KeyCorp (KeyBank): From Cleveland Roots to Continental Banking

I. Introduction & Episode Setup

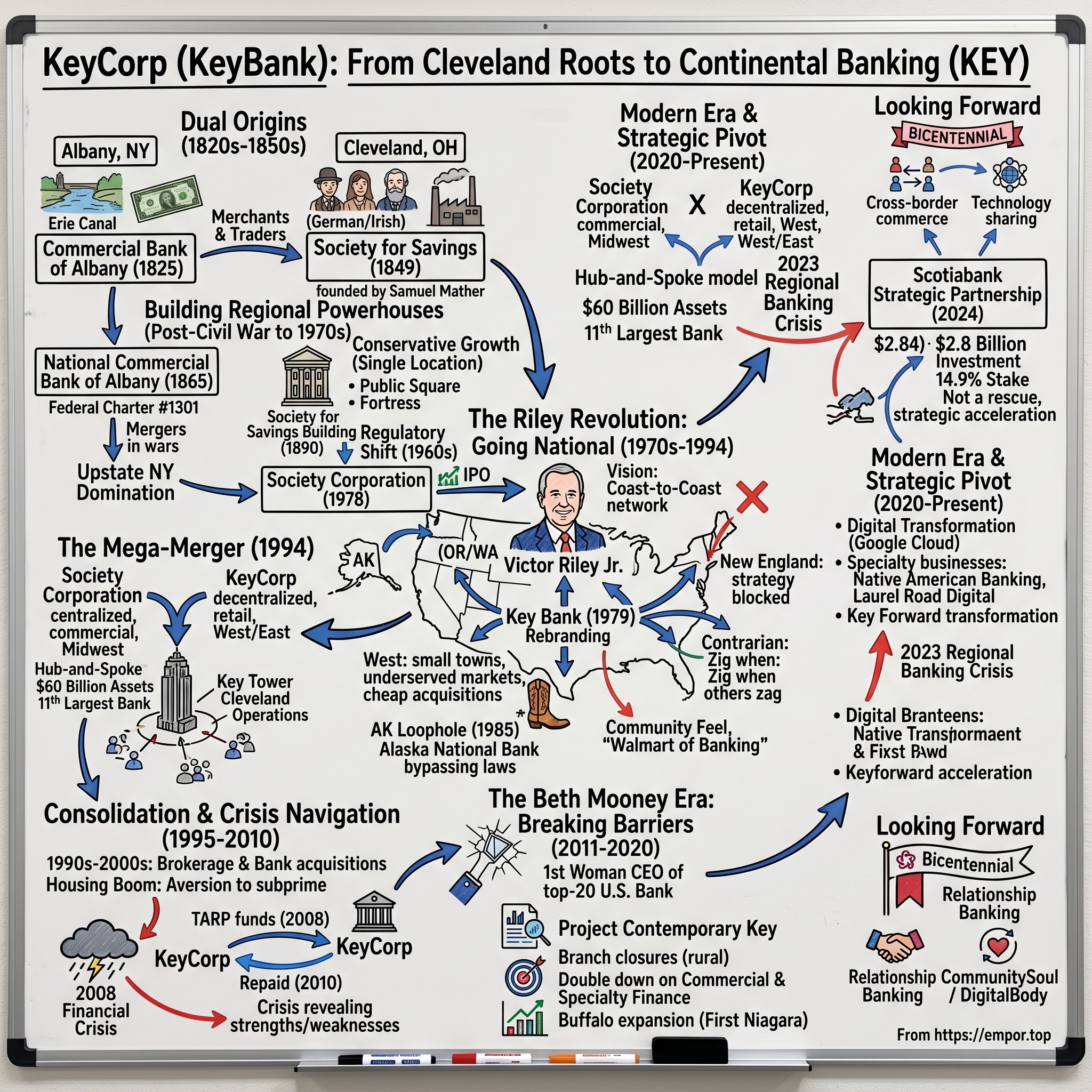

Picture this: It's March 1994, and two banking executives stand in a Cleveland boardroom, staring at a map of the United States dotted with hundreds of bank branches stretching from Maine to Alaska. Victor Riley Jr., the visionary from Albany who built KeyCorp into a western banking empire, and Robert Gillespie, the Cleveland native who transformed Society Corporation into Ohio's third-largest bank, are about to shake hands on one of the most geographically ambitious mergers in American banking history.

Fast forward to 2025, and KeyCorp celebrates its bicentennial—200 years since a group of Albany merchants pooled their capital to fund Erie Canal commerce. Today, with approximately $189 billion in assets, KeyBank operates one of the most uniquely distributed banking franchises in America, a sprawling network that defies the conventional wisdom of regional banking concentration.

The central question that drives this story isn't just how two 19th-century regional banks survived two centuries of panics, depressions, and technological disruption. It's how they created something that shouldn't exist according to banking orthodoxy: a super-regional bank that thrives in small Wyoming towns and Cleveland corporate boardrooms alike, that serves Native American communities in Alaska and tech entrepreneurs in Seattle, all while maintaining the folksy, community-bank feel that earned it the nickname "the Walmart of banking."

This is a tale of contrarian strategy, of zigging when others zagged. While competitors fought bloody pricing wars in saturated markets, Key quietly bought cheap banks in places others ignored. While mega-banks chased investment banking glory, Key doubled down on Main Street lending. And in 2024, when regional banking faced its greatest crisis of confidence since 2008, Key pulled off perhaps its most audacious move yet: convincing Canada's Scotiabank to invest $2.8 billion for a strategic minority stake.

Our journey spans from mutual savings societies helping immigrants save pennies in the 1840s to modern digital banking serving millions. We'll explore how a conservative Cleveland savings bank that operated from a single office for a century transformed into an acquisition machine, how an Albany banker's fascination with Asia-Pacific trade routes led to an Alaskan banking empire, and how the first woman to lead a top-20 U.S. bank navigated the treacherous post-crisis landscape to position Key for its third century.

But this isn't just a story of institutional evolution—it's about the people who saw opportunity where others saw obstacles, who understood that banking, at its core, is about serving communities, whether that community is dairy farmers in upstate New York or small businesses in Anchorage. As we trace Key's path from regional player to national presence, we'll discover how sometimes the best strategy isn't to be the biggest or the flashiest, but to be everywhere others aren't, serving customers others won't.

II. Dual Origins: Albany Commerce & Cleveland Society (1825–1849)

The year 1825 marked a transformative moment for American commerce. The Erie Canal was finally complete, creating a water highway from the Great Lakes to the Atlantic Ocean. In Albany, the eastern terminus of this engineering marvel, a group of merchants and traders recognized opportunity. They needed a financial institution to handle the explosive growth in trade that would surely follow. On April 15, 1825, New York Governor DeWitt Clinton—the same visionary who championed the canal—signed the charter for the Commercial Bank of Albany with an initial capital of $300,000.

The bank's founders weren't Wall Street financiers but local merchants who understood that Albany's strategic position would make it the gateway for goods flowing from the American frontier to eastern markets. They set up shop in a modest building on State Street, offering basic services: safekeeping of deposits, short-term loans for merchants, and critically, the issuance of bank notes that could facilitate trade along the canal route. Within its first year, Commercial Bank was financing everything from grain shipments to textile imports, establishing itself as the financial backbone of canal commerce.

Meanwhile, 450 miles west in Cleveland, a different kind of financial institution was taking shape, born not from commercial opportunity but from social necessity. The late 1840s brought waves of German and Irish immigrants to Cleveland's factories and docks. These workers, earning perhaps a dollar a day, had nowhere safe to keep their meager savings. Commercial banks of the era had no interest in small depositors—the administrative costs far exceeded any potential profit.

Enter Samuel H. Mather, scion of one of Cleveland's founding families and a man with a peculiar combination of Puritan ethics and progressive ideals. Mather had studied the mutual savings bank movement in New England, where institutions operated not for profit but for the benefit of depositors themselves. On February 23, 1849, Mather and 23 other prominent Clevelanders—including future president James A. Garfield's father—founded the Society for Savings.

The Society's early days were almost comically humble. Operating from a single room in the Merchants Bank Building, it was open just two hours each week—Saturday evenings from 6 to 8 PM, when workers received their pay. The first depositor was Jeremiah Breslin, an Irish laborer who entrusted his life savings of $3 to the institution. By year's end, the Society had attracted just 130 depositors with combined savings of $9,500—barely enough to cover operating expenses.

The Panic of 1857 nearly killed the young institution before it could mature. As banks across Ohio collapsed, depositors rushed to withdraw their savings. The Society's trustees, led by Mather, made a fateful decision: they would personally guarantee all deposits, putting their own fortunes on the line. Mather himself stood in the bank's lobby during the worst of the panic, calmly explaining to worried depositors that their money was safe. The gesture worked—not only did the Society survive, but it emerged with enhanced credibility. By 1859, deposits had grown to $90,000.

The Civil War transformed both institutions in unexpected ways. Commercial Bank of Albany became a crucial financial intermediary for Union war contracts, financing everything from uniform production to arms shipments. The volume of transactions flowing through Albany exploded, and by war's end, Commercial Bank had tripled its capital base.

For the Society for Savings, the war brought a different kind of growth. Cleveland's industries boomed with military contracts, wages rose, and suddenly even working-class families had money to save. The Society's deposits quadrupled during the war years. More importantly, the institution had proven its resilience and trustworthiness through national crisis.

Flush with post-war deposits, the Society made a bold statement about its permanence and ambitions. In 1867, it began construction of Cleveland's first skyscraper—a 10-story limestone and sandstone edifice on Public Square that would dominate the city's skyline for decades. The Society for Savings Building, completed in 1890, was more than just office space; it was a physical manifestation of the institution's role as guardian of the working class's wealth. The building's elaborate stonework and soaring interior spaces sent a message: your savings deserve the same grandeur as any millionaire's fortune.

By the Society's 1949 centennial, this conservative approach had created something remarkable. Still operating from that single Public Square location, never having opened a branch or pursued aggressive expansion, the Society held over $200 million in deposits from 140,000 customers—making it one of the largest mutual savings banks in America. The institution had survived the Panic of 1873, the Panic of 1893, the Great Depression, and two World Wars, never missing a dividend payment to depositors.

These parallel origin stories—one born from commercial ambition in Albany, the other from social mission in Cleveland—would define the DNA of the institution that would eventually become KeyCorp. The tension between aggressive expansion and conservative stability, between serving commerce and serving community, would play out again and again over the next century and a half. But first, each institution would need to navigate the profound changes that would transform American banking in the 20th century.

III. Parallel Evolution: Building Regional Powerhouses (1850s–1970s)

The end of the Civil War brought a fundamental restructuring of American banking. In 1865, the National Banking Act created a federal charter system designed to establish a uniform national currency and strengthen the federal government's financial position. For Commercial Bank of Albany, this presented both opportunity and challenge. The bank's leadership, recognizing that national charters would become the gold standard for commercial banking, reorganized under the new system, emerging as the National Commercial Bank of Albany with federal charter #1301.

This transformation was more than cosmetic. As a national bank, the institution could now issue national bank notes backed by U.S. Treasury securities, giving it a competitive advantage over state-chartered competitors. The bank's president, Erastus Corning Jr.—son of the railroad magnate—leveraged these new powers aggressively, expanding the bank's commercial lending throughout the Capital Region. By 1900, National Commercial had become the primary bank for the Delaware and Hudson Railway, the region's paper mills, and dozens of smaller manufacturers sprouting along the Hudson River.

Three hundred miles away in Syracuse, another piece of the future KeyCorp puzzle was taking shape. The Trust and Deposit Company of Onondaga, established in 1869, had carved out a unique niche serving the salt mining and chemical industries that dominated central New York. In 1919, recognizing the advantages of scale, Trust and Deposit merged with the First National Bank of Syracuse, creating an institution with the commercial lending power of a national bank and the fiduciary capabilities of a trust company.

The 1920s brought the first stirrings of what would become interstate banking. While federal law still prohibited banks from operating branches across state lines, creative lawyers found workarounds through holding company structures. But neither the Albany nor Syracuse institutions pursued such strategies—they remained focused on deepening their dominance in their home markets. This conservative approach proved prescient when the 1929 crash decimated banks that had overextended themselves in securities speculation.

Back in Cleveland, the Society for Savings maintained its almost monastic commitment to conservative growth. While other Cleveland banks opened branches throughout Cuyahoga County, the Society operated solely from its Public Square fortress. This wasn't stubbornness but strategy—the Society's trustees believed that a single, grand location reinforced the institution's stability and permanence in depositors' minds.

The Great Depression tested this philosophy severely. In March 1933, as banks across Ohio failed, Governor George White ordered a bank holiday. When banks were allowed to reopen, many Clevelanders discovered their institutions would never open again. The Society, however, reopened on schedule with full liquidity. The sight of the massive bronze doors of the Society Building swinging open that morning became a symbol of resilience for Depression-era Cleveland.

World War II transformed Cleveland into the "Arsenal of Democracy," and the Society's deposits swelled with defense workers' savings. But the real transformation came in the 1950s, as the post-war suburban boom finally forced the Society to reconsider its single-office strategy. The institution's new president, George Gund—later a famous philanthropist—recognized that Cleveland's population was fleeing to suburbs like Shaker Heights and Parma. If the Society didn't follow, newer, more aggressive competitors would capture this growing market.

The 1960s marked a watershed for both lineages. In Albany, a new generation of leadership recognized that the bank needed scale to compete with New York City giants that were increasingly encroaching on upstate markets. In 1971, First Trust and Deposit of Syracuse merged into National Commercial Bank and Trust Company, creating a $1.2 billion institution that dominated banking from Albany to Rochester.

The Society's transformation in the 1960s was even more dramatic. Under the leadership of George Baughman, the institution abandoned its century-old conservative approach and embarked on an aggressive regionalization strategy. Between 1960 and 1970, the Society acquired affiliate banks in Ohio, Indiana, Michigan, and even Florida. The mutual savings bank had transformed itself into a multi-state holding company, though still technically organized as a mutual owned by its depositors rather than shareholders.

The 1970s brought regulatory changes that would set the stage for the mega-mergers to come. The McFadden Act's restrictions on interstate banking were increasingly seen as anachronistic in an era of national corporations and electronic funds transfer. States began experimenting with regional banking compacts that allowed cross-border acquisitions within defined geographic areas.

In Cleveland, the Society faced a crucial decision. As a mutual savings bank, it couldn't access capital markets to fund expansion. In 1978, the institution converted to stock ownership, becoming Society Corporation. The initial public offering raised $78 million—capital that would fuel an acquisition spree throughout Ohio.

The 1986 merger with Centran Corporation represented the culmination of this strategy. Centran brought 51 branches and $2.1 billion in assets, making Society Ohio's third-largest bank holding company with $8.7 billion in total assets. But the most significant aspect of the merger was cultural—Centran had been an aggressive commercial lender, giving Society expertise in middle-market lending that complemented its retail banking strength.

By 1990, the two lineages that would soon merge had evolved into formidable regional powers. Society Corporation had grown from a single-office mutual savings bank into a $10 billion multi-state commercial banking operation. The Albany-based institution—soon to be renamed KeyCorp—had assembled a collection of banks across upstate New York with combined assets exceeding $3 billion.

Yet neither institution was prepared for the vision of one man who would transform not just these banks but the entire concept of regional banking in America. That man was Victor Riley Jr., and his strategy would redefine what it meant to be a "regional" bank. The conservative, locality-focused institutions of the past were about to become something entirely new: a coast-to-coast banking network that defied geographic logic but somehow worked.

IV. The Riley Revolution: Going National (1970s–1994)

Victor Riley Jr. didn't look like a banking revolutionary. Slight of build, soft-spoken, with wire-rimmed glasses that gave him a professorial air, Riley seemed more likely to quote poetry than hostile takeover statutes. Yet this unassuming Albany native would orchestrate one of the most audacious geographic expansions in American banking history, transforming a sleepy upstate New York bank into a coast-to-coast financial network that stretched from Maine to Alaska.

Riley joined National Commercial Bank in 1970 after a stint at Chase Manhattan, where he'd grown frustrated with big-bank bureaucracy. He rose quickly through the Albany institution's ranks, becoming president in 1971 at age 38. But it was his elevation to CEO in 1974 that marked the beginning of a radical transformation. Riley had spent years studying the patchwork of state and federal banking regulations, and where others saw insurmountable barriers, he saw a chess board waiting for the right sequence of moves.

His first masterstroke came in 1979 with a simple but profound rebranding. National Commercial Bank and Trust Company became Key Bank, N.A. The name wasn't chosen for its marketing appeal but for its versatility—short, memorable, and critically, without geographic association. While competitors proudly displayed their regional heritage (First National Bank of Syracuse, Society National Bank of Cleveland), Riley was already thinking beyond regional boundaries.

The early 1980s brought Riley's first major strategic setback, though it would prove instructive. He had identified New England as the logical expansion target—wealthy, adjacent to New York, with fragmented banking markets ripe for consolidation. Key Bank began acquiring small banks in Vermont and Maine, building what Riley called a "string of pearls" along the Eastern seaboard. But when Riley attempted to enter the lucrative Massachusetts and Connecticut markets, he discovered that these states' reciprocal banking laws specifically excluded New York banks—a protectionist measure aimed at keeping the New York City giants at bay.

Standing in his Albany office in 1983, staring at a map of the United States, Riley had what he later called his "Marco Polo moment." If he couldn't go east, why not go west—far west? Riley had been reading about the explosive growth in U.S.-Asia trade. California's ports were booming, Seattle was emerging as a Pacific gateway, and Alaska—Alaska was about to receive an influx of oil money that would transform its economy.

The strategy Riley developed was contrarian to the point of absurdity. While other super-regionals fought expensive battles for market share in saturated metropolitan areas, Key would buy small, cheap banks in underserved markets. "We're going where the competition isn't," Riley told his board. "Let the others fight over Philadelphia. We'll take Boise."

Between 1985 and 1990, Key Bank quintupled its assets from $3 billion to $15 billion through a series of acquisitions that read like a transcontinental road trip. Key bought banks in Wyoming ($180 million for First Wyoming Bancorp), Idaho ($43 million for Idaho First National), and Utah ($312 million for First Security Corporation's branch network). These weren't prestigious acquisitions—many of these banks served ranchers, small-town merchants, and mining companies. But they were profitable, undermanaged, and critically, cheap. Riley typically paid less than book value, a feat almost unheard of in the acquisition-frenzied 1980s.

The Alaska expansion of 1985-1986 showcased Riley's strategic genius. Alaska's banking laws were among the most liberal in the nation, allowing out-of-state banks to enter freely. Riley acquired Alaska National Bank of the North for $91 million, giving Key a foothold in a state awash with oil revenues. But the real masterstroke came next: Riley discovered that Alaska's interstate banking laws allowed Alaska-based banks to acquire institutions in other states. By using his new Alaska subsidiary as an acquisition vehicle, Riley could bypass the reciprocal banking restrictions that had blocked him elsewhere.

This "Alaska loophole" allowed Key to purchase Oregon banks that would have been off-limits to a New York-based institution. By 1987, Key had assembled a $2 billion franchise in the Pacific Northwest, all routed through its Anchorage subsidiary. Banking regulators were simultaneously impressed and alarmed—Riley was operating entirely within the law, but his creative interpretations were making a mockery of geographic banking restrictions.

Critics were savage. How could a bank headquartered in Albany possibly manage operations in Alaska? What did upstate New York bankers know about financing salmon fisheries or oil exploration? When oil prices crashed in 1986 and Alaska entered a severe recession, skeptics seemed vindicated. Key's Alaska operation posted losses of $47 million in 1987.

But Riley's response revealed the deeper strategy at work. He didn't panic or sell the Alaska franchise at fire-sale prices. Instead, he dispatched his best workout specialists to Anchorage, methodically working through problem loans while maintaining customer relationships. "Banking is banking," Riley told analysts. "A bad real estate loan in Anchorage isn't fundamentally different from a bad real estate loan in Albany. The key is having the patience and expertise to work through the problems."

By 1990, the Alaska operation had returned to profitability, and Riley's western expansion was vindicated. Key Bank had assembled a unique franchise—small-town and mid-market focused, geographically diversified in a way that provided natural hedges against regional economic downturns. When the Northeast entered recession in 1991, Key's western operations provided ballast. When the West struggled, the eastern franchise compensated.

The bank's culture reflected this geographic diversity in unusual ways. Key executives joked about needing multiple watches for different time zones. The annual managers' meeting became a logistical nightmare, with attendees flying in from Anchorage, Provo, and Portland. But this diversity also created unexpected strengths. Key developed expertise in industries most eastern banks ignored—mining, agriculture, Native American gaming. The bank became the largest lender to Native American tribes in Alaska, a relationship that required cultural sensitivity and long-term thinking but yielded deep customer loyalty.

Riley's management philosophy was as unconventional as his acquisition strategy. Rather than imposing rigid centralized control, he allowed acquired banks to maintain their local character and decision-making authority. "We're not conquistadors," he said. "We're partners. The bank president in Cheyenne knows his market better than anyone in Albany ever could." This decentralized approach reduced integration costs and maintained the community relationships that made these small banks valuable in the first place.

By 1993, Key had grown to $33 billion in assets with operations in 12 states. But Riley knew that the patchwork of banking regulations that had enabled his creative expansion was crumbling. The Riegle-Neal Act, which would allow true interstate banking, was moving through Congress. Soon, every major bank would be able to expand nationally. Key needed scale—real scale—to compete in this new environment.

That's when Riley received a call from Robert Gillespie in Cleveland. Society Corporation, Ohio's third-largest bank, was looking for a merger partner. The geographic fit was intriguing—Society's Midwest franchise would fill the gap between Key's eastern and western operations. But more importantly, Society had what Key lacked: a strong commercial banking operation, sophisticated technology infrastructure, and deep corporate relationships.

The negotiations that followed would create one of the most unlikely banking combinations in history: a decentralized, retail-focused, coast-to-coast network marrying a centralized, commercial-focused, Midwest powerhouse. It shouldn't have worked. But then again, nothing about Victor Riley's banking revolution had followed conventional wisdom. As 1994 dawned, the final pieces were falling into place for a merger that would create the first truly national super-regional bank.

V. The Mega-Merger: Society + KeyCorp = New KeyCorp (1994)

The Ritz-Carlton in Cleveland had seen its share of corporate drama, but the scene in the Presidential Suite on October 15, 1993, was unusual even by those standards. Victor Riley and Robert Gillespie sat across from each other at a mahogany table covered with maps, financial statements, and organization charts. Between them lay a single sheet of paper with a hand-drawn diagram showing how two banks with completely different cultures, strategies, and geographic footprints could become one.

"It's like merging the New York Yankees with the Green Bay Packers," Gillespie's CFO had warned him. Society Corporation was everything Key wasn't—centralized where Key was decentralized, urban-focused where Key was rural, commercial where Key was retail. Society ran its entire $30 billion operation from its Cleveland tower with military precision. Key's $33 billion was scattered across time zones, managed by local presidents who enjoyed remarkable autonomy.

But Gillespie saw what the skeptics missed. The banking world was consolidating rapidly. Chemical was buying Manufacturers Hanover. NationsBank was devouring everything in the Southeast. To survive as independents, both Society and Key needed scale, geographic diversity, and complementary capabilities. "We don't need to be alike," Gillespie told Riley. "We need to be complete."

The merger agreement, announced on January 10, 1994, sent shockwaves through the banking industry. The combined entity would have $60 billion in assets, making it the nation's 11th largest bank, with 1,300 branches in 18 states stretching from Maine to Alaska. The financial press struggled to even describe it—was it a super-regional? A proto-national bank? The American Banker called it "the oddest couple in banking."

The integration challenges were immense. Society's executives flew to Alaska in February 1994, experiencing firsthand the vast geographic span they were inheriting. The flight from Cleveland to Anchorage took longer than flying to London. In one memorable moment, a Society executive asked the Alaska team how they coordinated with Albany. "We don't," came the matter-of-fact reply. "Victor trusts us to run our business."

The cultural divide was equally vast. Society executives wore dark suits and worked in a gleaming modernist tower. Key's western bankers often showed up to meetings in bolo ties and cowboy boots. Society had invested millions in centralized technology systems. Key's various acquisitions ran on different core banking platforms, some dating to the 1970s. Society measured everything—daily P&L by product, hourly call center metrics. Key's rural branches sometimes didn't report results for weeks.

The decision of what to call the merged bank proved surprisingly contentious. Society had deeper roots and more prestige in corporate banking circles. But Key had a better geographic narrative and had spent years building a national brand. After weeks of debate, they chose to retain the Key name but use Society's Cleveland headquarters. The symbolism was deliberate—Key's vision and geographic reach combined with Society's operational excellence and corporate banking strength.

The merged bank's structure reflected this careful balance. The headquarters would be in Cleveland's Society Tower (quickly renamed Key Tower), but major operations would remain distributed. Commercial banking would run from Cleveland, retail from Albany, and the western operations would maintain regional headquarters in Seattle and Denver. It was a hub-and-spoke model that no other major bank had attempted.

March 1, 1994—merger completion day—brought unexpected drama. A late winter blizzard shut down Cleveland Hopkins Airport, preventing many out-of-town executives from attending the ceremonial first day. Riley, stuck in Albany, joined by videoconference—a fitting metaphor for the geographic challenges ahead. Meanwhile, computer systems that were supposed to integrate seamlessly crashed, leaving branches unable to access customer information for hours.

The leadership transition added another layer of complexity. Riley, at 61, had originally planned to remain CEO for three years to ensure smooth integration. But the stress of managing such a vast, disparate organization took its toll. By early 1995, he was spending 200 days a year traveling, trying to maintain personal connections with regional managers while also courting Wall Street analysts skeptical of the bank's unconventional structure.

In September 1995, Riley accelerated his retirement, handing the reins to Gillespie as CEO and chairman, with Henry Meyer—a Society veteran known for his operational expertise—as president and COO. Riley's departure marked the end of an era. The visionary who had imagined a coast-to-coast banking network was gone, replaced by operators who now had to make that vision actually work.

The immediate aftermath tested the new leadership. Key's stock price fell 15% in the six months following Riley's retirement as investors worried about integration execution. Several prominent commercial bankers left, uncomfortable with the decentralized culture. The Alaska operation, which Riley had personally championed, posted unexpected losses from failed fishing industry loans.

But Gillespie and Meyer gradually found their rhythm. They implemented what they called "coordinated autonomy"—local markets maintained decision-making authority for loans under $5 million, but larger credits required Cleveland approval. They standardized back-office operations while allowing front-office flexibility. Most cleverly, they used Society's technology infrastructure as a carrot rather than a stick, offering regional banks improved capabilities if they voluntarily adopted the standard systems.

The human dynamics of the merger played out in unexpected ways. Society's button-down corporate bankers learned to appreciate Key's entrepreneurial regional managers who had deep, decades-long community relationships. Key's rural bankers gained access to Society's sophisticated cash management and capital markets capabilities, allowing them to serve clients in ways they never could before.

One illustrative moment came during the 1995 annual managers meeting in Cleveland. A Key banker from Wyoming was explaining how he'd structured a complex financing for a cattle rancher, using derivatives to hedge feed costs. A Society executive expressed amazement that such sophisticated finance was happening in Cheyenne. The Wyoming banker smiled: "We may wear different boots, but we're all in the same business."

By the end of 1995, the merger was showing signs of success. The combined bank posted earnings of $935 million, exceeding analyst expectations. More importantly, customer retention remained strong—the feared mass defections hadn't materialized. The geographic diversity that skeptics had mocked was proving valuable as regional economic cycles offset each other.

The creation of the new KeyCorp represented more than just the combination of two banks. It was proof that American banking didn't have to follow a single model—that there was room for an institution that was simultaneously local and national, retail and commercial, centralized and decentralized. The merger had created something genuinely new in American finance: a super-regional bank that actually was super-regional, not just in scale but in scope.

As 1996 dawned, Gillespie stood in his office atop Key Tower, looking out at Lake Erie. The integration was far from complete, and challenges remained enormous. But the foundation was set. The unlikely marriage of Society and Key had created a platform that could compete with anyone—if they could hold it together. The next decade would test whether this unconventional structure could survive in an increasingly consolidated banking world.

VI. Consolidation & Crisis Navigation (1995–2010)

The late 1990s found KeyCorp at a crossroads. Robert Gillespie's vision extended beyond traditional banking—he imagined Key as a diversified financial services conglomerate that could compete with Citigroup and Bank of America in product breadth if not in scale. "The age of plain vanilla banking is over," he declared at the 1997 shareholders meeting. "Our customers want investment advice with their checking accounts, insurance with their mortgages, and sophisticated capital markets solutions for their businesses."

This transformation began with a 1997 acquisition that seemed minor at the time but would prove pivotal: McDonald Investments, a Cleveland-based brokerage and investment banking firm with $28 billion in assets under management. The $435 million purchase price raised eyebrows—it was Key's largest acquisition since the Society merger—but Gillespie saw it as the cornerstone of a new business model. Within 18 months, Key-branded investment centers appeared in 200 branches from Portland, Maine to Portland, Oregon.

The geographic expansion continued at a dizzying pace. Between 1998 and 2001, Key acquired 14 banks with combined assets of $7.8 billion, filling in gaps in its continental footprint. The acquisitions read like a geographic survey course: First National Bank of Evergreen (Colorado), Union Bankshares (Utah), Champion Bank (Colorado again), and memorably, Peoples Heritage Financial Group, which brought 239 branches across Maine, New Hampshire, and Massachusetts.

But the crown jewel came in 2001 with the $1.4 billion acquisition of Denver-based U.S. Bank's Colorado operations. This wasn't just about adding $3.6 billion in assets—it was about establishing Key as the dominant player in the Rocky Mountain region. The integration was flawless, a testament to the operational excellence that Henry Meyer had instilled. Customer attrition was less than 3%, and within a year, the Colorado franchise was exceeding its earnings targets.

The early 2000s also saw Key pushing into new business lines with mixed results. The bank launched Key Capital Partners, a private equity arm that invested in middle-market companies. Key Insurance was created to cross-sell property and casualty coverage to commercial clients. Key Equipment Finance became one of the largest lessors of construction equipment in North America. Each expansion made strategic sense in isolation, but collectively they stretched management attention and confused the bank's identity.

The housing boom of 2003-2007 presented Key with a defining choice. Competitors were diving headfirst into subprime mortgages, complex structured products, and aggressive real estate development loans. Key's board pressed management to boost returns by taking more risk. But CEO Henry Meyer, who had succeeded Gillespie in 2001, possessed an almost pathological aversion to credit losses. "I've seen too many banks die from bad real estate loans," he told the board. "We'll participate in the boom, but on our terms."

Those terms proved prescient. Key focused on traditional home equity lines of credit rather than subprime mortgages. The bank avoided the coastal markets where prices were soaring most dramatically, concentrating instead on the Midwest and Mountain West where valuations remained reasonable. Most critically, Key maintained strict underwriting standards even as competitors loosened theirs. The bank's loan officers joked darkly that they were losing every deal to more aggressive lenders, but Meyer held firm.

When the financial crisis struck in 2008, Key's conservative positioning initially seemed like genius. While Citigroup and Bank of America required massive bailouts, Key's losses were manageable. The bank's diverse geographic footprint helped—while Florida and California banks were collapsing, Key's Midwest and Mountain West markets experienced a gentler decline.

But Key wasn't immune to the crisis. The bank's commercial real estate portfolio, particularly in Michigan and Ohio, deteriorated rapidly as the automotive industry collapsed. Key's equipment financing business, which had seemed so promising, suddenly faced massive losses as construction ground to a halt. In the fourth quarter of 2008, Key posted a loss of $1.3 billion, its first quarterly loss since the 1994 merger.

The TARP (Troubled Asset Relief Program) decision tormented Meyer and the board. Key didn't need the capital to survive, but regulators strongly encouraged participation. On November 14, 2008, Key accepted $2.5 billion in TARP funds—money it would use not for survival but for opportunity. As smaller banks failed, Key quietly acquired their deposits and prime branches at fraction of book value. The bank picked up 37 former National City branches in choice locations, paying just $45 million.

The crisis revealed both Key's strengths and weaknesses. The geographic diversity that had been mocked in the 1990s proved invaluable—no single regional collapse could sink the bank. The conservative credit culture that had cost growth during the boom years preserved capital during the bust. But the crisis also exposed the complexity tax of Key's far-flung empire. Coordinating crisis response across 14 states and multiple business lines proved nearly impossible.

Meyer's response was radical simplification. Between 2009 and 2010, Key shed non-core businesses with ruthless efficiency. The private equity arm was sold to management. The indirect auto lending business was terminated. International operations were curtailed. Even some geographic markets were abandoned—Key sold its Wyoming franchise that Victor Riley had lovingly assembled, acknowledging that the state no longer fit the bank's strategic footprint.

The 2010 exit from TARP marked a turning point. Key repaid its $2.5 billion obligation plus $193 million in dividends, one of the first major regionals to fully exit government ownership. The symbolic importance was enormous—Key had survived the worst financial crisis since the Depression without requiring taxpayer support for survival.

But survival and thriving are different things. As 2010 ended, Key faced fundamental questions. The bank had $90 billion in assets but felt smaller, its stock price 70% below pre-crisis highs. Geographic diversity had become a burden as much as a benefit—the cost of maintaining branches from Alaska to Maine was crushing returns. Most troublingly, Key lacked a clear identity. It wasn't big enough to compete with the mega-banks in investment banking, but it was too complex to achieve the efficiency ratios of focused regionals.

The board's response was to look for new leadership, someone who could modernize Key for the post-crisis world while honoring its community banking heritage. They found their answer in an unlikely place: Key's own executive ranks, in a technology specialist named Beth Mooney who had quietly revolutionized the bank's retail operations. Her appointment would mark another historic first for Key and American banking—but first, she had to convince a skeptical board that a woman could lead one of America's largest banks through its most challenging period since the Great Depression.

VII. The Beth Mooney Era: Breaking Barriers (2011–2020)

Beth Mooney never intended to shatter glass ceilings. Growing up in Midland, Michigan, the daughter of a Dow Chemical engineer, she was more interested in systems and processes than symbolism. But on May 1, 2011, when she assumed the role of CEO at KeyCorp, she became the first woman to lead a top-20 U.S. bank—a distinction that would define her tenure whether she wanted it or not.

The boardroom had been skeptical when her name first surfaced. Not because she was a woman—at least, not explicitly—but because her background was unconventional. Mooney had joined Key in 2006 from AmSouth Bancorporation, where she'd run the retail banking division. At Key, she'd transformed the community banking operations through an obsessive focus on customer experience and operational efficiency. But she'd never run a commercial bank, never worked in capital markets, never managed through a credit cycle as CEO.

"I'm not here to be a symbol," Mooney told the board during her final interview. "I'm here because Key is dramatically underperforming its potential, and I know how to fix it." Her diagnosis was blunt: Key had become too complex, too expensive to operate, and too unclear about its value proposition. The bank was trying to be everything to everyone and succeeding at nothing.

Mooney's first hundred days established her leadership style—data-driven, decisive, and surprisingly ruthless when necessary. She initiated "Project Contemporary Key," a comprehensive review of every business line, every market, every major facility. Teams of analysts descended on branches from Bangor to Bellingham, measuring foot traffic, transaction volumes, and profitability per square foot.

The results were damning. Key operated 1,053 branches, but 400 of them were unprofitable. The bank maintained expensive operations in 14 states, but generated 70% of its earnings from just five. Most troublingly, Key's efficiency ratio—the percentage of revenue consumed by expenses—was 67%, far worse than the 55% achieved by top-performing regionals.

Mooney's response was surgical. Between 2011 and 2013, Key closed or sold 10% of its branch network, focusing cuts on rural markets that Riley had lovingly assembled but which no longer generated acceptable returns. The Alaska franchise, once Riley's crown jewel, was evaluated for sale (though ultimately retained after intensive restructuring). Even sacred cows weren't spared—Key sold its iconic Public Square branch in Cleveland, the very location where Society for Savings had operated since 1849.

But Mooney understood that cutting alone wouldn't restore Key's competitiveness. She needed growth engines, and she found them in unexpected places. Under her leadership, Key doubled down on two businesses that played to its strengths: middle-market commercial banking and specialty finance.

The commercial banking transformation was remarkable. Mooney poached top talent from J.P. Morgan and Wells Fargo, building specialized industry verticals in healthcare, energy, and technology. Key's commercial loan portfolio grew from $23 billion in 2011 to $48 billion by 2015, with margins expanding despite a low-rate environment. The secret was relationship depth—Key bankers were expected to provide not just loans but treasury services, investment banking, and wealth management to their clients.

The 2013 acquisition of mortgage servicing rights from Bank of America exemplified Mooney's strategic thinking. For $2.9 billion, Key acquired the servicing rights to 400,000 mortgages with $70 billion in unpaid principal. Critics called it risky—mortgage servicing was operationally complex and regulatory intensive. But Mooney saw opportunity. The acquisition immediately added $180 million to annual revenue while providing a natural hedge against rising interest rates.

The Buffalo expansion showcased Mooney's tactical brilliance. When First Niagara Financial Group announced it was acquiring HSBC's upstate New York branches in 2011, antitrust regulators required divestitures in certain markets. Key swooped in, acquiring 37 branches for just $110 million—a fraction of their replacement cost. Within two years, these branches were generating $50 million in annual profit.

But Mooney's masterstroke came in 2015 when she engineered the acquisition of First Niagara itself for $4.1 billion. This wasn't just another geographic expansion—it was a transformational deal that would strengthen Key's position in Upstate New York and New England while providing entry into Pennsylvania. The integration was flawless, with 94% customer retention and $400 million in cost synergies, exceeding all targets.

Throughout her tenure, Mooney maintained an unusual focus on social responsibility, particularly education. In 2011, she championed Key's partnership with "Say Yes to Education," a program guaranteeing college scholarships to students in Cleveland and Buffalo public schools. By 2019, Key had committed $100 million to the program, making it one of the largest corporate education initiatives in America.

"Banking is about more than returns on equity," Mooney explained at a 2016 conference. "We're stewards of communities. If Cleveland and Buffalo fail, we fail. It's that simple." This philosophy extended to Key's diversity initiatives. Under Mooney, the percentage of women in senior leadership roles rose from 19% to 35%. Key became the first major bank to achieve pay equity across gender and racial lines, a feat verified by independent audit.

The transformation showed in the numbers. Key's stock price rose 140% during Mooney's tenure, dramatically outperforming the KBW Bank Index. Return on equity improved from 7.8% to 13.5%. The efficiency ratio fell from 67% to 58%. By 2019, Key had become one of the most profitable regional banks in America, with earnings exceeding $1.8 billion.

But Mooney's greatest achievement might have been cultural. She transformed Key from a sleepy, sprawling confederation of community banks into a focused, professionally managed financial institution. She proved that a woman could not only lead a major bank but could do so while delivering superior returns. When Fortune named her one of the "Most Powerful Women in Banking" for the seventh consecutive year in 2019, it wasn't tokenism—it was recognition of genuine transformation.

As 2019 drew to a close, Mooney announced her plan to retire in May 2020, having agreed to stay on as Executive Chair to ensure smooth transition. Her chosen successor was Chris Gorman, a 30-year Key veteran who had run the corporate bank with distinction. The transition seemed seamless—until a global pandemic arrived to test everything Mooney had built.

Her final months as CEO, navigating COVID-19's initial impact, demonstrated the resilience of the institution she'd strengthened. Key processed more Paycheck Protection Program loans than banks twice its size, saving thousands of small businesses. The bank's technology investments allowed seamless remote work transitions. Most importantly, the strong capital position Mooney had built provided a buffer against whatever economic chaos lay ahead.

On May 1, 2020, exactly nine years after breaking banking's glass ceiling, Beth Mooney handed the CEO reins to Chris Gorman. She left behind a institution transformed—leaner, more profitable, more focused, and more inclusive. But she also left behind challenges: a low interest rate environment crushing margins, digital disruption threatening traditional banking, and economic uncertainty unlike anything since 2008. The question was whether Gorman could build on Mooney's foundation while navigating banking's next transformation.

VIII. Modern Era: Gorman's Leadership & Strategic Pivot (2020–Present)

Chris Gorman's first day as CEO of KeyCorp, May 1, 2020, was unlike any leadership transition in the bank's 195-year history. Instead of the traditional Town Hall meeting in Key Tower's auditorium, Gorman addressed 18,000 employees via Zoom from a makeshift studio in his suburban Cleveland home. Outside, the streets of downtown Cleveland were empty, businesses shuttered, the economy in freefall. The Federal Reserve had just slashed interest rates to near zero—a catastrophe for a bank that relied heavily on net interest margin.

"We're not just managing through a crisis," Gorman told his leadership team on a conference call that morning. "We're managing through three simultaneous crises—health, economic, and social. Our response will define Key for the next decade."

Gorman brought unique credentials to the role. A Harvard MBA who'd joined Key in 1990, he'd built the corporate banking division into a powerhouse, growing revenues from $800 million to $2.7 billion during his tenure as division head. But unlike previous Key CEOs who came from either retail or commercial banking, Gorman understood both sides of the house. He'd run retail banking in the Pacific Northwest, managed investment banking, even spent time in risk management. This breadth would prove invaluable.

The immediate challenge was existential: keeping the bank operational while protecting employees and customers. Within 72 hours of assuming control, Gorman had deployed 15,000 employees to work from home—a feat that would have been impossible without the technology investments Mooney had championed. Branch staff were equipped with plexiglass shields, masks, and strict sanitization protocols. Drive-through banking, an anachronism many thought would disappear, suddenly became essential.

But Gorman's defining moment came with the Paycheck Protection Program. When the Small Business Administration launched PPP in April 2020, the program's systems immediately crashed under volume. Large banks prioritized their biggest clients. Many community banks lacked the technology to process applications efficiently. Gorman saw opportunity in chaos.

He personally led daily 6 AM war room meetings, deploying 1,000 employees to process PPP applications. Key built a digital portal in 72 hours that could handle applications from any small business, not just existing customers. When competitors' systems failed, Key's remained operational. The bank ultimately processed 35,000 PPP loans totaling $7.8 billion, saving an estimated 750,000 jobs. More importantly, 60% of these loans went to new-to-bank customers, creating relationships that would prove valuable post-pandemic.

The social justice protests following George Floyd's murder in May 2020 presented another leadership test. While some bank CEOs issued carefully wordsmithed statements, Gorman took concrete action. Key committed $40 billion over five years to affordable housing and small business lending in low-to-moderate income communities. The bank created a $5 million social justice fund, supporting organizations fighting systemic racism. Gorman personally joined protest marches in Cleveland, images that ricocheted through social media.

"Banking has historically been part of the problem when it comes to racial inequality," Gorman acknowledged in a candid interview. "We can't undo the past, but we can sure as hell change the future."

As the acute phase of the pandemic passed, Gorman faced the strategic challenges that had been temporarily overshadowed. Key's stock had fallen 40% in early 2020. Net interest margin had compressed to historic lows. Credit losses, while manageable, were mounting. Most troublingly, digital-native competitors were eroding Key's customer base, particularly among millennials and Gen Z.

Gorman's strategic response crystallized in what he called "Key Forward," a comprehensive transformation announced in October 2021. The plan had three pillars: accelerate digital transformation, expand fee-based businesses, and achieve best-in-class efficiency. The goals were ambitious—reduce the efficiency ratio to 54%, increase fee income to 45% of total revenue, and achieve top-quartile digital adoption rates.

The digital transformation was radical. Key partnered with Google Cloud to rebuild its core banking platform, a $1 billion investment that would take five years to complete. The bank launched Laurel Road Digital Banking, a fully online platform targeting young professionals with student loan refinancing and mortgages. By 2023, Laurel Road had originated $7 billion in loans with zero physical branches.

The fee business expansion leveraged Key's commercial banking relationships. The bank built out its investment banking capabilities, hiring teams from larger competitors. Key's commercial payments business was expanded nationally, processing $1.8 trillion in annual volume by 2023. The wealth management division was reorganized to serve not just retail customers but the owners and executives of Key's commercial clients.

But the real breakthrough came in an unexpected area: Native American banking. Key had quietly served tribal communities since the 1990s, but Gorman elevated this to a strategic priority. The bank created dedicated Native American Financial Services teams, offering specialized treasury management for gaming operations and sovereign wealth funds. By 2024, Key managed over $15 billion in tribal assets, making it the largest non-Native bank serving these communities.

The financial results through 2023 were mixed but trending positive. Revenue in 2023 reached $6.21 billion, with fee income growing to 42% of total. The efficiency ratio improved to 61%, still short of target but moving in the right direction. Most encouragingly, digital adoption soared—78% of transactions were now digital, up from 45% in 2020.

Then came 2024, a year that would test every aspect of Gorman's leadership. The year began disastrously with revenue falling to $4.39 billion, the bank posting a net loss of $279 million in the fourth quarter. The regional banking crisis of 2023, triggered by Silicon Valley Bank's collapse, had created a crisis of confidence. Deposit outflows accelerated as customers moved funds to larger banks perceived as "too big to fail."

But Gorman had been preparing for this moment. In August 2024, he unveiled a transaction that stunned the banking world: Scotiabank would invest $2.8 billion for a 14.9% stake in KeyCorp. This wasn't a rescue—Key didn't need capital to survive. It was a strategic partnership that would provide Key with not just capital but access to Scotiabank's international expertise and Canadian market knowledge.

"This isn't about survival," Gorman explained to skeptical analysts. "It's about acceleration. With Scotia as a partner, we can pursue opportunities that would have been impossible alone."

The partnership's structure was clever. Scotiabank's investment came at $17.17 per share, a premium to market price, signaling confidence. The Canadian bank would get two board seats but wouldn't control Key. Most intriguingly, the partnership included commercial agreements that would allow Key to serve Canadian companies expanding into the U.S. and vice versa.

By the fourth quarter of 2024, green shoots were visible. Adjusted net income reached $378 million. Net interest income grew 10% quarter-over-quarter as the Fed's rate cuts paradoxically helped Key by steepening the yield curve. Client deposits grew 4%, reversing the outflow trend. The commercial loan pipeline was the strongest in five years.

As 2025 began, Gorman stood where Beth Mooney had once stood, looking out from Key Tower at Lake Erie. But his view was different—not just of the lake, but of banking itself. The industry was transforming from a business of branches and loans to one of technology and relationships. Regional banks were consolidating or failing. Digital natives were unbundling traditional banking services.

Yet Gorman remained optimistic. Key had survived 200 years of change—from canal financing to cryptocurrency. It had transformed from a mutual savings society to a super-regional bank to whatever it was becoming now. The Scotiabank partnership provided capital and strategic flexibility. The digital investments were beginning to pay off. Most importantly, Key's fundamental strength—deep, multi-generational relationships with middle-market companies and communities—remained intact.

"Banking is still about trust," Gorman reflected in a recent interview. "Technology changes how we deliver that trust, but it doesn't change the fundamental need. As long as businesses need capital and individuals need financial security, there will be a role for institutions like Key. Our job is to ensure we're delivering that trust in whatever form our customers need—whether that's a branch in Buffalo or an API in the cloud."

IX. The Scotiabank Partnership: A New Chapter (2024)

The conference room on the 47th floor of Key Tower had witnessed many pivotal moments, but the gathering on August 11, 2024, felt different. Chris Gorman sat across from Brian Porter, CEO of Scotiabank, as their teams finalized details of a transaction that would fundamentally reshape Key's trajectory. Outside, a summer storm rolled across Lake Erie, lightning illuminating the Cleveland skyline—an apt metaphor for the electric atmosphere in the room.

"This isn't a bailout," Gorman had insisted to his board when first proposing the partnership. "It's a strategic acceleration." The numbers told a complex story. Key's stock had fallen 30% year-to-date, victims of the regional banking crisis contagion despite the bank's fundamental soundness. The market was pricing in disaster scenarios that Gorman knew were unfounded, but perception had become reality. Key needed something dramatic to change the narrative.

The genesis of the partnership traced back to a chance encounter at the World Economic Forum in Davos six months earlier. Gorman and Porter found themselves seated together at a dinner discussing cross-border commerce. Porter mentioned Scotiabank's struggle to serve Canadian companies expanding into the U.S. Gorman described Key's mirror challenge with American firms entering Canada. By dessert, they were sketching deal structures on napkins.

What followed were six months of secret negotiations, code-named "Project Maple." The complexity was staggering—two banks, two regulatory regimes, countless stakeholders. Scotiabank wanted meaningful influence without triggering U.S. bank holding company regulations. Key needed capital and credibility without sacrificing independence. The solution they crafted was elegant in its sophistication.

Scotiabank would invest $2.8 billion at $17.17 per share—a 17% premium to Key's market price—acquiring 14.9% ownership, just below the 15% threshold that would trigger enhanced regulatory scrutiny. The investment would come in two tranches: $800 million immediately, $2 billion pending Federal Reserve approval. Scotiabank would get two board seats and specific commercial agreements, but Key would maintain full operational independence.

The August 12 announcement sent shockwaves through the banking world. Analysts who had been predicting Key's demise suddenly revised their models. The stock jumped 15% in minutes. But the real story wasn't the capital—it was what the partnership represented.

"This is the future of regional banking," declared Mike Mayo, the influential Wells Fargo analyst. "Not consolidation for consolidation's sake, but strategic partnerships that create value without destroying independence."

The strategic logic was compelling. Scotiabank, Canada's third-largest bank with extensive operations in Latin America and the Caribbean, needed better access to U.S. commercial markets. Key, despite its coast-to-coast presence, lacked international capabilities increasingly demanded by middle-market clients. Together, they could offer something neither could alone—seamless North American coverage with selective global reach.

The commercial agreements embedded in the deal were where the real value lay. Key would become Scotiabank's preferred partner for Canadian companies operating in the U.S., immediately adding 3,000 potential clients to Key's prospect pipeline. Scotiabank would refer U.S. companies expanding to Canada to its own commercial teams, but Key would maintain the U.S. relationship and share in fees. The banks would jointly develop technology platforms, sharing the $2 billion cost of digital transformation.

Inside Key, the partnership sparked intense debate. Some veterans saw it as an admission of weakness, a step toward eventual takeover. "Victor Riley would be rolling in his grave," one longtime executive muttered, referencing Key's founder-like figure who had championed fierce independence. Others worried about cultural clash—Canadian banking was notoriously conservative, even more so than U.S. regional banking.

Gorman addressed these concerns head-on in a company-wide videoconference. "This isn't about giving up who we are," he insisted. "It's about becoming who we need to be. The days of going it alone in banking are over. Scale matters, technology matters, and international connectivity matters. We can either partner strategically or be acquired entirely. I know which I prefer."

The regulatory approval process proved surprisingly smooth. The Federal Reserve, traumatized by the regional banking crisis, saw merit in a stable foreign investor providing capital without creating additional systemic risk. The December 12 approval came with minimal conditions—Scotiabank couldn't increase its stake beyond 14.9% without additional approval, and Key had to maintain specific capital ratios.

The December 27 closing ceremony was deliberately low-key. No champagne toasts or ribbon cuttings—Gorman insisted the focus remain on execution, not celebration. But privately, he allowed himself a moment of satisfaction. Key's capital ratios had jumped to among the strongest in regional banking. The stock had recovered to pre-crisis levels. Most importantly, the partnership had given Key strategic options it hadn't possessed in decades.

The integration began immediately. Joint working groups formed to identify commercial opportunities. Technology teams started mapping system integrations. Risk managers began harmonizing credit policies. By January 2025, the first joint client wins were announced—a Canadian pharmaceutical company expanding into Ohio, an American manufacturer entering Toronto markets.

But the partnership's most intriguing aspect was what it suggested about banking's future. Traditional M&A—where one bank swallows another—was becoming increasingly difficult due to regulatory constraints and integration challenges. Strategic minority investments offered an alternative: meaningful collaboration without full combination, shared capabilities without surrendered independence.

"We're pioneering a new model," Brian Porter explained in a rare joint interview with Gorman. "Not every problem needs an acquisition solution. Sometimes, partnership is more powerful than purchase."

The financial impact was immediate and substantial. Key's fourth-quarter 2024 results, released weeks after the partnership closed, showed the beginning of transformation. The bank's CET1 ratio reached 11.5%, among the highest in regional banking. The stock price had recovered to $18.50, validating Scotiabank's investment thesis. Most encouragingly, commercial loan originations were up 25% as clients responded positively to the enhanced capabilities.

Yet challenges remained. Some investors worried that Scotiabank would eventually demand full control, turning the partnership into a slow-motion acquisition. Others questioned whether two banks with different systems, cultures, and regulators could truly collaborate effectively. The technology integration alone would take years and cost billions.

Gorman remained philosophical about these concerns. "Every strategic decision carries risk," he acknowledged. "But the greater risk would be standing still. The regional banking model of the 20th century is dead. We're building the model for the 21st."

As winter settled over Cleveland, the partnership's early returns were promising. Joint commercial wins exceeded targets. Technology collaboration was yielding unexpected benefits—Scotiabank's superior mobile banking platform would be adapted for Key's retail customers. Cross-training programs were building cultural bridges. Most surprisingly, employee morale at Key had improved, the partnership seen as a vote of confidence rather than admission of weakness.

The partnership also opened intriguing future possibilities. If successful, could Key partner with other international banks for specific capabilities? Could the model be expanded beyond commercial banking into wealth management or capital markets? Could Key become the U.S. platform for multiple international banks seeking American exposure without regulatory burden?

"We're not just transforming Key," Gorman mused in a recent strategy session. "We might be transforming regional banking itself. The idea that you need to be enormous to be successful is being challenged. You need to be connected, you need to be capable, but you don't necessarily need to be colossal."

X. Business Model & Strategic Positioning

The nickname had followed KeyBank for decades, sometimes dismissively, sometimes affectionately: "The Walmart of Banking." Like the retail giant, Key had built its franchise by serving markets others ignored—small towns in Wyoming, rural communities in Alaska, rust-belt cities in Ohio. But as Chris Gorman explained to investors at the 2024 Barclays conference, the comparison, while simplistic, captured something essential about Key's enduring strategy.

"We go where the business is, not where the glamour is," Gorman said. "While others fight over Manhattan, we're the biggest bank in Anchorage. While they chase tech unicorns in Silicon Valley, we're financing manufacturing in Michigan. It's not sexy, but it's profitable."

Key's business model, refined over decades but fundamentally unchanged since the Riley era, rests on geographic diversification that provides natural economic hedges. When oil prices collapse and Alaska suffers, Ohio manufacturing might be booming from lower energy costs. When the Rust Belt struggles, the Mountain West often thrives. This portfolio effect has allowed Key to maintain more stable earnings than peers concentrated in single regions.

The bank operates through two primary segments that reflect its dual heritage. The Consumer Bank, serving individuals and small businesses through 1,000 branches across 15 states, generates about 40% of revenues but provides the stable, low-cost deposit funding that powers the entire institution. The Commercial Bank, serving middle-market companies with revenues between $10 million and $2 billion, contributes 60% of revenues and drives most of the bank's growth.

Within Consumer Banking, Key has carved out distinctive niches. The bank's relationship with Native American communities, particularly in Alaska and the Pacific Northwest, spans three decades. Key was the first major financial institution to create dedicated teams with cultural training to serve tribal communities. Today, the bank manages $15 billion in tribal assets, provides banking services to 180 tribal governments, and has funded over $3 billion in tribal economic development projects.

"It required patience and cultural sensitivity that most banks wouldn't invest," explained Sarah Johnston, who heads Key's Native American Financial Services. "You can't just parachute into tribal communities with standard products. You need to understand sovereignty issues, tribal law, unique cash flow patterns from gaming operations. It took us years to build trust, but now we have relationships that are essentially unassailable."

The Laurel Road digital banking platform, acquired in 2019 and expanded aggressively under Gorman, represents Key's attempt to solve the demographic challenge facing all traditional banks. Focused on medical and dental professionals with student loan refinancing and mortgages, Laurel Road has originated $9 billion in loans to 50,000 young professionals who might never set foot in a Key branch.

But it's the Commercial Bank where Key's strategy becomes most distinctive. Rather than competing with J.P. Morgan for Fortune 500 clients or with community banks for local small business, Key has dominated the middle market—companies large enough to need sophisticated financial services but small enough to value personal relationships.

The commercial strategy is built on seven industry verticals where Key has invested in specialized expertise: energy, real estate, healthcare, technology, consumer/retail, industrial, and institutionals. Each vertical has dedicated bankers who understand industry-specific challenges, from healthcare reimbursement complexities to energy price hedging.

"We'll never win the Facebook account," admitted Clark Khayat, who heads Key's technology vertical. "But we're the lead bank for dozens of B2B software companies with $50-$500 million in revenue. These companies need more than loans—they need treasury management for subscription revenues, foreign exchange for international customers, wealth management for founders. We provide the full suite with relationship consistency that mega-banks can't match."

Key's commercial payments business exemplifies this middle-market focus. The bank processes $1.8 trillion annually in payments, making it one of the largest non-money-center processors. But instead of chasing high-volume, low-margin consumer payments, Key focuses on complex B2B transactions—integrated payables, commercial card programs, electronic invoice presentment. These services are sticky, generate recurring fees, and deepen client relationships.

The investment banking and capital markets division, rebuilt under Mooney and expanded under Gorman, has found success by staying disciplined. Key will never compete with Goldman Sachs for mega-deals, but it's become a force in middle-market M&A, particularly in its core verticals. In 2024, Key advised on 127 transactions worth $18 billion—not huge by Wall Street standards, but highly profitable given lower cost structure.

The strategic fee-based businesses—wealth management, commercial payments, investment banking—now generate 42% of total revenues, up from 30% a decade ago. This transformation has been essential given persistent net interest margin compression. But unlike peers who bought fee businesses through expensive acquisitions, Key built most capabilities organically or through small, targeted purchases.

Key's approach to technology investment reflects its middle-market pragmatism. While peers spent billions building proprietary systems, Key has embraced partnerships. The Google Cloud partnership for core banking modernization, the FIS partnership for payments processing, the Black Knight partnership for mortgage technology—each allows Key to access cutting-edge capabilities without bearing full development costs.

"We're not trying to be a tech company," explained Amy Brady, Key's Chief Information Officer. "We're a relationship company that uses technology. The distinction matters. We invest where technology enhances relationships, not where it replaces them."

The efficiency initiatives under Gorman have been brutal but necessary. Key has closed 200 branches since 2020, reducing its footprint by 20%. But these weren't random cuts—sophisticated analytics identified branches where digital adoption made physical presence redundant. The savings have been redeployed into technology and talent, allowing Key to maintain its efficiency ratio at 61% despite revenue headwinds.

Risk management at Key reflects institutional memory of past crises. The bank maintains conservative underwriting standards that sometimes cost growth but ensure survival. Commercial real estate exposure is limited to 23% of total loans, below peer average. The securities portfolio is defensively positioned with limited duration risk. Credit loss provisions are consistently above peer averages—a drag on earnings in good times but crucial protection in downturns.

The geographic footprint that once seemed random now appears prescient. Key's presence in the Great Lakes region positions it for the industrial renaissance driven by reshoring manufacturing. The Mountain West franchise benefits from population migration and economic diversification. The Alaska operation, while small, provides outsized returns given limited competition. Even the scattered New England branches generate value through wealth management for aging populations.

Yet Key's business model faces structural challenges. The efficiency of digital-only competitors is hard to match with a thousand-branch network. The middle market Key dominates is increasingly served by alternative lenders offering speed and convenience traditional banks struggle to match. The fee businesses that provide diversification face their own disruption from fintech unbundling.

Gorman's response has been to double down on what Key does best while selectively modernizing. "We're not trying to out-fintech the fintechs," he explained. "We're trying to be the best relationship bank for middle-market companies and affluent individuals. That requires some branches, some bankers, some traditional infrastructure. But it also requires digital capabilities, data analytics, and partnerships we wouldn't have considered five years ago."

The Scotiabank partnership fits perfectly into this strategy. It provides Key with international capabilities its middle-market clients increasingly demand without the cost and complexity of building foreign operations. It offers technology cost-sharing that makes digital transformation affordable. Most importantly, it validates Key's relationship banking model—Scotiabank didn't invest for Key's technology or products but for its deep client relationships and market knowledge.

As Key enters its third century, its business model seems both anachronistic and prescient. In an era of digital everything, Key still believes in branches and bankers. In an age of global finance, Key focuses on local relationships. In a time of specialization, Key maintains broad geographic and business diversity. Whether this model can survive another decade of technological disruption remains uncertain. But for now, being the "Walmart of Banking"—serving everyone, everywhere, with everything they need—continues to work.

XI. Analysis & Investment Case

The investment case for KeyCorp in 2025 presents a fascinating study in contrarian value creation. After a tumultuous 2024 that saw the stock gyrate from crisis lows to partnership-driven highs, Key trades at compelling valuations that reflect neither its strategic transformation nor its improved capital position following the Scotiabank investment.

The Numbers Tell a Complex Story

Key's fourth quarter 2024 results encapsulated both the challenges and opportunities: a reported net loss of $279 million, or $0.28 per diluted share, but an adjusted net income of $378 million, or $0.38 per diluted share. This divergence between GAAP and adjusted earnings reflects one-time charges related to balance sheet repositioning—painful but necessary medicine for long-term health.

The underlying trends are more encouraging. Revenue increased 16% year-over-year, with net interest income rising 10% from the previous quarter. This acceleration is particularly impressive given the brutal net interest margin compression that plagued regional banks throughout 2024. Investment banking, payments, and wealth management fees surged 27% year-over-year, validating Gorman's strategy of diversifying beyond spread income.

Capital Strength: From Liability to Asset

The transformation in Key's capital position has been dramatic. The Common Equity Tier 1 ratio improved by 120 basis points to 12% quarter-over-quarter, placing Key among the best-capitalized regional banks in America. This isn't just regulatory box-checking—it's dry powder for growth. With peer banks struggling to maintain minimum ratios, Key can pursue selective acquisitions, increase dividends, or accelerate buybacks while others retrench.

Key's total assets stand at $187.2 billion with total equity of $18.2 billion, while total deposits are $149.8 billion against total loans of $102.9 billion. The loan-to-deposit ratio of 69% is conservative by industry standards, providing flexibility to increase lending as economic conditions improve without stretching funding.

Valuation: Priced for Disaster, Positioned for Recovery

At current levels around $15-17 per share, Key trades at historically depressed valuations. With the current price at $17.09 and book value per share of $14.48 for the quarter ending September 2024, Key's price-to-book ratio stands at 1.18. This is barely above tangible book value—a valuation typically reserved for banks in distress, not those with improving fundamentals and strategic partnerships.

The historical context is striking. During the past 13 years, Key's P/B ratio has ranged from a low of 0.57 to a high of 1.71, with a median of 1.22. The current valuation sits below the long-term median despite superior capital ratios, improved credit quality, and the strategic optionality provided by the Scotiabank partnership.

The Bull Case: Multiple Expansion Catalysts

Several factors could drive significant multiple expansion:

-

Rate Tailwinds Finally Arriving: After two years of net interest margin compression, the tide is turning. The steepening yield curve and stabilizing deposit costs created a 10% sequential increase in net interest income in Q4 2024. With $30 billion in fixed-rate assets repricing over the next 18 months at higher yields, margin expansion should accelerate.

-

Fee Business Momentum: Analysts forecast Key to grow earnings and revenue by 66.4% and 14.8% per annum respectively, with EPS expected to grow by 44.3% per annum. This explosive earnings growth reflects both easy comparisons to 2024's trough and genuine business momentum in fee-generating segments.

-

Strategic Optionality: The Scotiabank partnership provides options beyond capital. Joint technology development reduces costs. Cross-border referrals generate fee income. Most intriguingly, the partnership could evolve into deeper integration or attract other international partners seeking U.S. exposure without regulatory burden.

-

Credit Cycle Timing: Key maintains sufficient allowance for bad loans at 186% coverage, with bad loans at just 0.7% of total loans. This conservative positioning means Key has likely over-reserved relative to actual losses, creating potential for reserve releases that would boost earnings.

-

Geographic Diversification Premium: Key's presence in growing markets (Mountain West, Southeast) and stable markets (Midwest) provides natural hedges that single-market regionals lack. This diversification should command a premium, not the discount currently applied.

The Bear Case: Structural Headwinds Persist

Yet significant challenges remain:

-

Revenue Pressures: Despite recent improvement, Key's trailing twelve-month revenue of $4.24 billion produced losses of $304 million, or $0.32 per share. While 2024's results were impacted by one-time charges, the core revenue generation capability remains under pressure from digital competition and market saturation.

-

Efficiency Challenges: At 61%, Key's efficiency ratio remains well above the 54% target and peer best-in-class levels. The thousand-branch network is expensive to maintain, and closing branches risks customer attrition in relationship-dependent commercial banking.

-

Integration Execution Risk: The Scotiabank partnership's success depends on complex cross-border coordination. Technology integration, regulatory compliance, and cultural alignment present ongoing challenges that could derail projected synergies.

-

Market Structure Disadvantages: Key lacks the scale advantages of money-center banks and the simplicity benefits of focused regionals. This "stuck in the middle" positioning could become more problematic as industry consolidation continues.