Graphite India: The Carbon Empire That Powers Global Steel

I. Cold Open & Episode Roadmap

Picture this: A sprawling industrial complex in Durgapur, West Bengal, where temperatures inside massive furnaces reach 3,000 degrees Celsius—hot enough to melt steel itself. Giant electrodes, some weighing over three tons and stretching twenty feet long, glow white-hot as they channel enough electricity to power a small city. This is where carbon transforms into the unsung hero of modern civilization: graphite electrodes, the critical component without which no electric arc furnace can produce steel.

In 2017, something extraordinary happened. A company that had been grinding through nearly two decades of survival mode suddenly saw its stock price explode from ₹200 to over ₹900 in just eighteen months. Graphite India Limited, a sixty-year-old industrial manufacturer in one of the world's most commoditized markets, became the darling of Dalal Street. The catalyst? China's environmental crackdown had just eliminated half the world's graphite electrode capacity overnight.

But here's the paradox that makes this story fascinating: How does a company in a brutally cyclical, capital-intensive, commoditized industry not just survive six decades of boom-bust cycles, but emerge with a market capitalization of ₹10,494 crores and virtually no debt? How did a traditional Marwari family business from Rajasthan's dusty plains build one of the world's most sophisticated electrode manufacturing operations? And perhaps most intriguingly—in an era where everyone chases the next software unicorn, what can we learn from a company that makes giant carbon sticks?

This is the story of Graphite India—a tale that spans from post-independence industrial ambitions to modern global supply chains, from the License Raj to liberalization, from family patriarch to professional management. It's about the Bangur family's remarkable ability to play the long game in an industry where most players think quarter to quarter. It's about technical excellence in "boring" industries, the discipline of capital allocation through cycles, and why sometimes the best opportunities hide in plain sight in sectors investors ignore.

We'll journey through the company's founding as a technology partnership with America's Great Lakes Carbon Corporation, witness its expansion across India's industrial heartland, survive the "lost decade" of 1998-2008 when global oversupply nearly killed the industry, and experience the windfall years when China's policy decisions created a once-in-a-generation opportunity. Along the way, we'll decode the unit economics of electrode manufacturing, understand why this seemingly simple product requires extraordinary technical sophistication, and explore how a company making products from carbon positions itself for a decarbonizing future.

What emerges is not just a corporate history, but a masterclass in navigating cyclical industries, managing family business transitions, and building operational excellence when financial engineering isn't an option. It's about understanding that in commodity markets, the spoils don't go to the swift or the clever, but to those who can endure.

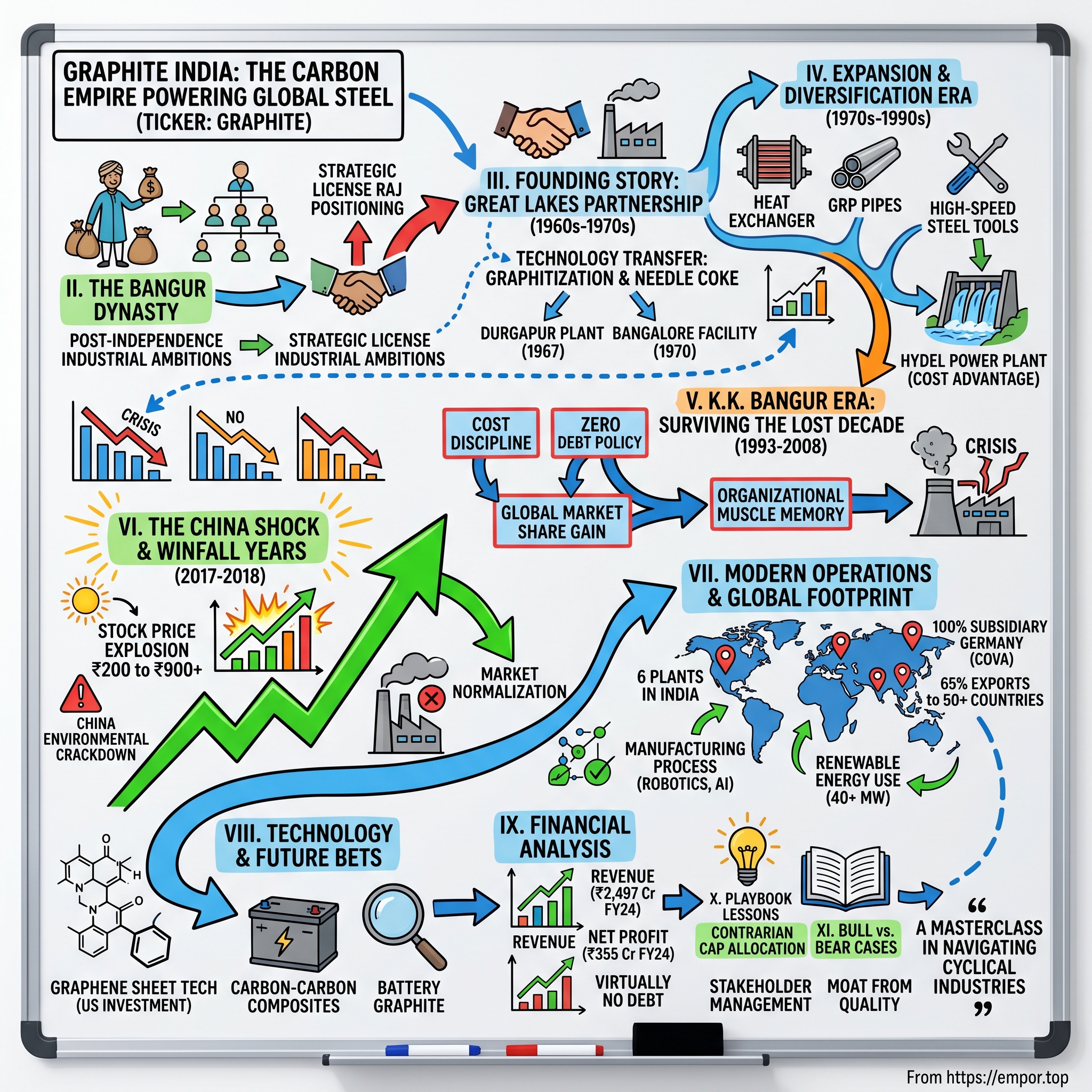

II. The Bangur Dynasty & Post-Independence India

The year is 1890. A young man named Mugneeram Bangur leaves the arid landscapes of Didwana in Rajasthan, carrying little more than ancestral trading instincts and an appetite for risk. He arrives in Calcutta—then the commercial capital of the British Raj—where fortunes were being made in jute, tea, and coal. This migration from Rajasthan's merchant communities to Bengal's industrial frontier would spawn one of India's most enduring business dynasties.

Mugneeram started as a trader, but his sons Govind Lal Bangur and later grandsons Rangnath and Narsingh Das Bangur transformed the family from merchants to industrialists. By the 1950s, as India gained independence and Nehru's vision of a socialist, self-reliant economy took shape, the Bangurs had already assembled an impressive portfolio: textiles in Bombay, synthetic fibers in Gujarat, a bank, shipping lines connecting India to global markets, paper mills, cement factories churning out material for India's infrastructure dreams, asbestos plants, tea estates sprawling across Assam, coffee plantations in Karnataka, and power cable manufacturing.

This wasn't diversification for its own sake—it was strategic positioning for the License Raj era. In Nehru's India, industrial licenses were gold. The government decided who could manufacture what, where, and how much. The Bangurs understood this game perfectly: secure licenses across industries, build capabilities, and wait for India's inevitable industrialization to create demand. They were patient capital personified, willing to build factories before markets existed, knowing that in a closed economy with limited competition, the early movers would dominate for decades.

The current torchbearer of this legacy is Krishna Kumar Bangur—known as K.K. Bangur in business circles—a man whose management philosophy seems lifted from Warren Buffett's playbook despite predating much of Buffett's public writings. K.K. and his family today hold 65.3% of Graphite India, a stake worth approximately ₹6,850 crores. This isn't just wealth; it's skin in the game at a scale that aligns the family's fortune entirely with minority shareholders.K.K. Bangur, who has been exposed to business and industry at an early age with more than 30 years of experience, became a Director of Graphite India in July 1988 and Chairman since July 1993. His management philosophy emerged during one of the industry's darkest periods, which would later prove prescient.

What set the Bangurs apart in post-independence India wasn't just their ability to secure licenses or build factories—it was their understanding that in capital-intensive industries, survival itself is a strategy. While peers leveraged aggressively during boom times, the Bangurs maintained conservative balance sheets. While others chased diversification into fashionable sectors, they stuck to heavy industry. This wasn't stubbornness; it was conviction that India's development would ultimately need steel, cement, and infrastructure more than consumer goods.

The License Raj created strange incentives. Companies hoarded licenses even for products they had no intention of manufacturing, just to prevent competitors from entering. The Bangurs played this game but with a difference—they actually built what they licensed. By the time India began liberalizing in 1991, the family had operational expertise across a dozen industries, technical partnerships with global leaders, and most importantly, the financial strength to survive the transition from protected markets to global competition.

Understanding the Bangur dynasty's approach to business is crucial because Graphite India cannot be understood outside this context. This is a company that thinks in decades, not quarters. It's a company where the promoter's wealth rises and falls with the stock price, creating perfect alignment with minority shareholders. It's a company that views downturns not as disasters but as opportunities to strengthen relative position.

Now a resident of Singapore, Krishna Kumar Bangur represents a unique breed of Indian industrialist—globally minded yet rooted in traditional business values, financially conservative yet technologically ambitious, family-controlled yet professionally managed. These apparent contradictions would prove essential in navigating the graphite electrode industry's violent cycles.

III. Founding Story: The Great Lakes Partnership (1960s-1970s)

The telegram arrived at the Bangur offices in Calcutta in early 1961. It was from Great Lakes Carbon Corporation, the American giant that dominated global electrode manufacturing. They were looking for an Indian partner to establish electrode production in the subcontinent. For the Bangurs, this represented more than a business opportunity—it was a chance to enter one of the most technically sophisticated industrial processes of the era.

Great Lakes Carbon wasn't just any American company. Founded in 1919 in Chicago, they had pioneered many of the technologies that made modern electrode manufacturing possible. They controlled patents on needle coke processing, the critical raw material that gave electrodes their unique properties. They had perfected the art of graphitization—the process of heating carbon to such extreme temperatures that its atomic structure reorganizes into layers of pure graphite. Their electrodes powered the electric arc furnaces that were rebuilding Europe and Japan after World War II.

Why did Great Lakes want an Indian partner? The answer lay in geopolitics and economics. India's Second Five Year Plan (1956-61) had prioritized heavy industry, particularly steel. The country was building massive integrated steel plants at Bhilai, Rourkela, and Durgapur with Soviet and German assistance. These plants would need electrodes—lots of them. Import substitution was official policy. If Great Lakes didn't manufacture locally, they would eventually be locked out of the Indian market entirely.

The company was formally established in 1962 in collaboration with American firm Great Lakes Carbon. But incorporation was just paperwork. The real challenge was building India's first electrode manufacturing facility from scratch. The site chosen was Durgapur in West Bengal—not coincidentally located near one of India's new steel plants. Graphite India Limited became the pioneer in India for manufacture of Graphite Electrodes.

The technology transfer agreement with Great Lakes was comprehensive but came with strings. The Americans would provide technical know-how, train Indian engineers, and help establish quality standards. In return, they took an equity stake and received royalties on production. More importantly, they controlled access to needle coke, which India couldn't produce domestically. This created a dependency that would last decades.

The first facility at Durgapur, operational by 1967, was a marvel of industrial engineering for its time. The manufacturing process was extraordinarily complex: petroleum coke and coal tar pitch had to be mixed in precise proportions, extruded into electrode shapes under massive pressure, baked for weeks in specially designed furnaces, impregnated with pitch to increase density, re-baked, and finally graphitized at temperatures exceeding 3,000°C. Each step required precise control—too much heat too fast and the electrodes would crack; too little and they wouldn't develop the necessary electrical and mechanical properties.

The early years were brutal. Indian engineers, despite training in America, struggled with the nuances of the process. Quality was inconsistent. Rejection rates exceeded 40%. Steel plants, themselves struggling with new technology, blamed electrode quality for their production problems. The partnership with Great Lakes became strained as the Americans grew frustrated with what they saw as Indian inefficiency, while the Indians resented what they perceived as technological colonialism.

A turning point came in 1970 when the company decided to establish a second manufacturing unit in Bangalore. This wasn't just expansion—it was a declaration of technological independence. The Bangalore facility would incorporate lessons learned from Durgapur but would also experiment with modifications to the Great Lakes process. Indian engineers had discovered that local raw materials required different processing parameters. They began developing their own formulations, their own quality control methods, their own maintenance protocols.

The Bangalore facility also housed what would become the company's specialty division. While Durgapur focused on large-diameter electrodes for steel production, Bangalore would manufacture smaller, ultra-high-power electrodes for specialty applications. This diversification proved prescient—specialty electrodes commanded premium prices and were less susceptible to cyclical downturns.

By the mid-1970s, Graphite India had achieved something remarkable: genuine technological capability in one of the world's most complex industrial processes. The company was no longer just assembling electrodes from imported materials using foreign technology. It was innovating, improving, adapting. Indian engineers were filing patents. Quality metrics approached international standards. Perhaps most importantly, the company had developed the institutional knowledge—the thousands of small insights and adjustments that couldn't be codified in manuals—that separated world-class manufacturers from mere license producers.

The relationship with Great Lakes evolved from dependency to partnership to, eventually, independence. By the late 1970s, Graphite India was exporting electrodes to markets that Great Lakes served. The student hadn't just learned from the master—in some areas, particularly in handling lower-quality raw materials and operating in challenging conditions, the student had surpassed the teacher.

This early history established patterns that would define Graphite India for decades: patient capability building, technical excellence as competitive advantage, and the confidence to compete globally despite starting from a position of technological disadvantage. The company had learned that in industries with high technical barriers, the ability to master complex processes created moats that financial engineering could never replicate.

IV. Expansion & Diversification Era (1970s-1990s)

The 1980s opened with India in economic crisis. Foreign exchange reserves had dwindled, inflation was soaring, and the government was forced to approach the IMF for emergency funding. For most Indian companies, this meant retrenchment. For Graphite India, it meant opportunity. While competitors struggled with foreign exchange allocations for importing needle coke, the company's strong relationship with Great Lakes and its growing export revenues provided access to dollars. Crisis became competitive advantage.

The decision to establish a specialty division at Bangalore in 1970 now paid unexpected dividends. The global steel industry was evolving rapidly. Japanese and Korean steel makers were pushing the boundaries of electric arc furnace technology, demanding electrodes that could handle higher current densities and longer campaigns. Traditional electrodes would crack or erode under these extreme conditions. Graphite India's Bangalore team had been quietly developing ultra-high-power (UHP) electrodes that could meet these demands.

But K.K. Bangur and his team saw beyond just electrodes. They recognized that their core competency wasn't making carbon sticks—it was managing high-temperature processes and understanding carbon chemistry at a molecular level. This insight led to a series of calculated diversification moves that would transform the company from a mono-product manufacturer to a carbon technology conglomerate.

The first move was into impervious graphite equipment. The same properties that made graphite excellent for electrodes—chemical inertness, thermal stability, electrical conductivity—also made it ideal for chemical processing equipment. The company established a division at Nashik to manufacture heat exchangers, columns, and vessels for the chemical and pharmaceutical industries. This wasn't random diversification; it leveraged existing technical capabilities while opening entirely new markets.

Next came glass-reinforced plastic (GRP) pipes. This might seem unrelated to graphite, but the connection was sophisticated composite materials technology. The same understanding of how to bind materials at a molecular level, how to create structures that were both strong and light, applied across both domains. The Nashik facility expanded to include GRP manufacturing, targeting India's growing chemical and infrastructure sectors.

The most ambitious diversification came through the 1993-94 amalgamation with Graphite Vicard India Limited. This wasn't just an acquisition—it was a transformation. Graphite Vicard brought technology from France's Societe des Electrodes et Refractaires Savoie (SERS), one of Europe's leading electrode manufacturers. The combined entity, renamed from Carbon Corporation Limited to Graphite India Limited, now had access to both American and European technology streams.

The amalgamation also brought unexpected assets: a high-speed steel division that manufactured cutting tools and specialty alloys. On the surface, steel production seemed distant from graphite electrodes. But the connection was profound—both required precise control of carbon content, understanding of phase transformations at high temperatures, and expertise in powder metallurgy. The steel division would eventually become a steady cash generator, providing ballast during electrode market downturns.

Perhaps the most visionary move was the establishment of a hydel power plant in Karnataka with 18 MW capacity. In the 1990s, India's power situation was dire. Industrial units faced daily power cuts. For an electrode manufacturer, where furnaces needed to run continuously for weeks, unreliable power meant product losses worth millions. The hydel plant provided energy security, but more importantly, it provided cost advantage. When power costs represent 40% of electrode manufacturing expenses, generating your own power at marginal cost transforms unit economics.

By the end of this era, GIL's manufacturing facilities were spread across 6 plants in India, each specialized yet interconnected. Durgapur remained the flagship for large-diameter electrodes. Bangalore housed UHP electrode production and R&D. Nashik manufactured specialty graphite and composite products. The company had also begun exploring international expansion, laying groundwork for what would eventually become a 100% owned subsidiary at Nuremberg, Germany, by name Graphite COVA GmbH.

The diversification strategy wasn't without critics. Analysts questioned why an electrode company was making steel tools and GRP pipes. The stock market, enamored with "pure play" stories, punished the company's valuation. But the Bangurs understood something the market didn't: in cyclical industries, diversification isn't about growth—it's about survival. When electrode markets crashed, specialty graphite provided revenue. When specialty graphite slowed, the steel division contributed. The hydel plant generated steady returns regardless of industrial cycles.

By 1993, when K.K. Bangur formally took over as Chairman, Graphite India had transformed from a single-product, single-location manufacturer to a diversified carbon technology company with national presence and global ambitions. Revenue had grown from ₹50 crores in 1980 to over ₹400 crores. More importantly, the company had built capabilities—in technology, operations, and management—that would prove invaluable in navigating the brutal decade ahead.

The expansion era taught crucial lessons: that related diversification could create resilience without losing focus, that controlling critical inputs like power provided strategic advantage, and that technological capability, once built, could be leveraged across adjacent markets. These lessons would soon be tested in ways no one could have anticipated.

V. The K.K. Bangur Era: Surviving the Lost Decade (1993-2008)

The fax machine in K.K. Bangur's office buzzed to life on a humid Calcutta morning in 1998. The message from their European customers was stark: electrode prices were being cut by 30%, effective immediately. Chinese producers had flooded the global market with electrodes priced below the cost of raw materials. This wasn't competition—it was carnage. Thus began what insiders would later call the "lost decade," a period that would destroy two-thirds of global electrode capacity and push several century-old companies into bankruptcy.

To understand the magnitude of this crisis, consider the numbers: Global electrode prices fell from $3,000 per metric ton in 1997 to $900 by 2001. Capacity utilization at Graphite India dropped from 85% to barely 40%. The company's stock price, which had touched ₹180 in 1996, crashed to ₹12 by 2001. International competitors like Germany's SGL Carbon and America's UCAR International filed for bankruptcy protection. The industry wasn't just in recession—it was in existential crisis.

K.K. Bangur's response to this crisis would define his legacy. Where others saw disaster, he saw a test of organizational character. His strategy was counterintuitive: instead of cutting costs indiscriminately, he would cut intelligently. Instead of abandoning markets, he would deepen relationships. Instead of stopping investments, he would invest selectively. The goal wasn't to maximize profits—profits were impossible in this environment. The goal was to survive with capabilities intact.

The first decision was about people. While competitors laid off thousands of workers, Bangur made a remarkable promise to his 3,000 employees: no one would lose their job because of market conditions. This wasn't charity—it was calculation. Training an electrode manufacturing technician took years. The specialized knowledge of furnace operators, quality control chemists, and maintenance engineers couldn't be quickly rebuilt. By keeping his workforce intact, Bangur was preserving institutional knowledge for the eventual upturn.

But keeping people employed didn't mean business as usual. The company implemented what Bangur called "cost discipline without quality compromise." Every expense was scrutinized. Travel was eliminated unless customer-facing. Consultant contracts were terminated. Corporate offices were consolidated. But critically, spending on raw material quality, maintenance, and safety was maintained. Bangur understood that in commodity markets, reputation for quality was the only differentiator. One batch of bad electrodes could lose a customer forever.

The company also restructured its customer relationships. Rather than chasing volume with discounts, Graphite India focused on technical service. Engineers were embedded at customer steel plants, helping optimize electrode consumption. The company developed custom electrode grades for specific furnace conditions. When a major European steel producer faced technical problems, Graphite India sent a team at its own expense to solve the issue. These investments in relationships would pay dividends when markets recovered.

Financial management during this period was extraordinarily conservative. Despite pressure from investors to leverage the balance sheet for acquisitions or buybacks, Bangur maintained near-zero debt. Cash was hoarded. Dividends were cut. Growth capital was frozen. This conservatism seemed excessive to observers who didn't understand the electrode industry's history of violent cycles. Bangur had studied the failures of American and European competitors—they had all shared one characteristic: high leverage when the cycle turned.

The discipline extended to capital allocation. While major expansion was frozen, selective investments continued. The company upgraded its graphitization furnaces with energy-efficient designs. It invested in IT systems for better inventory management. Most presciently, it began developing capabilities in needle coke calcination, reducing dependence on imported processed materials. These investments were small—₹10-20 crores annually—but targeted at structural cost reduction rather than capacity expansion.

The true test came in 2003 when China's domestic steel demand began growing at unprecedented rates. Chinese electrode producers, who had been dumping product internationally, suddenly redirected capacity to domestic markets. Global electrode prices began recovering. But rather than immediately ramping production, Bangur waited. He had seen false recoveries before. Only when prices sustained above $1,500 per ton for six consecutive months did Graphite India begin selective capacity expansion.

This patience proved prescient. Many competitors, desperate after years of losses, ramped capacity aggressively at the first sign of recovery. When China's demand briefly slowed in 2005, these companies were caught with excess inventory and debt. Graphite India, having expanded cautiously, weathered this mini-correction with minimal impact. By 2008, when the global financial crisis struck, the company had one of the strongest balance sheets in the global electrode industry: virtually no debt, positive cash flow even at trough utilization, and modernized facilities.

The numbers tell the story of this remarkable period: Despite electrode prices remaining below profitable levels for most of the decade, Graphite India never reported an annual loss. Revenue grew from ₹400 crores to ₹1,200 crores. The company maintained its dividend, albeit reduced. Most remarkably, it gained global market share, climbing from 6% in 1998 to 11% by 2008, even as overall industry capacity shrank.

But perhaps the greatest achievement was intangible: Graphite India emerged from the lost decade with its capabilities not just intact but enhanced. It had developed the organizational muscle memory of crisis management. It had proven that disciplined execution could overcome market hostility. Most importantly, it had demonstrated that in commodity industries, the capacity to endure was itself a competitive advantage.

Looking back, K.K. Bangur would later tell investors that 1998-2008 taught him that "in our industry, the race doesn't go to the swift or the clever, but to those who can survive with their capabilities intact until rationality returns to markets." This philosophy would position the company perfectly for the windfall that no one saw coming.

VI. The China Shock & Windfall Years (2017-2018)

The announcement came without warning on a Friday evening in January 2017. China's Ministry of Environmental Protection declared that 30% of the country's steel capacity would be shut down immediately for environmental violations. For the global electrode industry, this was the equivalent of a meteor strike. China produced 50% of the world's graphite electrodes and consumed 40%. Within hours, electrode spot prices in Asian markets had doubled. Within weeks, they had tripled. The windfall years had begun.

To understand the magnitude of this shock, consider that graphite electrode prices had languished between $1,500-2,500 per metric ton for nearly a decade. By December 2017, they had touched $35,000 per ton in some spot markets. Graphite India's average realization jumped from ₹65,000 per ton to ₹425,000. The company's quarterly profits exceeded its previous annual revenues. The stock price, which had been meandering around ₹90 in January 2017, shot past ₹900 by February 2018.But K.K. Bangur's response to this windfall revealed the discipline forged during the lost decade. While competitors announced massive capacity expansions and analysts projected permanent structural shortages, Bangur remained skeptical. In a private conversation with institutional investors, he reportedly said: "Mr. K.K. Bangur, Chairman of Graphite India Ltd., has been exposed to business and industry at an early age and has more than 30 years of experience"—that experience had taught him that windfalls in commodity markets are temporary by definition.

In October 2017, dozens of huge steel mills in China stopped or curtailed their operations. In northern China cement plants prepared to shut down entirely before Christmas. The measures were part of an aggressive action plan that aimed to cut wintertime particulate pollution by 15% year-on-year over the next five months. The scale was staggering: The operating restrictions affected one-quarter of China's total steel-making capacity and approximately 10% of cement production. The measures were expected to cut national steel output by over 10% in the next five months.

The impact on electrode markets was immediate and dramatic. Prices scaled $16,000 a metric tonne after China's curbs on pollution hurt supply of needle coke, a key raw material. But this was just the beginning. As Chinese electrode producers shut down and domestic steel producers scrambled for supply, global markets went into panic mode. Long-term contracts were torn up. Spot prices reached levels that seemed impossible just months earlier.

For Graphite India, this presented both opportunity and danger. The opportunity was obvious: at $30,000 per ton electrode prices, the company was generating EBITDA margins exceeding 70%. Cash was pouring in faster than it could be deployed. The stock market valued the company as if these prices would last forever. But the danger was equally clear: customers were furious about price increases, competitors were announcing capacity that would come online in 18-24 months, and China would eventually solve its environmental issues without permanently shuttering capacity.

Bangur's strategy during this period was masterful in its restraint. First, he honored all existing contracts even when spot prices were multiples higher. This decision cost hundreds of crores in foregone profits but preserved relationships with customers who remembered the loyalty when markets normalized. Second, while competitors announced grandiose expansion plans, Graphite India limited capacity additions to debottlenecking and efficiency improvements—investments that made sense even at normal electrode prices.

The capital allocation during the windfall was particularly instructive. Rather than paying special dividends or making acquisitions at peak valuations, the company strengthened its balance sheet, becoming virtually debt-free. It invested in backward integration, particularly in needle coke processing capabilities. Most presciently, it made a strategic investment of $18.5 million in General Graphene Corporation, a US company developing graphene sheet technology—a bet on the future of carbon materials beyond traditional electrodes.

The market's reaction was bipolar. The stock price movement told the story of greed turning to fear: from ₹90 in January 2017 to over ₹900 by February 2018, then crashing back to ₹200 by December 2018 as reality set in. Analysts who had projected permanent shortages suddenly worried about oversupply. Investors who had chased momentum fled just as quickly.

But inside Graphite India's boardroom, there was neither euphoria during the boom nor panic during the bust. The company had used the windfall exactly as intended: to strengthen its competitive position for the next cycle. By early 2019, as electrode prices normalized around $8,000 per ton—still healthy but far from windfall levels—Graphite India emerged with the strongest balance sheet in its history, enhanced technical capabilities, and customer relationships intact.

The China shock taught several crucial lessons. First, in commodity markets, supply disruptions that seem permanent rarely are—human ingenuity and capital eventually solve shortage problems. Second, windfalls should be used to prepare for lean times, not to bet on their continuation. Third, maintaining discipline when everyone else is losing theirs creates lasting competitive advantage.

Looking back, the 2017-2018 windfall was less important for the profits it generated than for what it revealed about Graphite India's organizational character. This was a company that had learned from history, that understood cycles, that could maintain discipline when discipline was hardest. These qualities would prove essential as the industry entered a new phase of technological disruption and environmental transformation.

VII. Modern Operations & Global Footprint

Standing inside Graphite India's Durgapur facility today, you witness an operation that would be unrecognizable to its founders. Robotic arms move three-ton electrodes with millimeter precision. Artificial intelligence algorithms optimize furnace temperatures in real-time. Quality control systems use ultrasonic testing to detect microscopic flaws invisible to human inspection. This is modern electrode manufacturing: a fusion of century-old carbon chemistry with cutting-edge automation.

Graphite India Limited (GIL) is the pioneer in India for manufacture of Graphite Electrodes as well as Carbon and Graphite Speciality products. GIL's manufacturing facilities are spread across 6 plants in India and it has also got a 100% owned subsidiary at Nuremberg, Germany, by name Graphite COVA GmbH. This global footprint isn't just about capacity—it's about capability differentiation across geographies.

The six Indian plants each serve distinct strategic purposes. Durgapur remains the volume leader, producing large-diameter electrodes for India's integrated steel plants. Its proximity to eastern India's steel belt minimizes logistics costs while enabling rapid technical support. The facility has been continuously modernized, with the latest upgrade introducing Industry 4.0 concepts: sensors throughout the production process feed data to a central control room where algorithms predict equipment failures before they occur.

Bangalore houses the innovation engine. Beyond manufacturing ultra-high-power electrodes, it's home to the company's R&D center where 50 scientists work on next-generation carbon materials. Recent breakthroughs include electrodes that can withstand 20% higher current densities and specialty grades for producing aerospace-grade titanium. The facility also pioneers sustainability initiatives, with solar panels providing 30% of power requirements and a zero-liquid-discharge system that recycles every drop of process water.

The Nashik complex represents diversification in action. Here, impervious graphite equipment shares space with GRP pipe manufacturing. The synergies are subtle but powerful: both require expertise in composite materials, both serve chemical process industries, and both benefit from shared logistics and commercial infrastructure. The impervious graphite division has become particularly strategic, with its heat exchangers essential for producing semiconductors—a market growing at 15% annually.

But it's the German subsidiary, Graphite COVA GmbH in Nuremberg, that represents Graphite India's global ambitions. Acquired to serve European customers demanding local supply and technical support, COVA has evolved into something more: a window into developed market customer needs and environmental regulations. European steel makers, facing stringent carbon taxes, demand electrodes that minimize energy consumption. COVA's engineers work directly with these customers, developing solutions that are then transferred to Indian operations.

The numbers paint a picture of truly global reach: 65% of production is exported to over 50 countries worldwide. This isn't commodity trading—each market requires specific product adaptations. Japanese customers demand electrodes that can withstand earthquakes without cracking. Middle Eastern producers need grades that perform in extreme heat. American mini-mills want rapid startup capabilities. Meeting these diverse needs requires not just manufacturing flexibility but deep customer intimacy.

The product portfolio has evolved far beyond traditional electrodes. Calcined Petroleum Coke, once purchased as raw material, is now a product itself, sold to aluminum smelters and titanium producers. High-speed steel from the specialty division commands premium prices in tool-making markets. Impervious graphite equipment serves industries from pharmaceuticals to semiconductors. Each product line shares DNA—carbon expertise—but serves distinct markets with different dynamics.

Energy independence has become a critical competitive advantage. Beyond the 18 MW Karnataka hydel plant, the company has added solar and wind generation capacity. Total renewable generation now exceeds 40 MW, meeting nearly 60% of manufacturing energy needs. In an industry where power represents the largest operating cost, generating your own renewable energy provides both cost advantage and carbon footprint reduction—increasingly important as customers face pressure to decarbonize supply chains.

Quality certifications tell the story of operational excellence: ISO 9001 for quality management, ISO 14001 for environmental management, OHSAS 18001 for occupational health and safety. But beyond certificates, the company has developed proprietary quality systems. Every electrode is individually tracked from raw material to customer delivery. Blockchain technology is being piloted to provide customers with immutable quality records. Artificial intelligence analyzes production data to predict quality issues before they manifest.

The human element remains crucial despite automation. The company employs over 3,000 people, with average tenure exceeding 15 years. This isn't just workforce stability—it's institutional knowledge. The senior furnace operator who can diagnose problems by the sound of the equipment. The quality engineer who knows exactly how monsoon humidity affects baking cycles. The maintenance technician who has memorized the quirks of machines installed decades ago. This tacit knowledge, impossible to codify in manuals, represents a competitive moat as real as any technology.

Customer relationships have evolved from transactional to strategic. Graphite India engineers are embedded at major customer sites, helping optimize electrode consumption. The company offers "cost-per-ton" contracts where payment is based on steel produced rather than electrodes consumed, aligning incentives perfectly. Technical service teams provide 24/7 support, with response times measured in hours, not days. These relationships, built over decades, explain why customers stayed loyal during the allocation shortages of 2017-2018.

Looking at modern operations, what emerges is a company that has successfully straddled multiple worlds: commodity manufacturer and technology innovator, Indian producer and global supplier, traditional industry and modern enterprise. This isn't a story of transformation—it's evolution, each capability built on previous foundations, each innovation preserving what worked while adapting what didn't.

VIII. Technology & Future Bets

The conference room in Graphite India's Bangalore R&D center is an unusual sight in a traditional manufacturing company. On one wall, molecular diagrams of graphene structures. On another, charts tracking battery energy density improvements. At the table, a team discussing artificial intelligence applications in furnace optimization. This is where a company making 20-foot carbon electrodes is betting its future lies: at the intersection of materials science, clean energy, and digital technology.

The most audacious bet came in 2018 when the company invested $18.5 million in General Graphene Corporation, a US company developing technology for mass-producing graphene sheets. To understand why an electrode manufacturer would make such an investment, consider what graphene represents: carbon atoms arranged in a two-dimensional honeycomb lattice, combining strength 200 times greater than steel with electrical conductivity superior to copper, all in a material one atom thick.

Graphene isn't just another advanced material—it's potentially transformative across industries. In batteries, graphene anodes could increase capacity by 50% while reducing charging time to minutes. In composites, graphene reinforcement could create materials light enough for aerospace yet strong enough for armor. In electronics, graphene transistors could operate at frequencies impossible with silicon. The challenge has always been manufacturing: producing high-quality graphene at industrial scale and acceptable cost.

General Graphene's breakthrough technology uses a proprietary process to exfoliate graphene from graphite—essentially unzipping the layered structure of graphite into individual atomic sheets. For Graphite India, this represents perfect backward integration: they produce the graphite feedstock and could become the scaled manufacturer if the technology proves commercially viable. The investment provides not just financial returns but technology transfer, with Indian engineers training at General Graphene's facilities and knowledge flowing both directions.

Beyond graphene, the company is developing carbon-carbon composites for aerospace applications. These materials, made by reinforcing carbon matrices with carbon fibers, maintain strength at temperatures that would melt steel. Indian defense agencies have shown interest in applications ranging from missile nose cones to aircraft brake discs. The technology builds on Graphite India's core competency—high-temperature carbon processing—while opening markets with strategic importance and premium pricing.

The battery chemicals initiative represents another strategic pivot. As electric vehicles proliferate, demand for battery-grade graphite is exploding. But this isn't the same graphite used in electrodes. Battery anodes require 99.95% purity, spherical particle morphology, and specific surface chemistry. Graphite India is developing purification and spheronization technology to transform natural graphite into battery-grade material. Early samples have achieved energy densities competitive with synthetic graphite at potentially half the cost.

Process technology upgradation continues in core electrode manufacturing. The company is implementing digital twins—virtual replicas of physical furnaces that enable simulation of process changes without production risk. Machine learning algorithms analyze decades of production data to identify patterns invisible to human operators. Predictive maintenance systems have reduced unplanned downtime by 40%. These aren't glamorous innovations, but in a capital-intensive industry, small efficiency improvements translate to crores in savings.

The company is also exploring additive manufacturing of graphite components. 3D printing with graphite enables complex geometries impossible with traditional machining. Prototype applications include customized electrode joints that reduce electrical resistance and specialty graphite components for semiconductor manufacturing. While volumes remain small, margins exceed 50%, demonstrating the value of technological differentiation.

Environmental technology has become increasingly critical. The company is developing processes to recycle electrode stubs—the unused portions returned from steel plants—into new electrodes. Carbon capture systems are being tested to reduce greenhouse gas emissions from graphitization furnaces. Water recycling has reached 95%, with plans for zero liquid discharge across all facilities. These investments are driven partly by regulation but increasingly by customer demands for sustainable supply chains.

The R&D organization has been restructured to balance incremental and breakthrough innovation. Core teams focus on continuous improvement—reducing electrode consumption rates, improving mechanical strength, extending campaign life. Advanced teams explore adjacent opportunities—specialty carbons, composites, coatings. Breakthrough teams investigate disruptive technologies—graphene, carbon nanotubes, solid-state battery materials. This portfolio approach ensures steady improvement while maintaining optionality on technological disruption.

Intellectual property has become a strategic focus. The company now holds over 50 patents, with applications pending for 20 more. Patents cover not just products but processes—methods for improving graphitization efficiency, techniques for producing specialty grades, systems for quality control. This IP portfolio provides defensive value against competitors and offensive potential through licensing.

Partnerships with academic institutions have deepened. Collaborations with IIT Bombay focus on computational modeling of carbon structures. Joint projects with the Indian Institute of Science explore bio-based carbon precursors. These relationships provide access to cutting-edge research while building a pipeline of technical talent.

The investment thesis for these technology bets is compelling yet uncertain. If graphene achieves commercial breakthrough, early investors could see 100x returns. If battery-grade graphite demand materializes as projected, margins could double. If carbon composites penetrate aerospace markets, revenue could transform. But these remain "ifs." The electrodes business, unglamorous as it seems, generates the cash flow that funds these bets without requiring external capital or compromising financial stability.

What's clear is that Graphite India is no longer betting solely on steel industry growth driving electrode demand. The company is positioning for a future where carbon materials enable everything from renewable energy storage to space exploration. Whether these bets succeed individually matters less than the organizational capability being built: the ability to innovate in materials science, to commercialize advanced technologies, and to evolve beyond commodity manufacturing.

IX. Financial Analysis & Unit Economics

The spreadsheet on the CFO's desk tells two stories. One is of declining glory: revenue down from ₹5,463 crores in FY2019 to ₹2,497 crores in FY2024, a five-year CAGR of -3.72%. The other is of remarkable resilience: despite this revenue collapse, the company remains profitable with ₹355 crores in net profit and virtually no debt. Understanding this paradox requires diving deep into the unit economics of electrode manufacturing and the financial architecture that enables survival through cycles.

Start with the basic unit economics of producing one metric ton of graphite electrodes. Raw materials—primarily needle coke and coal tar pitch—account for 45-55% of costs, depending on procurement timing and quality grades. Energy represents 25-30%, a massive component that explains why the company's investment in captive power generation provides such strategic advantage. Labor contributes 8-10%, relatively low due to automation but critical for quality. Maintenance and overheads add another 10-15%. At normalized prices of $8,000 per ton and these cost structures, EBITDA margins settle around 18-22%—healthy but not spectacular.

But these averages hide extreme volatility. During the 2017-2018 windfall, when electrode prices touched $35,000 per ton, EBITDA margins exceeded 70%. Raw material costs remained relatively stable as the company had long-term contracts for needle coke. Energy costs were fixed through captive generation. The operating leverage was extraordinary: a 4x increase in price translated to a 10x increase in EBITDA. Conversely, when prices crashed to $3,000 per ton in 2020, margins turned negative on a full-cost basis, though positive on a contribution basis due to the high fixed-cost component.

The working capital dynamics are particularly challenging. The production cycle from raw material to finished electrode spans 3-4 months. Raw materials must be purchased upfront, often with letters of credit for imports. Customers, particularly in India, negotiate 60-90 day payment terms. During upturns, working capital becomes a massive cash drain as the company funds inventory and receivables growth. During downturns, working capital releases provide crucial liquidity but signal underlying business contraction.

The company's response has been sophisticated working capital management. Inventory turns have improved from 3x to 5x through better demand forecasting and production planning. Receivables management has become stringent, with credit insurance for export sales and factoring arrangements for domestic receivables. Payables have been optimized without compromising supplier relationships—critical when needle coke allocation becomes tight during upturns.

Capital expenditure patterns reveal strategic discipline. During the windfall years, when competitors announced massive expansions, Graphite India limited capex to ₹200-300 crores annually, focused on debottlenecking and efficiency improvements. This restraint preserved cash for the downturn while avoiding the curse of peak-cycle capacity additions that plague cyclical industries. Maintenance capex runs ₹100-150 crores annually—non-negotiable in an industry where equipment failure can destroy millions in work-in-process inventory.

The balance sheet structure is remarkably conservative. As of FY2024, the company has virtually no long-term debt, with a debt-to-equity ratio near zero. Cash and investments exceed ₹500 crores, providing a buffer for working capital needs and opportunistic investments. This fortress balance sheet isn't just conservative financial management—it's competitive advantage in an industry where leveraged competitors face existential crisis during downturns.

Return metrics tell the story of cyclicality's impact. Three-year average ROE stands at a modest 4.63%, dragged down by recent years' low profitability. But this average masks extremes: ROE exceeded 50% during the windfall, then turned negative briefly before recovering. ROCE patterns similar volatility. These metrics frustrate investors seeking steady returns but reflect the reality of commodity manufacturing where multi-year losses can be followed by bonanza years that more than compensate patient capital.

The dividend policy balances shareholder returns with financial prudence. The company maintained dividends even during the lost decade, signaling confidence and rewarding long-term shareholders. But payout ratios remain conservative, typically 20-30% of profits, with excess cash retained for cycle management and growth investments. Special dividends during windfall years were notably absent—a sign of management's clear-eyed view of earnings sustainability.

Cost structure analysis reveals both strengths and vulnerabilities. Variable costs at 60-65% provide some downturn protection as production can be curtailed. But high fixed costs mean utilization below 60% generates losses. The company has worked to variabilize fixed costs where possible: outsourcing non-core activities, implementing flexible workforce arrangements, and negotiating power purchase agreements with variable components.

Segment analysis provides insight into diversification's value. While electrodes contribute 80% of revenue, specialty products—impervious graphite equipment, steel products, power generation—provide stable earnings that cushion electrode volatility. These segments earn lower margins but face less competition and cyclicality. During electrode downturns, they've prevented losses from becoming catastrophic.

The cash flow profile demonstrates the business model's resilience. Even in difficult years, operations generate positive cash flow due to working capital management and disciplined capex. Free cash flow yield, based on current market capitalization, exceeds 8%—attractive for a manufacturing company. The challenge is that cash generation is lumpy, with one good year potentially equaling five normal years.

Tax planning has become sophisticated given global operations. The German subsidiary provides access to European tax treaties. Transfer pricing between Indian and German operations optimizes overall tax efficiency while remaining compliant. The company benefits from various Indian government incentives for exports and renewable energy investments, though these contribute marginally to overall profitability.

Looking at financial metrics holistically, what emerges is a company architected for survival rather than growth. Every financial decision—from capital structure to dividend policy—reflects deep understanding of industry cycles. This isn't financial engineering for its own sake but recognition that in commodity industries, the ability to survive downturns with capabilities intact creates more value than aggressive expansion during upturns.

X. Playbook: Lessons in Cyclical Industries

In the boardroom of any cyclical industry company, there's a chart that everyone knows but few truly understand: the commodity price cycle. It looks like a sine wave drawn by someone with trembling hands—irregular peaks and troughs, false breakouts and breakdowns, patterns that seem clear in hindsight but opaque in real-time. Graphite India's six-decade navigation of these cycles offers a masterclass in what works, what doesn't, and what only becomes clear after the fact.

The first lesson concerns family business governance in capital-intensive industries. The Bangur family's approach differs markedly from typical Indian family businesses. There's no visible succession drama, no splitting of businesses among heirs, no diversification into vanity projects. K.K. Bangur has led since 1993—nearly three decades of consistent leadership through multiple cycles. This stability matters enormously in industries where relationships are built over decades and technical knowledge accumulates slowly.

The family maintains majority control—65.3% ownership—but operates with public company discipline. Related party transactions are minimal and transparent. The board includes independent directors with genuine influence. Management compensation is modest by global standards but aligned with long-term value creation through stock ownership. This governance structure provides the patience of family capital with the discipline of public markets—a rare combination.

The approach to capital allocation during cycles deserves particular attention. Most companies in cyclical industries follow predictable patterns: they expand aggressively during upturns when capital is plentiful and prices justify any investment, then cut desperately during downturns when survival becomes paramount. Graphite India does the opposite. Major expansions happen during downturns when equipment is cheap and competitors are distracted. During upturns, the focus shifts to optimization and debt reduction.

This contrarian approach requires exceptional discipline. When electrode prices hit $35,000 per ton in 2018 and analysts projected permanent shortages, the temptation to announce massive expansion must have been overwhelming. Competitors succumbed, announcing capacity additions that would take years to complete. Graphite India limited itself to incremental debottlenecking. When those competitors' capacity came online into a normalized market, they faced years of losses. Graphite India emerged with its balance sheet intact.

The management of stakeholder expectations through cycles is equally instructive. During upturns, management consistently dampens enthusiasm, warning that high prices are temporary and mean reversion inevitable. During downturns, they emphasize operational improvements and long-term positioning rather than promising quick recovery. This communication strategy frustrates momentum investors but attracts long-term capital that understands the business model.

Technical expertise in seemingly commoditized industries provides sustainable advantage. Graphite electrodes appear simple—carbon sticks that conduct electricity. But producing electrodes that can withstand 50,000-ampere currents while maintaining structural integrity requires deep materials science. Graphite India has invested consistently in technical capabilities even when financial returns seemed questionable. This expertise manifests in customer relationships: steel producers trust Graphite India to solve complex furnace problems, creating switching costs that transcend price.

The company's approach to technology adoption balances innovation with pragmatism. They're not early adopters chasing every new technology, nor are they Luddites resisting change. Instead, they fast-follow: letting others prove technologies before implementing improved versions. The digital twin implementation came years after the concept emerged but incorporated lessons from early adopters' failures. This approach may sacrifice first-mover advantages but avoids bleeding-edge risks.

Managing global competition from emerging markets requires strategic clarity. Chinese competitors have cost advantages from scale, subsidies, and lower environmental standards. Rather than matching them on price, Graphite India focuses on segments where quality, reliability, and technical service matter more than cost. This means accepting lower market share but higher margins and more sustainable positions.

Environmental and regulatory changes are viewed as opportunities rather than threats. When India implemented pollution controls, Graphite India had already invested in cleaner technologies. When European customers demanded carbon footprint reporting, the company's renewable energy investments became competitive advantage. This proactive approach to regulation requires upfront investment but prevents crisis response and creates differentiation.

The human capital strategy recognizes that in process industries, institutional knowledge matters more than individual brilliance. The company maintains employment through downturns, accepting short-term costs to preserve long-term capabilities. Training programs are extensive, with operators spending years learning their craft. This approach seems inefficient compared to hiring and firing with cycles, but it creates organizational capabilities that can't be quickly replicated.

Working with customers through cycles builds relationships that transcend transactions. During allocation shortages, Graphite India honored long-term contracts despite spot prices being multiples higher. During oversupply, they provided technical support to help customers optimize electrode consumption. These investments in relationships seem irrational from a pure economic perspective but create customer loyalty that manifests in preferential treatment during the next shortage.

Risk management goes beyond financial hedging to operational resilience. Multiple production sites provide redundancy. Diverse product lines cushion single-market exposure. Long-term raw material contracts balance spot purchases. Captive power generation reduces energy dependence. Each decision slightly reduces returns but dramatically reduces catastrophic risk.

The approach to M&A is notably restrained. Despite numerous opportunities to acquire distressed competitors during downturns, Graphite India has remained selective. The German subsidiary acquisition provided market access and technology. The graphene investment offers optionality on disruption. But there have been no transformative deals, no debt-funded acquisitions, no attempts to roll up the industry. This restraint preserves balance sheet strength and management focus.

Perhaps the most important lesson is the recognition that in cyclical industries, time horizon determines strategy. Quarter-to-quarter, the business appears chaotic. Year-to-year, patterns emerge but remain unpredictable. Decade-to-decade, the logic becomes clear: patient capital, operational excellence, and financial conservatism compound into sustainable competitive advantage.

XI. Bear vs. Bull Case

The investment debate around Graphite India crystallizes into two diametrically opposed narratives, each supported by compelling evidence yet reaching contradictory conclusions. Understanding both perspectives—not to resolve them but to appreciate their tension—provides insight into the company's fundamental investment proposition.

The Bear Case: Structural Decline Masked by Cyclical Recovery

Bears begin with a stark observation: China is expected to have Graphite Electrode capacity totalling 1.5 MnT by 2020, up 67% against 2017. With the increase in electric furnace steel, the demand for Graphite Electrodes will simultaneously rise, but the current utilization rate is only 53.33%. By 2020, production and sales will not exceed 800,000 tonnes, thus resulting in overcapacity. This overcapacity isn't temporary—it's structural, built on China's strategic push to dominate global carbon markets.

The technology disruption argument is equally concerning. Hydrogen-based steel production, while still experimental, could eliminate the need for electrodes entirely. Swedish company SSAB's HYBRIT project has already produced fossil-free steel using hydrogen reduction. If this technology scales—and European carbon taxes provide powerful incentives—electrode demand could face existential threat within a decade.

Bears point to the company's recent financial performance as evidence of secular decline. Five-year revenue CAGR of -3.72% isn't just cyclical weakness—it's market share loss to more aggressive competitors. ROE averaging 4.63% over three years destroys value relative to the cost of capital. These aren't metrics of a company with sustainable competitive advantages.

The customer concentration risk is severe. Five customers account for over 40% of revenue. These steel giants have enormous negotiating leverage, particularly as global steel production growth slows. India's steel capacity additions, while impressive, can't offset weakness in developed markets where electric arc furnace adoption has plateaued.

Environmental regulations pose escalating challenges. Graphitization, the core process in electrode manufacturing, is inherently energy-intensive and carbon-emitting. As carbon taxes spread globally, production costs will rise disproportionately for energy-intensive industries. The company's renewable energy investments, while admirable, can't offset the fundamental carbon intensity of the process.

The graphene and battery materials investments, bears argue, are expensive distractions. Graphene has been "five years from commercialization" for two decades. Even if breakthroughs occur, established chemical giants like BASF and Dow have far greater resources to dominate these markets. Graphite India's $18.5 million investment is a rounding error compared to what scaling graphene production would actually require.

Market valuation already prices in recovery that may not materialize. At ₹10,494 crores market cap for a company earning ₹355 crores, the P/E ratio of 30x seems excessive for a cyclical commodity manufacturer. The market is betting on return to windfall conditions that were anomalous, not normal.

The Bull Case: Misunderstood Compounder with Asymmetric Upside

Bulls counter with equally compelling logic. Start with the macro picture: India's infrastructure ambitions are staggering. India has been concentrating on increasing its steel production capacity and has set an ambitious goal of 300 million tons by 2030. India is actively adopting EAF technology to achieve this objective, significantly increasing demand for graphite electrodes. This isn't speculative—it's government policy backed by massive capital allocation.

The China overcapacity argument misses crucial nuance. "[Increased] EAF [usage] could be a general trend for steelmaking in China, [because this] is what national policies have been encouraging. With more EAF usage, graphite electrode demand is bound to increase." EAF steelmaking technologies have been strongly encouraged by decision-making bodies in China in attempts to reduce carbon emissions. Chinese capacity may grow, but so will Chinese consumption as environmental regulations force blast furnace closures.

Bulls see the financial metrics differently. The recent underperformance reflects the bottom of the electrode cycle, not structural decline. The company remained profitable even at cycle troughs—a testament to operational excellence. The balance sheet, with virtually no debt and substantial cash, provides optionality for the next upturn without dilution risk.

The technology investments aren't distractions but real options on disruption. Battery-grade graphite demand is exploding with EV adoption. If Graphite India captures even 1% of this market, it could double current revenues. The graphene investment provides exposure to potentially transformative technology with limited downside given the small investment size.

Operational excellence provides unappreciated moat. Producing UHP electrodes that can withstand extreme furnace conditions requires decades of accumulated expertise. Chinese competitors can match capacity but struggle with quality consistency. When steel producers run $100 million furnaces, they don't risk operations to save 10% on electrode costs.

The renewable energy strategy positions the company for carbon-adjusted competition. As carbon border taxes spread, Graphite India's renewable-powered production provides cost advantage over coal-dependent competitors. This isn't CSR window-dressing but strategic positioning for carbon-constrained markets.

Management quality deserves premium valuation. The Bangur family's track record through cycles demonstrates exceptional capital allocation. Their conservative approach may frustrate during upturns but preserves capital for opportunistic deployment. In cyclical industries, survival is strategy, and Graphite India has survived when many haven't.

The risk-reward is asymmetric. Downside is limited by asset value—the company's plants, technology, and working capital provide floor valuation around current levels. But upside could be multiples if electrode markets tighten again. China's dual control policy, infrastructure spending, or supply disruptions could trigger another shortage cycle.

The dividend yield provides payment for patience. Even at cycle troughs, the company maintains dividends, providing 2-3% yield. For patient investors, this income stream funds the wait for cycle recovery while maintaining exposure to significant upside.

The Synthesis: A Complex Reality

The truth, as always in cyclical industries, likely lies between extremes. Graphite India faces real structural challenges: Chinese competition, technology disruption, environmental pressures. But it also possesses genuine strengths: operational excellence, financial conservatism, strategic positioning in growing markets.

The investment case ultimately depends on time horizon and risk tolerance. For traders seeking momentum, better opportunities exist elsewhere. For value investors seeking asymmetric risk-reward, the current valuation may offer opportunity. For quality-focused investors, the cyclicality may prove too volatile regardless of underlying business strength.

What's clear is that Graphite India defies simple categorization. It's neither dying dinosaur nor hidden gem, neither value trap nor growth story. It's a complex industrial company navigating technological change, geopolitical shifts, and environmental transformation while managing brutal commodity cycles. Understanding this complexity—rather than simplifying it—is prerequisite for informed investment decisions.

XII. Epilogue: The Future of Carbon

The periodic table holds 118 elements, but only one—carbon—defines both our industrial past and our sustainable future. This paradox sits at the heart of Graphite India's next chapter. The company makes products from carbon for industries that must decarbonize. It enables steel production that governments want to make green. It powers electric arc furnaces that replace blast furnaces, trading one carbon form for another. In this contradiction lies both existential challenge and unprecedented opportunity.

Consider the absurdity and elegance of the situation: The world needs to reduce carbon emissions to prevent climate catastrophe. Yet carbon materials—graphite for batteries, carbon fiber for lightweight vehicles, graphene for next-generation electronics—are essential for the low-carbon transition. Graphite India sits at this intersection, making carbon products that enable decarbonization. It's like being an ice vendor in the age of refrigeration who discovers their ice is essential for making semiconductors.

India's industrial ambitions add another layer of complexity. The country needs to build infrastructure for 1.4 billion people while meeting climate commitments. This requires massive steel production—bridges, railways, buildings, factories. China is expected to increase its steel scrap usage by 23% to 320 million tons by 2025 to meet its climate commitments. With China rapidly trying to increase its steel production through EAFs, which require graphite electrodes, the market for graphite electrodes is expected to rise. The increase in EAF production is projected to increase steel scrap usage and generate tremendous opportunities for growth. The same dynamics apply to India, where steel demand will grow even as production methods must become cleaner.

The company's response to this paradox reveals strategic sophistication. Rather than defending the status quo or pivoting entirely, Graphite India is straddling both worlds. It continues making electrodes for steel production while investing in graphene for next-generation applications. It powers operations with renewable energy while serving carbon-intensive industries. It improves efficiency in traditional products while exploring breakthrough technologies.

This dual strategy makes sense when you understand that transitions take decades, not years. Electric vehicles may eventually dominate transport, but billions of conventional vehicles will be produced in the interim. Hydrogen steel might revolutionize production, but hundreds of electric arc furnaces will be built before then. The future may be carbon-neutral, but the path there runs through carbon materials.

The organizational capabilities built over six decades position Graphite India uniquely for this transition. The company understands carbon at a molecular level—how atoms arrange into different structures, how temperature and pressure transform properties, how to manipulate carbon into forms with seemingly contradictory characteristics. This knowledge doesn't become obsolete with decarbonization; it becomes more valuable as carbon materials enable the transition.

Can old-economy companies become new-economy winners? The question misses the point. Graphite India was never just an old-economy company—it was always a materials science company that happened to serve traditional industries. The same expertise that makes electrodes work at 3,000°C can develop batteries that charge in minutes. The same quality control that ensures electrode consistency can produce graphene with atomic precision. The capabilities remain relevant; only the applications change.

The investment implications are profound yet uncertain. If Graphite India successfully navigates this transition—maintaining electrode cash flows while building new growth engines—returns could be spectacular. But if technology shifts faster than expected or execution falters, the company could face terminal decline. This isn't a simple bet on mean reversion or secular growth, but a complex wager on management's ability to evolve while surviving.

K.K. Bangur, now in his fourth decade leading the company, understands this challenge intimately. In recent investor calls, he speaks less about electrode prices and more about technology development. The company's capital allocation has shifted from capacity expansion to capability building. The organization structure now includes teams focused on applications that don't yet generate revenue. This isn't transformation for its own sake but recognition that standing still means falling behind.

The broader lesson transcends Graphite India or even manufacturing. In a world of accelerating change, the most valuable asset isn't what you produce but your ability to adapt production. The most sustainable advantage isn't market position but organizational capability to evolve. The best strategy isn't predicting the future but maintaining optionality to capitalize on multiple futures.

As we conclude this exploration of Graphite India, what emerges is not a simple investment thesis but appreciation for complexity. This is a company that embodies contradictions: family-owned yet professionally managed, traditional yet innovative, Indian yet global, carbon-intensive yet enabling decarbonization. These contradictions aren't weaknesses to be resolved but tensions to be managed.

The final reflection brings us back to the beginning: those massive electrodes glowing white-hot in furnaces, channeling enormous energy to transform scrap into steel. It's a 100-year-old process that remains irreplaceable, performed by a 60-year-old company that continues evolving. In the end, Graphite India's story isn't about electrodes or graphene or batteries. It's about the remarkable ability of human organizations to persist, adapt, and occasionally thrive through cycles of creative destruction.

Whether Graphite India succeeds in its transition from electrode manufacturer to carbon technology company remains unknown. What's certain is that the attempt—rooted in six decades of operational excellence, guided by patient capital, and enabled by technical expertise—deserves attention from anyone interested in how traditional industries navigate technological disruption. The outcome may be uncertain, but the process offers lessons that transcend industries, geographies, and time.

In carbon we trust, until we don't, and then we trust in something else carbon enables. That's not paradox—that's progress.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube