Tamilnad Mercantile Bank: A Century of South Indian Banking

I. Introduction & Episode Roadmap

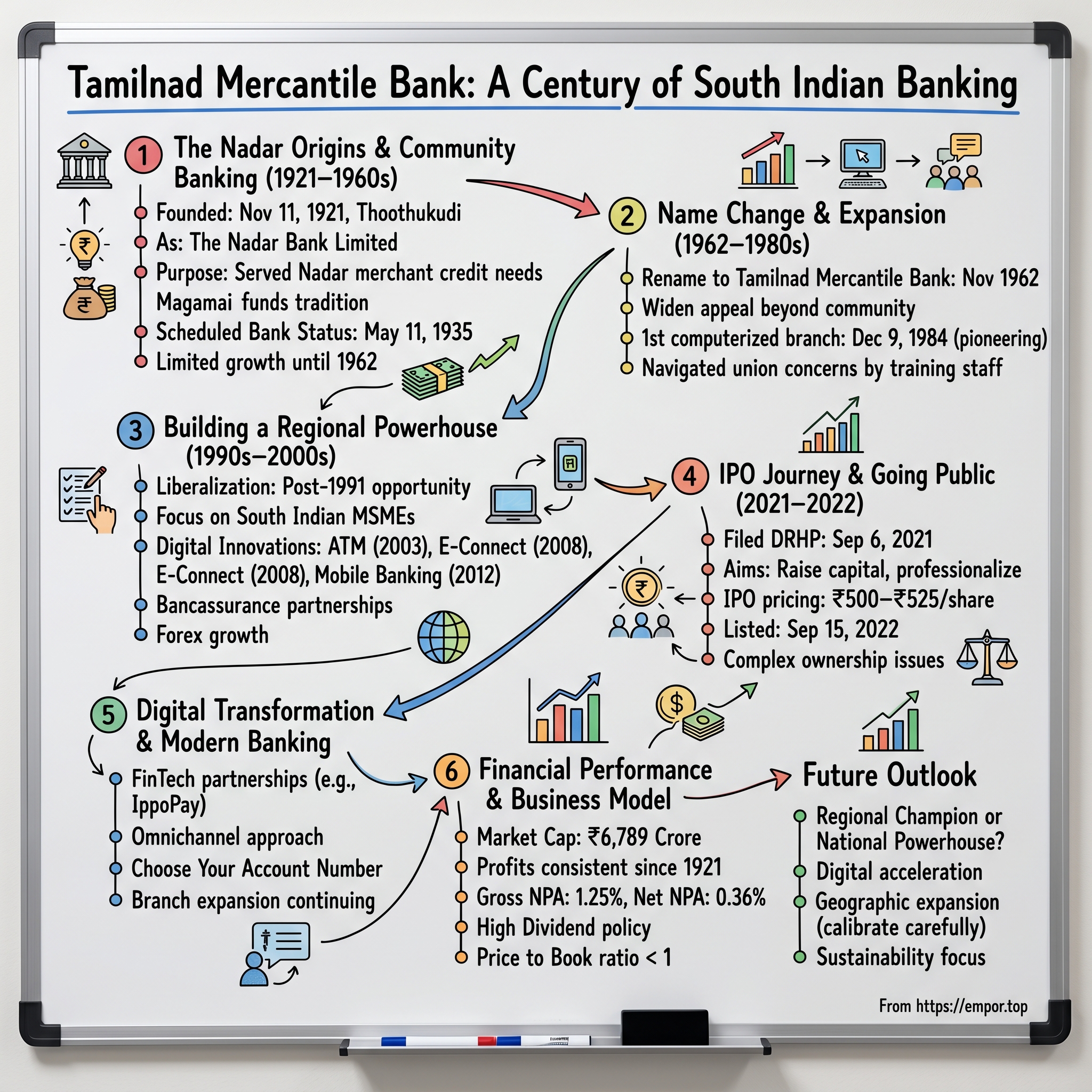

Picture this: November 11, 1921. In a modest building on South Raja Street in Thoothukudi—a port city where the Arabian Sea meets Tamil Nadu's southern coast—a gathering of local merchants and community leaders watches as T.V. Balagurusamy Nadar cuts the ribbon on what would become one of India's most enduring financial institutions. The Nadar Bank, as it was then called, opened its doors with a princely sum of ₹21,010 in deposits. Today, that same institution—now Tamilnad Mercantile Bank—manages over ₹53,000 crores in deposits and commands a market capitalization approaching ₹7,000 crores.

The question that frames our story is deceptively simple: How did a community bank founded to serve the financial needs of Nadar merchants in coastal Tamil Nadu transform into a modern private sector bank competing with giants like HDFC and ICICI? The answer reveals not just the evolution of one institution, but the entire arc of Indian banking from colonial commerce through liberalization to digital transformation.

TMB's journey mirrors India's own economic evolution—from community capitalism to universal banking, from ledger books to mobile apps, from serving local traders to going public on the NSE. Yet unlike many of its peers who either consolidated into mega-banks or disappeared entirely, TMB maintained its regional soul while building national ambitions. This is the story of how a 103-year-old bank learned new tricks without forgetting its old wisdom.

What makes TMB particularly fascinating for students of business history is its navigation of seemingly impossible contradictions. It's a conservative lender with aggressive digital ambitions. A regional specialist with national licenses. A bank where employee unions hold major shareholdings alongside public investors. Understanding these paradoxes—and how TMB turned them into competitive advantages—offers lessons far beyond banking.

Our exploration will take us from the founding vision of the Nadar community leaders through the strategic name change of 1962, the technology revolution of the 1980s, post-liberalization survival, and ultimately to its 2022 IPO that marked its transformation into a public company. Along the way, we'll examine how TMB built one of Indian banking's strongest balance sheets with NPAs at just 0.36%, why it trades at a curious discount to book value, and what its next century might hold.

II. The Nadar Origins & Community Banking (1921–1960s)

The story begins not in a boardroom but at a community gathering. In 1920, at the anniversary celebration of the Nadar Mahajana Sangam in Tuticorin (now Thoothukudi), an audacious idea emerged from heated discussions among community elders. The Nadars—traditionally toddy tappers who had transformed themselves into successful merchants and traders—faced a persistent problem: access to formal credit. British and Chettiar-controlled banks viewed them with suspicion, demanding collateral the community couldn't provide and charging rates that bordered on usurious.

"Why must we beg for capital to build our businesses?" The question, reportedly posed by a textile merchant whose name is lost to history, crystallized into action. Within months, the community mobilized with remarkable efficiency. Share subscriptions were gathered from Nadar businesses across southern Tamil Nadu—textile traders from Sivakasi, match manufacturers from Virudhunagar, shipping agents from Thoothukudi. On May 11, 1921, The Nadar Bank Limited was officially registered, marking the birth of what would become one of India's most resilient financial institutions. The election of M.V. Shanmugavel Nadar as the first chairman on November 4, 1921, marked more than a ceremonial appointment—it represented the community's determination to control its own financial destiny. Shanmugavel Nadar was elected as Chairman on Nov 04, 1921, bringing with him not just capital but a network of traders who understood the rhythms of regional commerce better than any outsider could.

The early numbers tell a story of patient accumulation. Starting with deposits of just ₹21,010 in 1921, the bank grew to ₹27 lakhs by 1946—a thousand-fold increase during a period encompassing global depression, world war, and the tumult of independence. By 1971, deposits had reached ₹182 lakhs, validating the community banking model that many colonial administrators had dismissed as parochial.

The Nadar community had historically been toddy-tappers, while the Chettiars were the traditional business community, with communities identified by their traditional livelihoods. This social positioning made access to formal credit nearly impossible for Nadar entrepreneurs. The creation of their own bank wasn't just about convenience—it was about dignity and self-determination.

The geographic expansion tells its own story of ambition meeting reality. In 1937, Nadar Bank opened a branch in Sri Lanka, but by 1939 it had closed it. By 1947, the bank had only four branches: Thoothukudi, Madurai, Sivakasi and Virudhunagar. This Sri Lankan misadventure—rarely discussed in official histories—reveals early international ambitions that proved premature. The retreat to four core branches in Tamil Nadu's Nadar heartland showed strategic wisdom: build strength at home before venturing abroad.

What made the Nadar Bank work wasn't just community solidarity but sophisticated financial practices adapted from traditional systems. The community had a tradition of 'Magamai' funds—similar to Islamic zakat—that grew substantial over time, with Shanars meeting monthly to discuss fund utilization for community benefit. This culture of collective saving and strategic deployment of capital provided the behavioral foundation for formal banking.

The achievement of Scheduled Bank status under the Reserve Bank of India Act on May 11, 1935—exactly 14 years after registration—marked a crucial transition. The bank became a Scheduled Bank under the Reserve Bank of India Act on May 11, 1935. This wasn't merely regulatory recognition; it meant access to RBI refinancing, participation in clearing houses, and most importantly, legitimacy in the eyes of non-Nadar customers who would become essential for growth beyond community boundaries.

By 1962, the leadership faced an existential question: remain a prosperous but limited community bank, or transform into something larger? The answer would reshape not just the institution but the very identity of Tamil Nadu banking.

III. The Name Change & Expansion Beyond Community (1962–1980s)

The boardroom discussion in November 1962 must have been electric with tension. For 41 years, "The Nadar Bank" name had been both shield and sword—protecting community interests while fighting for legitimacy. Now, directors proposed abandoning this identity for "Tamilnad Mercantile Bank." The older generation saw betrayal; the younger saw necessity.

TMB changed its name to Tamilnad Mercantile Bank in November 1962 to widen its appeal beyond the Nadar community. The strategic logic was unassailable: deposits had plateaued, non-Nadar businesses hesitated to bank with an explicitly community institution, and expansion beyond Tamil Nadu would be impossible with such a parochial identity. Yet the emotional cost was real—this was a community that had built its bank precisely because others had excluded them.

The name change coincided with a broader transformation in Indian banking. The 1960s saw bank nationalizations, credit controls, and directed lending mandates that could have suffocated a small private bank. TMB's response was counterintuitive: instead of resisting modernization, it embraced it ahead of the curve. The first branch outside Tamil Nadu opened in 1976 at Bengaluru—15 years after the name change, suggesting a deliberate patience in expansion strategy. But the real revolution came on December 9, 1984, when TMB opened India's first fully computerized bank branch at WGC Road, Thoothukudi.

This wasn't just a technology story—it was a leadership coup. The first fully computerized branch was opened at WGC Road, Thoothukudi on 9 December 1984, predating the Rangarajan Committee's recommendations by several years. While A Committee was set up in 1983 under the chairmanship of Dr. C. Rangarajan to look into modalities of drawing a phased plan of mechanization in the Banking Industry, covering the period 1985-89, and the Committee submitted its report in 1984 recommending introduction of computerization, TMB had already implemented what the committee would only recommend.

The contrast with the broader banking sector was stark. Those were the days of enormous delays in cheque clearances, with money taking weeks to get credited to accounts of customers, and there were lots of issues relating to reconciliation or tallying of transactions at the end of the day, with instances of funds being set aside in separate accounts to handle these discrepancies. Meanwhile, TMB was processing transactions in real-time, reconciling accounts automatically, and providing instant balance updates—capabilities that wouldn't become standard in Indian banking for another decade.

The resistance elsewhere was fierce. The resistance of unions and workers in Calcutta was so high that handling of payments and settlements, which involved computerisation or mechanisation, had to be done out of another office and not the main regional office of the RBI in that city. TMB faced similar union concerns but navigated them through a unique approach: positioning technology as a tool for employee empowerment rather than replacement. Branch staff were trained as computer operators, turning potential adversaries into advocates.

The strategic implications went beyond operational efficiency. By computerizing first, TMB could offer services that larger banks couldn't—instant inter-branch transfers, real-time account updates, automated interest calculations. For the MSME customers who formed TMB's core constituency, these weren't luxuries but competitive necessities. A Sivakasi fireworks manufacturer could instantly transfer funds to suppliers in Thoothukudi, while competitors banking with nationalized institutions waited days for the same transaction.

This period also saw TMB quietly building what would become one of Indian banking's most sophisticated risk management systems. Computerization enabled granular tracking of loan performance, early warning systems for NPAs, and data-driven credit decisions—capabilities that explain why TMB today maintains NPAs at a remarkable 0.36% while peers struggle with multiples of that figure.

The 1980s ended with TMB positioned uniquely: technologically ahead of giants, culturally rooted in community values, and strategically focused on the MSME segment that would drive India's next growth phase. The stage was set for navigating liberalization's upheavals.

IV. Building a Regional Powerhouse (1990s–2000s)

July 1991. Finance Minister Manmohan Singh rises in Parliament to deliver a budget that would reshape India's economy. For TMB's leadership watching from Thoothukudi, the speech represented both existential threat and unprecedented opportunity. Foreign banks would enter. New private banks would emerge. License Raj would crumble. The question wasn't whether to compete, but how.

TMB's response revealed strategic sophistication masked by operational simplicity. While new entrants like HDFC Bank raised capital through IPOs and foreign banks leveraged global balance sheets, TMB doubled down on what it knew best: the intricate financial needs of South Indian MSMEs. But this wasn't defensive retrenchment—it was offensive specialization. Consider the timeline of TMB's digital innovations: The Bank launched its ATM Card on 11 November 2003—the bank's 82nd anniversary, a symbolic choice. This was followed by TMB launched SMS banking services and internet banking facilities (TMB E-Connect) in 2008, and Launched mobile banking facilities in 2012. But the real innovation wasn't in the technology itself—it was in the deployment strategy.

TMB's masterstroke was launching the first insurance linked deposit scheme, Siranjeevee Recurring Deposit in 2005. This wasn't just product innovation; it was cultural translation. TMB understood that its core customers—small business owners and salary earners—valued security over returns. By bundling insurance with deposits, TMB addressed both savings and protection needs in one product, years before "bancassurance" became industry standard.

The bank's approach to partnerships revealed strategic sophistication. The bank has tie-up agreement with ICICI Prudential Mutual Fund, UTI Mutual Fund, Reliance Mutual Fund, Franklin Templeton Mutual Fund, Birla Sun Life Mutual Fund, Sundaram Mutual Fund and HDFC Mutual Fund for selling their Mutual Fund Products. Rather than seeing these giants as threats, TMB positioned itself as their distribution partner in tier-2 and tier-3 markets where the big banks had limited presence.

TMB was the first bank in south India to offer ASBA facilities and It was one of the first banks in the banking industry to have online deposit opening through the TMB e-connect facility. These weren't headline-grabbing innovations, but they solved real problems for TMB's customers—small investors who wanted IPO access and busy entrepreneurs who couldn't visit branches during banking hours.

The foreign exchange business became an unexpected growth engine. TMB achieved a turnover of ₹15,726 crores in foreign exchange for the year ended March 2019. In terms of forex turnover, TMB ranks first among the Tamil Nadu-based private sector banks. This dominance came from understanding the needs of Tamil Nadu's export-oriented MSMEs—textile exporters in Tirupur, auto component manufacturers in Coimbatore, seafood processors in Thoothukudi. TMB didn't just process their transactions; it became their financial advisor on hedging, documentation, and compliance.

By 2010, TMB had crossed a net worth of Rs. 1000 Crores, achieved without diluting equity or seeking external capital. This organic growth, funded entirely through retained earnings, would become crucial when the time came for the IPO—TMB could negotiate from strength, not desperation.

V. The IPO Journey & Going Public (2021–2022)

The boardroom at TMB's Thoothukudi headquarters must have witnessed intense debates in early 2021. For a century, the bank had remained closely held, with employee unions and long-term investors controlling its destiny. Now, regulatory pressures and growth ambitions pushed toward an inevitable conclusion: going public. The Tamilnad Mercantile Bank filed a draft red herring prospectus with the Securities and Exchange Board of India on September 6, 2021 to raise funds through an initial public offering. The timing wasn't coincidental—Basel III capital requirements loomed, digital transformation demanded investment, and most critically, RBI had restricted new branch openings pending resolution of shareholding issues.

The shareholding structure revealed a unique complexity: TMB does not have any identifiable promoter, while 37.7% of the equity is under dispute at various forums such as RBI, ED etc. for the past 15 years. This wasn't just a governance headache—it was existential. Without clear ownership, TMB couldn't raise capital, couldn't expand aggressively, and risked being left behind in India's banking consolidation wave.

The IPO structure itself was telling: Tamilnad Mercantile Bank IPO comprised fresh issue of 1,58,27,495 shares priced at ₹500 to ₹525 per share, aiming to raise around ₹832 crores. Notably, retail allocation is 10% (and not 35%, as bank's monetary assets exceed 50% of net tangible assets), a regulatory quirk that limited retail participation but perhaps protected small investors from volatility.

The market's initial response was lukewarm. The Tamilnad Mercantile Bank IPO is subscribed 2.86 times by September 7, 2022—respectable but not spectacular. Retail category of Tamilnad Mercantile Bank IPO subscribed 6.48 times, showing strong interest from TMB's traditional customer base who understood the bank's value proposition better than institutional investors.

What the subscription numbers masked was the transformation happening behind the scenes. Going public forced TMB to professionalize in ways a century of private ownership hadn't required. Independent directors replaced community representatives. Quarterly earnings calls replaced annual gatherings. Algorithmic risk models supplemented relationship-based lending.

The IPO listing date of September 15, 2022 marked not an ending but a beginning. TMB's stock opened at a modest premium, then settled into a trading range that suggested the market hadn't fully grasped what it was valuing—not just a regional bank, but a century of trust, relationships, and prudent growth.

The post-IPO period revealed the strategic benefits of going public. Capital adequacy improved, enabling branch expansion after years of regulatory restrictions. Employee ownership through stock options aligned interests. Most importantly, public scrutiny forced operational improvements that private ownership might have delayed.

VI. Digital Transformation & Modern Banking

The 103rd Annual General Meeting in August 2025 opened with an unusual admission from management: "We were late to digital, but we're determined to lead the next wave." This candor, rare in Indian banking, signaled TMB's evolved approach to technology—not as a defensive necessity but as an offensive weapon. The numbers tell part of the story: TMB's ATM network of 1,150 machines, 754 branches with 47% in semi-urban areas, 16% in urban, 22% in rural, and 15% in metropolitan centers, and The digital and branch transactions increased by a CAGR of 47% in last 3 years. But the real transformation was philosophical—from viewing technology as infrastructure to seeing it as strategy.

The partnership with IppoPay announced in 2024 exemplified TMB's evolved approach. IppoPay, a FinTech player based in Chennai, announced its partnership with Tamilnad Mercantile Bank (TMB) to provide UPI QR-based payment solutions to small businesses in South India's underserved segments, particularly in Tamil Nadu. As part of this partnership, Techfini's UPI switch will be processing all UPI payments using the TMB handle. This wasn't TMB trying to compete with fintech—it was TMB becoming the banking infrastructure that enabled fintech to thrive.

The strategy revealed sophisticated understanding of TMB's strengths and limitations. Rather than building proprietary payment apps to compete with PhonePe or Paytm, TMB positioned itself as the reliable banking partner that fintechs needed. Techfini's UPI switch can process 10,000 transactions per second (TPS) and provides customisable solutions, eliminating technical declines, scalability issues, and downtime—capabilities that smaller fintechs couldn't build independently but desperately needed.

TMB's digital transformation extended beyond partnerships. The bank introduced features that seemed mundane but solved real problems for its core customers. The "Choose Your Account Number" facility allowed customers to select memorable account numbers—crucial for small businesses sharing account details with hundreds of vendors. Missed call banking for balance inquiries served customers with basic phones. These weren't headline innovations, but they demonstrated deep understanding of customer needs.

The mobile app evolution was particularly telling. Due to security enhancements, TMB MBank app (Android: v1.0.24, iOS: v1.9.0) only supports Android version 10 or above and iOS version 17 or above—a decision that might exclude some customers but prioritized security for the majority. This wasn't Silicon Valley's "move fast and break things" but banking's "move deliberately and protect everything."

Branch expansion continued even as digital adoption accelerated. 584th Branch at Kayarambedu (Chengalpattu Dist., Tamilnadu) and 585th Branch at Malleswaram (Bengaluru, Karnataka) have been opened on 30/06/2025. The parallel investment in physical and digital channels reflected TMB's understanding that in India, omnichannel isn't a buzzword—it's a necessity.

VII. Financial Performance & Business Model

The numbers that matter in banking aren't always the ones that make headlines. TMB's financials reveal a institution that prioritizes resilience over growth, margins over market share, and trust over transactions.

Start with the headline figures: Market Cap of ₹6,789 Crore, Revenue of ₹5,396 Cr, and Profit of ₹1,200 Cr. But the real story lies in the ratios. The level of advances which stood at ₹52 Lakhs in the year 1962 has spurted to above ₹44,366 Crores as on March 31, 2025—representing not just growth but a fundamental transformation in scale while maintaining conservative underwriting.

The asset quality metrics border on unbelievable for Indian banking: Gross NPA ratio at 1.25% and Net NPA ratio at 0.36% as of March 31, 2025. To put this in perspective, the industry average for private banks hovers around 2-3% net NPAs. TMB achieves this not through aggressive write-offs but through what one analyst called "grandmother banking"—knowing your customers, their businesses, and their families before lending.

The deposit franchise tells another story. Deposits at Rs 53,689 crore with advances at Rs 44,366 crore yields a conservative loan-to-deposit ratio around 82%. While aggressive banks push this ratio above 90% to maximize returns, TMB maintains a buffer that has proven invaluable during liquidity crunches. The CASA (current and savings account) ratio, though not disclosed in recent filings, has historically been strong, providing low-cost funding that supports margins.

The bank, which had a Net Profit of ₹6,984.00 in the year 1921 had spurted its profit to ₹5.05 Lakhs in the year 1971 and ₹1183.00 Crores for the year ended March 2025. The consistency is remarkable—profitable every year since inception, through wars, recessions, demonetization, and pandemics.

The dividend policy deserves special attention. Tamilnad Mercantile Bank Ltd., is the only bank in India declaring consistently higher rate of dividend to its shareholders from the very beginning. The bank had declared 6% dividend to its shareholders in 1921. The recent AGM approved ₹11 dividend per share, maintaining this tradition. For a bank trading at ₹85 per share, that's a dividend yield of 2.56%—attractive in a low-rate environment but signaling management's confidence in sustainable earnings.

Book value per share at ₹568.90 with face value of ₹10 creates an interesting dynamic. The stock trades at a Price to Book ratio of just 0.73 times—a significant discount that suggests either market skepticism or a value opportunity. For comparison, well-run private banks typically trade at 2-3 times book value.

The business model itself has three distinct pillars: Treasury operations, Corporate/Wholesale Banking, and Retail Banking. But unlike universal banks that treat these as separate profit centers, TMB integrates them around its core MSME franchise. Treasury manages liquidity for trade finance. Corporate banking serves the larger suppliers and buyers of MSME clients. Retail banking captures employee accounts and owner families. It's an ecosystem approach before "ecosystem" became a buzzword.

The efficiency metrics reveal operational discipline. With Net profit rose 15.35% to Rs 291.90 crore in Q4 March 2025 against modest top-line growth, TMB is clearly focusing on productivity over expansion. The cost-to-income ratio, while not explicitly stated, can be inferred from the margin between revenue and profit to be competitive with larger peers despite TMB's smaller scale.

What's missing from the numbers is equally telling. No massive treasury gains from betting on interest rates. No fee income surge from pushing insurance products. No rapid loan growth in trendy but risky segments like unsecured personal loans. TMB makes money the old-fashioned way—careful lending with healthy spreads.

VIII. Competitive Landscape & Strategic Positioning

In Indian banking's heavyweight division, TMB might seem like a welterweight fighter. But as any boxing fan knows, the smartest fighters don't always compete on size—they compete on speed, technique, and knowing exactly where to land their punches.

TMB operates in a unique competitive space—too large to be a small finance bank, too small to be a universal bank, too old to be a new-age bank, too modern to be just another old private sector bank. This positioning, which might seem like strategic confusion, is actually strategic clarity.

Consider the competitive set. Among old private sector banks, TMB competes with City Union Bank, Karur Vysya Bank, and Federal Bank—regional champions who've survived consolidation waves that claimed weaker players. Against these peers, TMB's performance stands out. Its net NPAs of 0.36% compare favorably to City Union's 2.9%, Karur Vysya's 2.3%, and Federal's 0.98%. Its RoA of 1.66% exceeds peers at 1.35%, 0.86%, and 0.91% respectively.

But the real competition isn't other old private banks—it's the new reality of Indian banking. HDFC Bank with its ₹24 lakh crore balance sheet operates in a different universe. Yet in TMB's core markets—textile exporters in Tirupur, match manufacturers in Sivakasi, spice traders in Thoothukudi—HDFC's size becomes a disadvantage. These clients need bankers who understand seasonal cash flows, family dynamics, and unwritten business customs. TMB's relationship managers, often from the same communities, speak the language—literally and figuratively.

The threat from small finance banks and payment banks initially seemed existential. Entities like Equitas and Ujjivan targeted the same MSME segment with venture capital backing and digital-first strategies. Yet TMB's response revealed strategic maturity. Instead of competing on their terms—technology and pricing—TMB competed on trust and completeness. A Sivakasi fireworks manufacturer might use Paytm for collections but relies on TMB for working capital, term loans, and trade finance. The payment banks got the transactions; TMB kept the relationship.

The company has delivered a poor sales growth of 8.83% over past five years—a metric that seems concerning until you realize it's deliberate. While peers chased growth through unsecured lending and geographic expansion, TMB chose profitable consolidation. The result: superior asset quality and margins that more than compensate for slower growth.

The regional concentration strategy deserves scrutiny. 47% of branches are located in semi-urban areas, 16% in urban, 22% in rural, and 15% in metropolitan centers. This distribution, weighted toward semi-urban areas, positions TMB perfectly for India's next growth phase. As manufacturing shifts from metros to smaller cities, as GST formalizes tier-2 economies, as digital infrastructure reaches rural areas, TMB's branch network becomes increasingly valuable.

The competitive moat isn't technology or scale—it's embedded knowledge. TMB understands the difference between a power loom unit in Erode and one in Surat. It knows why Sivakasi fireworks manufacturers need credit in January but not July. It recognizes that a provisional GST registration might be more valuable collateral than property papers in certain businesses. This tacit knowledge, accumulated over a century, can't be replicated by algorithms or acquired through mergers.

The partnership strategy with fintechs transforms potential competitors into channels. By providing banking infrastructure to companies like IppoPay, TMB gains transaction volume without customer acquisition costs. The fintech handles the user interface; TMB handles the regulatory compliance and balance sheet. It's symbiosis, not competition.

Looking forward, TMB's strategic options are intriguing. Geographic expansion beyond South India seems logical but risky—the embedded knowledge advantage diminishes with distance. Scaling up to compete with large private banks would require capital and cultural transformation that might destroy what makes TMB special. The most likely path: deepening dominance in existing markets while carefully entering adjacent geographies where Tamil business communities have established presence—Sri Lanka, Singapore, Malaysia.

IX. Playbook: Lessons from TMB's Journey

Every successful institution teaches lessons, but century-old banks teach different lessons than unicorn startups. TMB's playbook isn't about disruption—it's about evolution, patience, and the compound effect of good decisions made consistently over time.

Lesson 1: Community Foundation, Universal Ambition TMB's transformation from Nadar Bank to Tamilnad Mercantile Bank offers a masterclass in strategic evolution. The bank maintained its community roots—providing employment, supporting local businesses, understanding cultural nuances—while systematically removing limitations. The name change in 1962 wasn't abandonment but expansion. Today's entrepreneurs building ethnic or community-focused businesses can learn from this: start narrow to build trust, then gradually expand the aperture while maintaining core values.

Lesson 2: Technology as Tool, Not Master TMB became India's first fully computerized bank branch in 1984, yet it still maintains 754 physical branches in 2025. The lesson: technology amplifies strategy; it doesn't replace it. While fintech evangelists preach digital-only futures, TMB demonstrates that technology works best when it enhances human relationships rather than replacing them. The bank's UPI partnership strategy—enabling fintechs rather than competing with them—shows sophisticated understanding of where technology adds value versus where relationships matter.

Lesson 3: Employee Ownership as Competitive Advantage The unusual structure where employee unions hold significant shareholdings could have been a governance nightmare. Instead, TMB turned it into alignment. Employees who own shares think like owners—more careful with credit, more focused on long-term value, more invested in institutional success. The consistently low NPAs aren't just about credit policies; they're about loan officers who know their personal wealth depends on portfolio quality.

Lesson 4: Profitable Growth Over Growth Poor sales growth of 8.83% over past five years would typically trigger panic in boardrooms and analyst calls. TMB treats it as strategy. By focusing on profitable relationships over asset accumulation, the bank maintains superior returns without the risks of aggressive expansion. The lesson for growth-obsessed startups: sometimes the best strategy is to grow slower than you could.

Lesson 5: Regulatory Compliance as Moat While peers fought regulations, TMB embraced them. Achieving Scheduled Bank status in 1935, early computerization, prompt IPO compliance—each regulatory milestone became competitive advantage. In India's heavily regulated banking sector, the ability to navigate compliance isn't overhead; it's a barrier to entry that protects incumbents from disruption.

Lesson 6: Crisis Management Through Conservatism TMB survived the 2008 financial crisis, 2016 demonetization, 2020 pandemic, and 2023's regional banking crisis in the US without significant distress. The recipe: conservative underwriting, diverse deposit base, limited exposure to trendy but risky segments. While aggressive banks capture headlines during booms, conservative banks capture market share during busts.

Lesson 7: The Power of Consistency TMB is the only bank in India declaring consistently higher rate of dividend to its shareholders from the very beginning. The bank had declared 6% dividend to its shareholders in 1921. This isn't just about shareholder returns—it's about institutional credibility. In a country where financial promises are often broken, TMB's century of consistent dividends builds trust that no marketing campaign could achieve.

Lesson 8: Geographic Focus as Strategy While peers pursued national footprints, TMB deepened regional dominance. The lesson: in businesses with local knowledge advantages, geographic focus beats geographic spread. TMB knows more about Tamil Nadu MSMEs than any national bank ever could. This deep, narrow expertise creates pricing power and relationship stickiness that broad, shallow presence cannot match.

Lesson 9: Cultural Translation TMB's ability to translate between traditional business practices and modern banking requirements creates unique value. The bank understands both the informal economy its clients operate in and the formal economy regulators demand. This translation capability—cultural, linguistic, financial—becomes increasingly valuable as India formalizes its economy.

Lesson 10: Patient Capital TMB's century-long journey demonstrates the power of patient capital. The bank didn't pursue quick exits, aggressive leverage, or risky bets to juice returns. Instead, it compound steady returns over decades. In an era of quarterly capitalism, TMB's century-thinking provides a different model—one where wealth creation happens through generations, not quarters.

X. Analysis & Investment Case

The investment case for TMB presents a fascinating paradox: a bank with fortress-like fundamentals trading at distressed valuations. With a P/E ratio of 5.66 and Price to Book at 0.73 times, the market prices TMB as if it's either hiding problems or facing obsolescence. The evidence suggests neither.

The Bear Case: Why the Discount Exists

The market's skepticism has identifiable sources. First, the growth trajectory: 8.83% sales growth over five years in a country growing at 7% GDP signals market share loss. Investors trained on HDFC Bank's 20% compound growth see TMB as stagnant. Second, the ownership complexity with 37.7% of equity under dispute creates uncertainty that markets despise. Third, geographic concentration in Tamil Nadu seems provincialin an era of national champions. Fourth, the employee union shareholding raises governance concerns about decision-making agility. Finally, poor analyst coverage means TMB operates below institutional radar—no coverage means no buyers.

The Bull Case: Hidden Value in Plain Sight

Yet each bear point has a counter-narrative. The slow growth is selective, not stagnant—TMB could grow faster by loosening credit standards but chooses not to. The ownership disputes, ongoing for 15 years, haven't impacted operations, suggesting resolution might be upside rather than necessity. Geographic concentration in India's manufacturing heartland positions TMB perfectly for industrial revival and China-plus-one strategies. Employee ownership aligns interests better than stock options—loan officers who own shares are careful with credit. The lack of coverage creates opportunity for investors willing to do primary research.

The valuation metrics tell a compelling story. At 0.73 times book value, you're buying ₹100 of shareholder equity for ₹73. With ROE at 14.0%, that equity compounds at attractive rates. The dividend yield of 2.56% provides income while you wait for revaluation. Compare this to peers: City Union trades at 1.8x book with inferior asset quality, Federal Bank at 1.2x with lower ROA. TMB's discount seems unjustified by fundamentals.

The Catalyst Path

Several catalysts could trigger revaluation. Resolution of ownership disputes would remove the primary overhang. RBI's repo rate cut by 50 basis points, with TMB reducing RLLR from 9.00% to 8.50%, should expand margins as the loan book reprices faster than deposits. Branch expansion post-IPO could accelerate growth without compromising quality. A strategic stake sale to a larger bank could crystallize value—TMB's clean assets and regional franchise would command premium valuations in M&A scenarios.

The macro environment favors TMB's positioning. India's formalization drive through GST pushes informal businesses into banking channels. Government's MSME focus through emergency credit lines and priority sector lending benefits specialized lenders. Tamil Nadu's industrial revival—from textiles to electronics manufacturing—creates credit demand in TMB's core markets. Rising rural incomes increase savings mobilization in TMB's semi-urban strongholds.

Risk Factors Beyond the Obvious

The sophisticated investor must consider non-obvious risks. Technology disruption might not come from fintechs but from CBDCs (Central Bank Digital Currencies) that could disintermediate deposit gathering. Climate change poses unique risks—TMB's coastal headquarters and client base face increasing weather volatility. Succession planning in a employee-owned structure might prove challenging as founding generation retires. Regional political changes could impact the Tamil Nadu-centric franchise more than diversified peers.

The Investment Approach

For fundamental investors, TMB represents a classic value situation—good business at cheap price with identifiable catalysts. The appropriate position sizing depends on risk tolerance for illiquidity and governance complexity. For income investors, the dividend consistency and yield offer bond-like returns with equity upside. For strategic buyers, TMB offers clean entry into South Indian MSME banking with established infrastructure.

The time horizon matters crucially. Short-term traders will find little to excite—low volumes, limited news flow, no momentum. But patient capital could see substantial revaluation as: governance clarifies post-IPO, digital investments bear fruit, Tamil Nadu's economy accelerates, and market discovers this hidden gem. A three-to-five year horizon seems appropriate for thesis validation.

XI. Epilogue & Future Outlook

As TMB enters its 104th year, the question isn't whether it will survive another century—institutions this resilient don't disappear—but what it will become. The next decade will likely determine whether TMB remains a regional champion or transforms into something larger.

The strategic crossroads ahead are clear. Digital transformation must accelerate without abandoning relationship banking. Geographic expansion beyond Tamil Nadu needs careful calibration—too fast risks asset quality, too slow risks relevance. The ownership structure needs resolution, but in a way that preserves employee alignment while improving governance. The balance sheet has room to leverage up, but credit discipline must be maintained. These aren't binary choices but delicate balances that will test leadership's judgment.

The macro tailwinds are favorable. India's demographic dividend, formalization drive, and manufacturing ambitions all play to TMB's strengths. The micro challenges are manageable. Technology gaps can be closed through partnerships, talent can be attracted post-IPO, brand awareness can be built gradually. The real question is ambition—does TMB want to remain a profitable niche player or become a regional powerhouse?

The M&A scenarios are intriguing. As consolidation continues in Indian banking, TMB's clean balance sheet and regional franchise make it an attractive target. A larger bank seeking South Indian presence could pay substantial premiums. Alternatively, TMB could be the acquirer, using its currency to buy stressed assets from weaker peers. The employee ownership structure complicates but doesn't prevent either scenario.

The technology roadmap will be crucial. TMB can't compete with big banks on technology spending, but it can be smarter about deployment. The partnership model with fintechs should expand beyond payments to lending, wealth management, and insurance. The branch network needs digital transformation—not closure but enhancement with technology that amplifies human capability rather than replacing it.

The sustainability agenda, barely discussed in TMB's communications, will become increasingly important. As climate risks intensify, TMB's coastal exposure needs proactive management. But there's opportunity too—financing renewable energy, supporting sustainable agriculture, enabling circular economy in textiles. TMB's community roots position it well to lead grassroots sustainability initiatives.

Looking ahead to 2030, several scenarios seem plausible. The base case: TMB continues steady growth, gradually expands beyond Tamil Nadu, maintains superior asset quality, and slowly rerates to peer valuations. The bull case: ownership resolution catalyzes transformation, digital investments pay off dramatically, Tamil Nadu becomes India's manufacturing hub, and TMB emerges as the definitive MSME bank trading at premium valuations. The bear case: technology disruption accelerates beyond TMB's adaptation capacity, regional concentration becomes liability as growth shifts elsewhere, and employee ownership prevents necessary restructuring.

The highest probability outcome lies between base and bull cases. TMB will likely remain independent, gradually modernize, selectively expand, and continue delivering steady returns to patient shareholders. The bank that opened with ₹21,010 in deposits in 1921 and now manages ₹53,689 crores has demonstrated remarkable adaptability without losing its essence. That's the real lesson of TMB—change is possible without betrayal of core values.

For students of business history, TMB offers rich lessons about longevity, community capitalism, and strategic patience. For investors, it presents an asymmetric opportunity—limited downside with substantial upside potential. For customers, it remains what it has always been—a trusted partner understanding local needs while providing global services.

As we conclude this analysis, it's worth remembering that TMB's story isn't just about banking—it's about institution building in a developing economy, about community advancement through financial inclusion, about the possibility of doing well by doing good. In an era of algorithmic trading and digital disruption, TMB reminds us that some things—trust, relationships, local knowledge—remain irreplaceable.

The next chapter of TMB's story remains unwritten. Will it be acquisition by a larger bank seeking regional presence? Will it be transformation into a national MSME lending champion? Will it be steady continuation of a proven model? Whatever the outcome, TMB has already achieved something remarkable—surviving and thriving for over a century while staying true to its founding mission of community service through banking excellence.

For those watching from outside, TMB offers lessons about patience in an impatient world. For those invested within, it offers returns both financial and philosophical. And for those served by it, TMB remains what T.V. Balagurusamy Nadar envisioned when he cut that ribbon in 1921—a bank of the people, by the people, for the people. In the end, perhaps that's the greatest return of all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube