Travel Food Services: How a Family Business Conquered India's Airport Food Empire

I. Introduction & The Airport Food Revolution

Picture this: You're rushing through Mumbai's Terminal 2 at 6 AM, desperate for coffee before your Delhi flight. The aroma of fresh dosas mingles with espresso as you pass a Starbucks, a local South Indian outlet, and a gleaming lounge entrance. Behind every one of these establishments—and dozens more across India's airports—stands a single company that most travelers have never heard of: Travel Food Services.

With a market capitalization hovering around ₹15,000 crores and control over 26% of India's airport quick-service restaurants and an astounding 45% of airport lounges, TFS has quietly built what might be the most dominant position in Indian travel hospitality. The company operates 442 QSRs and 37 lounges across 14 airports, serving millions of captive customers who have few alternatives once they've crossed security.

The central question isn't just how a Mumbai catering family built this empire—it's how they've maintained and expanded it through multiple economic cycles, regulatory changes, and the complete transformation of Indian aviation. This is a story of patient capital meeting perfect timing, of global partnerships enhancing local execution, and of understanding that airports aren't just transit points—they're captive marketplaces where convenience commands premium pricing.

Why do airports matter so much? Consider the economics: passengers spend 2-3 hours on average in terminals, they can't leave to find alternatives, and they're often expense-account or vacation-mode spenders. Add India's aviation boom—passenger traffic growing at 15% annually, new airports sprouting across tier-2 cities, and a middle class increasingly comfortable with air travel—and you have the perfect storm for a focused operator.

What unfolds is not just a business story but a masterclass in navigating India's complex regulatory environment, building trust with government entities, and recognizing when bringing in the right partner can unlock exponential growth. From JK Kapur's first restaurant in 1972 to the company's 2025 IPO at ₹1,100 per share, this journey spans three generations and reveals how sometimes the best businesses are hiding in plain sight—or in this case, behind the security checkpoint.

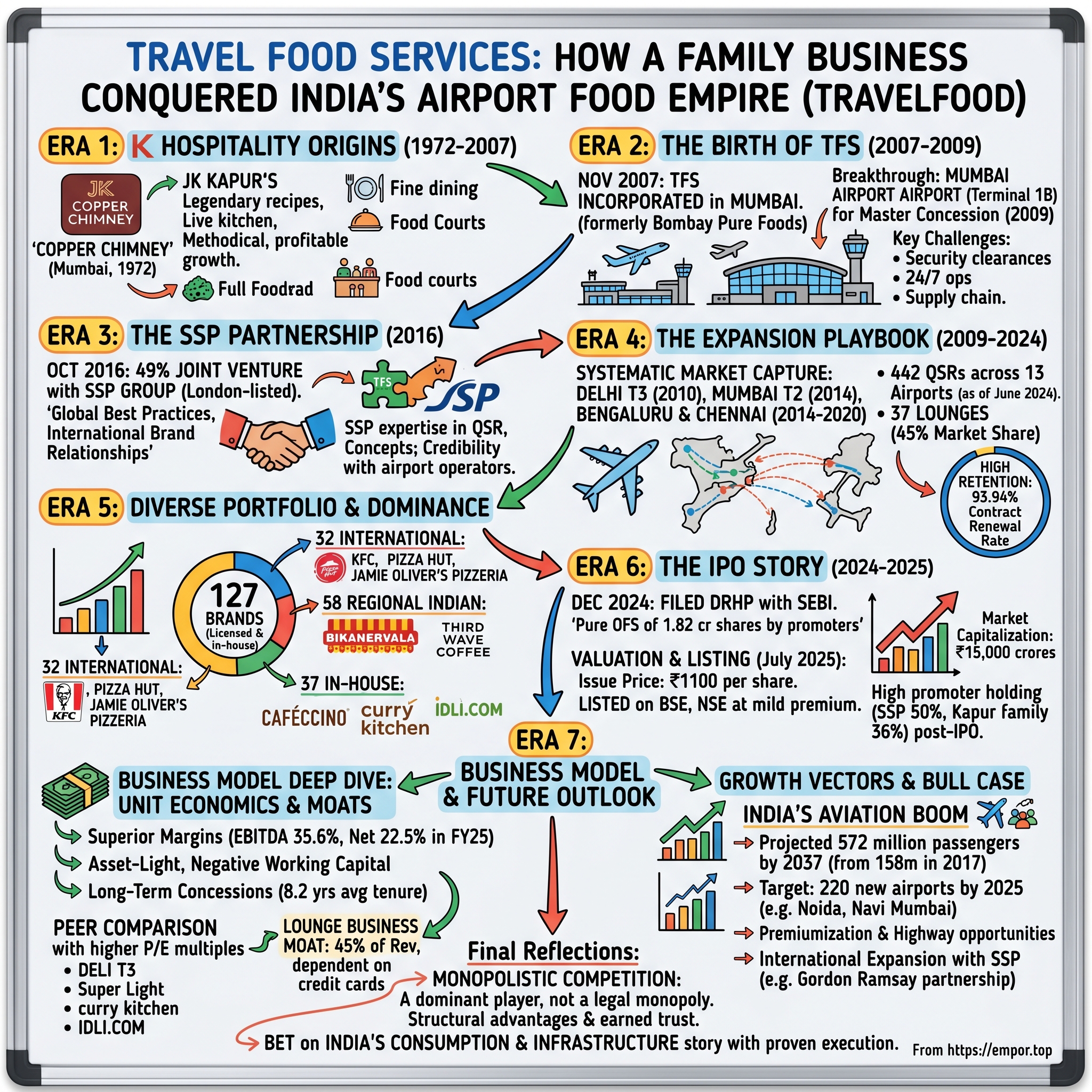

II. The Kapur Legacy & K Hospitality Origins (1972-2007)

In 1972, Mumbai was still finding its feet as India's commercial capital, just two decades after independence. The city's restaurant scene was dominated by Irani cafes and traditional eateries when JK Kapur, a partition refugee who had arrived in Bombay with little more than determination and family recipes, decided to transform how Indians experienced dining. JK Kapur had migrated as a refugee during partition, and had launched the now legendary Copper Chimney in Mumbai in 1972, using his home-made recipes that he had been perfecting over the years.

The founding of Copper Chimney in Worli wasn't just another restaurant opening—it was a revolution in Indian hospitality. JK Kapur opened India's first live open-kitchen Indian restaurant – Copper Chimney in Mumbai's Worli area. This transparency in cooking, now commonplace, was radical for its time. Customers could watch their food being prepared, building trust through visibility—a principle that would later become central to TFS's airport operations.

The business that was founded by JK Kapur, Sunil Kapur's father, with limited resources but unlimited ambition. What Kapur lacked in capital, he compensated with an intimate understanding of Indian palates and an obsession with consistency. Every dish that left the kitchen carried not just flavors but stories—recipes refined over years, many salvaged from pre-partition memories.

The growth trajectory from 1972 to 2007 reads like a masterclass in organic expansion. Over the past 5 decades, K Hospitality has launched more than 500 stores/restaurants, forayed into 6 business verticals, has a domestic footprint in 19 cities as well as presence in international markets like Middle East, UK, South East Asia and Africa. But this wasn't rapid, venture-funded scaling—it was methodical, profitable growth built on operational excellence.

By the early 2000s, K Hospitality had evolved far beyond a single restaurant. K Hospitality Corp is India's largest privately held F&B company, with 500+ outlets and 10000+ employees across multiple business verticals in the Food and Beverage sector in India and overseas. The company had mastered multiple formats: fine dining with Copper Chimney and Bombay Brasserie, banqueting through Blue Sea Catering, and food court operations in emerging malls.

In the 2000s, with the evolution of shopping malls, K Hospitality entered the food court space with multiple brands. Its vertical Global Kitchens operates as the exclusive F&B partner for large-scale real estate assets, like malls, to set up and manage F&B offerings across local, national, and global brands. This mall expansion proved crucial—it taught K Hospitality how to manage multiple brands simultaneously, negotiate with large landlords, and operate in high-rent environments with captive audiences. Sound familiar? These were exactly the skills needed for airport dominance.

The banqueting business, often overlooked by analysts, was particularly strategic. Running large-scale catering for weddings and corporate events required managing complex logistics, maintaining quality at scale, and dealing with demanding clients—all capabilities that would translate directly to airport operations. Its operations are spread across bars, QSRs, cafes, food courts, banqueting, corporate food services, outdoor catering, and travel F&B outlets, among others.

By 2007, when the Kapur family decided to enter the airport space, they weren't newcomers trying to figure out food service. They were battle-tested operators with 35 years of experience, thousands of employees, and deep relationships across India's F&B ecosystem. The foundation was set for what would become Travel Food Services—but first, they needed to crack the code of India's notoriously complex airport bureaucracy.

III. Birth of Travel Food Services (2007-2009)

In November 2007, amid the brewing global financial crisis and a year before Lehman Brothers' collapse, the Kapur family quietly incorporated Travel Food Services Limited in Mumbai - an Indian airport travel quick service restaurant ("Travel QSR") and lounge operator that would revolutionize India's travel hospitality.

The company began life with an unglamorous name—"Bombay Pure Foods Private Limited"—before being renamed Travel Food Services in March 2009. But behind this bureaucratic nomenclature was audacious ambition. Founded by one of India's leading hospitality giants, K Hospitality Corp in 2009, TFS is backed by K Hospitality Corp's 47-year-old expertise across the F&B industry.

The timing seemed counterintuitive. India's aviation sector in 2007-2009 was experiencing turbulence—Kingfisher Airlines was bleeding cash, Air Deccan had been absorbed, fuel prices were volatile. But the Kapurs saw what others missed: airports were being privatized, passenger volumes would inevitably grow with India's economic expansion, and the existing F&B offerings at Indian airports were, frankly, terrible.

I know, because I was there on the night the company was launched, way back on 12 May 2009 in Mumbai. The occasion coincided with the TFWA Asia Pacific show in Singapore but having been informed that TFS was no more a fledgling market entrant but a player of huge ambition and integrity underpinned by years of heritage in the food services sector, I honoured a promise to attend and address the audience. At the time TFS had just signed a memorandum of understanding with Mumbai International Airport Ltd for a master concession covering F&B space across domestic terminals and some international sites.

That Mumbai airport deal in 2009 was the breakthrough. Starting F&B operations at Mumbai airport terminal 1B, TFS didn't just win a contract—they secured a beachhead in India's busiest airport. Since the opening of its first Travel QSR outlet in 2009, it has built capabilities and processes to effectively execute in, and address the distinct challenges posed by the operationally complex and highly secure airport environment, such as security clearances, stringent rules and restrictions, 24/7 operations, multi-brand and multiunit concessions, alongside various supply chain and infrastructure constraints.

The airport concession model itself is fascinating—and massively misunderstood by outsiders. TFS operates under long-term concession agreements (5–20 years) with airports, offering stability and visibility. Unlike traditional retail leases, these agreements typically involve revenue-sharing arrangements where the operator pays the higher of a minimum guarantee or a percentage of sales. The economics are brutal at first—high upfront investments, complex logistics, stringent security requirements—but once established, the barriers to entry become your moat.

Consider the operational complexity: every employee needs security clearance, every delivery must be screened, ingredients must be stored in limited spaces, kitchens operate 24/7 across multiple outlets simultaneously, and you're dealing with customers from every corner of India and the world. Traditional restaurant operators would run screaming. The Kapurs saw opportunity.

Early challenges were numerous. Regulatory hurdles included navigating the Airports Authority of India's (AAI) byzantine tender processes, understanding each airport operator's unique requirements, and building credibility in an industry historically dominated by government-run canteens and small local operators. Capital requirements were substantial—fitting out airport spaces to international standards isn't cheap. Operational complexity meant recruiting and training staff who could handle everything from a rushed businessman wanting espresso to a family seeking familiar Indian comfort food.

But K Hospitality's decades of experience proved invaluable. They understood Indian tastes intimately, had relationships with equipment suppliers, knew how to manage multi-brand operations from their mall food courts, and critically, had the financial strength to absorb early losses while building scale.

Building credibility with AAI and private airport operators required more than just operational competence. It demanded a track record of compliance, financial stability, and the ability to enhance the airport's overall passenger experience. TFS positioned itself not as another F&B vendor but as a partner in modernizing India's airport infrastructure. They understood that airports increasingly view commercial revenues—including F&B—as critical to their business model, often contributing 40-50% of total airport revenues.

By 2009, when TFS officially launched, they weren't starting from scratch. They had the Mumbai airport contract, a clear vision of becoming India's dominant travel F&B operator, and most importantly, the patient capital and operational expertise to execute a long-term strategy. The foundation was set, but to truly scale, they would need a partner who understood the global travel retail game—enter SSP.

IV. The SSP Partnership: Going Global (2016)

October 2016: Seven years after launching TFS, the Kapur family partnered with SSP Group in a joint venture where SSP would own 49% stake in Travel Food Services Private Limited (TFS), the fast-rising Indian travel markets F&B operator. The announcement sent ripples through the global travel retail industry.

SSP wasn't just any partner. SSP is an operator of food and beverage outlets in travel locations. The company, headquartered in London, England, is listed on the London Stock Exchange and is a constituent of the FTSE 250 Index. With operations across 35+ countries and decades of experience running airport F&B globally, SSP brought exactly what TFS needed to scale from Indian champion to global player.

SSP CEO Kate Swann said: "This partnership is in line with the strategy we set out at our IPO. We have been looking for the right entry point into this exciting growth market and are delighted to have found an excellent partner in TFS. For SSP, India represented the ultimate growth market—a billion-plus population, rapidly expanding middle class, and aviation infrastructure still in its infancy. They had been searching for the right entry vehicle for years.

The financial structure of the deal was sophisticated. SSP Group plc (LSE:SSPG) agreed to acquire 49% stake in Travel Food Services Pvt Ltd. from Kapur Family Trust, SNVK Properties Private Limited and KAPCO Caterers for £61.4 million on October 20, 2016. The expected net consideration of £57.9 million is contingent on the performance of the business and is subject to a cap of an additional £3.5 million payment. The transaction was structured in phases—first phase with 33% stake (which includes the issuance of new shares of Travel Food Services, 8.82% stake) for £39 million by the end of February 2017 and second phase with the acquisition of additional 16% stake for approximately £18.9 million by the end of 2018.

K Hospitality Group and Travel Food Services Chairman Sunil Kapur: "SSP's international experience and proven track record, coupled with our knowledge and position in the region, means that we have a winning partnership to create a strong proposition for growth." K Hospitality Group Chairman Sunil Kapur said: "We are delighted to be partnering with SSP. SSP's international experience and proven track record, coupled with our knowledge and position in the region, means that we have a winning partnership to create a strong proposition for growth."

The strategic rationale went beyond capital. SSP brought global brand relationships—suddenly TFS could negotiate with international franchisors as part of a global network rather than as a standalone Indian operator. They brought operational best practices honed across hundreds of airports worldwide. Most importantly, they brought credibility with airport operators who increasingly preferred dealing with established global players.

TFS' revenue was £41.7 million (US$51.2 million) and EBITDA was £8.3 million (US$10.2 million) for the year ended 31 March 2016. In the year ending 31 March 2017, TFS will benefit from the first time inclusion of the recent buyout of certain joint venture partners, the full contribution of new units opened in 2016 and ongoing like for like sales growth. Taken together, these items are expected to add approximately £3.0 million to EBITDA in the year ending 31 March 2017.

The cultural integration could have been a disaster—British corporate governance meeting Indian entrepreneurship, global standardization meeting local market knowledge. Instead, it became a case study in successful joint ventures. The Kapurs retained operational control and deep involvement in day-to-day operations while SSP provided strategic guidance, global relationships, and capital market credibility.

"Since 2016, we have benefited from SSP's global Travel QSR expertise and best practices, alongside long-standing relationships with an extensive range of international brands and bespoke concepts. We look forward to growing our close partnership with SSP as we embark on this significant milestone for our joint venture." This wasn't corporate speak—the partnership genuinely transformed TFS's capabilities.

Building a successful Indian platform through the joint venture meant more than just combining resources. It required aligning incentives, respecting each partner's strengths, and creating governance structures that balanced control with autonomy. SSP understood that their role was to enhance, not replace, the local expertise that had made TFS successful.

The partnership unlocked international brand partnerships that would have been impossible for TFS alone. Global franchisors who wouldn't return calls to a standalone Indian operator suddenly saw TFS as part of SSP's global network. Operational best practices from SSP's operations in mature markets like the UK and US could be adapted for India. Technology systems, supply chain optimization, staff training programs—all upgraded to global standards while maintaining local relevance.

SSP acquired an initial stake in TFS in 2016, paying £57.9 million (US$73.9 million) for its 49% holding. It recently acquired a further 1.01% of TFS's share capital in advance of the listing. This additional stake acquisition ahead of the IPO would prove crucial for maintaining control post-listing.

The marriage of British corporate governance with Indian entrepreneurship created something unique in the travel retail space—a company with the operational excellence and relationships of a global player but the market intimacy and agility of a local champion. As TFS embarked on its next phase of expansion, this dual DNA would prove to be its greatest competitive advantage.

V. The Expansion Playbook: Airports, Brands & Lounges (2009-2024)

From 2009 to 2024, TFS systematically conquered India's airport F&B landscape. As of June 30, 2024, Travel Food Services were present in the Delhi airport for 14 years, the Mumbai airport for 15 years, the Bengaluru airport for 5 years and the Chennai airport for 11 years. It has been present in Delhi Terminal 3 and Mumbai Terminal 2 since their inaugurations in 2010 and 2014, respectively. Additionally, it also claims to have been the sole F&B concessionaire and lounge operator in Chennai and Kolkata airports operated by the Airports Authority of India (AAI) since 2014.

The numbers tell only part of the story. As of March 31, 2025, it had a total of 442 Travel QSRs, comprising 384 outlets across 13 airports in India, 29 outlets across two airports in Malaysia and 29 outlets across nine highway sites in India, operated directly through the Company and Subsidiaries and indirectly through its Associates and Joint Ventures. TFSL operated 270 Travel QSR outlets directly while the remaining 172 outlets were operated by its Associates and Joint Ventures, as of March 31, 2025. As of the said date, its F&B brand portfolio comprised 127 brands, of which 32 were international brands, 58 were regional Indian brands and 37 were in-house brands. The revenue is having contribution from Partner brands to the tune of 54+% and In-house brands contribution up to 45+%. As of March 31, 2025, it had operating units on 18 airports in three countries with 442 QSR outlets and 37 operating lounges.

The brand portfolio reads like a United Nations of food. Offers food and beverage services through a diverse mix of 127 brands: 32 International Brands (KFC, Pizza Hut, Jamie Oliver's Pizzeria, Krispy Kreme), 58 Regional Indian Brands (Hatti Kaapi, Bikanervala, Third Wave Coffee) and 37 In-House Brands (Caféccino, idli.com, Dilli Streat, Curry Kitchen). Travel Food Services Limited operates a diverse portfolio of partner F&B brands, including international names like KFC, Pizza Hut, and Krispy Kreme, regional Indian brands such as Bikanervala, and in-house brands like Caféccino. With 78 licensed partner brands and 39 in-house brands, this extensive range enables Travel Food Services Limited to cater to both local and international palates.

This wasn't random brand accumulation—it was strategic portfolio construction. International brands like KFC and Pizza Hut provided instant recognition and trust for foreign travelers. Regional Indian brands like Bikanervala and Wow Momo satisfied domestic passengers seeking familiar flavors. In-house brands allowed TFS to fill gaps, control margins, and rapidly adapt to local preferences without franchise restrictions.

The lounge business emerged as the crown jewel. TFSL's Lounge business comprises designated areas within airport terminals, accessible primarily by first and business class passengers, members of airline loyalty programmes, select credit card and debit card holders and members of other loyalty programmes. It had 37 Lounges across India, Malaysia and Hong Kong as of March 31, 2025. What started as an experiment became a 45% market share dominance story.

The lounge model is financially brilliant. Credit card companies pay for access as a customer acquisition tool. Airlines use lounges to differentiate premium offerings. Passengers pay directly for comfort. TFS collects from all three revenue streams while operating a single facility. The economics are so attractive that lounges generate disproportionate profits despite representing a smaller footprint than QSRs.

Long-term relationships became TFS's moat. Being the sole operator in Chennai and Kolkata airports since 2014 wasn't just about winning contracts—it was about becoming so embedded in airport operations that replacement became unthinkable. High Retention: 93.94% contract renewal rate. This retention rate is staggering in an industry where contracts go to tender every 7-10 years.

Technology innovations weren't afterthoughts but strategic differentiators. They've introduced self-ordering kiosks, online ordering, in-airport delivery, and contactless payment systems to streamline service times. Their "Food@Gate" service allows travellers to order food via kiosks or mobile and have it delivered to the boarding gate. In the constrained airport environment where every minute matters, these services command premium pricing.

The international expansion into Malaysia and Hong Kong proved the model's portability. These weren't vanity projects but calculated moves to establish TFS's credibility as a regional player, essential for winning contracts with global airport operators who preferred dealing with companies operating across multiple geographies.

The numbers from this period are remarkable. From a standing start in 2009 to 442 QSRs and 37 lounges by 2025. From one airport to presence in 14 of India's 15 largest airports, serving 74% of total air passenger traffic. From zero to 26% market share in QSRs and 45% in lounges. This wasn't growth—it was systematic market capture.

Local adaptation proved crucial. Additionally, the company claims to adapt menus and pricing to local demographics, offering regional product innovations, such as live sweet counters in Kolkata and local-style dosas in Bengaluru. A Mumbai airport outlet might emphasize vada pav while Bengaluru focused on filter coffee. This wasn't just menu tweaking—it was deep cultural understanding translated into commercial success.

The concession model itself evolved into an art form. TFS learned to structure bids that balanced aggressive growth with sustainable economics. They understood that winning wasn't about the highest bid but about demonstrating operational excellence, financial stability, and long-term commitment. Their ~94% retention rate proved they delivered on promises.

By 2024, TFS had transformed from an ambitious startup to India's undisputed airport F&B champion. But to unlock the next level of value—and provide liquidity to early investors—they needed to access public markets. The stage was set for one of 2025's most watched IPOs.

VI. The IPO Story: Timing, Structure & Execution (2024-2025)

December 2024. The timing seemed perfect. India's aviation sector was booming, new airports were being planned, and investors were hungry for quality infrastructure plays. Travel Food Services filed its draft red herring prospectus with SEBI, officially launching what would become one of 2025's most closely watched IPOs.

Travel Food Services IPO is a book build issue of ₹2,000.00 crores. The issue is entirely an offer for sale of 1.82 crore shares of ₹2,000.00 crore. This structure was crucial—no new money was being raised for the company. Travel Food Services IPO is a bookbuilding issue and is entirely an offer for sale (OFS) of 1.82 crore shares by its promoter, the Kapur Family Trust. Since the issue is completely an OFS, the Company will not get any IPO proceeds.

The pure OFS structure sent a message: TFS didn't need capital for growth—it generated plenty internally. This was about providing liquidity to the Kapur Family Trust, which had built immense value over decades but had that value locked in an illiquid private company. It was also about establishing a public market valuation for SSP's stake and providing currency for future acquisitions.

Travel Food Services IPO bidding started from Jul 7, 2025 and ended on Jul 9, 2025. The allotment for Travel Food Services IPO was finalized on Jul 10, 2025. The shares got listed on BSE, NSE on Jul 14, 2025. The three-day window saw intense activity, though perhaps not the frenzy some had expected.

Travel Food Services IPO price band is set at ₹1100.00 per share The pricing at the upper end of the ₹1,045-1,100 band reflected confidence, though some questioned whether the valuation fully reflected the company's growth potential versus execution risks.

SSP Group plc, SSP Group Holdings Limited, SSP Financing Limited, SSP Asia Pacific Holdings Limited and Kapur Family Trust, and Varun Kapur and Karan Kapur are the company promoters. Post-IPO, the promoter group would retain approximately 85-86% of the company—SSP at 50.01% and the Kapur family at around 36%. This high promoter holding was both a strength (alignment of interests) and a concern (limited float).

The investor backing read like a who's who of global institutional money. Travel Food Services IPO raises ₹598.80 crore from anchor investors. Travel Food Services IPO Anchor bid date is July 4, 2025. While specific names aren't disclosed in the search results, the anchor book reportedly included ADIA, ICICI Prudential, Fidelity, Norges Bank, and Kotak—smart money that understood both the India growth story and the airport concession business.

The IPO received moderate response with subscription of 3.03 times - QIB segment leading at 8.10 times, NII at 1.67 times, whilst retail participation remained subdued at 0.73 times and employee participation at 1.81 times. The subscription pattern was telling—institutions loved it, retail was skeptical. The QIB oversubscription of 8.10 times showed that sophisticated investors understood the business model. Retail's lukewarm 0.73 times subscription reflected concerns about valuation and the pure OFS nature.

Why go public now? Several factors converged. India's aviation boom was accelerating—passenger traffic growing at 15% annually, new airports in Noida and Navi Mumbai under construction, tier-2 cities upgrading infrastructure. The company had achieved sufficient scale to justify public market costs. International expansion opportunities required the credibility of a listed entity. And frankly, after 52 years of building value, the Kapur family deserved some liquidity.

Listing Price: The Travel Food Services share price opened at ₹1,126.20 on BSE on July 14, 2025, representing a premium of 2.38% from the issue price of ₹1,100, whilst NSE listing showed ₹1,125 per share with 2.27% premium, delivering moderate gains for investors in line with expectations. The flat debut wasn't a disappointment—it was realistic pricing meeting market reality.

Ahead of their debut, the unlisted shares of Travel Food Services were commanding a muted premium in the grey markets. Sources tracking unofficial market activity revealed that the company's shares were changing hands at around ₹1,108 each, implying a grey market premium (GMP) of ₹8 or approximately 0.73 per cent over the IPO issue price of ₹1,100. The current GMP trends indicate a lacklustre listing for Travel Food Services shares on the bourses. Should the current grey market trends sustain, Travel Food Services shares may list at around ₹1,108 apiece.

The muted listing in challenging market conditions didn't reflect operational weakness but rather broader market sentiment. July 2025 saw global markets grappling with uncertainty, and Indian markets were no exception. For a company trading at premium valuations in a specialized sector, a flat debut was actually a victory.

The IPO structure revealed sophisticated financial engineering. Kotak Mahindra Capital Company Limited, HSBC Securities & Capital Markets Pvt Ltd, ICICI Securities Limited, and Batlivala & Karani Securities India Private Limited are the book-running lead managers of the Travel Food Services IPO. The choice of bankers—a mix of global bulge brackets and domestic leaders—signaled the company's ambitions to appeal to both international and local investors.

The validation aspect mattered as much as the money. Being a public company meant quarterly scrutiny, governance standards, and transparency—all things that would help TFS win larger contracts, attract talent, and potentially make acquisitions. In the infrastructure and concession business, being listed is a credibility multiplier.

Travel Food Services delivered restrained debut performance with modest premium reflecting selective investor confidence in airport food service companies with established market positions. Despite concerns over high valuation and pure OFS structure, the company's market leadership position, established airport presence, and strong financial performance provide steady growth potential in India's expanding aviation market, though the restrained listing performance suggests investors are cautious about premium valuations in specialised sectors.

The IPO marked not an end but a beginning. For the Kapur family, it was validation of a 52-year journey. For SSP, it crystallized value creation from their 2016 investment. For TFS management, it provided the platform and currency for the next phase of growth. And for investors, it offered a pure play on India's aviation and consumption boom—if they were willing to pay the price.

VII. Business Model Deep Dive: Unit Economics & Moats

The numbers are staggering, even for seasoned investors. FY25 revenue of Rs. 1,688 cr grew 21% YoY, as number of outlets increased by 20% whereas like-for-like sales growth was at 4.6%. Due to higher average order value, gross margin is 82% leading to an operating EBITDA margin of 35.6%, much higher than peer (Jubilant, Devyani, Sapphire, Restaurant Brands) range of 11% to 20%. FY25 PAT was up 28% YoY to Rs. 380 cr, translating into a net margin of 22.5%.

Let that sink in—82% gross margin, 35.6% EBITDA margin, 22.5% net margin. These aren't just good numbers for a QSR operator; they're extraordinary for any business. It exhibits exceptional fundamentals with industry-leading margins (EBITDA margin: 40%), high PAT margin (21.5%), robust RoE of 35.5%, and strong cash flows. To understand why, we need to dissect the unit economics.

A typical street-side QSR battles brutal economics: high rent (15-20% of sales), intense competition, price-sensitive customers, delivery aggregator commissions. TFS operates in a parallel universe. Airport customers have already mentally written off their wallets—they're captive, time-constrained, and often on expense accounts. A ₹500 burger that would cause riots on the street barely raises eyebrows at Terminal 3.

The concession economics are counterintuitive but brilliant. TFS primarily functions as a concessionaire, winning long-term airport contracts (average tenure ~8.2 years) to run multi-unit QSRs and lounges. Yes, TFS pays hefty revenue shares to airports—often 30-40% of sales. But consider what they don't pay: no property acquisition costs, built-in foot traffic, zero marketing spend for customer acquisition, shared security and utilities. The airport handles the hard infrastructure; TFS just needs to serve food.

Superior margins stem from multiple sources. Premium pricing is obvious—airports command 2-3x street prices. But the real magic is in operational leverage. Once you've won a concession and built out outlets, incremental sales drop straight to the bottom line. Staff can be deployed across multiple outlets. Central kitchens serve entire terminals. One negotiation with Coca-Cola covers dozens of outlets.

A strong RoCE of 51.4% in FY25 highlights efficient capital utilization and operational strength. This 51% return on capital employed is almost unheard of in the restaurant business. It happens because TFS doesn't own the real estate, doesn't need massive marketing budgets, and generates cash immediately from operations. The capital goes into fit-outs and working capital, both of which generate returns immediately.

The lounge business takes these economics to another level. The Lounge business, which contributed nearly 45% of revenue over the past three fiscal years, relies heavily on customers accessing services through credit and debit cards. Credit card companies pay TFS for access—it's a customer acquisition cost for them. Airlines pay for their premium passengers. Individual walk-ins pay ₹2,000+ for a few hours of comfort. The same physical space generates three revenue streams simultaneously.

Why can't everyone replicate this? The moats are deeper than they appear. First, winning concessions requires track record, financial strength, and relationships—you can't just show up. Second, operational complexity is extreme. Running 20 outlets in a terminal requires sophisticated logistics, staff management, and quality control. Third, brand relationships matter. KFC doesn't franchise to anyone; they need confidence in execution.

The working capital dynamics are beautiful. Customers pay immediately—cash or card. Suppliers give 30-45 day credit. Airports typically collect revenue share monthly. TFS essentially gets negative working capital—using supplier credit to fund operations while collecting cash daily. Debtor days have improved from 29.8 to 23.0 days.

Capital allocation follows a predictable pattern. Win concession → Invest in fit-out (₹50-70 lakhs per outlet) → Generate 30%+ EBITDA margins → Reinvest in next concession. High Retention: 93.94% contract renewal rate. The 94% renewal rate means capital isn't wasted on replacing lost locations.

The asset-light model is often misunderstood. Yes, TFS doesn't own airports. But they invest substantially in each location—kitchen equipment, furniture, signage, technology. The difference is this capex generates returns immediately because the location comes with guaranteed traffic. There's no three-year waiting period for a new restaurant to find its audience.

Pricing power increases over time. As contracts mature and TFS proves operational excellence, they can negotiate better terms at renewal. Airports need reliable operators more than TFS needs any single airport. The switching costs for an airport to replace an established operator running dozens of outlets seamlessly are enormous.

Scale economics compound these advantages. Procurement becomes cheaper—buying for 442 outlets gives massive negotiating power. Training systems become more efficient. Technology investments spread across more locations. Brand partners offer better terms. Every new outlet makes the existing network stronger.

As per the offer document, the company has shown Jubilant Foodworks, Devyani Intl., Saphire Foods, Westlife Foodworld, and Restaurant Brands, as their listed peers. They are trading at a P/E of 205, NA, NA, 973.0, and NA (as of July 02, 2025). However, they are not truly comparable on an apple-to-apple basis. The peer comparison is almost meaningless—street QSRs trading at 200x+ P/E while TFS trades at 32x despite superior margins shows the market hasn't fully grasped the model.

The cash generation is remarkable. The company has paid a dividend of 3693.03% (FY24), 843.02% (FY25), and 456% (during Q1 of FY26). These aren't typos—TFS paid dividends of 3,693% in FY24. This reflects both massive cash generation and the pre-IPO desire to distribute accumulated profits.

What would break this model? Not competition—the concession structure prevents that. Not recession—airports recover quickly. The real risk would be fundamental changes to how airports operate or how travelers behave. But with India adding airports, not closing them, and air travel growing, not shrinking, the model appears sustainable for decades.

The financial fortress TFS has built—82% gross margins, 51% ROCE, negative working capital, 94% renewal rates—isn't just impressive. It's a masterclass in finding and exploiting a structural advantage. While street QSRs fight for survival, TFS prints money at 30,000 feet.

VIII. Competition, Risks & The Bear Case: Lounge Business Vulnerabilities

Every dominant business has its Achilles' heel, and for TFS, it might be hiding in plain sight within the lounge business. Dependence on card access is critical, as the Lounge business, which contributed nearly 45% of revenue over the past three fiscal years, relies heavily on customers accessing services through credit and debit cards. A decline or surge in such users could negatively affect footfall, service quality, and customer experience.

This isn't theoretical risk—it's happening globally. Credit card companies, facing pressure on interchange fees and profitability, are scaling back lounge benefits. What was once unlimited access is becoming limited visits. Premium cards that offered complimentary lounge access are adding spending requirements. The days of every mid-tier credit card offering lounge access as a loss-leader may be numbered.

The lounge economics are particularly vulnerable because they're triangular. TFS doesn't control its customer acquisition—credit card companies do. TFS doesn't set the access rules—card issuers do. TFS just operates the facility and hopes the music doesn't stop. If major card issuers simultaneously tighten access, lounge revenues could collapse overnight.

Already, anecdotal evidence suggests problems. I believe it is something to do with all flights operating at high PLFs as well as credit card companies commercializing the lounges. The exclusivity and luxury is missing now a days in the lounges all over India. We are cruising to a situation where the existing lounge infra is falling short significantly. Overcrowding degrades the experience, which reduces willingness to pay, which pressures economics.

The highway opportunity that bulls tout might be a mirage. Only 1% of revenue comes from highways despite years of trying. Highway economics are fundamentally different—customers have alternatives, price sensitivity is higher, and you're competing with local dhabas that have cult followings. TFS's premium positioning and high-cost structure might be incompatible with highway operations.

Revenue concentration risk: A significant portion of the company's revenue, 85.94% in FY25, comes from its Travel QSRs and Lounges at the top five airports, making it vulnerable to traffic declines or concession non-renewals at these key locations. Lose Delhi or Mumbai, and the business changes dramatically. This isn't diversification; it's concentration disguised by multiple outlet counts.

Concession renewal risk lurks perpetually. The 94% historical renewal rate breeds complacency, but past performance doesn't guarantee future results. Impact on operator model shift: Changes in airport operators' business models requiring majority stakes in concession-holding entities have led the company to form joint ventures like Semolina and GHL, reducing its direct control and profit share in key airports like Mumbai and Hyderabad.

This structural shift is concerning. Airports are realizing F&B isn't just ancillary revenue but core to their business model. Why let TFS capture 60% of the economics when airports could internalize more? The formation of JVs where TFS doesn't have full control suggests airports are already moving in this direction.

Emerging competition isn't from other organized players but from airports themselves. Udaan Café impact: Government-run Udaan Yatri Cafés offering low-cost food options at airports may divert customers from the company's Travel QSR outlets, potentially affecting sales, brand perception, and financial performance. If government-mandated affordable options proliferate, TFS's premium pricing power erodes.

Direct airline lounges pose another threat. Airlines globally are investing in proprietary lounges to differentiate their premium offerings. As Indian carriers mature and seek differentiation, they might bypass TFS entirely. Why would IndiGo or Air India let TFS intermediate their relationship with premium customers?

Regulatory scrutiny intensifies with dominance. The Competition Commission of India hasn't yet focused on airport concessions, but 45% market share in lounges and 26% in QSRs might eventually attract attention. Forced divestitures or price regulations aren't impossible in India's interventionist regulatory environment.

The international expansion story might be oversold. Malaysia and Hong Kong are nice validations, but they're tiny. Replicating the Indian dominance elsewhere seems unlikely—every market has entrenched incumbents, different consumer preferences, and unique regulatory requirements. TFS faces competition from global giants like HMSHost and Lite Bite Foods in Travel QSR and Lounge categories.

Technology disruption lurks. Food delivery to gates, automated vending, ghost kitchens operating from cheaper spaces—all could disrupt the current model. TFS's high-cost infrastructure might become a liability if passengers prefer convenience over ambiance.

Geographic concentration risk extends beyond airports. Airport pricing risk: Higher menu prices at the company's airport QSR outlets compared to non-airport locations may lead to customer dissatisfaction, reduced sales, and potential legal or regulatory challenges. Social media amplifies pricing complaints. One viral post about ₹500 sandwiches could trigger regulatory intervention.

The bear case ultimately rests on sustainability of supernormal profits. 35% EBITDA margins attract competition, regulatory attention, and customer backlash. History suggests such margins in consumer-facing businesses rarely persist indefinitely. Either competition emerges, regulations intervene, or consumer behavior shifts.

The dependency chain is troubling: TFS depends on → airports which depend on → airlines which depend on → economic growth which depends on → factors beyond anyone's control. A single break in this chain—airline consolidation, airport privatization reversal, economic slowdown—cascades through the model.

Perhaps most concerning is the inability to diversify meaningfully. TFS is structurally tied to airports. Highways don't work. Street locations would compete with K Hospitality. International expansion is slow. They're trapped in a golden cage—highly profitable but with limited optionality.

The question isn't whether TFS is a good business today—it clearly is. The question is whether paying 32x earnings for a business with such concentrated risks and limited growth levers makes sense. When the core business depends on third parties you don't control, in locations you don't own, serving customers acquired by others, at prices that attract scrutiny—is that a fortress or a house of cards?

The bear case isn't that TFS will collapse—it won't. It's that growth slows, margins compress, and multiples contract as the market realizes this isn't a growth story but a mature, regulated, utility-like business that happens to be very profitable today. And in markets, the transition from growth stock to value stock is rarely pleasant for existing shareholders.

IX. Growth Vectors & The Bull Case: India's Aviation Boom

Despite the risks, the bull case for TFS rests on one undeniable truth: India's aviation boom is just beginning. India's air passenger traffic is projected to grow at a strong pace of 7% in 2025, driven by a growing middle class and increasing air travel affordability, according to Director at Alton Aviation Consultancy, Mr. Joshua Ng. This is primarily because of the country's developing infrastructure, which is expected to increase passenger numbers from 158 million in 2017 to an estimated 572 million by 2037, mostly because of the country's growing middle class.

The numbers are staggering. India is expected to overtake China and the United States as the world's third-largest air passenger market in the next ten years, by 2030, according to the International Air Transport Association (IATA). For the five years from 2023-2027, India's Compound Annual Growth Rate (CAGR) for air passenger traffic is estimated at 9.5%, outpacing China's 8.8%. Even more impressive, India is projected to be the fastest-growing aviation market globally for the 2023-2053 period with a CAGR of 5.5%, substantially higher than China's 3.8%.

Infrastructure expansion validates this growth. India aims to have 220 new airports by 2025, said, Mr. Jyotiraditya Scindia, Minister of Civil Aviation. The Government has informed that India will spend US$ 11.88 billion by 2025 to boost regional connectivity by constructing airports and modernising existing ones. In 2023, the government has accorded 'In-Principle' approval for setting up 21 Greenfield Airports across the country.

For TFS, every new airport is a growth opportunity. Noida International Airport, Navi Mumbai Airport, expansions in tier-2 cities—each represents millions in potential revenue. The company's proven ability to win and operate concessions positions them perfectly to capture this growth. Their track record—present since inception at Delhi T3 and Mumbai T2—makes them the default choice for new airports seeking credible operators.

The per capita opportunity is massive. The Civil Aviation Secretary said air trips per capita per annum for India is 0.13. Compare that to 2+ for developed countries. Even reaching China's current 0.5 trips per capita would quadruple the market. India has the fastest-growing air passenger market in the world, with a population of almost 1.4 billion. The runway for growth extends decades.

Premiumization accelerates TFS's advantage. As Indian consumers move up the income ladder, they don't just fly more—they spend more per trip. Business class grows faster than economy. Lounge access becomes aspirational. Premium coffee replaces chai. Every basis point of premiumization drops directly to TFS's bottom line given their premium positioning.

The highway opportunity, while currently small, could surprise. The India Aviation Infrastructure Market size is expected to reach USD 103.41 billion in 2025 and grow at a CAGR of 4% to reach USD 125.81 billion by 2030. As highway infrastructure improves and travel patterns evolve, TFS's multi-brand model might crack the code where others failed. Even capturing 5% of the highway F&B market would double their addressable market.

International expansion through the SSP partnership opens global doors. SSP operates in 35+ countries. TFS's lounge expertise, proven in India, could be replicated globally. The "ARAYA" lounge brand could become what Priority Pass became—a global standard for premium travel experiences. Hong Kong was just the beginning.

The valuation disconnect creates opportunity. High-street QSR peers like Jubilant, Devyani, Sapphire etc. are ruling in three-digit PE multiples. TFS trades at 32x despite superior margins, better unit economics, and stronger growth prospects. As markets understand the model better, multiple expansion alone could drive 50%+ returns.

Technology becomes an enabler, not a threat. TFS's Food@Gate delivery, self-ordering kiosks, and contactless payments aren't defensive moves—they're margin enhancers. Technology allows serving more customers with fewer staff, reducing the largest operating expense while improving service. The company that masters airport F&B technology dominates the market.

New revenue streams keep emerging. Corporate lounges for business travelers. Premium meal pre-ordering for flights. Packaged foods for takeaway. Subscription models for frequent flyers. Each innovation leverages existing infrastructure while expanding the revenue pie.

The competitive moat deepens with scale. Every new airport makes winning the next one easier. Every successful renewal builds credibility. Every brand partnership strengthens the portfolio. Network effects mean TFS gets stronger while new entrants face higher barriers.

Operational leverage hasn't peaked. At 35% EBITDA margins, bears assume nowhere to go but down. But global airport F&B operators achieve 40%+ margins at scale. As TFS grows, fixed costs spread further, procurement improves, and margins could expand, not compress.

The Jefferies report forecasts that India could surpass China in passenger traffic growth by 2026, with a projected 10.5% growth rate compared to China's 8.9%. If India follows China's aviation development path—and there's no reason it shouldn't—TFS's current ₹15,000 crore market cap could look quaint in retrospect.

Management quality and alignment seal the case. Three generations of Kapurs remain deeply involved. SSP brings global best practices. Management owns meaningful stakes. This isn't hired-gun management optimizing quarterly earnings—it's owners building a century-long franchise.

The domestic aviation sector currently operates approximately 850 aircraft across 150–160 airports. This is a stark contrast to China's 4,000 aircraft and 250+ airports. If India reaches even half of China's aviation penetration, TFS's business quadruples without any market share gains.

The bull case ultimately rests on this: TFS offers pure-play exposure to India's consumption and infrastructure story with proven execution, dominant market position, and structural advantages that compound over time. In a world seeking quality growth at reasonable prices, TFS might be hiding in plain sight.

The question isn't whether India's aviation sector will grow—it will. The question is whether any company is better positioned to capture that growth than TFS. With their track record, market position, partnerships, and execution capabilities, the answer appears to be no. At 32x earnings for a business growing 20%+ with 35%+ margins in a market growing at 10%+ for decades—the risk might not be owning it, but not owning it.

X. Playbook & Lessons for Founders

The TFS story isn't just about airports and food—it's a masterclass in building enduring value through patient capital, strategic partnerships, and operational excellence. For founders navigating India's complex business landscape, the Kapur family's 52-year journey from a single Copper Chimney restaurant to a ₹15,000 crore public company offers timeless lessons.

The Power of Patient Capital

JK Kapur started Copper Chimney in 1972 with limited resources but unlimited ambition. For 35 years, the family built K Hospitality organically, reinvesting profits rather than raising external capital. This wasn't slow growth—it was foundation building. By the time they entered airports in 2007, they had the operational expertise, financial strength, and credibility that venture-funded competitors lacked.

The lesson: Patient capital creates competitive advantages that fast money can't buy. While others optimize for exits, patient builders optimize for dominance. The Kapurs waited 52 years for their liquidity event—and captured value that quick flippers never could.

When to Bring in Strategic Investors

The 2016 SSP partnership marked a crucial inflection point. After 44 years of sole ownership, why partner then? The Kapurs recognized that scaling from Indian champion to regional leader required capabilities they couldn't build internally fast enough—global brand relationships, international operational expertise, capital markets credibility.

But they didn't sell out. They brought in a 49% partner who added strategic value while maintaining family control. SSP wasn't just capital—they were a force multiplier. The timing was perfect: TFS had proven the model, airports were expanding, and competition was intensifying.

The lesson: Strategic investors should be brought in when they accelerate your vision, not just fund it. The best partnerships combine complementary strengths—SSP's global reach with Kapur's local expertise created something neither could achieve alone.

Building Trust with Government Stakeholders

Airports aren't just infrastructure—they're strategic national assets. Winning concessions requires more than the highest bid; it requires trust. TFS built this trust methodically: starting small (Mumbai Terminal 1B), executing flawlessly, then expanding. Their ~94% renewal rate reflects relationships built over decades.

The playbook included: Never missing service standards. Investing ahead of requirements. Being flexible during crisis (COVID). Treating airport operators as partners, not landlords. Understanding that government stakeholders value reliability over maximization.

The lesson: In regulated industries, trust is currency. Build it slowly, guard it carefully, and leverage it strategically. One broken promise can undo decades of relationship building.

Brand Portfolio Management: Licensed vs Owned

TFS's 127-brand portfolio seems unwieldy, but there's method to the madness. International brands (KFC, Pizza Hut) provide instant credibility. Regional brands (Bikanervala, Hatti Kaapi) offer local authenticity. In-house brands (Dilli Streat, Caféccino) fill gaps and capture higher margins.

The split—54% revenue from partner brands, 46% from in-house—is deliberately balanced. Partner brands drive traffic; owned brands drive margins. International brands attract foreign travelers; regional brands serve domestic passengers. Fast food serves rushed connections; cafes serve long layovers.

The lesson: Brand portfolio management is about solving customer jobs, not collecting logos. Each brand should have a clear role, target segment, and economic rationale. The mix should balance risk (franchise fees) with reward (higher margins on owned brands).

The Concession Game: How to Win and Retain

Winning airport concessions requires understanding that you're not just bidding—you're auditioning for a decade-long partnership. TFS's approach included: Demonstrating financial strength (bank guarantees, track record). Proposing comprehensive solutions (multiple brands, formats, price points). Committing to investments beyond minimum requirements. Highlighting operational expertise (security clearances, 24/7 operations). Building relationships before RFPs are issued.

Retention requires different skills: Consistent service delivery. Proactive renovation and refresh. Adapting to changing passenger demographics. Being flexible during disruptions. Never taking renewal for granted.

The lesson: In concession businesses, winning is about capability demonstration, not just price. Retention is about partnership, not just performance. The real competition happens before the tender is issued and after the contract is signed.

Family Business Transitions: Three Generations

The Kapur family navigated what destroys most family businesses—generational transition. JK Kapur founded it. Sunil Kapur scaled it. Varun and Karan Kapur are modernizing it. Each generation added value without destroying what came before.

Key principles included: Clear role definition (Varun runs travel retail, Karan runs restaurants). Merit-based progression (both sons worked elsewhere first). Professional management alongside family (CEO, CFO are professionals). Gradual transition (sons joined in 2008, took leadership roles by 2017). External validation (SSP partnership, public listing) to ensure objectivity.

The lesson: Successful family transitions require structure, patience, and humility. Each generation must earn their authority, not inherit it. Professional management provides objectivity that family dynamics can cloud.

The India Playbook: Organized Players in Fragmented Markets

TFS succeeded by bringing organized retail principles to fragmented markets. Indian airport F&B was dominated by local operators running single outlets. TFS brought scale, standards, and systems. They didn't compete with mom-and-pop shops—they replaced them.

The playbook works across sectors: Identify large, fragmented markets with poor customer experience. Build operational excellence that small players can't match. Use scale to negotiate better terms with suppliers and landlords. Standardize quality while maintaining local relevance. Roll up the market through superior execution, not just capital.

The lesson: In India, organized players in fragmented markets capture disproportionate value. The key isn't innovation—it's execution at scale with consistency.

Timing Markets vs Building Businesses

TFS didn't time the airport privatization wave—they prepared for it. When opportunities emerged, they were ready with capital, capabilities, and credibility. The 2025 IPO wasn't about market timing—it was about business readiness meeting market receptiveness.

The lesson: Build for inevitable trends, not market timing. India's aviation growth was predictable; TFS's execution made it profitable.

Managing Complexity at Scale

Running 442 outlets across 18 airports with 127 brands and 10,000+ employees requires systems that most founders underestimate. TFS built capabilities gradually: Single brand, single location → Multiple brands, single location → Multiple brands, multiple locations → Multiple brands, multiple locations, multiple countries.

Each phase required different skills: entrepreneurial hustle → operational excellence → systematic scaling → portfolio management.

The lesson: Complexity compounds exponentially. Build management systems ahead of growth, not in response to it. What works at 10 outlets breaks at 100.

The Partnership Paradox

TFS manages multiple, potentially conflicting partnerships simultaneously. They're partners with competing airports (Delhi vs Mumbai). They operate competing brands (KFC vs Pizza Hut). They serve competing airlines' lounges. They work with SSP while maintaining independence.

Managing this requires: Clear boundaries and governance. Transparent decision-making processes. Information barriers where necessary. Professional management that isn't conflicted. Understanding that good partnerships have conflicts—great partnerships manage them.

The lesson: Complex businesses require managing paradoxes, not avoiding them. The ability to be simultaneously cooperative and competitive creates unique advantages.

The Long Game Always Wins

Every significant decision in TFS's history—entering airports, partnering with SSP, going public—was made with decades-long horizons. They didn't optimize for quarterly earnings or quick exits. They built for permanence.

This manifested in: Investing ahead of requirements. Building relationships before needing them. Maintaining capabilities through cycles. Choosing partners for alignment, not just terms. Pricing IPO for long-term holders, not flippers.

The lesson: In businesses with long-term concessions, relationships, and capital cycles, patient players capture disproportionate value. The long game isn't just strategy—it's competitive advantage.

For founders, TFS demonstrates that building enduring value requires more than product-market fit or growth hacking. It requires patient capital, strategic partnerships, operational excellence, and most importantly, the discipline to build for decades, not quarters. In India's complex business environment, these lessons aren't just helpful—they're essential.

XI. Analysis & Final Thoughts

After examining TFS from every angle—its history, business model, competitive position, and future prospects—we arrive at the fundamental question: Is this a monopoly or an earned market position?

The answer is both, and that's what makes TFS fascinating.

It's not a monopoly in the legal sense—anyone can bid for airport concessions, no regulations prevent competition, and TFS doesn't control essential infrastructure. But it's achieved something perhaps more powerful: an earned dominance built on operational excellence, strategic positioning, and decades of trust-building that creates barriers no amount of capital can quickly overcome.

Comparison with Global Airport F&B Operators

When you examine global peers—HMSHost (part of Autogrill), SSP, Lagardère Travel Retail—TFS's margins stand out. Most global operators achieve 15-20% EBITDA margins; TFS delivers 35%+. This isn't accounting manipulation—it's structural advantage from operating in a high-growth, less-penetrated market with premium pricing power.

But the comparison also reveals TFS's limitations. Global operators run thousands of outlets across hundreds of airports. TFS has 442 outlets in 18 airports. Global players have diversified across airports, railways, highways. TFS is 85%+ dependent on five airports. The international giants are truly global; TFS is essentially an India story with token international presence.

The India Opportunity vs Execution Risk

India's aviation growth story is real. By 2030, it is anticipated that 300 million people will travel domestically by plane in India. The mathematics are compelling: 1.4 billion population × inevitable income growth × infrastructure expansion = massive market expansion.

But execution risk lurks everywhere. Can TFS maintain service quality while scaling rapidly? Will new airport operators demand different economics? Can they adapt to changing consumer preferences—health consciousness, local authenticity, sustainability demands? Will technology disruption arrive faster than expected?

The biggest execution risk might be complacency. When you're earning 35% EBITDA margins and have 94% renewal rates, it's easy to assume tomorrow looks like today. But Indian business history is littered with dominant players who missed inflection points—Hindustan Motors with Ambassador, MTNL in telecom, Doordarshan in broadcasting.

What Would Make This a 10x From Here?

For TFS to 10x from ₹15,000 crores to ₹150,000 crores requires multiple expansions:

- India reaching 1 billion passenger trips annually (from 400 million today)—plausible given China's at 700 million with similar population

- TFS maintaining 25%+ market share despite new entrants—challenging but achievable given their incumbency advantages

- International becoming 30%+ of revenue through lounge franchising and selective airport entry—requires execution beyond current demonstration

- Margins sustaining at 30%+ despite scale and competition—depends on premiumization offsetting pressure

- Multiple expansion to 50-60x as markets recognize the quality—reasonable if growth sustains

Is this impossible? No. Is it probable? The jury's out. It requires everything going right—macro, micro, execution, competition, regulation. But in India's history, several companies have achieved such transformations—HDFC Bank, Asian Paints, Titan. TFS has the ingredients; whether they have the recipe remains to be seen.

Key Metrics to Watch

For investors tracking TFS, focus on:

- Passenger growth at top 5 airports: 85% of revenue concentration means these matter most

- Spend per passenger trends: Premiumization vs trading down will determine margin trajectory

- Concession renewal outcomes: Each renewal is a referendum on the business model

- Lounge access economics: Credit card company decisions will impact 45% of revenue

- New airport win rates: Market share in new airports indicates competitive position

- Same-store sales growth: Organic growth vs just outlet addition shows underlying health

- Working capital trends: Deterioration would signal operational stress

- Employee cost per outlet: Labor inflation could pressure margins significantly

The Monopoly Question Revisited

TFS isn't a monopoly—it's a dominant player in a regulated, competitive market. The 26% QSR and 45% lounge market shares are significant but not insurmountable. New entrants can and will emerge. But TFS has built what Warren Buffett calls a "moat"—structural advantages that protect returns on capital.

The moat has multiple layers: Operational expertise in complex environments. Relationships built over decades. Scale economics in procurement and operations. Portfolio breadth to meet any RFP requirement. Financial strength to invest ahead of requirements. Partnership with global leader SSP.

Is this moat permanent? No moat is. But it's wide enough and deep enough to protect returns for years, possibly decades.

The Regulatory Wildcard

The elephant in the room is regulatory intervention. When any company earns 35% EBITDA margins from public infrastructure, political attention follows. We've seen this movie before—telecom AGR dues, retrospective taxation, price caps in various sectors.

Could regulators cap F&B prices at airports? Mandate minimum local vendor participation? Limit market share per operator? Require revenue sharing beyond current agreements? All possible in India's interventionist regulatory environment.

But TFS has natural defenses. They're providing quality service in challenging environments. They're paying substantial revenue shares already. They're creating employment and tax revenues. Most importantly, they're solving a problem—making Indian airports world-class—that regulators want solved.

Final Verdict: Monopolistic Competition

TFS operates in what economists call "monopolistic competition"—many sellers, differentiated products, barriers to entry, but not absolute pricing power. They have local monopolies (sole operator in Chennai, Kolkata) within broader competition.

This is actually the sweet spot. Pure monopolies attract regulation. Perfect competition destroys returns. Monopolistic competition allows superior operators to earn superior returns while maintaining competitive dynamics that prevent regulatory intervention.

The Investment Thesis Crystallized

TFS is a high-quality business with: - Structural growth tailwinds (India aviation boom) - Competitive advantages (scale, relationships, expertise) - Superior economics (35% EBITDA margins, 50%+ ROCE) - Reasonable valuation (32x PE vs peers at 100x+)

But it also has: - Concentration risks (airports, lounges, geography) - Regulatory vulnerabilities (high margins from public infrastructure) - Execution challenges (scaling while maintaining quality) - Limited optionality (trapped in airports)

For growth investors seeking India exposure, TFS offers pure-play access to consumption and infrastructure themes. For value investors, the margins and returns compensate for risks. For quality investors, the moats and management tick boxes.

But for skeptics, the concentrated risks and regulatory wildcards are deal-breakers.

The Philosophical Close

Perhaps the most interesting aspect of TFS isn't financial but philosophical. It represents a new breed of Indian companies—globally competitive yet locally rooted, professionally managed yet family-controlled, technology-enabled yet service-focused, profitable yet growing.

TFS proves Indian companies can build world-class operations in complex environments. They show that patient capital and strategic partnerships can create more value than aggressive financial engineering. They demonstrate that in India, solving basic problems well—feeding travelers good food quickly—can build billion-dollar businesses.

Whether TFS becomes a ten-bagger or a value trap, its journey from Copper Chimney to airport dominance has already validated a crucial principle: In India's growth story, execution beats innovation, consistency beats brilliance, and the long game always wins.

For investors, TFS isn't just a stock—it's a bet on India's transformation from a developing to developed economy, from price-conscious to experience-seeking consumers, from functional to world-class infrastructure.

That transformation seems inevitable. Whether TFS captures its fair share of that value creation is the ₹15,000 crore question. The answer, like India's future itself, remains unwritten but full of possibility.

XII. Recent News

The post-IPO era has begun with characteristic TFS execution. In Q1 FY26, Travel Food Services Limited delivered a healthy performance, with system-wide sales rising by 26.7% to ₹7,151 million and adjusted consolidated PAT increasing by 19.3%, despite temporary sector headwinds. These results, announced in August 2025, marked the company's first quarter as a public entity—a test of whether the premium valuation was justified.

The company posted robust numbers with Q1 PAT standing at ₹91.77 crores against revenue of ₹375.05 crores, with consolidated PAT rising 65.61% YoY during the first quarter of FY26. LFL sales growth was 5.5% YoY, despite some moderation in passenger traffic growth, demonstrating pricing power even in challenging conditions.

The Gordon Ramsay Coup

Perhaps no single announcement better encapsulates TFS's ambitions than the August 2025 launch of Gordon Ramsay Street Burger at Delhi Terminal 1. Gordon Ramsay Restaurants Global has introduced Street Burger at Terminal 1 of Indira Gandhi International Airport (IGIA) in Delhi, marking the chef's entrance to the Indian market in collaboration with Travel Food Services (TFS).

This marks only the fourth airport worldwide — after London Heathrow, Doha, and Hong Kong — where Ramsay has opened an outlet under his own brand. The significance extends beyond celebrity cachet—it signals TFS's ability to attract global brands that typically wouldn't consider India.

Varun Kapur, Managing Director and CEO of Travel Food Services Limited, commented: "Bringing Gordon Ramsay to India, and into the airport space for the first time, is a defining milestone for us at Travel Food Services Limited. This partnership combines our operational expertise with the Gordon Ramsay team's culinary excellence to meet the demand for global-quality dining that's fast, relevant, and elevated".

The menu adaptation shows sophisticated localization—from Tandoori Paneer and The Butternut Bhaji Burger alongside the global fan favourite Gordon's Fried Chicken (GFC) Burger. This isn't tokenism but thoughtful product development that respects both the global brand and local preferences.

Network Expansion & Brand Evolution

The company's strong system-wide network reached 454 Travel QSR outlets and 37 lounges as of June 30, 2025, with a portfolio of 130 in-house and partner brands. 57 new Travel QSR outlets were mobilised in the past 12 months, mainly at the Mumbai, Hyderabad, Ahmedabad and Lucknow airports, while lounges increased from 31 to 37 at system-wide level.

The expansion wasn't just quantity—quality improvements included launching India's first Nando's airport outlet at Delhi Terminal 3, strengthening the partnership with Coca-Cola across multiple airports, and transitioning to a direct partnership with American Express for lounge services.

Industry Recognition & Operational Excellence

TFS won eight awards at the prestigious 2025 FAB Awards in Barcelona, with recognition spanning across categories such as F&B innovation, sustainability, and inclusivity, thereby reinforcing TFS' strong position in airport hospitality in the Asia Pacific Region. Their Global Lounge at Kuala Lumpur International Airport, Malaysia, was honoured by Etihad Airways for service excellence to the Airline's guests in the quarter, underscoring commitment to exceptional guest experience, premium amenities, and culturally inspired hospitality.

Technology & Infrastructure Initiatives

Behind the headlines, TFS continued building infrastructure for the next decade. The company developed technology platforms for direct connection between banking and card network partners and lounge access systems—critical for managing the complex web of access arrangements that drive lounge economics.

Corporate Governance Evolution

Ashwani Kumar Puri was appointed as Chairman and Independent Director of the Company since November 23, 2024. With over 34 years of experience in the financial advisory and consulting sector, he previously served as a partner, leader of the financial advisory services practice in India, and member of the global advisory leadership team at PwC.

The board composition—mixing industry veterans with financial experts—signals preparation for the next phase: potential M&A, international expansion, and navigating public market expectations.

Market Response & Analyst Views

The scrip was listed at Rs 1,126.20, exhibiting a premium of 2.38% to the issue price, with the stock hitting a high of 1,128.90 and a low of 1,086. Post-listing performance has been volatile, reflecting broader market uncertainty and the small free float limiting liquidity.

Promoters seem not to be bullish about the company and have been selling shares in the open market, with latest quarter promoter holding at 86.19% versus 100.0% in the last quarter. While this reflects the IPO's OFS structure rather than lack of confidence, market perception matters.

Looking Ahead: Challenges & Opportunities

The temporary headwinds mentioned in Q1 results—geopolitical tensions and aircraft groundings—highlight the business's sensitivity to external factors. Yet management's tone remains confident, focusing on long-term structural growth rather than quarterly fluctuations.

Ramsay and TFS plan to open six dining outlets across Indian airports, including Gordon Ramsay Plane Food (all-day pre-departure dining), Street Pizza (artisanal pizzas), Street Burger (gourmet burgers), and Gordon Ramsay Plane Food To-Go (quick, high-quality meals). Mumbai Airport will host the second outlet, continuing the premium brand rollout strategy.

The Dividend Signal

The current dividend yield of Travel Food Services Ltd is 0.69, modest compared to the pre-IPO special dividends but signaling a shift from capital distribution to reinvestment—appropriate for a growth company with expansion opportunities.

XIII. Links & Resources

For investors and analysts tracking TFS, primary sources provide the most reliable information:

Company Resources: - Official Website: travelfoodservices.com/investors - Quarterly Results and Financial Statements (FY 2022-2026) - Earnings Call Transcripts and Audio Recordings - Investor Presentations and Press Releases - CRISIL Assessment of Indian Travel QSR and Global Lounges Industry (June 2025)

Regulatory Filings: - BSE Listing: BSE Code 544065 - NSE Listing: Symbol TRAVELFOOD - SEBI DRHP and RHP Documents - Corporate Governance Policies and Board Committee Details

Industry Reports: - IATA Aviation Statistics and Forecasts - Airports Authority of India Traffic Reports - Global Travel Retail Association Studies - SSP Group plc Annual Reports (for partnership context)

Key Metrics Tracking: - Monthly passenger traffic data from major airports - Credit card industry reports on lounge access trends - QSR industry reports from CRISIL, ICRA - Aviation infrastructure updates from Ministry of Civil Aviation

Academic & Case Studies: - IIM case studies on Indian aviation growth - Harvard Business Review articles on airport economics - McKinsey reports on Indian consumer behavior - BCG studies on travel retail trends

News & Analysis Sources: - Moneycontrol, Economic Times for daily updates - Mint, Business Standard for in-depth analysis - Restaurant India, Hospitality Biz for F&B industry coverage - Aviation Week, CAPA India for aviation sector insights

Final Reflections: The Journey Continues

As we conclude this deep dive into Travel Food Services, what emerges is more than just an investment thesis—it's a lens into India's transformation. From JK Kapur's first Copper Chimney in 1972 to Gordon Ramsay's Street Burger in 2025, TFS embodies the journey of Indian entrepreneurship: patient, adaptive, increasingly sophisticated, yet deeply rooted in local understanding.

The company stands at an inflection point. Public market scrutiny will test whether the exceptional margins are sustainable. Competition will intensify as the opportunity becomes obvious. Regulatory attention may follow success. Technology will reshape customer expectations. Yet TFS has navigated greater challenges—from partition refugee to public company is a longer journey than any ahead.

For investors, TFS presents a paradox: a mature business model in a nascent market, premium valuations for a value creator, concentrated risks with diversified opportunities. It's neither a pure growth story nor a value play, but something more nuanced—a quality compounder in a structural growth market.

The bear case—concentration risk, regulatory overhang, margin compression—is real and shouldn't be dismissed. But the bull case—India's aviation boom, execution excellence, partnership advantages—is equally compelling. Perhaps the truth lies not in choosing sides but in recognizing that great businesses often carry great risks, and the ability to navigate them defines long-term winners.

What makes TFS fascinating isn't just what it's achieved but what it represents: the maturation of Indian consumer businesses, the power of patient capital, the value of operational excellence over financial engineering. In a market often obsessed with the next unicorn, TFS reminds us that sometimes the most valuable businesses are built not in years but decades.

As Indian airports modernize, as travelers become more discerning, as the country's aviation ambitions soar, TFS will be there—serving coffee to rushed executives, comfort food to homesick travelers, global cuisine to adventurous millennials. It's a simple business—feeding people—executed with extraordinary sophistication in an extraordinarily complex environment.

The question for stakeholders—investors, partners, competitors—isn't whether TFS will grow; it's whether they can maintain excellence at scale, navigate success without hubris, and continue evolving without losing what made them special. The first 52 years built the foundation; the next decade will determine whether this becomes one of India's defining business success stories or a cautionary tale of peak margins and missed transitions.

For now, as passengers rush through Indian airports, most remain unaware of the company serving them. That anonymity might be TFS's greatest achievement—building a ₹15,000 crore empire so seamlessly integrated into travel infrastructure that it becomes invisible, essential, irreplaceable. In business, as in hospitality, sometimes the highest compliment is being taken for granted.