Vishal Mega Mart: India's Value Retail Revolution

I. Cold Open & Episode Setup

Picture this: It's December 2024, and the bourses of Dalal Street are buzzing with unusual energy. A retailer that most of Mumbai's financial elite have never shopped at—one that doesn't even have stores in South Mumbai's posh neighborhoods—has just crossed ₹64,000 crore in market capitalization. The company? Vishal Mega Mart, a chain whose typical customer earns less than ₹30,000 per month and whose idea of splurging is buying a ₹299 shirt instead of a ₹199 one.

The numbers tell a story that would make any private equity partner salivate: What began as a distressed asset bought for ₹70 crore in 2010 has transformed into one of India's most valuable retail companies. Partners Group, the Swiss alternative asset manager, has just orchestrated what might be their most successful India exit ever—turning roughly ₹3,000 crore into a stake worth over ₹15,000 crore at IPO, with plenty more still on the books.

But here's what makes this story truly remarkable: Unlike the typical Silicon Valley unicorn narrative of blitzscaling and cash burn, Vishal Mega Mart's ascent represents something far more difficult—the patient, methodical conquest of Bharat, not India. While India shops on Myntra and orders groceries from Blinkit, Bharat—that vast expanse of tier-2, tier-3, and tier-4 cities—still prefers to touch, feel, and bargain before buying. And in this India of 400 million middle-class aspirants, Vishal Mega Mart has quietly built an empire of 645 stores across 414 cities.

The journey from near-bankruptcy to blockbuster IPO spans three distinct ownership eras, each with its own playbook and lessons. There's the founder's ambitious expansion that nearly killed the company, TPG's clinical turnaround that brought it back from the brink, and the Kedaara-Partners Group partnership that scaled it into a retail powerhouse. It's a masterclass in operational excellence, patient capital deployment, and most importantly, understanding the Indian consumer psyche at its most fundamental level.

What unfolds is not just a business story, but a window into how India shops, saves, and aspires—told through the lens of bright yellow storefronts that have become landmarks in cities most of us can't pronounce. This is the story of how a company selling ₹99 t-shirts built more value than many companies selling ₹9,999 smartphones. Welcome to the Vishal Mega Mart saga.

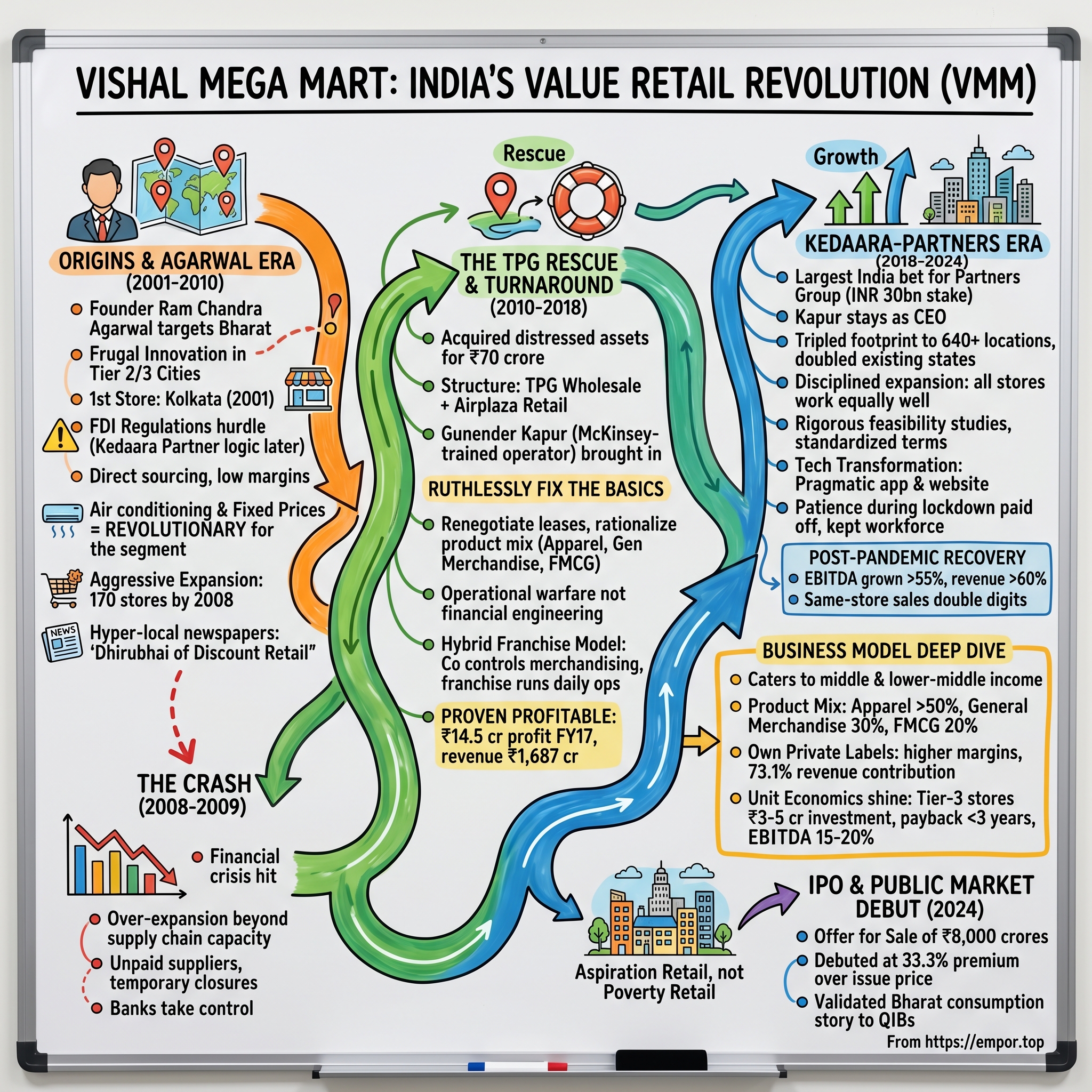

II. Origins & The Ram Chandra Agarwal Era (2001-2010)

The year was 2001, and in a modest corner of Kolkata's wholesale garment district, Ram Chandra Agarwal was wrestling with a problem that would define the next two decades of Indian retail. The textile trader had spent years watching middle-class families trek to crowded bazaars, haggling over unbranded clothes displayed in chaotic piles, with no trial rooms, no fixed prices, and certainly no air conditioning. "Why," he wondered, "should shopping for affordable clothes feel like punishment?"

Agarwal wasn't some MBA-wielding strategist with PowerPoint decks about market gaps. He was a traditional Marwari businessman who understood one thing deeply: the aspirations of India's emerging middle class far exceeded their wallets. These were families earning ₹10,000-15,000 per month who wanted to dress well, who watched the same Bollywood movies as everyone else, who desired dignity in their shopping experience—but couldn't afford Big Bazaar, let alone Shoppers Stop.

His solution was deceptively simple: create a modern retail format with the prices of a street market. The first Vishal Mega Mart opened in 2001, not in some prime mall location, but in a converted warehouse where rent was cheap. Agarwal's innovation wasn't technological—it was psychological. Fixed prices eliminated the exhaustion of bargaining. Air conditioning made summer shopping bearable. Trial rooms gave customers privacy. These seem trivial today, but in 2001's India, for this price point, they were revolutionary.

The early years were a masterclass in frugal innovation. Agarwal sourced directly from manufacturers in Tirupur and Ludhiana, cutting out three layers of middlemen. He bulk-bought end-of-season inventory from brands. He convinced suppliers to give him 60-day credit while he turned inventory in 30 days—classic negative working capital. Store employees were often family members of local suppliers, keeping wage costs minimal while ensuring community buy-in.

By 2005, Vishal had five stores, all profitable, all in tier-2 cities where real estate was cheap and competition non-existent. Revenue had crossed ₹100 crore. Local newspapers called Agarwal the "Dhirubhai of Discount Retail"—hyperbolic perhaps, but it captured something essential about his ambition. At industry conferences, he would declare his vision: "1,000 stores by 2015, in every district headquarters of India."

The expansion that followed was breathtaking in its pace and ultimately devastating in its consequences. Between 2006 and 2008, Vishal opened 170 stores. Agarwal was signing lease agreements faster than his team could conduct feasibility studies. The formula that worked in Patna was copy-pasted to Pune without adaptation. Store managers were promoted from cashiers after three-month training programs. The supply chain, designed for 20 stores, was suddenly servicing 150.

In boardrooms, Agarwal would spread out massive maps of India, colored pins marking existing stores, planned stores, potential stores. "See this?" he'd say, pointing to vast swathes of unpinned territory, "This is our opportunity. Speed is everything. If we don't capture these markets, someone else will." Banks, seduced by the growth story and the retail boom narrative, lined up to lend. State Bank of India, HSBC, ING Vysya—they all wanted a piece of India's retail revolution.

The 2008 financial crisis hit Vishal like a tsunami hitting a house of cards. Consumer spending froze overnight. Same-store sales growth turned negative for the first time. New stores in expensive locations bled cash. The company that had never needed working capital suddenly couldn't pay suppliers. By early 2009, debt had ballooned to ₹400 crore against annual revenues of barely ₹600 crore. Store employees hadn't been paid for three months. Suppliers were threatening legal action.

In a cramped conference room in Delhi's Karol Bagh, Agarwal faced his bankers. The man who had once commanded rooms with his vision now struggled to explain how it had all gone wrong. "The model works," he insisted, "we just expanded too fast." But the bankers weren't interested in philosophy. They wanted their money back. After twelve hours of negotiations, Agarwal signed over control of his company to a consortium of lenders. The entrepreneur who had started with one store was left with nothing but memories and regret.

The Agarwal era ended not with a bang but with a whimper—empty stores with "Temporarily Closed" signs, unpaid suppliers picketing outside headquarters, and a founder's vision crushed under the weight of its own ambition. But hidden in this failure were the seeds of something powerful: proof that Indians earning ₹15,000 per month would shop in organized retail if the price and experience were right. The model worked; the execution had failed. And that distinction would prove crucial for what came next.

III. The TPG Rescue & Turnaround (2010-2018)

The morning of March 14, 2011, inside the State Bank of India's headquarters on Nariman Point, a group of bankers stared at documents that would conclude one of Indian retail's most dramatic restructurings. TPG Capital and the Shriram Group were about to acquire the distressed assets of Vishal Retail for just ₹70 crore—a fire-sale price for a company that had once boasted 170 stores and dreams of conquering India.

Puneet Bhatia, TPG Capital India's managing director, saw something the bankers didn't. Where they saw ₹730 crore of debt and shuttered stores, he saw India's most underserved consumer segment waiting for someone to get the model right. "TPG brings a wealth of experience in managing and operating a multitude of businesses from across the world, including a track record of turning around portfolio companies," Bhatia would tell the press. But this wasn't going to be financial engineering—this would be operational warfare.

The structure TPG created was ingenious in its simplicity. TPG Wholesale Private Limited acquired the wholesale and franchise undertaking while Airplaza Retail Holdings, part of the Shriram Group, acquired the retail undertaking. TPG Wholesale would be the franchisor to Airplaza Retail and existing franchisee partners. This wasn't just legal maneuvering—it was a fundamental reimagining of how to run a retail chain in India's complex regulatory environment.

TPG committed ₹200 crore to turn the business around—nearly three times what they paid for it. But the real investment wasn't capital; it was bringing in Gunender Kapur, who joined in 2011 to lead the turnaround. Kapur was everything Ram Chandra Agarwal wasn't—a McKinsey-trained operator who understood that retail wasn't about vision but about execution, not about growth but about discipline.

The first year was triage. Of the 170 stores Vishal once operated, only 150 reopened under the new structure. These stores would be operated by Airplaza and 20 franchise partners. Kapur's team went store by store, renegotiating leases, often getting 40-50% reductions from landlords desperate to avoid vacancy. Suppliers who hadn't been paid in months were offered partial settlements with promises of future business. The message was clear: the old Vishal was dead, but something new could be built from its ashes.

Kapur's operational playbook was ruthlessly simple. First, fix the basics: ensure every store had adequate inventory, functioning air conditioning, and clean trial rooms. Second, rationalize the product mix: Agarwal had tried to sell everything from electronics to groceries; Kapur focused on three categories where margins were defensible—apparel, general merchandise, and FMCG. Third, and most importantly, build a sustainable franchise model that aligned incentives across the ecosystem.

The franchise innovation was particularly clever. Unlike traditional retail where the company owns stores and bears all operational risk, or pure franchise models where quality control becomes impossible, TPG created a hybrid. The company would control merchandising, supply chain, and brand standards, while franchisees would manage day-to-day operations and local relationships. This capital-light model meant expansion could happen without betting the company on each new store.

By 2013, the transformation was becoming visible. Same-store sales growth turned positive. New stores were opening—not 50 at a time like in Agarwal's era, but 10-15 annually, each one profitable from day one. The company discovered something profound: in tier-3 and tier-4 cities, where monthly household incomes ranged from ₹15,000 to ₹30,000, there was virtually no organized retail competition. These weren't markets that Future Group or Reliance were racing to enter. They were invisible to India's retail giants, but they represented 400 million consumers.

The discipline extended to working capital management. Where Agarwal had given suppliers 60-day payment terms while holding inventory for 90 days, Kapur reversed the equation. Suppliers were paid in 45 days, but inventory turned in 30. The company became a cash-generation machine, funding its own growth without external capital.

The company turned profitable in fiscal 2017 with ₹14.5 crore profit versus ₹40 crore loss previously, on revenue of ₹1,687 crore. This wasn't spectacular by any measure, but for a company that had been technically bankrupt just six years earlier, it was remarkable. More importantly, the unit economics were proven. Each store generated 15-20% EBITDA margins, with payback periods under three years.

By 2017, TPG had achieved what they set out to do: prove that the Vishal model worked when executed properly. The company now had over 200 stores, all profitable, with a replicable playbook for expansion. But TPG's fund cycle was ending, and they needed an exit. The hunt for buyers began, setting the stage for the next chapter of Vishal's evolution. The distressed asset bought for ₹70 crore was about to be valued at nearly 70 times that amount.

IV. The Kedaara-Partners Group Era (2018-2024)

In May 2018, inside a conference room at Partners Group's Zurich headquarters, Vageesh Gupta was making the case for what would become the Swiss firm's largest India bet. Partners Group and Kedaara Capital acquired Vishal in 2018 from TPG Capital and Shriram Group for approximately INR 50bn, with Partners Group contributing about INR 30bn. The structure was carefully designed—Kedaara, as the local partner, would maintain control to comply with FDI regulations, while Partners Group would bring the capital muscle and global retail expertise.

What sealed the deal wasn't just the financials—it was Gunender Kapur's decision to stay on. Kapur, who had experience from previous roles at TPG Capital, Reliance Retail and Unilever, had orchestrated the TPG-era turnaround. Now he would lead the next phase of growth, this time with deeper pockets and a longer investment horizon.

Under Kapur's leadership, they solved compliance issues, streamlined the entire apparel strategy, and optimised product sourcing to achieve a revenue CAGR of 24% in 2018. But the real transformation was about to begin. Partners Group didn't just want to fix Vishal—they wanted to build India's definitive value retail platform.

The expansion that followed was breathtaking yet disciplined. The most important progress was a tripling of the store footprint to about 640 locations nationwide, including doubling down on existing geographies and expanding into new states, with tier-one cities seeing store penetration increase as much as 4x.

But this wasn't the chaotic expansion of the Agarwal era. As Gupta explained, "The stores have to be good before you can press the pedal on an acceleration, and the consistency of box economics at Vishal was very high. All the stores worked, and they all worked equally well". Every new location underwent rigorous feasibility studies. Lease terms were standardized. Store managers went through six-month training programs, not three-week crash courses.

The technology transformation was equally important. While competitors chased the e-commerce dream in metros, Vishal built something more practical: a basic but functional mobile app and website that served as catalog and marketing tools more than revenue generators. The insight was profound—their customers wanted to see products online but still preferred buying in stores where they could touch fabric and try on clothes.

Then came March 2020, and with it, a test that no one had anticipated. As India went into lockdown, Vishal's 400+ stores shuttered overnight. Revenue went to zero. Fixed costs remained. This was the moment that could have undone everything.

In the first 15 days of the first lockdown, Partners Group pumped in enough capital that management never had to worry about runway. This patience has paid off in the last two years. While competitors laid off staff and permanently closed stores, Vishal kept its entire workforce employed. Kapur personally called franchise partners, assuring them the company would support them through the crisis.

The post-pandemic recovery validated every strategic choice. EBITDA has grown more than 55%, while revenue has increased by more than 60%. The stores that reopened found customers eager to shop in person after months of lockdown. Same-store sales growth hit double digits. New store openings accelerated.

By 2023, Vishal had become what Partners Group had envisioned: a 560+ store juggernaut generating consistent 15-20% EBITDA margins. The company had cracked the code that had eluded Indian retail for decades—serving the mass market profitably at scale.

As Gupta noted, "That's what attracted us to them in the first place, and I think that's what people bought into in the IPO as well. E-commerce economics are tougher at these price points. In this segment, your gross margin doesn't even begin to cover the costs of logistics, not to mention the cost of customer acquisition. It's a tough market to disrupt, and it has a long tail in terms of very low organized retail penetration".

The success attracted attention. Investment bankers started circling. IPO markets were heating up. By early 2024, Partners Group and Kedaara decided it was time to test public market appetite for their value retail story. What followed would be one of India's most successful PE-backed IPOs—and a validation of patient capital's power to transform businesses.

V. Business Model Deep Dive

To understand Vishal Mega Mart's business model is to understand a fundamental truth about Indian retail: the customer earning ₹20,000 per month shops differently than the one earning ₹200,000. Not just in what they buy, but how they buy, where they buy, and most importantly, why they buy.

Vishal Mega Mart Limited is a diversified retail company catering to middle and lower-middle-income groups in India. It offers products under three categories: apparel, general merchandise, and fast-moving consumer goods (FMCG). But this clinical categorization misses the genius of the model—it's not about what they sell, but how they've engineered every aspect of the business to serve a customer for whom a ₹50 saving matters.

The product mix tells the story. Apparel contributes over 50% of revenue, but it's not haute couture—it's ₹199 t-shirts, ₹299 jeans, ₹499 sarees. General merchandise—kitchen utensils, plastic containers, school bags—contributes another 30%. FMCG rounds out the basket, but even here, they're not selling premium shampoos but ₹1 sachets and ₹10 soaps. The company offers over 60,000 products, creating a one-stop-shop experience for families who can't afford multiple shopping trips.

The retail chain manufactures and sells its own private-label brands exclusively in its stores. These products are priced lower than national brands, helping customers save money while boosting the company's profit margins. The private label strategy is particularly clever—in categories like basic apparel, where brand loyalty is low, Vishal's own brands capture 70% of sales. A t-shirt that would retail for ₹399 under a national brand sells for ₹199 under Vishal's label, with higher absolute margins for the company.

But the real innovation lies in the operating model. Vishal Mega Mart operates through a mix of company-owned and franchise stores. This hybrid model allows for rapid expansion while minimizing capital investment, enabling the brand to grow its footprint efficiently across India. The franchise structure is unique—it's not a traditional franchise where the brand just licenses its name. Instead, Vishal controls the entire value chain: sourcing, pricing, merchandising, even store layouts. Franchisees essentially become operating partners, managing day-to-day execution while Vishal handles everything strategic.

Being a franchisee, you stand to benefit from 90% of the total income earned by your store which is relatively higher compared to many other franchising arrangements. This generous revenue sharing ensures franchisee buy-in and alignment. Most executives reported that they could make back their initial investment in 1 to 2 years, creating a waiting list of potential franchisees in every new market.

The unit economics are where the model truly shines. A typical 10,000 square foot store in a tier-3 city requires ₹3-5 crore in total investment. Monthly rent runs ₹3-5 per square foot—a fraction of metro rates. The store employs 30-40 people at minimum wages. Inventory turns 12 times annually. EBITDA margins consistently hit 15-20%. Payback period: under three years. These aren't sexy numbers, but they're remarkably consistent across geographies—what works in Patna works in Pune, what succeeds in Bareilly succeeds in Belgaum.

It operates 645 stores across 414 cities in India, complemented by an e-commerce platform (website and mobile app). The company utilizes a hub-and-spoke distribution model for efficient operations. The distribution architecture is built for efficiency, not speed. Unlike e-commerce players promising same-day delivery, Vishal's supply chain is optimized for cost. Regional distribution centers feed store clusters. Trucks are owned, not leased. Delivery schedules are weekly, not daily. Every decision trades convenience for cost savings that get passed to customers.

The competitive moat isn't technology or brand—it's understanding. Vishal knows that their customer doesn't care about organic cotton or sustainable sourcing. They care about whether the shirt will last six months of weekly washing. They know their customer doesn't want 50 varieties of shampoo—they want three options at three price points. They know their customer values the dignity of shopping in an air-conditioned store more than home delivery.

A significant part of Vishal Mega Mart's success lies in targeting smaller cities and rural areas. By tapping into the increasing purchasing power of these regions, the brand has established itself as a key player in underserved markets. This isn't poverty retail—it's aspiration retail. The family shopping at Vishal is moving up from unorganized retail, not down from premium formats. For them, Vishal represents progress: fixed prices instead of haggling, branded products instead of loose goods, a modern shopping experience instead of crowded bazaars.

The numbers validate the model. The company reported a profit of INR 4.6 billion ($54 million) on revenue of INR 89.1 billion for the fiscal year ending March 2024. These aren't venture-scale margins, but they're real, sustainable, and growing. More importantly, they're generated while serving customers that most of India's corporate sector ignores.

The model's resilience was tested during COVID and proved robust. While e-commerce players burned cash on customer acquisition, Vishal's customers returned to stores as soon as lockdowns lifted. While premium retailers struggled with inventory, Vishal's fast-moving basics flew off shelves. The company emerged from the pandemic stronger, validating a simple truth: in India, serving the masses profitably isn't just good business—it's the biggest business opportunity of all.

VI. The IPO & Public Markets Debut (2024)

March 2024, SEBI headquarters, Mumbai. The document on the table was 450 pages thick—Vishal Mega Mart's Draft Red Herring Prospectus. After years of speculation, Partners Group and Kedaara were finally ready to test public market appetite for their value retail story. The IPO would be structured as a pure Offer for Sale of 1,025,641,025 equity shares, aggregating to ₹8,000 crores—making it one of India's largest retail IPOs ever.

The timing seemed counterintuitive. Global markets were jittery. Foreign institutional investors were pulling money out of India. December—when the IPO was scheduled—was traditionally a dead period when international funds went into holiday mode. But Partners Group's Vageesh Gupta saw opportunity in adversity: "While we had that to some extent, this IPO happened in the second half of December, so a lot of foreign institutions were either pulling money out of India or going into their year-end breaks. Instead, we had pretty much all the largest Indian institutions [mutual funds and insurance companies] in the anchor book".

The investment banking lineup read like a who's who of global finance: Kotak Mahindra Capital Company Limited as the book-running lead manager, with ICICI Securities, J.P. Morgan India, Jefferies India, and Morgan Stanley India Company. Each bank pitched aggressively for the mandate, knowing this would be the marquee IPO of the year. The fees alone would run into hundreds of crores.

The price discovery process was fascinating. Initial whispers suggested a valuation of $5 billion. The bankers argued for pricing at ₹85-90 per share, pointing to D-Mart's premium valuations. But Kedaara and Partners Group were pragmatic—they wanted a successful listing more than a stretched valuation. The price band was set at ₹74 to ₹78 per share, valuing the company at approximately $4.3 billion at the upper band.

December 10, 2024, was anchor investor day. The response was overwhelming—₹2,400 crores raised from anchor investors, nearly 30% of the entire issue size. The list of anchors told its own story about who believed in the India consumption story: domestic mutual funds dominated, with SBI Mutual Fund, HDFC Mutual Fund, and ICICI Prudential taking large chunks.

The IPO opened for public subscription on December 11, 2024, and closed on December 13, 2024. The subscription numbers were closely watched—this would be the market's verdict on whether investors bought into the Bharat consumption story.

The retail response was measured but positive—2.31 times subscribed. These were individual investors betting their own money, many of them Vishal customers themselves who understood the business viscerally. The HNI (High Net Worth Individual) category saw stronger demand at over 9 times subscription.

But the real drama was in the QIB (Qualified Institutional Buyer) category. By the close of subscription, QIBs had bid for 80.746 times their allocation. This wasn't just oversubscription—it was validation. Institutional investors who had spent months analyzing the business, visiting stores, meeting management, were voting with billions of rupees.

The allotment was finalized on December 16, 2024. Given the oversubscription, retail investors received approximately 43% of their applied shares, while institutional allocations were done on a proportionate basis. The grey market premium, that unofficial barometer of listing expectations, suggested a 30-35% premium to the issue price.

December 18, 2024, 9:15 AM. The opening bell at the NSE. Vishal Mega Mart shares debuted at ₹104 apiece on the NSE, a premium of 33.33% over the issue price of ₹78. On the BSE, the opening was even stronger at ₹110, representing a 41% premium. Within minutes, over 50 million shares had changed hands. The market capitalization crossed ₹50,000 crores on day one.

For Partners Group, this was vindication on multiple levels. Partners Group sold about 23% of its position for about USD 630m, while their remaining stake was worth around USD 3bn. From an initial investment of roughly ₹3,000 crore in 2018, they had created value worth over ₹20,000 crore. It was the biggest India exit to date for the private equity firm.

The post-listing performance was equally impressive. Within three months, the stock had touched ₹143, nearly doubling from the issue price. By December 31, 2024, the company had 9.13 lakh retail investors, with domestic mutual funds holding 8.66% and foreign portfolio investors 6.68%.

What made this IPO special wasn't just the numbers—it was what it represented. In an era when loss-making new-age tech companies commanded astronomical valuations, here was an old-economy retailer, selling ₹99 t-shirts in tier-3 cities, creating more wealth than most unicorns. It proved that serving India's masses wasn't just socially important—it was enormously profitable.

The IPO also marked a transition. Samayat Services LLP and Kedaara Capital Fund II LLP remained as promoters, but now they had public market scrutiny. Quarterly earnings calls, analyst meetings, shareholder expectations—the company that had thrived in private equity ownership would now need to perform on a public stage.

For Gunender Kapur and his team, the IPO wasn't an end but a beginning. The capital raised wouldn't go to the company, but the currency of listed shares would enable future fundraising for expansion. More importantly, the public listing brought credibility that would help in lease negotiations, vendor relationships, and talent acquisition. The journey from distressed asset to public market darling was complete, but the real work of building India's definitive value retail platform had just begun.

VII. Financial Performance & Growth Story

The numbers tell a story of relentless execution. 2024 revenue of 107.16 billion (20.25% increase from 89.12 billion), earnings of 6.32 billion (36.81% increase)—these aren't just financial metrics but validation of a business model built for India's masses.

The most recent quarter exemplifies this momentum. Q3 FY25: Net profit rose 27.93% to Rs 262.72 crore, sales rose 19.53% to Rs 3135.94 crore. What makes these numbers remarkable is their consistency—quarter after quarter, year after year, the same story of 15-20% revenue growth and 25-30% profit growth.

But to understand Vishal's financial performance, you need to look beyond the headline numbers to the unit economics that drive them. A typical store generates ₹15-20 crore in annual revenue. With 696 stores as of March 2025, that's a revenue run rate approaching ₹12,000 crore. Each store operates at 15-20% EBITDA margins—not spectacular by global retail standards, but extraordinary for serving customers with average ticket sizes under ₹1,000.

The working capital efficiency is where the model truly shines. Inventory turns 12 times annually—once a month. In retail, where capital efficiency determines survival, this is gold. Compare this to fashion retailers who turn inventory 4-6 times annually, and you understand why Vishal generates cash rather than consuming it.

The company's operating profit, measured by EBITDA, climbed 18.3% to ₹505 crore, up from ₹427 crore in Q3 FY24. The EBITDA margin stood at 16.1%. These margins have been remarkably stable despite inflation, competitive pressure, and rapid expansion—testament to operational discipline.

The store expansion story is equally impressive. During the year, we expanded our retail footprint by 85 store additions bringing our total store count to 696 as of 31 March 2025. But this isn't growth for growth's sake. Each new store undergoes rigorous feasibility analysis. The payback period target is under three years. Stores that don't achieve positive EBITDA within 12 months are restructured or closed.

Same-store sales growth (SSSG)—the truest measure of retail health—tells its own story. During the quarter, same-stores sales growth (SSSG) stood at 10.5%. In a market where organized retailers struggle to achieve 5-7% SSSG, Vishal's double-digit growth reflects both market share gains from unorganized retail and increased wallet share from existing customers.

The category mix evolution is strategic. For FY25, the category-wise revenue contribution was 44% for apparel, 28% for general merchandise and 28% for FMCG. This balanced portfolio reduces dependence on any single category while maximizing store productivity. Apparel drives margins, FMCG drives footfall, general merchandise fills the basket.

Own brands contribution to revenue was 73.1% in FY25 as against 71.8% in FY24. This isn't just about margins—though private labels do generate 5-7% higher margins. It's about control: over quality, pricing, availability. When you're selling to customers for whom a ₹20 price difference matters, this control is everything.

The digital integration, while not headline-grabbing, is pragmatic and profitable. The company extended its quick commerce initiative to 656 stores across 429 cities and had a registered user base of 8.7 million. This isn't about competing with Blinkit or Zepto—it's about serving existing customers better, increasing touchpoints without increasing costs.

The company had a large and loyal consumer base of 145 million as on 31 March 2025. Think about that number—145 million Indians, nearly 10% of the population, shopping at Vishal. These aren't one-time customers but repeat buyers who return monthly for their household needs.

The capital efficiency metrics deserve special attention. Return on Capital Employed (ROCE) consistently exceeds 20%. For a capital-intensive retail business, this is exceptional. The asset-light model—all stores are leased, inventory is largely funded by vendors—means expansion doesn't require proportional capital investment.

Geographic diversification reduces risk. Unlike retailers concentrated in metros, Vishal's 696 stores across 458 cities create natural hedging. A slowdown in one region is offset by growth in another. Rural distress in one state is balanced by urban prosperity in another.

The resilience was tested during demonetization, GST implementation, and COVID—each crisis that decimated weak retailers. Vishal not only survived but emerged stronger, gaining market share from shuttered competition. Vishal Mega Mart has registered 36.8% rise in consolidated net profit to Rs 632 crore on a 20.2% rise in revenue from operations to Rs 10,716.3 crore in FY25 over FY24.

Looking forward, the runway remains massive. Vishal Mega Mart, operating 696 stores, aims to add over 100 stores annually. Strong financial metrics indicate robust growth, with projected revenue and profit increases through FY25-28. With organized retail penetration in tier-2/3 cities still under 10%, Vishal could triple its store count without saturating its target markets.

The financial story of Vishal Mega Mart isn't about explosive growth or revolutionary margins. It's about consistency, discipline, and the compound effect of getting the basics right, quarter after quarter. In a market obsessed with unicorns and moonshots, Vishal proves that serving the underserved, profitably and at scale, might be the biggest opportunity of all.

VIII. The India Retail Opportunity

To understand why Vishal Mega Mart matters, you need to understand two Indias. There's India—urban, English-speaking, ordering artisanal coffee on Swiggy. And there's Bharat—semi-urban, vernacular, buying ₹10 sachets of shampoo at the local kirana. India has 100 million people. Bharat has 1.3 billion. India gets 90% of venture capital. Bharat generates 70% of consumption.

The numbers are staggering. India's retail market is worth $1.1 trillion. Of this, organized retail is barely 12%. In categories Vishal operates in—apparel, general merchandise, FMCG—organized penetration in tier-2/3 cities is under 10%. This isn't a market share game; it's a market creation opportunity.

The demographic dividend everyone talks about? It's not happening in Bandra or Koramangala. It's happening in places like Gorakhpur, Guntur, and Guwahati. Cities with populations of 500,000 to 2 million, where the first generation of college graduates are earning ₹20,000-30,000 per month, where joint families are becoming nuclear, where aspirations are exploding but incomes aren't.

These consumers are fascinating in their complexity. They'll spend ₹50,000 on a wedding but haggle over ₹50 on daily groceries. They'll buy a ₹15,000 smartphone on EMI but need convincing to spend ₹300 on a branded shirt. They trust brands but can't afford brand premiums. They want modern retail experiences but with traditional bazaar prices.

The formalization of India's economy post-GST has been Vishal's tailwind. Every month, thousands of small traders shut shop, unable to navigate compliance requirements. Their customers don't disappear—they migrate to organized retail. Vishal, with its comparable prices and superior experience, becomes the natural destination.

The consumption patterns tell a story of gradual premiumization. The customer who bought ₹99 t-shirts two years ago now buys ₹149 ones. The family that shopped monthly now shops fortnightly. The basket that had only necessities now includes small indulgences—a ₹50 toy, a ₹100 perfume. Multiply these micro-upgrades by 145 million customers, and you have a growth engine.

But the real insight is about dignity. For Bharat consumers, shopping at Vishal isn't just about buying products—it's about participating in India's growth story. The air-conditioned store, the branded products, the fixed prices, the shopping bags with logos—these signal arrival, progress, respectability. Vishal isn't selling clothes; it's selling membership to modern India.

The competitive landscape in these markets is unique. D-Mart, the only comparable success story, focuses more on groceries and operates larger formats in bigger cities. Reliance Retail has the ambition but struggles with the economics—their cost structure is built for India, not Bharat. Regional players lack scale and sophistication. E-commerce players can't crack the unit economics at these price points.

Quick commerce, the current obsession of India's startup ecosystem, is irrelevant here. The economics of delivering a ₹200 order in 10 minutes don't work in cities where delivery boys earn ₹8,000 per month and petrol costs ₹100 per liter. More fundamentally, Bharat consumers don't need 10-minute delivery—they need trustworthy products at affordable prices.

The rise of digital payments has been transformative. UPI has made transactions frictionless, even for ₹100 purchases. This isn't just about convenience—it's about data. Every digital transaction creates a trail, enabling credit assessment, targeted marketing, inventory planning. Vishal's customers might earn ₹20,000 per month, but their digital footprints are invaluable.

Women are driving consumption in these markets. As workforce participation increases, as education levels rise, as family structures evolve, women are making more purchase decisions. Vishal's stores, safe and respectable, become spaces where women can shop independently—a small revolution in conservative tier-3 cities.

The infrastructure development—roads, electricity, internet—is accelerating consumption. A new highway reduces travel time to the nearest Vishal store from two hours to thirty minutes. 24-hour electricity means stores can stay open longer. 4G penetration means customers can browse products online before buying offline.

Climate patterns affect consumption in ways city dwellers don't understand. A good monsoon means strong rural income, which flows into tier-3 cities where farmers sell produce and buy necessities. A wedding season aligned with harvest creates consumption spikes. Vishal has learned to ride these cycles, stocking up before festivals, scaling down during lean periods.

The cultural nuances matter enormously. In South India, the color preferences, fabric choices, and sizing are completely different from North India. In the Northeast, winter wear sells year-round. In Gujarat, the vegetarian population means different FMCG product mixes. Vishal's store managers, usually locals, understand these subtleties in ways algorithms never could.

The education revolution in tier-2/3 cities is creating a new consumer class. Engineering colleges, nursing schools, polytechnics—these are producing young earners who want to signal their upward mobility through consumption. They might live in ₹3,000 per month PG accommodations, but they'll spend ₹500 on a branded jacket.

Government schemes like PM Awas Yojana, which provides housing for the poor, indirectly boost retail. A family moving from a slum to a pucca house needs everything—curtains, bedsheets, utensils, clothes. Vishal becomes the one-stop destination for setting up a new life.

The healthcare improvements—insurance coverage, generic medicines, government hospitals—mean families have more disposable income. Money previously kept aside for medical emergencies now flows into consumption. A ₹5,000 saving on medical expenses becomes a ₹5,000 shopping budget.

This is the India opportunity—not the 100 million people buying iPhones, but the 500 million entering the consumption economy. They don't want luxury; they want dignity. They don't need variety; they need reliability. They can't afford premiums; they can afford progress. And for this India, Vishal Mega Mart isn't just a retailer—it's a catalyst for social mobility, one ₹199 shirt at a time.

IX. Playbook: Lessons from the Turnaround

The Vishal Mega Mart story isn't just a business turnaround—it's a masterclass in transformation. From near-bankruptcy to billion-dollar valuation, the playbook written by TPG, refined by Partners Group, and executed by Gunender Kapur deserves its own business school case study.

Lesson 1: Sometimes the Best Strategy is Subtraction When TPG took over in 2010, their first instinct wasn't to expand but to contract. Of 170 stores, only 150 reopened. Product categories were slashed from seven to three. The supplier base was reduced from 1,000 to 300. Growth-obsessed founders rarely have the courage to shrink, but professional operators understand that sustainable growth requires solid foundations.

Lesson 2: Capital Structure Determines Destiny The genius of the TPG deal wasn't operational—it was financial. By splitting the business between TPG Wholesale and Airplaza Retail, they created a structure that minimized capital requirements while maintaining control. The franchise model meant expansion could happen with other people's money. This wasn't financial engineering for its own sake—it was architecture designed for sustainable growth.

Lesson 3: Patience is a Competitive Advantage TPG held Vishal for eight years. Partners Group has been invested for six and counting. In an era of quick flips and rapid exits, this patience enabled long-term thinking. Store leases were signed for 10 years, not three. Supplier relationships were nurtured over decades. Employee training programs lasted months, not weeks. When your investment horizon is measured in decades, you make different decisions.

Lesson 4: Operational Excellence Beats Strategic Brilliance Vishal's strategy is boringly simple: sell basic products at low prices in small cities. No artificial intelligence, no blockchain, no metaverse. The magic is in execution—ensuring every store has adequate inventory, every price tag is visible, every trial room is clean. In retail, the companies that win aren't the ones with the best strategies but the ones that execute basics flawlessly.

Lesson 5: Culture Eats Strategy for Breakfast The transformation from founder-led to professionally managed required cultural surgery. The cowboy culture of rapid expansion was replaced with disciplined growth. The personality-driven decision-making gave way to data-driven processes. But importantly, the customer-first DNA was preserved and amplified. Changing everything except what matters most—that's the art of transformation.

Lesson 6: The Right Leader for the Right Phase Ram Chandra Agarwal was perfect for starting Vishal—a visionary who saw opportunity where others saw poverty. But building a sustainable business required Gunender Kapur—an operator who understood systems, processes, and scale. The courage to change leadership, and the wisdom to pick the right leader, separated success from failure.

Lesson 7: Crises are Opportunities in Disguise Every crisis Vishal faced became a competitive advantage. The 2008 financial crisis led to the TPG acquisition and professional management. Demonetization accelerated digital payment adoption. COVID proved the resilience of the model. Companies that survive crises don't just endure—they evolve.

Lesson 8: Private Equity Can Add Real Value The caricature of private equity is financial engineers who cut costs and flip companies. The Vishal story shows PE at its best—bringing operational expertise, governance discipline, and patient capital. TPG didn't just provide money; they provided a playbook. Partners Group didn't just fund expansion; they enabled transformation.

Lesson 9: Understand Your Customer Better Than They Understand Themselves Vishal's customer insight goes beyond demographics. They understand that their customer doesn't want the cheapest products—they want products that look expensive but cost little. They don't want maximum variety—they want curated selection. They don't want just low prices—they want the dignity of shopping in a modern store. This psychological understanding drives every decision.

Lesson 10: The Unit Economics Must Work at Scale One The discipline of ensuring each store is profitable before opening the next seems obvious but is rarely practiced. The temptation to grow fast, to grab land, to plant flags is overwhelming. Vishal's discipline—proven unit economics before expansion—meant growth enhanced profitability rather than diluting it.

Lesson 11: Technology is a Tool, Not a Strategy While competitors chased digital dreams, Vishal used technology pragmatically. ERP systems for inventory management, not AI chatbots. Mobile apps for catalogs, not virtual reality shopping. Digital payments for convenience, not cryptocurrency experiments. Technology serving business needs, not business serving technology fantasies.

Lesson 12: Build for the Market You Have, Not the Market You Want Vishal could have chased the premium segment, competed with Shoppers Stop, targeted metros. But they understood their market—price-conscious, aspiration-filled, underserved. Building for the market you have, rather than the market you wish you had, is harder than it sounds.

Lesson 13: Franchising is About Alignment, Not Control The franchise model could have been a disaster—inconsistent experiences, quality issues, brand dilution. But by keeping franchisees invested (they keep 90% of revenue) while maintaining control (all merchandising, pricing, and branding decisions), Vishal created aligned incentives. The franchisees weren't vendors; they were partners.

Lesson 14: Debt is Poison for Retail Retail is a negative working capital business if done right—suppliers fund inventory, customers pay immediately. Adding debt to this equation is unnecessary and dangerous. Vishal's transformation began with debt elimination and continued with a philosophy of self-funded growth.

Lesson 15: Exit is Part of Entry From day one, TPG knew they would exit. This wasn't cynical—it was clarifying. Every decision was made with exit in mind: clean corporate structure, transparent accounting, scalable systems. Building to sell forced discipline that building to hold might not have.

The Vishal playbook isn't revolutionary—it's evolutionary. Take a broken business with a good concept. Fix the capital structure. Install professional management. Focus relentlessly on unit economics. Expand deliberately. Build systems that scale. Create value through operations, not financial engineering.

This playbook works beyond retail. Any business serving India's masses, any company in financial distress, any founder struggling with scale can learn from Vishal's journey. The lessons are universal: discipline beats vision, execution beats strategy, and patience beats speed.

For investors, the playbook offers a template for value creation in emerging markets. For operators, it provides a roadmap for transformation. For entrepreneurs, it's a cautionary tale about the perils of growth without profitability. But most importantly, it's proof that building a large, profitable business serving India's underserved isn't just possible—it's perhaps the greatest business opportunity of our time.

X. Bear Case vs. Bull Case

Bear Case: Why Vishal Mega Mart Might Stumble

The most glaring concern is valuation. Trading at a P/E of 100+, Vishal is priced for perfection. Any execution stumble, any growth deceleration, any margin compression, and the stock could face a violent correction. The current valuation implies Vishal will flawlessly execute store expansion while maintaining margins—a heroic assumption in retail, where Murphy's Law is the only law.

Company has a low return on equity of 8.53% over last 3 years. For a business generating 15-20% EBITDA margins, this ROE is surprisingly weak. It suggests that despite operational efficiency, the capital allocation might not be optimal. High-growth companies typically reinvest profits at high returns; Vishal's low ROE raises questions about future growth quality.

The competitive landscape is evolving rapidly. Reliance Retail, with infinite capital and political connections, is aggressively expanding into tier-2/3 cities. JioMart's integration with WhatsApp could change consumption patterns. D-Mart continues its methodical expansion. Regional players are consolidating. The white space Vishal enjoyed is shrinking.

Quick commerce might seem irrelevant today, but technology adoption in India has consistently surprised skeptics. If Blinkit or Zepto crack tier-2 city economics—through dark stores, micro-fulfillment centers, or innovative models—Vishal's store-based model could face existential questions. The shift might not happen in two years, but what about ten?

Execution risk with rapid expansion is real. Adding 100+ stores annually means hiring thousands of employees, signing hundreds of leases, managing complex supply chains. One food safety incident, one major fraud, one systematic failure in new store selection, and the entire growth story unravels. Retail is unforgiving—trust takes years to build, seconds to destroy.

The dependence on lower-income segments creates macroeconomic vulnerability. These consumers have no savings buffers. A recession, job losses, or inflation spike immediately impacts consumption. Unlike premium retailers whose customers can absorb shocks, Vishal's customers stop shopping when times get tough. The COVID resilience might have been luck, not structural strength.

Management succession remains unclear. Gunender Kapur has been instrumental in Vishal's transformation, but he's not young. Who succeeds him? Is there a second line of leadership? Can the culture survive a leadership transition? The history of retail is littered with companies that couldn't survive founder or key executive departures.

The franchise model, while capital-efficient, creates quality control challenges. As the network expands, maintaining standards becomes exponentially harder. One bad franchisee creating negative experiences could damage the brand. The 90% revenue share might incentivize sales over service, short-term gains over long-term brand building.

Inventory obsolescence is a perpetual risk in fashion retail. While Vishal focuses on basics, fashion trends affect even basic apparel. Excess inventory leads to markdowns, which destroy margins. The working capital efficiency Vishal enjoys could reverse quickly if inventory management falters.

Regulatory changes could impact economics. Changes in labor laws, real estate regulations, GST rates, or e-commerce policies could disproportionately affect organized retail. The government's populist tendencies mean policies favoring small traders over organized retail are always possible.

Bull Case: Why Vishal Mega Mart Could Soar

The growth runway is massive. With organized retail penetration in tier-2/3 cities under 10%, Vishal could triple its store count without market saturation. Adding 85 stores in FY25 to reach 696 stores is just the beginning. India has 500+ cities with populations over 100,000—each a potential Vishal location.

The unit economics are proven and consistent. Unlike speculative business models, every Vishal store follows a proven playbook with predictable returns. 15-20% EBITDA margins, three-year payback periods, positive cash flow from year one—this isn't hope, it's history. The model has worked across geographies, demographics, and economic cycles.

JP Morgan giving an Overweight rating and a target of Rs 133 signals institutional confidence. When global banks who've analyzed every retail model worldwide bet on Vishal, it suggests the opportunity is real. The recent stock performance validates this confidence.

Management has proven execution capability. The same team that managed the TPG turnaround, navigated COVID, and executed the IPO remains in place. They've demonstrated the ability to manage complexity, crisis, and growth simultaneously. This isn't a theoretical capability—it's demonstrated competence.

The consumption megatrend is unstoppable. India's per capita income is growing. Urbanization is accelerating. Nuclear families are proliferating. Women's workforce participation is increasing. These aren't cyclical trends but structural shifts that will drive consumption for decades.

Digital integration provides optionality. While stores remain core, the 8.7 million app users and quick commerce initiatives create multiple growth vectors. If e-commerce economics improve, Vishal is positioned to capture that opportunity. If they don't, the store model remains robust.

Private label penetration can expand further. At 73% of revenue, private labels already drive margins. But in categories like FMCG, private label penetration is still low. As customer trust increases, private label expansion could drive margin improvement without price increases.

The competitive moat is strengthening. Every new store increases buying power, improving terms with suppliers. The distribution network becomes more efficient with scale. The brand recognition in target markets deepens. These network effects make competing with Vishal increasingly difficult.

Operational leverage is kicking in. Fixed costs spread across more stores improve margins. Technology investments amortize over larger base. Management bandwidth utilized more efficiently. The next 100 stores will be more profitable than the last 100.

Capital allocation optionality exists. With strong cash generation and no debt, Vishal could pay dividends, buy back shares, or accelerate expansion. The capital flexibility means multiple paths to value creation exist.

The sustainability of the model has been proven. Through demonetization, GST, COVID—every crisis that should have killed Vishal made it stronger. This isn't luck but model resilience. If the business can survive black swan events, normal growth periods should be spectacular.

The Verdict

The bear case is about multiple compression and execution risk. The bull case is about a massive market opportunity and proven execution. Both are valid. The question isn't whether challenges exist—they do. It's whether the opportunity outweighs the risks.

For believers in India's consumption story, Vishal offers pure-play exposure to Bharat's rising aspirations. For skeptics, the valuation leaves no room for error. The truth, as always, lies somewhere in between. Vishal Mega Mart isn't a risk-free bet on India's future, but it might be one of the clearest ways to participate in the transformation of how 500 million Indians shop.

The ultimate arbiter will be execution. If Vishal can add 100 stores annually while maintaining margins, the bulls win. If competition intensifies, growth slows, or margins compress, the bears feast. In retail, there's no middle ground—you're either growing or dying. For Vishal Mega Mart, the next five years will determine which side of that equation they land on.

XI. Future Vision & Strategic Priorities

"Making aspirations affordable"—Vishal's tagline isn't just marketing copy, it's the organizing principle for the next decade of growth. As India adds 200 million people to its middle class by 2030, Vishal isn't just positioned to serve them—it's designed for them.

The immediate priority is geographic expansion, but not the scattershot approach of the past. The new strategy follows a cluster model: dominate a geography before moving to the next. In Uttar Pradesh, where Vishal has 150+ stores, the plan is to reach 250 before aggressive expansion elsewhere. This density creates economies of scale in distribution, marketing, and management that random expansion never could.

South India remains the white space. With limited presence in Karnataka, Tamil Nadu, and Andhra Pradesh, these markets represent 200 million consumers with higher per capita incomes than Vishal's current markets. But expansion here won't be copy-paste. South Indian consumers have different preferences—more formal wear, different color palettes, size variations. Vishal is building regional merchandising teams, conducting extensive consumer research, and potentially considering a different brand positioning for Southern markets.

Technology integration will accelerate, but pragmatically. The vision isn't to become an e-commerce player but to use technology to enhance store economics. RFID tags for inventory management, reducing shrinkage and stock-outs. Heat mapping in stores to optimize layouts. Predictive analytics for inventory planning. AI for personalized marketing to the 145 million customer base. Technology as an enabler, not an end in itself.

The omnichannel opportunity is unique for Vishal. Unlike metros where omnichannel means same-day delivery, in tier-3 cities it means different things. Click-and-collect, where customers order online but pick up from stores. Virtual inventory, where stores can sell products from other stores' inventory. Endless aisles, where stores can offer extended catalogs through kiosks. These models preserve store economics while expanding selection.

Category expansion will be selective. The temptation to add electronics, furniture, or other high-ticket categories exists, but Vishal's discipline will likely prevail. Instead, expansion within existing categories makes more sense. In apparel, moving slightly upmarket with a premium private label. In FMCG, adding more food categories as supply chain capabilities improve. In general merchandise, expanding home decor and lifestyle products as customers' disposable incomes grow.

Private label evolution is crucial. The current private labels are functional—they serve their purpose of offering value. The next generation will be aspirational. Sub-brands for different customer segments. Designer collaborations for festival collections. Sustainable lines for environmentally conscious consumers. The goal isn't to compete with national brands but to create Vishal-exclusive brands that customers seek out.

The financial services opportunity is tantalizing. Vishal's customers need credit for everything from children's education to home improvements. With transaction data on 145 million customers, Vishal could partner with fintechs to offer targeted credit products. Buy-now-pay-later for larger purchases. Gold loan counters in stores. Insurance products. This isn't about becoming a bank but about monetizing customer relationships beyond retail.

Supply chain sophistication will determine scalability. The current hub-and-spoke model works for 700 stores but might strain at 1,500. Investments in automation, regional distribution centers, and predictive logistics are planned. The goal is to reduce inventory days while improving fill rates—seemingly contradictory objectives that technology might reconcile.

Sustainability isn't just corporate responsibility—it's business strategy. Vishal's customers might not pay premiums for organic cotton, but they care about value. Sustainable practices that reduce costs—solar power for stores, efficient logistics routes, reduced packaging—align profit with purpose. The narrative of an Indian company serving Indian masses through sustainable practices resonates with stakeholders.

The talent challenge is real. Finding store managers who understand both retail operations and local markets is difficult. Vishal is investing in training programs, partnering with retail management institutes, and creating clear career paths from shop floor to senior management. The goal is to build a talent pipeline that can support 2,000 stores.

International expansion might seem premature, but neighboring markets beckon. Bangladesh, with similar demographics and consumption patterns, could be a natural extension. Nepal and Sri Lanka offer smaller but accessible opportunities. The playbook that works in Bihar might work in Dhaka. But this is vision, not plan—domestic opportunity remains enormous.

Consolidation opportunities will emerge. As formalization pressures intensify, regional chains will struggle. Vishal, with its operational excellence and capital access, could acquire distressed competitors. Not for their stores—most won't meet Vishal's standards—but for their market knowledge, supplier relationships, and talent.

The loyalty program evolution could be transformative. Currently transactional, the program could become a platform for engagement. Personalized offers based on purchase history. Tiered benefits creating aspiration. Community features connecting customers. In markets where customers are value-conscious but status-aware, a well-designed loyalty program could drive significant value.

Partnerships will multiply. With brands looking to reach Bharat consumers, Vishal offers unmatched access. Exclusive launches, co-branded products, brand shops within stores—these partnerships provide variety without inventory risk. For brands, Vishal offers distribution; for Vishal, brands provide differentiation.

The ultimate vision is audacious but achievable: becoming the Walmart of India. Not in size—that's unrealistic—but in significance. The default shopping destination for 500 million Indians. The platform through which global brands reach Bharat. The company that democratizes consumption while creating value for all stakeholders.

This vision faces challenges. Competition will intensify. Regulations might change. Technology could disrupt. Economic cycles will impact consumption. But Vishal's track record suggests they'll adapt, evolve, and ultimately thrive.

The next decade will determine whether Vishal Mega Mart becomes a footnote in India's retail history or a defining chapter. The strategy is clear, the execution capability proven, the opportunity massive. Making aspirations affordable isn't just a tagline—it's a mission that could transform how 500 million Indians experience prosperity. For Vishal Mega Mart, the future isn't about predicting change but creating it, one store, one customer, one affordable aspiration at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube