Waaree Energies: India's Solar Champion Takes on China

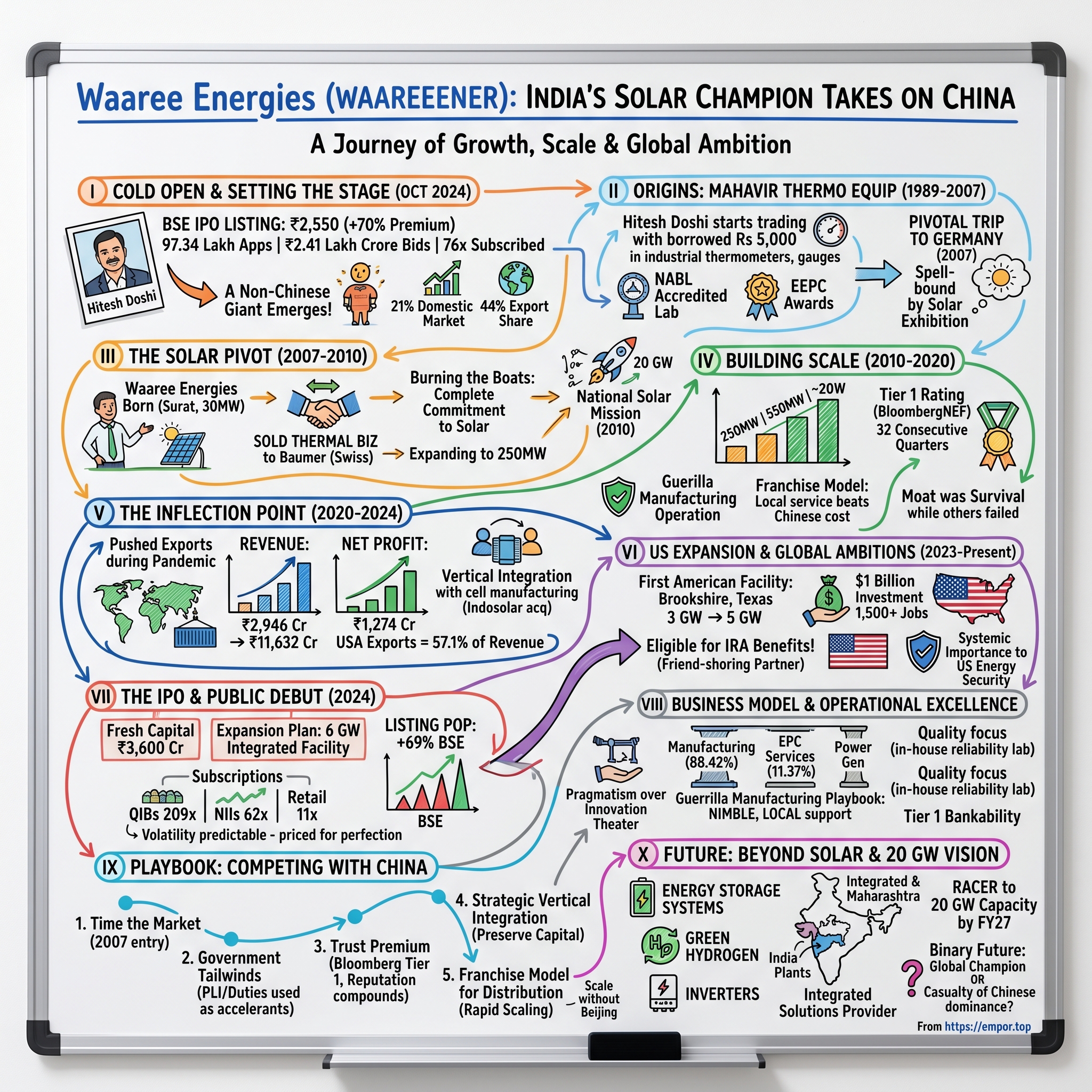

I. Cold Open & Setting the Stage

The trading floor at the Bombay Stock Exchange erupted at 10:16 AM on October 28, 2024. After weeks of unprecedented subscription frenzy, Waaree Energies—a name most Indians couldn't pronounce correctly six months earlier—opened for trading at ₹2,550, a staggering 70% premium over its issue price. In the VIP gallery, Hitesh Doshi, the company's 61-year-old founder, watched as his three-decade journey from trading thermal equipment in Gujarat's industrial corridors to building India's largest solar manufacturer reached its most public milestone yet.

The numbers defied belief: 97.34 lakh applications, ₹2.41 lakh crore in bids for a ₹4,321 crore offering—making it India's most subscribed IPO by application count in history. The retail portion was oversubscribed 10.79 times, non-institutional investors bid 62.49 times, and qualified institutional buyers—the smart money that supposedly knows better—threw in bids worth 208.63 times the allocation. For context, even Hyundai's blockbuster IPO just weeks earlier had managed "only" 2.37 times subscription.

But here's what makes this story remarkable: In an industry where China controls over 80% of global solar manufacturing, where Chinese companies benefit from decades of state support and economies of scale that should be insurmountable, a Gujarati trader-turned-manufacturer had somehow carved out not just survival, but dominance in one of the world's fastest-growing solar markets. Waaree commands 21% of India's domestic solar module market and an astounding 44% share of the country's solar module exports. The question reverberating through dalals and institutional investors alike: How did a thermal equipment trader from Surat build one of the few non-Chinese solar manufacturing giants? And perhaps more importantly, in a world where Beijing's solar dominance seems absolute, what does Waaree's ascent tell us about the future of global energy supply chains?

To understand this, we need to rewind three decades—to a very different India, where solar panels were science fiction and industrial thermometers were the height of technology ambition.

So what for investors: Waaree's listing premium of 70% on BSE at ₹2,550 and 66.33% on NSE suggests the market is pricing in significant execution risk but also massive opportunity. The key question: Is this another infrastructure bubble riding government subsidies, or the beginning of India's answer to China's solar dominance?

II. Origins: The Doshi Family & The Trading Years (1989-2007)

The year was 1989. The Berlin Wall was falling, India's economy was still two years away from liberalization, and in the industrial heartland of Gujarat, a young entrepreneur named Hitesh Chimanlal Doshi was starting what seemed like an unremarkable trading business. Mahavir Thermo Equip, as he called it, dealt in the unglamorous world of temperature gauges, pressure instruments, and industrial thermometers—the kind of equipment that kept factories running but never made headlines. But here's what the trading business masked: Doshi was born on Feb 22, 1967, in a small village, Tunki, in Maharashtra, where he grew up in an economic and resource-poor family. His father ran a modest grocery store and the village had limited amenities—electricity and telephones were rare luxuries. Education beyond the 7th standard required him to travel daily to a neighboring village by bicycle. This was a man who understood scarcity at a visceral level—and perhaps more importantly, understood the value of timing and technology transitions.

The early years of Waaree (the name comes from the Wari temple in Doshi's village) were defined by methodical, almost boring, execution. Launching Mahavir Thermo Equip with a borrowed capital of Rs 5,000, Hitesh began trading temperature and pressure gauges. By 1996, he'd moved from pure trading to manufacturing—a classic Indian business evolution. The company started producing its own temperature gauges, securing partnerships with international brands like Dwyer Instruments (USA), Keller (Switzerland), Inor (Sweden), and Nuovafima (Italy).

What separated Doshi from thousands of other Gujarati traders was his obsession with quality certification. In 2003, Waaree Instruments became India's first NABL (National Accreditation Board for Testing and Calibration Laboratories) accredited testing lab in its category. It's a detail that seems minor but would prove prophetic—this was a businessman who understood that to compete globally, Indian manufacturing needed to match international standards from day one. By the mid-2000s, Waaree Instruments had built something rare in Indian manufacturing: a profitable, export-oriented business with genuine technical capabilities. The company was exporting to the US and Canada, winning EEPC (Engineering Export Promotion Council) India awards, and generating steady cash flow. By 2007, Hitesh's business was exporting to the US and Canada, and seeing success in the thermal equipment market.

But then came the moment that would change everything. In 2007, during what should have been a routine business trip to Germany, Doshi attended a solar exhibition. "During a trip to Germany, I went to a solar exhibition and was spell-bound. I talked to people there to understand how solar energy worked, and it convinced me that it would be the next step not only for expanding the business but also developing India's solar manufacturing sector," he would later recall.

This wasn't just enthusiasm—it was recognition. Solar in 2007 was where computing had been in the 1980s: expensive, inefficient by today's standards, but clearly the future. Global solar installations were just 2.8 GW that year. China hadn't yet emerged as the dominant force. The game was still open.

The decision that followed was both radical and calculated. By 2010, Hitesh sold the thermal equipment company - Waaree Instruments - to the Swiss brand Baumer. The same year, he also expanded Waaree Energies' module manufacturing facility to 250MW. November 7, 2010 - Baumer Group acquired the majority of Waaree Instruments Ltd., one of India's leading suppliers of process control instruments. Financial terms weren't disclosed, but for Doshi, the sale represented more than just capital—it was burning the boats, a complete commitment to solar.

The Waaree Instruments sale to Baumer was masterfully timed. The Swiss company got an established Indian player with more than 500 well experienced employees and state-of-the-art manufacturing facilities. Doshi got capital, but more importantly, he got freedom to pursue what he saw as a generational opportunity in renewable energy.

So what for investors: The Waaree origin story reveals a critical pattern—this wasn't a momentum trader jumping on the solar bandwagon, but a methodical manufacturer who understood quality systems, international partnerships, and most importantly, when to pivot entirely. The sale of a profitable business to fund an unproven venture shows both conviction and timing that would define Waaree's next phase.

III. The Solar Pivot: Seeing the Light (2007-2010)

In 2007, Waaree Energies was born with a module manufacturing facility of 30MW in Surat. To understand how audacious this was, consider the context: India's total solar installations in 2007 were negligible. The National Solar Mission wouldn't launch until 2010. Chinese manufacturers hadn't yet achieved their crushing cost advantages. And here was a thermal equipment trader from Gujarat betting everything on photovoltaics.

The initial facility in Surat was modest—30 MW annual capacity when global leaders like First Solar were already approaching gigawatt scale. But Doshi's approach was distinctly different from the venture capital-funded solar startups proliferating in Silicon Valley at the time. This was bootstrapped, profitable from near day one, and focused obsessively on one thing: manufacturing excellence at Indian cost structures. The numbers tell the story: India had an installed solar capacity of 161 MW on 31 March 2010, about 2 and half months after the mission was launched on 11 January. When the Jawaharlal Nehru National Solar Mission by former Prime Minister Manmohan Singh on 11 January 2010 with a target of 20 GW by 2022, The Central Electricity Regulatory Commission (CERC) had approved a tariff of around Rs 17 for a unit of solar power. The cost of electricity from a new thermal plant was about Rs 4 per unit.

This was the market Doshi entered—where solar electricity cost more than four times conventional power, where government subsidies were uncertain, and where Chinese manufacturers were just beginning their relentless march toward market domination.

What Waaree did differently was focus not on the sexy, venture-fundable parts of solar (inverters, tracking systems, novel cell technologies) but on the boring, capital-intensive core: module manufacturing at scale. By 2010, the company had already expanded from 30 MW to 250 MW capacity—a nearly 10x growth in three years while most Indian companies were still debating whether to enter the sector.

The timing of selling Waaree Instruments becomes even more strategic in retrospect. Baumer Group acquired the majority of Waaree Instruments Ltd., one of India's leading suppliers of process control instruments in November 2010, giving Doshi capital just as the National Solar Mission was creating India's first real solar market. The company he'd built over two decades, with more than 500 well experienced employees, was sold to fund a bet on an industry that barely existed in India.

But Doshi saw what others missed. The solar industry in 2007-2010 wasn't about technology breakthroughs—crystalline silicon had been around since the 1950s. It was about manufacturing scale, supply chain optimization, and most critically, being ready when the market inflected. The real cause of solar power becoming so cheap has been the incredible success of China in lowering the costs of production. The Chinese dominate the global market. Our solar projects have been using panels imported from China.

Rather than fight this reality, Waaree embraced it. The company would import cells from China but add value through module assembly, quality control, and crucially, local availability and service—things Chinese manufacturers couldn't provide from thousands of miles away.

So what for investors: The 2007-2010 period reveals Waaree's core insight: in commodity manufacturing, timing and scale matter more than technology. While others waited for solar to become economical, Waaree built capacity assuming costs would fall—a bet that required deep conviction about the learning curve in solar manufacturing that would prove prescient.

IV. Building Scale: The Manufacturing Marathon (2010-2020)

The decade from 2010 to 2020 would separate the dreamers from the builders in Indian solar. It began with euphoria—the National Solar Mission had launched, global solar installations were exploding, and everyone from Tata to Reliance was announcing grand solar plans. It ended with a graveyard of abandoned factories and broken ambitions, with most Indian manufacturers either bankrupt or pivoted to other businesses. Everyone, that is, except Waaree.

The numbers tell a story of relentless, almost stubborn, capacity expansion: 250 MW in 2010, 550 MW by 2015-2016, and steadily approaching 2 GW by decade's end. But these numbers hide the brutal reality of what Waaree was up against. Chinese manufacturers, backed by provincial governments and state banks, were adding gigawatts of capacity annually. They had achieved economies of scale that should have been insurmountable—producing at costs Indian manufacturers couldn't match even for raw materials. Consider the headwinds: China alone produces at least 80% of the main components of PVs, with its average share of the solar panel supply chain going from 55% in 2010 to 84% by 2022. The China Development Bank provided $20 billion of financing to domestic solar manufacturers in 2010. A module made in China is 50% cheaper than that produced in Europe and 65% cheaper than the US.

Yet Waaree persisted. The company's strategy during this decade wasn't to compete head-on with China on cost—that would have been suicide. Instead, Waaree built what can only be described as a guerrilla manufacturing operation: staying nimble, focusing on niches Chinese giants ignored, and most importantly, building deep relationships with Indian project developers who valued local service and support over the absolute lowest price.

The franchise model Waaree developed during this period was particularly clever. Rather than building expensive retail infrastructure, the company created a network of franchisees across India—local entrepreneurs who understood their markets and could provide the last-mile service that Chinese manufacturers, despite their cost advantages, couldn't match. By 2020, this network had grown to hundreds of touchpoints across the country.

But the real achievement of this decade was something less visible: engineering excellence. Waaree became the only company with NABL accredited in-house reliability lab for 3X IEC extended testing. While Chinese manufacturers were racing to the bottom on price, Waaree was quietly building testing capabilities that would prove critical when customers started caring about quality and longevity, not just upfront cost.

The company also achieved something remarkable: Tier 1 rating by BloombergNEF for 32 consecutive quarters. This wasn't just a badge—it was validation from the global financial community that Waaree modules were bankable, that international project developers could trust them for 25-year investments. For context, maintaining Tier 1 status requires consistent delivery, financial stability, and proven field performance. Many larger companies have lost this rating; Waaree never did.

The financial performance during this period tells a story of patient capital and deferred gratification. Margins were thin, growth was steady but not spectacular, and the company repeatedly chose scale over profitability. While competitors either exited the market or retreated to niche segments, Waaree kept expanding capacity, betting that someday—somehow—the market would turn in favor of non-Chinese manufacturers.

That day seemed impossibly far away in 2015 when module prices hit new lows and even established Western manufacturers like SunEdison were heading toward bankruptcy. SunEdison of Belmont, Calif., filed for bankruptcy in April. The stocks of two other leading companies, First Solar and SunPower, were in the triple digits a decade ago. Now they are treading water, floating between 13 and 6 percent of their former values.

So what for investors: The 2010-2020 decade reveals Waaree's true moat wasn't technology or cost—it was survival. While competitors abandoned solar manufacturing, Waaree accumulated a decade of operational knowledge, customer relationships, and most critically, production capacity ready for when the geopolitical winds shifted. This patient approach to capacity building during the darkest days of solar manufacturing would prove prescient.

V. The Inflection Point: Scale, Vertical Integration & Market Leadership (2020-2024)

March 2020. The world locked down. Global supply chains froze. Solar installations ground to a halt. For most manufacturers, COVID-19 was a catastrophe. For Waaree, it was the moment everything changed.

"Pushed exports in US market and identified new supply channels during pandemic"—this understated line from company documents masks one of the most aggressive pivots in Indian manufacturing history. While competitors retreated, Waaree's team worked around the clock to establish new supply routes, secure shipping containers when they cost 10x normal rates, and most critically, position themselves as the reliable non-Chinese alternative just as the world was waking up to supply chain vulnerabilities.

The numbers from this period are staggering: Revenue surging from ₹2,945.85 crores in FY22 to ₹11,632.76 crores in FY24, marking a nearly fourfold increase over three years. The company's net profit trajectory is even more impressive, soaring from ₹79.65 crores in FY22 to ₹1,274.38 crores in FY24—a 14-fold rise.

But revenue growth alone doesn't capture the transformation. The real story was vertical integration at breakneck speed. In 2021, Waaree had 2 GW of module capacity. By June 2024, that had exploded to 12 GW, with an additional 1.3 GW at Noida through the acquisition of Indosolar Limited. This wasn't just expansion—it was a complete reimagining of what an Indian solar manufacturer could be. The Indosolar acquisition deserves special attention. On April 21st, 2022, the National Company Law Tribunal Delhi Bench (NCLT), approved the resolution plan it submitted towards the acquisition of Indosolar Limited. This wasn't just buying capacity—it was acquiring cell manufacturing capabilities, moving Waaree up the value chain. The deal expanded Waaree's planned PV cell production capacity from 4 GW to 5.4 GW, while complementing its module manufacturing—a critical step toward reducing dependence on Chinese cell imports.

But the real masterstroke was the U.S. expansion. The company aims to expand its presence in overseas markets by setting up a 3 GW manufacturing facility in the United States. At a time when the Inflation Reduction Act was reshaping global solar supply chains, when the U.S. was desperately seeking non-Chinese suppliers, Waaree positioned itself as the answer. For the financial year ended March 31, 2024, Waaree Energies reported a 154.73% year-on-year (YoY) rise in net profit to ₹1,274 crore. The company's total consolidated revenue for the fiscal jumped 69% YoY to ₹11,632 crore.

The export numbers tell the story: In FY24, export sales accounted for 57.6% of the total revenue, out of which 57.1% was from the USA. Waaree had quietly become America's backdoor to solar independence—an Indian company that could provide the volumes, quality, and most importantly, the non-Chinese origin certificates that U.S. project developers desperately needed.

By 2024, Waaree's transformation was complete: It has a market share of 21 per cent in India and a healthy 44 per cent share in exports of solar modules from India. The company that started with a 30 MW facility in 2007 now commanded nearly half of India's solar exports. The franchisee network had grown to 369 outlets. The order book stood at 16.66 GW—more than the entire installed solar capacity of many countries.

The financial metrics from this period are staggering: In FY24, Waaree Energies maintained a strong net profit margin of 10.96%. Despite a significant expansion of its equity base, the company achieved a robust Return on Equity (ROE) of 30.26% in FY24, surpassing the previous year's figure. These aren't the numbers of a commodity manufacturer grinding out thin margins—they're the metrics of a company that had found pricing power through strategic positioning.

So what for investors: The 2020-2024 transformation reveals the power of optionality in manufacturing. By building capacity ahead of demand and positioning for geopolitical shifts (U.S.-China tensions, India's PLI schemes, global supply chain diversification), Waaree captured value that pure-play Chinese manufacturers couldn't. The 14x profit growth wasn't luck—it was preparation meeting opportunity.

VI. The US Expansion & Global Ambitions (2023-Present)

Brookshire, Texas, 30 miles west of Houston. In what was once cattle country, bulldozers are clearing ground for what might be the most important factory in the U.S. solar industry's attempt to break free from Chinese dominance. Waaree's first American facility, with 3 GW initial capacity and plans for $1 billion investment to scale to 5 GW by 2027, represents something unprecedented: an Indian company becoming America's answer to energy independence.

The timing was surgical. The Inflation Reduction Act had just unleashed the largest clean energy subsidy program in American history. The U.S. was desperate for non-Chinese solar suppliers but faced a problem: building solar manufacturing from scratch would take years America didn't have. Enter Waaree—battle-tested from competing with China for a decade, with proven manufacturing capabilities, and most critically, eligible for IRA benefits as a "friend-shoring" partner.

The numbers backing this expansion are compelling: Waaree has already supplied over 4 GW modules to US customers and signed multi-GW supply agreements with major players like SB Energy. The company expects to create over 1,500 jobs in the U.S.—jobs that politicians can point to as evidence of manufacturing renaissance.

But what makes this expansion particularly clever is the structure. Rather than just exporting from India (subject to potential tariffs and trade disputes), Waaree is building genuine American manufacturing capacity. Modules made in Brookshire will qualify for domestic content bonuses under the IRA, commanding premium prices from developers seeking to maximize federal incentives. This isn't just manufacturing arbitrage—it's regulatory arbitrage at its finest.

The strategic positioning goes deeper. In a "China Plus One" world, where every major corporation is desperately seeking to diversify supply chains, Waaree offers something unique: scale without Beijing. The company can credibly promise gigawatt-scale deliveries without the geopolitical risks that come with Chinese suppliers. For American utilities signing 20-year power purchase agreements, that security is worth paying a premium.

The early results validate the strategy. Export sales reached 57.6% of total revenue in FY24, with the vast majority coming from the USA. Waaree has become one of the largest suppliers to the U.S. solar market without most Americans ever hearing the company's name—a testament to its B2B focus and execution over marketing.

So what for investors: The U.S. expansion isn't just about capturing IRA subsidies—it's about becoming systemically important to American energy security. Once Waaree's Texas facility is operational and supplying gigawatts to U.S. projects, the company becomes very difficult to displace, creating a multi-decade annuity stream backed by American energy policy.

VII. The IPO & Public Market Debut (2024)

The roadshow for Waaree's IPO in October 2024 was unlike anything India's capital markets had seen in renewable energy. Here was a company that had survived—thrived—where Suzlon had stumbled, where Moser Baer had collapsed, where countless others had given up. The pitch was simple: Waaree wasn't selling dreams of future technology or promises of government subsidies. They were selling proven execution in the world's toughest manufacturing sector.

Waaree Energies IPO price band is set at ₹1503 per share. Waaree Energies IPO is a main-board IPO of 2,87,52,095 equity shares of the face value of ₹10 aggregating up to ₹4,321.44 Crores. The issue is priced at ₹1503 per share.

The IPO structure itself was telling: ₹3,600 crores in fresh capital and only ₹721.44 crores as offer for sale. The Doshi family wasn't cashing out—they were doubling down. The fresh capital had a specific purpose: ₹2,750 crore for a 6 GW ingot wafer, solar cell, and solar module facility, targeting 20 GW total capacity by FY27. This wasn't financial engineering; it was industrial expansion at a scale India had rarely attempted in manufacturing.

The subscription numbers defied all logic. The overall issue received an overwhelming response and was subscribed 76.34 times. Qualified institutional buyers (QIBs) subscribed to the issue 208.63 times. Meanwhile, the portion set aside for high net-worth individuals and non-institutional buyers was subscribed 62.48 times. Retail investors subscribed to the issue 10.79 times, while the portion of the issue allocated to employees was subscribed 5.17 times.

When markets opened on October 28, 2024, the price action was violent. Waaree Energies shares made a bumper debut on the bourses on Monday. Waaree Energies shares listed at Rs 2,550 on the BSE, reflecting a premium of 69.66 per cent against the IPO allotment price of Rs 1,503. Similarly, on the NSE, Waaree Energies shares listed at a premium of 66.33 per cent against the IPO allotment price at Rs 2500.

But then came the reality check. After the stellar debut, shares of the company slipped in trade by over 10% and were trading at ₹2,367 per share. Waaree Energies' shares hit an intraday high of ₹2,624.40 per share and a low of ₹2,300. Shares of the company slid lower as investors booked profits upon listing.

The volatility was predictable—retail investors who'd received tiny allocations in the oversubscribed IPO were booking profits, while institutions were building positions. But beneath the noise, something fundamental had shifted. Waaree's market capitalization at listing exceeded ₹75,000 crores, making it one of India's most valuable renewable energy companies overnight.

The IPO proceeds deployment plan revealed ambition: beyond the 6 GW integrated facility, the company announced board approval for ₹2,754 crore for a 4 GW cell plant in Gujarat and 4 GW ingot wafer plant in Maharashtra. This wasn't just capacity addition—it was complete vertical integration, from polysilicon to modules, reducing dependency on Chinese supplies at every step.

So what for investors: The IPO's record subscription and listing premium reflect the market's hunger for the "China Plus One" theme, but also reveal execution risk. At 34x FY24 P/E, Waaree is priced for perfection. The company needs to execute flawlessly on its 20 GW expansion while navigating module price volatility, trade policies, and Chinese competition. The 70% listing pop may have pulled forward years of returns.

VIII. Business Model & Operational Excellence

Understanding Waaree's business model requires abandoning Silicon Valley frameworks of network effects and software margins. This is industrial capitalism at its most fundamental: buy raw materials, add value through manufacturing, sell products. Yet within this simplicity lies sophisticated operational excellence that has allowed Waaree to thrive where others failed.

The three-pillar strategy is deceptively straightforward: Manufacturing (88.42% of revenue), EPC services (11.37%), and a small power generation arm. But the devil is in the execution details. Unlike pure manufacturers who are hostage to commodity cycles, Waaree's EPC arm provides market intelligence, customer relationships, and most importantly, a natural hedge against module price volatility.

The technology portfolio reveals pragmatism over innovation theater: multicrystalline, monocrystalline, and Tunnel Oxide Passivated Contact (TopCon) modules. Waaree isn't trying to revolutionize solar cell chemistry—they're manufacturing proven technologies at scale, with relentless focus on quality and cost. The company's NABL accredited in-house reliability lab for 3X IEC extended testing isn't sexy, but it's why banks trust Waaree modules for 25-year project finance.

The manufacturing footprint—facilities in Chikhli, Surat, Tumb, Nandigram in Gujarat, and Noida—might seem scattered, but represents careful optimization. Gujarat provides port access, industrial infrastructure, and state government support. Multiple facilities provide redundancy and the ability to optimize production based on order requirements. The recent Noida addition through Indosolar brings cell manufacturing capabilities closer to North Indian markets.

But here's the uncomfortable truth hidden in the supply chain data: 90.4% of materials are imported in FY24, with China contributing 54.1% to total imported goods. Despite all the "Atmanirbhar Bharat" rhetoric, Waaree remains fundamentally dependent on Chinese supply chains for critical components. This isn't a failure of strategy—it's recognition of reality. China's dominance in polysilicon and cell production is so complete that trying to build a fully indigenous supply chain would be economic suicide.

Instead, Waaree has focused on what India can do competitively: final assembly, quality control, customization for local markets, and most importantly, relationship management. The franchise network of 369 outlets isn't just distribution—it's thousands of local relationships, technical support, and feedback loops that no Chinese manufacturer can replicate remotely.

So what for investors: Waaree's business model is essentially a leveraged bet on the cost differential between Chinese components and finished module prices. When module prices fall faster than component costs (as in 2024), margins compress dramatically. The company's operational excellence provides some buffer, but investors should understand this is fundamentally a commodity conversion business with cyclical characteristics.

IX. Financial Performance & Unit Economics

The Q1 FY25 numbers released just before the IPO told a story of a business hitting escape velocity: Net profit of ₹745 crore (20.3% sequential growth), revenue of ₹4,426 crore (30% YoY growth). By the June '25 quarter, revenue reached ₹4,597 crore with net profit of ₹772.89 crore. These aren't the numbers of a mature manufacturer—they're the metrics of a company capturing a generational expansion opportunity.

But the headline numbers obscure a more complex reality. Module prices hit $0.11 per watt in March 2024, a 43% YoY decrease. This precipitous decline in selling prices should have destroyed profitability. Instead, Waaree expanded margins. How? Through a combination of scale economics, operational efficiency, and most importantly, mix shift toward higher-value products and markets.

The FY24 metrics deserve scrutiny: Net profit margin of 10.96% and ROE of 30.26% in a commodity manufacturing business. For context, Chinese solar manufacturers typically operate at 3-5% net margins. Waaree's premium comes from three sources: the U.S. export premium (IRA-driven), the domestic market's preference for local suppliers (PLI-driven), and operational excellence that consistently delivers 2-3% better conversion costs than peers.

The working capital dynamics reveal sophisticated cash management. Despite explosive growth, Waaree has maintained negative working capital cycles through advance customer payments and favorable supplier terms. This isn't just good fortune—it's the result of decades-long relationships and a track record of reliable delivery that allows Waaree to essentially use customer and supplier capital to fund growth.

The future capex announcements are staggering: Board approved ₹2,754 crore for 4 GW cell plant in Gujarat and 4 GW ingot wafer plant in Maharashtra, on top of the IPO proceeds deployment. Total planned capex exceeds ₹6,000 crores—more than the company's entire revenue just three years ago. This is either prescient positioning for a solar super-cycle or dangerous overexpansion into a commoditizing industry.

The unit economics tell the real story: At current module prices, Waaree needs roughly 60% capacity utilization to break even, 75% to generate acceptable returns on capital. With an order book of 16.66 GW against 13.3 GW capacity, utilization isn't the constraint—execution is. Can the company simultaneously build new facilities, ramp production, maintain quality, and manage working capital? The next 24 months will tell.

So what for investors: The financial performance shows a business at an inflection point—transitioning from capital-constrained growth to execution-constrained scaling. The 30% ROE is unsustainably high and will normalize as capital deployment accelerates. More concerning: 90% of raw material imports means USD/INR movements directly impact margins. A 10% rupee depreciation could wipe out an entire year's margin expansion.

X. Playbook: Competing with China from India

Waaree's playbook for competing with China deserves to be studied in business schools, not for its brilliance but for its pragmatism. This wasn't David versus Goliath—it was David deciding to become Goliath's local partner while building capabilities to eventually compete.

First, timing the market. Waaree entered solar in 2007, not when it was profitable but when it was inevitable. The company built capacity through the bloody 2011-2015 period when Chinese manufacturers destroyed Western competitors, through the 2016-2019 doldrums when everyone declared solar manufacturing uninvestable. By the time governments worldwide realized the strategic vulnerability of Chinese solar dependence, Waaree had a decade of manufacturing experience and gigawatt-scale capacity.

Second, government tailwinds without government dependence. Yes, Make in India, PLI schemes, and anti-dumping duties helped. But Waaree was profitable before these policies, and would survive without them. The company used government support as an accelerant, not a crutch. When the PLI scheme offered incentives for integrated manufacturing, Waaree was ready with expansion plans. When the U.S. offered IRA benefits, Waaree had the credibility to raise capital for American facilities.

Third, the trust premium. Bloomberg Tier 1 rating for 32 consecutive quarters isn't just a certification—it's a moat. In infrastructure finance, reputation compounds. Every successful project with Waaree modules makes the next project easier to finance. Chinese manufacturers might offer lower prices, but can they offer local support, customization, and the intangible comfort of dealing with a local company?

Fourth, vertical integration as defense, not offense. Waaree isn't trying to compete with China on polysilicon production—that would be suicidal. Instead, the company is integrating strategically: cells and wafers to reduce dependency, but still sourcing polysilicon from the lowest-cost producers. This pragmatic approach to integration preserves capital while reducing supply chain risk.

Fifth, the franchise model for distribution. Rather than building expensive retail infrastructure, Waaree created entrepreneurs—local businesspeople who understood their markets, could provide technical support, and had skin in the game. This asset-light distribution model allowed rapid scaling without capital consumption.

Finally, export-first strategy to build scale. By focusing on exports to the U.S. and Europe—markets that pay premiums for non-Chinese supply—Waaree could build scale economies that made them competitive in the domestic market. The 57.6% export revenue isn't just diversification; it's the foundation that makes domestic manufacturing viable.

So what for investors: The playbook works until it doesn't. Waaree succeeded because it was the only scaled Indian manufacturer when geopolitics shifted. But success invites competition—Adani, Reliance, and international players are all building Indian capacity. The moats that protected Waaree for a decade may prove less durable in the next decade.

XI. Bear vs. Bull Case

The Bear Case: A Commodity Trap at Premium Valuations

The bear case starts with customer concentration: Revenue heavily reliant on a small number of customers, particularly in the U.S. market. If SB Energy or another major customer shifts suppliers, revenue could crater overnight. The 57.1% revenue from the USA is not diversification—it's concentration risk with a geopolitical overlay.

The China dependency paradox cuts deep: 90.4% imported materials with 54.1% from China means Waaree is essentially a Chinese supply chain with an Indian label. Any serious U.S.-China confrontation could destroy the business model overnight. The company is betting it can build indigenous supply chains faster than geopolitics deteriorates—a dangerous wager.

Module price deflation is relentless and accelerating. The 43% YoY price decrease in 2024 is not an anomaly—it's the industry norm. Solar manufacturing is condemned to perpetual price declines as technology improves and scale increases. Waaree is running faster just to stand still, building capacity into a market with structural oversupply.

Competition is coming from every direction. Adani Solar has government connections and unlimited capital. Reliance has the balance sheet to sustain losses for years. International manufacturers are building Indian facilities to access the same PLI benefits. Chinese manufacturers could easily set up Indian assembly operations if the premium becomes attractive enough. Waaree's first-mover advantage is evaporating.

The U.S. market concentration terrifies. One change in IRA implementation, one shift in trade policy, one election outcome could crater the 57% of revenue from exports. The company is betting its future on American political stability and continued China hawks controlling trade policy—hardly a safe assumption.

Valuation assumes flawless execution. At 34x P/E, the market is pricing in perfect capacity expansion, sustained margins despite price deflation, and continued government support. Any stumble—construction delays, quality issues, working capital problems—could trigger a devastating derating.

The Bull Case: The Renewable Energy Arms Dealer

The bull case starts with structural inevitability. The global renewable energy transition isn't optional—it's thermodynamically required to prevent civilizational collapse. Solar will be the largest source of new electricity generation for the next three decades. Waaree doesn't need to beat China; it just needs to capture a slice of inevitable growth.

India's largest manufacturer with 13.3 GW capacity isn't just scale—it's operational knowledge that takes decades to build. Manufacturing solar modules profitably requires thousands of small optimizations, supplier relationships, and technical knowledge that can't be replicated quickly. Waaree's decade of experience is a moat that deepens with time.

The China Plus One megatrend has barely started. Every boardroom in the West is desperately seeking supply chain diversification. Waaree offers the only proven, scaled alternative to Chinese manufacturing. As geopolitical tensions increase—and they will—the premium for non-Chinese supply will only expand.

The order book of 16.66 GW provides extraordinary visibility. These aren't letters of intent—they're firm contracts with creditworthy counterparties. At current capacity, that's over a year of full production already sold. The demand environment isn't the constraint; execution is.

Technology diversification into cells, wafers, and ingots transforms the business model. Every step up the value chain captures more margin and reduces supply dependency. The ₹6,000 crore capex program will make Waaree one of the few integrated manufacturers outside China—a strategic asset for any country seeking energy independence.

The U.S. expansion is a call option on American industrial policy. If the U.S. is serious about renewable energy independence—and both parties seem committed—Waaree's early position could be worth multiples of current valuation. The 5 GW planned capacity could generate $1 billion in revenue at premium ASPs.

So what for investors: The bear and bull cases aren't mutually exclusive—both could be right at different times. Short-term, the bears have valid concerns about customer concentration and margin pressure. Long-term, the bulls are probably right about structural demand and geopolitical premiums. The key question: Can Waaree survive the next 24 months of execution risk to capture the next decade of growth?

XII. The Future: Energy Transition & Beyond

Waaree's announced forays into energy storage systems, green hydrogen, inverters, and renewable infrastructure might seem like dangerous diversification, but they represent recognition of where the energy transition is heading. Solar panels are becoming a commodity input to integrated energy systems. The companies that survive will be those that can provide complete solutions, not just components.

The 20 GW vision isn't just about scale—it's about achieving critical mass in a consolidating industry. As module prices continue declining, only manufacturers with 20+ GW capacity will have the scale economics to survive. Waaree is racing to reach this threshold before the next down cycle forces industry consolidation.

India's solar manufacturing ecosystem is at an inflection point. The government's PLI schemes and import duties have created a temporary window for domestic manufacturers to build scale. But these protections won't last forever. Within 3-5 years, Indian manufacturers will need to compete globally without subsidies. Waaree is using this window to build capabilities that will survive subsidy withdrawal.

The competition landscape is evolving rapidly. Adani Solar brings unlimited capital and political connections. Vikram Solar has technology partnerships with global leaders. International players like First Solar are establishing Indian operations. The cozy oligopoly Waaree enjoyed is ending. The next phase will be brutal—a cost and technology race where only the most efficient survive.

What needs to go right for the next decade? First, execution on the massive capex program without destroying returns. Second, maintaining quality while scaling 3x—harder than it sounds in precision manufacturing. Third, navigating the U.S.-China technology cold war without getting caught in crossfire. Fourth, managing working capital through the next down cycle without covenant breaches. Fifth, developing new products and markets as solar modules commoditize.

The green hydrogen opportunity deserves special attention. As solar electricity becomes essentially free during peak hours (already happening in California and Germany), converting excess electricity to hydrogen becomes economical. Waaree's manufacturing capabilities could naturally extend to electrolyzers and hydrogen infrastructure—a market potentially larger than solar itself.

So what for investors: The future is binary. Either Waaree becomes one of 5-10 global solar champions with 50+ GW capacity and integrated renewable solutions, or it becomes another casualty of Chinese manufacturing dominance. Current valuation assumes the former, but probability might favor the latter. The next 24 months of execution will likely determine which path manifests.

XIII. Closing Thoughts & Key Takeaways

From thermal trader to solar champion—Waaree's journey is more than a business success story. It's a template for how developing world manufacturers can compete in industries dominated by Chinese scale. Not through technological leapfrogging or government protection, but through patient capital, operational excellence, and strategic positioning.

The power of pivots cannot be overstated. Hitesh Doshi didn't just change products when he sold Waaree Instruments and entered solar—he changed the company's entire time horizon. Thermal equipment was a stable, profitable business with limited growth. Solar was an uncertain, unprofitable industry with unlimited potential. Most entrepreneurs can't make that trade. Doshi did, at exactly the right moment.

Building manufacturing excellence in a Chinese-dominated industry required a different playbook than what American business schools teach. It wasn't about innovation or disruption—it was about survival, incremental improvement, and waiting for the world to recognize the strategic vulnerability of single-source dependence. Waaree played a decade-long game while competitors focused on quarters.

India's renewable energy story is really a manufacturing competitiveness story. Can India build globally competitive manufacturing beyond software and services? Waaree suggests yes, but with caveats. Success required perfect timing, government support, geopolitical shifts, and enormous execution risk. It's not a easily replicable model.

The role of patient capital and long-term thinking deserves emphasis. Waaree could have sold out to private equity in 2015, could have pivoted to trading when manufacturing got tough, could have financialized the business rather than building factories. Instead, the Doshi family kept building capacity through the darkest days of solar manufacturing. That patience is now worth ₹75,000+ crores.

Final Investment Thesis: Waaree at ₹2,500 per share is priced for perfect execution in an imperfect industry. The company has proven it can survive and thrive in the world's toughest manufacturing sector, but past performance won't guarantee future results. The structural drivers—energy transition, China Plus One, India's manufacturing ambitions—remain compelling. But the tactical risks—customer concentration, margin pressure, execution complexity—are equally real.

For long-term investors who believe in India's manufacturing story and the renewable energy transition, Waaree offers the only proven, scaled play. For those seeking near-term safety, the volatile module pricing and customer concentration should give pause. The stock is likely to be volatile, with 50% moves in either direction possible based on quarterly results and order announcements.

Grade: B+ (A for execution history, C for current valuation)

The Waaree story isn't finished—in many ways, it's just beginning. Whether the company becomes India's first global manufacturing champion or another cautionary tale of competing with China will be determined in the next few years. What's certain is that Hitesh Doshi and team have already achieved something remarkable: proving that Indian manufacturing can compete globally in the most challenging industries. That alone makes Waaree Energies worth watching, if not necessarily buying at current valuations.

XIV. Recent News

The months following Waaree's IPO have been a whirlwind of announcements, expansions, and strategic positioning that reveal both the company's ambitions and the challenges of executing at scale. In December 2024 alone, the company announced receiving orders of 1 GW solar modules featuring advanced TOPCon 580Wp bifacial glass modules, followed by securing orders for 398 MWp and 524 MWp of solar modules, bringing cumulative orders to about 1.9 GW for the month.

As of January 2025, Waaree's total order book stood at ₹50,000 crore (26.5 GW), with 54% coming from overseas markets including the U.S. This order visibility extends well into FY27, providing revenue certainty but also execution pressure. The company's U.S. subsidiary, Waaree Solar Americas, received a 452MW solar module order in August 2025 for FY2025-26 and FY2026-27 supply, demonstrating continued traction in the critical American market.

The operational milestones have been equally impressive. In January 2025, Waaree commenced trial production at its 5.4 GW solar cell manufacturing plant in Chikhli, Gujarat, followed by commercial production at its 1.4 GW Mono PERC solar cell line in February 2025. This vertical integration into cell manufacturing is critical—it reduces dependency on Chinese cell imports and captures additional margin in the value chain.

But the most significant development might be the potential storm clouds gathering over the U.S. business. The Trump administration introduced a 26% reciprocal tariff on all imports from India, effective April 9, 2025, with exceptions for sectors such as pharmaceuticals and energy, as part of a broader trade strategy aimed at correcting perceived global trade imbalances. India was specifically targeted due to its 52% tariff on goods imported from the U.S.

With the U.S. accounting for approximately 20% of Waaree's revenue and 54% of its order book coming from overseas markets, increased tariffs may force the company to absorb costs or pass them on to customers, potentially reducing profit margins or pricing competitiveness. The CEO mentioned in January 2025 the potential scaling up of production at its Texas Plant, which presently is at 1.6 GW capacity but can expand to 3 GW, which could help mitigate tariff impacts by producing locally for the U.S. market.

The financial performance has continued to impress despite these headwinds. In Q3FY25, revenue from operations grew by 117% YoY from ₹1,596 Crore in Q3FY24 to ₹3,457 Crore in Q3FY25, while net profit jumped by 371% YoY from ₹141 Crore to ₹507 Crore over the same period. These numbers suggest the company is successfully navigating the transition from IPO proceeds to operational execution.

The capacity expansion continues at breakneck pace. As of February 2025, Waaree has solar module manufacturing capacity of 13.3 GW in India, 1.6 GW in the USA, and 5.4 GW solar cell capacity domestically. The company has been awarded 6 GW under the PLI scheme for an integrated facility, with total capacities projected to reach 21 GW for modules, 11.4 GW for cells, and 6 GW for ingot-wafers by FY27.

Perhaps most telling is the company's stock performance post-IPO. The stock closed 2024 at ₹2,854.6 on the NSE with a market cap of ₹81,828 crore, having gained 89% since listing. Despite this strong performance, the shares closed on a recent Friday at ₹2,161.20 per share, 3.3% lower than the previous close of ₹2,234.9, suggesting some volatility as investors digest the implications of potential U.S. tariffs and rapid capacity expansion.

The strategic pivot beyond solar is also accelerating. Waaree's ambition is to move towards a broader energy transition theme, with the company foraying into green hydrogen and battery energy storage systems. This diversification could provide new growth avenues as the solar module business inevitably matures and commoditizes.

So what for investors: The recent developments reveal a company executing aggressively on its growth plans while navigating increasing geopolitical complexity. The strong order book provides revenue visibility, but the U.S. tariff situation and rapid capacity additions across the industry create execution and margin risks that warrant careful monitoring.

Final Analysis: The Road Ahead

As we close this deep dive into Waaree Energies, we're left with a company that defies simple categorization. It's neither a pure technology play nor a commodity manufacturer, neither fully Indian nor entirely global, neither dependent on government support nor truly independent of it. What Waaree represents is something more nuanced: a transition business, perfectly positioned for the messy middle period between fossil fuels and renewable energy dominance.

The investment case ultimately rests on three interconnected bets. First, that the global energy transition will continue accelerating regardless of political shifts or economic cycles—a bet that seems increasingly safe given climate realities. Second, that geopolitical tensions will create sustained premiums for non-Chinese supply chains—less certain but trending favorable. Third, that Waaree can execute one of the most ambitious manufacturing expansions in Indian corporate history without stumbling—the biggest unknown.

What's remarkable about Waaree's journey is how unremarkable it seemed for so long. For over a decade, the company quietly built capacity while flashier competitors grabbed headlines and then flamed out. This patient approach—what Charlie Munger might call "sitting on your ass investing" but applied to industrial building—created the foundation for today's explosive growth. The question is whether that same patience and discipline will survive the pressures of public markets and rapid scaling.

The numbers tell a story of transformation: from ₹2,945 crores revenue in FY22 to a ₹50,000 crore order book in 2025. But numbers don't capture the industrial knowledge accumulated over decades, the relationships built through cycles, or the operational muscle memory that allows a company to add gigawatts of capacity while maintaining quality. These intangibles might be Waaree's real moat.

Yet the risks are equally real. The solar industry's history is littered with companies that scaled too fast, borrowed too much, or bet wrong on technology transitions. Waaree's aggressive expansion—21 GW by FY27—could either position it as a global champion or leave it vulnerable to the next down cycle. The 90% dependence on imported materials, particularly from China, creates a strategic vulnerability that no amount of vertical integration can fully address.

The market's initial enthusiasm—89% gains since listing—has priced in substantial execution success. At current valuations, Waaree needs to deliver flawlessly on capacity expansion, maintain margins despite module price deflation, navigate U.S. trade policies, and fund massive capex without diluting returns. It's a high-wire act with limited room for error.

But perhaps the most interesting aspect of the Waaree story is what it represents for Indian manufacturing. If a thermal equipment trader from Gujarat can build a globally competitive solar manufacturer, what other industries might be ripe for similar transformation? Waaree's success or failure will influence how global capital views Indian manufacturing potential for the next decade.

In the end, Waaree Energies is a bet on execution in an industry where execution is everything. The company has proven it can survive when others couldn't, scale when others wouldn't, and pivot when others didn't see the opportunity. Whether it can now thrive as a public company with heightened scrutiny, ambitious targets, and intense competition remains to be seen.

For investors, Waaree offers exposure to multiple themes—renewable energy transition, China Plus One, Indian manufacturing, U.S. infrastructure spending—wrapped in a single stock. That's either brilliant diversification or dangerous complexity, depending on your perspective. What's certain is that the next 24 months will likely determine whether Waaree becomes India's first global renewable energy champion or another cautionary tale about the perils of scaling too fast in a commoditizing industry.

The story of Waaree Energies isn't finished. In many ways, despite three decades of history, it's just beginning. The transition from fossil fuels to renewable energy will be the defining economic shift of the 21st century, and Waaree has positioned itself at the center of that transition. Whether it can capitalize on that position while navigating the treacherous waters of global trade, technological change, and financial markets will determine not just the company's fate, but perhaps the trajectory of Indian manufacturing ambitions.

As Hitesh Doshi watches his company navigate these challenges, he might reflect on that moment in 2007 when he was "spell-bound" by a solar exhibition in Germany. That vision has brought Waaree further than anyone could have imagined. The question now is whether vision alone is enough, or whether the brutal realities of global manufacturing will have the final word. Time, as always in the solar industry where 25-year power purchase agreements are standard, will tell.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube