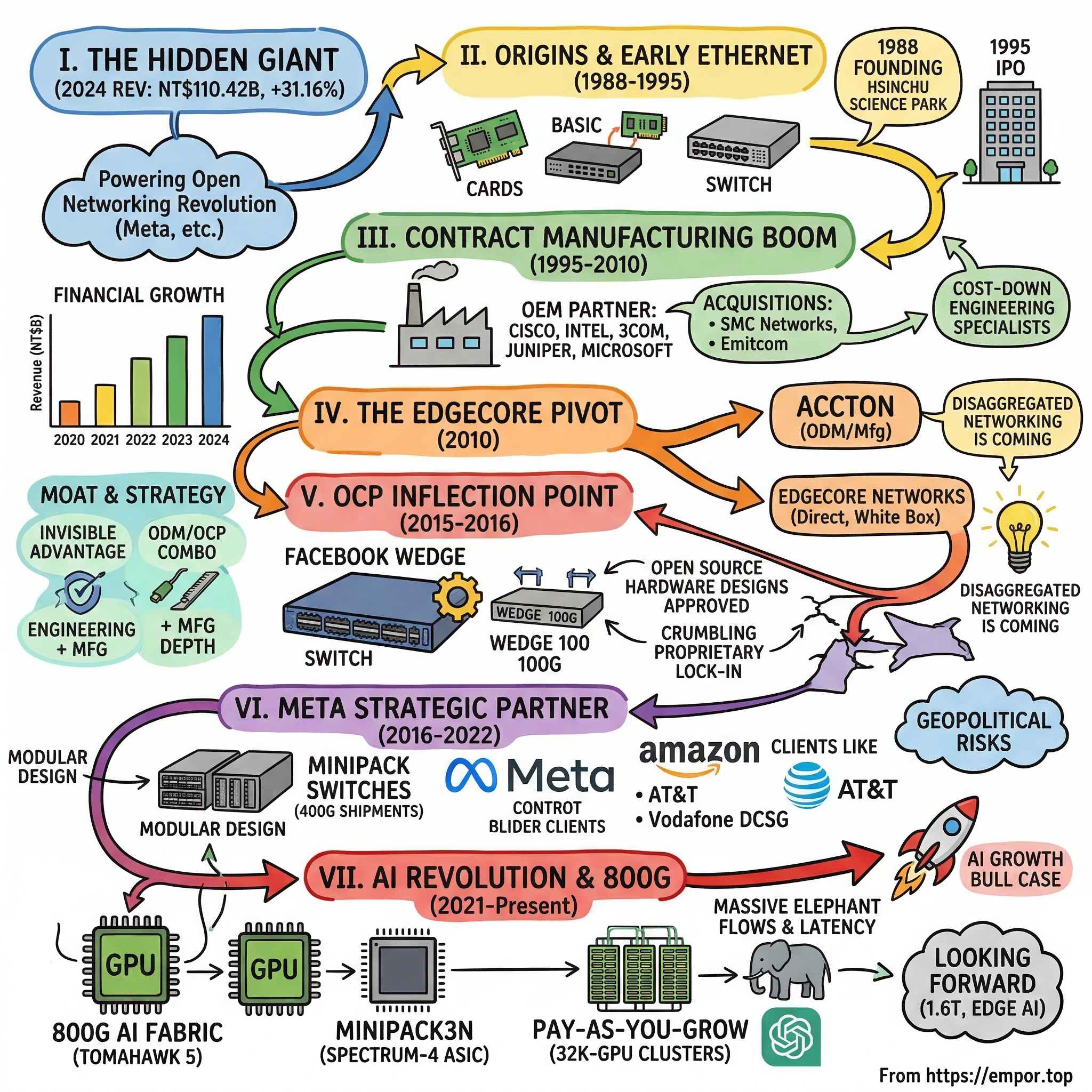

Accton Technology: The Hidden Giant Powering the Open Networking Revolution

I. Introduction & Cold Open

Picture this scene: Inside Meta's sprawling data center in Prineville, Oregon, thousands of servers hum with the computational intensity of training the next generation of AI models. The networking equipment connecting these machines—sleek, unassuming boxes marked only with cryptic model numbers—carries no household brand names. Yet these switches, manufactured by a Taiwanese company most people have never heard of, form the nervous system of the infrastructure powering billions of users across Facebook, Instagram, and WhatsApp.

In 2024, Accton Technology's revenue was 110.42 billion Taiwan dollars, an increase of 31.16% compared to the previous year's 84.19 billion—roughly $3.4 billion USD. The company's market capitalization now hovers around $19 billion, placing it among Taiwan's most valuable technology firms. Yet outside of hyperscale data center operators and networking engineers, Accton Technology remains virtually unknown.

Founded on February 9, 1988, and headquartered in Taiwan's Silicon Valley—the Hsinchu Science Park—Accton has spent nearly four decades perfecting the art of being invisible. While companies like Cisco and Juniper built their brands selling networking equipment to enterprises, Accton chose a different path: becoming the manufacturer behind the manufacturers, the engineering powerhouse that turns cutting-edge silicon into the switches that move the world's data.

The central question of Accton's story isn't just how a contract manufacturer became indispensable to the world's largest technology companies. It's how this Taiwanese ODM recognized, years before others, that the future of networking wouldn't be controlled by proprietary vendors but by open hardware, collaborative design, and the relentless demands of hyperscale computing. In an industry where brand recognition typically commands premium valuations, Accton built a multi-billion dollar empire by deliberately staying in the shadows—until the AI revolution thrust them into the spotlight.

II. Origins & Taiwan's Tech Emergence (1988-1995)

The late 1980s in Taiwan buzzed with the electricity of technological transformation. As Morris Chang's TSMC pioneered the pure-play foundry model and Terry Gou's Foxconn began its ascent in electronics manufacturing, a group of engineers in Hsinchu saw an opportunity in the nascent world of local area networking. Accton was founded on February 9, 1988, just as enterprises worldwide were beginning to wire their offices with Ethernet cables and connect their first PCs into networks.

The timing was no accident. Taiwan's government had spent the previous decade pouring resources into the Hsinchu Science-Based Industrial Park, creating a fertile ecosystem where engineers returning from Silicon Valley could launch technology ventures with government support and access to a growing supply chain. Accton's founders—whose names remain surprisingly obscure in public records—weren't building a company to challenge 3Com or Novell directly. They were betting on something more fundamental: that networking equipment, like semiconductors, would eventually become commoditized, and the winners would be those who could manufacture at scale with consistent quality.

In those early years, Accton focused on the unglamorous but essential building blocks of office networks: Ethernet adapter cards, basic hubs, and simple switches that could connect a handful of computers. Founded in 1988 with headquarters based in Taiwan, Accton Technology Corporation is a global OEM/ODM leader in advanced networking and communication equipment. The company's engineers became specialists in taking reference designs from chip companies like Intel and turning them into manufacturable products—a capability that would prove invaluable as networking speeds increased from 10 Mbps to 100 Mbps and beyond.

Accton filled its IPO in November 1995, going public on the Taiwan Stock Exchange at a time when the internet boom was just beginning to accelerate. The IPO prospectus painted a picture of a company with modest ambitions: to be Taiwan's leading networking equipment manufacturer, serving international brands that lacked their own production facilities. What it didn't reveal was that Accton's leadership was already thinking bigger—recognizing that as networks became more complex and speeds increased, the technical barriers to entry would rise, creating opportunities for those with deep engineering expertise.

The contrast with Taiwan's other tech giants was instructive. While TSMC focused solely on manufacturing others' chip designs and Foxconn assembled consumer electronics, Accton occupied a middle ground—they could both design and manufacture networking products, giving them flexibility to serve as either an Original Equipment Manufacturer (OEM) producing others' designs or an Original Design Manufacturer (ODM) creating their own products for customers to brand. This dual capability would become their secret weapon in the decades to come.

III. The Contract Manufacturing Years (1995-2010)

The late 1990s brought Accton its first taste of scale. As the dot-com boom drove explosive demand for networking equipment, established vendors scrambled to keep up. In 2002, the company was chosen as Microsoft's OEM partner to supply their Microsoft Broadband Networking product line—a validation that Accton could meet the quality and scale requirements of the world's largest software company.

Yet it was in the shadows of giants that Accton truly thrived. Since 1999, manufactured networking products for major OEMs such as Cisco, Intel, 3Com, Juniper, and Fujitsu. Walking through Accton's factory floor in Hsinchu during this period, you would have seen production lines churning out products destined to carry some of the biggest names in networking—except those names would be applied at the very last stage, like designer labels sewn into garments manufactured in anonymous factories.

The company's acquisition strategy during this era revealed its ambitions. In 1997, they acquired SMC Networks, gaining not just manufacturing capacity but also a window into the branded equipment business. The 1999 acquisition of Emitcom expanded their wireless capabilities just as Wi-Fi was emerging as a critical technology. These weren't the splashy, billion-dollar deals that captured headlines—they were surgical strikes to acquire specific capabilities and customer relationships.

Engineers at Accton developed a particular expertise in what the industry calls "cost-down engineering"—taking expensive, over-engineered products and redesigning them for mass production without sacrificing quality. A former Cisco engineer who worked with Accton during this period (speaking on condition of anonymity) described their approach: "They would take our reference design and come back with ten ways to reduce the cost by 30% while actually improving manufacturability. They understood that every cent mattered when you're shipping millions of units."

By 2009, Accton's revenue mix told the story of a company that had found its niche: 69% from switches, 14% from WLAN products, and the remainder from various networking gear. They had become the invisible backbone of the networking industry, manufacturing products that powered everything from small business networks to telecommunications infrastructure. But as the 2000s drew to a close, Accton's leadership recognized that pure contract manufacturing was becoming a race to the bottom. Chinese competitors could manufacture more cheaply, and their major customers were increasingly looking to do more design work in-house. The company needed a new strategy—one that would leverage their engineering depth rather than just their manufacturing scale.

IV. The Edgecore Spin-off and Strategic Pivot (2010)

The boardroom discussions at Accton in early 2010 were intense. The company faced a strategic dilemma that would define its next decade: how to move up the value chain without competing with their own customers. The solution was elegant in its simplicity but complex in execution—split the company in two.

In 2010, Edge-Core Networks was spun-off into an independent subsidiary. Accton's subsidiary, Edge-Core Networks, will market products implementing these designs as part of its open network switch product line that allows data center operators to deploy cost-effective and flexible public and private cloud infrastructures. The division was more than organizational—it was philosophical. Accton would continue as the ODM powerhouse, designing and manufacturing products for other brands. Edgecore would sell directly to customers, but with a twist: they would focus on "white box" or "bare metal" switches that customers could load with their own software.

George Tchaparian, who would become CEO of Edgecore Networks and GM of Data Center Networks at Accton, articulated the vision in internal meetings: disaggregated networking was coming, and Accton/Edgecore would be ready. The traditional model—where Cisco or Juniper sold you an integrated hardware-software solution at premium prices—was showing cracks. Cloud giants like Amazon and Google were already building their own networking software. They just needed hardware platforms to run it on.

The dual-brand strategy created some awkward moments. Edgecore sales representatives would sometimes find themselves competing against products that their parent company, Accton, had manufactured for other brands. But the strategy had a crucial advantage: Accton could learn from both sides of the market. They could see what large-scale customers wanted when they bought directly from Edgecore, and they could understand vendor requirements through their ODM relationships.

In 2015, Accton made a revealing move: they acquired SMC Networks from Edge-Core for $25.1 million, essentially buying back a piece they had previously assigned to the subsidiary. The transaction highlighted the fluid boundaries between Accton and Edgecore—they were separate when it served customer needs but could restructure when strategy demanded it.

This period also saw Accton's manufacturing footprint expand significantly. Accton has manufacturing plants in Taiwan (Hsinchu), China (Shenzhen), and Vietnam (Vĩnh Phúc), supported by research and development centers in Taiwan, Shanghai, and California. The geographic diversity wasn't just about cost—it was about being close to component suppliers, navigating trade restrictions, and providing redundancy for customers increasingly concerned about supply chain risks.

V. The Open Compute Project Inflection Point (2015-2016)

March 10, 2015, at the Open Compute Project Summit in San Jose. Frank Frankovsky, OCP's chairman, took the stage to announce something unprecedented: Facebook was open-sourcing its network switch design. Not just the software—the actual hardware specifications, down to the circuit board layouts and mechanical drawings. Standing in the audience, Accton's executives knew this moment would transform their company forever.

The backstory was even more remarkable. The first attempt at an open networking switch by Facebook was designed together with Taiwanese ODM Accton using Broadcom Trident II chip and is called Wedge. Facebook's engineers had approached Accton months earlier with a radical proposition: help us design a switch that we'll give away to the world. For a company built on protecting intellectual property and manufacturing secrets, it was counterintuitive. But Accton's leadership saw what others missed—open hardware would create a larger market than proprietary systems ever could.

The Wedge switch was deliberately simple: a single Broadcom Trident II ASIC for high-speed forwarding. Wedge will be available through Accton and its OEMs and channel partners. No fancy management software, no proprietary protocols—just raw packet-moving power that could be controlled by whatever software the customer chose to run. Edge-Core's parent company, Accton Technology, performed the design validation for Facebook and manufactures Wedge for Facebook's deployment. Edge-Core's parent company, Accton Technology, performed the design validation for Facebook and manufactures Wedge for Facebook's deployment.

But it was the Wedge 100, announced in 2016, that truly demonstrated the power of the open model. The Wedge 100 switch is now available as a commercial product from Edgecore Networks and its channel partners worldwide. Edgecore's Wedge 100-32X is fully compliant with the Wedge 100 OCP specification and is manufactured by Edgecore's parent company, Accton Technology, which also manufactures the Wedge 100 for our network deployment. This wasn't just a reference design—it was production-ready hardware that through the Open Compute Project (OCP), Accton had the opportunity to develop Meta's Wedge 100 that equip their hyperscale 100G data centers.

The implications rippled through the industry. Suddenly, any company could buy the same switching hardware that Facebook used in its data centers. Software companies like Cumulus Networks and Big Switch Networks could offer network operating systems that ran on open hardware. They will be available from the Taiwanese network equipment maker Accton Technology and its channel partners. The proprietary lock-in that had defined enterprise networking for decades was crumbling.

Inside Accton's engineering labs, the pace of innovation accelerated. Working directly with Facebook's network engineers gave them unprecedented insight into hyperscale requirements. They learned that these customers didn't care about features that enterprise vendors considered essential—complex management interfaces, support for legacy protocols, elaborate high-availability schemes. What mattered was raw performance, power efficiency, and the ability to manage thousands of switches programmatically.

VI. Becoming Meta's Strategic Partner (2016-2022)

The relationship between Accton and Meta (as Facebook rebranded itself) evolved from vendor-customer to something approaching technological symbiosis. Accton has played a crucial role in designing and manufacturing the Minipack switches that are integral to Meta's F16 data center network topology. These modular switches, tailored for 100G and 400G applications, are deployed in various capacities, including as fabric, spine, and aggregator, to efficiently manage data traffic across Meta's extensive network infrastructure.

The Minipack represented a philosophical shift in switch design. Unlike traditional chassis switches with expensive backplanes and supervisory modules, Minipack used a modular approach with hot-swappable "Port Interface Modules" (PIMs). As a new uniform building block for all infrastructure tiers of fabric, we created a 128-port 100G fabric switch, called Minipack. Minipack is a flexible, single ASIC design that uses half the power and half the space of Backpack. An Accton engineer involved in the project described the design challenge: "Meta wanted a switch that could be everything—spine, leaf, aggregator—depending on which PIMs you installed. It had to be simple enough to manufacture at scale but flexible enough to evolve with their network."

The numbers told the story of scale. That year Accton began shipping 400G switches at scale. The transition from 100G to 400G switches was driven by the increasing demands of 5G, Wi-Fi 6, IoT, AI, and digital transformations in consumer electronics and enterprise sectors. This escalation in demand is particularly notable among major tech companies like Google, Microsoft, and Facebook.

The Minipack AS8000 Switch — which was developed by Edgecore Networks, the division of Accton Technology specializing in traditional and open network solutions — is based on Broadcom's StrataXGS Tomahawk III Switch Series, but the real innovation was in the manufacturing and thermal design. Running 400G optics generates enormous heat, and cooling them efficiently required rethinking everything from airflow patterns to power supply placement.

Beyond Meta, Accton was quietly winning other hyperscale customers. In 2019, Accton designed and manufactured switches for Amazon, AT&T and NTT Com. Each customer brought unique requirements, but the pattern was consistent: they wanted open hardware they could control with their own software, manufactured at scale with near-perfect quality.

The company also demonstrated its ability to adapt to diverse networking needs. Also in 2022, Accton developed Vodafone's disaggregated cell site gateway (DCSG) routers for their 5G network. These routers are critical to Vodafone's strategy to automate networks and diversify vendors, supporting the company's expansion of its 5G infrastructure as part of its open RAN initiatives. This wasn't data center switching—it was telecommunications infrastructure, proving Accton could apply its ODM model across different market segments.

VII. The AI Revolution and 800G Transformation (2021-Present)

The ChatGPT moment in November 2022 changed everything. Suddenly, every technology company needed massive AI training clusters, and those clusters needed networking infrastructure unlike anything built before. At Accton's headquarters in Hsinchu, emergency meetings were called. The company had been preparing for the 400G-to-800G transition, but the AI boom compressed their timeline from years to months.

Since 2021, Accton has been involved in developing and producing multiple generations of Intel's Habana Labs GOYA AI Inference Card, GAUDI AI Training Card. But it was in networking where Accton would make its biggest AI bet. Accton's Tomahawk-based Ethernet fabric has already achieved First Customer Shipment (FCS) in July. Accton's Tomahawk-based Ethernet fabric has already achieved First Customer Shipment (FCS) in July 2024, representing one of the industry's first production deployments of 800G switching.

The technical challenges were staggering. Accton's 51.2 Tbps Broadcom StrataXGS® Tomahawk® 5 Series-based System. 51.2Tbps Ethernet switching bandwidth. 2X increase in the switching throughput of prior generation switch platforms deployed. These switches weren't just faster—they required entirely new approaches to power delivery, cooling, and signal integrity. An 800G optical module consumes as much power as entire switches from just a generation ago.

With Accton's 6RU, dual-Ramon3, 128x800G (dual-51.2 Tbps) fabric port switch and 2RU, Jericho3-AI, 18x800G (14.4 Tbps leaf) Ethernet network interface port switch, customers can build a 32K-GPU 800G/400G AI/ML cluster with a two-stage DDC network architecture to enable 400G GPU clusters now and migrate to 800G GPU clusters later with a software upgrade without replacing the switches. This provides excellent cost saving and investment protection that reduces capital spending while providing the flexibility for customers to "pay as you grow" without large upfront cost to enable AI and ML applications.

The "pay-as-you-grow" model was revolutionary for AI infrastructure. Instead of building a massive cluster upfront, companies could start with 400G connections and upgrade to 800G through software and optics changes, protecting their switch investment. For startups and enterprises attempting to compete in AI, this flexibility was crucial.

October 2025 brought a stunning announcement: The Minipack3N, a 51.2 Tbps switch (designed by Meta and manufactured by Accton) based on the NVIDIA Spectrum-4 Ethernet switching ASIC. The addition of Minipack3N, based on NVIDIA's Ethernet Spectrum-4 ASIC, to our portfolio of 51 Tbps OCP switches. This marked a significant shift—Meta was now using NVIDIA silicon alongside traditional Broadcom chips, and Accton was manufacturing switches for both architectures.

Meta's next-generation AI infrastructure requires open and efficient networking at a scale the industry has never seen before," said Gaya Nagarajan, vice president of networking engineering at Meta. "By integrating NVIDIA Spectrum Ethernet into the Minipack3N switch and FBOSS, we can extend our open networking approach while unlocking the efficiency and predictability needed to train ever-larger models and bring generative AI applications to billions of people.

The numbers behind AI networking were mind-boggling. Training a large language model like GPT-4 requires thousands of GPUs working in concert, generating network traffic patterns unlike anything seen in traditional data centers. Every GPU might need to communicate with every other GPU, creating an "all-to-all" traffic pattern that would overwhelm traditional hierarchical networks. Accton's switches had to handle not just the volume but the specific patterns of AI workloads—massive "elephant flows" during training, synchronized bursts during gradient updates, and the critical requirement for consistent, predictable latency.

VIII. Financial Performance & Scale

The transformation from contract manufacturer to AI infrastructure enabler showed dramatically in Accton's financial results. In 2024, Accton Technology's revenue was 110.42 billion Taiwan dollars, an increase of 31.16% compared to the previous year's 84.19 billion. Earnings were 12.00 billion, an increase of 34.51%. The acceleration was remarkable—revenues that had grown steadily for decades suddenly hockey-sticked as AI demand exploded.

2345's earnings have grown significantly by 21.9% per year over the past 5 years. Accelerating Growth: 2345's earnings growth over the past year (63.1%) exceeds its 5-year average (21.9% per year). For a company of Accton's maturity—37 years old—this kind of acceleration was almost unprecedented. High ROE: 2345's Return on Equity (37.4%) is considered high, indicating exceptional efficiency in generating profits from shareholder equity.

The margin structure revealed the value of moving up the technology stack. While pure contract manufacturers typically operated on single-digit margins, Accton's gross margins had expanded to over 20%, reflecting their transition from simple assembly to complex engineering and design work. The company was no longer just building products to others' specifications—they were co-designing the future of data center infrastructure with the world's most advanced technology companies.

Analyst coverage of Accton remained surprisingly thin—Accton Technology Corporation is covered by 17 analysts. 6 of those analysts submitted the estimates of revenue or earnings used as inputs to our report. This relative obscurity in financial markets, despite the company's critical role in global technology infrastructure, reflected both the company's low profile and the complexity of understanding its business model. Sell-side analysts struggled to categorize Accton—was it a contract manufacturer like Foxconn, a networking company like Cisco, or something entirely different?

The capital allocation strategy was conservative but strategic. Rather than paying large dividends or buying back stock aggressively, Accton reinvested heavily in R&D and manufacturing capacity. Building a production line for 800G switches required tens of millions in specialized equipment—optical test gear that could verify signal integrity at unprecedented speeds, automated assembly systems precise enough to handle hair-thin optical fibers, and environmental testing chambers that could simulate the extreme conditions of hyperscale data centers.

The geographic revenue mix told a story of concentration and opportunity. The vast majority of revenue came from North American hyperscalers—Meta, Amazon, Microsoft, and Google. This concentration was both a strength (deep, strategic relationships with the world's most demanding customers) and a risk (vulnerability to any single customer's spending decisions). Yet as AI adoption spread globally and other regions built their own hyperscale infrastructure, Accton was well-positioned to capture that growth.

IX. Playbook: The ODM/OCP Strategy

Accton's strategic playbook, refined over decades, contained lessons that challenged conventional wisdom about technology businesses. The first principle: invisibility could be more valuable than brand recognition. By staying behind the scenes, Accton avoided channel conflict with customers who might otherwise view them as competitors. When Cisco considered outsourcing production, they could work with Accton without fear that Accton would use that knowledge to compete directly. When startups needed a manufacturing partner for their innovative designs, Accton's neutrality made them a safe choice.

The dual-track strategy of maintaining both Accton (pure ODM) and Edgecore (branded products) created optionality. Accton Technology has empower its own branded subsidiaries, SMC Networks and Edgecore the complete network solutions from home to SOHO, to SMBs and enterprises. When customers wanted to buy directly, Edgecore was there. When they needed an ODM partner, Accton could serve that need. The information flow between the two entities—carefully managed to respect confidentiality—gave Accton insights into both sides of the market.

The Open Compute Project became the catalyst that transformed Accton from one of many ODMs to the essential partner for open networking. 'Last year, Accton submitted the design of a 10GbE top-of-rack switch to OCP, which became the first network design fully approved by OCP,' said Frank Frankovsky, President and Chairman of Open Compute Project Foundation. By embracing open hardware when proprietary vendors resisted, Accton positioned itself at the center of a new ecosystem.

The virtuous cycle of open hardware was powerful: open designs attracted more users, which increased volumes, which reduced costs through scale, which attracted even more users. Unlike proprietary vendors who limited their addressable market to their own customers, Accton could sell to anyone building on open designs. Every Facebook Wedge switch deployment became a reference architecture that other companies could adopt, expanding Accton's market without additional sales effort.

Manufacturing excellence combined with engineering depth created a moat that pure contract manufacturers couldn't cross. Headquartered in the heart of Taiwan's Hsinchu Science-Based Industrial Park, Accton's teams of engineers work on location with partners and from Accton R&D centers around the globe. Anyone could set up an assembly line, but few could take a reference design from Broadcom or NVIDIA and optimize it for mass production while maintaining signal integrity at 800 gigabits per second. The expertise required spanned electrical engineering, mechanical design, thermal dynamics, optical physics, and manufacturing process control.

The rapid technology transitions in networking created opportunities for prepared companies. Rapid AI growth presenting new opportunities to balance slower growth in other sectors. When the industry shifted from 100G to 400G, customers needed a partner who could manage that transition. When AI suddenly demanded 800G and beyond, Accton was ready because they had been investing in the technology before the market demanded it. This forward-looking investment, funded by steady profits from current-generation products, created a sustainable competitive advantage.

X. Bear & Bull Cases

The Bear Case rests on several interconnected risks that could undermine Accton's remarkable trajectory. Customer concentration looms as the most immediate threat—a handful of hyperscalers drive the majority of revenue. If Meta decided to develop its own manufacturing capabilities, or if Amazon shifted to another partner, the impact would be severe. The precedent exists: Google designs its own TPUs and has brought some manufacturing in-house. What stops Meta or Microsoft from following suit?

Geopolitical tensions add another layer of risk. Accton's manufacturing base in Taiwan sits at the center of U.S.-China technological competition. Any disruption to Taiwan's stability—whether economic, political, or military—would cripple global technology supply chains, with Accton particularly exposed. The company's facilities in China and Vietnam provide some diversification, but the core engineering and advanced manufacturing remain in Taiwan.

Commoditization pressure never disappears in hardware. As open designs proliferate and more ODMs develop capabilities in high-speed networking, Accton's margins could compress. Chinese competitors like Ruijie Networks are investing heavily to move up the value chain. While they currently lack Accton's expertise in 800G systems, that gap won't last forever. The history of technology manufacturing suggests that today's advanced capability becomes tomorrow's commodity.

The in-house development threat is subtle but real. As hyperscalers gain experience with open hardware, they might decide to cut out the middleman. Amazon's Annapurna Labs already designs custom chips. Microsoft has its own silicon efforts. If these companies decided to extend their vertical integration to switch manufacturing, Accton would lose its most valuable customers. The counter-argument—that manufacturing is hard and distracts from core competencies—held true for servers and storage, but networking might be different given its strategic importance to AI infrastructure.

The Bull Case starts with the explosive growth in AI infrastructure demand. The hype of generative AI has drastically accelerated the size and network bandwidth required in AI/ML clusters with the number of compute nodes and accelerators growing significantly. AI networks require high-capacity systems in a flat architecture that can handle large amounts of data with low latency and high throughput. To meet the demands of AI/ML workloads, either Ethernet-based fabrics or VoQ-based fabrics are being adopted to reduce job completion time. We're in the first innings of AI infrastructure buildout—McKinsey estimates that data center capital expenditure will exceed $250 billion annually by 2030, with networking representing 10-15% of that spend.

The Total Addressable Market expansion goes beyond just hyperscalers. Sovereign AI initiatives mean countries are building their own AI infrastructure. Enterprises are deploying private AI clouds. Telecommunications companies need 5G infrastructure. Each market requires the high-performance, open networking solutions that Accton specializes in. The company's proven ability to serve diverse markets—from Meta's data centers to Vodafone's 5G network—demonstrates adaptability that pure cloud-focused competitors lack.

Deep engineering expertise and trusted relationships create barriers that new entrants can't easily overcome. The significant increase in radix and throughput offered by the 800G AI fabric together with the reduced power consumption delivers a performance that will push the boundaries of efficiency in AI clusters. Building a 51.2 Tbps switch that actually works reliably at scale requires years of accumulated knowledge. The trust required for a hyperscaler to hand over their strategic switch designs for manufacturing takes even longer to build. Accton has both.

The open networking ecosystem continues to grow stronger. Meta is proud to be among the initial group of OCP members driving ESUN, alongside industry leaders that includes: AMD, Arista, ARM, Broadcom, Cisco, HPE, Marvell, Meta, Microsoft, NVIDIA, OpenAI, and Oracle. As more companies commit to open standards, Accton's position as the leading ODM for open networking hardware becomes more valuable. They're not selling products into a mature market—they're enabling the transformation of how networks are built and operated.

XI. Grading & Lessons

Category Creation: A- Accton didn't invent open networking, but they were instrumental in making it real. When Facebook proposed the radical idea of open-sourcing hardware designs, Accton had the courage to embrace a model that seemed to threaten their intellectual property-based business model. They recognized that open hardware would create a larger market than proprietary systems ever could. The only reason this isn't an A+ is that they were responding to customer innovation rather than driving it themselves.

Execution: A The consistency of delivery to the world's most demanding customers speaks for itself. Meta trusts them with designs that could cripple their global infrastructure if manufactured incorrectly. Some remarkable progress has been achieved, including a significant reduction in manufacturing lead times and an increase in one-time repair pass rates, these resulted in customer satisfaction, more opportunities for long-term collaboration, and an increase in the global market share of ODM switches of up to 30%. The successful navigation of technology transitions—from 100G to 400G to 800G—while maintaining quality and scale is remarkable.

Capital Allocation: B+ Accton's strategic acquisitions were well-timed and sensibly priced. The R&D investments in next-generation technologies consistently paid off. The decision to maintain both manufacturing capacity and engineering depth, rather than outsourcing to chase short-term margins, proved prescient. The only criticism might be their conservative approach to returning capital to shareholders, though given the capital intensity of leading-edge manufacturing, this conservatism appears justified.

Timing: A+ Nearly every major strategic decision was perfectly timed. Embracing OCP just as hyperscalers were ready to adopt open hardware. Investing in 400G before the AI boom made it essential. Developing 800G capabilities just as the ChatGPT moment created unprecedented demand. This wasn't luck—it was the result of staying close to leading customers and investing ahead of the curve.

Key Lessons:

The most profound lesson from Accton's journey is that invisibility can be a sustainable competitive advantage. In an industry obsessed with brand building and customer ownership, Accton proved that being the neutral enabler—the "Switzerland" of networking—could be more valuable than competing for end-user mindshare.

Open standards, contrary to conventional wisdom, don't always commoditize industries. When combined with manufacturing complexity and rapid technological change, open standards can create massive markets that reward execution excellence over proprietary lock-in. Accton benefited from every new entrant to open networking because it expanded their addressable market.

The combination of manufacturing excellence and engineering depth creates a moat that's difficult to replicate. Pure contract manufacturers lack the engineering capability to optimize complex designs. Pure design houses lack the manufacturing expertise to produce at scale. Accton's position at the intersection—enhanced by decades of accumulated knowledge—proves surprisingly defensible.

Finally, the power of being embedded in technology transitions cannot be overstated. Accton didn't just manufacture products for the AI revolution—they were building the infrastructure before most people knew a revolution was coming. This forward positioning, funded by steady profits from current products and guided by insights from leading customers, created compound advantages that accelerated over time.

XII. Looking Forward

The next frontier for networking is already visible in Accton's labs. The industry roadmap points toward 1.6 terabit switches, with some hyperscalers already discussing 3.2 Tbps systems for the late 2020s. The physics becomes increasingly challenging—optical modules that can maintain signal integrity at these speeds, cooling systems that can dissipate kilowatts of heat from a single switch, and manufacturing processes precise enough to handle components measured in nanometers.

AI inference at the edge represents another opportunity. As AI models move from centralized training clusters to distributed inference at the edge, the networking requirements change dramatically. Latency becomes paramount, power efficiency critical, and the ability to operate in non-data center environments essential. Accton's experience with Vodafone's 5G infrastructure suggests they understand these requirements.

The convergence of networking and compute accelerates with each generation. Modern switches already contain powerful CPUs for control plane operations. Incorporates Broadcom Tomahawk 5 51.2 Tbps switch silicon • Intel Ice Lake-D LLC CPU. Future switches might incorporate AI accelerators for in-network computing, transforming them from pure packet movers to computational elements in distributed AI systems. Accton's relationships with both networking silicon vendors (Broadcom, NVIDIA) and compute vendors (Intel, AMD) position them to navigate this convergence.

The question of whether Accton will eventually compete directly with Broadcom or NVIDIA by designing their own silicon seems inevitable. As software eats the world and AI eats software, will switch ASICs become strategic enough that Accton needs to control that layer? The capital requirements would be enormous, the technical challenges daunting. Yet TSMC's success in manufacturing might provide a model—focus on being the best at one layer rather than trying to control the entire stack.

The broader lesson from Accton's journey extends beyond networking or even technology. In an era of increasing complexity and specialization, the companies that enable others' innovation—the platforms, the infrastructure providers, the "picks and shovels" suppliers—often capture more value than those seeking the spotlight. Accton built a $19 billion enterprise not by putting their name on products that consumers would recognize, but by being the indispensable partner to those who do.

As data becomes the new oil and AI becomes the new electricity, the networks that connect and power this transformation become critical infrastructure for the global economy. Accton, the hidden giant from Taiwan, stands ready to build the nervous system of our AI-powered future—quietly, reliably, and profitably enabling the next chapter of human technological progress.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube