Solara Active Pharma Sciences: The Pure-Play API Story

I. Introduction & Episode Roadmap

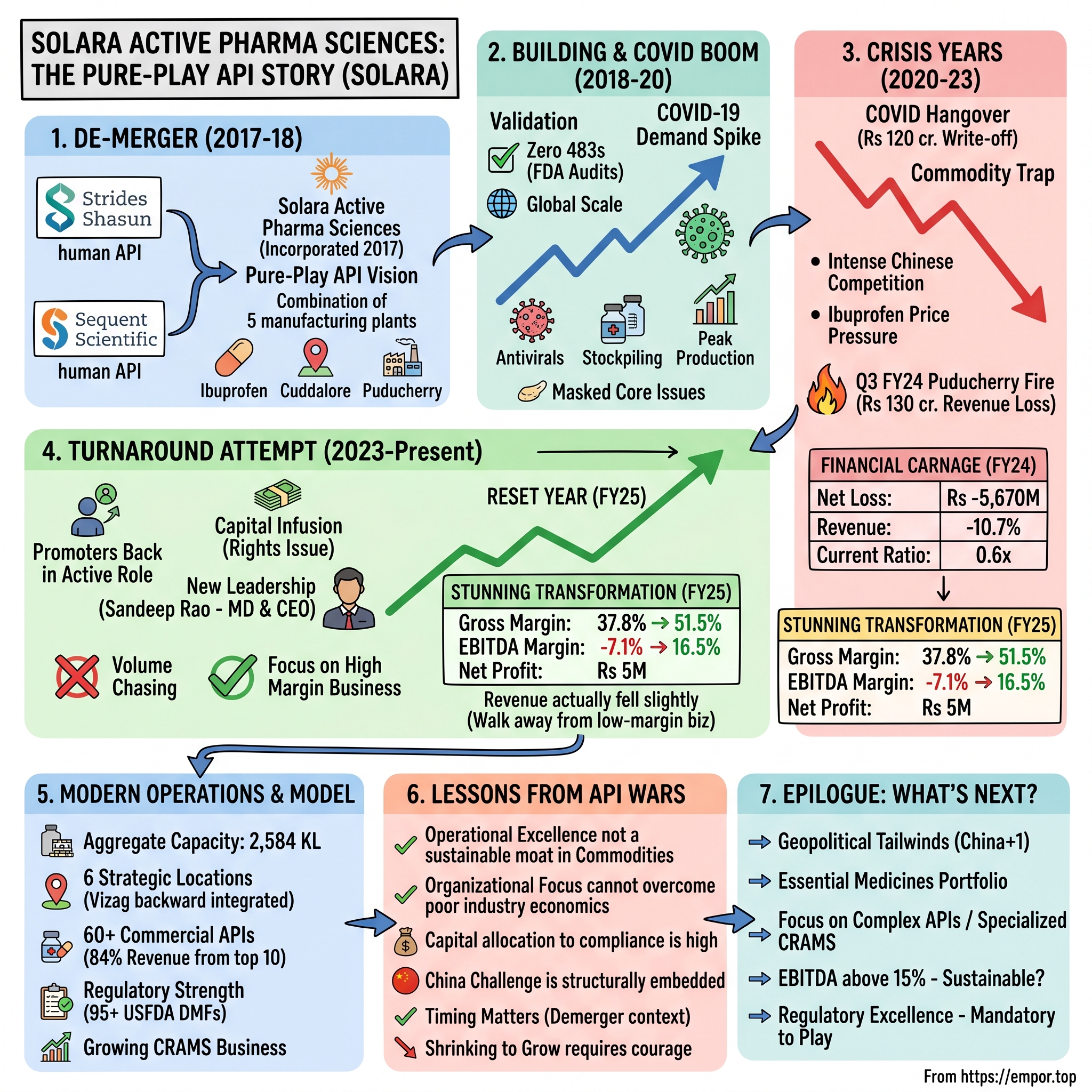

The monsoon rains lashed against the windows of the boardroom in Chennai on a humid evening in September 2023. Inside, the atmosphere was even more turbulent. The family and the promoters had just announced taking an active role in Solara approximately 6 months ago, focused on resetting the company for profitable growth. The numbers on the screen told a brutal story: For the year ended March 2024, SOLARA ACTIVE PHARMA SCIENCES reported 2448.1% decrease in net profit to Rs -5,670 million compared to net loss of Rs 223 million during FY23. Revenue fell 10.7% to Rs 12,889 million during FY24.

This wasn't supposed to be how the story unfolded. With three decades in pure-play API manufacturing, Solara Active Pharma has been guided by a pursuit to improve patients' lives. Yet here was a company that embodied one of Indian pharma's most fascinating paradoxes: technically only seven years old as a legal entity, founded in 2017, but inheriting the accumulated wisdom and wounds of two major pharmaceutical players – Strides Shasun and Sequent Scientific.

The question facing everyone in that boardroom was stark: How had a company born from the strategic vision of separating commodity APIs into a focused pure-play entity ended up bleeding red ink? More importantly, could it be saved?

This is not just a story about APIs – those essential but unglamorous building blocks that make modern medicine possible. It's a tale of corporate surgery gone awry, of COVID windfalls turned millstones, and ultimately, of whether there's any sustainable moat in the commodity pharmaceutical ingredients business. It's about the brutal economics of competing with China while maintaining Western quality standards, and the perpetual tightrope walk between compliance costs and razor-thin margins.

As we'll discover, Solara's journey from demerger to crisis to attempted turnaround offers profound lessons about the perils of commodity businesses, the importance of timing in corporate restructuring, and why sometimes being "pure-play" isn't enough when you're playing in pure commodities.

II. Origins: The Strides-Sequent Heritage

The story begins not in 2017, but decades earlier in the bustling pharmaceutical corridors of India's generic drug revolution. Solara has a legacy of over three decades and traces its origins to the API expertise of Strides Shasun Ltd. and the technical knowhow of human API business from Sequent Scientific Ltd. These weren't just any pharma companies – they were pioneers in India's march toward becoming the world's pharmacy.

Strides, founded by the entrepreneurial Arun Kumar in 1990, had built its reputation on complex generics and regulated market formulations. The company had grown through a series of audacious acquisitions and had developed significant API capabilities along the way. By the mid-2010s, Strides had assembled an impressive portfolio of manufacturing facilities, including plants in Puducherry and Cuddalore that would later become crown jewels in Solara's asset base.

The Puducherry facility, in particular, had a distinguished history. The Puducherry API manufacturing facility is the centre of excellence for the manufacturing of Ibuprofen and its derivative APIs. The facility was established in the year 1986 and is one of the largest Ibuprofen manufacturing sites in the world. This wasn't just any API facility – it was a global-scale operation producing one of the world's most widely used pain relievers.

Meanwhile, Sequent Scientific had carved out its own niche, initially focusing on veterinary APIs before expanding into human pharmaceuticals. The company had built three strategically located manufacturing facilities in Mangalore, Mahad (referred to as Ambernath in some documents), and Mysore, each with specific technical capabilities that complemented the broader portfolio.

But by 2016, both companies faced a strategic crossroads. The global API business was becoming increasingly commoditized. Chinese manufacturers were flooding the market with low-cost alternatives, putting immense pressure on margins. At the same time, regulatory compliance costs were escalating as the US FDA and European regulators tightened their oversight of foreign manufacturing facilities.

Arun Kumar, the executive vice-chairman and managing director said: with the commodity API business continuing to put pressure on margins with cost of compliance going up, it was better to hive off the low margin API's of drugs such as Ibuprofen, Gabapentin and Ranitidine while at the same time retaining API's for complex generics and other API's used in house. This wasn't a spur-of-the-moment decision – it was a calculated strategic move born from the recognition that commodity APIs and complex formulations required fundamentally different business models.

The Indian pharma landscape of the 2010s was undergoing a profound transformation. Companies were being forced to choose: either go deep into commodities with massive scale, or move up the value chain into complex molecules and finished formulations. Strides and Sequent chose the latter, but that meant finding a new home for their commodity API operations.

The logic was compelling on paper. There is a tremendous opportunity for the API players to bring value to the formulators but they find it risky to partner with companies that also have an interest in the finished dosage business. Therefore, with this demerger they will be able to capture the said market. A pure-play API company wouldn't compete with its customers in the formulations market – a critical concern for many global pharma companies looking for reliable API suppliers.

Thus, the stage was set for one of Indian pharma's most ambitious corporate restructurings. The plan was elegant: combine the API assets of both companies into a new entity that would have the scale, the regulatory approvals, and the focused management attention to compete globally. What could go wrong?

III. The Great Demerger: Creating Solara (2017-2018)

The transaction was approved by the board of directors of Sequent Scientific at a meeting held on March 20, 2017. What followed was a masterclass in complex corporate restructuring – or so it seemed at the time. The scheme wasn't just a simple spin-off; it was a carefully orchestrated three-way dance involving two listed companies and the creation of an entirely new entity.

Solara Active Pharma Sciences Limited was incorporated on February 23, 2017 to undertake business in manufacturing, production, processing, formulating, sale, import, export, merchandising, distributing, trading of and dealing in active pharmaceutical ingredients (APIs). The new company was born with high ambitions and what appeared to be substantial assets.

The mechanics of the demerger were intricate. The Scheme provided for the demerger of the commodity API business of Strides and the human API business of Sequent and transfer of the same to our Company pursuant to the provisions of Sections 230 to 232 of the Companies Act, 2013. The appointed date for the Scheme is October 1, 2017.

The valuation exercise revealed the relative worth of each contribution: As per the valuation carried out, value of Stride's – Commodity API business is Rs 859 crore (60.9%) and Sequent- Human API business is at Rs 552.50 crore (39.1%) which will merger into Solara. These weren't trivial assets – together they represented over Rs 1,400 crore in value, creating what would be one of India's largest pure-play API companies from day one.

The share swap ratios reflected these valuations: For every six shares held in Strides, one share of Solara will be allocated. And for every twenty five shares of Sequent, one share of Solara will be allocated. These ratios would determine the ownership structure of the new entity, with promoters and public shareholders of both parent companies becoming stakeholders in Solara.

The Hon'ble National Company Law Tribunal sanctioned the Scheme, Mumbai Bench by an order dated March 9, 2018 and issued on March 22, 2018. Strides, SeQuent and the Company made the Scheme effective on March 31, 2018 (Effective Date). After months of regulatory approvals, legal documentation, and shareholder meetings, the deed was done.

The assets Solara inherited were substantial. From Strides came two major manufacturing facilities: Solara will be owning Strides commodity (B2B) API business along with 2 manufacturing plants in Pondicherry and Cuddalore. From Sequent came Human API business (B2C) along with 3 manufacturing plants in Mangalore, Mahad and Mysore. Together, The all new API business will be having five manufacturing plants with three of them USFDA approved.

The regulatory pedigree was impressive. This site is inspected by various Regulatory Authorities including USFDA, MHRA, EDQM, WHO, PMDA, TGA, KFDA, and COFEPRIS. These weren't just manufacturing sheds – they were globally certified facilities capable of supplying APIs to the most regulated markets in the world.

Securities and Exchange Board of India (SEBI) vide letter dated June 20, 2018 has granted relaxation from the applicability of Rule 19(2)(b) of the Securities Contracts (Regulation) Rules, 1957. The Company has also received final listing/trading approval from both the BSE Limited ("BSE") and the National Stock Exchange of India Limited ("NSE") on June 25, 2018 and the equity shares of Solara commenced trading in BSE and NSE on June 27, 2018.

The market's initial reaction was cautiously optimistic. Solara, after an EBIDTA of Rs. 176 cr. is likely to earn a PAT of around Rs. 90 cr. Analysts projected the new entity would trade at reasonable valuations, with some estimating a market cap of around Rs 1,300 crore.

But beneath the surface, challenges were already emerging. The portfolio Solara inherited was heavily weighted toward commodity molecules with intense price competition. The integration of facilities from two different companies, each with their own cultures and operating procedures, would prove more complex than anticipated. And most critically, the global API market was about to undergo seismic shifts that no one in those boardrooms fully anticipated.

IV. Building the Pure-Play Vision (2018-2020)

The early days of independence brought remarkable validation. In an industry where US FDA inspections could make or break a company's reputation, Solara delivered a stunning performance. The USFDA inspection at the facility was scheduled and completed between July 1, 2019 and July 5, 2019. This is company's third consecutive US FDA audit with Zero 483s.

This wasn't just good news – it was exceptional. In the pharmaceutical world, receiving zero observations (known as 483s) from the FDA is like a perfect score on the most difficult exam imaginable. The agency's inspectors are notorious for finding issues, however minor. To achieve this not once, but multiple times in succession, suggested Solara had inherited world-class quality systems.

The momentum continued. The company's R&D centers in Chennai and Bengaluru were humming with activity. Apart from this, the Solara Active has two research and development units - in Bengaluru and Chennai - equipped with state-of-the-art facilities and a pipeline of 25+ products, at different stages of development. The pipeline focused on anthelmintic, anti-malarias, beta blockers, muscle relaxants, novel oral anticoagulants, anti-infective and other niche segments.

February 2020 brought more regulatory triumphs. The inspection established that the two sites are in an "Acceptable State of Compliance" with Zero Form 483 inspectional observations from USFDA. The agency with their designated auditors inspected the two facilities from 17th to 21st February 2020. These inspection outcomes are Solara's fourth consecutive US FDA audit with "Zero 483s".

The portfolio was taking shape with clear therapeutic focus areas. The company offers products and services, such as Anaesthetic, Analgesics, Antiviral, Retinod, Anti-emetic, Antimalarial, Diuretic, Muscle relaxant, Antiallergics, Antihypertensive, Calcimimetic agent, Anti-seizure, Antigout, Cardiovascular, Anti-infective, Cough suppressant and others. The crown jewel remained Ibuprofen, where Solara's Puducherry facility gave it genuine global scale.

The pure-play positioning was starting to resonate with customers. Global pharma companies, particularly those in the generic formulations space, appreciated having an API supplier that wouldn't compete with them downstream. The company was building relationships across 75+ countries, leveraging the established customer base inherited from its parent companies.

Then came COVID-19, and suddenly the world couldn't get enough APIs. Supply chains from China were disrupted. Governments were stockpiling essential medicines. Demand for antivirals, anti-infectives, and even basic pain management APIs skyrocketed. For a brief, shining moment, it seemed like Solara's timing couldn't have been better.

The company ramped up production to meet the unprecedented demand. Under voluntary licenses from innovators, Solara began manufacturing COVID-related APIs that would normally have been off-limits. We were sitting on approximately INR 120-odd crores of COVID inventory that was allowed for us to be manufactured under voluntary licenses from the innovators only during the COVID period.

The numbers looked fantastic. Orders were pouring in. The manufacturing facilities were running at peak capacity. Management spoke confidently about the company's role in supporting global healthcare during the pandemic. Industry observers praised Solara's operational excellence in maintaining production despite lockdowns and logistics challenges.

But this COVID boom contained the seeds of future crisis. The inventory being built up – those Rs 120 crores worth of COVID-related APIs – was manufactured under temporary emergency licenses. Once the pandemic emergency ended, this inventory couldn't be sold. It would become a massive millstone around Solara's neck.

Meanwhile, structural challenges in the base business were being masked by COVID demand. The core portfolio of commodity APIs – Ibuprofen, Gabapentin, Ranitidine – remained under intense pricing pressure from Chinese competitors. The company's EBITDA margins, while positive during the COVID surge, were built on temporary foundations.

By late 2020, as vaccines began rolling out and COVID treatments evolved, the writing was on the wall. The pandemic boom was ending, but Solara's warehouses were full of inventory that would soon become worthless. The pure-play vision, so compelling in theory, was about to face its harshest test in practice.

V. Crisis Years: Regulatory Challenges & COVID Hangover (2020-2023)

The unwinding began slowly, then all at once. As 2021 progressed, the extraordinary demand that had sustained Solara through the pandemic began to evaporate. Governments stopped stockpiling. Hospital systems normalized their inventory levels. The voluntary licenses that had allowed Solara to manufacture COVID-related APIs expired, leaving the company with mountains of unsaleable inventory.

The numbers began their downward spiral. The company has delivered a poor sales growth of -0.58% over past five years. This wasn't just a bad quarter or two – this was a sustained deterioration in the fundamental business. The COVID inventory that had once seemed like a strategic asset became a Rs 120 crore write-off waiting to happen.

But inventory was just the beginning of Solara's troubles. The base business, stripped of COVID-related demand, revealed deeper structural issues. The commodity API market had become even more brutally competitive. Chinese manufacturers, recovering from their own COVID disruptions, returned with a vengeance, flooding global markets with APIs priced at levels that made profitability nearly impossible for Indian manufacturers.

The Ibuprofen business, once Solara's crown jewel, became particularly problematic. The miss on the Revenue and EBITDA guidance is attributable to intense competition on the Ibuprofen range of products. Despite operating one of the world's largest Ibuprofen manufacturing facilities, Solara couldn't compete on price with Chinese producers who benefited from lower input costs, government subsidies, and less stringent environmental regulations.

Then came operational disasters. In Q3 FY24, a fire at the Puducherry facility delivered another blow. The firm stated that the third quarter was impacted by a fire at the company's Puducherry facility and a temporary deferment of sales which led to the loss of revenue of ₹130 crore. For a company already struggling with profitability, losing Rs 130 crore in revenue was devastating.

The financial statements told a story of accelerating decline. The losses mounted quarter after quarter, culminating in the shocking FY24 results. A net loss of Rs 5,670 million – a number so large it defied comprehension for a company of Solara's size. Net profit margins during the year declined from 1.5% in FY23 to 44.0% in FY24 – though calling them "profit margins" when the company was bleeding money seemed almost sardonic.

Working capital management became a crisis. The company's current ratio deteriorated and stood at 0.6x during FY24, from 1.1x during FY23. Suppliers wanted faster payments while customers, knowing Solara's distress, pushed for extended terms. The company was caught in a classic cash squeeze.

The interest coverage ratio painted an even grimmer picture. The company's interest coverage ratio deteriorated and stood at -3.6x during FY24, from 0.5x during FY23. Solara wasn't just unable to cover its interest payments from operating earnings – its operating losses were multiples of its interest obligations.

Return metrics became almost meaningless. The ROE for the company declined and down at -60.8% during FY24, from -1.5% during FY24. The company was destroying shareholder value at an alarming rate. Every rupee of equity was generating massive losses rather than returns.

Yet amidst this financial carnage, there were bright spots that made the situation even more perplexing. The company's quality and compliance standards remained exceptional. In August 2023, another FDA inspection yielded perfect results. The Agency, with its designated investigators, inspected the Cuddalore facility between July 31, 2023 - August 04, 2023. The inspection established that the facility is in an "Acceptable State of Compliance" with Zero Form 483 inspectional observations from the Agency. With this successful inspection outcome, the current inspection classification of Cuddalore site shall be reinstated to NAI (No Action Indicated).

This paradox defined Solara's crisis: operationally excellent, commercially disastrous. The company could meet the most stringent quality standards in the world, but it couldn't make money. It had world-class facilities and regulatory approvals, but it was competing in commodity markets where those advantages meant little against lower-cost producers.

By late 2023, something had to give. The company's market capitalization had collapsed. Debt levels were becoming unsustainable. The board faced a stark choice: radical restructuring or potential insolvency. It was at this critical juncture that the founding family decided to step back in, betting their reputation and capital on a turnaround that many thought impossible.

VI. The Turnaround Attempt (2023-Present)

The boardroom atmosphere in September 2023 was electric with a mixture of desperation and determination. After years of watching from the sidelines as professional management struggled to navigate the crisis, the founding family made a dramatic decision. They would return to active management, bringing with them not just fresh capital but a radically different approach to running the business.

The first order of business was brutal honesty about the COVID inventory situation. We had other actions that we had to take in Q4, mainly related to our COVID inventory. We were sitting on approximately INR 120-odd crores of COVID inventory that was allowed for us to be manufactured under voluntary licenses from the innovators only during the COVID period. Rather than continuing to carry this dead weight on the balance sheet, management decided to take the hit all at once.

New leadership was brought in to execute the turnaround. The management changes began in early 2024. Solara Active Pharma Sciences has appointed Arun Kumar Baskaran as Chief Financial Officer (CFO) w.e.f March 8, 2024. But the real shift came in early 2025 with wholesale leadership changes. Solara Active Pharma Sciences Limited has appointed Sandeep Rao as Managing Director (MD) and Chief Executive Officer (CEO) with effect from February 21, 2025 for a term of three years subject to approval of the shareholders of the company. He has been appointed in place of Poorvank Purohit who tendered his resignation as MD & CEO of the company, with effect from February 21, 2025, citing personal reasons.

The financial restructuring was equally dramatic. A rights issue was launched to shore up the balance sheet and provide working capital. The promoters didn't just endorse this dilutive transaction – they participated aggressively. The promoters are participating in the rights, and we also intend to upsize our entitlements. This wasn't just financial engineering; it was a vote of confidence from the very people who knew the business best.

The operational strategy underwent a complete overhaul. Instead of chasing volume in commodity APIs, the new management focused ruthlessly on margins. We continued to focus on profitable high margin and high quality business which led to Gross Margin expansion from 37.8% in FY24 to 51.5% in FY25 and EBITDA margin expansion from -7.1% in FY24 to 16.5% in FY25.

This margin expansion was remarkable – a 1,370 basis point improvement in gross margins and a stunning 2,360 basis point improvement in EBITDA margins. The company was literally transformed from massive losses to healthy profitability within a single fiscal year.

The product mix strategy shifted dramatically. Rather than trying to compete across the entire portfolio, management made hard choices about where to compete and where to retreat. The Ibuprofen business, despite the company's massive capacity and historical strength, was de-emphasized in favor of higher-margin molecules.

Quality achievements continued to provide a foundation for recovery. The inspection established that the site is in an Acceptable State of Compliance with Zero Form 483 inspectional observations from US FDA. The Agency with their designated investigator inspected the facility from 14th to 17th May 2024. Poorvank Purohit, MD & CEO, Solara Active Pharma Sciences, said, We are very happy with the successful inspection outcome of our Visakhapatnam API site with Zero 483 inspectional observation.

The Visakhapatnam facility inspection was particularly significant. Solaras Visakhapatnam (Vizag) facility is a green field project spread-over an area of 40 acres and has dedicated facilities for the manufacture of Ibuprofen API. The facility also manufactures its key starting material for Ibuprofen and thus achieved backward integration of its critical supply chain and ensures business continuity to its customers. This backward integration provided some protection against raw material price volatility.

The numbers began to turn. FY25 Gross Margin at Rs 6,649 million (51.5%) vs Rs 4,891 million (37.8%) in FY24; improvement by 1,370 bps YoY. FY25 EBITDA at Rs 2,138 million (16.5%) vs. negative Rs 917 million (-7%) in FY24; significant improvement by 2,360 bps YoY.

The transformation was remarkable but came with trade-offs. Revenue actually declined as the company walked away from low-margin business. For the year ended March 2025, SOLARA ACTIVE PHARMA SCIENCES reported 100.1% increase in net profit to Rs 5 million compared to net loss of Rs 5,670 million during FY24. Revenue of the company fell 0.4% to Rs 12,838 million during FY25. The company was smaller but healthier – a deliberate strategic choice.

Debt reduction became a priority. During the quarter, Gross debt reduced from Rs 9,994 million to Rs 8,333 million; a reduction of Rs 1,661 million partly from the Rights issue and balance from Operations. The improving cash generation from operations, combined with the rights issue proceeds, allowed for meaningful deleveraging.

Yet challenges remained formidable. Sandeep Rao, MD & CEO stated: "FY25 was a Reset year for Solara. While we regrettably missed our guidance both on Revenues and EBITDA, we continued to focus on profitable high margin and high quality business". Even with the dramatic margin improvement, the company was still missing its targets, highlighting how difficult the turnaround remained.

VII. Modern Operations & Business Model

Today's Solara operates as a significantly transformed entity from its crisis years, though the fundamental challenges of the commodity API business persist. The company's operational footprint remains impressive on paper: Its Manufacturing Facilities has an aggregate installed capacity of 2,584 KL as of December 31, 2023. These aren't just any facilities – SAPSL's Manufacturing Facilities are compliant with global manufacturing standards and most of manufacturing facilities have valid certifications from USFDA (United States), EU and PMDA (Japan).

The manufacturing network spans six strategic locations across India. The Puducherry facility remains the centerpiece for Ibuprofen production, leveraging its historical expertise and scale. The Cuddalore facility, established in 1991, handles multi-product API manufacturing with several independent production blocks. Solara's Visakhapatnam (Vizag) facility is a green field project spread over an area of 40 acres and has dedicated facilities for the manufacture of Ibuprofen API. The facility also manufactures its key starting material for Ibuprofen and thus achieves backward integration of its critical supply chain.

The product portfolio tells a story of both breadth and concentration. Its portfolio includes 60+ commercial APIs across key therapeutic segments, including anthelmintic, anti-malaria, anti-infective, etc. The top 10 molecules contribute to 84% of its total revenues. This concentration is both a strength and a vulnerability – it allows for operational focus but creates significant revenue risk if any major product faces pricing pressure or regulatory issues.

The regulatory filing portfolio demonstrates the company's commitment to maintaining global market access. The company has 67 APIs, 95 DMFs filed with USFDA, providing a pipeline of potential new business as these filings mature into commercial opportunities. Each DMF (Drug Master File) represents years of development work and regulatory investment, creating barriers to entry for competitors.

The CRAMS (Contract Research and Manufacturing Services) business has evolved from a minor sideline to a strategic focus area. Solara's contract research and manufacturing services support production scales from 500 g to 10-kilogram level, or higher quantities of multiple batches. This business model offers better margins than commodity APIs and deeper customer relationships.

The R&D infrastructure, split between Chennai and Bengaluru, employs over 140 scientists. These teams work on both process optimization for existing molecules and development of new APIs. The focus has shifted from purely cost-driven development to creating genuine intellectual property through non-infringing processes and complex chemistry capabilities.

But the commodity trap remains inescapable for much of the portfolio. Ibuprofen, despite Solara's massive capacity and backward integration, operates in a market where price is essentially the only differentiator. A tablet of Ibuprofen from Solara-supplied API is indistinguishable from one made with Chinese API – except the Chinese version costs less to produce.

The customer base reflects this reality. While Solara serves customers across 73 countries (as on February 29, 2024), maintaining these relationships requires constant price negotiations and quality audits. Every customer knows they have alternatives, particularly from Chinese suppliers who may offer prices 20-30% lower.

Geographic revenue distribution shows heavy concentration in Asia-Pacific markets, where price sensitivity is highest. The group has a business presence in the Asia Pacific, Europe, North America, South America, and other places, of which the majority of income is generated from the Asia Pacific countries. The company's attempts to focus more on regulated markets like the US and Europe face the challenge that these markets, while offering better prices, also have higher service expectations and longer sales cycles.

The operational excellence that once seemed like Solara's greatest asset – those perfect FDA inspections, the multiple international certifications – has proven necessary but insufficient. In the commodity API business, quality is table stakes. You need it to play, but it doesn't help you win. The Chinese competitors that undercut Solara's prices often have the same certifications.

The business model transformation attempted under new management – focusing on margins over volume – represents a fundamental shift. But it also means accepting a smaller company. The question remains whether Solara can find enough high-margin business to offset the volume it's walking away from, and whether this strategy is sustainable in a market where today's high-margin molecule becomes tomorrow's commodity.

VIII. Playbook: Lessons from the API Wars

The Solara story offers a masterclass in the harsh realities of commodity pharmaceutical manufacturing, with lessons that extend far beyond the API industry. The first and perhaps most brutal lesson: operational excellence doesn't create competitive advantage in commodity markets – it merely keeps you in the game.

Consider Solara's remarkable quality track record. Multiple consecutive FDA inspections with zero 483s. Certifications from every major regulatory body. State-of-the-art facilities. The result of these inspections demonstrates our commitment to regulatory excellence at our global manufacturing sites and our relentless focus on world-class quality and compliance. We stay committed to exhibit the highest level of compliance and constant focus on world-class quality with the validated quality systems established across Solara's manufacturing network. Yet none of this translated into pricing power. Why? Because in commodities, perfect quality is expected, not rewarded.

The pure-play positioning strategy reveals another crucial lesson: organizational focus doesn't overcome poor industry economics. The theory was sound – formulators would prefer buying APIs from a dedicated supplier rather than a potential competitor. But this preference wasn't worth paying premium prices for. Customers appreciated Solara's pure-play status, then bought from whoever offered the lowest price.

Capital allocation in high-compliance, low-margin businesses presents unique challenges. Every dollar spent on maintaining regulatory compliance is a dollar not available for growth or innovation. Solara found itself trapped in a vicious cycle: high compliance costs necessitated higher prices, which made them uncompetitive, which reduced volumes, which spread fixed compliance costs over fewer units, further raising per-unit costs.

The China challenge illuminates the difficulty of competing against state-supported industries. Chinese API manufacturers benefit not just from lower labor costs but from subsidized electricity, relaxed environmental standards during production ramp-ups, and strategic government support for export industries. Indian companies like Solara must match Chinese prices while bearing full environmental and regulatory costs – an almost impossible equation.

The COVID inventory debacle teaches perhaps the most painful lesson: windfall profits in commodity businesses are usually followed by equal or greater windfall losses. The Rs 120 crores of COVID inventory that seemed like a strategic asset became a massive write-off. The temporary licenses that enabled production during the emergency became prison bars once the emergency ended.

Managing stakeholder expectations during turnarounds requires brutal honesty. Before I start, I just want to give a little bit of recap. The family and the promoters announced taking an active role in Solara approximately 6 months ago. We have been very focused on resetting the company for a profitable growth. The founding family's return to active management sent a clear signal: previous strategies had failed, and radical change was needed.

The margin-over-volume strategy demonstrates the power and peril of strategic retreat. By walking away from low-margin business, Solara dramatically improved its profitability metrics. But this also meant accepting a smaller company with lower revenue. The lesson: sometimes shrinking to grow requires courage that public market investors rarely reward in the short term.

The importance of backward integration in commodity businesses cannot be overstated. The Visakhapatnam facility's ability to produce key starting materials for Ibuprofen provided some insulation from raw material price volatility. But even this advantage proved insufficient against competitors with lower overall cost structures.

Timing matters enormously in corporate restructuring. The 2017-2018 demerger seemed perfectly timed to capture the pure-play premium and potential consolidation in the API sector. But it actually positioned Solara as an independent entity just as the API market was entering its most challenging period. Had the demerger happened five years earlier or later, the outcome might have been very different.

The regulatory excellence paradox deserves special attention. Solara's perfect compliance record should have been a differentiator. In industries where single FDA warning letters can destroy billions in market value, zero 483s should command a premium. But in commodity APIs, customers assume compliance and won't pay extra for excellence. This creates a perverse incentive: why invest in world-class quality systems if the market doesn't reward them?

Finally, the Solara playbook teaches that in commodity businesses, there may be no sustainable moat. Every advantage is temporary. Scale can be replicated. Quality can be matched. Even customer relationships become transactional when products are interchangeable. The only sustainable strategy might be operational efficiency combined with financial flexibility to weather the inevitable cycles.

IX. Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Porter's 5 Forces Analysis

The API industry structure, as illuminated by Solara's struggles, presents one of the most challenging competitive landscapes in pharmaceuticals.

Supplier Power: High The dependence on Chinese raw materials creates enormous vulnerability. China controls over 70% of key starting materials for many APIs, giving suppliers significant leverage. Solara's backward integration attempts at Visakhapatnam only partially mitigate this risk. Suppliers can and do squeeze margins by raising prices during shortage periods, knowing API manufacturers have few alternatives.

Buyer Power: Very High Large pharmaceutical companies dominate purchasing, often putting API requirements out for global tender. With multiple qualified suppliers for commodity APIs, buyers ruthlessly play suppliers against each other. The miss on the Revenue and EBITDA guidance is attributable to intense competition on the Ibuprofen range of products – even in supposedly differentiated products like Ibuprofen, buyers treat APIs as commodities.

Threat of New Entrants: Moderate Regulatory barriers provide some protection. Obtaining FDA approval and maintaining compliance requires substantial investment and expertise. However, the Chinese government's support for new API manufacturers and the increasing technological capabilities of emerging market producers mean new entrants continue to appear, particularly in commodity molecules.

Threat of Substitutes: Low APIs are essential ingredients with no true substitutes. However, within therapeutic categories, multiple APIs often compete. If Ibuprofen becomes too expensive, formulators can switch to naproxen or other NSAIDs. This therapeutic substitution limits pricing power even for essential medicines.

Competitive Rivalry: Intense The rivalry among existing competitors is perhaps the most destructive force. Chinese manufacturers, Indian peers like Neuland Laboratories, Divi's Laboratories, Alkem Laboratories, and global players compete aggressively on price. The undifferentiated nature of commodity APIs means competition devolves to price wars that destroy industry profitability.

Hamilton's 7 Powers Analysis

Examining Solara through Hamilton Helmer's framework reveals why sustainable competitive advantage proves so elusive in commodity APIs.

Scale Economies: Weak Despite operating one of the largest Ibuprofen manufacturing sites in the world, Solara couldn't achieve meaningful scale economies. The problem: Chinese competitors operate at even larger scales with lower cost structures. Scale in commodity manufacturing provides minimal advantage when competitors have similar or greater scale.

Network Effects: None APIs exhibit no network effects. One customer using Solara's APIs doesn't make them more valuable to other customers. If anything, concentration risk makes customers want to diversify suppliers, creating negative network effects.

Counter-positioning: Attempted but Failed The pure-play positioning represented an attempt at counter-positioning – doing something integrated players couldn't or wouldn't do. There is a tremendous opportunity for the API players to bring value to the formulators but they find it risky to partner with companies that also have an interest in the finished dosage business. But customers valued this only marginally, insufficient to overcome price disadvantages.

Switching Costs: Moderate Regulatory approvals create some switching costs. Changing API suppliers requires regulatory filings and potentially bioequivalence studies. However, for commodity APIs, most formulators maintain multiple qualified suppliers specifically to avoid lock-in. The switching costs that exist don't translate to pricing power.

Branding: Minimal B2B commodity products offer virtually no branding opportunity. No end consumer knows or cares whether their Ibuprofen tablet contains Solara's API. Even among professional buyers, brand preference is minimal. Quality is assumed; price dominates decisions.

Cornered Resource: Limited Certain niche APIs where Solara has unique process knowledge or regulatory approvals might constitute cornered resources. But in the core portfolio of commodity APIs, no truly unique resources exist. The facilities, while impressive, can be replicated. The regulatory approvals, while valuable, don't prevent competition.

Process Power: Moderate The company's quality systems and ability to consistently achieve zero 483s suggest some process power. This continues to demonstrate our relentless focus on world-class quality and compliance, which remains a key pillar of our growth strategy. However, process advantages in commodity manufacturing provide minimal competitive advantage when the end product is identical.

Competitive Comparison

Against peers, Solara's positioning appears particularly challenged. Divi's Laboratories, with its focus on custom synthesis and complex APIs, enjoys better margins and customer stickiness. Laurus Labs' focuses on innovation, quality, and affordability in developing medicines. With a strong presence in anti-retroviral, Hepatitis C, and Oncology drugs – therapeutic areas with higher barriers to entry.

The comparison reveals Solara's strategic error: competing in the most commoditized segments of the API market without meaningful differentiation. While peers moved toward specialty and complex APIs, Solara remained concentrated in commodity molecules where competitive advantage is nearly impossible to sustain.

X. Bear vs. Bull Case

Bear Case: Structural Challenges in a Commodity Business

The bear case for Solara starts with a simple, damning fact: The company has delivered a poor sales growth of -0.58% over past five years. This isn't a temporary blip – it's a five-year track record of value destruction during a period when the global pharmaceutical market grew substantially.

The revenue trajectory tells a story of persistent decline. Despite operating six manufacturing facilities with impressive regulatory credentials, the company cannot grow. The FY25 revenue of Rs 12,838 million is actually lower than what the combined entities were generating before the demerger. This shrinkage isn't strategic – it's symptomatic of an inability to compete.

The commodity trap appears inescapable. With The top 10 molecules contribute to 84% of its total revenues, Solara remains dangerously concentrated in products where price is the only differentiator. Ibuprofen, the company's historical strength, has become an albatross. Chinese competitors can produce it cheaper, and customers know it.

Debt burden relative to profitability remains concerning despite recent improvement. While the company achieved positive EBITDA in FY25, the margins remain thin and vulnerable to any operational disruption. The interest coverage, while improved from negative territory, barely reaches sustainable levels. Any downturn in pricing or demand could quickly push the company back into distress.

Chinese competition continues to intensify. The structural advantages enjoyed by Chinese manufacturers – government subsidies, lower environmental compliance costs, cheaper raw materials – aren't going away. If anything, China's push for pharmaceutical self-sufficiency means more support for their API industry. Solara must compete against companies that operate with fundamentally different economics.

Limited pricing power condemns the company to perpetual margin pressure. In commodity APIs, the lowest-cost producer sets the price, and that's rarely Solara. The company's quality excellence, while admirable, doesn't translate to premium pricing. Customers appreciate zero 483s, then buy from whoever's cheapest.

The management revolving door raises governance concerns. The CEO change in early 2025, CFO changes, and the founding family's return to active management suggest strategic confusion. While positioned as a turnaround effort, frequent leadership changes often signal deeper organizational dysfunction.

Customer concentration and countervailing power present ongoing risks. Large pharma companies know Solara needs their business more than they need Solara. This asymmetry manifests in extended payment terms, last-minute order cancellations, and constant price renegotiation demands.

Bull Case: Turnaround Gaining Traction

The bull case begins with the remarkable FY25 turnaround: Gross Margin expansion from 37.8% in FY24 to 51.5% in FY25 and EBITDA margin expansion from -7.1% in FY24 to 16.5% in FY25. This isn't incremental improvement – it's transformation. Moving from negative EBITDA to 16.5% margins in one year demonstrates that the business can be profitable with the right strategy.

China Plus One dynamics are finally materializing. Geopolitical tensions, supply chain vulnerabilities exposed by COVID, and quality concerns about Chinese APIs are driving real diversification. Governments and pharma companies increasingly mandate multiple geographic sources for critical APIs. Solara, with its proven quality record and Indian manufacturing base, stands to benefit.

The regulatory track record remains genuinely exceptional. The Company is quality compliant, with the last USFDA inspection at its Manufacturing Facilities (except Mysuru facility) including the R&D Centre have been cleared with zero 483s observations. In an industry where single warning letters can exclude suppliers from entire markets, Solara's consistent compliance excellence provides real competitive advantage.

Management reset with promoter involvement signals serious commitment. The family and the promoters announced taking an active role in Solara approximately 6 months ago. We have been very focused on resetting the company for a profitable growth. Unlike hired management, the founding family has skin in the game. Their participation in the rights issue demonstrates confidence in the turnaround.

Essential medicines portfolio provides defensive characteristics. Anti-malarials, anti-infectives, and pain management APIs aren't discretionary. Demand may fluctuate, but it won't disappear. As global population ages and emerging markets expand healthcare access, volume growth in essential medicines seems assured.

The CRAMS opportunity offers a path beyond commodities. Contract manufacturing for innovator companies and complex generic players provides better margins and deeper relationships. Solara's regulatory credentials and manufacturing expertise position it well for this higher-value business.

Operational leverage potential remains significant. With facilities running below capacity and fixed costs already absorbed, incremental volume can drop straight to the bottom line. If demand recovers and capacity utilization improves, margins could expand dramatically from current levels.

Backward integration at Visakhapatnam provides strategic advantage. The facility also manufactures its key starting material for Ibuprofen and thus achieves backward integration of its critical supply chain. While not a complete solution to input cost pressures, controlling key starting materials provides some buffer against supply shocks and price volatility.

XI. Epilogue: What's Next?

As the monsoon clouds gather once again over Chennai in 2025, Solara Active Pharma Sciences stands at yet another inflection point. The turnaround has shown promising early results, but the fundamental question remains: Is there a sustainable moat in commodity APIs, or is Solara simply managing decline more skillfully?

The API consolidation thesis that drove the original demerger remains largely unfulfilled. The expected industry roll-up hasn't materialized. Instead of consolidation creating stronger players with better economics, the industry has seen continued fragmentation with new entrants, particularly from China, offsetting any exits. Solara finds itself not as a consolidator but as a potential target, though its challenged economics make it an unlikely acquisition candidate at attractive valuations.

Geopolitical tailwinds offer perhaps the best hope for structural improvement. The China Plus One narrative has evolved from corporate buzzword to government policy. The US BIOSECURE Act, European Union's pharmaceutical strategy, and India's Production Linked Incentive schemes all aim to reduce dependence on Chinese APIs. But translating policy support into sustainable competitive advantage requires more than good intentions.

The economic headwinds remain formidable. Input cost inflation, currency volatility, and the structural disadvantages of competing against state-supported Chinese manufacturers won't disappear. The commodity nature of most APIs means that even with geopolitical support, pricing power remains elusive. Solara must navigate between the Scylla of maintaining quality standards and the Charybdis of matching Chinese pricing.

Can Solara escape the commodity trap? The new management's strategy of focusing on margins over volume represents one path – becoming a smaller, more profitable company serving niche segments where quality and reliability command premiums. But this requires walking away from the scale ambitions that justified the original demerger. It means accepting that Solara will never be the global API champion envisioned in 2017.

The alternative path – moving up the value chain into complex APIs, controlled substances, or specialized contract manufacturing – requires capabilities and capital that Solara may struggle to marshal given its recent history. The company's excellent regulatory track record provides a foundation, but building differentiated technical capabilities while servicing existing debt and funding working capital needs presents a formidable challenge.

Key metrics to watch going forward tell the story of this balancing act. EBITDA margins must stay above 15% to demonstrate sustainable profitability – any slip back toward single digits would signal the turnaround is faltering. US FDA compliance must remain pristine; a single warning letter could unravel years of reputation building. New product approvals, particularly in complex or specialized APIs, would signal successful evolution beyond commodities.

The ultimate question facing Solara isn't whether commodity APIs can be profitable – they can, occasionally, in cycles. It's whether a pure-play commodity API company can generate returns that justify the capital employed and risks taken. The brutal arithmetic of commodity manufacturing suggests the answer is no. Quality is necessary but not sufficient. Scale helps but doesn't determine success. Even operational excellence, as Solara has painfully learned, guarantees nothing in markets where products are undifferentiated and buyers hold all the cards.

Looking ahead, Solara's story serves as a cautionary tale for Indian pharma's ambitions in the global API market. The dream of becoming the pharmacy of the world requires more than manufacturing capacity and regulatory compliance. It demands competitive advantages that commodity markets rarely allow. Whether Solara can transcend these limitations or remains trapped in the commodity cage will determine not just its own fate, but offer lessons for an entire industry grappling with similar challenges.

The rain continues to fall outside that Chennai boardroom, much as it did when this journey began. But unlike the eternal monsoon, Solara's time to prove its transformation is finite. The market's patience, the promoters' capital, and the competitive landscape all impose deadlines on a turnaround that has shown promise but not yet proven sustainability. The next 6-8 quarters, as management has promised, will determine whether Solara's story is one of redemption or merely a well-managed decline in an industry where sustainable competitive advantage remains perpetually out of reach.

For investors, employees, and industry observers, Solara embodies the central paradox of modern pharmaceutical manufacturing: essential products with commodity economics, operational excellence without pricing power, global aspirations constrained by brutal market realities. The company's journey from demerger to crisis to attempted turnaround offers no easy answers, only hard lessons about the limits of strategy in industries where structural forces overwhelm individual company efforts.

As this chapter closes, Solara Active Pharma Sciences remains a company in transition, its ultimate destination uncertain. The pure-play API story that began with such promise in 2017 has become something far more complex – a meditation on the challenges of competing in global commodity markets, the importance of timing in corporate strategy, and the sobering reality that in some industries, there may be no sustainable moat at all. Whether Solara proves this conclusion wrong or becomes its most prominent example remains to be written in the quarters ahead.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube