IRB Infrastructure Developers: The Toll Road Empire

I. Introduction & Episode Roadmap

Picture this: It's 5:30 AM on the Mumbai-Pune Expressway, and the sun hasn't yet broken through the Western Ghats. A steady stream of trucks, cars, and buses flows through the toll plaza at Khalapur—each vehicle contributing a small fee that, multiplied millions of times over, creates rivers of cash flow. This six-lane marvel of engineering, India's first modern expressway, is now operated by IRB Infrastructure Developers, a company that has quietly built one of the most formidable toll road empires in Asia.

How does a family road construction business from Mumbai transform into India's largest road Build-Operate-Transfer (BOT) operator? How do you convince banks to lend billions for projects that won't generate revenue for years? And perhaps most intriguingly, how do you build a business model where the government hands you the rights to collect tolls on public roads for decades? Welcome to the story of India's largest road BOT operator with a portfolio of 36 projects—a company that controls 37% of the total TOT market share and has a ~20% share in Golden Quadrilateral Highway Network. IRB Infrastructure Developers isn't just another infrastructure company; it's a masterclass in how to transform public assets into private wealth generation machines while navigating the treacherous waters of Indian politics, regulation, and capital markets.

This is a story about timing, political savvy, and financial engineering. It's about how a 19-year-old civil engineer named Virendra Mhaiskar turned his family's modest road construction business into an infrastructure empire worth over ₹27,000 crores. It's about being first—executing India's first ever BOT project, the Thane-Bhivandi Bypass, and sponsoring India's first Infrastructure Investment trust. But most importantly, it's about understanding that in infrastructure, the real money isn't in building roads—it's in owning the right to collect tolls on them for decades.

Today, we'll explore how IRB navigated multiple economic cycles, survived political investigations, pioneered financial structures that changed Indian infrastructure financing forever, and built what is essentially a perpetual annuity machine. We'll examine the playbook that turned government infrastructure gaps into private market opportunities, and we'll scrutinize whether this empire built on tolls can withstand the headwinds of electric vehicles, changing government policies, and evolving transportation patterns.

Our journey spans from the dusty construction sites of 1990s Maharashtra to the sophisticated boardrooms of Mumbai's financial district, from family business meetings to international bond markets. This isn't just a business story—it's a blueprint for how infrastructure gets built in the world's largest democracy, with all its complexities, contradictions, and opportunities. Let's begin where all great infrastructure stories start: with a problem that needed solving.

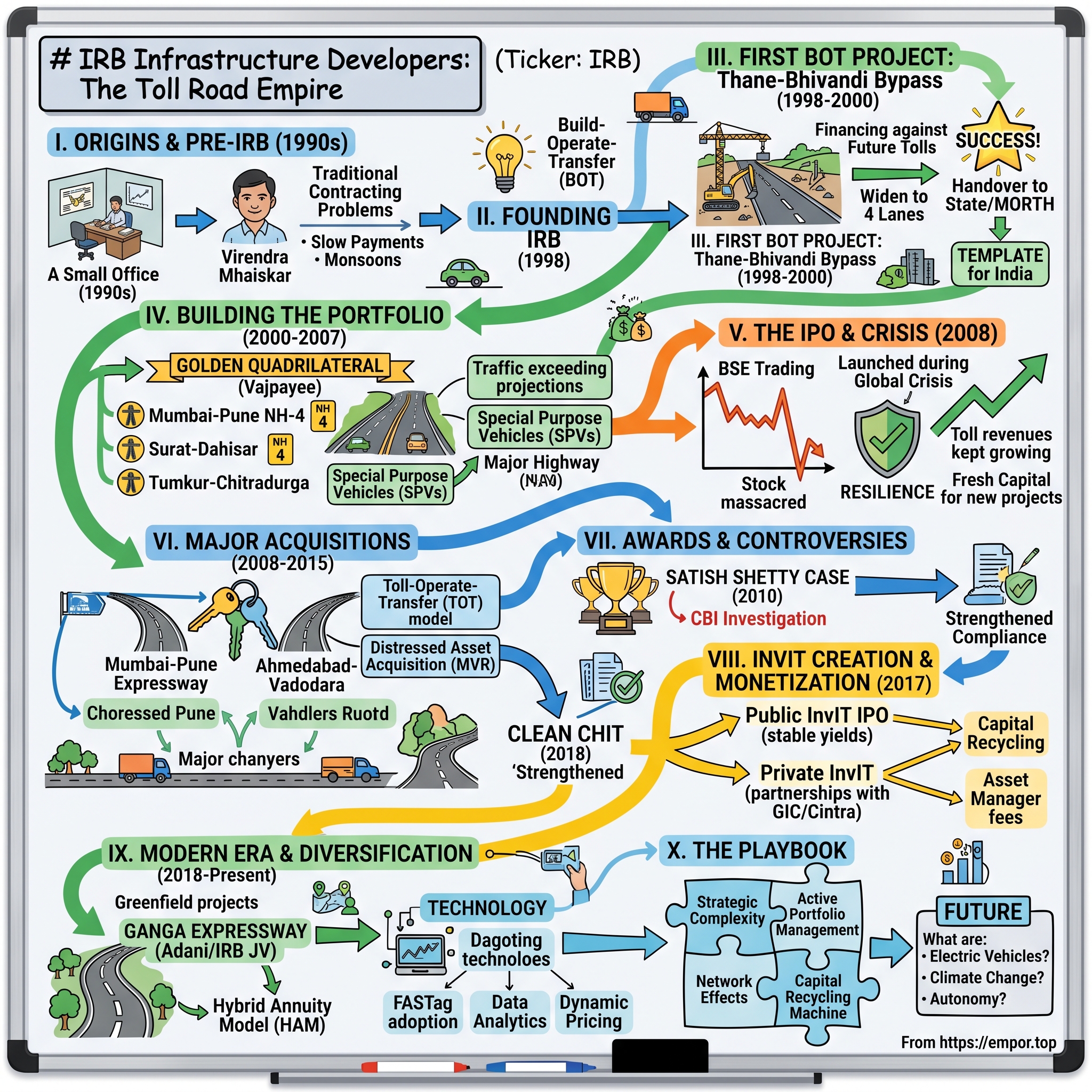

II. The Mhaiskar Family Origins & Pre-IRB Era

The year was 1990. India was on the cusp of economic liberalization, though nobody quite knew it yet. The Berlin Wall had just fallen, the Soviet Union was crumbling, and in a small office in Mumbai, a 19-year-old civil engineering student named Virendra Mhaiskar was making a decision that would reshape India's highway infrastructure landscape. He was joining the family road construction business—not because it was glamorous or lucrative, but because someone had to.

The Mhaiskar family had been in the road building business for years, operating as contractors for government projects. It was grueling work—managing labor, dealing with monsoons that could wash away months of progress, navigating the byzantine bureaucracy of the Public Works Department. The margins were thin, payments were chronically delayed, and corruption was endemic. Most road contractors in 1990s India operated on a simple principle: bid low, cut corners where possible, and hope the government paid you before you went bankrupt.

But Virendra saw something different. Fresh from the University of Bombay with a civil engineering degree, he understood that India's infrastructure deficit wasn't just a problem—it was an opportunity of generational proportions. The country had less than 2% of its road network that qualified as highways. The average speed on most "national highways" was 30 kilometers per hour. Moving goods from Delhi to Mumbai could take a week. This wasn't just inefficiency; it was a massive drag on economic growth.

The pre-liberalization era had created a peculiar dynamic in Indian infrastructure. The government monopolized all major projects but lacked both the capital and expertise to execute them efficiently. Private players were relegated to being mere contractors—building what the government designed, when the government decided, at prices the government determined. It was a system designed for mediocrity, and it delivered exactly that.

When economic liberalization arrived in 1991, it changed everything—except infrastructure. While telecom, aviation, and banking opened up to private participation, roads remained firmly in government hands. The conventional wisdom was simple: roads were public goods, tolls were politically sensitive, and no private player would invest billions in assets that took decades to generate returns. The Mhaiskar family business, like hundreds of others, continued as contractors, building stretches of road for state governments and collecting payments that arrived months or years late.

But Virendra was watching global trends. Countries like Malaysia, Thailand, and Chile had successfully implemented Build-Operate-Transfer (BOT) models for highways. Private companies would build roads with their own capital, operate them for 20-30 years collecting tolls, then transfer them back to the government. It aligned incentives perfectly—private efficiency in construction, long-term thinking in maintenance, and eventual public ownership of the asset. The model had one critical requirement though: trust. The government had to trust private players with public assets, and private players had to trust the government to honor multi-decade contracts.

By 1998, at age 27, Virendra had spent eight years learning every aspect of the road construction business. He understood soil mechanics and asphalt chemistry. He knew how to manage thousand-person work sites and negotiate with local politicians. Most importantly, he had built relationships—with banks who might fund projects, with bureaucrats who understood the need for change, and with engineers who shared his vision for what Indian infrastructure could become.

The family business had grown steadily but unspectacularly. They were known as reliable contractors who delivered projects on time, a rarity in an industry plagued by delays and cost overruns. But Virendra knew that being a good contractor was a recipe for permanent mediocrity. The real opportunity lay not in building roads for the government, but in owning and operating them. The question was: how do you convince the government to hand over one of its most visible public assets to a private company? And perhaps more challenging: how do you convince banks to fund projects that wouldn't generate revenue for years and required faith in toll collection projections that no one had ever tested in India?

The answer would come from an unlikely source: the Thane-Bhivandi bypass, a congested stretch of road outside Mumbai that nobody wanted to build. It would become India's first BOT project and the foundation of the IRB empire. But first, Virendra had to transform the family business from a traditional contractor into something India had never seen before—a professional infrastructure developer with the sophistication to structure complex financial deals and the operational excellence to deliver them. The transformation would begin with a simple but radical decision: incorporating IRB Infrastructure Developers Limited in 1998, signaling to the market that this wasn't just another family contractor, but a company built for the infrastructure opportunity of the century.

III. Founding IRB Infrastructure (1998) & Early Projects

The conference room at the Maharashtra State Road Development Corporation was suffocating. September 21, 1998—the monsoon hadn't quite ended, and the humidity made everyone's shirts stick to their backs. Virendra Mhaiskar sat across from government officials who looked skeptical, even hostile. On the table between them lay a document that would change Indian infrastructure forever: the concession agreement for the Thane-Bhivandi Bypass.

"You want us to give you a public road for 18 years?" the senior bureaucrat asked, his tone suggesting he thought Virendra was either naive or insane. The Thane-Bhivandi stretch was a nightmare—24 kilometers of congested two-lane road that connected Mumbai's industrial suburbs. Trucks queued for hours. Accidents were daily. The government had no money to widen it, and no contractor wanted to touch it without upfront payment.

IRB Infrastructure executed India's first ever BOT (build-operate-transfer) project, the Thane-Bhivandi Bypass. But this wasn't just about one road. Virendra had spent months studying successful BOT projects in Malaysia and Chile, understanding their financial structures, their risk allocations, their revenue models. He had convinced State Bank of India to consider project financing—lending against future toll revenues rather than physical collateral. It was a concept so foreign to Indian banking that the credit committee had spent three sessions just understanding the basic premise.

The negotiation had taken six months. Every clause was contested. Who would bear traffic risk? What happened if toll rates needed to increase? How would force majeure be defined? The government wanted the road widened but didn't want to pay for it. IRB wanted toll collection rights but needed traffic volume guarantees. The final structure was elegant in its simplicity: IRB would widen the existing 2-lane road to 4 lanes, build a new bridge on Kasheli Creek, and maintain everything for 18 years and 6 months, collecting tolls to recover their investment.

The numbers were daunting for a company that had just been incorporated. The project would cost approximately ₹100 crores—more money than the Mhaiskar family had seen in their entire history. But Virendra had done something clever. He had structured IRB Infrastructure Developers Limited not as a construction company that happened to do BOT projects, but as a developer that happened to have construction capabilities. The distinction was crucial for attracting institutional capital.

The early days of construction were brutal. The monsoon of 1999 flooded the construction site three times. Local politicians demanded "compensation" for disruption. Villagers protested the toll plaza locations. Environmental clearances were delayed. But IRB had an advantage that pure financial investors wouldn't have had—they were builders at heart. When contractors tried to inflate costs, Virendra knew exactly what concrete should cost per cubic meter. When engineers claimed technical impossibilities, he could sketch solutions on site.

The financial engineering was equally complex. This was before the era of infrastructure funds and specialized project finance. Banks didn't have models for toll road revenues. Insurance companies didn't know how to price construction risk. IRB had to educate an entire ecosystem while simultaneously executing the project. They created India's first traffic study models, hiring consultants to count vehicles and project growth rates. They pioneered escrow mechanisms that gave lenders comfort without strangling cash flows.

By late 2000, the widened road was operational. The first day of toll collection was a disaster—massive traffic jams as drivers, unaccustomed to paying tolls on this route, argued with collectors. Local newspapers ran headlines about "highway robbery." Politicians who had supported the project suddenly discovered populist opposition to tolls. But Virendra had anticipated this. IRB had spent months on community engagement, explaining how toll revenues would ensure proper maintenance, reduce accidents, and cut travel time in half.

The numbers told the real story. Travel time from Thane to Bhivandi dropped from 90 minutes to 35 minutes. Accident rates fell by 60%. Truck operators, despite paying tolls, saved money on fuel and time. Within six months, the protests died down. Within a year, traffic volumes exceeded projections by 15%. The project that nobody wanted to build was generating steady cash flows.

But the real victory wasn't financial—it was reputational. Upon successful completion of concession, the company handed over the Project to the Ministry of Road Transport & Highways (MORTH)/ PWD - Government of Maharashtra. IRB had proven that private companies could be trusted with public infrastructure. Banks had seen that toll revenues could service debt. The government had discovered a way to build infrastructure without budget allocations. Most importantly, IRB had created a template—legal, financial, and operational—that could be replicated across India.

The Thane-Bhivandi success opened doors that had been firmly shut. The National Highways Authority of India (NHAI), which had been skeptical of private participation, started drafting BOT policies. Banks created specialized infrastructure finance divisions. Other construction companies started reconsidering their business models. But IRB had a crucial first-mover advantage—they had live project data, proven execution capability, and most importantly, credibility with every stakeholder that mattered.

As 1998 turned to 1999, and then to 2000, Virendra's vision was crystallizing. India would need thousands of kilometers of new highways. The government had neither the money nor the capability to build them all. The BOT model could unlock trillions in private capital. And IRB, having proven the model with Thane-Bhivandi, was perfectly positioned to capture this opportunity. The family construction business had transformed into something unprecedented—a private infrastructure developer with the ambition to build India's highways and the credibility to make it happen. The question now wasn't whether the opportunity existed, but how fast IRB could scale to capture it.

IV. Building the BOT Portfolio (2000–2007)

January 6, 1999. Prime Minister Atal Bihari Vajpayee laid the foundation stone for what would become India's most ambitious infrastructure project—the Golden Quadrilateral. The foundation stone for the project was laid on 6 January 1999 by then prime minister Atal Bihari Vajpayee. Standing in his trademark dhoti and jacket, Vajpayee declared that India would build 5,846 kilometers of world-class highways connecting Delhi, Mumbai, Chennai, and Kolkata. The audience was skeptical. India had never built infrastructure at this scale or speed. But for Virendra Mhaiskar, watching the ceremony on television from his Mumbai office, this was the moment he had been preparing for.

The numbers were staggering. The project envisaged the development of about 13,150 km (8,170 mi) of four and six lane highways at an estimated cost of ₹540 billion. The government had neither the money nor the capacity to execute it alone. They needed private partners—companies that could build fast, finance creatively, and operate efficiently. IRB had spent two years since the Thane-Bhivandi success preparing for exactly this opportunity.

Virendra's strategy was counterintuitive. While other companies chased the glamorous Mumbai-Delhi or Chennai-Bangalore corridors, IRB focused on the "difficult" stretches—sections with land acquisition problems, complicated geology, or political sensitivity. These projects scared away pure financial investors but played to IRB's strengths as builder-operators. They could handle the construction complexity while structuring the financing to make the economics work.

The breakthrough came with the Mumbai-Pune section of NH-4, part of the Golden Quadrilateral's western corridor. This wasn't just any highway—it connected India's financial capital with its emerging IT hub, carrying massive commercial traffic through the challenging terrain of the Western Ghats. The project required 94 kilometers of six-lane highway, multiple tunnels, and engineering solutions for monsoon drainage that could wash away entire sections if done incorrectly.

IRB's bid was aggressive but calculated. They had traffic data from their operational projects showing that actual volumes consistently exceeded NHAI projections by 15-20%. They understood that truck operators, despite initial resistance to tolls, would pay for time savings and vehicle wear reduction. Most importantly, they had developed relationships with a consortium of banks—SBI, ICICI, and IDBI—who now understood the BOT model and trusted IRB's execution.

Over the years, its BOT portfolio (operational projects and projects under construction) in the country grew to a total length of around 12,000-lane km. But this growth wasn't random. Each project was selected based on three criteria: traffic potential, construction complexity that created barriers to entry, and strategic importance that ensured government support. The Surat-Dahisar section followed, then Tumkur-Chitradurga, then Jaipur-Deoli. By 2004, IRB was executing multiple projects simultaneously—a feat that required not just capital but organizational sophistication.

The operational innovation was as important as the financial engineering. IRB created dedicated Special Purpose Vehicles (SPVs) for each project, ring-fencing risks and making them bankable individually. They pioneered the use of independent engineers to certify construction milestones, giving lenders confidence. They developed India's first comprehensive toll management systems, using technology to reduce leakage—a critical issue when toll collectors were handling lakhs in cash daily.

The 2003-2007 period was transformative for Indian infrastructure financing. Banks, initially hesitant about 20-year project loans, started creating specialized infrastructure desks. Insurance companies, sitting on massive long-term liabilities, discovered that toll road bonds matched their duration needs perfectly. Foreign investors, through Mauritius structures, started participating in Indian infrastructure. IRB was at the center of this evolution, often structuring deals that became templates for the industry.

But success brought scrutiny. Local politicians questioned why private companies should collect tolls on "public" roads. Competing contractors spread rumors about IRB's political connections. Environmental activists challenged clearances. A Public Interest Litigation in 2005 questioned the entire BOT model's constitutionality. IRB navigated these challenges through a combination of transparency, stakeholder engagement, and most importantly, delivery. When the Surat-Dahisar section opened six months ahead of schedule, reducing Mumbai-Surat travel time from 8 hours to 4 hours, even critics acknowledged the transformation.

By 2007, IRB had created something unprecedented in Indian infrastructure—a portfolio of revenue-generating highway assets spread across multiple states. it has a ~20% share in Golden Quadrilateral Highway Network. They weren't just building roads; they were creating a new asset class. Pension funds started viewing toll roads as infrastructure bonds with equity upside. Private equity funds began calculating IRR on traffic growth. The Mumbai-Pune Expressway alone was generating ₹2 crores in daily toll revenue.

The company's internal capabilities had evolved dramatically. From a family-run construction firm with 50 employees in 1998, IRB now had over 500 engineers, financial analysts, and project managers. They had developed proprietary traffic forecasting models, construction techniques for Indian conditions, and most importantly, a reputation that opened doors. When NHAI officials said "IRB is bidding," banks paid attention.

But Virendra knew that going public was inevitable. The BOT model was capital-intensive—winning a project meant committing hundreds of crores upfront. Bank lending had limits. International investors wanted liquidity. Employees deserved stock options. Most importantly, being a listed company would provide the transparency and governance that would silence critics who questioned how a private company had won so many government contracts. The IPO preparation began in 2006, even as IRB continued bidding aggressively for new projects. The goal was ambitious: create India's first pure-play listed highway developer and use public markets to fund the next phase of growth. The timing, however, would prove to be more challenging than anyone anticipated.

V. The IPO & Going Public (2008)

The timing could not have been worse. Or perhaps, in hindsight, it was perfect.

January 31, 2008. The Bombay Stock Exchange was buzzing with nervous energy. Bear Stearns hedge funds had collapsed six months earlier. Northern Rock had been nationalized in the UK. But in India, the infrastructure story was still intact, the growth narrative unshaken. IRB Infra IPO opens on January 31, 2008, and closes on February 5, 2008—right in the eye of the gathering storm.

Virendra Mhaiskar stood in the trading hall, watching the screens flash with subscription numbers. The IPO was for 51,057,666 equity shares, a ₹944.57 crores bookbuilding issue. IRB Infra IPO price band is set at ₹185 per share to ₹220, valuing the company at approximately ₹4,500 crores at the upper end. For a company that started with family capital just a decade ago, these numbers were surreal.

The roadshow had been exhausting. Mumbai, Delhi, Singapore, London, New York—pitching to fund managers who were simultaneously excited about India's infrastructure opportunity and terrified about global credit markets. The questions were predictable but pointed: "What happens if traffic growth slows?" "How are you protected against interest rate increases?" "Why should we trust 20-year concession agreements with the Indian government?"

Deutsche Equities India Private Ltd and Kotak Mahindra Capital Company Limited were managing the issue, and they had crafted a compelling narrative. IRB wasn't just another construction company going public—it was offering investors a piece of India's infrastructure transformation. The pitch deck showed the Golden Quadrilateral map, traffic growth projections, and most importantly, the cash flows from operational projects that de-risked the growth story.

But behind the scenes, the global financial system was unraveling. The 2008 financial crisis, centered in the United States, had begun with the subprime mortgage crisis in early 2007 and would climax with the bankruptcy of Lehman Brothers in September 2008. Indian markets, initially thought to be insulated, were beginning to feel the tremors. FII selling had intensified. The Sensex had peaked at 21,000 in January and was beginning its descent.

The subscription period was nerve-wracking. Retail investors, attracted by the infrastructure story, subscribed strongly on the first day. But institutional subscription was sluggish. Foreign funds were pulling back from all emerging markets. Domestic institutions were cautious, waiting to see how others moved. By day three, whispers started: "Will it be fully subscribed?"

The final subscription numbers came as a relief—the issue was subscribed 1.5 times, respectable but not spectacular. The institutional portion was just covered, saved by late applications from LIC and domestic mutual funds who understood the long-term value. The retail portion was oversubscribed 2.1 times, a vote of confidence from individual investors who drove on IRB's roads daily.

The shares got listed on BSE, NSE on February 25, 2008. The listing day was volatile—the stock opened at ₹178, below the issue price of ₹185, traded as low as ₹165, but recovered to close at ₹182. It was a disappointing debut, but Virendra was philosophical. "We didn't come to the market for one-day gains," he told his team. "We came for long-term capital."

The use of proceeds had been clearly outlined—₹600 crores for new project development, ₹200 crores for debt repayment, and the balance for working capital. But within weeks of listing, the world changed. In the U.S., unemployment would rise to 10% by October 2009, the Dow Jones would fall by 53%, and one in four households would lose 75% or more of their net worth. In India, the Sensex crashed from 21,000 to 8,000. Infrastructure stocks were massacred as investors fled to safety.

IRB's stock price followed the market down, touching ₹89 by October 2008, less than half the IPO price. Short sellers circled, arguing that traffic growth would collapse, interest rates would spike, and the BOT model would unravel. Financial journalists wrote obituaries for infrastructure companies that had "mistimed" their IPOs. Employee morale plummeted as stock options went underwater.

But something interesting was happening on the ground. Traffic on IRB's operational roads didn't collapse—it kept growing. Trucks still needed to move goods. People still traveled between cities. Toll collections, while growing slower than projected, remained robust. The operational cash flows that IRB had pitched to investors were real, tangible, and resilient.

More importantly, the financial crisis created an unexpected opportunity. Competitors who had bid aggressively for projects couldn't achieve financial closure as banks stopped lending. International developers fled India. Project costs dropped as steel and cement prices crashed. IRB, with ₹944 crores of fresh capital and operational cash flows, was one of the few players who could still bid for and execute projects.

The government, desperate to stimulate the economy, accelerated infrastructure spending. NHAI relaxed bidding norms, offered better terms, and processed approvals faster. Projects that would have attracted ten bidders in 2007 now had three. IRB's financial discipline during the boom—not overleveraging, not overbidding—became its greatest strength during the bust.

By 2009, as markets began recovering, IRB had added three major projects to its portfolio at attractive terms. The stock, which had been written off at ₹89, crossed ₹200. Early investors who had stayed the course doubled their money. The financial crisis, rather than destroying IRB, had accelerated its consolidation of the Indian highway sector.

The IPO, despite its timing, had achieved its strategic objectives. It had provided growth capital when others had none. It had created a acquisition currency in a buyers' market. Most importantly, it had forced IRB to adopt institutional governance—quarterly earnings calls, independent directors, audit committees—that would become crucial as the company grew from a family business into an infrastructure institution. The 2008 IPO, launched in crisis and validated through resilience, had set the stage for IRB's next phase: becoming India's highway infrastructure powerhouse.

VI. Major Project Acquisitions & Expansion (2008–2015)

The conference room at the Maharashtra State Road Development Corporation was packed. March 2010. Outside, Mumbai's humidity was oppressive, but inside, the atmosphere was electric. On the table was one of India's most prized infrastructure assets—the Mumbai-Pune Expressway, the country's first six-lane concrete expressway, an engineering marvel that had transformed travel between India's commercial and IT capitals.

IRB Infrastructure acquired the Mumbai-Pune Expressway and the Mumbai-Pune National Highway. This wasn't just another road acquisition; it was a statement of intent. The expressway carried 35,000 vehicles daily, generated ₹2.5 crores in toll revenue every single day, and had become the benchmark for highway quality in India. For IRB to operate this asset meant they had arrived at the very top tier of Indian infrastructure companies.

The acquisition was complex—a rare Toll-Operate-Transfer (TOT) model where IRB would operate and collect tolls for 15 years, paying the government an upfront premium. The bidding had been fierce. Reliance Infrastructure, L&T, and GMR were all in the fray. But IRB had an edge—they understood toll operations better than anyone else, having pioneered electronic toll collection and leak-proof cash management systems.

The winning bid of ₹1,680 crores raised eyebrows. Analysts questioned whether IRB was overpaying. But Virendra had done his math differently. He saw what others missed—the expressway connected to Pune's IT corridor, where companies like Infosys and Wipro were expanding rapidly. Every new IT park meant thousands of daily commuters. Every new residential complex in Pune meant weekend traffic to Mumbai. The growth wasn't linear; it was exponential.

In July 2011, IRB Infrastructure signed an agreement to develop a 102.3 km section in the Ahmedabad-Vadodara NH8 into six lanes from the existing four lanes. This project was different—it connected two of Gujarat's most important commercial centers through a region that was witnessing an industrial boom. The Ahmedabad-Vadodara corridor had become India's pharmaceutical and chemical manufacturing hub. Every factory needed reliable logistics. Every percentage point of Gujarat's GDP growth translated directly into traffic growth.

But the real masterstroke came in 2012. In 2012, IRB acquired Tamil Nadu based BOT road builder MVR Infrastructure and Tollways for ₹130 crore. MVR was struggling—overleveraged, operationally weak, but sitting on fantastic assets in Tamil Nadu's industrial corridor. The acquisition price was a fraction of the project cost. It was distressed asset acquisition at its finest, reminiscent of how American infrastructure funds had consolidated assets during the S&L crisis.

The MVR acquisition showcased IRB's evolution from developer to consolidator. They weren't just building new roads; they were acquiring operational assets at distressed valuations, improving operations, and creating value through financial restructuring. The playbook was simple but powerful: identify distressed assets with good underlying traffic, acquire at attractive valuations, implement operational improvements, refinance expensive debt, and generate superior returns.

The financing innovation during this period was equally impressive. IRB pioneered the use of Non-Convertible Debentures (NCDs) in infrastructure financing, tapping insurance companies and pension funds who needed long-duration assets. They structured India's first amortizing project bonds, where principal was repaid gradually rather than as a bullet payment, reducing refinancing risk. They even accessed international markets, raising $200 million through a Reg S bond issue, among the first by an Indian infrastructure company.

By 2013, IRB was operating what was effectively a toll road network across Western and Southern India. Among its notable projects are the Mumbai-Pune Expressway and the Ahmedabad-Vadodara Expressway. The network effects were powerful. Truck operators preferred IRB roads because they knew the quality would be consistent. IRB could negotiate better terms with toll equipment suppliers due to scale. They could move maintenance crews between projects. Operating leverage was kicking in.

The organizational transformation was equally dramatic. IRB had created specialized teams—a central traffic monitoring cell that tracked vehicle movements across all projects in real-time, a financial structuring team that could model complex project finances, a government relations unit that managed relationships with multiple state governments and NHAI. The family business had become a professional infrastructure institution.

But growth brought challenges. In 2013, the Comptroller and Auditor General (CAG) questioned several BOT awards, including some to IRB. Environmental activists filed PILs against toll collection. The new Land Acquisition Act made new projects more expensive and complex. Most concerningly, traffic growth was slowing as India's GDP growth decelerated from 9% to 5%.

IRB's response was strategic retrenchment. They stopped bidding for marginal projects, focusing only on high-traffic corridors. They accelerated operational improvements, implementing FASTag electronic tolling ahead of government mandates. They refinanced high-cost debt, taking advantage of falling interest rates. Most importantly, they started thinking about the next evolution—how to monetize operational assets to fund new growth.

The period from 2008 to 2015 had seen IRB transform from an emerging infrastructure developer into India's largest private toll road operator. They had built and acquired over 10,000 lane kilometers of highways. They had created a portfolio generating over ₹1,000 crores in annual toll revenues. They had survived a global financial crisis, navigated Indian political volatility, and emerged stronger.

But Virendra knew that the next phase would require another transformation. The BOT model was becoming less attractive as the government shifted to different frameworks. Capital was becoming more expensive as interest rates rose. Most importantly, IRB's balance sheet was stretched—they had assets worth thousands of crores but needed fresh capital for growth. The solution would come from an innovation that would again transform Indian infrastructure financing—the Infrastructure Investment Trust (InvIT). But first, IRB would have to navigate through a period of intense scrutiny that would test not just their business model, but their reputation and resilience.

VII. Awards, Recognition & Controversies (2010–2018)

December 11, 2010. The Taj Lands End ballroom in Mumbai was packed with India's business elite. Virendra D. Mhaiskar, chairman and managing director of IRB, was conferred with the "Young Turk of the Year" award at the 6th Edition of CNBC TV 18 India Business Leader Awards on 11 December 2010. As he walked to the podium to accept the award, the applause was thunderous. Here was a first-generation entrepreneur who had built India's largest private toll road operator from scratch. The citation spoke of vision, execution excellence, and transforming Indian infrastructure.

But even as Virendra accepted the award, a shadow was lengthening over IRB. Satish Shetty (21 July 1970 – 13 January 2010), popularly known as "Satish", was an Indian social activist, noted for exposing many land scams in Maharashtra. He was killed on 13 January 2010, by unknown attackers in Talegaon. In recent years, Shetty had used the RTI Act to expose large scale land scams involving the leading real estate firm IRB Infrastructure and its subsidiary Aryan. In 2009, he filed a complaint that forged documents had been used by these firms to acquire large swathes of land in the Taje and Pimploli villages off the Pune-Mumbai highway.

The murder had sent shockwaves through Maharashtra's activist community. Shetty wasn't just another RTI activist—he was systematic, methodical, and fearless. His investigations had led to 90 sale deeds being cancelled, and sub-registrar Ashwini Kshirsagar was suspended. The land in question was prime real estate along the Mumbai-Pune Expressway, worth hundreds of crores. The company blamed land brokers for the irregularities, and the planned IRB township project was eventually scrapped.

Eventually the case was transferred to the CBI. In October 2012, CBI raided the offices of IRB Infrastructure and that of IRB advocate Ajit Kulkarni. The raids were dramatic—CBI officers arriving at IRB's Mumbai headquarters, sealing offices, seizing documents. The stock market reacted violently. In January 2013, CBI obtained permission to conduct polygraph tests on Mhaiskar, his attorney Kulkarni, and eight others, leading to a 15% drop in the company's share price.

For Virendra, this was the darkest period of his professional life. The man who had built highways across India was now being investigated for possible involvement in murder. Board meetings became tense affairs. Independent directors asked uncomfortable questions. Banks that had lent thousands of crores wondered about reputational risk. International investors pulled back. Employee morale plummeted as media coverage intensified.

The investigation dragged on for years. Stocks regained 3% after it was said that the polygraph tests of Mhaiskar may not have revealed any incriminating aspects. But the damage to reputation was severe. Every article about IRB mentioned the investigation. Every analyst report had a risk disclosure about "ongoing legal matters." Competitors whispered about IRB's troubles in government corridors.

In April 2018, Virendra Mhaiskar, the chairman and managing director of IRB Infrastructure, and all other officials got a clean chit from CBI with regards to any sort of involvement in the murder of RTI activist Satish Shetty. They were summoned in May 2012 by the CBI, suspecting a connection with the case. During the investigation, CBI had asked Virendra Mhaiskar and other suspects to undergo a polygraph test. Mhaiskar along with the company officials had to undergo the polygraph test.

The clean chit was vindication, but the scars remained. The investigation had cost IRB not just in legal fees and lost opportunities, but in something more valuable—reputation. The company that had pioneered BOT in India, that had built the Mumbai-Pune Expressway, was now forever linked in public memory with controversy.

But the period wasn't all darkness. IRB continued winning awards for its operational excellence. The company also won the CNBC TV 18 Essar Steel Infrastructure Excellence Award in the Highways & Flyovers category for Mumbai-Pune section of NH-4 in 2009. IRB Infrastructure Ltd won the Construction Times 2017 Award under the Best Executed Highway Project of the Year category for building the Ahmedabad–Vadodara Expressway Project.

The controversy taught IRB important lessons about operating in India's complex political economy. They strengthened compliance systems, creating multiple layers of verification for land acquisition. They increased transparency, publishing detailed project reports and financial statements beyond regulatory requirements. They engaged more actively with civil society, creating forums for public feedback on projects.

More importantly, the experience hardened IRB's resolve to professionalize further. They hired senior executives from multinational corporations. They implemented global best practices in governance. They created a whistleblower mechanism and ethics hotline. The family business that had started in 1990 was transforming into an institution.

The period also saw IRB navigate the challenging transition in government policy. The UPA government, facing criticism over corruption in infrastructure awards, had virtually stopped new BOT projects. The model that IRB had pioneered was under attack. Existing projects faced aggressive toll rate negotiations. New projects required higher equity commitment. The golden age of BOT was ending.

But Virendra saw opportunity in crisis. While others retreated, IRB used this period to consolidate. They improved operational efficiency, reducing toll leakage from 5% to less than 1%. They renegotiated debt, taking advantage of falling interest rates. They settled old disputes, cleaning up the balance sheet. Most importantly, they started thinking about the next evolution—how to unlock value from operational assets.

The answer would come from financial innovation—the Infrastructure Investment Trust (InvIT), a structure that would allow IRB to monetize operational roads while retaining management control. It would be India's first InvIT, another pioneering move from a company that had made a habit of being first. But implementing it would require navigating skeptical regulators, educating confused investors, and most importantly, proving that IRB had emerged from controversy stronger and more transparent than before.

VIII. Financial Engineering: InvIT Creation & Asset Monetization

May 2017. The conference room at SEBI's Mumbai headquarters was tense. Around the table sat India's top infrastructure financiers, investment bankers, and Virendra Mhaiskar. They were finalizing the structure for something that had never been done before in India—a publicly listed Infrastructure Investment Trust. IRB InvIT is India's first Infrastructure Investment trust sponsored by IRB Infrastructure Developers Ltd.

The concept was simple but revolutionary. IRB would transfer operational toll roads worth thousands of crores into a trust structure. The trust would issue units to investors, who would receive regular distributions from toll collections. IRB would continue managing the roads, earning fees, while recycling capital for new projects. It was financial engineering at its finest—turning illiquid infrastructure assets into tradable securities.

But the execution was fiendishly complex. Indian regulations for InvITs had been notified in 2014, but nobody had actually done one. The tax structure was unclear. Investor appetite was unknown. Valuation methodologies were disputed. Every decision was precedent-setting. Should the trust own roads directly or through SPVs? How should toll revenue risk be allocated? What governance structure would protect minority unitholders?

Virendra's vision went beyond just raising capital. He saw InvITs as the solution to India's infrastructure financing challenge. Banks had asset-liability mismatches—they borrowed short-term but infrastructure needed long-term funding. Insurance companies and pension funds needed long-duration assets but couldn't directly own and operate roads. InvITs could bridge this gap, channeling patient capital into operating infrastructure while providing liquidity through market trading.

The structure they created was elegant. Its 22 projects are held under three entities; it owns seven projects, which include 1 TOT, 2 BOT and 4 HAM projects, a private infrastructure investment trust owned 10 BOT projects, of which the Company owns a 51% stake, and a public infrastructure investment trust owns five BOT projects, of which IRB owns 16% stake. This multi-tiered structure allowed IRB to optimize for different investor preferences—some wanted stable yields, others wanted growth, and yet others wanted control.

The roadshow for India's first InvIT IPO was fascinating. Traditional equity investors didn't understand it—was it debt or equity? Fixed income investors were confused—how could infrastructure assets trade on exchanges? International investors compared it to REITs, but roads weren't real estate. Retail investors, attracted by promised yields of 12%, didn't understand the risks.

The education process was exhaustive. IRB created detailed models showing how toll revenues translated into distributions. They explained the difference between return of capital and return on capital. They demonstrated how traffic growth would drive unit price appreciation beyond just distributions. Slowly, understanding dawned. Insurance companies saw it as an alternative to corporate bonds. Mutual funds saw it as a new asset class. Foreign funds saw it as a play on India's infrastructure story.

The IPO in May 2017 raised ₹4,300 crores, making it one of the largest infrastructure fundraisings in India. The units listed at a premium, validating the model. But more importantly, it created a template that others would follow. Within two years, India would have multiple listed InvITs, creating a new asset class worth tens of thousands of crores.

But IRB's innovation didn't stop at the public InvIT. They recognized that different assets required different structures. Mature, stable toll roads with predictable cash flows were perfect for public InvITs seeking yield. But newer projects, or those with higher growth potential, needed patient capital willing to accept J-curve returns. This led to the creation of the private InvIT.

The private InvIT was even more sophisticated. IRB partnered with international infrastructure funds like GIC (Singapore's sovereign wealth fund) and Cintra (the Spanish infrastructure giant). MMK is jointly owned by the Sponsor (51%); GIC (25%) and Cintra (24%). These sophisticated investors understood infrastructure, accepted development risk, and brought global best practices.

The partnership structure was carefully calibrated. IRB retained 51% to maintain control and alignment. GIC brought patient capital and international credibility. Cintra brought operational expertise from managing toll roads globally. Together, they created a platform that could bid for large projects, something IRB alone couldn't do given balance sheet constraints.

The financial impact was transformative. Through the public and private InvITs, IRB monetized assets worth over ₹15,000 crores while retaining management control. The capital recycled allowed them to bid for new projects without stretching the balance sheet. The fee income from managing InvIT assets provided steady revenue regardless of construction cycles. Most importantly, it demonstrated IRB's evolution from a builder to an asset manager.

The operational complexity of managing assets across multiple structures was immense. Each InvIT had independent trustees, separate boards, and distinct investor bases. Conflicts of interest had to be managed carefully—when allocating new projects between structures, pricing inter-company transactions, or deciding capital allocation. IRB created Chinese walls, independent committees, and detailed policies to manage these conflicts.

The success of the InvIT model validated Virendra's vision of infrastructure as an asset class. Toll roads weren't just public goods or construction projects—they were financial assets that could be structured, traded, and optimized like any other security. This financialization of infrastructure was controversial. Critics argued it prioritized returns over public service. Supporters countered that it brought efficiency and capital that government alone couldn't provide.

By 2018, IRB had created something unique globally—a fully integrated infrastructure platform spanning development, construction, operation, and asset management. They could originate projects, build them efficiently, operate them professionally, and monetize them optimally. Each part of the value chain reinforced the others. Construction capabilities helped win BOT bids. Operational excellence attracted InvIT investors. InvIT capital enabled new project development.

But the world was changing again. The government, wary of the BOT model's complexity, was shifting to a new framework—the Hybrid Annuity Model (HAM). Unlike BOT where private players took traffic risk, HAM provided government payments for availability. It was lower risk but also lower return. IRB would need to adapt once again, leveraging their InvIT platform to play in this new paradigm while maintaining returns. The financial engineering that had created InvITs would need to evolve for a new era of Indian infrastructure.

IX. Modern Era: HAM Projects & Diversification (2018–Present)

March 2018. The Ministry of Road Transport and Highways conference room in New Delhi was buzzing with uncertainty. The BOT model that had defined Indian highway development for two decades was effectively dead. Traffic projections had proven optimistic. Land acquisition had become a nightmare after the 2013 Act. Banks were nursing NPAs from aggressive infrastructure lending. The government's solution was radical: the Hybrid Annuity Model (HAM).

In March 2018, IRB Infrastructure won two hybrid annuity projects under NHDP phase IV in the state of Tamil Nadu at a cost of ₹2,169 crore. The construction period is 730 days and the operation period is 15 years. This wasn't the high-return BOT model IRB had pioneered. Under HAM, the government paid for land acquisition and 40% of project cost during construction. The concessionaire invested the remaining 60%, receiving fixed semi-annual payments over the operations period. No traffic risk, but also no upside from traffic growth.

For Virendra, HAM represented both a challenge and an opportunity. The returns were lower—12-14% versus 16-18% for BOT projects. The growth potential was capped. But HAM projects had one crucial advantage: predictability. In a world where investors had become risk-averse after infrastructure NPAs, predictable returns were valuable. IRB's strategy was sophisticated—use HAM projects to provide stable base returns while BOT assets in the InvITs captured growth.

But the real transformation came in December 2021. Adani Enterprises and IRB Infrastructure win the expressway's construction work for the Ganga Expressway, Uttar Pradesh's most ambitious infrastructure project. The expressway spans a design length of 129.7 km, connecting Bijoli (Meerut) to Nagla Barah (Budaun) in Uttar Pradesh. The Rs 36,230 crore greenfield expressway project is divided into four sections, with Adani Group winning the contract for three and one by IRB Infrastructure.

The Ganga Expressway wasn't just another road—it was a statement project for the new Uttar Pradesh. Traversing through 12 districts — Meerut, Hapur, Bulandshahr, Amroha, Sambhal, Badaun, Shahjahanpur, Hardoi, Unnao, Rae Bareilly, Pratapgarh and Prayagraj — the expressway would connect the eastern and western parts of the state. This expressway reduces travel time between Delhi and Prayagraj by half from 10-11 hours to just 6-7 hours.

IRB's approach to Ganga was innovative. Rather than bidding through the parent company, IRB Infrastructure Developers Limited announced updates on its Ganga Expressway Project, which will be executed through its associate, the Private InvIT (IRB Infrastructure Trust). The project, valued at over ₹20,890 million, has been managed by Meerut Budaun Expressway Limited (MBEL), a 51:49 joint venture between IRB Infrastructure and a GIC affiliate.

This structure was financial engineering at its most sophisticated. IRB Infrastructure will implement the remaining Ganga Expressway project via Private InvIT, monetising ₹874.61 crore and receiving ₹6,422 crore for project management. Under the project implementation agreement, IRB Infrastructure is set to receive approximately ₹6,422 crore (plus taxes) for managing the remaining project phases. IRB was essentially getting paid to build a road it would partially own through the InvIT structure.

The execution challenges were immense. The Ganga Expressway traversed some of Uttar Pradesh's most densely populated districts. Land acquisition, despite government support, faced resistance. The expressway had to cross multiple rivers, requiring complex bridge engineering. Environmental clearances were contentious given proximity to the Ganga. But IRB had built capabilities over two decades that made them uniquely qualified—relationships with local contractors, understanding of UP's political economy, and most importantly, credibility with the state government.

The modern era also saw IRB adapt to technological disruption. FASTag became mandatory in 2021, fundamentally changing toll collection. IRB had anticipated this, implementing electronic tolling years earlier. But they went further, using data analytics to optimize toll plaza throughput, predictive maintenance to reduce downtime, and IoT sensors to monitor road conditions in real-time. The company that had started with manual toll collection was now running some of India's most technologically advanced highways.

It manages and operates over 12000 lane kilometers (km) across 22 assets. Its 22 projects are held under three entities; it owns seven projects, which include 1 TOT, 2 BOT and 4 HAM projects, a private infrastructure investment trust owned 10 BOT projects, of which the Company owns a 51% stake, and a public infrastructure investment trust owns five BOT projects, of which IRB owns 16% stake.

This portfolio diversity was deliberate. BOT projects provided growth, HAM projects offered stability, TOT assets generated immediate cash, and InvITs enabled capital recycling. Each model had different risk-return profiles, creating a balanced portfolio that could weather economic cycles. When GDP growth slowed, HAM projects provided steady returns. When traffic boomed, BOT assets captured the upside.

The financial performance reflected this strategy. Despite challenges—COVID-19 decimating traffic in 2020, rising interest rates pressuring debt service, competitive intensity in bidding—IRB maintained steady cash flows. Toll collections recovered quickly post-pandemic as goods movement resumed. The InvIT structure provided regular distributions to investors even during volatility. The management fees from InvITs created an annuity-like revenue stream independent of construction cycles.

But challenges remained significant. Company has low interest coverage ratio. The company has delivered a poor sales growth of 2.13% over past five years. The shift from BOT to HAM had compressed returns. New competitors, backed by deep pockets, were bidding aggressively. The government's focus was shifting from highways to railways and waterways. Most concerningly, technological disruption loomed—autonomous vehicles, hyperloop proposals, and drone delivery threatened the fundamental economics of road transport.

IRB's response was strategic evolution rather than revolution. They doubled down on operational excellence, reducing costs through automation and predictive maintenance. They explored adjacencies—rest stops, logistics parks, and highway-side real estate development. They strengthened their balance sheet, reducing leverage and improving interest coverage. Most importantly, they prepared for the next wave of infrastructure development—smart cities, dedicated freight corridors, and multi-modal transport hubs.

By 2024, IRB had survived and thrived through multiple cycles—from family business to public company, from BOT pioneer to HAM adapter, from builder to asset manager. The company that had started with one bypass road now managed one of Asia's largest toll road portfolios. But the future remained uncertain. Electric vehicles were reducing fuel tax collections, potentially affecting government highway spending. Climate change was increasing construction and maintenance costs. The next generation of the Mhaiskar family was taking leadership positions, bringing fresh perspectives but also generational transition challenges. The story of IRB Infrastructure was far from over.

X. Playbook: Business & Operating Model Lessons

After twenty-five years of building, operating, and financing India's highways, IRB Infrastructure has developed a playbook that reads like a masterclass in infrastructure capitalism. It's not just about pouring concrete and collecting tolls—it's about understanding the intricate dance between government policy, financial engineering, and operational excellence.

The Art of Project Selection

IRB's first rule: not all roads are created equal. While competitors chased prestigious projects on major corridors, IRB focused on what they call "strategic complexity"—projects difficult enough to deter pure financial investors but positioned on routes with inevitable traffic growth. The Mumbai-Pune Expressway exemplified this perfectly: challenging terrain that required real engineering expertise, but connecting two economic powerhouses guaranteed traffic growth.

Their traffic modeling goes beyond simple GDP correlations. They study industrial development plans, track building permits in catchment areas, monitor fuel consumption patterns, and even analyze satellite imagery of urban sprawl. When evaluating the Ahmedabad-Vadodara corridor, they didn't just see current traffic—they saw Gujarat's pharmaceutical cluster expansion, new industrial parks, and the multiplier effect of improved connectivity.

The BOT/TOT/HAM Arbitrage

IRB has mastered what they call "model arbitrage"—using different concession structures to optimize risk-return profiles. BOT projects are for corridors where they have conviction on traffic growth exceeding projections. HAM projects provide stable base returns when government payments are certain. TOT assets offer immediate monetization opportunities when operational improvements can unlock value.

The genius lies in portfolio construction. During economic booms, BOT projects capture upside. During downturns, HAM projects provide stability. TOT acquisitions happen when distressed sellers emerge. This isn't passive diversification—it's active portfolio management based on economic cycles and government policy shifts.

Capital Recycling Through Financial Innovation

The InvIT structure wasn't just about raising capital—it was about creating a perpetual growth machine. By monetizing operational assets while retaining management control, IRB freed capital for new projects while generating fee income. The dual InvIT structure—public for stable assets, private for growth projects—allows them to tap different investor pools with different risk appetites.

The numbers are compelling: through InvITs, IRB monetized over ₹15,000 crores of assets while maintaining 51% control and earning management fees of 2-3% annually. This transforms the economics—instead of being capital-constrained, they became capital-allocators, choosing which projects to develop rather than which they could afford.

Operational Excellence as Competitive Advantage

In tolling, the difference between 95% and 99% collection efficiency translates to hundreds of crores. IRB's toll management system is a case study in operational excellence. They pioneered 24/7 CCTV monitoring of all toll plazas from a central command center. Anomaly detection algorithms flag unusual patterns—a toll collector whose shift shows lower collections than historical averages, vehicles misclassified to pay lower tolls, or peak hour throughput below capacity.

But technology is just one part. IRB discovered that toll collector recruitment from local communities reduced both attrition and leakage. Eight-hour shifts instead of twelve-hour shifts improved accuracy. Performance bonuses based on throughput, not just collection, incentivized efficiency. Small operational improvements compound—reducing average transaction time by 5 seconds across all plazas saves thousands of vehicle-hours daily.

Managing Government Relations

Perhaps IRB's most underappreciated skill is navigating India's complex political economy. They maintain relationships across party lines, understanding that infrastructure transcends political cycles. When the UPA government froze BOT projects, IRB worked with state governments. When NDA promoted HAM, they quickly adapted. They never publicly criticize policy—instead, they provide "technical inputs" through industry associations.

Their approach to land acquisition showcases this sophistication. Instead of relying solely on government acquisition, they deploy "relationship managers" months before formal processes begin, engaging with farmers, understanding concerns, and often facilitating better compensation than government rates. This proactive approach has reduced their project delays significantly compared to industry averages.

Risk Management Through Structure

Every IRB project is housed in a Special Purpose Vehicle (SPV), ring-fencing risks. But the structuring goes deeper. They negotiate step-in rights for lenders, ensuring project continuity even during financial stress. They insist on formula-based toll rate revisions, removing political discretion. They structure debt with multiple tranches—senior debt for construction, mezzanine for ramp-up, and refinancing once operations stabilize.

The 2008 financial crisis validated this approach. While competitors with aggressive structures faced distress, IRB's conservative leverage (rarely exceeding 70% debt) and diverse funding sources (banks, bonds, ECBs) ensured continuous access to capital. They've never had a project default or require restructuring—remarkable in an industry plagued by NPAs.

The Network Effect

As IRB's portfolio grew, network effects emerged. Maintenance contracts could be bundled for better pricing. Equipment could be shared across projects. Most importantly, institutional knowledge accumulated—the engineer who solved a drainage problem on one project could apply that solution across the portfolio. This operational leverage means each new project is more profitable than the last.

Technology Adoption

While not technology pioneers, IRB are fast followers. They implemented FASTag before mandates, understanding that electronic tolling wasn't just about efficiency but data. Every electronic transaction provides vehicle type, time, origin-destination patterns—invaluable for traffic forecasting and dynamic pricing. They're now experimenting with AI for predictive maintenance, using sensors to identify road deterioration before it becomes visible.

The Talent Equation

Infrastructure is ultimately a people business. IRB's management development program rotates high-performers through construction, operations, finance, and government relations. This creates leaders who understand the full value chain. They've also been early in hiring from adjacent industries—investment bankers for financial structuring, technology professionals for digital initiatives, and even consumer goods executives for customer service at toll plazas.

Future-Proofing the Model

IRB recognizes that the highway boom won't last forever. Their adjacency strategy is carefully planned—logistics parks at highway intersections, rest stops with retail opportunities, and land banks for future development. They're also exploring international opportunities, leveraging India's infrastructure expertise in emerging markets. The playbook that worked in India—navigating complex stakeholders, managing difficult construction, and structuring innovative financing—is applicable across the developing world.

This playbook wasn't developed overnight. It's the result of hundreds of projects, thousands of negotiations, and millions of vehicles passing through toll plazas. It's a playbook for building infrastructure in a complex democracy, where every stakeholder—from farmers whose land is acquired to commuters who pay tolls—has a voice. And perhaps most importantly, it's a playbook that recognizes infrastructure isn't just about building assets—it's about creating the arteries through which economic growth flows.

XI. Analysis & Bull vs. Bear Case

The investment case for IRB Infrastructure presents a fascinating paradox. Here's a company with Market Cap ₹ 27,043 Cr., operating in an essential sector with enormous growth potential, yet trading at valuations that suggest deep market skepticism. The bulls see an infrastructure play on India's growth story. The bears see a leveraged bet on government policy and traffic projections. Both are right, which makes IRB one of the most interesting and controversial infrastructure investments in India.

The Bull Case: Infrastructure Alpha in a Growing Economy

Start with the macro picture. India needs $1.4 trillion in infrastructure investment by 2025. The government can fund perhaps half. Private capital must bridge the gap, and IRB is one of the few proven platforms capable of deploying capital at scale. With manages and operates over 12000 lane kilometers (km) across 22 assets, they have the largest private road portfolio in India.

The InvIT structure has transformed IRB's economics. Instead of being capital-constrained, they're now asset managers earning fees on a growing AUM. As the largest integrated private toll roads and highways infrastructure developer in India, IRB has an asset base of approx. Rs.80,000 Crs. in 12 States across the parent company and two InvITs. The fee income alone—2-3% on ₹80,000 crores—provides ₹1,600-2,400 crores annually, a significant cushion against construction cycles.

Traffic growth remains robust despite economic headwinds. Even assuming modest 5-8% annual growth (down from historical 10-12%), the compounding effect on toll revenues is substantial. India's vehicle penetration is still just 22 per 1,000 people versus 980 in the US. As income levels rise, vehicle ownership explodes, and IRB's roads capture that growth.

The Ganga Expressway showcases IRB's continued execution capability. The project, valued at over ₹20,890 million, has been managed by Meerut Budaun Expressway Limited (MBEL), a 51:49 joint venture between IRB Infrastructure and a GIC affiliate. Having GIC as a partner validates IRB's institutional credibility and provides patient capital for large projects.

Operational leverage is finally showing. After years of heavy investment, IRB's maintenance capex is declining as a percentage of revenues. Toll collection efficiency has improved with FASTag adoption. The company is generating free cash flow after years of consumption. This inflection point, if sustained, could drive significant rerating.

The Bear Case: Structural Headwinds and Financial Stress

The numbers tell a sobering story. Company has low interest coverage ratio. The company has delivered a poor sales growth of 2.13% over past five years. This isn't just a temporary blip—it reflects structural challenges in the business model.

Leverage remains concerning. Promoter Holding: 30.4% but promoters have pledged or encumbered 55.5% of their holding. This suggests financial stress at the promoter level, potentially limiting their ability to support the company during downturns. When controlling shareholders are themselves leveraged, minority investors face additional risk.

The shift from BOT to HAM has structurally reduced returns. Where BOT projects could generate 18-20% IRRs with traffic upside, HAM projects cap returns at 12-14%. This isn't a cyclical issue—it's a permanent shift in industry economics. As the high-return BOT portfolio matures and new additions are primarily HAM, overall returns must decline.

Competition has intensified dramatically. The Adani Group's aggressive entry into roads, backed by seemingly unlimited capital, has driven down bid returns. Regional players have emerged with local political connections. International infrastructure funds are directly bidding for projects. IRB's first-mover advantage has eroded.

Traffic growth assumptions may prove optimistic. Work-from-home has reduced commuter traffic on some corridors. E-commerce consolidation means fewer small shipments and more efficient logistics. Electric vehicles, while still nascent, could reduce the fuel tax pool that funds highway development. These are secular headwinds that traffic models haven't fully captured.

Regulatory risks remain elevated. Toll rates are politically sensitive—protests against toll increases are common. The government's push for "one nation, one FASTag" could lead to revenue sharing or cross-subsidization requirements. Environmental regulations are tightening, increasing construction costs and delays.

Financial Metrics: The Numbers Don't Lie

Debtor days have improved from 48.8 to 15.9 days. This improvement in working capital is positive but happened during a period of limited new project additions. As construction activity picks up, working capital requirements will increase again.

The return on equity of 5.30% over the last three years is particularly concerning for a company in a capital-intensive business. This means IRB is generating returns below the cost of capital—destroying value rather than creating it. Unless ROE improves dramatically, the equity story doesn't work.

The company's market share of around 38% in the TOT space sounds impressive, but TOT is a small, non-growing segment. The real growth is in greenfield projects where competition is most intense and returns are compressing.

Valuation: Priced for Mediocrity

At current valuations, the market is pricing IRB as a low-growth, high-risk utility. The P/E ratio of around 4x suggests extreme skepticism about reported earnings quality or sustainability. The EV/EBITDA of 8x is below replacement cost for the asset base.

This could represent deep value or a value trap. The bull case says the market doesn't understand the InvIT transformation and operational inflection. The bear case says the market correctly perceives structural challenges and financial stress.

Risk-Reward: Asymmetric but Unclear Direction

The asymmetry is clear—limited downside given asset backing, substantial upside if the business model transformation succeeds. But the timing and catalysts are uncertain. IRB could remain "cheap" for years if traffic growth disappoints or leverage concerns persist.

For investors, IRB represents a complex bet on multiple variables: India's infrastructure spending, traffic growth patterns, government policy stability, interest rate cycles, and management execution. It's not a simple growth story or value play—it's a sophisticated infrastructure platform with both tremendous potential and significant risks.

The most likely scenario is neither dramatic success nor failure, but a gradual transformation into a lower-return, stable infrastructure yield play. For investors seeking 20% IRRs, IRB will disappoint. For those accepting 12-15% returns with infrastructure exposure, it could deliver. The question is whether current valuations adequately reflect this reality. The market's extreme skepticism suggests opportunity, but the fundamental challenges suggest caution. In infrastructure investing, as on the highways IRB builds, the journey matters as much as the destination.

XII. Epilogue & Looking Forward

As morning traffic builds on the Mumbai-Pune Expressway, Virendra Mhaiskar stands in IRB's command center, watching real-time feeds from hundreds of toll plazas across India. Each blinking light represents a vehicle, a transaction, a tiny contribution to the rivers of cash flow that sustain this infrastructure empire. At 54, he has spent thirty-five years transforming a family construction business into India's largest private toll road operator. The question now isn't what has been built, but what comes next.

The infrastructure landscape of 2025 bears little resemblance to the India of 1998 when IRB was incorporated. The National Infrastructure Pipeline envisions ₹111 lakh crores of investment by 2025. The government speaks of "Gati Shakti"—integrated infrastructure planning connecting roads, railways, ports, and airports. The ambition is staggering, but so are the challenges.

Electric vehicles represent both threat and opportunity. As EVs proliferate, fuel tax collections—which fund highway development—will decline. Governments globally are experimenting with alternatives: distance-based tolling, congestion pricing, carbon taxes. IRB is positioning for this transition, investing in charging infrastructure at rest stops and exploring dynamic pricing models that could optimize traffic flow and revenue.

The technology disruption goes deeper. Autonomous vehicles, still a decade away from mass adoption in India, could fundamentally alter highway economics. If vehicles can travel closer together at higher speeds safely, road capacity effectively increases without new construction. If trucks can operate 24/7 without driver rest requirements, traffic patterns shift dramatically. IRB is partnering with technology companies to understand these implications, preparing for a future where roads are as much about data as concrete.

Climate change poses existential questions. Extreme weather events are increasing—floods that wash away roads, heat waves that buckle concrete, unseasonal rains that delay construction. IRB's engineering standards, developed for historical weather patterns, need updating for climate resilience. The cost is substantial, but the cost of not adapting is catastrophic.

The competitive landscape continues evolving. The Adani Group's infrastructure ambitions seem unlimited. International pension funds are directly acquiring road assets globally. Chinese construction giants are eyeing international BOT opportunities. IRB's response is selective internationalization—leveraging Indian expertise in complex stakeholder management for similar markets in Southeast Asia and Africa.

Governance and succession present delicate challenges. The Mhaiskar family's entrepreneurial drive built IRB, but institutional investors demand professional management. The next generation brings global education and fresh perspectives but must prove themselves beyond the family name. The transition from founder-led to institutionally-governed is never smooth, particularly in infrastructure where relationships matter as much as capital.

The financial architecture continues evolving. REITs have proven successful in real estate; InvITs are establishing themselves in infrastructure. The next innovation might be tokenization—fractional ownership of infrastructure through blockchain, enabling retail investors to own pieces of highways. IRB is exploring these frontiers, understanding that financial innovation has always been central to their success.

Recent developments suggest momentum. Witnessed aggregate toll collection growth of 32% Y-o-Y for the quarter under review in the assets under IRB Infra portfolio and the assets under IRB Infrastructure Trust. The toll collection for Q1FY25 was Rs.1,556 Crs as against Rs.1,183 Crs in the corresponding quarter of FY24. This growth, while partly recovery from COVID impacts, indicates underlying strength in traffic patterns.

But the India growth story that underpinned IRB's rise faces headwinds. GDP growth is moderating, fiscal deficits are concerning, and global economic uncertainty is rising. Infrastructure spending, historically the first casualty of fiscal consolidation, could slow. IRB's strategy assumes continued government commitment to infrastructure—a reasonable but not guaranteed assumption.

The social license to operate is increasingly important. Toll roads in India face regular protests against rate increases. Environmental activists challenge new projects. Land acquisition remains contentious despite regulatory changes. IRB's response has been proactive stakeholder engagement, but managing diverse interests while maintaining returns is increasingly difficult.

Looking forward, IRB faces three scenarios. The optimistic case sees India's infrastructure boom continuing, traffic growing steadily, and IRB's platform capturing disproportionate value. The pessimistic case sees government spending curtailed, traffic growth stalling, and returns compressing below capital costs. The realistic case—most likely—sees moderate growth, continued competition, and gradual transformation into a yield-focused infrastructure utility.

The Company has strong track record of constructing, tolling, operating, and maintaining around 18,500 lane Kms pan India in its existence of more than 25 years in India; of which 15,500 Lane Kms are under operations at present. This operational footprint provides resilience, but past performance doesn't guarantee future success. The highway sector that created IRB is maturing. The next growth phase requires different capabilities—technology integration, sustainability focus, and international expansion.

For investors, IRB represents a bet on India's infrastructure transformation. It's not a simple bet—success requires navigating government policy, economic cycles, technological disruption, and climate change. But infrastructure remains the backbone of economic development. Countries that build world-class infrastructure prosper; those that don't stagnate. India's ambitions require private capital and execution capability. IRB, despite challenges, remains one of the few proven platforms.

As traffic peaks on the Mumbai-Pune Expressway, toll revenues for the morning rush hour exceed ₹50 lakhs. Each vehicle represents a choice—to pay for speed, safety, and reliability. That millions make this choice daily validates the BOT model IRB pioneered. The roads they built don't just connect cities; they enable commerce, facilitate development, and embody India's infrastructure ambitions.

The story of IRB Infrastructure is far from over. From a family construction business to India's toll road giant, from BOT pioneer to InvIT innovator, they've consistently evolved. The next chapter—whether triumph or challenge—will be written on the highways of India and beyond. For a company that has spent twenty-five years building the arteries of economic growth, the road ahead remains long, complex, but full of possibility.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube