Kalpataru Projects International: India's Infrastructure Empire Builder

I. Introduction & Episode Setup

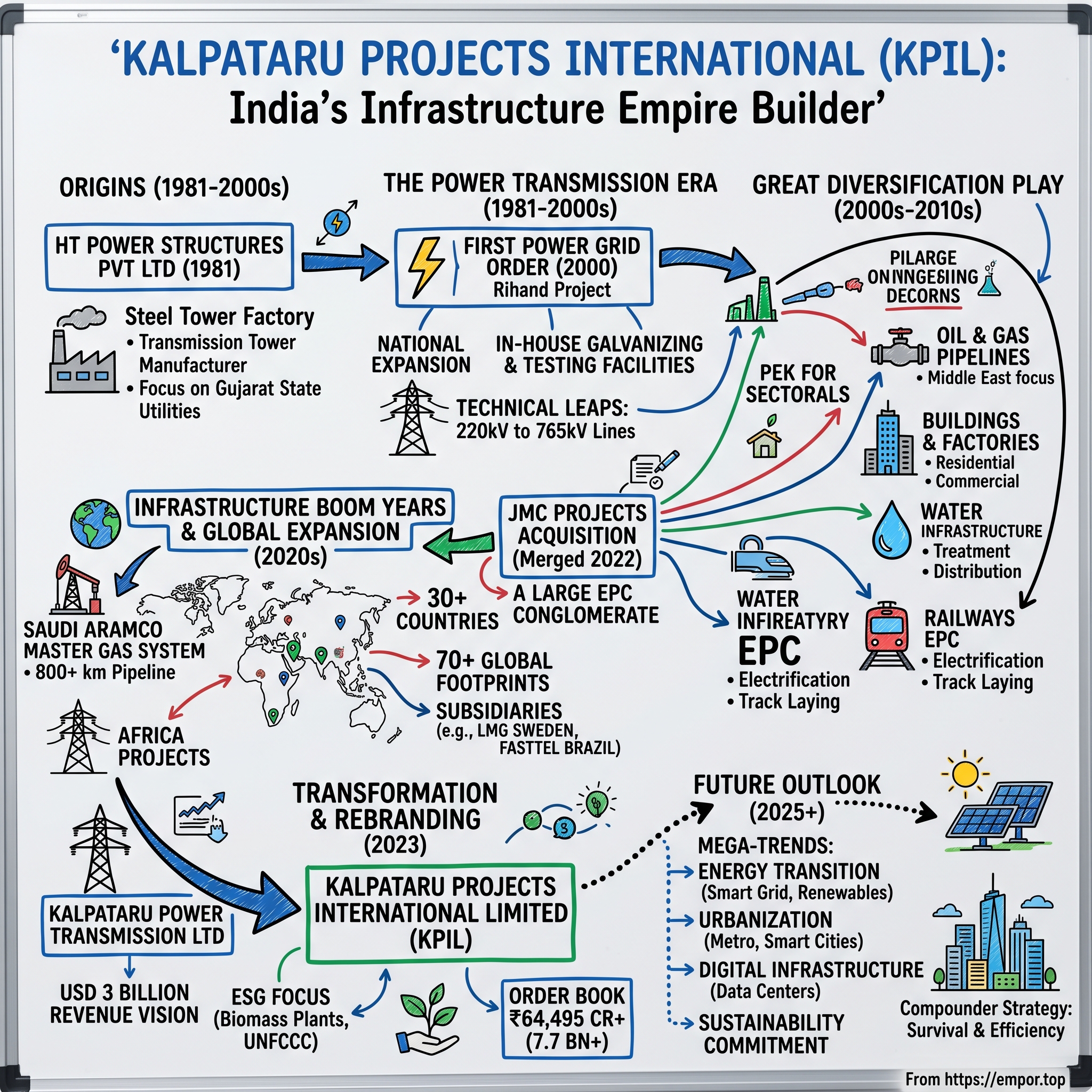

Picture this: It's 2023, and in a boardroom overlooking Mumbai's skyline, the leadership of a 42-year-old infrastructure company makes a decision that would seem minor to outsiders but signals everything to insiders. They're changing their name—dropping "Power Transmission" for "Projects International." This isn't corporate vanity. It's the culmination of a four-decade transformation from a single-product manufacturer into one of India's most globally ambitious infrastructure conglomerates.

Kalpataru Projects International Limited—KPIL to those who track it—operates in over 30 countries, has touched infrastructure in 73 nations, and carries an order book worth ₹64,495 crore. That's roughly $7.7 billion in projects spanning transmission towers in African savannas, metro stations in Indian megacities, water treatment plants serving 15 million people, and cross-country oil pipelines that fuel economies. The company employs 22,225 people and generated ₹22,300+ crore in revenue last year.

But here's what makes KPIL fascinating for students of business strategy: while peers like L&T became engineering behemoths through sheer scale, and companies like KEC International stayed focused on transmission dominance, Kalpataru chose a third path—methodical diversification without losing its engineering DNA. They built capabilities project by project, country by country, creating what might be India's most internationally battle-tested mid-sized EPC player.

The central question isn't just how a power transmission company became an infrastructure conglomerate—it's how they did it while maintaining execution discipline across wildly different project types, from laying pipelines in Middle Eastern deserts to constructing biomass plants registered with the UNFCCC. This is a story about the unglamorous art of infrastructure execution, the patient accumulation of capabilities, and the strategic courage to transform when your original market no longer defines your potential.

Today we're diving deep into how Kalpataru built its empire, why 2023's rebranding represents more than semantics, and what their journey teaches us about succeeding in the brutal, capital-intensive, politically complex world of global infrastructure. We'll explore their playbook for managing everything from currency risks in Africa to working capital cycles that can stretch for years, and examine whether their recent record order book signals a new growth chapter or masks deeper challenges.

The infrastructure sector isn't sexy—it's about concrete, steel, and decades-long relationships with governments. But as we'll see, Kalpataru's story reveals how methodical execution in boring industries can create extraordinary value. After all, someone has to build the physical world that our digital economy runs on.

II. Origins & The Kalpataru Foundation

The year was 1981. India was still deep in the License Raj era, where getting permission to manufacture anything required navigating Byzantine bureaucracy. Indira Gandhi had just returned to power after the Emergency years, and the country's infrastructure was decades behind its ambitions. Power cuts were routine—not just in villages but in major cities. The national grid was more aspiration than reality.

Into this environment, a group of entrepreneurs saw opportunity where others saw only obstacles. They incorporated a company called "HT Power Structures Private Limited" in April 1981, initially as a subsidiary focused on manufacturing transmission towers—the skeletal steel giants that would eventually carry electricity across India's vast geography. The name was utilitarian, the mission narrow: build the physical backbone for India's electrification.

But to understand KPIL's DNA, you need to go back further. The Kalpataru Group itself was founded in 1969, twelve years before this power transmission venture. The group's founders understood something fundamental about post-independence India: the country would need massive infrastructure buildout, and whoever could execute reliably in this space would thrive. They started with real estate and gradually expanded into infrastructure-adjacent businesses, building relationships with government agencies and understanding the peculiar rhythms of public sector contracting.

By 1997, sixteen years after incorporation, the transmission business had grown substantial enough to warrant a transformation. The company converted to a public limited entity and adopted the name Kalpataru Power Transmission Limited—a signal that this was no longer just a manufacturing outfit but an ambitious player in the infrastructure space. The timing was prescient. India was just beginning its economic liberalization journey, and the demand for power infrastructure was about to explode.

What made early Kalpataru different wasn't technological superiority—transmission towers aren't exactly cutting-edge tech. It was their approach to execution in an environment where most projects faced delays, cost overruns, and quality issues. They invested in two manufacturing plants with in-house galvanizing facilities when others outsourced. They built testing capabilities when competitors relied on third-party certification. They hired engineers who understood not just design but the realities of erecting towers in remote locations during monsoons.

The 1980s and 1990s were about building fundamental capabilities: understanding government tendering processes, managing working capital when payments could be delayed by months, maintaining quality when operating in harsh field conditions. These weren't glamorous years—the company was essentially a B2G supplier of steel structures. But every project completed on time, every tower that withstood cyclones and earthquakes, built credibility in a market where trust was scarce.

The broader context matters here. India's per capita electricity consumption in 1981 was about 150 kWh annually—compared to over 5,000 kWh in developed nations. The government's ambitious plans to electrify villages and industrial corridors meant thousands of kilometers of transmission lines needed to be built. Kalpataru positioned itself as the reliable executor of these nation-building projects, understanding that in infrastructure, reputation compounds over decades.

By the late 1990s, as India's economy began opening up, Kalpataru had established itself as one of the largest transmission tower manufacturers in the country. They weren't the biggest—that distinction belonged to companies like L&T. But they had something valuable: a proven ability to execute complex projects in difficult conditions, relationships with power utilities across states, and the financial discipline to survive in a business where cash conversion cycles could stretch over 200 days.

This foundation—built on unglamorous manufacturing, government relationships, and execution reliability—would prove crucial when the company decided to transform itself in the 2000s. The question was no longer whether they could build transmission infrastructure, but whether those capabilities could translate into entirely different domains.

III. The Power Transmission Era (1981-2000s)

The turn of the millennium marked the beginning of India's true infrastructure awakening. In 2000, Kalpataru secured what would become a watershed moment—their first major order from Power Grid Corporation of India Limited (PGCIL) for the Rihand transmission packages. This wasn't just another contract; it was validation that a Gujarat-based manufacturer could compete with national giants for the most critical infrastructure projects.

Initially, the company had started off as a Gujarat-based company, largely catering to the state power utilities of Gujarat. But this local focus had actually been strategic genius. Gujarat's power sector was among India's most progressive, with relatively better payment cycles and more professional utility management. By mastering execution in this environment, Kalpataru built capabilities that would translate nationally.

The technical evolution during this period was remarkable. They became one of the largest transmission tower manufacturing companies with in-house galvanizing and painting facilities spread across two plants in India. This wasn't just about scale—it was about control. When you're erecting 400kV transmission lines across the Thar Desert or through the Western Ghats during monsoons, quality variance of even 1% can mean catastrophic failure. In-house galvanizing meant they could ensure every tower could withstand decades of weather extremes.

After the Rihand project, they established themselves as a serious player and built strong credentials. The numbers tell the story: The Company developed an annual production capacity of over 240,000 MT of transmission towers at its state-of-the-art manufacturing facilities in India and an ultra-modern tower testing facility. That testing facility was crucial—it allowed them to simulate cyclonic winds, seismic loads, and temperature extremes that towers might face over 50-year lifespans.

But the real competitive advantage wasn't just manufacturing prowess. It was understanding the peculiar dance of Indian infrastructure execution. Government contracts meant dealing with land acquisition delays, right-of-way issues with thousands of farmers, environmental clearances that could take years, and payment cycles that could stretch to 200+ days. While multinational competitors struggled with these realities, Kalpataru had learned to price these risks, manage cash flows accordingly, and maintain relationships across dozens of state electricity boards.

The competition was fierce. L&T brought scale and diversification. KEC International, part of the RPG Group, had similar transmission expertise. Bajaj Electricals competed on equipment. But Kalpataru carved out a specific niche: complex, high-voltage transmission projects in difficult terrains where execution excellence mattered more than just price.

By the mid-2000s, India's power sector was undergoing fundamental transformation. The Electricity Act of 2003 had unbundled generation, transmission, and distribution. Private sector participation was increasing. Interstate transmission systems were being upgraded from 220kV to 400kV and even 765kV. Each technical leap required new capabilities—different tower designs, stronger foundations, more sophisticated stringing techniques.

Kalpataru didn't just adapt; they anticipated. They invested in design capabilities that could handle everything from narrow-base towers for congested urban corridors to special foundations for marshy terrains in the Northeast. They developed expertise in live-line maintenance—working on energized lines without power cuts, crucial for India's growing economy that couldn't afford outages.

The international forays began tentatively. First to neighboring countries—Nepal, Bangladesh, Sri Lanka—where Indian standards were accepted and payment risks were manageable. Then to Africa, where Chinese competitors were dominant but Indian companies had the advantage of English-language documentation and British-standard engineering that many African countries preferred.

KPIL successfully positioned its High Voltage Substation business both in air insulated (AIS) and gas insulated (GIS) segment in domestic as well as international market. This was crucial diversification within the transmission space. Substations are the nodes where voltage is stepped up or down, where power flow is controlled. They're technically complex, requiring civil, electrical, and control system integration. Mastering substations meant Kalpataru could bid for complete transmission systems, not just tower supply.

The financial model during this era was straightforward but capital-intensive. Win a contract, mobilize resources, execute over 18-24 months, manage working capital carefully, and hope the electricity board paid on time. Margins were decent—8-12% EBITDA—but return on capital employed rarely exceeded 15% due to the working capital intensity.

What's remarkable about this period is what Kalpataru chose not to do. They didn't chase the generation boom—no power plants, no coal mining. They didn't go downstream into distribution. They didn't diversify into unrelated businesses like many Indian conglomerates. They stayed focused on the unsexy but essential business of building the skeleton that would carry India's electricity.

By 2010, they had executed transmission lines across every major Indian state, dealt with every state electricity board, and survived multiple economic cycles. The foundation was complete. The question now was whether transmission expertise could translate into broader infrastructure capabilities, and whether the company had the ambition to transform from a specialist into something much larger.

IV. The Great Diversification Play (2000s-2010s)

The decision came in a conference room in 2008, as global markets were melting down. While Lehman Brothers was collapsing and infrastructure companies worldwide were retrenching, Kalpataru's leadership made a counterintuitive call: this was the moment to diversify aggressively. Their logic was simple but bold—when everyone else was pulling back, assets were cheap, talent was available, and governments would soon need to spend on infrastructure to revive their economies.

The transformation didn't happen overnight. It began with adjacent capabilities. KPIL became a leading player in the Oil & Gas pipeline business in India, covering cross-country Oil & Gas pipelines, processing facilities, refineries, and fertilizer plants. The company delivered projects covering design & engineering, civil, electrical, mechanical, procurement, construction management, testing, and commissioning. This wasn't a random leap—laying pipelines required similar project management skills as transmission lines: dealing with right-of-way issues, managing linear construction across hundreds of kilometers, coordinating with multiple stakeholders.

The entry into Buildings & Factories was more ambitious. Equipped with PAN India reach, expertise, and experienced manpower to undertake all types of building and housing projects, KPIL provides world-class infrastructure support to India's growing Healthcare, Institutional, Residential, Townships, Commercial, Industrial, Hospitality, IT office spaces, Data centers, Manufacturing Plants, and Services sectors. This required different capabilities—architectural coordination, HVAC systems, finishing work. But Kalpataru saw an opportunity: India's real estate sector was notorious for delays and quality issues. A company with disciplined project management could differentiate itself.

Water infrastructure came next, and the scale achieved was remarkable. The company's water projects now serve over 15 million beneficiaries and 7.5 lakh house service connections worldwide, providing EPC solutions for drinking water supply and distribution systems, wastewater collection treatment, and irrigation. Water projects were technically complex—requiring understanding of hydraulics, treatment processes, and distribution networks—but politically even more so. Water was a state subject in India, meaning navigating different state regulations and local politics.

As a leading EPC contractor in the railways infrastructure space, KPIL caters to turnkey solutions for conventional rail lines and metro rail. The company undertakes comprehensive railway projects encompassing overhead electrification, traction substations, track laying, earthwork, bridges, buildings, stations, workshops, signaling & telecommunications, and 3rd Rail DC systems. Railways was perhaps the most audacious diversification. Indian Railways was a closed ecosystem with its own standards, its own bureaucracy, its own way of doing business. Breaking in required not just technical capabilities but understanding an entirely different procurement and execution culture.

The masterstroke, however, was the JMC Projects acquisition and eventual merger. The National Company Law Tribunal approved the merger making it one of the country's largest listed engineering and construction companies. The combined entity will have a significant presence in India and projects in 67 countries, with offerings in well diversified areas of power transmission and distribution, buildings and factories, water, railways, oil and gas and heavy civil infrastructure.

JMC wasn't just bought; it was cultivated. JMC has been involved in the construction of landmark edifices and has developed expertise in areas like highways, expressways, bridges, flyovers, townships, highrise buildings, commercial buildings, IT-ITES parks, hospitals, educational complexes, industrial units, metro rail, water supply and power plants. The merger, approved in December 2022, created "combined order visibility of nearly Rs 43,000 crores".

What made this diversification strategy work wasn't just ambition—it was execution discipline. Each new vertical was approached methodically: start with small projects to understand the domain, build capabilities organically, hire sector experts, then scale gradually. They didn't try to become L&T overnight. They picked specific niches where their project management DNA could create competitive advantage.

The international expansion during this period was equally strategic. JMC has expanded its operations in the international EPC market with presence in Sri Lanka, Ethiopia, Mongolia and Maldives. Rather than chasing projects globally, they focused on markets where Indian EPC companies had natural advantages—countries with similar development challenges, Commonwealth nations with compatible legal systems, regions where Chinese competition wasn't overwhelming.

Risk management became increasingly sophisticated. Currency hedging for international projects, commodity price escalation clauses, termination compensation provisions—the contracts became as complex as the projects themselves. They learned expensive lessons: a pipeline project delayed by environmental clearances, a building project stuck in litigation, a railway contract with scope creep. Each failure refined their bidding and execution processes.

By 2020, Kalpataru had transformed from a transmission tower manufacturer into something entirely different—a full-spectrum infrastructure company. The vision articulated during the merger was ambitious: "being a USD 3 billion revenue organisation by 2025". The diversification wasn't just about growth; it was about resilience. When transmission orders slowed, buildings compensated. When domestic projects faced delays, international ones provided cash flow.

The transformation set the stage for the next phase—competing not just with Indian peers but positioning for the global infrastructure opportunity that the 2020s would bring.

V. The Infrastructure Boom Years & Global Expansion

The map in Kalpataru's war room tells a story of audacious ambition. Red pins mark active projects across continents: transmission lines cutting through Ethiopian highlands, water treatment plants in Sri Lankan coastal cities, metro stations rising in congested Asian capitals, and most recently, over 800 kilometers of gas pipelines for Saudi Aramco's Master Gas System. KPIL has announced securing significant engineering, procurement, and construction (EPC) contracts from Saudi oil giant Aramco for its pivotal Master Gas System Network (MGS‐3) project in the kingdom, with the EPC scope encompassing laying over 800 km of lateral gas pipeline.

KPIL is currently executing projects in over 30 countries and has global footprints in 70+ countries like America, Australia, Africa, CIS, Middle East, SAARC & Asia-Pacific. This isn't just geographic expansion—it's a masterclass in navigating the complexities of emerging market infrastructure.

The international journey began with calculated steps into familiar territory. SAARC nations—Nepal, Bangladesh, Sri Lanka—offered cultural affinity and compatible technical standards. But the real test came when venturing into Africa, where Chinese state-backed companies had seemingly insurmountable advantages: cheaper financing, government support, and willingness to accept lower returns.

Kalpataru's Africa strategy was different. Instead of competing on price with Chinese firms, they focused on complex, technically challenging projects where execution excellence mattered more than financing terms. A 400kV transmission line through Kenya's Rift Valley, where seismic activity and extreme weather created engineering nightmares. Water treatment facilities in Tanzania that required not just construction but community engagement and local capacity building.

The Middle East presented different challenges and opportunities. With approximately two decades of experience in cross‐country pipelines, processing facilities, refineries, and fertilizer plants, KPIL has successfully commissioned over 10,000 kilometres of oil and gas and water pipelines in the Middle East and India. Here, the competition wasn't Chinese but Korean and European companies with decades-long relationships. Kalpataru broke through by positioning itself as the "Goldilocks option"—more sophisticated than local contractors but more cost-effective than Western firms.

Currency risk management became an art form. A project bid in Ethiopian Birr, executed with equipment purchased in Euros, labor paid in Indian Rupees, and revenues ultimately converted to dollars—each project was a complex financial derivative. They developed sophisticated hedging strategies, sometimes accepting lower margins for currency stability, other times taking calculated risks when local currencies seemed undervalued.

Political risk was even more complex. A coup in Myanmar froze projects mid-execution. Currency controls in Nigeria trapped cash for months. Environmental protests in Kenya delayed transmission lines. Each crisis taught expensive lessons about the importance of political risk insurance, local partnerships, and maintaining relationships across political divides.

KPIL has three main subsidiary companies – Linjemontage I GrastorpAB in Sweden, Fasttel Engenharia in Brazil and Shree Shubham Logistics Ltd in India. These weren't just acquisitions but strategic beachheads. The Swedish subsidiary provided entry into Nordic markets and credibility in European tenders. The Brazilian operation opened doors in Latin America, where Portuguese language capabilities and understanding of civil law systems were crucial.

The execution complexity of international projects dwarfed domestic ones. Consider a typical African transmission project: equipment manufactured in India, shipped through Dubai, cleared through customs in Mombasa, transported through three countries to a project site where the nearest town might be 200 kilometers away. Local labor needed training, expatriate engineers needed security, and every delay cost thousands of dollars per day.

Projects under execution: 300+ Globally executed order book: USD 12+ Billion Managing 300+ simultaneous projects across continents required building organizational capabilities that few Indian companies possessed. They invested in enterprise resource planning systems that could handle multiple currencies and tax regimes. They developed a cadre of international project managers comfortable working everywhere from Saudi deserts to African rainforests.

The competition evolved with geography. In Southeast Asia, they faced Japanese trading houses with deep pockets and patient capital. In the Middle East, Turkish contractors who could mobilize thousands of workers within weeks. In Africa, Chinese state-owned enterprises that treated infrastructure projects as loss leaders for broader economic influence. Each market required different strategies, different partnering approaches, different risk appetites.

Local partnerships became crucial differentiators. In Ethiopia, partnering with local construction firms not only provided market knowledge but also political insurance—local partners had incentives to navigate bureaucratic challenges. In Saudi Arabia, joint ventures with established local players were often mandatory but also provided invaluable wasta (influence) in navigating the kingdom's complex business environment.

Technology adoption varied dramatically across markets. While Indian projects might still rely on paper documentation, Middle Eastern clients demanded Building Information Modeling (BIM) and digital project management. African projects required innovative solutions for remote monitoring—using satellite imagery to track progress when site visits were impossible due to security concerns.

The human dimension of global expansion was perhaps most challenging. Convincing Indian engineers to relocate to African project sites, managing multicultural teams where a morning meeting might include Indians, Filipinos, Kenyans, and Chinese, ensuring safety standards in countries where construction casualties were considered routine—each required careful management and cultural sensitivity.

The financial rewards justified the complexity. International projects typically offered better margins than cutthroat domestic tenders. More importantly, geographic diversification provided resilience—when Indian infrastructure spending slowed, Middle Eastern projects compensated; when oil prices crashed affecting Gulf projects, African infrastructure funded by Chinese loans continued.

The infrastructure boom years established Kalpataru as a truly global player. But with global reach came global risks, and the company would soon need to transform once again to maintain its competitive edge in an rapidly evolving market.

VI. The Transformation & Rebranding (2020s)

The moment came in April 2023. The board had gathered to approve what seemed like a routine corporate action—a name change. But for those who understood Kalpataru's journey, this was the formal acknowledgment of a transformation that had been decades in the making. The company that once manufactured transmission towers was now executing airport projects, building data centers, and had just landed its largest-ever Buildings & Factories contract—a design-and-build development of 12 million sq ft of residential space with supporting infrastructure.

As of June 30, 2025, KPIL's outstanding order book was Rs.65,475 crore—a number that would have seemed fantastical just a decade earlier. More remarkably, power T&D enjoying a 41 per cent share, followed by the B&F segment with 25 per cent. The diversification wasn't just real; it had fundamentally altered the company's DNA.

The rebranding from Kalpataru Power Transmission Limited to Kalpataru Projects International Limited wasn't marketing fluff. The new Company name - Kalpataru Projects International Limited truly reflects the well-diversified EPC business and global presence of our Company. It signaled to customers, especially international ones, that this wasn't just a power company dabbling in other sectors but a comprehensive infrastructure solutions provider.

The transformation was most visible in the order book composition. In FY26 (April 1, 2025 up to August 7, 2025) stood at Rs.9,899 crore with the B&F segment accounting for 68 per cent (or Rs.6,711 crore) and power T&D making up for the remaining 32 per cent. Buildings & Factories had become the growth engine, a remarkable pivot for a company built on transmission towers.

Largest-ever B&F contract: Design-and-build development of 12 million sq ft of residential space with supporting infrastructure represented a new level of ambition. This wasn't just construction; it was comprehensive development including design, infrastructure, and project management for what would essentially be a new township. The scale dwarfed anything Indian EPC companies typically attempted.

The sustainability focus wasn't greenwashing but strategic positioning for future opportunities. Two Biomass power plants in the state of Rajasthan with a combined capacity of 15.8 MW (7.8 MW and 8.0 MW) using Direct Combustion Boiler technology. KPIL was one of the top companies to get registered with UNFCCC in 2005. This early move into renewable energy and carbon credits positioned them well for the ESG-focused infrastructure boom of the 2020s.

Technology adoption accelerated dramatically. expanding civil business in international markets, adding large size orders in T&D in India and international markets, and ventured into newer areas like airports, solar EPC, data centers etc. Data centers, in particular, represented a fascinating evolution—from building transmission infrastructure to constructing the physical homes for digital infrastructure.

The financial performance validated the transformation strategy. A ₹ 9 final dividend per share (450% of face value) demonstrated confidence in cash generation despite the capital-intensive nature of the business. This wasn't typical for infrastructure companies, where cash was usually recycled into growth rather than returned to shareholders.

Management's communication became notably more sophisticated. Quarterly earnings calls now discussed not just order books but execution margins by segment, working capital optimization strategies, and return on capital employed improvements. The company was speaking the language of global institutional investors, not just domestic infrastructure watchers.

The international subsidiaries evolved from acquisition targets to growth drivers. the order book of LMG, as of June 30, 2025, was Rs.3,494 crore and that of Fasttel, Rs.551 crore. These weren't just flags on a map but operational centers driving regional expansion—LMG in Nordic markets, Fasttel in Latin America.

Risk management became increasingly sophisticated as projects grew in complexity. The 12 million square foot residential development required managing not just construction risk but market risk—what if residential demand softened? Currency hedging for a Rs.65,000+ crore order book spanning multiple currencies required treasury operations that resembled a small bank.

The human capital transformation was equally dramatic. MOUs in Bihar with Government ITIs, West Muzaffarpur (Muzaffarpur) & Raniganj (Araria), to establish the Kalpataru Skill Development Academy (KSDA) within their premises. These centers will provide a 2-month skill development program for ITI & Non-ITI candidates in Masonry, Bar Bending, and Formwork Carpentry trades. The initiative aims not only to impart skills but also to instil professionalism, bridging the gap between education and employment. After successful training, the candidates will seamlessly transition into employment at Kalpataru's project sites. This wasn't corporate social responsibility but strategic workforce development, ensuring skilled labor availability for massive project pipelines.

Competition dynamics shifted with the transformation. They were no longer competing just with transmission specialists like KEC but with diversified giants like L&T across multiple sectors. In buildings, they faced real estate developers turning to EPC. In water, they competed with specialized water infrastructure companies. Each sector required different competitive strategies, different relationship management, different risk appetites.

The transformation validated a fundamental insight: in infrastructure, execution excellence is transferable across sectors. The skills needed to manage a transmission project in Ethiopia—stakeholder management, logistics, quality control, cash flow management—translated remarkably well to building a data center in India or laying pipelines in Saudi Arabia. The rebranding was simply acknowledgment of what Kalpataru had become: not a power company that diversified, but an execution machine that happened to start in power.

VII. Modern Operations & Business Model

Walk into Kalpataru's project monitoring center in Mumbai, and you're looking at the nerve center of a ₹23,900 crore revenue machine. Giant screens display real-time updates from 300+ active projects: a transmission line being strung in Kenya updates progress every hour via satellite imagery, a water treatment plant in Gujarat streams turbidity readings, workers checking into a residential construction site in Pune through biometric systems. Business Segments 1) EPC (97% in 9M FY25 vs 96% in FY23)—the core remains engineering, procurement, and construction, but the sophistication of execution has evolved dramatically.

The numbers tell a story of operational excellence: The company posted a consolidated net profit of ₹213.59 crore, marking a 155% jump compared to ₹83.95 crore in the same quarter last year (Q1 FY25). Revenue from operations grew by 35%, reaching ₹6,171.17 crore, up from ₹4,586.60 crore in Q1 FY25. But these headline figures mask the complexity of managing such diverse operations.

The working capital story is perhaps most impressive. Net Working Capital: Standalone improved to 94 days; consolidated improved to 79 days. In an industry where 150-200 day cycles are common, this efficiency represents millions in freed capital. They've achieved this through sophisticated vendor financing, aggressive collection strategies, and most importantly, careful project selection that prioritizes clients with strong payment track records.

Human capital management at 22,225 employees is a logistics challenge comparable to running a small city. The workforce spans from PhD engineers designing transmission systems to skilled welders working in 45-degree heat in Middle Eastern deserts. Each requires different management approaches, compensation structures, safety protocols. The company runs its own training academies, not as CSR but as strategic necessity—when you need 500 bar benders for a massive construction project, you can't rely on the open market.

Technology adoption has accelerated beyond recognition from the manual processes of a decade ago. Building Information Modeling (BIM) is now standard for complex projects. Drones monitor linear construction progress. IoT sensors track equipment utilization. Machine learning algorithms predict project delays based on weather patterns, supplier performance, and hundreds of other variables. This isn't tech for tech's sake—it's about squeezing efficiency from operations where 1% improvement in execution can mean crores in additional profit.

The segment performance reveals strategic choices. T&D Business Revenue: Crossed INR10,000 crores with 28% YoY growth. Despite diversification, transmission remains the cash cow, generating predictable margins and leveraging four decades of expertise. Urban Infra Revenue Growth: 10% increase for FY25. The newer segments grow more slowly but offer diversification and often better margins on complex projects.

International subsidiaries have evolved into profit centers. LMG Sweden Revenue Growth: 79% increase with an order book of over INR2,800 crores. The Swedish operation isn't just about Nordic markets—it's become the gateway to European standards and relationships that open doors globally.

But challenges persist. The Water business faced challenges due to delayed collections and deferred fund allocation, impacting revenue growth in FY25. Consolidated margins were affected by losses in subsidiaries, including Fasttel Brazil and historical projects in Saudi Arabia. The railway segment is experiencing intense competition, leading to cautious order booking and potential revenue decline.

Financial management has become increasingly sophisticated. Standalone Net Debt: Declined 40% YoY to INR1,107 crores. Consolidated Net Debt: Declined 25% YoY to INR1,953 crores. This debt reduction while maintaining growth represents careful capital allocation—using operational cash flow to deleverage while funding growth through internal accruals rather than additional borrowing.

EBITDA came in at ₹525 crore, up 38.6% from ₹379 crore last year, indicating strong operational performance. Meanwhile, EBITDA margin improved slightly to 8.5%, compared to 8.3% in the previous year. These margins might seem modest compared to asset-light businesses, but in the EPC world where 5-6% EBITDA margins are common, consistent 8%+ margins indicate pricing discipline and execution excellence.

The order book composition reveals strategic positioning. Order Book: Reached INR64,495 crores; order inflows of INR25,475 crores in FY25. With nearly three years of revenue visibility, the company can be selective about new projects, choosing based on margins and strategic fit rather than desperation for growth.

Risk management has evolved from reactive to predictive. Every project goes through a rigorous risk scoring before bidding—evaluating client credibility, geographic risks, technical complexity, and working capital requirements. Projects that score poorly are either avoided or priced with sufficient risk premiums. This discipline means walking away from headline-grabbing mega projects that could destroy value.

Competition varies dramatically by segment and geography. In Indian transmission, they compete with KEC International and L&T on price and execution speed. In Middle Eastern oil & gas, it's about technical capabilities and safety records. In African water projects, it's about financing structures and local partnerships. Each requires different strategies, different teams, different approaches.

The business model has evolved from a construction company to something more sophisticated—a solutions provider that happens to execute through construction. When they bid for a data center project, they're not just offering to build a structure but providing integrated solutions including power infrastructure, cooling systems, and sometimes even operational support. This value addition allows premium pricing and creates competitive moats.

Looking at the numbers—Revenue: 23,900 Cr · Profit: 697 Cr · The company has delivered a poor sales growth of 12.0% over past five years. · Company has a low return on equity of 9.56% over last 3 years.—reveals both strength and challenge. The revenue scale is impressive, but growth has been measured, and returns remain modest. This is the fundamental tension of the EPC business: growth requires capital, but capital discipline is essential for survival.

The modern Kalpataru operates less like a traditional construction company and more like a distributed manufacturing system, producing infrastructure instead of products. Each project is a temporary factory, assembled for a specific purpose, operated with manufacturing-like efficiency, then disbanded. The ability to repeatedly create and manage these temporary organizations across diverse geographies and sectors—that's the real competitive advantage, built over four decades and nearly impossible to replicate quickly.

VIII. Playbook: Infrastructure EPC Lessons

The conference room in Kalpataru's Mumbai headquarters has witnessed thousands of bid decisions over four decades. The walls could tell stories of projects won at razor-thin margins that nearly bankrupted the company, of bold bets on new geographies that paid off spectacularly, of painful lessons learned when scope creep turned profitable projects into money pits. These experiences have crystallized into an unwritten playbook that governs how Kalpataru approaches the brutal, capital-intensive world of infrastructure EPC.

The Art of Bidding: The 70-20-10 Rule

"Never bid on emotion, always bid on data," is the mantra repeated before every major tender submission. Kalpataru's bidding philosophy follows what internally they call the 70-20-10 rule. Pursue projects where you have 70% confidence in execution based on past experience. Add 20% stretch—new elements that push capabilities but aren't revolutionary. Accept 10% uncertainty because perfect information never exists. Projects that violate this ratio get rejected, regardless of size or prestige.

The discipline is harder than it sounds. When a ₹5,000 crore metro project tender hits the market, every EPC player salivates. The temptation to underbid for glory is immense. Kalpataru has learned to resist. They've watched competitors win "trophy projects" at 3% margins only to lose money when steel prices spike or monsoons delay execution. Their bidding committee has a simple rule: if you can't model at least three scenarios where the project remains profitable, don't bid.

Execution Excellence: The Power of Boring

In infrastructure, boring is beautiful. Kalpataru's execution philosophy prioritizes predictability over heroics. They've developed something called the "Module Library"—standardized approaches to common project elements. Foundation work for transmission towers in black cotton soil? There's a module. Welding protocols for gas pipelines in desert conditions? Another module. Managing tribal area permissions for railway projects? Module.

This standardization might seem to stifle innovation, but it's precisely the opposite. When 80% of a project follows proven protocols, teams can focus creative energy on the 20% that's unique. A project manager in Ethiopia doesn't need to reinvent how to manage concrete curing in high temperatures—that knowledge is codified from dozens of similar projects across Africa and the Middle East.

Working Capital: The Silent Killer

More EPC companies die from cash flow than from bad execution. Kalpataru learned this lesson expensively in the early 2000s when a technically perfect project nearly sank them because the client—a state electricity board—delayed payments by 18 months. Since then, working capital management has become almost religious.

Every project has three financial models: the bid model (optimistic), the execution model (realistic), and the stress model (pessimistic). The stress model assumes payments delayed by six months, cost escalations of 15%, and scope changes of 20%. If the stress model shows negative cash flow beyond acceptable limits, the project gets restructured or rejected.

They've also mastered the art of payment structuring. Advance payments, milestone-based releases, equipment-linked payments, retention guarantees—each contract is carefully crafted to minimize working capital exposure. In international projects, they often insist on letters of credit or escrow accounts, accepting lower margins for payment certainty.

Risk Mitigation: The Swiss Cheese Model

Borrowed from aviation safety, Kalpataru uses a "Swiss Cheese Model" for risk management. Every project has multiple layers of risk mitigation, like slices of Swiss cheese. Each layer has holes (potential failures), but when properly aligned, the holes don't line up, preventing catastrophic failure.

Layer one: Technical risk assessment during bidding. Layer two: Contractual protections including force majeure, variation clauses, and escalation provisions. Layer three: Insurance covering everything from equipment damage to political risk. Layer four: Local partnerships that provide on-ground intelligence and relationship capital. Layer five: Financial hedging for currency and commodity exposure. Layer six: Operational redundancy—backup suppliers, equipment, even project managers.

Local Partnerships: The Make-or-Break Factor

In international projects, the right local partner can mean the difference between profit and disaster. But choosing partners is an art. Too small, and they lack capability. Too large, and they might sideline you. Too connected, and you're vulnerable to regime changes. Too clean, and they can't navigate local realities.

Kalpataru's approach is pragmatic. They maintain a database of potential partners in key markets, tracked over years. They watch how partners perform with competitors, how they handle disputes, how they weather political changes. When entering a new market, they often start with small projects to test partnerships before committing to major ventures.

The partnership structuring is equally crucial. Clear delineation of responsibilities, transparent financial arrangements, dispute resolution mechanisms, and crucially, exit clauses. Every partnership agreement assumes the partnership might fail and plans accordingly.

Technology Adoption: Evolution, Not Revolution

While Silicon Valley disrupts, infrastructure evolves. Kalpataru's technology adoption follows this reality. They don't chase bleeding-edge tech but focus on proven technologies that can be reliably deployed in harsh field conditions.

Their technology stack is practical: GPS tracking for equipment utilization, satellite imagery for progress monitoring, mobile apps for quality checkpoints, cloud-based project management systems. Nothing revolutionary, but when deployed across 300+ projects, the cumulative efficiency gains are substantial.

The real innovation is in integration. Data from multiple systems feeds into a central dashboard that gives real-time visibility into project health. A delay in steel delivery to a Kenya project triggers automatic alerts to procurement, finance, and project management. This integrated visibility prevents small problems from becoming crises.

Government Relations: The Delicate Dance

Infrastructure EPC is inherently political. Projects require countless approvals, face constant scrutiny, and often become political footballs. Kalpataru has learned to navigate this through what they call "institutional engagement"—building relationships with institutions rather than individuals.

They maintain dedicated teams for regulatory compliance, ensuring every permission is documented, every approval is transparent. They avoid shortcuts that competitors might take, understanding that short-term gains from regulatory compromises lead to long-term vulnerabilities.

When disputes arise—and they always do—the approach is litigation as last resort. Negotiation, mediation, arbitration are preferred, not from weakness but from practicality. A project stuck in court for five years is a failed project, regardless of who wins the case.

The Ultimate Lesson: Discipline Over Growth

The biggest lesson from Kalpataru's playbook is counterintuitive: in infrastructure EPC, discipline beats growth. The companies that survive decades aren't necessarily the ones that grow fastest but those that maintain execution discipline, financial prudence, and strategic focus.

This means saying no to more projects than you say yes to. It means accepting that some years will show modest growth because the right opportunities weren't available at the right prices. It means watching competitors celebrate massive order wins while you quietly execute profitable projects.

The infrastructure EPC game is ultimately a marathon, not a sprint. The playbook that Kalpataru has developed over four decades reflects this reality—prioritizing sustainability over splash, execution over expansion, and discipline over drama. In an industry littered with spectacular failures of once-high-flying companies, sometimes the best strategy is simply to survive and compound.

IX. Bull vs. Bear Case Analysis

The investment thesis for Kalpataru Projects International sparks heated debates in Mumbai's financial districts. At ₹1,200 per share, with a market cap hovering around ₹21,000 crore, the company trades at valuations that seem either compellingly cheap or dangerously fair, depending on your perspective. The bull and bear cases aren't just about numbers—they're about fundamentally different views on India's infrastructure future and Kalpataru's ability to capture it.

The Bull Case: Infrastructure's Golden Decade

The bulls start with a simple observation: As of June 30, 2025, KPIL's outstanding order book was Rs.65,475 crore—nearly three years of revenue visibility at current run rates. This isn't speculative backlog but confirmed orders from creditworthy clients across diversified sectors and geographies. "Our order book stands at record level of Rs.65,475 crore and business visibility remains robust", management notes, and bulls see this as conservative given India's infrastructure ambitions.

The margin story is equally compelling. In FY25, standalone EBITDA rose 16% YoY to INR 1,587 crore, while consolidated EBITDA climbed 13% YoY to INR 1,834 crore. Profit before tax (PBT) before exceptional items stood at INR 929 crore on a standalone basis, marking a 20% increase year-on-year. On a consolidated level, PBT reached INR 823 crore, up 17% from the previous fiscal. This isn't just growth—it's profitable growth with expanding margins, suggesting operational leverage is finally kicking in.

India's infrastructure opportunity is massive and accelerating. The government's ₹100 lakh crore National Infrastructure Pipeline, the energy transition requiring massive grid upgrades, urbanization driving real estate and metro projects—each trend alone could sustain decades of growth. Kalpataru, with proven execution across all these sectors, is uniquely positioned to benefit regardless of which sector sees fastest growth.

The diversification strategy has created resilience that peers lack. When transmission orders slow, buildings compensate. When domestic projects face delays, international ones provide growth. This isn't theoretical—it's been demonstrated through multiple cycles. The company has survived and thrived through the 2008 financial crisis, 2013 taper tantrum, COVID-19 pandemic, and various domestic economic slowdowns.

ROCE improvement tells a story of capital efficiency gains. After years of heavy investments in capabilities and subsidiaries, the company is entering harvest phase. Standalone Net Debt: Declined 40% YoY to INR1,107 crores. Consolidated Net Debt: Declined 25% YoY to INR1,953 crores. This deleveraging while maintaining growth suggests the business is generating substantial free cash flow.

The international opportunity is underappreciated. KPIL is currently executing projects in over 30 countries and has global footprints in 70 + countries. As developed nations upgrade aging infrastructure and emerging markets build new capacity, Kalpataru's proven international execution capabilities become increasingly valuable. The Saudi Aramco contract wins demonstrate ability to compete for the most prestigious global projects.

Management quality and execution track record deserve premium valuation. Over four decades, they've successfully navigated India's complex business environment, expanded internationally, diversified across sectors, and maintained financial discipline. This isn't a company that needs to prove execution—it's proven over thousands of projects.

The replacement cost argument is compelling. Building Kalpataru's capabilities from scratch—manufacturing facilities, international subsidiaries, trained workforce, client relationships, prequalifications across sectors—would cost multiples of current market cap and take decades. The stock trades at significant discount to replacement value.

The Bear Case: Structural Challenges and Cyclical Headwinds

Bears point to uncomfortable realities hidden in the headline numbers. The company has delivered a poor sales growth of 12.0% over past five years. Company has a low return on equity of 9.56% over last 3 years. For a company in India's supposedly booming infrastructure sector, 12% five-year revenue CAGR is disappointing. The ROE below 10% suggests this is a capital-intensive business with limited ability to generate superior returns.

Promoter holding has decreased over last 3 years: -18.0% Promoter selling is never a positive signal. If insiders are reducing stakes despite the supposedly bright future, what do they know that outside investors don't?

Competition is intensifying across all segments. L&T's engineering division is 10x larger with better access to capital. Chinese companies are aggressively entering markets where Kalpataru operates. New players like Adani and GMR are entering infrastructure EPC. Technology companies are disrupting traditional project management. The competitive moat is narrowing.

Working capital intensity remains a fundamental challenge. Despite improvements, Net Working Capital: Standalone improved to 94 days still means the company needs substantial capital just to maintain operations. In a rising interest rate environment, this becomes a significant drag on returns.

Execution risks are multiplying. The company faces challenges in labor availability, which could impact the execution of large-scale projects. Skilled labor shortages, commodity price volatility, and supply chain disruptions post-COVID make project execution increasingly challenging. One major project failure could wipe out years of profits.

The segment-specific challenges are concerning. The Water business faced challenges due to delayed collections and deferred fund allocation, impacting revenue growth in FY25... The railway segment is experiencing intense competition, leading to cautious order booking and potential revenue decline. If diversified segments are struggling, the growth story becomes questionable.

Government dependency remains high. Despite diversification, a significant portion of revenues still comes from government contracts. Payment delays, policy changes, and political interference are perpetual risks. The recent focus on fiscal consolidation could slow infrastructure spending.

International risks are underestimated. Currency fluctuations, political instability, and payment risks in emerging markets create volatility. Consolidated margins were affected by losses in subsidiaries, including Fasttel Brazil and historical projects in Saudi Arabia. International expansion isn't always profitable.

The commodity super-cycle poses risks. Steel, copper, aluminum—key inputs—are seeing price volatility. While contracts have escalation clauses, these don't always fully protect margins. A sustained commodity price spike could squeeze profitability.

Technology disruption is a long-term threat. Modular construction, 3D printing, AI-driven project management—emerging technologies could disrupt traditional EPC models. Kalpataru's investments in technology seem incremental rather than transformational.

The Verdict: Nuanced Reality

The truth, as always, lies somewhere between extreme optimism and pessimism. Kalpataru represents a solid infrastructure play with proven execution capabilities and reasonable valuations. The record order book provides near-term visibility, while India's infrastructure needs offer long-term growth potential.

However, structural challenges—low ROE, working capital intensity, competitive pressures—cap the upside potential. This isn't a company that will deliver venture-style returns. It's a steady compounder that might deliver 12-15% annual returns through cycles.

For investors, the decision comes down to investment philosophy. If you believe in India's infrastructure story and want exposure through a proven executor, Kalpataru offers compelling risk-reward. If you're seeking high growth or superior returns on capital, look elsewhere.

The stock is neither dramatically undervalued nor dangerously expensive. It's fairly priced for what it is—a well-managed, diversified infrastructure company operating in a challenging but essential industry. In a market often driven by extremes, sometimes fair value is exactly what sophisticated investors should seek.

X. Future Outlook & Strategic Positioning

Standing at the crossroads of 2025, Kalpataru Projects International faces a future that's both exhilarating and treacherous. India's infrastructure ambitions have never been grander—₹100 lakh crore investment pipeline, renewable energy transformation requiring grid overhaul, hundred smart cities, thousands of kilometers of high-speed rail. Yet the path forward is strewn with challenges that could derail even the most capable executor.

The Mega-Trends Reshaping Infrastructure

The energy transition isn't just another trend—it's a complete rewiring of how power systems work. India's commitment to 500 GW renewable capacity by 2030 means transmission infrastructure designed for centralized coal plants must be rebuilt for distributed solar and wind generation. Kalpataru's transmission expertise positions them perfectly, but the technical complexity is unprecedented. Grid stability with intermittent renewable sources, energy storage integration, smart grid technologies—each requires capabilities beyond traditional EPC.

Urbanization is accelerating beyond projections. By 2030, 600 million Indians will live in cities—equivalent to the entire population of Latin America. This isn't just about building more—it's about building differently. Mixed-use developments, integrated transportation systems, sustainable water management, waste-to-energy plants. Kalpataru's recent 12 million square foot residential project signals ambition to capture this opportunity, but execution at this scale requires transformation from project executor to urban developer.

The digital infrastructure boom is creating entirely new categories of construction. Data centers alone could see $10 billion investment in India by 2027. But building data centers isn't like building warehouses—it requires understanding of cooling systems, power redundancy, network architecture. Kalpataru's entry into data centers is strategic but requires rapid capability building in a domain where technology companies have natural advantages.

Climate resilience is becoming non-negotiable. Every infrastructure project now needs to account for extreme weather events that are becoming routine. Transmission towers must withstand super-cyclones, water treatment plants must handle unprecedented floods, buildings must survive heat waves. This isn't just about stronger structures—it's about fundamentally rethinking design principles developed for a more stable climate.

International Opportunities and Threats

The global infrastructure opportunity dwarfs India's. Africa needs $170 billion annual infrastructure investment. Southeast Asia requires $2 trillion by 2030. Middle East's economic diversification drives massive construction. Latin America's infrastructure deficit creates decades of opportunity. Kalpataru's presence in 30+ countries positions them well, but competition is fierce.

Chinese companies remain the elephant in the room. With state backing, unlimited capital, and willingness to accept lower returns, they've dominated international infrastructure. Kalpataru must find niches where Indian execution, English-language capabilities, and democratic credentials provide advantages. The recent Saudi Aramco wins suggest this strategy can work, but it requires careful market selection.

Developed markets offer different opportunities. America's infrastructure bill, Europe's green deal, Australia's renewable buildout—these markets offer better payments and margins but demand highest standards. Kalpataru's Swedish and Brazilian subsidiaries provide entry points, but competing with established Western firms requires continued capability upgrading.

Geopolitical realignment creates both opportunities and risks. The China-plus-one strategy helps Indian companies, but also increases project risks in contested regions. Infrastructure projects are becoming geopolitical tools, and companies must navigate carefully to avoid becoming pawns in larger games.

Technology Adoption: The Imperative

The infrastructure industry stands at the cusp of technological transformation that could be as significant as mechanization was a century ago. Building Information Modeling (BIM) is becoming mandatory for complex projects. Artificial intelligence is moving from experiment to essential for project planning and risk management. Robotics and automation are entering construction sites. Kalpataru must decide whether to be technology adopter or leader.

The company's approach has been pragmatic—adopting proven technologies rather than experimenting with cutting-edge solutions. This reduces risk but might leave them vulnerable to disruption. A startup using AI to optimize project schedules could potentially deliver projects 20% faster. A competitor using modular construction could dramatically reduce costs. The balance between prudent adoption and innovative leadership will determine competitive positioning.

Digital twins—virtual replicas of physical infrastructure—are becoming standard for asset management. Clients increasingly expect not just construction but digital models that enable predictive maintenance, performance optimization, and lifecycle management. This requires capabilities beyond traditional EPC, blurring lines between construction and technology services.

Sustainability: From Compliance to Competitive Advantage

ESG isn't just about compliance anymore—it's becoming a competitive differentiator. International clients, especially in developed markets, increasingly mandate carbon footprint reporting, sustainable material usage, and social impact assessments. Kalpataru's early move into biomass power and UNFCCC registration shows foresight, but much more is needed.

Green financing is reshaping project economics. Projects with strong sustainability credentials access cheaper capital. Green bonds, sustainability-linked loans, and ESG-focused investors are creating financial incentives for sustainable infrastructure. Companies that can't demonstrate ESG excellence will face both higher capital costs and reduced access to projects.

The circular economy is entering construction. Recycled materials, modular designs enabling reuse, waste reduction through precise planning—these aren't just nice-to-haves but increasingly mandatory. Kalpataru needs to embed circular principles into project design and execution, requiring fundamental changes to procurement and construction processes.

Strategic Imperatives

Capital allocation becomes crucial with multiple growth opportunities. Should they double down on high-margin segments like oil & gas? Expand international presence through acquisitions? Invest in technology capabilities? Build asset ownership models for recurring revenue? Each path requires different capital deployment and risk appetite.

Human capital is the binding constraint. Manish Mohnot, MD & CEO, KPIL, said, "Building on our capabilities and diversified business profile, we remain firmly aligned and on track to deliver targeted revenue growth and profitability for FY26 and going forward." But delivering on this promise requires not just workers but skilled engineers, project managers, and technology specialists. The war for talent in infrastructure is intensifying.

Partnership strategies need evolution. Traditional subcontracting models are giving way to strategic partnerships where risks and rewards are shared. Technology partnerships for digital capabilities, financial partnerships for capital-intensive projects, operational partnerships for new geographies—each requires different structuring and management approaches.

The Path Forward

Kalpataru stands at an inflection point. The infrastructure opportunity—in India and globally—has never been larger. Their capabilities, track record, and financial position provide a strong foundation. But the industry is changing faster than ever, with new technologies, new competitors, and new customer expectations.

Success requires threading multiple needles simultaneously: maintaining execution excellence while adopting new technologies, expanding internationally while managing risks, diversifying offerings while maintaining focus, growing rapidly while preserving margins. It's a challenging balance that few companies manage successfully.

The next five years will determine whether Kalpataru transforms from a successful Indian EPC company into a global infrastructure major. The pieces are in place—record order book, proven capabilities, strategic diversification. But execution, as always in infrastructure, will make the difference between ambition and achievement.

The company's future isn't just about building infrastructure—it's about building the capabilities to thrive in an industry being transformed by technology, sustainability, and changing global dynamics. Those who adapt will capture enormous value. Those who don't will become case studies in disruption. For Kalpataru, the choice—and opportunity—has never been clearer.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube