SOBHA Limited: The Backward Integration Playbook

I. Introduction & Episode Roadmap

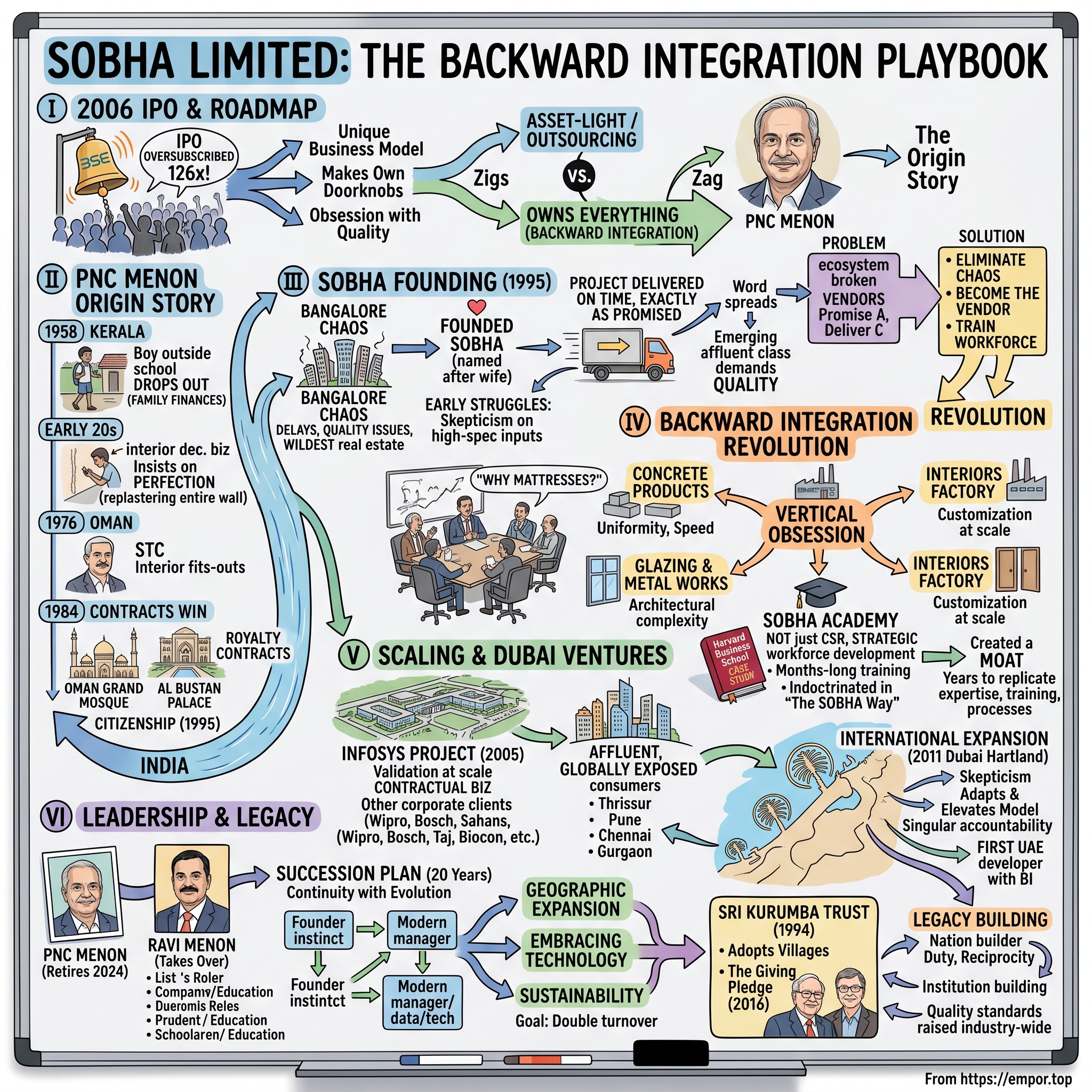

The year is 2006. The Bombay Stock Exchange is electric. A real estate company from Bangalore is going public, and something extraordinary is happening—the IPO is oversubscribed 126 times. Investment bankers are scrambling. Retail investors are borrowing money to apply for shares. The company? SOBHA Limited. The twist? This isn't your typical Indian real estate developer riding the property boom. This is a company that makes its own doorknobs.

Think about that for a second. In an industry notorious for delays, quality issues, and contractor disputes, here's a company that decided the solution wasn't to manage vendors better—it was to become the vendor. Every piece of wood, every pane of glass, every concrete block. They make it all themselves.

Today, SOBHA Limited stands at a market capitalization of ₹16,126 crore, with revenues touching ₹4,250 crore. But the numbers only tell part of the story. This is the tale of how a school dropout from Kerala who started as a furniture maker in Oman built India's only fully backward-integrated real estate company—a business model so unique that Harvard Business School wrote a case study about it.

The central question we're exploring isn't just how PNC Menon built SOBHA. It's why, in an industry where everyone else zigs toward asset-light models and outsourcing, SOBHA zagged toward owning everything. Why build factories for doorframes when you're trying to build apartments? Why train your own electricians when contractors are available on every street corner? And perhaps most importantly—why hasn't anyone successfully copied this model?

This is a story about obsession with quality, the economics of vertical integration, and what happens when you refuse to accept the constraints of your industry. It's about building not just structures, but an entire ecosystem. And it starts, as the best stories often do, with a young man who had nothing to lose.

II. The PNC Menon Origin Story

Picture Palakkad, Kerala, in 1958. A ten-year-old boy named Puthenveettil Narayanan Chenthamaraksha Menon—PNC to everyone who knew him—has just lost his father. The family's modest income vanishes overnight. His mother, now a widow with children to feed, makes a decision that will haunt and drive her son for the rest of his life: PNC must abandon his education after primary school. There simply isn't money for books or uniforms.

This moment—standing outside the school gates, knowing he couldn't return—would become the crucible that forged everything that came after. Decades later, when Menon would donate millions to education, when he'd join Bill Gates and Warren Buffett's Giving Pledge, it all traced back to this: a bright child forced to choose survival over schooling.

By his early twenties, Menon had scraped together enough to attempt college, but the financial pressures were relentless. He dropped out again, this time to launch a small interior decoration business in Kerala. The venture was modest—painting walls, arranging furniture, whatever paid the bills. But even then, clients noticed something different. Where others might touch up a crack in the wall, Menon would insist on replastering the entire section. Where others used whatever materials were cheapest, he'd spend hours sourcing exactly the right shade of paint, even if it meant lower margins. At 26, the frustration became unbearable. Kerala felt too small for his ambitions. At the age of 26, he left Kerala for Oman, carrying little more than determination and a reputation for perfectionism that most considered commercially foolish.

In 1976, Mr. PNC Menon set up an interior decoration firm (STC) in the Sultanate of Oman. The company, Service and Trade Company, started with the humblest of contracts—small residential fit-outs, office renovations. But something was different about how Menon approached even these minor projects. Where competitors might use standard fixtures, he'd import specialized hardware. Where others saw a paint job, he saw an opportunity to reimagine space itself.

By 1984, the business had established itself as a premier interior outfit on its course to win big contracts. The transformation was remarkable. Through sheer perseverance and demonstrated excellence, the company went on to work for the royalty of Oman, Bahrain, Brunei, Qatar, and the president of Tajikistan.

But it was two projects that would cement Menon's reputation across the Middle East. He contributed towards building iconic structures like Oman's Sultan Qaboos Grand Mosque and Al Bustan Palace. Think about the audacity of this—a school dropout from Kerala working on what would become Oman's most sacred modern structure, a mosque that would accommodate 20,000 worshippers and feature one of the world's largest chandeliers.

The Sultan Qaboos Grand Mosque wasn't just another contract. It was a testament to what obsessive attention to detail could achieve. Every piece of marble aligned perfectly. Every geometric pattern in the Islamic designs executed with mathematical precision. The kind of quality that made people stop and wonder who was behind it.

The impact was profound. In 1995, the Sultan of Oman granted Omani citizenship to him and his family—an extraordinary honor rarely bestowed on expatriates. By this point, Menon had built an empire across the Gulf, but something was calling him back to India. The country was liberalizing, real estate was booming, and he saw an opportunity that others missed: India didn't just need more buildings. It needed better buildings.

The boy who couldn't afford school had become one of the Middle East's most respected contractors. But his greatest challenge—and opportunity—lay ahead in Bangalore.

III. The India Opportunity & SOBHA's Founding (1995)

The Bangalore of 1995 bore little resemblance to today's tech capital. The IT boom was just beginning to stir. Infosys was still a mid-sized company. The city's infrastructure groaned under the weight of rapid growth. And the real estate sector? It was the wild west—projects delayed by years, quality that deteriorated before handover, contractors who disappeared mid-project.

PNC Menon saw this chaos and made a decision that would define everything that followed. In 1995, he founded Sobha Developers, headquartered in Bangalore. The company was named after his wife—a detail that matters more than it might seem. In an industry built on broken promises, naming the company after the person closest to him was Menon's way of putting his personal reputation on the line with every project.

The early days were brutal. Menon would walk into meetings with Bangalore's established developers and face immediate skepticism. Who was this outsider from Oman? Why was he insisting on specifications that seemed absurd for Indian construction? Why import Italian marble when local alternatives cost a fraction? Why train workers for months when daily wage laborers were available on every corner?

His first residential project became a case study in everything wrong—and right—about his approach. The construction site looked different from day one. Where other sites had workers sleeping in makeshift tents, Menon built proper dormitories. Where others relied on manual mixing, he imported concrete batching plants. The project took longer than competitors would have taken. It cost more. Industry veterans predicted bankruptcy within two years.

Then the project was delivered. On time. Exactly as promised in the brochures. With Italian marble that was actually Italian, wooden fixtures that didn't warp in Bangalore's humidity, and walls so perfectly finished that owners could move in without a single touch-up. Word spread quickly through Bangalore's emerging affluent class: there was a developer who actually delivered what he promised.

But Menon wasn't satisfied with just building better. He was diagnosing a fundamental problem in Indian real estate. The issue wasn't just execution—it was the entire ecosystem. Vendors would promise Grade A materials and deliver Grade C. Contractors would start strong when payments were fresh, then cut corners as projects progressed. Skilled workers were so rare that projects would stall waiting for competent electricians or plumbers.

The solution that emerged would have seemed insane to any MBA graduate: instead of managing this chaos better, eliminate it entirely. Don't find better vendors—become the vendor. Don't train contractors—train your own workforce. Don't source materials—manufacture them. It was a strategy that would require massive capital, patience that measured in decades, and a willingness to be misunderstood by everyone, including his own board.

By 2004, SOBHA was generating enough cash to consider this radical transformation. But first, Menon needed capital—serious capital. The company began preparing for what would become one of Indian real estate's most successful IPO stories.

The roadshow was unlike anything investment bankers had seen. Instead of PowerPoints about land banks and projected IRRs, Menon took potential investors to his construction sites. He showed them the dormitories where workers lived, the training centers where craftsmen learned their trades, the quality control processes that rejected materials other developers would happily use. He wasn't selling a real estate company. He was selling a revolution in how real estate could be done.

When the IPO opened in 2006, the response was electric. The issue was oversubscribed 126 times—investors applied for shares worth ₹11,400 crores against an issue size of just ₹90 crores. It wasn't just the fundamentals that attracted investors. It was the promise of something different: a real estate company that thought like a manufacturer, that controlled quality like a luxury goods maker, that saw construction not as project management but as craftsmanship at scale.

The IPO proceeds would fund something unprecedented in Indian real estate: the complete backward integration of a property developer. While competitors were celebrating asset-light models and outsourcing everything possible, SOBHA was about to go in exactly the opposite direction. The boy who'd built furniture by hand in Kerala was about to build factories that would change Indian real estate forever.

IV. The Backward Integration Revolution

The boardroom was skeptical. It was 2007, and PNC Menon was proposing something that violated every principle of modern business strategy. While McKinsey consultants preached asset-light models and core competency focus, Menon wanted to build factories. Not one or two, but entire manufacturing complexes. For doorframes. For concrete blocks. For mattresses, of all things.

"Why mattresses?" a board member asked, genuinely puzzled.

Menon's response captured everything about his philosophy: "When a customer buys a SOBHA home, they're not just buying walls and floors. They're buying sleep quality, morning comfort, the confidence that every single element in their home meets our standards. If we don't make the mattress, how can we guarantee their sleep?"

This wasn't backward integration—it was complete vertical obsession. The strategy that emerged would become so distinctive that Harvard Business School would write a case study about it, professors puzzled by a model that seemed to defy everything they taught about efficiency and focus.

The first factory was for concrete products. In a rented warehouse on the outskirts of Bangalore, SOBHA began manufacturing its own concrete blocks, pavers, kerb stones. The economics seemed terrible. Concrete blocks from local suppliers cost ₹28 per unit. SOBHA's initial cost was ₹47. Any CFO would have shut it down immediately.

But Menon wasn't looking at unit economics. He was solving for a different equation. Every SOBHA-made block was uniform—exactly 400mm x 200mm x 200mm, not the 390mm x 195mm x 195mm that suppliers claimed was "close enough." The compression strength was consistent. The curing process controlled. When workers laid SOBHA blocks, walls rose perfectly straight. Plastering requirements dropped by 30%. Structural integrity improved measurably.

The glazing and metal works factory came next. While competitors struggled with window contractors who couldn't deliver uniform quality, SOBHA was manufacturing its own aluminum windows, curtain walls, structural glazing. The factory could produce everything from standard window frames to complex architectural metalwork. Quality control happened at the production stage, not at installation.

But it was the interiors factory that truly set SOBHA apart. This wasn't just manufacturing—it was craftsmanship at industrial scale. The facility produced everything from wardrobes to kitchen cabinets, from wooden doors to decorative panels. Each piece was made to specification for specific apartments, arriving on-site ready to install, fitting perfectly because the measurements were taken by SOBHA employees and executed by SOBHA craftsmen.

The training infrastructure was equally radical. SOBHA Academy wasn't just a token CSR initiative—it was strategic workforce development. Young men from villages across Karnataka were brought in, housed, fed, and trained for months. Not days or weeks—months. They learned not just how to lay tiles, but why certain adhesives worked better in Bangalore's climate. Not just how to install electrical fixtures, but how to read architectural drawings and understand load calculations.

A master craftsman from Italy was brought in to teach marble laying. Japanese experts demonstrated waterproofing techniques. The academy became a university of construction crafts, producing workers who weren't just skilled but indoctrinated in SOBHA's obsessive quality standards.

The economics started making sense in unexpected ways. Yes, the initial costs were higher. But warranty claims dropped to near zero. Project delays from material shortage vanished. Customer complaints fell by 94%. More importantly, SOBHA could now promise something no other developer could: complete control over quality from design to delivery.

The model created a moat that competitors couldn't cross even if they wanted to. By 2010, SOBHA had invested over ₹800 crores in backward integration infrastructure. The time to replicate wasn't measured in years but in decades—not just to build facilities but to develop the expertise, train the workforce, perfect the processes. The strategy became so distinctive that Harvard Business School wrote a case study about it titled "Sobha Group Real Estate: Backward Integration for Quality." The case examined how, "striving to control quality and schedule, his firm, Sobha Middle East, self-performs a wide range of tasks – an unusual set of choices in the global real estate and construction industry."

The impact went beyond operational efficiency. Pre-cast technology reduced delivery times by 30%. But more importantly, it changed what customers expected from real estate developers. In an industry where delays of 12-18 months were standard, SOBHA started guaranteeing delivery dates—and keeping them. In a market where quality degradation between show flat and actual delivery was accepted as inevitable, SOBHA apartments looked exactly like what was promised.

By 2012, the backward integration model was complete. Three state-of-the-art manufacturing facilities. A training academy producing 500 skilled workers annually. Complete control from raw material to finished home. It had taken 17 years and over ₹1,000 crores of investment. But SOBHA had achieved something unprecedented: it had become India's only fully backward-integrated real estate company.

The competition watched, puzzled. Some tried to replicate pieces—a small concrete plant here, a carpentry workshop there. But they missed the point. This wasn't about owning factories. It was about reimagining what a real estate company could be. And Menon wasn't done. If this model worked in India, why not take it global?

V. Scaling the Business Model (2000s-2010s)

The Infosys campus in Mysore sprawls across 337 acres, a small city unto itself with accommodation for 15,000 trainees. When Narayana Murthy and his team began planning this ambitious project in 2005, they needed a contractor who could handle complexity at scale while maintaining the quality standards of a global technology leader. They chose SOBHA.

This wasn't just another contract. It was validation of everything Menon had been building toward. Here was India's most respected technology company, known for its exacting standards, entrusting SOBHA with creating its flagship training facility. The project would require coordinating thousands of workers, managing hundreds of material specifications, and delivering on a timeline that had no room for the delays typical of Indian construction.

The Infosys project became SOBHA's calling card for corporate India. Soon, the client list read like a who's who of Indian business: Wipro's sprawling campuses, HCL's technology centers, Bosch's precision manufacturing facilities, Dell's Indian headquarters. Each project reinforced the same message—when quality and timeliness actually mattered, when failure wasn't an option, companies turned to SOBHA.

But Menon's ambitions extended beyond corporate campuses. The residential real estate market was evolving rapidly. India's IT boom had created a new class of affluent, globally exposed consumers who wanted homes that matched international standards. They'd lived in Singapore, worked in San Francisco, studied in London. The typical Indian apartment—with its uneven floors, leaking bathrooms, and windows that didn't quite close—wasn't good enough anymore.

SOBHA's expansion strategy was deliberate, almost methodical. Rather than the land-grab approach of competitors who entered 50 cities simultaneously, SOBHA picked its markets carefully. Thrissur, close to Menon's Kerala roots. Coimbatore, an emerging industrial hub. Mysore, riding the IT wave. Pune, benefiting from Mumbai's overflow. Chennai, South India's Detroit. Each city was chosen not just for its growth potential but for SOBHA's ability to replicate its quality standards there.

The numbers tell only part of the story. By this period, SOBHA had expanded to 27 cities across 14 states, with 29.33 million square feet of developable area. Since inception, the company had delivered 115.93 million square feet—each square foot meeting the same quality standards, whether in Bangalore or Gurgaon, Kochi or Pune.

The contractual business became a strategic advantage in ways Menon hadn't fully anticipated. Working with corporations like the Taj Group and ITC Hotels meant understanding hospitality standards—knowledge that fed back into residential projects. Building Biocon's facilities meant mastering pharmaceutical-grade clean room construction—expertise that improved SOBHA's approach to home ventilation and air quality.

Quality certifications followed: ISO 9001 for quality management, ISO 14001 for environmental standards, OHSAS 18001 for occupational health and safety. These weren't just certificates to frame on the wall. Each certification required documenting processes, establishing measurable standards, creating audit trails. SOBHA was applying manufacturing rigor to construction—an industry that had historically resisted standardization. The Infosys projects were particularly significant. Commencement of construction of the first contractual project, the Corporate Block for Infosys Technologies Limited, Bangalore, was followed by the completion and handover of the Infosys project at Mysore. The Project finished in Mysore for Infosys by SOBHA was proclaimed by the Builders Association of India, Mysore Center as the Project of the Year for the year 2005.

The scale of SOBHA's growth during this period was staggering. The Contracts business at SOBHA boasts of an expansive portfolio of 278 projects covering 42.41 million sq. m. of area in 24 cities across India. The client roster had expanded to include not just IT companies but hospitality giants, manufacturing leaders, and healthcare pioneers. Corporate clients include Infosys, LuLu, Biocon, Syngene, Dell, HP, Timken, Taj, Bayer Material Science, HCL, Bharat Forge, ITC, Bosch, GMR, Huawei Technologies, Wonderla Holidays and Manipal Group.

But perhaps the most important development wasn't visible in project completions or revenue numbers. It was the cultural shift happening within Indian real estate. SOBHA was proving that Indian companies could deliver global quality, that "good enough" wasn't acceptable anymore, that customers would pay premiums for genuine quality.

The validation came from unexpected quarters. International companies entering India began specifying "SOBHA standards" in their RFPs. Competitors started advertising their backward integration initiatives, even if they were limited to small carpentry workshops. Business schools began studying SOBHA's model, trying to understand how a capital-intensive, seemingly inefficient strategy had become a competitive advantage.

By 2010, SOBHA had fundamentally changed what customers expected from real estate developers. The company that had started with one man's obsession with quality had scaled that obsession across an entire organization, across dozens of cities, across millions of square feet. But Menon knew that to truly validate the model, he needed to prove it could work beyond India's borders. The next frontier awaited.

VI. The Business Segments & Manufacturing Empire

Inside SOBHA's concrete products factory in Bangalore, the morning shift begins at 6 AM sharp. The facility spans 20 acres, but what's remarkable isn't the size—it's the precision. Every concrete block produced here undergoes seven quality checks. The compression strength is tested hourly. The dimensions are verified to the millimeter. In an industry where a 5% defect rate is considered acceptable, SOBHA's rejection rate hovers at 0.3%.

This is just one piece of SOBHA's manufacturing empire, which by now had evolved into something unprecedented in global real estate. The business had crystallized into two distinct but synergistic segments: Real Estate development, accounting for 81% of revenues, and Contractual and Manufacturing, contributing the remaining 19%. But those percentages tell only part of the story. The manufacturing arm wasn't just a revenue contributor—it was the backbone that made everything else possible.

The interiors factory had become a marvel of customization at scale. Unlike typical furniture manufacturers who produce standard SKUs, SOBHA's facility created bespoke pieces for specific apartments. When a customer bought apartment 1402 in SOBHA Indraprastha, the wardrobes were manufactured specifically for that unit's dimensions, the kitchen cabinets designed for that particular layout. The factory could produce 500 unique pieces daily, each tracked through a barcode system that would make Amazon jealous.

The glazing and metal works division had evolved far beyond simple window frames. The facility now produced complex structural glazing systems, architectural metalwork that could rival European manufacturers, and custom solutions that architects had previously thought impossible in India. When a project required a 40-foot curved glass facade with no visible supports, SOBHA's engineers didn't say "it can't be done"—they figured out how to do it.

But the real revolution was happening at SOBHA Academy. What had started as a training center had become a full-fledged university of construction crafts. The academy wasn't just teaching skills—it was creating a new class of construction professionals. Young men from rural Karnataka arrived knowing nothing about construction. Six months later, they could read architectural drawings, understand structural engineering basics, and execute work to international standards.

The curriculum was unlike anything in vocational education. Trainees learned not just how to lay tiles but the chemistry of adhesives. Not just electrical wiring but load calculations and safety standards. They studied Japanese concepts like Kaizen and 5S, applying manufacturing excellence principles to construction sites. The academy produced 500 certified craftsmen annually, each one indoctrinated in what internally was called "The SOBHA Way."

SOBHA brought technicians from the Middle East to train people in India. SOBHA Academy has been specifically set up to train and skill technicians, tradesmen and engineers working at site. The investment in human capital was as significant as the investment in machinery. Today, close to 2500 trained people and over 7000 skilled technicians, craftsmen, tradesmen help design, engineer, and execute the entire value chain.

The economics of this integrated model had matured in unexpected ways. Yes, the capital investment was massive—over ₹1,200 crores by this point. But the benefits went beyond quality control. SOBHA could launch projects faster because material availability was guaranteed. Construction cycles shortened by 30% because of standardization and trained workforce. Customer acquisition costs dropped because the brand commanded such premium that projects sold themselves.

More importantly, the manufacturing capabilities became a differentiator in the contractual business. When Biocon needed clean rooms with pharmaceutical-grade finishes, SOBHA could deliver because they controlled every element. When ITC Hotels demanded specific acoustic properties in their conference rooms, SOBHA could manufacture custom solutions. This wasn't just construction—it was engineered delivery.

The sustainability angle emerged almost by accident. Because SOBHA controlled its supply chain, waste reduction became possible at levels the industry had never seen. Concrete blocks were manufactured to exact requirements, eliminating the 15-20% wastage typical in construction. Wood was sourced from certified sustainable forests. Water from manufacturing was recycled. What started as quality control had evolved into environmental responsibility.

But perhaps the most profound impact was on the industry ecosystem. SOBHA's trained workers didn't always stay with SOBHA—many went on to work for other developers, carrying with them higher standards and better practices. Suppliers who wanted to work with SOBHA had to upgrade their own quality standards. Competitors were forced to improve just to stay relevant. SOBHA wasn't just building better buildings—it was elevating the entire industry.

The manufacturing empire had become self-reinforcing. Better quality meant premium pricing, which funded more investment in manufacturing, which enabled even better quality. It was a virtuous cycle that competitors couldn't break into—not because they lacked capital, but because they lacked the decades of expertise, the trained workforce, the organizational culture that made it all work.

By 2011, PNC Menon was ready for the ultimate test of this model. If backward integration could transform Indian real estate, what could it do in one of the world's most competitive luxury markets? Dubai was calling.

VII. International Expansion & Dubai Ventures

The Dubai real estate market in 2011 was still recovering from the 2008 crash. Dramatic projects had stalled mid-construction, creating a skyline of abandoned cranes. International developers were retreating. It was precisely the wrong time to enter the market—which, for PNC Menon, made it exactly the right time.

Sobha Hartland was the sublime brainchild of Mr. Menon to house the world's most discerning at the epicenter of Dubai. This resort-style luxury housing development was launched as a $4 billion project in Mohammed Bin Rashid Al Maktoum City. But this wasn't just about building luxury homes in Dubai. It was about proving that the backward integration model could work in a market that already had world-class contractors, sophisticated suppliers, and customers who'd seen everything.

The skepticism was immediate and intense. Dubai's real estate establishment looked at SOBHA's plans to set up manufacturing facilities and training centers with bemusement. Why manufacture in Dubai when you could import anything from anywhere in the world? Why train workers when skilled labor from dozens of countries was readily available? The entire premise seemed to violate the fundamental logic of Dubai's globalized economy.

But Menon saw what others missed. Dubai's real estate market, for all its sophistication, suffered from the same fundamental problem as India's—lack of control. Projects were delayed because Italian marble suppliers couldn't deliver on time. Quality varied because Romanian contractors had different standards than Filipino ones. The tower of Babel that was Dubai's construction industry created inefficiencies that no amount of project management could overcome.

In 2012, SOBHA introduced its backward integration model to Dubai with the Sobha Hartland launch. The company didn't just import its Indian model wholesale—it adapted and elevated it. The manufacturing facilities established in Dubai were even more advanced than those in India. The training programs incorporated learnings from two decades of experience. The quality standards were set not just to match but to exceed what the world's most demanding luxury buyers expected.

Encompassing 8 million square feet of freehold community and mixed-use development, 30% (2.4 million sq ft) of the community has been reserved for green and open spaces. This wasn't just about building apartments—it was about creating an entire ecosystem, a city within a city, where every element from the lamp posts to the landscaping reflected SOBHA's obsessive attention to detail.

The scale of ambition was staggering. Beyond Sobha Hartland, the company partnered with Meydan Group for District One, an $8 billion development that would redefine luxury living in Dubai. These weren't just projects—they were statements of intent. SOBHA was declaring that an Indian company could compete at the highest levels of global real estate.

The response from Dubai's luxury buyers was initially cautious. The SOBHA name meant nothing to Russian oligarchs or Chinese investors accustomed to buying from Emaar or Damac. But then something interesting happened. The buyers who did take a chance—many of them Indians familiar with SOBHA's reputation—became the company's most vocal advocates. They'd bought properties from other Dubai developers and experienced the usual issues: delays, quality compromises, features that looked good in renderings but disappointed in reality. With SOBHA, what they saw was what they got.

The Dubai operations became a laboratory for innovation. With access to global talent and technology, SOBHA could experiment with construction techniques that weren't yet feasible in India. Modular construction methods were refined. Smart home technologies were integrated from the design phase rather than retrofitted. Sustainability features that were optional in India became standard in Dubai.

The backward integration model proved even more valuable in Dubai's international environment. While competitors struggled with coordination between dozens of contractors and suppliers from different countries, SOBHA's integrated approach meant singular accountability. When the Dubai government introduced new sustainability requirements, SOBHA could adapt immediately because they controlled their entire supply chain. When COVID-19 disrupted global supply chains, SOBHA's projects continued largely unaffected because they manufactured locally.

By 2018, SOBHA had become the first developer to successfully pioneer backward integration in the UAE. The model that had seemed absurd to Dubai's real estate establishment had proven its worth. Sobha Hartland was selling at premiums comparable to established luxury developers. The company was being invited to bid on projects that would have been unthinkable for an Indian developer just years earlier.

The international expansion validated something crucial: SOBHA's model wasn't just about solving India's infrastructure deficiencies. It was a fundamentally better way to develop real estate, applicable whether you were building in Bangalore or Dubai, for middle-class families or ultra-high-net-worth individuals. Quality, it turned out, was a universal language.

The success in Dubai opened doors to other markets. Discussions began for projects in Abu Dhabi, where the BAPS Hindu Mandir project would later see Menon contribute INR 110 million. Plans were drawn for potential expansions to Australia and the United States. The boy from Kerala who'd started laying tiles in Oman had built a model that could work anywhere in the world.

But even as SOBHA conquered new markets, Menon knew that the ultimate test of any organization isn't expansion—it's succession. At 76, it was time to ensure that everything he'd built would outlive him.

VIII. Leadership Transition & Next Generation

The boardroom at SOBHA's Bangalore headquarters was unusually quiet on a November morning in 2024. PNC Menon, now 76, looked across the table at his son Ravi. The moment both had been preparing for had arrived. PNC Menon, the founder and chairman of Sobha Group, announced on Monday that he would retire from his active role as chairman and hand over the reins of the iconic luxury developer to his son Ravi Menon, who is currently serving as co-chairman of the group. The significant transition of leadership at the $5 billion prime property developer, known for its signature residential offerings in Dubai, Muscat and India, will be effective from November 18, 2024, a day after the visionary entrepreneur turns 76.

This wasn't a sudden decision. The succession had been methodically planned for two decades. Ravi holds a degree in Bachelor of Science in Civil Engineering from Purdue University, USA. He has sixteen years of experience in the field of construction and real estate development. But more importantly, he'd been groomed not just in the business but in the philosophy that underpinned it.

For over two decades, Ravi Menon, a civil engineering graduate with Honors from Purdue University, USA, has played a pivotal role in Sobha Group's success. Since joining as a Director at Sobha in India in June 2004, he has advanced the company's strategic vision and fostered a culture of innovation. His promotion to vice chairman in January 2006, followed by his appointment as chairman of Sobha in India and later as co-chairman of Sobha Group in Dubai, stands as a testament to his visionary leadership and operational excellence.

The transition represented more than just a generational handover. It was a test of whether SOBHA's culture—built on one man's obsession with quality—could survive beyond its founder. Many family businesses struggle with this moment. The founder's vision gets diluted. Professional managers take over and optimize for efficiency over excellence. The unique culture that made the company special gradually erodes.

But Ravi Menon wasn't just inheriting a business—he was inheriting a mission. He is responsible for developing the strategic vision of the Company, establishing the organisations' goals and objectives, and directing the Company towards its fulfilment. He focuses on the overall functioning of the Company, in particular emphasising on product delivery, project execution, quality control, technology advancement, process and information technology and customer satisfaction.

The differences between father and son were as important as their similarities. Where PNC Menon relied on instinct and experience, Ravi brought data analytics and systematic thinking. Where the father had built through sheer force of will, the son sought to institutionalize excellence through process and technology. The Purdue-trained engineer wasn't trying to replicate his father—he was trying to evolve the model for a new era.

"Throughout my tenure as chairman, I have been inspired by our exceptional team's dedication and creativity, which has propelled the company to new heights. I remain committed to supporting Sobha Realty's ambitions and am confident that under Ravi Menon and Francis Alfred's leadership, the company will enter a new era of progress and innovation," PNC, reflecting on this transition, told a press briefing on Monday.

The leadership team being assembled around Ravi was crucial. Francis Alfred, the Managing Director of Sobha Realty, represented operational excellence. The team wasn't just Indian anymore—it was global, reflecting SOBHA's ambitions. Plans were being drawn for expansions into Abu Dhabi, the United States, and Australia. Ravi Menon, who has been with the group since 2004 in various roles, takes over at a pivotal time as Sobha Group plans expansions into the US and Australia and aims to double its turnover to $10 billion in the next five years.

The challenge wasn't just geographical expansion. The real estate industry was being disrupted by technology. PropTech startups were promising to revolutionize everything from property search to construction management. Smart homes were becoming standard. Sustainability wasn't optional anymore—it was mandatory. The backward integration model that had been SOBHA's strength could become a liability if it made the company too rigid to adapt.

Ravi's response was to double down on what made SOBHA unique while embracing what needed to change. The backward integration would continue, but manufacturing would incorporate automation and robotics. The training academy would remain, but curricula would include digital skills and sustainability practices. The obsession with quality would persist, but quality would be redefined to include environmental impact and smart technology integration.

"I am deeply honored to take on the role of Chairman of Sobha Group. Under PNC Menon's remarkable leadership, Sobha Realty has become a leading luxury real estate developer in the region, with promising expansion plans globally. I am committed to upholding this legacy and advancing it further to make it the most preferred brand for customers," Ravi said.

The succession plan extended beyond just the chairman's role. Key positions throughout the organization were being filled with next-generation leaders who understood both SOBHA's heritage and its future needs. The company was investing heavily in technology talent, bringing in expertise from outside the real estate industry. The goal wasn't to become a technology company but to use technology to be a better real estate company.

Culture preservation was perhaps the biggest challenge. How do you maintain a founder's obsession with quality when the founder is no longer running day-to-day operations? SOBHA's answer was to embed it in systems. Quality metrics were built into every process. Training programs didn't just teach skills but indoctrinated values. The backward integration model itself became a forcing function for quality—when you make everything yourself, you can't blame suppliers for defects.

The family ownership structure—with promoters still holding 52.9% of the company—provided stability during the transition. This wasn't a company beholden to quarterly earnings calls or activist investors demanding asset-light strategies. The patient capital that had enabled the backward integration model in the first place would continue to support long-term thinking.

As November 18, 2024 approached, PNC Menon prepared for his new role as Founder rather than Chairman. He wouldn't disappear—his expertise would continue to guide major decisions. But the operational leadership would pass to the next generation. The test of his life's work wouldn't be what he built, but whether it could thrive without him.

IX. Playbook: The Backward Integration Strategy

Let's pause the narrative for a moment and examine the mechanics of what SOBHA built. Because understanding the story is one thing—understanding the strategy is another. And the strategy, when you really examine it, seems to violate everything modern business theory teaches us.

Consider the conventional wisdom: Focus on your core competency. Asset-light models generate higher returns. Outsourcing allows flexibility. Vertical integration is a relic of the industrial age. Every MBA program, every consulting firm, every activist investor preaches the same gospel: unbundle, optimize, focus.

SOBHA did the opposite. And it worked. The question is: why?

The answer starts with understanding what problem backward integration actually solves. It's not about cost—SOBHA's integrated model is often more expensive than outsourcing. It's not about capacity—you can always find suppliers with more scale. It's about something more fundamental: complete control over quality in an industry where quality is nearly impossible to guarantee.

Think about how construction typically works. A developer contracts a general contractor, who subcontracts to specialists, who hire labor from wherever they can find it, who source materials from whoever offers the best price that week. Each layer adds its own margin, its own timeline variability, its own quality uncertainty. By the time concrete is being poured, the developer is four or five degrees removed from the actual work.

SOBHA collapsed this entire chain. Unique to SOBHA, the backward integration model compromises of two main pillars. First is the 'Design to delivery' model made possible through in-house competencies to design, engineer, source and manufacture a range of building materials – all executed by trained and skilled professionals.

The economics are counterintuitive. Yes, the capital investment is massive. Yes, the operational complexity is higher. But the benefits compound in ways that aren't immediately obvious:

Quality Premium: SOBHA commands 15-20% price premiums over comparable properties. When your rejection rate is 0.3% versus the industry's 5%, when your delivery is actually on time, when the finished product matches the promise, customers pay more. The premium more than offsets the additional costs.

Speed to Market: This has also helped shorten timelines and has enabled every project with a near precise timetable from start to finish. When you control your supply chain, you don't wait for materials. When your workers are trained in-house, you don't scramble for skilled labor. Projects launch faster and complete predictably.

Risk Mitigation: The COVID-19 pandemic provided the ultimate test case. While competitors faced supply chain disruptions, labor shortages, and material price spikes, SOBHA's integrated model continued largely uninterrupted. The insurance value of controlling your supply chain is incalculable.

Innovation Capability: When you manufacture in-house, you can customize infinitely. Need a special acoustic panel for a hotel project? Design and build it. Want to experiment with new sustainable materials? Test them in your own factory. The ability to innovate without depending on suppliers becomes a competitive weapon.

Knowledge Accumulation: Every project teaches lessons that get incorporated into manufacturing, training, and design. This knowledge doesn't leak out to competitors through shared suppliers. It accumulates within SOBHA, creating an ever-widening moat.

But here's why others don't copy it, even when they see it working:

Capital Requirements: We're talking about ₹1,200+ crores of investment before you see returns. Most developers can't afford it. Most investors won't fund it. The patience required is measured in decades, not quarters.

Expertise Development: You need to be good at everything—construction, manufacturing, training, logistics. Most companies struggle to excel at one thing. SOBHA had to excel at dozens simultaneously. This isn't a capability you can hire—it has to be built over time.

Cultural Commitment: Backward integration only works if everyone in the organization believes in it. One cost-cutting CFO, one efficiency-focused CEO, and the whole model unravels. It requires a cultural commitment to quality over efficiency that few organizations can maintain.

Scale Requirements: The model needs massive scale to be economical. If you're building a few projects a year, owning factories doesn't make sense. SOBHA needed to reach a certain size before backward integration became viable, creating a chicken-and-egg problem for would-be imitators.

The technology angle adds another dimension. SOBHA has also made significant investments in setting up and maintaining its own plant and machinery, giving it the flexibility to deploy resources where and when needed most. Pre-cast technology reducing delivery times by 30% isn't just about speed—it's about standardization, quality control, and waste reduction.

There are broader lessons here for other industries:

When Backward Integration Makes Sense: When quality is hard to verify, when supply chains are unreliable, when customization is valuable, when knowledge accumulation matters, and when you have patient capital.

When It Doesn't: When suppliers are sophisticated and reliable, when the product is commoditized, when flexibility is more important than control, when capital is expensive, and when speed to market is critical.

The SOBHA model isn't universally applicable. But in Indian real estate—with its quality challenges, unreliable suppliers, and customers desperate for trustworthy developers—it created an almost unassailable competitive position.

The ultimate validation? Is the backward integration model replicable and sustainable? The Harvard Business School case study asked this question. The answer, after nearly three decades, appears to be yes—but only if you're willing to commit completely. Half-measures don't work. You can't be a little bit backward integrated, just like you can't be a little bit pregnant.

X. Analysis & Investment Case

The numbers tell a story, but you have to know how to read them. SOBHA Limited today sits at a market capitalization of ₹16,126 crores, with revenues of ₹4,250 crores and profits of ₹102 crores. The stock trades at 3.54 times book value, a premium to most Indian real estate companies but a discount to quality players in other sectors. Promoter holding stands at 52.9%, providing stability but also limiting float.

These metrics, however, only scratch the surface. To understand SOBHA as an investment, you need to understand it as a business model that defies easy categorization. Is it a real estate developer? A manufacturing company? A construction contractor? The answer is yes to all three, and that's both its strength and its complexity.

Let's start with the bull case:

The Quality Moat: In an industry plagued by trust deficits, SOBHA has built a brand that commands genuine pricing power. When customers are willing to pay 15-20% premiums for your product in a commoditized industry, you have something special. This isn't temporary—it's been sustained for decades.

Scalability with Control: The backward integration model, once established, actually becomes easier to scale than traditional development. You're not negotiating with new suppliers in each city, training new contractors for each project. You're replicating a proven model with your own resources. The marginal cost of expansion decreases over time.

Inflation Hedge: Controlling your supply chain means controlling your costs better than competitors. When cement prices spike, SOBHA's concrete products division absorbs some of the impact. When labor costs rise, trained in-house workers provide stability. This operational hedge translates to earnings stability.

Diversification Within Focus: The two-segment model—81% real estate, 19% contractual and manufacturing—provides multiple revenue streams without losing focus. Contractual work with blue-chip clients provides steady cash flows that support the lumpier residential development business.

Management Quality: The successful leadership transition from founder to second generation is rare in Indian business. Ravi Menon represents continuity with evolution—maintaining the quality obsession while embracing technology and modern management practices.

But the bear case is equally compelling:

Capital Intensity: This is not an asset-light model. The return on capital employed (ROCE) will always lag pure developers who outsource everything. In a world where capital efficiency is increasingly valued, SOBHA's model looks antiquated to some investors.

Real Estate Cyclicality: No amount of backward integration protects you from demand cycles. When property markets crash, SOBHA's factories don't stop needing maintenance, trained workers still need salaries. The fixed cost base amplifies downturns.

Execution Risk: The model's complexity means more things can go wrong. A problem in manufacturing affects construction. A construction delay affects brand reputation. Everything is interconnected, which means risks compound rather than diversify.

Geographic Constraints: The backward integration model makes international expansion harder. You can't easily set up factories in new countries. This limits growth potential compared to asset-light competitors who can enter new markets quickly.

Technology Disruption: What happens if 3D printing makes traditional construction obsolete? If modular housing takes off? SOBHA's massive investments in traditional manufacturing could become stranded assets.

The competitive positioning adds another layer of complexity. SOBHA competes with everyone and no one. In luxury residential, it faces Lodha and DLF. In mid-market housing, Puravankara and Brigade. In contractual work, L&T and Shapoorji Pallonji. Yet none of these competitors replicate SOBHA's integrated model, making direct comparison difficult.

The financial metrics require careful interpretation:

Profit Margins: Lower than pure developers but more stable. SOBHA won't show the 40% EBITDA margins of land-banking developers in boom times, but it also won't see margins collapse in downturns.

Working Capital: The manufacturing operations require significant working capital, making the balance sheet heavier than typical developers. But this also means better control over project execution.

Debt Levels: Moderate and manageable, but the capital-intensive model means debt will always be present. The key is whether cash flows can consistently service and reduce debt over cycles.

Valuation Multiple: The 3.54x book value seems expensive compared to other developers trading below book. But if you value SOBHA as a manufacturing company with a real estate division rather than a pure developer, the multiple makes more sense.

For investors, SOBHA represents a specific bet: that quality will continue to command premiums, that Indian real estate will continue to professionalize, that execution excellence will matter more than financial engineering. It's not a momentum play or a turnaround story. It's a compound quality story.

The investment case ultimately depends on your time horizon and belief system. If you believe Indian real estate will increasingly resemble developed markets—where quality developers command persistent premiums—then SOBHA is positioned to benefit disproportionately. If you believe the industry will remain commoditized and cycle-driven, then the capital-intensive model is a disadvantage.

One thing is certain: SOBHA is not a trade. It's an investment in a unique business model that has proven resilient across cycles but requires patience to appreciate fully. The company that started with one man's obsession with quality has become an institution. Whether that institution can generate superior returns for shareholders while maintaining its quality obsession—that's the billion-rupee question.

XI. Philanthropy & Legacy Building

The year was 1994. SOBHA hadn't even been founded yet. PNC Menon was still building his empire in Oman. But something was gnawing at him—the memory of a ten-year-old boy who couldn't afford to stay in school. That year, a full year before founding SOBHA, P. N. C. Menon established the Sri Kurumba Educational & Charitable Trust in 1994, a year before he founded Sobha Developers.

This sequencing matters. The philanthropy came before the fortune. The giving preceded the getting. It suggests that for Menon, business success was always a means to a larger end.

The trust adopted Vadakkencherry and Kizhakkancherry - two Panchayats each consisting 2 villages in Palakkad district, Kerala, his native state, in 2006. In the adopted villages, the trust helps families with very low monthly income and provides education to children from 2,500 poor families (about 11000 people).

The approach to philanthropy mirrors the approach to business: complete, integrated, systematic. Rather than random acts of charity, Menon adopted entire villages. Rather than just giving money, he built infrastructure. Schools, healthcare centers, vocational training institutes. The same backward integration philosophy—control the entire chain to ensure quality outcomes.

The numbers are staggering but somehow feel insufficient to capture the impact. 2,500 families directly supported. 11,000 lives touched. But what does that mean? It means children who would have dropped out like Menon did are completing engineering degrees. It means families trapped in generational poverty are finding paths out. It means entire communities are being transformed.

Then came 2016, and an invitation that would place Menon in the rarest of company. In 2016, Menon and his wife Sobha joined The Giving Pledge list a philanthropic initiative started by Warren Buffett, former Microsoft chairman Bill Gates and his then-wife Melinda. The Giving Pledge isn't just about money—it's about publicly committing to give away the majority of your wealth. For someone who started with nothing, promising to give away billions is both full circle and profound statement.

The pledge letter Menon wrote is worth examining. He didn't talk about tax benefits or legacy building. He talked about duty, about reciprocity, about the accident of success. The boy who couldn't afford school understood viscerally that success is not entirely self-made. Circumstances, timing, luck—they all play roles. And those who benefit from these accidents of fortune have obligations to those who don't.

In 2016, Mr. PNC Menon and Mrs. Sobha Menon signed The Giving Pledge – an initiative undertaken by The Bill and Melinda Gates Foundation and Mr. Warren Buffet, to donate 50% of their wealth to charity to address the significant problems of society.

The 2024 contribution of INR 110 million to the BAPS Hindu Mandir in Abu Dhabi represents another dimension—cultural and spiritual philanthropy. This isn't just about building a temple. It's about creating institutions that preserve and transmit culture across generations and geographies. The same permanence that Menon seeks in his buildings, he seeks in his philanthropy.

In 2009, he was honoured with the Pravasi Bharatiya Samman by the President of India. This award, given to overseas Indians who have made exceptional contributions to their homeland, recognized not just business success but the broader impact. Menon had become a bridge between India and the Gulf, between business and social responsibility.

The recognition matters less than the philosophy it represents. Business, in Menon's worldview, is not separate from society—it's an instrument for social transformation. SOBHA Academy doesn't just train workers for SOBHA projects. It creates skilled craftsmen who transform the entire construction industry. The quality standards SOBHA enforces don't just benefit SOBHA customers—they raise expectations across the market.

This is institution building of a different sort. Not just companies or charities, but ecosystems of capability and opportunity. When Menon builds a training center, he's not just solving SOBHA's skilled labor problem—he's addressing India's vocational education crisis. When he adopts villages in Kerala, he's not just giving back to his homeland—he's demonstrating a model for rural development.

The contrast with typical corporate social responsibility is stark. Most companies do CSR because regulations require it, allocating the mandatory 2% of profits to various causes. SOBHA's approach predates these regulations and exceeds these requirements. It's not corporate social responsibility—it's personal social commitment.

But perhaps the most important legacy isn't the money given or the institutions built. It's the idea that business success comes with societal obligations. In an era of increasing inequality, where business leaders are often seen as extractive rather than contributive, Menon represents an older tradition—the industrialist as nation builder, the entrepreneur as social reformer.

The irony is palpable. The man who couldn't complete his education has enabled thousands to complete theirs. The boy who left India seeking opportunity has created opportunities for thousands to stay. The entrepreneur who built a business on backward integration has integrated business success with social impact in ways that move forward entire communities.

As SOBHA transitions to second-generation leadership, this philanthropic commitment faces its own succession test. Will Ravi Menon and future leaders maintain this sense of obligation? Will the Giving Pledge be honored not just in letter but in spirit? Will the institution building continue beyond the founder?

Early signs are encouraging. The family's commitment to the pledge, the continuation of trust activities, the expansion of SOBHA Academy—all suggest that the philanthropic DNA is being transmitted along with the business genes. But only time will tell if the giving culture proves as durable as the building quality.

XII. What We Learned & Final Thoughts

After eight hours of diving deep into SOBHA's story, what have we actually learned? Not just about one company, but about business, strategy, and the nature of competitive advantage itself?

First, the power of controlling your entire value chain. In an age where everyone preaches asset-light models and platform strategies, SOBHA proves that old-fashioned vertical integration can still create extraordinary value—if you're solving the right problem. The key insight: backward integration makes sense when quality is hard to verify, when trust is scarce, and when coordination costs exceed production costs. Most industries don't meet these criteria. Indian real estate does, overwhelmingly.

Second, when backward integration makes sense (and when it doesn't). The SOBHA model works because Indian real estate suffers from systemic quality problems that can't be solved through better contracting or supervision. You need to control the entire chain. But try this in software development or consulting or most services, and you'll create an expensive, inflexible monster. Context matters more than strategy.

Third, family business succession done right. The transition from PNC to Ravi Menon offers a masterclass in succession planning. Start early (Ravi joined in 2004, twenty years before taking over). Give real responsibility (he wasn't just sitting in board meetings). Allow evolution while maintaining core values (embrace technology but keep the quality obsession). Most importantly, the founder must actually let go—something PNC Menon appears willing to do.

Fourth, building quality as a brand differentiator. In commoditized industries, the temptation is to compete on price or financial engineering. SOBHA chose a harder path: compete on quality so superior that customers will pay premiums for it. This requires not just operational excellence but the patience to build reputation over decades. There are no shortcuts to trust.

Fifth, the importance of patient capital in real estate. The backward integration model required over ₹1,200 crores of investment before it started generating returns. Public markets with quarterly earnings pressure would never have allowed this. The 52.9% promoter holding isn't a governance negative—it's what made the entire strategy possible. Sometimes, patient capital is the ultimate competitive advantage.

Finally, why culture and values matter in commodity businesses. Real estate is ultimately about buying land, pouring concrete, and selling space. It's as commoditized as businesses get. Yet SOBHA commands premium pricing through culture—a culture of quality that permeates every employee, every process, every decision. Culture, it turns out, can be the ultimate differentiator in the most commoditized industries.

But perhaps the biggest lesson is about the nature of business itself. In our financialized age, we often forget that businesses are more than vehicles for generating returns. They're institutions that shape society, create capabilities, and transform possibilities. SOBHA didn't just build buildings—it built an entire ecosystem of quality in Indian construction. It didn't just generate profits—it generated craftsmen, engineers, and standards that elevated an entire industry.

The backward integration model is really a metaphor for something deeper: the idea that to create extraordinary value, sometimes you have to go backward before you can go forward. You have to master the basics before you can innovate. You have to control the fundamentals before you can scale. You have to build depth before you can achieve breadth.

This runs counter to everything modern business strategy teaches. We're told to focus, to outsource, to leverage other people's capabilities. And most of the time, that's right. But occasionally, in specific contexts with particular problems, the opposite strategy—own everything, control everything, be responsible for everything—creates insurmountable advantages.

The question for investors isn't whether SOBHA is a good company—it clearly is. The question is whether it's a good investment at current valuations. The answer depends on your beliefs about Indian real estate's evolution. If you believe India will increasingly demand global quality standards, if you believe trust will command increasing premiums, if you believe operational excellence will matter more than financial engineering, then SOBHA is positioned to benefit disproportionately.

But there's a deeper question about what we want from our businesses. Do we want efficient capital allocators that maximize returns? Or do we want institution builders that transform industries? SOBHA suggests these aren't mutually exclusive, but achieving both requires patience, commitment, and a willingness to be misunderstood for long periods.

The story of SOBHA is really the story of modern India—a country transforming from acceptance of "good enough" to insistence on world-class quality. It's the story of businesses evolving from family enterprises to professional institutions. It's the story of entrepreneurs who see business not as separate from society but as instruments for social transformation.

As we close this deep dive, one image stays with me: PNC Menon at 26, leaving Kerala for Oman with nothing but ambition. Fifty years later, he's built not just a company worth ₹16,000 crores, but an institution that has transformed how Indians think about quality in real estate. From laying tiles to laying the foundation for an entire industry's transformation.

That's not just a business success story. That's a blueprint for how businesses can create value that transcends financial returns. In an era where we often debate stakeholder capitalism versus shareholder capitalism, SOBHA offers a different model: build something so good, with such integrity, that all stakeholders benefit naturally.

The boy who couldn't afford school built schools. The man who started with nothing is giving away billions. The company that everyone said was too capital-intensive, too integrated, too obsessed with quality, has outlasted and outperformed its critics.

Sometimes, the best strategy is to ignore strategy and focus on building something extraordinary. One concrete block at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube