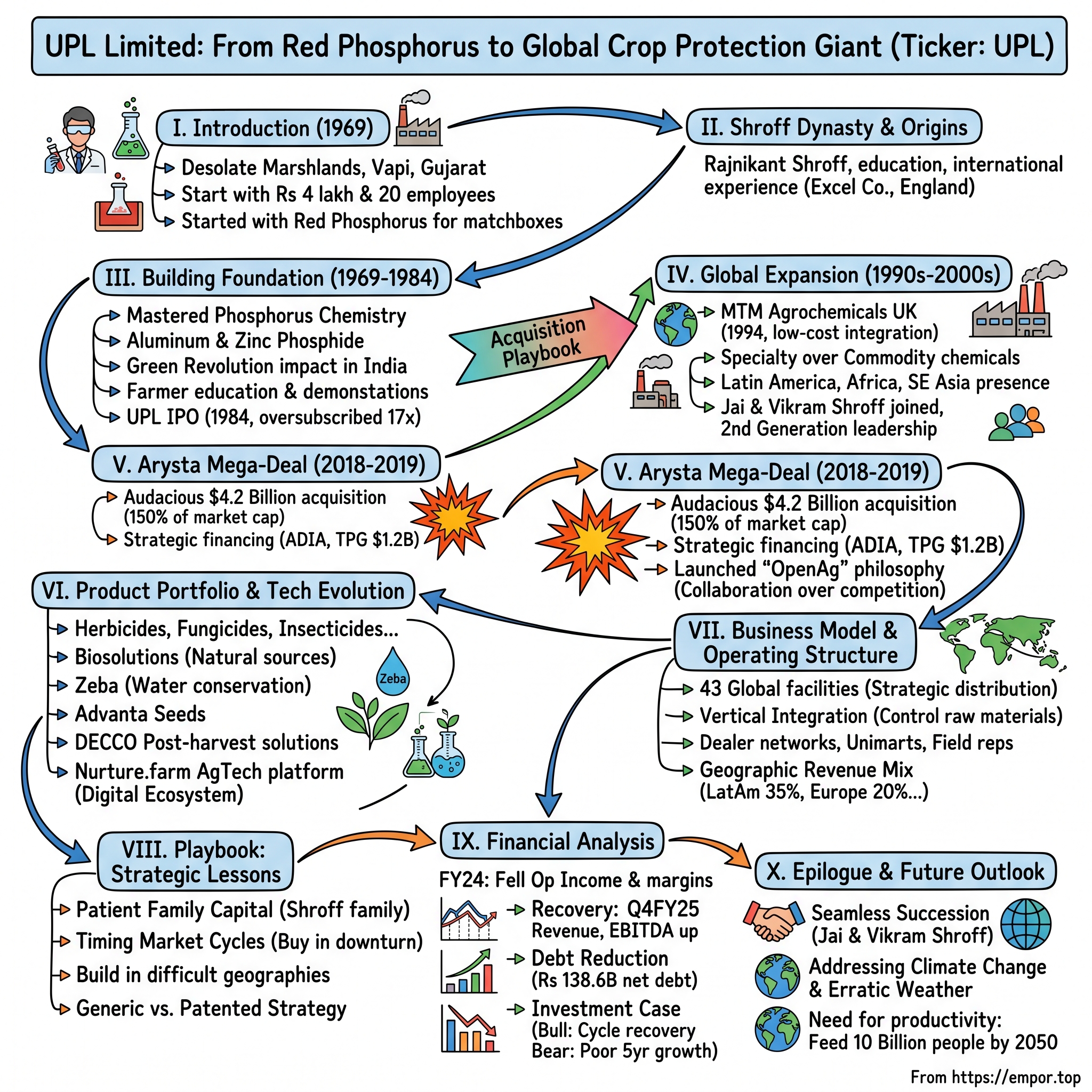

UPL Limited: From Red Phosphorus to Global Crop Protection Giant

I. Introduction & Episode Setup

Picture this: A young chemist in 1969, standing in the desolate marshlands of Vapi, Gujarat, where electricity is a luxury and the nearest paved road is hours away. The monsoon has turned the ground to mud. Industrial infrastructure? Non-existent. Yet Rajnikant Shroff sees something others don't—the future headquarters of what will become India's agricultural chemical empire.

Today, UPL Limited stands as the world's fifth-largest agrochemical company, with annual revenues exceeding $5 billion and operations spanning 140 countries. The company touches 90% of the world's food basket—a staggering reach for a business that started with just Rs 4 lakh and 20 employees manufacturing red phosphorus for matchboxes.

The transformation is almost incomprehensible. How does a small chemical factory in newly independent India, operating from industrial wastelands, evolve into a global agricultural powerhouse that would eventually execute one of the largest acquisitions in agrochemical history? How does a family business from Gujarat end up competing toe-to-toe with century-old German chemical giants and American agricultural conglomerates?

This is the story of three generations of the Shroff family, multiple strategic pivots, dozens of acquisitions, and one massive $4.2 billion bet that would reshape the global crop protection landscape. It's a playbook in patient capital deployment, emerging market arbitrage, and the power of being the underdog willing to build where others won't.

The journey takes us from the Green Revolution's early days through India's economic liberalization, from commodity chemicals to sophisticated biologicals, from family-run operations to professionally managed global enterprise. Along the way, we'll discover how UPL turned India's agricultural challenges into competitive advantages, why building in difficult geographies became their moat, and how they timed the market cycles to perfection—including their transformative Arysta LifeScience acquisition during the 2018 agricultural downturn.

II. The Shroff Dynasty & Origins

The Shroff family story begins not with chemicals, but with textiles and traditional remedies. Rajnikant Shroff, born in 1934 in a small village in Kutch, Gujarat, grew up in a business family that had been in textiles since before India's independence. When the Great Depression devastated global markets, his father Devidasbhai and uncle pivoted—they started manufacturing pain balm and hair oil, products that required basic chemical knowledge but served immediate local needs.

Young Rajnikant's education at Bombay University wasn't just academic—it was transformative. After graduation, he joined the R&D department of the family factory, which had expanded into manufacturing mercuric chloride. Here's where the story takes its first international turn: European demand for mercuric chloride was soaring in the 1950s. The Shroffs, sensing opportunity, did something audacious for an Indian family in 1956—they set up a factory in England.

Think about that timing. India had been independent for less than a decade. Indian businesses were still finding their feet domestically, yet here was a Gujarati family establishing manufacturing operations in their former colonial ruler's backyard. Rajnikant founded Excel Company in London, ran it successfully for two years, then sold it to a British rival—generating capital and, more importantly, learning how global chemical markets operated.

But the real genesis moment came in 1969. Rajnikant, now 35 and armed with international experience, saw an opportunity everyone else missed. Red phosphorus—the chemical that makes matchboxes strike—had no domestic manufacturer in India. Every matchbox company was importing this critical input. With Rs 4 lakh in capital (roughly $50,000 at 1969 exchange rates) and 20 employees, he founded United Phosphorus Limited in Vapi, Gujarat.

The choice of Vapi seems insane in retrospect. This wasn't Mumbai or Delhi with established infrastructure. Vapi in the late 1960s was essentially marshland. No reliable electricity. No water supply. The journey to Mumbai—India's commercial capital—took 6-7 hours on barely motorable roads. During monsoons, the entire area would flood. Yet Rajnikant saw what others didn't: Gujarat's new industrial estate policy offered land at throwaway prices, tax holidays, and the promise of future infrastructure. He was betting on India's industrial future before that future existed.

The early days were brutal. Employees would often sleep in the factory because commuting was impossible. Power cuts meant production happened in spurts. Quality control meant Rajnikant personally inspecting every batch. But within two years, UPL had captured the entire Indian red phosphorus market. Every matchbox manufacturer in India was now their customer. The monopoly was so complete that when competitors finally emerged years later, customers stayed with UPL out of loyalty to the company that had ended their import dependence.

III. Building the Foundation: Red Phosphorus to Agrochemicals (1969–1984)

The transition from red phosphorus to agrochemicals wasn't planned—it was discovered through chemistry and circumstance. By 1971, UPL had mastered phosphorus chemistry. The logical next step? Aluminum phosphide, a fumigant that protects stored grain from pests. Then came zinc phosphide, a rodenticide. Both products shared a common thread: they were phosphorus-based, leveraged UPL's existing expertise, and served India's agricultural sector.

The timing couldn't have been better. India's Green Revolution was transforming agriculture in the 1970s. Norman Borlaug's high-yielding wheat varieties were spreading across Punjab and Haryana. Farmers were adopting new practices, but agricultural inputs remained expensive and controlled by multinational corporations. A bag of imported pesticide could cost a farmer a month's income. Storage losses due to pests were destroying 20-30% of harvests.

Rajnikant Shroff saw the gap: Indian farmers needed affordable, effective crop protection products designed for Indian conditions. Not Swiss formulations for Alpine weather or American products for Midwest soil—but solutions for monsoon-fed agriculture, tropical pests, and price-sensitive farmers. UPL's aluminum phosphide tablets, priced at a fraction of imports, became the farmer's first line of defense against storage pests.

The 1970s became UPL's laboratory for understanding Indian agriculture. They didn't just sell chemicals; they educated farmers. UPL representatives would travel to villages, conducting demonstrations on proper fumigation techniques. They printed instruction manuals in local languages—Hindi, Gujarati, Punjabi, Tamil. This wasn't corporate social responsibility; it was market development. Every educated farmer became a lifetime customer.

By 1980, demand had outstripped the Vapi facility's capacity. UPL established a 1,000 MT facility in Ankleshwar, Gujarat, to produce yellow phosphorus—the raw material for their expanding product line. This backward integration move was classic Shroff strategy: control your inputs, control your margins. While competitors imported yellow phosphorus from China or Kazakhstan, UPL was self-sufficient.

The masterstroke came in 1984: UPL went public on Indian stock exchanges. The IPO was oversubscribed 17 times. For context, this was still License Raj India—private enterprise was viewed with suspicion, stock markets were nascent, and most Indians kept savings in gold or fixed deposits. Yet UPL's IPO captured imagination because it told a story Indians wanted to believe: a domestic company could compete globally.

The capital raised—approximately Rs 5 crore—seems quaint now, but it transformed UPL's trajectory. They could now fund R&D, expand production, and most importantly, start looking beyond India's borders. The foundation was set for what would become one of India's most aggressive international expansion stories.

IV. Global Expansion & The Acquisition Playbook (1990s–2000s)

The 1990s began with India's economic liberalization, but UPL was already thinking globally. Their first major international move came in 1994 with the acquisition of MTM Agrochemicals in the UK—a struggling herbicides manufacturer with good products but poor management. The price? Just £2 million. Within three years, UPL had turned MTM profitable by combining its formulations with UPL's low-cost manufacturing base in India.

This established the UPL acquisition playbook that would be repeated dozens of times: find distressed or non-core chemical assets in developed markets, acquire them cheaply, integrate their technology with Indian manufacturing, and use their registrations and distribution networks to enter new geographies. It was arbitrage at its finest—Western technology meets Eastern efficiency.

The 1980s had seen UPL launch an "avalanche" of crop protection products (as company documents dramatically describe it). By the 1990s, they were moving from commodity chemicals to specialty crop protection. The difference? Commodity chemicals compete on price; specialty products compete on efficacy. A farmer will pay premium for a fungicide that saves his cotton crop, but red phosphorus is red phosphorus.

The international expansion accelerated through the 2000s. UPL acquired businesses in South Africa, Brazil, Argentina, Mexico. Each acquisition brought three things: local product registrations (which could take years and millions to obtain organically), distribution networks, and customer relationships. In Brazil, for instance, UPL bought a small local player for $15 million in 2004. That acquisition gave them access to Brazilian soybean farmers—who would become the world's largest soybean exporters within a decade.

Here's where the next generation enters the story. Jai Shroff, Rajnikant's elder son, joined in 1991 after studying in the US. Vikram, the younger son, joined in 1995. The brothers brought complementary skills—Jai focused on strategy and finance, Vikram on operations and technology. But more importantly, they brought ambition to transform UPL from an Indian company with international operations to a truly global entity.

October 2013 marked a symbolic shift: the company changed its name from United Phosphorus Limited to UPL Limited. The phosphorus that had defined their origin was now just one element in a vast portfolio. They were signaling to markets, employees, and themselves—we're not just a phosphorus company anymore.

By 2015, UPL had built distribution networks across 130 countries. But here's the remarkable part: 60% of revenues came from emerging markets—Latin America, Africa, Southeast Asia. While competitors focused on high-margin developed markets, UPL was building positions in tomorrow's agricultural powerhouses. They understood something fundamental: the future of agriculture wasn't in Iowa or France, but in Mato Grosso and Punjab, in Nigerian cassava fields and Vietnamese rice paddies.

V. The Arysta LifeScience Mega-Deal (2018-2019)

July 2018. The agricultural chemicals industry was in turmoil. Bayer was digesting its $63 billion Monsanto acquisition. DowDuPont was splitting apart. ChemChina had just swallowed Syngenta for $43 billion. In this chaos of mega-mergers, UPL—ranked ninth globally with $2.7 billion in revenues—seemed destined to remain a regional player, forever looking up at the giants.

Then came the call that changed everything.

Platform Specialty Products, a roll-up vehicle run by serial acquirer Martin Franklin, needed to sell Arysta LifeScience to focus on its performance chemicals business. Arysta wasn't just any asset—it was a $1.5 billion revenue business with premium positioning in specialty crops, biologicals, and seed treatment. For UPL, acquiring Arysta for approximately US$4.2 billion in cash wasn't just ambitious—it was audacious. The acquisition price was 150% of UPL's entire market capitalization.

But Jai Shroff saw what others missed. The acquisition would be transformational, with Arysta's differentiated position in specialty applications and tailored local solutions aligning with UPL's vision of becoming a premier global provider of agricultural solutions. The complementarity was almost too perfect: UPL was strong in Asia and Latin America; Arysta dominated North America and Japan. UPL focused on broad-acre crops; Arysta specialized in fruits and vegetables. UPL had manufacturing muscle; Arysta had innovation and registrations.

The financing structure revealed sophisticated financial engineering. ADIA and TPG agreed to invest $600 million each in UPL Corporation Limited, supporting the $4.2 billion acquisition and creating a global market leader with proforma revenues of over $4 billion and pre-tax earnings of over $1 billion. This wasn't just debt financing—it was strategic capital from two of the world's most sophisticated investors betting on UPL's integration capabilities.

The transaction completion in February 2019, signed in July 2018, marked a major step in UPL's history. But here's what made this deal special: timing. Agricultural commodity prices were depressed. Trade wars were disrupting global supply chains. Most companies were retrenching. UPL was buying—at exactly the right moment.

The integration happened during COVID-19, perhaps the most challenging environment imaginable for combining two global organizations. Yet UPL didn't just integrate Arysta—they reimagined their entire corporate philosophy. They launched 'OpenAg', standing for open minded partnerships and creating win-win partnerships to transform agriculture by creating an open agriculture network. This wasn't corporate speak—it was a fundamental shift from competition to collaboration.

The new UPL became one of the top 5 agricultural solutions companies worldwide, with revenue of approximately $5 billion, footprint in 76 countries and sales in 130+ countries, representing a compelling value proposition in a consolidating market. The transformation was complete: a matchbox chemical manufacturer from Gujarat had become a global agricultural powerhouse.

VI. Product Portfolio & Technology Evolution

Walk into a UPL research facility today and you'll find scientists working on everything from RNA interference to drone-based application systems. The product portfolio that started with red phosphorus now spans the entire agricultural value chain—herbicides, fungicides, insecticides, acaricides, seed treatment products, adjuvants, biosolutions, public health products, fumigants, and post-harvest solutions. It's a staggering breadth that took five decades to build.

The numbers tell part of the story: more than 13,600 product registrations globally. Each registration represents years of trials, millions in investment, and regulatory navigation across different countries. But what's more interesting is the portfolio composition. While competitors chase the next blockbuster molecule, UPL has built a portfolio of hundreds of smaller products, each solving specific problems for specific crops in specific geographies. It's death by a thousand cuts rather than a single knockout punch.

Take biosolutions—products derived from natural sources like bacteria, fungi, or plant extracts. Five years ago, this was a curiosity category for UPL. Today, following the Arysta acquisition, they have one of the industry's most comprehensive biological portfolios. These aren't just "green" alternatives; they're often more effective than chemicals for certain applications. A bacterial strain that colonizes plant roots and fights fungal infections. A protein that triggers the plant's own defense mechanisms. Natural predators that control pests without chemicals.

The innovation extends beyond traditional crop protection. Zeba, their water conservation product, is essentially a starch-based polymer that acts like a sponge in soil, absorbing water during irrigation and releasing it slowly during dry periods. In water-stressed regions from California to Karnataka, it can reduce irrigation needs by 25%. Advanta Seeds, their seed division, isn't trying to compete with Monsanto's GMO corn—instead, they're developing climate-adapted varieties for crops like sorghum and sunflower that multinationals ignore.

DECCO, their post-harvest business acquired with Arysta, solves a problem most consumers never think about: how do you keep fruit fresh during the months it takes to travel from a Chilean orchard to a Shanghai supermarket? Their coatings and treatments extend shelf life, reduce spoilage, and maintain quality—turning logistics from a race against time to a manageable process.

But the real revolution is happening in digital agriculture. Nurture.farm, UPL's AgTech platform, has transformed from a simple app to a comprehensive ecosystem. Farmers can book mechanized spraying services (think Uber for tractors), access satellite-based crop monitoring, get AI-powered advisory services, and even purchase inputs—all through their smartphones. With approximately 3 million registered farmers and over 85,000 retailers on the platform, it's becoming the operating system for Indian agriculture.

The platform solves real problems. A farmer in Bihar can't afford a $50,000 tractor, but he can pay $20 to have his field sprayed by a drone. A retailer in Tamil Nadu doesn't know which pesticide to recommend for a new pest—the app's image recognition and expert system provides instant guidance. The data generated—crop patterns, pest outbreaks, weather impacts—gives UPL unprecedented market intelligence.

This technology evolution represents a fundamental shift in UPL's business model. They're no longer just selling products; they're providing solutions. The farmer doesn't buy insecticide; he buys protection from bollworm. The food processor doesn't buy post-harvest treatment; she buys extended shelf life. The transformation from chemical manufacturer to agricultural solution provider is complete.

VII. Business Model & Operating Structure

Understanding UPL's business model requires thinking in three dimensions: products, geographies, and channels. The company operates through three main segments—Crop Protection (85% of revenues), Seeds Business (8%), and Non-Agro (7%)—but this segmentation understates the complexity of their go-to-market strategy.

Start with manufacturing—43 facilities spread across the globe. But unlike competitors who concentrate production in low-cost countries, UPL's facilities are strategically distributed. A plant in Brazil doesn't just serve Brazil; it's the hub for all of Latin America. The facility in South Africa covers sub-Saharan Africa. This isn't just about cost—it's about regulatory compliance, supply chain resilience, and customer proximity. When Brazil suddenly bans imports of a particular formulation, UPL can reformulate locally while competitors wait months for new import permits.

The distribution network is where UPL's emerging market heritage becomes a competitive advantage. In India alone, they have 25,000 dealer relationships and 600 experience centers (Unimarts) where farmers can see product demonstrations, get soil testing, and receive agronomic advice. The workforce of over 5,000 field representatives doesn't just sell—they educate, demonstrate, and build relationships that span generations.

Consider the complexity: a field representative in Maharashtra needs to understand cotton cultivation, local pest pressures, soil conditions, weather patterns, government subsidy programs, and the financial situation of hundreds of small farmers. They need to speak Marathi, understand local customs, and be trusted enough that a farmer will follow their advice on products that could determine whether his family eats this year. This isn't a job—it's a calling.

The backward integration strategy deserves special attention. While competitors rely on Chinese suppliers for active ingredients, UPL manufactures many of their own intermediates. When COVID-19 disrupted global supply chains and active ingredient prices spiked 300%, UPL's margins actually expanded because they controlled their raw materials. This vertical integration extends from basic chemicals to formulated products to application services—capturing value at every step.

Geographic revenue mix tells another story. Unlike Western competitors who generate 60-70% of revenues from North America and Europe, UPL's revenue is distributed: Latin America (35%), Europe (20%), India (15%), North America (15%), Rest of Asia (10%), Africa & Middle East (5%). This isn't random—it's a deliberate strategy to be present in high-growth markets before they become attractive to giants.

Each geography requires different approaches. In Brazil, UPL sells directly to large soybean farms that span thousands of hectares. In India, they reach smallholder farmers through village-level entrepreneurs. In the US, they partner with distributors who serve specialized crops like almonds and grapes. In Africa, they work with NGOs and government programs to reach subsistence farmers. One company, multiple business models, adapted to local realities.

The capital allocation within this structure is particularly clever. High-margin specialty products fund expansion in emerging markets. Generic products provide volume and cash flow. The seed business offers recurring revenue. Post-harvest solutions lock in food processors as long-term customers. Digital platforms create network effects and switching costs. Each business reinforces the others, creating a flywheel effect.

But the real innovation is the "asset-light" expansion in developed markets. Rather than building expensive manufacturing in the US or Europe, UPL partners with local formulators, provides the active ingredient, and shares the margin. They get market access without capital investment. The partner gets products without R&D risk. It's the kind of win-win that only works when you're not trying to dominate but rather to participate profitably.

VIII. Playbook: Strategic & Investing Lessons

The UPL story offers a masterclass in strategic thinking for emerging market companies with global ambitions. Let's decode the playbook that transformed a Vapi chemical factory into a global agricultural giant.

Patient Family Capital: The Shroff family still controls UPL, holding approximately 28% equity. This isn't about wealth preservation—it's about time horizon. When you're building for grandchildren rather than quarterly earnings, you make different decisions. The Arysta acquisition diluted family ownership but expanded the empire. A public company CEO might have balked; the Shroffs saw it as planting trees they'd never sit under.

Timing Market Cycles: Every major UPL acquisition happened during a downturn. MTM Agrochemicals in 1994—during the European recession. Brazilian acquisitions in 2002-2004—during the Argentine crisis spillover. Arysta in 2018—during the agricultural commodity collapse. This isn't luck; it's discipline. As Jai Shroff once noted, "When others are selling, we're buying. When others are buying, we're integrating."

Building in Difficult Geographies: Starting in Vapi's industrial wasteland wasn't a handicap—it was an advantage. If you can manufacture chemicals profitably where there's no infrastructure, you can manufacture anywhere. If you can distribute to Indian farmers with 2-hectare plots, Brazilian fazendas are easy. If you can navigate India's bureaucracy, other regulatory regimes seem simple. Difficulty breeds capability.

The Conglomerate Arbitrage: UPL leverages group synergies in ways that focused competitors can't. Their industrial chemicals business provides raw materials to crop protection. The Indian distribution network sells both pesticides and seeds. The same regulatory team handles registrations across divisions. Manufacturing facilities produce multiple products. This operational leverage means UPL's cost base is structurally lower than specialized competitors.

Generic vs. Patented Strategy: While Bayer spends billions developing new molecules, UPL focuses on off-patent products with clever formulations. A generic active ingredient combined with proprietary adjuvants can be 80% as effective as a patented product at 30% of the price. For emerging market farmers, that math works. UPL isn't trying to win Nobel Prizes; they're trying to protect crops affordably.

Distribution as Moat: In emerging markets, distribution is everything. You can copy a chemical formula, but you can't replicate 25,000 dealer relationships built over decades. You can't suddenly create trust with millions of smallholder farmers. You can't instantly understand the agronomic needs of 140 countries. UPL's distribution network isn't just a channel—it's an almost impregnable competitive moat.

The "OpenAg" Philosophy: Rather than vertical integration and exclusivity (the traditional agrochemical model), UPL embraces partnership. They'll formulate products for competitors. They'll share distribution with rivals. They'll open their digital platform to third parties. This isn't altruism—it's network effects. The more participants in your ecosystem, the more valuable the ecosystem becomes.

The investment lessons are equally powerful. First, boring businesses in essential industries can create extraordinary wealth—red phosphorus isn't sexy, but food production is eternal. Second, regulatory complexity is a feature, not a bug—those 13,600 product registrations are a barrier competitors can't quickly overcome. Third, emerging market leaders who go global have structural advantages their developed market peers can't replicate.

IX. Financial Analysis & Investment Case

The numbers tell a story of transformation and challenge. UPL's current market capitalization stands at Rs 51,439 crore, reflecting the market's assessment of a company navigating through one of the most difficult periods in agrochemical history. Let's dissect the financial reality behind the global expansion narrative.

Operating income during FY24 fell 19.6% year-on-year, with operating profit decreasing by 60.3%. Operating profit margins contracted dramatically from 19.0% in FY23 to 9.4% in FY24. These aren't just numbers—they represent the brutal reality of the post-COVID agricultural chemical market: inventory destocking, price deflation, and margin compression hitting simultaneously.

Yet the most recent results show remarkable recovery. Revenue increased to Rs 155.7 billion in Q4FY25, compared to Rs 140.8 billion in Q4FY24, led by 11% volume growth. EBITDA grew 68% to Rs 32.4 billion with margins improving by 710 basis points to 20.8%. The turnaround is real—volumes are recovering, margins are expanding, and the worst appears behind them.

The debt story deserves special attention. The Arysta acquisition loaded UPL with significant leverage—net debt peaked at over Rs 220 billion. But here's what's impressive: they reduced net debt by Rs 83.2 billion to Rs 138.6 billion, driven by strong operating free cash flow of Rs 44.5 billion and proceeds from capital transactions. This isn't financial engineering—it's disciplined capital management during crisis.

However, challenges remain: the company has delivered poor sales growth of 5.46% over the past five years and maintains a low interest coverage ratio. For investors, this presents the classic value question: is this a cyclical trough or structural decline?

The Bull Case: UPL is emerging from the worst agricultural chemical downturn in decades with intact market positions, reduced debt, and improving margins. The differentiated and sustainable portfolio is gaining share—rising approximately 700 basis points year-on-year to 35% of crop protection revenue in FY24. Geographic diversification provides resilience. The Arysta integration is complete, synergies are flowing, and the combined entity has critical scale in a consolidating industry.

The Bear Case: The 5-year growth trajectory is concerning. Commodity chemical exposure remains high despite portfolio shifts. Climate volatility and regulatory pressures on chemical usage are structural headwinds. Competition from Chinese generics continues to intensify. The debt burden, while reduced, still constrains flexibility. Return on equity remains depressed at 4.27% over the last three years.

Comparative Valuation: Trading at a P/E of -17.3x (due to recent losses) and P/B of 1.6x, UPL appears cheap relative to global peers. Corteva trades at 25x P/E, FMC at 18x, even generic-focused companies like ADAMA trade at higher multiples. Either the market is missing the recovery story, or it's pricing in continued challenges.

The investment case ultimately hinges on cycle timing. If agricultural markets have indeed bottomed and UPL's operational improvements are sustainable, current valuations offer compelling entry. If structural challenges in agrochemicals persist, the recovery could prove temporary. The company's guidance suggests confidence: management enters FY26 with "a sharper business model, stronger margins, and renewed momentum to capture emerging opportunities".

X. Epilogue & Future Outlook

The conference room at UPL's Mumbai headquarters has a wall of photographs—Rajnikant Shroff with farmers in Punjab fields, the original Vapi factory, the ribbon-cutting at international acquisitions. At 90, Rajnikant still comes to office, though he's passed operational control to his sons. In 2021, the Indian government awarded him the Padma Bhushan, one of the nation's highest civilian honors, recognizing not just business success but contribution to Indian agriculture.

The succession has been seamless—perhaps because it was planned over decades, not years. Jai Shroff serves as Chairman and Global CEO, bringing strategic vision and financial acumen. Vikram Shroff, as Executive Director, focuses on operations and technology. Unlike many family businesses that fracture in transition, the Shroff brothers have clearly delineated roles and mutual respect. The third generation is already in the business, learning the ropes in field offices and R&D labs.

But the future of UPL—and agricultural chemicals broadly—faces fundamental questions. Climate change isn't a distant threat; it's current reality. Erratic monsoons, unprecedented pest outbreaks, soil degradation—these aren't risks anymore, they're certainties. The industry that helped feed the world through chemistry must now reinvent itself for a world demanding sustainability.

UPL's response has been to embrace biological solutions and digital agriculture, but the transformation is harder than it appears. Biologicals require different development processes, regulatory pathways, and farmer education. Digital platforms need continuous investment with uncertain monetization. The company that built its fortune on phosphorus chemistry must now compete with Silicon Valley AgTech startups and biotech giants.

Competition is evolving too. Chinese generic manufacturers aren't just copycats anymore—they're innovating, backed by government support and massive scale. At the other end, companies like Bayer and Corteva are using AI and gene editing to develop next-generation solutions. UPL must navigate between commoditization from below and innovation from above.

Yet there's reason for optimism. The fundamental driver of UPL's business—the need to feed a growing population with shrinking arable land—remains intact. By 2050, agricultural productivity must increase by 70% to feed 10 billion people. This can't happen without crop protection, whether chemical, biological, or digital. UPL's presence across the agricultural value chain, from seeds to post-harvest, positions them to capture this growth.

The next chapter will be written by how well UPL executes its transformation from chemical manufacturer to agricultural solution provider. Can they maintain cost leadership while moving up the innovation curve? Can they leverage their emerging market distribution to introduce new technologies? Can they balance the needs of smallholder farmers with demands of industrial agriculture?

Perhaps most critically: can they maintain the entrepreneurial spirit that built the company while operating at global scale? The Vapi marshlands where Rajnikant Shroff started with 20 employees now hosts one of many UPL facilities worldwide. The company that began by making matchboxes strike now helps feed 90% of the world's population.

The story of UPL is ultimately the story of Indian entrepreneurship—starting with disadvantages, building through difficulties, and emerging as global competitors. It's a reminder that competitive advantage doesn't always come from superior resources or technology, but from willingness to build where others won't, serve customers others ignore, and persist when others retreat.

As global agriculture faces its greatest challenges—climate change, resource scarcity, population growth—companies like UPL become more important, not less. They bridge the gap between agricultural innovation and farmer adoption, between global technology and local application, between feeding the world and preserving it for future generations.

The journey from red phosphorus to global agriculture isn't complete. In many ways, it's just beginning.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube