Apollo Global Management: The Story of Wall Street's Credit Colossus

I. Introduction & Episode Roadmap

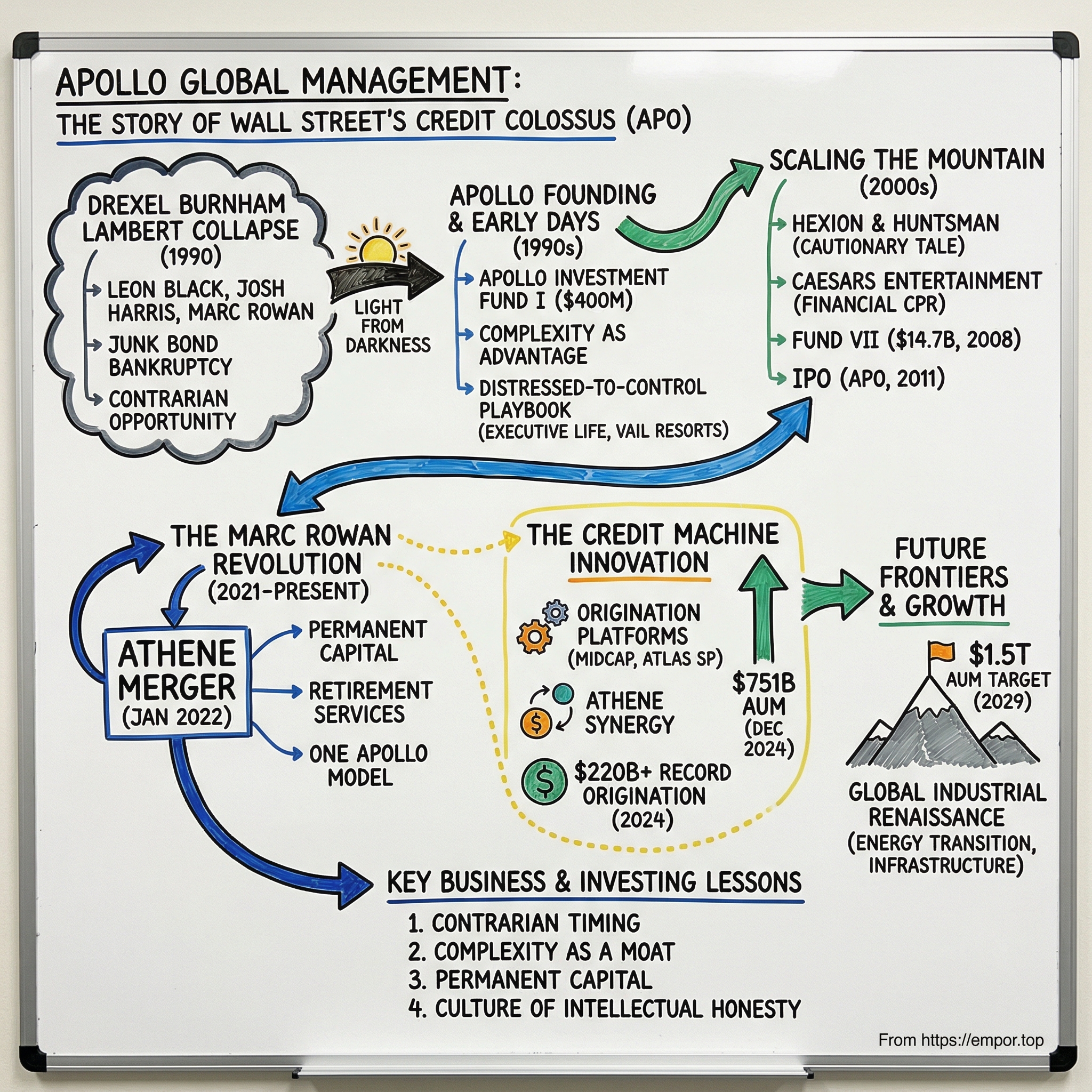

Picture this: It's March 1990, and the legendary Drexel Burnham Lambert—the fifth-largest investment bank in America, the house that junk bonds built—is collapsing into bankruptcy. As federal prosecutors circle and clients flee, three executives meet in a Manhattan conference room. They're watching their empire burn, but instead of despair, they see opportunity. Leon Black, the firm's former head of mergers and acquisitions, turns to his lieutenants Josh Harris and Marc Rowan. "Everyone thinks high-yield is dead," he says. "That's exactly why we need to start now."

That contrarian bet would spawn Apollo Global Management, today a $650 billion behemoth that has fundamentally reshaped how Wall Street thinks about credit, retirement, and the very nature of banking itself. This isn't just another private equity success story—it's the tale of how three refugees from finance's most spectacular implosion built something far more powerful than what they left behind. The question everyone asks is: How did Apollo become what traditional banks used to be—and arguably much more? The answer lies not in private equity deals that grab headlines, but in a credit machine that now manages $392 billion invested in credit and has fundamentally reimagined what it means to be a lender in the 21st century. In 2024, the firm's record origination activity exceeded $220 billion—more lending than many major banks.

But here's the twist that makes this story fascinating: While competitors like Blackstone and KKR built their empires on leveraged buyouts and the classic private equity playbook, Apollo quietly assembled something different—a perpetual capital vehicle through insurance that would transform it from a fund manager into something approaching a financial institution. The approximately $751 billion of assets under management as of December 31, 2024 tells only part of the story. The real revolution was turning retirement anxiety into Wall Street gold.

Over the next several hours, we'll trace this unlikely journey from the ashes of Drexel through the creation of a new kind of financial powerhouse. We'll explore how three men built a firm that doesn't just invest money but originates it, doesn't just manage funds but creates permanent capital, and doesn't just compete with banks but may be rendering them obsolete in entire segments of the market.

This is the story of contrarian timing, institutional innovation, and the transformation of American finance. It's about seeing opportunity where others see only risk, building complexity as a competitive moat, and ultimately, creating a business model so powerful that it's reshaping how trillions of dollars flow through the global economy.

II. The Drexel Burnham Lambert Origins

The conference room at 60 Broad Street reeked of cigarette smoke and desperation on that February morning in 1990. Drexel Burnham Lambert, the firm that had revolutionized American finance with high-yield bonds, was dying. Federal investigators had already extracted a $650 million fine—the largest in securities history. Michael Milken, the junk bond king himself, would soon be heading to federal prison. As employees packed boxes and clients pulled billions in assets, Leon Black sat in his corner office, making phone calls that would change his life.

Black wasn't just any Drexel executive. As head of mergers and acquisitions, he had been Milken's East Coast lieutenant, the bridge between the junk bond machine in Beverly Hills and the establishment bankers in Manhattan. While Milken created the securities, Black figured out how to use them—engineering leveraged buyouts that would have been impossible just years earlier. He understood something that would prove invaluable: Drexel's collapse wasn't the end of high-yield; it was the beginning of an extraordinary opportunity.

"Everyone thought we were radioactive," Josh Harris would later recall about those early days. Harris, then just 26, had joined Drexel straight from Harvard Business School and quickly became one of Black's protégés. Where Black was intense and demanding—known for his 3 a.m. phone calls and encyclopedic knowledge of bond covenants—Harris brought operational discipline and an ability to execute complex transactions under pressure.

The third member of this unlikely trinity was Marc Rowan, a tax lawyer turned investment banker who had joined Drexel from a white-shoe law firm. If Black was the visionary and Harris the operator, Rowan was the architect—the one who could structure deals that seemed impossibly complex, finding value in the fine print that others overlooked. His ability to see around corners would later prove essential to Apollo's most audacious moves.

The Drexel DNA ran deep in all three men, but it wasn't nostalgia that brought them together. It was pragmatism. They had learned from Milken that credit markets were inefficient, that fear created opportunity, and that patient capital could generate extraordinary returns. But they had also witnessed firsthand what happened when ambition outran ethics, when leverage became recklessness. By June 1990—just months after Drexel's demise—they had done something remarkable. Within six months after the collapse of Drexel, Apollo launched Apollo Investment Fund L.P., the first of its private-equity investment funds, formed to make investments in distressed companies. Apollo raised around $400 million of investor commitments based on Leon Black's reputation as a prominent lieutenant of Michael Milken and a key player in the buyout boom of the 1980s.

Think about that timing. The savings and loan crisis was destroying regional banks. The high-yield market had essentially ceased to exist. Commercial real estate was in free fall. Most rational investors were running for the exits. But Black saw what others missed: When everyone is selling, that's precisely when you should be buying.

The name "Apollo" itself was telling—the Greek god of prophecy, light emerging from darkness. It signaled both ambition and resurrection. But the early days were far from divine. The trio worked out of cramped offices, with Black famously conducting meetings while pacing around conference tables, interrogating every assumption, every model, every risk.

Tony Ressler, another Drexel alumnus who would later leave to found Ares Management, was also among the original founding team. His presence added another layer of credit expertise, though his departure in 1997 would later create one of Apollo's fiercest competitors—a reminder that even in the beginning, the seeds of future rivalries were being planted.

What made Apollo different from the start wasn't just contrarian timing—it was intellectual framework. While other firms were chasing leveraged buyouts at peak multiples, Apollo was developing what would become its signature approach: complexity as competitive advantage. They would do deals others couldn't understand, structure transactions others couldn't execute, and find value where others saw only wreckage.

The Drexel collapse had taught them that leverage without discipline was destruction waiting to happen. But it had also shown them that credit markets were fundamentally inefficient, that patient capital could generate extraordinary returns, and that distress created opportunity for those brave enough to seize it. These lessons, learned in the ashes of Wall Street's most spectacular failure, would shape everything that followed.

III. The Distressed-to-Control Playbook (1990s)

The opportunity came faster than anyone expected. In April 1991, Executive Life Insurance Company of California—once the nation's largest junk bond investor—collapsed under the weight of its Drexel-era portfolio. State regulators seized the company, suddenly needing to offload $8 billion in assets that nobody wanted to touch. For Apollo, this wasn't just a deal; it was destiny.

In one of the firm's earliest and most successful deals, Apollo acquires Executive Life Insurance Company's bond portfolio, establishing what will become the largest credit platform among alternative asset managers. The transaction was byzantine in its complexity, involving French bank Crédit Lyonnais and a web of offshore entities that would later attract regulatory scrutiny. But at its core was a simple insight: These bonds weren't worthless—they were just unfashionable.

Apollo paid roughly 50 cents on the dollar for securities that, with patience and restructuring, would eventually return multiples of that investment. The deal generated returns exceeding 30% annually and established Apollo's reputation as the firm that could handle complexity others wouldn't touch. It also provided something even more valuable: a template.

The distressed-to-control playbook was elegant in its brutality. Find companies crushed by debt but with viable operations. Buy the distressed debt at deep discounts. Convert that debt to equity through bankruptcy proceedings. Exit with control of a restructured company at a fraction of its potential value. Rinse, repeat, compound.

Vail Resorts became an early proof of concept. The iconic ski resort had filed for bankruptcy in 1991, buried under debt from an ill-timed expansion. Apollo acquired the senior debt, converted to equity, brought in new management, and eventually took the company public in 1997 for a spectacular return. What had been a distressed asset became a crown jewel.

The Resolution Trust Corporation, created to handle the savings and loan crisis wreckage, became Apollo's shopping mall. While others saw toxic assets, Apollo saw mispriced opportunities. They acquired loan portfolios, real estate holdings, and distressed securities at prices that assumed permanent impairment. Time after time, patient workout strategies proved those assumptions wrong.

But the real genius of the 1990s wasn't just the deals—it was the culture being forged. Apollo developed what insiders called "the machine": rigorous analytical processes that could dissect complex capital structures, model multiple scenarios, and identify the precise fulcrum security that would maximize returns. Every Monday morning, the entire investment team would gather for what became known as "Monday meetings"—grueling sessions where Black would interrogate every assumption, challenge every thesis, and demand intellectual honesty above all else. The 1997 departure of Tony Ressler to co-found Ares Management with former Apollo partner John H. Kissick marked a critical juncture. In 1997, he co-founded Ares Management with former Apollo Global Management co-worker John H. Kissick and Bennett Rosenthal, who joined the group from the global leveraged finance group at Merrill Lynch, to manage a $1.2 billion market value collateralized debt obligation vehicle. The split was amicable on the surface—Ressler was Black's brother-in-law, married to his sister Debra—but it represented a philosophical divergence. Ares would focus more purely on credit strategies, while Apollo increasingly looked toward traditional private equity. The competition would push both firms to excellence.

By decade's end, Apollo had established itself as the master of complexity. Fund III, raised in 1995 with $1.5 billion from investors including CalPERS and the General Motors pension fund, proved that institutional capital was ready to embrace distressed strategies at scale. The firm's ability to navigate bankruptcy courts, restructure operations, and create value from chaos had become legendary.

But the real innovation was psychological. While competitors feared distressed situations, Apollo embraced them. They understood that complexity created barriers to entry, that patience generated alpha, and that the best investments were often the ones nobody else wanted to make. This contrarian DNA, forged in the crucible of the 1990s, would define everything that followed.

IV. Scaling the Mountain: Private Equity Expansion (2000s)

The millennium arrived with a problem Apollo hadn't anticipated: They were too successful at distressed investing. As the economy recovered from the 1990s crises, distressed opportunities became scarce. The firm faced an existential choice—remain a niche distressed player or evolve into something bigger. The answer came in the form of traditional leveraged buyouts, but with an Apollo twist.

The 2004 IPO of Apollo Investment Corporation marked the firm's first foray into public markets, raising $930 million for a business development company that would provide direct lending to middle-market companies. It was a prescient move—Apollo was building credit origination capabilities that would later prove revolutionary. But at the time, it was simply about finding new ways to deploy capital in a world awash with liquidity.

The Hexion Specialty Chemicals saga epitomized both Apollo's ambition and the dangers of that ambition. In 2005, Apollo orchestrated the creation of Hexion through a series of chemical company acquisitions, building a specialty chemicals giant from scratch. Then came the audacious $10.6 billion agreement to acquire Huntsman Corporation in 2007—a deal that would create a global chemicals powerhouse.

But as credit markets froze in 2008, Apollo tried to walk away from the deal, claiming material adverse changes. Huntsman sued. The Delaware courts sided with Huntsman. The result: a humiliating $1 billion settlement that became a cautionary tale about hubris in leveraged finance. Yet even in failure, Apollo learned—about deal certainty, about reputation risk, about the importance of following through on commitments. Then came the deal that would haunt Apollo for years: the massive $30.7 billion acquisition of Caesars Entertainment (then called Harrah's) announced in December 2006. The deal was valued at approximately $27.8 billion, including the assumption of approximately $10.7 billion of debt. Apollo and TPG acquired Caesars in a $31 billion buyout in December 2006. The deal did not close until January 2008, largely due to the lengthy background checks regulators conducted on both private equity partners.

The timing could not have been worse. By the time the deal closed in January 2008, the financial crisis was beginning. What looked like a brilliant consolidation play in the casino industry became an albatross. The company that had generated stable cash flows for decades suddenly faced collapsing consumer spending, frozen credit markets, and a debt load that would prove unsustainable.

Yet even in crisis, Apollo demonstrated why it was different. Led by Marc Rowan and a young protégé named David Sambur, Apollo engineered what one observer called "over 50 increasingly complex financial transactions" to keep Caesars alive. They shifted assets between subsidiaries, converted debt to equity, sold properties, and essentially performed financial CPR on a dying patient for seven years.

The 2008 financial crisis, paradoxically, became Apollo's greatest opportunity. While Caesars struggled, Apollo raised Fund VII with approximately $14.7 billion of investor commitments—its largest fund ever at that point. The firm was raising money when others couldn't, deploying capital when others were retreating, and building positions that would generate extraordinary returns as markets recovered.

The decade taught Apollo crucial lessons. Scale mattered—you needed size to compete for the biggest deals. Complexity could be both blessing and curse—it created opportunity but also operational risk. Most importantly, having permanent capital rather than just fund commitments would provide strategic flexibility that traditional private equity lacked. These insights would drive the next phase of Apollo's evolution.

V. Going Public & The Leon Black Era (2011–2021)

The morning of March 29, 2011, Leon Black stood on the floor of the New York Stock Exchange, surrounded by his partners and watching as APO—Apollo's newly minted ticker symbol—began trading. The IPO raised $565 million, valuing the firm at roughly $3.7 billion. For Black, it was vindication—proof that a firm born from Drexel's ashes had become an institution worthy of public markets.

But going public was about more than prestige. It provided permanent capital for growth, currency for acquisitions, and most importantly, the foundation for what would become Apollo's true differentiator: the ability to originate credit at scale rather than just invest in it.

The public Apollo of the 2010s was a deal-making machine. Great Wolf Resorts, acquired in 2012 for $703 million when the family resort operator was unprofitable, exemplified the Apollo playbook—operational improvement, strategic repositioning, and patient capital. Within five years, the company's value had more than doubled.

Chuck E. Cheese, Rackspace, Qdoba—the deals kept coming, each one adding to Apollo's reputation as the firm that could handle complexity. But beneath the headline-grabbing buyouts, something more fundamental was happening. Apollo was quietly building what would become the world's largest alternative credit platform.

The transformation accelerated with strategic acquisitions. Stone Tower Capital in 2011 brought structured credit expertise. CVC Credit Partners in 2013 added European leveraged finance capabilities. Midcap Financial in 2013 provided direct lending origination. Each acquisition wasn't just about assets under management—it was about capabilities, about building the infrastructure to compete with banks.

By 2016, Apollo's credit business had grown to over $100 billion in assets under management, surpassing its private equity holdings. The firm was no longer just buying distressed debt; it was originating loans, structuring securities, and essentially operating as a parallel banking system without the regulatory constraints of traditional banks. But in October 2019, a bombshell: news reports revealed Leon Black's financial relationship with Jeffrey Epstein. The subsequent investigation found that Black paid Epstein $158 million between 2012 and 2017 for what was described as tax and estate planning advice. The payments came after Epstein's 2008 conviction for soliciting prostitution from a minor, a fact that made Black's continued relationship with him inexplicable to many.

The scandal consumed Apollo. Institutional investors threatened to pull capital. Employees demanded answers. The board commissioned an independent investigation by law firm Dechert, which found no evidence that Black was involved in Epstein's criminal activities but confirmed the massive payments for what it described as legitimate tax advice that potentially saved Black over $1 billion in estate taxes.

On January 25, 2021, Black announced he would step down as CEO by his 70th birthday in July, though he would remain as chairman. But the pressure continued. Activist investors pushed for complete separation. Finally, in March 2021, Black resigned all positions at Apollo, ending his three-decade reign.

The Black era had transformed Apollo from a $400 million fund into a global powerhouse managing over $450 billion. But it ended in scandal, raising fundamental questions about governance, judgment, and the concentration of power in alternative asset management. The firm that had survived Drexel's collapse, the dot-com bust, and the financial crisis nearly didn't survive the reputational damage from one man's inexplicable relationship.

VI. The Marc Rowan Revolution (2021–Present)

Marc Rowan didn't give speeches when he became CEO in March 2021. He didn't promise transformation or revolution. He simply went to work, methodically dismantling the cult of personality that had defined Apollo and replacing it with something more powerful: institutional permanence.

Where Black had been mercurial and commanding, Rowan was analytical and collaborative. Where Black had centralized decision-making, Rowan distributed it. Most importantly, where Black had seen Apollo as a private equity firm with a credit business, Rowan saw something entirely different—a retirement services company that happened to do deals. The transformative Athene acquisition, completed in January 2022, was Rowan's masterstroke. Apollo and Athene announced the successful completion of their merger under Apollo Global Management, Inc., a high-growth alternative asset manager with asset management and retirement services capabilities. The $11 billion all-stock deal brought in-house an annuities provider that Apollo had worked with since 2009, creating what Rowan called the "One Apollo" model.

This wasn't just vertical integration—it was a fundamental reimagining of what Apollo could be. Athene provided something no amount of fundraising could match: permanent capital. Insurance float doesn't demand quarterly returns or have redemption rights. It sits, it compounds, and it allows for patient investment strategies that traditional fund structures can't accommodate.

The numbers told the story. By 2024, Apollo's credit business had grown to $392 billion invested in credit, including mezzanine capital, hedge funds, non-performing loans, and collateralized loan obligations, while private equity represented $99 billion invested in private equity. The firm had become what Rowan envisioned: not a private equity firm that did credit, but a retirement services company that happened to do deals.

Josh Harris's departure in January 2022 to focus on sports ownership (he owns the Washington Commanders and Philadelphia 76ers) marked the end of the founding era. In January 2022, co-founder Josh Harris left the company to focus on other business ventures. Of the three men who met in Drexel's ashes, only Rowan remained. But rather than weakening Apollo, the transition strengthened it. The firm was no longer dependent on individual genius but on institutional capability.

The recent mega-deals reflected this evolution. The 90% acquisition of Yahoo in September 2021, the $7.1 billion acquisition of Tenneco in July 2022, and the telecommunications infrastructure plays weren't traditional private equity deals. They were credit origination opportunities, platforms for generating yield in a world starved for income.

Under Rowan, Apollo has also embraced what he calls the "global industrial renaissance"—the massive infrastructure spending required for energy transition, digital transformation, and reshoring of manufacturing. The firm has committed to deploying $50 billion in climate and energy transition investments by 2027, seeing opportunity where others see only cost.

The governance reforms have been equally dramatic. Apollo moved to a single-class share structure, appointed former SEC Chair Jay Clayton as independent board chair, and implemented rigorous compliance protocols. The cowboy culture of the early days has given way to institutional discipline.

Today's Apollo is unrecognizable from the firm that emerged from Drexel's collapse. With approximately $751 billion of assets under management as of December 31, 2024, it has become what traditional banks used to be—a provider of capital to the real economy, but without the regulatory constraints, legacy costs, or geographic limitations of banks.

VII. The Credit Machine: Apollo's Core Innovation

To understand Apollo's true innovation, forget everything you know about private equity. The leveraged buyouts, the operational improvements, the exit multiples—they're all sideshow. The main event, the thing that separates Apollo from every other alternative asset manager, is its ability to originate credit at scale. Not buy it. Not trade it. Create it.

Consider this: In 2024, Apollo originated over $220 billion in new loans and credit investments. That's more origination than many major banks. But unlike banks, Apollo doesn't need branches, doesn't face Basel III capital requirements, and doesn't have depositors who might panic. It has something better: insurance float from Athene that needs to be invested for decades, not quarters.

The credit machine works through three interlocking gears. First, origination platforms—16 distinct businesses that source deals directly. These aren't passive investments in other people's loans; they're boots-on-the-ground operations that compete directly with banks for lending opportunities. MidCap Financial, acquired in 2013, provides direct lending to middle-market companies. Atlas SP, formed from Credit Suisse's securitized products group, structures asset-backed securities. Each platform is a specialist, but they share Apollo's risk management framework and funding sources.

Second, the Athene synergy. Traditional asset managers must return capital to limited partners after investment periods end. But insurance premiums create perpetual inflows that must be invested immediately. This permanent capital base allows Apollo to hold investments to maturity, capturing illiquidity premiums that fund investors can't access. It's patient capital in its purest form.

Third, the "One Apollo" approach breaks down silos between strategies. A company might start as a private equity buyout, transition to credit when it needs growth capital, and eventually become a source of asset-backed securities. Apollo can provide capital across the entire lifecycle, creating stickiness that pure-play lenders can't match.

The sophistication of this machine is staggering. Apollo doesn't just make loans; it creates entire capital structures. Take the recent telecom infrastructure deals. Apollo provides the senior debt, the mezzanine layer, the preferred equity, and sometimes even the common equity. It's not participating in the capital markets; it is the capital market.

But the real genius is risk management. Every investment runs through the same rigorous process that Black instituted in the 1990s. The Monday meetings still happen, though now they're supplemented by quantitative models, stress testing, and scenario analysis that would make a bank risk manager jealous. The firm has essentially built a parallel banking system, but one designed for the 21st century rather than the 19th.

The numbers validate the strategy. Apollo's credit business generates returns in the high single digits to low teens—not spectacular by private equity standards, but extraordinary for fixed income in a world of zero interest rates. More importantly, these returns come with lower volatility and more predictable cash flows than traditional private equity. The September 2024 announcement of a $25 billion private credit partnership with Citigroup represents the future. Apollo formed an exclusive agreement with Citi to create a landmark private credit, direct lending program that will finance approximately $25 billion of debt opportunities over several years. This isn't Apollo borrowing from Citi or investing alongside them—it's the two firms creating an entirely new lending platform that combines Citi's client relationships with Apollo's balance sheet.

The implications are staggering. Traditional banks, constrained by regulation and capital requirements, are essentially outsourcing their lending to firms like Apollo. The credit machine has become so sophisticated that it's not competing with banks—it's replacing them in entire segments of the market.

Most remarkably, Apollo's credit strategy isn't about taking more risk—it's about taking different risk. By focusing on complexity, illiquidity, and patience, Apollo captures premiums that public markets can't access. The firm's loan loss rates are often lower than traditional banks, despite operating in supposedly riskier segments. It turns out that when you can hold loans to maturity, structure them properly, and manage them actively, credit becomes remarkably predictable.

VIII. Playbook: Business & Investing Lessons

The Apollo story offers a masterclass in building enduring value in finance, but the lessons extend far beyond Wall Street. At its core, this is a story about seeing opportunity where others see only risk, building complexity as competitive advantage, and creating institutional permanence from entrepreneurial chaos.

Lesson 1: Contrarian Timing Is Everything

Apollo has consistently started or accelerated when others were retreating. Founded amid Drexel's collapse, raised its largest funds during crises, and made its biggest acquisitions when markets were frozen. The pattern isn't luck—it's discipline. When capital is scarce, returns are highest. When fear dominates, opportunity abounds. But this requires more than courage; it requires preparation. Apollo always had dry powder when others were forced sellers.

Lesson 2: Complexity as a Moat

While competitors chase simplicity, Apollo embraces complexity. Caesars required over 50 financial transactions to keep alive. The Athene integration created structures most analysts still don't fully understand. The credit origination platforms operate across dozens of strategies simultaneously. This complexity isn't accidental—it's strategic. It creates barriers to entry, allows for value capture that simpler strategies miss, and provides optionality that pure-play competitors lack.

Lesson 3: Permanent Capital Changes Everything

The traditional private equity model—raise fund, invest, harvest, repeat—has inherent limitations. Funds have fixed lives. LPs have liquidity needs. Market windows open and close. But insurance float is different. It's permanent, patient, and predictable. This allows for strategies that simply aren't possible with traditional fund structures. You can hold investments through cycles, provide complete capital solutions, and build platforms rather than just making investments.

Lesson 4: Culture of Paranoia and Intellectual Honesty

The Monday morning meetings that Black instituted in the 1990s still happen today. Every investment gets challenged. Every assumption gets tested. Every thesis gets stress-tested. This isn't about being negative—it's about being rigorous. The culture demands that people argue positions they don't believe, find flaws in their own ideas, and admit when they're wrong. In a business where overconfidence kills, paranoia keeps you alive.

Lesson 5: Aligned Incentives Drive Performance

Apollo's professionals invest alongside their funds. The firm invests alongside Athene. Everyone eats their own cooking. This alignment goes beyond simple co-investment—it's about duration matching. The people making 30-year credit decisions have 30-year incentive plans. The insurance executives managing permanent capital have permanent incentive structures. When incentives align with outcomes, behavior follows.

Lesson 6: Platform Beats Product

Any firm can raise a fund. Many can execute deals. But building a platform—interconnected capabilities that reinforce each other—creates exponential value. Apollo's credit platform doesn't just make loans; it originates, structures, syndicates, and manages them. Each capability strengthens the others. The sum becomes greater than the parts, creating competitive advantages that are nearly impossible to replicate.

Lesson 7: Managing Founder Transitions

The transition from Black to Rowan could have destroyed Apollo. Founder-led firms often struggle with succession. But Apollo managed it by institutionalizing what mattered—the analytical rigor, the contrarian mindset, the long-term orientation—while allowing the firm to evolve beyond any individual. The lesson: Build systems and cultures that outlast their creators.

Lesson 8: Alternative Assets Are Eating Traditional Finance

Apollo's growth reflects a fundamental shift in global finance. As public markets become more efficient and regulated, private markets capture more value. As banks retreat from lending, private credit expands. As retail investors seek yield, alternatives become mainstream. Apollo isn't just riding this wave—it's creating it.

The playbook ultimately reduces to this: Find complex problems others won't solve. Build capabilities others can't replicate. Maintain discipline others won't match. And always, always have capital when others need it most.

IX. Analysis & Bear vs. Bull Case

Standing at nearly a trillion dollars in assets under management, Apollo presents one of the most compelling yet complex investment cases in modern finance. The bull case rests on structural tailwinds so powerful they seem almost inevitable. The bear case warns of risks that could unwind decades of value creation. Let's examine both with the rigor Apollo itself would demand.

The Bull Case: Structural Transformation of Finance

The retirement crisis is real and accelerating. Seventy-five million Americans are approaching retirement with insufficient savings. Traditional pensions are extinct. Social Security is underfunded. The only solution is private capital, and Apollo sits at the intersection of every trend that matters.

Consider the math: $100 trillion in global retirement assets needs to generate returns in a world where government bonds yield less than inflation. Apollo's ability to generate 6-8% returns in investment-grade private credit isn't just attractive—it's essential. The firm isn't selling a product; it's solving an existential problem for an entire generation.

The shift from public to private markets is equally inexorable. In 1996, there were 7,322 listed companies in the United States. Today, there are fewer than 4,000. The best companies stay private longer, sometimes forever. Apollo provides the capital that used to come from public markets but with better terms, more flexibility, and patient partnership. The firm estimates the private credit market alone will grow from $1.5 trillion today to $3-5 trillion by 2030.

Meanwhile, banking regulation has created an opportunity that may never repeat. Basel III, Dodd-Frank, and other post-crisis regulations have forced banks to retreat from entire lending segments. Apollo has stepped into this void, but without the regulatory burden, legacy technology, or geographic constraints of traditional banks. It's regulatory arbitrage at unprecedented scale.

The platform effects are just beginning to compound. Each new origination capability creates more investment opportunities. Each new investment creates more data and expertise. Each successful exit creates more reputation and relationships. Network effects in finance are rare, but Apollo has achieved them.

The Bear Case: Complexity and Concentration Risk

But complexity cuts both ways. Apollo's structure is so intricate that even sophisticated investors struggle to understand it. The interplay between the asset management business and Athene creates conflicts that no amount of governance can fully resolve. When the next crisis comes—and it always does—this complexity could become a liability.

The concentration risk with Athene is particularly concerning. Through Athene, our retirement services business, we specialize in helping clients achieve financial security by providing a suite of retirement savings products and acting as a solutions provider to institutions. Athene represents not just a large portion of AUM but the strategic rationale for the entire credit platform. If insurance regulators change capital requirements, if annuity sales slow, if credit losses spike, the entire model could unravel.

Regulatory risk looms large. Private credit has grown so fast that regulators haven't caught up. When they do, the requirements could be crushing. The SEC is already examining private fund advisers more aggressively. Banking regulators are questioning whether private credit creates systemic risk. Insurance regulators are scrutinizing the assets backing annuities. Apollo operates at the intersection of all three regulatory regimes.

Key person risk remains despite the successful transition from Black. Marc Rowan is brilliant, but he's also irreplaceable in the near term. The next generation of leadership isn't as visible or tested. In a business built on relationships and reputation, leadership transitions are always dangerous.

Market cycle vulnerability is inevitable. Apollo has never operated in a sustained high-interest-rate environment as a public company. The firm's credit models assume certain loss rates, recovery values, and refinancing availability. If these assumptions prove wrong—as they did with Caesars—the losses could be spectacular.

Competition is intensifying from every direction. Blackstone, KKR, and Ares are all building similar platforms. Banks are launching their own private credit funds. Even technology companies are entering lending. Apollo's first-mover advantage is real but eroding.

The Verdict: Transformation vs. Reversion

The investment case ultimately comes down to a fundamental question: Is Apollo riding a secular transformation of finance, or is it simply the latest iteration of Wall Street excess that will end badly when the cycle turns?

The evidence suggests transformation. The retirement crisis isn't cyclical—it's structural. The shift to private markets isn't a fad—it's a response to fundamental changes in how companies create value. The retreat of banks isn't temporary—it's the new regulatory reality.

But transformation doesn't eliminate risk—it changes its nature. Apollo isn't subject to bank runs, but it could face redemption pressure. It doesn't have deposit insurance, but it has insurance regulators. It avoids public market volatility, but it accepts illiquidity risk.

For investors, Apollo represents a complex bet on the future of finance itself. If private markets continue to grow, if retirement assets keep flowing to alternatives, if regulation remains favorable, Apollo could compound value for decades. But if any of these assumptions break, the unwind could be severe.

The most likely scenario is neither pure bull nor pure bear but continued evolution. Apollo will face crises—every financial firm does. But its culture of paranoia, diversified platform, and permanent capital base suggest it will survive and potentially thrive through them. The firm that emerged from Drexel's ashes has proven remarkably adept at turning crisis into opportunity.

X. Epilogue & "What's Next for Apollo"

As Marc Rowan stands before investors at Apollo's 2024 investor day, he projects a number that would have seemed absurd when the firm started with $400 million in 1990: $1.5 trillion in assets under management by 2029. According to the fund, it is already close to meeting the targets for 2026 that were laid out at its last investor day, in 2021, which included reaching $1 trillion in assets under management. The fund updated its 2029 target to $1.5 trillion AUM, more than double the $696 billion the fund managed across its units as of June 30. But in the context of Apollo's trajectory, it seems almost conservative.

The future of Apollo isn't about getting bigger—it's about becoming something fundamentally different. The firm is positioning itself as the Amazon Web Services of finance: the infrastructure layer that powers thousands of other businesses. Just as AWS provides computing power to companies that could never build their own data centers, Apollo provides capital to businesses that can't access traditional financing.

The global industrial renaissance that Rowan speaks about will require an estimated $30-50 trillion for energy transition alone. Traditional banks can't fund it. Governments can't afford it. Public markets won't wait for it. But patient, permanent capital can. Apollo is building the platform to intermediate these massive capital flows, taking a fee at every step.

International expansion represents the next frontier. While Apollo has offices globally, its penetration outside the United States remains limited. European insurance companies face the same retirement challenges as American ones but with even lower yields. Asian markets are beginning to embrace alternative assets. The playbook that worked in America can be exported, adapted, and scaled.

Technology, surprisingly, may be Apollo's secret weapon. While Silicon Valley focuses on disrupting finance, Apollo is using technology to enhance it. Artificial intelligence can underwrite loans faster than humans. Machine learning can identify patterns in credit losses. Blockchain can streamline settlement. Apollo isn't trying to be a tech company, but it's using technology to do what it's always done—find value where others can't.

The retirement crisis will only accelerate. As defined benefit pensions disappear and defined contribution plans prove insufficient, products like annuities become essential. Apollo, through Athene, is positioned to capture this wave. But more importantly, it's creating new products that didn't exist before—hybrid structures that combine guarantees with upside, portability with security. Private credit itself is expected to explode. Private credit expanded to approximately $1.5 trillion at the start of 2024, up from $1 trillion in 2020, and is estimated to soar to $2.6 trillion by 2029. Some estimates are even more aggressive, with the private credit market estimated to grow to $2.8 trillion by 2028. McKinsey suggests the size of the addressable market for private credit could be more than $30 trillion in the United States alone. Apollo isn't just participating in this growth—it's driving it.

The competitive landscape is evolving but in Apollo's favor. While new entrants crowd into direct lending, Apollo is moving up the complexity curve. Investment-grade private credit, asset-backed finance, infrastructure lending—these are areas where scale, expertise, and patient capital create insurmountable advantages.

Perhaps most intriguingly, Apollo is positioning itself for the next crisis, not the last one. Rowan speaks often about "playing offense during defense"—having dry powder when others are forced sellers. The firm is raising larger funds, diversifying funding sources, and building operational capabilities that will allow it to act quickly when opportunity arrives.

The cultural evolution continues. The paranoia remains, but it's now institutionalized rather than personalized. The intellectual honesty persists, but it's systematic rather than sporadic. The firm that was once three men in a conference room is now thousands of professionals across the globe, but the DNA—contrarian, analytical, opportunistic—remains unchanged.

As we look toward 2030 and beyond, Apollo's story becomes less about the firm itself and more about the transformation of global finance. The traditional banking system, built for an industrial economy, is giving way to something new—a market-based system where firms like Apollo intermediate capital flows without the constraints of traditional financial institutions.

This isn't without risk or controversy. Critics worry about systemic risk, opacity, and conflicts of interest. Regulators struggle to oversee firms that don't fit traditional categories. Competitors work to replicate Apollo's model. But the fundamental forces driving Apollo's growth—aging demographics, insufficient retirement savings, regulatory constraints on banks, the need for patient capital—aren't going away.

XI. Recent News

The drumbeat of Apollo's expansion continues relentlessly into 2025. Recent developments confirm both the firm's ambitious growth targets and its evolution beyond traditional private equity into a comprehensive financial services platform. In February 2025, Apollo announced the acquisition of Bridge Investment Group in an all-stock transaction valued at approximately $1.5 billion. Bridge, founded in 2009, is an established leader in residential and industrial real estate. The acquisition will provide Apollo with immediate scale to its real estate equity platform and enhance origination capabilities in both real estate equity and credit—another example of Apollo building platforms rather than just making investments.

The July 2025 completion of the $6.3 billion acquisition of International Game Technology's Gaming & Digital Business and Everi represents Apollo's continued push into technology-enabled sectors. Apollo Funds completed the acquisitions, bringing together complementary businesses to form a privately held global leader in gaming, digital and financial technology solutions.

The infrastructure push accelerates. In August 2025, Apollo Global Management Inc. agreed to acquire a majority stake in Stream Data Centers, making its first major data center acquisition as demand for digital infrastructure explodes. The acquisition of Argo Infrastructure Partners LLC adds approximately $6 billion worth of assets to Apollo's infrastructure platform, positioning the firm to capture the massive capital requirements of the AI revolution.

XII. Links & Resources

For those seeking to understand Apollo more deeply, the following resources provide essential context and ongoing coverage:

Primary Sources: - Apollo Investor Relations (ir.apollo.com) - Quarterly earnings, presentations, and SEC filings - Apollo Annual Reports - Comprehensive business overview and financial statements - Athene Financial Reports - Critical for understanding the insurance synergies

Books on Apollo and Private Equity History: - "The Carlyle Group: The Masters of Private Equity and Power" by Dan Briody - Context on industry evolution - "Barbarians at the Gate" by Bryan Burrough - The original LBO story that inspired a generation - "King of Capital" by David Carey - The Blackstone story, Apollo's main competitor

Academic Research: - "The Economics of Private Equity" (Journal of Economic Perspectives) - Framework for understanding the industry - "Private Equity Performance: What Do We Know?" (Journal of Finance) - Returns analysis - Harvard Business School cases on Apollo deals - Detailed transaction analysis

Industry Reports: - Preqin Global Private Markets Report - Annual industry overview - McKinsey Global Private Markets Review - Strategic analysis - Cambridge Associates Private Credit Benchmarks - Performance data

Key Interviews and Speeches: - Marc Rowan at Milken Institute conferences - Annual strategic updates - Apollo Investor Days - Deep dives into business segments - Congressional testimony on private credit - Regulatory perspective

The story of Apollo Global Management is ultimately a story about transformation—of finance, of retirement, of capitalism itself. From three men meeting in the ashes of Drexel Burnham Lambert to a trillion-dollar platform reshaping global capital markets, Apollo has proven that in finance, as in mythology, destruction and creation are often the same process. The firm that emerged from Wall Street's most spectacular collapse may well be building its future.

As Marc Rowan likes to say, "We're not in the business of predicting the future. We're in the business of preparing for it." With $840 billion under management and growing, with permanent capital through insurance, with origination capabilities that rival major banks, Apollo isn't just prepared for the future of finance—it's creating it.

Whether that future brings triumph or tragedy, innovation or regulation, growth or retrenchment, one thing seems certain: Apollo will be there, finding opportunity in complexity, building value from distress, and proving once again that on Wall Street, the only constant is change—and those who master change master everything.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube