AMH (American Homes 4 Rent): How a Real Estate Legend Turned the 2008 Housing Crisis into a New Asset Class

I. Introduction & Episode Roadmap

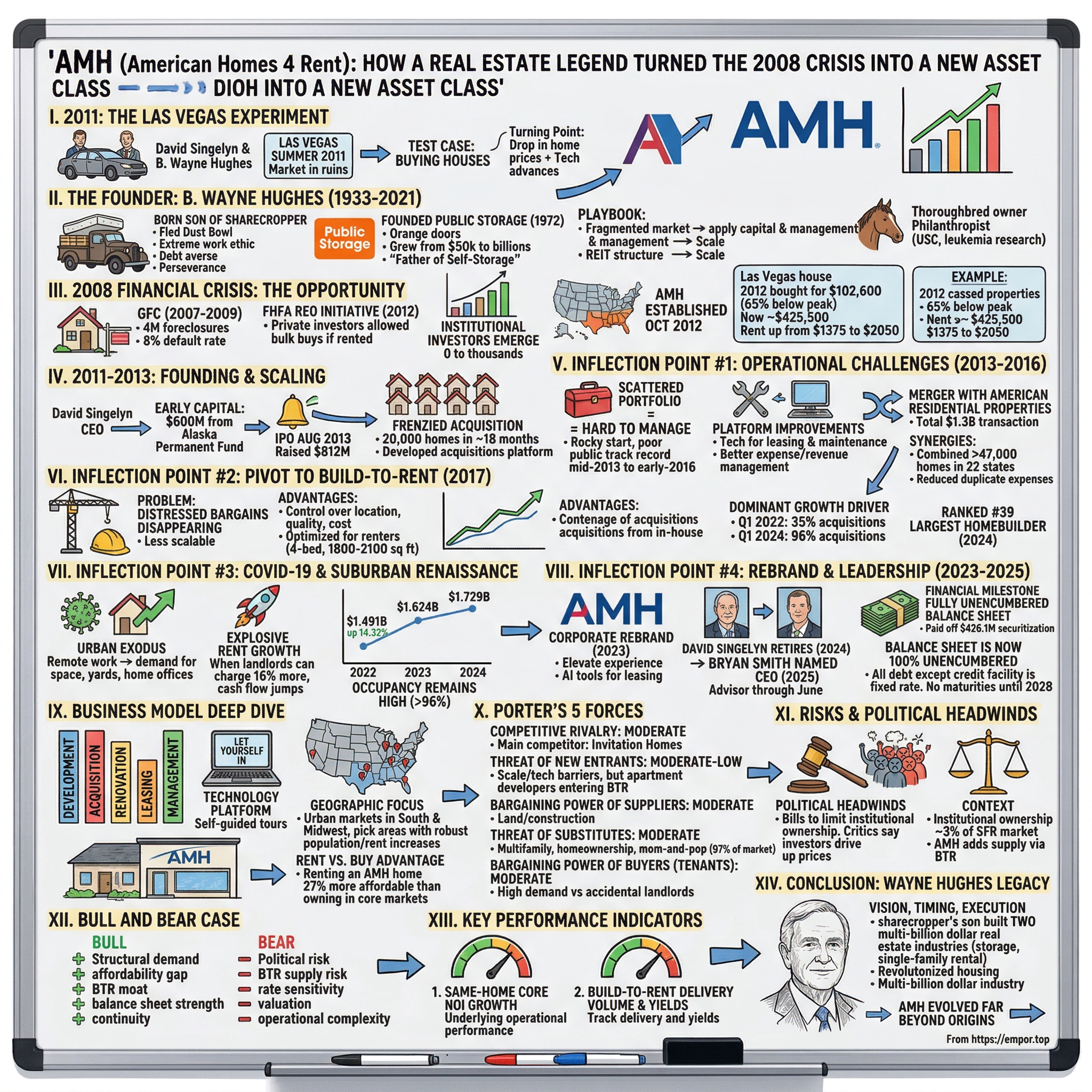

Picture Las Vegas in the scorching summer of 2011. The housing market lies in ruins. Foreclosure notices paper the doors of suburban homes from Henderson to North Las Vegas. Home values have cratered by more than 60% from their peak. Banks are desperate to unload inventory. Into this landscape of financial devastation drive two men in a rental car: David Singelyn, a veteran real estate executive, and B. Wayne Hughes, a billionaire septuagenarian who had already built one of America's largest real estate empires.

They weren't there to mourn. They were there to buy.

"In the summer of 2011, David Singelyn, now the CEO of American Homes 4 Rent, and Wayne Hughes, founder of Public Storage, bought a few houses in Las Vegas as a test case to see if they wanted to create a business focused on single-family home rentals. Singelyn says that year was a turning point in the residential real estate segment. 'First, home prices dropped, but second, and just as important, tech advances reached a point where it was easier to access data like school information and demographics to make investment choices.'"

What emerged from that Las Vegas experiment would become American Homes 4 Rent—now simply AMH—a real estate investment trust reporting trailing twelve-month revenues of approximately $1.83 billion as of late 2025, driven by its portfolio of over 61,000 single-family properties across the US.

But this isn't just a story about buying cheap houses during a crisis. It's the story of how a serial disruptor recognized that America's most fragmented real estate category—single-family rentals—was ripe for institutionalization. American Homes 4 Rent was founded through Hughes' "vision of offering families across the United States more desirable and affordable housing choices. That vision revolutionized the homebuilding industry and his legacy now extends far beyond our company, as evidenced by the ever-growing multibillion-dollar single family rental industry."

The central question that drives this deep dive is deceptively simple: How did a billionaire who revolutionized self-storage create an entirely new institutional asset class out of America's greatest housing collapse? The answers reveal lessons about timing, capital deployment, operational innovation, and the kind of contrarian vision that separates great investors from merely good ones.

AMH's vertically integrated model, which includes a successful Build-to-Rent program, is a key differentiator, plus they achieved a major financial milestone by fully unencumbering their balance sheet in the third quarter of 2025. The company expects its Core Funds from Operations (Core FFO) per share to hit a midpoint of $1.87 for the full year—a 5.6% growth.

Today, AMH stands as the second-largest institutional owner of single-family rental homes in America, trailing only Invitation Homes. The company has evolved from a voracious acquirer of distressed foreclosures into one of the nation's largest homebuilders—recognized by Builder Magazine as the 39th largest homebuilder in the United States. That metamorphosis, from crisis opportunist to developer, tells a story about how successful companies adapt when their original playbook becomes obsolete.

II. The Founder: B. Wayne Hughes — A Serial Real Estate Disruptor

Before we can understand AMH, we must understand the man who created it. Bradley Wayne Hughes wasn't born to wealth. He was born in Gotebo, Oklahoma, on September 28, 1933. His family relocated to Los Angeles during the Dust Bowl, before making their home in El Monte, California. This origin story—the son of sharecroppers fleeing the devastation of the Oklahoma prairies, arriving in California with nothing—would shape his entire approach to business.

Born the son of a sharecropper, he moved with his family to Southern California as a child. After saving for college by working a newspaper delivery route as a teen, he enrolled at the University of Southern California in Los Angeles, graduating in 1957 with a B.A. in business. He went on to serve in the U.S. Navy as an officer.

The Dust Bowl migration imprinted certain values on Hughes that colleagues would later describe as fundamental to his success. "I think it really all ties back to his early roots of poverty, losing it all, riding out to California out of Oklahoma was nothing more than a mattress in an old jalopy. And that gave him some very basic tenants that served him well throughout his life. Number one, he had an extreme work ethic he clearly didn't want to stay in poverty. Number two, he was very debt averse. Number three, he liked to live simply. And number four, he just had a whole lot perseverance and dedication."

Hughes spent his post-Navy career learning Los Angeles real estate. He started his career in Los Angeles real estate until the early 1970s, when he subsequently established Public Storage in 1972. The founding story of Public Storage has become legend in the REIT world: According to Public Storage lore, Hughes came across a small storage facility while on a trip through Texas and learned that all of its units had sold out. He pitched his business partner Kenneth Volk the idea of starting their own storage warehouse and they scraped together $25,000 each in seed money, forming the new company.

They opened their first Public Storage location in El Cajon, California, painting the doors of the rental units their trademark bright orange to attract drivers on a nearby highway. The business took off, growing their $50,000 investment into a multi-billion dollar fortune and expanding Public Storage to more than 2,500 locations.

The Public Storage playbook established the template Hughes would later apply to single-family rentals. Hughes is the "father" of the self-storage industry, having grown Public Storage from scratch into the world's largest self-storage REIT with over 2,500 locations in the U.S. and overseas. The pattern was clear: identify a fragmented, inefficient market dominated by mom-and-pop operators; apply institutional capital and professional management; use the REIT structure to access public capital markets; and scale relentlessly.

Hughes' management philosophy was famously unpretentious. "You don't get money unless you have a lot of talent, which I don't have. Or you work hard, which is what I do. We don't have any golden touch around here." But this modesty masked genuine insight. Ron Havner, company chairman of the board of trustees, said: "Wayne was my mentor in every sense of the word. His practical, no-nonsense approach to business and natural ability to 'think outside the box' were the keys to Public Storage's success. He continually pushed us to innovate, so we made lots of mistakes; but we learned, kept growing and improved the business."

Beyond business, Hughes cultivated passions that revealed another dimension of his character. Hughes was an owner of Thoroughbred racehorses since 1972. His horse, Authentic, won the 2020 Kentucky Derby and Breeders' Cup Classic. He acquired the historic 700-acre Spendthrift Farm near Lexington, Kentucky, in June 2004.

His philanthropy was equally noteworthy—and equally understated. As of 2019, Hughes had donated between $400–450 million to USC, by far the most generous donor in the university's history. Most of the donations were anonymous. His commitment to philanthropy was evident in the time, effort and financial resources he committed to the battle to defeat cancer. With a goal of eradicating childhood leukemia, he established the William Lawrence and Blanche Hughes Foundation in memory of his son Parker, who passed away in 1998. The organization's efforts would notch a number of key research breakthroughs in subsequent years.

When Hughes turned his attention to single-family rentals in his late seventies, many doubted whether the model could work at institutional scale. Managing thousands of individual homes scattered across vast metropolitan areas seemed fundamentally different from managing self-storage facilities with on-site managers. But Hughes saw the similarities: a fragmented market, rising demand, operational inefficiencies that technology could solve, and a vast untapped opportunity for institutional capital.

B. Wayne Hughes Sr., who built Public Storage into an industry behemoth and repeated the feat four decades later in single-family rentals with American Homes 4 Rent, died on August 18, 2021. He was 87. The billionaire died at Spendthrift Farm in Kentucky, a legendary Thoroughbred breeding ranch that he bought in 2004.

III. The 2008 Financial Crisis: The Opportunity of a Lifetime

To understand why AMH exists, you must first understand the housing apocalypse that created it. The financial crisis that began in 2007 wasn't just a market correction—it was a generational transfer of housing wealth from distressed homeowners to those with capital and courage to act.

The GFC resulted in a single-family mortgage default rate of more than 8 percent, and 4 million homes went into foreclosure. Many were purchased by investors at foreclosure auctions. In 2012, the Federal Housing Finance Agency (FHFA) created the Real Estate Owned (REO) Initiative. This allowed private investors to buy properties in bulk as real estate investment trusts (REITs) if they rented the homes for a certain number of years. Several large firms—Invitation Homes, American Homes 4 Rent, Colony, American Residential Properties, Waypoint, Amherst, Progress Residential, Silver Bay and others—entered the market at an attractive entry point.

The crisis transformed the single-family rental landscape. Millions of homeowners defaulted on their mortgages during the 2007-2009 financial crisis. Institutional investors—companies that own a lot of single-family rental homes—bought many of these foreclosed homes in bulk and converted them into rental housing, especially in states across the southern U.S. Researchers found that institutional investors may have contributed to increasing home prices and rents following the financial crisis.

The numbers tell the story of how quickly institutional investors emerged from nothing. Studies found that no investor owned 1,000 or more single-family rental homes as of late 2011. However, by 2015, institutional investors collectively owned an estimated 170,000-300,000 homes.

For Hughes and Singelyn, the opportunity wasn't just about buying cheap houses—it was about recognizing a structural shift in American housing. American Homes 4 Rent was established in October 2012, emerging right after the U.S. financial crisis created a huge supply of foreclosed, single-family homes at attractive prices.

Consider the concrete example of one Las Vegas property that illustrates the magnitude of the opportunity: Near the desert edge of Las Vegas lies a four-bedroom suburban home at 8025 Peaceful Woods St. This 1,800-square-foot single-family home is a prime example of the bargain buys that American Homes 4 Rent secured during the depths of the Great Financial Crisis housing bust. In 2012, AMH purchased the home for $102,600—65% below the $295,826 the previous owner paid in October 2004. Fast-forward to today, and the home is valued at around $425,500, according to Zillow. As of last summer, the giant landlord listed the home for rent at $2,050 per month, up from $1,375 in 2017.

The competitive landscape was forming rapidly. The company was established in October 2012 by B. Wayne Hughes, the founder of Public Storage. It was one of the first large public companies to begin investing heavily in single-family homes, following the entry of The Blackstone Group into the field in 2012. Blackstone had entered through Invitation Homes, which would become AMH's primary competitor.

Why did this opportunity exist? Several factors converged: homeownership rates plunged as millions lost their homes to foreclosure; credit standards tightened dramatically, preventing many former homeowners from buying again; demographic shifts were increasing rental demand; and technology had finally made it feasible to manage large portfolios of scattered single-family homes.

"At the same time, there was an opportunity to invest in a management platform and a tech platform to better serve renters." American Homes was one of the first single-family rental REITs.

The timing was critical. By 2012, home prices had bottomed in many markets, but inventory remained abundant from foreclosures. Aided by access to capital through various sources, institutional investors had a funding advantage over smaller investors at a time when mortgage lenders were generally reducing lending. Additionally, technological advancements allowed companies to acquire and manage large portfolios of single-family homes more easily. Institutional investors initially relied on bulk purchases but then shifted to making smaller-scale purchases, merging with other investors, or building homes for rent. These activities have contributed to their growth over time.

IV. Founding & Scaling: 2011-2013

The formal incorporation came in late 2012, but the foundation was laid earlier. American Homes 4 Rent (AMH) was established on October 19, 2012, as an internally managed Maryland real estate investment trust by B. Wayne Hughes, founder of Public Storage, to capitalize on the post-2008 housing crisis landscape of distressed single-family properties and rising rental demand. The firm built upon initial investments from AH LLC, formed by Hughes in 2011, with early capital including a $600 million infusion to acquire foreclosed or undervalued homes in suburban markets across the southern and western United States.

The founding CEO was David Singelyn, who helped steer the company's rapid growth and strategic shifts. To scale quickly, AMH secured significant early capital, including a notable $600 million investment from the Alaska Permanent Fund. This initial war chest allowed it to compete with other large institutional investors. In August 2013, the company went public via an Initial Public Offering (IPO), raising approximately $812 million to fuel even faster portfolio expansion.

The Alaska Permanent Fund investment demonstrated Hughes' ability to tap institutional capital even before the company went public. This sovereign wealth fund, built from Alaska's oil revenues, provided the kind of patient, long-term capital that enabled rapid scaling.

The early acquisition phase was frenzied. Industry participants described it in vivid terms. As one contemporary recalled: "It was like drinking from a fire hose, buying thousands of homes a week." The challenge was building operational capacity as fast as properties were being acquired.

Under CEO David Singelyn, AMH prioritized properties suitable for renovation and long-term leasing, targeting markets with strong employment and population growth to achieve economies of scale in property management. The company went public via an initial public offering on August 1, 2013, pricing shares at $16 and raising funds to fuel further acquisitions, at which point its portfolio comprised approximately 20,000 single-family homes.

Growing from zero to 20,000 homes in roughly 18 months required extraordinary operational innovation. The company had to develop an acquisitions platform capable of screening, inspecting, and underwriting thousands of available homes monthly. This wasn't just about buying properties—it was about building the entire infrastructure to operate them: maintenance crews, leasing platforms, tenant screening systems, and property management protocols.

Hughes stepped down from Public Storage's board in 2011 and a year later founded the single-family rental business American Homes 4 Rent. American Homes 4 Rent thrived in the wake of the mortgage crisis and within a year amassed a portfolio of around 10,000 homes.

The IPO marked a milestone not just for AMH but for the entire single-family rental industry. It proved that public markets would embrace this new asset class, opening the door for institutional capital to flow into what had been an entirely mom-and-pop business.

The early days required balancing aggressive acquisition with building operational credibility. The REIT structure meant the company had to demonstrate it could generate consistent rental income and eventually pay dividends to shareholders. Every property acquired had to be renovated, marketed, leased, and managed—often in markets where the company was simultaneously building its local presence.

V. Key Inflection Point #1: The Early Operating Challenges (2013-2016)

The narrative of AMH's early success obscures a more complicated reality: the company struggled operationally before it thrived. Going from startup to publicly traded REIT with tens of thousands of scattered properties exposed the challenges of institutionalizing a fundamentally local, high-touch business.

Following a rocky start, the company refined its operating platforms in late 2015 and early 2016. The initial public-market track record for single-family rental REITs was poor from mid-2013 through early 2016, when they began to dramatically improve operations.

The operational challenges were substantial. Unlike apartment buildings where property managers can walk hallways, single-family rentals require sending maintenance crews across vast suburban areas. Tenant screening, rent collection, and lease enforcement had to be standardized across diverse local markets with different regulations and tenant expectations.

What changed? Several factors converged. Improvements in expense and revenue management represent one of the biggest tailwinds for the sector. Ten years ago, the business would have been nearly impossible to operate without the technological tools used to support scaled operations in areas such as leasing and maintenance. The large public REITs and some smaller private operators have made substantial investments in their platforms and management teams. These platform improvements have alleviated prior concerns from investors that management teams can successfully run this operationally-intensive business.

The 2016 merger with American Residential Properties represented a strategic decision to consolidate in a maturing market. American Homes 4 Rent and American Residential Properties, Inc. announced the completion of the previously announced merger of the two companies at a total transaction value of approximately $1.3 billion. In the merger, American Homes 4 Rent issued approximately 38 million common shares and limited partnership units and assumed or repaid a total of approximately $0.8 billion of American Residential Properties' debt. The stockholders of American Residential Properties approved the merger at a meeting held on February 26, 2016. "We are delighted to announce the completion of our merger with American Residential Properties, further establishing American Homes 4 Rent as the largest publicly traded owner and operator of single-family rental homes," stated David Singelyn.

The merger enhanced the size of the largest publicly-traded single-family rental company. The combined company was expected to own more than 47,000 homes in 22 states and to have an equity market capitalization of $5.5 billion and an aggregate real estate cost basis of over $8 billion. Given the geographic overlap of American Homes 4 Rent and American Residential Properties portfolios, operational synergies were expected to be achieved by reducing duplicate expenses for internet charges, supervisory property management personnel, management information systems and other back-office functions. The merger was expected to be accretive to American Homes 4 Rent Core FFO.

The 2016 merger with American Residential Properties (ARPI) significantly increased portfolio size and geographic diversity by acquiring approximately 9,000 homes, consolidating its market leadership.

The merger wasn't just about scale—it was about proving that consolidation could create operational efficiencies in a business where efficiency was the difference between profitability and losses. Big operators were proving they could control costs, improve margins, and grow rents.

The single-family rental REITs, such as American Homes, are focusing now on developing depth and scale in particular markets. "There's additional synergy in owning more properties in any one market," analysts noted. "The more you own, the more you can rely on contractors and suppliers to work with you."

By mid-2016, AMH had turned the corner. Operational metrics improved, investor skepticism faded, and the stock began to reflect the underlying value of the platform the company had built.

VI. Key Inflection Point #2: The Strategic Pivot to Build-to-Rent (2017)

If the 2012-2016 period was about buying distressed homes and proving the operating model could work, the 2017 pivot to build-to-rent (BTR) was about securing the company's future in a normalizing housing market.

The problem was simple: the bargains were disappearing. "Recognizing that acquiring existing homes was becoming less scalable and more competitive as the housing market recovered, the company launched its internal development program in 2017. This strategic shift to building new homes for rent (Build-to-Rent) was transformative. It gave AMH control over the location, quality, and cost of its assets, leading to better operational efficiencies and higher resident satisfaction."

The gap between 2013-era acquisition economics and the normalized market was stark. In the early days, AMH could buy foreclosures at 15% discounts to market prices. By 2017, those discounts had largely evaporated.

AMH announced its 10,000th new home delivery and recognition by Builder Magazine as the 39th largest homebuilder in the United States on its 2024 Builder 100 List. This milestone reaffirms the company's commitment to creating new attainable housing at scale at a time of critical supply shortages in the U.S. AMH launched its development program in 2017 in response to rising demand for high-quality single-family rental homes in sought-after locations. By 2021, the company had debuted on the Builder 100 List as the 45th largest homebuilder in the U.S. and the highest-ranked builder solely focused on single-family rental homes. Since its debut, AMH has climbed the Builder 100 List and notched the 39th spot for its completion of 2,317 homes in 2023.

The BTR strategy offered several advantages. Control over quality, design, and product: By developing its own homes, AMH can ensure that the properties meet its standards for quality and design, making them more attractive to the renters it's targeting. Scalability: Owning the build-to-rent process allows AMH to scale its operations more efficiently. Long-term thinking: Developing new communities allows AMH to strategically select locations and develop properties that are likely to have the best long-term outlooks.

The company builds three-bedroom, four-bedroom, and five-bedroom homes. Its most popular offering is four-bedroom homes that range from 1,800 to 2,100 square feet. These purpose-built rentals feature design elements optimized for renters—durable finishes that minimize maintenance, layouts that appeal to families, and community amenities that justify premium rents.

Through its build-to-rent program, established in 2017, AMH has already delivered more than 7,000 new homes in over 100 communities nationwide, with thousands more under development.

The scale of this transformation is remarkable. The company has developed an in-house homebuilding division and, according to the latest Builder 100 ranking, is the 39th largest homebuilder in America. Of AMH's portfolio of more than 59,000 single-family rentals, about 10,000 were constructed by their homebuilding operation. In addition, AMH has roughly 10,000 build-to-rent homes in its development pipeline.

The shift to BTR became especially critical as interest rates rose in 2022 and scattered homebuying became economically unattractive. While many institutional landlords had an uptick in scatter homebuying during the pandemic housing boom, that quickly fizzled out once interest rates spiked in summer 2022. Since then, in-house homebuilding has been the dominant force driving AMH's portfolio growth. In Q1 2022, AMH acquired 931 homes, with 325 coming from its in-house homebuilding division, accounting for 35% of its acquisitions. Compare that to Q1 of last year, when 299 of the 312 homes AMH acquired came from its in-house homebuilding division, accounting for 96% of its acquisitions. Again in Q1 this year, 96% of AMH's acquisitions were from its in-house homebuilding division.

This evolution from distressed-asset acquirer to integrated homebuilder represents one of the most dramatic strategic pivots in REIT history. AMH didn't abandon its original business model because it failed—it evolved because the opportunity set changed.

VII. Key Inflection Point #3: COVID-19 and the Suburban Renaissance (2020-2022)

The COVID-19 pandemic could have devastated a business built on collecting rent from tenants whose jobs were suddenly at risk. Instead, it accelerated trends that benefited single-family rentals and transformed AMH's growth trajectory.

Single Family Rental REITs are primed to outperform over the next few years due to strong tailwinds that were accelerated by COVID-19.

The pandemic triggered an urban exodus as remote work untethered millions of workers from city offices. Families crammed into apartments during lockdowns suddenly prioritized space, yards, and home offices. The single-family rental became the beneficiary of this flight.

During 2020-2022, rent growth exploded. When landlords can charge 16% more in rent than the prior year, cash flow jumps dramatically, providing more capital to expand the business. AMH and its competitors saw inventory additions—meaning homes built to rent—roughly quadruple during this period.

The occupancy metrics told the story. Average occupancy rates remained extraordinarily high—above 96%—even as the company raised rents aggressively. The company's Same-Home Core Net Operating Income (NOI) grew by 4.1%, driven by a 4.3% blended rate increase on new leases and renewals, while occupancy rates remained robust at 96.3%.

The pandemic also validated the structural advantage of single-family rentals over apartments. When people are confined to their homes, square footage matters. When remote work becomes permanent for millions, the difference between a cramped apartment and a house with a yard becomes existential rather than preferential.

American Homes 4 Rent annual revenue for 2024 was $1.729B, a 6.47% increase from 2023. American Homes 4 Rent annual revenue for 2023 was $1.624B, an 8.93% increase from 2022. American Homes 4 Rent annual revenue for 2022 was $1.491B, a 14.32% increase from 2021. The 14% revenue jump in 2022 reflects both rent growth and portfolio expansion during this period of extraordinary demand.

VIII. Key Inflection Point #4: The Rebrand and Leadership Transition (2023-2025)

In January 2023, American Homes 4 Rent unveiled a transformation that went beyond a new logo. AMH (NYSE: AMH), a leading single-family rental operator and top U.S. homebuilder previously known as American Homes 4 Rent, unveiled a new corporate brand identity that embraces its DNA with a modern outlook.

"This year, we celebrate ten years dedicated to simplifying how America lives by delivering professionally managed homes and services that elevate the experience of single-family living," said David Singelyn, co-founder and chief executive officer of AMH. "Our goal is to make leasing a high-quality home easy, so our residents can focus on what really matters to them in life. Now, we're simplifying our brand, too, to better reflect our focus on making the home experience easier for our residents."

This branding leverages the company's rich heritage, people-first employer culture and industry-leading sustainability program. Rooted in extensive third-party consumer research, this year-long rebranding initiative also includes updated resident touchpoints through a simplified digital and mobile experience, including a new user-friendly website. "Today at AMH, we do much more than just rent homes. We're reimagining the future of housing while improving people's everyday lives," said Bryan Smith, then chief operating officer of AMH. "Our new brand reflects our differentiation in the industry through an elevated customer experience."

The following year brought leadership transition. AMH announced that David P. Singelyn, who had served as Chief Executive Officer since the Company's inception, announced his intent to retire effective December 31, 2024. The Company's Board of Trustees named Bryan Smith, the Company's Chief Operating Officer, as the next Chief Executive Officer effective January 1, 2025. Subsequently, Mr. Singelyn would serve as an advisor through June 2025.

Matthew J. Hart, Chairperson of the Board, said "Since co-founding the Company with B. Wayne Hughes in 2012, Dave Singelyn has built AMH into a market leader with nearly 60,000 high-quality single-family properties, which over 200,000 people today call home." "Bryan is a talented and experienced executive who has driven our business, our strategy, and our operations during the past 12 years," said Mr. Singelyn. "His operational expertise, leadership skills, and commitment to our ongoing success make him an excellent choice to lead the Company into an exciting future."

Bryan Smith was appointed Chief Executive Officer of AMH and named a member of the company's Board of Trustees in January of 2025. Prior to his current appointment, Smith served as Chief Operating Officer since 2019, helping drive the company's growth to become a leading owner, operator, and developer.

The leadership transition occurred as the company achieved a major financial milestone. During the third quarter of 2025, the Company paid off the outstanding principal of approximately $426.1 million on the AMH 2015-SFR2 asset-backed securitization, resulting in a fully unencumbered balance sheet. The company raised Full Year 2025 Core FFO attributable to common share and unit holders guidance midpoint by $0.01 per share and unit to $1.87, representing anticipated full year growth of 5.6% over prior year.

"Our balance sheet is now 100% unencumbered, marking an exciting milestone in AMH's history. Additionally, all debt other than our credit facility is fixed rate and we have zero maturities until 2028."

Wayne Hughes didn't live to see these milestones. Hughes died on August 18, 2021, at his home on Spendthrift Farm near Lexington, Kentucky, a month before his 88th birthday. But the company he founded has grown into exactly what he envisioned: a professionally managed alternative to fragmented mom-and-pop rental housing, delivered at institutional scale.

IX. The Business Model Deep Dive

AMH's business model has evolved from simple opportunistic acquisition into something far more sophisticated: a vertically integrated platform that develops, acquires, renovates, leases, and manages single-family homes.

The Vertically Integrated Model

A key strategic move for AMH has been its focus on internal development, constructing new built-to-rent home communities. This approach has allowed AMH to build over 12,000 homes across 200 communities since 2017, with plans for more growth. This strategy enables control over construction quality and costs, complementing traditional acquisition methods. In 2024, AMH was ranked as the 39th top homebuilder in the U.S. by Builder100, moving up to 37th in 2025.

Technology Platform

AMH has invested heavily in technology to manage its scattered portfolio efficiently. American Homes 4 Rent®, AMH®, AH4R®, Let Yourself In®, AMH Development®, American Residential®, and 4Residents® are registered trademarks of American Homes 4 Rent, LP. The "Let Yourself In" trademark refers to the company's self-guided tour technology, introduced in 2013, which allows prospective tenants to schedule and conduct property tours via mobile access without agent accompaniment.

In 2025, AMH rolled out AI tools to improve prospect experience and internal leasing efficiency, with anticipated retention and process benefits rolling into 2026.

Geographic Focus

The company's real estate portfolio is largely comprised of single-family properties in urban markets in the Southern and Midwestern regions of the U.S. The firm's geographical markets include Dallas, Texas; Indianapolis, Indiana; Atlanta, Georgia; and Charlotte, North Carolina in terms of the number of properties in each.

The geographic concentration is intentional. SFR investors, particularly mega investors, are highly concentrated in fast-growing MSAs. As long-term rental operators, these investors try to pick areas that are likely to have robust rent increases, and population increases in an environment with limited housing supply is a good predictor of this. The population growth rate in the top 20 MSAs for mega investors was 16.75 percent from 2010 to 2021, compared with 7.29 percent nationally. The growth rate for households in the top 20 MSAs for mega investors was 21.57 percent over the same period, compared with 11.33 percent nationally.

Financial Performance

Rents and other single-family property revenues increased 7.5% year-over-year to $478.5 million for the third quarter of 2025. Net income attributable to common shareholders totaled $99.7 million, or $0.27 per diluted share, for the third quarter of 2025, compared to $73.8 million, or $0.20 per diluted share, for the third quarter of 2024. Core Funds from Operations ("Core FFO") attributable to common share and unit holders increased 6.2% year-over-year to $0.47 per FFO share and unit for the third quarter of 2025.

As of September 30, 2025, the Company had cash and cash equivalents of $45.6 million and total outstanding debt of $4.9 billion, with a weighted-average interest rate of 4.5% and a weighted-average term to maturity of 8.6 years, which includes $110.0 million of outstanding borrowings on its $1.25 billion revolving credit facility.

The Rent vs. Buy Advantage

A critical demand driver for AMH is the affordability gap between renting and owning. The structural shift in housing affordability works directly in AMH's favor; renting an AMH home is currently about 27% more affordable than owning in their core markets, creating a large, stable demand pool.

ATTOM's 2024 Rental Affordability Report shows that median three-bedroom rents in the U.S. are more affordable than owning a similarly-sized home in nearly 90 percent of local markets around the nation. Median rental rates still require a smaller portion of average wages than major home-ownership expenses on three-bedroom properties in 296, or 88 percent, of the 338 U.S. counties with enough data to analyze.

X. Porter's 5 Forces Analysis and Strategic Assessment

Understanding AMH's competitive position requires analyzing the forces that shape profitability in the single-family rental industry.

Threat of New Entrants: MODERATE-LOW

Ten years ago, the business would have been nearly impossible to operate without the technological tools used to support scaled operations in areas such as leasing and maintenance. Building the operational infrastructure to manage tens of thousands of scattered homes requires massive capital investment—not just in real estate but in technology, personnel, and local market expertise.

First-mover advantage is significant. AMH has spent over a decade building its platform, securing land pipelines, and developing builder relationships. A new entrant would face years of catching up.

However, competition is increasing from adjacent industries. Many large apartment developers are now entering the crowded build-to-rent field. Greystar, the nation's largest apartment manager, has launched entirely new brands. Even homebuilders like Lennar and D.R. Horton have launched BTR divisions.

Bargaining Power of Suppliers: MODERATE

Land and construction costs are key inputs for the build-to-rent model. Development program yields for 2025 are tracking just below mid-5% due to soft rent conditions, with project construction costs flat compared to 2024.

Vertical integration reduces supplier power—by building its own homes, AMH is less dependent on third-party homebuilders. "There's additional synergy in owning more properties in any one market. The more you own, the more you can rely on contractors and suppliers to work with you."

Bargaining Power of Buyers (Tenants): MODERATE

The demand for single-family rentals is high, fueled by America's acute housing shortage and soaring home prices. High occupancy rates (95%+) indicate demand exceeds supply, giving landlords pricing power.

However, a new competitive dynamic is emerging. When homeowners cannot sell their properties, some convert to rentals, creating "accidental landlords" who expand supply without institutional discipline around pricing.

Threat of Substitutes: MODERATE

Substitutes include multifamily apartments, homeownership, and mom-and-pop rentals. Institutional investors make up only a small percentage (1 percent) of the total SFR market. The fragmented nature of ownership means AMH competes not just against other institutional landlords but against millions of individual property owners.

Competitive Rivalry: MODERATE

The lack of incoming supply and greater barriers to entry are two constraints that continue to serve as tailwinds. At present, American Homes 4 Rent (AMH) is their primary competitor in the space. Invitation Homes is larger by portfolio size, but the two companies have different strategic emphases—INVH focuses more on West Coast and Florida markets, while AMH has stronger Sunbelt exposure outside California.

Invitation Home has higher revenue and earnings than American Homes 4 Rent. American Homes 4 Rent is trading at a lower price-to-earnings ratio than Invitation Home, indicating that it is currently the more affordable of the two stocks.

Hamilton Helmer's 7 Powers Framework

Scale Economies: AMH benefits from fixed cost leverage—technology platforms, corporate overhead, and regional management infrastructure cost roughly the same whether managing 50,000 or 70,000 homes. Every additional home added to a market improves unit economics.

Network Effects: Limited direct network effects, but local density creates operational advantages—more efficient maintenance routing, better contractor relationships, stronger brand awareness.

Counter-Positioning: The build-to-rent pivot represents counter-positioning against traditional homebuilders who historically sold rather than rented. Builders are now copying this model, eroding this advantage.

Switching Costs: Moderate for tenants—moving costs create some friction, but tenants can switch to competitor properties or homeownership when leases expire.

Branding: Growing importance as AMH invests in the resident experience. The 2023 rebrand reflects this strategic focus.

Cornered Resource: Land pipeline is a key cornered resource—AMH has secured development lots that will take years to build out, providing visibility into future growth.

Process Power: The company has developed proprietary processes for acquisitions underwriting, renovation management, and property operations that create sustainable efficiency advantages.

XI. Risks and Political Headwinds

No analysis of AMH would be complete without examining the political and regulatory risks that have emerged around institutional ownership of single-family homes.

The Legislature will consider at least three bills this year to keep so-called institutional investors from gobbling up too many of the state's widely coveted single-family homes. Apartment buildings have long been an asset of interest for big investment companies, but the Big Money-owned single-family rental is a 21st Century invention. During the Great Recession new companies began cobbling together rental empires out of the nation's glut of foreclosed single-family homes. Defenders of the business model applaud the role it played in propping up local housing markets and quickly filling homes that would have otherwise sat vacant and derelict. Critics liken these investors to financial vultures depriving would-be homeowners of a shot at the American Dream while hoarding the profits of the last decade's run-up in national home prices and rents.

Representatives reintroduced the Stop Wall Street Landlords Act to end large institutional investors' ability to use taxpayer dollars to subsidize the acquisition of single-family residential homes. Since the 2008 housing crash and subsequent foreclosure crisis, increased investor activity in America's housing market has normalized excessive fees and abusive practices while artificially driving up housing and rent prices. Investors bought 18% of all homes that sold in the fourth quarter of this year and 26% of the most affordable homes. In California, Nevada, Florida, Georgia, and other states where corporate landlords own a large concentration of single-family homes used as rental properties, investors are driving up the cost of rent.

As part of a growing push over the last two years to limit Wall Street's grip on the housing market, in December Senator Jeff Merkley, an Oregon Democrat, introduced a bill to end corporate ownership of single-family houses. Lawmakers in eight states have also introduced bills over the last year that would limit or penalize corporate investors who purchase single-family homes.

However, context matters. Research suggests that while these entities make easy scapegoats, they are at best symptoms of the supply-demand imbalance. To put it bluntly, housing was unaffordable even before many of these entities were established. Vilifying institutional landlords and other entities distracts from the underlying issues facing the housing market.

Institutions currently own only about 600,000 SFR units or 3% of the 17 million single-family rental homes in the U.S. Institutional investors make up only a small percentage (1 percent) of the total SFR market.

The political risk is real but should be kept in proportion. AMH has responded by emphasizing its build-to-rent strategy, which adds housing supply rather than competing with homebuyers for existing inventory.

XII. The Bull and Bear Case

The Bull Case

Structural Demand: America faces a chronic housing shortage. Long-term tailwinds such as national high-quality single-family housing shortage, limited new construction, single-family rents being a lot cheaper than home ownership costs, and millennials aging into prime single-family living years, tend to favor AMH.

Affordability Gap: Renting an AMH home is currently about 27% more affordable than owning in the company's top markets, which creates a powerful secular tailwind for demand.

Build-to-Rent Moat: AMH has built an in-house development capability that most competitors cannot replicate quickly. Of those rental homes, 10,000 were built by AMH's homebuilding/build-to-rent operation. Additionally, AMH has another 10,000 build-to-rent homes in its development pipeline.

Balance Sheet Strength: AMH's balance sheet is now fully unencumbered, with all debt at fixed rates and no maturities until 2028.

Management Continuity: The leadership transition from Singelyn to Smith represents internal promotion of an executive who has been with the company since its early days, providing strategic continuity.

The Bear Case

Political Risk: Legislation targeting institutional landlords could restrict growth or impose additional costs.

Supply Risk: The increase in build-to-rent supply poses a significant challenge to rent growth potential. As more purpose-built rental homes enter the market, competition for tenants may intensify, potentially putting downward pressure on rental rates. This could lead to slower revenue growth.

Interest Rate Sensitivity: While AMH's debt is fixed-rate, higher rates affect both acquisition economics and home affordability dynamics.

Valuation: The stock trades at a premium valuation relative to historical averages, leaving less room for multiple expansion.

Operational Challenges: Managing 60,000+ scattered homes across 24 states creates inherent operational complexity.

XIII. Key Performance Indicators

For investors tracking AMH, two KPIs matter most:

1. Same-Home Core NOI Growth This metric strips out the impact of acquisitions and dispositions to reveal underlying operational performance. It captures both rent growth and expense management—the two levers that drive profitability on the existing portfolio. Same-Home Core NOI Growth came in at 4.1% for Q2 2025. Consistent mid-single-digit growth here indicates healthy operating performance.

2. Build-to-Rent Delivery Volume and Yields As acquisition economics have deteriorated, AMH's growth increasingly depends on its development program. Track both the number of homes delivered and the initial yields on those deliveries. 2025 yields are tracking just below mid-5% due to soft rent conditions. If yields fall significantly below 5%, the development program's economic rationale weakens.

XIV. Conclusion: The Wayne Hughes Legacy

The story of AMH is ultimately a story about vision, timing, and execution. Wayne Hughes saw something in the 2008 crisis that few others did: not just cheap houses to buy, but the opportunity to create an entirely new institutional asset class.

B. Wayne Hughes, founder of single-family rental pioneer American Homes 4 Rent as well as Public Storage, the world's largest self-storage company, is remembered as a real estate industry icon. Ten years ago, Hughes revolutionized the housing industry by unveiling American Homes 4 Rent, a company designed to provide single-family rental home options to American families. That founding helped revolutionize the home building industry. Hughes' legacy transcends his own company, and is reflected in the swiftly-growing multi-billion-dollar single-family rental industry.

The company Hughes founded has evolved far beyond its origins. From crisis opportunist buying foreclosed homes in Las Vegas to nationally recognized homebuilder delivering thousands of purpose-built rentals annually, AMH has navigated multiple strategic pivots while maintaining operational excellence.

"Our solid third quarter results once again demonstrate the benefits of the AMH strategy and outstanding execution from our team, driving Core FFO per share growth of 6.2%," stated Bryan Smith, AMH's Chief Executive Officer. "As we head into 2026, we are focused on driving momentum and leaning into the AMH strategy that continues to deliver industry-leading earnings growth and long-term shareholder value."

The single-family rental industry that Hughes helped create now manages hundreds of thousands of homes and houses millions of Americans. Whether you view that as solving a housing need or exacerbating affordability challenges depends on your perspective. What's undeniable is that Wayne Hughes, the sharecropper's son who rode to California during the Dust Bowl, saw an opportunity that others missed—twice—and built two of America's largest real estate companies as a result.

There really will never be anyone again like B. Wayne Hughes in the storage industry. He was the founder of the industry, the largest owner of storage that will probably ever have lived, and an inspiring story for all.

The same could now be said of single-family rentals.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube