Tube Investments of India: The Murugappa Group's Engineering Powerhouse

I. Introduction & Episode Roadmap

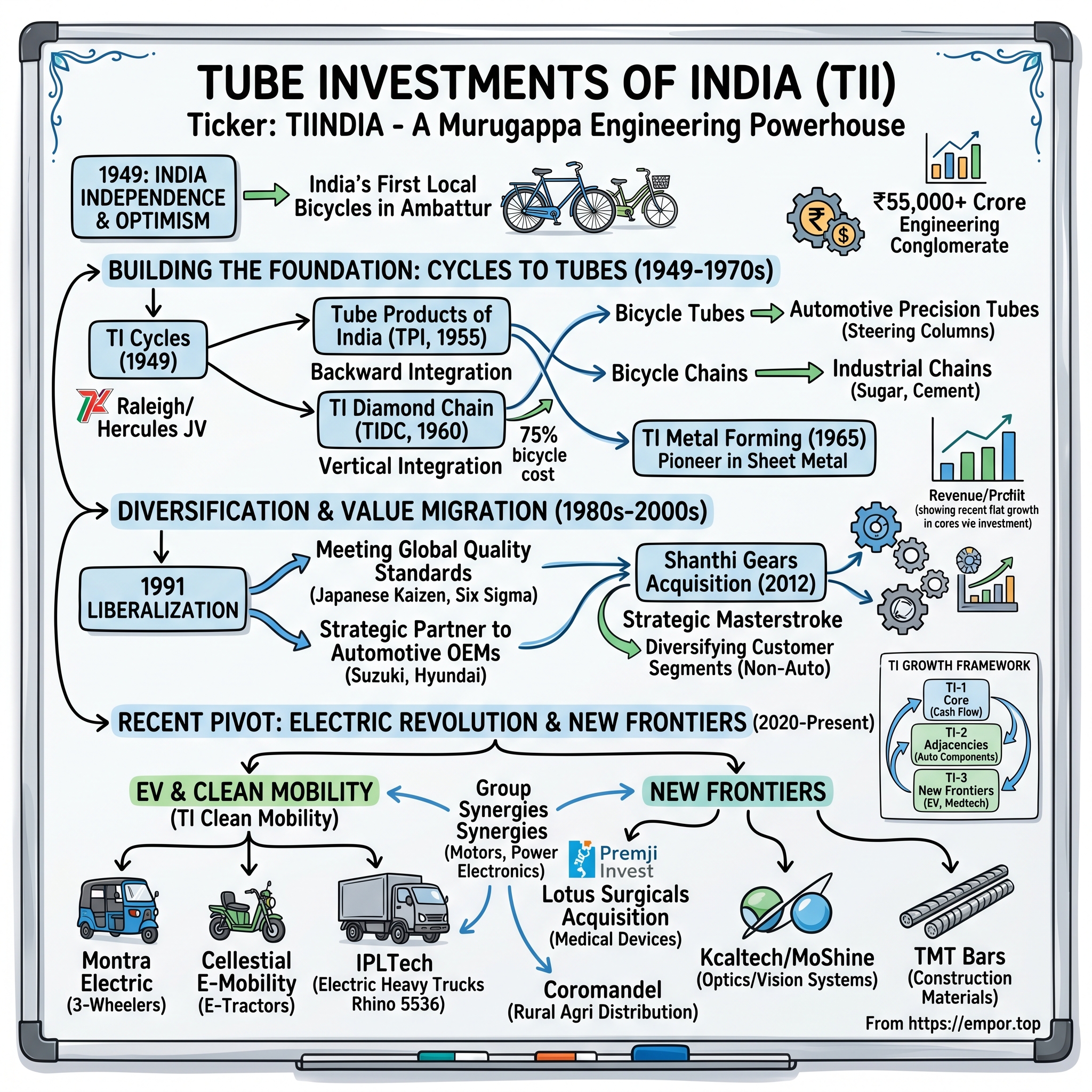

Picture this: It's 1949, and India has just gained independence. The streets of Chennai are filled with the optimism of a new nation, but also the practical challenges of building an industrial base from scratch. In a modest factory in Ambattur, a group of engineers and workers are assembling India's first locally-manufactured bicycles. They couldn't have imagined that this humble beginning would spawn a ₹55,000+ crore engineering conglomerate that would one day be at the forefront of India's electric vehicle revolution.

This is the story of Tube Investments of India Limited—TII to those who know it well—a company that embodies the classic conglomerate playbook of patient capital, strategic diversification, and relentless focus on engineering excellence. Today, TII operates across three main verticals: Engineering, Metal Formed Products, and Mobility, touching everything from the precision tubes in your car's steering column to the electric three-wheelers navigating India's congested streets.

The central question we're exploring isn't just how a bicycle company became a diversified engineering powerhouse—it's how TII managed to repeatedly reinvent itself at critical junctures, moving from cycles to automotive components, and now betting big on electric mobility and medical devices. It's a masterclass in industrial evolution, where each phase built deliberately on the last, creating what the Murugappa Group calls "adjacencies with synergies."

What makes TII particularly fascinating is its timing. At every major industrial transition in India—from import substitution to liberalization, from the automotive boom to the current EV revolution—TII has managed to position itself ahead of the curve. But this isn't a story of lucky bets. It's about methodical capability building, a distinctly Indian approach to technology absorption through joint ventures, and the patience that comes from being part of a 124-year-old business house.

As we journey through seven decades of TII's evolution, we'll uncover the strategic patterns that allowed a company to maintain uninterrupted dividend payments since 1954 while simultaneously making bold bets on emerging technologies. We'll explore how the Murugappa Group's unique governance structure—balancing family ownership with professional management—created an environment where long-term thinking could flourish even as quarterly pressures mounted.

The TII story also offers a window into India's manufacturing evolution itself. From the License Raj era when getting permission to expand bicycle production required government approval, to today's ambitious PLI schemes aimed at making India a global manufacturing hub, TII has been both a witness and a participant in this transformation. The company's journey mirrors India's own industrial aspirations—starting with basic manufacturing, moving up the value chain, and now competing globally in sophisticated engineering products.

II. The Murugappa Legacy & Founding Context

The year is 1900, and in the bustling ports of Burma, a young Tamil entrepreneur named A.M. Murugappa Chettiar is building what would become one of India's most enduring business empires. The Chettiars were traditionally money-lenders and traders, but Murugappa had grander ambitions. Starting with banking and money-lending operations in Moulmein (now Mawlamyine), he expanded across British Malaya, Ceylon, Dutch East Indies, and French Indo-China—essentially following the Tamil diaspora across Southeast Asia. The Murugappa story is also fundamentally about adaptation. In the 1930s the business was moved back to India, just ahead of the Japanese invasion of Burma during World War II—a prescient move that saved the family's wealth. But here's where it gets interesting: unlike many business families who would have continued in traditional trading and banking, the Murugappas made a bold decision. At that meeting a rather painful decision was taken to give up banking and go in for manufacturing in a big way.

Post-independence India in 1949 was a fascinating moment for industrial entrepreneurs. The British were leaving, creating both a vacuum and an opportunity. Foreign companies were looking for Indian partners to maintain their market presence, while the new Indian government was pushing for import substitution and self-reliance. It was in this context that TI Cycles of India Limited was established in collaboration with Tube Investments Limited, UK, the world's largest manufacturer of bicycles at the time.

Think about the symbolism of bicycles in 1949 India. This wasn't just about transportation—it was about democratizing mobility for a newly independent nation. While the elite had cars and the poor walked, the emerging middle class needed something in between. The bicycle represented progress, self-reliance, and modernity. It was the perfect product for a nation finding its economic feet.

After very quick and amicable negotiations with Tube Investments Ltd., UK – then the world's largest manufacturers of bicycles – the TI Cycles of India factory was established in 1949 itself at Ambattur, near Madras. The choice of partner was crucial. Tube Investments UK wasn't just any company—they owned Raleigh, BSA, and Hercules, some of the most prestigious bicycle brands in the world. This gave the Indian venture immediate access to world-class technology and brand equity.

But perhaps the most underappreciated aspect of the Murugappa philosophy was their approach to joint ventures. Unlike many Indian business houses who viewed foreign partnerships as necessary evils to be endured until they could go solo, the Murugappas saw them as learning opportunities. They absorbed technology, management practices, and quality standards that would become the foundation of their engineering excellence.

The family structure itself was unique. The Nagarathar or Nattukottai Chettiar community had centuries of experience in banking and trade across Southeast Asia. They brought with them not just capital, but sophisticated financial management systems. "The factor that prevented the nationalisation calamity from turning into a disaster for us was our financial accounting system, under which all collections made by the branches were required to be remitted to our head office at Madras". This centralized treasury management would later become a competitive advantage in managing a diversified conglomerate.

What's remarkable is how the group maintained its values across generations. When the International Institute of Management (IMD, Lausanne), a prestigious business school and non-profit foundation presented its Distinguished Family Business Award 2001 to the Murugappa Group in Rome, it became not only the first Indian company to win this recognition but also the first Asian one. This wasn't just about business success—it was recognition of their governance model that balanced family ownership with professional management.

The foundation laid in 1949 with TI Cycles wasn't just about manufacturing bicycles—it was about creating an industrial culture that could scale across sectors. The discipline of precision engineering, the obsession with quality, and the patient approach to capability building would all become hallmarks of the Murugappa way. As we'll see in the next section, these early lessons in manufacturing excellence would enable the company's systematic expansion into tubes, chains, and eventually, the entire automotive value chain.

III. Building the Foundation: Cycles to Tubes (1949–1970s)

The Ambattur factory in 1950 was a marvel of industrial ambition. Picture rows of workers—many who had never worked in a factory before—learning to weld frames, true wheels, and assemble India's first mass-produced bicycles. The British engineers from Tube Investments UK walked the shop floor, transferring not just technology but an entire manufacturing culture. Every measurement mattered. Every weld had to be perfect. This wasn't just about making bicycles; it was about proving that Indian manufacturing could match global standards. The genius of TII's backward integration strategy becomes clear when you understand the economics of bicycle manufacturing in the 1950s. Tube Products of India Ltd was established in 1955, in collaboration with Tube Products (Old Bury) Limited-UK, as a measure of backward integration with the bicycles plant. In 1959, Tube Investments of India (TII) was formed by merging TI Cycles of India and Tube Products of India. This wasn't just about cost savings—it was about controlling quality at every stage of production.

Consider what this meant in practical terms. A bicycle frame accounts for roughly 30-40% of the cost of a bicycle. By bringing tube manufacturing in-house, TII not only captured these margins but also gained the ability to innovate on frame design without depending on external suppliers. The 1955 establishment of Tube Products of India (TPI) transformed what could have been a simple assembly operation into genuine manufacturing capability.

TI Diamond Chain (TIDC), incorporated in 1960, in collaboration with a global company from the USA, was merged with Tube Investments of India Ltd in 2004. The chain represented another 15-20% of bicycle cost. By 1960, TII controlled the three most critical components of a bicycle: the frame, the chain, and the assembly. This vertical integration gave them pricing power that no competitor could match.

But here's what most analysts miss: Over a period of time these two businesses have moved up the value chain from bicycle parts to higher technology products. The tubes that started as bicycle frames became precision components for automotive steering columns. The chains that powered bicycles evolved into industrial chains for sugar mills and cement plants. Each backward integration move created a platform for forward diversification.

The manufacturing discipline instilled by the British partners was extraordinary. Today, TPI is the most preferred supplier of precision tubes, Electric Resistance Welded (ERW) and Cold Drawn Welded (CDW), to major automotive companies in India and abroad. TPI is India's undisputed market leader in CDW tubes for the Automotive industry. This didn't happen overnight—it was the result of decades of incremental capability building.

The numbers tell the story of market dominance. It has a manufacturing capacity of around three million bicycles per year. By the 1970s, TII's brands—BSA, Hercules, Phillips—had become household names across India. The company had effectively created the Indian bicycle market, defining what a quality bicycle meant to millions of Indians.

Established in 1965, TI Metal Forming is a pioneer and leader in precision value added sheet metal formed components. The establishment of TI Metal Forming in 1965 marked the beginning of TII's transition from consumer products to industrial components. This wasn't diversification for its own sake—it was a logical extension of their metallurgical expertise.

The strategic pattern that emerges is fascinating. Each new venture built on existing capabilities while opening doors to new markets. Bicycle tubes led to automotive tubes. Bicycle chains led to industrial chains. Sheet metal forming for bicycles led to precision components for cars. It's a textbook example of what strategists call "related diversification"—expanding into areas where your existing capabilities give you a competitive advantage.

What's particularly impressive is how TII managed this expansion while maintaining quality standards. In an era when "Made in India" often meant compromised quality, TII products commanded premium prices. Their Total Quality Management approach, adopted early and implemented rigorously, created a culture where quality wasn't negotiable.

The transformation from a bicycle company to a diversified engineering conglomerate was complete by the late 1970s. But this was just the foundation. As India's economy began to liberalize in the 1980s and 1990s, TII was perfectly positioned to capture the automotive boom that would follow.

IV. Diversification & Value Migration (1980s–2000s)

The year was 1991, and India was in crisis. Foreign exchange reserves had dwindled to barely three weeks of imports. The government was forced to airlift gold to London as collateral for emergency loans. But for companies like TII, crisis spelled opportunity. The liberalization that followed would transform India's automotive landscape—and TII was perfectly positioned to ride the wave.

As India began to liberalise its automobile market in 1991, a number of foreign firms also initiated joint ventures with existing Indian companies. The entry of Suzuki, Hyundai, Honda, and Toyota meant that suddenly, Indian component suppliers had to meet Japanese quality standards. For most, this was a terrifying prospect. For TII, with four decades of manufacturing excellence behind them, it was validation of everything they'd been building toward.

The transformation of TII during this period wasn't just about selling tubes and chains to new customers. It was about fundamentally reimagining what an auto component company could be. While competitors were content to be tier-2 or tier-3 suppliers, TII aimed to become a strategic partner to OEMs. They invested in co-design capabilities, set up dedicated R&D centers near customer plants, and most importantly, learned to speak the language of total cost optimization rather than just component pricing.

By 2000, there were 12 large automotive companies in the Indian market, most of them offshoots of global companies. Each brought different standards, different expectations, and different opportunities. TII's engineering teams became multilingual in manufacturing standards—they could work with Japanese kaizen, American Six Sigma, or European ISO standards with equal fluency.

The precision tubes business exemplifies this evolution. What started as simple bicycle frame tubes had evolved into CDW (Cold Drawn Welded) tubes with tolerances measured in microns. These weren't just tubes anymore—they were critical safety components in steering columns, airbag deployment systems, and fuel injection lines. A steering column failure could be catastrophic; TII's tubes had zero-defect requirements.

The chains business underwent a similar transformation. Industrial chains for sugar mills and cement plants require completely different engineering than bicycle chains. They operate under extreme loads, in harsh environments, with maintenance windows measured in years rather than months. TII didn't just manufacture these chains—they provided total lifecycle solutions, including predictive maintenance algorithms that could forecast chain wear based on operational parameters. The 2012 acquisition of Shanthi Gears for Rs 464 crore marked a pivotal moment in TII's evolution. Tube Investments of India, a Murugappa group company, acquired Shanthi Gears Ltd. in 2012. The acquisition by the Group's flagship company was aimed at diversifying its customer segments and getting stronger foothold on non-auto sector. This wasn't just another acquisition—it was a strategic masterstroke that would reshape TII's growth trajectory for the next decade.

P. Subramanian founded Shanthi Gears in the 1970s, which was acquired by Tube Investments of India Limited in 2012. The company got itself listed on the stock exchange in 1986 and became India's third-largest player in the gears industry. The acquisition brought TII something money couldn't easily buy: four decades of gear manufacturing expertise and relationships across industries from steel to textiles to cement.

What made the Shanthi Gears acquisition particularly shrewd was its financial profile. Shanthi Gears is a debt-free company with Rs.65-70 crore cash balance. Shanthi Gears is debt-free as on March 31, 2012. TII wasn't buying distressed assets; they were acquiring a profitable, well-managed company with untapped potential.

The strategic logic was compelling. L Ramkumar, managing director, stated: "Addition of Shanthi's product portfolio substantially enhances our ability to service other industry segments and reduce our reliance on the auto sector". At the time, the auto sector accounted for over 70% of TII's revenues. Shanthi Gears opened doors to wind turbines, steel mills, and power plants—sectors with different cycles and growth drivers.

The TQM (Total Quality Management) journey that TII embarked upon during this period deserves special attention. While Six Sigma and Lean Manufacturing were becoming buzzwords in Indian industry, TII went deeper. They didn't just implement quality systems; they created a quality culture. Every worker on the shop floor understood statistical process control. Suppliers were trained in TII's quality standards. Customer complaints weren't just addressed—they were analyzed for systemic improvements.

By the early 2000s, TII had transformed from a bicycle and tube manufacturer into a sophisticated engineering company. The metal forming division alone was producing car door frames, window and guide channels, impact beams, and hydro-formed parts—components that required precision engineering and metallurgical expertise far beyond what bicycle manufacturing had demanded.

The international expansion during this period was equally strategic. Rather than chasing volumes in commodity products, TII focused on high-value, engineered solutions. They weren't competing with Chinese manufacturers on price; they were competing with German and Japanese companies on quality and innovation. The acquisition of Sedis in France gave them access to European technology and markets, particularly in industrial chains where precision and reliability commanded premium prices.

The financial discipline throughout this diversification was remarkable. Despite multiple acquisitions and capacity expansions, TII maintained its record of uninterrupted dividend payments. This wasn't growth at any cost—it was calculated, profitable expansion that created value for all stakeholders.

As the 2000s drew to a close, TII had successfully navigated the transition from a domestic player to a global engineering company. But the biggest transformation was yet to come. The electric revolution was on the horizon, and TII was about to make its boldest bet yet.

V. The Electric Revolution: EV & Clean Mobility Pivot (2020–Present)

The scene is a boardroom in Chennai, February 2022. The Murugappa Group leadership is making what might be their most audacious bet in 122 years of business. India's electric vehicle market is nascent, infrastructure is non-existent, consumer acceptance uncertain. Yet here they are, committing hundreds of crores to a future that hasn't arrived yet. TI Clean Mobility Private Limited is a wholly owned subsidiary of Tube Investments of India Limited (Initially established as TI Cycles of India Limited, Madras), a Murugappa Group Company, effective from 12 February 2022.

This wasn't a tentative toe-dip into EVs. It was a full-scale assault across four platforms: three-wheelers, tractors, heavy commercial vehicles, and small commercial vehicles. The company will be infusing initial capital to the tune of Rs 350 crore into the new subsidiary for clean mobility, through a combination of equity, preference and debt instruments. By the time the dust settled, TII would commit over Rs 650 crore to electric mobility acquisitions alone.

The three-wheeler strategy came first with the Montra Electric brand. Branded as Montra, the TI Clean Mobility has three variants of three wheelers – soft top (price Rs 3.02 lakh), hard top (Rs 3.10 lakh) and long range (Rs 3.43 lakh). But this wasn't just about building electric rickshaws. TII understood that the three-wheeler market in India isn't just transportation—it's livelihood for millions. The economics had to work not just for the environment but for the driver who needed to make EMIs and feed his family.

The tractor acquisition was particularly bold. TICMPL acquired e-tractor company Cellestial E-Mobility in 2023. The 70 per cent stake was acquired for Rs 161 crore. Think about the audacity of electrifying tractors in a country where most farms don't have reliable electricity. But TII saw what others missed: tractors in India often spend hours idling during operations like threshing or pumping water—perfect use cases for electric powertrains.

Cellestial is a start-up company engaged in design and development of electric tractors. Post-acquisition, Cellestial will become a wholly-owned subsidiary of TICMPL. The founders, Siddhartha Durairajan and Syed Mubasheer Ali, weren't just engineers—they were visionaries who understood rural India's unique requirements. Their electric tractors weren't simply diesel tractors with batteries; they were reimagined from the ground up for Indian farming conditions.

The heavy commercial vehicle play through IPLTech was equally strategic. For Rs 246 crore, TI Clean Mobility will purchase a 65 percent stake in IPL Tech Electric. IPLTech manufactures 55T electric Trucks Rhino 5536. These weren't last-mile delivery vans but serious heavy-duty trucks designed for mining and port operations—controlled environments where electric vehicles could demonstrate clear TCO advantages.

The joint venture with Jayem Auto for small commercial vehicles completed the portfolio. TICMPL holding 80% stake gave them control while leveraging Jayem's expertise in vehicle development. This wasn't about competing with Tata Ace or Mahindra's small trucks on price—it was about creating a new category of urban delivery vehicles optimized for e-commerce and quick commerce applications.

What's remarkable about TII's EV strategy is its industrial logic. Unlike pure-play EV startups burning cash to capture market share, TII brought genuine manufacturing capabilities to the table. Their decades of experience in precision engineering, their relationships with automotive OEMs, their understanding of Indian market dynamics—all of these became competitive advantages in the EV space.

The synergies within the Murugappa Group became force multipliers. According to Paul, there are synergies that exist between the group's various companies and electric vehicle company TI Clean Mobility. For instance, the group company CG Power and Industrial Solutions makes big motors now. This wasn't just about shared services or procurement savings—it was about leveraging a century of engineering expertise across the group.

The target of 15-20% market share in all chosen EV segments by 2027-28 might seem aggressive, but TII has a track record of market dominance. They didn't become India's bicycle leader by being second-best. The same engineering excellence, quality obsession, and patient capital that built their traditional businesses are now being deployed in electric mobility.

The company sold 1,386 units of Super Auto in 2023. From Jan'24 to July'24, it sold ~3,224 units, securing 4th position among L5M EV OEMs. These numbers might seem modest, but remember: Tesla sold only 2,650 Roadsters in its first four years. The EV revolution isn't about immediate volumes—it's about being positioned for the inflection point.

The four-platform strategy also provides portfolio resilience. If passenger three-wheelers face regulatory challenges, commercial vehicles can compensate. If tractor adoption is slower than expected, heavy trucks in controlled environments can drive growth. This isn't putting all eggs in one basket—it's creating an EV ecosystem where learnings from one segment accelerate development in others.

As India pushes toward net-zero emissions and urban air quality becomes a political flashpoint, TII's early moves in electric mobility look increasingly prescient. But the company isn't stopping at vehicles. The next frontier—medical devices—represents an even more dramatic departure from their engineering roots.

VI. Medical Devices & New Frontiers (2020s)

The conference room at Dare House, TII's Chennai headquarters, March 2023. Across the table sits representatives from Premji Invest, Azim Premji's family office that manages over $2 billion. The discussion isn't about tubes or chains or even electric vehicles. It's about surgical sutures—a product as far from TII's traditional business as one could imagine. Yet by the meeting's end, they would commit Rs 348 crore to acquire Lotus Surgicals, marking TII's entry into medical devices.

TII will acquire 67% while Premji Invest will acquire the balance 33% subject to completion of certain conditions precedent. TII will invest up to Rs 233 crore and Premji Invest will invest up to Rs 115 crore to acquire equity shares from the existing shareholders of Lotus. This wasn't just a diversification—it was a fundamental reimagining of what an engineering company could become.

The logic becomes clearer when you understand what TII saw that others missed. According to Tube Investments, Lotus Surgicals with a turnover of Rs 116 crore is into manufacturing and supply of surgical sutures and other medical devices. Surgical sutures require precision manufacturing tolerances that would make automotive engineers blush. A suture thread must maintain consistent tensile strength across diameters measured in fractions of a human hair. The needle must penetrate tissue with minimal trauma while maintaining structural integrity. These are engineering challenges, just in a different domain.

The platform draws inspiration from the vision of "Atmanirbhar Bharat" and aspires to become a global platform to design, manufacture and distribute innovative world class medical products at affordable price points. This wasn't just corporate speak. India imports over 80% of its medical devices, creating a $16 billion trade deficit. For a company that had built its reputation on import substitution in bicycles and automotive components, this represented a massive opportunity.

The partnership with Premji Invest was particularly strategic. The acquisition is the first step for TII and PI to initiate a medtech platform partnership. The platform aims to scale up through both organic growth and inorganic acquisitions. Premji Invest brought more than capital—they brought deep healthcare expertise from their portfolio investments and a shared vision of building at scale.

M.A.M Arunachalam (also known as Arun Murugappan), executive chairman of TII said, "the acquisition of Lotus marks our entry into the med-tech business. For Arun Murugappan, representing the fifth generation of the Murugappa family, this was about more than business. It was about societal impact—bringing affordable, quality medical devices to India's masses, much like his ancestors had done with bicycles seven decades earlier.

The medical devices foray also leveraged TII's hidden strengths. Their clean room manufacturing capabilities developed for precision automotive components translated directly to medical device production. Their quality systems, already certified to automotive standards more stringent than most medical device requirements, gave them a head start. Their distribution network, reaching into India's smallest towns through bicycle dealers, could be reimagined for medical supplies.

But TII's ambitions extended beyond just medical devices. The acquisition of Kcaltech System India and MoShine Electronics signaled a push into optics and vision systems. These weren't random acquisitions—they were building blocks for a larger play in automotive ADAS (Advanced Driver Assistance Systems) and potentially, medical imaging devices. The same precision optics used in automotive cameras could find applications in endoscopes and diagnostic equipment.

The TMT bars expansion into construction materials might seem like a departure from this high-tech trajectory, but it follows the same pattern of leveraging core capabilities. The metallurgical expertise developed over decades of tube manufacturing translated naturally into producing high-strength reinforcement bars for construction. In a country spending trillions on infrastructure, this was a market too large to ignore.

The TI-1, TI-2, TI-3 growth strategy framework that guides these expansions is elegantly simple. TI-1 represents the core businesses—tubes, chains, metal forming—that generate stable cash flows. TI-2 encompasses growth adjacencies like automotive components and engineering products. TI-3 covers new frontiers—electric vehicles, medical devices, and other emerging opportunities. Each tier funds the next, creating a self-sustaining growth engine.

What's remarkable is how TII maintains focus despite this diversification. Each new business must meet three criteria: it must leverage existing capabilities, it must have potential for market leadership, and it must be financially accretive within a defined timeframe. This discipline prevents the conglomerate sprawl that has destroyed value at so many Indian business houses.

The medical devices platform, still in its infancy, represents perhaps TII's boldest bet yet. Unlike electric vehicles where they can leverage automotive relationships, or TMT bars where construction is a known market, medical devices require building entirely new capabilities, regulatory expertise, and customer relationships. It's a testament to TII's confidence in their ability to learn and adapt—qualities that have defined them since 1949.

VII. Group Synergies & Conglomerate Dynamics

To understand TII's competitive advantages, you must first understand the Murugappa Group ecosystem. The Group has 29 businesses including 10 companies listed on the NSE and the BSE. Headquartered in Chennai, the major companies of the Group include Carborundum Universal, Cholamandalam Financial Holdings, Cholamandalam Investment and Finance, Cholamandalam MS General Insurance, Coromandel International, EID Parry, Parry Agro Industries, Shanthi Gears, Tube Investments of India, Wendt (India), and CG Power and Industrial Solutions.

This isn't a random collection of businesses. Each company creates value for the others in ways that outsiders often miss. When TII's electric three-wheelers need financing, Cholamandalam Investment and Finance Company—with its AUM crossing INR 1.7 Lakh Crore and serving over 40 Lakh customers—provides tailored financial products. When those same vehicles need insurance, Cholamandalam MS General Insurance steps in with specialized coverage designed specifically for commercial EVs.

The agricultural synergies are particularly powerful. Coromandel International Limited is one of India's largest phosphate fertilizer producer and also markets speciality nutrients and crop protection products. Coromandel is the largest private sector NPK player and the largest single super phosphate player. Operates the largest network of agri-retail chains, 'Mana Gromor' in India with over 750 centres. This massive rural distribution network becomes a potential channel for TII's electric tractors, reaching farmers who would never visit a traditional dealership.

EID Parry, with its 200-year heritage in sugar manufacturing, provides another fascinating synergy. E.I.D. Parry is a leader in the sugar industry, and has now entered the FMCG space. The company serves 1.5 lakh farmers. These farmer relationships become test beds for TII's agricultural innovations. When TII develops an electric tractor, they have immediate access to thousands of potential customers who already trust the Murugappa name.

The technical synergies run even deeper. CUMI is a pioneer and industry leader in materials science and engineering, and is one of the largest silicon carbide producers in the world. Silicon carbide is crucial for next-generation power electronics in electric vehicles. While competitors scramble for semiconductor supplies, TII has a sister company that's been mastering these materials for decades.

CG Power and Industrial Solutions is an engineering conglomerate which has made a foray into the semiconductor industry, and is a leader in the electrical engineering industry. As TII scales its EV operations, CG Power's expertise in motors, drives, and power electronics becomes invaluable. This isn't just about procurement savings—it's about co-developing technologies that neither company could create alone.

The capital allocation within the group deserves special attention. Unlike Western conglomerates that operate as financial holding companies, the Murugappa Group functions more like a Japanese keiretsu or Korean chaebol—with deep operational integration and patient capital flows. When TII needed hundreds of crores for its EV pivot, the group could mobilize resources without diluting public shareholders or taking on expensive debt.

The governance structure balances family control with professional management in a uniquely Indian way. With over 50,000 employees, the group fosters a professional work environment. Family members must earn their positions—they need external experience and proven competence before joining group companies. This meritocratic approach within a family structure creates stability without stagnation.

The financial discipline across the group is remarkable. Despite operating in cyclical industries like sugar, commodities, and automotive, the group has maintained consistent profitability. For FY22, Murugappa Group revealed a turnover of ₹54,722 crore, a surge of 31.2% from the previous year's records. The net profit rose by 23.2% to reach ₹5,520 crore for the same period. This isn't luck—it's the result of portfolio diversification where different businesses peak at different times.

The international partnerships reveal another dimension of group synergies. Murugappa Group has formed strong partnerships with renowned international companies such as Groupe Chimique Tunisien, Foskor, Mitsui Sumitomo, Morgan Advanced Materials, Sociedad Química y Minera de Chile (SQM), Yanmar & Co., and Compagnie Des Phosphat De Gafsa (CPG). Each partnership brings technology and market access that benefits not just the immediate venture but the entire group.

What's particularly interesting is how the group manages competing priorities. TII competes with Bajaj in three-wheelers, yet Cholamandalam finances Bajaj vehicles. Coromandel sells to farmers who might choose competitors' tractors over TII's electric ones. This ability to maintain Chinese walls while leveraging synergies requires sophisticated management that few conglomerates achieve.

The uninterrupted dividend distribution since 1954 reflects not just TII's individual strength but the group's collective resilience. In years when engineering struggled, financial services compensated. When agriculture faced headwinds, abrasives delivered. This portfolio effect creates a stability that allows for long-term strategic bets like electric vehicles and medical devices. As we'll explore next, these strategic patterns offer valuable lessons for any company navigating technological transitions.

VIII. Playbook: Engineering Excellence & Strategic Lessons

The TII playbook reads like a masterclass in industrial strategy, but it's the execution that separates theory from results. The backward integration strategy that began with bicycle tubes in 1955 has evolved into a sophisticated capability-building machine that systematically conquers new domains.

Consider the sequence: bicycles require tubes, so they built a tube factory. Tubes require precision steel strips, so they integrated further backward. But here's the genius—each backward integration created a forward opportunity. Bicycle tubes led to automotive tubes. Steel strips for bicycles became precision components for cars. The same welding expertise that joined bicycle frames now creates crash-resistant automotive structures. This isn't diversification—it's capability multiplication.

The joint venture management approach deserves its own business school case study. Since 1949, TII has partnered with companies from the UK, USA, France, and Japan. Yet unlike many Indian companies that remained perpetually dependent on foreign partners, TII systematically absorbed technology and eventually stood as equals. The Sedis acquisition in France flipped the script—an Indian company acquiring European technology, not the other way around.

The timing of market transitions reveals pattern recognition at its finest. TII entered automotive components just as India's car market was taking off in the 1990s. They acquired Shanthi Gears when industrial automation was accelerating. They launched electric vehicles before the government announced PLI schemes. This isn't luck—it's the result of being deeply embedded in industrial value chains where weak signals become visible early.

Moving up the value chain systematically requires discipline most companies lack. It's tempting to chase high-margin products immediately, but TII understood that capabilities must be earned. They spent decades perfecting ERW tubes before attempting CDW tubes. They mastered bicycle chains before attempting industrial chains. Each step built on the last, creating cumulative advantages that new entrants couldn't replicate.

The build versus buy decision framework at TII is particularly nuanced. They build when the capability is core to their strategy—like EV powertrains. They buy when speed matters more than organic development—like medical devices. They partner when technology access is critical—like the original bicycle venture. This isn't opportunistic M&A; it's strategic capability assembly.

Managing cyclical and structural businesses together requires a portfolio mindset that most focused companies can't develop. Bicycles are consumer discretionary, affected by fashion and disposable income. Automotive components are tied to vehicle production cycles. Industrial chains depend on capital investment cycles. By operating across these cycles, TII achieves a stability that pure-play companies envy.

The patient capital advantage of family-owned conglomerates becomes clear in TII's investment horizon. Public companies might balk at spending Rs 650 crore on EV acquisitions with uncertain returns. But when your dividend track record spans seven decades and your shareholders include family members thinking in generations, not quarters, these bets become possible. This isn't recklessness—it's the luxury of long-term thinking.

The quality philosophy embedded since the British partnership days has evolved into a competitive moat. When your tubes go into steering columns where failure means death, quality isn't negotiable. This zero-defect mindset, applied to bicycles that don't need it, creates products that last decades. Indian families still ride BSA bicycles bought in the 1970s—that's brand equity money can't buy.

The localization strategy reveals deep understanding of Indian markets. While competitors imported designs wholesale, TII adapted products for Indian conditions. Their bicycles had stronger frames for potholed roads. Their chains were designed for dusty environments. Their electric three-wheelers are built for drivers who can't afford downtime. This isn't cost engineering—it's empathetic engineering.

The technology absorption model pioneered by TII has become the template for Indian manufacturing. Start with a foreign partnership, learn the technology, adapt it for Indian conditions, then innovate beyond the original. This progression from licensee to competitor to innovator is the story of Indian industry itself, and TII wrote the playbook.

The capital efficiency metrics tell a story of disciplined execution. Despite massive investments in new businesses, return on capital employed has remained healthy. This isn't financial engineering—it's operational excellence where every rupee of investment is sweated for maximum return. The ability to maintain this discipline while pursuing growth is what separates great companies from merely good ones.

The cultural elements of the TII playbook are harder to replicate than the strategic ones. The engineering mindset that measures everything. The quality obsession that treats customer complaints as learning opportunities. The long-term orientation that plants trees for the next generation. These soft factors, embedded over decades, become the hard advantages that competitors can't copy.

IX. Financial Analysis & Investment Case

The numbers tell a story of transformation under pressure. Market cap of ₹55,838 Crore, Revenue of ₹20,196 Cr, Profit of ₹1,041 Cr, Stock trading at 10.1 times its book value. But these headline figures mask a more complex narrative of a company navigating multiple transitions simultaneously.

Q1 FY2026 results: Rs.5309 Cr revenue, Rs.449 Cr PBT; consolidated revenue Rs.5309 Cr, PBT Rs.445 Cr. The recent quarterly performance reflects the challenges of building new businesses while maintaining legacy operations. The EV segment, still in investment mode, is dragging down consolidated margins, yet this is exactly what long-term value creation looks like in real time.

The segment-wise breakdown reveals the portfolio dynamics at play. Engineering continues to be the cash cow, generating stable returns from precision tubes and automotive components. Metal Formed Products maintains healthy margins despite commodity volatility. Bicycles, often dismissed as a legacy business, still generates respectable returns with minimal capital requirements. The new ventures—EVs and medical devices—are currently margin-dilutive but represent optionality on India's future.

The company's net profit surged to ₹814 crore, compared to ₹248 crore in the same quarter last year, primarily driven by a one-time gain of ₹569 crore. However, the company's revenue remained flat, declining slightly by 0.3% YoY, amounting to ₹1,957.3 crore against ₹1,962.5 crore in Q4 FY2024. The EBITDA rose by 5%, reaching ₹228 crore from ₹217.2 crore, while the EBITDA margin improved slightly to 11.6% from 11% YoY.

The capital efficiency metrics deserve attention. Despite massive investments in EVs and medical devices, the company maintains a healthy balance sheet with manageable debt levels. This isn't leveraged growth—it's self-funded transformation, where profitable legacy businesses fund future growth engines. The ability to do this while maintaining dividend payments showcases exceptional capital allocation.

Tube Investments of India Ltd (TIINDIA) has seen a 36% decline from its peak price of Rs 4,810.80. The stock has delivered almost no returns since October 2023, closing at Rs 3,067. The company reported a slight revenue decline for Q1 FY25, with a full-year revenue growth of only 3.7%. Overall, the stock's performance has been flat over the past 19.5 months.

The stock's underperformance reflects market skepticism about the EV transition. Investors see current margins compressed by new ventures without clear visibility on when these investments will pay off. This creates an interesting divergence between market perception and business reality—the company is stronger than ever in its core businesses while building options on multiple future growth vectors.

The Bear Case: The risks are real and mounting. The EV business faces execution challenges in a market where even global giants struggle. The three-wheeler market is getting crowded with well-funded startups and established players. Electric tractors might be too early for Indian agriculture. Medical devices require regulatory expertise TII doesn't possess. Meanwhile, the core automotive business faces the secular decline of ICE vehicles.

Competition is intensifying across segments. In tubes, cheap imports pressure margins. In bicycles, e-commerce players with venture capital backing are disrupting distribution. In automotive components, the shift to EVs threatens to strand investments in ICE-specific products. The conglomerate structure itself might become a liability in an era where focused plays command premium valuations.

The capital allocation concerns are valid. Hundreds of crores invested in EVs with uncertain returns. Medical devices requiring continuous investment with long gestation periods. TMT bars entering a commoditized market with established players. Each new venture dilutes focus and potentially destroys value if execution falters.

The Bull Case: But the bull case rests on pattern recognition. This is the same company that transformed from bicycles to automotive components when skeptics doubted. The same discipline that built market leadership in tubes and chains is now being applied to EVs and medical devices. The track record of successful diversification spanning seven decades suggests betting against TII is historically unwise.

The EV opportunity alone could justify the current valuation. India's three-wheeler market will inevitably electrify—it's not whether but when. TII's early investments position them to capture disproportionate value when the inflection point arrives. Unlike startups burning cash for market share, TII can afford to build methodically, achieving profitability from day one in chosen segments.

The portfolio effect provides downside protection that focused companies lack. Even if EVs disappoint, the core engineering business generates enough cash to fund multiple experiments. The medical devices platform, backed by Premji Invest's expertise, could become a multi-thousand crore business. TMT bars provide exposure to India's infrastructure boom. Multiple ways to win, limited ways to lose completely.

The valuation at 10.1 times book value might seem expensive, but consider what you're buying: market leadership in multiple segments, a proven management team, patient capital structure, and options on India's most promising growth sectors. The current stock price effectively values the new ventures at zero—any success becomes pure upside.

X. Future Vision & Strategic Imperatives

The road ahead for TII resembles India's own development journey—ambitious, complex, and fraught with execution challenges. The target of 15-20% market share in chosen EV segments by 2027-28 requires flawless execution in an industry where even Tesla struggled initially. But TII isn't trying to be Tesla; they're building the Maruti of electric mobility—reliable, affordable, and deeply Indian.

The EV transition execution presents unique challenges. Unlike software where you can iterate quickly, manufacturing requires massive upfront investments in tooling and production lines. TII must simultaneously manage battery supply chains, develop charging infrastructure partnerships, and convince skeptical customers to switch from proven diesel vehicles. The three-wheeler drivers they're targeting make purchase decisions based on daily earnings calculations, not environmental consciousness.

The medical devices opportunity represents an even more dramatic departure. Success requires building regulatory expertise for multiple geographies, each with different standards. Clinical validation takes years, not months. Distribution requires relationships with hospitals and healthcare providers, completely different from TII's traditional customers. Yet the market opportunity—import substitution in a $16 billion market—justifies the complexity.

Global expansion possibilities multiply the strategic options. TII's precision tubes already export globally, but EVs and medical devices offer branded product opportunities. Imagine Montra three-wheelers in African cities or TII surgical sutures in Southeast Asian hospitals. The Murugappa Group's century-old relationships across these markets provide entry points competitors lack.

Technology partnerships will determine competitive advantage. TII needs battery technology for EVs, IoT capabilities for connected vehicles, and advanced materials for medical devices. The group's existing partnerships with global leaders provide a foundation, but new alliances—perhaps with Chinese battery manufacturers or Israeli medtech companies—will be crucial.

The M&A pipeline remains active. Management has signaled continued acquisitions in EVs and medical devices. Each target must meet strict criteria: strategic fit, reasonable valuations, and integration feasibility. The Shanthi Gears and Lotus Surgicals acquisitions provide the template—buy quality assets with untapped potential, then leverage group capabilities to accelerate growth.

ESG initiatives aren't just compliance—they're competitive advantage. Electric vehicles directly address environmental concerns. Medical devices improve healthcare access. The company's manufacturing processes increasingly emphasize sustainability. For global customers increasingly demanding ESG compliance from suppliers, TII's initiatives open doors that remain closed to competitors.

The next generation leadership transition is already underway. The fifth generation of the Murugappa family, educated at global universities and trained at international companies, brings fresh perspectives while respecting institutional knowledge. The balance between family wisdom and professional management will determine whether TII can maintain its culture while adapting to new realities.

The strategic imperatives are clear: Execute the EV transition without compromising core business profitability. Scale medical devices into a meaningful contributor within five years. Maintain technology leadership in traditional businesses facing disruption. Balance growth investments with shareholder returns. Navigate the family-professional management dynamic as leadership transitions.

The next decade will test whether TII's seven-decade playbook works in an exponentially changing world. Can a company that took 30 years to move from bicycles to automotive components now successfully pivot to EVs in five years? Can engineering excellence in metal forming translate to medical devices? Can a 75-year-old company maintain entrepreneurial agility?

XI. Epilogue & Reflections

Standing back from the detailed analysis, several counterintuitive insights emerge. First, conglomerate structures, often dismissed as value-destroying, can actually enable bold strategic pivots that focused companies can't attempt. TII's ability to fund speculative EV ventures while maintaining dividends showcases this advantage.

Second, the supposed conflict between family ownership and professional management might be false. The Murugappa structure suggests that family values—long-term thinking, reputation consciousness, stakeholder balance—combined with professional execution might be the optimal governance model for emerging markets.

Third, technological disruption doesn't necessarily favor startups. TII's EV entry shows how incumbents with manufacturing expertise, distribution networks, and patient capital can potentially outexecute venture-funded startups once market timing aligns.

The lessons for conglomerate builders are profound. Diversification works when each new business leverages existing capabilities. Patient capital enables strategies that quarterly earnings pressure would kill. Culture and values, often dismissed as soft factors, become the binding agent that makes portfolio companies more than the sum of their parts.

What would different strategic choices have meant? If TII had remained focused on bicycles, they'd be a marginal player in a commoditized market. If they'd eschewed EVs for ICE components, they'd face existential threats within a decade. If they'd chosen aggressive leverage over patient equity funding, the 2008 or 2020 crises might have been fatal. Each conservative choice that seemed suboptimal at the time enabled future optionality.

The India manufacturing story through TII's lens reveals important truths. Manufacturing excellence isn't about cheap labor—it's about systematic capability building over decades. Indian companies can successfully absorb and improve upon global technologies. The transition from import substitution to global competitiveness is possible but requires generations of patient effort.

Looking forward, TII embodies India's industrial possibilities and challenges. Like India, it must manage multiple transitions simultaneously—technological, generational, and strategic. Like India, it has strong foundations but uncertain execution. Like India, its success isn't guaranteed but its potential is immense.

The surprise isn't that a bicycle company became an engineering conglomerate—it's that more companies haven't followed this playbook. Perhaps the seven-decade commitment required is too daunting for modern managers focused on quarterly results. Perhaps the family governance structure that enables such patience is impossible to replicate. Or perhaps TII's story is uniquely Indian—a product of specific historical circumstances that can't be reproduced.

For investors, TII represents a fascinating risk-reward proposition. You're betting on execution in unfamiliar territories against the track record of successful diversification. You're weighing current margin pressure against future optionality. You're trusting management's capital allocation against market skepticism. It's not an easy decision, but then again, the easy decisions rarely generate exceptional returns.

The story of Tube Investments of India is far from over. The next chapters—will EVs achieve profitability? Can medical devices scale? Will the sixth generation maintain the culture?—remain unwritten. But if history is any guide, betting against a company that has successfully navigated India's economic evolution from independence to emergence might be premature.

What started in 1949 as a simple ambition to manufacture bicycles for newly independent India has evolved into something far more complex and valuable—a platform for industrial capability building that can attack any engineering challenge. Whether the challenge is precision tubes, electric tractors, or surgical sutures, the TII playbook remains consistent: understand the market deeply, build capabilities systematically, execute with excellence, and think in decades, not quarters.

That might not be a formula for explosive growth, but it's proven to be a recipe for enduring value creation. In a world obsessed with disruption and transformation, there's something deeply reassuring about a company that has been transforming continuously for 75 years, one careful step at a time. The Murugappa Group's motto—"Perform, Transform, Repeat"—isn't just corporate speak. It's the distilled wisdom of a century in business, executed daily in factories from Chennai to Coimbatore.

For India, companies like TII represent more than investment opportunities. They're proof that Indian manufacturing can compete globally, that family businesses can professionalize without losing their soul, and that patient capital and engineering excellence can create enduring value. In a nation still finding its industrial identity, TII offers a template worth studying, if not replicating.

The bicycle that started it all—simple, efficient, democratizing mobility—remains the perfect metaphor for TII's journey. Just as that bicycle gave millions of Indians their first taste of personal transportation, TII's evolution gives Indian industry a model for systematic capability building. The journey from Ambattur to the world, from bicycles to electric vehicles, from tubes to surgical sutures, isn't just a corporate story.

It's a thoroughly Indian story of ambition, patience, and the relentless pursuit of excellence.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube