Vesuvius India: The Refractory Empire That Powers India's Steel

I. Introduction & Episode Roadmap

Picture this: Inside every steel plant in India, from the towering blast furnaces of Tata Steel in Jamshedpur to the gleaming facilities of JSW in Vijayanagar, there's a silent guardian. Not the massive machinery that captures headlines, not the thousands of workers who operate them, but something far more fundamental—ceramic linings that withstand temperatures hot enough to vaporize rock. These are refractories, and without them, not a single ton of steel could be produced in this country.

Welcome to the story of Vesuvius India Limited—a company with a market cap of ₹10,501 crore that most investors have never heard of, yet one that touches every piece of steel infrastructure you encounter daily. From the railways carrying millions of passengers to the skyscrapers reshaping India's skyline, Vesuvius's products are the unsung heroes of industrial India.

Here's what's remarkable: despite generating ₹1,897 crore in revenue and ₹255 crore in profit, Vesuvius operates in near-complete obscurity. No consumer brands, no flashy advertisements, no retail presence. Yet this British ceramics giant's Indian subsidiary has become so essential that steel plants would literally shut down within days without their products. It's the ultimate B2B moat story—one where switching costs aren't just high, they're potentially catastrophic.

What we're about to explore isn't just a corporate history. It's a masterclass in how foreign technology, local execution, and perfect timing can create an industrial empire. We'll uncover how a company founded in 1704 on the banks of England's River Tyne became indispensable to India's steel revolution. We'll examine the economics of selling consumables to cyclical industries, the art of building trust in long-sales-cycle businesses, and why sometimes the best investments are in companies that nobody talks about at cocktail parties.

This is also a story about industrial infrastructure that underpins modern civilization—the picks and shovels of the steel age that nobody sees but everyone depends on. As India races toward becoming the world's second-largest steel producer, Vesuvius sits at the intersection of this transformation, quietly powering the furnaces that forge the nation's future.

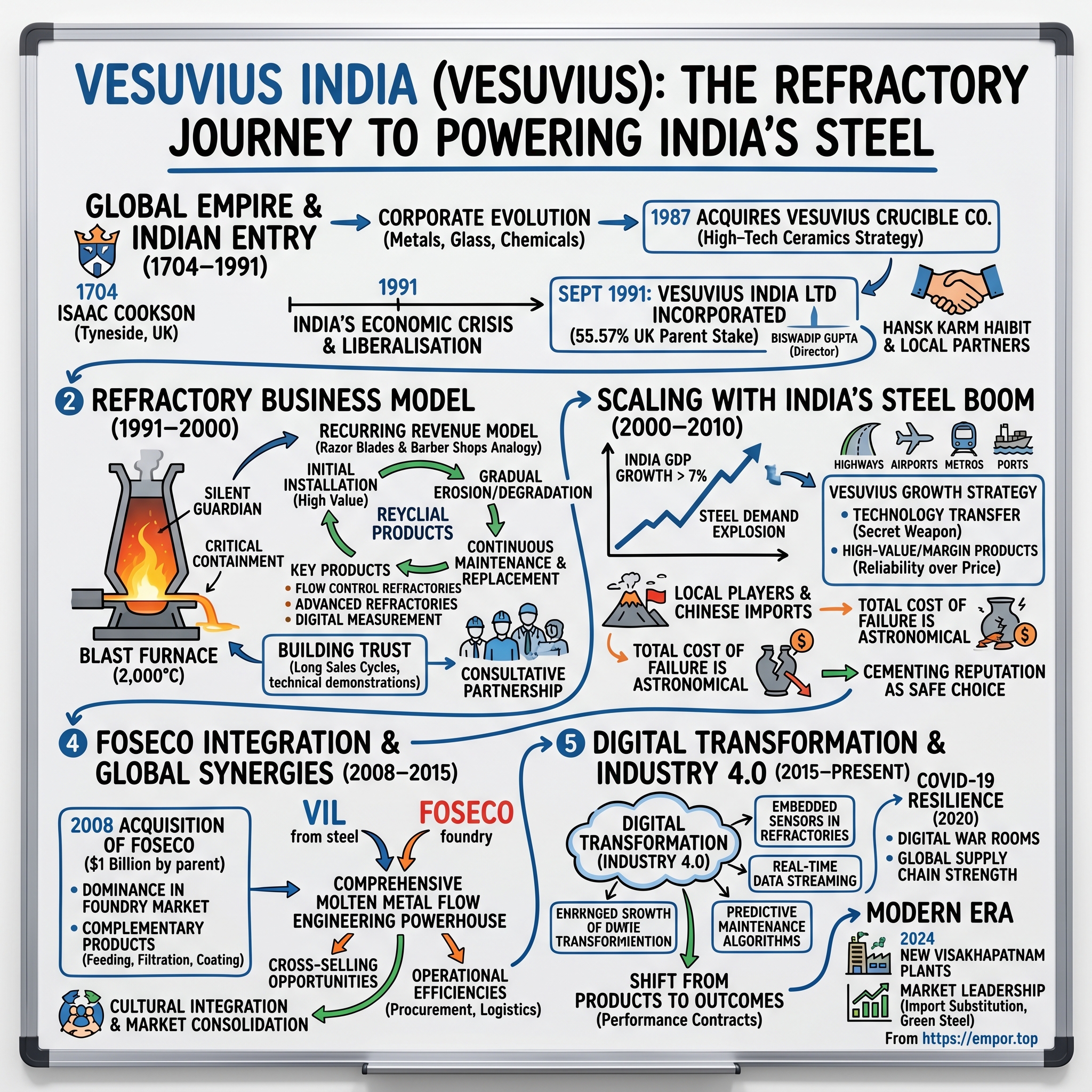

II. The Vesuvius Global Empire & Indian Entry (1704–1991)

The year is 1704. Queen Anne rules Britain, the Act of Union is three years away, and on Tyneside in northeast England, Isaac Cookson establishes what seems like just another metals and glass trading business. Cookson couldn't have imagined that his modest enterprise would evolve into a global industrial powerhouse, let alone that it would one day control the flow of molten metal in steel plants halfway around the world.

For nearly three centuries, the Cookson business morphed through Britain's industrial revolution like a corporate chameleon. It traded metals, manufactured glass, dabbled in chemicals, and gradually built expertise in materials that could withstand extreme conditions. The real transformation came in 1982 when the sprawling conglomerate, then known as Lead Industries Group, rebranded itself as Cookson Group—a signal that lead was no longer the future. Five years later, in 1987, came the masterstroke: Cookson acquired the Vesuvius Crucible Company, an American ceramics supplier whose products were becoming essential to steel production worldwide.

The Vesuvius acquisition wasn't just about adding another product line. It represented a fundamental shift in strategy—from trading and basic manufacturing to high-technology ceramics that solved critical problems in metal production. Vesuvius's refractories weren't commodities; they were engineered solutions that could mean the difference between a steel plant running efficiently or suffering catastrophic failure. Meanwhile, halfway across the world, India stood at its own crossroads in 1991. The country was in the midst of its worst economic crisis since independence—foreign exchange reserves had dwindled to barely three weeks of imports, gold was being airlifted to secure emergency loans, and the old socialist model had run its course. India's foreign exchange reserves fell to dangerously low levels, covering less than three weeks of imports. The country had to airlift gold to secure emergency loans.

It was in this crucible of crisis that opportunity emerged. Although some attempts at liberalisation were made in 1966 and the early 1980s, a more thorough liberalisation was initiated in 1991. For Vesuvius UK, India's liberalization presented a once-in-a-generation opportunity. Here was a massive steel market about to be unleashed, with antiquated production facilities that desperately needed modernization and virtually no domestic competition in advanced refractories.

The timing couldn't have been more perfect. India's steel industry, long shackled by the License Raj, was about to explode. Private players would soon be allowed to enter steel production, existing plants would need to modernize to compete globally, and the demand for sophisticated refractory solutions would skyrocket. Vesuvius moved swiftly, incorporating Vesuvius India Limited (originally named Vesuvius Refractories Limited) in September 1991, with the UK parent taking a 55.57% stake.

BISWADIP GUPTA was appointed the director of VESUVIUS INDIA LTD on 07-09-1991. The association with Biswadip Gupta and other local partners wasn't just about regulatory compliance—it was about understanding the labyrinthine world of Indian industrial relationships. In a country where business relationships often span generations and trust is built over decades, having the right local partners was as crucial as having the right technology.

What Vesuvius brought to India wasn't just products but an entire ecosystem of metallurgical expertise built over centuries. They understood something fundamental that many foreign entrants missed: India didn't need charity or hand-me-down technology. It needed world-class solutions adapted to local conditions—the scorching heat of Rajasthan where plants operated, the monsoon deluges that disrupted supply chains, the unique grade of iron ore from Odisha mines.

The company's entry strategy was surgical in its precision. Rather than trying to serve the entire subcontinent from imported products, Vesuvius committed to local manufacturing from day one. This wasn't the typical foreign company playbook of testing waters with imports before considering local production. It was a bold bet that India's steel industry was about to enter a golden age, and Vesuvius wanted to be embedded in its foundation.

III. The Refractory Business Model: Selling to Steel (1991–2000)

Inside a steel plant blast furnace, temperatures reach 2,000°C—hot enough to melt rock, vaporize most metals, and turn sand into glass within seconds. At these temperatures, molten iron flows like water, and without the right containment, it would burn through concrete, steel, or any conventional material like tissue paper. This is where refractories enter the picture—specialized ceramic materials that can withstand these hellish conditions while maintaining their structural integrity.

To understand Vesuvius's business model, imagine selling razor blades to barber shops. The initial sale of a furnace lining might be substantial, but the real value lies in the continuous need for replacement and maintenance. Every ton of steel produced gradually erodes the refractory lining. Every thermal cycle—heating and cooling—creates microscopic cracks. Every chemical reaction between molten metal and lining degrades the ceramic structure. This isn't a flaw; it's physics. And it's the foundation of one of the most elegant recurring revenue models in industrial B2B.

Vesuvius's product portfolio reads like an encyclopedia of materials science: flow control refractories that regulate the movement of molten steel from ladle to mold, advanced refractories that line the furnaces and vessels, digital measurement systems that monitor temperature and chemical composition in real-time, and crucibles for specialized melting applications. Each product category serves a critical function in steel production, and failure of any component can result in catastrophic consequences—not just equipment damage but potential loss of life. The Company's early manufacturing infrastructure consisted of four factories one each at Kolkata, Mehsana and two at Visakhapatnam. Commercial production started in its first factory at Kolkata from July 1, 1994. The factory at Kolkata, which is highly automated, has been set up for manufacture of Continuous Casting Refractories with the latest technology imported from the foreign collaborators, Vesuvius Crucible Company, USA.

Building trust with India's steel giants—Tata Steel, SAIL, JSW—was like courting royalty. These weren't customers you could win with a PowerPoint presentation and a handshake. The sales cycles stretched for years, involving countless plant visits, technical demonstrations, and pilot projects. Engineers from Vesuvius would spend weeks at customer sites, studying their specific processes, understanding their pain points, and customizing solutions.

Consider the complexity: A typical integrated steel plant has dozens of furnaces, each with unique operating conditions. The blast furnace operates continuously for years, the basic oxygen furnace undergoes violent chemical reactions with each batch, and the electric arc furnace subjects refractories to intense thermal shock. Each application demands different refractory formulations—some prioritizing thermal resistance, others chemical inertness, still others mechanical strength.

The genius of Vesuvius's approach lay in positioning themselves not as vendors but as metallurgical partners. When a steel plant faced quality issues—inclusions in the steel, inconsistent chemistry, surface defects—Vesuvius engineers would diagnose whether refractory contamination was the culprit. When productivity dropped, they'd analyze if flow control systems needed optimization. This consultative approach transformed a commodity sale into a technical partnership.

Latest technology is also provided to the Monolithics factories at Visakhapatnam and to the crucible manufacturing factory at Mehsana by the Vesuvius Group. The factory at Mehsana manufactures crucibles, nozzles etc with technology received from Becker & Piscantor now known as Vesuvius, Germany. This technology transfer from the parent wasn't just about importing machinery—it was about transplanting decades of metallurgical knowledge into Indian operations.

The economics were compelling. A steel plant might spend ₹50-100 crores on initial refractory installation, but the annual replacement and maintenance could run ₹10-20 crores—every year, forever. Miss one replacement cycle, and you risk a breakout—molten steel burning through the furnace shell, potentially causing millions in damage and weeks of lost production. This created switching costs that weren't just financial but existential.

By 2000, Vesuvius had cracked the code of Indian steel. They understood that Indian plants, operating with lower-grade ore and higher ash content than their global counterparts, needed specialized refractory formulations. They learned that monsoon humidity affected product storage and developed packaging solutions. They recognized that Indian customers valued technical support as much as product quality and built teams of field engineers who became fixtures at customer plants.

The trust-building paid off spectacularly. Once Vesuvius products were specified into a plant's operations, displacement became nearly impossible. Switching refractory suppliers meant retraining operators, recalibrating processes, and accepting months of operational risk as new products were tested. For risk-averse plant managers, the calculation was simple: why gamble with alternatives when Vesuvius delivered consistent performance?

IV. Scaling with India's Steel Boom (2000–2010)

The new millennium dawned with India consuming just 30 kilograms of steel per capita—a tenth of the global average and a fraction of what developed nations used. For perspective, Americans consumed 400 kilograms per person, the Chinese were rapidly climbing past 100, and even Brazil used twice as much as India. This wasn't just a statistic; it was a coiled spring of pent-up demand waiting to explode.

What followed was one of the most spectacular industrial expansions in history. India's GDP growth accelerated past 7%, then 8%, touching 9% in boom years. Every percentage point of GDP growth pulled steel demand higher—new airports, highways, metros, ports, power plants, commercial complexes. The Golden Quadrilateral highway project alone consumed millions of tons of steel. The Delhi Metro, Mumbai's sea link, IT parks in Bangalore—each project was a steel plant's order book for months. For Vesuvius, this wasn't just growth—it was a gold rush. Every new steel plant needed refractories, every capacity expansion required their products, every modernization drive meant replacing old linings with advanced materials. In 2009, Vesuvius India reported a significant financial milestone with a revenue of approximately ₹382 crore. By 2022, Vesuvius India achieved a revenue of around ₹770 crore, reflecting a compounded annual growth rate (CAGR) of roughly 15% from 2009.

The competitive landscape during this period resembled a Wild West shootout. Local players, sensing opportunity, mushroomed across industrial belts. Chinese manufacturers, armed with rock-bottom prices, began flooding the market with basic refractories. European competitors like RHI Magnesita and domestic players like IFGL Refractories expanded aggressively. Yet Vesuvius maintained its edge through a simple but powerful moat: when you're pouring molten steel at 1,600°C, nobody wants to experiment with untested suppliers to save 10% on costs.

The technology transfer from the parent company became Vesuvius India's secret weapon. While competitors sold products, Vesuvius sold solutions backed by global R&D. When Indian steel plants struggled with inclusion problems—tiny impurities that weakened steel—Vesuvius introduced isostatically pressed products that minimized contamination. When continuous casting became the norm, replacing traditional ingot casting, Vesuvius had ready solutions tested in plants from Pittsburgh to Pohang.

Building the distribution and service network was like constructing a parallel steel industry. Vesuvius established warehouses near every major steel cluster—Bokaro, Rourkela, Bellary, Salem. They recruited metallurgical engineers from IITs and NITs, trained them in facilities abroad, and embedded them at customer sites. These weren't salespeople; they were technical consultants who spoke the language of blast furnace operators and understood the chemistry of slag formation.

The company's growth strategy during this decade was remarkably disciplined. Rather than chasing every opportunity, they focused on high-value, high-margin products where technology mattered. Basic bricks for furnace walls? Let the commodity players fight over those. But the submerged entry nozzle that controls steel flow in continuous casting? The slide gate that regulates molten metal with millimeter precision? These were Vesuvius's domain, where a single product failure could cost millions and where customers paid premiums for reliability.

One telling anecdote from this period: A major steel plant in Eastern India suffered a catastrophic breakout when a competitor's refractory failed. Molten steel burst through the furnace shell, causing ₹50 crores in damage and shutting production for three weeks. The plant immediately switched all critical applications to Vesuvius products. The competitor's refractory might have been 20% cheaper, but the total cost of failure was astronomical. Stories like these spread through the tight-knit steel industry, cementing Vesuvius's reputation as the safe choice.

The financial metrics during this boom period tell only part of the story. Revenue grew steadily, but more importantly, customer relationships deepened. Vesuvius wasn't just riding India's steel wave—they were helping to create it, enabling plants to push productivity higher, quality better, and costs lower. As India's steel production doubled from 30 million tons to 60 million tons during the decade, Vesuvius's products touched virtually every ton.

V. The Foseco Integration & Global Synergies (2008–2015)

In 2008, while the world teetered on the brink of financial collapse, Vesuvius's parent company made a billion-dollar bet that would transform its Indian operations. The acquisition of Foseco, a British supplier to the foundry and steel industries, for $1 billion wasn't just another corporate deal—it was a strategic masterstroke that would double Vesuvius's addressable market in India overnight.

Foseco brought something Vesuvius India desperately needed: dominance in the foundry market. While Vesuvius had conquered steel plants, India's thousands of foundries—producing everything from automotive components to pump castings—remained largely untapped. These foundries, scattered across industrial clusters from Coimbatore to Rajkot, represented a market as large as steel but far more fragmented and technically diverse.

The integration wasn't without challenges. Foseco had its own legacy, dating back to 1932, its own customer relationships, and critically, its own product technologies that complemented rather than competed with Vesuvius's portfolio. Feeding systems that ensured defect-free castings, filtration products that removed impurities, coating materials that prevented metal-mold reactions—suddenly, Vesuvius India could offer complete solutions to both steel plants and foundries.

The timing of this integration coincided with the 2008 financial crisis, which initially seemed catastrophic. Global steel demand plummeted, automotive production crashed, and industrial investment froze. Vesuvius India's customers delayed expansion plans, stretched payment terms, and squeezed suppliers for discounts. Revenue growth stalled, margins compressed, and the integration of Foseco's operations had to be managed while fighting fires on multiple fronts.

Yet crisis breeds opportunity for those positioned to seize it. As weaker competitors struggled with working capital and banks tightened lending, Vesuvius leveraged its parent's balance sheet strength to maintain inventory, extend credit to customers, and most importantly, continue investing in technical support. When a major auto components manufacturer in Chennai faced quality issues that threatened exports to Germany, Vesuvius's newly integrated Foseco team solved the problem with specialized coatings, cementing a relationship worth crores annually.

The real magic of the Foseco integration revealed itself in cross-selling opportunities. A steel plant using Vesuvius refractories often had an attached foundry for producing spare parts. A foundry customer buying Foseco feeding systems might have a sister company with steel melting furnaces. The combined entity could now walk into any metallurgical operation in India with solutions for every molten metal challenge.

Product portfolio expansion went beyond simple addition. The combined R&D capabilities enabled innovations at the intersection of technologies. Digital services, which neither company could have justified alone, became viable with the larger combined customer base. Predictive maintenance systems that used sensors to monitor refractory wear, previously tested in European plants, could now be economically deployed in India.

Operational efficiencies from the merger were substantial but subtle. Raw material procurement consolidated, giving better negotiating power with suppliers. The logistics network optimized, with Foseco products moving through Vesuvius warehouses. Technical teams cross-trained, creating engineers who understood both steel and foundry applications. Even seemingly minor synergies, like combined trade show booths and unified customer seminars, reduced costs while projecting greater market presence.

The integration also brought cultural challenges that required delicate navigation. Foseco's foundry sales approach—relationship-driven, highly personalized, often involving years of trust-building with family-owned foundries—differed from Vesuvius's more technical, process-oriented steel industry approach. Merging these cultures without alienating either customer base or sales team required careful orchestration.

By 2015, the integration had transformed Vesuvius India from a steel refractories company into a comprehensive molten metal flow engineering powerhouse. The company could now claim to touch virtually every ton of metal—ferrous or non-ferrous—cast in India. The financial crisis that initially threatened to derail the integration had instead accelerated market consolidation, leaving Vesuvius stronger and competitors weakened.

VI. Digital Transformation & Industry 4.0 (2015–2020)

The year 2015 marked an inflection point in global manufacturing, and inside Vesuvius India's R&D center in Kolkata, engineers were grappling with a radical question: What if refractories could talk? Not literally, of course, but what if these ceramic linings could communicate their condition, predict their own failure, and optimize their own performance? This wasn't science fiction—it was the dawn of Industry 4.0 in refractory technology.

The transformation began with a simple observation: steel plant operators were flying blind. They knew refractories were wearing out—that was inevitable—but they didn't know exactly how fast, where the wear was critical, or when replacement was optimal. Too early, and you waste money replacing functional materials. Too late, and you risk catastrophic failure. The traditional solution? Conservative guesswork and excessive safety margins.

Vesuvius's digital journey started with embedding sensors in critical refractories. These weren't ordinary sensors—they had to survive 1,600°C temperatures, violent chemical reactions, and mechanical stresses that would destroy normal electronics. The company leveraged its parent's global R&D, adapting technologies tested in Japanese and German plants for Indian conditions. The first installations were disasters—sensors failed, data transmission was erratic, and skeptical plant managers questioned the value.

But persistence paid off. By 2017, Vesuvius had developed robust sensing systems that could monitor temperature gradients, track erosion patterns, and detect chemical infiltration in real-time. The data streamed to cloud platforms where machine learning algorithms, trained on decades of failure patterns, could predict remaining refractory life with stunning accuracy. A steel plant in Gujarat became the poster child—predictive maintenance reduced unplanned downtime by 30% and extended refractory life by 15%.

The shift from selling products to selling outcomes fundamentally changed Vesuvius's business model. Instead of simply supplying refractories and hoping they lasted, the company began offering performance contracts. "We guarantee your refractory costs won't exceed X rupees per ton of steel produced," became the pitch. If refractories lasted longer than expected, Vesuvius shared the savings. If they failed prematurely, Vesuvius bore the cost. This aligned incentives perfectly—suddenly, Vesuvius's profits depended not on selling more refractories but on making them last longer. Digital services and technical assistance weren't just add-ons—they became central to customer relationships. When Indian steel plants faced increasing pressure to reduce costs during the global commodity downturn of 2015-2016, Vesuvius's value proposition shifted from "we supply quality refractories" to "we optimize your total refractory cost per ton of output." This subtle but profound change meant Vesuvius engineers were now measured not on how much they sold but on how efficiently their customers operated.

The company also pioneered remote diagnostic services. Using augmented reality, a plant operator in Jharkhand could show a crack pattern to a Vesuvius expert in Kolkata, who could diagnose the issue and recommend corrective action in real-time. This wasn't just about technology—it was about building trust that digital solutions could match or exceed traditional on-site expertise.

Then came March 2020. India announced one of the world's strictest lockdowns, and steel plants—classified as essential services—had to continue operating with skeleton crews. Lockdowns were announced in Kerala on 23 March, and in the rest of the country on 25 March. For Vesuvius, this created an existential challenge: How do you service critical industrial infrastructure when movement is restricted, supply chains are disrupted, and customer plants are operating in crisis mode?

The company's response showcased remarkable resilience. Within weeks, Vesuvius created "digital war rooms" where technical teams could remotely monitor multiple plants simultaneously. Emergency inventory was pre-positioned at customer sites. Mobile testing laboratories were deployed to ensure quality control when regular logistics failed. Most importantly, the company guaranteed supply continuity even as smaller competitors faltered.

While India's GDP contracted 7.3% in FY 2020–21, COVID-19 deepened and exposed the fault lines of the economy. Yet for Vesuvius, the crisis accelerated digital adoption by years. Steel plants that had resisted remote monitoring suddenly embraced it as a necessity. Performance-based contracts, previously a hard sell, became attractive as customers sought to variabilize costs during uncertain times.

The pandemic also revealed the strength of Vesuvius's global supply chain. When raw material sources in one region were disrupted, the parent company's network enabled rapid substitution from alternative sources. This flexibility, impossible for standalone domestic players, meant Vesuvius could maintain production when competitors faced shortages.

By late 2020, as India's economy began recovering, Vesuvius emerged stronger. The company had not only survived the crisis but had deepened customer relationships, accelerated digital transformation, and gained market share from weakened competitors. The forced experiment of remote operations had proven that many traditional practices were outdated, paving the way for a more efficient, technology-driven future.

VII. The Modern Era: Capacity Expansion & Market Leadership (2020–Present)

November 2024, Visakhapatnam. The ribbon falls on Vesuvius India's newest manufacturing complex—state-of-the-art Alumina-Silica (AlSi) and Basic Monolithic plants that represent not just capacity addition but a technological leap. Inaugurated new Alumina-Silica (AlSi) and Basic Monolithic manufacturing plants in Visakhapatnam in November 2024 The timing is no coincidence. India's steel production, already the world's second-largest, is targeting 300 million tons by 2030, and every ton will need Vesuvius's products. The financial performance tells a story of relentless execution. For the full fiscal year ending December 2024, Vesuvius India's net profit increased by 24.22% to Rs 264.52 crore, while net sales grew by 17.20% to Rs 1,864.97 crore, compared to the previous fiscal year. These aren't just numbers—they represent market share gains in a competitive landscape where Chinese players are aggressively pricing and domestic competitors are scaling up.

The stock split decision announced in February 2025—dividing each existing equity share with a face value of Rs 10 into ten shares with a face value of Rs 1 each—signals management's confidence and desire to broaden retail participation. When a B2B industrial company that sells to steel plants decides to make its stock more accessible to retail investors, it's betting that the India growth story has legs.

Competition from Chinese players has intensified, but Vesuvius's response has been strategic rather than reactive. Instead of matching Chinese prices on commodity refractories, the company has moved further up the value chain. Advanced ceramics that can extend furnace campaigns by 20%, flow control systems that reduce steel defects by 30%, digital solutions that optimize entire plants—these are products where technology trumps price.

The import substitution narrative has also worked in Vesuvius's favor. As India pushes for self-reliance in critical industries, steel plants are increasingly wary of depending on Chinese suppliers for essential consumables. Vesuvius, with its local manufacturing and global technology access, positions itself as the ideal partner—Indian enough to be trusted, global enough to be world-class.

ESG initiatives have transformed from compliance checkboxes to competitive advantages. Steel plants facing pressure to reduce carbon emissions find Vesuvius's products essential—refractories that enable higher energy efficiency, materials that reduce waste, digital systems that optimize resource consumption. The green steel revolution isn't just an environmental imperative; it's reshaping the entire value chain, and Vesuvius sits at its heart.

The company's expansion into adjacent verticals—solar glass manufacturing, specialized foundries for electric vehicles, even semiconductor fabrication facilities—demonstrates strategic foresight. Each of these industries requires high-temperature materials and molten metal handling expertise. The same core competencies that dominate steel refractories translate into new growth avenues.

What's particularly impressive is the operational discipline. Despite rapid expansion, working capital management has improved. Despite inflationary pressures, margins have expanded. Despite market volatility, cash generation has strengthened. This isn't the profile of a cyclical commodity supplier but of a technology-driven industrial franchise.

The modern Vesuvius India barely resembles the company that entered India in 1991. From four factories to an integrated manufacturing network, from basic refractories to digital solutions, from steel industry supplier to multi-industry partner—the transformation has been remarkable. Yet the fundamental business model remains unchanged: selling mission-critical consumables to industries that cannot afford failure.

VIII. Financial Deep Dive & Unit Economics

Inside Vesuvius India's financial statements lies one of the most elegant business models in Indian manufacturing. Company is almost debt free. Company has delivered good profit growth of 24.2% CAGR over last 5 years But these headline numbers only scratch the surface of what makes this business exceptional.

The consumables model is the cornerstone. Approximately 70% of revenue comes from products that must be regularly replaced—a built-in annuity that smooths the inherent cyclicality of steel markets. When a steel plant installs Vesuvius refractories in a blast furnace, they're not just buying a product; they're entering a 5-7 year relationship where replacement cycles are as predictable as monsoons.

Consider the unit economics of a typical continuous casting installation. The initial setup might cost ₹5 crores, but annual consumables—submerged entry nozzles, tundish linings, mold fluxes—run ₹1-2 crores. Over a decade, the consumables revenue is 2-4 times the initial capital sale. More importantly, switching suppliers mid-campaign risks production disruptions worth hundreds of crores, creating switching costs that dwarf any potential savings.

Pre-tax margin of 19% is exceptional for an industrial products company, especially one exposed to commodity cycles. This pricing power doesn't come from monopoly but from criticality. When your product failure can cause a ₹100 crore production loss, customers don't haggle over a few percentage points of price. The value-in-use far exceeds the cost, creating a pricing umbrella that commodity players can't penetrate.

ROE of 18% reflects optimal capital allocation. Unlike steel plants that require massive capital for expansion, Vesuvius's asset-light model generates returns that compound beautifully. A new product line might require ₹20-30 crores of investment but can generate ₹100 crores of annual revenue within three years. This capital efficiency enables both growth investment and generous dividends—a rare combination in industrial businesses.

Stock trading at 7.35 times its book value might seem expensive, but consider the intangibles not captured on the balance sheet. Customer relationships built over decades, technical expertise that takes years to develop, the trust that comes from never causing a plant shutdown—these assets don't appear in book value but drive the earnings power.

Working capital management reveals operational excellence. In a business where customers are large steel plants with negotiating leverage, Vesuvius maintains reasonable payment terms while managing inventory efficiently. The company doesn't just sell products; it maintains consignment stocks at customer sites, charging only upon consumption. This increases working capital needs but deepens customer stickiness—a strategic trade-off that pays dividends in customer retention.

The cash conversion story is particularly compelling. Despite growing revenues, cash generation has outpaced profit growth due to working capital optimization and minimal maintenance capex needs. Unlike asset-heavy industries where depreciation is a real economic cost, Vesuvius's depreciation largely reflects growth investments that enhance competitive position.

Segment economics reveal strategic focus. The advanced refractories segment, contributing about 60% of revenue, generates disproportionate profits due to higher technology content. The services segment, though smaller, carries minimal capital requirements and generates recurring revenue through long-term contracts. This portfolio approach balances growth, profitability, and stability.

The financial resilience during downturns deserves attention. During the 2015-2016 steel crisis, when steel companies globally faced existential threats, Vesuvius maintained profitability. During COVID-19, when industrial production collapsed, the company remained cash-positive. This isn't luck—it's the result of variable cost structures, diversified customer base, and essential product characteristics.

What's hidden in these numbers is optionality value. Every new steel plant is a decade-long revenue stream. Every environmental regulation that requires cleaner steel production drives demand for advanced refractories. Every push toward quality steel for infrastructure creates need for better flow control. The company isn't just riding current trends; it's positioned to benefit from multiple future scenarios.

IX. Playbook: B2B Industrial Moats

The Vesuvius India story offers a masterclass in building and defending B2B industrial moats. Unlike consumer businesses where brand and distribution create advantages, industrial moats require different architecture—one built on technical expertise, switching costs, and embedded relationships.

High switching costs form the first moat. When a steel plant manager considers changing refractory suppliers, the decision tree is sobering. Requalification takes 6-12 months. Production trials risk quality issues. Operator retraining disrupts established routines. Inventory systems need reconfiguration. A 10% price saving might translate to ₹2 crores annually, but a single production mishap could cost ₹50 crores. The math inevitably favors the incumbent.

Technical expertise as competitive advantage goes beyond having good engineers. It's about accumulated knowledge—understanding why a particular steel grade requires specific refractory chemistry, knowing how monsoon humidity affects product performance, recognizing early warning signs of refractory failure. This tacit knowledge, built through thousands of plant interactions over decades, can't be hired away or reverse-engineered.

The parent-subsidiary dynamic creates unique advantages. Technology access from Vesuvius plc means Indian operations can leverage global R&D without bearing full development costs. When a breakthrough in sensor technology happens in Germany, Indian customers benefit within months. Conversely, solutions developed for Indian conditions—like handling high-ash coal in blast furnaces—get deployed globally, cementing the subsidiary's importance within the group.

Distribution and service network effects compound over time. Each field engineer stationed at a customer plant becomes a sensing node, identifying problems, suggesting improvements, and deepening relationships. This distributed intelligence network creates a learning system where insights from one plant improve operations at another. Competitors can match products but can't replicate decades of accumulated field knowledge.

R&D investments and product innovation cycles create a moving target for competitors. By the time competitors reverse-engineer current products, Vesuvius has moved to next-generation solutions. The company spends approximately 2% of revenue on R&D—modest by pharmaceutical standards but significant for industrial products. More importantly, this R&D is directed by actual customer problems, not academic curiosity, ensuring commercial relevance.

The playbook extends beyond products to business model innovation. Performance-based contracts align incentives. Digital services create recurring revenue streams. Predictive maintenance shifts value from reactive to proactive. Each innovation adds another layer to the moat, making displacement increasingly difficult.

Customer concentration, often seen as risk, becomes an advantage when properly managed. Vesuvius doesn't just serve steel plants; it becomes embedded in their operations. Engineers attend production meetings. Technical teams participate in expansion planning. This integration level means changing suppliers requires unwinding years of process integration—a deterrent that grows stronger over time.

The lessons for other industrial B2B businesses are clear. First, focus on mission-critical applications where failure costs dwarf product costs. Second, invest in technical capabilities that compound over time. Third, create switching costs through integration, not lock-in. Fourth, leverage global resources while maintaining local responsiveness. Fifth, shift from selling products to delivering outcomes.

The playbook also reveals what doesn't work. Competing on price in technical products is a race to the bottom. Geographic expansion without technical differentiation invites local competition. Vertical integration into customer operations risks channel conflict. The discipline to stay within the circle of competence, while continuously expanding that circle's edge, defines successful B2B industrial companies.

What makes Vesuvius's playbook particularly powerful is its applicability across industrial transitions. Whether steel production shifts to hydrogen-based processes, electric arc furnaces dominate, or entirely new materials emerge, the core competency—managing materials at extreme conditions—remains valuable. The company isn't betting on specific technologies but on the perpetual need for materials that perform where others fail.

X. Bear vs. Bull Case Analysis

Bull Case: The India Infrastructure Supercycle

India's steel consumption per capita sits at 80 kilograms, compared to the global average of 230 kilograms and China's 650 kilograms. This isn't just a gap—it's a coiled spring of demand waiting to unleash over the next decade. As India builds infrastructure equivalent to adding a new United Kingdom every year, steel demand could double by 2030. Every ton of additional steel production requires Vesuvius's products, creating a revenue runway measured in decades, not years.

The import substitution narrative strengthens with geopolitical tensions. Steel plants increasingly prefer local suppliers with global technology over Chinese imports with supply chain risks. Vesuvius's sweet spot—Indian manufacturing with British technology—positions it perfectly for this shift. The government's production-linked incentive schemes and quality control orders further tilt the playing field toward established domestic manufacturers.

Technology leadership through parent support provides sustained competitive advantage. While local competitors struggle with R&D investments, Vesuvius accesses cutting-edge developments from global operations. The upcoming shift to green steel—using hydrogen instead of coal—requires entirely new refractory solutions. Vesuvius's parent has already deployed these technologies in European plants, giving the Indian subsidiary a multi-year head start.

The debt-free balance sheet in a capital-intensive industry is like bringing a gun to a knife fight. While competitors struggle with interest costs and capital constraints, Vesuvius can invest counter-cyclically, gain market share during downturns, and pursue strategic acquisitions. The strong cash generation funds both growth and dividends, attracting quality investors who provide stable share prices during volatile periods.

Expansion into new verticals—solar glass, lithium-ion battery manufacturing, semiconductor fabrication—opens addressable markets beyond steel. Each vertical requires high-temperature materials expertise, playing to Vesuvius's core strengths. The solar glass opportunity alone could add ₹200-300 crores in revenue as India builds gigawatt-scale solar capacity.

Bear Case: The Cyclical Sword of Damocles

Steel industry cyclicality remains the fundamental risk. When global steel prices collapse, as they did in 2015-2016, steel plants defer maintenance, extend refractory life dangerously, and squeeze suppliers mercilessly. Vesuvius's revenue might be more stable than steel prices, but it's not immune. A prolonged steel downturn could slash revenues by 20-30% and compress margins even more.

Chinese competition intensifies with every passing year. Chinese refractory manufacturers, backed by state support and massive scale, are moving up the technology curve. What was a 30% price discount on basic refractories is becoming a 20% discount on advanced products. As Chinese quality improves, the technical moat narrows, forcing Vesuvius to compete more on price.

High valuation multiples leave little room for disappointment. Trading at 40+ times earnings and 7+ times book value, the stock prices in perfect execution and sustained growth. Any earnings miss, margin compression, or growth deceleration could trigger significant multiple compression. The stock's outperformance has created expectations that become increasingly difficult to meet.

Customer concentration risk is real and growing. The top 10 customers contribute over 60% of revenues. If a major customer like Tata Steel or JSW decided to backward integrate or switch to Chinese suppliers for even part of their requirements, the revenue impact would be severe. The concentrated Indian steel industry structure amplifies this risk.

Raw material cost inflation poses ongoing challenges. Key inputs like alumina, graphite, and specialty chemicals face supply constraints and price volatility. While Vesuvius has pricing power, there's always a lag between cost inflation and price realization. Sustained input cost pressure could compress margins, especially if steel industry customers push back on price increases during their own challenging periods.

Environmental regulations could disrupt traditional business models. As steel production shifts toward electric arc furnaces and hydrogen-based processes, demand for traditional refractories might decline. While Vesuvius is developing solutions for these new technologies, the transition period could see revenue pressure as old technologies phase out faster than new ones scale up.

The Balanced View

The truth, as always, lies between extremes. Vesuvius India is neither a risk-free compounder nor a cyclical value trap. It's a high-quality business with structural growth drivers, operating in a cyclical industry with real risks. The company's competitive advantages are genuine but not impregnable. The growth opportunity is substantial but not guaranteed.

For investors, the key question isn't whether Vesuvius is a good business—it clearly is. The question is whether it's a good investment at current valuations. The answer depends on time horizon, risk tolerance, and belief in India's infrastructure story. For those convinced that India will build its way to prosperity over the next decade, Vesuvius offers a picks-and-shovels approach to that theme. For those worried about near-term cyclical pressures or valuation multiples, patience might be prudent.

XI. Epilogue: The Future of Industrial India

As dawn breaks over the Visakhapatnam plant, where automated systems now produce refractories that will line furnaces from Jamshedpur to Salem, the future of industrial India takes shape. It's a future where green steel produced with hydrogen replaces coal-based production, where artificial intelligence optimizes furnace operations, where sustainability isn't just compliance but competitive advantage. In this future, Vesuvius India isn't just a supplier but an architect of transformation.

The green steel revolution presents both disruption and opportunity. Traditional blast furnaces that burn coal will gradually give way to direct reduced iron processes using green hydrogen. Electric arc furnaces will dominate new capacity additions. Each transition requires new refractory solutions—materials that can withstand different chemical environments, thermal cycles, and mechanical stresses. For a company with century-old expertise in materials science and metallurgy, this isn't a threat but a generational opportunity to reset competitive dynamics.

Industry consolidation opportunities abound. India's refractory industry remains fragmented with dozens of small players serving local markets. As steel plants consolidate and modernize, they'll prefer suppliers who can serve multiple locations with consistent quality. Vesuvius, with its national presence and global backing, is positioned to lead this consolidation either through acquisitions or organic market share gains.

Southeast Asia expansion potential mirrors India's growth trajectory from a decade ago. Vietnam, Indonesia, and Bangladesh are building steel capacity to support their infrastructure ambitions. Vesuvius India, with its experience in emerging markets and cost-competitive manufacturing, could become the regional hub serving these markets. The parent company's global network provides market entry support while Indian operations offer relevant expertise.

Digital services revenue growth represents the highest-margin opportunity. As steel plants digitize operations, they need partners who understand both bytes and blast furnaces. Vesuvius's digital solutions—combining IoT sensors, analytics, and metallurgical expertise—can expand from 5% of revenue today to 20% by 2030. These services carry 40%+ margins and create even stickier customer relationships.

What would we do as CEOs? First, accelerate digital transformation, making Vesuvius the "Bloomberg Terminal" of refractories—indispensable for daily operations. Second, pursue strategic acquisitions in adjacent materials like technical ceramics for electronics or specialized coatings for renewable energy. Third, establish innovation centers at customer sites, embedding Vesuvius even deeper into their operations. Fourth, develop sustainability solutions that help customers achieve net-zero targets. Fifth, build optionality for multiple futures rather than betting on single scenarios.

The key lessons for investors and entrepreneurs are timeless yet timely. First, B2B businesses selling mission-critical products to growing industries can generate exceptional returns with lower volatility than consumer businesses. Second, technical moats based on accumulated expertise and switching costs prove more durable than brand or scale advantages. Third, the intersection of global technology and local execution creates sustainable competitive advantages in emerging markets.

The Vesuvius India story also challenges conventional wisdom. Who would have thought that a company selling ceramic linings to steel plants could generate 20%+ profit growth? That a 300-year-old British company's Indian subsidiary would become essential to India's infrastructure ambitions? That products invisible to consumers could create more value than celebrated consumer brands?

As India stands at the cusp of a manufacturing renaissance, companies like Vesuvius will play crucial but uncelebrated roles. They won't feature in advertisements or trending hashtags. Their CEOs won't become household names. But when future historians write about India's transformation from a $3 trillion to $10 trillion economy, they'll recognize that it was built on a foundation of steel—and that steel was made possible by companies like Vesuvius.

The story comes full circle. From Isaac Cookson's modest trading business on the River Tyne to a ₹10,000+ crore company powering India's industrial ambitions, Vesuvius embodies the patient accumulation of expertise, the power of technological evolution, and the value of being essential rather than visible. In a world obsessed with disruption, Vesuvius reminds us that some businesses succeed by enabling others' transformations while continuously reinventing themselves.

For those willing to look beyond the glamorous and seek the essential, for investors who value cash flows over narratives, for entrepreneurs who understand that solving hard problems creates lasting value—the Vesuvius story offers both inspiration and instruction. The future belongs not to those who make the most noise but to those who make the most difference. In the furnaces of India's steel plants, where Vesuvius products silently perform their crucial role, that future is being forged today.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube