Berkshire Hathaway: The Empire Warren Built

I. Introduction & Episode Roadmap

On the morning of February 28, 2026, Greg Abel released his first shareholder letter as CEO of Berkshire Hathaway. It was a quiet, workmanlike document — focused on capital discipline, risk management, and cultural continuity. There were no fireworks, no grand proclamations, and no departures from the playbook. That, in itself, told the entire story.

Because Berkshire Hathaway is not a company built on spectacle. It is a company built on compounding — the patient, relentless accumulation of value over six decades that turned a failing New England textile mill into a trillion-dollar empire. As of today, Berkshire Hathaway commands a market capitalization north of $1.07 trillion, making it the eleventh most valuable company on the planet. Its stock portfolio alone holds roughly $300 billion in publicly traded equities. Its cash pile sits at $373 billion — a sum larger than the GDP of most nations. And its collection of wholly owned subsidiaries spans railroads, utilities, insurance, manufacturing, retail, and real estate, employing hundreds of thousands of people across dozens of industries.

The central question of this story is deceptively simple: how did an angry stock purchase in a dying textile company become the greatest wealth-creation machine in the history of capital markets?

The numbers are almost absurd. From 1965 through 2024, Berkshire Hathaway's per-share market value compounded at roughly 19.8% annually, compared to 10.2% for the S&P 500 including dividends. A single dollar invested in Berkshire at the start of that period grew to over $43,000. The same dollar in the S&P would have become about $390. Berkshire's book value per share compounded at approximately 18.3% annually over the same span. These are not returns from a brief hot streak or a single brilliant trade — they represent six decades of sustained, disciplined capital allocation that defies almost every academic model of market efficiency.

But this is not merely a story about returns. It is a story about the evolution of an investment philosophy — from Benjamin Graham's cigar-butt deep value to Charlie Munger's quality-at-a-fair-price revolution. It is a story about the power of insurance float as a funding mechanism, about decentralized management as a competitive moat, and about the extraordinary difficulty of deploying capital at scale. It is a story about two men — Warren Buffett and Charlie Munger — whose intellectual partnership reshaped how the world thinks about investing, business ownership, and the relationship between the two. And now, in 2026, it is a story about what happens when the architect steps back and the building must stand on its own.

This story unfolds across three distinct eras: the accidental origin, the golden age of compounding, and the uncertain transition to a post-Buffett world. Along the way, we will examine how insurance float became the most ingenious funding mechanism in financial history, why a twenty-seven-person headquarters can oversee a trillion-dollar enterprise, and what the $373 billion cash pile tells us about both the genius and the limitations of Berkshire's model.

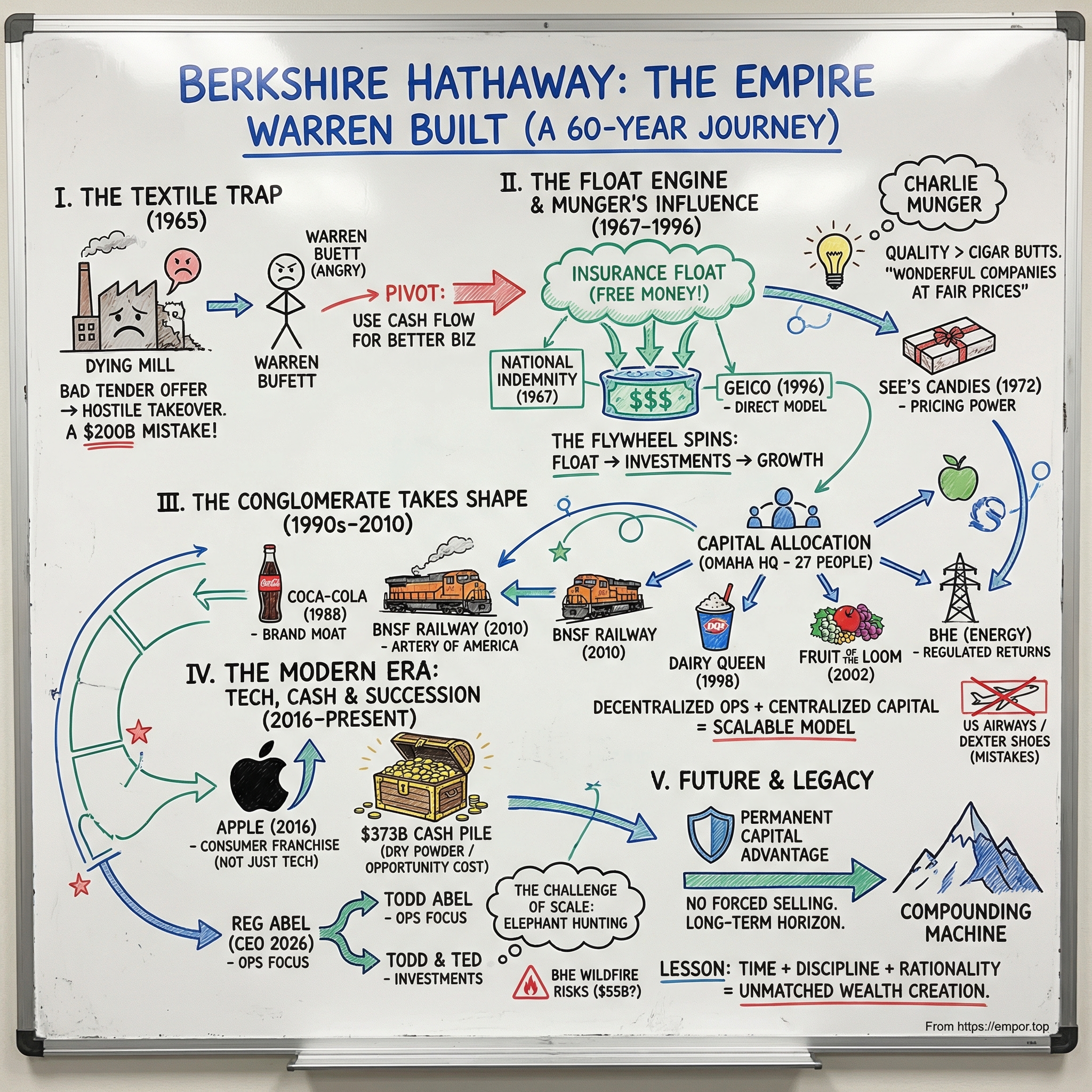

To understand Berkshire Hathaway, we need to start where all great origin stories begin: with a mistake.

II. The Textile Trap: Origins & Early Years (1839-1965)

The story of Berkshire Hathaway begins not in Omaha but in the mill towns of Massachusetts and Rhode Island, where the industrial revolution first took root in America. In 1839, a company called Valley Falls was incorporated in Rhode Island to manufacture cotton textiles. Across the border in Massachusetts, the Hathaway Manufacturing Company was established in 1888 in New Bedford — a whaling port that had pivoted to textiles as the whale oil industry collapsed. For decades, these companies thrived in an era when New England was the undisputed center of American textile production.

But by the mid-twentieth century, the economics had shifted decisively. Southern states offered cheaper labor, lower taxes, and newer facilities. Foreign competition from Asia was intensifying. The great New England textile migration was underway, and firms that had operated profitably for a century found themselves in a death spiral. In 1955, Berkshire Fine Spinning Associates — a successor to Valley Falls — merged with Hathaway Manufacturing to form Berkshire Hathaway. The logic was straightforward: combine two struggling operations to achieve scale economies and survive the industry downturn. It did not work.

By the late 1950s, the merged company had already lost seven of its fifteen plants. Revenues were declining, margins were evaporating, and the stock price reflected the market's judgment that this was a business in terminal decline. The company was burning through its working capital — selling off assets just to fund operations, a classic sign of a business that is slowly liquidating itself.

Enter Warren Buffett. In the early 1960s, Buffett's partnership began quietly accumulating Berkshire Hathaway shares. The stock was trading around $8 per share, while the company's working capital alone was roughly $19 per share. This was the classic Benjamin Graham playbook: buy a business for less than its liquidation value, wait for the market to recognize the discrepancy, and profit from the reversion. Buffett was not buying Berkshire because he loved textiles. He was buying it because the numbers said it was cheap.

What happened next became one of the most famous anecdotes in financial history. Seabury Stanton, Berkshire's president, approached Buffett and offered to buy back his shares in a tender offer. They agreed verbally on a price of $11.50 per share — a modest profit on Buffett's cost basis, and a clean exit from a declining business. When the formal written offer arrived, however, the price was $11.375 — an eighth of a dollar less than what Buffett believed had been promised.

For most investors, twelve and a half cents per share would be a rounding error. For Warren Buffett, it was an act of bad faith. He was furious — not about the money, but about the principle. Rather than tendering his shares, he bought more. He acquired enough stock to take control of the company, removed Stanton, and installed himself as chairman. An investment that was supposed to be a quick, dispassionate arbitrage had become a hostile takeover driven by wounded pride. It was, by Buffett's own later admission, one of the worst decisions of his career — not because it failed, but because it succeeded in the wrong way.

Buffett has called this his "$200 billion mistake." Not because the company failed — obviously it did not — but because the act of buying a textile business consumed years of capital and attention that could have been deployed directly into insurance and other high-return businesses from the start. As Buffett told shareholders decades later, if he had simply invested in insurance companies directly instead of routing everything through a textile shell, the compounding math suggests Berkshire would be worth roughly $200 billion more than it was. The anger-driven acquisition of a dying textile mill was, by Buffett's own reckoning, one of the most expensive fits of pique in business history.

But the genius of what followed was recognizing the mistake early and pivoting decisively. Buffett did not try to revive the textile business. He did not invest in new looms or modern facilities. He did not attempt a turnaround strategy with new products or new markets. Instead, he used Berkshire's corporate structure and remaining cash flows as a platform — a vessel through which he could deploy capital into better businesses.

The textile operations limped along through the 1970s and early 1980s, generating modest cash that Buffett systematically redirected into insurance, stocks, and other acquisitions. The contrast was striking: the textile division was earning anemic returns on capital while Berkshire's investment portfolio and insurance subsidiaries were compounding at rates that would have seemed fantastical to Stanton and the old textile hands. Every year the gap widened, and every year the textile operations became a smaller and more irrelevant part of what Berkshire was becoming.

When the economics became truly untenable — foreign competition had driven margins to zero, and the capital expenditure required just to maintain operations exceeded the returns the business could generate — Buffett shut down the last textile operations in 1985, ending 146 years of manufacturing history. He donated the looms and machinery; they had essentially no resale value. By that point, Berkshire Hathaway was already something entirely different. The caterpillar had become a butterfly, and the cocoon was made of insurance float.

III. The Oracle's Foundation: Buffett's Early Years (1930-1965)

To understand why Berkshire Hathaway became what it became, you have to understand the mind that built it. Warren Edward Buffett was born on August 30, 1930, in Omaha, Nebraska — the second of three children of Howard Buffett, a stockbroker who would later serve four terms in the United States Congress. The family was comfortable but not wealthy, and politics and markets were discussed at the dinner table with equal intensity. Howard Buffett was an ardent fiscal conservative who worried about government spending and monetary policy — concerns that would echo in his son's later thinking about inflation, debt, and the long-term value of productive assets.

Warren showed entrepreneurial instincts almost before he could ride a bicycle. At age six, he bought six-packs of Coca-Cola from his grandfather's grocery store for twenty-five cents and sold individual bottles door-to-door for a nickel each — a 20% margin on a consumer staple. By eleven, he purchased his first stock: three shares of Cities Service Preferred at $38 per share. The stock dropped to $27, and the young Buffett held on until it recovered to $40, at which point he sold for a small profit. It subsequently rose to $200. The experience taught him two lessons he would carry forever: the emotional difficulty of holding through drawdowns, and the enormous cost of selling too early.

By sixteen, Buffett had accumulated a portfolio worth $53,000 — the equivalent of roughly half a million dollars today. He had run a paper route, sold golf balls, operated pinball machines in barbershops, and owned a small farm. He was not playing at business; he was practicing it with the intensity of a young musician training for Carnegie Hall.

Buffett enrolled at the Wharton School at the University of Pennsylvania but found the coursework insufficiently practical. He transferred to the University of Nebraska, where he completed his undergraduate degree, and then applied to Harvard Business School, which famously rejected him. It was the best thing that ever happened to him. Turned away from Cambridge, Buffett discovered that Benjamin Graham — the father of value investing and author of "Security Analysis" and "The Intelligent Investor" — was teaching at Columbia Business School. Buffett enrolled immediately.

Graham's framework was revelatory. The core idea was elegantly simple: stocks are not lottery tickets or abstract symbols; they are fractional ownership stakes in real businesses. The job of an investor is to determine what a business is worth — based on its assets, earnings, and cash flows — and then buy shares only when they trade at a significant discount to that intrinsic value. Graham called this gap the "margin of safety," and it became the foundational concept of Buffett's investment philosophy. Graham also introduced the allegory of Mr. Market — an imaginary business partner who shows up every day offering to buy your shares or sell you his, often at irrational prices driven by emotion rather than fundamentals. The investor's job was not to follow Mr. Market but to exploit him.

After graduating from Columbia, Buffett worked for Graham's investment firm in New York for two years before returning to Omaha in 1956. He was twenty-five years old, had accumulated $174,000 in personal savings, and decided to start his own investment partnership. The initial structure was modest: seven investors contributed $105,000, and Buffett put in $100. His compensation was 25% of profits above a 6% annual hurdle rate, with no management fee. If he did not beat 6%, he did not get paid. This alignment of incentives — "eat what you kill" — would become a hallmark of everything he built.

The Buffett Partnership generated returns that bordered on the impossible. Over thirteen years, from 1957 to 1969, the partnership compounded at 29.5% annually before fees, compared to 7.4% for the Dow Jones Industrial Average. In no single year did the partnership lose money. Not one. In a business where even the greatest managers routinely experience down years, Buffett delivered positive returns in every single calendar year across more than a decade of investing.

The strategies were varied and creative. Buffett engaged in what he called "workouts" — merger arbitrage situations where one company was acquiring another, and the partnership could buy the target at a discount to the announced deal price. He bought controlling stakes in small companies and unlocked value through operational improvements or asset sales. He made significant positions in undervalued blue chips. And he occasionally found "generals" — broadly diversified positions in cheap stocks that required nothing more than patience for the market to recognize their value. The common thread was not a single strategy but a single discipline: never pay more for an asset than it is worth, and always demand a margin of safety between price and value.

By the time Buffett dissolved the partnership in 1969 — convinced that the go-go market of the late 1960s had eliminated the kind of bargains he required — his personal net worth had grown to approximately $25 million. He returned his partners' capital, recommended they invest with a young money manager named Bill Ruane (who would go on to run the legendary Sequoia Fund), and effectively retired from money management at the age of thirty-nine. Of course, he did not actually retire. He pivoted to running Berkshire Hathaway, transforming himself from a money manager into a business owner — a transition that would prove far more consequential than anything he had done in the partnership era.

But the most consequential event of this period was not a trade. It was a dinner. In 1959, mutual friends introduced Buffett to Charlie Munger, a fellow Omaha native who had become a successful Los Angeles attorney. The two men talked for hours and discovered an immediate intellectual kinship. Munger was brilliant, acerbic, and widely read — a polymath who drew on psychology, physics, biology, and history to understand business and human behavior. Where Buffett was folksy and diplomatic, Munger was blunt and contrarian. Where Buffett had been trained in Graham's pure quantitative approach, Munger brought a qualitative lens that emphasized the character of management, the durability of competitive advantages, and the superiority of great businesses over merely cheap ones.

Munger's influence would gradually transform Buffett's investment philosophy from buying "cigar butts" — mediocre businesses with one last puff of value left — to buying "wonderful companies at fair prices." This was the intellectual leap that made Berkshire Hathaway possible. Without Munger, Buffett might have remained a spectacularly successful deep-value investor. With Munger, he became the greatest capital allocator in history.

As Buffett began building his stake in Berkshire Hathaway in the early 1960s, these two strands — the quantitative rigor of Graham and the qualitative wisdom of Munger — were already beginning to intertwine. The textile company was a Graham-style cigar butt. What Buffett would build inside it was pure Munger. The vehicle was about to become the vessel for a far more ambitious experiment in permanent capital allocation.

IV. The Insurance Revolution: Finding the Float (1967-1996)

In March 1967, Berkshire Hathaway paid $8.6 million to acquire National Indemnity Company, a small Omaha-based insurer specializing in unusual risks — things like taxi fleets, carnival rides, and other lines that larger insurers avoided. It was, by any conventional measure, a minor transaction. But it was the single most important acquisition in Berkshire's history, because it introduced Buffett to the concept that would fuel everything that followed: insurance float.

Float is one of those financial concepts that sounds technical but is actually beautifully simple. When an insurance company collects premiums from policyholders, it holds that money until claims come due — which could be months, years, or even decades later. During that holding period, the insurer can invest the funds. If the insurance operation breaks even on its underwriting — meaning premiums collected roughly equal claims paid plus operating expenses — then the float is essentially free money to invest. And if the insurance company actually earns an underwriting profit, as Berkshire's operations have done in most years, the float is better than free. It is money that someone pays you to hold.

Think of it this way: imagine you run a bank, but instead of paying depositors interest, they pay you. That is the economics of well-run insurance float. As of the end of 2025, Berkshire Hathaway's total insurance float stood at approximately $176 billion — up from under $20 million when National Indemnity was first acquired. This float has grown at a compounded rate that roughly matches Berkshire's overall growth, and it has been the primary funding source for the vast majority of Berkshire's investments and acquisitions over six decades.

The genius of Buffett's insight was recognizing that insurance was not merely a business to own — it was a financing mechanism. Most companies fund their investments with equity (expensive) or debt (risky). Buffett funded his with float — capital that had negative cost in good years and near-zero cost even in bad ones. This gave Berkshire a structural advantage that no hedge fund, private equity firm, or competing conglomerate could replicate.

The insurance empire grew steadily through the 1970s and 1980s. National Indemnity became the seed from which an entire forest grew. Berkshire added specialty lines, catastrophe reinsurance, and eventually large-scale property and casualty operations. Each acquisition brought more float, and each dollar of float was deployed into Buffett's growing portfolio of stocks and businesses.

The 1998 acquisition of General Re for roughly $22 billion was the largest insurance deal in Berkshire's history. General Re was one of the world's premier reinsurance franchises — a company that insured other insurance companies against catastrophic losses. The acquisition was troubled initially; General Re had underwriting discipline problems and a problematic derivatives book that took years to unwind. But once cleaned up, General Re added an enormous, stable pool of long-duration float that became a cornerstone of Berkshire's investment capacity. The crown jewel of the insurance portfolio, however — and one of the most important relationships in Buffett's career — was GEICO.

Buffett's connection to GEICO predated even the partnership era and reads like a scene from a movie. As a graduate student at Columbia in 1951, the twenty-year-old Buffett discovered that his mentor Benjamin Graham sat on the board of an insurance company called the Government Employees Insurance Company. On a Saturday morning, Buffett took a train to Washington, D.C., walked to GEICO's headquarters, and found the building locked. He banged on the door until a janitor let him in. Upstairs, he found Lorimer Davidson, a young financial vice president who happened to be working that weekend.

What was supposed to be a brief introduction turned into a four-hour tutorial on the insurance industry. Davidson explained GEICO's revolutionary model: selling auto insurance directly to consumers through the mail, completely bypassing the traditional network of independent agents who typically consumed fifteen to twenty cents of every premium dollar in commissions. By eliminating the middleman, GEICO could offer lower prices to customers while maintaining better margins than competitors. Lower prices attracted more careful drivers — government employees were the original target market, precisely because they tended to be responsible, low-risk policyholders. Fewer accidents meant fewer claims. Fewer claims meant even lower costs. It was a virtuous cycle that could compound indefinitely. Buffett walked out of that meeting knowing he had found something special.

He began buying GEICO stock in the 1970s when the company nearly went bankrupt due to reckless expansion and inadequate loss reserving. The stock had collapsed. Most investors ran. Buffett saw the near-death experience as an opportunity: the underlying business model — the structural cost advantage of direct distribution — was completely intact. The problem was management execution, not competitive position. By 1976, he had accumulated a significant stake at deeply discounted prices. Over the next two decades, he watched as GEICO was nursed back to health under new leadership and resumed its growth trajectory. In 1996, Berkshire acquired the remaining shares it did not already own for $2.3 billion, bringing GEICO fully into the fold. By 2024, GEICO generated $7.8 billion in pre-tax underwriting profit with a combined ratio of 81.5% — meaning for every dollar of premiums collected, GEICO paid out only about 82 cents in claims and expenses. The remaining 18 cents was pure profit, on top of the investment income generated by the float.

But the insurance revolution was not just about GEICO. It was about the philosophical transformation that occurred alongside it. In 1972, Berkshire acquired See's Candies — the legendary California chocolatier — for $25 million. See's was earning about $2 million a year in pre-tax profit at the time, and the price seemed steep by Graham's standards. Charlie Munger pushed Buffett to do the deal anyway, arguing that See's extraordinary brand loyalty, pricing power, and minimal capital requirements made it a business worth paying up for.

Munger was right. Over the next five decades, See's generated cumulative pre-tax earnings of over $2 billion on virtually no incremental capital investment. It was the deal that crystallized the Munger revolution in Buffett's thinking. Quality businesses that could grow earnings without requiring proportional capital reinvestment were infinitely superior to cheap businesses that demanded constant reinvestment just to tread water. The shift from "cigar butts to quality" was not instantaneous — it evolved over years of conversation and experience — but See's Candies was the proof point that made it real.

By the mid-1990s, Berkshire had assembled an insurance platform that generated billions in float, a portfolio of exceptional wholly owned businesses, and a publicly traded stock portfolio that included massive positions in companies like Coca-Cola, American Express, Gillette, and The Washington Post. Each of these investments embodied the Munger philosophy: businesses with extraordinary brand power, high returns on capital, and the ability to raise prices without losing customers. American Express had a network effect that made it more valuable as more merchants accepted it. Gillette had a razor-and-blade model that generated recurring revenue with minimal customer acquisition costs. The Washington Post dominated its local market with near-monopoly control of advertising.

The flywheel was spinning: insurance generated float, float funded investments, investments generated returns, returns attracted more float, and the cycle repeated. The question was no longer whether Berkshire could compound — it was how large the machine could grow before the laws of mathematics made further compounding impossible.

V. The Conglomerate Takes Shape: Major Acquisitions Era (1990s-2010)

The story of Berkshire's expansion from a $10 billion company in the late 1980s to a $200 billion enterprise by 2010 is really a story about one skill: capital allocation. Not operations. Not product innovation. Not marketing brilliance. Capital allocation — the art and science of deciding where to put money to generate the highest risk-adjusted returns over time. And the signature move of this era was Coca-Cola.

In 1988, Buffett began buying shares of The Coca-Cola Company. By 1989, he had accumulated roughly $1 billion worth of stock — about 7% of the company. Wall Street was puzzled. Coca-Cola was not cheap by any traditional value metric. The stock traded at a significant premium to book value and at earnings multiples that would have made Benjamin Graham uncomfortable. But Buffett saw something the quant-driven value crowd missed: the most powerful brand in the world, a global distribution network that was essentially impossible to replicate, and a business model that converted sugar water into rivers of cash with minimal capital requirements.

By 2025, that original billion-dollar investment had generated over $700 million per year in dividends alone — meaning Berkshire recovered its entire initial outlay roughly every eighteen months just from dividend payments. The total return, including unrealized appreciation, was astronomical. Berkshire still held all 400 million shares as of early 2026, and at no point in thirty-seven years had Buffett sold a single one. It was the purest expression of his "buy and hold forever" philosophy.

Coca-Cola taught Buffett — and the investing world — that paying a fair price for an extraordinary business was vastly superior to paying a bargain price for a mediocre one. It was the Munger thesis, proven at scale. The key insight was not about Coke's brand or its distribution — those were obvious to anyone. The insight was about reinvestment economics. Coca-Cola generated enormous returns on capital and could grow those returns by expanding internationally without proportional capital investment. The combination of high returns on existing capital and the ability to grow without consuming more capital is the holy grail of business economics — and Buffett recognized it more clearly than anyone.

The capital allocation machine that powered these investments was elegant in its simplicity. Insurance operations generated float. Float was invested in stocks and bonds. Wholly owned subsidiaries generated operating earnings. Those earnings, combined with investment income, provided capital for further acquisitions.

And crucially, Berkshire never paid a dividend — every dollar of earnings was retained and redeployed. This was not an oversight or a quirk; it was a deliberate strategic choice. Buffett's annual letter effectively served as his pitch to shareholders: trust me to allocate your capital better than you could allocate it yourselves, and in exchange, accept that you will never receive a dividend check. For sixty years, shareholders who accepted that bargain were handsomely rewarded.

The acquisition pace accelerated through the 1990s and 2000s, and the deals told a consistent story about what Buffett valued. Dairy Queen came in 1998 for approximately $585 million — a beloved, cash-generating brand with loyal customers and modest capital requirements. Fruit of the Loom was acquired out of bankruptcy in 2002 for about $835 million — a dominant brand that had been mismanaged and over-leveraged, but whose underlying market position remained strong. Shaw Industries, the world's largest carpet manufacturer, was purchased in 2001 for roughly $2 billion — a market leader in a fragmented industry with meaningful scale advantages. Nebraska Furniture Mart, Borsheims, the Buffalo News — each acquisition followed a recognizable pattern.

The common thread was unmistakable: simple, understandable businesses with durable competitive advantages, run by managers Buffett trusted and admired, purchased at prices that made mathematical sense given their earning power. And once acquired, the businesses were left alone. Buffett did not send in consultants, restructure management teams, or impose corporate synergies. He bought good businesses, kept good managers, and let them operate. The CEOs of Berkshire subsidiaries report directly to Omaha and have virtually complete operational autonomy — a freedom that is extraordinarily rare in corporate America and that serves as a powerful recruitment tool when Berkshire is competing with private equity firms to acquire family-owned businesses.

This decentralized management model was not an accident — it was a deliberate competitive strategy. By promising acquired companies operational autonomy, Berkshire became the buyer of choice for family-owned businesses and founder-led companies that did not want to sell to private equity firms or strategic acquirers who would slash costs, fire people, and strip the business for parts. Buffett offered something no one else could: permanent capital and permanent independence. The business would never be flipped, never be taken public, and never be subjected to the quarterly earnings treadmill. For many sellers, this was worth accepting a slightly lower price.

Not every deal worked, and the failures are as instructive as the successes. Buffett invested $358 million in US Airways preferred stock in 1989, attracted by what appeared to be a temporary distress discount on a business with strong brands and captive customers. The timing was disastrous. The airline industry entered one of its periodic death spirals — fare wars, overcapacity, fuel price spikes, and the first Gulf War combined to push multiple carriers into bankruptcy. US Airways' stock plummeted, and Buffett's preferred shares briefly traded at pennies on the dollar. He eventually recovered his capital plus some interest years later, but the experience reinforced his permanent aversion to airlines. "Investors have poured money into a bottomless pit," he later said of the industry, noting that the aggregate profits of every airline in history were negative.

Dexter Shoes, acquired in 1993, was arguably worse. Buffett paid $433 million for the Maine-based shoemaker — but he paid in Berkshire stock, not cash. The shoe business deteriorated rapidly as production shifted to Asia, and the company eventually became worthless. But the Berkshire shares Buffett used as currency went on to compound at extraordinary rates. By the time he tallied the damage years later, those shares would have been worth billions. He has called Dexter the worst deal he ever made, precisely because the currency of payment amplified the loss enormously. The lesson was searing: never pay for an uncertain asset with a certain one.

These failures, however, were dwarfed by the successes. And they reinforced a lesson Buffett emphasized repeatedly: in investing, you do not need to be right about everything. You need to be right about the big things and avoid catastrophic, unrecoverable errors. The batting average matters far less than the slugging percentage. A few grand slams — Coca-Cola, GEICO, See's Candies — can more than compensate for the occasional strikeout, as long as you never bet so much on a single idea that you cannot survive being wrong.

By 2010, Berkshire Hathaway had become something unprecedented in American business: a conglomerate that actually worked. While General Electric, Tyco, and other diversified companies were stumbling — and in some cases, spectacularly imploding — Berkshire kept compounding. The reason was structural. Most conglomerates destroyed value because they used the complexity of their operations to obscure poor capital allocation, rewarded executives for empire-building rather than returns on capital, and created bureaucratic overhead that suffocated individual business units. Berkshire did none of these things. Its corporate headquarters in Omaha employed approximately twenty-seven people. Its CEO made a salary of $100,000 per year. Its operating businesses ran themselves. The entire corporate overhead was a rounding error on a company generating tens of billions in annual earnings.

The conglomerate was taking shape — but its most transformative deals were yet to come.

VI. The Mega-Deal Era: BNSF & Beyond (2010-2016)

On a cold November morning in 2009, Warren Buffett announced the largest acquisition in Berkshire Hathaway's history: the purchase of Burlington Northern Santa Fe Railway for approximately $26.5 billion in cash and stock, plus the assumption of $10 billion in debt. The total enterprise value approached $44 billion. It was, at the time, one of the largest corporate acquisitions ever — and the first time Buffett had used Berkshire stock as part of a deal payment in decades, a signal of how badly he wanted BNSF and how rich the price was relative to his usual cash-only approach.

Buffett called it "an all-in wager on the economic future of the United States." It was the kind of statement that sounded like folksy Buffett wisdom but was actually a precise description of the investment thesis. If America continued to grow — if goods needed to move from coast to coast, if grain needed to reach ports, if consumer products needed to flow from factories to distribution centers — then BNSF would prosper. The bet was not on railroads per se but on the American economy, expressed through the most efficient overland freight transportation network ever built.

Railroads are the arteries of the American economy, and their economics are better than most people realize. They move roughly 40% of all intercity freight in the United States — coal, grain, consumer goods, industrial materials, and increasingly, intermodal containers that were previously the domain of long-haul trucking. A single train can move one ton of freight roughly 500 miles on a single gallon of diesel fuel — four times the efficiency of a truck. This fuel efficiency advantage is not a temporary technology gap; it is rooted in the fundamental physics of steel wheels on steel rails versus rubber tires on asphalt. As fuel costs rise and environmental regulations tighten, the economic advantage of rail only grows.

BNSF operates approximately 32,500 miles of track across twenty-eight states and two Canadian provinces, connecting the ports of the Pacific Coast with the industrial heartland and agricultural breadbasket. The network itself is essentially irreplaceable. No one is building new transcontinental railroads in the twenty-first century — the rights-of-way alone would cost many multiples of what Buffett paid, even if the regulatory and environmental approvals could be obtained, which they almost certainly could not. This is the purest form of barrier to entry: physical assets that cannot be replicated at any reasonable cost.

The acquisition fit Buffett's framework perfectly. Railroads have enormous barriers to entry — perhaps the highest of any industry outside of regulated utilities. They generate massive free cash flow once the infrastructure is built, though they require significant ongoing capital expenditure for maintenance and expansion. They benefit from the secular growth of the American economy. And they have pricing power that allows them to raise rates faster than inflation over long periods. The downside was that railroads are capital-intensive, cyclically exposed, and increasingly sensitive to shifts in energy markets — particularly the decline of coal, which had historically been the single most profitable commodity for rail transport.

BNSF's performance under Berkshire's ownership has been solid if unspectacular. In 2024, the railroad generated pre-tax earnings of $6.64 billion on revenue of $23.35 billion. Through the first nine months of 2025, pre-tax earnings rose to $5.3 billion, up modestly from the prior year. The railroad announced a $3.8 billion capital investment plan for 2025, focused on safety, efficiency, and capacity expansion. These are not the kinds of returns that make hedge fund managers salivate, but they are the durable, inflation-protected cash flows that a permanent capital vehicle like Berkshire prizes.

The energy business was another major area of expansion. Berkshire Hathaway Energy — originally MidAmerican Energy when Berkshire first invested in 2000 — has grown into one of the largest utility and renewable energy operators in the United States. BHE's portfolio includes PacifiCorp (serving six Western states), MidAmerican Energy (Iowa), NV Energy (Nevada), and significant renewable energy and natural gas pipeline operations. The thesis was similar to railroads: regulated, capital-intensive businesses with predictable cash flows, inflation-indexed revenues, and massive barriers to entry.

BHE invested heavily in renewable energy, becoming one of the largest wind and solar operators in North America. The regulated utility model provides stable returns because customers cannot easily switch providers and regulators allow utilities to earn a reasonable return on invested capital. But regulation is a double-edged sword: it protects incumbents from competition while also constraining their ability to raise prices, and it exposes utilities to political risk when things go wrong. BHE's earnings recovered strongly through 2025, posting $1.1 billion in the first quarter and $1.5 billion in the third quarter — a meaningful rebound from a difficult 2023.

However, BHE has also become the source of Berkshire's most significant unresolved financial risk. PacifiCorp, BHE's largest subsidiary, faces approximately $55 billion in total wildfire-related claims stemming primarily from the 2020 Labor Day fires in Oregon and subsequent events. The sheer scale of these claims dwarfs anything in PacifiCorp's financial capacity — the subsidiary's total assets are a fraction of the potential liability. Through early 2026, PacifiCorp had settled roughly $2.3 billion in claims, including a $575 million settlement with the U.S. government announced in February 2026. Additional bellwether trials and wrongful death cases are ongoing. Utah and Washington State have passed legislation to help manage wildfire liability for utilities, but the legal and financial uncertainty remains substantial.

Buffett acknowledged in his 2024 letter that BHE's results had "disappointed," a rare public admission of difficulty from a man known for accentuating the positive. The wildfire situation raises a fundamental question about the utility business model: can a regulated utility with capped upside survive in an era of uncapped downside from climate-related catastrophes? The answer to that question has implications not just for BHE but for the entire American utility sector.

The crown of the mega-deal era, however, was the 2016 acquisition of Precision Castparts for $37.2 billion — the largest single deal in Berkshire's history. Precision Castparts manufactured complex metal components for the aerospace, energy, and industrial markets. Its products — turbine blades, structural castings, fasteners — were embedded in virtually every commercial aircraft engine in production. The company had dominant market share, high switching costs, and long-term contracts with customers like Boeing, Airbus, General Electric, and Rolls-Royce. Certification requirements from the FAA meant that switching to an alternative supplier could take years — a moat that appeared nearly impenetrable.

The timing could not have been worse. The aerospace downturn triggered by the COVID-19 pandemic devastated demand for aircraft components, and Precision Castparts' earnings collapsed. In 2020, Berkshire took an approximately $10 billion write-down on the acquisition — one of the largest impairments in corporate history. Buffett was characteristically candid: "I paid too much for the company," he told shareholders. "No one misled me in any way — I was simply too optimistic about Precision Castparts' normalized earnings." It was a reminder that even the greatest investors are fallible, and that overpaying for a good business can produce mediocre returns just as surely as buying a bad business at any price.

The other major acquisition of this era unfolded in slow motion. Berkshire first invested in Pilot Travel Centers — the largest truck stop and travel center network in North America — in 2017, acquiring a 38.6% stake. The agreement called for Berkshire to purchase additional shares over time, eventually reaching full ownership. In early 2023, Berkshire acquired another 41.4%, and in January 2024, it purchased the final 20% from the Haslam family for $2.6 billion, completing the roughly $13.6 billion total investment. The final stage was preceded by litigation between Berkshire and the Haslam family over valuation — a rare acrimonious note in a company known for friendly, handshake-style deals.

By 2016, the challenge of scale had become Berkshire's defining strategic problem. With a market capitalization approaching $400 billion and growing, the company needed increasingly larger acquisitions to move the needle. Buffett described it as "elephant hunting" — the need to find deals of $5 billion, $10 billion, or even $20 billion or more just to meaningfully impact Berkshire's overall returns. The universe of potential targets at that scale was small, and the competition from private equity firms flush with cheap capital was intense. This tension — between the compounding machine's need for deployment and the shrinking opportunity set at Berkshire's size — would define the next era of the company's evolution.

VII. The Modern Berkshire: Tech, Cash, and Succession (2016-Present)

In early 2016, a line item appeared in Berkshire Hathaway's 13F filing that made Wall Street do a double take: a new position in Apple. The initial purchase, attributed to investment managers Todd Combs or Ted Weschler, was relatively modest — roughly $1 billion. But Buffett, who had famously avoided technology stocks for decades, saw something in Apple that transcended his traditional definition of "tech." He saw a consumer products company with an ecosystem so deeply embedded in its customers' daily lives that switching costs were effectively infinite. Apple was not a technology company in the way Buffett feared technology companies — dependent on rapid innovation cycles and vulnerable to disruption. It was a consumer franchise with the stickiest customer base in the world.

Buffett began buying aggressively. By the end of 2018, Berkshire had accumulated over 250 million split-adjusted shares, making Apple Berkshire's single largest equity holding by a wide margin. At its peak, the Apple position was worth over $170 billion — representing roughly 50% of Berkshire's entire public equity portfolio. It was the most concentrated bet Buffett had ever made, and it paid off spectacularly as Apple's stock price tripled and then quadrupled from Berkshire's average cost basis.

Then, starting in 2024, something shifted. Berkshire began systematically trimming its Apple stake — not in small increments, but in massive blocks that signaled a deliberate portfolio rebalancing rather than a loss of conviction. Through 2024 and 2025, Buffett sold roughly three-quarters of the position — reducing from over 900 million shares to approximately 228 million shares by the end of 2025. The selling was steady and disciplined: 20 million shares in the second quarter of 2025, 42 million in the third quarter, another 10 million in the fourth.

Even after this massive reduction, the remaining position was worth roughly $62 billion, still Berkshire's largest single equity holding at about 21% of the stock portfolio. Think about that for a moment: Buffett sold three-quarters of his Apple stake, and the remaining quarter was still the largest position in a $300 billion portfolio. That is the power of compounding applied to a great business over nearly a decade.

Buffett cited tax efficiency and valuation as factors, noting that Apple was trading at elevated multiples — roughly 34 times forward earnings — that offered less margin of safety than when he first purchased the stock at 10-12 times earnings. Some observers speculated that the selling was also designed to crystallize gains and simplify the portfolio ahead of the CEO transition, allowing Abel to inherit a more balanced portfolio rather than one dominated by a single position.

The Apple saga illustrated both Berkshire's extraordinary investment capability and its evolving challenge. The investment generated tens of billions in gains and demonstrated that Buffett's framework could adapt to modern businesses. But the trimming revealed a deeper tension: when your best investment becomes so large that it dominates your entire portfolio, risk management eventually requires you to sell, even if you still love the business. Concentration is the friend of wealth creation and the enemy of wealth preservation — and as Berkshire crossed the trillion-dollar threshold, preservation began to matter as much as creation.

The other defining feature of modern Berkshire has been its extraordinary accumulation of cash. By the third quarter of 2025, Berkshire's cash and equivalents peaked at $381.7 billion — a figure that included over $305 billion in short-term U.S. Treasury bills, making Berkshire a larger holder of T-bills than Switzerland. The cash pile settled to $373.3 billion by year-end 2025, still an almost incomprehensible sum. To put it in perspective, that cash position alone would make Berkshire approximately the thirtieth most valuable company on the S&P 500 if it were its own entity.

The cash accumulation reflected several realities. First, Berkshire's operating businesses and investment portfolio were generating cash far faster than Buffett could find attractive deployment opportunities.

Second, Buffett was unwilling to make acquisitions at prices he considered excessive. The combination of cheap debt, abundant private equity capital, and elevated asset valuations had pushed prices for quality businesses to levels he found unattractive. Private equity firms, armed with hundreds of billions in committed capital and willing to pay aggressive multiples, had driven deal prices to levels where even Berkshire's patient approach could not justify the math.

Third, there was a strategic logic to maintaining optionality. A $373 billion cash reserve meant that Berkshire could be the buyer of last resort in any future financial crisis, acquiring distressed assets at bargain prices just as it had done during the 2008-2009 financial crisis when it invested in Goldman Sachs, General Electric, and Bank of America on highly favorable terms.

Yet the cash pile also represented an implicit cost. Cash earns Treasury rates — roughly 4-5% in the current interest rate environment — while Berkshire's historical returns on invested capital have been far higher. Every dollar sitting in T-bills is a dollar not compounding at 15-20% in a productive business. As Berkshire grew larger, the opportunity cost of uninvested cash became increasingly significant. The math is unforgiving: $373 billion earning 4% generates about $15 billion per year, while the same capital deployed at Berkshire's historical 15% return would generate over $55 billion. That $40 billion gap is the annual cost of patience — an enormous number by any standard, even for a company of Berkshire's scale.

Meanwhile, Berkshire completed its acquisition of Alleghany Corporation in October 2022 for $11.6 billion in cash — the largest deal since Precision Castparts. Alleghany, a holding company primarily focused on reinsurance through its TransRe subsidiary, added approximately $14 billion in insurance float and strengthened Berkshire's already dominant position in the reinsurance market. The acquisition was classic late-Buffett: an insurance business with excellent underwriting discipline, a reasonable price, and a management team that shared Berkshire's culture. Joe Brandon, Alleghany's CEO, continued to lead the business after the acquisition — another example of Berkshire's hands-off approach to management.

Berkshire also paused its share buyback program entirely through 2025 — five consecutive quarters without a single repurchase. This was notable because buybacks had been a significant capital return mechanism in 2020 and 2021, when Buffett repurchased over $50 billion in Berkshire stock. The halt reflected Buffett's valuation discipline: Berkshire's stock was trading at a premium to its ten-year average price-to-sales ratio, and Buffett has always insisted that buybacks should only occur when shares trade at a meaningful discount to intrinsic value. The absence of buybacks, combined with the absence of major acquisitions, explained the relentless growth of the cash pile.

The succession question, which had lingered for decades, was decisively answered in 2025. At the annual shareholders meeting on May 3, 2025, Warren Buffett stunned the crowd by announcing his intention to step down as CEO by year-end. He proposed Greg Abel — the Vice Chairman of Non-Insurance Operations who had long been identified as the heir apparent — as his successor. The crowd gave a standing ovation. On September 30, 2025, Berkshire's board formally amended the bylaws to separate the Chairman and CEO roles for the first time in company history. Abel officially became CEO on January 1, 2026, with Buffett retaining the title of Chairman.

Abel's background is distinctly operational, and his path to the top of Berkshire is a story of quiet, relentless competence. Born in Edmonton, Alberta, Abel trained as an accountant and spent years at PricewaterhouseCoopers before moving into the energy business. He joined CalEnergy (later MidAmerican Energy, later Berkshire Hathaway Energy) in 1992 and rose through the ranks by mastering the complex intersection of utility regulation, capital investment, and operational execution. Colleagues describe him as a workaholic who knows the details of his businesses at a granular level — the kind of executive who can discuss transformer replacement schedules and generation dispatch curves with the same fluency that Buffett discusses price-to-earnings ratios.

He is not Buffett — nobody is — but his selection signaled that Berkshire's board valued operational competence and cultural continuity over investment brilliance. The distinction matters. Buffett's genius was primarily in capital allocation — deciding where to put money. Abel's strength is in operational management — making sure the money earns the returns it is supposed to. The investment portfolio would be managed by Todd Combs and Ted Weschler, each of whom already oversees roughly $20 billion in public equities. The capital allocation function — the most critical job at Berkshire — would be shared between Abel and the board, guided by the principles Buffett codified over six decades.

Recent portfolio moves suggest the transition is already underway. Berkshire initiated a new position in Alphabet in the third quarter of 2025, buying roughly $4.5 billion worth of Google's parent company — a clear signal that the investment team was comfortable moving into AI-adjacent technology. A new stake in the New York Times appeared in the fourth quarter of 2025, echoing Buffett's longstanding affinity for quality media properties. The Japanese trading house investments — positions in Itochu, Marubeni, Mitsubishi, Mitsui, and Sumitomo that collectively exceeded $30 billion by late 2025 — continued to expand, with several stakes crossing the 10% ownership threshold. And in October 2025, Berkshire announced the acquisition of OxyChem, Occidental Petroleum's petrochemical division, for $9.7 billion — described by Buffett as potentially his last major deal as CEO.

The first shareholder letter of the Abel era, released today, was characteristically modest. It focused on discipline, risk management, and the enduring importance of Berkshire's culture. The market barely blinked. And perhaps that was the highest compliment: the machine that Warren built appeared to be running just fine without his hand on the controls.

VIII. The Berkshire Operating System

To call Berkshire Hathaway a "conglomerate" is technically accurate and fundamentally misleading. Conglomerates — GE, ITT, Tyco, Honeywell — have historically destroyed value through bureaucratic overhead, empire-building acquisitions, and the concealment of poor capital allocation behind complex financial reporting. Berkshire has done the opposite. Understanding why requires looking beyond what Berkshire owns and examining how it operates — the organizational architecture that makes the whole vastly more valuable than the sum of its parts.

Start with the most astonishing organizational fact in all of corporate America: Berkshire Hathaway's corporate headquarters in Omaha employs approximately twenty-seven people to oversee a trillion-dollar enterprise with hundreds of thousands of employees, dozens of major subsidiaries, and operations spanning virtually every sector of the economy. There is no chief operating officer. There is no head of human resources. There are no strategic planning departments, no centralized procurement offices, and until recently, no chief technology officer. The corporate office handles financial reporting, tax compliance, capital allocation, and communications. Everything else is delegated to the individual business units.

This is not laziness or neglect. It is a deliberate design choice rooted in a profound insight about organizational incentives. Most corporate bureaucracies exist not to create value but to justify their own existence. Strategy departments produce strategy decks. HR departments produce policies. Compliance departments produce procedures. Each layer of oversight adds cost, slows decision-making, and — most damagingly — strips autonomy from the people who actually understand the business.

Berkshire's radical decentralization eliminates all of this. Subsidiary CEOs run their businesses as if they were independent companies, with full authority over operations, hiring, pricing, and strategy. The only thing they cannot do without permission from Omaha is allocate capital above certain thresholds.

Capital allocation is the core competency — the single function that the corporate center performs better than any individual subsidiary could perform on its own. Buffett (and now Abel) decides where excess cash flows should be deployed: reinvested in existing businesses, used to acquire new ones, invested in public equities, or returned to shareholders via buybacks. This centralization of capital allocation, combined with total decentralization of operations, creates a structure that is unique in corporate history. It captures the advantages of scale and diversification while avoiding the disadvantages of centralized management.

The funding engine that powers this structure is insurance float. Berkshire's insurance operations — GEICO, General Re, Berkshire Hathaway Reinsurance Group, and the Alleghany subsidiaries — collectively held approximately $176 billion in float at the end of 2025. This float represents premiums collected but not yet paid out in claims. While the float is technically a liability on Berkshire's balance sheet, it behaves like permanent, low-cost equity capital because it is continuously renewed as old policies expire and new ones are written. In most years, Berkshire's insurance operations generate underwriting profits — meaning the cost of the float is literally negative. Berkshire gets paid to hold other people's money, and then invests that money at returns that have historically exceeded 15% annually.

The cultural architecture is equally distinctive. Berkshire operates on a foundation of trust that would be alien to most public companies. Subsidiary CEOs are not subjected to the quarterly earnings calls, guidance games, and short-term performance metrics that dominate corporate America.

They are expected to think and act like owners — to make decisions that maximize long-term value even if those decisions depress short-term results. In exchange, they receive autonomy, respect, and the knowledge that they will never be fired for making a good long-term decision that produces a bad short-term outcome. This contract — autonomy in exchange for integrity and long-term thinking — is the cultural glue that holds the entire enterprise together.

This culture is reinforced through Berkshire's most famous ritual: the annual shareholder meeting and the chairman's letter. Buffett's annual letters — which he has written every year since 1965 — are masterpieces of financial communication. They are clear, honest, self-deprecating, and educational. They explain mistakes as candidly as they celebrate successes. They treat shareholders as partners and owners rather than as a nuisance to be managed.

Consider the contrast with typical corporate communications. Most annual reports are written by lawyers and investor relations professionals, designed to convey as little useful information as possible while technically complying with disclosure requirements. Buffett's letters read like a conversation between friends. He explains his reasoning, admits his errors, and educates shareholders on accounting, valuation, and business economics. The 2024 letter, for example, devoted several paragraphs to explaining why Berkshire's reported net income — which includes unrealized gains and losses on the stock portfolio — is essentially meaningless as a measure of business performance, while operating earnings provide a far more useful picture. No other CEO in America would spend shareholder letter real estate explaining why one of their own reported numbers should be ignored.

Over sixty years, these letters built a shareholder base that is extraordinarily loyal, long-term oriented, and aligned with management's philosophy. The annual meeting in Omaha — which draws over 40,000 attendees and has been dubbed "Woodstock for Capitalists" — is both a celebration of this culture and a mechanism for perpetuating it. For an entire weekend, shareholders from around the world gather at the CHI Health Center to hear Buffett and, until his passing, Munger answer questions for six hours straight. The event includes a shareholder shopping day where attendees can buy products from Berkshire subsidiaries at special discounts — See's Candies, Dairy Queen Blizzards, Brooks running shoes, Duracell batteries, Fruit of the Loom underwear. It is part corporate governance, part revival meeting, and entirely unlike anything else in the corporate world.

The Berkshire operating system, then, consists of four interlocking elements: decentralized operations, centralized capital allocation, insurance float as the funding mechanism, and a culture of trust, autonomy, and long-term thinking.

Each element reinforces the others. Decentralization requires trust. Trust enables autonomy. Autonomy attracts exceptional managers. Exceptional managers generate returns that justify further capital allocation. And the float provides the fuel that keeps the entire machine compounding. Remove any one element and the system degrades; remove two and it collapses entirely.

The question that has haunted Berkshire for decades is whether this system can survive its creator. The early evidence from the Abel era suggests it can — but the real test will come not during calm markets, but during the next crisis, when the pressure to abandon long-term thinking is most intense.

IX. Playbook: Investment Philosophy & Business Lessons

The Buffett-Munger investment philosophy is simultaneously the most studied and least replicated approach in financial history. Thousands of books, academic papers, and conference presentations have dissected their methods. Business schools teach case studies on their major investments. And yet, despite the complete transparency of their approach — every investment thesis, every mistake, every principle laid out in plain English across sixty years of shareholder letters — remarkably few investors have been able to replicate their results. Understanding why requires going beyond the surface-level maxims and examining the deeper structural and psychological advantages that make the Berkshire approach work.

The philosophical foundation begins with Benjamin Graham's concept of intrinsic value: every business has a calculable worth based on its future cash flows, discounted back to the present. The investor's job is to estimate that value and buy only when the market price is significantly below it — the margin of safety.

Graham's approach was primarily quantitative: he looked at balance sheets, working capital, and asset values. Munger's contribution was to expand the framework to include qualitative factors — the durability of competitive advantages, the quality of management, the predictability of future cash flows, and the reinvestment dynamics of the business model.

The synthesis of Graham and Munger produced a framework that can be distilled to a handful of principles. First, stay within your circle of competence — invest only in businesses you genuinely understand, and be ruthlessly honest about the boundaries of your knowledge. Buffett's decades-long avoidance of technology stocks was not a blind spot; it was a discipline. He did not invest in things he could not predict with reasonable confidence, and the rapid pace of technological change made most tech businesses fundamentally unpredictable. When he finally invested in Apple, it was because he understood it not as a technology company but as a consumer franchise — a distinction that mattered enormously.

Second, think about stocks as fractional ownership stakes in real businesses, not as trading instruments. This sounds obvious but is violated constantly by professional investors who make decisions based on price momentum, quarterly earnings beats, index weightings, and other factors that have nothing to do with the underlying economics of the business.

Buffett's holding periods are measured in decades, not quarters. His concentration — willingness to put 20-40% of the portfolio in a single position if the opportunity warrants it — reflects a conviction that is alien to the diversification-obsessed world of modern portfolio management.

Third, understand the power of compounding and the extraordinary cost of interrupting it. Compounding works best when left alone. Every time you sell a winning position, you trigger taxes, transaction costs, and the need to find a replacement investment that is equally attractive.

Most investors dramatically underestimate the cumulative drag of these frictions over long time periods. Buffett's approach — buy great businesses and hold them essentially forever — minimizes these frictions and allows compounding to work uninterrupted.

Fourth, be greedy when others are fearful and fearful when others are greedy. This is Buffett's most famous dictum, and it is far harder to execute than it sounds.

During the 2008 financial crisis, when the global financial system appeared to be on the verge of collapse, Buffett invested billions in Goldman Sachs, General Electric, and Bank of America on terms that were extraordinarily favorable to Berkshire. These investments were not acts of bravery — they were acts of rationality, made possible by Berkshire's massive cash reserves and by Buffett's emotional temperament, which allows him to think clearly when everyone around him is panicking.

Fifth, management matters enormously, but capital allocation matters more. Buffett has repeatedly emphasized that the most important job of a CEO is not operations, strategy, or innovation — it is deciding what to do with the company's cash flows. A CEO who generates 15% returns on invested capital but reinvests in projects that earn 5% is destroying value regardless of how operationally brilliant the core business might be. This insight — that capital allocation is the primary determinant of long-term shareholder returns — is perhaps Buffett's most underappreciated contribution to business thinking.

It is also worth noting what is not in the Buffett-Munger playbook. There is no use of leverage to amplify returns. There are no complex derivative strategies — Buffett famously called derivatives "financial weapons of mass destruction" after the near-collapse of Long-Term Capital Management in 1998, though Berkshire itself has used derivatives selectively. There is no short selling. There is no market timing. And there is no hedging of currency or interest rate risk in the traditional sense. The portfolio is designed to withstand adversity, not to avoid it. This simplicity is itself a competitive advantage: in a world where most institutional portfolios are layered with hedges, swaps, and risk management overlays, Berkshire's straightforward approach eliminates an entire category of costs and complexity.

The reason this philosophy is so difficult to replicate is not intellectual — the ideas are simple and clearly articulated. It is psychological and structural.

Psychologically, most people cannot tolerate the concentration, the patience, and the willingness to do nothing for extended periods that the Berkshire approach requires. Buffett has described investing as a game where you stand at the plate and pitches come at you all day — stocks, bonds, real estate, private businesses — and you never have to swing. There are no called strikes. You can let a thousand pitches go by and wait for the one that is exactly in your sweet spot. Most investors, pressured by clients, bosses, or their own egos, swing at everything. They cannot tolerate inactivity. They confuse motion with progress.

Structurally, most investment vehicles impose constraints that make true long-term, concentrated investing impossible. Hedge funds face quarterly redemptions — if performance dips, investors pull their money, forcing sales at the worst possible time. Mutual funds must maintain daily liquidity and are often prohibited from holding more than 5-10% of the portfolio in a single position. Private equity funds have ten-year lifespans that force sales regardless of whether the timing is optimal. Berkshire faces none of these constraints. Its permanent capital structure, which eliminates the risk of investor withdrawals, is perhaps its most important competitive advantage. Buffett never has to sell because an investor wants their money back. He never has to raise cash to meet redemptions. He never has to explain a quarterly drawdown to an impatient allocator. This structural freedom is the invisible foundation on which everything else is built.

X. Bear vs. Bull Case & Comparative Analysis

The bull case for Berkshire Hathaway starts with the balance sheet. With $373 billion in cash and a portfolio of businesses that collectively generate over $44 billion in annual operating earnings, Berkshire possesses financial optionality that is unmatched in corporate America. In a world of elevated asset prices and rising economic uncertainty, Berkshire's fortress balance sheet is a genuine strategic asset. If markets correct sharply — a recession, a financial crisis, a geopolitical shock — Berkshire has the resources to be the buyer of last resort, acquiring high-quality assets at distressed prices just as it did in 2008-2009. This optionality is essentially free: the cash earns Treasury rates while waiting for deployment, and the opportunity cost is partially offset by the insurance float that provides much of the capital.

The operating businesses are diversified across sectors that are largely non-discretionary — insurance, railroads, energy utilities, and industrial manufacturing do not disappear during recessions. They may experience cyclical downturns, but their underlying demand is persistent.

BNSF will move freight regardless of which party controls Congress. GEICO will insure cars regardless of whether the stock market is up or down. Berkshire Hathaway Energy will generate and distribute electricity through virtually any economic scenario. This diversification provides earnings stability that most companies — and most conglomerate structures — cannot match. Full-year 2024 operating earnings hit a record $47.4 billion, and even the softer 2025 year still produced $44.5 billion — a level of earnings consistency that reflects the defensive quality of the underlying businesses.

The insurance franchise is a competitive moat of extraordinary depth. Berkshire's $176 billion in float, generated at a negative cost in most years, gives it a structural funding advantage that is essentially impossible to replicate. No startup can build an insurance franchise of this scale. No existing competitor can match the combination of underwriting discipline, scale, and permanence of capital that Berkshire offers. GEICO's direct-to-consumer model continues to gain market share, and the Alleghany acquisition strengthened the reinsurance platform significantly.

Through the lens of Hamilton Helmer's 7 Powers framework, Berkshire exhibits several durable competitive advantages.

Scale economies in insurance allow it to spread fixed costs over an enormous premium base while maintaining underwriting discipline that smaller competitors cannot match. The brand — built over six decades of transparent, shareholder-friendly management — creates a powerful network effect in acquisitions: the best sellers want to sell to Berkshire, which gives Berkshire access to the best businesses, which further enhances the brand.

The counter-positioning advantage is structural: Berkshire's permanent capital model and decentralized management are so fundamentally different from the private equity and strategic acquirer models that competitors cannot copy them without dismantling their own business models. A private equity firm cannot offer permanent capital because its fund structure requires exits. A public conglomerate cannot offer Berkshire's level of autonomy because its shareholders demand centralized oversight.

And the cornered resource of Buffett's judgment — while not perfectly transferable — has been partially institutionalized through the culture, the letters, the annual meeting, and the investment team of Combs and Weschler.

A Porter's Five Forces analysis reveals a similarly strong position. The threat of new entrants into Berkshire's core businesses is negligible — nobody is building new railroads or replicating GEICO's brand and cost structure at comparable scale. Supplier power is limited because Berkshire's businesses are the buyers, not the sellers, of most critical inputs.

Buyer power is constrained by the essential nature of insurance, freight transport, and electricity — these are services that customers need, not luxuries they can defer. The threat of substitutes exists — autonomous vehicles could reduce auto insurance demand, and renewable distributed energy could challenge centralized utilities — but these are long-term, gradual shifts rather than near-term disruptions. Competitive rivalry among incumbents is moderate: BNSF competes with Union Pacific and a handful of other Class I railroads, but the industry is effectively an oligopoly with rational pricing behavior.

The rivalry of the S&P 500 index fund deserves special attention. Buffett himself has long argued that most investors would be better served by a low-cost index fund than by any active manager — including, implicitly, himself. He famously wagered $1 million in 2007 that an S&P 500 index fund would outperform a basket of hedge funds over ten years, and he won decisively. The irony is that Berkshire itself is increasingly measured against the very index fund that Buffett champions. If Abel's Berkshire merely matches the S&P 500, many investors will question why they should accept the complexity and opacity of a conglomerate when they could own a transparent, diversified index for nearly zero cost.

The bear case, however, extends beyond the index fund challenge. Start with succession. No matter how carefully planned, the transition from a singular genius to a professional management team introduces execution risk. Abel is competent and well-prepared, but he has never been tested as the sole decision-maker during a major crisis — and crises are where the great capital allocators separate themselves from the merely competent. The investment portfolio, managed by Combs and Weschler, has not consistently outperformed simple index strategies in the years it has been tracked. The premium that investors assign to Berkshire stock — the implied belief that Berkshire's management will deploy capital more intelligently than shareholders could themselves — may narrow if the post-Buffett returns merely match the market.

Specific operating businesses face real headwinds. BHE's wildfire liabilities at PacifiCorp, totaling potentially $55 billion in claims, represent a material financial risk that could absorb significant capital and management attention for years.

BNSF faces secular headwinds from the decline of coal transport — once the railroad's most profitable commodity — and potential future competition from autonomous trucking. GEICO, while highly profitable today, competes in a market where telematics, usage-based insurance, and autonomous driving could fundamentally reshape pricing and risk models over the next decade.

Size itself may be the most formidable obstacle. At over $1 trillion in market capitalization, Berkshire needs to generate roughly $100-150 billion in value annually just to match the S&P 500's long-term returns. Finding acquisitions, investments, and organic growth opportunities of that magnitude is extraordinarily difficult.

The cash pile, while providing optionality, also creates a drag on returns — $373 billion earning 4-5% in Treasury bills when the historical return on invested capital has been 15-20% represents a significant headwind to overall performance. Buffett acknowledged this constraint repeatedly in his letters, noting that the days of extraordinary outperformance were likely behind Berkshire simply because of the mathematics of scale.

The comparison with other conglomerates is instructive and, for Berkshire bulls, sobering. General Electric, once America's most admired company and the gold standard for diversified industrial management under Jack Welch, ultimately proved that the conglomerate model masked capital allocation failures and earnings management. GE has been broken into three independent entities — GE Aerospace, GE Vernova, and GE HealthCare — after decades of value destruction. Johnson & Johnson split into two companies. 3M spun off its healthcare division. Even Honeywell has faced pressure to simplify. The era of the diversified conglomerate appears to be ending, with capital markets increasingly favoring focused, pure-play businesses that investors can analyze and value independently.

Berkshire has so far defied this trend, but the structural pressure toward simplification may intensify as the founder's influence wanes. The "conglomerate discount" — the tendency for diversified companies to trade at lower multiples than focused peers — is a well-documented phenomenon in academic finance. Berkshire has historically avoided this discount because the market trusted Buffett's capital allocation more than it trusted investors' ability to allocate the capital themselves. If that trust erodes under new leadership, activist investors or market forces could push for a breakup that would likely unlock tens of billions in value but destroy the organizational architecture that makes Berkshire unique.

For investors tracking Berkshire going forward, the key performance indicators to watch are deceptively simple: operating earnings growth per share, which measures the underlying earning power of the business absent mark-to-market fluctuations in the stock portfolio, and book value per share growth relative to the S&P 500 total return, which was Berkshire's original scorecard and remains the most honest measure of whether the company is creating or destroying value for shareholders relative to the passive alternative.

XI. Power Analysis & Future Scenarios

Berkshire Hathaway's sources of durable competitive power are unusual in that they are primarily structural rather than operational. Most companies derive their advantages from proprietary technology, brand strength in a specific market, or operational excellence in a particular domain. Berkshire's advantages are architectural — they emerge from the design of the organization itself.

The most powerful of these is what might be called the "permanent capital" advantage. Because Berkshire has no debt maturities that force liquidation, no investor redemptions that require selling, and no dividend obligations that drain cash, it can make investment and acquisition decisions on a truly long-term basis.

This advantage is nearly impossible to replicate within the constraints of modern institutional investing. Hedge funds face quarterly redemptions. Private equity funds have ten-year lifespans. Mutual funds must maintain daily liquidity. Even sovereign wealth funds face political pressures to deploy capital in specific ways. Berkshire faces none of these constraints, and this freedom allows it to be patient, contrarian, and opportunistic in ways that are structurally denied to its competitors.

The "Berkshire premium" — the extent to which the stock trades above its book value or the sum of its parts — is both an asset and a vulnerability. When investors believe that Berkshire's management will compound capital at rates above the market, the stock commands a premium. If that belief erodes — because post-Buffett returns disappoint, because the cash pile grows too large without attractive deployment, or because the conglomerate discount becomes conventional wisdom — the premium could narrow or disappear entirely. This is perhaps the most significant risk to Berkshire shareholders in the medium term: not that the businesses will deteriorate, but that the market's willingness to pay a premium for the Berkshire structure will diminish.