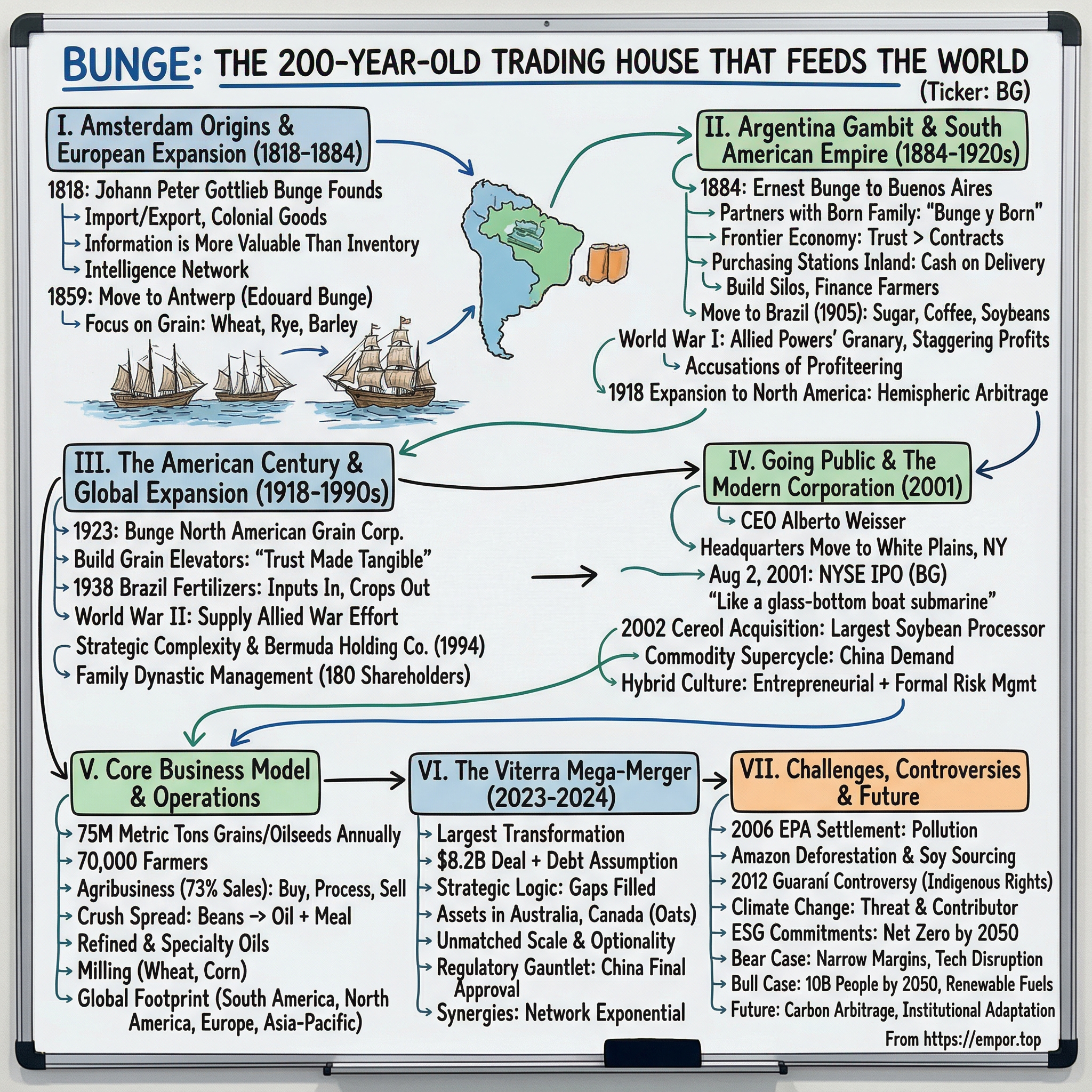

Bunge: The 200-Year-Old Trading House That Feeds the World

I. Introduction & Opening

Picture this: Every morning, before you've had your first cup of coffee, a vast invisible machine has already been working for hours to ensure your breakfast exists. The oil in your cooking pan, the flour in your bread, the feed that grew the chickens that laid your eggs—all of it flows through a handful of companies so essential yet so unknown that they might as well be shadow governments of global food. Among these titans stands Bunge Global SA, a name that most people can't pronounce (it's "BOON-geh," by the way) but whose decisions ripple through every grocery store on Earth.

From its headquarters in St. Louis, Missouri—though incorporated in Geneva, Switzerland, a detail that hints at two centuries of strategic geography—Bunge controls a sprawling empire that would make 19th-century colonial powers envious. This is a company that talks to 70,000 farmers before most executives check their email, that moves 75 million metric tons of grains and oilseeds annually through a network so complex it requires its own weather forecasting systems, and that, along with its three rivals—ADM, Cargill, and Louis Dreyfus—forms the "ABCD" quartet controlling an estimated 90% of the global grain trade.

The central question isn't just how a small Amsterdam trading house founded by Johann Peter Gottlieb Bunge in 1818 became one of the four horsemen of the agricultural apocalypse (or salvation, depending on your perspective). It's how this company survived Napoleon, two world wars, countless coups, commodity crashes, and family feuds to emerge as a publicly traded giant that literally feeds billions while remaining virtually invisible to those billions.

What makes Bunge's story particularly fascinating isn't just the commodity trading playbook—though we'll decode that—or the financial engineering that took it public in 2001. It's the family saga spanning six generations, the geopolitical chess games played with food as pawns, and the almost mystical ability to be everywhere and nowhere simultaneously. This is a company that has mastered the art of being essential infrastructure for human civilization while maintaining the opacity of a Swiss bank.

We're about to trace a journey from European merchant houses to South American agricultural empires, from family dynasties to Wall Street, from moving bags of grain on horse carts to using satellite imagery to predict harvests. Along the way, we'll uncover how Bunge and its competitors created the template for global capitalism itself—turning the most basic human need, food, into the most sophisticated financial instrument.

So why should investors care about a 200-year-old grain trader? Because in an era of supply chain fragility, climate volatility, and geopolitical tension, the companies that control how food moves from farm to fork aren't just businesses—they're the architects of global stability. And Bunge, fresh off its massive Viterra merger, is rewriting the rules of that architecture.

II. The Amsterdam Origins & European Expansion (1818-1884)

The year 1818 was a peculiar time to start a trading company. Europe was still catching its breath from the Napoleonic Wars, the Congress of Vienna had just redrawn the continent's map, and in Amsterdam, the once-mighty Dutch trading empire was adjusting to its diminished role on the world stage. Into this uncertainty stepped Johann Peter Gottlieb Bunge, a merchant with a vision that seemed modest at the time: create an import-export business that could navigate the treacherous waters of post-war European commerce.

Johann wasn't trying to build a global empire. His ambition was refreshingly local—move colonial goods into Amsterdam, move Dutch products out. Spices from the East Indies, textiles, anything that Amsterdam's merchants could buy low and sell high. The original Bunge & Co. was essentially a one-man arbitrage operation with a keen eye for price discrepancies between markets that moved information at the speed of sailing ships.

But here's what separated Johann from the hundreds of other traders crowding Amsterdam's exchanges: he understood that information was more valuable than inventory. While others focused on owning warehouses full of goods, Bunge built relationships. Every ship captain, every dock worker, every merchant became a node in an intelligence network. When a ship arrived with news of a failed harvest in Russia or a bumper crop in America, Bunge knew before his competitors. This wasn't insider trading—it was the 19th-century equivalent of high-frequency trading, where "high-frequency" meant getting news days or weeks before others.

The real genius move came in 1859 when Johann's grandson, Edouard Bunge, recognized that Amsterdam was yesterday's news. The future of European trade was shifting south to Antwerp, where Belgium's new independence and industrial ambitions were creating a rival to Amsterdam's centuries-old dominance. Moving the company to Antwerp wasn't just a geographic shift—it was a bet on the future of European industrialization.

Edouard transformed his grandfather's trading post into something resembling a modern corporation. He established what would become the Bunge playbook: never own when you can trade, never trade when you can arbitrage, and never arbitrage without intelligence. The company began specializing in what seemed like the most boring possible commodity: grain. While others chased exotic spices or precious metals, Bunge focused on wheat, rye, and barley—the stuff that kept European workers fed and European governments stable.

The timing was perfect. The 1860s and 1870s saw Europe's population explode while its agricultural productivity struggled to keep pace. Countries that had been self-sufficient in food suddenly needed imports. The American Midwest was opening up, Russia was modernizing its agriculture, and Argentina was about to become the world's breadbasket. Someone needed to connect these dots, and Edouard Bunge was building the infrastructure to do exactly that.

By the 1870s, Bunge had offices across Northern Europe—Rotterdam, London, Hamburg. Each office wasn't just a trading post but an intelligence node, gathering information on harvests, prices, shipping rates, and political developments. The company developed its own code system for telegraphs, allowing it to transmit market-sensitive information faster and more securely than competitors. Think of it as the Victorian-era equivalent of Bloomberg terminals.

The family dynamics during this period set patterns that would define Bunge for the next century. This wasn't a company with outside shareholders or professional managers—it was a family enterprise where sons were groomed from childhood to take over, where daughters were married to solidify business alliances, and where family meetings were indistinguishable from board meetings. The Bunges practiced a form of corporate dynasticism that would make the Medicis proud.

But Edouard's masterstroke wasn't just building a European trading network—it was recognizing that Europe itself was too small. As the 1880s approached, he began sending family members on reconnaissance missions to the Americas. His younger brother Ernest drew the long straw—or short straw, depending on your appetite for adventure. In 1884, Ernest would board a steamship for Buenos Aires, carrying with him the Bunge name, a modest amount of capital, and instructions to build an empire.

The European chapter of Bunge's story was ending just as the age of global trade was beginning. What started as a modest Amsterdam trading house had evolved into a sophisticated intelligence and logistics network spanning a continent. But Europe was just the prelude. The real symphony was about to begin 8,000 miles away, where the pampas stretched endlessly under the Southern Cross, and where Ernest Bunge was about to make a gambit that would transform a family business into a global power.

III. The Argentina Gambit & South American Empire (1884-1920s)

Ernest Bunge stepped off the steamship in Buenos Aires harbor in 1884 and into a scene of controlled chaos. The port was a babel of languages—Italian, Spanish, German, English—as waves of European immigrants poured into Argentina, chasing dreams of land and prosperity. The air smelled of coal smoke, horse manure, and opportunity. Argentina in the 1880s was experiencing one of history's great economic miracles, transforming from a backwater into one of the world's richest countries, and Ernest had arrived just in time for the party.

But Ernest didn't come alone, and this detail would prove crucial. He quickly partnered with the Born family, fellow European merchants who brought complementary skills and, more importantly, capital. The formation of Bunge y Born wasn't just a business partnership—it was a merger of two merchant dynasties that understood a fundamental truth: in a frontier economy, trust matters more than contracts. Their handshake deal would outlast most constitutions.

Why Argentina? The answer lay in the pampas, that vast fertile plain stretching from Buenos Aires to the Andes. This was some of the richest agricultural land on Earth, capable of producing wheat yields that made European farms look like garden plots. The Argentine government was practically giving land away to anyone willing to farm it. Railways were being built at breakneck speed, financed by British capital and constructed by Italian labor. It was the perfect storm of fertile land, cheap labor, foreign investment, and political stability—at least by Latin American standards.

Bunge y Born's initial strategy was deceptively simple: buy grain from farmers, store it, and sell it to European buyers. But the execution was where the magic happened. While competitors focused on Buenos Aires, Bunge y Born went inland, establishing purchasing stations in tiny pueblos across the pampas. They offered farmers something revolutionary: cash on delivery. No more waiting months for payment from Buenos Aires middlemen. No more getting cheated on weights and measures. Bunge y Born showed up with scales, cash, and consistent prices.

The company's expansion through the 1890s reads like a military campaign. Each new railway line that pushed into the interior was followed by Bunge y Born purchasing stations. They built silos where none existed, creating the physical infrastructure for Argentina's grain explosion. By 1900, they weren't just buying grain—they were financing farmers, providing seeds, even building schools and hospitals in rural communities. This wasn't corporate social responsibility; it was building a captive supply chain.

The move to Brazil in 1905 showed the next evolution of the strategy. While Argentina was about wheat and the temperate pampas, Brazil offered sugar, coffee, and eventually soybeans. The company didn't just replicate its Argentine model; it adapted to Brazil's different agricultural systems, political structures, and business cultures. In Argentina, Bunge y Born dealt with European immigrant farmers who understood commercial agriculture. In Brazil, they navigated complex relationships with traditional landowners, former slave plantations transitioning to wage labor, and a Portuguese-speaking bureaucracy that operated by entirely different rules.

World War I transformed Bunge y Born from a successful regional player into a global power. As European farms turned into battlefields and shipping became a deadly gamble, neutral Argentina became the Allied powers' granary. Food prices skyrocketed. A bushel of wheat that sold for $1 in 1914 hit $3 by 1917. Bunge y Born wasn't just moving grain; they were determining whether European cities starved or survived.

The wartime profits were staggering, but they came with a price. The company faced accusations of profiteering, of holding grain off the market to drive up prices, of being "merchants of hunger." The Born and Bunge families, many of whom still held European passports, found themselves in an impossible position—selling Argentine grain at premium prices to their former homelands. They responded by becoming more Argentine than the Argentines, funding cultural institutions, supporting local charities, and embedding themselves in the fabric of Argentine society.

The 1918 expansion to North America wasn't just geographic—it was a fundamental shift in ambition. The United States was both a competitor and an opportunity. American grain dominated global markets, but American farmers needed buyers, and American consumers needed South American products in the off-season. Bunge y Born saw the possibility of arbitraging between hemispheres, buying Northern Hemisphere grain in the fall and Southern Hemisphere grain in the spring, maintaining constant flow and constant profits.

The organizational structure that emerged during this period was fascinatingly complex. Bunge y Born wasn't really one company but a web of partnerships, subsidiaries, and affiliates, each optimized for local laws, taxes, and politics. The Buenos Aires office might be buying wheat from one subsidiary, selling it to another, financing it through a third, and shipping it on vessels owned by a fourth. This complexity wasn't bureaucracy—it was camouflage, making it nearly impossible for governments, competitors, or even employees to understand the full scope of operations.

By the 1920s, Bunge y Born had become something unprecedented: a South American multinational that could compete with European and American giants. They controlled significant portions of Argentina's grain exports, Brazil's coffee trade, and were expanding into manufacturing—flour mills, oil processing, textiles. The families that ran it—primarily the Bunges, Borns, Hirschs, and Engels—operated like a transnational aristocracy, educated in European universities, married across continents, and moving seamlessly between Buenos Aires, São Paulo, Antwerp, and New York.

The transformation from European trading house to South American empire was complete. But success brought scrutiny, and size brought vulnerability. The company that had thrived in the shadows was about to be dragged into the harsh light of the American century, where antitrust laws, securities regulations, and shareholder capitalism would challenge every assumption that had built the Bunge y Born empire.

IV. The American Century & Global Expansion (1918-1990s)

The formation of Bunge North American Grain Corporation in 1923 marked a pivot that would define the company's next century. The executives who signed the incorporation papers in New York did so with European fountain pens, speaking Spanish-inflected English, representing a company that was legally Argentine but culturally stateless. America wasn't just another market—it was a different universe with different rules, and Bunge would have to evolve or die.

The North American operation started modestly, focusing on what Bunge knew best: grain trading. But the American agricultural system was unlike anything in South America. The Midwest wasn't the pampas with its vast estates and seasonal labor. This was a landscape of family farms, each one a small business, fiercely independent and deeply suspicious of foreign buyers. Bunge's representatives, often bearing Germanic surnames and accented English, faced skepticism in Iowa and Kansas that they'd never encountered in Córdoba or Rio Grande do Sul.

The solution was brilliantly American: infrastructure. Rather than just buying grain, Bunge began building and acquiring grain elevators along the Mississippi River and Great Lakes. These massive concrete silos weren't just storage—they were trust made tangible. Farmers could see their grain going into a Bunge elevator, could drive by and confirm it was still there, could understand the physical reality of the transaction in a way that abstract futures contracts never provided.

The 1938 expansion into Brazilian fertilizers seems, in retrospect, almost prescient. While competitors focused on moving agricultural products out of South America, Bunge started moving inputs in. Fertilizer was the perfect complement to grain trading—farmers who bought Bunge fertilizer often sold Bunge their crops, creating a virtuous cycle of credit, supply, and purchase that locked in relationships for generations.

World War II tested every assumption about global trade. Unlike WWI, where Bunge profited from neutrality, WWII forced choices. The company's operations were spread across Allied, Axis, and neutral territories. The Bunge family members themselves held passports from a dozen different nations. Some were drafted into opposing armies. The Buenos Aires office was trading with both sides until Argentina's late entry into the war. The U.S. operation was supplying the Allied war effort while the European remnants of the original company were operating under Nazi occupation.

The post-war period brought a reckoning. The age of family-controlled trading houses was ending, replaced by professional management and regulatory oversight. But Bunge adapted again, this time through a strategy of strategic complexity. Instead of simplifying its structure, the company made it more byzantine. The 1994 conversion to Bermuda-registered Bunge International was masterful financial engineering—maintaining the valuable Bunge y Born brand in Argentina while creating a holding structure that could operate globally without being trapped by any single jurisdiction's taxes or regulations.

The family control structure during this period was a marvel of dynastic management. Around 180 shareholders from the main families—Hirsch, Bunge, Born, Engels, and De La Tour—operated through a trust structure that would make a Shakespearean drama look simple. Voting rights, economic rights, and management rights were separated and recombined in ways that ensured no single family could take control while preventing any outsider from understanding who actually owned what.

This opacity was a feature, not a bug. In the commodity trading business, information asymmetry is everything. If competitors knew Bunge's positions, they could trade against them. If governments knew Bunge's profits, they could tax them. If farmers knew Bunge's inventory, they could demand higher prices. The labyrinthine corporate structure wasn't just about tax optimization—it was about maintaining the information advantage that had been Bunge's edge since those first telegraph codes in 1870s Antwerp.

The diversification throughout the latter half of the 20th century followed a clear logic: own the entire value chain but make it look like you don't. Bunge acquired flour mills but kept them as separate brands. They bought shipping companies but chartered vessels through intermediaries. They expanded into food processing but maintained arm's length relationships that obscured the full integration. This wasn't vertical integration as practiced by Standard Oil or U.S. Steel—it was something more subtle, more flexible, and ultimately more powerful.

By the 1990s, Bunge had evolved into something unique in corporate history: a 175-year-old startup. It had the deep relationships and institutional knowledge of a company that had been trading grain since before the telephone was invented, combined with the aggressive expansion mindset of a Silicon Valley unicorn. It operated in dozens of countries but belonged to none. It employed thousands but was controlled by hundreds. It fed billions but was known by few.

The decision to maintain this structure while the world moved toward transparency, standardization, and public markets seemed increasingly anachronistic. Competitors like ADM had gone public decades earlier. Cargill remained private but at least had a clear ownership structure. Bunge International was neither fish nor fowl—too big to hide but too opaque to trust.

As the new millennium approached, the pressure to choose became irresistible. The commodity supercycle was beginning, China was industrializing, and global food demand was about to explode. To capture these opportunities, Bunge needed capital—lots of it. The family shareholders, now in their fourth and fifth generations, wanted liquidity. The regulators wanted transparency. The markets wanted in.

The stage was set for one of the most remarkable IPOs in history: taking a two-century-old family trading house public without destroying what made it successful. The man chosen to perform this high-wire act was Alberto Weisser, a Brazilian executive who understood both the old world of relationship trading and the new world of capital markets. His task: transform Bunge from a virtual company that "didn't physically exist" into a New York Stock Exchange-listed corporation while somehow maintaining the strategic advantages of obscurity.

V. Going Public & The Modern Corporation (2001)

Alberto Weisser stood at the podium of the New York Stock Exchange on August 2, 2001, preparing to ring the opening bell. Behind him, a collection of Bunge family members—some meeting for the first time despite sharing ancestry—watched their birthright transform into ticker symbol BG. The irony wasn't lost on anyone: a company that had thrived in opacity for 183 years was about to become as transparent as SEC regulations demanded. Weisser would later describe this moment as "like asking a submarine to become a glass-bottom boat while still diving deep."

The road to this moment had been anything but smooth. When Weisser took the helm in 1999, Bunge was, in his own words, "a virtual company"—it existed everywhere and nowhere simultaneously. The headquarters move from São Paulo to White Plains, New York, was more than geographic. It was an acknowledgment that Bunge needed to speak the language of Wall Street, quite literally. The White Plains office, deliberately chosen for its proximity to New York City but distance from the trading floors, represented a careful balance: close enough to capital markets to be credible, far enough to maintain independence.

The IPO preparation revealed just how byzantine Bunge's structure had become. Investment bankers from Morgan Stanley and Goldman Sachs spent months trying to create an organizational chart that made sense to public market investors. They discovered subsidiaries that owned each other in circular patterns, profit centers that existed only on paper, and trading relationships so complex that even Bunge's own executives couldn't fully explain them. One banker allegedly quipped, "We're not taking a company public; we're solving a Rubik's Cube blindfolded."

The prospectus filed with the SEC was a masterpiece of saying everything while revealing nothing. Yes, Bunge disclosed its financials, but the real business—the intelligence networks, the political relationships, the handshake deals with farmers spanning generations—none of that could be captured in GAAP accounting. How do you value a phone call that reveals a drought in Ukraine two weeks before satellites confirm it? How do you price the trust of a Brazilian farmer who's sold to Bunge for three generations?

The timing of the IPO, just weeks before 9/11, seemed catastrophic. Markets crashed, investors fled to safety, and a Brazilian-Argentine-European-American agricultural conglomerate wasn't anyone's idea of a safe haven. Bunge's stock, priced at $16, promptly fell. But Weisser and his team recognized something others missed: global uncertainty would increase the value of food security, and food security was Bunge's business.

The 2002 acquisition of Cereol, completed barely a year after going public, demonstrated the new Bunge's ambitions. This wasn't a small bolt-on acquisition—Cereol brought Central Soya and CanAmera Foods, making Bunge the world's largest soybean processor overnight. The $830 million price tag would have been impossible under the old family structure. But as a public company, Bunge could issue shares, raise debt, and move with a speed that stunned competitors who still thought of it as a sleepy trading house.

The strategic logic was elegant: soybeans were becoming the crude oil of agriculture. They could be crushed into oil for cooking, meal for animal feed, lecithin for food processing, and increasingly, biodiesel for fuel. By controlling soybean processing, Bunge wasn't just trading commodities—it was creating them, transforming raw beans into dozens of products, each with its own market dynamics and profit margins.

The commodity supercycle of the 2000s turned Bunge's IPO from a qualified success into a spectacular win. China's industrialization drove unprecedented demand for soybeans to feed livestock for its growing middle class. Bunge's stock, which had languished around $20 in 2002, hit $150 by 2008. The family shareholders who had reluctantly agreed to go public were suddenly worth billions. The Brazilian farmer's son who rang the bell at the NYSE had created more wealth in seven years than the previous six generations combined.

But going public changed Bunge in ways beyond the balance sheet. Quarterly earnings calls replaced family meetings. Risk management became formalized, documented, and regulated rather than intuitive and relationship-based. The company that had operated on handshakes now needed armies of lawyers. The traders who had kept positions in their heads now faced value-at-risk models and compliance officers.

Weisser navigated these changes by creating what he called a "hybrid culture." The trading floor maintained its aggressive, entrepreneurial spirit—stories circulated of traders making hundred-million-dollar bets on weather patterns. But these cowboys now operated within risk parameters set by committees, reported to independent directors, and faced clawbacks if bets went wrong. It was like putting a Formula 1 engine in a Volvo—all the power, but with airbags and anti-lock brakes.

The public market structure also forced Bunge to articulate what it actually did. The old answer—"we trade grain"—wasn't sufficient for analysts who wanted to model earnings. Bunge had to explain crush spreads (the difference between soybean prices and the combined value of oil and meal), basis risk (the difference between local and futures prices), and dozens of other concepts that had been trade secrets. Every earnings call became a masterclass in commodity market dynamics, educating competitors as much as investors.

The transformation from family-controlled to public company culminated in a profound shift in time horizon. The families had thought in generations—a bad year was noise in a two-century signal. Public markets think in quarters—a bad harvest becomes a missed earnings estimate becomes a stock price collapse. Weisser and his successors would have to balance these competing temporal demands: investing for the long term while satisfying short-term market expectations.

By 2010, the transformation was complete. Bunge had successfully evolved from a family trading house into a modern public corporation without losing its essential advantages. It maintained its intelligence networks while adding analytical capabilities. It kept its entrepreneurial culture while implementing corporate governance. It preserved its relationships while standardizing its operations.

The submarine had indeed become a glass-bottom boat, but it had learned to dive deeper than ever. The company that emerged from this transformation was something new in corporate history: a two-century-old firm with startup agility, a family business with public accountability, a commodity trader with industrial operations. This hybrid would soon face its greatest test yet in the form of a transformative merger that would redefine global agriculture.

VI. The Core Business Model & Operations

To understand Bunge's business model, imagine you're standing in a control room that looks like NASA mission control mixed with a Wall Street trading floor. Screens display satellite images of Brazilian soybean fields, real-time shipping positions in the South China Sea, Chicago futures prices updating every millisecond, and weather forecasts for the Ukrainian wheat belt. This is Bunge's nerve center in White Plains, where approximately 75 million metric tons of grains and oilseeds—enough to fill 3,000 Titanics—are tracked, traded, and transformed annually.

The Agribusiness segment, Bunge's historical core and still its largest division, operates on a deceptively simple premise: buy agricultural commodities from farmers, process them into useful products, and sell those products to end users. But calling this "simple" is like calling chess "moving pieces on a board." The execution involves a symphony of logistics, finance, and risk management that would make a Swiss watchmaker weep with envy. Start with the 70,000 farmers: that's more individual relationships than most consumer brands have retail locations. Bunge connects farmers to consumers to deliver essential food, feed and fuel to the world, but the mechanics of this connection involve processing oilseeds, such as soybeans, rapeseed, and sunflower seeds, into various products, including oils, meals, and protein concentrates. The company operates approximately 23,000 employees in 40 countries, managing a network that would make Amazon's logistics look straightforward.

Let's decode the segments. The Agribusiness division—accounting for approximately 73% of total net sales in 2024—isn't just buying and selling grain. It's a massive arbitrage machine that exploits price differences across time (storing grain from harvest to lean seasons), geography (moving Brazilian soybeans to Chinese ports), and form (converting whole soybeans into oil and meal, capturing the "crush spread"). When a trader in White Plains sees that Brazilian soybeans plus shipping costs are $10 per ton cheaper than Chicago futures for delivery in three months, that's not just information—it's money waiting to be collected.

The genius of the crush spread deserves its own MBA case study. A soybean isn't valuable as a soybean—it's valuable as 79% meal (for animal feed) and 18.5% oil (for cooking, biodiesel, industrial uses), with the remainder as waste. The spread between the input cost (whole soybeans) and output value (oil plus meal) fluctuates constantly based on everything from Chinese pork demand to European biodiesel mandates. Bunge's traders don't just bet on this spread; they lock it in through complex hedging strategies that would make a derivatives trader's head spin.

The Refined and Specialty Oils segment transforms that crude soybean oil into hundreds of specialized products. Need a specific melting point for your chocolate coating? Bunge has a fat for that. Want a trans-fat-free solution that still gives pastries that perfect flake? There's a specialty oil designed precisely for that application. This isn't commodity trading anymore—it's molecular engineering with soybeans.

The Milling segment, while smaller, provides crucial diversification. The company produces wheat flour for bread, pasta, and baked goods, as well as cornmeal, corn flour, and corn grits for snack foods and breakfast cereals. These products have different demand drivers, different customer bases, and different margin structures than oilseeds, providing natural hedging against sector-specific downturns.

But the real competitive advantage isn't in any single segment—it's in the integration. Bunge's balanced global footprint spans six continents and includes grain elevators, oilseed processing plants and strategically located port terminals, with approximately 36% of processing capacity in South America, 26% in North America, 23% in Europe and 15% in Asia-Pacific. This geographic distribution isn't random—it's a carefully orchestrated arbitrage between the Northern and Southern hemispheres' opposing harvest cycles.

Consider the seasonality arbitrage: when U.S. farmers harvest soybeans in October, prices typically hit annual lows. Bunge buys, stores, and processes. Come February, when South American soybeans are still growing and global supplies tighten, those stored U.S. soybeans are worth significantly more. Reverse the process in April when Brazilian farmers flood the market with their harvest. This isn't speculation—it's systematic exploitation of predictable seasonal patterns, backed by physical assets that can store millions of tons of grain.

The risk management infrastructure supporting all this makes NASA's mission control look simple. Every position—physical grain in a silo, futures contracts in Chicago, currency hedges for Brazilian real exposure, freight derivatives for shipping costs—must be tracked, valued, and hedged in real-time. A drought in Iowa doesn't just affect corn prices; it cascades through livestock feed demand, ethanol production, export schedules, and ultimately impacts Bunge's positions across dozens of markets. Bunge's financial risk management services include structuring and marketing risk management products to enable agricultural producers and end users of commodities to manage commodity price risk exposures. The sophistication here goes beyond simple futures hedging. The financial risk management desk manages a book of exotic derivatives sold to farmers and consumers, essentially becoming an investment bank for agriculture. When a Brazilian farmer wants to lock in fertilizer costs but maintain upside if soybean prices spike, Bunge can structure a collar option that provides exactly that exposure.

The intelligence apparatus supporting all this would make intelligence agencies envious. A large research group provides estimates of agricultural and soft commodity fundamentals that underlie most of the risk taking. This isn't just reading USDA reports—it's satellite analysis of crop conditions, proprietary weather modeling, real-time tracking of vessel movements, and networks of informants in farming regions who report on planting intentions before official surveys.

Bunge provides financing services to farmers, primarily in Brazil, from whom they purchase soybeans and other agricultural commodities. These farmer financing activities are an integral part of grain and oilseed origination activities as they help assure the annual supply of raw materials for Brazilian agribusiness operations. This creates a virtuous cycle: finance the farmers, sell them inputs, buy their crops, process the crops, sell the products. Each step generates margin and locks in relationships that span generations.

The logistics network deserves its own appreciation. Bunge operates a global network of grain storage facilities strategically located near key agricultural production regions, allowing it to source commodities from a wide range of suppliers. The storage facilities are equipped with state-of-the-art technology that enables it to maintain the quality and condition of the commodities it stores. But storage isn't passive—it's active value creation. Grain in a silo isn't just sitting there; it's being dried to optimal moisture levels, blended to meet specific quality specifications, and timed for release when basis (the local cash price minus futures price) is most favorable.

The company's approach to risk has evolved significantly since going public. Bunge now has a single enterprise-wide credit and counterparty risk management solution that empowers management to more easily implement the firm's credit policies across regions and businesses globally. This shift from intuitive, relationship-based risk assessment to quantitative, systematic risk management represents a fundamental transformation in how the company operates.

Yet for all this sophistication, the core business model remains remarkably simple: stand between those who grow food and those who consume it, capturing value at every step of the transformation. The complexity lies not in the concept but in the execution—managing millions of transactions, thousands of counterparties, and hundreds of risk factors simultaneously while maintaining margins that often measure in single-digit percentages.

This model has proven remarkably resilient across economic cycles, but it's about to be tested by the largest transformation in Bunge's history. The Viterra merger isn't just adding scale—it's fundamentally reshaping what it means to be a global agricultural trader in the 21st century.

VII. The Viterra Mega-Merger (2023-2024)

When Greg Heckman stood before investors on June 13, 2023, to announce Bunge's merger with Viterra, he wasn't just unveiling another acquisition. He was orchestrating the largest transformation in agricultural trading since the original ABCD companies formed over a century ago. The deal structure was staggering: Viterra shareholders would receive approximately 65.6 million shares of Bunge stock worth $6.2 billion and $2.0 billion in cash, while Bunge would assume $9.8 billion of Viterra debt, which was associated with approximately $9.0 billion of highly-liquid Readily Marketable Inventories.

The strategic logic was elegant, almost poetic in its simplicity. Merging with Viterra augments Bunge's existing footprint with significant grain and softseed handling capacity, while expanding origination capabilities in key regions and crops where Bunge is underrepresented. This wasn't just adding scale—it was filling gaps in a global chess board where every empty square represented missed arbitrage opportunities.

Viterra brought assets that read like a wish list for any agricultural trader. More than 10 million tonnes of grain storage capacity in Australia meant Bunge could now play the Pacific wheat trade. Viterra specialized in grain handling and marketing, and was one of Canada's largest agri-product retailers with more than 250 retail locations in Western Canada and 17 in Australia. Viterra is the largest producer of industrial oats in North America. These weren't random assets—they were strategic positions in markets where Bunge had been structurally disadvantaged.

The combined entity's scale defies comprehension. The combined company owns and operates more than 300 grain storage facilities, more than 40 port terminals and more than 155 processing, refining and packaging facilities. Bunge now will have a presence in more than 50 countries and employ more than 37,000 people—though post-merger, the two companies will have more than 50,000 employees worldwide and total revenues north of $100 billion.

But scale alone doesn't justify a merger of this magnitude. The real value lies in what Heckman called "optionality." When you control grain elevators in Saskatchewan, ports in Brazil, crushing facilities in China, and now Australian wheat terminals, you're not just moving commodities—you're orchestrating global food flows. A drought in Australia? Route Canadian wheat through those same terminals. Brazilian soybean crop delayed? Fill Chinese contracts with U.S. supplies. Every disruption becomes an opportunity when you have alternatives.

The regulatory gauntlet proved more challenging than anticipated. The companies had hoped to have the deal completed in 2024, but the regulatory approval process took longer than expected. The Canadian Competition Bureau's concerns were particularly sharp. The Competition Bureau concluded that the proposed acquisition is likely to result in substantial anti-competitive effects and a significant loss of rivalry between Viterra and Bunge in agricultural markets in Canada, specifically citing harm to competition in markets for grain purchasing in Western Canada, as well as for the sale of canola oil in Eastern Canada.

The Chinese approval, which came last week before the July 2025 closing, was the final piece of a complex puzzle. The merger was approved last week by China, which was the last regulatory hurdle Bunge needed to clear to finalize the deal after gaining conditional approvals from regulators in Canada, the European Union and other markets. China's blessing wasn't just regulatory—it was geopolitical validation that even in an era of deglobalization, food security trumps protectionism.

The financial engineering behind the deal was as sophisticated as the operational logic. Bunge plans to repurchase $2.0 billion of Bunge's stock to enhance accretion to adjusted EPS, intending to commence repurchases as soon as practically possible and complete the Repurchase Plan no later than 18 months post transaction close. This buyback serves multiple purposes: it concentrates ownership for existing shareholders, signals management confidence, and mathematically ensures the deal is accretive from day one.

The synergy targets seem conservative at first glance—approximately $250 million of annual gross pre-tax operational synergies within three years of completion. But the real value isn't in cost cutting; it's in what the merger announcement delicately calls "significant incremental network synergies across joint commercial excellence opportunities, vertical integration efficiencies, and improved logistics optimization and trading optionality from a larger and broader network". Translation: when you combine two intelligence networks, two sets of customer relationships, and two trading books, the value creation isn't additive—it's exponential.

The governance structure reflects the delicate balance of power. The Bunge Board of Directors is expected to be comprised of eight Bunge nominated representatives and four representatives nominated by Viterra shareholders. Glencore and CPP Investments will each enter into a shareholder agreement with Bunge and each will initially be able to nominate two Bunge board members. This isn't just corporate democracy—it's ensuring that Glencore, one of the world's most sophisticated commodity traders, has a voice in strategic decisions.

The leadership structure announced for the combined entity signals continuity with transformation. Greg Heckman remains CEO, John Neppl continues as CFO, while Viterra CEO David Mattiske joins as Co-Chief Operating Officer alongside Julio Garros. As co-COOs, they will jointly oversee commercial activities including global commodity value chains, country/regional management teams, renewable fuels initiatives, regenerative agriculture solutions and industrial operations & safety.

The timing of the merger, closing in July 2025 amid weak oilseed processing margins—particularly in South America—and a nearly 50% drop in full-year net income for fiscal 2024, might seem counterintuitive. But that's exactly the point. Commodity trading is cyclical, and the best time to double down is when margins are compressed and competitors are retreating. The combined entity's relatively more stable cash flows from the larger, more diversified footprint means it can weather downturns that would cripple smaller players.

Perhaps most intriguingly, the merger positions Bunge for a future that goes beyond traditional commodity trading. The emphasis on "renewable fuels initiatives" and "regenerative agriculture solutions" in the leadership structure isn't corporate greenwashing—it's recognition that the next century of agricultural trading will be defined by carbon as much as calories. When you control the infrastructure that moves food from farm to fork, you also control the data, the relationships, and the leverage points needed to transform how food is produced, not just how it's traded.

VIII. Challenges, Controversies & ESG Issues

The year 2006 should have been a victory lap for Bunge. Commodity prices were soaring, China's appetite for soybeans seemed insatiable, and the company's stock had tripled since its IPO. Instead, Bunge found itself in the crosshairs of the Environmental Protection Agency. The EPA filed charges against Bunge regarding pollution emissions involving twelve soybean processing plants and corn mills in eight states throughout the US. The lawsuit claimed Bunge violated the Clean Air Act by constructing major modifications that increased emissions. Bunge was required to implement engineering changes and pollution control projects, estimated to cost $12 million, to reduce emissions at the facilities by 2,200 tons a year.

The EPA settlement was more than a financial hit—it was a wake-up call that the era of operating in the shadows was over. The settlement also called for Bunge to pay a cash penalty of $625,000 and to spend $1.25 million to fund community-based environmental projects. For a company that had spent two centuries avoiding attention, being forced to fund community projects was almost more painful than the fines. It meant acknowledgment that Bunge's operations had community impacts, that its facilities weren't just nodes in a global network but neighbors to real people breathing real air.

But air pollution was just the beginning of Bunge's environmental challenges. The real reputational risk lay in the Amazon, where the company's soybean sourcing was increasingly linked to deforestation. The logic of agricultural expansion is brutal in its simplicity: forest land is cheap, cleared land is valuable, and soybeans grow well on recently deforested soil. Bunge didn't need to cut down a single tree to be complicit—it just needed to buy soybeans from farmers who did.

The 2012 confrontation with Survival International exposed an even darker side of agricultural expansion. Bunge came under criticism from NGO Survival International for sourcing sugarcane from the ancestral land of the Guaraní people in Brazil. It has been reported by the tribe that crop production has brought pesticides and machinery that has damaged their health, as well as restricting them to a small area that has prevented them from hunting and practicing their traditions. The human cost became tragically concrete when in January 2003, opposition from the tribe had led to the killing of their chief Marcus Vernon by ranchers.

The Guaraní controversy forced Bunge to confront a fundamental contradiction in its business model. The company's entire value proposition rested on efficiently connecting farmers to consumers, but what happened when those farmers were farming on stolen land? When efficiency meant indigenous displacement? In 2012, survivors were requesting Bunge follows the example of the company Raízen, which agreed to stop the sourcing of sugarcane from the area. The fact that competitors were already taking action made Bunge's position even more untenable.

The company's response to these challenges has evolved from denial to damage control to genuine transformation—though skeptics argue it's still more rhetoric than reality. Bunge now publishes sustainability reports that would have seemed like science fiction to Johann Bunge in his Amsterdam counting house. The company has committed to achieving deforestation-free supply chains, though the definition of "deforestation-free" remains conveniently flexible.

The climate change dimension adds another layer of complexity. Bunge's business model is both threatened by and contributing to climate change. Extreme weather events—droughts, floods, unexpected freezes—can destroy carefully hedged positions in minutes. A trader might have locked in a margin on Brazilian soybeans, only to watch the entire crop disappear in unprecedented flooding. Climate volatility isn't just a risk to manage; it's an existential threat to a business model predicated on predictable seasonal patterns.

Yet Bunge is also part of the climate problem. The company's scope 3 emissions—those from its supply chain—dwarf its direct emissions. Every hectare of forest cleared for soybean production, every ton of nitrogen fertilizer applied to corn fields, every diesel-powered combine harvesting wheat contributes to emissions that ultimately trace back to Bunge's demand for commodities. The company can make its own operations carbon neutral, but if its suppliers are carbon intensive, is that anything more than greenwashing?

The social challenges extend beyond indigenous rights. Bunge operates in some of the world's most corrupt and violent regions. Brazilian agribusiness has long been associated with land grabbing, slave labor, and assassination of environmental activists. The company can claim it doesn't engage in these practices directly, but when you're buying commodities in a market where such practices are endemic, how clean can your hands really be?

The governance challenges of managing a global commodity trader add another dimension of risk. The information asymmetries that create trading profits also create opportunities for manipulation. When your traders know about a drought before markets do, when they can influence prices through strategic buying or selling, when they operate in jurisdictions with weak regulatory oversight—the temptation for market manipulation is constant. The modern Bunge has responded with increasingly sophisticated ESG commitments. The company has set an ambition to achieve net zero GHG emissions by 2050 or sooner, including at least 95% of its Scope 1 and 2 emissions. Bunge announced Science-Based Targets to achieve absolute reduction in carbon emissions for its own operations and in supply chains. To meet these targets, Bunge will make significant enhancements across global operations, promote regenerative farming practices, and emphasize decarbonization in shipping and logistics.

The progress has been measurable if incremental. Bunge revealed that in 2023 it achieved a total reduction of its Scope 1 and 2 emissions of around 15.8% and saw a reduction of 10.6% in Scope 3 emissions from its value chains. In 2025, the company's Global Sustainability Report reveals it has successfully reduced its Scope 1 and 2 emissions by 19.7% and its Scope 3 emissions by 6.7%, all measured against a 2020 baseline.

But critics remain unconvinced. NGO Mighty Earth has complained that the soy giant remains out of step with the European Union Deforestation Regulation (EUDR) which has a legally binding 2020 cut-off date. The Environmental Investigation Agency (EIA) has also alleged that Bunge has been purchasing palm oil from mills linked to recent deforestation in Indonesia. As Alex Wijeratna of Mighty Earth warns: "Our concern is there will be a race this year to deforest even more natural ecosystems, pushing the Cerrado and other biomes like the Pantanal even further towards collapse."

The company has achieved 100% traceability in monitoring soybean sources from priority Brazilian regions affected by deforestation and Land Use Change. But traceability isn't the same as sustainability. Knowing exactly which farm destroyed which patch of Cerrado doesn't make the destruction disappear—it just makes it documented.

The financial integration of ESG is perhaps the most interesting development. As of January 1, 2021, performance-based sustainability goals are a component of the annual incentive bonuses paid to Bunge's executive team and over 5,500 of employees. The interest rate on credit facilities is linked to credit ratings and to five core sustainability targets, creating a meaningful connection between Bunge's capital structure and sustainability strategy.

This isn't just greenwashing—it's putting real money at stake. When traders' bonuses depend partly on reducing emissions, when the CFO's cost of capital rises if deforestation targets are missed, sustainability moves from corporate communications to corporate strategy. The compensation framework based on a pay-for-performance philosophy with payout now directly impacted by attainment of certain sustainability targets creates aligned incentives throughout the organization.

The recognition has followed. For 2021 and 2022 Bunge was named "Most Responsible Companies" by Newsweek Magazine. Over 3,000 investors surveyed by Institutional Investor placed Bunge at #3 in the Food Producer category for ESG performance and transparency. In 2021, Bunge received "B" ratings—leading scores in their peer group—for CDP Forests, Water and Climate.

Yet the fundamental tension remains unresolved. Bunge's business model depends on agricultural expansion and intensification. Every ton of additional soybean production requires either more land (deforestation risk) or more inputs (chemical pollution risk). The company can make its operations more efficient, its supply chains more traceable, its governance more transparent, but can it truly be sustainable while facilitating the conversion of natural ecosystems into industrial monocultures?

The answer may lie in transformation rather than optimization. Bunge's investments in regenerative agriculture, alternative proteins, and renewable fuels suggest a recognition that the future of agricultural trading might look very different from its past. The company that once profited from clearing the pampas might need to profit from restoring them. The traders who once arbitraged grain might need to arbitrage carbon credits.

IX. Business Model Analysis & Playbook

To understand Bunge's business model at its deepest level, imagine you're playing a massively multiplayer game where the board is Earth itself, the pieces are ships and silos and processing plants, and the currency is information converted into arbitrage. The rules are simple: buy low, sell high, and never be caught without options. The execution is anything but.

The foundation of Bunge's playbook rests on information asymmetry—not the illegal kind that lands you in prison, but the legal kind that builds empires. When a Bunge trader in Singapore knows about a drought in Australia before a buyer in Jakarta, that knowledge gap represents pure profit. The company doesn't need to manipulate markets; it just needs to understand them faster and deeper than anyone else.

This information advantage comes from what military strategists would call "defense in depth." Bunge doesn't rely on a single source or method. Satellite imagery provides one layer—tracking vegetation indices that reveal crop stress weeks before it's visible to the human eye. Ground networks provide another—those 70,000 farmer relationships aren't just commercial transactions but intelligence nodes, each one reporting on local conditions, planting intentions, harvest timing. Financial markets provide a third—futures prices, currency movements, shipping rates all contain signals about supply and demand imbalances.

The physical assets aren't just infrastructure—they're options on future price movements. Every grain silo is essentially a time machine, allowing Bunge to buy grain in October and sell it in February. Every processing plant is an alchemist's laboratory, transforming cheap soybeans into more valuable oil and meal. Every port terminal is a gateway between price regimes, connecting low-price production regions to high-price consumption markets.

The vertical integration strategy follows a counterintuitive logic: own the bottlenecks, outsource everything else. Bunge doesn't own farms—too capital intensive, too risky, too visible. But it owns the grain elevators where farmers must deliver their crops. It doesn't own ships—charter rates are volatile and vessels are expensive. But it owns the port terminals where those ships must load. This selective ownership creates what economists call "monopolistic competition"—not quite a monopoly, but close enough to extract rents.

Risk management at Bunge operates on multiple dimensions simultaneously. Price risk gets hedged through futures markets—but not completely, because perfect hedges eliminate profits along with risks. Basis risk (the difference between local cash prices and futures) gets managed through strategic inventory positioning. Currency risk gets hedged selectively—protecting against catastrophic moves while maintaining exposure to favorable trends. Credit risk gets managed through elaborate documentation, insurance, and the ultimate enforcement mechanism: if you don't pay Bunge, you don't eat.

The capital allocation philosophy reflects a fundamental truth about commodity trading: returns are volatile but mean-reverting. In good years, Bunge generates massive cash flows—the question is what to do with them. The answer has evolved from family dividends to public buybacks, but the principle remains: extract capital during feast years to survive famine years. This isn't short-term thinking; it's recognition that commodity cycles are as inevitable as seasons.

The competitive dynamics among the ABCD companies resemble a Cold War more than hot competition. Each company knows that aggressive price competition would destroy margins for everyone. Instead, they compete on execution—who can move grain from Brazil to China a day faster, a dollar cheaper, a grade better. They compete on relationships—which company do farmers trust when credit is tight, which do food manufacturers call when supplies are uncertain. They compete on intelligence—who knows first, who understands best, who acts fastest.

The lessons for entrepreneurs are profound but not easily replicated. Patient capital matters—Bunge spent two centuries building its network, and no amount of venture funding can compress that timeline. Geographic diversification isn't just risk management; it's opportunity multiplication—every market dislocation somewhere creates arbitrage opportunities elsewhere. Vertical integration in commodities isn't about controlling everything; it's about controlling the crucial nodes where value crystallizes.

The power of Bunge's model lies in its antifragility—it doesn't just survive volatility; it feeds on it. A stable world with predictable harvests, steady prices, and smooth trade would be Bunge's nightmare. Every disruption—whether drought, war, pandemic, or policy change—creates price dislocations that traders can exploit. The company has survived Napoleon's blockades, two world wars, countless coups, and multiple commodity crashes not despite these disruptions but because of them.

Modern technology is amplifying these advantages rather than eroding them. Machine learning algorithms can process satellite imagery faster, but they still need ground truth from farmer relationships. Blockchain can make transactions more transparent, but it can't replace the trust built over generations. Digital platforms can connect buyers and sellers directly, but they can't manage the physical logistics of moving 75 million tons of grain across oceans.

The sustainability transformation adds another layer to the playbook. Carbon markets are essentially commodity markets with a moral dimension. Regenerative agriculture creates new products to trade—carbon credits, biodiversity offsets, water rights. The company that mastered arbitraging calories might master arbitraging carbon. The infrastructure that moves soybeans from farm to fork can move environmental attributes from producers to consumers.

The Viterra merger represents the ultimate expression of this playbook: when you can't build fast enough, buy. When markets consolidate, consolidate faster. When regulators scrutinize, comply minimally but completely. When stakeholders demand change, change visibly but preserve optionality. It's not cynical; it's strategic. The company that survived 200 years didn't do so by fighting change but by surfing it.

For investors evaluating Bunge, the question isn't whether the business model works—history has proven it does. The question is whether it can evolve fast enough for a world where food security, climate change, and social justice are converging into a single crisis. Can a company built on exploiting inefficiencies thrive in a world demanding efficiency? Can traders trained to profit from volatility adapt to stakeholders demanding stability? Can an enterprise rooted in opacity succeed in an age of transparency?

X. Bear vs. Bull Case & Future Outlook

The bull case for Bunge writes itself in the demographics of hunger and the geography of abundance. By 2050, Earth will host 10 billion people, most of them in cities, most wanting to eat meat, all needing protein. The gap between where food is produced (the Americas, Australia, the Black Sea region) and where it's consumed (Asia, Africa, the Middle East) isn't closing—it's widening. Every mouth that shifts from rice to beef multiplies the demand for soybeans to feed those cattle. Every hectare of farmland that becomes a city increases dependence on the remaining farms. Bunge doesn't just benefit from these trends; it's the infrastructure that makes them possible.

The Viterra merger transforms a strong position into a dominant one. Combined, the two companies market more than 230 million metric tons of commodities and products annually. That's not just scale—it's gravitational pull that bends markets around it. When you control that much flow, you don't predict prices; you influence them simply by choosing when and where to move inventory. The merger creates unmatched scale and reach that competitors can't replicate without triggering antitrust interventions that Bunge has already navigated.

Climate change, paradoxically, strengthens Bunge's position. Not because climate change is good—it's catastrophic—but because it makes agricultural production more volatile and geography more important. When Brazilian droughts coincide with Ukrainian floods, when Canadian wheat freezes while Australian wheat burns, the company with positions in all these markets can arbitrage catastrophe into profit. The combined company's relatively more stable cash flows from the larger, more diversified footprint means it can weather disruptions that destroy single-region players.

The renewable fuels revolution opens entirely new markets. Biodiesel, renewable diesel, sustainable aviation fuel—all require feedstocks that Bunge controls. The same soybeans that feed Chinese pigs can power European trucks, depending on which market pays more. The infrastructure built for food can seamlessly shift to fuel, doubling the addressable market without doubling the assets. Bunge's expertise in crushing oilseeds translates directly into producing renewable fuel feedstocks.

Alternative proteins paradoxically benefit Bunge despite threatening traditional meat. Plant-based meat requires protein isolates, oils, and other ingredients that come from the same soybeans and other crops Bunge already processes. Whether consumers eat beef or Beyond Beef, Bunge wins. The company's expertise in molecular manipulation of plant compounds positions it perfectly for a world where food is increasingly engineered rather than grown.

The digital transformation of agriculture creates new moats rather than destroying old ones. Bunge's vast data set—decades of yield data, price patterns, weather correlations—becomes more valuable when fed into machine learning models. The company that knows how every field performed for the last 50 years has an insurmountable advantage in predicting how it will perform next year. Digital platforms don't disintermediate Bunge; they amplify its intelligence advantage.

But the bear case carries its own compelling logic. Start with the obvious: Bunge operates in a brutal industry where margins are measured in single digits and mistakes measured in hundreds of millions. The company cited weak oilseed processing margins—particularly in South America—dragging down quarterly earnings and contributing to a nearly 50% drop in full-year net income for fiscal 2024. When your best year can be followed by your worst, what multiple should investors pay?

The commodity supercycle that lifted all boats from 2000 to 2014 has ended, replaced by a grinding bear market where supply consistently exceeds demand. China's growth is slowing, its protein consumption plateauing, its soybean imports moderating. The great Chinese bid that drove two decades of agricultural expansion is weakening just as productive capacity peaks. Brazil alone could feed the world's additional soybean demand for the next decade without clearing another hectare.

Technological disruption threatens from multiple angles. Precision agriculture reduces the inefficiencies that traders exploit—when farmers know exactly how much fertilizer to apply, when to plant, when to harvest, the information asymmetries narrow. Direct farmer-to-consumer platforms bypass traditional traders. Blockchain enables trust without intermediaries. Synthetic biology promises proteins without agriculture. What happens to soybean crushers when soybeans become obsolete?

ESG pressures are more than reputational risks—they're existential threats to the business model. European regulations on deforestation aren't just compliance costs; they're barriers to sourcing from the lowest-cost regions. Carbon taxes don't just increase expenses; they fundamentally alter the economics of moving bulk commodities across oceans. When your business model depends on turning fossil fuels into food and shipping it globally, how do you survive in a net-zero world?

The Viterra merger itself might be a trap. Mega-mergers in commodity industries have a terrible track record—Glencore's acquisition of Xstrata, BHP's pursuit of Rio Tinto, Vale's purchase of Inco all destroyed value. The promised synergies rarely materialize while the integration costs always exceed budgets. Combining two complex global organizations during a commodity down cycle while facing regulatory scrutiny and stakeholder pressure is a recipe for disaster, not dominance.

Competition is intensifying from unexpected directions. State-owned enterprises from China and the Middle East are buying direct stakes in farmland and infrastructure, bypassing traders entirely. Tech giants like Microsoft and Amazon are entering agriculture with AI and cloud services that democratize information advantages. Even farmers are organizing into cooperatives that market directly to end users, cutting out middlemen.

The scenarios for the next decade span from triumph to catastrophe. In the optimistic case, Bunge successfully integrates Viterra, captures the synergies, and emerges as the undisputed leader in global agricultural trade. Margins recover as supply and demand rebalance. The company successfully transitions to sustainable sourcing while maintaining profitability. The stock re-rates from a cyclical commodity trader to a stable food infrastructure play, commanding multiples similar to consumer staples companies.

The pessimistic scenario sees integration failures compound operational challenges. Key talent leaves during the merger chaos. Regulatory interventions force asset sales at fire-sale prices. Climate events create losses that overwhelm risk management systems. ESG pressures make entire sourcing regions untouchable. The company enters a vicious cycle of declining margins, reduced investment, and loss of market share to more nimble competitors.

The most likely scenario lies between these extremes: Bunge muddles through, capturing some synergies while missing others, adapting partially to sustainability demands while resisting others, maintaining its position without significantly expanding it. The company remains essential but unloved, profitable but not valuable, surviving but not thriving.

For investors, the fundamental question isn't whether Bunge will exist in 10 years—it will. The question is whether it will be worth more or less than today. The answer depends on variables largely outside management's control: Chinese protein demand, Brazilian weather, regulatory evolution, technological disruption. Betting on Bunge is betting on volatility itself—appropriate for a company that has turned chaos into profit for two centuries.

XI. Closing Thoughts

Standing back from the spreadsheets and supply chains, the weather derivatives and crushing spreads, what does Bunge really tell us about capitalism, globalization, and the future of food? The answer is both inspiring and unsettling, a reminder that the systems feeding humanity are as fragile as they are essential.

The two-century survival of Bunge offers a masterclass in institutional adaptation. This is a company that predates the telephone yet now uses artificial intelligence, that started moving goods by horse cart and now tracks shipments by satellite. Each generation of leadership faced existential threats—wars, revolutions, technological disruptions—and somehow found ways not just to survive but to thrive. The lesson isn't about any specific strategy but about the meta-strategy of maintaining flexibility within structure, innovation within tradition.

What makes Bunge fascinating is the paradox of invisible giants—companies so essential that civilization would collapse without them, yet so unknown that most people can't pronounce their names. The average person interacts with Bunge's products dozens of times daily—the oil in their salad dressing, the feed that grew their chicken, the fuel in their biodiesel—without any awareness of the company's existence. This invisibility is both a weakness (no brand loyalty, no pricing power) and a strength (no boycotts, no political targeting).

The family business that became a public corporation offers lessons about the lifecycle of enterprises. The Bunge and Born families built something that transcended their own mortality, creating an institution that survived long after the founders' grandchildren forgot why great-grandfather left Amsterdam. Yet something was lost in the transition from family to market control—the patient capital that could weather bad decades, the relationship focus that valued trust over contracts, the sense of mission beyond margins.

The globalization story that Bunge embodies is ending, replaced by something we don't yet understand. The company thrived in an era of falling trade barriers, cheaper shipping, and expanding supply chains. Now it must navigate rising protectionism, supply chain reshoring, and food nationalism. The infrastructure built to connect global markets might need to be reconfigured for regional autarky. The arbitrageur of global inefficiencies might become the manager of regional redundancies.

The commodity trading model itself faces an existential question: what is the social value of speculation? Bunge would argue it provides price discovery, risk management, and supply chain efficiency. Critics would counter that it extracts rents from farmers and consumers while contributing nothing tangible. The truth, as always, lies somewhere between—Bunge does create value through logistics and processing, but it also captures value through information advantages and market power that seem increasingly anachronistic in a digital age.

The sustainability transformation isn't just about carbon credits and deforestation pledges—it's about whether a company built on exploiting nature can learn to regenerate it. Can the same capabilities that turned the Cerrado into soybean fields turn degraded pastures into carbon sinks? Can the intelligence network that tracks crop yields track biodiversity? Can the risk management systems that hedge price volatility hedge planetary boundaries? These aren't just corporate strategy questions; they're existential questions for humanity.

The Viterra merger represents more than corporate consolidation—it's a bet on the future of food itself. By combining these assets, Bunge is essentially saying that despite all the disruption—alternative proteins, vertical farming, synthetic biology—the fundamental business of moving bulk commodities from where they're grown to where they're consumed will remain essential. It's a conservative bet in revolutionary times, a doubling down on the physical when everything is becoming digital.

For students of business history, Bunge offers a crucial lesson: longevity comes not from avoiding change but from surfing it. The company didn't survive 200 years by doing the same thing; it survived by doing different things with the same capabilities. The core competence wasn't grain trading—it was arbitrage. The sustainable advantage wasn't infrastructure—it was intelligence. The moat wasn't capital—it was relationships.

Yet Bunge also illustrates the limits of corporate adaptation. No matter how sophisticated its risk management, it can't hedge against the exhaustion of soil. No matter how efficient its logistics, it can't move water from where it's abundant to where it's scarce. No matter how clever its trading, it can't create calories from nothing. The company that mastered the movement of food confronts the harder challenge of ensuring food exists to move.

The final paradox is that Bunge's greatest success might be its eventual obsolescence. If humanity successfully develops local food systems, alternative proteins, and circular agriculture, the need for global commodity traders diminishes. If technology democratizes information and logistics, the advantages of scale erode. If sustainability demands shorter supply chains, the infrastructure spanning oceans becomes stranded assets. Bunge's ultimate victory might be creating a world that no longer needs Bunge.

But until that distant future arrives—if it ever does—someone needs to perform the mundane miracle of feeding billions of people who live nowhere near farms. Someone needs to bear the risks of weather and war, managing the complexity of turning seeds into sustenance. Someone needs to stand at the intersection of agriculture and industry, nature and culture, scarcity and abundance, making markets that make meals possible.

For two centuries, that someone has been Bunge. The Amsterdam trading house that became a global giant, the family firm that became a public corporation, the grain trader that became a food system architect. Its story isn't just corporate history—it's the hidden infrastructure of human civilization, the invisible hand made manifest in soybeans and shipping routes.

Whether Bunge thrives or merely survives in its third century depends on questions nobody can answer: Will the world become more connected or more fragmented? Will climate change destroy agriculture or transform it? Will technology democratize food production or concentrate it further? Will society value resilience over efficiency, sustainability over scale, transparency over expertise?

What's certain is that the questions Bunge must answer—how to feed 10 billion people on a finite planet—are questions humanity must answer. The company's solutions might not be our solutions, its interests might not align with our interests, but its challenges are absolutely our challenges. In wrestling with these challenges, Bunge isn't just writing its next chapter; it's helping write ours.

The grain traders of tomorrow might look nothing like the grain traders of today, but they'll face the same fundamental challenge that Johann Peter Gottlieb Bunge faced in 1818: how to move value across space and time, turning surplus into sustenance, scarcity into opportunity, chaos into commerce. The methods will evolve, the markets will transform, but the mission remains: connecting those who grow with those who consume, those who have with those who need, those who risk with those who reward.

That's the real lesson of Bunge's 200-year journey—not that any particular strategy or structure guarantees success, but that serving essential human needs while adapting to changing conditions creates a kind of institutional immortality. The company that feeds the world becomes, in a very real sense, too essential to fail. Whether that's a promise or a threat depends on your perspective. But either way, it's a fact that investors, regulators, and society itself must reckon with.

In the end, Bunge's story is our story—a tale of how humanity learned to feed itself at scale, with all the triumph and tragedy that entails. It's a story still being written, with chapters yet unknown. But one thing seems certain: as long as people need to eat and food needs to move, something like Bunge will exist to make it happen. The names might change, the ownership might shift, the methods might evolve, but the function remains eternal. In that sense, Bunge isn't just a company—it's a civilization requirement, dressed up in corporate form, as essential and problematic as civilization itself.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube