Jubilant Pharmova: The Nuclear Medicine Mogul and the Pharmaceutical Pivot

I. Introduction & Episode Roadmap

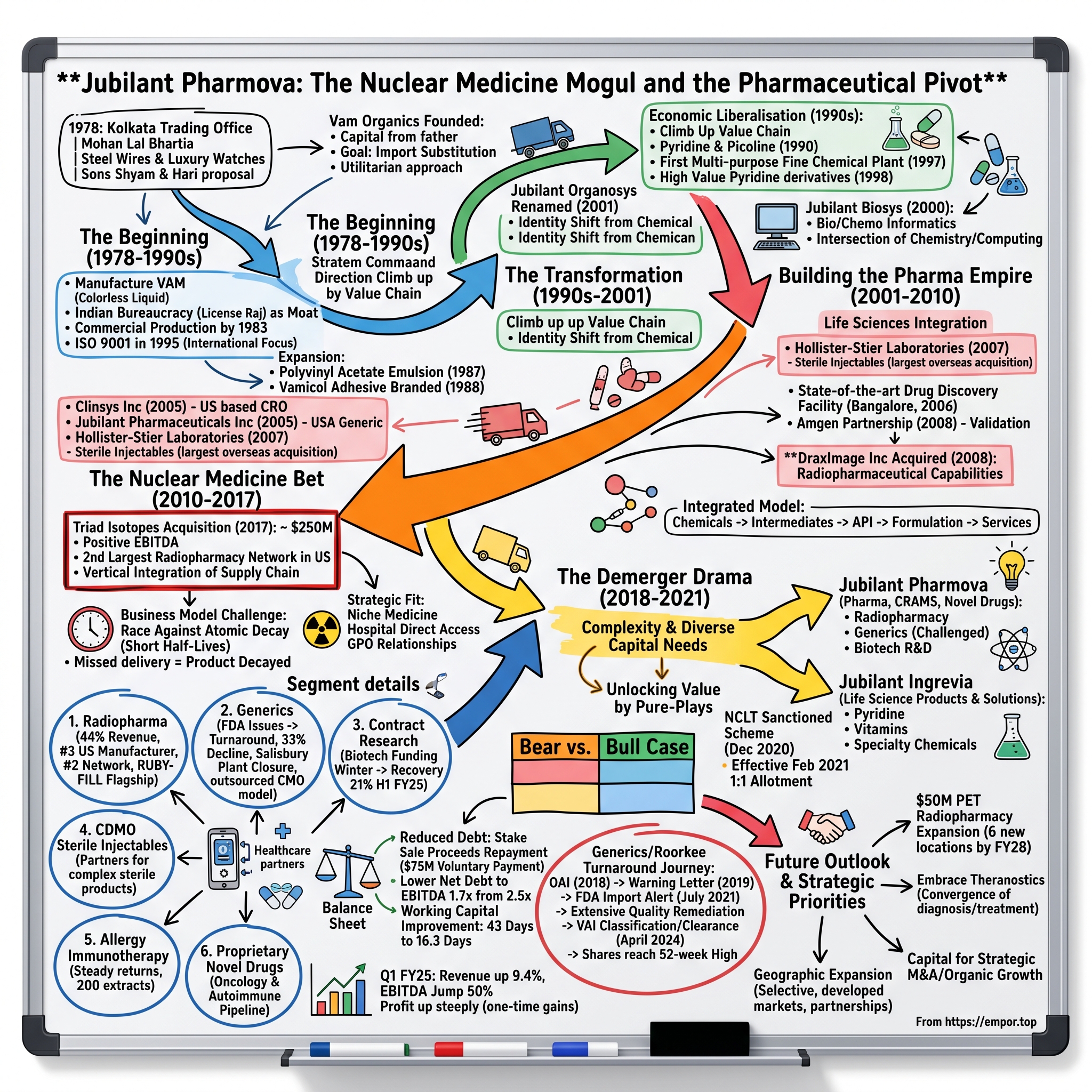

Picture this: A modest trading office in Kolkata, 1978. Steel wires and luxury watches line the shelves—the bread and butter of Mohan Lal Bhartia's import business. His two sons, Shyam and Hari, approach with an audacious proposal: they want to manufacture vinyl acetate monomer, a chemical compound most Indians couldn't pronounce, let alone understand its industrial significance. Fast forward to 2024, and that leap of faith has morphed into Jubilant Pharmova—a ₹17,526 crore pharmaceutical conglomerate that holds the #3 position in U.S. radiopharmaceutical manufacturing and operates the second-largest network of radiopharmacies in America with 46 facilities.

The journey from VAM to nuclear medicine reads like a masterclass in strategic pivots. While most Indian chemical companies of the License Raj era remained content with import substitution, the Bhartia brothers systematically climbed the value chain—from commodity chemicals to specialty ingredients, from active pharmaceutical ingredients to finished formulations, and ultimately to the rarefied world of radiopharmaceuticals where they now deliver over 3 million patient doses annually.

This is not just another family business success story. It's a tale of how two brothers recognized that the real money in chemicals wasn't in selling commodities but in solving complex problems. They understood that each regulatory hurdle, each technical challenge, each capital-intensive facility was not a barrier but a moat. Today, when a cancer patient in Ohio receives a radioactive tracer for their PET scan, there's a good chance it came from a Jubilant radiopharmacy—a remarkable achievement for a company that started by making industrial adhesive components.

What makes Jubilant Pharmova particularly fascinating is its contrarian bet on radiopharmaceuticals at a time when most Indian pharma companies were chasing generic blockbusters. While others fought price wars in crowded therapeutic areas, Jubilant quietly built capabilities in nuclear medicine—a field so specialized that even today, most investors struggle to understand its economics. The result? A business segment that now contributes 44% of revenues with margins that would make generic manufacturers weep with envy.

But this isn't a story without setbacks. The company's generics division faced an FDA import alert at its Roorkee facility in 2021, revenues in that segment plummeted from ₹1,160 crore to ₹775 crore, and the biotech funding winter hammered their drug discovery services. Yet through strategic demergers, operational pivots, and sheer persistence, they've begun turning these challenged divisions around while doubling down on their nuclear medicine dominance.

II. The Brothers & The Beginning: VAM to Vision (1978–1990s)

The steel wire trader's office in Kolkata hummed with activity that June day in 1978. Mohan Lal Bhartia had built a respectable business importing industrial materials and luxury goods—including being one of the few authorized Rolex dealers in eastern India. But his sons had grander ambitions. Shyam Sundar Bhartia, the elder, had married into the influential Shobhana Bhartia family (she would later helm Hindustan Times), bringing both social capital and business acumen to the partnership. Younger brother Hari brought operational expertise and an engineer's precision to problem-solving. Their choice of product was telling. Vinyl acetate monomer (VAM) is a colorless liquid organic compound that serves as an intermediate in manufacturing industrial polymers and resins for adhesives, coatings, paints, films and textiles. In 1978's India, this was as unglamorous as it got. No consumer brand prestige, no pharmaceutical margins—just a commodity chemical that most people had never heard of. But the brothers saw opportunity where others saw obscurity.

The business was seeded with funds obtained from their father Mohan Lal Bhartia, who was a steel wire and Rolex watch trader in Kolkata. The initial capital wasn't massive—this wasn't a Tata or Birla-scale launch. But it was enough to set up a modest manufacturing facility and begin the arduous process of import substitution. The company name itself was utilitarian: Vam Organics, an abbreviation of the product they manufactured, vinyl acetate monomer.

The timing was both terrible and perfect. India's License Raj was at its peak—every expansion required permits, every import needed approval, and every price was controlled. But this regulatory maze also created protective moats. Foreign competition was limited, and domestic players who could navigate the bureaucracy had guaranteed markets. The Bhartias didn't just navigate; they excelled. By 1983, commercial production of VAM had begun, marking India's first domestic manufacturing of this critical industrial chemical.

What distinguished the brothers early on was their approach to quality. In an era when "good enough for India" was the prevailing standard, they pursued international certifications. The company received ISO 9001 certification for its quality systems in 1995—among the first Indian chemical companies to achieve this. This wasn't just about certificates on the wall; it was a statement of intent. They weren't building for the protected Indian market of the 1980s but for the globalized economy they could see coming.

The late 1980s brought subtle but important expansions. In 1987, the company introduced polyvinyl acetate emulsion for paint, textile, paper & packaging and woodworking industries. In 1988, they launched their first branded product under the name Vamicol, an adhesive product. These weren't revolutionary moves, but they showed strategic thinking: moving from pure commodity chemicals to slightly more specialized products with brand potential.

Vam Organics gained opportunities to carry out higher-value work for drug and chemical industries following economic liberalisation in India in the 1990s. The dismantling of the License Raj wasn't just about removing restrictions—it fundamentally changed what was possible. Suddenly, importing technology became easier, partnering with foreign companies was allowed, and most importantly, Indian companies could dream beyond substituting imports to actually competing globally.

The 1990s transformation was swift. The plant for Pyridine & Picoline started in 1990, marking their entry into pharmaceutical intermediates—chemicals one step closer to actual drugs. In 1997, the first multi-purpose fine chemicals plant went on stream. By 1998, they had entered high value-added Pyridine derivatives, commissioning Pyridine HBR and Cyano Pyridine plants.

Each of these moves represented a climb up the value chain. VAM sells for dollars per kilogram; pharmaceutical intermediates sell for tens or hundreds of dollars per kilogram. The margins improve, but so does the complexity. You need better technology, stricter quality control, and critically, regulatory approvals from buyers' countries. In 1998, the company formed a marketing subsidiary in the USA and acquired an acetyl plant in western India—their first international presence and their first acquisition.

By the decade's end, the Bhartia brothers had transformed their father's seed capital into something far more ambitious. They weren't just making chemicals; they were building capabilities. They weren't just serving Indian markets; they were eyeing the world. And most importantly, they had learned a crucial lesson that would drive their next transformation: in chemicals, as in life, the money isn't in doing simple things at scale—it's in solving complex problems that others can't or won't tackle.

III. The Transformation: From Chemicals to Pharma (1990s–2001)

The new millennium arrived with Y2K fears gripping the world's computer systems, but in a nondescript conference room in Noida, the Bhartia brothers were planning a different kind of systems upgrade. The question on the table: What should Vam Organics become? The answer would transform not just their company's trajectory but its very identity.

The company was renamed Jubilant Organosys in 2001, which began the use of the name "Jubilant" for the group. The name change was more than cosmetic—it was a declaration of intent. "Jubilant" suggested celebration, success, arrival. No longer would they be defined by a single chemical compound. They were building something bigger.

The strategic logic was compelling. Their chemical business had taught them three critical lessons: First, commodities are a race to the bottom unless you have massive scale. Second, regulatory complexity is a moat, not a burden, if you can master it. Third, the real value in chemicals comes from what you enable downstream—and nothing downstream was more valuable than pharmaceuticals.

Consider the economics: A kilogram of VAM might sell for $2. A kilogram of a pharmaceutical intermediate could fetch $50. A kilogram of an active pharmaceutical ingredient (API) could command $500. And a kilogram of a specialized drug? Thousands. The Bhartias weren't just climbing the value chain; they were pole-vaulting up it.

The company had penetrated the bio/chemo informatics arena by setting up Jubilant Biosys Ltd in 2000. This was prescient. Just as the Human Genome Project was completing, just as computational drug discovery was becoming feasible, Jubilant was positioning itself at the intersection of chemistry and computing. They weren't trying to discover new drugs themselves—not yet—but they would provide the computational infrastructure for those who were.

The early 2000s Indian pharma landscape was undergoing its own transformation. The global generic drug opportunity was exploding as blockbuster drugs lost patent protection. Indian companies had proven they could reverse-engineer almost any molecule. But Jubilant took a different path. Instead of competing in the crowded generic formulations space, they focused on the less glamorous but more defensible business of making the active ingredients themselves.

Their pharmaceutical strategy had three pillars. First, leverage existing chemical capabilities—their pyridine chemistry expertise could produce key intermediates for anti-TB drugs, anti-retrovirals, and other essential medicines. Second, build regulatory credibility—getting US FDA approval for their facilities even before they had major US customers. Third, pursue complexity—focusing on molecules that required multi-step synthesis, specialized equipment, or handling of hazardous materials.

The operational transformation was immense. Pharmaceutical manufacturing isn't just stricter than chemical manufacturing; it's a different universe. Every batch needs documentation that could fill a filing cabinet. Equipment must be validated not just to work, but to work exactly the same way every time. Quality control moves from sampling to testing every single parameter. The brothers brought in pharmaceutical veterans from established companies, often paying premium salaries to lure them from comfortable MNC jobs to their ambitious but unproven venture.

By 2005, Jubilant Organosys had multiple US FDA-approved facilities, a portfolio of over 30 APIs, and relationships with most major generic drug companies. Revenue had crossed ₹1,000 crore. But more importantly, they had successfully transformed their identity. When industry conferences discussed Jubilant, they no longer talked about it as a chemical company that did some pharma. It was now a pharmaceutical company with chemical heritage.

The international expansion accelerated. They established subsidiaries in China to access raw materials, in Europe to be closer to customers, and strengthened their US presence to understand the world's largest pharmaceutical market. Each geography taught them something new. China showed them scale, Europe showed them regulatory excellence, and America showed them innovation.

Yet the most audacious move was still to come. While building their pharmaceutical capabilities, the brothers had noticed something interesting. Certain niches in healthcare were surprisingly underserved. Not because they weren't profitable, but because they required unusual combinations of capabilities. One such niche would become their defining bet: radiopharmaceuticals. But that story would unfold in the next phase of Jubilant's evolution, as they transformed from a pharmaceutical company into something even more specialized—a nuclear medicine powerhouse that would eventually command premium valuations and defensible moats that their commodity chemical origins could never have imagined.

IV. Building the Pharma Empire: Life Sciences Integration (2001–2010)

The boardroom at Jubilant Organosys hummed with nervous energy in July 2010 as the directors voted on yet another name change. The company was renamed Jubilant Organosys Limited in 2001, and Jubilant Life Sciences Limited in July 2010. This wasn't just rebranding—it was a declaration that they had evolved from a chemical company with pharma interests into a full-fledged life sciences conglomerate.

The numbers told the transformation story. By 2010, Jubilant operated 6 USFDA approved manufacturing facilities in the US, Canada and India, a remarkable achievement for a company that had zero pharmaceutical facilities just a decade earlier. Revenue had exploded from hundreds of crores to crossing ₹3,000 crore. But the real story wasn't in the numbers—it was in the strategic chess moves that got them there.

The acquisition spree began modestly but accelerated rapidly. In 2005, JLSL acquired Target Research Associates, Inc and renamed it Clinsys Inc., a US based Clinical Research Organisation. Also in the same year, the company acquired Trinity Laboratories, Inc. and its wholly owned subsidiary, Trigen Laboratories, Inc., renamed Jubilant Pharmaceuticals, Inc., a generic pharmaceutical company in USA having a US FDA approved formulations manufacturing facility. These weren't just asset purchases; they were capability acquisitions. Each brought something Jubilant couldn't build organically fast enough—FDA approvals, customer relationships, or specialized expertise.

The crown jewel acquisition came in 2007. As of June 2007, JLSL had completed the largest overseas acquisition in Contract Manufacturing by an Indian company, through its purchase of Hollister-Stier Laboratories. Hollister-Stier wasn't just a manufacturing facility; it was a gateway to the lucrative contract manufacturing business for sterile injectables—products with high barriers to entry and attractive margins.

But perhaps the most prescient move was their early bet on drug discovery services. Jubilant's state-of-the-art Drug Discovery facility was inaugurated in Bangalore during November of 2006, the largest of its kind in India for providing integrated Drug Discovery solutions. This wasn't following the herd into generics; it was positioning for where the industry would be in a decade—when Big Pharma would increasingly outsource early-stage research to cut costs.

The partnership strategy was equally sophisticated. The Company and Amgen Inc, Thousand Oaks, California, the largest US based Biotech Company, made a drug discovery partnership in July 2008 through Jubilant Biosys Ltd subsidiary, under which Amgen and Jubilant collaborate to develop a portfolio of novel drugs in new target areas. Landing Amgen as a partner was like getting Harvard to validate your educational credentials—it signaled to the entire industry that Jubilant was a serious player.

The integrated model they built was elegant in its complexity. Start with basic chemical building blocks from their legacy business. Use these to manufacture pharmaceutical intermediates. Convert those into active pharmaceutical ingredients. Formulate those APIs into finished dosage forms. And wrap it all with drug discovery services that could help customers develop the next generation of molecules. Each step of the value chain reinforced the others.

Jubilant Life Sciences acquired a 100% stake in DRAXIS Health in April 2008 for a price of $255M. DRAXIS brought something special—radiopharmaceutical capabilities. While most investors scratched their heads at the price tag for a niche business, the Bhartias saw what others missed: a highly specialized field with massive barriers to entry where established players enjoyed quasi-monopolistic positions.

The operational complexity of managing this empire was staggering. They were simultaneously running commodity chemical plants in India requiring cost optimization, FDA-inspected pharmaceutical facilities requiring quality perfection, drug discovery labs requiring cutting-edge science, and radiopharmaceutical operations requiring nuclear regulatory compliance. Most companies would have collapsed under the complexity. Jubilant thrived.

By 2010, Jubilant Life Sciences had a team of around 7,700 multicultural people across the globe. The transformation from a family-run chemical company to a global pharmaceutical conglomerate was complete. Or so it seemed. In reality, the most audacious pivot was yet to come. While the world focused on their generic drug business and contract manufacturing capabilities, the Bhartias were quietly building what would become their most valuable asset: a dominant position in nuclear medicine that would redefine the company's identity and valuation trajectory for the next decade.

V. The Nuclear Medicine Bet: Radiopharmaceuticals (2010–2017)

The conference room in Orlando was packed with radiopharmacy executives in May 2017, the annual industry gathering where everyone knew everyone. When news broke that morning of Jubilant's agreement to acquire Triad Isotopes for an undisclosed amount (later revealed to be around $250 million), the reaction was shock. Not because the deal was surprising—consolidation in radiopharmaceuticals was inevitable—but because an Indian pharmaceutical company had just made one of the boldest bets in nuclear medicine history.

Triad recorded revenues in excess of $225 million in 2016 with positive EBITDA and operated the second largest radiopharmacy network in the US with more than 50 pharmacies. To understand why this mattered, you need to understand what radiopharmaceuticals are not. They're not like regular drugs you can manufacture, warehouse, and ship. These are radioactive compounds with half-lives measured in hours or days. You literally race against atomic decay to get them to patients.

The business model is unlike anything else in pharmaceuticals. A radiopharmacy receives radioactive isotopes—often flown in daily from nuclear reactors—and compounds them into patient-specific doses in hot cells (lead-lined chambers). These doses are then rushed to hospitals and imaging centers, often multiple times per day, for procedures like PET scans and cardiac imaging. Miss a delivery window by an hour, and the product might be too decayed to use. It's pharmaceutical manufacturing meets FedEx logistics meets nuclear physics.

Speaking on the occasion, Mr. Shyam S Bhartia, Chairman, and Mr. Hari S Bhartia, Co-Chairman and Managing Director, said: 'The acquisition is a strategic fit to our niche nuclear medicine business and will provide Jubilant with direct access to hospital networks with ability to deliver more than 3 Million patient doses annually through approximately 1,700 customers'.

But the Triad acquisition wasn't Jubilant's first foray into nuclear medicine. They had been methodically building capabilities since their DRAXIS acquisition in 2008. DRAXIS had given them manufacturing capabilities for radiopharmaceutical products. Now Triad would give them the distribution network—the radiopharmacies themselves. It was vertical integration of the most complex kind.

The strategic rationale was brilliant in its simplicity. Radiopharmaceuticals had three characteristics that made them perfect for Jubilant. First, massive barriers to entry—you need nuclear regulatory licenses, specialized facilities, and trained nuclear pharmacists. Second, sticky customer relationships—hospitals don't switch radiopharmacy providers lightly when patient care depends on clockwork reliability. Third, favorable demographics—an aging population needing more cardiac and cancer imaging.

This acquisition was funded through JPL's internal accruals with no increase in debt for Jubilant Life Sciences, a detail that revealed how cash-generative their existing businesses had become. They could drop a quarter-billion dollars without leveraging up—a far cry from the days of borrowing from dad to start a VAM plant.

The operational complexity of integrating Triad was staggering. Each radiopharmacy operates under strict Nuclear Regulatory Commission oversight. You can't just walk in and change procedures; every modification requires regulatory approval. The workforce—nuclear pharmacists and technicians—are highly specialized and in short supply. One mass exodus could cripple operations.

Triad had an experienced management team, customer focus and strong relationships with GPOs in the United States. Group Purchasing Organizations (GPOs) are the gatekeepers in US healthcare, aggregating purchasing power for hospitals. Having those relationships meant Jubilant wasn't just buying pharmacies; they were buying market access.

The timing of the acquisition was fortuitous. The radiopharmaceutical industry was on the cusp of transformation. New isotopes were being developed for both diagnosis and treatment—theranostics, where the same targeting molecule could be used first to image cancer and then to deliver radiation directly to tumors. Jubilant was positioning itself for this future while competitors focused on traditional pharmaceuticals.

Jubilant Radiopharma was acquired on 01-Sep-2017. Jubilant Radiopharma was acquired by Jubilant Pharmova, marking the successful closing of one of the most strategic acquisitions in the company's history.

The integration proceeded smoothly, defying skeptics who doubted an Indian company could manage such a complex US operation. They retained key management, maintained service levels, and gradually introduced operational improvements. Within a year, the acquisition was earnings accretive, validating the strategic bet.

By 2017's end, Jubilant had transformed from a company with radiopharmaceutical manufacturing capabilities into one of the dominant players in US nuclear medicine. They controlled the entire value chain—from isotope procurement to patient delivery. It was a position that would prove invaluable as the company prepared for its next transformation: the great demerger that would create focused, pure-play entities designed to unlock value that the conglomerate structure had obscured.

VI. The Demerger Drama: Focus and Restructuring (2018–2021)

The boardroom atmosphere at Jubilant Life Sciences headquarters in Noida was electric on October 25, 2019. After months of deliberation, the board had just approved what would become one of the most complex corporate restructurings in Indian pharmaceutical history. The conglomerate that the Bhartia brothers had painstakingly built over four decades would be split in two. It was both an admission that complexity had become a burden and a bet that focused entities would unlock value that the market couldn't see in the sprawling whole.

The strategic logic was compelling but painful. Jubilant Life Sciences had become too diverse for its own good. On one side, you had pharmaceutical businesses—radiopharmaceuticals, generics, contract manufacturing, drug discovery. On the other, life science ingredients—pyridines, vitamins, specialty chemicals. The synergies that once justified keeping them together had become tenuous. Worse, each business required different capital allocation priorities, had different growth trajectories, and appealed to different investor bases.

The Hon'ble National Company Law Tribunal, Allahabad Bench ('NCLT') has, by its Order dated 23 December 2020, sanctioned the Composite Scheme of Arrangement under Sections 230 to 232 read with Section 66 and other applicable provisions of the Companies Act, 2013. The legal complexity was staggering. This wasn't just splitting one company into two—it involved amalgamating certain promoter-controlled entities while simultaneously demerging the Life Science Ingredients business.

The market initially reacted with confusion. Why split a company that had been growing steadily? The answer lay in valuation arbitrage. Pure-play pharmaceutical companies traded at higher multiples than chemical companies. By keeping them together, Jubilant was getting valued at a blended multiple that undervalued its high-margin pharma businesses while not giving full credit to its chemical business's cash generation.

Jubilant Life Sciences has fixed 05 February 2021 as record date for allotment of 1 (one) equity share of Jubilant Ingrevia for every 1 (one) equity share held in Jubilant Life Sciences pursuant to composite scheme of arrangement. This 1:1 ratio meant shareholders wouldn't be diluted—they'd own the same economic interest, just split across two focused entities.

The naming itself told a story. Pharmova is born out of a combination of 'Pharma' and 'Nova' (New) and Jubilant Pharmova Limited will continue to focus on offering products and services with, excellence in research and manufacturing, catering to the unmet health needs at an affordable price. Meanwhile, Ingrevia is born out of a union of 'Ingredients' and 'Life' ('Vie' in French). Jubilant Ingrevia Limited is committed to offering high quality and innovative life science ingredients to enrich all forms of life.

The demerger wasn't without operational challenges. Systems had to be separated, employees allocated, contracts renegotiated. Shared services that had created economies of scale now needed to be duplicated. The radiopharmacy network, the crown jewel, stayed with Pharmova. The pyridine and vitamin businesses, steady cash generators, went to Ingrevia.

The demerger is effective from 1 February 2021 and creates separate and focused entities: Jubilant Pharmova for pharmaceuticals, contract research and development services and proprietary novel drugs businesses and Jubilant Ingrevia for life science products and innovative solutions business; that will help in unlocking shareholder value.

The immediate financial impact was positive. Jubilant Pharmova (erstwhile Jubilant Life Sciences) hit an upper circuit of 5% at Rs 954.45 after the company reported 52% jump in net profit to Rs 310 crore on a 15% rise in revenue from operations to Rs 2,664 crore in Q3 FY21 over Q3 FY20. Profit before tax in Q3 FY21 stood at Rs 453 crore, up by 54% from Rs 293 crore in Q3 FY20.

Jubilant Ingrevia was listed on the Bombay Stock Exchange on 19 March 2021, marking the successful completion of one of the most complex demergers in Indian corporate history. The market's verdict was swift and positive—both entities saw their valuations re-rate upward as investors could finally value each business on its own merits.

But the demerger also revealed challenges that had been masked by the conglomerate structure. Pharmova's generics business was struggling with FDA issues. The drug discovery segment was facing headwinds from the biotech funding winter. Without the cushion of the chemical business's steady cash flows, these problems became more visible and urgent.

The Bhartia brothers had made a calculated bet: that transparency and focus would ultimately create more value than diversification and synergy. They were betting that investors would reward pure-play stories over conglomerate complexity. Most importantly, they were positioning each entity to pursue its own strategic priorities without being constrained by the capital needs or risk profile of the other. As 2021 dawned with two listed entities instead of one, the real test of this strategy was just beginning.

VII. Current Business Portfolio: Six Segments of Growth

The sterile production floor at Jubilant's Montreal facility hummed with activity as technicians carefully handled the lead-shielded containers. Inside: radioactive rubidium-82 generators worth tens of thousands of dollars each, destined for cardiac imaging centers across North America. This scene, replicated across 46 radiopharmacies, represents the crown jewel of Jubilant Pharmova's six-segment strategy—a portfolio that generates ₹7,404 crore in revenue but whose complexity confounds many investors.

Radiopharma: The Nuclear Medicine Dominance (~44% revenue contribution)

The company is the #3 radiopharmaceutical manufacturer in the US and has the #2 network in the US with 46 radiopharmacies. In 9MFY24, sale of Mertiatide, Sulfur colloid) and Ruby-Fill did very well. RUBY-FILL is a cardiac imaging product. The radiopharmaceutical segment isn't just Jubilant's largest; it's their moat. Consider RUBY-FILL, their flagship cardiac imaging product. RUBY-FILL is used for cardiac PET imaging under rest or pharmacologic stress conditions to evaluate regional myocardial perfusion in patients with suspected or existing coronary artery disease. Since the FDA approval of RUBY-FILL in 2016, Jubilant Radiopharma has partnered with health care providers across the U.S. to establish and grow cardiac PET programs.

The brilliance of RUBY-FILL lies not just in the product but in the ecosystem Jubilant built around it. Jubilant DraxImage Inc., dba Jubilant Radiopharma, a wholly-owned subsidiary of Jubilant Pharma Limited, announced the clearance by the FDA to use its RUBY Rubidium Elution System and RUBY-FILL (Rubidium Rb82 generator) in mobile settings. This mobile capability opened up entirely new markets—smaller hospitals that couldn't justify a full-time cardiac PET program could now offer the service part-time.

The Radiopharmacies Division is the second largest radiopharmacy network in the US with 46 pharmacies distributing nuclear medicine products to the largest national Group Purchasing Organisations (GPOs), regional health systems, stand-alone imaging centres, cardiologists and hospitals. This business has over 30 years of experience in serving the US nuclear medicine community and its current geographical reach enables it to serve over four million patients yearly. The Radiopharmacies Division complements the company's niche radiopharmaceuticals business and provides it with direct access to hospital networks.

Allergy Immunotherapy: The Quiet Performer

While radiopharmaceuticals grab headlines, the allergy immunotherapy business quietly generates steady returns. Offering range of over 200 different allergenic extracts and standard allergy vaccine, this segment serves a growing market driven by increasing allergy prevalence. The business model is attractive: recurring revenue from patients needing regular treatments, high switching costs, and limited competition due to regulatory barriers.

CDMO Sterile Injectables: The Contract Manufacturing Opportunity

Jubilant Pharma Limited (JPL), a Company incorporated under the laws of Singapore and a wholly-owned subsidiary of Jubilant Pharmova Limited, is an integrated global pharmaceutical company engaged in manufacturing and supply of Radiopharmaceuticals with a network of 46 radio-pharmacies in the US, Allergy Immunotherapy, Contract Manufacturing of Sterile Injectables and Non-sterile products and Solid Dosage Formulations through five manufacturing facilities that cater to all the regulated market including USA, Europe and other geographies.

The CDMO business leverages Jubilant's FDA-approved facilities to manufacture products for other companies. In an era of drug shortages and supply chain concerns, having reliable contract manufacturing partners has become critical for pharma companies. Jubilant's track record of FDA compliance (recent Roorkee issues notwithstanding) and experience with complex sterile manufacturing makes them an attractive partner.

Contract Research & Development: The Innovation Engine

The drug discovery services segment faced significant headwinds. The biotech funding winter that began in 2022 hit this business hard, with revenues declining 14% year-over-year in FY24. But green shoots are emerging. Management noted in recent earnings calls that with gradual recovery in biotech funding, the segment is expected to perform well in 2025—a prediction already showing in H1 FY25 results where the drug discovery segment saw 21% year-over-year growth.

Generics: The Turnaround Story

The generics business represents both Jubilant's biggest challenge and potentially its greatest near-term opportunity. After the Roorkee facility received an import alert in July 2021, topline declined from ₹1,160 crore in FY22 to ₹775 crore in FY24. The facility received FDA clearance in April 2024, setting the stage for recovery. With the facility back online, management is focused on recapturing lost market share and launching delayed products.

Proprietary Novel Drugs: The Future Pipeline

The smallest but potentially most valuable segment focuses on developing novel therapies in oncology and autoimmune disorders. While not yet revenue-generating, this represents Jubilant's bet on moving from services and generics to innovation. Success here could transform valuations—novel drug companies trade at multiples far exceeding generic or service businesses.

The portfolio strategy makes sense when viewed holistically. Radiopharmaceuticals and allergy provide stable, high-margin cash flows. CDMO and drug discovery services offer growth tied to industry outsourcing trends. Generics, once stabilized, provide volume and scale. Novel drugs offer optionality on breakthrough innovation. It's a portfolio designed to deliver steady returns while maintaining upside potential—exactly what you'd expect from a company that spent four decades climbing from commodity chemicals to nuclear medicine.

VIII. Operational Challenges & Turnarounds (2021–Present)

The email from the FDA landed like a bombshell on July 15, 2021. After years of warnings and attempted remediations, the agency had placed Jubilant's Roorkee facility under import alert—the regulatory equivalent of a death sentence for U.S. market access. In the executive conference room, the mood was grim. This wasn't just about one facility; it was about credibility, investor confidence, and the harsh reality that even industry veterans could stumble on quality compliance.

Jubilant Pharmova Limited has announced that in response to the US FDA inspection conducted at its dosage formulations facility at Roorkee during March 2021, the agency has placed the facility under import alert. Earlier, the Roorkee facility received an OAI in December 2018 and then a Warning Letter in March 2019. The progression from Official Action Indicated (OAI) to Warning Letter to import alert represented a systematic failure to address FDA concerns—a failure that would cost the company dearly.

The products that get impacted due to the import alert contributed to less than 3% of FY21 total revenues for the company. Management's attempt to minimize the impact rang hollow. While 3% of revenue might seem manageable, the real damage was to growth trajectory. The generic business has faced significant challenges after its Roorkee facility received an import alert in Jul-21. As a result, its topline declined from ₹1,160 crore in FY22 to ₹775 crore in FY24—a 33% collapse that revealed how quickly regulatory issues could eviscerate a business.

The operational response was swift but painful. Resources were diverted from growth initiatives to remediation. Quality consultants were brought in at premium rates. Standard operating procedures were rewritten from scratch. Every batch record was scrutinized. The company implemented what it called a "quality transformation program," though skeptics noted this should have happened before, not after, the import alert.

Meanwhile, the ripple effects spread beyond Roorkee. Customer confidence eroded. New product launches were delayed. Competitors swooped in to capture market share. The drug discovery business, already struggling, faced additional headwinds as the biotech funding winter coincided with Jubilant's regulatory troubles. Jubilant's drug discovery business faced challenges over the past two years due to the biotech funding winter in the U.S., resulting in a 14% YoY decline in FY24 topline.

The turning point came slowly. The United States Food and Drug Administration (USFDA) inspected JGLs solid dosage manufacturing facility at Roorkee in India from 25 January to 2 February 2024. Based on this inspection and the USFDA VAI classification, the facility is considered to be in acceptable state of compliance with regard to current good manufacturing practices (cGMP). With this, the FDA has concluded that this inspection is closed.

Jubilant Pharmova's shares reached a 52-week high of 699.15 in early trading on April 18, following the US Food and Drug Administration (US FDA) designation of the company's arm as "voluntary action indicated" (VAI). The market's euphoric reaction to the VAI classification revealed just how heavily the Roorkee overhang had weighed on valuations.

But receiving FDA clearance was just the beginning of the turnaround journey. The company had to rebuild customer relationships, re-establish supply chains, and recapture lost market share. Further, the company expects the exports from the Roorkee facility to the US market to increase in a meaningful and gradual manner. As of now the facility, was exporting only one product, Risperidone to the US market.

The broader strategic pivot was even more dramatic. Over the last few years the US Generics market has been witnessing significant pricing pressure leading to significant losses at Jubilant Cadista since FY2022 onwards. In order to move the US generics business to profitability, the company decided to change the operating model from in-house manufacturing to outsourced manufacturing by selected USFDA approved CMOs for the US market. This wasn't just closing a facility; it was acknowledging that the generics game had changed and Jubilant needed to adapt or exit.

The drug discovery turnaround showed more promise. With a gradual recovery in biotech funding, the segment is expected to perform well in 2025. This is already reflected in the H1 FY25 results, where the drug discovery segment saw a 21% YoY growth. After two years of decline, the business was finally showing signs of life, helped by both market recovery and internal improvements.

The lessons from this period were expensive but valuable. Quality systems aren't just compliance checkboxes; they're the foundation of pharmaceutical operations. Market position can evaporate faster than it's built. And sometimes, the best strategic move is acknowledging when a business model no longer works and having the courage to change it. As 2024 progressed, Jubilant emerged from its operational nadir leaner, more focused, and with hard-won insights about what it takes to compete in global pharmaceutical markets.

IX. Financial Performance & Market Position

The numbers tell a story of transformation, struggle, and resilience. Revenue: 7,404 Cr, Profit: 457 Cr—figures that place Jubilant Pharmova firmly in mid-cap pharmaceutical territory with a Mkt Cap: 16,714 Crore. But beneath these headline numbers lies a more complex narrative of a company navigating operational headwinds while trying to convince markets of its underlying value.

The financial trajectory reveals the scars of recent battles. The company has delivered a poor sales growth of 3.90% over past five years. Company has a low return on equity of 1.36% over last 3 years. These metrics would make any growth investor wince. Yet context matters: this period encompassed the Roorkee facility crisis, the biotech funding winter, and a painful generics market collapse. The question isn't why returns were poor, but how the company survived at all.

The balance sheet transformation tells a more encouraging story. Company has reduced debt. Company's working capital requirements have reduced from 43.0 days to 16.3 days. This dramatic improvement in working capital efficiency—from 43 days to just 16—reveals operational tightening that often precedes financial recovery. Management wasn't just firefighting regulatory issues; they were fundamentally restructuring how the business operates.

The Q1 FY25 results marked an inflection point. Jubilant Pharmova jumped 3.31% to Rs 764.25 after the company's consolidated net profit stood at Rs 482.10 crore in Q1 FY25, steeply higher than Rs 6.40 crore in Q1 FY24. Total income increased by 9.41% to Rs 1,745.7 crore in Q1 FY25 as compared with Rs 1,595.5 crore posted in corresponding quarter last year. The profit explosion—from ₹6.4 crore to ₹482 crore—wasn't operational but included one-time gains from stake sales. Still, the underlying revenue growth and margin expansion were real.

EBITDA jumped 50% to Rs 266 crore as compared to Rs 177 crore during the corresponding period of previous year. EBITDA margin increased to 15.2% in Q1 FY25 as against 11.1% in Q1 FY24. A 410 basis point margin expansion in one year doesn't happen by accident. It reflects the cumulative impact of closing loss-making facilities, improving product mix, and the radiopharmacy business finally achieving scale.

The debt reduction story deserves special attention. Meanwhile, in June 2024, the consequent to the receipt of stake sale proceeds in Sofie Biosciences, totaling up to $115.9 million, the company made a voluntary debt repayment of $75 million, equivalent to Rs 626 crore. Correspondingly, net debt dropped to Rs 1,869 crore from Rs 2,509 crore as on March24. Net debt or EBITDA also improved to 1.7x from 2.5x as on March24. This leverage reduction from 2.5x to 1.7x EBITDA moves Jubilant from stressed to comfortable territory.

The competitive positioning varies dramatically by segment. In radiopharmaceuticals, The company is the #3 radiopharmaceutical manufacturer in the US and has the #2 network in the US with 46 radiopharmacies. This dominant position translates to pricing power and stable margins. But in generics, they're a small player in a brutally competitive market where scale matters and Jubilant lacks it.

The valuation metrics present a puzzle. Stock is trading at 2.67 times its book value, while The price to earnings (P/E) ratio, at the current price of Rs 851.9, stands at 25.9 times its trailing twelve months earnings. The price to book value (P/BV) ratio at current price levels stands at 2.5 times, while the price to sales ratio stands at 2.0 times. These multiples suggest the market is pricing in recovery but remains skeptical about sustained growth.

Capital allocation priorities have shifted dramatically. Further, the company said that its wholly owned subsidiary, Jubilant Draximage announced an investment of $ 50 million to expand its PET radiopharmacy network by adding six PET radiopharmacies in strategic locations throughout the United States. The said investment shall position the company in the growing PET Imaging segment and shall also enable it to secure long term contracts with the leading PET radiopharmaceutical manufacturers. The new PET radiopharmacies shall be fully operational in FY28. This $50 million investment in PET radiopharmacies represents a doubling down on their strongest business.

The cash flow picture has improved markedly. JUBILANT PHARMOVA 's cash flow from operating activities (CFO) during FY24 stood at Rs 10 billion, an improvement of 47.0% on a YoY basis. Overall, net cash flows for the company during FY24 stood at Rs -575 million from the Rs 301 million net cash flows seen during FY23. Operating cash flow improvement of 47% year-over-year signals the business is generating real cash, not just accounting profits.

The market position summary: Jubilant is a tale of two companies. In radiopharmaceuticals and specialty segments, it's a dominant player with moats and pricing power. In generics and drug discovery, it's subscale and struggling. The financial performance reflects this duality—strong cash generation from core businesses funding turnarounds in challenged segments. Whether this strategy succeeds depends on execution in the next 12-24 months as Roorkee ramps up and biotech funding recovers.

X. Playbook: Business & Investing Lessons

The conference room at Harvard Business School, 2019. A case study discussion on Indian pharmaceutical companies. When Jubilant's name comes up, a student asks: "Why would anyone build six different businesses under one roof?" The professor's response: "Sometimes the best strategies emerge not from planning but from opportunistic evolution. Jubilant didn't set out to become a six-headed hydra. They followed value wherever it led." That observation captures both the genius and the challenge of the Jubilant model.

The Power of Finding and Dominating Niches

Jubilant's radiopharmaceutical dominance didn't happen by accident. While competitors chased blockbuster generics with billion-dollar market opportunities, Jubilant identified a $500 million niche that everyone else ignored. The lesson: In pharmaceuticals, a dominant position in a small market often beats being the tenth player in a large one. Their 46 radiopharmacies don't just distribute products; they create switching costs so high that hospitals would rather complain about pricing than change suppliers.

The niche strategy extends beyond radiopharmaceuticals. In allergy immunotherapy, they offer over 200 different extracts—not because each generates significant revenue, but because completeness matters to allergists. One missing extract could lose an entire account. It's the pharmaceutical equivalent of Amazon's "everything store" strategy, applied to a tiny corner of medicine.

Managing Complexity: Six Businesses Under One Roof

Running six distinct businesses would break most management teams. Jubilant makes it work through radical decentralization. Each business has its own P&L, its own leadership, its own strategy. The corporate center provides capital allocation and regulatory expertise but doesn't pretend to understand the nuances of radiopharmacy logistics or biotech research partnerships. The lesson: Complexity is manageable if you resist the urge to over-centralize.

The flip side of this complexity is resilience. When the Roorkee facility faced FDA issues, the radiopharmacy business kept generating cash. When biotech funding dried up, the allergy business provided stability. This portfolio approach—unfashionable in an era of "pure plays"—provided survival optionality that focused competitors lacked.

The Demerger Decision: When to Split for Focus

The 2021 demerger offers a masterclass in strategic clarity. The decision wasn't driven by crisis but by recognition that chemical and pharmaceutical businesses attract different investors, require different capabilities, and operate on different timescales. The courage to split a successful conglomerate—essentially admitting that synergies had become dissynergies—is rare in family-controlled businesses where size often equals prestige.

Post-demerger performance validated the strategy. Both entities saw valuation re-ratings as investors could finally understand what they were buying. The lesson: Sometimes the best way to create value is to make it visible by simplifying the story.

Navigating FDA Regulations and Quality Issues

Jubilant's Roorkee saga offers harsh lessons in pharmaceutical quality. First, warning letters are aptly named—ignore them at your peril. Second, FDA remediation isn't just about fixing problems; it's about changing culture. Third, the cost of quality failures extends far beyond lost sales—it includes customer relationships that take years to rebuild.

But there's a contrarian lesson too. FDA troubles that don't involve data integrity can be overcome. Jubilant's eventual clearance and return to market demonstrates that regulatory setbacks, while painful, needn't be terminal. The key is transparency with regulators, systematic remediation, and patience—lots of patience.

Building in Emerging Markets vs Acquiring in Developed Markets

Jubilant's growth strategy reveals sophisticated market understanding. In India, they built organically—leveraging low costs and local knowledge. In the US, they acquired—buying market access and regulatory approvals that would take decades to build. This hybrid approach maximizes capital efficiency while minimizing execution risk.

The Triad acquisition exemplifies this philosophy. Instead of trying to build a US radiopharmacy network from scratch—facing regulatory hurdles, hiring challenges, and customer acquisition costs—they paid $250 million for an established player. Expensive? Yes. But cheaper than a decade of organic building with uncertain outcomes.

The Importance of Patient Capital in Pharmaceuticals

The Bhartia family's control provided something public markets rarely offer: patience. Building pharmaceutical capabilities takes decades. FDA approvals take years. Customer relationships take time. Market investors wanting quarterly growth would have forced short-term decisions that destroyed long-term value. Family control, despite its governance challenges, enabled Jubilant to play long games in an industry where short-term thinking is often fatal.

Family-Run Businesses and Professional Management Balance

Jubilant navigates the family business paradox skillfully. The Bhartias provide vision and patient capital but have progressively professionalized operations. Key positions are held by industry veterans, not family members. Board committees have independent directors with real power. The result: family control with professional execution—getting the benefits of both models while minimizing their weaknesses.

The deeper lesson: In pharmaceuticals, where technical expertise matters more than relationships, family businesses must professionalize or perish. Jubilant's willingness to hire expensive external talent, even when it diluted family influence, enabled their transformation from chemical traders to pharmaceutical manufacturers. The family that insists on running everything directly rarely builds anything worth running.

XI. Bear vs. Bull Case

The investment committee meeting at a Mumbai mutual fund, present day. The analyst presenting Jubilant Pharmova pauses before her final slide. "This is either a massive turnaround story or a value trap," she says. "The bulls see a radiopharmaceutical giant trading at generic multiples. The bears see a confused conglomerate with execution issues. Both might be right."

Bull Case: The Nuclear Medicine Thesis

The demographic math is undeniable. America is aging, cancer incidence is rising, and cardiac disease remains the leading killer. Each trend drives demand for nuclear medicine imaging. Jubilant's 46 radiopharmacies are perfectly positioned to capture this secular growth. With PET scanning becoming standard of care and new radiopharmaceuticals entering the market, the company's infrastructure becomes increasingly valuable.

The radiopharmaceutical market structure is the bull's dream. High barriers to entry—nuclear licenses, specialized facilities, trained personnel—limit competition. Customer switching costs are enormous; hospitals won't change radiopharmacy providers to save 5% when patient care depends on reliable daily delivery. The result: stable market share, predictable revenues, and expanding margins as volumes grow.

Successful turnaround of generics and drug discovery segments could provide dramatic upside. The Roorkee facility's FDA clearance in April 2024 removes a major overhang. With the facility back online and new products launching, the generics business could return to its ₹1,160 crore peak revenue. Meanwhile, recovering biotech funding is already driving drug discovery growth—21% year-over-year in H1 FY25. If both segments achieve management targets, earnings could double within two years.

Operational improvements are already flowing through. Working capital reduction from 43 days to 16 days has freed up hundreds of crores in cash. Debt reduction to 1.7x EBITDA provides financial flexibility for growth investments. The closure of the loss-making Salisbury facility eliminates a persistent drag on profitability. These aren't promises; they're completed actions with measurable impact.

Strong market position in radiopharmaceuticals provides competitive moat. As the #3 manufacturer and #2 network operator in the US, Jubilant has scale advantages smaller players can't match. Their ability to sign exclusive distribution agreements with manufacturers and secure long-term hospital contracts creates a virtuous cycle—more products attract more customers, which attracts more products.

Bear Case: The Execution Skeptic's View

Regulatory risks and FDA compliance history flash red warnings. The Roorkee facility's journey from OAI to Warning Letter to Import Alert reveals systemic quality issues, not isolated incidents. Even after clearance, the facility received four observations in its latest inspection. History suggests this isn't over—FDA issues tend to recur, and the next warning letter could be catastrophic.

Intense competition in generics makes recovery unlikely. The US generic market has structurally changed. Consolidated buyers, increased FDA approvals, and Indian competition have permanently compressed margins. Jubilant's subscale position—less than 1% market share—means they're price takers in a market where only scale players survive. The Salisbury closure admission of defeat suggests management knows this but won't admit it publicly.

Poor sales growth of 3.90% over past five years. Low return on equity of 1.36% over last 3 years. These aren't temporary setbacks but persistent underperformance. Five years is long enough to execute a turnaround, yet sales growth barely exceeded inflation. Return on equity below cost of capital destroys value, not creates it. Past performance suggests execution capability doesn't match strategic ambition.

Complex business model with varying margins creates management challenges. Running six businesses means six different competitive dynamics, regulatory requirements, and capital needs. Management attention is finite—focus on radiopharmaceuticals means neglecting generics, fixing drug discovery means ignoring CDMO opportunities. The complexity tax is real and compounds over time.

Dependence on US market creates concentration risk. Over 70% of revenues come from the United States, exposing Jubilant to regulatory changes, healthcare reform, and dollar fluctuations. A single policy change—like Medicare reimbursement cuts for nuclear imaging—could devastate profitability. Geographic concentration in the world's most litigious market adds legal risk to operational challenges.

The Valuation Debate

Bulls argue the sum-of-parts value far exceeds market capitalization. Value the radiopharmaceutical business at specialized pharmaceutical multiples (15-20x EBITDA), not generic multiples (8-10x). Add the allergy business at steady-state multiples, assign option value to drug discovery, and the stock could double. The market is pricing Jubilant like a troubled generic company when it's really a specialized pharmaceutical leader.

Bears counter that complexity deserves a conglomerate discount. Six subscale businesses are worth less than one focused leader. The market correctly recognizes that management can't optimize all segments simultaneously. Until Jubilant simplifies—selling non-core assets or achieving clear market leadership—it deserves to trade at discounted multiples.

The critical variables for resolution: FDA inspection outcomes over the next 12 months, radiopharmaceutical market growth rates, success of the $50 million PET expansion, and generic product launch trajectory. If Jubilant executes on even half its initiatives, bulls win. If operational challenges persist, bears feast. The binary nature of the outcome makes this a high-conviction bet either way—exactly the kind of situation that creates opportunity for investors willing to do the work and take a stand.

XII. Future Outlook & Strategic Priorities

The strategy offsite at Jubilant's Noida headquarters, early 2025. The leadership team stares at a simple slide: "Where will growth come from?" The answer isn't in new businesses or transformative acquisitions. It's in executing what they already have, particularly in the high-growth nuclear medicine market where demographics and technology converge to create a generational opportunity.

Growth Drivers: Radiopharmaceuticals Expansion

The $50 million PET expansion announced in 2024 represents just the beginning. Jubilant Draximage announced an investment of $ 50 million to expand its PET radiopharmacy network by adding six PET radiopharmacies in strategic locations throughout the United States. The said investment shall position the company in the growing PET Imaging segment and shall also enable it to secure long term contracts with the leading PET radiopharmaceutical manufacturers. The new PET radiopharmacies shall be fully operational in FY28. These aren't just distribution points; they're strategic nodes in an emerging ecosystem where PET imaging replaces traditional modalities.

The real opportunity lies in theranostics—using the same molecular targeting for both diagnosis and treatment. Imagine detecting prostate cancer with a radioactive tracer, then treating it with a therapeutic dose of the same molecule. Jubilant's radiopharmacy network positions them perfectly for this revolution. They already have the infrastructure, regulatory approvals, and customer relationships. As new theranostic agents gain FDA approval, Jubilant becomes the natural distribution partner.

Recovery Catalysts in Challenged Segments

With a gradual recovery in biotech funding, the segment is expected to perform well in 2025. This is already reflected in the H1 FY25 results, where the drug discovery segment saw a 21% YoY growth. The biotech funding winter is thawing. AI-driven drug discovery is attracting capital again. Jubilant's established capabilities in computational chemistry and biologics position them well for this recovery. The question isn't if the business recovers, but how fast.

The generics turnaround depends on product selection, not volume. With Roorkee back online, management is focusing on complex generics with limited competition rather than commodity products. Six to eight launches per year might seem modest, but if chosen correctly—targeting products with three or fewer competitors—margins can exceed 40%. It's a rifle shot strategy replacing the previous shotgun approach.

Theranostics and Precision Medicine Opportunities

The convergence of diagnostics and therapeutics represents a $10 billion opportunity by 2030. Jubilant's unique position—manufacturing capabilities plus distribution network—makes them an ideal partner for innovator companies developing novel radiopharmaceuticals. They don't need to discover the next breakthrough; they just need to be the preferred channel for bringing it to market.

Consider the Lutathera model. This radioligand therapy for neuroendocrine tumors requires specialized handling, patient scheduling, and injection protocols. Jubilant's radiopharmacies already manage this complexity. As more radioligand therapies gain approval—for prostate cancer, breast cancer, brain tumors—Jubilant's infrastructure becomes increasingly valuable. They're selling picks and shovels in a gold rush.

Geographic Expansion Plans

While US dominance provides stability, geographic concentration creates risk. Management is exploring selective international expansion, but not through the traditional emerging markets playbook. Instead, they're targeting developed markets with established nuclear medicine infrastructure—Germany, Japan, Australia. These markets offer attractive pricing, stable regulations, and aging populations without the cutthroat competition of the US generic market.

The approach is partnerships, not acquisition. Joint ventures with local radiopharmacy operators, leveraging Jubilant's operational expertise and product portfolio. It's capital-light expansion that minimizes execution risk while providing optionality on international growth.

M&A Possibilities and Capital Deployment

With net debt down to 1.7x EBITDA and operational cash flow improving, Jubilant has firepower for strategic acquisitions. But management's comments suggest discipline. They're not looking for transformative deals but tactical additions—a specialized radiopharmacy in an underserved market, a complementary product portfolio, or manufacturing capabilities for emerging isotopes.

The more likely capital deployment is organic expansion. Building new radiopharmacies, upgrading existing facilities for handling alpha-emitting isotopes, and investing in cold chain logistics for temperature-sensitive radiopharmaceuticals. These investments offer 20%+ returns with minimal execution risk—far better than the integration challenges of major acquisitions.

Strategic Priorities for Sustainable Growth

First, protect and expand the radiopharmaceutical moat. Every competitor entering the space validates the opportunity while making Jubilant's established position more valuable. The priority is maintaining service levels, securing exclusive distribution agreements, and investing ahead of demand to prevent capacity constraints.

Second, achieve profitability in generics or exit. The halfway house of subscale participation destroys value. Either commit resources to achieve meaningful scale or divest to someone who can. Management's shift to outsourced manufacturing suggests they understand this, but execution remains uncertain.

Third, prepare for the next technological shift. Quantum computing could revolutionize drug discovery. Cell and gene therapies might obsolete traditional pharmaceuticals. AI could automate radiopharmacy operations. Jubilant needs to invest in capabilities for tomorrow while maximizing today's opportunities.

The path forward is clear: double down on radiopharmaceuticals, fix or exit subscale businesses, and maintain financial flexibility for emerging opportunities. It's not a glamorous strategy, but in pharmaceuticals, execution beats vision every time. Jubilant has spent four decades building capabilities and surviving crises. The next decade will determine whether they transform from a resilient survivor into a dominant specialist. The pieces are in place; now it's about putting them together.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube