Broadridge Financial Solutions: The Hidden Infrastructure of Wall Street

I. Introduction & Episode Setup

Picture this: It's proxy season 2023, and somewhere in a gleaming Manhattan tower, a portfolio manager at BlackRock clicks "vote" on a shareholder proposal. That single click triggers a cascade through systems that will touch 80% of all outstanding U.S. shares. The company processing that vote? Not BlackRock. Not the NYSE. Not even the company whose shares are being voted on. It's Broadridge Financial Solutions—a $29.7 billion market cap company that most investors have never heard of, yet couldn't live without.

From its headquarters in Lake Success, New York, Broadridge operates as the invisible circulatory system of modern capital markets. With 14,000 employees spread across the globe and $6.77 billion in trailing twelve-month revenue, this isn't some scrappy fintech startup. It's the monopolistic plumbing of Wall Street—processing proxy votes, distributing shareholder communications, and increasingly, powering the front-office trading systems of the world's largest financial institutions.

Here's the hook that makes this an Acquired-worthy story: How did a back-office division of a payroll processor—yes, a payroll processor—become so essential that Congress itself has acknowledged its near-monopoly position? How did something so boring become so powerful?

The thesis is deceptively simple: Behind every trade execution, every proxy vote cast, and every prospectus delivered lies Broadridge's invisible infrastructure. They've built what might be the most boring monopoly in finance—and that's precisely what makes it brilliant. No sexy consumer app. No viral growth hacks. Just pure, unadulterated infrastructure that financial markets literally cannot function without.

What makes this a great business story isn't just the monopoly position—it's how they got there. Through a masterclass in exploiting regulatory complexity, network effects that compound with every new client, and the strategic genius of being so deeply embedded in workflows that ripping them out would be like performing open-heart surgery on the financial system while it's still beating. This is a story about the power of being boring but essential, of building moats through mundane excellence, and why sometimes the best businesses are the ones nobody wants to compete with because they're just too damn complicated.

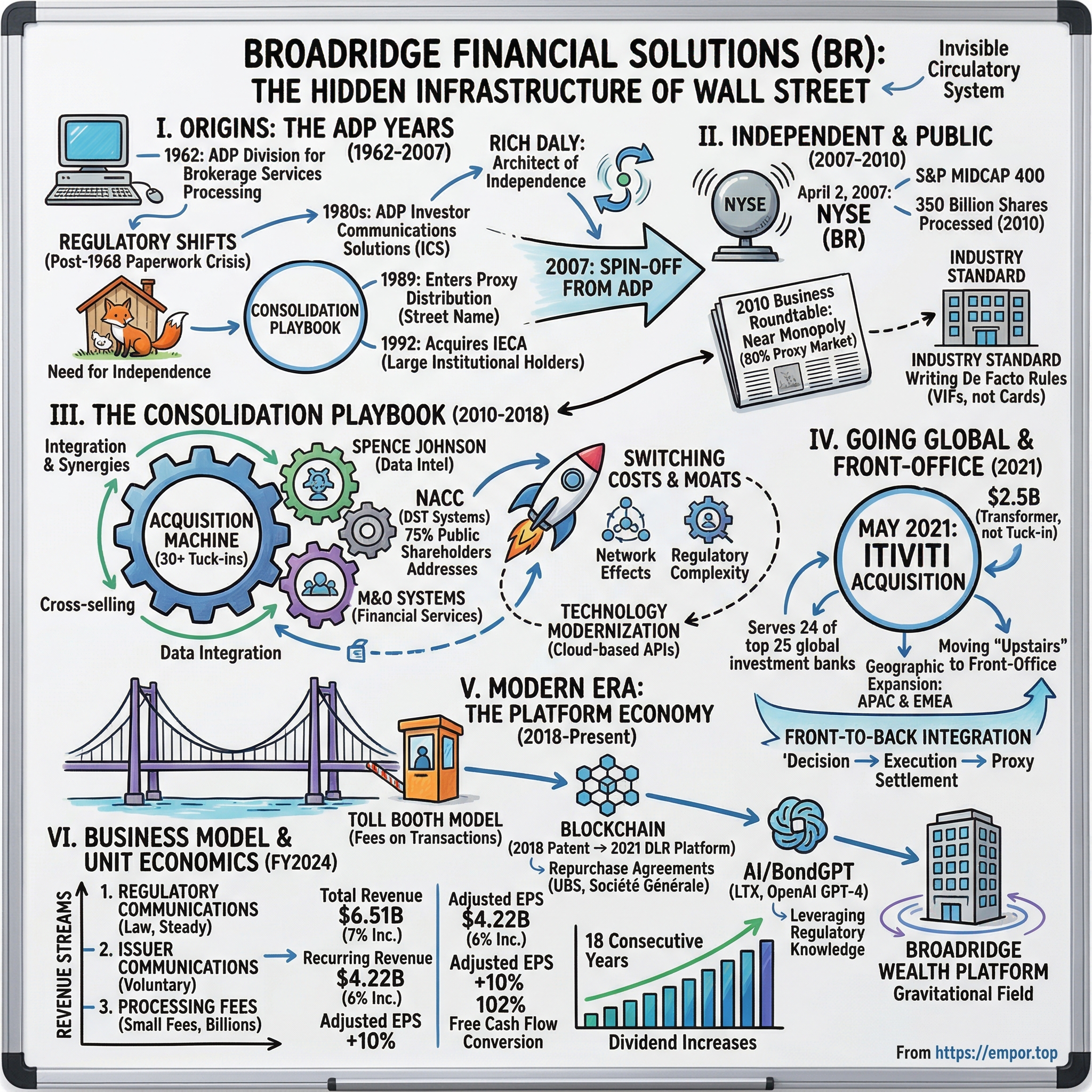

II. Origins: The ADP Years (1962-2007)

The year was 1962, and automatic data processing was still a radical concept. In a small office in New Jersey, a company called Automatic Data Processing—later known as ADP—launched a new division to handle something most people had never heard of: brokerage services processing. Their first client was a single brokerage firm. Their nightly volume? Three hundred trades. That's it. Three hundred trades that would be processed overnight on hulking mainframe computers that cost more than most people's houses.

But here's where the story gets interesting. The 1960s and 70s weren't just about technological change—they were about regulatory transformation. Congress, reacting to various market scandals and the paperwork crisis of 1968 (when trading volumes overwhelmed Wall Street's paper-based systems), began implementing sweeping changes to securities law. These changes did something profound: they created a need for intermediaries between companies and their shareholders.

Before these regulatory shifts, the proxy voting process was simple, if inefficient. Banks and brokers maintained their own in-house proxy departments—rooms full of clerks manually processing voting cards, tallying results, and mailing materials. It was labor-intensive, error-prone, and desperately unscalable. But the new regulations didn't just require accuracy; they demanded speed, audit trails, and most critically, independence. Suddenly, having your broker count your proxy votes was like having the fox count the chickens. Enter Rich Daly, the architect of independence. A veteran of the ADP machine, Daly understood something fundamental: the proxy business wasn't just a service—it was infrastructure. And infrastructure, properly managed, could be more valuable than the conglomerate that housed it. By the 1980s, ADP had created an offering for investor communications business, which served over 30 major clients in its first year, and re-architected the laborious time-consuming proxy process, becoming the largest full-service brokerage processor with approximately 80% of the market.

The consolidation story is remarkable for its methodical ruthlessness. ADP entered the proxy distribution business in 1989, sending out stockholder reports and proxy statements to investors whose stock was held in "street name" by brokerage houses, and then processing the returned proxy votes. Then came the masterstroke: In 1992 ADP acquired another major proxy distribution company, Independent Election Corp. of America. While the ADP service was directed at individual customers of brokerage houses, Independent dealt with large institutional holders.

Think about the genius of this move. They weren't just buying market share—they were buying different client segments and stitching them together into an ecosystem where leaving became increasingly painful. Every acquisition wasn't just additive; it was multiplicative, creating network effects that would make competition not just difficult but economically irrational.

By the mid-1990s, ADP's Brokerage Services Group operated as one of those intermediaries, and by the mid-1990s, Automatic Data Processing dominated the proxy voting and shareholder communications services industry. The monopoly wasn't built through innovation or superior technology—it was built through systematic consolidation of a fragmented industry that nobody else wanted to touch because it was too boring, too complex, and too entangled with regulation. But here's the fascinating wrinkle in this origin story: Rich joined ADP as Senior Vice President of the Brokerage Services Group in 1989, when ADP acquired his Investor Communications Solutions (ICS) business. The man who would lead the spin-off had actually built the original business himself—ICS had two employees when he sold it to ADP in 1989, and today the business, now Broadridge, has over 11,000 associates in 18 countries. Daly wasn't just an executive; he was the founder who had sold his baby to ADP and then stuck around to nurture it within the corporate behemoth.

By the 1990s, Introduces internet proxy voting and digital delivery of shareholder communications and begins processing regulatory mailings and proxies for mutual funds in North America and the UK. The company wasn't just processing paper anymore—they were building the digital rails that would carry the future of shareholder democracy.

The decision to spin off wasn't sudden. By the mid-2000s, ADP's leadership recognized what Daly had long understood: the brokerage services division was fundamentally different from payroll processing. It required different expertise, different relationships, and most importantly, different capital allocation priorities. The proxy business needed massive technology investments that didn't make sense for a payroll processor. The synergies that justified keeping them together in 1989 had become dis-synergies by 2007.

As the spin-off approached, Mr. Daly served as our CEO from 2007 to 2019, and as our President from 2014 to 2017. Prior to the 2007 spin-off of Broadridge from ADP, Mr. Daly served as Group President of the Brokerage Services—positioning himself as the natural leader of the new entity. This wasn't a corporate raider breaking up a conglomerate; this was a founder reclaiming his creation after eighteen years of corporate custody.

The infrastructure they'd built by 2007 was staggering: With over 50 years of experience, Broadridge's infrastructure underpins proxy voting services for over 90% of public companies and mutual funds in North America and processes on average $5 trillion in equity and fixed income trades per day. This wasn't just market dominance—it was market definition. They weren't the biggest player in the proxy processing industry; they essentially were the industry.

III. The Spin-off & Going Public (2007-2010)

Broadridge Financial Solutions, Inc. (NYSE: BR) CEO Rich Daly and COO John Hogan will greet members of the New York Stock Exchange this morning to begin the first trading day of Broadridge as an independent, public company focused on providing services to the financial services industry. Broadridge Financial Solutions, Inc. was officially spun off from Automatic Data Processing, Inc. (NYSE: ADP) on Friday, March 30th. The newly independent company begins trading as a member of the S&P MidCap 400 Index.

April 2, 2007. Rich Daly stands on the floor of the New York Stock Exchange, a bell in his hand, about to ring in not just a new trading day but a new era. The man who had built a two-person company, sold it, and then spent eighteen years growing it within ADP was finally setting it free. The symbolism wasn't lost on anyone watching: Broadridge would now process the very proxy votes that would determine its own corporate governance.

As a result of the spin off, ADP shareholders received one share of Broadridge Financial Solutions, Inc. stock for every four shares of stock they held in ADP on March 23, 2007. Approximately 138.5 million shares of Broadridge stock were distributed on Friday March 30th to ADP shareholders. The mechanics were clean, the execution flawless—exactly what you'd expect from a company whose entire business was built on operational excellence.

But the market's initial reception was... complicated. Here was a company with a near-monopoly position in a critical market function, yet it was boring. Deeply, profoundly, magnificently boring. No consumer brand. No sexy technology story. Just pure infrastructure. The initial market cap was around $2.7 billion—respectable, but hardly earth-shattering for a company processing trillions in trades. "This is a very exciting milestone for Broadridge that exemplifies our commitment to pursue continued growth and build value for our shareholders and clients," said Broadridge CEO, Rich Daly. "As an independent company focused on providing solutions to the financial services industry, we believe Broadridge is well positioned to execute strategic initiatives specific to our business needs, provide expanded solutions for our clients and increase oppor[tunities]."

What Daly didn't say—but what everyone in the industry understood—was that independence meant freedom from ADP's conservative capital allocation framework. Broadridge could now invest aggressively in technology modernization, pursue acquisitions without justifying them to a payroll-focused board, and most importantly, build the relationships with regulators that would cement their position as essential infrastructure.

By 2010, the scale of their dominance was becoming undeniable. The company had a near monopoly by processing 350 billion shares for companies under its client portfolio. Think about that number for a moment. Three hundred and fifty billion shares. Every one of those shares representing a piece of ownership in American capitalism, and virtually all of them flowing through Broadridge's systems.

In 2010 a report submitted to the House Committee on Financial Services by a coalition headed by Business Roundtable noted the near monopoly position of Broadridge in handling proxy voting. This wasn't some fringe activist group complaining—this was the Business Roundtable, the CEOs of America's largest corporations, essentially admitting that a single company controlled the mechanism by which their shareholders exercised control.

The regulatory scrutiny could have been devastating. But Broadridge had built something more powerful than a monopoly—they'd built infrastructure so complex, so deeply embedded, that even Congress couldn't figure out how to unwind it. But good monopolies are regulated monopolies, and Broadridge isn't regulated. Whenever the SEC updates rules governing the proxy process, they usually have to ask Broadridge how things are actually done.

The early strategic decisions during this period were crucial. Rather than chase growth through flashy new products or international expansion, Broadridge doubled down on what they did best: boring excellence. They focused on scale—making their systems handle more volume at lower marginal cost. They invested in technology—not bleeding-edge innovation, but the kind of steady modernization that keeps critical infrastructure running smoothly. And most importantly, they focused on client retention—because in a business with switching costs this high, keeping a client was worth ten times more than acquiring a new one.

By choosing how to do things, Broadridge makes de facto rules. A perfect example is Voting Instruction Form (VIFs). These look and feel like proxy cards, but they are not. Broadridge mails out VIFs with shareowners' proxy materials in lieu of proxy cards. The way Broadridge explains it, shareowners fill out VIFs to indicate how they want their proxies voted, which is not the same thing as filling out a proxy.

This wasn't just market power—it was market definition. Broadridge wasn't playing by the rules; they were writing them through the simple act of implementation. Every decision about how to process a vote, how to format a document, how to route a communication became industry standard simply because Broadridge did it that way.

The competitive moats being built during this period were extraordinary. Network effects meant that every new client made the system more valuable for existing clients. Regulatory complexity meant that potential competitors would need years just to understand the requirements, let alone build systems to meet them. And the switching costs—oh, the switching costs. Imagine trying to change the plumbing in your house while the water is still running. Now imagine that house is the entire U.S. financial system.

IV. The Consolidation Playbook (2010-2018)

The acquisition machine that Broadridge became after independence wasn't born from opportunism—it was architected with the precision of a chess grandmaster playing thirty moves ahead. According to analysts at Evercore ISI, "Broadridge has a long history of successful tuck-in acquisitions," and between 2007 and 2018, the company made over 30 acquisitions in total. Thirty acquisitions in eleven years. That's nearly three per year, each one carefully selected not for immediate revenue impact but for how it strengthened the overall ecosystem.

The playbook was deceptively simple but brutally effective. Find a company doing something adjacent to your core business. Something that your clients need but you don't currently provide. Buy it. Integrate it so deeply into your existing platform that clients can't tell where one service ends and another begins. Extract synergies not just through cost-cutting but through cross-selling and data sharing. Rinse. Repeat.

2016 was the year this strategy reached its apex. First came Spence Johnson, an institutional financial flow data intelligence firm. On its own, Spence Johnson was a nice little business—providing data and analytics to institutional investors. But in Broadridge's hands, it became something more. Now they didn't just process trades and proxy votes; they could tell clients what those trades and votes meant, how they compared to peers, what trends were emerging. Data became intelligence, and intelligence became stickiness.

Broadridge acquired the North America Customer Communications (NACC) unit of DST Systems, a business services provider, which provided the company with addressing information for about 75% of all public company shareholders in the United States and Canada. Stop and think about what that means. Three-quarters of all public company shareholders in North America. Broadridge didn't just know how to reach them—they were the only ones who knew how to reach them at scale.

Later in 2016, Broadridge bought M&O Systems, a small Manhattan-based financial services company. M&O wasn't flashy. It wasn't transformational. But it filled a gap, added capabilities, and most importantly, removed a potential competitor from the board. This was the genius of the consolidation playbook—every acquisition served multiple purposes.

The integration story is where Broadridge truly distinguished itself from typical serial acquirers. Most companies struggle to integrate one major acquisition. Broadridge was integrating three a year, and making it look easy. How? By having a system. A repeatable, scalable process for taking a standalone company and weaving it into the Broadridge fabric so thoroughly that within eighteen months, even the original founders couldn't extract it.

First, they'd identify the overlaps—where the acquired company's capabilities duplicated Broadridge's existing services. Those got rationalized quickly, usually keeping the better technology or process regardless of which company it came from. Then came the cross-selling opportunities—introducing the acquired company's products to Broadridge's massive client base and vice versa. Finally, and most powerfully, came the data integration. Every new acquisition brought new data streams, new insights, new ways to make the overall platform more valuable.

In a 2018 letter to the SEC, Broadridge stated its mailings reached 140 million investor accounts. By 2018, that number had grown from the already-staggering figures of 2010. They weren't just growing; they were approaching total market saturation. There were only so many investor accounts in North America, and Broadridge was reaching nearly all of them.

The technology modernization happening during this period was less visible but equally important. Broadridge was quietly moving from legacy mainframe systems—some dating back to the ADP days—to modern, cloud-based architectures. But they did it carefully, methodically, never risking the stability of the core platform. It was like performing engine maintenance on a plane while it was flying—except the plane was carrying the entire U.S. financial system.

APIs became the new frontier. Instead of just processing transactions, Broadridge began offering ways for clients to integrate directly with their systems. This created an even deeper lock-in. Once a bank or broker had built their own systems to talk directly to Broadridge's APIs, switching providers didn't just mean changing vendors—it meant rewriting code, retesting systems, retraining staff. The switching costs went from high to astronomical.

The expansion of the moat during this period was remarkable. Each acquisition didn't just add revenue; it added a new dimension to the competitive barriers. Data companies provided intelligence moats. Communication companies provided reach moats. Technology companies provided integration moats. By 2018, competing with Broadridge didn't mean building one business—it meant building thirty businesses and somehow making them work together as seamlessly as Broadridge had.

2019 - Broadridge acquired ClearStructure Financial Technology, which provides portfolio management solutions. 2020 - Broadridge acquired FundsLibrary, which specializes in fund document and data dissemination. Even as the decade closed, the acquisition machine kept humming, each deal adding another layer to an already impenetrable fortress.

V. The Itiviti Acquisition: Going Global & Front-Office (2021)

May 2021. The financial world was still reeling from the GameStop saga, questioning the very infrastructure of trading. Into this moment of uncertainty, Broadridge dropped a bombshell: Broadridge acquired Itiviti, a capital markets trading technology provider. The company agreed in 2021 to acquire the Sweden-based Itiviti from Nordic Capital for $2.5 billion.

Two and a half billion dollars. For context, that was more than Broadridge had spent on all its previous acquisitions combined. This wasn't a tuck-in. This wasn't filling a gap. This was transformation.

To understand why Itiviti mattered, you need to understand the division between front-office and back-office in financial services. Broadridge had conquered the back-office—the boring, essential stuff that happens after trades are made. But the front-office—where trades actually happen, where decisions get made, where the money gets allocated—that was foreign territory. Itiviti was their beachhead. With offices in 16 countries, Itiviti serves 24 of the top 25 global investment banks and over 2,000 leading brokers, trading firms and asset managers across 50 countries. Read that again. Twenty-four of the top twenty-five global investment banks. The only question worth asking: who was the holdout, and how long before they capitulated?

Itiviti's solutions and services provide financial institutions with comprehensive tools for connectivity and flexible, cross-asset trading solutions that cover the full trade lifecycle. This wasn't just about adding capabilities—it was about changing Broadridge's entire strategic position. They were no longer the plumbing hidden in the basement; they were moving upstairs to where the decisions got made.

The strategic rationale was compelling on multiple levels. First, the front-to-back integration opportunity. Imagine being able to track a trade from the moment a portfolio manager decides to buy, through execution, settlement, proxy voting, and eventually corporate actions. That's not just efficiency—that's intelligence. Every step generates data, and when you control every step, you control all the data.

Second, the geographic expansion. The addition of Itiviti's footprint in APAC and EMEA also increases Broadridge's scale outside of North America to better serve global clients. Broadridge had been overwhelmingly North American. Itiviti gave them instant credibility and infrastructure in Europe and Asia—markets where American financial infrastructure companies had historically struggled to penetrate.

But perhaps most importantly, this was about relevance. The financial services industry was undergoing massive transformation—AI, blockchain, digital assets. The back-office wasn't where innovation was happening; it was in the front-office, in trading systems, in execution algorithms. By acquiring Itiviti, Broadridge bought themselves a seat at the innovation table.

The integration challenges were immense. Itiviti's culture was Nordic—collaborative, consensus-driven, engineering-focused. Broadridge's culture was New York—aggressive, sales-driven, financially engineered. Itiviti will become part of Broadridge's Global Technology and Operations segment and its senior management team, led by CEO Rob Mackay, will remain with the company to drive future growth. The decision to keep Itiviti's management team wasn't just smart—it was essential. You can't integrate what you don't understand, and Broadridge's leadership had the wisdom to recognize that.

The acquisition of Itiviti is expected to be accretive to Adjusted EPS in the first full year after closing and generate attractive financial returns for Broadridge's shareholders. The financial engineering was typically elegant. In addition, the acquisition is expected to contribute 2.5-3 points to Broadridge's recurring revenue compound annual growth rate ("CAGR") and 2 points to its Adjusted EPS CAGR over the fiscal year 2020-2023 time period.

The transformation this represented cannot be overstated. Broadridge was no longer just an infrastructure provider—they were becoming what Tim Gokey called "a leading front-to-back capital markets technology and operations provider." From proxy votes to trade execution, from shareholder communications to market connectivity, they were building an end-to-end platform that touched every aspect of the financial markets.

VI. Modern Era: The Platform Economy (2018-Present)

The pandemic didn't create the need for digital transformation in financial services—it just compressed a decade of change into eighteen months. For Broadridge, Covid wasn't a crisis; it was an accelerant. Virtual annual meetings went from curiosity to necessity overnight. Digital proxy voting went from nice-to-have to must-have. And Broadridge, having spent years building the infrastructure, was ready. The blockchain story is particularly instructive about how Broadridge approaches innovation. In 2018, they announced that the U.S. Patent and Trademark Office granted U.S. Patent No. 9,967,238 (the "'238 Patent") directed to blockchain technology that will enhance the processes for proxy voting and repurchase, or repo, agreements. But this wasn't blockchain for blockchain's sake—this was blockchain as a tool to solve real problems.

By 2021, Broadridge announced the successful go-live of its transformative distributed ledger repo (DLR) platform. Leveraging Broadridge's leading fixed income trade processing platform, DLR utilizes Daml smart contracts from Digital Asset as well as VMware Blockchain, a highly scalable distributed ledger platform. The platform wasn't revolutionary—it was evolutionary, taking existing processes and making them incrementally better.

After Broadridge began testing the use of blockchain for proxy voting in 2018, by 2023, companies such as UBS and Société Générale were using Broadridge's VMWare Blockchain distributed ledger software to facilitate repurchase agreements. Notice the timeline: five years from testing to major bank adoption. That's not Silicon Valley speed, but for infrastructure that handles trillions in transactions, that's actually remarkably fast. The AI story reached its next chapter in June 2023, when LTX, a corporate bond trading platform owned by Broadridge, launched BondGPT, a chatbot focused on bonds and utilizing OpenAI's GPT-4. BondGPT combines the power of GPT-4 with LTX's patent-pending analytics and comprehensive underlying dataset for data timeliness, accuracy and compliance in a highly regulated financial services sector, avoiding hallucination issues common in other implementations.

This wasn't Broadridge jumping on the AI bandwagon—this was strategic positioning. BondGPT is the first of many products and services Broadridge will release to our clients using this powerful technology in a safe manner, leveraging our deep regulatory knowledge and data privacy standards. The key phrase there: "in a safe manner." While Silicon Valley was moving fast and breaking things with AI, Broadridge was moving deliberately and breaking nothing.

The platform economy that Broadridge has built isn't just about technology—it's about ecosystem dominance. In 2023 Broadridge stated it had around 1,100 clients who were brokers, and that it provided proxy services for around 80% of outstanding shares in the United States. Every one of those clients represents not just revenue but a node in a network that becomes more valuable with every connection. The Kyndryl acquisition in 2024 shows that the acquisition machine continues to hum. Global Fintech leader Broadridge Financial Solutions, Inc. (NYSE:BR) has completed its previously announced acquisition of Kyndryl's Securities Industry Services (SIS) platform, which provides wealth management and capital markets software solutions to Canadian financial services firms. The transaction is not expected to have a material impact on Broadridge's financial results—in other words, it's a tuck-in, a gap-filler, another brick in the wall.

The modern era of Broadridge is defined by platform thinking. They're not selling products anymore; they're selling ecosystems. The Broadridge Wealth Platform isn't just software—it's a gravitational field that pulls in clients, partners, and competitors alike. Once you're in the ecosystem, leaving becomes not just difficult but irrational.

Virtual annual meetings, once a novelty, have become a profit center. Digital communications that were once cost centers have become revenue generators. And throughout it all, Broadridge maintains its monopolistic grip on the proxy voting infrastructure that makes corporate democracy possible—or at least, makes it function.

VII. Business Model & Unit Economics

To understand Broadridge's business model, imagine running a toll booth on the only bridge between Manhattan and the rest of the world. Now imagine that bridge carries not cars but every piece of financial information, every proxy vote, every trade confirmation. That's Broadridge. They don't create the traffic—they just make sure it gets where it needs to go. And they collect a toll on every single transaction.

The company operates through two segments, each with distinct economics but complementary dynamics. Investor Communication Solutions (ICS) is the cash cow—steady, predictable, regulated, and virtually monopolistic. Global Technology and Operations (GTO) is the growth engine—more competitive but also more dynamic, with higher margins and greater expansion potential. The numbers tell a story of relentless consistency. FY2024: Total revenue reaching $6.51 billion in 2024. This marks a 7% increase compared to $6.06 billion in 2023. A significant portion of this growth comes from recurring revenues, which rose by 6% to $4.22 billion. That recurring revenue number is the key—it's the foundation that allows Broadridge to invest, acquire, and return capital to shareholders with confidence.

The beauty of the recurring revenue model cannot be overstated. 6% Recurring revenue growth, 10% Adjusted EPS growth, and Free cash flow conversion of 102%. That 102% free cash flow conversion is particularly remarkable—they're generating more cash than their reported earnings, a sign of a business with minimal capital intensity and maximum efficiency.

The ICS segment generates revenue through three primary streams. First, regulatory communications—the stuff companies have to send to shareholders by law. This is as close to guaranteed revenue as you can get in business. Second, issuer communications—the voluntary stuff companies want to send. And third, the processing fees for all of it. Every proxy vote, every annual report, every trade confirmation generates a small fee. Small fees, billions of transactions, massive revenue.

GTO operates on a different model—more competitive but also more lucrative. This is where the technology platforms live, where the Itiviti acquisition plays out, where the future growth comes from. The margins here are higher because once you've built the platform, the marginal cost of adding another client approaches zero.

Event-driven revenues also contributed strongly, climbing 35% to $285 million, largely driven by increased corporate action communications and mutual fund proxy activity. This is the cherry on top—unpredictable but highly profitable revenue that comes from contested proxy fights, special situations, and market volatility. When activist investors attack, when companies merge, when markets get volatile, Broadridge makes money.

The operating leverage in this business is extraordinary. Adjusted Operating income margin was 16.6%—and that's with significant ongoing technology investments. As the business scales, as more volume flows through the same infrastructure, those margins expand naturally. Every additional proxy vote, every additional trade, every additional communication flows through systems that are already built, already running, already paid for. The capital allocation story is where the financial engineering meets strategic discipline. In fiscal year 2024, we repurchased $450 million of our shares and announced three tuck-in acquisitions. I am also pleased to report that our Board has approved a 10% increase in our annual dividend to $3.52, marking the 12th double-digit increase in the past thirteen years.

This isn't just returning capital—it's a statement of confidence. With this increase, the Company's annual dividend has increased for the 18th consecutive year since becoming a public company in 2007. Eighteen consecutive years. Through the financial crisis, through Covid, through every market cycle, Broadridge has increased its dividend.

The balance is remarkable. $450 million in share repurchases while still pursuing acquisitions, while still investing in technology, while still increasing the dividend. This is what happens when you have a business that generates cash like a machine—you can do everything at once without compromising anything.

VIII. Competitive Dynamics & Market Position

The monopoly question isn't whether Broadridge has one—it's why nobody can do anything about it. Controlling ~80% of US proxy voting market—that's not market leadership; that's market ownership. But here's the fascinating part: everyone knows it, including Congress, and yet the monopoly persists. Why?

The answer lies in the nature of infrastructure monopolies. You could theoretically compete with Broadridge. All you'd need is a few billion dollars, a decade to build the technology, relationships with every broker-dealer in America, regulatory approval from multiple agencies, and the trust of the entire financial system. Oh, and you'd need to convince thousands of financial institutions to simultaneously switch from a system that works perfectly to your unproven alternative. Good luck with that.

The regulatory scrutiny has been ongoing for years, but it's toothless. Regulators understand that Broadridge's monopoly isn't the result of anti-competitive behavior—it's the result of being the only company willing and able to do an incredibly complex, boring, essential job. Breaking up Broadridge wouldn't create competition; it would create chaos.

The international expansion challenges are real but surmountable. Every country has different regulations, different market structures, different languages, different everything. But that's where acquisitions like Itiviti come in—buying your way into new markets with established players who already understand the local complexity.

The fintech disruption question is the most interesting. Could blockchain eliminate the need for Broadridge? Could AI make their services obsolete? The answer, surprisingly, is that Broadridge is more likely to be the disruptor than the disrupted. They have the client relationships, the regulatory knowledge, and increasingly, the technology itself. When blockchain comes to proxy voting, it will probably be Broadridge's blockchain. When AI transforms financial communications, it will probably be Broadridge's AI.

The client concentration risk is worth noting. Serving the biggest financial institutions means that losing even one client would be material. But it also means that those clients are so deeply integrated with Broadridge's systems that leaving would be like performing surgery on themselves. The switching costs aren't just high—they're prohibitive.

Competition analysis reveals a fascinating dynamic: there essentially isn't any. Not because competitors don't exist, but because they exist in different universes. FIS, Fiserv, and others compete in pieces of what Broadridge does, but nobody competes with the whole. It's like saying McDonald's competes with a Michelin-starred restaurant because they both serve food.

IX. Leadership & Culture

The transition from Rich Daly to Tim Gokey in 2019 was a masterclass in succession planning. On January 2, 2019, Tim Gokey succeeded Rich Daly as chief executive officer, with Daly becoming Executive Chairman. This wasn't a palace coup or a board-driven change—this was a founder handing over the keys to a carefully groomed successor while staying around to ensure continuity.

Gokey's background is instructive. He joined Broadridge in 2010 to lead the Company's growth initiatives. He was named Chief Operating Officer in 2012 and President in August 2017. Prior to joining Broadridge, Mr. Gokey was President of the Retail Tax business at H&R Block, where he had a strong record of innovation and profitable growth. Previously, he spent 13 years at McKinsey and Company, where he led McKinsey's North American Financial Services Sales and Marketing Practice.

The McKinsey-to-operations pipeline is well-worn in corporate America, but Gokey represents the best of it. Strategic thinking combined with operational excellence. The ability to see the forest and the trees simultaneously. Under his leadership, Broadridge hasn't just continued Daly's legacy—it's accelerated it.

The culture at Broadridge is fascinatingly paradoxical. On one hand, it's a company built on boring excellence—doing the essential, unglamorous work that makes financial markets function. On the other hand, it's aggressively innovative, constantly pushing into new technologies and markets. The key is that the innovation serves the boring excellence, not the other way around.

Building a culture of "boring excellence" sounds like an oxymoron, but it's Broadridge's superpower. They've somehow made infrastructure sexy to their employees. They've convinced top talent that building the plumbing of financial markets is not just important but exciting. That's not easy in an era where every engineer wants to work on consumer apps or AI startups.

Innovation within constraints is how Broadridge approaches technology. They can't move fast and break things—breaking things when you're processing trillions in securities would be catastrophic. So they innovate carefully, methodically, always with one eye on stability and another on the future.

The talent challenge is real and growing. Competing for tech talent against Silicon Valley giants with their stock options and ping-pong tables isn't easy when your main selling point is "we process proxy votes." But Broadridge has found its niche—engineers who value stability, who appreciate working on systems that matter, who find beauty in complexity and scale.

Chris Perry as President represents the next generation of leadership, already being groomed for eventual succession. The board composition—mixing financial services veterans with technology experts—reflects the dual nature of the business.

X. Financial Analysis & Valuation

The numbers tell a story of relentless execution. FY2024: Closed sales rose 39% to $342 million—not just growth, but accelerating growth. This isn't a mature business coasting on its monopoly; it's a growth company that happens to have monopolistic characteristics.

The capital allocation framework is a thing of beauty. $450M share repurchases in FY2024; 10% dividend increase to $3.52 (12th double-digit increase in 13 years). This is having your cake and eating it too—returning massive amounts of capital while still investing for growth.

FY2025 guidance: 5-7% recurring revenue growth constant currency, 8-12% Adjusted EPS growth. These aren't shoot-the-moon targets; they're conservative guidance from a management team that consistently under-promises and over-delivers. The fact that they're guiding to 8-12% EPS growth on 5-7% revenue growth tells you everything about the operating leverage in this business.

The valuation framework for Broadridge is complex because it sits at the intersection of multiple categories. Is it a financial services company? A technology company? An infrastructure play? The answer is yes to all three, which makes traditional multiples challenging.

Trading at roughly 25-30x forward earnings (depending on when you're reading this), Broadridge commands a premium to traditional financial services but a discount to high-growth software. That feels about right for a company growing steadily with monopolistic characteristics but without the explosive growth of a true tech disruptor.

The bear case centers on three main risks. First, disruption from blockchain or other technologies that could eliminate the need for intermediaries. Second, client loss—even one major client departure would be material. Third, regulatory changes that could force unbundling or price controls. Each of these is possible but unlikely, and even less likely to happen quickly enough to prevent Broadridge from adapting.

The bull case is more compelling. Continued consolidation in financial services creates more need for Broadridge's services. International expansion opens massive new markets. New products like BondGPT show they can innovate beyond their core. And the secular trend toward passive investing actually increases the importance of proxy voting infrastructure.

Comparison to other financial infrastructure plays shows Broadridge in a unique position. Unlike pure processors like FIS or Fiserv, Broadridge has regulatory moats. Unlike exchanges like ICE or CME, Broadridge doesn't face direct competition. It's almost like a utility, but one that's still growing.

XI. Playbook: Lessons for Builders & Investors

The Broadridge story offers a masterclass in building monopolistic businesses in regulated industries. The first lesson: embrace the boring. The most valuable businesses are often the least glamorous. Nobody dreams of processing proxy votes, but somebody has to do it, and whoever does it well can build an empire.

Building monopolies through regulatory complexity is an art form Broadridge has perfected. They didn't capture the market and then get regulated; they grew because of regulation. Every new rule, every additional requirement, every compliance burden makes it harder for competitors to enter and easier for Broadridge to extend its lead.

The roll-up strategy in fragmented, regulated markets is replicable across industries. Find a market with hundreds of small players, complex regulations, and high switching costs. Buy the best ones. Integrate them deeply. Extract synergies. Repeat. It's not sexy, but it works.

Network effects in B2B are different from consumer but equally powerful. Every new client makes Broadridge more valuable to existing clients. Every new service makes switching harder. Every new integration makes the network stronger. It's not the viral growth of social media, but it's more durable.

The importance of patient capital and long-term thinking cannot be overstated. Broadridge spent decades building its monopoly. They didn't flip it to private equity. They didn't chase quarterly earnings. They built for the long term, and the long term paid off.

Knowing when to go from organic growth to acquisition mode is crucial. Broadridge grew organically when they were building the core platform. They turned to acquisitions when they needed to expand the moat. The timing wasn't random—it was strategic.

Managing technology transitions in mission-critical systems requires a different mindset than Silicon Valley innovation. You can't just deprecate old systems. You have to run parallel systems, migrate carefully, test exhaustively. It's expensive and slow, but it's the only way when failure isn't an option.

The value of high switching costs and embedded workflows is often underestimated. Every system that integrates with Broadridge, every workflow that depends on their data, every process that assumes their presence—each one is a hook that makes leaving harder. Building these hooks deliberately is a strategic imperative.

XII. Power & Grading

Applying Hamilton Helmer's Seven Powers framework to Broadridge reveals a company with multiple, reinforcing moats.

Scale economies: Absolutely. The marginal cost of processing additional transactions approaches zero. Every new client makes the economics better for everyone.

Network effects: Check, but subtle. This isn't Facebook where users attract users. It's a B2B network where standardization creates value. The more participants use Broadridge, the more valuable standardization becomes.

Switching costs: Astronomical. We're not talking about learning new software. We're talking about rewiring the entire operational infrastructure of a financial institution. The switching costs aren't just financial—they're existential.

Regulatory capture: Partial check. Broadridge doesn't write the regulations, but they effectively define how regulations are implemented. When the SEC needs to understand how proxy voting actually works, they ask Broadridge.

What power does Broadridge truly have? The power to be boring but essential. The power to be so embedded in the financial system that removing them would be like removing the foundation of a building—theoretically possible but practically catastrophic.

Grading the business across dimensions:

Execution: A+. Consistent delivery, successful integrations, operational excellence.

Strategy: A. The Itiviti acquisition was brilliant. The platform strategy is working. The international expansion is proceeding.

Capital allocation: A. Balanced approach, consistent returns to shareholders, strategic acquisitions.

The ultimate question: Is this a forever business? In its current form, probably not—technology and regulations will eventually force evolution. But as an essential function that someone needs to provide? Absolutely. And Broadridge is positioned better than anyone to evolve with the market while maintaining its dominance.

XIII. Looking Forward & Epilogue

The next decade for Broadridge will be defined by three mega-trends: AI integration, blockchain adoption, and infrastructure modernization. Each represents both opportunity and threat, but Broadridge's track record suggests they'll navigate all three successfully.

AI isn't just about BondGPT—it's about using machine learning to make every process more efficient, every communication more targeted, every service more valuable. Broadridge has the data advantage here. Decades of transaction data, voting patterns, communication responses—it's a treasure trove that competitors can't replicate.

Blockchain will eventually transform proxy voting and settlement, but it won't eliminate the need for Broadridge—it will change what Broadridge does. Someone still needs to manage the blockchain, ensure compliance, handle exceptions. Broadridge is positioning itself to be that someone.

Infrastructure modernization is the biggest opportunity. Financial services firms are desperate to modernize but terrified of risk. Broadridge offers modernization without migration—new capabilities built on proven infrastructure. It's the perfect pitch for risk-averse financial institutions.

Expansion opportunities abound. International markets are still fragmented and inefficient. Adjacent verticals like insurance and healthcare have similar infrastructure needs. The Broadridge playbook could work in any regulated, complex, fragmented market.

The biggest risks are also the most unlikely. Regulatory changes that force unbundling would require political will that doesn't exist. Technology disruption would require someone to build a better mousetrap and convince everyone to switch simultaneously. Concentration risk is real but manageable through deep integration and excellent service.

If we were running Broadridge, the strategic priorities would be clear. First, accelerate international expansion through targeted acquisitions. Second, build the AI and blockchain capabilities that will define the next generation of financial infrastructure. Third, expand into adjacent markets that have similar characteristics to financial services.

The final reflection on building essential infrastructure businesses: they're not glamorous, they're not exciting, and they're not easy. But they're valuable, durable, and defensible. In a world obsessed with disruption, there's something beautiful about a business that just keeps working, keeps growing, keeps generating cash.

Broadridge isn't trying to change the world. They're trying to make sure the world's financial markets keep functioning. And in doing so, they've built one of the most powerful, profitable, and underappreciated businesses in the market. That's the Broadridge paradox: boring is beautiful, infrastructure is invaluable, and sometimes the best business is the one nobody else wants to build.

The story of Broadridge is ultimately a story about the power of compound advantages. Each year, the moat gets a little wider. Each acquisition makes the network a little stronger. Each innovation makes switching a little harder. It's not dramatic, but it's inexorable. And for long-term investors, inexorable beats dramatic every time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube