Zensar Technologies: India's Mid-Tier IT Transformation Story

I. Introduction & Episode Setup

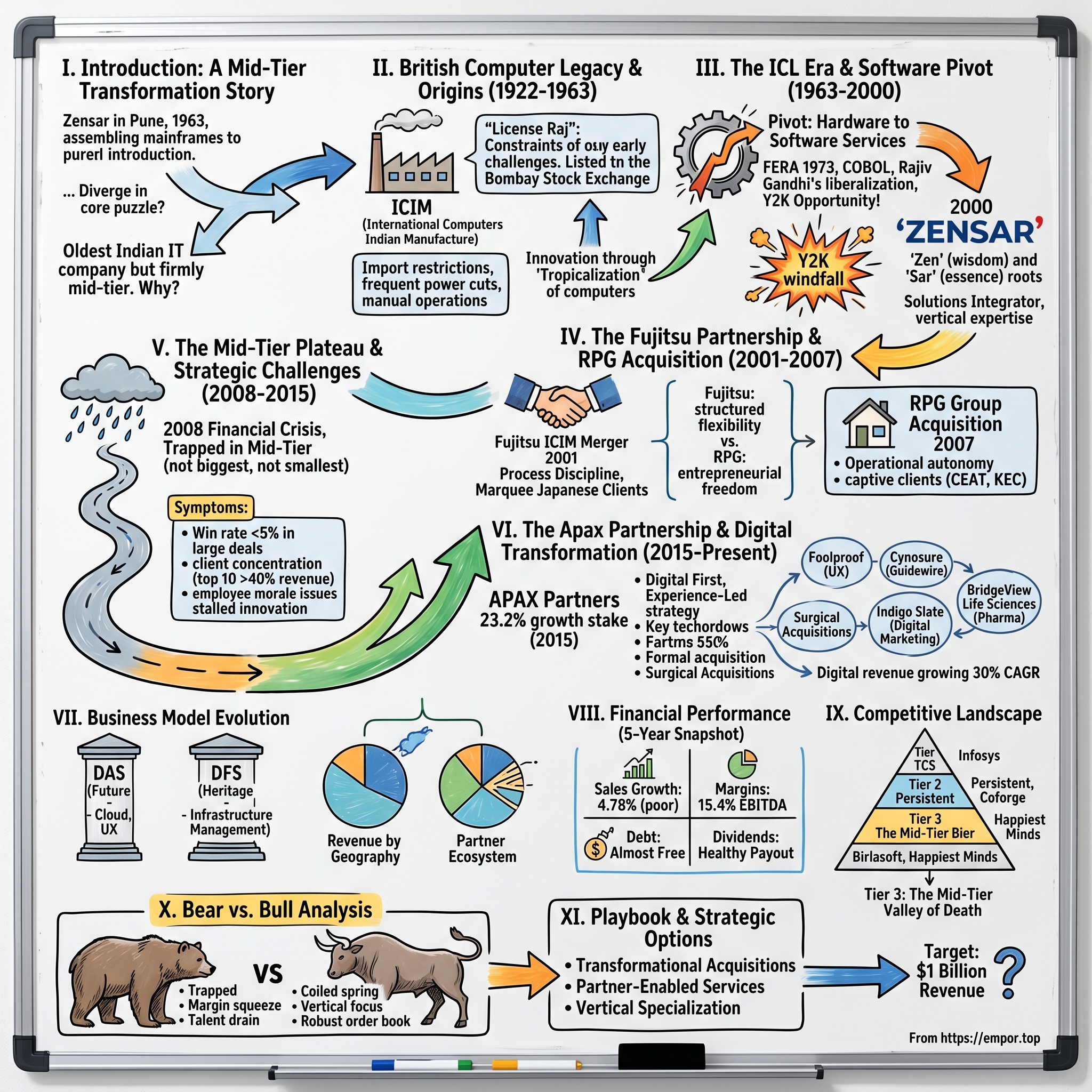

Picture this: It's 1963 in Pune, a city still finding its identity in post-independence India. While Silicon Valley pioneers are tinkering with transistors in California garages, a group of engineers in Maharashtra are assembling mainframe computers under license from a British manufacturer. These weren't just any computers—they were ICL machines, state-of-the-art for their time, being built in a country where most businesses still ran on paper ledgers and mechanical calculators.

Fast forward six decades. That same company, now called Zensar Technologies, manages digital transformations for Fortune 500 companies, employs over 10,500 professionals across 30+ global locations, and generates over ₹5,378 crores in annual revenue. Yet here's the puzzle: despite being one of India's oldest IT companies—predating Infosys by 18 years and TCS's independent operations by several years—Zensar remains firmly in the mid-tier, with a market cap of ₹18,373 crores while its younger peers command valuations in the hundreds of thousands of crores. The central question driving this narrative isn't just about technology or growth rates. It's about what happens when you're neither the biggest nor the smallest, when you're old enough to have legacy but young enough to transform, when you're Indian in heritage but global in ambition. This is the story of how a company navigated six decades of technological upheaval, ownership changes, and market dynamics to become what it is today: part of the RPG Enterprises with diverse business interests spanning infrastructure, tyres, pharma, IT and specialty, yet still searching for its definitive breakthrough moment.

What makes Zensar particularly fascinating for students of business history is its journey through multiple identities—from British colonial enterprise to Indian manufacturing subsidiary, from hardware assembler to software services provider, from family-owned to private equity-backed. Each transformation tells us something profound about India's economic evolution and the global technology industry's shifting centers of gravity.

As we unpack this story, we'll explore how strategic decisions made in Pune boardrooms rippled across global markets, why being "mid-tier" might be both a curse and a blessing, and what Zensar's trajectory tells us about the future of India's IT services industry. The company has delivered a poor sales growth of 4.78% over past five years, yet the company is almost debt free and maintains healthy margins. This paradox—profitable but not growing, established but not dominant—sits at the heart of our investigation.

II. The British Computer Legacy & Origins (1922-1963)

The monsoon of 1922 brought more than rain to Pune. It brought the machinery and engineers of a British original-equipment manufacturer, setting up what would become one of India's most enduring technology enterprises. The colonial administrators chose Pune not for its weather—the summers were brutal and the monsoons unpredictable—but for its strategic location between Bombay's ports and the Deccan's interior markets. What started as a regional manufacturing unit for British industrial equipment would, over four decades, morph into something far more ambitious.

By the late 1950s, the world was changing. Computers were no longer room-sized curiosities but becoming essential business tools. In Britain, a company called Hollerith Limited saw opportunity in India's nascent market for data processing equipment. In 1959, they acquired the Indian operations and rechristened it International Computers and Tabulators Limited, operating under the "I.C.T." trademark. The timing was prescient—India had just launched its second Five Year Plan, emphasizing industrialization and scientific advancement.

The real transformation came in 1963. As India was still finding its feet in the post-Nehru era, grappling with wars, food shortages, and the challenge of building a modern economy, a group of engineers in Pune were doing something remarkable: assembling mainframe computers under license from ICL (International Computers Limited), the British computing giant. They called the company ICIM—International Computers Indian Manufacture—and listed it on the Bombay Stock Exchange that same year.

Think about the audacity of this moment. India's per capita income was around $80. Most businesses still used mechanical calculators and paper ledgers. The country had perhaps a few dozen computers in total, mostly in government research institutions. Yet here was a company betting that India would need—and could afford—modern computing infrastructure. The early employees, many recruited from India's prestigious engineering colleges, recall working in facilities where they had to explain to visitors what a computer actually did.

ICIM's early years were defined by a peculiar set of challenges. Import restrictions meant that many components had to be locally sourced or manufactured—forcing innovation where Western companies could simply import. The License Raj meant that every expansion, every new product line, required government approval. Power cuts were frequent; the company had to install massive diesel generators to keep the assembly lines running. Air conditioning, essential for computer manufacturing, was considered a luxury and attracted extra taxes.

Yet these constraints bred ingenuity. ICIM's engineers became experts at tropicalization—modifying computer designs to withstand India's heat, humidity, and dust. They developed innovative cooling systems that used less power. They created training programs for technicians who had never seen a computer before. One veteran engineer recalled how they would sometimes hand-carry magnetic drums from the factory to customers because they didn't trust the transportation infrastructure.

The company's first major breakthrough came with a contract to supply computers to Life Insurance Corporation of India. The mainframes, each costing more than a luxury apartment in Bombay, would process millions of insurance policies. The installation required months of preparation—reinforcing floors to bear the weight, installing dedicated power lines, training dozens of operators. When the first LIC computer successfully processed its batch of policies, the ICIM team celebrated with rosogullas distributed across the factory floor.

By the late 1960s, ICIM had established itself as India's de facto computer company. When the government needed computing power for the census, they turned to ICIM. When banks wanted to modernize their operations, ICIM provided the solution. The company wasn't just selling computers; it was evangelizing a vision of digital India decades before the term existed.

But success brought scrutiny. Critics questioned why India needed expensive computers when millions lacked basic necessities. Labor unions worried about job losses from automation. Politicians debated whether computing technology should be imported or indigenous. ICIM found itself at the center of India's modernization debate—a position that would define its evolution for decades to come.

The transformation from a British manufacturer's outpost to India's computer pioneer wasn't just about technology transfer. It was about building an ecosystem—training engineers, developing supply chains, creating service networks, educating customers. Every computer sold required ICIM to also sell a vision of the future, one where Indian businesses could compete globally through technology.

As the 1960s drew to a close, change was in the air. ICL was consolidating its global operations. India was asserting greater control over foreign-owned businesses. And somewhere in the company's Pune headquarters, forward-thinking executives were beginning to realize that software, not hardware, might be the future. The stage was set for ICIM's next transformation—one that would redefine not just the company but India's entire technology industry.

III. The ICL Era & Software Pivot (1963-2000)

The 1970s opened with ICIM facing an existential question: What happens when your primary business—manufacturing computers under license—collides with a nationalist government determined to reduce foreign dependence? The Foreign Exchange Regulation Act (FERA) of 1973 sent shockwaves through India's business community, forcing foreign companies to dilute their stakes or exit. IBM famously chose to leave. ICL, ICIM's British parent, had to make a similar choice.

But ICIM's Indian management saw opportunity in crisis. Led by a cadre of engineers who had spent years absorbing ICL's technology and methods, they proposed something radical: pivot from hardware to software. The logic was compelling. Software required no imports, attracted no customs duties, needed minimal capital investment, and—crucially—could be exported for precious foreign exchange. One senior manager from that era recalled the board meeting where they made the decision: "We looked at our strengths—English-speaking engineers, mathematical prowess, low costs—and realized we could compete globally in software in ways we never could in hardware."

The transition wasn't smooth. Hardware engineers had to be retrained in programming languages like COBOL and FORTRAN. The company's identity, built around tangible products you could touch and see, had to shift to something abstract—lines of code that solved business problems. Customer relationships, cultivated over years of hardware sales, had to be reimagined around services rather than products. Many old-timers resisted, arguing that "real" engineering meant building things, not writing code.

Yet external forces accelerated the pivot. The 1980s brought economic liberalization's first whispers. Prime Minister Rajiv Gandhi, fascinated by technology, launched initiatives to promote software exports. ICIM secured contracts to develop software for international clients, initially through body-shopping arrangements where Indian engineers worked on-site at client locations. The work was unglamorous—maintaining legacy systems, fixing bugs, documenting code—but it generated crucial foreign exchange and expertise.

The real catalyst came in 1996 when ICIL (the renamed entity) made a strategic decision to formally separate its software business. In October 1996, ICIL purchased the software division from ICIM, creating a focused entity dedicated to IT services. This wasn't just a corporate restructuring; it was a declaration of intent. Software wasn't a sideline anymore—it was the future.

Then came Y2K—the millennium bug that threatened to crash computer systems worldwide. What seemed like a catastrophe became India's opportunity, and ICIM/ICIL was perfectly positioned. With thousands of COBOL programmers and experience in legacy systems, the company won contracts from banks, insurance companies, and government agencies desperate to make their systems Y2K-compliant. Revenue soared. Margins expanded. The company hired aggressively, training fresh engineering graduates in assembly-line fashion.

One project manager from that era described the Y2K years as "controlled chaos": "We had engineers working in three shifts, conference calls with clients at all hours, code reviews happening around the clock. The Pune campus looked like a college hostel—people sleeping under desks, eating at their workstations. But we delivered. Every single project. On time."

As the millennium approached, leadership recognized that Y2K was both a blessing and a curse. It had brought revenue and recognition, but it had also branded Indian IT as backend-focused, doing work that Western companies didn't want to do themselves. The company needed a new identity for the new millennium.

On January 14, 2000—just two weeks after the Y2K non-event—the company unveiled its new identity: Zensar Technologies Limited. The name itself was carefully chosen. "Zen" suggested tranquility and wisdom, appealing to Western sensibilities. "Sar" came from Sanskrit, meaning essence or core, rooting the company in Indian heritage. Together, they represented the company's dual identity—globally facing yet proudly Indian.

The rebranding was more than cosmetic. Zensar positioned itself as a "solutions integrator," moving beyond staff augmentation to offer complete project ownership. The company invested in building vertical expertise—retail, manufacturing, insurance—rather than being a generalist. It established development centers with specialized capabilities, moving work offshore rather than sending people onsite. The goal was clear: compete on value, not just cost.

By late 2000, Zensar had completed its transformation from British computer manufacturer to Indian software services company. The journey had taken nearly four decades, through independence movements and economic liberalization, from mainframes to distributed computing, from products to services. The company had survived where others had perished, adapted where others had remained rigid.

But as the new millennium dawned, Zensar faced a new challenge. The Y2K windfall was ending. Competitors like Infosys and Wipro were growing exponentially, leveraging scale and brand recognition. Global technology giants were setting up their own Indian operations. The question was no longer whether an Indian company could succeed in global IT services—that had been proven. The question was whether a mid-sized player like Zensar could thrive in an industry increasingly dominated by giants. The answer would come from an unexpected source: Japan's technology establishment and one of India's most storied business houses.

IV. The Fujitsu Partnership & RPG Acquisition (2001-2007)

August 16, 2001, marked a pivotal moment in Zensar's history. While the world's attention was focused on the dot-com bust's aftermath, a quiet ceremony in Pune celebrated the merger of Zensar with Fujitsu ICIM Limited. The Japanese technology giant wasn't just bringing capital—it was bringing process discipline, quality frameworks, and access to marquee Japanese clients who had historically been wary of Indian IT vendors.

The merger's architect was Ganesh Natarajan, who had just been appointed CEO. Natarajan was an unusual choice—an IIT graduate who had spent years at Aptech, understanding both technology and education. His first all-hands meeting set the tone: "We're not going to be another Indian IT company. We're going to be a global company that happens to be headquartered in India." Employees remember his style as professorial yet demanding, combining strategic vision with obsessive attention to operational metrics.

Under Natarajan's leadership, Zensar embarked on what he called "the transformation trilogy": people, processes, and platforms. The people transformation meant hiring differently—not just engineers but domain experts, design thinkers, and relationship managers. The process transformation involved adopting Fujitsu's rigorous quality standards while maintaining Indian IT's flexibility. The platform transformation focused on building repeatable solutions rather than custom applications.

From 2000 to 2005, the company's strategic focus crystallized around application management services. This wasn't the glamorous work of new development but the steady, reliable work of keeping critical business systems running. One senior executive explained the logic: "Everyone wants to build the next big application. Few want to maintain it for the next decade. We saw opportunity in that gap."

The Fujitsu partnership brought unexpected benefits. Japanese clients, notorious for their exacting standards, became Zensar's finishing school. A project manager recalled working with a Japanese bank: "They would review our code line by line, question every design decision, demand documentation that was perfect down to the comma. It was exhausting but transformative. We learned that good enough wasn't good enough."

The relationship also brought cultural challenges. Japanese decision-making, consensus-driven and deliberate, clashed with Indian IT's entrepreneurial speed. Zensar employees joke about "the Tokyo test"—any major decision had to be explained in Tokyo, defended in Pune, and then re-explained in Tokyo. Yet this friction produced innovation. Zensar developed hybrid methodologies that combined Japanese quality with Indian agility, creating what they called "structured flexibility."

By 2006, cracks were appearing in the partnership. Fujitsu Services was planning its own India expansion, creating potential conflicts with Zensar's ambitions. The Japanese company needed full control of its Indian operations to compete with global rivals. Meanwhile, Zensar's management chafed at the constraints of being a subsidiary, unable to pursue acquisitions or enter new markets without lengthy approvals.

Enter the RPG Group, one of India's most respected business conglomerates. Founded by R.P. Goenka and led by his son Harsh Goenka, RPG had interests spanning from tyres to power but limited presence in technology. Harsh Goenka, known for his Twitter wit and business acumen, saw in Zensar an opportunity to enter the digital economy without building from scratch.

The 2007 acquisition negotiations were complex, involving multiple stakeholders across three continents. Fujitsu wanted a clean exit but also continuity for its clients. RPG wanted control but recognized the value of Zensar's independence. The management team, led by Natarajan, wanted assurance that Zensar wouldn't become just another division of a conglomerate. The final deal, valued at over $200 million, gave RPG controlling stake while ensuring Zensar maintained operational autonomy.

The ownership transition was remarkably smooth, defying predictions of cultural clash. Where Fujitsu had brought process discipline, RPG brought entrepreneurial freedom. Harsh Goenka's first board meeting set expectations: "I don't understand technology like you do. But I understand business. Show me the growth, and you'll have my support." This arms-length approach allowed Zensar's management to pursue aggressive expansion while having the backing of a stable, patient parent.

The RPG acquisition also brought unexpected synergies. The group's other businesses—CEAT tyres, KEC International, Harrisons Malayalam—became testing grounds for Zensar's solutions. These captive clients provided steady revenue and real-world validation. When Zensar claimed it could digitize manufacturing operations, it could point to CEAT's transformed factories. When it pitched infrastructure management, it showcased KEC's global project management systems.

By 2007's end, Zensar had successfully navigated ownership transition while maintaining business momentum. The company had grown to approximately 6,000 employees, with revenue approaching $200 million. It had development centers in Pune, Hyderabad, and Chennai, with sales offices across the United States, Europe, and Asia-Pacific. The Fujitsu years had brought discipline and credibility; the RPG acquisition promised growth and independence.

Yet as Natarajan and his team celebrated the successful transition, they were aware of a looming challenge. The global financial crisis was beginning to unfold, threatening IT budgets worldwide. Competitors were consolidating, creating scale advantages Zensar couldn't match. The company had survived ownership changes and market transitions, but its biggest test—establishing sustainable differentiation in an increasingly commoditized industry—lay ahead. The next phase would determine whether Zensar could break out of the mid-tier or remain perpetually in the shadow of larger rivals.

V. The Mid-Tier Plateau & Strategic Challenges (2008-2015)

The 2008 financial crisis hit Zensar's Pune headquarters like a delayed monsoon—everyone knew it was coming, but nobody was prepared for its intensity. Within weeks, three major American clients froze IT budgets, two European banks cancelled transformation projects, and the company's stock price halved. CFO S. Balasubramaniam recalled emergency board meetings: "We went from planning expansion to planning survival in a matter of days."

But the crisis revealed something more troubling than temporary revenue loss. Despite being founded in 1963, making it older than most Indian IT giants, Zensar had somehow remained stuck in the industry's middle tier. The numbers were sobering: while Infosys, founded in 1981, was approaching $5 billion in revenue, Zensar struggled to cross $300 million. The question haunting management wasn't about survival—it was about relevance.

Ganesh Natarajan, now five years into his CEO tenure, articulated the challenge with characteristic candor: "For the big IT deals, we weren't even invited. Clients would call TCS, Infosys, Wipro, maybe Cognizant. We weren't even on the radar. So the concern was: Where will future growth come from?" This wasn't false modesty—it was mathematical reality. In deals above $50 million, Zensar's win rate was less than 5%. In deals below $5 million, they faced competition from hundreds of smaller, hungrier companies.

By 2012, the company had approximately 11,000 employees servicing 400 clients in over 20 global locations, but the growth trajectory remained frustratingly flat. The company tried multiple strategies—vertical specialization, horizontal service expansion, geographic diversification—yet nothing delivered breakthrough growth. One senior executive likened it to "running on a treadmill—lots of motion, no movement."

The middle tier trap manifested in multiple ways. Zensar lacked the scale to invest in massive R&D initiatives or build proprietary platforms. It couldn't afford the army of pre-sales consultants that larger competitors deployed. Its brand recognition outside existing clients was minimal. Yet it was too large to be nimble like boutique firms, too established to take radical risks, too diversified to claim deep specialization.

Employee morale became a creeping concern. The company's Pune campus, once buzzing with Y2K energy, felt subdued. Talented engineers, seeing limited growth opportunities, left for competitors or startups. Campus recruitment became harder—why join Zensar when TCS offered brand prestige or startups offered stock options? The company found itself in a vicious cycle: limited growth meant limited opportunities, which meant talent exodus, which further constrained growth.

The client concentration problem was particularly acute. Zensar's top 10 clients contributed over 40% of revenue, creating vulnerability to account losses. When a major insurance client reduced spending in 2011, it wiped out an entire quarter's growth. The sales team scrambled to replace lost revenue, often accepting lower-margin projects just to maintain utilization rates. Quality suffered. Client satisfaction scores declined. The downward spiral seemed inexorable.

Geographic expansion offered false hope. Zensar opened offices in new markets—South Africa, Middle East, Latin America—but without local brand recognition or relationships, progress was glacial. The company's "follow the sun" delivery model, with development centers across time zones, was technically sound but commercially unclear. Clients appreciated 24-hour support but wouldn't pay premiums for it.

Innovation initiatives launched with fanfare but fizzled quietly. A cloud computing practice started in 2010 never achieved critical mass. A mobility center of excellence produced impressive demos but few commercial wins. Social media solutions, analytics platforms, digital marketing services—each consumed investment without generating returns. The pattern was consistent: good ideas, decent execution, inadequate scale.

The Oracle relationship exemplified both opportunity and limitation. Zensar had built strong Oracle expertise, becoming a platinum partner with hundreds of certified consultants. Yet Oracle's enterprise clients preferred working with larger integrators for mission-critical implementations. Zensar got the smaller projects, the support work, the staff augmentation—profitable but unglamorous, necessary but not transformational.

Industry analyst reports from this period paint a picture of competent mediocrity. Zensar appeared in quadrants but never as a leader. It received mentions but not recommendations. One Gartner report noted: "Zensar demonstrates solid delivery capabilities and client satisfaction but lacks the scale and investment capacity to compete for large transformational deals." The message was clear—good but not good enough.

By 2014, pressure was mounting from all directions. RPG Group, patient through the crisis years, wanted returns on its investment. Employees wanted career growth that the company couldn't provide. Clients wanted innovation that Zensar couldn't afford. The market wanted growth that seemed perpetually out of reach. Something had to change.

The irony wasn't lost on industry observers. Zensar Technologies sat in the third tier alongside Intellect Design, Newgen Software, Sonata Software, Birlasoft, and Happiest Minds, companies mostly younger but more focused. Zensar had survived every technology transition, every economic crisis, every ownership change—yet survival hadn't translated into success. The company closed fiscal 2016 with revenue of approximately $450 million, respectable but not remarkable, profitable but not growing, established but not essential.

As Natarajan prepared to step down after 15 years as CEO, he reflected on the journey: "We built a good company. The question is whether good is enough anymore." The answer would come from an unexpected source—private equity players who saw opportunity where others saw stagnation, and a new leadership team willing to challenge every assumption that had kept Zensar in the middle tier.

VI. The Apax Partnership & Digital Transformation (2015-Present)

October 2015 brought Mumbai's first hint of winter cool and Zensar's most significant strategic shift in a decade. APAX Partners, the global private equity giant, announced it was acquiring a 23.2% stake for ₹860 crores—not for control, but as a catalyst for transformation. The PE firm's India head explained their thesis: "We don't see a mid-tier IT company. We see a digital transformation player trapped in a legacy services body."

The APAX deal was structured unusually. Rather than a typical buyout, it was positioned as a "growth partnership" with specific transformation milestones. APAX brought more than capital—they brought Silicon Valley connections, European client relationships, and a playbook for digital disruption. Their first board presentation challenged everything: Why accept 10% margins when digital natives commanded 25%? Why compete on cost when you could compete on experience? Why remain a services company when you could build products?

The leadership transition in 2016 was carefully orchestrated. Ganesh Natarajan, after 15 years at the helm, passed the baton to Sandeep Kishore, an industry veteran with a remarkable resume—ex-McKinsey, former Cognizant executive, and most recently, head of sales at HCL Technologies. Kishore's appointment signaled intent: this wasn't about continuity but disruption. His first town hall was memorable: "We're going to become unrecognizable. Not because we're abandoning our heritage, but because we're finally fulfilling our potential."

Kishore's transformation strategy had three pillars: "digital first, experience-led, and platform-powered." Digital first meant no more legacy maintenance contracts unless they funded digital initiatives. Experience-led meant hiring designers, anthropologists, and behavioral scientists alongside engineers. Platform-powered meant building repeatable solutions rather than custom applications. The strategy was clear; execution would be brutal.

The company identified 12 key areas for 'tuck-in' acquisitions, each valued between $25-75 million—small enough to integrate quickly, large enough to matter. The acquisition strategy was surgical: buy capability, not capacity; expertise, not revenue; future, not past. The first major move came with Foolproof, a UK-based user experience agency with clients like Google and BBC. The price tag was modest, but the signal was powerful—Zensar was serious about design-led transformation. The acquisition spree accelerated: Cynosure Inc. for about $33 million in March, bringing deep Guidewire expertise for insurance clients. Indigo Slate for around $18 million, adding digital marketing muscle with revenues of approximately $20M in fiscal 2018. Each acquisition followed a pattern: buy expertise, integrate culture, leverage capabilities across the portfolio. Digital revenues were growing at a 30% CAGR and contributed to more than 38% of Zensar's fiscal 2018 revenue, one of the highest ratios in the industry.

The cultural transformation was equally dramatic. Zensar's Pune campus, once dominated by engineers in formal wear, now hosted design thinking workshops with post-it notes covering glass walls. The company hired from NIFT and Srishti, not just IITs. Friday demos showcased prototypes, not PowerPoints. Client visits included sessions with anthropologists discussing user behavior, not just architects reviewing system designs.

In December 2020, leadership transitioned again with Ajay S. Bhutoria taking over as CEO. Bhutoria brought a different energy—less Silicon Valley, more pragmatic execution. His focus was operational excellence: improving margins, increasing utilization, reducing debt. The transformation agenda continued but with greater financial discipline. The mantra shifted from "growth at any cost" to "profitable growth. "The most recent strategic move came in July 2024 with the acquisition of BridgeView Life Sciences for $25 million. Pune-headquartered IT company Zensar Technologies announced the acquisition of pharma and life sciences consulting firm BridgeView Lifesciences for a total deal value of $25 million. The company will make an aggregate upfront payment of $14 million subject to customary adjustments for working capital, debt and cash on closing, and an additional payment of up to $11 million by December 31, 2027, contingent on achievement of performance and employment continuity thresholds. This wasn't just another acquisition—it was a statement about Zensar's ambition to dominate specific verticals rather than compete broadly.

The transformation numbers tell a compelling story. Digital revenues now constitute a significant portion of total revenue, growing at rates that outpace traditional services. The company has moved from being a cost center for global enterprises to a strategic partner in their digital journeys. Client conversations have shifted from "How many resources can you provide?" to "How can you help us reimagine our business?"

Yet challenges remain. The APAX partnership, while transformative, hasn't delivered the explosive growth initially envisioned. Competition in digital services is fierce, with everyone from Accenture to boutique consultancies claiming similar capabilities. Talent retention in hot areas like AI and cloud remains difficult. The company's brand, while stronger, still lacks the recognition of larger peers.

As 2024 unfolds, Zensar stands at an interesting juncture. The digital transformation is real but incomplete. The acquisition strategy has added capability but also complexity. The financial performance is solid but not spectacular. The third tier includes Zensar Technologies, Intellect Design, Newgen Software, Sonata Software, Birlasoft, and Happiest Minds. Since October, only four companies — Persistent, Coforge, Zensar Technologies, and Intellect Design — have delivered positive returns. This relative outperformance suggests the market is beginning to recognize value in Zensar's transformation story.

The APAX years have fundamentally altered Zensar's trajectory. No longer content to be a traditional IT services provider, the company has repositioned itself as an experience-led engineering firm. Whether this positioning translates into sustained competitive advantage remains the central question. What's clear is that Zensar, after decades of patient evolution, has finally chosen disruption over continuity, growth over stability, transformation over tradition.

VII. Business Model & Portfolio Evolution

Walk into Zensar's Pune headquarters today, and you'll encounter a wall displaying the company's client logos—145 of them, ranging from Fortune 500 giants to emerging unicorns. But behind this impressive array lies a fundamental tension that has defined Zensar's business model evolution: How do you serve everyone without becoming nothing to anyone?

The company segments include Digital and Application Services (DAS) and Digital Foundation Services (DFS). It generates maximum revenue from the DAS segment. The DAS segment represents Zensar's future—custom application development, cloud migration, experience design, and digital transformation consulting. It's higher margin, intellectually challenging work that attracts top talent and commands premium pricing. The DFS segment—infrastructure management, application maintenance, testing—represents the company's heritage, providing steady cash flows but limited growth potential.

Geographically, the majority of its revenue comes from the Americas and the rest from Europe, and the rest of the world. The Americas dominance isn't just about market size; it reflects decades of relationship building, from early Y2K projects to current digital transformations. Yet this concentration creates vulnerability—American economic cycles disproportionately impact Zensar's performance, and currency fluctuations can devastate quarterly results.

The vertical strategy has been both blessing and curse. Zensar focuses on four key sectors: Hi-tech & manufacturing, consumer services, banking, financial services, and insurance (BFSI), and increasingly, healthcare and life sciences. Each vertical has dedicated teams, specialized solutions, and deep domain expertise. A Zensar consultant working with a manufacturing client understands shop floor operations, supply chain complexities, and Industry 4.0 implications—not just technology implementation.

The technology partnership ecosystem reveals Zensar's pragmatic approach to innovation. With 60+ technology partners including Oracle, Salesforce, SAP, Guidewire, Adobe, and UiPath, the company has chosen to be an integrator rather than inventor. One senior executive explained: "We could spend millions developing our own platforms and fail, or we could master the platforms our clients already use. The choice was obvious."

The Oracle relationship deserves special attention. Zensar has been an Oracle partner since the 1990s, accumulating certifications, developing accelerators, and building one of the industry's deepest Oracle practices. When a global retailer needed to migrate from on-premise Oracle systems to Oracle Cloud, Zensar won against larger competitors because they could demonstrate not just technical capability but decades of Oracle evolution understanding. They knew why certain customizations existed, which integrations were critical, what could be standardized versus what needed preservation.

The Guidewire expertise, strengthened through the Cynosure acquisition, has transformed Zensar's insurance vertical. Guidewire powers core systems for property and casualty insurers worldwide, and Zensar has become one of the few partners capable of end-to-end Guidewire implementation. A North American insurer's CTO remarked: "Most vendors know Guidewire technically. Zensar understands how underwriters actually use it."

The shift from labor arbitrage to experience-led engineering represents Zensar's most fundamental business model evolution. In the early 2000s, the value proposition was simple: Indian engineers at one-third the cost of Western counterparts. Today, with the Foolproof acquisition bringing design thinking capabilities and Indigo Slate adding digital marketing expertise, Zensar sells outcomes, not hours. A typical engagement now starts with anthropologists studying user behavior, designers creating prototypes, and engineers building solutions—a far cry from the staff augmentation model of yesteryear.

The company's approach to AI and automation illustrates this evolution. Rather than positioning AI as a job replacer, Zensar frames it as an augmenter. Their "AI-first" methodology doesn't mean replacing humans with machines but embedding intelligence into every solution. When a European bank wanted to automate loan processing, Zensar's solution combined RPA for data entry, machine learning for risk assessment, and human expertise for exception handling. The result: 70% reduction in processing time, not 70% reduction in workforce.

The platform strategy has yielded mixed results. Zensar has developed several proprietary solutions—ZenDART for data analytics, ZenSOC for security operations, ZenESG for sustainability reporting. These platforms showcase capability but haven't achieved significant commercial success. The challenge is scale: without thousands of implementations, platforms can't match the functionality of established competitors. Yet abandoning platform development means remaining forever in the services business, with its inherent limitations.

Client concentration remains a structural challenge. The top 10 clients contribute a significant portion of revenue, creating both stability and vulnerability. These relationships, some spanning decades, provide predictable revenue and deep domain knowledge. But they also limit pricing power and create dependency. When a major insurance client reduced IT spending in 2019, Zensar's quarterly results suffered immediately. Diversification efforts have had limited success—winning new large clients requires investments the company can't always afford.

The pricing evolution tells its own story. Zensar has experimented with various models—time and materials, fixed price, outcome-based, subscription. Each has trade-offs. Fixed price requires accurate estimation capabilities that remain elusive. Outcome-based pricing sounds attractive but requires risk appetite that mid-tier players often lack. The company increasingly favors hybrid models—fixed price for defined outcomes, time and materials for exploration, subscription for platform usage.

As the business model continues evolving, fundamental questions persist. Can Zensar achieve the scale needed for platform success? Will vertical specialization provide sufficient differentiation? Can experience-led engineering command premium pricing in a cost-conscious market? The answers will determine whether Zensar's business model evolution represents transformation or merely adaptation.

VIII. Financial Performance & Recent Trajectory

The numbers tell a story of resilience, not revolution. Zensar's financial trajectory over the past five years reads like a master class in managing mediocrity—profitable enough to survive, not growing fast enough to thrive. The company has delivered a poor sales growth of 4.78% over past five years. In an industry where double-digit growth is expected and 20%+ celebrated, this performance raises uncomfortable questions about strategic choices and execution capabilities. The Q2FY25 numbers provide a snapshot of current performance: revenue of $156.2M, sequential QoQ growth of 1.2% in reported currency. On a YoY basis, this translates to 4.0% growth in reported currency and 3.3% in constant currency. These aren't disaster numbers, but they're hardly the stuff of growth stories. The EBITDA stood at 15.4% of revenues, respectable for a services company but below the 20%+ margins that digital natives command.

What's particularly revealing is the variance across verticals. Banking and Financial Services reported a sequential QoQ revenue growth of 4.2% and quarterly YoY revenue growth of 14.0% in reported currency—a bright spot driven by digital transformation initiatives and the Guidewire expertise from Cynosure. Meanwhile, Telecommunication, Media and Technology reported a sequential QoQ revenue decline of 8.6% and quarterly YoY revenue decline of 14.4% in reported currency, reflecting the sector's broader challenges and Zensar's struggle to remain relevant in rapidly evolving technology markets.

The cash position tells a story of financial prudence if not ambition. DSO improved to 71 days, cash and cash equivalents of $255.0M. Company is almost debt free, a remarkable achievement in an industry where acquisitions often burden balance sheets. This financial strength provides optionality—the ability to weather downturns, make strategic acquisitions, or invest in new capabilities without dilution or distress.

Looking at Q3 FY2024-2025 results, revenue jumped 8.83% since last year same period to ₹1,356.30Cr. On a quarterly growth basis, Zensar Technologies Ltd has generated 0.53% jump in its revenue since last 3-months. However, profitability tells a different story: net profit fell -1.18% since last year same period to ₹159.80Cr. On a quarterly growth basis, Zensar Technologies Ltd has generated 2.63% jump in its net profits since last 3-months.

The margin compression is concerning. Net profit margin fell -9.2% since last year same period to 11.78% in the Q3 2024-2025. On a quarterly growth basis, Zensar Technologies Ltd has generated 2.09% jump in its net profit margins since last 3-months. This suggests pricing pressure, rising costs, or both—classic symptoms of mid-tier squeeze where you lack the scale for efficiency or the differentiation for premium pricing.

The order book provides some optimism. Our highest ever order book this quarter reflects the continued focus on client-centricity and commitment of our employees to drive value and innovations, noted CEO Manish Tandon. Yet order books in IT services can be misleading—large deals signed today might take quarters to ramp up, and cancellation clauses can make seemingly solid bookings evaporate.

The dividend policy reflects confidence or complacency, depending on perspective. Company has been maintaining a healthy dividend payout of 36.9%. For income investors, this consistency is attractive. For growth investors, it raises questions about capital allocation—why return cash when the business desperately needs scale?

The stock market's reaction has been mixed. While Since October, only four companies — Persistent, Coforge, Zensar Technologies, and Intellect Design — have delivered positive returns, suggesting relative outperformance, the absolute returns remain modest. The market seems to be saying: "We believe in the transformation story, but show us the growth."

Currency headwinds continue to impact reported numbers. The difference between constant currency and reported currency growth—often 50-100 basis points—might seem minor but compounds over time. For a company with significant dollar revenues and rupee costs, currency volatility adds another layer of complexity to an already challenging business model.

The financial trajectory raises fundamental questions about Zensar's strategy. Is slow, steady growth acceptable in a winner-take-all industry? Can the company afford to be patient when competitors are scaling rapidly through aggressive investments? Is financial conservatism a strength that will enable opportunistic moves, or a weakness that ensures perpetual mediocrity?

As fiscal 2025 progresses, the financial performance will be the ultimate arbiter of strategic success. The transformation initiatives, digital pivots, and acquisition strategies all sound compelling in boardroom presentations. But until they translate into sustained revenue growth, expanding margins, and market share gains, Zensar remains what the numbers say it is: a profitable, stable, slow-growing mid-tier IT services company searching for its breakthrough moment.

IX. Competitive Landscape & Market Position

The Indian IT services industry resembles a pyramid, and Zensar sits uncomfortably in its middle—too small to compete with the giants at the top, too large to match the agility of boutiques at the base. With 10,500+ workforce across 30+ global locations, the company occupies what strategists call "the valley of death"—that treacherous middle ground where you have all the costs of scale without its benefits.

India's top 20 IT companies (with market caps above $1 billion) have collectively lost nearly 15% of their value since October 2024. The sector's top tier — comprising TCS, Infosys, HCL Technologies, Wipro, L&T Mindtree, and Tech Mahindra — sits at the core. The second tier includes Persistent, Oracle Financial Services, Coforge, Mphasis, Tata Elxsi, and KPIT Technologies. The third tier includes Zensar Technologies, Intellect Design, Newgen Software, Sonata Software, Birlasoft, and Happiest Minds.

This tiering isn't just about size—it's about strategic options. Top-tier companies can bid for billion-dollar deals, invest hundreds of millions in R&D, and weather economic downturns through sheer diversification. Second-tier players often have specialized capabilities—Persistent in product engineering, Mphasis in banking technology—that command premium pricing. Third-tier companies like Zensar must find their own path, neither large enough for scale advantages nor specialized enough for niche premiums.

The competitive dynamics are brutal. When a Fortune 500 company issues an RFP for digital transformation, the shortlist is predictable: Accenture for strategy, TCS for scale, Infosys for innovation, maybe Cognizant for cost-effectiveness. Zensar might make the longlist but rarely the final cut. One sales executive described the frustration: "We'd spend months on proposals, demonstrate superior technical capability, offer competitive pricing, and still lose because the client wanted a 'safe' choice."

Yet there are advantages to Zensar's position. Unlike TCS with its 600,000+ employees, Zensar can pivot quickly. When blockchain emerged as a technology trend, Zensar had a practice team operational within months while larger competitors navigated layers of approval. When a mid-sized insurance company needs a partner, Zensar can offer CEO-level attention that would be impossible at Infosys. The company has learned to win where giants can't be bothered to compete.

The geographic distribution of competition adds complexity. In the United States, Zensar competes not just with Indian firms but with global system integrators like Capgemini and local boutiques like Slalom Consulting. In Europe, the competition includes nearshore providers from Eastern Europe offering similar cost advantages with better cultural alignment. In emerging markets, local champions often have government relationships that no amount of technical capability can overcome.

The specialization versus generalization debate defines Zensar's competitive challenge. Pure-play specialists—EPAM in product engineering, Endava in digital transformation, GlobalLogic in R&D services—command valuations multiples higher than Zensar's. Yet specialization requires saying no to opportunities, something mid-tier companies struggling for growth find difficult. Zensar has chosen a hybrid approach—broad capabilities with pockets of deep expertise—that satisfies neither investors seeking focus nor clients seeking specialization.

Mid-cap players are driving industry growth, with the six mid-cap IT companies grew at 59.6% and the six small-cap firms grew at 51.9% compared to the top six IT majors grew at only 30.3%. This suggests the industry's growth dynamics are shifting, creating opportunities for companies like Zensar if they can execute effectively.

The partnership ecosystem reveals competitive positioning. While Zensar has 60+ technology partnerships, the depth varies significantly. TCS has thousands of SAP consultants; Zensar has hundreds. Infosys co-innovates with Microsoft; Zensar implements Microsoft solutions. The difference between strategic partner and implementation vendor is subtle but significant—it determines who gets called for transformation versus who gets called for staff augmentation.

Private equity ownership adds another dimension. While competitors like Wipro and Infosys are widely held public companies with quarterly earnings pressure, Zensar benefits from RPG's patient capital and APAX's transformation expertise. This should theoretically enable longer-term thinking and bolder bets. In practice, the advantages are less clear—private equity brings its own pressures for returns, and family ownership can mean conservatism as easily as entrepreneurship.

The talent war exemplifies competitive challenges. When Zensar recruits from IITs, it competes with the same companies for the same candidates but with different propositions. TCS offers brand prestige and global exposure. Startups offer stock options and cutting-edge technology. Zensar offers... what exactly? The pitch has evolved from "good work-life balance" (code for less demanding) to "entrepreneurial opportunity within stability" (code for smaller company within a large group). It works for some but not enough.

Client concentration patterns reveal competitive vulnerabilities. While Zensar serves 145+ clients, the revenue concentration suggests deep relationships with few rather than broad relationships with many. When a competitor targets a top Zensar account, they can afford to underprice, over-deliver, and wait—knowing that winning even one major account significantly damages Zensar's growth trajectory. Defense becomes as important as offense.

The innovation narrative shows both progress and gaps. Zensar talks about AI, automation, and digital transformation—but so does everyone else. The company has filed few patents, built no breakthrough platforms, created no industry standards. Innovation happens at the project level—clever solutions for specific clients—rather than the company level. This tactical innovation helps win deals but doesn't change competitive positioning.

Price competition remains relentless. Indian IT's original arbitrage—skilled engineers at lower costs—has eroded as salaries rise and competitors from Philippines, Eastern Europe, and Latin America emerge. Zensar can't match the pricing of offshore-only providers or the value proposition of onshore specialists. The company occupies an uncomfortable middle ground—not cheap enough for cost-focused buyers, not premium enough for value-focused ones.

As competition intensifies, Zensar's market position becomes increasingly precarious. The company must choose: Scale up to compete with larger players, specialize to compete with boutiques, or find a third way that leverages its unique characteristics. The current strategy—trying to be everything to everyone while being nothing to no one—is unsustainable. The market is forcing a choice that Zensar has avoided for decades.

X. Playbook: Lessons from the Mid-Tier

After six decades of evolution, multiple ownership changes, and countless strategic pivots, Zensar Technologies has inadvertently written the playbook for mid-tier survival in a scale-obsessed industry. These aren't lessons from triumph but from tenacity—how to endure when you can't dominate, how to matter when you can't lead, how to profit when you can't price.

Lesson 1: Patient Capital Is Oxygen, Not Luxury

The RPG Group's ownership since 2007 demonstrates the value of patient capital. Unlike publicly traded competitors facing quarterly earnings pressure or PE-owned peers dealing with exit timelines, Zensar has had the luxury of thinking in years, not quarters. When digital transformation investments took time to pay off, when acquisitions needed integration, when new practices required cultivation, RPG provided breathing room. The lesson: In industries with long sales cycles and longer transformation cycles, patient capital isn't just helpful—it's essential.

Lesson 2: Cultural Arbitrage Beats Cost Arbitrage

While larger competitors pursued pure labor arbitrage—moving work to the lowest-cost location—Zensar learned to arbitrage culture. The Fujitsu years taught Japanese quality standards. The Foolproof acquisition brought British design thinking. The BridgeView deal added American healthcare expertise. By becoming culturally multilingual, Zensar could serve Japanese banks requiring precision, British retailers demanding creativity, and American insurers needing compliance. The premium for cultural fit often exceeds the discount for smaller scale.

Lesson 3: Complexity Is Both Burden and Moat

Managing multiple verticals, technologies, and geographies creates operational complexity that constrains margins and slows decision-making. Yet this same complexity becomes a competitive moat. When a client needs Oracle expertise for their ERP, Salesforce for CRM, and AWS for infrastructure—all integrated with legacy mainframes—Zensar's broad capability set becomes valuable. Larger competitors might have deeper expertise in each area but struggle with integration. Smaller competitors lack the breadth entirely. Complexity, properly managed, becomes differentiation.

Lesson 4: Strategic Schizophrenia Can Be Strategic

Zensar has simultaneously pursued contradictory strategies—seeking scale while maintaining boutique client attention, expanding globally while strengthening local presence, standardizing delivery while customizing solutions. Traditional strategy would call this lack of focus. But in the messy middle of the market, this schizophrenia enables flexibility. When a client wants global delivery, Zensar emphasizes its international presence. When they want local partnership, Zensar highlights its regional offices. The ability to shapeshift based on client needs compensates for lack of clear positioning.

Lesson 5: Acquisition Integration Determines Value Creation

The difference between successful acquisitions (Cynosure, BridgeView) and struggling ones lies not in price paid or strategic fit but in integration approach. Zensar learned to maintain acquired companies' entrepreneurial spirit while leveraging parent company resources. Cynosure kept its Guidewire expertise and client relationships while gaining Zensar's delivery scale. Foolproof retained its design culture while accessing Zensar's engineering capability. The playbook: Buy capability, not capacity; preserve culture, not just talent; integrate operations, not organizations.

Lesson 6: The Middle Market Is Underserved and Undervalued

While everyone chases Fortune 500 accounts, Zensar discovered profitable opportunities in the Fortune 5000. Mid-sized companies need digital transformation but can't afford Accenture. They require global capability but want personal attention. They value relationships over credentials, flexibility over frameworks, pragmatism over PowerPoints. By focusing on the "forgotten middle," Zensar found clients who valued what it offered rather than lamenting what it lacked.

Lesson 7: Vertical Expertise Compensates for Horizontal Limitations

Unable to compete broadly, Zensar went deep in select verticals. In insurance, the company understands not just technology but underwriting, claims processing, regulatory compliance. In manufacturing, they know shop floor operations, supply chain complexity, quality systems. This domain depth enables value-based conversations that pure technology providers can't match. The lesson: When you can't be everything to everyone, be everything to someone.

Lesson 8: Timing Transformations Matters More Than Attempting Them

Zensar's history is littered with transformations—from hardware to software, from products to services, from onsite to offshore, from services to digital. Most companies attempt transformation; few time it right. Zensar's Y2K pivot succeeded because the market was ready. The digital transformation is gaining traction because clients finally understand its necessity. The lesson: Being early is often as bad as being late. Time transformations to market readiness, not market rhetoric.

Lesson 9: Managing Stakeholder Expectations Is Survival

With RPG Group as majority owner, APAX as strategic investor, public market minorities, employees across continents, and clients spanning industries, Zensar manages competing expectations daily. The playbook involves careful communication—growth story for investors, stability narrative for employees, innovation messaging for clients, independence assertion for partners. This stakeholder juggling act, exhausting as it is, becomes a core competency for mid-tier companies lacking the luxury of single-minded focus.

Lesson 10: Embrace the Paradox of Being "Good Enough"

Zensar will never have TCS's scale, Infosys's brand, or Accenture's pricing power. But for many clients, many projects, many situations, Zensar is good enough. Good enough capability at better pricing. Good enough scale with better attention. Good enough innovation with better execution. In a world obsessed with being the best, there's profitable space for being good enough. The challenge is embracing this reality without accepting mediocrity.

These lessons don't guarantee success—Zensar's modest growth demonstrates that. But they enable survival in an industry where most mid-tier players either scale up, sell out, or shut down. The playbook isn't about winning; it's about enduring. And sometimes, in industries with long cycles and longer memories, endurance becomes its own form of victory.

XI. Bear vs. Bull Analysis

The Bear Case: Trapped in Perpetual Mediocrity

The pessimist's view of Zensar starts with a simple, damning statistic: The company has delivered a poor sales growth of 4.78% over past five years. In an industry where double-digit growth is table stakes and 20%+ gets you noticed, this performance is not just disappointing—it's existential. The bear case isn't about failure; it's about irrelevance.

Start with the structural disadvantages. At roughly $630 million in revenue, Zensar lacks the scale to compete for mega-deals that drive step-function growth. When a global bank wants to transform its technology infrastructure—a potential $500 million engagement—Zensar isn't even invited to bid. The company lacks the balance sheet strength to take on transformation risk, the delivery capacity to handle massive concurrent projects, and the brand credibility to be trusted with mission-critical transformations.

The talent challenge compounds over time. Why would a top-tier AI researcher join Zensar over Google? Why would a digital transformation expert choose Zensar over Accenture? The company becomes a training ground where people build skills before moving to better-paying, more prestigious competitors. This talent drain creates a vicious cycle: limited expertise limits winning deals, which limits growth, which limits ability to attract talent.

Client concentration remains alarming despite decades of diversification efforts. The top clients still contribute disproportionately to revenue, creating vulnerability that manifests in volatile quarterly results. When a single client's budget cut can erase a quarter's growth, when a contract loss can trigger layoffs, when a project delay can miss earnings—the business model lacks resilience.

The margin trajectory tells its own troubling story. Net profit margin fell -9.2% since last year same period to 11.78% in the Q3 2024-2025. This isn't just quarterly variation; it's structural pressure. As digital transformation work becomes commoditized, as automation reduces billable hours, as clients demand more for less, margins compress inexorably. The company lacks the pricing power to push back or the efficiency to absorb pressure.

Geographic concentration in the Americas exposes Zensar to economic cycles, regulatory changes, and currency fluctuations beyond its control. When U.S. companies tighten IT spending, when H-1B visa restrictions limit mobility, when dollar weakens against rupee—Zensar suffers disproportionately. Diversification efforts in Europe and Asia have yielded marginal revenue, not meaningful risk reduction.

The innovation deficit is glaring. While competitors file patents, build platforms, and create intellectual property, Zensar remains a services company selling time and materials. The acquisitions—Foolproof, Cynosure, BridgeView—add capability but not breakthrough innovation. The company talks about AI and automation but implements others' innovations rather than creating its own.

Competition intensifies from all directions. Global giants leverage scale and brand. Indian peers grow faster with similar cost structures. Boutique specialists command premium pricing with deeper expertise. New-age digital natives born in the cloud era lack legacy infrastructure burden. Zensar competes with everyone while differentiating from no one.

The parent company relationship, while providing stability, may also constrain ambition. RPG Group's diversified portfolio means Zensar is one business among many, not the crown jewel deserving unlimited investment. The conservative approach that ensured survival may prevent the bold bets required for breakthrough growth.

Market dynamics favor consolidation, and Zensar lacks the currency to be an acquirer or the scale to avoid being acquired. As the industry consolidates into mega-providers and specialized boutiques, mid-tier players face existential pressure. Zensar might survive as an independent entity, but survival and success are different outcomes.

The Bull Case: Coiled Spring Ready to Unleash

The optimist's view of Zensar sees not stagnation but preparation, not weakness but untapped potential. Start with the foundation: Company is almost debt free with cash and cash equivalents of $255.0M. This financial strength provides optionality—to acquire, invest, or weather downturns—that leveraged competitors lack.

The RPG parentage provides unappreciated stability. While competitors face quarterly earnings pressure or private equity exit deadlines, Zensar can think long-term. Harsh Goenka's commitment to the business, evidenced by continued investment despite modest returns, suggests patience that could enable transformation where others would demand immediate results.

The acquisition strategy is bearing fruit. Digital revenues have been growing at a 30% CAGR for Zensar and contributed to more than 38% of Zensar's fiscal 2018 revenue. Each acquisition—Foolproof for design, Cynosure for Guidewire, BridgeView for life sciences—adds specific capability that enhances win rates in targeted segments. The whole is becoming greater than the sum of parts.

Our highest ever order book this quarter suggests momentum building beneath tepid reported growth. Order books in IT services are leading indicators; today's bookings become tomorrow's revenue. If execution improves and deal conversion accelerates, the growth trajectory could inflect positively.

The vertical focus in insurance and healthcare positions Zensar in industries undergoing massive transformation. Insurance companies must digitize to survive. Healthcare providers need technology to manage costs and improve outcomes. Zensar's domain expertise in these sectors, strengthened through acquisitions, positions it to capture disproportionate share of this transformation spending.

Since October, only four companies — Persistent, Coforge, Zensar Technologies, and Intellect Design — have delivered positive returns. This relative outperformance suggests the market is beginning to recognize value that metrics don't yet reflect. Smart money might be positioning before transformation becomes obvious.

The mid-tier positioning, traditionally a disadvantage, could become an advantage as clients seek alternatives to expensive global integrators and unproven boutiques. Zensar offers the sweet spot—enough scale for complex projects, enough agility for customization, enough stability for long-term partnership. The "good enough at better value" proposition resonates in cost-conscious times.

Technology shifts create opportunity for disruption. As cloud becomes standard, as AI democratizes, as low-code platforms reduce development complexity, traditional scale advantages erode. Smaller, agile players can compete where previously only giants could play. Zensar's breadth of capability positions it to capitalize on these shifts.

The management team under Manish Tandon brings fresh energy and proven execution. Their focus on operational excellence, margin improvement, and customer satisfaction suggests professional management replacing founder syndrome. If they can maintain momentum while accelerating growth, the transformation could surprise skeptics.

Valuation provides margin of safety. Trading at modest multiples relative to peers, Zensar doesn't need perfection for appreciation. Modest improvement in growth rates, margin expansion, or multiple re-rating could drive significant returns. The risk-reward appears asymmetric—limited downside with meaningful upside potential.

The Verdict: A Question of Time Horizons

The bear and bull cases aren't mutually exclusive—they're different time horizons. Near-term, the bears are right: growth remains anemic, competition intensifies, structural challenges persist. Long-term, the bulls might prevail: financial strength enables patience, vertical expertise drives differentiation, transformation eventually manifests.

For investors, the question isn't whether Zensar is good or bad, but whether it's appropriate for their objectives. Income investors might appreciate the stability and dividends. Growth investors will find better opportunities elsewhere. Value investors might see unrecognized potential. Momentum investors should look away.

The ultimate arbiter will be execution. Every mid-tier IT services company talks transformation. Few achieve it. Zensar has the ingredients—capital, capability, captive market. Whether management can combine them into breakthrough growth remains the central uncertainty. The next 24 months will likely determine whether Zensar breaks out of the middle tier or remains trapped within it.

XII. Looking Forward & Strategic Options

Standing at the threshold of 2025, Zensar Technologies faces strategic choices that will determine whether its seventh decade brings breakthrough or more of the same. The path to $1 billion revenue—that psychological barrier separating mid-tier from meaningful—requires more than incremental improvement. It demands strategic courage that the company has historically lacked.

The Billion-Dollar Question

At current growth rates, Zensar will reach $1 billion revenue sometime in the 2030s—too late to matter in an industry where scale advantages compound daily. The math is unforgiving: achieving this milestone by 2027 requires 20%+ annual growth, by 2030 needs 15%+. Neither is achievable through organic expansion alone. The company must choose between three paths: aggressive acquisition, transformational pivot, or strategic combination.

The acquisition path would require deploying the war chest more boldly. Instead of $25-50 million tuck-in acquisitions, Zensar needs $100-200 million transformational deals. Acquiring a European digital consultancy would provide geographic diversification and higher-margin revenue. Buying a specialized cloud migration firm would add capability and capacity. The risk: integration complexity could overwhelm management bandwidth, and cultural clashes could destroy value rather than create it.

AI and Automation: Threat or Opportunity?

The AI revolution presents existential questions for companies like Zensar. If AI can write code, design systems, and manage infrastructure, what happens to IT services companies selling human expertise? The bear case sees margin compression and revenue decline as clients need fewer consultants. The bull case envisions Zensar as an AI implementation partner, helping clients navigate complexity they can't handle alone.

Zensar's approach must be pragmatic rather than visionary. The company lacks resources to develop proprietary AI platforms but can excel at practical implementation. When a manufacturer wants to use AI for quality control, when an insurer needs machine learning for claims processing, when a retailer requires recommendation engines—Zensar could be the partner that makes it work. The key is positioning as an AI enabler, not an AI creator.

The Platform Imperative

Services companies trade at 1-2x revenue multiples; platform companies command 5-10x. This valuation gap drives every IT services company to claim platform capability, but few successfully transition. Zensar's platform attempts have been modest—point solutions rather than transformational offerings. The strategic question: double down or abandon the platform dream?

The pragmatic approach might be partnering rather than building. Instead of creating another analytics platform, become the best implementer of existing platforms. Instead of developing proprietary solutions, co-create with clients and technology partners. This "platform-enabled services" positioning captures some platform premium without platform investment.

Geographic Expansion vs. Vertical Depth

Zensar faces a classic strategy dilemma: go broader or go deeper? Geographic expansion into high-growth markets like Middle East or Latin America offers new revenue pools but requires investment and involves risk. Vertical depth in existing strengths like insurance and healthcare provides differentiation but limits addressable market.

The answer might be selective expansion. Follow existing clients into new geographies rather than prospecting cold. Deepen vertical expertise in markets where Zensar already has presence. This "land and expand" strategy leverages existing relationships while managing risk.

The Partnership Play

Strategic partnerships could accelerate growth without acquisition cost. Deeper relationships with hyperscalers like AWS or Azure could drive cloud transformation revenue. Exclusive partnerships with emerging technology providers could provide differentiation. Joint ventures with local players in new markets could enable expansion without infrastructure investment.

The recent BridgeView acquisition strengthened Zensar's partnership with Veeva Systems. Similar moves—acquiring partners of strategic technology providers—could create defensible niches. When Veeva needs implementation partners, Zensar becomes the default choice. Replicate this model across multiple technologies and verticals, and sustainable differentiation emerges.

Capital Structure Optimization

Company is almost debt free—a conservative position that might be too conservative. Modest leverage could fund transformational acquisitions without dilution. The strong cash generation and stable parent company support could easily service debt. The question is whether management has the risk appetite to leverage the balance sheet for growth.

Alternatively, Zensar could pursue strategic investors beyond APAX. Bringing in a technology-focused private equity firm or strategic corporate investor could provide not just capital but capability. Imagine if Microsoft or Salesforce took a stake—suddenly Zensar gains credibility, access, and opportunity that money alone can't buy.

The Nuclear Option: Strategic Combination

The most dramatic option is also the most likely: strategic combination with a peer. Merging with another mid-tier player could create scale advantages neither possesses alone. Combining with a specialized boutique could add differentiation. Being acquired by a larger player could provide resources for breakthrough growth.

The RPG Group's commitment complicates but doesn't preclude strategic combinations. A merger of equals where RPG remains significant shareholder could work. A reverse merger where Zensar acquires a larger entity could maintain independence while achieving scale. The key is finding a partner where one plus one equals three, not one and a half.

Key Metrics to Watch

Investors monitoring Zensar's strategic evolution should focus on several indicators: - Digital revenue percentage: Must exceed 50% to claim transformation - Revenue per employee: Should increase as work moves up the value chain - Client concentration: Top 10 clients should contribute less than 30% - Geographic mix: Americas dependence should decrease below 60% - Margin trajectory: EBITDA margins should expand toward 18-20% - Organic growth: Must exceed 10% to demonstrate momentum

The Time Horizon Reality

Strategic transformation takes time—typically 3-5 years from initiation to results. Zensar is perhaps 2-3 years into its journey, suggesting another 2-3 years before transformation fully manifests. Investors must decide whether they have the patience to wait and the confidence that management can execute.

The optimistic scenario sees Zensar in 2030 as a $1.5 billion revenue company with 20%+ margins, recognized leadership in insurance and healthcare technology, and strategic partnerships that provide differentiation. The pessimistic scenario sees continued muddling through—profitable but uninspiring, surviving but not thriving.

The realistic scenario likely lies between: moderate growth acceleration to 8-10% annually, gradual margin expansion through automation, successful integration of recent acquisitions, and eventual strategic combination that provides scale breakthrough. Not the stuff of case studies, but perhaps enough for patient investors who understand that in the marathon of IT services, tortoise strategies sometimes beat hare ambitions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube