NetApp: The Data Storage Underdog That Survived the Giants

Introduction & Episode Roadmap

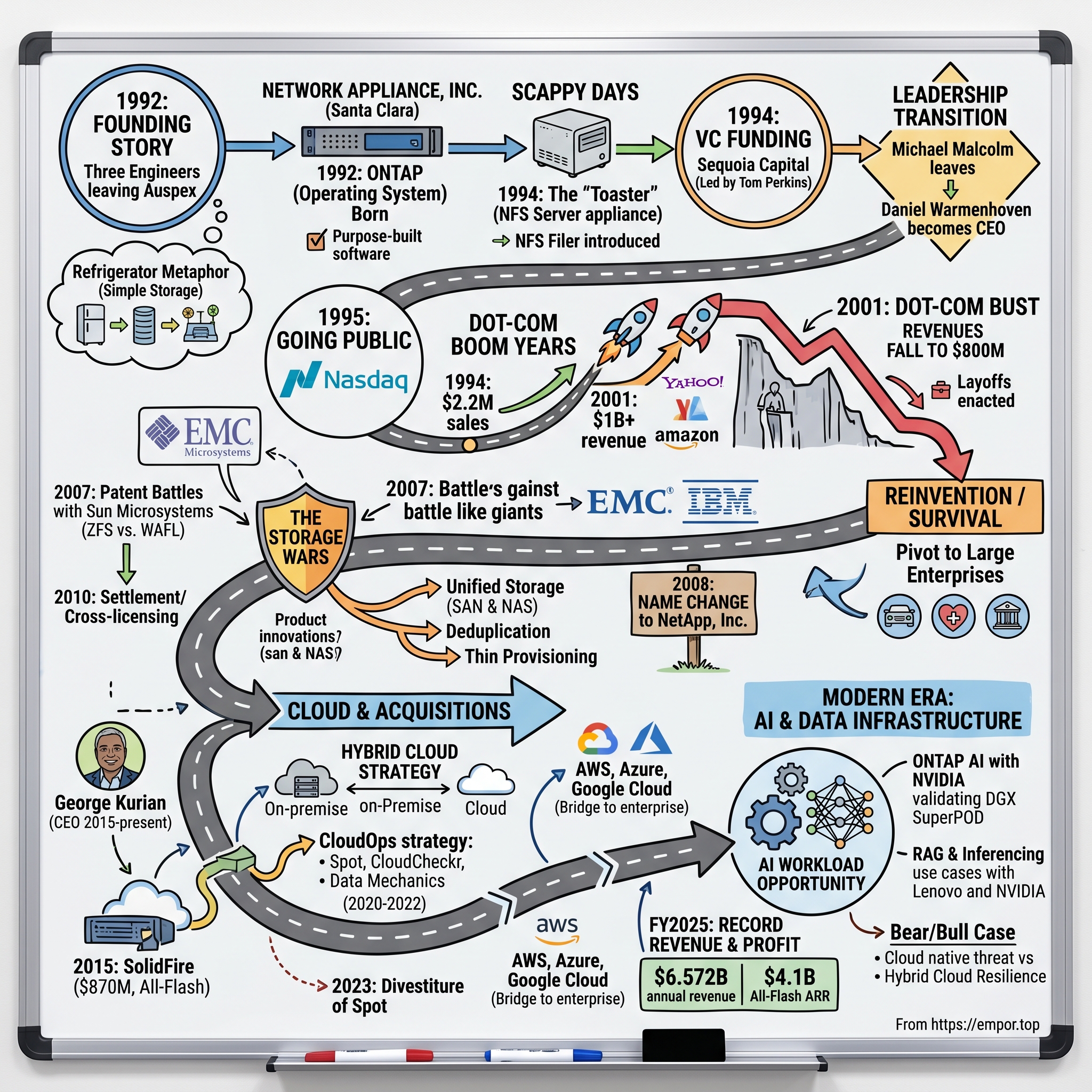

Picture this: It's 1992, and the data storage industry is dominated by giants—Sun Microsystems is printing money with its servers, EMC is building its empire, and IBM towers over everyone with decades of enterprise relationships. Into this arena walks a startup with a refrigerator metaphor and three engineers who think they can simplify an entire industry. That startup would become NetApp, today a $6.572 billion revenue powerhouse that somehow survived when dozens of its contemporaries vanished into the footnotes of tech history.

The central question isn't just how NetApp survived—it's how a company that started by making storage "boring" ended up at the forefront of every major data infrastructure transition for three decades. From network-attached storage to cloud computing to artificial intelligence workloads, NetApp has consistently reinvented itself while competitors either got acquired, went bankrupt, or became irrelevant.

This is a story about technical innovation meeting market timing, about surviving near-death experiences, and about the unglamorous but essential infrastructure that powers the digital economy. It's about building a business that Wall Street alternately loves and ignores, but that enterprises can't live without. Most importantly, it's about focus—the decision to be exceptional at one thing rather than mediocre at many.

We'll journey from those three engineers leaving Auspex Corporation with a radical simplification idea, through the dot-com boom that sent revenues soaring and the crash that nearly killed the company, into the storage wars with EMC and Sun, and finally to today's AI-driven data infrastructure renaissance. Along the way, we'll unpack the strategic decisions, the near-misses, and the operational excellence that allowed NetApp to outlast competitors with deeper pockets and bigger headlines.

The Founding Story: Three Engineers and a Refrigerator

The conference room at Auspex Corporation in 1991 was tense. David Hitz, a software engineer with a philosophy degree from Princeton, was growing frustrated. Auspex made high-performance file servers—complex, expensive machines that required teams of specialists to operate. Every customer deployment felt like a small war, with endless customization and configuration battles. Sitting across from him was James Lau, a hardware engineer who shared Hitz's growing conviction: there had to be a better way.

"What if storage was just... simple?" Hitz would later recall thinking. Not simple as in cheap or low-quality, but simple as in focused, purposeful, elegant. The metaphor that stuck was a refrigerator. You don't need a PhD to operate a refrigerator. You open the door, take something out, close the door. It keeps things cold. That's it. Why couldn't enterprise storage work the same way? By early 1992, Hitz, Lau, and a third engineer named Michael Malcolm decided to leave Auspex and found Network Appliance, Inc. The timing seemed insane—Sun Microsystems was worth billions, EMC was growing rapidly, and the storage industry was consolidating around a few massive players. But the trio saw opportunity in simplification. They believed in building dedicated storage appliances rather than general-purpose computing systems that were too complex, drawing inspiration from how Cisco had simplified networking.

The early days were scrappy. The team raised $12.8 million in venture capital and private funding to get started. Working out of a small office in Santa Clara, they literally took apart the storage components of computer servers and rebuilt them as dedicated, non-programmable devices. Hitz and Lau—self-described hippies—built their first NFS server affectionately known as the "Toaster", a name that perfectly captured their philosophy: this wasn't a supercomputer, it was an appliance.

What made their approach revolutionary wasn't just the hardware—it was the software philosophy. Along with the hardware, ONTAP, NetApp's proprietary operating system, was born in 1992. This wasn't just another Unix variant; it was purpose-built for storage management, incorporating ideas that would later become industry standards like snapshots and data deduplication.

The personal backgrounds of the founders added color to the startup story. Before his career in the computer industry, Hitz had worked as a cowboy, where he got valuable management experience by herding, branding, and castrating cattle—experience he would later immortalize in his business book with the memorable title "How to Castrate a Bull." This wasn't your typical Silicon Valley founding team. In 1994, NetApp received venture capital funding from Sequoia Capital, marking a crucial validation from one of Silicon Valley's most prestigious investors. Network Appliance brought the product to market in 1994, aided by nearly $13 million in venture funding that was led by Sequoia Capital. The timing was significant—Sequoia had recently backed Cisco, Yahoo, and would soon invest in Google. Their bet on NetApp represented a conviction that storage could be as transformational as networking.

That same year, NetApp introduced its first-generation Network Attached Storage (NAS) appliance, the "filer." The first ever functional product introduced to the market was the filer in the year 1994. This wasn't just another storage product—it was a philosophical statement. While competitors built complex, general-purpose systems loaded with features, NetApp's filer did one thing exceptionally well: it stored and served files over a network.

The simplicity was radical. Initially, NetApp marketed its filers to Unix-based technical workgroups writing client-server programming software for the Network File System. These early customers—engineers and developers who valued simplicity and reliability over bells and whistles—would become NetApp's most passionate evangelists.

But the early days weren't without drama. Malcolm was NetApp's first president and CEO but was forced out in 1994 by investors preparing to take the company public. Daniel Warmenhoven replaced Malcolm and led NetApp to its initial public offering of stock in November 1995. This leadership transition, while painful, would prove pivotal. Warmenhoven brought the operational discipline needed to transform a startup with a clever product into a company that could compete with established giants.

In fiscal 1994, the company registered $2.2 million in sales, but posted a loss of $1.8 million. The numbers were modest, the losses concerning, but the vision remained clear: storage didn't need to be complicated. As they prepared for their public debut, the refrigerator metaphor had evolved into something more tangible—a business model that would soon capture Wall Street's imagination.

Going Public and the Dot-Com Rocket Ship

The morning of November 21, 1995, was crisp in Santa Clara. Inside NetApp's modest offices, employees gathered around computer screens watching Nasdaq tick toward opening bell. Years of sixteen-hour days, engineering debates, and customer evangelism had led to this moment. When the market opened, NetApp became a public company via an initial public offering, opening on Nasdaq at $13.50 per share.

The stock sale raised nearly $26 million, "just in the nick of time, because we were out of money," Hitz wrote in his memoir. This wasn't hyperbole—the company had been operating on fumes, stretching every dollar while racing to fulfill orders. The IPO wasn't just a financial milestone; it was survival.

What followed was one of the most spectacular growth stories of the internet era. NetApp thrived in the internet bubble years of the mid-1990s to 2001, during which the company grew to $1 billion in annual revenue. Think about that trajectory: from $2.2 million in 1994 to $1 billion by 2001—a 450-fold increase in seven years.

The secret sauce was perfect market timing meeting perfect product-market fit. NetApp shifted gears to ride the internet wave, selling storage products to high-tech and internet-based companies. Every dot-com startup needed storage for their websites, databases, and user data. Every telecommunications company building internet infrastructure needed reliable, scalable storage. And unlike traditional storage vendors who required armies of consultants for deployment, NetApp's appliances could be installed and running in hours, not weeks.

Revenues grew from roughly $250 million to more than $1 billion between 1999 and 2001. About 70% of NetApp sales came from internet-based firms during that time. The company became the storage vendor of choice for Yahoo, Amazon, and hundreds of other internet pioneers. Their filers weren't just storing data; they were storing the internet itself.

The competition with Auspex Systems—NetApp's former employer turned rival—intensified during this period. At the time, its major competitor was Auspex Systems. Auspex had the head start, the enterprise relationships, and the engineering pedigree. But NetApp had simplicity and momentum. While Auspex built increasingly complex systems for demanding enterprise customers, NetApp kept iterating on its core philosophy: make storage simple, reliable, and fast.

The stock market loved the story. The price for NetApp stock soared to $150 per share at its high point—an 11-fold increase from its IPO price. Employees who had joined for modest salaries and stock options were suddenly millionaires. The parking lot filled with Porsches and Teslas (the Roadster had just launched). Silicon Valley was awash in optimism, and NetApp was riding the wave.

But beneath the euphoria, the company was also building something more durable: ONTAP, their operating system, was evolving rapidly. ONTAP, NetApp's proprietary operating system, is born. NetApp IPOs in 1995, quickly growing to $1B+ in revenue. Each release added features that would become industry standards—snapshots for instant backups, replication for disaster recovery, deduplication for storage efficiency. While competitors focused on raw performance or capacity, NetApp was building an intelligent storage platform.

The customer wins during this period read like a who's who of the new economy. Internet service providers, web hosting companies, streaming media pioneers—they all needed NetApp's combination of simplicity and scale. The company's mantra became "Fast, Simple, Reliable," and unlike many corporate slogans, this one actually meant something to customers drowning in complexity.

By 2001, NetApp had transformed from a startup with a clever idea into a legitimate force in enterprise storage. They had survived the transition from founder-CEO to professional management, scaled from millions to billions in revenue, and built a product portfolio that extended far beyond the original filer concept. But storm clouds were gathering. The Nasdaq had peaked in March 2000, and by 2001, the dot-com boom was becoming the dot-com bust. NetApp's rocket ship ride was about to hit severe turbulence.

The Crash and Near-Death Experience

The autumn of 2001 felt like a different universe from just eighteen months earlier. In NetApp's Sunnyvale headquarters, the energy had shifted from exuberant growth to survival mode. Customer after customer—the dot-coms that had fueled their meteoric rise—were shutting down. Orders weren't just slowing; they were evaporating. After the bubble burst, NetApp's revenues quickly declined to $800 million in its fiscal year 2002, a 20% drop from their billion-dollar peak.

By 2001, NetApp revenues fell to $800 million, and share prices dropped to approximately $6, forcing NetApp to enact its first round of layoffs. From $150 to $6—a 96% decline in stock price. Employees watched their paper millions vanish. The parking lot Porsches disappeared, replaced by nervous conversations about whether the company would survive.

CEO Dan Warmenhoven faced the crisis of his career. The company that had grown by riding the internet wave now had to fundamentally reinvent itself or die. His response was swift and sometimes brutal. Costs were slashed, entire departments eliminated, and the company's focus shifted dramatically. Following the collapse, NetApp began focusing on large enterprise customers across vertical markets, including automotive, energy, government, healthcare, manufacturing, banking and financial services.

This pivot to enterprise wasn't just a market shift—it required rethinking everything. Internet startups bought storage like they bought servers: quickly, with minimal customization, often with credit cards. Enterprise customers demanded proof-of-concepts, integration with existing systems, service-level agreements, and armies of support personnel. NetApp had to grow up fast.

The technical evolution was equally dramatic. In 2002, in an attempt to increase market share, NetApp added block storage access as well. Today, NetApp systems support it via FC protocol, the iSCSI protocol, and the emerging Fibre Channel over Ethernet (FCoE) protocol. This was heretical to storage purists. NetApp had built its reputation on NAS (Network Attached Storage), positioning itself against the complexity of SAN (Storage Area Networks). Now they were embracing both. The message to the market: we'll meet you where you are.

Internally, the company culture transformed. The freewheeling startup that celebrated simplicity above all else had to learn enterprise discipline. Sales cycles stretched from weeks to quarters. Support became a 24/7 operation. The company that had once mocked the complexity of competitors now offered professional services, complex configurations, and enterprise-grade redundancy.

But something remarkable happened: NetApp survived. More than survived—they started growing again. Since then, the company's revenue has steadily climbed. By 2003, revenues were recovering. By 2004, they exceeded pre-crash levels. The company that many had written off as a dot-com casualty was proving it had staying power.

The survival tactics weren't just about cutting costs and chasing enterprise deals. NetApp doubled down on R&D during the downturn, betting that innovation would differentiate them when the market recovered. They developed technologies like FlexVol (flexible volumes), SnapVault (backup and recovery), and continued enhancing ONTAP. While competitors retreated, NetApp invested in the future.

By 2002, a discernible shift in the source of the company's business had occurred, with 60 percent of annual sales coming from customers in financial services, the federal government, telecommunications, energy, and manufacturing. Looking ahead from 2002, prognostications were sanguine, an attitude projected by Warmenhoven.

The leadership lessons from this period became Silicon Valley legend. Warmenhoven's ability to navigate from boom to bust to recovery became a Harvard Business School case study. His key insight: in a crisis, you can't shrink your way to greatness. You have to cut what doesn't matter and invest in what does. For NetApp, that meant maintaining R&D investment while cutting everything else to the bone.

The near-death experience of 2001-2002 fundamentally changed NetApp's DNA. The company that emerged was tougher, more focused, and ironically, more complex than the simple appliance company founded a decade earlier. But it had learned something crucial: survival in enterprise technology requires more than good products. It requires the ability to reinvent yourself when markets shift. This lesson would prove invaluable as the storage wars were about to begin in earnest.

The Storage Wars: EMC, Sun, and Patent Battles

By 2005, the enterprise storage industry had become a battlefield, and NetApp found itself in the crosshairs of giants. EMC, the undisputed king of storage with its Symmetrix arrays, viewed NetApp's growing enterprise presence as a direct threat. Sun Microsystems, riding high on its server business, was pushing into storage. IBM loomed over everyone with decades of enterprise relationships. The gentleman's competition of the 1990s had evolved into all-out war.

The most dramatic confrontation erupted in September 2007. In September 2007, NetApp started proceedings against Sun Microsystems, claiming that the ZFS File System developed by Sun infringed its patents. This wasn't just another patent dispute—it was a battle for the future of storage architecture. Sun's ZFS represented a fundamental challenge to NetApp's WAFL (Write Anywhere File Layout) technology, the crown jewel of their ONTAP operating system. The following month, Sun announced plans to countersue.

The lawsuit sent shockwaves through the industry. Here was NetApp, David to Sun's Goliath, asserting its intellectual property against one of Silicon Valley's most iconic companies. The technical community was divided—many developers loved ZFS's open-source promise, while others recognized NetApp's legitimate innovations in storage technology. The legal battle would drag on for years, ultimately settling in 2010 with a complex cross-licensing agreement.

But the patent wars were just one front in a multi-dimensional competitive battle. EMC, under Joe Tucci's leadership, was executing a brilliant strategy of acquisition and integration. They bought VMware, Data Domain, and Isilon, assembling a storage empire that dwarfed NetApp. Every quarter, industry analysts would compare market share numbers, with EMC consistently maintaining its dominant position while NetApp fought for second or third place.

According to a 2014 IDC report, NetApp ranked second in the network storage industry "Big 5's list", behind EMC (Dell), and ahead of IBM, HP and Hitachi. This #2 position became both a source of pride and frustration. NetApp had proven it could compete with the giants, but breaking EMC's stranglehold seemed impossible.

The competitive dynamics shaped NetApp's product strategy in profound ways. Unable to match EMC's acquisition war chest or Sun's engineering resources, NetApp chose focus over breadth. They refined ONTAP obsessively, adding features like unified storage (supporting both SAN and NAS from the same system), deduplication, and thin provisioning. NetApp creates the first unified SAN and NAS appliances–simplifying life for our customers (and our marketing team). NetApp releases thin provisioning and NetApp® FlexClone® technology, enabling our customers to compound storage efficiencies. NetApp creates the first unified deduplication for primary and secondary storage.

The company also made strategic divestments. In 2006, NetApp sold the NetCache product line to Blue Coat Systems, recognizing that web caching was becoming commoditized and distracting from their core storage focus. This discipline—knowing what not to do—became a hallmark of NetApp's strategy during the storage wars.

Perhaps the most symbolic change came in 2008. In 2008, Network Appliance officially changed its legal name to NetApp, Inc., reflecting the nickname by which it was already well-known. For years customers affectionately referred to us as NetApp. In 2008 we decided to make it official. The formal name change represented more than branding—it was an acknowledgment that the company had evolved far beyond its simple appliance roots.

Throughout this period, NetApp's approach to competition remained distinctive. While EMC acquired companies to eliminate competitors and gain technology, NetApp preferred organic development and selective partnerships. While Sun and IBM leveraged their broader portfolios to bundle storage with servers and software, NetApp remained focused on storage excellence. This focus-versus-breadth debate would define enterprise technology strategy for the next decade.

The storage wars taught NetApp crucial lessons about resilience and differentiation. They couldn't outspend EMC, out-engineer Sun, or out-relationship IBM. But they could be more agile, more focused, and more innovative in their specific domain. As the 2000s drew to a close, with virtualization reshaping data centers and cloud computing on the horizon, these lessons would prove invaluable. The next battle wouldn't be fought with patents and acquisitions—it would be fought in the cloud.

The Cloud Transition and Acquisitions Strategy

June 1, 2015, marked a watershed moment in NetApp's history. Tom Georgens stepped down as CEO and was replaced by George Kurian. Kurian, who had been with the company since 2011, inherited a profitable but struggling enterprise—revenues had stagnated, the stock price was stuck, and most critically, NetApp was dangerously behind in the cloud revolution that was reshaping enterprise IT.Kurian's background was telling—he was the twin brother of Thomas Kurian, who would later become CEO of Google Cloud. Both had worked at Oracle, both understood enterprise software, and both saw that the future of infrastructure was hybrid. He is the twin brother of Google Cloud CEO, Thomas Kurian. George's diverse background included roles at Akamai Technologies, McKinsey & Company, and leading teams at Oracle and Cisco. He wasn't just a storage executive; he was a technologist who understood the broader shifts happening in enterprise IT.

His first major move was radical: acknowledge reality. NetApp had been fighting the cloud, positioning itself as the on-premises alternative. Kurian flipped the narrative—NetApp would become the bridge between on-premises and cloud, the company that helped enterprises navigate hybrid reality rather than forcing them to choose sides. Under his leadership, NetApp has successfully navigated the shift towards cloud data services, significantly enhancing its portfolio and market position. The acquisition strategy under Kurian marked a sharp departure from NetApp's traditionally organic growth approach. In December 2015 (closing in January 2016), NetApp acquired founded in 2009 flash storage vendor SolidFire for $870 million. This wasn't just buying technology—it was buying credibility in the all-flash market where NetApp had been dangerously behind.

"This acquisition will benefit current and future customers looking to gain the benefits of webscale cloud providers for their own data centres," said NetApp CEO George Kurian. The SolidFire deal was strategic on multiple levels. SolidFire specializes in scale-out all-flash arrays for web-scale data centers, the kinds of data centers operated by cloud infrastructure providers or other massive internet services. NetApp wasn't just catching up to the flash revolution; they were positioning themselves for the cloud-native world.

The integration wasn't without challenges. It's probably harsh but fair to say that SolidFire's all-flash hardware and Elements OS software technology has not been a great success at NetApp, having been eclipsed by the ONTAP mothership and its AFF array hardware/software combination. But the acquisition served its purpose—it gave NetApp immediate credibility in all-flash and bought them time to develop their own offerings. The acquisition pace accelerated dramatically between 2020 and 2022. NetApp's strategic acquisitions, including Spot, CloudCheckr, Data Mechanics, Fylamynt and now Instaclustr represented a comprehensive CloudOps strategy. These weren't random purchases—they were building blocks for a hybrid cloud platform. The acquisition of CloudCheckr complements and expands the Spot by NetApp portfolio to create an industry leading suite of CloudOps services.

But not all acquisitions worked out as planned. Last week, Flexera announced intent to acquire Spot by NetApp to the tune of $100 million, a considerable drop from the $450 million that NetApp paid to acquire Spot. The promised convergence of CloudCheckr and Spot from 2021 never materialized. NetApp's journey into cloud cost management never really fit with the storage and data infrastructure focus of the company, nor did it achieve the synergy needed to maintain its acquisitions.

This divestiture, while painful financially, represented strategic clarity. As NetApp refocuses on its core strengths, a quick divestment from Spot and CloudCheckr to a more aligned FinOps owner in Flexera makes a lot of sense. The company was acknowledging what it did well—storage and data infrastructure—and what it didn't—FinOps and cloud cost management.

Meanwhile, the partnerships with hyperscalers were bearing fruit. NetApp had successfully positioned itself as the enterprise storage layer for AWS, Azure, and Google Cloud. Rather than competing with the cloud providers, NetApp became their bridge to enterprise customers who wanted cloud flexibility without abandoning their existing infrastructure investments.

The all-flash transformation was perhaps the most dramatic technical pivot. From being late to the party with the SolidFire acquisition, NetApp transformed into a leader in all-flash arrays. The company that had once mocked complexity now offered sophisticated all-flash solutions across multiple market segments—from traditional enterprise to web-scale infrastructure.

Modern Era: AI, Data Infrastructure, and Market Position

May 2018 marked a technical milestone that few outside the storage industry noticed but that would prove prophetic. In May 2018, NetApp announced its first end-to-end NVMe array called All Flash FAS A800 with the release of ONTAP 9.4 software. This wasn't just another product launch—it was NetApp positioning itself for the AI revolution that was still three years away from mainstream consciousness.

The timing seemed prescient in retrospect. While the world was focused on cloud migrations and digital transformation, NetApp was quietly building the infrastructure that would be essential for AI workloads. NVMe (Non-Volatile Memory Express) offered the ultra-low latency and massive throughput that machine learning models demanded. NetApp claims over 1.3 million IOPS at 500 microseconds per high-availability pair—numbers that seemed excessive in 2018 but would prove essential by 2024.

January 2019 brought the end of an era. In January 2019, Dave Hitz announced his retirement from NetApp. The last founder was leaving, twenty-seven years after that initial refrigerator metaphor. His departure symbolized NetApp's complete transformation from startup to enterprise stalwart. The company that three engineers had founded with $12.8 million was now generating over $6 billion in annual revenue. The current financial performance tells a remarkable turnaround story. Fiscal Year 2025 marked many revenue and profitability records, driven by significant market share gains in all-flash storage and accelerating growth in first party and marketplace storage services. NetApp annual revenue for 2025 was $6.572B, a 4.85% increase from 2024. All-flash array ARR: $4.1 billion, compared to $3.6 billion in the fourth quarter of fiscal year 2024; a year-over-year increase of 14%.

These numbers matter because they represent NetApp's successful navigation of yet another technology transition. The company that nearly died when the dot-com bubble burst, that fought patent wars with Sun, that was late to flash storage—that same company is now posting record profits in the AI era. "During the year, we refreshed our entire systems portfolio, sharpened the focus of our cloud services, and positioned ourselves to lead in the enterprise AI market," said George Kurian, Chief Executive Officer

The competitive landscape in 2024 looks radically different from the storage wars of the 2000s. Pure Storage, founded in 2009, has emerged as NetApp's most direct competitor in the all-flash market, with a market cap that sometimes exceeds NetApp's despite having less than half the revenue. Dell Technologies, after absorbing EMC in 2016's $67 billion mega-merger, remains the market share leader but struggles with debt and integration challenges. HPE, having acquired Nimble Storage and SimpliVity, competes across the hybrid cloud spectrum.

But the real competition now comes from an unexpected quarter: the cloud providers themselves. AWS, Azure, and Google Cloud offer native storage services that bypass traditional storage vendors entirely. This existential threat has forced NetApp to evolve from hardware vendor to software and services provider. The company's response has been to embed itself deeper into these cloud platforms rather than fight them—offering NetApp Cloud Volumes as fully managed services within the hyperscalers' marketplaces.

The AI opportunity represents NetApp's most significant growth vector since the dot-com boom. As enterprises rush to build AI capabilities, they're discovering that data infrastructure is the bottleneck. Training large language models requires moving massive datasets at unprecedented speeds. Inference workloads demand consistent low latency. NetApp's ONTAP AI, validated with NVIDIA's DGX systems, positions them as the storage layer for enterprise AI ambitions. NetApp has begun the NVIDIA certification process of NetApp ONTAP storage on the AFF A90 platform with NVIDIA DGX SuperPOD AI infrastructure, positioning itself to handle the largest enterprise AI deployments. The company's partnerships extend beyond hardware validation to complete solution stacks. NetApp and Lenovo are collaborating on converged infrastructure solutions designed for retrieval-augmented generation (RAG) and inferencing use cases for GenAI, with Lenovo high-performance ThinkSystem servers utilizing NVIDIA L40S GPUs and NetApp AFF storage.

The strategic positioning goes deeper than partnerships. "The rise of AI is ushering in a new disrupt-or-die era," says Gabie Boko, Chief Marketing Officer at NetApp. This isn't hyperbole—it's recognition that data infrastructure has become the constraining factor in AI adoption. Maximizing GPU usage is critical for cost-effective AI operations, because underused resources can result in increased expenses, and NetApp's ability to feed data fast enough to keep expensive GPUs utilized becomes a competitive differentiator.

Playbook: Strategic & Technical Lessons

The NetApp story offers a masterclass in technology company survival and evolution. Unlike many of its contemporaries who either died or got acquired, NetApp navigated multiple technology transitions while maintaining independence. The lessons from their journey read like a survival guide for enterprise technology companies.

The Power of Focus: Single-Purpose Appliances vs. General Computing

NetApp's founding insight—that storage should be simple like a refrigerator—seems obvious in retrospect but was revolutionary in 1992. While competitors built increasingly complex general-purpose systems, NetApp stayed focused on doing one thing exceptionally well. This focus allowed them to move faster, iterate more quickly, and build deeper expertise than competitors spreading resources across multiple domains.

The refrigerator metaphor wasn't just marketing; it was architectural philosophy. By constraining the problem space, NetApp could optimize every aspect of their systems for storage performance. This focus extended to their go-to-market strategy—they didn't try to be everything to everyone but instead targeted specific use cases where their simplicity provided maximum value.

Even during growth periods, NetApp resisted the temptation to diversify too broadly. The 2006 sale of NetCache to Blue Coat Systems demonstrated this discipline—recognizing that web caching was becoming commoditized and moving away from their core competency. This ability to say no, to define what they wouldn't do, proved as important as their technical innovations.

Surviving Technology Transitions: From NAS to SAN to Cloud

NetApp's history is punctuated by moments where they had to cannibalize their own business to survive. The 2002 decision to add block storage (SAN) support was heretical for a company that had built its reputation on the simplicity of file storage (NAS). But recognizing that enterprise customers needed both, they chose evolution over ideological purity.

The cloud transition under George Kurian represents perhaps the most dramatic pivot. Rather than positioning against the cloud (a losing battle), NetApp repositioned as the bridge between on-premises and cloud infrastructure. This wasn't just marketing repositioning—it required fundamental changes to their technology stack, business model, and partnerships.

Each transition followed a pattern: initial resistance, recognition of market reality, rapid pivot, and eventual leadership in the new paradigm. The company that was late to flash storage with the SolidFire acquisition became a leader in all-flash arrays. The company that initially fought the cloud became embedded in all three major cloud providers.

Building an Enterprise Sales Machine

The dot-com crash forced NetApp to transform from selling to credit-card-wielding startups to complex enterprise sales cycles. This wasn't just hiring more salespeople—it required building an entirely different organizational capability. Enterprise customers demanded proof-of-concepts, complex integrations, service-level agreements, and 24/7 support.

NetApp learned that enterprise sales is about relationships, not just products. They invested in professional services, built deep technical expertise in vertical industries, and created reference architectures for specific use cases. The company that once mocked the complexity of enterprise vendors had to embrace that same complexity to survive.

The sales transformation also meant geographic expansion. While Silicon Valley startups could be served from Sunnyvale, enterprise customers required local presence, local support, and local relationships. NetApp built a global sales and support infrastructure that could compete with IBM and HP for multinational contracts.

The Importance of Software (ONTAP) as a Competitive Moat

ONTAP, born alongside the company in 1992, evolved from a simple storage operating system into NetApp's primary competitive advantage. While hardware could be commoditized and copied, ONTAP's features—snapshots, deduplication, replication, FlexVol—created switching costs and customer lock-in.

The strategic importance of ONTAP became clear during the patent battle with Sun over ZFS. NetApp wasn't just protecting lines of code; they were protecting decades of innovation embedded in their software stack. ONTAP became the unifying element across all NetApp products, from entry-level systems to high-end arrays to cloud services.

The decision to port ONTAP to the cloud rather than building cloud-native alternatives proved prescient. Customers wanted consistency across their hybrid infrastructure, and ONTAP provided that bridge. The software that started as firmware for a simple appliance became the foundation for a multi-billion-dollar business.

Capital Allocation: Why NetApp Never Made Mega-Acquisitions

While EMC spent $67 billion to merge with Dell and acquired VMware for $635 million, NetApp's largest acquisition was SolidFire for $870 million. This wasn't due to lack of opportunity or capital—it was strategic choice. NetApp preferred organic development and selective technology acquisitions over transformative mega-deals.

This discipline in capital allocation allowed NetApp to maintain focus and avoid integration challenges that plagued competitors. The recent divestiture of Spot to Flexera for $100 million (a $350 million loss) demonstrated willingness to admit mistakes rather than throwing good money after bad. NetApp recognized that FinOps and cloud cost management didn't align with their core storage focus.

The company's approach to returning capital to shareholders through dividends and buybacks rather than empire-building acquisitions appealed to a certain type of investor. While this meant slower growth than acquisition-hungry competitors, it also meant more predictable returns and less integration risk.

Managing Through Cycles: Dot-com, 2008, COVID, and Beyond

NetApp has survived multiple economic cycles, each teaching different lessons. The dot-com crash taught the importance of customer diversification. The 2008 financial crisis reinforced the need for operational flexibility. COVID accelerated digital transformation, benefiting NetApp's cloud transition.

The key to cycle management was maintaining R&D investment during downturns. While competitors cut research budgets to preserve margins, NetApp continued developing new technologies. Features developed during the dot-com bust became competitive advantages during the recovery. This counter-cyclical investment strategy required courage and long-term thinking.

Financial discipline during good times created cushions for bad times. NetApp never leveraged up during boom periods, maintaining a strong balance sheet that provided flexibility during downturns. This conservative financial management might have limited growth during expansions but ensured survival during contractions.

Bear vs. Bull Case Analysis

Bear Case: The Structural Challenges

The bear case for NetApp starts with the fundamental question: does independent storage hardware have a future? The hyperscalers—AWS, Azure, and Google Cloud—offer native storage services that are increasingly sophisticated and price-competitive. Why would enterprises buy NetApp arrays when cloud storage is elastic, requires no capital expenditure, and comes with built-in redundancy?

The commoditization risk extends beyond cloud providers. Open-source alternatives like Ceph and MinIO offer "good enough" storage for many use cases. The hardware itself—SSDs, NVMe drives, networking equipment—is largely commoditized. What NetApp sells is essentially software and services wrapped around commodity hardware, and that wrapper is getting thinner.

Growth metrics paint a concerning picture. While NetApp celebrates 4.85% revenue growth, Pure Storage and other modern storage companies are growing much faster. NetApp's customer base, while loyal, is aging. The company that rode the dot-com wave is now serving enterprises that themselves face disruption from cloud-native competitors.

Market maturity presents another challenge. The enterprise storage market isn't growing significantly—it's reshuffling. Every NetApp win comes at the expense of Dell, HPE, or another traditional vendor. Without market expansion, growth becomes a zero-sum game, and NetApp lacks the scale of Dell or the diversification of HPE.

Technical debt from decades of ONTAP development creates complexity that cloud-native alternatives avoid. While ONTAP's features create lock-in for existing customers, they also create barriers for new adopters. Young companies starting today are more likely to choose cloud-native storage than learn ONTAP's intricacies.

The AI opportunity, while real, might not materialize as expected for NetApp. The largest AI workloads run in hyperscaler data centers using proprietary infrastructure. While enterprises will adopt AI, their storage needs might be met by existing infrastructure or cloud services rather than new NetApp purchases.

Bull Case: The Resilience and Opportunity

The bull case begins with NetApp's remarkable financial performance. Fiscal Year 2025 marked revenue and profitability records, driven by significant market share gains in all-flash storage. The company generating $6.572 billion in revenue with healthy margins isn't a dying business—it's a profitable, growing enterprise.

The hybrid cloud reality favors NetApp's positioning. Despite cloud evangelism, most enterprises run hybrid infrastructure and will for decades. Data gravity, regulatory requirements, and economic reality mean on-premises infrastructure isn't disappearing. NetApp's ability to span on-premises and cloud uniquely positions them for this hybrid future.

The AI infrastructure opportunity is massive and immediate. 40% of global technology executives believe that unprecedented investment in AI and data management will be required for their companies in 2025. NetApp's partnerships with NVIDIA, validated architectures, and enterprise relationships position them to capture significant share of this investment.

Operational excellence sets NetApp apart from competitors. The company consistently generates strong cash flow, maintains healthy margins, and returns capital to shareholders. This isn't a growth-at-all-costs story—it's a profitable technology company with a sustainable business model.

The installed base provides a powerful moat. Thousands of enterprises run mission-critical workloads on NetApp infrastructure. These customers face significant switching costs—not just financial but operational. Migrating petabytes of data, retraining staff, and rearchitecting applications creates inertia that benefits NetApp.

Trust matters in enterprise infrastructure, and NetApp has earned it over three decades. When companies bet their business on storage infrastructure, they choose vendors with proven reliability, support, and longevity. NetApp's survival through multiple technology transitions demonstrates staying power that startups can't match.

Power Analysis & Moats

Switching Costs: The ONTAP Ecosystem Lock-in

The most powerful moat in NetApp's arsenal is the switching cost embedded in ONTAP deployments. Once an enterprise builds its storage infrastructure on ONTAP, extraction becomes exponentially complex. This isn't just about moving data—it's about rewriting automation scripts, retraining administrators, rebuilding disaster recovery processes, and rearchitecting applications that depend on ONTAP-specific features.

Consider snapshots, a feature NetApp pioneered. Enterprises might take thousands of snapshots daily for backup, development, and compliance. These snapshots integrate with backup software, orchestration platforms, and business processes. Replacing NetApp means rebuilding all these integrations—a multi-year project with significant risk and no clear business benefit.

The lock-in extends to skills and knowledge. Thousands of IT professionals have built careers on ONTAP expertise. These administrators understand its quirks, optimize its performance, and trust its reliability. Switching to another platform means retraining entire teams or hiring new staff—costs that don't appear in TCO calculations but dramatically impact switching decisions.

Network Effects: Partner Ecosystem and Integrations

NetApp has cultivated an extensive ecosystem of partners, integrators, and ISVs (Independent Software Vendors) that amplifies its value. Backup vendors like Veeam and Commvault deeply integrate with ONTAP. Virtualization platforms from VMware and Citrix are optimized for NetApp storage. This ecosystem creates network effects—the more partners integrate with NetApp, the more valuable NetApp becomes to customers.

The cloud provider relationships represent a modern form of network effect. Being the primary enterprise storage option for AWS, Azure, and Google Cloud means customers can maintain consistency across hybrid deployments. As more enterprises adopt multi-cloud strategies, NetApp's presence across all major clouds becomes increasingly valuable.

Channel partners and system integrators have built practices around NetApp technologies. These partners don't just resell products—they provide implementation services, ongoing support, and industry-specific solutions. This channel creates distribution leverage and customer intimacy that would take competitors years to replicate.

Scale Economies: R&D Leverage and Manufacturing

With over $6 billion in revenue, NetApp can spread R&D costs across a large customer base. Developing features like deduplication or NVMe support requires massive investment that smaller competitors can't match. This R&D scale allows NetApp to maintain technical parity or leadership while generating healthy margins.

Manufacturing scale provides cost advantages in component procurement and production efficiency. NetApp's volume allows negotiation leverage with suppliers and justifies investments in automation and quality control. These scale advantages compound—lower costs enable competitive pricing, which drives volume, which further reduces costs.

The support infrastructure represents another scale economy. NetApp's global support organization, 24/7 operations, and deep technical expertise require massive fixed investment. Spreading these costs across thousands of customers makes enterprise-grade support economically viable.

Brand: Enterprise Trust and Reliability Reputation

Three decades of enterprise deployments have built a brand that resonates with IT decision-makers. When careers depend on infrastructure reliability, brand matters. NetApp's reputation for reliability, built through millions of hours of uptime across thousands of customers, can't be manufactured through marketing—it must be earned through consistent execution.

The brand extends beyond reliability to innovation leadership. NetApp's pioneering work in snapshots, deduplication, and unified storage established them as thought leaders. This innovation reputation attracts top engineering talent and early adopter customers, creating a virtuous cycle of innovation and market validation.

Enterprise customers value vendor stability. NetApp's survival through multiple economic cycles and technology transitions demonstrates longevity that startups can't claim. When enterprises make ten-year infrastructure commitments, they choose vendors likely to exist in ten years.

Counter-positioning: Hybrid Cloud vs. Pure Cloud Players

NetApp has successfully positioned itself in the gap between pure cloud providers and traditional on-premises vendors. While AWS and Azure push cloud-only futures, and Dell and HPE defend on-premises infrastructure, NetApp embraces hybrid reality. This positioning resonates with enterprises navigating complex transitions.

The counter-positioning extends to operational model. While cloud providers push OpEx consumption models and traditional vendors push CapEx purchases, NetApp offers both. This flexibility appeals to CFOs managing budgets and CIOs managing technology transitions.

Against pure-play storage startups, NetApp counter-positions with enterprise maturity. While startups offer modern architectures and aggressive pricing, NetApp provides proven reliability, global support, and integration breadth. This trade-off—innovation versus stability—often favors NetApp in risk-averse enterprises.

Epilogue: What's Next for NetApp?

The AI infrastructure opportunity represents the most significant growth catalyst since the dot-com boom, but capturing it requires careful execution. The market is moving fast—every major technology company claims AI leadership, and customers struggle to separate reality from hype. NetApp must demonstrate concrete value: faster model training, improved GPU utilization, simplified data pipeline management. The partnerships with NVIDIA and positioning for RAG workloads are promising starts, but execution will determine whether NetApp captures this opportunity or watches it pass by.

Industry consolidation seems inevitable. The storage industry has too many vendors chasing too few customers. NetApp could be acquirer or acquired—their $14 billion market cap makes them digestible for larger players while their cash generation enables selective acquisitions. The recent Spot divestiture suggests discipline in portfolio management, but larger moves might be necessary. Watch for NetApp to acquire AI-specific technologies or consider merging with complementary infrastructure providers.

The future of data management in a multi-cloud world remains uncertain. Will enterprises centralize on single cloud providers, embrace true multi-cloud architectures, or retreat to on-premises infrastructure? NetApp is betting on hybrid complexity persisting, but this bet requires constant adaptation. The company must balance supporting legacy ONTAP deployments while developing cloud-native services, serving traditional enterprises while attracting modern workloads. Key metrics to watch going forward crystallize around several critical indicators. NetApp is forecast to grow earnings and revenue by 5.9% and 4.6% per annum respectively. EPS is expected to grow by 7.1% per annum. All-flash ARR growth remains the most important near-term metric—the 14% year-over-year increase to $4.1 billion demonstrates momentum, but sustaining double-digit growth will prove challenging as the base expands. Cloud segment revenue, currently at $665 million annually, needs to accelerate beyond the current 9% growth rate to validate the hybrid cloud strategy.

The AI infrastructure adoption rate will serve as a leading indicator. Watch for mentions of GPU-attached storage deployments, NVIDIA certification completions, and enterprise AI customer wins in earnings calls. If NetApp can demonstrate measurable improvements in GPU utilization rates and model training times, they'll validate their AI positioning beyond marketing rhetoric.

Operational efficiency metrics deserve attention. Return on equity is forecast to be 104.8% in 3 years. This exceptional ROE reflects both strong profitability and aggressive capital management, but also highlights the company's mature market position where growth investments generate diminishing returns.

Stock performance reflects this complexity. The 16 analysts that cover NetApp stock have a consensus rating of "Buy" and an average price target of $122.27, which forecasts a 16.51% increase in the stock price over the next year. Yet beneath this consensus lies significant divergence—The lowest target is $100 and the highest is $160. This 60% spread between bull and bear cases reflects fundamental uncertainty about NetApp's future.

Final reflections on NetApp's journey reveal a company that has defied Silicon Valley's creative destruction repeatedly. From the dot-com crash to the cloud revolution, NetApp has survived transitions that killed dozens of storage competitors. They've evolved from simple appliance maker to enterprise infrastructure provider to hybrid cloud enabler, each transformation requiring fundamental reinvention.

The lessons for founders are profound. Technical excellence alone doesn't ensure survival—NetApp succeeded through operational discipline, strategic focus, and willingness to cannibalize existing businesses for future opportunities. They demonstrate that B2B infrastructure companies can build lasting value without consumer glamour or viral growth. Sometimes, being boring and profitable beats being exciting and unprofitable.

NetApp's story isn't finished. At thirty-two years old, the company faces its next existential challenge: remaining relevant as AI reshapes enterprise computing. The refrigerator metaphor that launched the company has evolved into intelligent data infrastructure managing exabytes of information. Whether NetApp thrives for another three decades or becomes another footnote in technology history depends on their ability to navigate yet another fundamental transition.

The data storage underdog that survived the giants has become a giant itself—not through acquisition or financial engineering, but through consistent execution and constant reinvention. In an industry that worships disruption, NetApp's durability stands as testament to a different path: evolution over revolution, focus over diversification, and profitability over growth at any cost. For investors, customers, and competitors alike, NetApp remains what it has always been—easy to underestimate, hard to kill, and essential to the infrastructure that powers our digital world.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube