Piramal Enterprises: The Master of Capital Recycling

I. Introduction & Episode Roadmap

Picture this scene: Mumbai's Nariman Point, the heart of India's financial district, on a humid September morning in 2021. Ajay Piramal had just concluded the acquisition of Dewan Housing Finance Corporation (DHFL) under the Insolvency and Bankruptcy Code (IBC)—the first successful resolution under the IBC route in the financial services sector. The deal size? Approximately Rs 34,250 crore at the completion of the acquisition, including an upfront cash component of approximately Rs 14,700 crore and issuance of debt instruments of approximately Rs 19,550 crore.

Most businessmen would have balked at buying a scandal-ridden, bankrupt lender. But for Ajay Piramal, this was just another Tuesday—another masterclass in the art of buying distressed, building value, and sometimes, selling at astronomical premiums. This is the story of how a textile mill owner's son became India's dealmaking legend by perfecting the art of capital recycling.

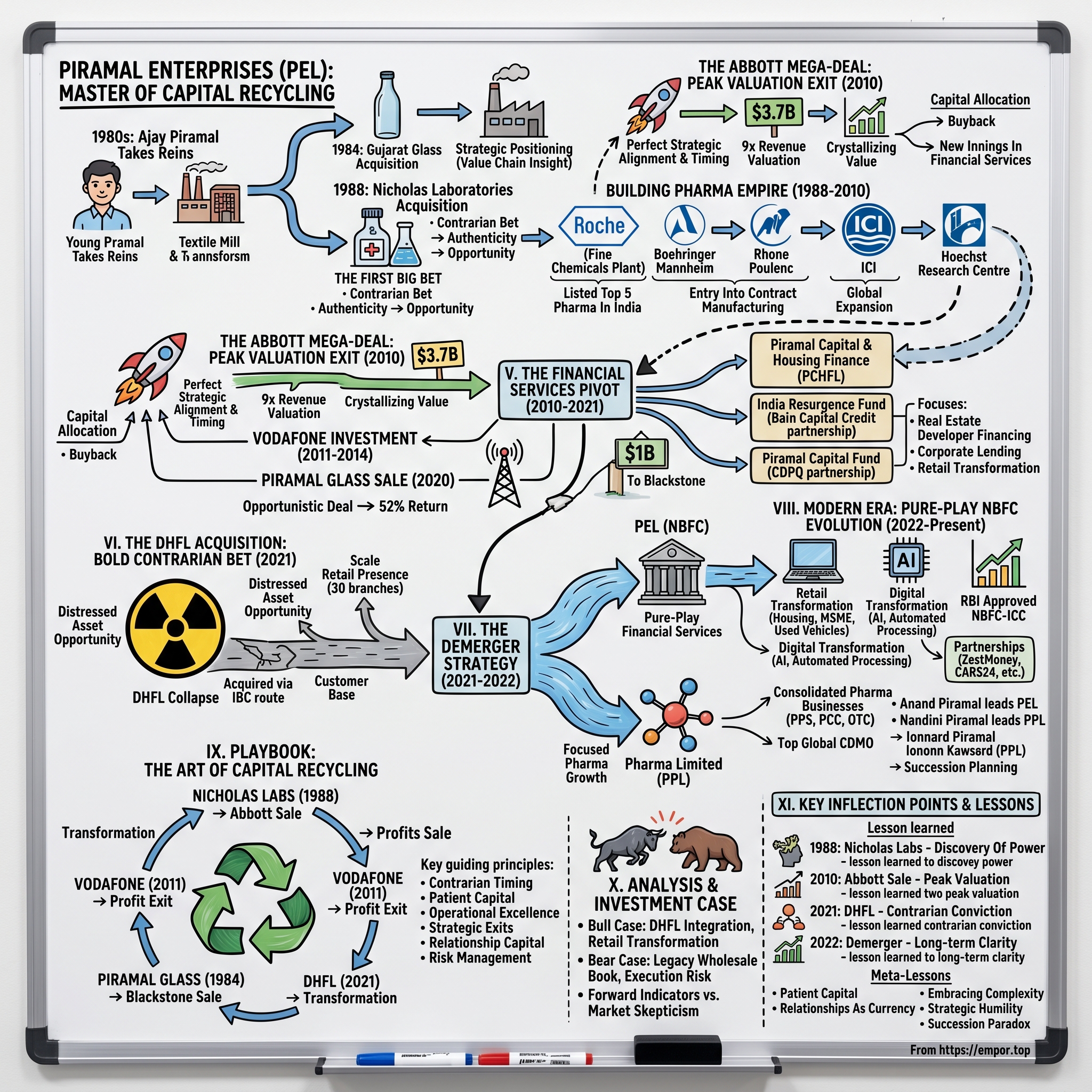

The company's journey reads like a financial thriller: In the early 1980s, Ajay Piramal took over the reins of Piramal Group. In 1984, the group acquired Gujarat Glass Limited (later renamed as Piramal Glass), a manufacturer of glass packaging for pharmaceutical and cosmetic products. In 1988, the group bought Nicholas Laboratories, which later flourished and by 2010 reached the highest valuation in the pharmaceutical industry.

What makes Piramal Enterprises unique isn't just the deals themselves—it's the timing. Selling the pharma business to Abbott for $3.7 billion in 2010. Buying 11% in Vodafone Essar in 2011–12, then selling its 11% Stake in Vodafone India to Prime Metals, an indirect subsidiary of Vodafone Group in 2014. In 2020, The Blackstone Group announced that it would acquire Piramal Glass for US$1 billion. After the acquisition was completed in March 2021, the company was renamed to PGP Glass.

This episode unpacks how Piramal Enterprises transformed from a textile business into India's most dramatic corporate shapeshifter—pharma giant, financial services powerhouse, and now, one of India's leading NBFCs. It's a story of strategic pivots, contrarian bets, and the relentless pursuit of value creation in emerging India.

II. Origins: From Textiles to the First Big Bet (1980s-1988)

The Piramal story begins not with fanfare, but with tragedy. Ajay Piramal was born to Gopikisan Piramal and Lalita Piramal in Rajasthan, India on 3 August 1955. In 1977, at age 22, Piramal started out in his family's textile business, founded in 1934 by his grandfather Piramal Chatrabhuj. His father, Gopikisan Piramal, died in 1979, and after five years he lost an older brother to cancer, prompting him to take over the business.

Imagine being thrust into leadership at 24, your father gone, your brother lost to cancer, and you're staring at a traditional textile business in an India that's rapidly modernizing. Most would have played it safe. Ajay Piramal did the opposite.

Ajay Piramal joined the family business in the late 1970s after the sudden demise of his father. Initially involved in textiles, he quickly demonstrated leadership by taking charge of the group during a time of crisis and steering it toward stability and growth. But textiles weren't the future he envisioned.

The first hint of Piramal's acquisition DNA came in 1984. This drive of theirs was initiated with the acquisition of Gujarat Glass Limited. The company used to manufacture glass packaging for pharmaceutical and cosmetic products. While into it, he had understood that the next boom that will happen in India would be in the pharmaceutical industry. This wasn't just an acquisition—it was strategic positioning. Glass packaging for pharma products? That's understanding the value chain before entering the main game.

Then came the moment that would define everything: Nicholas Laboratories. In 1988, Ajay had heard from a friend that an Australian MNC called Nicholas Laboratories, was planning to exit from India and was intending to sell his company here. Obviously, there were many bidders that too from the industry, but nevertheless, Ajay decided to meet the man in-charge of the sale – Mike Barker.

The negotiation itself was pure Piramal—brutally honest and disarmingly confident. Very bluntly, he told him that he was just 33 years of age, didn't belong to this industry and did not have any track record to show him as well. Who walks into a pharma acquisition meeting and leads with their weaknesses? Someone who understands that authenticity can be more powerful than any pitch deck.

But Ajay also strongly believed that – "the best acquisitions are the ones where you find, that there are some issues which others cannot solve, but you can"! This philosophy would guide every major deal for the next four decades.

As a matter of fact while the deal was in process, Nicholas Labs themselves seemed very scared of some excise or contingent liabilities which they had found in an agreement that they had done with another multinational. But when Ajay evaluated them, he realized that those liabilities barely had any chances of occurring. While others saw risk, Piramal saw mispriced opportunity—a pattern that would repeat throughout the company's history.

III. Building the Pharma Empire (1988-2010)

The Nicholas Laboratories acquisition in 1988 wasn't just a deal—it was the beginning of an empire built through strategic M&A. In 1988, he made a landmark acquisition by purchasing Nicholas Laboratories, a small pharmaceutical company. This marked the beginning of Piramal's foray into healthcare, a bold move that transformed the company's identity and set the stage for global expansion in the pharmaceutical space. This acquisition became the foundation for one of India's most successful pharma businesses.

What followed was a masterclass in consolidation. Anyways, soon after the acquisition of Nicholas Laboratories, under this banner itself, the company went on a spree of acquisitions like the Indian subsidiaries of Roche, Boehringer Mannheim, Rhone Poulenc, ICI and Hoechst Research Centre which eventually grew the company to become listed amongst the top five pharmaceutical companies in India.

The Roche acquisition in 1993 was particularly significant. In November 1993, Swiss drug multinational Hoffmann-La Roche sold its Indian subsidiary, Roche Products (India) Ltd to Piramal Enterprises, including its assets like the Vitamin-A producing Fine Chemicals Plant in Balkum. This wasn't just buying a business—it was acquiring sophisticated manufacturing capabilities and formulations that would typically take decades to develop organically.

The pattern was clear: multinational pharma companies exiting India or restructuring their operations found a willing buyer in Piramal. Each acquisition brought something unique—ICI Pharma brought respiratory products, Boehringer Mannheim added diagnostics capabilities, Rhone Poulenc expanded the portfolio in antibiotics.

By the mid-2000s, Piramal wasn't content with just the Indian market. Acquired Morpeth facility from Pfizer. This UK facility acquisition from Pfizer marked Piramal's entry into contract manufacturing for global markets—a crucial capability that would later attract Abbott's attention.

The company's growth trajectory was staggering. From a small acquisition in 1988, In 2010, Nicholas had reached the highest valuation in the whole of pharmaceutical industry. The business had grown through a combination of organic growth (riding India's pharma boom) and inorganic expansion (acquiring and integrating over a dozen businesses).

What made this growth remarkable wasn't just the scale but the execution. Each acquired business was integrated, optimized, and scaled. Manufacturing processes were upgraded, distribution networks were consolidated, and product portfolios were rationalized. The renamed Nicholas Piramal India Limited (later Piramal Healthcare) became a formidable force with:

- Over 350 brands in the domestic market

- Presence across multiple therapeutic areas including antibiotics, respiratory, cardiovascular, pain, and neuroscience

- Manufacturing facilities meeting global standards

- A field force that was among the largest in India

2011 saw Fortune 500 ranking Piramal Healthcare in the top-50 largest corporations across India. UN Conference on Trade and Development's World Investment Report 2011 ranked Piramal Healthcare as No. 5 in the top 10 pharmaceutical contract manufacturers worldwide.

The business model was validated not just by rankings but by the interest it generated. By 2010, Piramal Healthcare had become the third-largest pharmaceutical company in India—a position built entirely through acquisitions over just 22 years. The stage was set for what would become one of the most talked-about deals in Indian corporate history.

IV. The Abbott Mega-Deal: Peak Valuation Exit (2010)

May 21, 2010. The news hit the markets like a thunderbolt. U.S.-based Abbott Labs secured the top spot in India's growing pharmaceutical industry with its US$3.72 billion takeover of Piramal Healthcare's branded generics business. Abbott will pay US$2.12 billion upfront and four annual installments of US$400 million from 2011.

The valuation was staggering—"the valuation of about nine times shows the value we could create in the domestic market in the last 22 years", Ajay Piramal noted. To put this in perspective, most pharma deals in emerging markets were happening at 3-4x revenues. Abbott was paying 9x.

Why would Abbott pay such a premium? The answer lay in perfect strategic alignment and timing. Abbott's Warmuth says: "We want to expand in emerging markets, and you can't be taken seriously without having a strong or dominating presence in India. Emerging markets will in the next few years account for 70% of the growth in the global pharmaceutical industry, and India is 'an important and critical part' of that. He expects Abbott's Indian revenues to grow to US$2.5 billion in the next decade, up from the combined company's current revenues of about US$500 million. Also, India's US$8 billion pharmaceutical industry is poised to double by 2015.

The deal structure itself was fascinating. Abbott, through a wholly-owned subsidiary, purchased the assets of Piramal's Healthcare Solutions business for a $2.2 billion up-front payment with additional payments of $400 million annually for the next four years, beginning in 2011. This wasn't just a lump sum payment—it was structured to ensure Abbott's continued commitment while giving Piramal steady cash flows for future investments.

From a common man's point of view, over the counter products like Saridon and Lacto Calamine will continue to be brands of Piramal Healthcare, while popular cough syrup Phensedyl will become part of Abbott. After the acquisition, over 350 brands and about 5,500 employees and manufacturing units at Baddi in Himachal Pradesh will become part of Abbott's Indian operations.

But here's what made this deal truly remarkable—the timing. Emerging markets will grow by 14% to 17% between now and 2014, compared with 3% to 6% in developed markets, according to an April 2010 report from IMS Health. Piramal was selling at the exact moment when global pharma companies were desperate for emerging market exposure.

The negotiation dynamics revealed Piramal's mastery. On his company's transition from an acquirer to acquired, Piramal said: "I don't think we were in a position to take the company global. Abbott has the strength and aspirations to do that." Adding: "There aren't too many markets growing at 25 per cent annually and it's a good opportunity" for Abbott to be in India.

This wasn't admission of weakness—it was strategic humility. Piramal recognized that taking an Indian pharma company global would require massive R&D investments, global regulatory expertise, and decades of brand building. Instead of that uncertain path, he chose to crystallize value at peak multiples.

The capital allocation post-deal was equally strategic. PEL received approximately INR 15,000 crore from Abbott deal. After paying capital gains tax of approximately Rs 3,740 crore, the company had a war chest of over Rs 11,000 crore.

PEL bought back 41.8 million shares which represented 20% of the equity share capital at a price of INR 600 per share. The buyback price represented a premium of 19% over the average share price for the last three months at the time of the announcement of buyback (October 22, 2010).

What do you do with billions in cash when you've just sold your core business? For most companies, this would be an existential crisis. For Piramal, it was an opportunity to reinvent—again.

V. The Financial Services Pivot (2010-2021)

With the Abbott deal proceeds in hand, Ajay Piramal faced a crucial decision. He could have distributed most of it to shareholders, acquired another pharma business, or ventured into entirely new territory. He chose the path less traveled—building a financial services empire from scratch.

This cash kitty gave birth to Ajay Piramal's new innings in financial services and that grew larger with the acquisition of DHFL in September 2021. But the journey from 2010 to 2021 was anything but straightforward.

The timing seemed counterintuitive. Post-2008 financial crisis, global financial services were in turmoil. In India, infrastructure financing was becoming increasingly challenging with mounting NPAs. Yet Piramal saw opportunity where others saw obstacles. The company began building Piramal Capital & Housing Finance (PCHFL), focusing initially on real estate and wholesale lending—sectors that traditional banks were increasingly wary of.

The strategy was quintessentially Piramal: go where others fear to tread, but with disciplined underwriting. The company focused on structured deals, mezzanine financing, and construction finance for residential projects. These were complex, high-margin businesses that required deep expertise and patient capital—exactly what Piramal had.

Partnerships became a cornerstone of the strategy. Since 2016, Piramal Enterprises and Bain Capital Credit have been operating a partnership called India Resurgence Fund (IndiaRF), an investment fund for financially distressed Indian companies. Piramal Capital Fund (PCF), a partnership between Piramal Enterprises and CDPQ that was started in 2020, provides corporate financing services.

These weren't just capital partnerships—they brought global expertise, risk-sharing, and credibility to a relatively new player in Indian financial services. The Bain Capital partnership particularly focused on stressed assets, allowing Piramal to participate in the resolution of distressed companies without taking on entire balance sheet risk.

But the most audacious move came in between—the Vodafone investment. One of the pre-IPO investors was Ajay Piramal who via Piramal Enterprises purchased 11% stake in 2011-12. He paid ₹5,864 crore but when it became obvious that the IPO plans were not going through, he also sold them in 2014. And, he received ₹8,900 crore, a whopping 52% return or $1.4 billion, as per the exit agreement.

Ajay Piramal also took an opportunistic investment call in Vodafone in 2012 for a short stint and exited with 52% returns for $1.4 billion in a matter of 2 years. This wasn't a strategic investment—it was pure financial engineering. Piramal had negotiated multiple exit options including IPO participation rights and a put option to Vodafone Group.

Ajay Piramal, chairman of pharmaceutical giant Piramal Group said in a statement: "The equity purchase in Vodafone was consistent with our objective of making investments that offer opportunity to generate attractive long term return on equity. I am glad to say that we have delivered against our targeted returns with this investment."

Meanwhile, the core NBFC business was steadily growing. By 2020, the loan book had expanded to over $5 billion, with a presence across:

- Real estate developer financing

- Corporate lending to mid-market companies

- Structured credit solutions

- Housing finance to individuals

PEL also holds 10% stake in Shriram Capital, the holding company of Shriram Finance. This strategic investment gave Piramal exposure to vehicle financing and SME lending without building these capabilities from scratch.

The company also divested non-core assets during this period. This was later sold for $1 billion to PE Blackstone in December 2020. The Piramal Glass sale to Blackstone for $1 billion in 2020 provided additional capital just as a massive opportunity was emerging.

By early 2021, Piramal Enterprises had transformed itself into a diversified financial services player with strong capital adequacy, multiple funding sources, and partnerships with global investors. The stage was set for the biggest and most controversial deal of Piramal's career—the acquisition of DHFL.

VI. The DHFL Acquisition: Bold Contrarian Bet (2021)

November 2019. Dewan Housing Finance Corporation (DHFL), once India's third-largest pure-play mortgage lender, had collapsed spectacularly. DHFL had gone bankrupt with more than Rs 90,000 crore in debt to various lenders, including banks, mutual funds and individual investors who kept fixed deposits with the company.

The company wasn't just bankrupt—it was radioactive. Cobrapost, an Indian investigative journalist group, published an exposé of DHFL for using various shell corporations to siphon more than ₹ 31,000 crores of public money for the personal gains of the DHFL's primary stakeholders. CBI filed a new suit against DHFL and its promoters Kapil Wadhawan and Dheeraj Wadhawan, wherein the later were accused of syphoning off the welfare subsidy fund of Pradhan Mantri Awas Yojana by creating 260,000 fake home loan accounts.

Most financial institutions wouldn't touch DHFL with a ten-foot pole. Ajay Piramal saw India's largest distressed asset opportunity.

In January 2021, 94% of the Creditors of DHFL voted in favor of Piramal's resolution plan. The structure was complex but elegant. PCHFL has merged into DHFL with effect from September 30, 2021 pursuant to the reverse merger as contemplated under scheme of arrangement provided under the resolution plan. Consequent to the Reverse Merger, DHFL shall issue such number of equity shares to the shareholders of PCHFL i.e. to Piramal Enterprises Limited (PEL), in accordance with the scheme of arrangement provided under the resolution plan. Upon allotment of equity shares to PEL, DHFL will become a wholly-owned subsidiary of PEL.

The economics were compelling. The creditors of DHFL (including FD holders) would recover an aggregate amount of approximately Rs 38,000 crore from the resolution process of DHFL. There were approximately 70,000 creditors of DHFL and most of them are recovering nearly 46% of their pending dues through the successful completion of resolution process.

What Piramal acquired wasn't just distressed debt. The merged entity combines Piramal's financial strength, core values and institutional credibility with DHFL's geographic footprint and distribution network of 301 branches and 2,338 employees catering to approximately 1 million lifetime customers across 24 states.

This was classic Piramal playbook—buy a distressed asset, inject capital and credibility, leverage existing infrastructure, and transform it. The DHFL branch network gave Piramal instant retail presence across India, something that would have taken decades and billions to build organically.

Ajay Piramal, chairman, Piramal Group said, "We are very pleased to announce the consideration payment made towards the completion of this exciting acquisition. This accelerates our plans to become a leading digitally oriented, diversified financial services conglomerate that focuses on serving the financial needs of the unserved and underserved customers of our country. An important characteristic of any advanced economy is a robust insolvency code. The landmark bankruptcy reforms have made it possible to solve complex resolutions like this in a more complete and timely way."

The strategic rationale was multi-faceted: 1. Instant Scale: The combined entity became one of India's largest housing finance companies overnight 2. Retail Presence: 301 branches provided immediate retail lending capabilities 3. Customer Base: Access to 1 million existing customers for cross-selling 4. Valuation Arbitrage: Acquiring assets at distressed valuations with potential for significant value recovery

But the challenges were equally formidable. DHFL's reputation was in tatters. Employee morale was at rock bottom. Systems and processes needed complete overhaul. Regulatory scrutiny was intense. Recovery from the legacy bad loan book was uncertain.

The integration strategy focused on three pillars: - Cultural Transformation: Infusing Piramal's values and governance standards - Technology Upgrade: Modernizing DHFL's legacy systems with digital capabilities - Portfolio Cleanup: Aggressive resolution of stressed assets while growing the retail book

The DHFL acquisition marked Piramal's complete transformation into a financial services company. From textiles to pharma to finance—the journey had come full circle. But one more transformation awaited.

VII. The Demerger Strategy (2021-2022)

By 2021, Piramal Enterprises had become a conglomerate with two distinct businesses—financial services (now strengthened with DHFL) and pharmaceuticals (which had continued to grow post the Abbott deal through the contract manufacturing and critical care segments). The market was struggling to value this complexity.

The latest corporation action was the demerger of PEL into two businesses. It also seems to be a part of the succession planning of the group with Ajay Piramal's son Anand Piramal taking the lead at PEL and Nandini Piramal taking the lead at PPL.

The demerger announcement came in October 2021, with a clear rationale. The NCLT order has now paved the way toward the creation of two separate listed entities - Piramal Enterprises Limited (NBFC) and Piramal Pharma Limited. Ajay Piramal, Chairperson of Piramal Enterprises, said in a statement: "The approval from the Honourable NCLT on the demerger of our Pharma business and the simplification of the corporate structure is a significant milestone. We are on track to achieve the completion of demerger and separate listing of Piramal Pharma by the third quarter of the current financial year."

The demerger structure was shareholder-friendly. Investors will get four PPL shares for each PEL share held. According to Piramal Enterprises, the company will issue 4 equity shares of Rs 10 each of Piramal Pharma for every 1 equity share of Rs 2 each to shareholders of Piramal Enterprises Limited.

The strategic logic was compelling: - Focused Entities: Each business could pursue its growth strategy without capital allocation conflicts - Valuation Clarity: Pure-play companies typically command better valuations than conglomerates - Succession Planning: Clear leadership structure with next generation taking charge - Capital Access: Each entity could raise capital based on its own merits

After the National Company Law Tribunal (NCLT) approved the demerger on August 12, 2022, the group's pharma businesses were consolidated into PPL, which was then listed on the bourses on October 19.

The pharma business under Piramal Pharma Limited included: PPL includes Piramal Pharma Solutions (PPS), a contract development and manufacturing organisation (CDMO) that also provides discovery and development services; Piramal Critical Care (PCC), a complex hospital generics business; and the India consumer healthcare business that sells OTC products. Its CDMO business is among the top three in India and 13th largest globally, while the consumer and PCC businesses are also well positioned with differentiated products and business models.

But the market's reaction was brutal. Just prior to the effective date of demerger, the stock or PEL was quoting at Rs.2,000 per share and at a market value of Rs.48,000 crore representing the combined the value of both the businesses. As we write this article, PEL's marktcap is at Rs 19,153 crore while that of the pharma stock (Piramal Pharma) is Rs 11,020 crore – totalling to Rs 30,173 crore. This is a 37% erosion post demerger.

The value destruction was puzzling. Both businesses had strong fundamentals: - PEL had successfully integrated DHFL and was seeing strong growth in retail lending - PPL had a robust CDMO business with global clients and growing hospital generics portfolio

Several factors contributed to the market's skepticism: 1. Timing: The demerger came during a period of global market volatility 2. NBFC Concerns: Rising interest rates were pressuring NBFC valuations 3. Pharma Headwinds: Global pharma spending was slowing post-COVID 4. Complexity: Investors struggled to understand the sum-of-parts valuation

Post demerger, promoters will hold a 44% stake in PEL, and 35% in PPL. Meanwhile, Carlyle will hold 20% in PPL. The presence of Carlyle as a significant shareholder in PPL provided some validation, but wasn't enough to prevent the value erosion.

Despite the immediate market reaction, the demerger achieved its strategic objectives. Two focused entities emerged, each with clear leadership and strategy. The stage was set for the next chapter.

VIII. Modern Era: Pure-Play NBFC Evolution (2022-Present)

Post-demerger, Piramal Enterprises emerged as a pure-play financial services company. But the transformation wasn't complete. The company structure still had complexity with PCHFL (including the merged DHFL) as a subsidiary.

In April 2025, the Reserve Bank of India (RBI) approved the company's transition from a Housing Finance Company (HFC) to a Non-Banking Financial Company – Investment and Credit Company (NBFC-ICC). This regulatory change provided greater operational flexibility, allowing the company to expand beyond housing finance into broader retail and wholesale lending.

The next major simplification came through another merger. In May 2025, Piramal Enterprises Limited announced a proposed merger of Piramal Finance Limited with the parent entity. This would create a single, unified NBFC entity—eliminating holding company discounts and simplifying the corporate structure.

The modern Piramal Enterprises is dramatically different from even five years ago. Piramal Enterprises along with its subsidiaries, associates and joint ventures is a leading diversified NBFC with presence across retail lending, wholesale lending, and fund-based platforms. PEL Group has built a technology platform driven by artificial intelligence (AI), with innovative financial solutions that cater to the needs of varied industry verticals.

The retail transformation has been particularly striking. From being primarily a wholesale lender, the company now has: - Housing loans for affordable and mid-income segments - Loan against property for small businesses - MSME lending for working capital needs - Used vehicle financing - Digital lending partnerships with fintech platforms

PCHFL's retail finance division provides microlending and buy now, pay later services on behalf of partner fintech companies like ZestMoney, Moneyview, EarlySalary, Navi Group and KreditBee, and is also engaged in vehicle financing for partner companies like CARS24, CarDekho and Spinn

The digital transformation has been equally significant. The company has invested heavily in: - AI-based credit underwriting models - Digital customer acquisition channels - Automated loan processing systems - Data analytics for risk management

But challenges remain significant. The company's legacy wholesale book, while generating good yields, requires constant monitoring in a volatile real estate market. Competition from banks, other NBFCs, and fintech players is intensifying. Regulatory requirements are becoming more stringent.

The management under Anand Piramal is focusing on several key initiatives: 1. Retail Growth: Targeting 50%+ of loan book from retail by FY26 2. Digital First: Moving 70% of originations to digital channels 3. Asset Quality: Maintaining gross NPAs below 3% 4. Capital Efficiency: Improving ROE to 15%+ through operating leverage

IX. Playbook: The Art of Capital Recycling

After four decades of dealmaking, the Piramal formula has become clear: Buy distressed or undervalued assets, build value through operational improvements and strategic positioning, then sell at peak valuations—or hold and transform if the opportunity is compelling enough.

The pattern is remarkably consistent across sectors:

Nicholas Laboratories (1988): Bought when MNC was exiting, built into India's third-largest pharma company, sold at 9x revenue to Abbott.

Vodafone India (2011-2014): The healthcare company made a 52% profit from the sale of its 11% stake, originally acquired in 2012, back to Vodafone for $1.48bn. Pure financial investment with well-negotiated exit options.

Piramal Glass (1984-2020): Acquired for minimal investment, built over 36 years, The Competition Commission of India (CCI) has approved the $1 billion acquisition of Piramal Glass by the Blackstone private equity group. The acquisition is the largest ever transaction for a packaging company in India.

DHFL (2021): Acquired through IBC at distressed valuation, now being transformed into a retail lending powerhouse.

What makes this playbook work?

1. Contrarian Timing: Piramal consistently buys when others are fearful. Nicholas when MNCs were exiting India. DHFL when the company was radioactive. Real estate lending when banks were pulling back.

2. Patient Capital: Unlike private equity funds with fixed horizons, Piramal can hold assets for decades. The pharma business was built over 22 years. Glass was held for 36 years.

3. Operational Excellence: This isn't financial engineering alone. Each acquired business sees genuine operational improvements—whether it's upgrading manufacturing, expanding distribution, or improving governance.

4. Strategic Exits: Piramal doesn't fall in love with assets. When Abbott offered 9x revenue, he sold. When Blackstone offered $1 billion for glass, he sold. Emotion doesn't cloud judgment.

5. Relationship Capital: Deals come through relationships built over decades. The Nicholas acquisition came through a friend's tip. Global partnerships with Bain, CDPQ bring both capital and deal flow.

6. Risk Management: Despite the bold moves, risk is carefully managed. The Vodafone investment had multiple exit clauses. The DHFL acquisition was done through IBC with legal clarity. Partnerships share risk in stressed asset investments.

The succession planning adds another dimension. Nandini Piramal, 41, daughter of industrialist Ajay Piramal, Chairman of the Piramal Group. Nandini earlier headed the OTC (over-the-counter) business of PEL, and provided assistance in areas such as setting the strategy and driving results at the group's pharma business. As Chairperson of PPL, Nandini is gearing up to take the new entity on a path of sustained growth.

With Anand leading PEL and Nandini heading PPL, the next generation is being groomed with distinct responsibilities. This isn't just succession—it's evolution, with each leader bringing fresh perspectives while maintaining the core Piramal DNA.

X. Analysis & Investment Case

Where does Piramal Enterprises stand today as an investment proposition?

Market Cap ₹ 24,327 Cr. The company has recovered from post-demerger lows but remains well below the combined pre-demerger valuation. The current metrics paint a mixed picture:

The company has delivered a poor sales growth of -4.51% over past five years. Company has a low return on equity of 3.14% over last 3 years. These backward-looking metrics reflect the transition period—moving from pharma to financial services, integrating DHFL, and navigating the demerger.

But forward-looking indicators tell a different story. The company's Q4 FY25 results showed: Piramal Enterprises Ltd's net profit fell -25.28% since last year same period to ₹102.44Cr in the Q4 2024-2025. While the year-over-year comparison looks weak, the sequential improvement has been strong.

The Bull Case:

-

DHFL Integration Success: The retail loan book is growing at 25%+ annually. Asset quality is improving with recoveries from legacy portfolio. The branch network is being leveraged for cross-selling.

-

Retail Transformation: Moving from wholesale to retail lending improves risk diversification, provides stable margins, and opens a massive addressable market in under-served segments.

-

India Credit Story: India's credit-to-GDP ratio at ~55% remains well below peers. Rising income levels and formalization drive credit demand. Government's push for affordable housing benefits the company's focus segments.

-

Valuation Discount: Trading at ~1x book value versus 2-4x for leading NBFCs. Successful retail transformation could drive rerating. The simplified structure post-merger removes holding company discount.

The Bear Case:

-

Legacy Wholesale Book: Large exposure to real estate developers remains risky. Any major default could impact profitability and sentiment. The commercial real estate sector faces headwinds.

-

Competitive Intensity: Banks are aggressively entering the affordable housing segment. Fintech players are disrupting traditional lending models. Margin compression is likely as competition intensifies.

-

Execution Risk: Transforming from wholesale to retail is complex. Building risk management capabilities for retail takes time. Technology investments may pressure near-term profitability.

-

Regulatory Overhang: RBI's increasing scrutiny on NBFCs. Potential changes in priority sector lending norms. Any adverse regulatory action on DHFL legacy issues could impact.

The comparison with peers is instructive. Bajaj Finance trades at 5x book with ROE of 20%+. Shriram Finance trades at 2x book with established retail franchise. Piramal at 1x book suggests significant discount—justified by transition risks or opportunity for rerating?

The demerger value destruction remains puzzling. PEL's marktcap is at Rs 19,153 crore while that of the pharma stock (Piramal Pharma) is Rs 11,020 crore – totalling to Rs 30,173 crore. Even accounting for market volatility, the 37% erosion suggests investor skepticism about the separated entities' growth prospects.

XI. Key Inflection Points & Lessons

The Piramal journey offers masterclasses in corporate strategy, capital allocation, and value creation. Four critical inflection points defined the company's trajectory:

1988 - Nicholas Laboratories Acquisition: This wasn't just entering pharma—it was discovering the power of buying MNC exits in India. The lesson: In emerging markets, global companies' strategic retreats create local opportunities.

2010 - Abbott Sale at $3.7 Billion: Selling the crown jewel at peak valuation took courage. Most founder-entrepreneurs can't let go. The lesson: No asset is permanent. When someone offers you peak cycle valuations, take it.

2021 - DHFL Acquisition: Buying India's most controversial bankruptcy showed contrarian conviction. While others saw reputational risk, Piramal saw infrastructure value. The lesson: In distressed situations, separate the asset from the narrative.

2022 - Pharma Demerger: Splitting the company during market volatility seemed poorly timed. Yet it provided focus and succession clarity. The lesson: Long-term strategic clarity trumps short-term market reactions.

Beyond these inflection points, several meta-lessons emerge:

The Power of Patient Capital: Unlike listed private equity funds or traditional corporates, Piramal could play multi-decade games. Building pharma over 22 years. Holding glass for 36 years. This time arbitrage is a massive competitive advantage.

Relationships as Currency: Every major deal came through relationships. The Nicholas tip from a friend. Global partnerships with Bain and CDPQ. In emerging markets, trust and relationships often matter more than spreadsheets.

Embracing Complexity: While markets punish conglomerates, Piramal used complexity as a weapon. The ability to move capital across sectors, leverage capabilities across businesses, and see patterns across industries created unique advantages.

Strategic Humility: Knowing what you can't do is as important as knowing what you can. Piramal knew he couldn't take Indian pharma global competitively. He knew he needed partners for stressed assets. This self-awareness prevented costly mistakes.

The Succession Paradox: Most Indian business families struggle with succession. Piramal solved it by dividing the empire—giving each generation member a distinct domain. Sometimes division creates more value than unity.

XII. Epilogue & Future Outlook

As we look toward 2030, what might Piramal Enterprises become?

The company has set ambitious targets. Management aims to double the loan book to ~₹150,000 crore by FY28. Retail should constitute 60%+ of the portfolio. ROE should exceed 15%. Digital origination should reach 70%+.

These aren't unrealistic if execution delivers. India's financial services sector is at an inflection point. Credit penetration remains low. Digital infrastructure through UPI, Aadhaar, and GST enables new lending models. The formalization of the economy expands the addressable market.

But success isn't guaranteed. The competitive landscape is brutal. Traditional banks are modernizing rapidly. New-age NBFCs like Bajaj Finance have set high performance bars. Fintech players are reimagining customer acquisition and underwriting. Foreign banks and PE funds are entering wholesale lending.

The regulatory environment adds complexity. RBI's framework for NBFCs is converging with banks—higher capital requirements, stricter ALM norms, enhanced governance standards. Any benefits of regulatory arbitrage are disappearing.

Technology will be the decisive factor. Can Piramal build true digital capabilities or will it remain a traditional lender with digital lipstick? The partnerships with fintech platforms provide distribution but also create dependency. Building proprietary technology platforms requires massive investments with uncertain returns.

The leadership transition adds another variable. Anand Piramal brings youth and dynamism but lacks his father's deal-making track record. His connection to the Ambani family through marriage creates interesting possibilities—or potential conflicts. Can he maintain Piramal's independence while leveraging strategic relationships?

Mr Ajay Piramal has steered the conglomerate to global prominence across 30 countries and over 100 markets. His 'Doing Well and Doing Good' philosophy drives both business success and social impact. This philosophy now faces its biggest test. Can financial services, inherently about risk and return, maintain the same ethical standards as pharma or manufacturing?

The international expansion question looms. Unlike pharma or glass, financial services are harder to globalize. Will Piramal remain India-focused or attempt international expansion? The diaspora lending opportunity, trade finance, or acquiring distressed financial assets globally—all present opportunities and risks.

ESG considerations are becoming crucial. How does a wholesale lender to real estate developers align with sustainability goals? Can retail lending to underserved segments balance social impact with profitability? These aren't just compliance issues but fundamental strategy questions.

The ultimate question: Will Piramal Enterprises remain independent? At current valuations, it's an attractive acquisition target for global financial institutions seeking Indian exposure. Would the family consider another transformative sale, like Abbott, if the valuation is compelling?

Looking at the 40-year journey, one pattern is clear—Piramal never stands still. Every decade brought reinvention. Textiles to pharma. Pharma to finance. Wholesale to retail. What's the next transformation?

Perhaps the answer lies not in predicting the future but in understanding the process. Piramal's edge wasn't in always being right but in being adaptable. In buying when others sold. In selling when others bought. In seeing value where others saw risk.

As markets evolve, regulations change, and technologies disrupt, this adaptability matters more than any specific strategy. The company that started as a textile mill and became a pharma giant, then a financial services player, will likely become something else entirely by 2030.

The Piramal story isn't about permanent success in any sector. It's about permanent reinvention in response to opportunity. In that sense, the company's future is both uncertain and certain—uncertain in form, certain in its willingness to transform.

For investors, employees, and observers, this creates both anxiety and excitement. You never quite know what Piramal Enterprises will become. But you know it won't be boring. In Indian corporate history, few companies have demonstrated such repeated ability to destroy and create value, to build and sell, to transform and adapt.

The master of capital recycling continues to turn. Where the wheel stops next, only time will tell. But if history is any guide, it will be wherever the combination of contrarian thinking, patient capital, and strategic courage creates the next great opportunity. In Ajay Piramal's India, that could be anywhere.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube