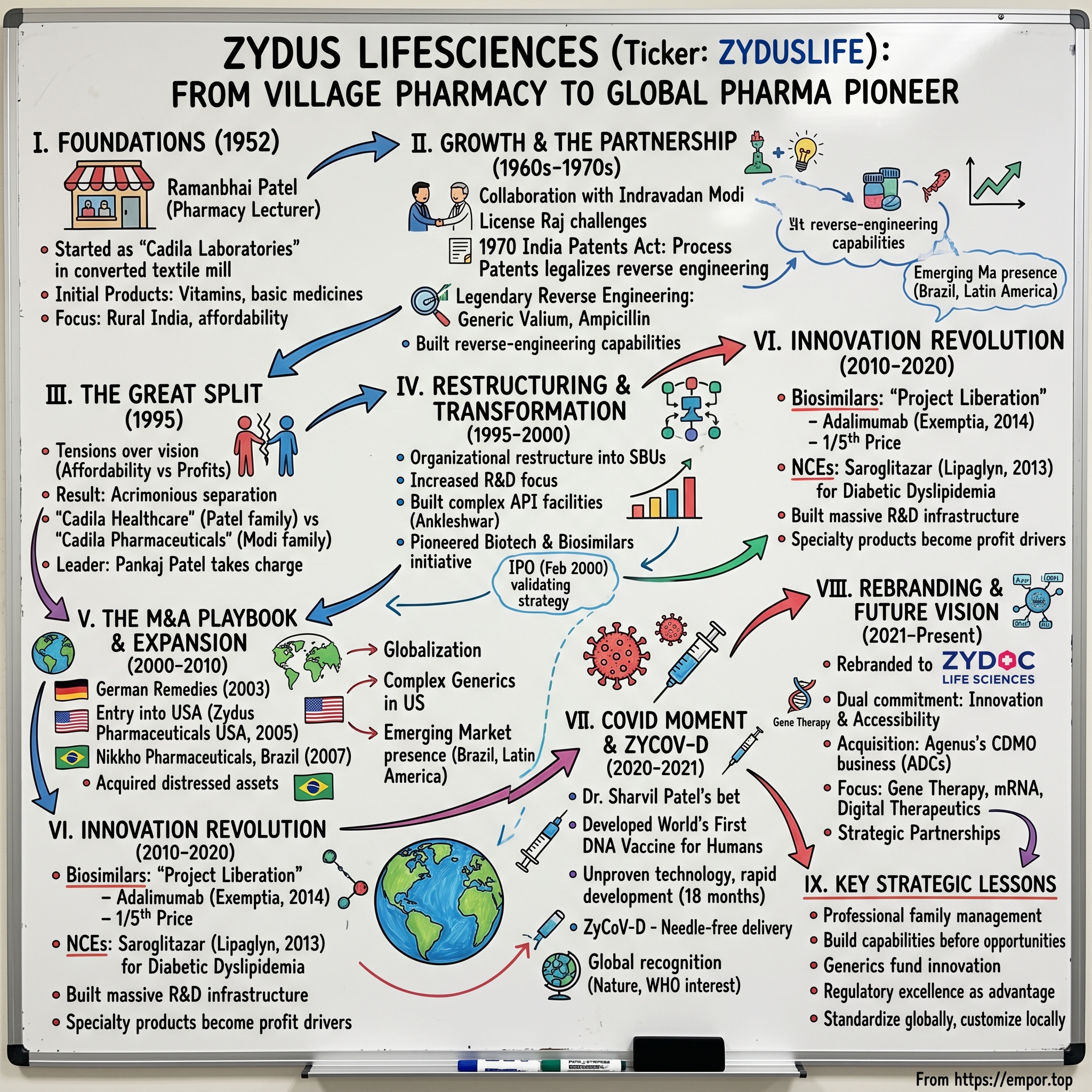

ZYDUSLIFE: From Village Pharmacy to Global Pharma Pioneer

I. Cold Open & Story Setup

The monsoon rains had just begun to fall on Ahmedabad when Dr. Sharvil Patel stood before a room of skeptical scientists on a humid morning in February 2020. Outside, the world was beginning to grasp the gravity of a novel coronavirus spreading from Wuhan. Inside Zydus's Vaccine Technology Centre, Patel—the third generation of a pharmaceutical dynasty—was proposing something audacious: India would develop the world's first DNA vaccine.

"We can do this in eighteen months," he said, knowing full well that traditional vaccine development took a decade. The room fell silent. Even for a company that had built its reputation on bold bets, this seemed impossible. No DNA vaccine had ever been approved for human use anywhere in the world. The technology was theoretical, promising but unproven. Yet eighteen months later, almost to the day, ZyCoV-D would receive emergency authorization, marking not just a triumph over COVID-19 but a defining moment in the transformation of Indian pharmaceutical innovation.

How did a company that began in 1952 as a modest operation founded by a pharmacy lecturer's son become the force that would deliver this breakthrough? The answer lies not in a single moment of genius but in seven decades of calculated risks, family drama worthy of a soap opera, and an almost obsessive belief that Indian science could compete with—and beat—the West at its own game.

This is the story of Zydus Lifesciences, India's fourth-largest pharmaceutical company, though calling it merely "fourth-largest" understates its significance. While competitors focused on copying Western drugs, Zydus built a dual engine: a cash-generating generics business that funded moonshot innovations. While others expanded cautiously, Zydus acquired aggressively, swallowing companies from Germany to Brazil. And while the global pharmaceutical establishment dismissed Indian companies as mere copycats, Zydus quietly assembled 1,400 researchers across nineteen sites, creating what would become one of the developing world's most ambitious R&D operations.

The company's journey mirrors India's own pharmaceutical evolution—from import dependence to self-sufficiency, from reverse engineering to original research, from serving local markets to competing globally. But unlike the neat narrative of national progress, Zydus's story is messier, more human, filled with partnership breakups, regulatory battles, and bets that nearly broke the company.

Today, Zydus generates over ₹15,000 crores in annual revenue, maintains thirty manufacturing plants across three continents, and holds the distinction of creating both India's first novel chemical entity to reach market and the world's first DNA vaccine. Yet these achievements only hint at the deeper transformation: how a family business from Gujarat became a case study in balancing tradition with innovation, emerging market constraints with global ambitions, and affordable healthcare with sustainable profits.

What makes this story particularly relevant now is not just the COVID breakthrough, though that certainly captured headlines. It's that Zydus represents a new model for pharmaceutical companies from the developing world—one that doesn't choose between serving local needs and global innovation but insists on doing both. As we'll see, this wasn't always the plan. Like many great business stories, it emerged from necessity, ambition, and more than a few moments when everything could have fallen apart.

II. Origins: The Ramanbhai Patel Story & Foundation (1952-1995)

Ramanbhai Patel didn't set out to build a pharmaceutical empire. In 1952, as a thirty-year-old pharmacy lecturer at L.M. College in Ahmedabad, his ambitions were modest: perhaps run a small manufacturing unit, maybe supply medicines to local chemists. India had been independent for just five years, and the pharmaceutical landscape was a colonial hangover—foreign multinationals controlled 90% of the market, importing everything from aspirin to antibiotics at prices that put them beyond reach of ordinary Indians.

The timing of Patel's entry was both terrible and perfect. Terrible because India's License Raj had just begun to tighten its grip, requiring permits for everything from importing raw materials to expanding production capacity. Perfect because Prime Minister Nehru's government, recognizing the strategic importance of pharmaceutical self-sufficiency, had begun offering incentives for domestic production. Patel saw an opening that few others recognized: while multinationals focused on urban markets and premium products, vast swaths of rural India remained medically underserved.

His initial capital came from personal savings and a loan against his father's agricultural land—a detail that would later become part of company lore, the pharmacist's son who bet the family farm on pharmaceuticals. But Patel knew he needed more than money. He needed someone who understood business, someone who could navigate the byzantine world of government permits and supplier negotiations while he focused on the technical side.

That someone was Indravadan Modi, a shrewd businessman who had made his initial fortune in textiles before looking for new opportunities. Their partnership, formalized with a handshake in 1952, created Cadila Laboratories. The name itself was carefully chosen—derived from "Cadi," referencing the Kadva Patidar community both men belonged to, and "la," simply because it sounded modern and Western. In an era when Indian products were considered inferior, even the name needed to inspire confidence.

Their first facility was a converted textile mill in Bochasan village, about 50 kilometers from Ahmedabad. The equipment was secondhand, purchased from a defunct British-owned pharmaceutical plant. The initial product line was deliberately unglamorous: basic vitamins, simple analgesics, and anti-infectives that could be produced without sophisticated technology. But Patel had noticed something crucial—these basic medicines had enormous demand in rural areas where doctors prescribed them daily, yet supplies were erratic and expensive.

The early years were marked by what Patel would later call "jugaad innovation"—the distinctly Indian art of making do with less. When imported active pharmaceutical ingredients became too expensive, they figured out how to synthesize them locally. When the government restricted foreign exchange for importing equipment, they reverse-engineered machines using local engineering workshops. This wasn't cutting-edge science; it was survival through ingenuity.

By 1958, Cadila had grown enough to move operations to Ahmedabad proper, setting up a larger facility in the Satellite area. The timing coincided with a crucial shift in Indian pharmaceutical policy. The government, frustrated with multinational companies' high prices and limited technology transfer, began actively supporting domestic manufacturers. Cadila was perfectly positioned to benefit, having spent six years building capabilities that others were just beginning to develop.

The 1960s brought rapid expansion but also the first signs of strain in the Modi-Patel partnership. As the business grew, their visions began to diverge. Modi wanted to maximize profits through focus on high-margin products for urban markets. Patel remained committed to affordable medicines for the masses, even if margins were thinner. These philosophical differences were papered over by growth—revenues were doubling every few years, and there was enough success for both visions to coexist.

The 1970 Indian Patents Act proved to be a watershed moment, not just for Cadila but for Indian pharma as a whole. The act recognized only process patents, not product patents, effectively legalizing the reverse engineering of any drug as long as the manufacturing process was different. While Western pharmaceutical companies howled in protest, Patel saw it as divine providence. Suddenly, Cadila could legally manufacture versions of expensive Western drugs at a fraction of the cost.

The company's reverse-engineering capabilities became legendary within Indian pharmaceutical circles. When Roche's Valium became a global blockbuster, Cadila had a generic version ready within months. When antibiotics like ampicillin commanded premium prices, Cadila figured out alternative synthesis routes that cut costs by 80%. This wasn't mere copying—it required serious chemistry skills to develop new processes that were both economically viable and could pass quality standards.

By the 1980s, Cadila had become one of India's largest pharmaceutical companies, but success brought its own complications. The Modi and Patel families, now in their second generation, had different ideas about the future. The Modi faction wanted to diversify into other industries, seeing pharmaceuticals as just one vertical in a larger conglomerate. The Patel faction, led by Ramanbhai's son Pankaj who had joined the business in 1976 after completing his pharmacy degree, wanted to double down on pharmaceuticals and begin investing in research.

The tensions came to a head in 1994 when disagreements over a proposed acquisition turned into open conflict. Board meetings became battlegrounds, with each family marshaling their allies and proxies. Employees were forced to choose sides, suppliers were caught in the crossfire, and for several months, it seemed the company might implode entirely. The business press had a field day covering what they called "the great Cadila split," though neither family would speak publicly about the details.

The resolution, finalized in 1995, was both a divorce and a rebirth. The Modi family would keep the Cadila name and certain assets, creating what would become Cadila Pharmaceuticals. The Patel family would retain the bulk of the operations but needed a new identity, choosing to operate under the Zydus group banner with the pharmaceutical business restructured as Cadila Healthcare. The split was acrimonious enough that for years afterward, the two companies would compete fiercely in the same therapeutic areas, each trying to prove they were the "real" inheritor of the Cadila legacy.

What emerged from this corporate divorce was a leaner, more focused entity under Pankaj Patel's leadership. The younger Patel had spent nearly two decades in the business, working his way through manufacturing, quality control, and marketing. He had watched his father build through frugality and focus on affordability. But Pankaj had also spent time studying successful global pharmaceutical companies and understood that the future lay not just in reverse engineering but in original research. The split, painful as it was, freed him to pursue a vision his father had planted but never fully realized: transforming an Indian generics company into a global pharmaceutical innovator.

III. The Restructuring & Transformation Era (1995-2000)

Pankaj Patel stood in the empty boardroom of the newly christened Cadila Healthcare on a sweltering April morning in 1995, staring at an organizational chart that looked more like a battlefield map than a corporate structure. The split with the Modi family had left him with ₹250 crores in revenue, a collection of manufacturing facilities, and a workforce demoralized by months of corporate civil war. Half the senior management had departed with the Modis, taking crucial relationships and institutional knowledge. Banks were nervous, suppliers demanded cash upfront, and competitors circled like vultures, poaching talent and customers.

"We have six months to prove we're not just the losing half of a broken company," Patel told his remaining leadership team. His approach was counterintuitive for a company in crisis: instead of retrenching, he would expand. Instead of cutting R&D, he would double it. Instead of focusing solely on the domestic market, he would prepare for globalization. It was either visionary or delusional, and for the first year, even Patel wasn't sure which.

The first challenge was organizational. The split had created a leadership vacuum that Patel filled with an unusual mix of internal promotions and external hires. He elevated young managers who had proven loyal during the split, giving thirty-somethings responsibilities typically reserved for industry veterans. From outside, he recruited scientists from government laboratories and managers from multinational pharmaceutical companies, offering them something rarely found in Indian companies at the time: genuine autonomy and resources for innovation.

Dr. Mukul Jain, recruited from Ranbaxy to head R&D, recalled his first meeting with Patel: "He didn't talk about margins or market share. He asked, 'What would it take to develop a new molecule in India?' When I gave him a number that was probably twice what he expected, he simply said, 'Let's start with half that and prove the model.'" This interaction would define the Patel approach—ambitious but pragmatic, willing to invest but demanding proof of concept.

The restructuring went beyond personnel. Patel reimagined the entire business architecture, organizing it into focused strategic business units (SBUs) rather than functional silos. Each SBU—formulations, active pharmaceutical ingredients (APIs), biotechnology—operated with profit-and-loss responsibility, fostering entrepreneurship within the larger corporate structure. This was radical for an Indian family business, where centralized control was gospel.

The formulations SBU, the company's traditional cash cow, received immediate attention but not in the way anyone expected. Rather than simply producing more of the same generic drugs, Patel pushed for sophisticated delivery systems—sustained-release formulations, combination therapies, and novel dosage forms that could command premium pricing even in the generics market. The team developed a once-daily formulation of metformin when competitors were selling twice-daily versions, a seemingly small innovation that captured significant market share from established players.

The API division represented a bigger gamble. Most Indian companies were content to import Chinese APIs and focus on formulation. Patel saw this as a strategic vulnerability. He authorized construction of a new API facility in Ankleshwar, designed not just for current needs but for complex molecules the company didn't yet know how to make. The board was skeptical—the investment was enormous for a company still finding its feet. But Patel understood something others missed: as global pharmaceutical companies faced pressure to reduce costs, they would eventually need reliable API suppliers who could meet stringent quality standards. Being ready before that wave hit would provide first-mover advantages.

The biotechnology initiative was where Patel's vision diverged most dramatically from industry orthodoxy. In 1997, biotechnology in India meant brewing beer and making vaccines in government institutes. The idea that a private Indian company could develop biosimilars—complex biological drugs that were similar to branded biologics—seemed fantastical. Yet Patel allocated precious capital to establish Zydus Research Centre, recruiting Dr. Kiran Mazumdar-Shaw as an advisor (before she became famous with Biocon) and sending teams to Europe to learn fermentation technologies.

The transformation wasn't just internal. Patel understood that credibility required external validation. In 1998, Cadila Healthcare became one of the first Indian companies to invite international quality auditors to inspect facilities not because regulations required it, but because Patel wanted proof that Indian manufacturing could meet global standards. When the auditors' report came back with minimal observations—remarkably clean for a first audit—Patel framed it and hung it in the reception area. "Quality isn't a department," he would tell visitors, "it's a religion."

The financial engineering was equally sophisticated. Rather than relying solely on debt or diluting equity, Patel structured innovative financing arrangements. He negotiated technology transfer agreements where payment was linked to future sales, conserving cash while accessing cutting-edge capabilities. He created joint ventures for specific therapeutic areas, sharing risk while maintaining control. When traditional banks hesitated, he tapped into development finance institutions that supported pharmaceutical self-sufficiency.

By 1999, the transformation was showing results. Revenues had grown to ₹500 crores, double the post-split baseline. More importantly, the product mix had shifted toward higher-margin formulations, R&D spending had increased to 6% of sales (exceptional for an Indian company), and the company had filed its first drug master files with the U.S. FDA, laying groundwork for eventual American market entry.

The decision to go public wasn't just about raising capital—it was about forcing discipline and transparency on a family business. The IPO process in late 1999 required Patel to articulate his vision to skeptical institutional investors who wondered why anyone would invest in the smaller, less established half of the former Cadila. His pitch was simple but powerful: "We're not selling our past. We're selling our future. A future where Indian companies don't just copy drugs but create them."

The IPO roadshow revealed both opportunity and challenge. International investors were intrigued but wanted proof that an Indian company could navigate regulated markets. Domestic investors liked the growth story but worried about R&D spending eating into profits. Patel addressed both concerns with characteristic pragmatism: "We'll earn our right to innovate by executing flawlessly on generics. Every dollar of profit from copying funds development of something original."

February 2000 marked not just the successful IPO but a symbolic transition. The company that listed on the Bombay Stock Exchange bore little resemblance to the entity that emerged from the 1995 split. It had research facilities that rivaled government institutions, manufacturing plants that could pass international inspections, and a pipeline of products targeting not just India but the world. The stock opened at ₹80 and closed the first day at ₹127, a 58% premium that validated Patel's strategy.

Yet Patel's speech at the listing ceremony revealed his deeper ambition: "Today we join the capital markets not as a company that has arrived, but as one that has just begun. The real measure of our success won't be stock price or market capitalization. It will be whether a farmer in Bihar can afford the same quality medicine as a banker in Boston. That's the company we're building."

The restructuring era had transformed Cadila Healthcare from a wounded entity fighting for survival into a platform for global ambition. But transformation and execution are different challenges entirely. As the millennium turned, Patel and his team would discover that having a vision for global expansion and actually achieving it would require not just strategy but a series of bold acquisitions that would test every capability they had built.

IV. The M&A and Expansion Playbook (2000-2010)

The conference room at Boehringer Mannheim's Frankfurt headquarters in December 2002 was austere to the point of severity—white walls, gray carpet, and a single piece of abstract art that might have been either very expensive or picked up from a flea market. Pankaj Patel sat across from Dr. Hans Mueller, the German executive managing the divestment of German Remedies' Indian operations. Between them lay a deal that would either catapult Cadila Healthcare into the pharmaceutical major leagues or saddle it with an expensive mistake.

"Mr. Patel," Mueller said in accented English, "German Remedies has been in India since 1963. Our brands are household names. Why should we trust them to a company that's barely seven years old in its current form?"

Patel's response would become legend within Zydus: "Because, Dr. Mueller, we're not buying your past. We're buying our future. And unlike you, our future is only in pharmaceuticals, only in emerging markets, and entirely dependent on making these brands succeed."

The German Remedies acquisition, finalized in early 2003 for ₹730 crores, wasn't just Cadila Healthcare's largest deal to date—it was a masterclass in strategic acquisition. German Remedies brought fourteen manufacturing facilities, a portfolio of established brands in cardiovascular and gastrointestinal therapy, and something invaluable: relationships with thousands of doctors who had prescribed these brands for decades. But what Patel saw that others missed was the technological capability hidden in those aging facilities—German Remedies had been doing complex chemistry long before it became fashionable.

The integration challenged every assumption about how Indian companies handled acquisitions. Rather than the typical approach of slashing costs and milking brands, Patel invested heavily in upgrading German Remedies' facilities. He retained most of the scientific staff, even giving them enhanced roles in the combined entity's R&D structure. When competitors predicted culture clash between German precision and Indian flexibility, Patel created integration teams that celebrated both, using German systematic approaches for quality while maintaining Indian agility in decision-making.

The real genius was in portfolio optimization. German Remedies had several drugs nearing patent expiry in Western markets but still protected in India. Patel's team developed next-generation versions—extended-release formulations, combination products, new indications—that extended the commercial life while providing genuine therapeutic benefits. Revenues from the acquired portfolio grew 30% in the first year alone, validating the premium price paid.

But Patel wasn't content with domestic expansion. In 2004, while Indian companies were still celebrating entry into semi-regulated markets, he set his sights on the United States. The strategy was counterintuitive: instead of starting with simple generics where competition was fierce and margins thin, Cadila would focus on complex generics—products difficult to manufacture, requiring sophisticated technology, commanding better prices.

The U.S. subsidiary, Zydus Pharmaceuticals USA, was established in Princeton, New Jersey, not because Patel wanted a prestigious address but because proximity to pharmaceutical talent from Merck, J&J, and Bristol-Myers Squibb provided recruiting advantages. The initial team was a fascinating mix: Indian scientists who understood cost-efficient development, American regulatory experts who could navigate FDA complexities, and European technical specialists who brought advanced manufacturing knowledge.

The first U.S. product launch in 2005—a generic version of an anti-inflammatory drug—generated modest revenues but enormous learning. The FDA's inspection of the Indian manufacturing facility supplying the product was brutal. Inspectors found nothing that would prevent approval, but their observations revealed gaps between Indian "good enough" and American "perfect." Patel's response was characteristic: he hired the recently retired FDA inspector as a consultant, essentially paying to be criticized until standards exceeded requirements.

While building American capabilities, Patel spotted an opportunity in Brazil that others had overlooked. Nikkho Pharmaceuticals, a mid-sized Brazilian company, was struggling despite having good products and manufacturing facilities. The problem was management—the founding family had lost interest, professional managers were risk-averse, and the company was slowly dying despite Brazil's booming pharmaceutical market.

The 2007 acquisition of Nikkho for $70 million was Patel's first international acquisition, and he approached it differently than German Remedies. Instead of integration, he opted for transformation. He replaced most senior management but promoted promising middle managers who had been stifled under the previous regime. He introduced Indian cost-efficiency practices while maintaining Brazilian market knowledge. Most importantly, he used Nikkho as a gateway to Latin America, leveraging Brazil's Mercosur advantages to enter Argentina, Chile, and Colombia.

The Brazilian experience taught valuable lessons about emerging market expansion. Unlike India where relationships and brand loyalty dominated, Brazil was price-sensitive but quality-conscious. Unlike the U.S. where regulatory approval was everything, Brazil required navigation of complex public health bureaucracy. The Nikkho team developed a hybrid model: Indian efficiency in manufacturing, Brazilian expertise in government relations, and global best practices in quality.

Back in the United States, Cadila's ANDA (Abbreviated New Drug Application) filings were accelerating. By 2008, the company had filed 50 ANDAs with 20 approvals, but the portfolio strategy was becoming clear. While competitors fought over blockbuster generics where thirty companies might compete, Cadila targeted niche products—specialized dosage forms, difficult-to-manufacture APIs, products requiring clinical trials. These "complex generics" had fewer competitors and better margins.

The financial crisis of 2008 created unexpected opportunities. As Western pharmaceutical companies retrenched, assets became available at distressed prices. Patel authorized a war chest for opportunistic acquisitions but with strict criteria: the target must bring either technology, market access, or regulatory expertise that would take years to build organically. Several deals were explored but ultimately abandoned when due diligence revealed hidden liabilities or cultural incompatibilities.

The decade's expansion wasn't without setbacks. A joint venture in Russia collapsed when the local partner was investigated for corruption. An acquisition target in South Africa fell through when regulatory changes made the market unviable. A promising collaboration with a Japanese company ended when strategic priorities diverged. Each failure was dissected in what Patel called "post-mortem sessions," extracting lessons that informed future decisions.

By 2010, the M&A strategy had transformed Cadila Healthcare's footprint. From a purely domestic player, it had become genuinely multinational with manufacturing in four countries, sales in twenty-five markets, and regulatory filings in all major jurisdictions. Revenues had grown to ₹3,500 crores, but more importantly, the revenue mix had shifted—40% now came from international markets, providing currency diversification and exposure to different growth dynamics.

The human capital transformation was equally impressive. The company now employed scientists from fifteen nationalities, creating what internal documents called a "global innovation ecosystem." The Princeton office became a training ground where Indian scientists learned FDA regulations while American colleagues discovered cost-effective development approaches. The Brazil operation pioneered patient assistance programs later replicated globally. The German Remedies integration created a quality culture that permeated the entire organization.

Yet Patel knew that acquisition-driven growth had limits. Speaking at an investor conference in Mumbai, he outlined the next phase: "We've proven we can buy and integrate. We've proven we can compete in regulated markets. Now we must prove we can innovate. The next decade won't be about acquiring other companies' products but creating our own. Not just generics, however complex, but new molecules, new biologics, new therapeutic approaches."

The room was skeptical—no Indian company had successfully developed and commercialized novel drugs. But Patel had been skeptical too when he started the transformation in 1995, the restructuring in 1997, the global expansion in 2000. Each time, methodical execution had converted vision into reality. As the decade closed, Cadila Healthcare had the infrastructure, capabilities, and capital for its most ambitious phase yet: becoming not just a global generic company but a genuine pharmaceutical innovator.

V. The Innovation Revolution: Biosimilars & NCEs (2010-2020)

Dr. Pankaj Salunkhe stood before a bioreactor containing 10,000 liters of genetically modified Chinese hamster ovary cells at Zydus's biotechnology facility in Ahmedabad on a humid July morning in 2012. Inside that sterile steel vessel, microscopic cells were producing proteins that would eventually become Exemptia, India's first biosimilar of Adalimumab—the world's best-selling drug with annual revenues exceeding $16 billion. Salunkhe, who had spent fifteen years at Genentech before Patel convinced him to return to India, understood the magnitude of this moment. If successful, they would break the monopoly of a drug that cost Indian patients ₹40,000 per injection, making it accessible at one-fifth the price.

"We're not just copying a molecule," Salunkhe told his team of young scientists, many recruited straight from India's top biotechnology programs. "We're reverse-engineering one of the most complex proteins ever commercialized, proving it's identical in every clinically meaningful way, and doing it without infringing valid patents. If we succeed, we change the biosimilar game globally."

The journey to this moment had begun in 2009 when Patel made a strategic decision that puzzled analysts. While competitors were maximizing profits from simple generics, he allocated ₹500 crores—nearly 15% of annual revenue—to biotechnology infrastructure. The investment seemed excessive for uncertain returns. Biosimilars were unproven commercially, regulatory pathways were unclear, and the scientific challenges were immense. Unlike chemical drugs where the molecule is identical, biological drugs are produced by living cells, making exact replication impossible. The goal was to create something "similar" enough to have the same therapeutic effect.

Patel's logic was compelling in its simplicity: "Chemical drugs are becoming commoditized. Future pharmaceutical value will come from biologics—proteins, antibodies, cell therapies. If we don't build these capabilities now, we'll be permanently locked out of tomorrow's pharmaceutical industry." He was betting that Zydus could leapfrog the traditional development curve, moving directly from generics to cutting-edge biologics without the intermediate steps Western companies had taken.

The Adalimumab project, codenamed "Project Liberation" internally, exemplified this ambition. Humira, as Abbott (later AbbVie) branded it, treated everything from rheumatoid arthritis to Crohn's disease. Its complexity was legendary—a Y-shaped antibody with 1,330 amino acids requiring precise folding to maintain biological activity. Even minor variations in manufacturing could render it ineffective or, worse, trigger immune responses.

The development process was unlike anything Zydus had attempted. Traditional drug development involved chemistry—mixing compounds, purifying products, analyzing structures. Biosimilar development was more like brewing beer crossed with semiconductor manufacturing. Temperature variations of half a degree could change protein structure. Oxygen levels, pH, mixing speeds—every parameter required optimization. The team ran over 250 experimental batches before achieving consistent production.

Regulatory strategy was equally complex. India had no biosimilar guidelines when development began. The team worked with regulators to establish frameworks, essentially writing rules while following them. International markets were even more challenging. The European Medicines Agency had the world's most stringent biosimilar requirements. The FDA was still developing guidelines. Each jurisdiction required different clinical trials, analytical methods, and manufacturing standards.

The clinical trials for Exemptia revealed the human dimension of innovation. Patients with rheumatoid arthritis, many unable to afford Humira, volunteered for trials knowing they might receive placebo. Dr. Rashmi Mehta, who led clinical development, recalled: "One patient, a classical musician who hadn't played in years due to joint deformity, performed a concert after treatment. That's when we knew we weren't just developing a drug but restoring lives."

December 2014 marked the watershed: Exemptia received Indian regulatory approval, launching at ₹8,000 per injection versus Humira's ₹40,000. The price point was carefully calculated—low enough to expand access dramatically, high enough to recoup investment and fund future research. Within six months, Exemptia had captured 15% of the Indian adalimumab market, validating the biosimilar model.

But Patel's innovation ambitions extended beyond biosimilars. In parallel, Zydus was pursuing something even more audacious: developing entirely new molecules, called New Chemical Entities (NCEs). The poster child was Saroglitazar, branded as Lipaglyn, targeting diabetic dyslipidemia—a condition affecting millions of Indians with both diabetes and cholesterol problems.

The Saroglitazar story began in 2001 when Dr. Rajesh Bahekar, a medicinal chemist at Zydus Research Centre, noticed that existing diabetes drugs addressed either glucose or lipids but not both. The idea seemed obvious: create a dual-action molecule. The execution was anything but obvious. It took eleven years, testing over 1,500 molecular variations, conducting trials on 3,000 patients, and investing ₹800 crores before Lipaglyn received approval in 2013.

What made Lipaglyn special wasn't just that it was India's first indigenously developed NCE to reach market. It was that Zydus had achieved something considered impossible for an emerging market company: creating a drug that wasn't just "me-too" but genuinely innovative, addressing an unmet medical need with a novel mechanism of action. When The Lancet published clinical trial results showing Lipaglyn's unique efficacy profile, it marked Indian pharmaceutical research joining global scientific discourse as equals, not imitators.

The innovation infrastructure supporting these breakthroughs was equally impressive. By 2015, Zydus operated nineteen research facilities employing 1,400 scientists. The Zydus Research Centre in Ahmedabad became a pilgrimage site for aspiring pharmaceutical researchers, featuring equipment that wouldn't look out of place at Pfizer or Novartis. The company pioneered unusual practices: scientists received bonuses for failed experiments if they generated valuable learning, patent filings were celebrated even if commercially unviable, and cross-functional teams mixed chemists with clinicians, regulatory experts with manufacturing engineers.

The acquisition of Sentynl Therapeutics in 2017 for $171 million added another dimension to the innovation strategy. Sentynl brought a portfolio of specialized pain management products and, more importantly, relationships with U.S. hospitals and specialty pharmacies. This wasn't just market access—it was learning how to commercialize innovative products in the world's most sophisticated pharmaceutical market.

The innovation pipeline by decade's end was remarkable in breadth and ambition. Beyond Exemptia and Lipaglyn, Zydus had developed biosimilars for cancer, autoimmune diseases, and growth disorders. The NCE pipeline included molecules for rare diseases, novel antibiotics addressing resistance, and combination therapies for metabolic disorders. Each program represented not just scientific achievement but strategic positioning for future pharmaceutical paradigms.

Financial returns validated the innovation investment. By 2020, specialty products—biosimilars, NCEs, and complex generics—contributed 35% of revenues but 50% of profits. The market recognized this transformation: Zydus's price-to-earnings ratio expanded from 15 in 2010 to 25 in 2020, reflecting investor belief in innovation-driven growth. Analysts who had questioned R&D spending now praised the "innovation premium" in valuations.

Yet the human stories behind these achievements were equally compelling. Dr. Salunkhe's team that developed Exemptia included a former software engineer who retrained in biotechnology, a young woman from rural Gujarat who became one of India's leading antibody engineers, and a retired professor who joined because he wanted to make medicines affordable for his diabetic grandson. The Lipaglyn team worked through personal tragedies, failed trials, and moments when the entire project nearly died, bound together by belief that Indian science could create, not just copy.

The decade closed with Patel addressing the annual R&D conference, his hair now more gray than black, but his ambition undimmed: "We've proven Indian companies can innovate. We've shown that affordable doesn't mean inferior. We've demonstrated that emerging market constraints can drive creative solutions. But we're not done. The next frontier isn't just new drugs but new modalities—gene therapy, cell therapy, precision medicine. The question isn't whether we can compete with Big Pharma but whether we can redefine what pharmaceutical innovation means."

As 2020 arrived, bringing an unexpected global pandemic, these weren't just words but prophecy. The innovation capabilities built over a decade would soon be tested by the ultimate challenge: developing a vaccine for a novel virus, using unproven technology, under unprecedented time pressure. The biosimilar expertise, the NCE experience, the regulatory knowledge, the clinical trial capabilities—everything would converge in humanity's darkest hour, proving that innovation isn't just about commercial success but societal impact.

VI. The COVID Moment: ZyCoV-D and Global Recognition (2020-2021)

The WhatsApp message arrived at 2:47 AM on January 30, 2020. Dr. Sharvil Patel, CEO of Zydus's vaccine division and Pankaj Patel's son, was in San Francisco attending the J.P. Morgan Healthcare Conference when his research director in Ahmedabad forwarded a scientific paper from Chinese researchers. They had published the genetic sequence of a novel coronavirus causing mysterious pneumonia in Wuhan. The message ended with a question that would define the next eighteen months: "Should we start working on a vaccine?"

By the time Sharvil's flight landed in Delhi thirty hours later, he had made a decision that would have seemed insane to anyone watching. Zydus would develop a DNA vaccine—a platform never successfully used in humans—against a virus nobody fully understood, in a timeframe that defied every precedent in pharmaceutical history. He called his father from the airport. "We're going to need ₹500 crores and permission to fail," he said. Pankaj's response was immediate: "You have both."

The Vaccine Technology Centre in Ahmedabad became ground zero for what insiders called "Mission Impossible." Dr. Khyati Patel (no relation), who led the DNA platform development, had spent five years preparing for this moment without knowing it. Since 2015, her team had been experimenting with DNA vaccines for rabies, influenza, and Ebola—diseases where traditional vaccine approaches had limitations. None had reached market, but each failure had taught valuable lessons about plasmid design, delivery mechanisms, and immune responses.

DNA vaccines were scientifically elegant but practically problematic. Unlike traditional vaccines using weakened viruses or mRNA vaccines using genetic instructions, DNA vaccines contained circular pieces of genetic code (plasmids) that, once inside human cells, instructed them to produce viral proteins, triggering immune response. The advantages were compelling: DNA was stable at room temperature (crucial for India's climate), manufacturing was rapid and scalable, and safety profiles were excellent since no actual virus was involved. The disadvantage was singular but significant: they didn't work very well in humans, producing weak immune responses that required multiple doses or special delivery devices.

The Zydus team's breakthrough came from an unexpected source. Dr. Arun Sharma, a young scientist who had joined straight from IIT, suggested looking at veterinary DNA vaccines where the technology had shown more success. "Animals don't have the same skin barrier humans do," he explained. "What if the problem isn't the vaccine but the delivery?" This insight led to collaboration with a medical device team that had been developing needle-free injection systems for diabetics.

By March 2020, as India entered its first lockdown, the vaccine team had been isolated in a makeshift biosecure facility within the research center. Forty scientists volunteered to live on-site for three months, sleeping in converted conference rooms, eating meals prepared by staff who also agreed to isolation. Families were informed through video calls. The outside world was panicking about toilet paper while inside, they were racing to design humanity's first DNA vaccine.

The initial plasmid designs were disasters. The first construct produced robust antibodies in mice but failed in larger animals. The second caused strong T-cell responses but weak antibody production. The third seemed perfect until stability testing showed degradation within days. Each failure meant two weeks lost—time they didn't have as global death tolls mounted. The breakthrough came in iteration number seven: a plasmid encoding not just the spike protein but specific mutations that stabilized it in the prefusion confirmation, essentially freezing the protein in its most immunogenic shape.

April brought the first animal trials. The protocol required testing in mice, then rabbits, then non-human primates—a sequence that typically took a year compressed into ten weeks. The animal facility operated twenty-four hours, with scientists working in shifts to monitor immune responses, measure antibody titers, and perform challenge studies where vaccinated animals were exposed to the virus. When rhesus macaques showed complete protection after two doses, champagne was opened—briefly, before everyone returned to work.

The collaboration with Biotechnology Industry Research Assistance Council (BIRAC) provided crucial government support without bureaucratic interference. Dr. Renu Swarup, BIRAC's director, understood that speed required breaking rules intelligently. Regulatory meetings that typically took months happened in days. Approvals that required sequential review occurred in parallel. Import permits for specialized equipment were expedited. "We're not cutting corners," Swarup told critics, "we're straightening the path."

Human trials began in July 2020, making ZyCoV-D among the world's first COVID vaccine candidates to enter clinical testing. The Phase 1 trial at Ahmedabad Civil Hospital was surreal. Outside, the city was in lockdown with streets empty except for ambulances. Inside, volunteers lined up to receive an experimental vaccine based on technology never proven in humans. The first volunteer, a 32-year-old nurse named Priya who had seen colleagues die from COVID, told reporters: "If this works, I'm part of history. If it doesn't, at least we tried."

The adaptive trial design was ingenious in its efficiency. Instead of separate Phase 1, 2, and 3 trials taking years, Zydus ran overlapping studies where data from early phases informed later ones in real-time. The Data Safety Monitoring Board met weekly instead of quarterly. Statistical analyses that typically took months were completed in days using AI-powered systems. Every process was examined for unnecessary delays and eliminated.

Phase 2 results in September showed strong immunogenicity with an unusual twist: three doses produced dramatically better responses than two, with antibody levels comparable to mRNA vaccines. The scientific community was skeptical—three doses seemed commercially unviable when competitors required only two. But Sharvil saw opportunity: "In India, people are used to multiple-dose vaccines. If three doses mean better protection without cold chain requirements, that's a trade-off worth making."

The Phase 3 trial, launched in December 2020, was the largest clinical trial ever conducted by an Indian company: 28,000 participants across fifty sites. The logistics were staggering. Each participant required three visits for vaccination plus follow-ups. Blood samples needed processing within hours. Adverse events required immediate investigation. COVID cases needed genomic sequencing to determine variants. The trial occurred during India's devastating second wave when the Delta variant emerged, providing an unfortunate but scientifically valuable opportunity to test efficacy against the most transmissible variant yet seen.

The needle-free delivery system, developed in parallel, was revolutionary in its simplicity. The PharmaJet device used a spring-powered mechanism to deliver vaccine through skin using a high-pressure stream thinner than a human hair. No needles meant no sharps disposal, no needlestick injuries, and critically for vaccine-hesitant populations, no injection fear. The device could be operated by minimally trained personnel, enabling vaccination in rural areas lacking healthcare infrastructure.

March 2021 brought preliminary efficacy data: 66.6% protection against symptomatic COVID, rising to 100% against moderate to severe disease. Critics immediately compared it unfavorably to mRNA vaccines showing 95% efficacy. But context mattered: ZyCoV-D was tested against Delta when other vaccines were tested against less transmissible variants. The vaccine remained stable at 2-8°C for three months and at 25°C for several weeks—game-changing for tropical countries lacking ultra-cold freezers.

The regulatory approval process was unprecedented in its scrutiny. The Subject Expert Committee reviewed 50,000 pages of data across multiple meetings. Every adverse event was investigated, every protocol deviation scrutinized, every statistical analysis challenged. International observers were invited to ensure transparency. When approval finally came on August 20, 2021, India had the world's first DNA vaccine for human use and the first needle-free COVID vaccine.

The global recognition was immediate and profound. Nature published an editorial calling it "a milestone for DNA vaccines." The WHO requested detailed data for potential Emergency Use Listing. Scientists from Oxford, Harvard, and the Gates Foundation reached out for collaborations. Countries from Africa and Southeast Asia, struggling with cold chain requirements of mRNA vaccines, expressed interest in technology transfer.

But for the Zydus team, the most meaningful recognition came from an unexpected source. Dr. Margaret Liu, a pioneer of DNA vaccines who had spent thirty years trying to make the technology work, sent a handwritten note to Khyati Patel: "You did what we couldn't. You proved DNA vaccines aren't just scientifically interesting but practically useful. This changes everything."

The economic model was deliberately different from Western vaccines. While Pfizer and Moderna maximized profits during the pandemic, Zydus priced ZyCoV-D at ₹358 per dose for government procurement—enough to cover costs and fund future research but not exploit crisis. Private market pricing was higher but still accessible to middle-class Indians. Technology transfer agreements with manufacturers in Africa and Asia prioritized access over revenue.

VII. US Operations: Building a Generics Powerhouse

The FDA inspector's flashlight illuminated a corner of the sterile manufacturing suite at Zydus's Moraiya facility in Gujarat at 3 AM on a humid Tuesday in March 2012. She had been examining the plant for six straight days, checking everything from air particle counts to employee training records. This wasn't a routine inspection—it was a Pre-Approval Inspection for what would become Zydus's most important U.S. product launch: a generic version of Lipitor, the world's best-selling drug that had generated $125 billion in sales for Pfizer. The inspector turned to the plant manager and said something that would become company lore: "This is cleaner than some American facilities I've seen."

That moment represented years of painstaking work transforming Zydus from an ambitious Indian company into America's fifth-largest generic pharmaceutical corporation by prescription volume. The journey had been neither linear nor easy, littered with FDA warning letters, failed launches, and moments when the entire U.S. strategy seemed doomed. Yet by 2024, Zydus would dispense over 200 million prescriptions annually in America, operating facilities in New Jersey and manufacturing over 500 different products for the world's most regulated pharmaceutical market.

The U.S. odyssey truly began in 2006 when Pankaj Patel hired Dr. Richard Mansfield, a former FDA reviewer who had spent twenty years at the agency before joining industry. Mansfield's mandate was blunt: build a regulatory affairs team that didn't just meet FDA standards but exceeded them. "The FDA doesn't trust Indian companies," Mansfield told his first team meeting. "We need to be twice as good to be considered equal."

Mansfield instituted what became known internally as "FDA Plus"—quality standards that went beyond regulatory requirements. Every batch record was reviewed by two independent quality officers. Every deviation, however minor, triggered root cause analysis. Every customer complaint, even if clearly unfounded, received full investigation. The approach was expensive and slowed production, but it built something invaluable: regulatory credibility.

The product selection strategy was counterintuitive. While competitors rushed to file applications for blockbuster generics where thirty companies might compete, Zydus focused on "complex generics"—products difficult to manufacture, requiring specialized equipment or expertise. Transdermal patches, modified-release formulations, sterile injectables, topical creams with complex rheology—products where manufacturing capability, not just regulatory approval, determined success.

The Mesalamine story exemplified this approach. Used to treat ulcerative colitis, Mesalamine required delayed-release technology ensuring drug release in the colon, not stomach. The innovator product used a pH-sensitive coating that dissolved at specific intestinal pH levels. Zydus developed an alternative formulation using time-based release, avoiding patents while providing equivalent therapeutic effect. Development took four years and cost $15 million, but when approved in 2011, only three other companies had competing products versus twenty-plus for simpler generics.

The U.S. commercial infrastructure evolved through expensive lessons. Initial attempts to sell directly to pharmacy chains failed—Zydus lacked the scale for favorable negotiations. Partnering with wholesalers meant accepting lower margins but provided immediate market access. The breakthrough came through relationships with Group Purchasing Organizations (GPOs) representing hospital systems. These buyers valued supply reliability over lowest price, playing to Zydus's strengths in manufacturing consistency.

2013 brought crisis and transformation. An FDA inspection at the Moraiya facility identified "significant violations" of good manufacturing practices—not product quality issues but documentation gaps that suggested inadequate quality systems. The Warning Letter, published publicly, caused customer defections and delayed multiple product approvals. Stock price dropped 30% in two days. Critics questioned whether Indian companies could ever meet U.S. standards consistently.

Patel's response was radical: he hired Barbara Pirola, a former FDA compliance director, gave her unprecedented authority, and told senior management that anyone resisting her changes would be terminated. Pirola instituted a quality transformation that went beyond fixing violations. She created a "Quality Council" with veto power over commercial decisions. She mandated that every employee, from machine operators to senior executives, undergo annual FDA regulation training. She established metrics where quality incidents affected bonuses more than sales achievements.

The transformation was painful. Production efficiency dropped as procedures were rewritten. Experienced managers resigned rather than adapt to new requirements. Costs increased as documentation requirements multiplied. But within eighteen months, the FDA removed the Warning Letter, noting "significant improvements in quality systems and culture." More importantly, customer confidence returned stronger than before—buyers saw a company that responded to problems decisively.

The product portfolio evolution reflected increasing sophistication. Early approvals were for simple tablets and capsules. By 2015, Zydus was launching complex injectables requiring specialized manufacturing in isolator technology. By 2018, the portfolio included biosimilars, requiring entirely different manufacturing and regulatory capabilities. By 2020, the company was developing 505(b)(2) applications—hybrid filings that required clinical trials but offered market exclusivity.

The Tobramycin inhalation solution launch in 2019 showcased evolved capabilities. Used for cystic fibrosis patients, this product required sterile manufacturing, specialized nebulizer compatibility testing, and patient training programs. Only three companies had successfully developed generics due to complexity. Zydus's version, priced 40% below the brand, captured 25% market share within a year while maintaining perfect quality record—no recalls, no complaints, no regulatory issues.

Manufacturing footprint expansion was strategic rather than opportunistic. The 2017 acquisition of Sentynl Therapeutics brought not just products but a U.S.-based manufacturing facility in Louisiana, providing "Made in USA" credentials important for certain buyers. The 2020 investment in a new sterile injectable facility in Ahmedabad specifically for U.S. supply created dedicated capacity, avoiding quality issues from multi-market manufacturing. Each facility specialized in specific technologies, creating centers of excellence rather than generalized capabilities.

The commercial model evolved toward partnerships and value-added services. Rather than pure price competition, Zydus offered supply chain solutions—consignment inventory, demand forecasting, custom packaging. The company pioneered "virtual inventory" programs where hospital systems could access emergency supplies from strategically located distribution centers, reducing their carrying costs while ensuring availability.

By 2023, the numbers told a remarkable story. Zydus held 288 ANDA approvals with 120 pending—one of the industry's largest pipelines. The company ranked among top five suppliers in multiple therapeutic categories: cardiovascular, central nervous system, gastrointestinal. Market share in specific products exceeded 50%—remarkable for a generic competitor. U.S. revenues exceeded $1 billion annually, contributing 30% of global sales but 40% of profits due to higher margins.

The competitive dynamics were fascinating. Against Israeli companies like Teva, Zydus leveraged lower development costs. Against other Indian companies, it emphasized quality track record and complex product capabilities. Against U.S. manufacturers, it offered cost advantages while maintaining equivalent quality. The sweet spot was products too complex for pure cost competitors but not valuable enough for originators to defend aggressively.

Yet challenges persisted. Pricing pressure intensified as buying consortiums consolidated—three purchasers controlled 90% of generic volumes. Regulatory requirements continued expanding with FDA implementing new quality metrics, serialization requirements, and supply chain security mandates. Chinese companies, initially focused on APIs, began entering finished dosage markets with aggressive pricing. Patent challenges became more expensive as innovator companies used legal systems to delay generic entry.

The human capital strategy was crucial for sustained success. The Princeton office employed 200 people, primarily Americans with deep industry experience. Key positions—regulatory affairs, quality assurance, commercial leadership—were staffed by executives recruited from established companies. But equally important was reverse knowledge transfer: American executives spent time in India understanding cost structures, Indian managers worked in U.S. understanding market dynamics. This cross-pollination created unique capabilities combining American market knowledge with Indian execution efficiency.

Speaking at a 2024 investor conference, the head of U.S. operations outlined future strategy: "We've proven we can compete in the world's toughest generic market. The next decade is about moving beyond traditional generics toward specialty pharmaceuticals, biosimilars, and novel drug delivery systems. We're not trying to be the biggest—we're positioning to be the most innovative generic company in America."

VIII. Global Footprint & Manufacturing Excellence

The alert came at 4:17 PM on a Friday afternoon in November 2019: contamination detected in Batch #TMZ-4421 at the Baddi facility in Himachal Pradesh. Within minutes, a crisis management protocol activated across three continents. The quality team in India isolated the batch, the regulatory team in Princeton notified the FDA proactively, and the supply chain team in São Paulo began assessing impact on Brazilian deliveries. By 6 PM, root cause was identified—a microscopic crack in a sterile filter. By Monday morning, corrective actions were implemented, and no product had reached patients. This seamless response across Zydus's thirty manufacturing plants worldwide exemplified a transformation from local manufacturer to global production powerhouse.

The manufacturing philosophy that enabled this coordination emerged from painful experience. In 2008, different Zydus facilities operated as independent kingdoms with unique procedures, quality standards, and even documentation languages. A product manufactured in Ahmedabad couldn't easily transfer to Baddi. Brazilian facilities used different testing methods than Indian ones. The FDA inspection that could approve one plant might find violations at another supposedly following identical procedures.

Dr. Wolfgang Fischer, recruited from Novartis to head global manufacturing in 2010, introduced what became known as the "One Zydus System." His first all-hands meeting was legendary for its bluntness: "We have thirty facilities but no manufacturing network. We have local excellence but no global standards. This changes now, or we'll never be truly multinational."

The standardization journey was methodical and expensive. Every Standard Operating Procedure was rewritten in a common format, translated into seven languages, and validated at each site. Equipment specifications were harmonized—new autoclaves in India matched those in Brazil, ensuring product transferability. Laboratory methods were unified using a "Gold Standard" protocol where every facility tested identical samples quarterly, with deviations triggering retraining. The investment exceeded ₹300 crores over three years, but the payoff was transformational: any product could be manufactured at any suitable facility with identical quality.

The Moraiya SEZ (Special Economic Zone) facility, completed in 2015, showcased manufacturing ambition. Spread across 100 acres, it wasn't just large but sophisticated—oral solid dosage forms, sterile injectables, and biological products manufactured in separate blocks with dedicated utilities. The design borrowed from semiconductor manufacturing: unidirectional flow preventing cross-contamination, automated material handling reducing human error, and real-time environmental monitoring ensuring consistent conditions. When Japanese regulators inspected in 2017, they commented it exceeded many facilities in Japan—high praise from the world's most demanding quality culture.

The U.S. manufacturing presence, established through acquisition and greenfield investment, served strategic purposes beyond production. The Louisiana facility, acquired with Sentynl, manufactured controlled substances—products requiring DEA licensing that created barriers for offshore competitors. The New Jersey packaging operation enabled "Made in USA" labeling important for certain government contracts. These facilities also served as training grounds where Indian engineers learned American operational practices while American workers discovered Indian efficiency improvements.

Brazil operations revealed different challenges. Unlike India's cost focus or America's quality obsession, Brazil required navigating complex labor laws, environmental regulations, and local content requirements. The São Paulo facility, expanded in 2016, became a model for emerging market manufacturing: automated where possible to manage labor costs, flexible to handle small batches for multiple countries, and integrated with local suppliers to meet nationalization requirements.

The supply chain orchestration across facilities was remarkably complex. Active pharmaceutical ingredients manufactured in Ankleshwar might be sent to Baddi for formulation, then to New Jersey for packaging, before distribution across America. A biosimilar produced in Ahmedabad could be filled in Brazil for Latin American markets. This complexity required sophisticated planning systems but provided remarkable flexibility—when COVID disrupted Indian operations, production shifted to Brazil and the U.S. within weeks.

Quality systems evolution was continuous and sometimes painful. The 2013 FDA Warning Letter triggered a complete quality transformation. The 2016 European inspection resulted in minor observations but major learning. The 2018 Brazilian regulatory change required extensive revalidation. Each challenge strengthened global systems. By 2020, Zydus facilities had undergone 200+ regulatory inspections across 25 countries with a 98% first-time approval rate—exceptional for any pharmaceutical company, remarkable for one operating primarily in emerging markets.

The technological infrastructure supporting manufacturing was increasingly sophisticated. Manufacturing Execution Systems (MES) provided real-time visibility into production across all facilities. Quality Management Systems (QMS) ensured deviations in India triggered alerts in America. Enterprise Resource Planning (ERP) integrated planning, production, and distribution globally. The investment in IT systems exceeded ₹500 crores, but enabled coordination impossible through manual systems.

Environmental and sustainability initiatives, initially driven by regulation, became competitive advantages. The Dahej facility, commissioned in 2018, featured zero liquid discharge, solar power generation, and green chemistry processes reducing solvent use by 60%. These investments, while expensive, resonated with environmentally conscious buyers and regulators. When the EU introduced environmental criteria for pharmaceutical procurement, Zydus was already compliant.

The human dimension of manufacturing excellence was crucial. The company employed 8,000+ people in production roles globally, from PhD chemical engineers to high school graduates operating packaging lines. Training investment was enormous—every employee received 40 hours annual training, supervisors received 80 hours, and site heads attended global conferences. The "Zydus Production Academy" established in 2019 standardized training globally, ensuring a machine operator in Brazil received identical instruction to one in India.

Technology adoption accelerated after COVID. Automated visual inspection replaced manual checking for injectable products. Continuous manufacturing, long discussed but rarely implemented, was piloted for high-volume products. Artificial intelligence predicted equipment failures before they occurred. Digital twins—virtual replicas of physical facilities—enabled process optimization without disrupting production. These weren't just efficiency improvements but necessary evolution as products became more complex and regulations more stringent.

The cost structure achieved through this global network was remarkable. Indian facilities provided 40-60% cost advantages versus Western manufacturing. Brazilian operations, while more expensive than India, were 30% cheaper than U.S. production. The U.S. facilities, despite high costs, enabled premium pricing for locally manufactured products. This portfolio approach—low-cost production where possible, local manufacturing where valuable—created competitive advantages difficult to replicate.

By 2024, manufacturing capabilities had evolved far beyond traditional pharmaceuticals. Cell culture facilities produced biosimilars competing with originator biologics. Vaccine production used novel platforms like DNA and viral vectors. The newly acquired CDMO business from Agenus added antibody-drug conjugate capabilities—among the most complex pharmaceutical manufacturing. Each expansion wasn't just capacity addition but capability enhancement, moving up the value chain from simple generics to specialized therapeutics.

The regulatory excellence achieved across facilities was noteworthy. FDA inspections, once dreaded events, became routine confirmations of quality systems. European inspectors, notoriously demanding, consistently approved Zydus facilities for supplying regulated markets. Even Japanese authorities, with unique requirements often creating barriers for foreign manufacturers, certified multiple facilities. This regulatory track record, built through years of investment and learning, created a moat competitors couldn't easily cross.

Speaking at a manufacturing excellence conference, Fischer reflected on the transformation: "When I joined, we had thirty facilities making products. Now we have a global manufacturing network creating healthcare solutions. The difference isn't just semantic—it's fundamental. We don't just manufacture drugs; we ensure consistent quality whether a patient receives our product in Manhattan or Mumbai, São Paulo or Stockholm."

IX. The Rebranding & Future Vision (2021-Present)

The boardroom was silent as Pankaj Patel unveiled the new logo on March 23, 2021. After 69 years, Cadila Healthcare would cease to exist, replaced by Zydus Lifesciences. The marketing team had proposed dozens of alternatives—keeping Cadila for brand recognition, adding modifiers like "Global" or "Innovative," creating sub-brands for different divisions. Patel rejected them all. "Cadila was my father's legacy," he said. "Zydus is what we're building for my grandchildren. We're not erasing history; we're acknowledging evolution."

The rebranding was more than cosmetic. Since the 1995 split with the Modi family, who retained rights to "Cadila Pharmaceuticals," confusion persisted in markets. Doctors prescribed "Cadila" products not knowing which company manufactured them. International partners struggled with similar-sounding entities. Legal disputes over trademark boundaries consumed resources. The clean break to "Zydus Lifesciences" eliminated ambiguity while signaling transformation from traditional pharmaceutical manufacturer to life sciences innovator.

The timing was deliberate. Fresh off the ZyCoV-D success, Zydus had global attention. The company had just reported its strongest financial year, with revenues crossing ₹15,000 crores. The innovation pipeline was robust, the balance sheet was strong, and leadership transition was underway with Sharvil Patel increasingly taking operational responsibilities. If there was ever a moment to redefine corporate identity, this was it.

But rebranding meant nothing without strategic evolution. The new mission statement—"Empowering healthier lives globally through innovative and accessible healthcare solutions"—signaled dual commitments often considered mutually exclusive. Innovation typically meant expensive products for wealthy markets. Accessibility usually meant cheap generics for developing countries. Zydus insisted on both, betting that future pharmaceutical value would come from making advanced therapies affordable.

The January 2025 acquisition of Agenus's CDMO business in Fremont, California, exemplified this strategy. The facility, capable of manufacturing antibody-drug conjugates (ADCs), represented cutting-edge biologics manufacturing. ADCs, which combine antibodies with chemotherapy drugs for targeted cancer treatment, were among the most complex and expensive pharmaceuticals. By acquiring manufacturing capability, Zydus could both produce its own ADCs and offer contract manufacturing to companies lacking facilities—a services business with 50%+ margins.

The innovation pipeline reflected increased ambition. Beyond traditional small molecules and biosimilars, Zydus was developing novel modalities. The gene therapy program for sickle cell disease, initiated in 2022, targeted a condition affecting millions in India and Africa but ignored by Western companies due to limited commercial potential. The mRNA platform, building on DNA vaccine expertise, aimed at both infectious diseases and cancer vaccines. The digital therapeutics initiative, partnering with technology companies, created app-based interventions for diabetes and mental health.

Digital transformation accelerated across all operations. The "Zydus 4.0" initiative, launched in 2023, wasn't just about automation but fundamental reimagination of pharmaceutical development and delivery. Artificial intelligence screened millions of compounds for drug potential. Machine learning predicted clinical trial outcomes. Blockchain ensured supply chain integrity. Digital twins optimized manufacturing processes. These weren't pilot projects but production systems processing real data and making actual decisions.

The commercial model evolution was equally significant. Traditional pharmaceutical companies sold pills through distributors to pharmacies. Zydus began experimenting with direct-to-patient models, subscription services for chronic medications, and outcome-based pricing where payment depended on therapeutic success. In India, the "Zydus Care" program provided free diagnostics, subsidized medicines, and lifestyle counseling for diabetes patients—building brand loyalty while gathering real-world data on drug effectiveness.

Geographical expansion took new forms. Rather than just exporting products, Zydus began establishing innovation centers in key markets. The Boston innovation hub, opened in 2023, focused on rare disease research leveraging proximity to Harvard and MIT. The Shanghai office, established despite India-China tensions, accessed Chinese biological research capabilities. The São Paulo center developed treatments for tropical diseases affecting Latin America. Each location brought unique capabilities impossible to replicate from India alone.

The sustainability agenda, previously peripheral, became central to strategy. The commitment to carbon neutrality by 2030 required fundamental changes: renewable energy for all facilities, green chemistry reducing environmental impact, and circular economy principles minimizing waste. This wasn't just corporate responsibility but business necessity as customers, regulators, and investors increasingly demanded environmental accountability.

Talent strategy evolved to match ambitions. The Zydus Leadership Academy, established in 2022, didn't just train existing employees but recruited globally. The "Boomerang" program attracted Indian scientists from Western companies with promises of impact impossible in Big Pharma. The entrepreneur-in-residence program brought startup founders into corporate structure. The sabbatical policy allowed employees to pursue academic research or social ventures. These initiatives recognized that innovation required not just investment but culture supporting creativity and risk-taking.

The regulatory strategy became more sophisticated and proactive. Rather than simply meeting requirements, Zydus began shaping regulations. Company executives served on WHO advisory panels, FDA working groups, and Indian government committees. When regulations for AI in drug discovery were being drafted, Zydus provided technical expertise. When biosimilar guidelines were updated, Zydus shared clinical trial data. This engagement positioned the company as a thought leader, not just compliance follower.

Financial engineering supported strategic ambitions. The ₹2,000 crore Qualified Institutional Placement in 2023 funded R&D without diluting control. The sustainability-linked bond, India's first by a pharmaceutical company, tied interest rates to environmental targets. The innovation fund, committing 15% of profits to breakthrough research, signaled long-term thinking rare in quarterly-earnings-focused markets.

Challenges remained substantial. Chinese pharmaceutical companies, backed by government support and massive domestic markets, competed aggressively globally. Western companies, facing patent cliffs, defended markets more vigorously through legal challenges and authorized generics. Regulatory requirements continued expanding, with new mandates for cybersecurity, supply chain transparency, and environmental impact. Healthcare systems, struggling with budget constraints, demanded ever-lower prices despite rising development costs.

The competitive positioning was unique but precarious. Against Western innovators, Zydus emphasized affordable innovation. Against Chinese manufacturers, it stressed quality and regulatory track record. Against Indian peers, it highlighted global presence and innovation pipeline. This multi-front competition required excellence across dimensions—not just good enough but genuinely superior in specific areas.

Yet optimism prevailed, grounded in achievements rather than hope. The company that began as a village pharmacy had developed the world's first DNA vaccine. The firm that started by copying Western drugs now licensed technologies to multinational corporations. The business that once struggled for bank loans now generated ₹10,000+ crores in annual cash flow. These weren't just metrics but validation of a model combining emerging market insights with global capabilities.

X. Financial Analysis & Business Model

The Excel spreadsheet on CFO Nitin Parekh's screen told a story of transformation through numbers. In fiscal year 2000, when Cadila Healthcare went public, revenues were ₹312 crores with a net margin of 8%. By Q3 FY2025, quarterly revenue alone reached ₹5,269 crores with net margins of 19.4%. The thousand-fold growth over 25 years was impressive, but what the numbers revealed about the underlying business model evolution was more instructive than the headline growth.

The revenue composition shift was dramatic. In 2000, 85% of sales came from India, primarily acute care generics sold through traditional distribution. By 2025, India contributed 45% of revenues but from entirely different sources: specialty therapies, biosimilars, consumer health products, and increasingly, direct-to-patient programs. The U.S., non-existent in 2000, now generated 35% of sales. Emerging markets contributed 15%, and Europe 5%. This geographical diversification provided natural hedging against currency fluctuations and country-specific risks.

The product mix transformation was equally striking. Simple generics, once 90% of portfolio, now represented just 40% of revenues but only 25% of profits. Specialty products—biosimilars, complex generics, NCEs—contributed 35% of revenues but 50% of profits. The vaccine and biologics segment, non-existent before 2010, generated 15% of sales with the highest margins. Consumer health, a recent addition, provided 10% of revenues with steady, predictable cash flows.

Margin evolution revealed operational excellence. Gross margins expanded from 45% in 2000 to 65% in 2025, driven by product mix shift toward complex products, vertical integration reducing raw material costs, and manufacturing efficiency improvements. EBITDA margins improved from 12% to 28% despite increased R&D spending, reflecting operational leverage as fixed costs spread across larger revenue base. Net margins nearly doubled from 8% to 19.4%, even after higher tax rates as tax holidays expired.

The R&D investment trajectory was remarkable for an Indian company. From ₹20 crores (6% of sales) in 2000, research spending reached ₹1,200 crores (8% of sales) in 2025. But composition changed dramatically: basic generic development decreased from 80% to 30% of R&D budget, biosimilar development grew to 25%, novel drug discovery consumed 30%, and emerging modalities (gene therapy, mRNA, digital therapeutics) took 15%. This wasn't just more spending but strategic allocation toward higher-value innovation.

Return on R&D investment validated the strategy. Every rupee spent on generic development generated ₹4 in cumulative sales over five years—acceptable but declining as competition intensified. Biosimilar R&D returned ₹8 per rupee invested, reflecting higher barriers to entry. Novel drug development, while riskier, showed ₹15 returns when successful, though many programs failed. The portfolio approach—steady returns from generics funding moonshot innovations—balanced risk while maintaining growth.

Capital allocation philosophy evolved from pure organic growth to balanced approach. In the early 2000s, 80% of capital went to capacity expansion. By 2025, allocation was more sophisticated: 30% for maintenance and capacity, 30% for R&D and innovation, 20% for strategic acquisitions, and 20% returned to shareholders through dividends and buybacks. This reflected maturation from growth-at-any-cost to optimizing returns on invested capital.

The acquisition track record was mixed but improving. Early deals like German Remedies were transformational, generating returns exceeding 30% IRR. The Brazilian acquisition provided market access worth multiples of purchase price. Recent U.S. acquisitions were expensive but strategic, providing capabilities difficult to build organically. The discipline to walk away from overpriced deals, even when strategically attractive, preserved capital for better opportunities.

Working capital management showed operational maturity. Days Sales Outstanding improved from 120 days in 2000 to 75 days in 2025 through better collections and customer mix. Inventory turns increased from 4x to 6x through demand planning and supply chain optimization. Days Payable Outstanding extended from 60 to 90 days as supplier relationships strengthened. The cash conversion cycle shortened from 180 to 90 days, freeing capital for investment.