WABAG: The Story of India's Water Technology Pioneer

I. Introduction & Episode Roadmap

Picture this: A German water filtration company founded in 1924, changing hands through wars and corporate acquisitions, eventually landing in the portfolio of Austrian conglomerate VA Technologie. Its Indian subsidiary, a modest operation with 180 employees in Chennai, seemed destined to remain a small cog in a European engineering empire. Yet today, that same Indian entity commands a market capitalization of ₹9,492 crores, has executed over 6,500 projects across 25 countries, and serves 88 million people with clean water. The plot twist? The subsidiary didn't just break free—it turned around and swallowed its parent whole.

This is the improbable story of VA Tech Wabag Limited, a company that embodies the audacity of emerging market entrepreneurship. From a management buyout orchestrated with venture capital backing to a reverse acquisition that stunned the infrastructure world, Wabag's journey reads like a business school case study written by thriller novelists. How does a filtration technology born in Weimar-era Germany become India's water technology champion? How did four Indian executives convince ICICI Venture to help them buy out their employer, then use the acquired entity to purchase their former Austrian parent from Siemens?

The numbers tell one story: design, supply, installation, and operational management of drinking water treatment plants, wastewater facilities, industrial water systems, and desalination projects. The reality tells another: a masterclass in value creation through strategic audacity, technological accumulation, and the transformation of a cyclical EPC business into a solutions powerhouse.

Our journey spans from the cobblestones of Breslau (now Wrocław, Poland) to the boardrooms of Chennai, through the corridors of Siemens' Vienna offices to the trading floors of the NSE. We'll dissect the management buyout that started it all, the reverse acquisition that shocked the industry, and the public market story that followed. Along the way, we'll uncover how a company navigates the intersection of emerging market dynamism and developed market technology, and what it means to build critical infrastructure in an era of accelerating water scarcity.

II. Origins: From German Engineering to Indian Ambitions

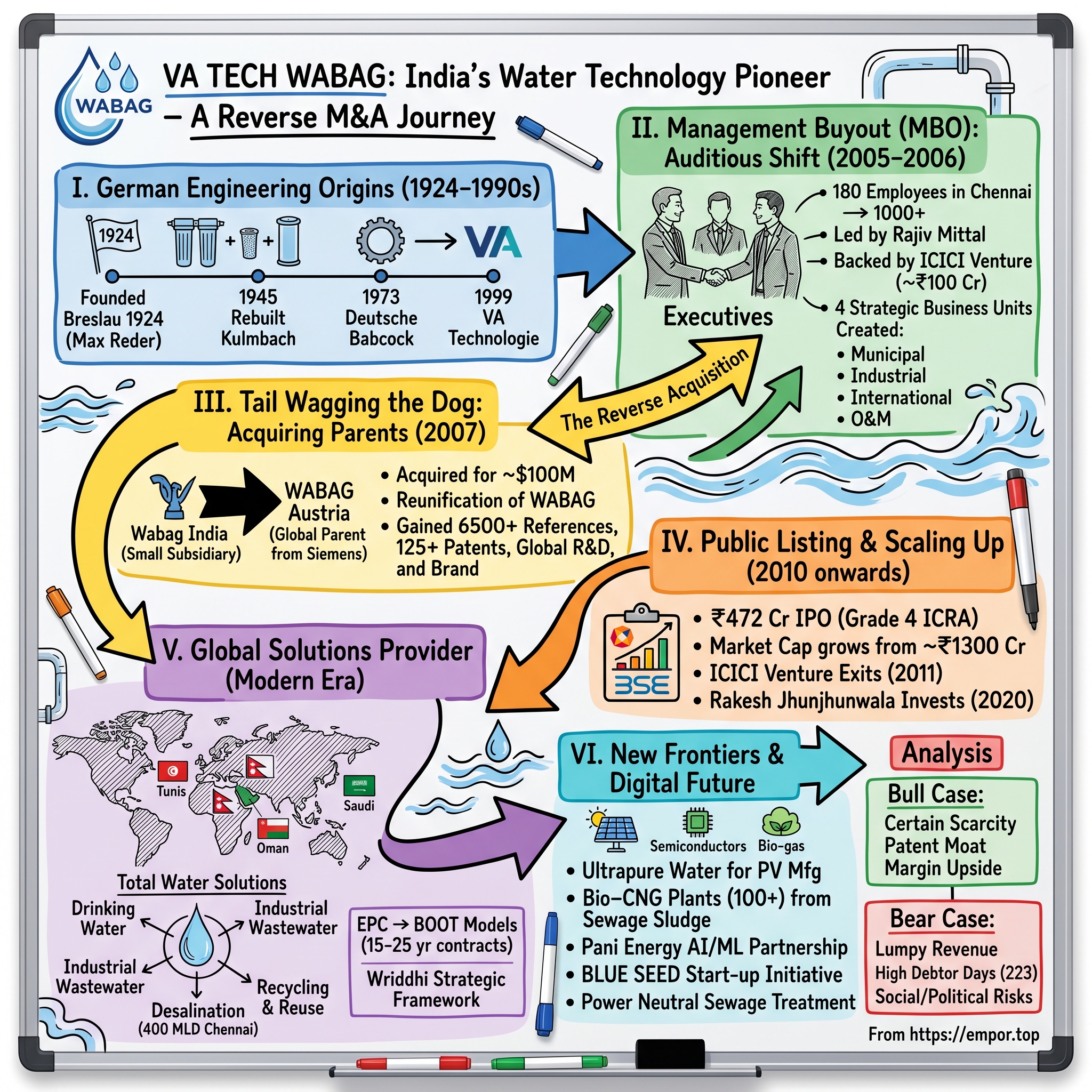

The year is 1924. In the industrial heartland of Breslau—then part of the German Empire, now Polish Wrocław—an entrepreneur named Max Reder sees opportunity where others see only pipes and filters. On August 1, 1924, Reder founds WABAG Wasserreinigungsbau GmbH with a focused mission: "the creation of facilities for the treatment of water unsuitable in its raw state for drinking or industrial use." It's an unglamorous business in an era of coal and steel, yet Reder understands something fundamental: civilization runs on clean water.

A year later, in 1925, a young engineer named Alfred Kretzschmar joins WABAG, quickly rising to chief engineer and authorized signatory. Together, Reder and Kretzschmar begin transforming water filtration from craft to science. They develop the WABAG filter nozzle, unveil the WABAG gravel filter at Munich's 1926 Brewery Exhibition, and achieve what amounts to a monopoly in large-scale filter plant construction. By 1934, they're pioneering rapid filtration systems—technology that would define municipal water treatment for decades.

The company grows steadily through the 1930s, reaching 100 employees by 1939. Then comes the war. In early 1945, during the battles for Breslau, WABAG's buildings and workshops are completely destroyed. Max Reder disappears, presumed dead. The original WABAG, it seems, has perished with the Third Reich.

But Alfred Kretzschmar survives. In June 1945, just weeks after Germany's surrender, he begins rebuilding the company in Kulmbach, Bavaria, on land allocated by the American military government, starting with repairs to bombed water treatment facilities. By 1949, he's back to 40 employees. The post-war reconstruction boom becomes WABAG's renaissance: drinking water plants in Karachi and Lahore in 1954, expansion across Africa, Eastern Europe, and South America through the 1960s.

The company's ownership journey reads like a chronicle of German industrial consolidation. Deutsche Babcock becomes majority shareholder in 1973 and eventually takes full control. But the real transformation comes from an unexpected direction: Austria. In 1999, VA Technologie—itself a spinoff from the steel giant VOEST Alpine—acquires the Wabag Group from Deutsche Babcock, creating VA Tech Wabag GmbH within its Austrian Energy & Environment division.

Meanwhile, 4,000 miles away in India, a different story unfolds. The entity that would become VA Tech Wabag Limited begins life in 1995 as "Balcke Dürr Cooling Towers Limited"—about as far from its eventual destiny as imaginable. Through a series of name changes—first to Balcke Dürr and Wabag Technologies Limited, then to VA Tech Wabag Limited in 1999—the company evolves from cooling towers to water treatment. In 2000, after the Madras High Court approves separating water operations from other businesses, VA Tech Wabag Ltd. is formally established.

At this point, the Indian operation is a small outpost of Austrian engineering excellence: competent, steady, unremarkable. It has the backing of a serious parent company with decades of water treatment expertise and over 120 patents. It serves Indian municipalities and industries with proven German-Austrian technology. A perfectly respectable subsidiary business.

But in Chennai, a group of Indian executives led by Rajiv Mittal see something different. They don't see a branch office—they see the foundation of something much larger. The stage is set for one of the most audacious management buyouts in emerging market history.

III. The Management Buyout: David vs Goliath

July 14, 2005. The European Commission approves Siemens AG Österreich's acquisition of VA Technologie AG for approximately one billion euros. For Siemens, it's a strategic move to strengthen its Eastern European presence. For the 180-odd employees of VA Tech Wabag's Indian subsidiary in Chennai, it looks like another change in distant ownership—from Austrian engineering conglomerate to German industrial giant.

But Rajiv Mittal, who had been deputed from WABAG UK to India in 1996 to set up the water business unit, sees an opportunity hidden in corporate complexity. Siemens faces antitrust concerns and must divest certain VA Tech assets. The water business, while valuable, isn't core to Siemens' strategic vision. For a management team with the right backing, this creates a once-in-a-lifetime window.

Mittal assembles his core team: Amit Sengupta, Shiv Narayan Saraf, and S. Varadarajan—executives who understand both the Indian water market's potential and the value of WABAG's technology heritage. They approach ICICI Venture, one of India's leading private equity funds, with an audacious proposition: help us buy out our employer.

In August 2006, the management buyout is completed for approximately ₹100 crores, with Rajiv Mittal, S Varadarajan, Amit Sengupta, and Shiv Narayan Saraf, backed by ICICI Ventures, taking the majority stake in the company. ICICI Ventures holds 65 percent of the equity, providing not just capital but credibility—this isn't a leveraged buyout driven by financial engineering, but a strategic bet on Indian entrepreneurship and market opportunity.

The transformation begins immediately. When the management buyout occurred in September 2005, the WABAG India team size was around 180+ people—by the time of the IPO five years later, it would exceed 1,000, eventually reaching over 2,000 water professionals. This isn't just headcount growth; it's capability building on an industrial scale.

In April 2007, less than a year after the buyout, the new management creates four strategic business units: municipal, industrial, international, and operations business group. The structure reveals the ambition—this isn't going to remain a local player serving Indian municipalities. The international SBU signals intent to compete globally, while the operations group represents a shift from pure EPC (engineering, procurement, construction) to ongoing service relationships.

The management buyout becomes the first ever in corporate history in the water industry—a distinction that matters less for bragging rights than for what it signals about emerging market dynamism. Here's an Indian management team, backed by local venture capital, taking control of a business with nearly a century of German-Austrian technological heritage. It's a reversal of the traditional technology transfer narrative.

But Mittal and his team aren't done. The management buyout was just the opening move in a larger strategic game. They now control the Indian operations, but the real prize—the technology, the patents, the global reference projects—still sits with the Austrian parent company, now owned by Siemens. What happens next will stun the infrastructure world and rewrite the rules of emerging market M&A.

IV. The Reverse Acquisition: Tail Wagging the Dog

Late 2007. The boardrooms of Siemens in Vienna are processing what must seem like an improbable request. The Indian subsidiary they acquired just two years ago as part of the billion-euro VA Technologie deal now wants to buy the entire global water business—the Austrian parent company, the European subsidiaries, the technology portfolio, everything. The subsidiary buying the parent? In the infrastructure world, this simply doesn't happen.

But Rajiv Mittal and his team have assembled the pieces carefully. The management group that had bought out the Chennai-based VA Tech India in 2005 now moves to acquire the erstwhile Austrian parent from Siemens for about $100 million in 2007. For Siemens, still digesting the massive VA Technologie acquisition and facing antitrust pressures, the water business represents a non-core asset. For the Indian management team, it represents the crown jewels.

On November 6, 2007, the company through their wholly owned subsidiary Wabag Singapore acquired the entire shareholding of Wabag Austria, making Wabag Austria and their subsidiaries into subsidiary companies. The structure is elegant: VA Tech Wabag Limited uses its Singapore subsidiary as the acquisition vehicle, maintaining clean corporate lines while executing one of the most audacious reverse acquisitions in infrastructure history.

The strategic rationale goes beyond mere corporate maneuvering. As Mittal would later explain, their mantra was "Reunification of WABAG"—they didn't want to give the feeling of acquisition by an Indian company. This wasn't about national pride but business pragmatism. The acquisition brought with it 6,500+ plant references spanning nearly a century, 125+ patents representing decades of R&D investment, established R&D centers in Europe, developed market relationships, and experienced talent who understood water treatment at the molecular level.

Consider what the Indian entity gains overnight: subsidiaries in Austria, Czech Republic, Romania, and other European markets; technology portfolios covering everything from membrane bioreactors to advanced oxidation processes; reference projects that include some of Europe's most sophisticated water treatment facilities; and crucially, the WABAG brand itself—a name that carries weight from Munich to Manila.

The cultural integration challenges are immense. German and Austrian engineers who've spent careers in the hierarchical world of European industrial conglomerates suddenly report to Chennai. The Indian team, meanwhile, must prove they can manage not just local municipal contracts but complex international operations spanning multiple time zones, languages, and regulatory regimes.

Yet the presence of ICICI Venture as a shareholder proves crucial. This isn't perceived as Indian nationalism but as venture-backed entrepreneurship—a language that translates across borders. The strong vision articulated by Mittal's team—becoming a global water solutions leader based out of emerging markets—provides the narrative framework that helps integrate disparate operations.

The post-acquisition growth validates the strategy. The management team that carried out the buyout in 2005 formed 4 Strategic Business Units in 2007 and played a key role in the reverse acquisition of the erstwhile parent Company in Austria in 2007. The Indian organization grows 6x in five years following the acquisition, transforming from a subsidiary executing projects to a total water solution provider—a competency none of the other subsidiaries within the WABAG Group possessed at that time.

The reverse acquisition rewrites the playbook for emerging market companies. It demonstrates that with the right backing, vision, and timing, David can not only defeat Goliath but can turn around and acquire Goliath's entire family. For the global infrastructure industry watching from the sidelines, it's a wake-up call: the traditional flow of technology and ownership from developed to developing markets is no longer a one-way street.

V. IPO and Building the Public Company

September 22, 2010. The opening bell at the Bombay Stock Exchange signals more than just another IPO—it marks the transformation of a private equity-backed infrastructure play into a public company with global ambitions. VA Tech Wabag IPO bidding started from Sep 22, 2010 and ended on Sep 27, 2010. The shares got listed on BSE, NSE on Oct 13, 2010.

VA Tech Wabag IPO is a main-board IPO of 36,07,581 equity shares of the face value of ₹5 aggregating up to ₹472.59 Crores. The issue is priced at ₹1310 per share. The structure tells the story: a fresh issue of 9,54,198 equity Shares aggregating to Rs. 125.00 Crores and an offer for sale of 26,53,383 equity shares by India Advantage Fund I, Dynamic India Fund I, Rainbow Fund Trust, GLG Emerging Markets Fund and Passport India Investments (Mauritius) Limited (The Selling Shareholders), aggregating Rs. 347.59 Crores. ICICI Venture, having backed the management buyout and reverse acquisition, now begins its exit journey.

The timing is deliberate. Infrastructure is hot, water is becoming recognized as a critical resource, and Indian companies with global operations are finding favor with investors. The company positions itself carefully in the prospectus: not as an Indian EPC contractor, but as a multinational water technology player with presence across the value chain.

ICRA has assigned an IPO Grade 4 to VA Tech Wabag Limited IPO. This means as per ICRA company has 'Above Average Fundamentals'. In the conservative world of infrastructure ratings, this is a solid endorsement. The company articulates clear use of proceeds: funding working capital requirements, construction of a corporate office, and implementation of global IT systems—the unglamorous but essential investments in institutional capability.

The market response is emphatic. The IPO is oversubscribed by nearly 31 times, with institutional investors particularly enthusiastic. At listing on October 13, 2010, the stock debuts strongly, validating the transformation story. The offering values the company at over ₹1,300 crores—a remarkable journey from the ₹100 crore management buyout just four years earlier.

By 2011, ICICI Ventures completes its exit, having generated exceptional returns. The capital structure evolves: By 2011, ICICI Ventures had completely exited from the company. In the same year, the Rs5 shares were split into shares with a face value of Rs2. The management team, led by Rajiv Mittal, now controls a listed entity with the flexibility to raise capital for growth while maintaining strategic control.

The post-IPO years reveal the challenges of being a public infrastructure company. Project execution risks, working capital intensity, and the lumpy nature of order booking create volatility. The company maintains high debtor days—a structural challenge in the municipal water business where government payments can be delayed. Yet the access to capital markets provides crucial flexibility for bidding on large projects and investing in technology.

In 2020, the company raised Rs120 crore through a preferential issue made to Rakesh Jhunjhunwala, Anand Jain, and his family at a price of Rs160 per share. The entry of Jhunjhunwala, India's most celebrated investor, provides both capital and credibility—a signal that sophisticated investors see long-term value in water infrastructure.

The evolution from private to public company fundamentally changes WABAG's strategic calculus. No longer constrained by private equity exit timelines, management can pursue longer-term bets: BOOT projects with 15-20 year horizons, technology investments with uncertain payoffs, market entries that might take years to mature. The quarterly earnings calls become a platform to educate investors about water scarcity, technology evolution, and the company's positioning in global water markets.

Today, with Promoter holding in Va Tech Wabag Ltd has gone up to 19.12 per cent as of Jun 2025—relatively low by Indian standards—the company represents a unique model: professional management with skin in the game but not absolute control, forcing transparency and performance discipline while maintaining strategic flexibility. It's a governance structure more common in developed markets, reflecting WABAG's hybrid identity as an Indian company with global operations and ambitions.

VI. Global Expansion and Technology Leadership

The conference room in Chennai buzzes with multiple languages—Tamil, English, German, Arabic, Mandarin. It's 2024, and WABAG's project managers are coordinating operations across four continents, managing everything from a desalination plant in Saudi Arabia to wastewater treatment facilities in Nepal. The transformation from Indian subsidiary to global water solutions leader is complete.

VA TECH WABAG continues to expand its footprint with significant project wins across Tunisia, Nepal, and Oman. These projects, secured against strong international competition, underscore WABAG's technical prowess and commitment to sustainable water solutions.

The Tunisia story exemplifies WABAG's global reach. WABAG has been awarded a substantial consortium order from the Office National De L'assainissement (ONAS) in Tunisia, valued at 114.22 million Tunisian Dinars (approximately 34 million Euros). This project involves the design, build, and operation (DBO) of a 36 MLD Wastewater Treatment Plant (WTP) at Sousse Hamdoun II. Funded by the French Development Agency (AFD), the European Investment Bank (BEI), and the European Union (EU). The funding structure—multilateral development finance—signals that WABAG now competes at the highest levels of international infrastructure.

This order solidifies WABAG's leadership in Tunisia and the North African region, building on a three-decade-long relationship with ONAS. Three decades—longer than the company has been Indian-owned, a relationship that survived ownership changes, management buyouts, and geopolitical shifts. It's a testament to something deeper than corporate structure: technical competence and execution reliability.

In Nepal, the scale expands further. WABAG has secured an approximately USD 49 million order from Kathmandu Upatyaka Khanepani Limited (KUKL). Funded by the Asian Development Bank (ADB), this project involves the design, build, and operation (DBO) of three wastewater treatment plants in Sallaghari, Kodku, and Dhobighat. These plants will collectively treat 69 MLD of wastewater.

The technology portfolio accumulated through the reverse acquisition proves its worth daily. The company offers solutions spanning the entire water value chain: drinking water treatment, industrial water & wastewater treatment, desalination of sea & brackish water, sludge treatment, and recycling. Each solution backed by those 125+ patents, representing decades of R&D investment across multiple technology centers.

The geographic expansion follows a clear strategy. Focus on emerging markets where water scarcity meets rapid urbanization—Middle East, North Africa, Southeast Asia. Leverage relationships with multilateral development banks who value technical competence and execution track record. Build local partnerships that provide market access while WABAG brings technology and project management expertise.

The R&D centers in India and Europe operate as a unified innovation network. European centers focus on cutting-edge membrane technologies and energy recovery systems. Indian centers adapt these technologies for emerging market conditions—higher turbidity, extreme temperatures, cost constraints that would break European business models. This bidirectional innovation flow creates solutions that work in Chennai and Zurich, Tunis and Kathmandu.

Key international wins tell the story of technological leadership meeting market opportunity. WABAG's 400 MLD desalination plant in Chennai, one of Asia's largest, demonstrates capability at scale. The company's entry into specialized sectors—ultrapure water for semiconductor manufacturing, water treatment for green hydrogen production—shows technology depth beyond municipal contracts.

The transformation from EPC contractor to technology leader required fundamental changes. Engineers who once focused on construction schedules now discuss membrane flux rates and energy recovery ratios. Project managers coordinate not just construction crews but also patent filings, technology transfers, and R&D collaborations. The company that once depended on European technology now exports Indian innovations back to developed markets.

By 2024, WABAG has executed 6,500+ projects benefiting 88+ million people—numbers that represent not just business success but infrastructure impact at population scale. The company that started as Max Reder's filtration business in 1924 Breslau now shapes water security for entire cities and industries across the developing world.

VII. Business Model Evolution: From EPC to Solutions

The boardroom debate in 2015 centers on a fundamental question: Should WABAG remain primarily an EPC contractor—building plants and moving on—or transform into a solutions provider with long-term customer relationships? The answer shapes everything that follows.

The EPC foundation remains robust. The company undertakes engineering procurement and construction (EPC) projects, providing services ranging from conceptualizing to commissioning. This is the bread and butter, the capability that generates immediate cash flow and builds reference projects. But EPC alone is a treadmill—constantly bidding, building, collecting, and starting over.

The shift begins with BOOT projects—Build-Own-Operate-Transfer. Under its build-own-operate-transfer (BOOT) model, the Company provides solutions for financing, construction and operation of water and wastewater projects. Instead of just building and leaving, WABAG now finances, constructs, owns, and operates plants for 15-25 years before transferring them back. It's a fundamental change in risk profile and capital structure, but it creates annuity revenues and deep customer relationships.

The Chennai desalination story exemplifies this evolution. The Company got Rs 4,400 Crore for the Development, Construction, and Operation of a 400-Million Litres a Day (MLD) Desalination Plant in Chennai in 2024. This isn't just construction—it's a 20-year relationship with Chennai Metropolitan Water Supply and Sewerage Board. Post successful completion, WABAG will be responsible for 20 years of Operation and Maintenance (O&M).

The technical specifications reveal the sophistication: The desalination process includes Lamella Clarifiers, Dissolved Air Flotation System, Gravity Dual Media Filters, Reverse Osmosis, and Re-mineralization. Each component represents years of technology development, patents, and operational expertise. But the real value lies in integration—making these disparate technologies work together reliably at scale.

With the completion of the project, Chennai will emerge as the Desalination Capital of India, with producing over 750 million liters of desalinated water every day out of which WABAG's contribution will rise to an impressive 70%. Think about that—one company responsible for 70% of desalinated water in India's sixth-largest city. That's not vendor relationship; that's infrastructure partnership.

The O&M business becomes the strategic differentiator. Twenty years of operating a plant generates data, relationships, and upgrade opportunities that no EPC-only competitor can match. When Chennai needs to expand capacity or upgrade technology, who else would they call? The operator who's kept the plant running for two decades knows every pump, every membrane, every seasonal variation in seawater salinity.

The financial model transformation is equally profound. EPC revenues are lumpy—huge inflows when projects complete, drought periods between wins. O&M revenues are predictable—monthly payments for decades. Capital markets love predictability. The stock price responds accordingly.

The "Wriddhi" strategic framework codifies this evolution. This performance is underpinned by the company's long-term strategic framework, "Wriddhi", which has consistently driven both profitable growth and execution excellence. Wriddhi—Sanskrit for prosperity—signals the Indian identity while encompassing global ambitions. It's not just about building more plants but creating sustainable water solutions that generate value across the entire lifecycle.

The business model evolution enables new market entry strategies. In the solar PV sector, WABAG doesn't just build water treatment plants for semiconductor fabs—it guarantees ultrapure water quality standards that directly impact chip yields. In industrial parks, it doesn't just treat effluent—it creates water recycling systems that reduce freshwater consumption by 70-80%. Each solution deepens customer dependency and raises switching costs.

Asset-light remains the mantra despite BOOT projects. WABAG continued to execute complex water infrastructure projects across diverse geographies while maintaining its asset-light business model. How? Through sophisticated project finance structures, partnerships with infrastructure funds, and careful risk allocation. The company owns the technology and operations expertise, not necessarily the physical assets.

The transformation from EPC to solutions isn't complete—it's ongoing. Every project now includes an O&M component. Every industrial customer engagement explores recycling and zero liquid discharge possibilities. Every municipal contract considers future expansion and technology upgrades. The company that once sold projects now sells outcomes: water security, regulatory compliance, sustainability metrics. It's a business model evolution that mirrors the broader infrastructure sector's shift from building assets to delivering services.

VIII. Modern Era: New Frontiers and Digital Transformation

The year 2024 finds WABAG at an inflection point. Water treatment—traditionally a conservative, slow-moving infrastructure business—suddenly intersects with the most dynamic sectors of the global economy: renewable energy, semiconductors, artificial intelligence, and the circular economy.

WABAG has made a strategic entry into the fast-growing solar PV sector for the supply of ultrapure water for PV cell manufacturing. The ₹1,000 crore order from Indosol Solar Private Limited to set up a 100 MLD desalination plant for a 10 GW integrated solar PV manufacturing unit represents more than just another project—it signals WABAG's evolution from water utility contractor to critical enabler of the energy transition.

The technical requirements for semiconductor and solar PV manufacturing water are extreme—parts per billion impurity levels, consistent quality 24/7, zero tolerance for deviation. A single contamination event can destroy millions of dollars in wafer production. WABAG's ability to guarantee these standards, backed by decades of operational data and 125+ patents, creates switching costs that approach infinity. Once you're providing ultrapure water to a fab, you're essentially married to that customer.

The Bio-CNG initiative with Peak Sustainability Ventures exemplifies the new WABAG. The company formed a strategic alliance with Peak Sustainability Ventures to establish 100 Bio-CNG plants. The business potential for the establishment of 100 Bio-CNG plants is expected to be over USD 200 Million and this collaboration aims to generate over 73 Million Kgs of Bio-CNG per annum.

Think about the elegance of this model: WABAG already operates sewage treatment plants across India. These plants generate sludge—traditionally a waste disposal problem. Now that sludge becomes feedstock for Bio-CNG production. The sewage treatment plant transforms from cost center to profit center, from waste processor to energy producer. WABAG is already producing more than 40 MWh of green energy through its various installed plants.

Digital transformation arrives through partnership, not internal development. The company partnered with Pani Energy, a tech leader in AI/ML-based solutions, to drive digitalisation and operational intelligence across its treatment plants. This isn't technology for technology's sake—it's about predictive maintenance, energy optimization, and operational efficiency at scale.

The AI applications are practical, immediate: predicting membrane fouling before it happens, optimizing chemical dosing in real-time based on influent quality variations, detecting pump cavitation through vibration analysis. Each optimization might save just 2-3% in operating costs, but across hundreds of plants operating for decades, the cumulative impact is massive.

The "Blue Seed" initiative reveals ambition beyond organic growth. WABAG today announced the launch of "BLUE SEED" a pioneering initiative designed to foster innovation and support emerging start-ups in the water sector. Rather than trying to develop all technologies internally, WABAG becomes a platform for water innovation, investing in and nurturing startups that can accelerate technology development.

The strategic positioning is clear: as water becomes the constraint for everything from semiconductor fabs to green hydrogen production to data center cooling, WABAG positions itself as the essential enabler. It's not just about treating water anymore—it's about enabling the industries that will define the next century.

WABAG pioneered the concept of wastewater treatment with power neutral model and re-demonstrated at the 140 MLD sewage treatment plant under Namami Gange at Varanasi. Power neutral—a sewage treatment plant that generates as much energy as it consumes. It sounds impossible until you understand the biogas potential in sewage sludge, the energy recovery from treated water hydraulics, the optimization possible through AI-driven operations.

The numbers tell the transformation story. In FY25, WABAG secured new orders worth approximately Rs 5,700 Cr, reinforcing its healthy order book at Rs 13,667 Cr, reflecting a 21% YoY growth. But the composition matters more than the quantum—increasing share from industrial customers, growing proportion with O&M components, entry into new sectors like solar PV and green hydrogen.

The modern WABAG is three companies in one: a traditional EPC contractor executing large municipal projects, a technology company developing and deploying advanced water treatment solutions, and a digital services provider optimizing water infrastructure through AI and IoT. Each reinforces the others, creating competitive advantages that compound over time.

IX. Playbook: Business & Investing Lessons

Step back from the operational details and WABAG's journey reveals a masterclass in value creation through strategic audacity. The playbook reads like a business school curriculum, but one written by practitioners rather than professors.

Management buyout as a value creation tool—but not the leveraged, financial engineering variety that dominated the 1980s. The WABAG buyout was strategic, backed by venture capital rather than debt, focused on capability building rather than cost cutting. The presence of ICICI Venture provided not just capital but credibility, governance, and an exit path that aligned incentives without constraining strategic flexibility.

The lesson: in emerging markets, management buyouts can unlock value by removing the constraints of distant corporate parents who don't understand local market dynamics. But success requires patient capital, operational expertise, and a strategic vision beyond financial arbitrage.

The power of reverse acquisitions for emerging market companies—perhaps WABAG's most audacious move. The conventional wisdom says technology flows from developed to developing markets, that subsidiaries serve parents, that David doesn't swallow Goliath. WABAG shattered all three assumptions simultaneously.

The reverse acquisition worked because of timing and strategic logic. Siemens needed to divest non-core assets, the Austrian operations needed emerging market growth, and the Indian team had proven execution capability. The reunification narrative—"we're not acquiring, we're reuniting the WABAG family"—provided cultural cover for what was essentially an emerging market company taking control of developed market assets.

Building technology moats in infrastructure businesses—harder than in software but more durable once established. WABAG's 125+ patents aren't just legal documents; they represent decades of solving real-world problems, each solution building on the last. The R&D centers in India and Europe create bidirectional innovation flow—European precision meeting Indian frugality, developed market technology adapted for emerging market conditions.

The moat deepens through operational data. Twenty years of running a desalination plant generates insights no competitor can replicate. When membranes foul, pumps cavitate, or influent quality shifts, WABAG has seen it before, solved it before, optimized it before.

Asset-light models in capital-intensive industries—seemingly paradoxical but increasingly essential. WABAG executes multi-hundred crore projects while maintaining an asset-light balance sheet through sophisticated project finance, infrastructure funds partnerships, and BOOT structures where asset ownership is temporary and purposeful.

The key insight: own the technology and operational expertise, not necessarily the physical assets. Let infrastructure funds own the steel and concrete while WABAG owns the knowledge that makes them valuable. It's the difference between being a landlord and being an architect.

Balancing project execution with recurring revenue streams—the holy grail of infrastructure businesses. Pure EPC is a treadmill; pure O&M lacks growth. WABAG's evolution toward integrated solutions—build plus operate, technology plus service—creates both growth and stability.

Every project now includes an O&M tail, transforming lumpy EPC revenues into predictable annuity streams. The stock market rewards this predictability with higher multiples, creating a virtuous cycle where better valuations enable better project bidding, which enables more O&M contracts, which improves valuations further.

Becoming a total water solution provider—a capability none of the other subsidiaries within the WABAG Group had at the time of the reverse acquisition. This wasn't just adding services; it was reimagining the business model. Instead of selling equipment or projects, WABAG sells outcomes: water security, regulatory compliance, sustainability metrics.

The transformation required new capabilities: financial structuring for BOOT projects, regulatory expertise across multiple jurisdictions, technology integration across the treatment spectrum. But it also created competitive advantages that are nearly impossible to replicate.

The importance of patient capital and vision alignment—perhaps the metalesson encompassing all others. ICICI Venture's patience through the buyout and reverse acquisition, public market investors' acceptance of long-term BOOT projects, management's willingness to invest in R&D and digital transformation—all required alignment around a vision beyond quarterly earnings.

WABAG's story demonstrates that in infrastructure, the biggest returns come from the longest views. The management team that bought out their employer in 2005 wasn't thinking about flipping the company in three years. They were thinking about building India's water technology champion, and that required patient capital willing to wait for compound returns rather than quick exits.

X. Analysis & Bear vs. Bull Case

Bull Case:

The numbers paint a compelling growth story. The company is targeting an order book equivalent to 3 times its revenue and anticipates revenue growth at a CAGR of 15%–20% over the next 3–5 years. With an order book at Rs 13,667 Cr reflecting a 21% YoY growth, visibility extends well into the future.

But the real bull case transcends financial metrics. Water scarcity isn't a risk—it's a certainty. By 2050, 5 billion people will face water scarcity. Every semiconductor fab, solar panel factory, and data center needs ultrapure water. Every coastal city needs desalination. Every municipality needs wastewater treatment. WABAG sits at the intersection of necessity and capability.

The targeted revenue mix—comprising over 50% from international projects, 30% from industrial customers, 20% from O&M, and one-third of EPC being EP projects—is expected to drive margin improvement. This isn't just diversification; it's strategic positioning toward higher-margin, stickier revenue streams. EBITDA margins ranging between 13%–15% with EBITDA/PAT growth projected to outpace revenue growth as operating leverage kicks in.

The technology leadership with 125+ patents creates competitive moats that deepen with time. Every project adds to the knowledge base, every operational year generates data, every innovation builds on previous solutions. It's compound knowledge creation that accelerates rather than decelerates with scale.

Regulatory tailwinds strengthen globally. India's Namami Gange project, Middle East's water security initiatives, Europe's circular economy regulations—all create demand for WABAG's solutions. Regulations don't just create one-time opportunities; they establish baselines that require ongoing compliance, creating permanent demand.

Bear Case:

The company has delivered poor sales growth of 5.19% over past five years. For all the strategic positioning and technology leadership, revenue growth has disappointed. The infrastructure sector's inherent lumpiness means even strong order books don't guarantee smooth revenue recognition.

Company has high debtors of 223 days. In a business where customers are primarily governments and municipalities, payment delays are structural, not cyclical. Every project requires working capital financing, and delays cascade through the financial system. High debtor days mean cash is tied up in receivables rather than funding growth.

Project execution risks in emerging markets remain substantial. Political instability, currency fluctuations, regulatory changes—any can derail a project mid-execution. WABAG's geographic diversification helps but doesn't eliminate these risks. A single large project failure can wipe out years of profits from smaller successes.

Competition from global majors and Chinese players intensifies. Veolia and Suez bring century-old expertise and global scale. Chinese companies bring government backing and aggressive pricing. Local players understand regional dynamics better. WABAG must compete on multiple fronts simultaneously.

The capital intensity of growth constrains returns. Even with asset-light models and project finance, growth requires capital. BOOT projects tie up capital for decades. Technology development requires continuous R&D investment. Digital transformation demands IT spending. The capital needs never end, even as the company scales.

Management ownership at 19.1% is relatively low by Indian standards. While this ensures professional management and governance, it also means less skin in the game during challenging times. The absence of a large strategic shareholder could leave the company vulnerable during sectoral downturns.

The water sector's social and political sensitivity creates unique risks. Water is essential, emotional, and political. Pricing is often below economic levels. Projects face community opposition. Elections can change project priorities overnight. WABAG operates in a sector where pure economic logic doesn't always prevail.

XI. Epilogue & "If We Were CEOs"

The water crisis is not coming—it's here. Chennai ran out of water in 2019. Cape Town nearly hit "Day Zero" in 2018. The Colorado River is drying up. The Ogallala Aquifer is depleting. Against this backdrop, WABAG isn't just a business opportunity; it's an essential service for humanity's future.

If we were CEOs, the strategic priorities would be clear but the execution complex.

Building the next phase of growth requires betting on sectors that don't fully exist yet. Green hydrogen production needs 9 liters of ultrapure water per kilogram of hydrogen. As the hydrogen economy scales, water becomes the bottleneck. WABAG should position itself as the water partner for every green hydrogen project globally, creating standard solutions that can be rapidly deployed as the sector explodes.

Semiconductor fabs are coming to India, Europe, and the Americas as supply chains regionalize. Each fab needs ultrapure water systems that cost hundreds of crores and require decades of operational expertise. WABAG should create a specialized semiconductor water division, perhaps through acquisition of specialized technology, to capture this opportunity.

The circular economy isn't just about recycling—it's about resource loops. Every liter of water treated is a liter that doesn't need to be extracted. WABAG should pioneer closed-loop water systems for industrial parks, where wastewater from one facility becomes process water for another, creating industrial symbiosis at scale.

Geographic expansion versus deepening existing markets presents a classic strategy dilemma. The temptation is to plant flags in new countries, but the value often lies in market penetration. India alone needs thousands of sewage treatment plants, hundreds of desalination facilities, and countless industrial water systems. Dominating the home market might create more value than spreading thin globally.

Yet certain international markets are too strategic to ignore. Saudi Arabia's NEOM project, Egypt's New Administrative Capital, Indonesia's new capital Nusantara—these mega-projects need water infrastructure at unprecedented scale. WABAG should selectively pursue transformational international projects while deepening presence in core markets.

Technology investments must balance immediate application with long-term disruption. AI and ML for operational optimization—absolutely, the ROI is clear and immediate. Digital twins for plant design and operation—yes, they reduce project risk and improve performance. But what about breakthrough technologies like atmospheric water harvesting or graphene membranes? The CEO must allocate resources between evolutionary and revolutionary innovation.

Automation presents opportunity and threat. Fully automated plants reduce operational costs but also reduce O&M revenues. WABAG must navigate this transition carefully, perhaps moving up the value chain to plant optimization and performance guarantees rather than just operations.

Capital allocation priorities start with maintaining the technology edge. R&D spending should increase, not as a percentage of revenue but in absolute terms. Every patent, every innovation, every operational insight adds to the competitive moat.

Strategic acquisitions could accelerate capability building. A specialized membrane technology company, an AI-driven optimization platform, a player in atmospheric water generation—each could add capabilities that would take years to develop internally.

But the biggest capital allocation decision is how much to invest in owned assets versus asset-light models. BOOT projects generate stable returns but tie up capital. Pure O&M contracts generate lower margins but higher returns on capital. The optimal mix depends on cost of capital, market opportunities, and competitive dynamics.

Lessons for entrepreneurs in infrastructure and emerging markets emerge clearly from WABAG's journey. First, timing matters enormously—the management buyout worked because of specific circumstances that might never repeat. Second, patient capital is essential—infrastructure businesses compound slowly but surely. Third, technology moats in infrastructure are harder to build but more durable than in software.

Most importantly, emerging market companies can acquire and integrate developed market assets, but success requires cultural sensitivity, strategic clarity, and exceptional execution. The narrative matters as much as the numbers—"reunification" rather than "acquisition," "partnership" rather than "takeover."

The water sector offers perhaps the most essential investment opportunity of the next century. Water is irreplaceable, demand is growing, supply is constrained, and technology can bridge the gap. WABAG sits at the center of this opportunity, with the technology, expertise, and track record to capitalize on it.

The question isn't whether water infrastructure will be built—it must be. The question is who will build it, how they'll finance it, and what returns they'll generate. WABAG's journey from German filtration company to Indian multinational to global water solutions provider offers a template, but the next chapter remains unwritten.

The CEO who guides WABAG through the next decade will shape not just a company but an essential component of global infrastructure. In a world where water scarcity threatens economic growth, social stability, and human health, WABAG's success matters far beyond its shareholders. It's a business where doing well and doing good converge, where financial returns and social impact align, where the biggest opportunities come from solving humanity's most pressing challenges.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube