CDW maintained Sirius as a distinct brand and operating unit. Joe Mertens, Sirius's CEO, stayed on to lead the division. The Sirius team kept their offices, their processes, and most importantly, their customer relationships. This wasn't a typical acquisition where the buyer guts the target; CDW understood that Sirius's value was in its people and expertise.

The financial impact was immediate and significant. The acquisition delivered gross margin expansion, as services carry higher margins than product sales. CDW's gross margin expanded from 20.5% to 21.8% within a year of the acquisition. More importantly, the services mix increased CDW's recurring revenue streams. Managed services contracts typically run 3-5 years with high renewal rates, providing predictable, high-margin revenue that investors value at premium multiples.

The market reaction was initially skeptical—CDW's stock fell 5% on the announcement as investors worried about integration risk and the debt load. But as the synergies materialized, sentiment shifted. By 2023, the Sirius acquisition was being hailed as transformative, having successfully repositioned CDW from a products distributor to a comprehensive IT services provider.

IX. Business Model Evolution & Competitive Positioning

The evolution of CDW's business model reads like a masterclass in strategic transformation. Stage One (1984-1995): Direct sales of commodity hardware with superior customer service. Stage Two (1995-2010): Multi-channel distribution across specialized segments with basic configuration services. Stage Three (2010-present): Comprehensive IT solutions provider delivering outcomes across the technology stack. Each transition required cannibalizing the previous model while maintaining the core that made CDW successful—obsessive customer focus.

The numbers tell the transformation story. In 1995, hardware sales represented 85% of revenue and 70% of gross profit. By 2023, the mix had completely shifted: hardware was just 55% of revenue but only 35% of gross profit. Software, cloud subscriptions, and services now drive the majority of economic value. This isn't just mix shift; it's a fundamental reimagining of what CDW sells. They're no longer selling products; they're selling business outcomes enabled by technology.

The customer segmentation strategy has become increasingly sophisticated. Corporate (serving commercial customers) generates roughly 35% of revenue. Small Business contributes 10%. But the real growth engine is Public segment, serving government, education, and healthcare, which represents 35% of revenue but growing at double-digit rates. CDW operates a specialized division, CDW-G, which focuses exclusively on providing IT solutions to U.S. governmental entities, including K-12 schools, universities, non-profit healthcare organizations, and local, state, and federal governments. Each segment has distinct needs, buying patterns, and margin profiles, allowing CDW to optimize its approach.

The vendor ecosystem represents both CDW's greatest strength and potential vulnerability. CDW maintains relationships with over 1,000 technology vendors, from giants like Microsoft and Cisco to emerging cloud and security startups. These aren't just transactional relationships; CDW often gets preferential pricing, early access to products, and co-marketing support. But concentration risk is real: Microsoft, Cisco, Dell, and HP combined represent over 50% of purchases. Any disruption in these relationships could be catastrophic. The competitive landscape reveals both CDW's strengths and vulnerabilities. CDW's main competitors include Insight Enterprises, SHI International, Softchoice, and Connection in the VAR (Value Added Reseller) space. But increasingly, CDW faces competition from multiple directions: systems integrators like Accenture and Deloitte moving downstream into mid-market; cloud providers like AWS and Microsoft selling directly to enterprises; and emerging digital-native distributors disrupting traditional models.

CDW's competitive advantages are substantial but not impregnable. Scale matters enormously in distribution—CDW's $21 billion in revenue provides purchasing power that smaller competitors can't match. The company's 250,000 customers create network effects: more customers attract more vendors, which attracts more solutions, which attracts more customers. The specialized expertise in government and education markets creates barriers to entry—you can't just decide to sell to the federal government; it requires years of certifications and relationship building.

But the disintermediation threat is real and growing. Cloud providers increasingly sell directly to enterprises, cutting out the middleman. Software vendors are moving to subscription models that reduce the need for resellers. Hardware margins continue to compress as products commoditize. CDW's response has been to move up the value chain into services where disintermediation is harder—you can't download consulting expertise or managed services from a website.

The financial model has evolved to reflect this transformation. Working capital management remains critical—CDW essentially operates on negative working capital, collecting from customers before paying vendors. But the mix shift to services has changed the dynamics. Services require upfront investment in people and capabilities before revenue materializes. The payoff is higher margins and more predictable revenue streams, but the transition requires careful execution.

Capital allocation has become increasingly sophisticated. CDW generates over $1 billion in free cash flow annually. The priorities are clear: first, invest in organic growth through hiring and capability building; second, pursue strategic acquisitions that accelerate transformation; third, return excess capital through dividends and buybacks. The company has increased its dividend every year since returning to public markets in 2013, demonstrating confidence in the model's durability.

X. Playbook: Business & Investing Lessons

The CDW story offers a masterclass in building competitive advantages in a commoditized industry. Lesson One: Customer service can be a sustainable moat, but only if you're willing to invest relentlessly. CDW's "Circle of Service" isn't just marketing—it's embedded in compensation structures, training programs, and operational metrics. When your average salesperson earns over $100,000 and stays with the company for years, they develop relationships that Amazon can't replicate with algorithms.

The power of direct sales in the B2B market remains underappreciated. While consumer markets have largely moved online, B2B technology sales still rely heavily on human interaction. Why? Because businesses aren't buying products; they're buying solutions to problems, and problems require diagnosis. CDW's 6,500 salespeople aren't order-takers; they're technology advisors who understand their customers' businesses. This consultative approach creates switching costs that pure e-commerce players can't overcome.

Building through both organic growth and M&A requires different muscles, and CDW has developed both. Organic growth comes from hiring, training, and retaining talent. M&A requires identifying targets, negotiating deals, and—most critically—integrating without destroying value. The Sirius acquisition demonstrates mastery: maintain the brand, keep the leadership, preserve the culture, but integrate the back-office for synergies. Too many acquirers try to swallow companies whole and end up with indigestion.

Navigating technology transitions requires cannibalization courage. When cloud computing emerged, CDW could have fought it to protect hardware sales. Instead, they embraced it, becoming one of the largest cloud solution providers despite lower unit margins. When AI emerged, they didn't just resell AI tools; they built internal capabilities first, then helped customers on the same journey. Each transition requires letting go of yesterday's business model to grab tomorrow's opportunity.

The private equity lessons are sobering but instructive. Madison Dearborn and Providence bought at exactly the wrong time—peak market, peak leverage, just before a historic crash. But they didn't panic. They brought in operational talent, cut costs without cutting muscle, and invested in capabilities during the downturn. The lesson: timing matters enormously in leveraged buyouts, but operational excellence can salvage even poorly timed deals. Sometimes not losing money is its own victory.

Scale advantages in IT distribution compound over time. Larger players get better pricing from vendors, can afford broader inventory, and spread fixed costs over more revenue. But scale without service is vulnerability—customers will switch for 2% savings unless you give them reasons to stay. CDW's genius is using scale to fund service, creating a virtuous cycle that's hard for competitors to break.

The services transformation playbook is increasingly relevant across industries. Start with products, add basic services, then gradually move toward solutions and managed services. But the transition requires patience—services have longer sales cycles, require different talent, and need sustained investment before profitability. CDW spent a decade building services capabilities before they became material to financial results. Most companies lack this patience, creating opportunity for those who do.

XI. Analysis & Bear vs. Bull Case

The Bull Case: CDW sits at the intersection of several powerful secular trends. Digital transformation isn't slowing—if anything, AI is accelerating it. Every company needs help navigating cloud migration, cybersecurity, and now AI implementation. CDW's positioned perfectly: relationships with 250,000 customers who trust them, expertise across the technology stack, and vendor partnerships that provide access to innovation. The services transformation is working—margins are expanding, recurring revenue is growing, and customer lifetime values are increasing.

The market opportunity remains enormous. IT spending in the U.S. alone exceeds $1 trillion annually, and CDW has less than 2% market share. The fragmented competitive landscape—thousands of small VARs and consultants—provides endless acquisition opportunities. International expansion is still early innings; CDW generates less than 10% of revenue outside North America versus 40%+ for true global players. There's runway for decades of growth.

The financial model is increasingly attractive. CDW generates 15%+ returns on invested capital, well above its cost of capital. Free cash flow conversion exceeds 100% of net income. The balance sheet is conservative with net leverage under 3x. This isn't a story that requires multiple expansion; even at current valuations, high-single-digit revenue growth plus margin expansion plus capital returns could generate low-teens total returns.

The Bear Case: The disintermediation threat is existential and accelerating. Cloud providers are getting more aggressive about direct sales. Software vendors are moving to direct subscription models. Even hardware vendors like Dell and HP are investing in direct channels. CDW's role as middleman becomes less relevant every year. Why would a sophisticated enterprise need CDW to implement Microsoft Azure when Microsoft has its own professional services?

Vendor concentration creates massive risk. If Microsoft or Cisco changed their channel strategy, CDW's economics would implode overnight. These vendors hold all the cards—they control pricing, terms, and whether CDW gets access to products at all. CDW is essentially a commissioned salesperson for Big Tech, and commissions always face pressure over time.

The economics of the services transformation may not work long-term. Services require people, and people are expensive. CDW's competing against Indian outsourcers who can provide similar services at 30% lower cost. The company's also competing against hyperscalers who can afford to lose money on services to lock in cloud consumption. CDW's stuck in the middle—too expensive to win on price, not specialized enough to win on expertise.

Margin pressure seems inevitable. Hardware margins have compressed for decades and won't stop. Software is moving to consumption models with lower upfront margins. Services face wage inflation and competition from lower-cost providers. Meanwhile, CDW's cost structure is largely fixed—distribution centers, sales force, corporate overhead. Operating leverage works both ways, and a revenue decline would devastate profitability.

Economic sensitivity remains high despite diversification efforts. IT spending is notoriously cyclical—it's the first budget cut in downturns and last to recover. CDW's government exposure provides some stability, but even government spending faces pressure. The company barely survived 2008-2009; another severe recession could be catastrophic given current debt levels.

The valuation leaves little room for error. At 20x forward earnings, CDW trades at a premium to the S&P 500 despite being in a mature, cyclical industry. The market's pricing in successful services transformation, continued market share gains, and no major disruption. Any disappointment—a vendor conflict, integration issues, or economic slowdown—could trigger significant multiple compression.

XII. Epilogue & "If We Were CEOs"

If we were running CDW, the strategic priorities would be clear but execution would be complex. First, accelerate the AI services build-out. The company that becomes the trusted AI implementation partner for the Fortune 5000 will dominate the next decade. CDW has the customer relationships and trust; they need to rapidly build expertise. Acquire an AI consultancy, hire data scientists, develop proprietary frameworks for AI implementation. Be the company that helps enterprises separate AI hype from reality.

International expansion needs to shift from opportunistic to strategic. The UK acquisition through Kelway was smart, but CDW needs presence in high-growth markets. Asia-Pacific represents 40% of global IT spending but less than 1% of CDW revenue. Build or buy capabilities in Singapore, Sydney, Tokyo. The playbook is proven; CDW just needs to execute it globally.

Vertical specialization should deepen dramatically. Healthcare, financial services, and manufacturing have unique technology needs and regulatory requirements. Build practices with deep domain expertise—hire former CIOs from these industries, develop vertical-specific solutions, become indispensable to these sectors. Generalists will lose to specialists as technology becomes more complex.

The managed services opportunity is undertapped. CDW should manage entire IT environments for mid-market companies that can't afford full IT departments. This is sticky, high-margin, recurring revenue. Build Security Operations Centers, Network Operations Centers, cloud management capabilities. Become the outsourced CIO for the Fortune 5000's suppliers and partners.

Strategic vendor relationships need restructuring. CDW's too dependent on a handful of vendors who could disintermediate them tomorrow. Develop proprietary solutions that vendors need. Build direct relationships with emerging vendors before they get big. Create switching costs for vendors—make CDW's channel so valuable that vendors can't afford to go direct.

The capital allocation strategy should embrace programmatic M&A. Acquire 3-5 smaller specialized solutions providers annually. Focus on capabilities, not revenue—buy expertise in emerging technologies, vertical solutions, and geographic presence. Keep acquisitions small enough to integrate easily but frequent enough to continuously add capabilities.

Most importantly, preserve the cultural core while evolving the business model. CDW's customer obsession created the company; losing it while chasing margins would be fatal. The challenge is maintaining high-touch service while building scalable solutions. Technology can enhance human connection, not replace it. The companies that figure this out will dominate the next generation of B2B services.

The CDW story ultimately demonstrates that competitive advantages in business are rarely about unique products or proprietary technology. They're about execution, culture, and the compound effect of thousands of small decisions made correctly over decades. Michael Krasny's $3 newspaper ad didn't launch a tech giant; it revealed a customer need that CDW has spent 40 years learning to serve better than anyone else.

For investors, CDW represents a fascinating study in transformation. This isn't a sexy SaaS company with 80% gross margins and viral growth. It's a distribution business that's methodically climbed the value chain, survived existential threats, and emerged stronger from each challenge. Whether that journey continues successfully depends on CDW's ability to navigate the next transformation: from selling technology to delivering intelligence in an AI-powered world.

The questions facing CDW today—How do you stay relevant when vendors can go direct? How do you build services capabilities while maintaining capital efficiency? How do you serve global enterprises while keeping the personal touch that built your business?—are the same questions facing every traditional business in the digital age. CDW's answers, whether successful or not, will provide lessons for a generation of companies attempting similar transformations.

In the end, CDW's story is distinctly American: immigrant entrepreneur sees opportunity, builds business through relentless execution, creates thousands of jobs, and generates billions in value. It's also a cautionary tale about the perils of leverage, the challenges of transformation, and the constant threat of disruption. But most of all, it's an ongoing experiment in whether a company built on human relationships can thrive in an increasingly automated world. That experiment is far from over.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube