Whirlpool of India: From American Dreams to Indian Reality

I. Introduction & Episode Roadmap

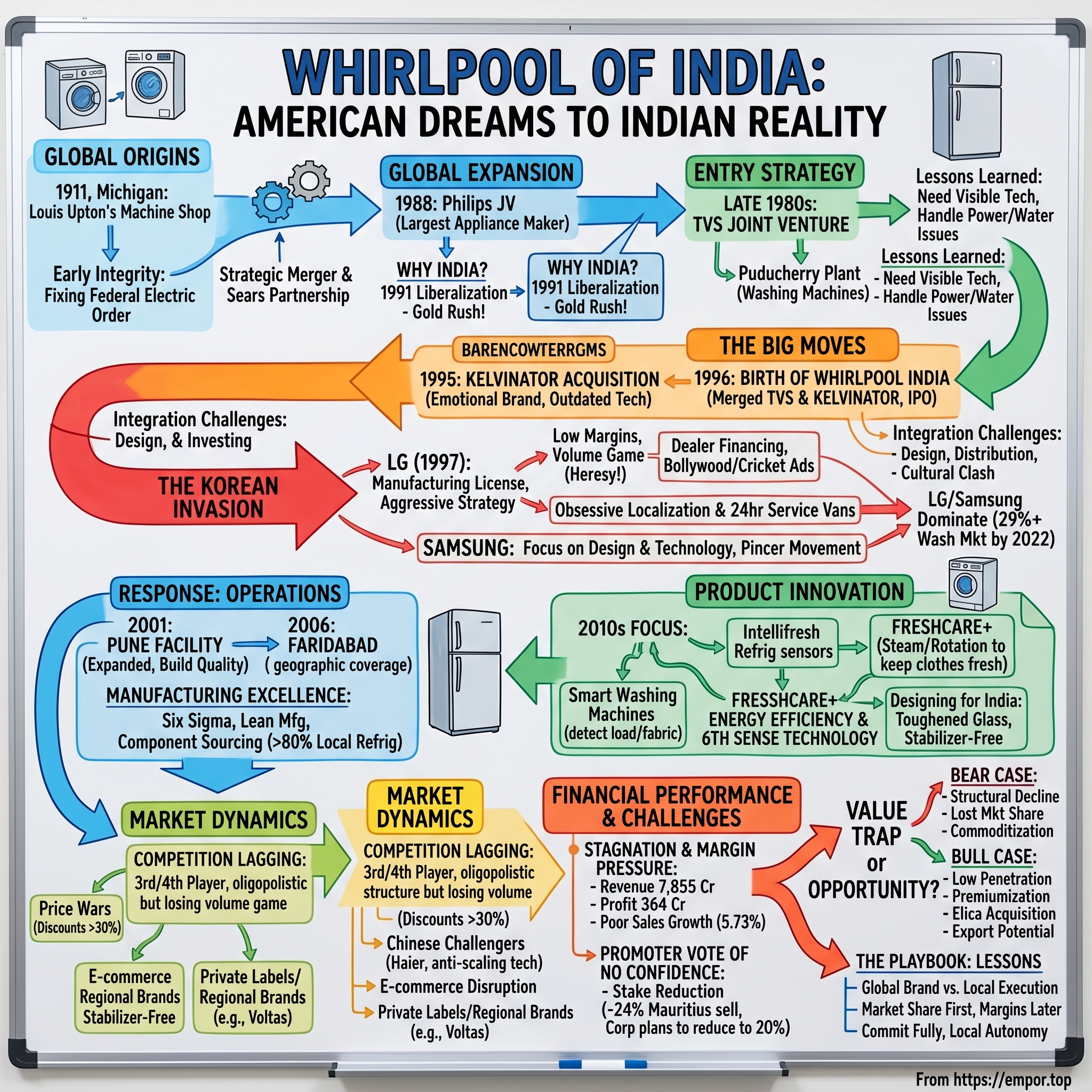

Picture this: It's 1996 in New Delhi. The Indian economy has just opened its doors to the world after decades of socialist policies. Shopping malls are sprouting up, cable TV is bringing global brands into middle-class homes, and suddenly, owning a washing machine isn't just for the ultra-rich anymore. Into this churning market steps Whirlpool Corporation—the Michigan-based appliance giant that had conquered America—ready to plant its flag in what would become one of the world's most promising consumer markets.

Today, Whirlpool of India generates ₹7,855 crores in revenue, operates three massive manufacturing facilities, and battles daily with Korean giants in one of the world's most competitive appliance markets. But here's the thing that should keep you up at night if you're an investor: despite being one of the first movers among global brands in liberalized India, Whirlpool currently holds just the fourth position in market share, trailing LG, Samsung, and even local player Videocon in various categories.

How did an American appliance giant with a century of manufacturing excellence end up playing catch-up in a market it entered before its fiercest competitors? Why does a company with Whirlpool Corporation's global scale and technology struggle to dominate in India while Korean brands that arrived later now rule the roost?

This is a story of joint ventures and acquisitions, of global ambitions meeting local realities, of premium technology clashing with price-sensitive consumers. It's about how localization isn't just about making smaller refrigerators or cheaper washing machines—it's about understanding that an Indian family might use their washing machine twice a day during monsoons but worry about water scarcity in summer. It's about realizing that "Made in America" doesn't automatically mean premium in a market where Korean brands outspend you 10-to-1 on cricket sponsorships.

We'll trace Whirlpool's journey from its calculated entry through the TVS joint venture, through the ambitious Kelvinator acquisition that should have cemented its dominance, to the Korean invasion that changed everything. We'll examine why a company that makes excellent products with strong manufacturing capabilities trades at modest multiples while the market it operates in continues to grow at double digits.

Most importantly, we'll extract the playbook—what works and what doesn't when a global giant enters an emerging market. Because Whirlpool of India's story isn't just about appliances. It's about the perpetual challenge every multinational faces: How do you balance global scale with local relevance? How do you compete when your competitors are willing to lose money for a decade to gain market share? And ultimately, is being a solid number four in a massive growing market better than being number one in a mature, slow-growth market?

The answers might surprise you. And they definitely matter if you're thinking about the next decade of consumer businesses in emerging markets.

II. The Whirlpool Corporation Story & Global Context

Let's start in 1911 St. Joseph, Michigan—a small town on the shores of Lake Michigan, where winters were brutal and doing laundry meant backbreaking work over washboards and tubs. Louis Cassius Upton, a failed insurance salesman who'd just lost his investment in an appliance dealership, received an unusual form of compensation: a patent for a manual clothes washer. Most people would have seen it as worthless paper. Louis saw opportunity.

He approached his uncle Emory, who owned a machine shop, with a simple question: could they add an electric motor to this design? With a $5,000 investment from Chicago retail executive Lowell Bassford, they began producing electric motor-driven wringer washers. On November 11, 1911, the Upton Machine Company was officially formed—not in some grand industrial facility, but in what was essentially a converted machine shop.

The early days were defined by a philosophy that would echo through a century: do the right thing, even when it hurts. When their first major order of 100 washing machines from Federal Electric revealed a catastrophic flaw—every single cast-iron gear failed—Louis Upton personally worked with Federal's management to fix the problem, replacing each gear with a new cut-steel piece. Federal, impressed by this integrity, immediately ordered 100 more machines. In an era when caveat emptor ruled business, this was revolutionary thinking.

By 1916, the Uptons had caught the attention of a Chicago retailer that was revolutionizing American commerce: Sears, Roebuck and Company. The partnership that began with washers sold under Sears' "Allen" brand would become one of the longest-running supplier relationships in American business history. By 1925, Upton had become the exclusive supplier of electric and gasoline-powered washing machines for Sears—a relationship that would fundamentally shape both companies' destinies.

The transformation from regional supplier to national player came through a strategic merger. In 1929, the increasing volume of sales led Upton to merge with the Nineteen Hundred Washer Company of Binghamton, New York, adopting the name Nineteen Hundred Corporation. This wasn't just about scale—it was about survival through the Great Depression that would soon devastate American industry.

World War II tested the company's adaptability. Factories converted to armament production, but leadership was already thinking ahead. In 1947, they introduced an automatic, spinner-type washer sold by Sears under the "Kenmore" brand, and a year later under their own "Whirlpool" brand name. This dual-brand strategy—private label for Sears, proprietary brand for independent dealers—would become a template for appliance industry distribution.

The pivotal moment came in 1949. The Nineteen Hundred Corporation was renamed as the Whirlpool Corporation, signaling ambitions beyond washing machines. Lou Upton retired as president and was replaced by Elisha "Bud" Gray II, marking a transition from founder-led to professional management—a shift that would enable massive expansion.

The 1950s brought aggressive diversification. In 1955, Whirlpool acquired Seeger Refrigerator Company and RCA's air conditioner and cooking range lines, transforming from a laundry specialist to a full-line appliance manufacturer. The 1986 acquisition of KitchenAid added premium positioning. By 1978, annual revenues exceeded $2 billion.

But it was the global expansion strategy of the late 1980s that would lead Whirlpool to India. In 1988, Whirlpool bought a 53% stake in the large-appliance division of Philips N.V., creating a joint venture that made Whirlpool the world's largest manufacturer of major appliances, with annual sales of approximately $6 billion. The company wasn't just buying market share—it was building a platform for emerging market entry. Why India? For Whirlpool Corporation, watching the world's second-most populous nation emerge from decades of socialist policies was like watching a massive consumer market being born in real-time. In 1991, India faced a severe balance of payments crisis—foreign exchange reserves fell to dangerously low levels, covering less than three weeks of imports. The reforms formally began on July 1, 1991, when RBI devalued the rupee by 9% and by a further 11% on July 3.

This wasn't just another economic adjustment. This was the dismantling of the License Raj—a Byzantine system of permits and quotas that had strangled Indian business for four decades. From 1992 to 2005, foreign investment increased by 316.9%, and India's GDP grew from $266 billion in 1991 to $2.3 trillion in 2018. For American multinationals, it was the California Gold Rush and the opening of China rolled into one.

The appliance market that Whirlpool would enter was nothing like the mature American market they dominated. In the late 1980s, washing machine penetration in India was less than 5%. Refrigerators? Maybe 10% in urban areas. This wasn't a market share battle—this was about creating the market itself. Indian families were transitioning from storing food in earthen pots to electric refrigeration, from washing clothes by hand to machine washing. Every sale wasn't replacing a competitor's product; it was replacing centuries-old habits.

But here's where global executives consistently misread India: low penetration didn't mean easy sales. The Indian consumer of the early 1990s was perhaps the world's most demanding customer—wanting global quality at local prices, requiring products that could handle 250-volt power surges and 100-volt drops, demanding machines that could work with hard water, soft water, or sometimes no water at all.

III. Entry Strategy: The TVS Joint Venture Era (Late 1980s–1995)

Whirlpool entered the Indian market in the late 1980s as part of its global expansion strategy. It founded a joint venture with the TVS Group and established the first Whirlpool manufacturing facility in Puducherry, where it manufactured washing machines. But understanding why TVS made the perfect partner requires understanding what TVS represented in Indian business culture.

T. V. Sundram Iyengar founded the group in 1911, the same year Louis Upton was starting his washing machine company in Michigan. By the 1980s, TVS Group had grown into one of India's largest industrial entities with over fifty companies, employing more than 50,000 people worldwide. More importantly, TVS embodied exactly what foreign companies needed in India: manufacturing excellence, distribution networks, and most crucially, the ability to navigate India's labyrinthine regulatory environment.

The late 1980s joint venture wasn't Whirlpool's first tentative step into India—it was a calculated move during a unique window of opportunity. The Indian government, while not yet fully liberalized, had begun allowing selective foreign partnerships in non-core sectors. Appliances weren't steel or telecommunications; they were consumer goods that could improve quality of life without threatening strategic industries.

The Puducherry factory location was no accident. Tamil Nadu offered better infrastructure than most Indian states, proximity to ports for importing components, and a state government eager to attract manufacturing investment. The factory started small—just washing machines, semi-automatic models that could handle the peculiarities of Indian laundry habits. Indian consumers didn't just want clean clothes; they wanted to inspect the wash, add fabric softener mid-cycle, and use the same water for multiple loads during water shortages.

What Whirlpool learned in those early years through TVS was invaluable: Indian consumers would pay a premium, but only for visible technology. A Korean washing machine with a transparent lid and LED lights would outsell an American one with superior motor technology every time. The Indian middle-class housewife—and it was almost always the housewife making these decisions—wanted to see the wash happening, wanted control over every cycle, wanted machines that announced their technological superiority.

The competition landscape in the late 1980s seemed manageable. Godrej, the Mumbai-based conglomerate, dominated refrigerators with over 60% market share but had limited presence in washing machines. BPL and Videocon were strong in televisions but just entering white goods. The market was fragmented, under-penetrated, and seemingly ripe for consolidation by a global player with deep pockets and superior technology.

But Whirlpool-TVS faced challenges that would preview everything that would go wrong later. Power cuts meant machines needed to restart mid-cycle without resetting. Water pressure varied not just by city but by floor in apartment buildings. Servicing was a nightmare—Indian consumers expected technicians to come to their homes, often multiple times, and fix problems that were frequently user error rather than mechanical failure. The joint venture was spending as much on education—teaching consumers how to use washing machines—as on marketing.

By 1994, as India's liberalization was in full swing, Whirlpool made a decision that would transform its Indian operations. The joint venture had given them local knowledge and manufacturing capability, but TVS was fundamentally a components company, not a consumer brand builder. Whirlpool needed full control to implement its global strategy. It began buying out TVS's stake, setting the stage for the next phase: the Kelvinator acquisition that would theoretically give them instant scale and market presence.

IV. The Kelvinator Acquisition & Birth of Whirlpool India (1995–1996)

In 1995, Whirlpool made what seemed like a masterstroke. They acquired Kelvinator India Limited, a brand that had been India's refrigerator king since the 1970s. In the 1970-1980, Kelvinator was the leader in the refrigerator market in India. The brand carried emotional resonance—for an entire generation of Indians, "Kelvinator" was synonymous with refrigerator, the way "Xerox" meant photocopying.

But beneath the iconic brand lay a troubled business. Jamshed Desai originally controlled Kelvinator India Limited (KIL). The Kelvinator brand belonged to Electrolux Group but was franchised to KIL in which Electrolux had about 13% shareholding. The company had struggled during 1991-1993, caught between the old protected economy and the new liberalized market. Its factories were outdated, its dealer network demoralized, and its product line hadn't been refreshed in years.

For Whirlpool, this was supposed to be transformative. With one acquisition, they would get brand recognition that would take decades to build organically, manufacturing facilities for refrigerators to complement their washing machine operations, and most importantly, a distribution network that reached into India's vast hinterland. The price wasn't disclosed, but industry insiders suggested Whirlpool paid a premium for what was essentially a distressed asset with a golden brand name.

In 1996, the Kelvinator and TVS acquisitions were merged to create Whirlpool of India Limited. This wasn't just corporate restructuring—it was the birth of an entity that Whirlpool Corporation believed would dominate Indian appliances for decades. The combined company now had washing machines from the TVS venture, refrigerators from Kelvinator, and the backing of the world's largest appliance manufacturer.

The integration challenges were immediate and brutal. Kelvinator's refrigerator designs were a decade old—basic single-door units when the market was moving toward frost-free double doors. The dealer network, while extensive, had been trained to sell on brand heritage, not features. Meanwhile, Whirlpool's American management wanted to introduce global products with minimal localization, believing Indian consumers would pay for superior technology.

The cultural clash was even more pronounced. Kelvinator's Indian managers, many with decades of experience, suddenly reported to American executives who'd never sold a refrigerator for less than $500. The Americans talked about "premiumization" and "value migration"; the Indians knew that 90% of refrigerators sold in India were still single-door units bought on installment plans.

The newly formed Whirlpool of India went public, listing on both the Bombay Stock Exchange and National Stock Exchange. The IPO was marketed as a chance to own part of the global appliance revolution coming to India. Institutional investors were told about synergies, technology transfer, and the massive under-penetrated Indian market. Retail investors were sold on the Kelvinator legacy and Whirlpool's global might.

What nobody fully understood was that the Indian appliance market was about to be disrupted not by American technology or Indian heritage, but by Korean marketing genius and a willingness to lose money for market share that would make even the deepest-pocketed American corporations blink.

V. The Korean Invasion: LG & Samsung Change Everything (1997–2005)

In 1997, a plane from Seoul landed in New Delhi carrying the advance team of LG Electronics. They weren't the first Korean company to try India—Lucky Goldstar (as LG was then known) had twice entered the Indian market with local partners in the late 1980s and early 1990s; both ventures failed. But this time was different. This time, they had permission to set up their own manufacturing facilities, and more importantly, they had a war chest and a strategy that would rewrite the rules of Indian consumer marketing.

In 1997, LG finally got permission to set up its own manufacturing facilities. What followed was a masterclass in emerging market domination. Revenues in 1997 were US$33.97 million; last year, LG India earned US$2.37 billion. The transformation wasn't luck—it was the systematic destruction of every assumption Whirlpool and other multinationals had about the Indian market.

LG's entry strategy was to establish its presence across the country, offering a range of affordable but feature-rich products. Margins in the consumer electronics industry are traditionally very low, and the company didn't try to push them up. Instead, it clung to the "value-plus" platform, counting on volume to bring in revenues. This was heresy to American MBAs trained on Porter's differentiation strategies. You either competed on cost or differentiation, not both. LG said: watch us.

The first shock to the system was dealer financing. Indian appliance dealers traditionally operated on thin working capital, taking goods on consignment or very short credit terms. LG walked in and offered 45-day credit, then 60 days, sometimes 90 days. They weren't just selling products; they were financing an entire ecosystem. Dealers who had been loyal to Godrej or Videocon for decades suddenly found they could stock three times the inventory with LG's terms.

Then came the marketing blitz. While Whirlpool was still running print ads in English newspapers targeting urban elites, LG bought every cricket sponsorship available. They signed Abhishek Bachchan and Aishwarya Rai—Bollywood royalty—as brand ambassadors. They didn't just advertise during cricket matches; they created cricket-themed promotions where buying a refrigerator entered you into a draw to meet Sachin Tendulkar.

Samsung, on the other hand, focused on creating a premium brand image by emphasizing the design and technology aspects of its higher-priced products and building a more affluent customer base. The two Korean giants were executing a pincer movement—LG from the bottom, Samsung from the top—that would squeeze established players from both ends.

The product localization was obsessive. LG's Indian engineers designed refrigerators with larger vegetable crispers because Indian households stored more fresh produce. They created "Diwali" and "Monsoon" settings on air conditioners. Their washing machines had "saree" cycles. These weren't gimmicks—they were the result of thousands of hours of consumer research, of engineers sitting in Indian homes watching how families actually used appliances.

But the real genius was in distribution and service. In any customer-facing business, your product, brand and distribution decide your success. Moreover, in the durables industry, after-sales service and product innovation are also key factors. LG didn't just set up service centers; they created mobile service vans that would come to your home within 24 hours. In a country where getting anything repaired was a multi-week odyssey, this was revolutionary.

The results were devastating for incumbents. In just over 10 years, the Korean duo has established dominance over the Indian white goods market, edging out traditional multinational companies and Indian competitors. Between them, they account for the largest share of the $6 billion consumer durables, electronics and appliances market. By 2022, LG commanded around 29% of the washing machine market. Samsung wasn't far behind.

For Whirlpool, watching this happen was like being in slow-motion car crash. Every quarter, market share reports showed the same story: LG and Samsung gaining, everyone else losing. The company tried to respond—launching new products, increasing marketing spend, improving service networks. But they were playing catch-up in a game where the rules had been rewritten.

The Korean invasion exposed a fundamental flaw in Whirlpool's strategy: they had assumed that being a global leader with superior technology would naturally translate to market leadership. They hadn't accounted for competitors willing to lose money for years to build market share, to finance entire distribution networks, to treat marketing as a fixed cost rather than a percentage of sales.

VI. Manufacturing Excellence & Localization (2001–2010)

Faced with the Korean onslaught, Whirlpool doubled down on what it knew best: manufacturing excellence. The company launched its first major manufacturing facility in Pune in 2001, which played a crucial role in meeting the rising demand for home appliances in India. This wasn't just adding capacity—it was a statement that Whirlpool would fight the market share battle through operational efficiency rather than marketing theatrics.

In 2006, the company further enhanced its capabilities by establishing an advanced manufacturing plant in Faridabad. Whirlpool of India Limited is headquartered in Gurgaon, and it owns three manufacturing facilities at Faridabad, Puducherry and Pune. The three-plant strategy gave Whirlpool geographic coverage across India's major industrial corridors—Faridabad for the North, Pune for the West, and Puducherry for the South.

The Pune plant, inaugurated in October 1996 but significantly expanded in 2001, became the centerpiece of Whirlpool's refrigerator manufacturing. The facility was designed to produce both single-door and double-door refrigerators, with flexibility to shift production based on market demand. But here's where the strategy got interesting: instead of competing with LG and Samsung on features, Whirlpool focused on build quality and energy efficiency.

The localization drive went deep into the supply chain. Component sourcing became an obsession. Every imported part was a vulnerability—not just because of cost, but because of lead times and currency fluctuations. Whirlpool's procurement teams worked with Indian vendors to develop local alternatives for compressors, plastic moldings, and electronic controls. By 2005, local content in Whirlpool refrigerators exceeded 80%, compared to less than 50% for Korean competitors who still imported key components from their home countries.

Technology transfer from global operations was supposed to be Whirlpool's ace card. The company brought in manufacturing processes from its American and European plants—Six Sigma quality controls, lean manufacturing principles, automated testing procedures. Indian engineers were sent to Benton Harbor for training; American manufacturing experts spent months in Pune and Faridabad implementing global best practices.

But technology transfer isn't just about machinery and processes—it's about mindset. The American approach emphasized standardization and efficiency; the Indian market demanded customization and flexibility. A refrigerator designed for consistent 110V American power supply couldn't handle Indian voltage fluctuations that swung from 170V to 270V within minutes. Compressors that worked perfectly in climate-controlled American homes failed in Indian summers where ambient temperatures exceeded 45°C.

The quality versus cost debate became a daily battle within Whirlpool India. Global management pushed for maintaining Whirlpool's worldwide quality standards. Local management knew that a refrigerator priced 20% higher than LG's needed to offer something tangible to justify the premium. The compromise was elegant but expensive: Whirlpool would maintain global quality standards but develop India-specific features that showcased this quality.

The result was products like the "Protton" series of refrigerators—built with toughened glass shelves that could hold 175 kg (because Indian families stored heavy vessels), with special compartments for storing Indian vegetables that needed different temperature and humidity levels, and with stabilizer-free operation that could handle voltage fluctuations. These weren't just marketing gimmicks; they were genuine innovations that addressed real consumer pain points.

The distribution network expansion during this period was methodical but uninspiring compared to the Korean blitzkrieg. Whirlpool focused on tier-1 and tier-2 cities, believing that rural markets weren't ready for branded appliances. Meanwhile, LG was setting up dealerships in towns with populations under 50,000, financing inventory for small retailers who'd never stocked appliances before.

Service network development revealed another cultural gap. Whirlpool's global service model emphasized efficiency—minimize service calls through better quality, handle necessary repairs quickly through trained technicians. The Indian consumer expected something different: they wanted technicians who would explain problems, offer preventive maintenance advice, and sometimes just reassure them that their expensive purchase was working fine. LG understood this; their technicians were trained to spend time with customers, to treat service calls as relationship-building opportunities rather than problems to be solved quickly.

By 2010, Whirlpool's manufacturing infrastructure was world-class. The plants could produce products matching global quality standards at costs competitive with local manufacturers. The company had successfully navigated the transition from imported components to local sourcing. Product development cycles had shortened from 18 months to 12 months. Yet market share continued to lag behind the Korean giants.

VII. Product Innovation & Market Positioning (2010s)

The 2010s marked Whirlpool India's pivot from manufacturing excellence to product innovation. In the 2010s, Whirlpool of India began to focus heavily on innovation and sustainability. The company launched a range of energy-efficient washing machines and refrigerators. But the crown jewel of this innovation push was the introduction of 6th Sense technology—a suite of intelligent features that was supposed to differentiate Whirlpool from the feature-focused Korean competition.

On 5 July 2016, Whirlpool of India introduced its all new NeoFresh range of double door refrigerators with innovative 6th Sense Intellifresh technology. The technology wasn't just a marketing gimmick—it used sensors to monitor temperature, humidity, and usage patterns to optimize cooling and reduce energy consumption. The promise was compelling: refrigerators that could think, that could adapt to Indian conditions automatically.

6TH SENSE Technology automatically detects the size and type of load and chooses the best washing parameters to deliver optimal results. In washing machines, sensors and algorithms recognized the amount of laundry and fabric type, automatically adapting temperature, water level, and motor torque accordingly. This was genuine innovation, the kind of technology leadership that should have given Whirlpool a decisive edge.

Then came FreshCare+, perhaps the most innovative feature Whirlpool introduced in India. This purposeful technology gently rotated clothes and used steam to keep laundry fresh for up to 6 hours after the cycle finished. For Indian households where family members returned home at different times, where the person who started the wash might not be home when it finished, this solved a real problem. No more musty-smelling clothes forgotten in the machine; no more rewashing because clothes sat wet for too long.

The innovation lab in Pune became a showcase for "designing for Indian conditions." Engineers studied how Indian families used appliances—not through surveys but through home visits, through watching actual usage patterns. They discovered that Indian consumers used the vegetable crisper in refrigerators differently than Americans—it needed to maintain different humidity levels for tropical vegetables. They found that washing machines needed special cycles for heavily soiled clothes common in India's dusty environment.

Key product launches reflected this deep consumer understanding. The "Ace" series of semi-automatic washing machines targeted the vast middle market that couldn't afford fully automatic machines but wanted branded quality. The "Protton" refrigerators addressed durability concerns with toughened glass shelves and robust compressors. The "3D Cool" air conditioners promised uniform cooling even in rooms with poor ventilation—common in Indian homes.

But here's where Whirlpool's strategy revealed its fundamental flaw: they were solving problems consumers didn't know they had, while Korean brands were delivering benefits consumers actively wanted. LG's refrigerators had door-in-door designs that looked futuristic; Whirlpool's had better vegetable crispers. Samsung's washing machines had LED displays and multiple wash programs with fancy names; Whirlpool's had genuinely superior wash quality that was invisible to the consumer at point of purchase.

The premium versus mass market strategy debates within Whirlpool India became increasingly heated. Global management pushed for maintaining premium positioning—after all, Whirlpool commanded premium prices in America and Europe. But India wasn't America. Here, premium meant Samsung and LG, brands that had invested billions in creating aspirational value through celebrity endorsements and sports sponsorships.

On 14 November 2014, Whirlpool of India announced the opening of its first exclusive Built-in showroom called Whirlpool Haute Kitchen in Jaipur. It brings the best of European styling and functionality offering a complete range of Built-in products. This was an attempt to create a super-premium segment where Whirlpool's global reputation might matter. But built-in kitchens were a tiny niche in India where most homes had traditional cooking spaces.

Distribution network expansion continued, but it felt reactive rather than proactive. From metros to Tier 3 cities, Whirlpool was present but not dominant. E-commerce was initially viewed with suspicion—how could you sell a refrigerator online without the customer touching and feeling it? By the time Whirlpool embraced online sales, Flipkart and Amazon had already struck exclusive deals with Korean brands for their private label products.

The service network underwent modernization, but again, it was catching up rather than leading. Mobile apps for service requests, 24-hour helplines, annual maintenance contracts—all good initiatives that competitors had already implemented. Whirlpool's service was good, but good wasn't good enough when LG's service was spectacular and cheaper.

Private label threats emerged as a new challenge. Flipkart's MarQ, Amazon's AmazonBasics, and retailer brands were eating into margins from below while Korean brands dominated from above. These private labels often used the same manufacturers as branded products but sold at 20-30% lower prices. For price-conscious Indian consumers, a Flipkart-branded refrigerator with similar features to Whirlpool's at a lower price was an easy choice.

The story of the 2010s for Whirlpool India was one of solid products that failed to capture imagination, of genuine innovation that couldn't overcome inferior brand perception, of a company doing many things right but nothing spectacularly enough to change its market position.

VIII. Market Dynamics & Competition Analysis

The current market structure tells a brutal story of competitive dynamics. In 2022, LG held the leading position in the Indian refrigerator market with more than 30 percent of the market share. LG was the leader in the Indian refrigerator market with more than 30 percent of the market share. Whirlpool ranked the third following Samsung. The Indian home appliance market is competitive and moderately consolidated, as top players have a high market share in the industry of big and small appliances. Some of the major players are Electrolux AB, Haier Electronics Group Co Ltd, LG Electronics, Robert Bosch GmbH, Whirlpool Corporation, and Samsung, among others.

This isn't just about losing market share—it's about the fundamental economics of the business. It features an oligopolistic structure in premium segments, where Samsung, LG and Whirlpool dominate through advanced technology and extensive retail networks. But dominance in premium segments means little when the volume game is being played in mass markets where margins are razor-thin and scale is everything.

The Korean companies' strategy has been consistent for over two decades: sacrifice margins for market share, invest disproportionately in marketing and distribution, and use global profits to subsidize Indian operations. Smart refrigerators from Samsung and LG, smart air conditioners from Voltas, and smart washing machines from Bosch are gaining popularity in India. These appliances offer features such as remote control via smartphone apps, energy usage monitoring, and compatibility with virtual assistants like Amazon Alexa. Leading brands like Whirlpool, Haier, and Godrej are introducing a range of energy-efficient appliances in the Indian market, such as 5-star rated refrigerators, inverter technology air conditioners, and eco-friendly washing machines. These appliances help consumers save on electricity bills.

Price wars have become a permanent feature of the Indian appliance market. During festival seasons—Diwali, Dussehra, the Amazon and Flipkart sales—discounts routinely exceed 30%. Korean brands lead with aggressive pricing, forcing everyone else to follow or lose sales. Whirlpool, with its American corporate culture of maintaining margins, has struggled to compete in this environment.

The entry of Chinese players added another layer of complexity. In March 2023, Haier, announced the launch of its new line-up of anti-scaling top load washing machines. Powered by Haier's anti-scaling technology, bionic magic filter, and 3D rolling wash, the new range complements modern lifestyle needs making the laundry experience efficient, simple, and effortless along with taking care for fabric. Haier, Midea, and others brought Chinese manufacturing scale and a willingness to operate at even lower margins than the Koreans.

E-commerce disruption changed the rules of distribution. Traditional multi-brand outlets, where salespeople could be influenced by dealer margins and brand relationships, gave way to online platforms where price and reviews determined purchase decisions. Companies like Panasonic and Symphony are expanding their distribution networks and retail presence in tier-2 and tier-3 cities of the country to reach a wider customer base. These brands, by entering into partnerships with local retailers and leveraging e-commerce platforms, are making their products more accessible to consumers in smaller towns and cities.

Private label products from retailers emerged as another threat. Flipkart's MarQ refrigerators, Amazon Basics microwaves—these weren't just cheaper alternatives but products that matched 80% of features at 60% of the price. For a market where a ₹2,000 difference could swing a purchase decision, this was devastating for branded players trying to maintain premium positioning.

The rise of regional brands added to the pressure. Voltas (backed by Tata), Godrej (with decades of trust), and newer entrants leveraged local manufacturing and lower overheads to offer competitive products. Voltas became the first brand to surpass the 2-million-unit sales figure in in the fiscal year 2023-24. The company recorded a robust 35% year-on-year growth in sales, driven by strong consumer demand and its extensive distribution network across the country.

For Whirlpool, being a consistent third or fourth player in most categories meant living in a vicious cycle. Lower market share meant lower volumes, which meant higher per-unit costs, which made it harder to compete on price, which led to lower market share. Breaking this cycle required either massive investment to buy market share or acceptance of a niche premium position—neither palatable to a company used to market leadership.

IX. Financial Performance & Challenges (2018–2024)

The numbers tell a story of stagnation and margin pressure that would make any investor nervous. Revenue: 7,855 Cr, Profit: 364 Cr. The company has delivered a poor sales growth of 5.73% over past five years. Company has a low return on equity of 7.39% over last 3 years. The revenue of Whirlpool of India Limited in the financial year 2023 amounted to 66.7 billion Indian rupees.

Let's put these numbers in perspective. A 5.73% five-year CAGR in a market growing at double digits means Whirlpool has been losing market share every single year. When inflation alone runs at 4-5%, real growth has been near zero. This isn't just poor performance; it's a company treading water while competitors surf past on waves of consumer demand. Even more telling is the promoter story. Promoter holding has decreased over last 3 years: -24.0%. In February 2024, Whirlpool Mauritius sold 24% stake worth US$451 million at Rs 1,230 per share, reducing promoter holding from 75% to 51%. Then in January 2025, Whirlpool Corporation announced its intention to sell down its ownership interest in Whirlpool India to approximately 20 per cent by mid-to-late 2025. The company expects net cash proceeds of $550 to $600 million from the anticipated India transaction.

This isn't just portfolio rebalancing—it's a vote of no confidence from the parent company. When a global corporation systematically reduces its stake in what should be one of its most promising growth markets, it signals either a fundamental reassessment of market potential or an acknowledgment that they can't win with their current strategy.

Stock performance has been equally disappointing. Market Cap: 16,932 Crore (down -37.4% in 1 year). The stock is trading at 4.29 times its book value—seemingly reasonable until you realize that competitors with higher growth trade at similar or better multiples. The market is essentially saying that Whirlpool's assets aren't generating adequate returns.

Operational challenges compound the financial woes. Input cost inflation hit Whirlpool particularly hard because their premium positioning made it difficult to pass on costs fully. When steel prices rose 30%, LG could absorb it through volume; Whirlpool, selling fewer units at higher prices, saw margins evaporate. Currency headwinds added another layer of pain—imported components became more expensive just as competition intensified.

The comparison with competitors is stark. While Voltas became the first brand to surpass the 2-million-unit sales figure in fiscal year 2023-24 with a robust 35% year-on-year growth, Whirlpool struggled to maintain flat volumes. This isn't just about different product categories; it's about momentum, market perception, and the ability to capture growth.

The cash position remains healthy—the company is almost debt-free with strong cash flows from operations. But this raises uncomfortable questions: Why isn't this cash being deployed aggressively to gain market share? Why maintain a conservative balance sheet when competitors are investing heavily in growth? The answer seems to be that the parent company has given up on aggressive expansion, preferring to milk the Indian subsidiary for dividends rather than reinvest for growth.

X. Playbook: Lessons from the Indian Appliance Wars

The Whirlpool India story offers a masterclass in how global success doesn't guarantee local dominance. Every strategic decision, viewed through the lens of hindsight, reveals fundamental lessons about competing in emerging markets.

Global brand vs local execution: The balancing act was Whirlpool's perpetual challenge. The company tried to leverage its global reputation for quality while adapting products for local needs. But they misunderstood the hierarchy of consumer preferences. In India, visible technology trumps invisible quality. A refrigerator with LED displays and multiple compartments sells better than one with a superior compressor that lasts twice as long. Whirlpool built products for American consumers who research Consumer Reports; India needed products for consumers who trust their local dealer's recommendation.

Why market share matters more than margins (initially) is perhaps the most painful lesson. The Korean strategy of accepting losses for market share seemed irrational to American MBAs trained on maximizing shareholder value. But in a market growing at 15-20% annually, today's market share determines tomorrow's economies of scale. LG's willingness to lose money for five years to become number one gave them the volume to negotiate better component prices, afford bigger marketing budgets, and attract the best retail locations. Whirlpool's focus on maintaining "reasonable" margins kept them perpetually subscale.

Distribution as moat proved more important than product superiority. LG and Samsung didn't just sell to dealers; they financed entire distribution networks. They provided inventory financing, set up exclusive brand stores, and trained armies of sales promoters. A Whirlpool refrigerator might be superior, but if the dealer makes more money selling LG, guides customers toward LG, and has his working capital financed by LG, product quality becomes irrelevant.

Product localization: Not just smaller sizes but different use cases required deep cultural understanding. Indians don't use appliances the way Americans do. A washing machine isn't run once a week with sorted loads; it might run twice daily with mixed fabrics. A refrigerator isn't just for storing food; it's for cooling water bottles in summer. The Korean companies understood this implicitly—their Asian heritage gave them cultural proximity. Whirlpool had to learn it through expensive market research.

Brand building in emerging markets: Trust, quality, and aspiration follows different rules than in developed markets. In America, Whirlpool could rely on decades of brand equity. In India, they were starting from zero, competing against LG's Bollywood celebrities and Samsung's cricket sponsorships. The Korean companies understood that in emerging markets, brands need to signal success and social mobility, not just functional benefits.

Capital allocation: When to invest vs harvest became Whirlpool's fatal dilemma. The company was profitable enough to satisfy headquarters but not growing fast enough to excite investors. Should they sacrifice profitability to buy market share? Should they accept their niche position and maximize margins? The middle path they chose—moderate investment for moderate growth—satisfied no one.

Parent company dynamics: Global synergies vs local autonomy created perpetual tension. Whirlpool India was supposed to benefit from global R&D, worldwide sourcing, and technology transfer. In practice, products designed for American kitchens needed extensive modification for India. Global sourcing contracts didn't account for Indian import duties. Technology transfer happened, but at a pace too slow for the fast-moving Indian market.

The playbook that emerges is clear but brutal: In emerging markets, commit fully or don't enter. Half-measures lead to perpetual mediocrity. You need to be willing to lose money for years, to invest disproportionately in distribution and marketing, to give local management real autonomy, and to accept that what works in developed markets might be completely wrong for emerging ones.

The irony is that Whirlpool did many things right. They manufactured locally, developed India-specific products, built a service network, and maintained quality standards. But in a market where Korean companies were doing everything right and then some—financing dealers, carpet-bombing advertising, accepting massive losses—being good wasn't good enough.

XI. Bear vs Bull Case & Future Outlook

Bear Case: The Structural Decline Thesis

The bear case for Whirlpool India isn't just about current challenges—it's about structural disadvantages that seem impossible to overcome. Start with the persistent market share losses to Korean competitors. This isn't a recent phenomenon but a two-decade trend. When you've been losing market share for twenty years despite multiple strategy pivots, it suggests the problem isn't tactical but fundamental.

The commoditization of appliances accelerates every year. When a Flipkart-branded refrigerator offers 80% of Whirlpool's features at 60% of the price, brand premium evaporates. The Indian consumer, increasingly price-conscious and deal-savvy, sees appliances as functional commodities rather than lifestyle statements. In this environment, Whirlpool's quality advantage—real as it might be—becomes invisible and therefore worthless.

Rising Chinese competition adds another layer of threat. Haier has already established itself; Midea is expanding; TCL is entering. These companies bring Chinese manufacturing scale, a willingness to operate at minimal margins, and experience competing in the world's most cutthroat consumer market. If Korean companies disrupted the market with 10% lower prices, Chinese companies might do it with 20% lower prices.

The parent company's systematic stake reduction sends an unmistakable signal. When Whirlpool Corporation reduces its holding from 75% to potentially 20%, they're essentially saying: "India isn't core to our global strategy." Without full parent support—technology transfer, global sourcing benefits, marketing investment—Whirlpool India becomes an orphan, too small to compete independently, too unimportant to receive serious investment.

The financial metrics tell a story of decay: 5.73% five-year revenue CAGR in a market growing at double digits, ROE of 7.39%, declining margins. These aren't numbers that attract growth investors or excite management teams. They're the numbers of a company in gradual decline, maintaining enough profitability to avoid crisis but lacking the growth to build a future.

Bull Case: The Turnaround Opportunity

But the bull case has merit, starting with India's low appliance penetration. Washing machine penetration is still below 15%; air conditioner penetration under 10%. As India adds 10 million middle-class households annually, the market opportunity is massive. Even maintaining current market share in a market that could triple in size means substantial growth.

Premiumization trends favor global brands—eventually. As Indian consumers mature, they move from "cheapest option" to "best value" to "best quality." We've seen this in automobiles where Maruti dominated initially but now loses share to Hyundai and Kia at the premium end. Whirlpool, with its global heritage and quality reputation, is well-positioned for when Indian consumers start prioritizing longevity over initial price.

The manufacturing expertise and local production advantage shouldn't be dismissed. Three well-established plants, decades of supplier relationships, trained workforce—these are real assets. As "Make in India" initiatives add import barriers and local manufacturing incentives, Whirlpool's established infrastructure becomes more valuable.

The parent company's technology pipeline, even with reduced stake, remains accessible. Whirlpool Corporation spends over $500 million annually on R&D. Technologies developed for global markets—IoT integration, energy efficiency, sustainable materials—can be adapted for India. The brand license alone, which will continue even with reduced shareholding, has value in premium segments.

Recent strategic moves suggest management isn't giving up. The Elica acquisition, taking stake from 49% to 87%, brings premium built-in kitchen appliances—exactly the segment where brand and quality matter most. The focus on energy-efficient products aligns with government initiatives and changing consumer preferences.

Future Trends: The Next Decade

The smart appliances and IoT integration wave is just beginning in India. While Korean brands lead in visible technology, Whirlpool's global expertise in connected appliances could provide an edge as Indian homes become smarter. The company's 6th Sense technology, properly marketed, could resonate with tech-savvy millennials.

Energy efficiency regulations will drive replacement cycles. As the government tightens efficiency standards, millions of old appliances will need replacement. Whirlpool's focus on 5-star rated products positions them well for this replacement wave.

Rural market penetration remains the largest untapped opportunity. As electricity reaches every village and rural incomes rise, first-time appliance buyers will enter the market. The question is whether Whirlpool can develop distribution and products for these markets before competitors lock them up.

Export potential from the India manufacturing base is underexploited. With three efficient plants and competitive labor costs, Whirlpool India could become an export hub for South Asia, Africa, and the Middle East. This would provide scale benefits without depending solely on the competitive domestic market.

The Verdict: A Value Trap or Contrarian Opportunity?

Whirlpool India presents the classic dilemma: Is it a value trap—cheap for good reasons that won't change? Or a contrarian opportunity—unloved and undervalued, ready for revival? The answer depends on your belief in three key variables:

First, can new management (potentially with reduced parent company interference) execute a successful turnaround? Second, will Indian consumers eventually value quality over features and brand heritage over marketing flash? Third, can the company find a profitable niche even if it never regains market leadership?

For long-term fundamental investors, the risk-reward might be attractive at current valuations. The stock trades at modest multiples, the company has no debt, and the market opportunity is undeniable. But this requires patience measured in years, not quarters, and faith that structural disadvantages can be overcome through execution excellence.

XII. Epilogue & Reflections

Standing back from the quarterly results and market share statistics, Whirlpool India's story is fundamentally about the collision between American corporate culture and Indian market reality. It's about how being good at what you do isn't enough when competitors are willing to reimagine the entire game.

What Whirlpool got right deserves recognition. They were early movers in liberalized India, built world-class manufacturing facilities, maintained quality standards, and developed genuine product innovations. They played by the rules of responsible capitalism—maintaining margins, generating profits, paying dividends. In any MBA classroom, their strategy would seem textbook perfect.

What Whirlpool got wrong was more subtle but ultimately more important. They confused their global success for universal applicability. They believed Indian consumers would eventually behave like American consumers. They thought quality would triumph over marketing, that distribution was about logistics not relationships, that profitable growth was better than unprofitable market share gains.

The perpetual challenge—global scale versus local relevance—was never truly resolved. Whirlpool tried to be both global and local, premium and mass market, innovative and cost-competitive. In trying to be everything, they became nothing distinctive. The Korean companies, by contrast, picked a lane and accelerated: LG chose mass market dominance, Samsung chose accessible premium.

What different strategic choices might have meant is worth contemplating. What if Whirlpool had accepted five years of losses to build dominant market share? What if they'd acquired a strong local brand like Voltas or Godrej instead of the struggling Kelvinator? What if they'd given the Indian subsidiary true autonomy, letting local management make decisions without seeking Benton Harbor's approval?

The alternative history might have seen Whirlpool as India's appliance leader, leveraging first-mover advantage and global technology to build an unassailable position. Instead, they became a cautionary tale of how global giants can stumble in emerging markets, outmaneuvered by hungrier, more adaptable competitors.

Key takeaways for operators and investors are sobering but valuable:

For operators entering emerging markets: Commit fully or stay out. Half-measures lead to perpetual disadvantage. Be prepared to lose money for longer than seems rational. Understand that distribution and relationships matter more than product superiority. Give local management real autonomy. Accept that your global playbook might be completely wrong.

For investors evaluating emerging market stories: Look beyond the brand name and global parentage. Assess whether the company is playing to win or playing not to lose. Understand the competitive dynamics—who's willing to lose money for market share? Evaluate distribution strength, not just manufacturing capability. Be skeptical of "premium positioning" in price-conscious markets.

The Whirlpool India story continues to unfold. With the parent company reducing its stake, new chapters might be written. Perhaps freed from global constraints, local management can execute a turnaround. Perhaps a strategic investor will see value where the market sees stagnation. Or perhaps this is simply the slow decline of a company that arrived early but never truly understood the market it entered.

What's certain is that the Indian appliance market will continue growing, consumers will continue buying refrigerators and washing machines, and someone will capture that value. Whether Whirlpool participates in that growth as a leader, a niche player, or a cautionary footnote remains to be seen.

The lessons, however, are already clear: In emerging markets, success requires more than good products and strong brands. It requires a willingness to reimagine everything you think you know about business, to compete by different rules, and to commit resources that seem irrational by developed market standards. Whirlpool India learned these lessons too late. The question for other global companies eyeing emerging markets is: Will you learn from their experience, or repeat it?

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube