Tilaknagar Industries: India's Brandy Empire

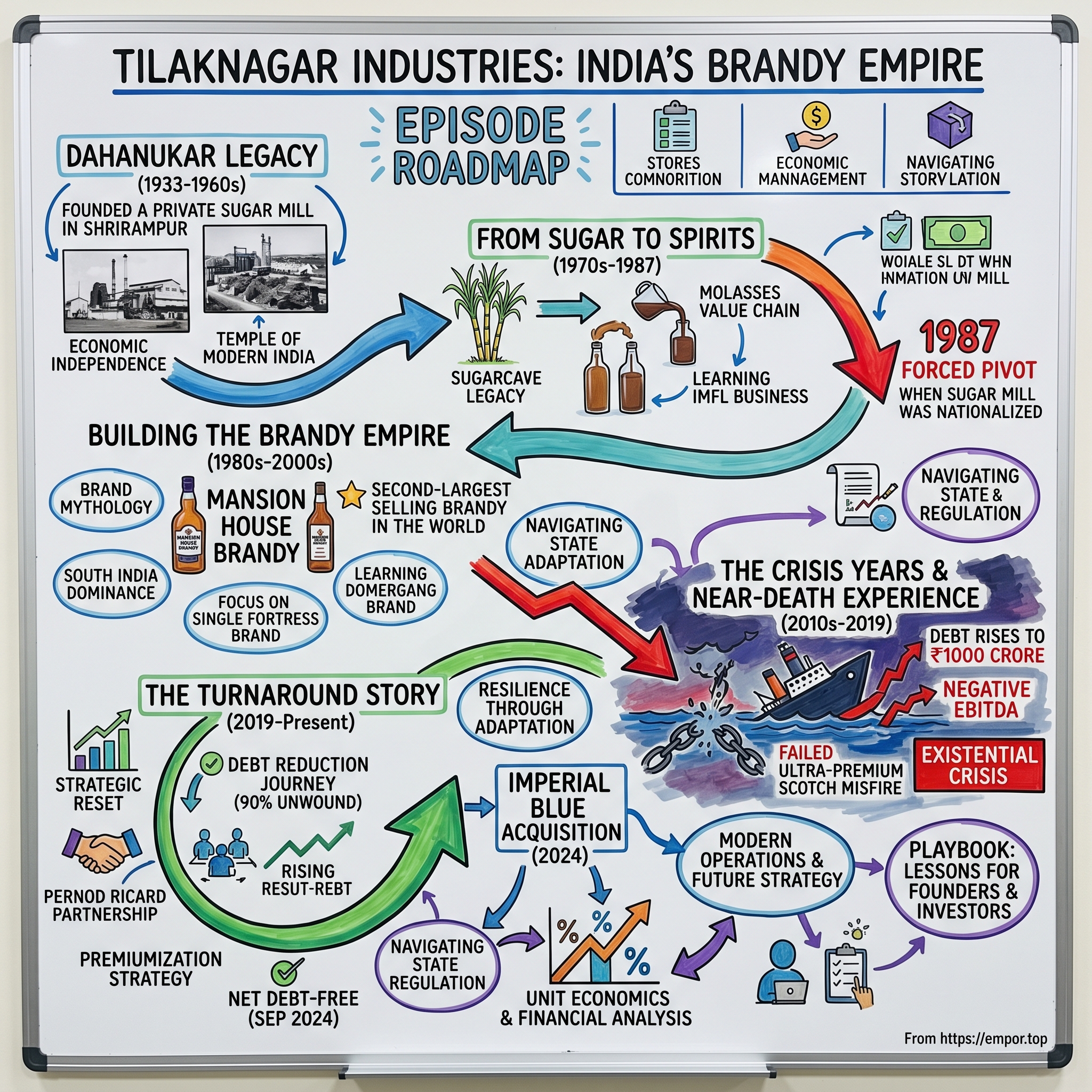

I. Introduction & Episode Roadmap

Picture this: In the heart of Maharashtra's sugarcane fields, where molasses flows like liquid gold, stands a distillery empire that almost nobody outside India has heard of—yet it produces the second-largest selling brandy brand in the world. Not France. Not Spain. But Shrirampur, Maharashtra, population 88,000.

Tilaknagar Industries commands a market capitalization of ₹9,568 crore with revenues touching ₹1,530 crore. The company's flagship Mansion House Brandy moves more bottles annually than Hennessy in volume terms—a staggering achievement for a brand most Western spirits connoisseurs couldn't identify in a blind tasting. This is the paradox of Indian liquor: massive scale hiding in plain sight, trapped behind state borders and regulatory mazes that would make American Prohibition look straightforward.

The central question isn't just how a pre-independence sugar mill became India's brandy powerhouse. It's how any company survives—let alone thrives—in an industry where your product is illegal in some states, heavily taxed in others, and where distribution rights can vanish overnight with a change in government. This is a story of forced pivots, near-death experiences, and the peculiar alchemy of turning sugarcane waste into liquid gold.

What makes Tilaknagar fascinating isn't just its survival—it's what the company reveals about Indian capitalism itself. Here's a business that embodies every contradiction of the Indian market: sophisticated enough to produce world-class spirits, yet operating in a regulatory environment that treats alcohol like controlled contraband; large enough to dominate categories, yet small enough to be nearly crushed by debt just five years ago; modern enough for ESG initiatives, yet rooted in pre-independence industrial traditions.

The themes we'll explore cut deeper than spirits. This is about nation-building through private enterprise, about families who named factories after freedom fighters, about what happens when the government suddenly declares your core business illegal, and about building consumer brands in markets where advertising your product is often banned. It's the Acquired playbook, but played on hard mode—where every state is a different country, every excise policy a potential existential threat, and where success means convincing millions of Indians that French-sounding brandy made in Maharashtra is worth choosing over traditional arrack or imported Scotch.

II. The Dahanukar Legacy & Founding Vision (1933–1960s)

The year was 1933. While Gandhi led salt marches and the British Raj tightened its grip, a Maharashtrian industrialist named Shri Mahadev L. Dahanukar was plotting something audacious: India's first private sugar mill. Not a British-owned enterprise. Not a princely state venture. But a genuinely Indian private industrial undertaking at a time when Indians weren't supposed to be industrialists.

Dahanukar wasn't just building a sugar mill—he was making a statement. The Maharashtra Sugar Mills Limited represented something profound in pre-independence India: the possibility of Indian industrial self-sufficiency. While the Congress debated political freedom, entrepreneurs like Dahanukar were laying the groundwork for economic independence, one factory at a time.

The choice of sugar wasn't accidental. Sugar represented both sustenance and sovereignty. The British had long controlled India's sugar trade, importing refined sugar while India exported raw sugarcane—the classic colonial value extraction model. Dahanukar's mill would flip this equation, processing Indian sugarcane into Indian sugar for Indian consumers. It was import substitution before economists had coined the term.

But what set Dahanukar apart was his naming decision. When it came time to christen his production facilities, he didn't name them after himself or seek some Sanskrit invocation of prosperity. Instead, he named them Tilaknagar—Tilak's City—after his friend Bal Gangadhar Tilak, the firebrand freedom fighter who had declared "Swaraj is my birthright." This wasn't just sentiment; it was positioning. In one stroke, Dahanukar aligned his industrial project with the freedom movement, making his factory floors an extension of the independence struggle.

The pre-independence business environment was brutal for Indian entrepreneurs. The British had structured the economy to favor their own trading houses and manufacturers. Railways were built not to connect Indian markets but to move raw materials to ports. Banking was controlled by British institutions that rarely lent to Indian industrialists. The regulatory framework—from licensing to taxation—was designed to maintain British commercial supremacy.

Yet Dahanukar persevered. He understood something crucial: in a colonized economy, building industrial capacity was itself an act of rebellion. Every ton of sugar processed in Tilaknagar was a ton that didn't need to be imported from British refineries. Every worker employed was a family freed from agricultural dependency. Every profit retained was capital that could fund further Indian enterprise.

The Dahanukar family ethos emerged from this crucible. They weren't just businessmen; they saw themselves as nation-builders. The sugar mill wasn't just a commercial venture; it was infrastructure for a free India that didn't yet exist. This vision—of business as patriotic duty—would define Tilaknagar's culture for generations.

By the 1940s, as independence approached, Maharashtra Sugar Mills had become one of western India's industrial success stories. The company had proven that Indians could build and operate complex industrial enterprises. They had created a template: take an agricultural commodity, add industrial processing, create employment, reduce imports, build wealth. It was a playbook that newly independent India would desperately need.

The timing proved prescient. When independence arrived in 1947, India inherited an economy that was 85% agricultural, with virtually no industrial base. Entrepreneurs like Dahanukar, who had built capacity during the colonial period, suddenly found themselves as pillars of the new nation's economic architecture. The Maharashtra Sugar Mills wasn't just a sugar company anymore—it was part of Nehru's "temples of modern India."

Through the 1950s and 1960s, the company thrived in the controlled economy of the License Raj. While the socialist framework constrained many businesses, established players like Dahanukar had an advantage: they already had the licenses, the land, the infrastructure. The very regulations meant to control capitalism ended up protecting incumbents. Maharashtra Sugar Mills expanded steadily, adding capacity and integrating vertically.

But beneath this success lay a ticking time bomb. The sugar industry's real value didn't lie in sugar—it lay in molasses, the black gold byproduct that could be distilled into alcohol. The Dahanukars knew this. They had been experimenting with alcohol production since the 1960s, seeing it as natural value addition. What they didn't know was that government policy would soon force them to choose between sugar and spirits—and that this forced choice would define Tilaknagar's destiny for the next half-century.

III. From Sugar to Spirits: The Forced Pivot (1970s–1987)

The boardroom at Maharashtra Sugar Mills in 1973 must have felt electric with possibility. The directors had just approved a diversification that seemed like natural evolution: moving into industrial alcohol and Indian Made Foreign Liquor. After four decades of crushing sugarcane, they would now distill its byproduct into something far more valuable. Nobody in that room could have imagined that within 14 years, the government would essentially confiscate their core sugar business, forcing them to bet everything on this new venture.

The year 1973 marked Tilaknagar Industries' entry into what would become its destiny: industrial alcohol, IMFL, and even sugar cubes—a peculiar portfolio that made perfect sense if you understood the molasses value chain. Every ton of sugar produced yielded molasses, and molasses could become industrial alcohol, which could become potable alcohol, which could become branded spirits. It was vertical integration at its most elegant.

Maharashtra's decades of sugar production had created an unexpected advantage. The company didn't just understand molasses as a byproduct—they understood its chemistry, its seasonality, its storage challenges, its transportation economics. When sugar mills across India treated molasses as waste to be disposed of, Tilaknagar saw liquid gold waiting to be refined. This expertise would prove invaluable as they entered the complex world of alcohol production.

Learning the IMFL business, however, was like learning a new language while blindfolded. The sugar business was straightforward: crush cane, extract juice, crystallize sugar, sell to distributors. The liquor business was byzantine: source molasses, ferment, distill, age, blend, bottle, then navigate a maze of state excise policies, distribution monopolies, and consumption regulations that changed at every state border. If sugar was arithmetic, spirits was calculus.

The company's first attempts at creating IMFL brands were earnest but unremarkable. They produced rum—a natural choice given their molasses base—and attempted gin and whisky. The products were technically competent but lacked distinction. In a market dominated by established players like McDowell's and inherited British brands, Tilaknagar was just another contract manufacturer trying to build a brand.

Then came 1987—the year everything changed. The Maharashtra government, in a stunning act of socialist overreach, declared that all sugar production would henceforth be managed exclusively by cooperative societies. Private sugar mills were effectively nationalized without compensation, forced to cease operations or convert to cooperatives. For Maharashtra Sugar Mills, it was an existential shock. Their core business, built over 54 years, was suddenly illegal.

The irony was devastating. A company founded on the principle of Indian private enterprise, named after a freedom fighter, was having its freedom stripped away by the very government that freedom fighter had helped create. The Dahanukar family faced a choice: fight a probably futile legal battle, accept cooperative conversion and lose control, or pivot entirely to their nascent alcohol business.

They chose the pivot—not because they wanted to, but because they had to. The sugar mill assets were frozen, but the distillery could continue. The company would have to transform from a sugar company with an alcohol division into an alcohol company that used to make sugar. It was corporate reincarnation under duress.

The forced transformation revealed both vulnerabilities and hidden strengths. The vulnerability was obvious: they had lost their primary business and steady cash flow. The strength was subtler: they owned one of Maharashtra's most efficient distilleries, had relationships with molasses suppliers across the state, and understood alcohol production at a molecular level. While competitors outsourced distillation, Tilaknagar controlled the entire process.

Re-learning the business from scratch meant understanding that IMFL wasn't about production—it was about three things: brand building in a market where advertising was restricted, distribution in a state-controlled system, and managing working capital in a business with long cash cycles. Each presented unique challenges.

Brand building without traditional advertising required creativity. Since liquor ads were banned in most media, companies relied on surrogate advertising—promoting soda water or music CDs that happened to share the brand name. Tilaknagar experimented with everything from Mansion House playing cards to calendar art, learning that in the absence of mass media, point-of-sale presence was everything.

Distribution was even more complex. Each state had different rules—some had government monopolies, others allowed private wholesale but controlled retail, still others had auction systems for licenses. Tilaknagar had to build separate strategies for each state, essentially running 20 different businesses within India. They learned that in Tamil Nadu, palmyra toddy shops were the key channel, while in Canteen Stores Department territories, military procurement officers were the gatekeepers.

The working capital challenge nearly killed them multiple times. Alcohol had to be produced, aged, bottled, shipped to government warehouses, sold, and then payment collected—a cycle that could stretch six months. Meanwhile, excise duties had to be paid upfront. The company was perpetually cash-strapped, borrowing to fund growth, then growing to service borrowing.

By 1990, the forced pivot was complete. Tilaknagar Industries was no longer a sugar company—it was a spirits company, whether it liked it or not. The question now was whether it could survive in an industry where it was a forced immigrant rather than a native. The answer would come from an unlikely source: brandy, a category most Indians didn't even know they wanted.

IV. Building the Brandy Empire: Mansion House (1980s–2000s)

The conference room in Shrirampur, 1984. The marketing team had spread out bottles across the table—McDowell's No.1, Haywards, Bagpiper, Old Monk. All successful. All brown spirits. All targeting the vast Indian middle class emerging from the License Raj. The question on everyone's mind: What gap exists in this market that Tilaknagar could fill?

The answer came from an unexpected insight. While whisky dominated aspiration and rum owned nostalgia, brandy occupied a curious middle ground—sophisticated enough to gift, affordable enough to drink, and crucially, perceived as "smoother" than whisky by the Indian palate accustomed to sweet flavors. The team didn't know it yet, but they had identified what would become a 300-million-liter annual category.

Creating Mansion House wasn't just about liquid in a bottle—it was about crafting mythology in a market that bought stories as much as spirits. The name itself was a masterstroke of positioning. "Mansion House" evoked British colonial grandeur while being entirely Indian-made. It suggested premium heritage without premium pricing. In a country where foreign-sounding names carried cache, Mansion House sounded imported while being fundamentally swadeshi.

The early years were brutal. In 1985, Mansion House sold barely 50,000 cases. Distributors were skeptical—why stock another brown spirit when whisky was flying off shelves? Retailers were dismissive—their customers asked for whisky or rum, never brandy. The sales team spent more time educating than selling, explaining that brandy was made from grapes (even though theirs was made from molasses), that it was popular in Europe (though their version would horrify a Cognac producer), and that it mixed better with water than whisky (a crucial consideration for value-conscious Indian drinkers who stretched every bottle).

The breakthrough came from two unexpected channels: the Canteen Stores Department and South India, particularly Andhra Pradesh and Tamil Nadu. The CSD, which supplied alcohol to military personnel, became an early adopter. Military officers, exposed to global spirits during postings, understood brandy as a category. More importantly, CSD's price advantages made Mansion House exceptional value—premium positioning at economy prices.

South India proved even more crucial. The Tamil palate, influenced by centuries of palm toddy consumption, preferred sweeter, smoother spirits. Brandy fit perfectly. While North India remained whisky territory, Mansion House began dominating Tamil Nadu and Andhra Pradesh. By 1990, the brand was selling more in Hyderabad than in Mumbai, more in Chennai than in Delhi. Tilaknagar had discovered something profound: in a country as diverse as India, you didn't need to win everywhere—you needed to dominate somewhere.

Understanding the Indian consumption pattern became Tilaknagar's secret weapon. They observed that Indian drinkers rarely drank neat spirits—everything was mixed with water or soda. This meant smoothness mattered more than complexity. They noticed that bottles were often shared among groups, making the 180ml "quarter" bottle more popular than full bottles. They learned that Indians drank spirits with food, not as aperitifs, requiring different flavor profiles than Western spirits.

Distribution in state-controlled markets required political savvy as much as business acumen. Each state change of government could upend distribution arrangements. Tamil Nadu's TASMAC (state monopoly) could change procurement policies overnight. Karnataka's excise department could alter taxation without warning. Tilaknagar learned to maintain relationships across political parties, bureaucratic levels, and regional power structures. They became experts not just in distillation but in navigation—through India's labyrinthine alcohol regulations.

The 1993 merger that created modern Tilaknagar Industries brought new complexity but also new capability. The company now had production facilities across Maharashtra, distribution networks across South India, and brands across categories. The merger wasn't just corporate consolidation—it was the creation of a platform that could support Mansion House's ambitious growth.

Building brand loyalty without traditional advertising required guerrilla tactics. Tilaknagar pioneered what they called "touch point marketing"—being present at every moment of potential consumption. They sponsored local festivals where advertising was allowed. They created elaborate point-of-sale displays that served as mini-billboards. They distributed branded glasses to bars, ensuring every drink served reminded consumers of Mansion House. When regulations prevented them from advertising the liquor, they advertised "Mansion House Premium Water"—which happened to share the same logo.

The fight against established players was asymmetric warfare. United Spirits had deeper pockets, Radico Khaitan had better distribution, regional players had local political connections. Tilaknagar's weapon was focus. While competitors managed portfolios of 20-30 brands, Tilaknagar bet everything on Mansion House. Every rupee of marketing, every sales incentive, every management minute focused on building this single fortress brand.

By 2000, the strategy had worked—perhaps too well. Mansion House had become the largest-selling brandy in India, moving over 4 million cases annually. But success brought new challenges. The company had built a castle on a foundation of debt, borrowing to fund growth, assuming that scale would eventually deliver profitability. They had created a successful brand but not necessarily a successful business. The next decade would test whether Mansion House was a genuine empire or just an elaborate facade.

Regional preferences had crystallized into market dominance. In Andhra Pradesh, Mansion House commanded over 60% of the brandy market. In Tamil Nadu, it was the second-largest spirits brand across all categories. The CSD channel, covering military bases across India, provided steady, profitable volume. Yet North India remained unconquered territory, skeptical of brandy, loyal to whisky, and controlled by different power structures.

The two-decade journey from startup brand to market leader had transformed Tilaknagar from a forced pivot survivor into a genuine spirits player. But building a brand and building a sustainable business are different achievements. As the millennium turned, Mansion House sat atop the Indian brandy market—a throne that would soon prove as precarious as it was prominent.

V. The Crisis Years & Near-Death Experience (2010s–2019)

The Tilaknagar board meeting in 2010 should have been a celebration. Mansion House was selling 8 million cases annually, revenues had crossed ₹1,000 crore, and the company had just launched ambitious expansion plans. Instead, the CFO was explaining why, despite record sales, the company was technically insolvent. Debt had ballooned to ₹800 crore, interest coverage was negative, and working capital had evaporated. Success, it turned out, could be more dangerous than failure.

The debt accumulation hadn't happened overnight—it was death by a thousand cuts, each seeming reasonable at the time. Expand production? Borrow. Enter new states? Borrow. Launch premium variants? Borrow. Build inventory for peak season? Borrow. Fight price wars with United Spirits? Borrow and discount. The alcohol business's cruel mathematics meant that growth consumed cash rather than generated it. Every case sold required upfront excise payment, inventory holding, credit to distributors, and prayers that the government wouldn't change payment terms.

Then came the ambitious misfire that would haunt them for years: Seven Islands. In 2012, Tilaknagar announced with great fanfare the launch of an ultra-premium Scotch whisky, produced at Scotland's BenRiach distillery, positioned for global luxury markets. The London launch was lavish—crystal decanters, celebrity endorsements, talk of challenging Johnnie Walker Blue Label. It was Tilaknagar's moonshot, their attempt to escape the low-margin domestic game.

Seven Islands crashed harder than anyone anticipated. The global luxury market didn't care about an unknown Indian company's Scottish experiment. The brand lacked the heritage story that luxury consumers paid for. Distribution costs in international markets ate through margins. Most damaging, management attention shifted from their core Indian business to this Scottish adventure. By 2014, Seven Islands was effectively dead, leaving behind millions in sunk costs and damaged credibility.

The operational challenges went deeper than failed experiments. Tilaknagar had grown through a patchwork of owned facilities, leased units, and contract manufacturers—12 production sites spread across India. Each operated as a fiefdom with different cost structures, quality standards, and reporting systems. The company didn't have one supply chain—it had a dozen, none talking to each other. Inventory piled up in some locations while others faced stockouts. Working capital became a black hole that consumed cash without explanation.

State regulatory changes became existential threats rather than manageable risks. When Andhra Pradesh banned alcohol in 2019, Tilaknagar lost 30% of revenues overnight. When Tamil Nadu changed its procurement policy, payment terms stretched from 45 to 120 days. When Maharashtra increased excise duties, margins evaporated. The company that had built its fortune navigating state regulations was now drowning in them.

Management musical chairs reflected the chaos. Between 2010 and 2018, Tilaknagar had five different CEOs. Each arrived with transformation plans—premiumization, cost-cutting, geographic expansion, portfolio rationalization. Each left with those plans half-executed, creating strategic whiplash. The organization, once focused entirely on Mansion House, now pulled in multiple directions simultaneously, achieving nothing completely.

The 2015 takeover attempt by Allied Blenders & Distillers should have been salvation. Allied offered to acquire Tilaknagar, assuming its debt, providing growth capital, and combining complementary portfolios. Due diligence began, bankers were appointed, and employees started dreaming of stability. Then it fell apart—reportedly over valuation disputes, though insiders suggested Allied had discovered problems that even Tilaknagar's management didn't fully understand.

When the deal collapsed, it triggered a crisis of confidence. Lenders who had been patient expecting Allied's backing suddenly demanded action. Suppliers who had extended credit started demanding cash upfront. Distributors, sensing weakness, delayed payments. The stock price crashed 70% in three months. Tilaknagar wasn't just financially distressed—it was in a death spiral where each problem created two more.

By 2017, the situation was desperate. Debt had crossed ₹1,000 crore while EBITDA turned negative. The company was borrowing to pay interest, selling assets to fund operations, and pledging everything including the promoter's shares to stay afloat. Plants operated at 40% capacity because there was no working capital to buy molasses. Sales teams were demoralized, with top performers jumping to competitors. Brand equity, built over decades, eroded as quality became inconsistent and availability sporadic.

The fight for survival required choosing between bad options. Should they sell Mansion House, their crown jewel, to raise cash? Should they shut down unprofitable states and cede market share permanently? Should they accept dilution at distressed valuations? Every choice felt like amputation—cutting off parts of the business to save the whole.

The regulatory environment, always challenging, became actively hostile. States saw distressed alcohol companies as easy targets for revenue extraction. Excise duties increased, new fees appeared, payment terms worsened. The Reserve Bank of India classified Tilaknagar's loans as non-performing assets, triggering provisioning requirements that made new lending impossible. The company that had survived the government confiscating its sugar business now faced the market confiscating its future.

Yet somehow, Tilaknagar limped through. Not thriving, barely surviving, but not quite dying either. Mansion House, despite everything, kept selling—testament to brand loyalty built over decades. The distribution network, threadbare but intact, continued moving product. The production facilities, undermaintained but functional, kept distilling. It was corporate persistence through inertia—too established to die quickly, too wounded to recover alone.

By 2019, Tilaknagar Industries presented a paradox: owner of India's largest brandy brand, generator of ₹1,500 crore in revenues, yet technically bankrupt. The company needed more than financial restructuring—it needed resurrection. That resurrection would come from an unexpected source: new management with a radical idea—what if Tilaknagar stopped trying to be everything and focused on being excellent at one thing?

VI. The Turnaround Story (2019–Present)

The new management team that walked into Tilaknagar's Shrirampur headquarters in late 2019 faced a crime scene of corporate destruction. Debt exceeded market capitalization by 300%. Plants were running at survival-mode capacity. The sales team hadn't received incentives in quarters. Morale had collapsed so thoroughly that security guards were checking employees for stolen inventory. Yet within five years, this same company would be virtually debt-free, delivering 26.5% profit CAGR, and signing production deals with Pernod Ricard. The turnaround ranks among the most dramatic in Indian corporate history.

The strategic reset began with brutal simplification. The previous decade's strategy could be summarized as "try everything, hope something works"—premium whisky, value rum, export ventures, contract manufacturing, real estate development. The new approach was monastically focused: Mansion House brandy was the core, everything else was negotiable. SKUs were slashed from 50 to 15. States where the company lost money for five consecutive years were abandoned. The entire organization would march behind a single flag. The debt reduction journey was nothing short of miraculous. From a peak of Rs 1,199 crore as of March 2019 to Rs 323 crore as of December 2022, the company systematically unwound decades of financial mismanagement. The February 2020 Master Restructuring Agreement with Edelweiss Asset Reconstruction Company became the turning point—not just restructuring debt but creating a roadmap where every milestone achieved triggered debt waivers. A debt waiver of Rs 126.63 crore was given by EARC following prepayments, effectively turning creditors into partners in the turnaround.

Operational efficiency became religion. The company discovered it was bleeding cash from a thousand cuts—unoptimized logistics routes, excess inventory at wrong locations, energy-inefficient distillation, overstaffing in some plants while others ran understaffed. A consulting firm would have charged millions for the insights Tilaknagar generated internally: consolidate production in efficient facilities, optimize the supply chain for speed not size, and treat working capital like oxygen—essential but toxic in excess.

The focus on core brands delivered immediate results. By concentrating all marketing spend on Mansion House and its variants, the brand achieved something remarkable—growth without heavy promotion. Market share in core territories increased even as overall marketing expenses decreased. The company discovered that in spirits, consistency matters more than creativity. Consumers wanted their Mansion House to taste the same every time, be available always, and priced predictably.

Then came the masterstroke: the Pernod Ricard partnership. The Company has commenced production of brands of French multinational Pernod Ricard India Private Limited at its Shrirampur bottling facility in Maharashtra, from February 15, 2022. This wasn't just contract manufacturing—it was validation. Pernod, with its global standards, was trusting Tilaknagar with production. The partnership brought steady revenue, improved capacity utilization, and most importantly, forced Tilaknagar to upgrade its quality systems to international standards.

The premiumization strategy emerged organically from market feedback. Mansion House Chambers, launched in 2023, targeted the growing segment of consumers willing to pay more for perceived quality. Monarch Legacy Edition, positioned as luxury brandy, seemed audacious for a company that nearly died from debt. Yet it worked—not in volumes but in changing perception. If Tilaknagar could make luxury brandy, perhaps their regular brandy was better than assumed.

Geographic expansion followed a conservative playbook—no grand conquests, just steady infiltration. Instead of attacking whisky strongholds in North India, Tilaknagar focused on brandy-friendly pockets within hostile territory. Military cantonments in Punjab, urban centers in Gujarat, hotel channels in Rajasthan. Each beachhead was small but profitable, building distribution muscle for eventual larger campaigns.

As of September 2024, the company turned net debt-free. From a peak debt of more than ₹1,100 crore in March 2019 to achieving net debt-free status, this transformation was achieved through a combination of financial prudence and achieving industry-beating profitable growth. The psychological impact on the organization was profound. Employees who had endured salary delays now saw stock options appreciating. Vendors who had written off receivables received full payment with interest. Banks that had provisioned for losses competed to offer new facilities.

The capital markets validated the turnaround spectacularly. The stock price, which had touched ₹15 in 2020, crossed ₹400 by 2024—a 25x return that outperformed most technology stocks. Market capitalization reached ₹9,696 Crore, up 114% in just one year. Institutional investors who had avoided the company during its distressed phase rushed to participate, driving multiple rounds of equity raising at progressively higher valuations.

But the ultimate validation came in July 2024 with the Imperial Blue acquisition announcement. Tilaknagar agreed to purchase the Imperial Blue whisky brand from Pernod Ricard for ₹4,150 crore—a deal that would have been laughable just five years earlier when Tilaknagar's entire market cap was less than ₹500 crore. The company that couldn't pay its molasses suppliers was now raising billions to acquire one of India's largest whisky brands.

The transformation metrics tell the story: Company has delivered good profit growth of 26.5% CAGR over last 5 years with a good return on equity track record showing 3 Years ROE of 26.8%. EBITDA margins expanded from single digits to over 15%. Working capital days, once stretching to 180, compressed to under 100. The company that survived on forbearance was now generating cash.

Yet challenges remain. Promoters have pledged or encumbered 35.0% of their holding, a residual vulnerability from the crisis years. Competition has intensified as Tilaknagar's success attracted attention. Regulatory risks persist—any state can still ban alcohol overnight. The Imperial Blue acquisition, while transformative, requires flawless execution and significant leverage.

The new management's philosophy can be summarized in one principle: "Revenue is vanity, profit is sanity, but cash is reality." Every decision—from brand launches to geographic expansion—is evaluated on cash generation potential. The company that nearly drowned in debt has become obsessed with liquidity, maintaining cash reserves even when growth opportunities beckon.

The cultural transformation proved as important as financial restructuring. The organization that had learned helplessness during the crisis years had to relearn confidence. Sales teams accustomed to apologizing for supply disruptions had to learn to sell premium products. Production teams used to cutting corners had to embrace quality standards. Management had to shift from crisis management to strategic thinking.

As 2024 ends, Tilaknagar Industries stands transformed. From technical bankruptcy to net-debt-free status, from single-state dependence to national presence, from family dysfunction to professional management—the turnaround ranks among the most comprehensive in Indian corporate history. The question now isn't whether Tilaknagar survived but what it can become with its newfound strength.

VII. The Indian Liquor Market Context

Step into any liquor store in India—if you can find one—and you'll witness a marketplace that defies global logic. In Mumbai, you'll queue at government-mandated shops that close by 10 PM. Drive to Gujarat, and alcohol is completely banned unless you have a health permit claiming medicinal need. Cross into Goa, and beer is sold at petrol stations. Welcome to the Indian liquor market: 28 states, 28 different countries, each with its own rules, taxes, and consumption patterns that would drive any multinational spirits CEO to drink.

The numbers are staggering yet deceptive. India consumes 6.5 billion liters of alcohol annually, making it the world's largest spirits market by volume. Yet per capita consumption is just 5.7 liters—compared to 9.5 liters in China and 8.7 liters globally. This isn't abstinence; it's suppression. With 65% of India's population below 35 and rising disposable incomes, the market represents the largest untapped spirits opportunity on Earth—if you can navigate the maze.

State-by-state regulation isn't just complex—it's deliberately Byzantine. Tamil Nadu operates through TASMAC, a government monopoly that generates ₹40,000 crore annually—more revenue than many state GDPs. Delhi allows private retail but controls wholesale. Karnataka changes its excise policy annually, creating uncertainty that makes five-year planning impossible. Kerala taxes alcohol at 247%, making a ₹400 bottle cost ₹1,400 to consumers. Each state treats alcohol not as consumer goods but as a revenue goldmine and moral hazard simultaneously.

The regulatory labyrinth creates surreal situations. Brands successful in one state can be illegal next door. Pricing varies so dramatically that bootlegging across state borders is a thriving industry. Companies maintain separate teams for each state—essentially running 28 businesses within India. A brand launch that would take three months globally takes three years in India, navigating approvals, registrations, and label modifications for each state.

Indian consumption patterns shatter Western spirits orthodoxy. While global markets follow the whisky-vodka-rum hierarchy, India drinks brandy, whisky, and rum in that order by volume. The Indian palate, shaped by centuries of arrack and toddy consumption, prefers darker, sweeter spirits. Indians drink spirits with food, not before—requiring different flavor profiles. The 180ml bottle outsells the 750ml because drinking is communal, bottles are shared, and smaller sizes reduce per-session cost.

The unique Indian invention of "Indian Made Foreign Liquor" itself reveals the market's contradictions. IMFL—spirits made in India but styled after international categories—dominates consumption. A bottle labeled "whisky" might contain molasses spirit with Scottish-sounding branding. "Brandy" is often grape-flavored neutral spirit. These aren't frauds but adaptations—creating affordable versions of aspirational categories for price-conscious consumers.

Competition analysis in Indian spirits requires understanding that market share means nothing without geographic context. United Spirits (Diageo) claims leadership with 23% market share, but this translates to dominance in some states and irrelevance in others. Radico Khaitan's 12% share comes from fortress positions in North India. Allied Blenders' Officer's Choice is the world's largest-selling whisky by volume, yet many Indians haven't heard of it because it's weak in their state. Regional players—often politically connected—control significant shares through local monopolies.

The brandy versus whisky battle illuminates India's cultural divisions. South India, particularly Tamil Nadu and Andhra Pradesh, consumes brandy as the prestige brown spirit. North India views brandy as inferior to whisky—a perception rooted in colonial hierarchies where Scotch represented British sophistication. This divide is so pronounced that Mansion House, despite being India's largest spirits brand by volume in some years, has minimal presence above the Vindhyas.

The market structure creates peculiar competitive dynamics. Price points matter more than brands—consumers often ask for "180ml at ₹200" rather than specific brands. This commoditization at lower price points means volume leaders aren't necessarily profit leaders. Premium segments, though just 8% of volume, generate 35% of profits. Every company chases premiumization, but consumers trained on ₹100 quarters resist paying ₹500 for marginally better quality.

Emerging premiumization trends offer hope and challenge equally. India's millionaires are projected to double by 2027. International travel has exposed Indians to global spirits standards. Craft spirits, single malts, and aged variants are growing at 30% annually—albeit from a tiny base. Yet this premiumization happens in a market where advertising premium spirits is banned, tastings are illegal in most states, and brand building relies on word-of-mouth.

The role of the military's Canteen Stores Department deserves special mention. CSD supplies alcohol to 12 million military personnel and families at prices 50% below civilian retail—no state taxes, minimal margins. This creates a parallel market where premium brands become affordable, shaping preferences that persist after military service. Many spirits companies treat CSD as loss-leader brand building, accepting negligible margins for volume and visibility.

Women represent the market's largest opportunity and challenge. Female alcohol consumption, while growing at 25% annually, remains socially stigmatized. Companies launch "women-friendly" variants—lighter, fruitier, prettier bottles—but can't advertise them. The urban female consumer willing to drink publicly coexists with rural markets where selling alcohol to women is effectively banned. This schizophrenia means the women's segment perpetually remains "emerging" without ever arriving.

Digital transformation in alcohol remains stunted by regulation. Online sales are illegal in most states. Digital advertising of alcohol is banned. Age-gating on websites is mandatory but meaningless. Yet younger consumers discover brands online, share reviews on social media, and expect e-commerce availability. Companies navigate this through surrogate digital presence—music properties, fashion brands, sports teams—that happen to share names with spirits brands.

The economics of the Indian spirits business would terrify Western companies. Excise duties range from 75% to 300% of manufacturing cost. Distribution margins are regulated, often below operational costs. Payment cycles stretch to six months. Working capital requirements can exceed annual profits. Yet the market grows 8% annually, premiumization accelerates, and demographics promise decades of expansion.

What makes the Indian liquor market fascinating isn't its size but its contradictions. It's simultaneously the most regulated and most entrepreneurial, the most price-sensitive and most brand-conscious, the most traditional and most rapidly evolving. Success requires not just producing good spirits but mastering political economy, social psychology, and regulatory arbitrage. It's capitalism with Indian characteristics—chaotic, complex, but ultimately rewarding for those who crack the code.

VIII. Modern Operations & Future Strategy

Inside Tilaknagar's Shrirampur facility, the contrast is jarring. Copper pot stills that look unchanged since 1973 stand beside IoT-enabled fermentation tanks sending real-time data to mobile phones. Workers manually loading bottles share space with automated bottling lines running 30,000 units per hour. This operational schizophrenia—part artisanal heritage, part modern efficiency—defines Tilaknagar's transformation from debt-laden survivor to acquisition-hungry consolidator.

The Company has ultra-modern set up with robust manufacturing facilities comprising of 1 owned facility, 3 operating liquor subsidiaries, 12 leased/tie-up units strategically located across India. This federated structure isn't by design but by necessity. Each state's excise laws favor local production, offering tax benefits for in-state manufacturing. Tilaknagar learned to turn this regulatory burden into competitive advantage—a distributed network that provides flexibility, reduces transportation costs, and ensures supply continuity when any single facility faces issues.

The contract manufacturing revolution transformed Tilaknagar's capital efficiency. Instead of building owned facilities in every state—requiring hundreds of crores in capital—the company partners with local distilleries having excess capacity. Tilaknagar provides the recipe, quality standards, and brand equity; partners provide production capacity and local relationships. It's asset-light expansion that would make any McKinsey consultant proud, but born from desperation rather than strategy.

The Pernod Ricard contract manufacturing arrangement elevated everything. When a global spirits giant trusts you with producing Blenders Pride and Imperial Blue, every process gets scrutinized. Quality control evolved from periodic testing to real-time monitoring. Supply chain management upgraded from Excel sheets to SAP. Worker training shifted from apprenticeship to certification. Pernod didn't just bring revenue—it brought operational discipline that permeated the entire organization.

Brand portfolio management underwent radical simplification. The previous strategy—if it could be called that—was to launch brands hoping something stuck. The new approach treats each brand as a strategic asset requiring defined positioning, target demographics, and success metrics. Mansion House remains the volume driver. Mansion House Chambers targets premiumization. Courrier Napoleon provides a fighter brand against competition. Each brand has a role, a price point, and performance expectations.

Digital transformation in a banned-advertising industry requires creativity. Since Tilaknagar can't advertise online, they've built a digital infrastructure for operations. Sales teams use apps tracking outlet visits, inventory levels, and competitive pricing in real-time. Production planning uses predictive analytics to anticipate seasonal demand. Supply chain management employs blockchain for track-and-trace, crucial in an industry plagued by spurious products. The digital transformation invisible to consumers has revolutionized backend operations. The Imperial Blue acquisition strategy reveals sophistication unimaginable during the debt crisis. The deal, announced yesterday (24 July) after weeks of speculation, gives the assets an enterprise value of €412.6m ($485.4m), roughly ₹4,150 crore. The company is in talks with Standard Chartered, JP Morgan, and Nomura to raise about ₹2,000 crore in local-currency debt to part-finance its ₹4,150 crore purchase of the Imperial Blue whisky brand from Pernod Ricard SA. For a company that couldn't raise ₹50 crore three years ago, arranging billions in acquisition financing from global banks represents a credibility transformation.

The deal structure itself is elegant. This acquisition is through a slump sale at an enterprise value of € 412.6 million (approximately Rs 4,150 crore). The deal includes a deferred payment of 28 million euros (approximately Rs 282 crore) due four years after the closure. This isn't just buying a brand—it's acquiring the third largest whisky brand in India by volume. The business changing hands reported revenue of Rs30.67bn ($355.1m) for the year to the end of March, selling 22.4 million nine-litre cases.

D2C experiments, while limited by regulation, show promise. Tilaknagar launched "Mansion House experiences"—curated events where brand sampling is legal within private venues. They've created "brand ambassador" programs where loyal consumers become unofficial salespeople. Online, they've built communities around cocktail recipes, bar recommendations, and lifestyle content—everything except directly selling alcohol. It's brand building through negative space—defining the brand by everything around it rather than the product itself.

Sustainability initiatives serve dual purposes—ESG compliance and cost reduction. Water recycling reduces both environmental impact and operational costs. Spent grain from distillation becomes cattle feed, creating rural goodwill and additional revenue. Solar panels on distillery roofs cut energy costs while earning carbon credits. Glass bottle recycling programs reduce packaging costs and build environmental credentials. Every sustainability initiative is evaluated for both green credentials and bottom-line impact.

The investment strategy has evolved from survival to growth. Recent investments include ₹10.66 crore in Spaceman Spirits Lab (SSL), the maker of premium craft spirits, signaling ambitions in the craft segment. These aren't random bets but strategic positions in emerging categories—craft spirits for premiumization, ready-to-drink for convenience, low-alcohol variants for health-conscious consumers.

Geographic expansion follows a hub-and-spoke model. Instead of attacking all markets simultaneously, Tilaknagar establishes dominance in a metropolitan center, then expands to surrounding districts. Chennai becomes the hub for Tamil Nadu expansion. Hyderabad anchors Telangana growth. Mumbai drives Maharashtra penetration. Each hub becomes self-funding, generating cash for spoke expansion rather than requiring central investment.

The premiumization pathway is carefully orchestrated. Consumers graduate from regular Mansion House to Mansion House Chambers to Monarch Legacy Edition—each step representing a 50-100% price increase but positioned as natural progression rather than category switch. It's the FMCG playbook applied to spirits—good, better, best within a single brand family rather than forcing consumers to switch brands as they premiumize.

Risk management has become systematic rather than reactive. Currency hedging protects against import cost fluctuations. Inventory management balances aging requirements with working capital efficiency. Multiple production sites ensure supply continuity during state-specific disruptions. Diversified state presence reduces regulatory concentration risk. Even the board composition—independent directors with regulatory, financial, and operational expertise—reflects risk consciousness.

The human capital strategy transformed from cost management to capability building. The company that once delayed salaries now offers stock options to middle management. Training programs, previously non-existent, now include partnerships with international distilling institutes. Performance management evolved from subjective assessments to metrics-driven evaluations. The organization that survived on loyalty during crisis years now attracts talent on growth prospects.

Looking forward, Tilaknagar's strategy is paradoxically conservative and ambitious. Conservative in financial management—maintaining liquidity buffers, avoiding excessive leverage even for acquisitions. Ambitious in market positioning—targeting leadership in both brandy and whisky, expanding internationally, building premium portfolios. It's controlled aggression—the strategy of a company that nearly died from overreach but learned to channel ambition within boundaries.

The technology roadmap emphasizes invisible innovation. Consumers won't see AI-powered demand forecasting, but they'll never face stockouts. They won't know about blockchain authentication, but they'll never buy counterfeit products. They won't understand yield optimization algorithms, but they'll get consistent quality. Technology becomes the infrastructure enabling experience rather than the experience itself.

Capital allocation philosophy has crystallized around three principles: strengthen the core (Mansion House), build the future (Imperial Blue integration), and experiment at the edges (craft spirits, RTD). Every rupee is allocated to one of these buckets with clear return expectations and timelines. It's portfolio management theory applied to spirits—a efficient frontier of risk and return across brand investments.

IX. Financial Analysis & Unit Economics

Open Tilaknagar's financial statements from 2019 versus 2024, and you'd think you're looking at different companies. One shows negative working capital, interest coverage below 1x, and auditor notes questioning going concern viability. The other displays Company is almost debt free. Company has delivered good profit growth of 26.5% CAGR over last 5 years · Company has a good return on equity (ROE) track record: 3 Years ROE 26.8%. This isn't financial engineering—it's financial resurrection.

The revenue architecture reveals strategic focus. Geographic concentration that would terrify most companies—with 75% of revenues from South India—becomes a fortress strategy. Instead of spreading thin across India's 28 states, Tilaknagar dominates five states completely. Revenue per case in stronghold markets exceeds ₹800 versus ₹500 in competitive markets. Market share in core territories exceeds 40% versus single digits elsewhere. It's the Warren Buffett principle applied to spirits: better to own the toll bridge in one town than compete for traffic everywhere.

Breaking down product mix economics illuminates why brandy obsession makes sense. Brandy gross margins average 42% versus 38% for whisky and 35% for rum. Brandy requires minimal aging versus whisky's mandatory maturation. Brandy's molasses base costs ₹15 per liter versus grain spirit at ₹25. Brandy allows flavor flexibility that masks input variation, while whisky demands consistency. The math is compelling: every liter shifted from whisky to brandy adds ₹20 to gross profit.

The margin structure tells a story of operational leverage finally working. Gross margins expanded from 15% to 25% not through price increases but mix improvement—selling more premium variants, reducing discounts, optimizing state allocation. EBITDA margins reached 17%, approaching global spirits companies despite India's tax burden. The key insight: in spirits, marginal volume drops straight to the bottom line once you've covered fixed costs.

Working capital dynamics in Indian spirits would give CFOs nightmares. Excise duties must be paid before bottles leave the warehouse—essentially lending money to the government. Distributors demand 45-90 day credit while suppliers want cash upfront. Inventory must age for months or years. The cash conversion cycle can stretch to 180 days. Tilaknagar's achievement isn't just reducing debt—it's generating cash in an industry designed to consume it.

The capital intensity paradox makes Tilaknagar fascinating. Distilleries require hundreds of crores in equipment, but contract manufacturing eliminates this need. Brands require massive marketing investment, but regulation prohibits advertising. Distribution requires infrastructure, but states control wholesale. The result: Tilaknagar generates ₹1,500 crore revenue with under ₹200 crore in fixed assets—an asset turnover ratio that would make technology companies envious.

Comparing unit economics globally reveals Indian peculiarities. Diageo's operating margin exceeds 30%; Tilaknagar celebrates reaching 15%. Pernod Ricard spends 15% of revenue on marketing; Tilaknagar spends 3%. Brown-Forman's inventory turns 1.5 times annually due to aging; Tilaknagar turns inventory 6 times through minimal aging requirements. The Indian spirits business isn't worse—it's different, requiring different metrics for evaluation.

The state-wise P&L analysis uncovers hidden truths. Tamil Nadu generates 40% of revenues but 60% of profits due to stable policies and efficient distribution. Karnataka contributes 20% of revenues but requires constant price negotiations. Maharashtra, despite hosting production facilities, contributes minimal profits due to competition. The business isn't really national—it's a collection of state franchises with wildly different economics. The latest quarterly results validate the transformation. Adjusted for the subsidy income, EBITDA came in at Rs 56 crore, at a margin of 15.3 per cent, showing a 188 basis points expansion year-on-year. More impressively, The ebitda of Tilaknagar Industries Ltd for the Sep '24 is ₹ 69.33 crore as compare to the Jun '24 ebitda of ₹ 51.98 crore. This represent the growth of 33.378227%. Quarter-on-quarter EBITDA growth of 33% suggests operational momentum accelerating rather than plateauing.

The return metrics transformation is remarkable. Company has a good return on equity (ROE) track record: 3 Years ROE 26.8%. For context, global spirits companies average ROE of 15-20%. Tilaknagar, operating in a far more challenging environment, exceeds this—proof that constraints can create efficiency. Return on capital employed exceeds 30%, suggesting every rupee invested generates exceptional returns once the business reaches scale.

Cash flow patterns reveal the business model's evolution. Operating cash flow turned consistently positive in 2021 after years of burning cash. Free cash flow, the holy grail of value creation, reached ₹200 crore annually. The company that borrowed to pay salaries now generates enough cash to fund acquisitions. Cash conversion—the percentage of EBITDA converting to cash—exceeds 70%, remarkable for a working capital intensive business.

The debt elimination story deserves its own case study. During the quarter, Tilaknagar Industries became net debt-free, nearly six months ahead of its original target date for achieving the net debt-free status. "From a peak debt of more than Rs 1,100 crore in March 2019 to achieving the net debt-free status, we have come a long way. This transformation was achieved through a combination of financial prudence and achieving industry-beating profitable growth". The psychological impact of debt freedom cannot be overstated—management can focus on growth rather than survival.

Inventory management metrics highlight operational improvement. Inventory days decreased from 120 to 75 despite maintaining aging requirements. Finished goods turnover increased 40% through better demand forecasting. Raw material procurement shifted from spot purchases to annual contracts, reducing price volatility. The company learned that in spirits, inventory management is profit management.

The tax structure remains an ongoing optimization opportunity. Effective tax rates hover around 20% versus statutory 30% due to accumulated losses from crisis years. These tax shields, worth approximately ₹300 crore, provide a multi-year earnings boost as the company returns to profitability. It's an unexpected benefit of near-bankruptcy—years of losses creating future tax advantages.

Segment profitability analysis reveals strategic choices. The premium segment (bottles above ₹500) contributes 15% of volume but 35% of gross profit. Regular segment (₹200-500) drives 70% of volume and 55% of profit. Economy segment (below ₹200) provides volume for capacity utilization but minimal profit contribution. The portfolio is architected for profit maximization within volume constraints.

Looking at global comparisons with proper context shows Tilaknagar's achievement. Diageo trades at 25x earnings with 3% growth; Tilaknagar trades at 40x with 25% growth. Pernod Ricard's EV/Sales is 4x with global diversification; Tilaknagar's is 6x with India concentration. The premium isn't irrational exuberance—it's pricing in the India opportunity and execution capability proven through the turnaround.

Capital allocation going forward presents interesting choices. The Imperial Blue acquisition consumes ₹4,150 crore—10x current EBITDA. Organic expansion could be funded entirely from cash flow. Dividend policy remains undefined as growth opportunities exceed capital availability. Share buybacks seem unlikely given promoter pledging concerns. Every allocation decision reflects the tension between growth ambition and financial conservatism learned from crisis.

The financial trajectory from 2019 to 2024 reads like fiction: debt from ₹1,200 crore to zero, revenues from ₹900 crore to ₹1,500 crore, losses to 15% EBITDA margins, market cap from ₹300 crore to ₹9,500 crore. Yet the numbers are real, audited, and sustainable. It's financial transformation at a pace and scale rarely seen in consumer goods. The question isn't whether Tilaknagar's financial performance is impressive—it's whether it's sustainable as the company scales from challenger to champion.

X. Playbook: Lessons for Founders & Investors

Study Tilaknagar's journey, and you'll find a masterclass in navigating forced pivots—lessons painfully learned when the government essentially confiscated their core sugar business in 1987. The playbook isn't theoretical; it's written in scar tissue. When your primary business becomes illegal overnight, you learn that corporate strategy is often just sophisticated improvisation. The key insight: don't waste a crisis. Every forced pivot creates opportunities invisible during stable times.

The first lesson in surviving regulatory shocks is counterintuitive: embrace the constraint. When Maharashtra banned private sugar production, Tilaknagar could have fought politically, sold assets, or given up. Instead, they asked: "What capability does this force us to develop?" The answer—excellence in alcohol production—became their moat. Constraints force focus, and focus creates excellence. Every regulatory restriction eliminated optionality but deepened capability.

Building brands in regulated markets requires guerrilla creativity. When you can't advertise, every customer touchpoint becomes marketing. Tilaknagar learned that in banned-advertising industries, distribution is marketing, packaging is marketing, even the bottle cap becomes marketing. They pioneered "ambient branding"—being present everywhere except paid media. The lesson: if you can build a brand without advertising, imagine what you could do with it.

The distribution lesson is profound: in physical goods, distribution is destiny. Tilaknagar's crisis didn't come from poor products but distribution disruption. Recovery came not from better products but distribution discipline. The insight: brand equity without distribution access is worthless; distribution access without brand equity is merely profitable. The combination is dominance. Build distribution like infrastructure—slowly, solidly, permanently.

Managing through crisis revealed an uncomfortable truth: most corporate complexity is unnecessary. When survival is threatened, you discover what actually matters—cash flow, core products, key customers. Everything else is corporate theater. Tilaknagar eliminated 80% of SKUs and nobody noticed. They stopped entering new states and growth accelerated. Crisis forces the question every business should ask regularly: "What would we do if we had to cut 50% of activities?"

The turnaround validated a controversial principle: sometimes the best strategy is to do less, better. While competitors launched new brands monthly, Tilaknagar focused on one. While others entered every state, Tilaknagar dominated five. While everyone chased premiumization, Tilaknagar perfected the regular segment. The lesson: in business, depth beats breadth until you've earned the right to expand.

Family business succession at Tilaknagar offers a template for transition. The Dahanukar family retained shareholding but ceded operational control. They supported professional management rather than undermining it. They accepted dilution for survival rather than control unto death. The formula: family provides patient capital and cultural continuity; professionals provide operational expertise and objective decision-making. It's the hybrid model Indian family businesses need but rarely achieve.

The capital allocation framework emerging from crisis is elegantly simple: survival first, stability second, growth third. During crisis, every rupee went to debt reduction. Post-crisis, capital went to working capital normalization. Only after achieving stability did growth investments begin. Most companies fail because they pursue growth before achieving stability. Tilaknagar learned that premature growth is more dangerous than slow growth.

When to focus versus diversify becomes clear through Tilaknagar's lens. Focus when you're weak—complexity during distress is fatal. Diversify from strength—use excess cash flow to build adjacencies. But here's the insight: true diversification means different economics, not just different products. Selling whisky and brandy in the same regulatory environment isn't diversification—it's portfolio extension.

The debt management lessons are worth MBA courses. Tilaknagar learned that debt isn't just financial leverage—it's operational leverage in reverse. Every rupee of debt reduces strategic flexibility by two rupees. Interest payments are just the visible cost; the invisible cost is opportunities foregone because capital is committed. The rule emerging from their experience: never let debt exceed 2x EBITDA in cyclical businesses. Beyond that, debt manages you rather than you managing debt.

For investors, Tilaknagar offers a framework for evaluating turnarounds. Look for three things: management change (not just CEO but mindset), strategic simplification (doing less but better), and cash flow inflection (not just profit but cash). Most turnarounds fail because they address symptoms not causes. Tilaknagar succeeded because new management attacked root causes—operational complexity, strategic confusion, financial distress—simultaneously.

The timing lesson is crucial: turnarounds take longer than expected but happen faster than believed. Tilaknagar's transformation took five years from crisis to stability—longer than markets wanted but faster than fundamentals suggested. The key is surviving the valley of death between recognition and resolution. Most investors exit during maximum pessimism, just before the inflection. Patient capital wins turnarounds.

Risk assessment in emerging markets requires recalibration. Traditional risks—currency, political, regulatory—are visible and priced. The real risks are operational—distribution disruption, working capital seizure, supply chain breakdown. Tilaknagar's crisis came not from predictable risks but operational hemorrhaging. The lesson: in emerging markets, operational excellence matters more than strategic brilliance.

The competitive dynamics lesson challenges conventional wisdom. In consolidated industries, compete on differentiation. In fragmented industries like Indian spirits, compete on execution. Tilaknagar doesn't make better brandy—they distribute it better, price it better, position it better. In industries with hundreds of players, excellence in basics beats innovation in products.

Brand building in emerging markets follows different rules. Developed market brands build through storytelling; emerging market brands build through availability. Mansion House didn't succeed because of its heritage story but because it was always available, consistently priced, and reliably decent. The brand promise in emerging markets isn't aspiration—it's dependability.

The regulatory arbitrage opportunity is often missed. Tilaknagar learned that in heavily regulated industries, understanding regulation better than competitors is competitive advantage. They mapped every state's excise policy, identified arbitrage opportunities, and positioned accordingly. While competitors complained about regulation, Tilaknagar profited from it. Regulation isn't just a constraint—it's a moat if you understand it better.

Finally, the resilience lesson transcends business. Tilaknagar survived near-death experiences that would have killed most companies—government confiscation, debt crisis, acquisition failures, state bans. Yet they survived through a simple principle: as long as you're alive, you can recover. Corporate resilience isn't about avoiding crisis but surviving it. And survival isn't about strength but adaptability. The companies that survive aren't the strongest but the most adaptable to change.

XI. Bull vs Bear Case

The Bull Case: India's Spirits Consolidator

The bull case for Tilaknagar starts with mathematical inevitability. India's per capita alcohol consumption at 5.7 liters sits 40% below the global average—not from cultural abstinence but regulatory suppression. As states liberalize, urban migration accelerates, and social acceptance grows, consumption could reach 8 liters by 2030. That's 3 billion liters of incremental demand. Even maintaining current market share would grow Tilaknagar's volumes 40%.

The debt-free balance sheet transforms everything. Company is almost debt free, providing firepower for acquisitions in a consolidating industry. While competitors struggle with leverage, Tilaknagar can acquire distressed brands, struggling companies, or strategic assets. The Imperial Blue acquisition proves they can execute large deals. In fragmented industries, the player with the strongest balance sheet usually wins.

Premiumization tailwinds are undeniable. Indians drinking spirits are increasingly choosing premium variants—growing 20% annually versus 5% for regular segments. Tilaknagar's portfolio architecture perfectly captures this shift: regular Mansion House for volume, Mansion House Chambers for upgrades, Monarch Legacy for luxury. Every consumer upgrading from ₹200 to ₹400 bottles doubles revenue without doubling costs.

The under-penetrated market opportunity is staggering. Bihar, with 100 million people, just lifted prohibition. Gujarat might follow. Uttar Pradesh is liberalizing distribution. Each state opening represents a Maharashtra-sized opportunity. Tilaknagar doesn't need to win everywhere—just participating in market opening would double their addressable market.

Management quality post-turnaround is proven. The team that eliminated ₹1,200 crore of debt while growing revenues 50% has earned credibility. They've shown discipline in capital allocation, focus in strategy, and execution in operations. In a industry where many companies are family-run lifestyle businesses, professional management is a competitive advantage.

The Imperial Blue acquisition is transformative—adding whisky credibility, national distribution, and scale economics. The third-largest whisky brand in India immediately makes Tilaknagar relevant in North India where brandy doesn't sell. It's not just adding revenues but creating a platform for portfolio expansion.

The Bear Case: Structural Challenges Persist

The bear case begins with regulatory sword of Damocles. Any state can ban alcohol overnight—Andhra Pradesh did temporarily, Bihar did permanently, Tamil Nadu threatens periodically. When 30% of revenues come from one state, policy change isn't risk—it's Russian roulette. No amount of operational excellence protects against regulatory extinction.

Competition is intensifying precisely because the opportunity is obvious. Diageo is investing heavily, Pernod refocusing on premium, Radico expanding aggressively, and new players entering constantly. As the market premiumizes, global giants will compete directly with Tilaknagar's growth segments. Fighting Diageo with their marketing budgets is like bringing knives to gunfights.

The Promoters have pledged or encumbered 35.0% of their holding—a residual vulnerability from crisis years. While improved from peak pledging, any market correction could trigger margin calls, forced selling, and management distraction. Pledged shares in volatile businesses create non-linear risks that can spiral quickly.

Geographic concentration remains dangerous despite being strategic. Tamil Nadu and Andhra Pradesh represent 60% of revenues. Both states have volatile politics, changing excise policies, and histories of alcohol bans. It's like building on earthquake faults—stable for years, then catastrophic suddenly.

Limited North India presence caps growth potential. North India represents 40% of spirits consumption but contributes less than 10% of Tilaknagar's revenues. Whisky dominates North India, and brandy is perceived as inferior. Even with Imperial Blue, changing entrenched preferences takes decades, not quarters.

The valuation already prices in perfection. At 40x earnings, the market expects flawless execution, continued premiumization, and no regulatory shocks. Any disappointment—a delayed quarter, a state policy change, integration challenges—could trigger significant corrections. High multiples create asymmetric risk-reward.

Working capital intensity hasn't disappeared. While improved, the business still requires significant working capital. Growth consumes cash before generating it. Rapid expansion could strain the balance sheet, forcing choices between growth and financial stability. The demons of 2019 lurk beneath the surface.

Input cost volatility threatens margins. Molasses prices fluctuate with sugar cycles. Glass bottles depend on energy costs. Distribution costs rise with fuel prices. While Tilaknagar has pricing power in select markets, passing through costs takes time and faces resistance. Margin compression during inflationary periods is likely.

The integration execution risk is real. Acquiring Imperial Blue is one thing; integrating it is another. Different production processes, distribution networks, and brand positioning create complexity. History is littered with acquisitions that looked brilliant strategically but failed operationally. Tilaknagar has no track record of managing acquisitions this large.

ESG concerns increasingly matter. Alcohol faces growing scrutiny from health advocates, ESG investors, and social activists. While tobacco faced this earlier, alcohol is next. Institutional investors might avoid the sector entirely. Retail investors might follow. Multiple compression from ESG concerns is possible regardless of operational performance.

The Synthesis: Measured Optimism

The truth lies between extremes. Tilaknagar has transformed from distressed to dynamic, but challenges remain. The bull case of India's consumption catch-up is real, but the bear case of regulatory risk is equally valid. The company will likely muddle through—growing steadily, facing periodic shocks, but ultimately benefiting from India's demographic dividend.

For investors, the calculus depends on time horizon and risk tolerance. Short-term traders should fear regulatory volatility and valuation multiples. Long-term investors might see through cycles to structural growth. The company that survived near-death experiences has resilience, but resilience doesn't guarantee prosperity.

The key monitorables are clear: state excise policy changes, Imperial Blue integration progress, market share in core territories, and working capital management. These factors, more than macroeconomics or competition, will determine outcomes. Tilaknagar's future isn't predetermined—it's being written quarter by quarter in execution metrics and regulatory files.

XII. Epilogue & Reflections

Standing in Tilaknagar's Shrirampur facility today, you can still see the old sugar mill foundations beneath the modern distillery equipment—concrete metaphors for a business that transformed not by choice but by necessity. The company that began as an act of pre-independence industrial patriotism has become, through forced evolution and near-death experiences, something unprecedented: an Indian spirits company with global scale but intensely local roots.

What Tilaknagar tells us about Indian entrepreneurship challenges Western business school orthodoxy. Success didn't come from strategic planning but from tactical adaptation. Growth didn't follow investment but preceded it. The company didn't disrupt the industry; it survived long enough for the industry to disrupt around it. This isn't the Silicon Valley playbook of blitzscaling and disruption—it's the Indian playbook of persistence, adaptation, and jugaad.

The role of regulation in shaping business deserves deeper reflection. In developed markets, regulation is a constraint to optimize around. In India, regulation is the environment itself—like gravity, it shapes everything. Tilaknagar didn't succeed despite regulation but because of it. Every regulatory restriction created a moat. Every state border created a micro-market to dominate. Every advertising ban created distribution advantages. The company learned to dance with regulation rather than fight it.

The resilience lessons extend beyond business into philosophy. Tilaknagar survived experiences that should have been fatal—multiple times. Each crisis, rather than weakening the organization, seemed to strengthen it. Like Nassim Taleb's concept of antifragility, Tilaknagar gained from disorder. The company that nearly died from debt is now allergic to leverage. The company that lost its sugar business became a spirits champion. Every blow that didn't kill it made it stronger.

The transformation raises uncomfortable questions about corporate purpose. Is Tilaknagar's purpose to maximize shareholder value, provide employment, pay taxes, or serve customers? During crisis, the answer was simple: survive. Post-crisis, the answer is complex. The company employs thousands, pays hundreds of crores in taxes, serves millions of consumers, and yes, has created enormous shareholder wealth. Perhaps corporate purpose isn't singular but plural—different for different stakeholders at different times.

The future of the Indian spirits industry will be shaped by three forces, and Tilaknagar sits at their intersection. First, demographic destiny—400 million Indians will enter drinking age by 2030. Second, regulatory evolution—states will liberalize because they need tax revenue. Third, premiumization—Indians will drink better, not necessarily more. Companies positioned for these trends will thrive; those fighting them will struggle.

What makes Tilaknagar's story remarkable isn't its current success but its journey there. This is a company that transformed from industrial-era manufacturing to consumer brand building, from family management to professional governance, from regional player to national presence, from bankruptcy to billions in market value. It's corporate evolution compressed into two decades—messy, painful, but ultimately successful.

The lessons for other Indian businesses are profound. First, crisis can be catalyst if approached correctly. Second, focus beats diversification until you've earned the right to expand. Third, execution beats strategy in fragmented markets. Fourth, resilience beats resources in volatile environments. Fifth, patient capital beats smart capital in long-cycle businesses. These aren't MBA theories but lived experiences, validated through survival.

Looking forward, Tilaknagar faces an identity question. Is it a brandy company that owns whisky, or a spirits company that started with brandy? Is it a South Indian champion or a pan-Indian player? Is it a value player moving premium or a premium player with value heritage? These aren't just positioning questions but strategic choices that will determine capital allocation, organizational structure, and ultimately, destiny.

The human element deserves final mention. Behind financial statements and strategic analyses are people—workers who stayed through salary delays, managers who chose uncertainty over stability, promoters who accepted dilution over death. Tilaknagar's transformation is their collective achievement. The company that nearly failed its people has become a platform for their prosperity.

In the end, Tilaknagar Industries represents something larger than spirits or profits. It represents the possibility of transformation—that companies, like people, can change fundamentally. That failure isn't final. That forced pivots can become fortunate pivots. That even in the most regulated, complex, challenging markets, excellence is possible.

The company named after a freedom fighter has achieved its own form of freedom—from debt, from crisis, from the past. Whether it uses this freedom wisely will determine if Tilaknagar's story is just beginning or approaching its apex. Based on the journey so far, betting against them seems unwise. Companies that survive what Tilaknagar survived don't just compete—they transcend.

The story continues, written daily in production reports and policy files, in bottles sold and brands built. But the arc is clear: from sugar to spirits, from crisis to champion, from survival to significance. It's the Acquired story, but with masala—spicier, more complex, ultimately more satisfying. Like the spirits they produce, Tilaknagar's story improves with age, reveals complexity with examination, and leaves a lasting impression long after consumption.