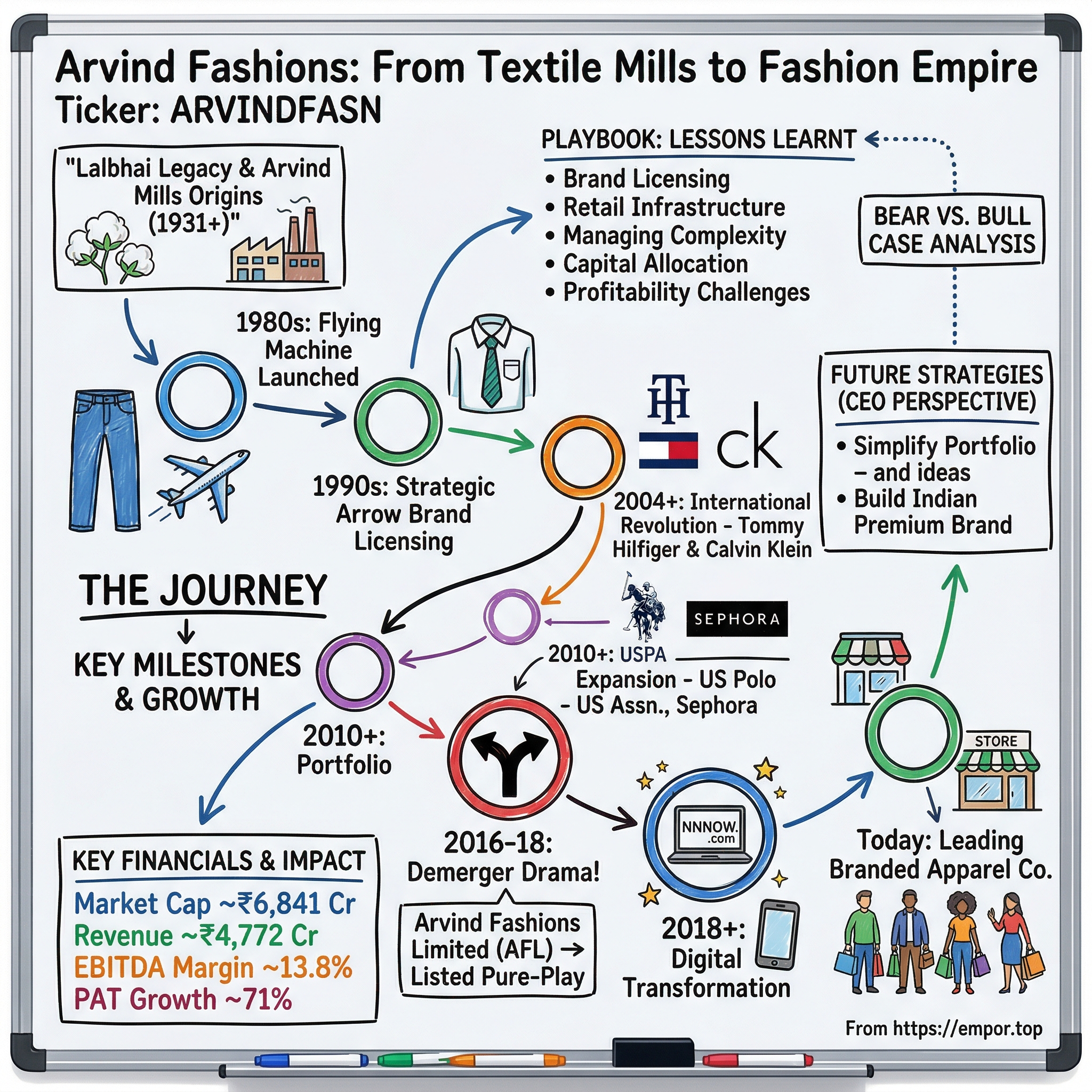

Arvind Fashions: From Textile Mills to Fashion Empire

I. Introduction & Episode Roadmap

Picture this: Inside a gleaming mall in Bangalore, a young software engineer walks past a Tommy Hilfiger store, its red-white-blue logo catching the afternoon light. Next door, a U.S. Polo Assn. outlet buzzes with weekend shoppers. Around the corner, Calvin Klein's minimalist storefront whispers luxury. What connects these global fashion icons in India? They're all part of one company's audacious bet that India could leapfrog from unbranded textiles to premium fashion—a bet placed by Arvind Fashions.

Today, Arvind Fashions stands as India's leading branded apparel company, commanding a market capitalization of ₹6,841 crore with revenues touching ₹4,772 crore. But this isn't just another retail conglomerate story. It's the tale of how a textile mill offshoot, born from Gandhi's Swadeshi movement, transformed itself into India's gateway for global fashion brands—managing over 28 distinguished brands across 1,300 standalone stores and 5,000 department store touchpoints spanning 192 cities.

The question that drives our exploration today: How did a company rooted in manufacturing cotton textiles for a newly independent India become the architect of premium fashion retail in the world's most populous nation? The answer reveals profound lessons about brand building in emerging markets, the art of international partnerships, and the delicate balance between aspiration and accessibility that defines modern Indian consumption.

Our journey spans nearly a century—from the Lalbhai family's response to Gandhi's call for self-reliance to today's omnichannel fashion powerhouse. We'll explore the denim revolution that democratized jeans in India, the strategic chess moves that brought Tommy Hilfiger and Calvin Klein to Indian streets, and the dramatic demerger that unlocked billions in shareholder value. Along the way, we'll uncover what Arvind Fashions teaches us about building fashion empires in markets where 'branded' itself was once a foreign concept.

II. The Lalbhai Legacy & Arvind Mills Origins

In 1931, the world was gripped by the Great Depression. Mills were shuttering across Lancashire, once the epicenter of global textile manufacturing. But in Ahmedabad, Gujarat, three brothers saw opportunity where others saw catastrophe. Kasturbhai, Narottambhai, and Chimanbhai Lalbhai established Arvind Mills in 1931, not despite the global economic turmoil, but because of it.

The founding was a direct response to Mahatma Gandhi's call for Swadeshi during India's independence struggle. Gandhi had urged Indians to boycott imported British textiles—particularly the fine and superfine fabrics that symbolized colonial economic dominance. People across India began boycotting these imported fabrics from England, creating both a political statement and a market vacuum.

The Lalbhai brothers reasoned brilliantly: the demand for quality fabrics hadn't disappeared; it had merely become politically unacceptable to import them. The Lalbhais reasoned that the demand for fine and superfine fabrics still existed, and any Indian company that met this demand would surely prosper. They raised ₹25.25 lakh in share capital—substantial money during the Depression—and acquired state-of-the-art machinery from England at fire-sale prices, as British mills desperately offloaded equipment.

The Lalbhai legacy stretched back further. The journey began in 1897 when Lalbhai Dalpatbhai decided to start manufacturing textiles and floated The Saraspur Manufacturing Company. This wasn't just business; it was nation-building through commerce. Lalbhai Dalpatbhai established Saraspur cotton mill in 1896, which became part of the swadeshi movement in India.

Kasturbhai Lalbhai, the driving force behind Arvind Mills, embodied the fusion of traditional merchant wisdom and modern industrial ambition. Born to a preeminent Jain family in 1894, he was forced to discontinue his studies at age 17 when his father died in 1912. He joined Raipur Mill as chairman in 1912, starting as a timekeeper but quickly moving to work with suppliers, traveling widely to understand the supplier market.

By the late 1930s, Arvind Mills wasn't just competing with imported textiles—it was beating them at their own game. Arvind's butta voiles were being exported to Switzerland and United Kingdom, thereby realizing the full potential of the spirit behind Swadeshi. The irony was delicious: a company born from boycotting British textiles was now exporting premium fabrics back to Britain. The transformation that occurred in the 1980s under Sanjay Lalbhai's leadership was nothing short of revolutionary. In the early 1980s, he led the 'Reno-vision' whereby the company brought denim into the domestic market, thus starting the jeans revolution in India. This wasn't incremental change—it was a complete reimagination of what an Indian textile company could be.

Consider the context: In 1980, jeans were virtually unknown in India. The idea of young Indians wearing denim was culturally alien, economically aspirational, and practically unavailable. Sanjay Lalbhai, who had taken over leadership from his father's generation, saw what others missed: India's youth were ready for a fashion revolution.

Over last four decades he has led the transformation of Arvind from a traditional textile mill into one of the world's leading manufacturers of denims, fine woven fabrics, and apparel solutions. He laid the foundations for the branded apparel business by bringing India's initial brands Flying Machine and Arrow, and opening Exclusive Brand Outlets.

The numbers tell a stunning story of growth. 1991: Arvind reached 100 million meters of denim per year, becoming the fourth-largest producer of denim in the world. By 1998: Arvind Mills emerged as the world's third largest manufacturer of denim. From zero to global top three in less than two decades—this wasn't just growth; it was conquest.

But the real genius lay not just in manufacturing but in brand creation. Flying Machine, India's first denim apparel brand, was launched to meet the aspira[tions] of a new generation. The company didn't just make fabric; it created desire, identity, and aspiration wrapped in indigo-dyed cotton.

As we transition from this industrial transformation to the fashion revolution that followed, we see how Arvind's mastery of denim manufacturing became the foundation for something far more ambitious: turning a textile manufacturer into India's premier fashion house.

III. The Birth of Fashion Business: Flying Machine & Early Brands (1980s-2000s)

Flying Machine wasn't born—it erupted. In 1980, when only smuggled jeans were available in India, when branded fashion was a concept understood only by the elite who traveled abroad, Arvind Mills did something audacious: they launched India's first homegrown denim brand. Born in the year 1980, we were considered a cult for the next 10 years. It's really hard to find a fashion conscious male from that time in India who did not wear denims made by us.

The timing couldn't have been more perfect—or more risky. India's middle class was awakening to global culture through Bollywood, liberalization was on the horizon, and young Indians were hungry for self-expression. Flying Machine didn't just fill a market gap; it created an entire category. Cornered substantial market with innovations of Indian fit, a 'guaranteed brand' available at a decent price.

By 1994 it had become a leader in branded jeans in India and remained trendy and premium. The transformation was remarkable: in just 14 years, Flying Machine went from an experiment in domestic denim to market dominance. Flying Machine's growth story began in 1994, when it became the first Indian denim brand to introduce stone-washed denim, a popular trend at the time.

But Flying Machine was just the opening act. It also started retail outlets for 'Arrow' brand and became the first company in India to bring international shirt brand 'Arrow'. Arrow represented something entirely different—the promise of American corporate success, the crisp white shirt that signaled professional arrival. This wasn't about rebellion; it was about aspiration. The genius of Arrow's introduction to India lay in perfect timing and positioning. Arrow is known for its classic American styling. The brand's heritage is in dress shirts, and its offerings have expanded to include sportswear. Arrow is licensed in approximately 120 territories, with almost 400 free-standing stores globally. When Arvind brought Arrow to India, they weren't just importing shirts—they were importing the American Dream, tailored for Indian ambitions.

Arrow has always been a preferred brand for Indian professionals due to its rich heritage value, impeccable style, and strong sense of innovation. The brand's main goal is to cater to the ever-changing sartorial needs of India's working men. This wasn't accidental positioning—it was surgical precision targeting of India's emerging white-collar workforce.

The infrastructure Arvind built during this period was staggering. Arrow currently has over 200 exclusive stores and is available in over 1000 multi-brand outlets in 109 cities across India. This wasn't just distribution; it was colonization of India's retail landscape before modern retail even existed.

But perhaps the most important development of this era was the creation of a playbook that would serve Arvind for decades: identify global brands that resonate with Indian aspirations, secure licensing rights, leverage manufacturing capabilities for local production, build exclusive retail infrastructure, and scale rapidly across the country. This formula, perfected with Flying Machine and Arrow, would become the foundation for everything that followed.

The export business that developed alongside domestic brands was equally impressive. The company's ability to manufacture for global brands while building its own created a virtuous cycle of capability enhancement and market understanding that competitors couldn't match.

As we move into the story of international brand partnerships, we see how these early experiments with Flying Machine and Arrow weren't just successful products—they were proof of concept for a much grander vision.

IV. The International Brand Revolution (2004-2014)

In April 2004, the Murjani Group launched the first International Lifestyle Designer Brand in India – Tommy Hilfiger. This wasn't just another licensing deal—it was a cultural earthquake. For the first time, a truly global premium fashion brand was available in Indian stores, not through grey market imports or duty-free shops, but as a legitimate, locally supported business.

The partnership structure was sophisticated: Murjani Group held the master license while Arvind handled manufacturing and retail through a joint venture called Arvind Murjani Brands. AMB has been the apparel sublicensee of the Tommy Hilfiger brand since its introduction in the Indian market in 2004. This tripartite arrangement leveraged Murjani's global brand relationships, Arvind's manufacturing prowess, and both parties' understanding of the Indian market.

The numbers were staggering. According to sources, Tommy Hilfiger is doing business of around Rs 200 crore in India and growing at 50 per cent every year. Fifty percent annual growth—in any market, that's explosive. In India's nascent premium fashion market, it was revolutionary. The real magic happened when Mr. Shailesh Chaturvedi joined Arvind in 2006 to lead our Tommy Hilfiger JV. Over the past 15 years, he has made Tommy one of the most admired and aspirational brands in the country. Chaturvedi wasn't just a manager—he was an architect of aspiration. With expertise in development of premium fashion brands, Shailesh has 25 years of work experience in apparel retail industry. He runs business of Tommy Hilfiger and Calvin Klein brands of US Multinational company PVH as their 'Managing Director and CEO' in India in their JV with Arvind grp here.

The transformation was remarkable. The business has retail size in excess of Rs 1,000 Cr—from ₹200 crore to over ₹1,000 crore, a five-fold increase that validated the strategy. Tommy Hilfiger products are distributed in India through a network of more than 80 standalone stores and shop-in-shops across 30 cities, including Delhi, Mumbai, Bangalore, Chandigarh and Hyderabad.

By 2011, the partnership evolved dramatically. Owned by PVH Corp, the American group recently announced that it has bought out Murjani Group's license for the Tommy Hilfiger trademarks in India. It has also purchased Murjani Group's 50 per cent stake in Arvind Murjani Brands, which has been the apparel sub-licensee of the Tommy Hilfiger brand since its introduction in the Indian market in 2004. Tommy Hilfiger has now become a joint-venture partner with Arvind Limited, which continues to own the remaining 50 per cent stake. The Calvin Klein partnership in 2014 represented the culmination of Arvind's international brand strategy. PVH Corp, the owner of the Calvin Klein trademarks worldwide, announced that Arvind Brands and Retail Limited, a subsidiary of Arvind Limited, has replaced PVH's prior joint venture partners in Premium Garments Wholesale Trading Private Limited, the licensee of the Calvin Klein trademarks in India.

The significance of this deal cannot be overstated. Calvin Klein is one of the strongest fashion brands in the world and we are delighted to be JV partners with PVH for Calvin Klein in India. This relationship also strengthens our 20 years association with PVH, which started with the ARROW license and since has been extended to our joint venture with PVH for the Tommy Hilfiger business and the license for IZOD.

What made these partnerships revolutionary wasn't just the brands themselves but the infrastructure Arvind built to support them. By focusing on exclusive brand outlets (EBOs), Arvind created temple-like retail experiences that elevated shopping from transaction to aspiration. These weren't just stores—they were embassies of global fashion culture planted in Indian soil.

The numbers validated the strategy magnificently. By 31 March 2024, the JV operated a total of 221 exclusive brand outlets (EBOs) in India—136 Tommy Hilfiger and 85 Calvin Klein. The infrastructure build-out during this period was nothing short of remarkable—Arvind wasn't just distributing brands; it was creating an entirely new retail ecosystem.

The licensing model Arvind perfected during this era became a template for emerging market brand building: secure rights to aspirational global brands, leverage local manufacturing capabilities to manage costs, build exclusive retail infrastructure to control brand experience, and scale rapidly before competitors could react.

As we transition to the portfolio expansion phase, we'll see how these international partnerships became the foundation for an even more ambitious strategy: building India's first true fashion conglomerate.

V. The Portfolio Expansion: Building a Fashion Conglomerate (2010-2016)

U.S. Polo Assn. became the cornerstone of Arvind's affordable premium strategy—a brand that carried American heritage but at price points accessible to India's burgeoning middle class. Arvind Brands has been the exclusive manager and authorized supplier of the U.S. Polo Assn. brand in India since 2007.

The brand's growth trajectory was explosive. Out of the company's revenue last year of Rs 4259 crore, US Polo was close to Rs 2,000 crore. From inception to becoming nearly half of Arvind Fashions' revenue—this wasn't just success; it was domination of the affordable premium segment.

What made U.S. Polo Assn. brilliant positioning was its authentic connection to sport while remaining accessible. brand products are authentic and officially sanctioned by the United States Polo Association, the governing body for the sport of polo in the United States since 1890. This gave it legitimacy that copycat brands couldn't match, while its pricing made it attainable for aspirational consumers who couldn't afford Tommy Hilfiger or Calvin Klein.

The infrastructure buildup during this period was staggering. USPA Properties, Inc. and Arvind expect to operate a total of 100 stores in India by the end of 2012. The actual growth exceeded even these ambitious targets. Today, our brands grace over 1,300 standalone stores and approximately 5,000 departmental and multi-brand stores in more than 192 cities and towns across India. The Bridge to Luxury segment represented Arvind's most ambitious move yet. Sephora, which first launched into the Indian beauty market in 2012 has been ran by Arvind Fashions for the past eight years. This wasn't just adding another fashion brand—it was entering an entirely new category: prestige beauty retail.

The acquisition of business operations was systematic and strategic. On 27 September 2012, Arvind's subsidiary Arvind Lifestyle Brands announced the acquisition of the business operations of British fashion retailers Debenhams and Next and American Lifestyle brand Nautica in India from Planet Retail. The acquisition of Debenhams signals the entry of Arvind into the Bridge to Luxury Department Store Segment.

What made this portfolio expansion brilliant was its comprehensiveness. We take great pride in having an unmatched future ready portfolio including iconic global brands GANT, NAUTICA, Calvin Klein and Sephora which dominate our Bridge to Luxury segment. Arvind wasn't just collecting brands; it was building a fashion ecosystem that covered every price point, every occasion, and every aspiration level of the Indian consumer.

The numbers during this period were extraordinary. Today Arvind Fashions is home to over 28 distinguished brands cutting across all formats of retail. From a single homegrown denim brand to 28 distinguished brands—this transformation represented one of the most aggressive brand portfolio expansions in global fashion retail history.

Category expansion was equally impressive. Arvind moved beyond apparel into beauty (Sephora), footwear (through brand extensions), accessories, and even innerwear. Each expansion leveraged existing infrastructure while opening new revenue streams.

The operational complexity of managing this portfolio was staggering. Each brand required distinct positioning, separate supply chains, unique marketing strategies, and dedicated teams. Yet Arvind made it work through what they called their "Will Do" culture—a relentless focus on execution that turned complexity into competitive advantage.

As we approach the demerger story, we'll see how this massive portfolio expansion set the stage for one of Indian retail's most significant corporate restructurings.

VI. The Demerger Drama: Birth of a Listed Fashion Pure-Play (2016-2018)

October 2016 marked a watershed moment. Arvind Ltd, one of India's largest integrated textile and apparel companies, has divested 10 per cent stake in its brand business subsidiary Arvind Lifestyle Brands to Multiples, the private equity firm founded by Renuka Ramnath. At an enterprise value of Rs 8,000 crore, the deal is valued at Rs 740 crore.

The valuation was stunning—₹8,000 crore for a business that had been built over just two decades. This wasn't just financial engineering; it was validation of Arvind's transformation from textile manufacturer to fashion powerhouse. The deal crystallized value that had been hidden within the conglomerate structure.

But the Multiples investment was just the opening act. On 8 November 2017, Arvind Limited, India's largest textile and branded apparel player, announced its decision to demerge its Branded Apparel and Engineering businesses from the parent company. The Branded Apparel business will be demerged into the entity Arvind Fashions Limited.

The demerger structure was elegant in its simplicity. Shareholders of Arvind Limited will be entitled for 1 equity shares of Arvind Fashions Limited for every 5 shares held by them. This meant existing shareholders automatically became owners of the new fashion pure-play without having to invest additional capital.

The rationale was compelling. Textile manufacturing and fashion retail are fundamentally different businesses—different capital requirements, different growth trajectories, different valuation multiples. By separating them, each entity could pursue focused strategies, access appropriate capital, and be valued on its own merits.

The market response validated the strategy. Post-demerger, investors could choose between a stable, cash-generating textile business and a high-growth fashion retail play. The sum of the parts proved greater than the whole—exactly as management had predicted.

The demerger also solved a crucial problem: complexity. Managing 28 brands while running textile manufacturing operations had created operational and strategic tensions. Now, Arvind Fashions could focus purely on brand building and retail expansion without the distraction of manufacturing concerns.

As we move into the digital transformation era, we'll see how this newly independent Arvind Fashions leveraged its focused structure to accelerate omnichannel capabilities and navigate the COVID-19 crisis.

VII. Digital Transformation & Omnichannel Evolution (2018-Present)

The launch of NNNOW.com marked Arvind Fashions' entry into the digital commerce era. They are also available online on our proprietary e-commerce platform, NNNOW.COM, and other third-party online marketplaces. Under the leadership of Nitesh Kanchan is the CEO of NNNOW at AFL and is responsible for strategising, building and growing the globally renowned speciality beauty retailer. The platform became the digital backbone for Arvind's omnichannel strategy, unifying inventory across stores and online channels.

The timing couldn't have been more prescient. When COVID-19 struck in March 2020, Arvind's digital infrastructure became its lifeline. Arvind Fashions Ltd (AFL), part of Ahmedabad-based Lalbhai group, has opted to use moratorium on loan repayment amid closure of stores resulting in significant weakening of cash flows due to national lockdown to combat coronavirus spread.

The pandemic's impact was devastating. Arvind Fashions Ltd has registered a consolidated loss after tax of Rs 217.79 crore for the quarter ended September 30, 2020 in financial year 2020-21. Revenue collapsed as With the outbreak of Covid-19, while footfalls had started getting impacted from early March, malls were already being asked to close by mid-March, a complete lockdown implemented across the country starting March 25, this led to full shutdown of the store network, offices and warehouses.

But Arvind's response was swift and strategic. In addition, structural reductions have been effected in the cost structure that will have the impact of reducing company's breakeven levels by 35%. The company pivoted aggressively to digital, accelerating online fulfillment capabilities and reimagining the customer journey.

The recovery demonstrated remarkable resilience. By FY25, the transformation was evident: 4,620 Cr (+8% YoY), EBITDA: Rs. 637 Cr (+17%), PAT: Rs. 85 Cr (+71%) with ROCE ~20% The company had not just recovered—it had emerged stronger.

Shailesh Chaturvedi, who assumed leadership in the post-pandemic period, focused on profitability and portfolio rationalization. He steered the company out of COVID-induced disruption, improving gross margins to ~54%, expanding EBITDA margins to 13.8%, and growing PAT by 71% in FY25. Chaturvedi championed sharper category focus (especially in women's and footwear), exited non-performing labels reduced debt, and improved inventory turns.

The digital transformation extended beyond e-commerce. Arvind integrated technology across operations—from inventory management to customer analytics, from supply chain optimization to personalized marketing. The company built capabilities in social commerce, influencer partnerships, and direct-to-consumer channels that traditional retailers struggled to match.

VIII. Current Portfolio & Market Position

Today's Arvind Fashions stands as a testament to strategic focus and operational excellence. On a full-year basis, the company's revenue rose to Rs 4,620 crore in FY25, clocking a growth of 8.5 per cent YoY with a carefully curated portfolio that balances aspiration with accessibility.

The brand performance tells a story of concentration and excellence. U.S. Polo Assn. remains the crown jewel, contributing nearly half of revenues while maintaining strong growth momentum. Tommy Hilfiger and Calvin Klein continue to dominate the premium segment, with Core focus: US Polo Assn., Arrow, Flying Machine, Tommy Hilfiger, Calvin Klein (targeting Rs. 500–Rs. 1,000 Cr per brand)

The retail footprint has evolved from mere expansion to strategic densification. Retail network (as of Mar'25): 977 exclusive brand outlets + ~0.12 m sq ft net expansion; presence in ~9,000 MBOs/department stores Each store location is now data-driven, optimized for catchment demographics and competitive dynamics.

The competition landscape has intensified dramatically. Aditya Birla Fashion, with its acquisition spree including Forever 21 and Reebok, poses a formidable challenge. Reliance Brands leverages its parent's retail infrastructure and deep pockets to secure premium licenses. Tata CLiQ brings the credibility of the Tata brand to online fashion retail.

Yet Arvind maintains distinct advantages. Its decades-long relationships with global brands create switching costs competitors can't overcome. The manufacturing heritage provides cost advantages and speed-to-market capabilities pure retailers lack. Most importantly, the institutional knowledge of Indian consumers—their fit preferences, price sensitivities, and aspiration patterns—creates a moat that's hard to replicate.

The India fashion market opportunity remains massive and underpenetrated. With per capita apparel spending at just $60 compared to $300+ in developed markets, the runway for growth extends decades. The formalization of retail, the rise of tier-2 and tier-3 cities, and the demographic dividend of young consumers entering their peak earning years all point to sustained expansion.

Portfolio management has become increasingly sophisticated. The exit from Sephora—Notable exits: Sold Sephora division (Rs. 337 Cr revenue in FY23) to Reliance Retail (~Rs. 99 Cr deal, 26 stores across 13 cities)—demonstrated discipline in pruning non-core assets. The focus on five power brands allows for deeper investment in each, creating stronger competitive positions.

The operational metrics reflect this focus. Gross margin at ~54%, EBITDA margin at ~13.8%, Net debt reduced from Rs. 300 Cr to Rs. 225 Cr These aren't just numbers—they represent a fundamental transformation in how Arvind Fashions operates, from a growth-at-any-cost mentality to profitable, sustainable expansion.

IX. Playbook: Business & Investing Lessons

The Arvind Fashions story offers a masterclass in building fashion businesses in emerging markets. The playbook they've developed over decades reveals timeless principles that transcend industries and geographies.

The Art of Brand Licensing in Emerging Markets

Arvind's approach to international partnerships demonstrates that successful licensing isn't about passive distribution—it's about active brand building. The company doesn't just sell Tommy Hilfiger shirts; it creates the entire ecosystem that makes Tommy Hilfiger relevant to Indian consumers. This includes localized sizing, culturally appropriate marketing, and price architecture that balances aspiration with accessibility.

The genius lies in the structure: joint ventures rather than pure licensing ensure skin in the game from both parties. Global brands bring heritage and design; Arvind brings market knowledge and execution. This alignment of interests creates sustainable partnerships measured in decades, not years.

Building Retail Infrastructure from Scratch

When Arvind started opening exclusive brand outlets in the 1990s, organized retail barely existed in India. The company had to create everything—from training sales staff who had never worked in modern retail to educating mall developers about international brand requirements.

This infrastructure investment seemed irrational at the time. Why build expensive stores when wholesale distribution was profitable and asset-light? The answer became clear over time: controlling the brand experience was worth the capital investment. Today, Arvind's EBO network is its biggest competitive advantage, creating barriers to entry that pure online players can't match.

Managing Portfolio Complexity

Running 28 brands simultaneously seems like a recipe for disaster. Yet Arvind made it work through what they call "commonality with differentiation"—shared back-end infrastructure with distinct front-end experiences. Warehouses, logistics, and technology systems are common across brands. But each brand maintains its unique identity through separate buying teams, marketing strategies, and store designs.

The key insight: complexity is manageable if you standardize what customers don't see and differentiate what they do see. This allows for economies of scale without brand dilution.

Capital Allocation in Fashion Retail

Fashion retail is notoriously capital-intensive, with three major buckets competing for resources: inventory, marketing, and store expansion. Arvind's capital allocation framework prioritizes based on return velocity rather than absolute returns.

Inventory turns faster than stores generate returns, so working capital gets first priority. Marketing spend that drives same-store sales growth gets priority over new store openings. This disciplined approach explains how Arvind maintained growth even during capital-constrained periods.

The Challenge of Profitability in Indian Retail

Indian retail presents unique profitability challenges: high real estate costs relative to purchasing power, fragmented supply chains that increase logistics costs, and cultural expectations of discounts and sales. Arvind's solution was vertical integration—not complete manufacturing ownership, but strategic control of critical nodes in the value chain.

By maintaining some manufacturing capability, Arvind can capture margin at multiple points: brand licensing fees, manufacturing margins, and retail margins. This multi-layer profitability model provides cushion during downturns and leverage during upturns.

X. Analysis & Bear vs. Bull Case

Bull Case: The India Consumption Story Has Just Begun

The bullish argument for Arvind Fashions rests on three pillars: market growth, operational leverage, and brand strength.

India's fashion market is at an inflection point. With 65% of the population under 35, rising disposable incomes, and increasing fashion consciousness, the addressable market expands daily. The shift from unbranded to branded apparel—still only 35% of the total market—represents a multi-decade opportunity.

Arvind's operational leverage is finally showing. After years of investment in infrastructure, technology, and brands, incremental revenue now flows disproportionately to the bottom line. Our mantra of profitable growth has helped in achieving the milestone of ROCE crossing 20 per cent," stated Shailesh Chaturvedi, Managing Director (MD) and Chief Executive Officer (CEO), Arvind Fashions.

The brand portfolio, carefully curated over decades, covers every price point and occasion. This isn't easily replicable—relationships with global brands like PVH take decades to build and can't be bought with capital alone.

The successful expansion into new categories—footwear growing at 30%+ annually, women's wear approaching 40% of sales—demonstrates that the growth algorithm works beyond the core men's apparel business. Each category expansion leverages existing infrastructure while opening new TAM.

Digital capabilities, accelerated by COVID, position Arvind well for the omnichannel future. While pure online players struggle with profitability and traditional retailers struggle with digital, Arvind operates profitably across channels.

Bear Case: Structural Challenges in a Changing Market

The bearish perspective points to concerning trends beneath the surface growth.

The company has delivered a poor sales growth of 5.04% over past five years. Company has a low return on equity of 3.11% over last 3 years. These metrics suggest that despite the India growth story, Arvind hasn't been able to capture value proportional to market expansion.

Competition has intensified dramatically. Reliance Brands' unlimited capital, Aditya Birla Fashion's aggressive M&A, and nimble D2C brands attacking specific categories all pressure margins and market share. The moats that protected Arvind for decades—brand relationships and retail infrastructure—matter less in a digital-first world.

Consumer preferences are shifting faster than ever. The rise of fast fashion, sustainable fashion, and athleisure all challenge Arvind's traditional brand portfolio. Younger consumers show less brand loyalty and more price consciousness than previous generations.

The dependence on mall retail remains concerning. Despite digital investments, 70%+ of revenue still comes from physical stores, mostly in malls. Any structural shift away from mall shopping—accelerated by COVID but continuing post-pandemic—directly impacts Arvind's economics.

Working capital requirements remain stubbornly high. Fashion retail requires significant inventory investment, and Arvind's multi-brand model multiplies this challenge. In a rising interest rate environment, this capital intensity becomes a drag on returns.

The international brand dependency creates vulnerability. If PVH or USPA decides to go direct in India—as many brands eventually do in large markets—Arvind loses not just revenue but identity. The company's own brands like Flying Machine haven't achieved the scale or profitability to compensate for potential license losses.

XI. Epilogue & "If We Were CEOs"

If we were sitting in the CEO's chair at Arvind Fashions today, the path forward would require bold choices that balance heritage with disruption.

First, we'd dramatically simplify the portfolio. Five power brands—U.S. Polo Assn., Tommy Hilfiger, Calvin Klein, Arrow, and Flying Machine—would receive 90% of resources. Everything else would be divested or discontinued. Complexity is a hidden tax that prevents excellence.

Second, we'd build a true Indian premium brand from scratch. Flying Machine proved Arvind can create brands, not just distribute them. India's cultural confidence has never been higher—witness the global success of Indian music, movies, and cuisine. A premium Indian fashion brand that celebrates this confidence could be Arvind's next billion-dollar opportunity.

Third, we'd separate the licensing business from owned brands, potentially through a tracking stock or subsidiary listing. These are fundamentally different businesses with different risk profiles and growth trajectories. Investors should be able to choose their exposure.

Fourth, we'd accelerate the shift from retail to platform. Instead of opening more stores, we'd create infrastructure that enables other brands to succeed in India. This could include logistics networks, technology platforms, or even brand incubation services. The goal: capture value from India's fashion growth without bearing all the inventory risk.

Finally, we'd prepare for the post-license future. Every international brand partnership will eventually end—either through termination or acquisition. Building capabilities that survive beyond any single brand relationship ensures long-term sustainability.

What Arvind Fashions teaches us transcends fashion or India. It's a story about building bridges—between global and local, between aspiration and accessibility, between heritage and modernity. In emerging markets, success comes not from importing developed market models wholesale but from creative adaptation that respects local context while embracing global standards.

The company that started as a response to Gandhi's call for self-reliance became India's gateway to global fashion. The next chapter will determine whether it can transcend this gateway role to become a global fashion force in its own right. The foundation is built, the capabilities exist, and the market opportunity has never been larger.

For investors, Arvind Fashions represents a complex but compelling opportunity. It's a play on Indian consumption, a bet on premiumization, and a wager that execution can overcome structural challenges. The stock won't move in straight lines—fashion never does—but for those willing to embrace the volatility, the long-term opportunity mirrors India's own transformation from emerging to emerged.

The threads that Kasturbhai Lalbhai began spinning in 1931 have woven themselves into the fabric of modern India. From khadi to Calvin Klein, from textile mills to Tommy Hilfiger, from Flying Machine to fashion empire—Arvind's journey mirrors India's own evolution. And like India itself, the best chapters may still be unwritten.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube