Dover Corporation: The Story of an Industrial Conglomerate's Quiet Excellence

I. Introduction & Episode Roadmap

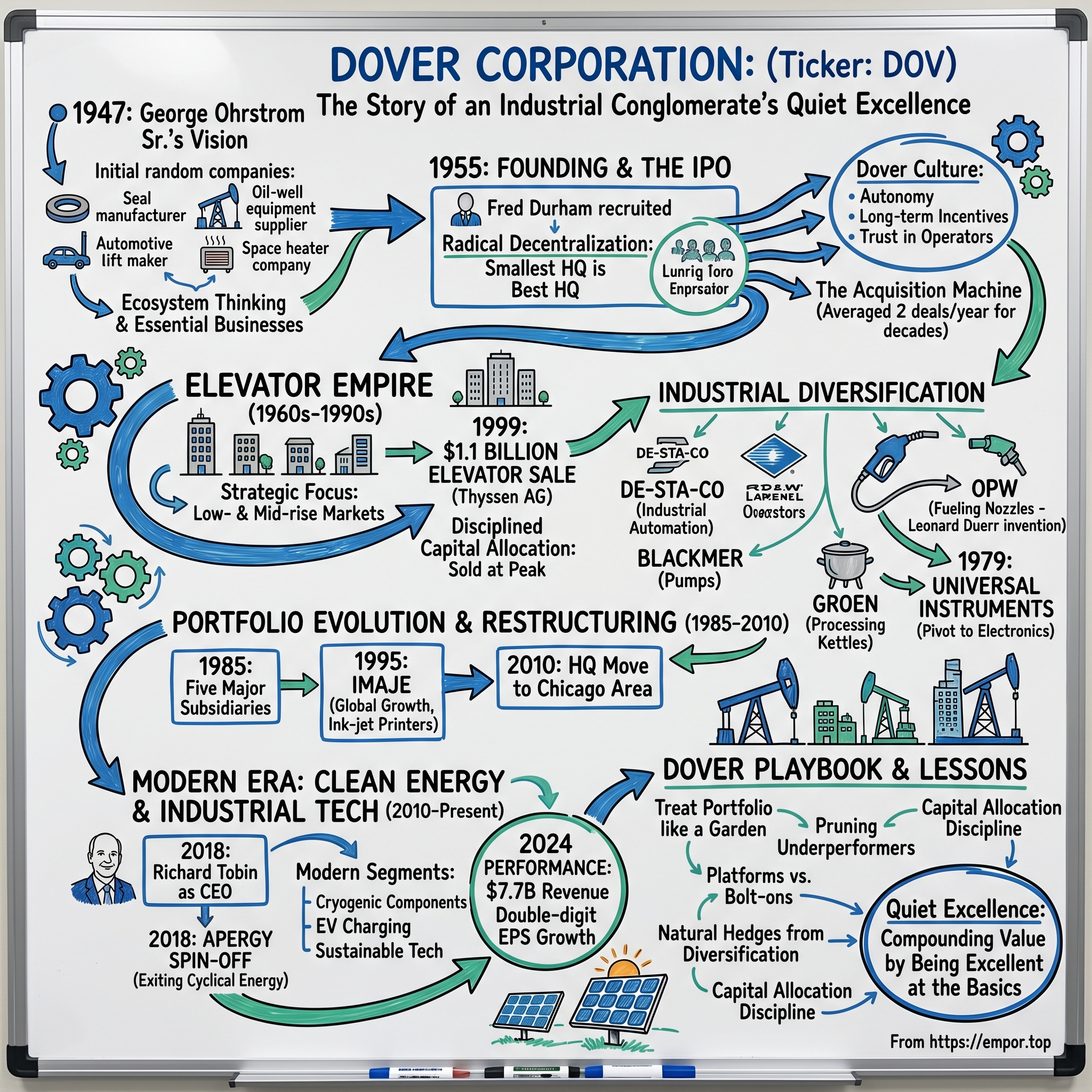

Picture this: A Manhattan stockbroker in 1947, staring at four seemingly random industrial companies spread across his desk—a seal manufacturer, an automotive lift maker, an oil-well equipment supplier, and a space heater company. George Ohrstrom Sr. saw something others didn't. Not just four businesses, but the foundation of what would become one of America's most enduring industrial success stories. Today, Dover Corporation generates over $7 billion in annual revenue, has completed more than 100 acquisitions, and has quietly outperformed most flashier conglomerates you've actually heard of.

The central question isn't just how a post-war elevator company became a sprawling industrial empire—it's how Dover mastered the art of decentralized excellence while others stumbled trying to control everything from the center. This is the story of a company that turned the conglomerate playbook upside down, treating its subsidiaries not as vassals but as independent kingdoms, each with its own ruler and its own P&L destiny.

What unfolds is a masterclass in three critical disciplines: First, the radical decentralization that gave Dover its edge—imagine running 100+ companies with a corporate staff smaller than most startups. Second, the acquisition machine that averaged two deals per year for decades, each one surgically selected and culturally integrated. Third, the portfolio evolution that saw Dover sell billion-dollar divisions at their peak rather than riding them down—including the legendary $1.1 billion elevator sale that defined disciplined capital allocation.

We'll trace Dover's journey from Ohrstrom's original vision through the Fred Durham culture revolution, the elevator empire years, the acquisition binge of the 1980s and 90s, and into today's clean energy pivot. Along the way, we'll uncover why boring B2B industrial companies often make the best investments, how decentralization can beat command-and-control, and what happens when you give smart operators real autonomy.

For investors and operators alike, Dover offers lessons in patient capital allocation, the power of platforms versus bolt-ons, and why sometimes the best headquarters is the smallest one. This isn't just industrial history—it's a blueprint for building enduring value in unsexy markets.

II. Origins: George Ohrstrom's Vision (1940s-1955)

The year was 1945, and George Ohrstrom Sr. wasn't celebrating V-J Day like most Americans. Instead, the New York City stockbroker was hunched over financial statements, studying the industrial landscape that would emerge from wartime production. While others chased consumer goods plays, Ohrstrom saw opportunity in the unglamorous backbone of American industry—the pumps, seals, lifts, and heaters that would power the post-war boom.

His first moves were deliberate, almost surgical. The C. Lee Cook Company manufactured seals and piston rings—boring products that every piece of industrial equipment needed. Rotary Lift made automotive lifts at the exact moment America's love affair with cars was exploding. W.C. Norris produced sucker rods for oil wells just as Texas crude was fueling suburban expansion. Peerless built space heaters for the factories and warehouses sprouting across the Midwest. Dover Corporation was incorporated in 1947, but Ohrstrom wasn't simply assembling a random collection of industrial assets. Each piece fit a thesis about the coming industrial expansion. America was building highways, drilling for oil, modernizing factories, and constructing the infrastructure of prosperity. These weren't glamorous businesses—nobody was writing magazine profiles about piston ring manufacturers—but they were essential.

The genius wasn't in the individual companies but in how Ohrstrom thought about them. Unlike the conglomerate builders who would follow in the 1960s, chasing earnings through unrelated diversification, Ohrstrom saw interconnected industrial markets. A car on a Rotary Lift needed C. Lee Cook's seals. The same industrial customers buying oil-well equipment from Norris might need Peerless heaters for their facilities. This wasn't empire building—it was ecosystem thinking, decades before Silicon Valley made the term fashionable.

Dover Corporation was formed in 1955, when New York stockbroker George Ohrstrom, Sr., recruited Fred D. Durham to manage four companies he had bought in the 1930s and 1940s. The recruitment of Durham would prove pivotal—Ohrstrom had the vision and the capital, but Durham would bring something equally valuable: a management philosophy that would define Dover for the next seven decades.

Dover Corporation went public on the New York Stock Exchange. As such, the year 1955 marks the company's official founding. The IPO raised capital, but more importantly, it forced discipline. Public markets demanded transparency and performance, creating accountability that would shape Dover's acquisition strategy for decades to come.

The post-war context cannot be overstated. Industrial production had doubled during the war years, and peacetime conversion created massive demand for civilian industrial goods. The Interstate Highway System was just beginning, the suburbs were exploding, and American manufacturing dominated global markets. While others chased consumer goods—televisions, appliances, the visible symbols of prosperity—Ohrstrom bet on the picks and shovels. His investment philosophy was simple: own the boring, essential businesses that enabled everything else.

By 1955, when Dover went public with 930,000 shares, the foundation was set. Four industrial companies, minimal corporate overhead, and a radical idea: that the best way to manage diverse industrial businesses was to barely manage them at all. The seeds of Dover's decentralized model were planted from day one, though it would take Fred Durham to fully cultivate this approach into Dover's defining characteristic.

III. The Fred Durham Era: Building the Culture (1955-1970s)

"Business, like any other human enterprise, thrives best where creativity and initiative are encouraged in an atmosphere of maximum autonomy." Durham set out to give Dover an environment in which executives could work creatively and without the hindrance of bureaucracy. As Durham intended, autonomy, decentralization, and a minimal corporate staff became Dover's hallmarks.

Fred Durham didn't just run Dover—he architected its soul. When he took the reins in 1955, the conventional wisdom said conglomerates needed strong central control, layers of corporate staff, and standardized processes. Durham looked at this playbook and essentially lit it on fire. At the end of Dover's first year of operation the corporate staff consisted of three people, including Durham. Three people to oversee four companies. In an era when corporations were building management pyramids, Durham was building something closer to a federation.

The recruitment story itself reveals Durham's character. C. Lee Cook had been built largely by its owner and president, Fred Durham, before being sold to Ohrstrom. Durham wasn't some outside hire brought in to professionalize operations—he was an operator who had built and sold a business, who understood the entrepreneurial mindset because he lived it. When Ohrstrom tapped him to run the combined entity, he wasn't hiring a manager; he was recruiting a philosophical architect.

Fred Durham influenced Dover's corporate culture, emphasizing autonomy, decentralization and few corporate staff members. As a result, divisions were run in an independent fashion, each with its own president. This wasn't just delegation—it was radical trust. Each division president ran their business like an owner, with their own board of directors, their own strategic planning, their own capital allocation decisions within limits. Dover corporate didn't tell them how to run their businesses; it simply asked them to deliver results.

The compensation philosophy reflected this ownership mentality. Dover-subsidiary managers operate with great independence and are rewarded on the basis of long-term earnings growth and return on investment of individual businesses. Note the emphasis on "long-term"—this wasn't quarterly capitalism but patient industrial building. Managers were incentivized to think in years and decades, not quarters.

The company is often thought of as a portfolio of companies rather than a conglomerate because of its hands-off organizational structure and philosophy of management. This distinction mattered. Conglomerates of the era—ITT, Litton Industries, LTV—were command-and-control operations where corporate headquarters made key decisions. Dover was something different: a holding company that actually held rather than strangled.

The early acquisitions under Durham showed the model in action. Dover's purchase of the Shepard Warner Elevator Company in 1958 marked the beginning of an effort to grow the elevator business. But Durham didn't install Dover executives to run Shepard Warner. The existing management stayed, now with Dover's balance sheet behind them and Durham's philosophy protecting their autonomy. This wasn't just good business—it was a signal to every future acquisition target: join Dover and keep your culture, your team, your entrepreneurial spirit.

As part of Dover, the acquired companies retained much of their autonomy, and, in most cases, their preacquisition management, while benefiting from Dover's financial strength. This retention rate was extraordinary for the era. While other conglomerates gutted acquired companies, installing their own people and processes, Dover kept the entrepreneurs who built the businesses. They understood something profound: you can't separate a business from its builders without losing something essential.

By the end of the 1970s, Durham's model had proven itself. Between 1955 and 1979, Dover acquired 14 companies. Fourteen companies in 24 years might seem modest compared to modern serial acquirers, but each acquisition was carefully selected, culturally aligned, and given room to breathe. The Durham era established three principles that would define Dover for generations: radical decentralization, patient capital, and trust in operators. These weren't just management techniques—they were competitive advantages that compounded over decades.

IV. The Elevator Empire Years (1960s-1990s)

The Otis Elevator Company dominated American vertical transportation with almost monopolistic control. Westinghouse leveraged its electrical expertise to claim second place. For any other company, challenging these giants would have been corporate suicide. But Dover saw an opening—not to beat them at their own game, but to play a different one entirely.

Dover acquired Acme Elevator, Elevator Service, Reddy Elevator Company in 1964 and Hunter-Hayes Elevator Company in 1970. With these purchases, Dover soon became the third largest elevator company in the U.S. The speed was breathtaking—from zero to number three in less than a decade. But the strategy was even more impressive than the pace.

While Otis focused on new construction and prestige projects—the Empire State Building, the World Trade Center—Dover targeted a different market: the tens of thousands of low- and mid-rise buildings that needed reliable, affordable elevator service. These weren't glamorous installations, but they were profitable. A four-story apartment building in Cleveland might not make the architectural magazines, but it needed elevators that worked, parts that arrived quickly, and service technicians who actually showed up.

The acquisition strategy was surgical. Each target brought something specific: regional presence, service capabilities, or technical expertise. Dover continued to expand its elevator division throughout the 1960s and 1970s with the purchases of Moody & Rowe, Burch, Turnbull, Burlington, Hammond & Champness, Louisiana Elevator and W.W. Moore. These weren't random purchases but deliberate market coverage—Moody & Rowe gave them West Coast presence, Louisiana Elevator opened the Gulf region, Burlington brought Canadian operations.

The genius was in the integration—or rather, the lack of it. Each acquired elevator company kept its local brand, its relationships, its service network. A building owner in Baton Rouge still called Louisiana Elevator for service, not some faceless corporation in New York. The technicians were the same guys who had been maintaining those elevators for years. Dover provided capital, best practices, and purchasing power, but the local touch remained.

Managing the number three position required strategic discipline. Dover never tried to out-Otis Otis. They didn't bid on landmark projects or chase market share for its own sake. Instead, they focused on operational excellence and service density. In markets where they operated, Dover elevator companies often had the best response times, the deepest parts inventory, and the most experienced technicians. They turned the disadvantage of being third into an advantage—the hungry competitor who tried harder.

The financials told the story of this focused execution. Dover Elevator had a pretax operating profit of $93 million in 1997. For context, this represented margins that many pure-play elevator companies couldn't match, achieved through operational discipline and the Dover management model that kept corporate overhead minimal.

But by the late 1990s, the elevator industry was consolidating globally. European giants were acquiring American players, and scale was becoming increasingly important in winning large contracts. Dover faced a choice: invest billions to compete globally or exit at the peak. Dover sold its elevator division in 1999 to Thyssen AG for $1.1 billion.

The timing was exquisite. Dover sold into strength, not weakness. They captured maximum value—over 11 times pretax earnings—and redeployed capital into higher-growth industrial segments. The sale allowed Dover to focus on building its other businesses and moved ThyssenKrupp Elevator Americas to the number three spot worldwide in the elevator and escalator industry.

The elevator chapter offers profound lessons in portfolio management. Dover built a billion-dollar business from scratch through disciplined acquisition, operated it with excellence for decades, and then sold it without sentimentality when the strategic logic changed. No ego, no empire building—just cold, clear capital allocation. They understood that in business, as in poker, the key isn't just knowing when to bet—it's knowing when to fold a winning hand.

V. Diversification & The Acquisition Machine (1970s-1990s)

While Dover was building its elevator empire, a parallel story was unfolding across dozens of other industrial niches. The company was perfecting an acquisition machine that would ultimately complete over 100 deals, each one following a disciplined playbook that turned industrial orphans into profitable dynasties.

In 1962, Dover made two notable acquisitions: Detroit Stamping Company, now DE-STA-CO, specializing in the design and manufacturing of clamping, gripping, transferring and robotic tooling. DE-STA-CO wasn't sexy—they made clamps and grippers for industrial automation—but every manufacturing line in America needed their products. The business had 90%+ market share in several niche categories, the kind of dominance that's invisible to outsiders but obvious to anyone who's ever designed a production line.

The OPW acquisition revealed Dover's knack for finding hidden technological gems. The company was shortened to OPW, and in 1949 one of its engineers, Leonard H. Duerr, invented the automatic shutoff fuel-dispensing nozzle valve. Think about that—every time you pump gas and the nozzle automatically stops when your tank is full, you're using technology Dover has owned since the 1960s. It's the kind of omnipresent but unnoticed innovation that Dover specialized in acquiring.

The 1970s brought more industrial workhorses into the fold. Blackmer Pump Company made pumps for everything from chocolate syrup to crude oil—unglamorous products with irreplaceable applications. Groen Manufacturing produced steam-jacketed kettles that cooked soup in every major food processing plant in America. These weren't businesses that would ever IPO or attract venture capital, but they generated returns that would make any investor envious. The 1979 acquisition of Universal Instruments marked Dover's boldest strategic pivot yet. In July 1979 Dover acquired Universal Instruments Corporation of Binghamton, New York. Universal, the world's leading manufacturer of automated assembly equipment for electronic circuitry, moved Dover into the electronics business. This wasn't just buying another industrial company—it was betting on the electronics revolution before most industrials even understood what was happening.

By 1980 the electronics market had become the second most important growth area for Dover, following petroleum-production products. The speed of this transformation was remarkable. In just one year, electronics went from zero to Dover's second-largest growth driver. Universal Instruments brought Dover into the heart of the technology supply chain, making the machines that assembled the circuit boards powering everything from computers to telecommunications equipment.

The acquisition pace accelerated dramatically in the 1980s. Dover bought about 25 companies between 1985 and 1989, for $460 million, but has taken on relatively little debt. Think about that math—25 companies in five years, averaging $18 million each. These weren't blockbuster deals making headlines; they were surgical strikes on niche leaders. In general, Dover's capital expenditures were financed with internally generated resources.

The discipline was remarkable. In 1989 the company made no acquisitions, for the first time since 1980. The reason for this reticence was the inflated prices for acquisitions engendered by the leveraged buyout boom; Dover was following its traditional practice of not overpaying for the companies it acquired. While everyone else was playing with leveraged buyout monopoly money, Dover sat on its hands. They understood that the best deal is sometimes no deal.

The acquisition criteria remained consistent: They were market leaders, or had proprietary lines that meshed with Dover's existing businesses and had good growth prospects. Dover acquisitions, almost without exception, had higher-than-average returns on invested capital. This wasn't spray-and-pray diversification but targeted platform building.

In just over 45 years, Dover has acquired more than 100 manufacturing companies. This acquisition strategy has benefitted Dover stockholders, employees and customers. The numbers tell only part of the story. Each acquisition brought not just products and profits but people, patents, and customer relationships. The machine wasn't just buying companies—it was assembling an industrial ecosystem where each piece made the others stronger.

The segment structure evolved to manage this complexity. Each unit operated with an independent president and a board of directors until 1985, when the management structure was reconfigured to account for its growing complexity. Dover wasn't becoming more centralized as it grew—it was creating new layers of independence, Russian dolls of autonomy that preserved entrepreneurial spirit at every level.

VI. Portfolio Evolution & Restructuring (1985-2010)

By 1985, Dover faced a classic organizational paradox. The company had grown too complex for its original structure—40+ companies reporting through informal channels—but centralizing control would kill the entrepreneurial culture that made Dover special. The solution was elegant: create structure that preserved independence.

Thus, in 1985, Dover's management was restructured. The resulting arrangement created five major subsidiaries, each with between five and nine of its own related subsidiaries headed by a chief executive officer. The presidents of the approximately 40 companies that comprised Dover reported to the CEO of one of the five subsidiaries. The five subsidiary chiefs reported to the Dover CEO. Each subsidiary continued to seek to add complimentary acquisitions.

Five major subsidiaries were represented in four sections: building industries (Dover Elevator International); electronic products (Dover Technologies); petroleum (Dover Resources); and industrial and aerospace products (Dover Industries, Dover Sargent). This wasn't bureaucracy—it was federalism. Each sector CEO ran their own mini-conglomerate, with acquisition authority, capital allocation power, and strategic autonomy. Dover corporate remained lean, more like a private equity firm than a traditional headquarters.

Leadership transitions tested the model. A result of this effort included the acquisition of Dieterich Standard, which manufactured liquid-measurement instruments and whose president, Gary Roubos, went on to become Dover's chief operating officer (COO) and president in 1977. Later, Roubos became Dover's chief executive officer (CEO) in 1981. Roubos wasn't an outside CEO brought in to "transform" Dover—he was an operator who came through acquisition, understood the business, and preserved the culture.

In the years Roubos served as president, from 1977 to 1989, sales doubled from $1 billion to a little over $2 billion. But growth alone wasn't the achievement. Roubos navigated the 1980s—a decade of hostile takeovers, leveraged buyouts, and conglomerate breakups—without losing Dover's soul. While raiders dismantled industrial companies for parts, Dover kept building. The 1995 acquisition of Imaje marked a watershed moment. In September 1995 Dover paid $200 million for an 88 percent interest in Valance, France-based Imaje, S.A., one of the world's three largest manufacturers of industrial continuous ink-jet printers and specialized inks. The largest of these, and the company's largest purchase to date, also represented the company's increasing concentration on overseas growth. Dover wasn't just buying another American industrial company—they were going global, acquiring European technology leadership in a growing market.

In 1989 Dover again revised its structure, into six sectors, to reflect shifts in market activity. The constant restructuring wasn't organizational churning but adaptive evolution. As markets shifted, Dover's structure shifted with them, always maintaining the balance between autonomy and coordination.

The dot-com era tested Dover's discipline. While Dover acquired more than seventy companies between 1998 and 2002, the company's acquisition rate slowed in the early 2000s. Dover sold eight companies in 2001 for a total of $400 million. While tech companies soared on promises, Dover kept buying real businesses with real cash flows. They looked old-fashioned until the bubble burst, then they looked prescient.

The headquarters move in 2010 symbolized a broader transformation. Under Livingston's leadership, Dover moved its corporate headquarters from New York City to the Chicago area in 2010. Factors at play in this decision included Chicago's central location, wide variety of housing options for employees, quality of life, and nearby air service to national and global destinations. The choice to move to Downers Grove, Illinois, was also partially impacted by an effort to consolidate operations, and reduce administration costs.

This wasn't just cost-cutting—it was cultural realignment. Moving from Manhattan to suburban Illinois sent a message: Dover was an industrial company, not a financial engineering firm. The consolidation brought segment headquarters under one roof while maintaining operational independence—physical proximity without organizational interference.

VII. Modern Era: Clean Energy & Industrial Tech (2010-Present)

The appointment of Robert Livingston as CEO in 2008 represented continuity through crisis. In 2008, Robert Livingston was appointed Dover's new CEO and president. Livingston's Dover career began twenty-nine years earlier with the acquisition of K&L Microwave, where he was a vice president. After joining Dover, Livingston also served as COO and vice president of Dover Corporation, president and CEO of Dover Engineered Systems, and president and CEO of Dover Electronics. Another operator-CEO who understood Dover from the ground up.

The financial crisis could have destroyed Dover's acquisition machine, but instead it created opportunity. While competitors retrenched, Dover kept buying, picking up distressed assets at attractive prices. The discipline to buy in downturns—when capital was scarce and fear dominated—separated Dover from fair-weather acquirers. The 2018 transition marked another evolution. Richard J. Tobin took over as president and CEO of Dover in 2018. Dover also announced that Richard J. Tobin, who most recently served as the Chief Executive Officer of CNH Industrial, N.V. ("CNH") and who serves as a member of Dover's Board of Directors, will become Dover's President and Chief Executive Officer, effective May 1, 2018. Unlike his predecessors who came up through Dover acquisitions, Tobin brought outside perspective—but critically, he had already served on Dover's board since 2016, understanding the culture before taking the helm.

The timing was strategic. The latest CEO appointment comes when Dover is undergoing a portfolio transition. In December 2017, the company decided to spin-off its Wellsite business, now known as Apergy, into a stand-alone, publicly-traded company. Dover spun off a large portion of its Energy segment including upstream energy businesses into a standalone publicly traded company, Apergy (2018). The Downers Grove, Illinois-based company is spinning off its billion-dollar Wellsite business, now known as Apergy, which makes drill bits and other oilfield equipment.

This wasn't retreat but refinement. Dover's Wellsite business, which includes Dover Artificial Lift, Dover Energy Automation, and US Synthetic, operates in the oil & gas drilling and production industry. The spin-off decision reflected Dover's discipline—exiting cyclical, capital-intensive businesses at the right time, just as they had with elevators two decades earlier. The modern portfolio reflects decades of evolution. Current business segments: Engineered Products, Clean Energy and Fueling, Imaging & Identification, Pumps & Process Solutions and Climate and Sustainability Technologies. Five segments, each a collection of market-leading businesses, each run with the Dover DNA of decentralization and operational excellence. The recent portfolio moves demonstrate Dover's continued discipline. German firm Stabilus purchased DESTACO for $680 million in a transaction announced in October 2023 and closed in April 2024, while Terex acquired the Environmental Solutions Group division for $2 billion. These weren't distressed sales but strategic portfolio optimization—selling strong businesses when valuations were attractive and the strategic fit had evolved.

The clean energy pivot represents Dover's next evolution. We have completed six acquisitions over the last three years to create a new platform in cryogenic components within our Clean Energy & Fueling segment, and we are very excited about the future value creation through margin expansion and durable, secular end market growth. Dover isn't chasing buzzwords but building real positions in hydrogen infrastructure, EV charging, and sustainable technologies—markets where their industrial expertise creates competitive advantage.

VIII. Financial Performance & Operating Model

The 2024 numbers tell a story of resilience and discipline. For the year ended December 31, 2024, Dover generated revenue of $7.7 billion, an increase of 1% compared to the prior year. GAAP earnings from continuing operations of $1.4 billion increased by 48%, and GAAP diluted EPS from continuing operations of $10.09 was up 50%. In a year of industrial uncertainty, Dover delivered double-digit earnings growth—the power of portfolio management and operational excellence.

The margin story is even more impressive. While revenue grew modestly, earnings exploded. This wasn't financial engineering but the compound effect of decades of choices: pruning low-margin businesses, investing in high-return niches, and maintaining cost discipline even in good times. The 48% earnings growth on 1% revenue growth represents operating leverage that only comes from owning the right businesses and running them exceptionally well.

The business philosophy remains unchanged from the Durham era: perceive our customers' real needs for products and support; provide better products and services than the competition; invest to maintain our competitive edge; ask our customers to pay a fair price for the extra value we add. Service to our customers, product quality, innovation and a long-term orientation are implicit in this credo. Pursuit of this market leadership philosophy by all our businesses, plus value oriented acquisitions of companies that share this philosophy, plus a decentralized management style that gives the greatest scope to the talented people who manage these companies have combined to produce results featuring: long-term earnings growth; high cash flow; superior returns on stockholders' equity.

The capital allocation framework follows clear priorities. First, invest organically in high-return projects within existing businesses. Second, pursue bolt-on acquisitions that strengthen platforms. Third, return excess capital to shareholders through dividends and buybacks. We recently closed two bolt-on acquisitions within our high-priority Pumps & Process Solutions segment, and our acquisition pipeline remains robust. The discipline is in what Dover doesn't do—no transformational mega-deals, no unrelated diversification, no empire building.

The decentralized model continues to drive performance. Dover-subsidiary managers operate with great independence and are rewarded on the basis of long-term earnings growth and return on investment of individual businesses. The company is often thought of as a portfolio of companies rather than a conglomerate because of its hands-off organizational structure and philosophy of management. Each business president runs their operation like an owner because, through compensation design, they essentially are.

The operational excellence shows in the details. Working capital management, inventory turns, cash conversion—the blocking and tackling of industrial management executed consistently across dozens of businesses. ESG's efficient operating model with low net working capital will drive a meaningful improvement in free cash flow accretion—this discipline was why Dover could sell ESG for $2 billion, capturing value created through operational improvement.

The segment structure provides both focus and flexibility. We deliver innovative equipment and components, consumable supplies, aftermarket parts, software and digital solutions, and support services through five operating segments: Engineered Products, Clean Energy & Fueling, Imaging & Identification, Pumps & Process Solutions and Climate & Sustainability Technologies. Each segment contains multiple platforms, each platform multiple businesses, creating natural hedges against market cycles while maintaining operational focus.

IX. Playbook: Business & Investing Lessons

The Dover story offers a masterclass in several timeless business principles, each proven over seven decades of execution.

The Power of Decentralization in Industrial Conglomerates: Dover proves that you can manage complexity through simplicity. By pushing decision-making down to operating units, Dover harnesses entrepreneurial energy while maintaining financial discipline. The model works because it aligns incentives—business presidents think like owners because they're compensated like owners. The minimal corporate staff isn't about cost savings; it's about preventing the bureaucratic creep that kills innovation and speed in large organizations.

Acquisition Discipline: When to Buy, When to Sell: Dover's acquisition record—over 100 companies bought, dozens sold—demonstrates that successful M&A isn't about deal volume but deal quality. They buy market leaders or strong number twos in fragmented industries. They keep existing management. They don't overpay—sitting out the late 1980s LBO boom and the late 1990s tech bubble. Most importantly, they sell without sentimentality, as shown by the billion-dollar elevator exit and recent ESG sale.

Portfolio Management: Pruning Underperformers: Dover treats its portfolio like a garden—constant cultivation, selective pruning, strategic replanting. Underperforming businesses aren't hidden in segment averages or given endless turnaround time. Typically divisions that have been sold were not a good fit with Dover's other product lines. The discipline to exit good businesses that no longer fit the strategy—like elevators in 1999—separates Dover from conglomerates that become prisoners of their own history.

Managing Cyclicality in Industrial Markets: Dover's structure creates natural hedges. When oil and gas struggles, clean energy might thrive. When industrial automation slows, food equipment might accelerate. But the real hedge is operational flexibility—the ability to cut costs quickly in downturns while maintaining investment in growth areas. The decentralized model means each business can respond to its specific market conditions without waiting for corporate approval.

The "Portfolio of Companies" vs. Traditional Conglomerate Model: Dover isn't ITT or GE—sprawling conglomerates trying to find synergies where none exist. Dover's businesses share DNA (industrial manufacturing excellence) but not forced integration. There's no Dover Way imposed from headquarters, no shared services creating dependencies. Each business stands alone, which paradoxically makes the whole stronger—there's no systemic risk from one unit's problems spreading to others.

Capital Allocation Across Diverse End Markets: Dover's capital allocation works because it's both disciplined and flexible. Corporate sets hurdle rates and return requirements, but operating units decide specific investments. This creates a natural competition for capital—only the best projects get funded. The willingness to sell strong businesses when valuations peak (elevators, ESG) and redeploy into higher-growth areas shows dynamic capital allocation at its best.

Building Platforms vs. Bolt-on Acquisitions: Dover doesn't just buy random industrial companies; they build platforms. DE-STA-CO became a clamping and automation platform. OPW anchored a fueling systems platform. Universal Instruments started an electronics platform. Once a platform is established, bolt-on acquisitions can be integrated more easily, creating revenue and cost synergies while maintaining operational independence.

X. Analysis & Bear vs. Bull Case

Bull Case:

The bull thesis rests on Dover's proven ability to compound value through cycles. The acquisition track record speaks for itself—decades of buying at reasonable multiples, improving operations, and selling at peak valuations. The company has navigated everything from 1970s stagflation to 2008's financial crisis to COVID-19, emerging stronger each time.

The clean energy and sustainability tailwinds provide secular growth drivers. Dover isn't betting the company on green technology but selectively building positions where industrial expertise matters—hydrogen infrastructure, EV charging, heat pumps. These aren't science projects but real businesses with real customers and real profits. The sustainability angle also helps with talent acquisition and customer relationships in an ESG-conscious world.

The balance sheet strength enables opportunistic moves. With modest leverage and strong cash generation, Dover can pursue acquisitions when others are retrenching. The recent acquisition pace—six deals in three years for the cryogenic platform alone—shows the machine is still working. We ended the year with a significant cash position that provides flexibility as we pursue value-creating capital deployment.

Diversification across industrial end markets provides resilience. Dover serves waste management, food processing, telecommunications, automotive, aerospace, and dozens of other sectors. No single customer or industry can tank the company. This diversification, combined with the recurring revenue from parts and service, creates earnings stability through cycles.

Management execution deserves premium valuation. The Tobin era has continued Dover's tradition of operational excellence while modernizing for digital transformation. The willingness to exit businesses at peak values (DE-STA-CO, ESG) shows continued capital allocation discipline. Management has consistently delivered on guidance, building credibility with investors.

Bear Case:

The bear thesis starts with industrial cyclicality. Despite diversification, Dover can't escape industrial recession. When capital spending freezes, Dover's customers stop buying equipment. The 1% revenue growth in 2024 shows that even in a decent economy, organic growth is challenging. Industrial markets are mature, and Dover is fighting for share in slow-growth sectors.

Competition from focused specialists threatens market positions. In every niche Dover operates, there's a pure-play competitor with deeper expertise and singular focus. These specialists can often out-innovate and out-service Dover's businesses. The decentralized model, while preserving autonomy, may prevent Dover from leveraging scale advantages against focused competitors.

Integration complexity limits synergy capture. Dover's hands-off approach preserves entrepreneurial spirit but may leave money on the table. Competitors with more integrated models might achieve better purchasing power, shared R&D, or customer cross-selling. The numerous small acquisitions create integration overhead without transformational impact.

Mature end markets constrain growth. Many of Dover's markets—pumps, compressors, industrial automation—are GDP-growth businesses at best. While Dover can gain share through acquisition, organic growth remains challenging. The shift to clean energy is necessary but expensive, requiring investment in new capabilities while traditional markets slow.

The conglomerate discount may persist regardless of execution. Markets consistently value focused companies higher than diversified industrials. Despite Dover's track record, it trades at a discount to pure-play peers. This valuation gap makes Dover a perpetual acquisition candidate itself, potentially limiting upside for long-term holders.

XI. Epilogue & "If We Were CEOs"

The Dover model feels anachronistic in an era of activist investors and demands for focus. Yet it keeps working. While flashier conglomerates imploded—GE's dramatic shrinkage, United Technologies' breakup—Dover quietly compounds value. The secret isn't complexity but simplicity: buy good businesses, run them well, sell when appropriate, repeat.

If we were running Dover, the temptation would be to modernize—more integration, more technology, more central control. But that misses the genius. Dover works precisely because it doesn't try to be something it's not. It's not a technology company, though it uses technology. It's not a services company, though service is crucial. It's an industrial operator that happens to be great at capital allocation.

The next decade will test the model. Industrial digitalization, sustainability mandates, reshoring dynamics—each creates opportunities and threats. Dover's decentralized structure should help it adapt faster than centralized competitors. Each business can pursue its own digital strategy, its own sustainability approach, suited to its specific market. The corporate role remains minimal—provide capital, set standards, get out of the way.

The lessons for founders transcend industrial markets. Building through M&A requires discipline most don't have—the discipline to walk away from bad deals, to keep good management in place, to sell successful businesses when logic dictates. The hardest lesson: sometimes the best management is the least management. Dover's corporate staff remains tiny not from cheapness but from wisdom—the recognition that value creation happens in operating units, not conference rooms.

The quiet excellence of B2B industrial companies offers an investment lesson too. While markets obsess over the next consumer app or AI breakthrough, companies like Dover compound wealth by making things that make things. Unglamorous? Absolutely. Profitable? Consistently. In a world of hype and disruption, there's something reassuring about a company that's been quietly excellent for seven decades.

Dover will never be Tesla or Apple—beloved brands with devoted followers. It will never be Amazon or Google—transforming how we live and work. But for seven decades, Dover has done something perhaps more impressive: created enormous value by being excellent at the basics. In business, as in life, that's often enough. More than enough, actually—it's everything.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube