CRH: The Quiet Giant That Built the World

I. Introduction & Episode Roadmap

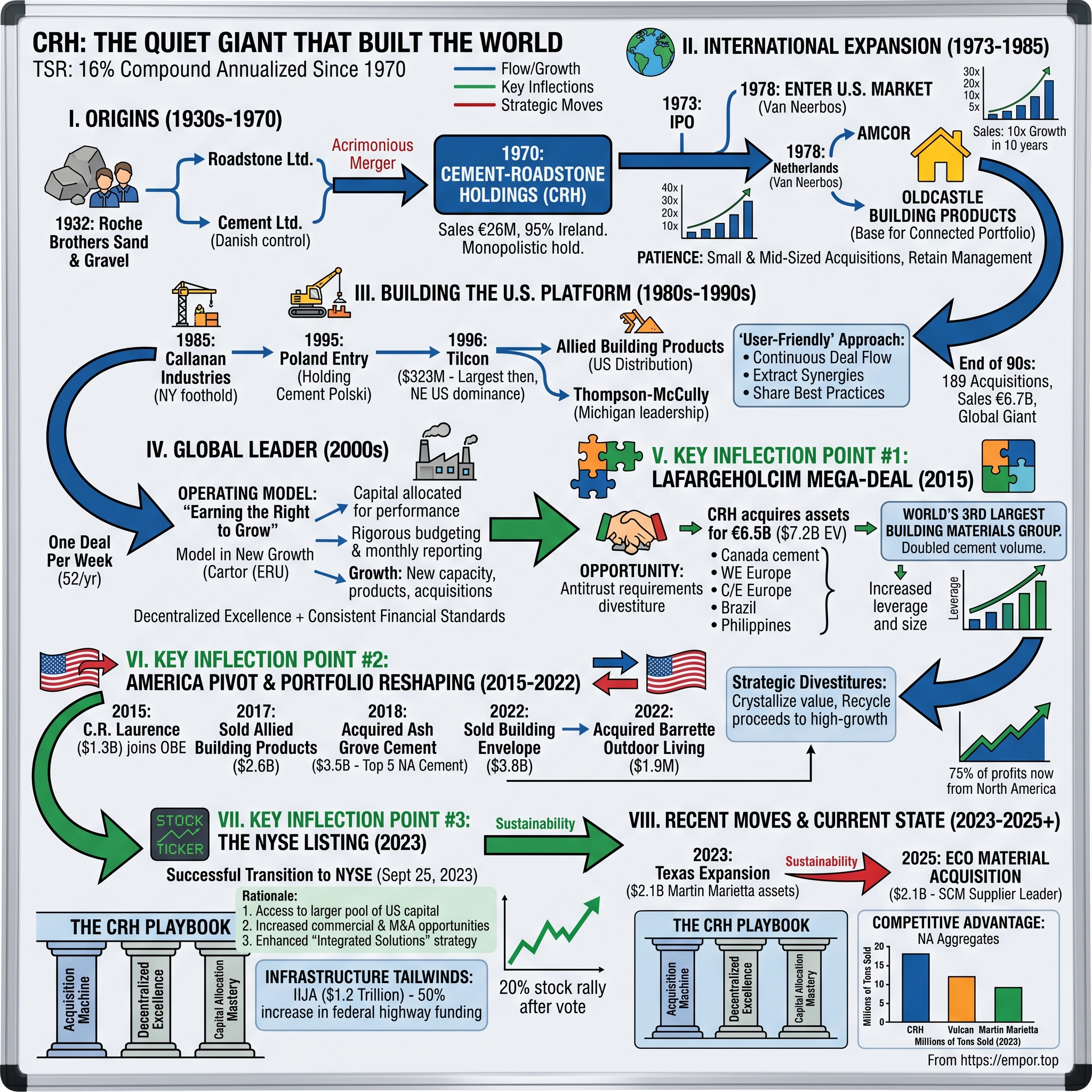

Imagine standing at the construction site of virtually any major infrastructure project in North America—a highway widening in Texas, a bridge repair in the Northeast, a data center foundation in Virginia. The odds are overwhelming that somewhere in the supply chain, you'd encounter materials bearing names like Oldcastle, Ash Grove, or Texas Materials. Trace the ownership of any of those brands, and every trail leads back to a corporate headquarters in Dublin, Ireland, and a company most Americans have never heard of: CRH.

CRH plc is a building materials provider headquartered in Dublin, operating in 28 countries through 3,816 locations with 79,800 employees, providing materials and integrated services for construction projects in transportation, infrastructure, buildings, and outdoor living sectors. How did a tiny Irish cement company born from an acrimonious merger become the largest building materials company in North America? The answer involves one of the most disciplined, patient, and relentlessly executed acquisition strategies in industrial history—a story that spans five decades, hundreds of acquisitions, and a transformation from a €27 million Irish monopoly into a $75+ billion global juggernaut.

CRH plc has a market cap of $75.74 billion, with an enterprise value of $92.20 billion. The Americas division employs approximately 47,400 people, accounting for 59% of CRH's global workforce, and operates 2,008 locations, representing 52% of the company's total locations. This division contributes roughly three-quarters of the company's overall profits.

What makes CRH's story remarkable isn't just the scale it achieved—it's how the company achieved it. While competitors like Cemex nearly went bankrupt during the 2008 financial crisis after aggressive debt-financed acquisitions, and Holcim diluted shareholders by 77% to acquire Lafarge, CRH pursued a fundamentally different playbook. It acquired hundreds of small and mid-sized family businesses, retained their management, extracted synergies through best-practice sharing rather than aggressive headcount cuts, and maintained the financial discipline to keep buying through multiple cycles.

Since 1970, CRH has achieved an industry-leading compound annualized long-term total shareholder return (TSR) of 16%. To put that in perspective: a $10,000 investment in CRH at its IPO would be worth millions today, vastly outperforming the broader market. This is the story of how a company selling rocks, cement, and asphalt—among the least glamorous businesses imaginable—became one of the greatest compounders in industrial history.

II. Origins: The Roach Brothers and Ireland's Cement Duopoly (1930s–1970)

The Founding Story

In 1932, on the rain-swept roads outside Dublin, two brothers named Tom and Donal Roche saw opportunity where others saw only mud. Ireland was a newly independent nation desperate to build infrastructure, and someone had to supply the sand, gravel, and stone that would pave its roads and construct its buildings. CRH's origins trace to 1932, when two brothers, Tom and Donal Roche, set up a sand-and-gravel haulage business. This would expand to become Roadstone Ltd., which then merged with Cement Ltd.

CRH started out in the 1930s as an aggregates business founded by the Roach brothers. Their company became Roadstone Ltd. in 1949, and for the next two decades remained one of only two authorized cement producers in Ireland. This was no accident—Ireland's regulatory environment created a protected duopoly, with only two companies licensed to produce cement for the entire nation.

The other licensed producer was the far larger Irish Cement, which was in fact owned by Danish interests. There's rich irony here: in a country fiercely proud of its independence from foreign control, the dominant cement producer was controlled from Copenhagen. This dynamic would eventually create the pressure that forged CRH.

The Irish economy and the construction industry languished during the 1950's, and although Roadstone continued to expand, the company went through difficult times. However, during the 60's Ireland entered a period of rapid economic growth, and it was then that management acquired key geographic land acquisitions with sound underlying stone reserves in preparation for the future. Some of these reserves continue to prosper today.

Tom Roche led the engineering and production side of the company while Donal Roche had the difficult task of ensuring finance and administration kept pace with growth of the company. At this time, the company also cultivated key people who brought new professionalism to planning, development, investment and people skills.

By the end of the 60's, Irish Cement had become the largest industrial company quoted on the Irish Stock Exchange, with Roadstone the third largest. In 1970, the two companies merged to become Cement-Roadstone Holdings, now known as CRH plc.

The "Acrimonious" Merger

In 1970, a merger—described as "acrimonious"—was pushed through, combining Roadstone and Irish Cement into a new company, Cement Roadstone Holdings, later known as CRH. The new company included operations in cement, aggregates, asphalt, and concrete products. Nearly all of the group's sales, which stood at the equivalent of €26 million in 1970, were generated in Ireland.

The term "acrimonious" barely captures the tension. The Danish-controlled Irish Cement had scale and capital; the Roche brothers' Roadstone had entrepreneurial energy and local relationships. Forcing these two cultures together required political pressure and regulatory arm-twisting. But from this contested union emerged a company with an unusual DNA: the operational excellence of a well-capitalized European industrial company combined with the deal-making instincts of ambitious Irish entrepreneurs.

The name itself tells the story of compromise: "Cement Roadstone Holdings" abbreviated to "CRH" simply to avoid favoring either legacy brand. Today, most people who know the company have no idea what the letters originally stood for—they've been reduced to a three-letter stock ticker that appears on the New York Stock Exchange alongside America's industrial elite.

What's remarkable is that from these €26 million beginnings in a small island nation, management already saw the limitations of their domestic market and began planning for something far more ambitious. The cement and aggregates industries are fundamentally local—transportation costs mean you can't ship crushed stone or ready-mix concrete economically over long distances. But the know-how, the operational systems, the acquisition playbook—those could travel anywhere.

III. The IPO and International Expansion Strategy (1973–1985)

Going Public

CRH, led by Tom Roach, went public in 1973. The public offering was made in part to fuel the group's expansion objectives. Although the group enjoyed a near-monopoly hold on much of Ireland's primary building materials sector, the country's small population left little room for growth.

The timing was propitious in another way: Coinciding with Ireland's entry into the European Economic Community (EEC), CRH expanded onto mainland Europe, establishing a presence in the Netherlands. The newly public company had a war chest for acquisitions and access to capital markets that would fund decades of growth to come.

CRH's strategic logic was crystalline: Ireland's population of around 3 million people could never support a major building materials company at global scale. Construction markets are cyclical, and concentration in a single small market meant vulnerability to local economic downturns. The only path to sustained growth—and protection against cyclicality—was geographic diversification.

First International Moves

In 1973, the same year it went public, CRH made its first international acquisition: CRH expanded into mainland Europe, establishing a presence in the Netherlands through the acquisition of Van Neerbos, a builders merchant with concrete products operations.

Five years later came the move that would ultimately define the company's future:

In 1978, the company entered the U.S. market with purchase of Amcor and formed a U.S. holding company, Oldcastle Building Products. Crossing the Atlantic, CRH took its first steps into the US market with the acquisition of Amcor, a concrete products company based in Utah. This was the foundation for the development of CRH's extensive and connected portfolio of Building Products.

This was a modest foothold—a concrete products company in Utah, hardly the center of American construction activity. But it established the beachhead that would eventually become an empire. The name "Oldcastle" would become CRH's primary brand in North America, eventually housing dozens of acquired businesses under its umbrella.

The Decade of Transformation

In 1970, the Group had sales of approximately €27 million, with 95% in Ireland. By 1979, it had grown to €328 million of annual sales, had completed 16 acquisitions, and was operating in four countries.

The growth rate was staggering: over 10x revenue growth in a single decade, with the share of Irish business dropping from 95% to a minority position. Management had proven they could identify targets, execute acquisitions, and integrate businesses across borders. The playbook was taking shape: find well-run family businesses with strong local positions, acquire them at reasonable valuations, retain management, share best practices across the portfolio, and repeat.

What distinguished CRH's approach from competitors was patience. Rather than pursuing transformational mega-deals, CRH accumulated dozens of smaller transactions. Each one was individually manageable, reducing integration risk. Each one brought local knowledge and relationships that would have been impossible to build organically. And each one was funded primarily from cash flow, minimizing the need for dilutive equity issuances or dangerous debt loads.

IV. Building the US Platform (1980s–1990s)

The 1980s: Strategic Growth Despite Recession

The early 1980s brought a global recession that devastated construction markets. Many building materials companies retreated, conserving cash and deferring expansion plans. CRH saw opportunity.

In 1985, Callanan Industries of New York was acquired. This wasn't just another bolt-on deal—it represented a strategic foothold in the massive Northeastern U.S. market. The New York metropolitan area and its surrounding region represented some of the most valuable construction markets in America, with virtually unlimited demand for infrastructure maintenance and renovation.

The Callanan acquisition proved prescient: it became a cornerstone of CRH's later dominance in the New York and Northeastern building materials markets. By establishing a presence in high-value markets early, CRH positioned itself to consolidate further as fragmented family businesses became available.

The "User-Friendly" Acquisition Approach

The Dublin, Ireland-based company has long pursued an active acquisition program, spending as much as €1 billion in a single year and typically targeting small and mid-sized businesses in order to build up an international network of companies. Most of CRH's acquisitions continue to operate under their former names and management, while taking advantage of their parent company's strong market position and international infrastructure.

This approach deserves deeper examination because it explains so much of CRH's success. The building materials industry is dominated by family-owned businesses, many of which have been operated by the same families for generations. A quarry owner in Pennsylvania or an asphalt producer in Ohio often has deep ties to local contractors, personal relationships with municipal procurement officers, and institutional knowledge about local geology and transportation routes that would take decades to replicate.

When CRH approaches an acquisition target, it promises something that private equity buyers typically cannot: continuity. The owner's name often stays on the building. The management team usually remains in place. Local employees keep their jobs. The company becomes part of a broader network that provides purchasing power, technical expertise, and growth capital—but the day-to-day character of the business remains largely unchanged.

This "user-friendly" approach has created a virtuous cycle. Satisfied sellers become evangelists, recommending CRH to peers considering their own exits. Deal flow begets deal flow. And because CRH develops a reputation for treating sellers fairly, it can often acquire businesses without competitive bidding, at valuations that create immediate value for shareholders.

The 1990s: Acceleration Phase

The next two decades marked rapid expansion as CRH entered new markets and increased its footprint across North America, while cementing its presence in Eastern Europe. By the end of the 1990s, CRH had more than a dozen operations in Poland, had completed 189 acquisitions, and sales reached €6.7 billion.

In 1995, CRH made its first entry into Poland, buying Holding Cement Polski, which later gained majority control of Cementownia Ozarow, one of the country's major cement producers. That acquisition also marked the first CRH cement manufacturing operation outside of Ireland. By the end of the decade, CRH numbered more than a dozen operations in Poland.

The purchase of Tilcon for $323 million was CRH's largest acquisition at that time, establishing a unique regional position in the materials markets of the Northeastern US. In the same year, the acquisition of Allied Building Products gave CRH a fifth core business in the US and a first presence in US distribution.

Approaching its 30th anniversary, CRH continued its expansion into the US Midwestern materials market with the acquisition of Thompson-McCully, the leading aggregates and asphalt manufacturer in southern Michigan. In Europe, CRH entered cement in the Ukraine and strengthened its position in concrete and aggregates in Poland. It also purchased Finnsementti and Lohja Rudus, gaining a leading market position in cement, aggregates and concrete products in Finland and a presence in the Baltic region for the first time.

The pattern was consistent: identify attractive markets, establish positions through well-timed acquisitions, then consolidate and optimize. By the end of the 1990s, CRH had transformed from an Irish company with international operations to a genuinely global building materials giant with leading positions across multiple continents.

V. The 2000s: Becoming a Global Leader

One Deal Per Week

By the turn of the century, CRH had become an international building materials leader, raising the bar even higher and completing a further 52 acquisitions per year in the 2000s, roughly one deal per week.

By the turn of the century, CRH had established itself as one of the world's leading building materials companies, with 37,000 employees at more than 1,100 locations in 18 countries worldwide and sales of close to €7 billion. The 2000s saw CRH continuing to raise the bar, completing on average a further 52 acquisitions per year, or roughly one deal per week.

Think about what one deal per week means operationally. Every week, somewhere in the CRH organization, a team was identifying a target, conducting due diligence, negotiating terms, executing legal documentation, and beginning integration planning. This requires institutional capability that few companies possess—dedicated M&A teams, standardized processes for valuation and integration, and a corporate culture that views acquisitions as a core competency rather than occasional events.

The Operating Model

Throughout the Group, businesses are required to deliver performance by achieving a targeted return on capital employed, thereby earning the right to grow: key performance metrics are understood and consistently applied across the Group; financial control is exercised through a rigorous annual budgeting process and timely monthly reporting; monthly results are vetted by Divisional management and critically reviewed at Group headquarters. Growth is achieved through investing in new capacity, developing new products and markets, by acquiring and growing mid-sized companies, augmented from time to time with larger deals.

The phrase "earning the right to grow" captures CRH's philosophy. Capital allocation is not centrally dictated—it flows to business units that demonstrate they can generate attractive returns. This creates powerful incentives for local management to optimize operations, because the reward for strong performance is additional capital for growth investments. Conversely, underperforming units find their capital constrained until they demonstrate improvement.

This decentralized approach solved a problem that has plagued many acquisition-driven companies: how to maintain entrepreneurial energy as the organization scales. By preserving local autonomy while enforcing consistent financial standards, CRH avoided both the bureaucratic ossification of over-centralized companies and the chaos of loosely managed conglomerates.

VI. Key Inflection Point #1: The LafargeHolcim Mega-Deal (2015)

The Opportunity

In 2015, the cement industry witnessed a seismic shift. France's Lafarge and Swiss peer Holcim announced merger plans, hoping to cut costs and tackle overcapacity and weak demand. The new company would be the world's biggest cement maker with $44 billion in annual sales.

But creating the world's largest cement company came with a significant complication: antitrust regulators required LafargeHolcim to divest substantial assets in markets where the combined company would have excessive market share. This created a once-in-a-generation opportunity for a disciplined buyer willing to write a large check.

Irish building supplies group CRH said it had agreed to pay €6.5 billion ($7.35 billion) for assets Lafarge and Holcim were obliged to sell ahead of their planned merger. CRH said it will fund the acquisition with cash, new debt and a 9.99 percent equity placing, and beat a consortium led by Blackstone, who were also in the running.

The Transformation

In February 2015, CRH acquired assets worth US$6.5 billion from LafargeHolcim, becoming the world's third-largest building materials group by market value. This acquisition almost tripled CRH's net debt, bringing it to €6.6 billion.

CRH entered the top three in building materials globally with the acquisition of a portfolio of assets from Lafarge-Holcim for an enterprise value of $7.2 billion. The deal doubled CRH's cement volume and expanded the Company's cement, aggregates and readymixed concrete portfolio.

"Today we extend a warm welcome to 15,000 new colleagues joining CRH. With their expertise and talent on board, combined with the strength of our existing employee base, CRH is a step closer to achieving our aim of becoming the world's leading building materials company. The businesses we are acquiring, which represent an excellent geographic fit with CRH's existing operations, are all strong performers in their respective areas."

The acquired assets included: the largest cement producer in central Canada; major cement and aggregates operations in western Europe's three largest markets—the UK, France and Germany; leading cement and aggregates companies in the growth regions of central and eastern Europe, creating a strong regional cluster in which CRH became the number one heavy-side building materials company; and entry positions of scale in two emerging economic regions—Brazil and the Philippines.

Why This Deal Matters

The LafargeHolcim deal represented a departure from CRH's traditional bolt-on strategy—this was transformational, not incremental. But it exemplified CRH's opportunistic discipline: acquiring quality assets at attractive valuations when forced sellers had limited alternatives.

Critically, CRH did not overpay. By competing against a Blackstone-led consortium rather than strategic buyers, CRH avoided a bidding war with competitors who might have assigned strategic premiums. The assets were acquired at cycle-appropriate valuations, with meaningful synergy potential through integration with existing CRH operations.

The deal also demonstrated CRH's ability to mobilize capital at scale. The combination of cash, debt, and a modest equity placing showed financial markets that CRH could execute large transactions without imperiling its investment-grade credit rating or massively diluting shareholders.

VII. Key Inflection Point #2: The America Pivot & Portfolio Reshaping (2015–2022)

Doubling Down on North America

Following the LafargeHolcim deal, CRH's strategic direction became unmistakable: North America was the future, and the company would reshape its portfolio accordingly.

In August 2015, C.R. Laurence Co. Inc. announced it would be acquired by Oldcastle BuildingEnvelope, a subsidiary of Irish building products giant CRH Group, for $1.3 billion in cash. With 48 locations in North America and 4,500 employees, OBE had the largest footprint in the industry. Forecasted CRL sales for 2015 were $570 million, on which EBITDA of $115 million was expected.

By 2017, CRH's share price had increased 80% since 2014. The market was rewarding CRH's strategic clarity and execution excellence.

On 21 September 2017, CRH announced that it had reached an agreement to acquire Ash Grove Cement Company, a leading U.S. cement manufacturer headquartered in Overland Park, Kansas, for a total consideration of US$3.5 billion. The transaction closed in June 2018.

Ash Grove Cement Company was a cement manufacturer based in Overland Park, Kansas. It was the largest US-owned cement company until it was acquired in 2018 by CRH, a global building materials business headquartered in Ireland.

The divestment of the US Distribution business at a high multiple provided the opportunity to recycle the proceeds into higher growth areas, and shortly after CRH acquired Ash Grove Cement Company in the US for a total consideration of $3.5 billion, complementing its cement portfolio. Now, CRH was a top five cement producer in North America, with operations across Florida, Texas, the Midwest and Western US, and Canada.

Strategic Divestitures

Portfolio optimization wasn't just about acquisitions—CRH also proved willing to exit businesses that no longer fit strategically.

In 2017, CRH sold Allied Building Products to Beacon Roofing Supply for $2.6 billion.

The company's portfolio restructuring continued in 2022. In February, CRH sold its Building Envelope business to KPS Capital Partners for $3.8 billion. In June, the company acquired Barrette Outdoor Living, an Ohio-based manufacturer with ten U.S. facilities, for $1.9 billion.

The Building Envelope divestiture was particularly notable—this was a business CRH had built through acquisitions including C.R. Laurence, which it had purchased just seven years earlier. But management concluded that the business was worth more to a buyer focused on that specific segment than to CRH, which could redeploy the proceeds into higher-margin, more strategic opportunities.

This willingness to sell positions that have appreciated—to crystallize value rather than hold indefinitely—distinguishes truly disciplined capital allocators from empire builders who can never part with assets they've acquired.

VIII. Key Inflection Point #3: The NYSE Listing (2023)

The Historic Move

CRH plc announced the successful transition of its primary listing to the New York Stock Exchange (NYSE) on September 25, 2023, which marked a historic milestone for the Group.

Shareholders overwhelmingly approved the unanimous recommendation of the Board and management team to transition to a US primary listing on the New York Stock Exchange at an Extraordinary General Meeting. The Group retained a standard listing on the London Stock Exchange and de-listed from Euronext Dublin.

For a company founded in Ireland, this was a momentous decision. CRH had been a cornerstone of the Irish stock market for over fifty years, one of the largest Irish-headquartered public companies. Moving the primary listing to New York sent an unmistakable signal about where CRH saw its future.

The Rationale

North America represents approximately 75% of Group EBITDA and the US is expected to be a key driver of future growth for CRH due to continued economic expansion, a growing population and significant construction needs.

A US primary listing would bring increased commercial, operational and acquisition opportunities for the business, further accelerating the successful integrated solutions strategy and delivering even higher levels of profitability, returns and cash for shareholders.

CRH now generates three-quarters of its earnings in North America. The building materials giant remained headquartered and tax resident in Ireland. However, it is believed its advisers thought it would be easier for the S&P 500 committee to include the company on the benchmark index if it were not also listed in Dublin, where most of the trading volume in the stock takes place.

Irish building product giant CRH Plc's move to transfer its primary listing from London to New York sparked a rally that lifted the stock 20% in British pound terms since shareholders voted to approve the shift, helped in no small part by becoming one of the most popular hedge fund buys in the third quarter.

The listing change also served practical purposes: American institutional investors, who manage the vast majority of global equity capital, often face restrictions on holding foreign-listed securities. By listing primarily on the NYSE, CRH made itself accessible to a far larger pool of potential shareholders, including index funds that track US benchmarks.

Infrastructure Tailwinds

The timing aligned with massive tailwinds for US infrastructure spending. The Infrastructure Investment and Jobs Act (IIJA), also known as the Bipartisan Infrastructure Law, was signed into law by President Biden on November 15, 2021. The law authorizes $1.2 trillion for transportation and infrastructure spending with $550 billion of that figure going toward "new" investments and programs.

As the largest roadbuilder in North America, CRH is well positioned to commence public infrastructure projects underpinned by the $1.2 trillion Infrastructure Investment and Jobs Act, which will see a 50% increase in federal highway funding.

"As IIJA is implemented, my company and the entire construction industry find it critical to ensure the funds authorized and appropriated continue to flow as intended for the life of the bill," a CRH executive stated. "The IIJA will provide certainty to state DOTs and everyone involved in delivering infrastructure projects."

IX. Recent Moves & Current State (2023–2025)

Texas Expansion

CRH reached an agreement to acquire an attractive portfolio of cement and readymixed concrete assets in Texas from Martin Marietta Materials, Inc. for a total consideration of $2.1 billion. The combined portfolio of assets was expected to generate pro-forma 2023 EBITDA of approximately $170 million. The Assets comprised a 2.1mt capacity cement plant located between San Antonio and Austin, a network of terminals along the eastern gulf coast of Texas and a portfolio of 20 readymixed concrete plants with annual shipments of approximately 1.6m cubic yards serving the Austin and San Antonio markets.

One reason why CRH may have gone all out for a cement plant in Texas is because it is one of the few states in the US where cement shipments actually increased in 2023. Data from the United States Geological Survey shows that shipments of Portland and blended cement fell by 2% year-on-year, yet Texas comprehensively bucked this trend with shipments rising by 10% to 8.04Mt.

The Eco Material Acquisition (2025)

On July 29, 2025, CRH announced that it had signed an agreement to acquire Eco Material Technologies (Eco Material), a leading supplier of Supplementary Cementitious Materials (SCMs) in North America, for a total consideration of $2.1 billion. The business will operate as Eco Material Technologies, a CRH Company.

"This strategic acquisition further positions CRH as a leading cementitious player in North America with both cement and SCM capabilities. This transaction demonstrates CRH's disciplined approach to capital allocation, building market-leading positions in higher-growth markets with secular tailwinds and superior returns."

The transaction secures the long-term supply of critical materials for future growth and puts CRH at the forefront of the transition to next generation cement and concrete. With more than 1,100 Eco Material employees joining the CRH team, the combined operations create a more connected business to better serve customers.

CRH previously announced on July 29, 2025 that it had reached an agreement to acquire North America's leading supplier of Supplementary Cementitious Materials (SCMs) for a total consideration of $2.1 billion. The acquisition subsequently closed in September 2025.

Latest Results

CRH reported third quarter 2025 financial results with total revenues of $11.1 billion (Q3 2024: $10.5 billion), 5% ahead of the prior year period driven by positive demand, strong commercial execution and contributions from acquisitions.

CRH's net income margin of 13.7% was ahead of Q3 2024 (13.2%), while Adjusted EBITDA margin of 24.3% (Q3 2024: 23.3%) was also ahead of the comparable prior year period. During the quarter, CRH completed nine acquisitions for a total consideration of $2.5 billion, enabled by CRH's unmatched scale, connected portfolio, and proven growth capabilities.

Year-to-date, CRH has invested $3.5 billion in 27 acquisitions, enhancing growth opportunities.

Jim Mintern, Chief Executive Officer, stated "CRH delivered a strong third quarter performance driven by favorable underlying demand, positive pricing momentum and further contributions from acquisitions. We are pleased to reaffirm Net income and raise our Adjusted EBITDA guidance for 2025, representing another record year for CRH."

Leadership Transition

In a significant transition, CRH appointed Jim Mintern as its next CEO. He started in 2025 following the retirement of Albert Manifold, who had planned to retire at the end of 2024. Manifold continued as an advisor to CRH until the end of 2025.

Mintern was CRH's Chief Financial Officer and had been a director of its board since mid-2021. He holds over 30 years of experience in the building materials industry and has worked for CRH for 22 years in various management positions. Mintern joined CRH in 2002 as the Finance Director for Roadstone, and other postings since then included Country Manager for Ireland, Managing Director of each of the Western and Eastern regions of the group's Europe Materials Division and Chief of Staff to the CEO. He also led the transition of CRH's primary listing to the New York Stock Exchange. Mintern is a graduate from University College Dublin with degrees in accounting and commerce.

During Albert Manifold's 26-year career at CRH, he served in a number of senior positions, including chief executive officer from 2014 until December 2024. He is recognized for building CRH into one of the leading providers of building materials solutions in North America and Europe, growing the company from a traditional seller of cement and other base materials into full-scale construction services. During Manifold's 11 years as CEO, CRH's share price surged 400 percent on the London Stock Exchange.

X. The CRH Playbook: Business & Investing Lessons

The Acquisition Machine

Despite slight misses versus consensus estimates, CRH demonstrated robust growth in net income and adjusted EBITDA, driven by favorable demand and strategic acquisitions. CRH is a prominent global manufacturer of building products, operating through a vertically integrated business model. Over the past decade, CRH has evolved into a leading building materials business, with increasing exposure to upstream building activities such as aggregates and cement.

What makes CRH's acquisition model work? Several elements combine:

Scale without bureaucracy: CRH maintains standardized financial reporting and performance metrics across thousands of locations while preserving local operational autonomy. Central teams provide best-practice sharing, procurement leverage, and capital allocation discipline without micromanaging day-to-day operations.

Seller-friendly reputation: By treating acquired businesses and their management teams well, CRH generates proprietary deal flow. Sellers seek out CRH, reducing competition and enabling more favorable pricing.

Countercyclical courage: CRH has consistently acquired during downturns when others retreated, securing assets at attractive valuations that compound value over subsequent cycles.

Integration without destruction: Rather than gutting acquired businesses, CRH extracts synergies through shared services, purchasing power, and operational best practices while preserving the local relationships and institutional knowledge that made those businesses attractive acquisition targets in the first place.

Decentralized Excellence

In aggregates, competition is typically localized due to high transportation costs, with market leadership often determined by proximity to reserves and end markets. CRH's extensive quarry network and strategic locations provide competitive advantages in many markets.

This geographic reality shapes CRH's operating model. Because materials can't economically travel far, local positions matter enormously. A quarry in the right location—near growing metropolitan areas, with access to transportation infrastructure—can generate attractive returns for decades. CRH's strategy of acquiring well-positioned local businesses gives it access to these irreplaceable geographic assets.

Capital Allocation Mastery

CRH reduced its shares outstanding from 785 million in 2020 to 683 million by 2024, a reduction of over 13%. This has provided a substantial boost to earnings per share and is a key driver of its outperformance against peers like Holcim and Heidelberg on a total shareholder return basis.

CRH wins on overall financials by a wide margin, due to superior profitability, a much stronger balance sheet, and consistent shareholder returns. Over the past decade, CRH has been a steady compounder of value, delivering consistent revenue and EPS growth.

CRH's capital allocation framework balances four priorities: organic growth investment, acquisitions, debt management, and shareholder returns. Rather than rigidly adhering to any single priority, management flexes between them based on relative opportunity costs. When acquisition targets are scarce or expensive, buybacks accelerate. When transformational opportunities arise, the company can mobilize substantial capital without straining its balance sheet.

XI. Porter's 5 Forces & Hamilton's 7 Powers Analysis

Porter's Five Forces

1. Threat of New Entrants: LOW

In aggregates, competition is typically localized due to high transportation costs, with market leadership often determined by proximity to reserves and end markets. CRH's extensive quarry network and strategic locations provide competitive advantages in many markets.

Building a new quarry or cement plant requires years of permitting, massive capital investment, and access to geological reserves that are finite and often already controlled by incumbents. Environmental regulations have made it nearly impossible to permit new quarries near urban centers where demand is highest. These barriers create durable moats around existing operations.

2. Bargaining Power of Suppliers: LOW-MODERATE

CRH controls its own raw materials through thousands of quarries and cement plants, dramatically reducing supplier dependency. The primary cost exposure is energy (for cement kilns) and labor, where the company has limited negotiating leverage but benefits from scale in procurement.

3. Bargaining Power of Buyers: MODERATE

Construction contractors need materials delivered reliably and proximally. While large contractors can negotiate pricing, they cannot easily source materials from distant suppliers due to transportation costs. This creates natural geographic pricing power for local suppliers. However, commodity-like materials face pricing pressure during economic downturns when multiple suppliers compete for reduced demand.

4. Threat of Substitutes: LOW

There are no meaningful substitutes for aggregates, cement, and asphalt in construction applications. Alternative materials have emerged in some building envelope applications, but for infrastructure—roads, bridges, foundations—traditional materials remain essential. The sustainability push may shift cement formulations (hence CRH's Eco Material acquisition) but won't eliminate cement demand.

5. Competitive Rivalry: MODERATE

CRH operates in highly competitive regional building materials markets, competing against both large multinational companies and smaller regional players. In North America, the company's primary competitors include Vulcan Materials Company, Martin Marietta Materials, and Heidelberg Materials. These companies compete primarily in aggregates, cement, and ready-mixed concrete markets across overlapping geographic regions.

On crushed stone production rankings, Vulcan Materials tops the list as the nation's largest crushed stone producer. Martin Marietta again ranks second, followed by CRH Americas Materials (No. 3), Heidelberg Materials (No. 4) and Holcim US (No. 5).

Competition is intense but disciplined among major players, who generally avoid destructive price wars. Geographic segmentation means different competitors dominate different regions, reducing direct head-to-head conflict.

Hamilton's 7 Powers

Process Power: CRH's acquisition integration playbook, developed over hundreds of transactions across five decades, represents institutionalized organizational knowledge that competitors cannot easily replicate. The company's ability to execute one deal per week during peak acquisition periods reflects process excellence that took decades to develop.

Scale Economies: CRH's purchasing power across 3,800+ locations provides meaningful procurement advantages. The company can negotiate better terms with equipment suppliers, insurance providers, and other vendors than smaller regional competitors.

Switching Costs: While individual product switching costs are low, CRH's integrated solutions approach creates broader customer relationships. A contractor using CRH for aggregates, cement, ready-mix concrete, and asphalt faces higher switching costs than one sourcing each material separately.

Network Effects: Limited in the traditional sense, but CRH's acquisition reputation creates a form of network effect in the M&A market—the more successful acquisitions CRH completes, the more sellers seek it out, improving future deal flow.

Counter-Positioning: CRH's decentralized model represents a strategic choice that large European competitors have been slow to adopt. Attempting to copy CRH's approach would require competitors to accept lower control, different organizational structures, and patient capital deployment timeframes that may conflict with their existing models.

Branding: Individual CRH brands (Oldcastle, Ash Grove, etc.) have strong local recognition, though CRH itself has limited brand value with end consumers. Brand matters more with professional contractors who value reliability and local relationships.

Cornered Resource: CRH's quarry reserves represent finite geographic assets that cannot be replicated. Many quarries are located near high-demand urban markets where new permits are virtually impossible to obtain, creating perpetual geographic advantages.

XII. Key Metrics to Watch

For investors tracking CRH's ongoing performance, three key performance indicators merit particular attention:

1. Return on Capital Employed (ROCE)

This is CRH's internal "North Star" metric, representing the return generated on invested capital. Consistently high ROCE (historically 10-15%) indicates disciplined capital allocation and validates the acquisition strategy. Declining ROCE could signal overpayment for acquisitions or operational deterioration. CRH's ability to maintain ROCE above its cost of capital while deploying billions annually in acquisitions demonstrates the quality of its capital allocation process.

2. EBITDA Margin Expansion

CRH's Adjusted EBITDA margin of 24.3% (Q3 2024: 23.3%) was ahead of the comparable prior year period. Consistent margin expansion indicates pricing power, operational improvement, and successful integration of acquired businesses. CRH has delivered eleven consecutive years of margin expansion—any reversal would warrant careful scrutiny.

3. Acquisition Spending vs. Organic Growth Investment

CRH deploys capital through both acquisitions and organic growth projects. The balance between these—and the returns generated from each—indicates management's assessment of relative opportunity. Heavy acquisition spending suggests attractive external opportunities; increased organic investment suggests high-return internal projects. Monitoring the split helps investors understand strategic priorities and capital allocation discipline.

XIII. Bull Case vs. Bear Case

Bull Case

Infrastructure supercycle: The $1.2 trillion Infrastructure Investment and Jobs Act provides a five-year runway of elevated federal infrastructure spending, with CRH positioned as the largest supplier of materials for roads, bridges, and utility infrastructure in North America. This secular tailwind underpins demand visibility unprecedented in the company's history.

Compounding machine: With a 16% compound annual TSR since 1970, CRH has demonstrated the ability to compound value across multiple economic cycles, management teams, and market environments. The acquisition playbook, financial discipline, and decentralized excellence create a durable formula for continued compounding.

Market leadership advantages: As the largest producer of aggregates and asphalt in the United States, CRH benefits from scale economies, quarry reserve advantages, and geographic positioning that smaller competitors cannot match. Consolidation opportunities remain abundant in a still-fragmented industry.

Sustainability positioning: The Eco Material acquisition positions CRH for the transition to lower-carbon cement and concrete products. Rather than viewing decarbonization as a threat, CRH is positioning itself to lead the industry transition, potentially capturing share from competitors slower to adapt.

Bear Case

Cyclical exposure: Construction is inherently cyclical, and CRH's revenues would decline significantly in a severe recession. The 2008-2009 financial crisis devastated the industry, and similar conditions would pressure even well-positioned players.

Political risk to infrastructure funding: The IIJA funding runway depends on continued political support. Future administrations or congressional majorities could redirect funding, delay implementation, or alter project priorities in ways that reduce demand for CRH's products.

Acquisition integration risk: While CRH has an excellent historical track record, any acquisition-dependent strategy faces risks from overpayment, integration failures, or cultural mismatches. A single large failed acquisition could impair returns for years.

Interest rate sensitivity: Construction activity correlates with interest rates—higher rates reduce residential construction and can delay commercial projects. While CRH's infrastructure exposure provides some insulation, sustained high interest rates would pressure certain end markets.

XIV. Conclusion: The Quiet Giant's Future

From €27 million in sales in an Irish duopoly to $75+ billion in market capitalization as the largest building materials company in North America, CRH's journey represents one of the most remarkable value creation stories in industrial history. The company's success stems not from technological breakthroughs or visionary products but from relentless execution of a fundamentally sound strategy: acquire well-positioned local businesses, retain their management and local knowledge, extract synergies through scale and best-practice sharing, and deploy capital with discipline across cycles.

Since 1970, CRH has achieved an industry-leading compound annualized long-term total shareholder return (TSR) of 16%. This performance didn't result from luck or timing—it reflects five decades of consistent execution by multiple management teams adhering to a proven playbook.

Looking forward, CRH faces a strategic environment arguably more favorable than at any point in its history. The US infrastructure funding picture provides unprecedented demand visibility. The company's portfolio is optimized around its highest-margin, highest-growth North American markets. The NYSE listing provides access to the deepest capital markets in the world. And the decarbonization transition, through the Eco Material acquisition, positions CRH as a leader rather than a laggard.

The quiet giant that built much of the physical infrastructure of North America and Europe now stands positioned to build the next generation. For investors seeking exposure to the physical economy—to the roads, bridges, and buildings that underpin modern civilization—few companies offer the combination of scale, discipline, and track record that CRH has demonstrated.

The letters "CRH" may have started as an abbreviation of "Cement Roadstone Holdings," but today they represent something far more significant: a masterclass in patient capital deployment, operational excellence, and the power of compounding returns over decades.

XV. Comparative Competitive Analysis

CRH vs. Global Peers

Understanding CRH's competitive position requires examining how it stacks up against the other titans of the global building materials industry. The comparison reveals why CRH has delivered superior shareholder returns despite operating in what appears to be a commodity business.The North American Aggregates Triumvirate

In North America, CRH competes head-to-head with two formidable rivals: Vulcan Materials and Martin Marietta Materials. CRH is the largest aggregates company in the Americas with 230 million tons of aggregates sold, primarily in the US, in 2024, representing approximately 9.5% market share, and 18.4 billion tons of proven and probable reserves. Vulcan Materials is the second largest aggregates company in the Americas with 224 million tons sold in 2024 and 16.5 billion tons of reserves. Martin Marietta is third-largest with 191 million tons sold and 16.8 billion tons of reserves.

CRH, Vulcan Materials, and Martin Marietta Materials possess all the elements necessary—dominant physical networks plus NIMBY dynamics plus increasing demand—to serve as durable toll collectors on North American construction. The competitive dynamics among these three giants are notable for their discipline: rather than destructive price wars, the industry has evolved toward rational competition focused on service quality and geographic positioning.

CRH offers a more diversified approach with a very strong North American presence, solid profitability, and a more attractive valuation. Vulcan's key strengths are its phenomenal moat in U.S. aggregates and its correspondingly high profit margins (operating margin approximately 20%), though its valuation prices in much of its future success.

The European Giants

Globally, CRH competes against the other members of what industry observers call "The Big Four" of heavy building materials: Holcim, Heidelberg Materials, and CEMEX. These companies have diverse product lines serving worldwide markets, specifically in cement, aggregates, ready-mix concrete, and aligned verticals, emerging as leaders in scale of operations, decarbonization, and innovation across Europe and the Americas.

CRH retains market leading position as the largest heavy-side materials organization in both Europe and North America. CRH's success as a business is largely due to its unique and differentiated strategy, running not as a materials business but as an integrated solutions organization.

Heidelberg Materials stands as another of the "big three" global cement and aggregates producers, competing directly with CRH across Europe and North America. Like CRH, it is a vertically integrated giant, but its historical core has been in cement production. In contrast to CRH's aggressive M&A-fueled expansion and pivot to North America, Heidelberg has been more focused on portfolio optimization and debt reduction following its large Italcementi acquisition, making it a more financially disciplined, if somewhat slower-growing, competitor.

Compared to peers, S&P views Heidelberg Materials as less diversified with a smaller absolute free operating cash flow base and somewhat higher leverage than companies like Holcim, CRH, and Compagnie de Saint-Gobain.

The Valuation Gap

One of the most interesting competitive dynamics involves valuation disparities between US-listed and European-listed building materials companies. Restoring the United States's infrastructure and reshoring its manufacturing requires a gargantuan amount of rocks. Suppliers of cement and granular aggregates are set to be huge beneficiaries of federal investment—and the winners include several European giants: CRH, Holcim, and Heidelberg Materials. Yet their shares have been valued at a fraction of US peers. Listing shares in the US, as CRH did, might encourage investors to give them a second look.

This valuation arbitrage was a key driver behind CRH's decision to move its primary listing to the NYSE—and the subsequent stock appreciation validated the strategic logic.

XVI. Management and Governance

The Albert Manifold Era

Any analysis of CRH's modern success must acknowledge the transformational leadership of Albert Manifold, who served as CEO from 2014 until December 2024. During his tenure, Manifold oversaw CRH's evolution from a traditional European building materials company into the dominant North American infrastructure supplier.

Manifold's strategic clarity proved exceptional. He recognized earlier than many peers that North America offered superior growth prospects and returns, and he systematically repositioned CRH's portfolio to capture this opportunity. The LafargeHolcim acquisition, the NYSE listing, and the sustained focus on operational excellence all bore his strategic fingerprints.

Board Structure and Oversight

The CRH Board is responsible for the leadership, oversight, control, development and long-term success of the Group. It is also responsible for instilling the appropriate culture, values and behavior throughout the organization.

Richie Boucher has served as Chairman since 2018. Prior to this, he served as Chief Executive of Bank of Ireland Group plc from 2009 to 2017 and held several positions at Bank of Ireland, Royal Bank of Scotland, and Ulster Bank. He currently serves as a Director at Kennedy-Wilson Holdings Inc. and Clonbio Group Limited.

The Board operates through several key committees that provide specialized oversight:

The Nomination & Corporate Governance Committee's primary responsibilities include identifying and recommending candidates to fill Board vacancies, reviewing the independence of each Director, considering succession planning for Directors and other senior executives, and keeping under review the leadership needs of the Group with a view to ensuring continued ability to compete effectively in the marketplace.

The Safety, Environment & Social Responsibility Committee reviews at least annually the safety, environment, and social responsibility performance of the Group, reviews findings from audits of safety and environment performance across the Group, reviews management's implementation of recommendations to improve performance, and makes periodic visits to locations worldwide to become familiar with the nature of operations.

The Jim Mintern Succession

The transition from Albert Manifold to Jim Mintern represents continuity rather than disruption. Mintern's deep institutional knowledge—over 22 years with CRH across multiple roles including Finance Director for Roadstone, Country Manager for Ireland, Managing Director of European divisions, and Chief Financial Officer—provides strategic continuity while bringing fresh perspective to execution.

Jim Mintern has served as Chief Executive Officer and a Director of the company since 2021. Prior to this, he served as Director of Finance at the company.

The fact that CRH promotes CEOs from within, after decades of experience across the organization, reflects both the complexity of the business and the importance of institutional knowledge. An outsider CEO would require years to understand the nuances of CRH's decentralized operating model, its acquisition integration processes, and its relationships with thousands of acquired businesses.

Ownership Structure

CRH's shareholder base reflects its transformed identity as a primarily American company listed in New York. Major institutional shareholders include Fidelity Management & Research Co. LLC and BlackRock Advisors LLC. The transition to NYSE listing has attracted substantial American institutional capital, supporting both the company's trading liquidity and its strategic access to North American acquisition targets.

XVII. Sustainability and the Decarbonization Challenge

The Carbon Problem

Cement production is among the most carbon-intensive industrial processes on Earth, responsible for approximately 7-8% of global CO2 emissions. The chemistry is unavoidable: producing Portland cement requires heating limestone (calcium carbonate) to extremely high temperatures, which releases CO2 both from the chemical reaction and from the fuel combustion required to achieve those temperatures.

For CRH, with its massive cement operations across North America and Europe, decarbonization represents both an existential challenge and a strategic opportunity. Companies that solve the carbon problem will dominate the industry's future; those that fail to adapt will face regulatory pressure, customer defection, and stranded assets.

CRH's Decarbonization Strategy

CRH has established ambitious, Science-Based Targets initiative (SBTi) validated decarbonization commitments. CRH commits to reduce gross Scope 1 and Scope 2 Greenhouse Gas emissions 33.5% per tonne of cementitious product by 2030 from a 2021 base year. CRH also commits to reduce absolute gross Scope 1 and Scope 2 GHG emissions from other activities 42.0% by 2030 from a 2021 base year. CRH further commits to reduce gross Scope 3 GHG emissions 23.5% from purchased clinker and cement per tonne purchased over the same timeframe.

The company has developed a decarbonization roadmap with a long-term goal of achieving net-zero emissions by 2050. This roadmap includes interim targets, such as reducing cement-specific net CO2 emissions to 520 kg CO2e per tonne by 2025, down from 777 kg CO2e in 1990.

CRH is not relying on carbon offsetting to achieve its 2030 emission reduction target and is committed to decarbonizing its operations and value chain.

Practical Decarbonization Initiatives

CRH is pursuing multiple pathways to reduce emissions:

CRH Company Ash Grove lowered the clinker factor by 6% between 2021 and 2024 in the Leamington cement plant while maintaining product performance. Replacing clinker with limestone reduced CO2 emissions by 50,000 tonnes.

Romcim, in CRH's International Division, installed five wind turbines with a total capacity of approximately 30 MW at their cement plant site in Medgidia. The wind farm is Romania's first wind farm exclusively powering a cement plant and will generate clean and renewable energy, contributing a reduction of over 36,000 tonnes of CO2 annually.

CRH's cement plant in Rohožník, Slovakia has made clinker efficiencies through the replacement of 20% raw materials with alternatives.

Investment in Breakthrough Technologies

Beyond operational improvements, CRH is investing in next-generation technologies that could fundamentally transform cement production. Holcim and CRH have announced plans to invest $75 million in a low-carbon cement production method developed by Sublime Systems, looking for ways to decarbonize the cement production process in their operations.

Sublime came up with a method for cement production that provides an electrochemical alternative to the heating up of limestone with fossil-fuel-based kilns. According to Leah Ellis, co-founder and CEO at Sublime, tests conducted at their 250-ton-per-year pilot plant showed a 90% reduction in CO2 emissions compared to traditional concrete production.

CRH Ventures, the venture capital unit of CRH, launched its Sustainable Building Materials accelerator. The program aims to identify innovative materials and applications to lower emissions, reduce waste and improve energy use—leveraging CRH's extensive network and expertise to drive forward innovative and sustainable solutions for the built environment. The accelerator focuses on sustainable binder solutions, new materials and applications, and CO2 mineralized materials.

The Eco Material Strategic Rationale

The Eco Material Technologies acquisition, which closed in September 2025, represents CRH's most significant sustainability-focused transaction. Supplementary cementitious materials (SCMs) like fly ash and slag can substitute for Portland cement in concrete mixes, dramatically reducing the carbon intensity of the final product while often improving performance characteristics.

By acquiring the leading SCM supplier in North America, CRH positions itself to meet growing customer demand for lower-carbon concrete solutions. As building codes and procurement standards increasingly mandate embodied carbon reductions, CRH's combined cement and SCM capabilities provide a competitive advantage that pure-play cement producers cannot match.

ESG Recognition

CRH was awarded the highest available rating of AAA in the MSCI ESG Ratings. The company has achieved this score for eleven consecutive years, an accomplishment that remains unmatched in its sector.

CRH was designated a constituent member of the Dow Jones Best-in-Class North America Index, comprising sustainability leaders selected by the S&P Global ESG Score.

XVIII. Risks and Challenges

Cyclical Exposure

Despite its geographic and product diversification, CRH remains fundamentally tied to construction activity cycles. A severe recession would reduce demand for aggregates, cement, and asphalt across all end markets simultaneously. The 2008-2009 financial crisis demonstrated how quickly construction volumes can collapse—US cement consumption dropped by over 40% from peak to trough. While CRH's financial discipline provides balance sheet resilience to weather downturns, its earnings would decline materially in a prolonged construction recession.

Geographic Concentration Risk

CRH's primary weakness and risk is its increasing reliance on the North American economic cycle.

With approximately 75% of EBITDA generated in North America, CRH's performance is heavily dependent on US and Canadian economic conditions. While this concentration has been beneficial during the current infrastructure spending cycle, it creates vulnerability to US-specific economic shocks.

Debt and Valuation Concerns

CRH presents a mixed investment outlook. However, investors should be cautious of the company's significant debt load.

The aggressive acquisition strategy requires ongoing capital deployment, and the balance sheet must support both continued M&A activity and potential economic downturns. Maintaining investment-grade credit ratings while funding growth requires careful calibration.

Political and Regulatory Risk

Infrastructure spending is inherently political. While the Infrastructure Investment and Jobs Act provides a multi-year funding runway, future administrations could redirect priorities, delay implementation, or alter procurement requirements. Environmental regulations affecting quarry operations, cement plant emissions, and construction practices could also impact CRH's operations and cost structure.

Integration Risk

While CRH has an exceptional track record of successful acquisitions, any acquisition-dependent strategy carries integration risk. The company's ability to maintain its decentralized operating model while achieving synergies depends on continued execution excellence. A single large failed acquisition could impair returns for years.

Competitive Dynamics

CRH operates in highly competitive regional building materials markets, competing against both large multinational companies and smaller regional players. In North America, the company's primary competitors include Vulcan Materials Company, Martin Marietta Materials, and Heidelberg Materials. These companies compete primarily in aggregates, cement, and ready-mixed concrete markets across overlapping geographic regions.

While competition has historically been rational, price wars in specific markets could pressure margins. Additionally, increased regulatory scrutiny of industry consolidation could limit future acquisition opportunities.

XIX. The Road Ahead

Near-Term Outlook

CRH enters 2026 from a position of strength. The company delivered record results in 2025, with EBITDA margins expanding and acquisitions contributing incremental growth. The infrastructure spending tailwinds from federal legislation remain in early innings, with project funding continuing to flow into state and municipal construction programs.

Management has demonstrated willingness to maintain aggressive acquisition activity, with 40 deals guided for fiscal year 2025 alone. The integration of Eco Material Technologies adds capabilities in the fastest-growing segment of the cementitious business, positioning CRH to capture demand for lower-carbon concrete solutions.

Medium-Term Strategic Priorities

Several strategic initiatives will shape CRH's trajectory over the coming years:

Continued North American Consolidation: The building materials industry remains highly fragmented, with substantial runway for additional bolt-on acquisitions. CRH's scale, reputation, and integration capabilities position it favorably to continue consolidating regional players.

Sustainability Leadership: Meeting and exceeding decarbonization commitments will become increasingly important as customers, regulators, and investors focus on embodied carbon in construction. CRH's investments in SCMs, alternative fuels, and breakthrough technologies position it to lead rather than follow this transition.

Operational Excellence: Continued margin expansion through best-practice sharing, productivity improvements, and pricing discipline will drive value creation even absent transformational acquisitions.

Capital Returns: With strong cash generation and modest leverage, CRH can continue returning capital to shareholders through dividends and buybacks while maintaining acquisition capacity.

Long-Term Vision

CRH's stated ambition is to be the world's leading building materials company. The path to that position runs through continued North American dominance, selective international growth in attractive markets, and leadership in sustainable construction materials.

The company's unique combination of scale, operational excellence, acquisition capability, and financial discipline creates a durable competitive position. While individual years will vary with economic cycles, the long-term compounding potential remains substantial.

XX. Final Analysis: Why CRH Matters

CRH's story offers several lessons that extend beyond the building materials industry:

Patience Compounds: The company's 55-year journey from Irish cement monopoly to global leader demonstrates the power of consistent execution over decades. There was no single transformational moment—rather, hundreds of disciplined decisions accumulating into an extraordinary outcome.

Capital Allocation Trumps Strategy: Many companies articulate compelling strategic visions but fail to execute. CRH's success derives less from strategic insight than from relentless execution of a proven playbook: buy well-positioned businesses at reasonable prices, retain management, extract synergies, and repeat.

Local Businesses Can Scale Globally: Building materials are inherently local—you cannot economically ship crushed stone across the ocean. Yet CRH built a global empire by applying consistent operational and financial discipline to fundamentally local businesses. The knowledge traveled even if the rocks could not.

Boring Can Be Beautiful: CRH sells rocks, cement, and asphalt. There is nothing exciting about the products themselves. Yet the combination of essential demand, local geographic advantages, and disciplined management created extraordinary shareholder returns. Sometimes the best investments hide in plain sight, too mundane for most investors to notice.

Timing Matters, But Not How You Think: CRH's success came not from perfect market timing but from consistency through cycles. By maintaining financial discipline during booms and continuing to acquire during busts, the company optimized long-term returns rather than short-term performance.

The quiet giant from Dublin has built much of the physical infrastructure of North America and Europe. Its products—the roads we drive on, the foundations our buildings rest upon, the utility infrastructure that powers modern life—are invisible precisely because they work. CRH's business may lack the glamour of technology or the excitement of consumer brands, but it provides something perhaps more valuable: the essential materials upon which everything else depends.

As infrastructure spending accelerates to address decades of underinvestment, as sustainability requirements reshape construction practices, and as consolidation continues in a fragmented industry, CRH stands positioned to extend its remarkable compounding record. The letters that once stood for "Cement Roadstone Holdings" now represent something far more significant: a masterclass in building enduring value, one quarry, one cement plant, and one acquisition at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube