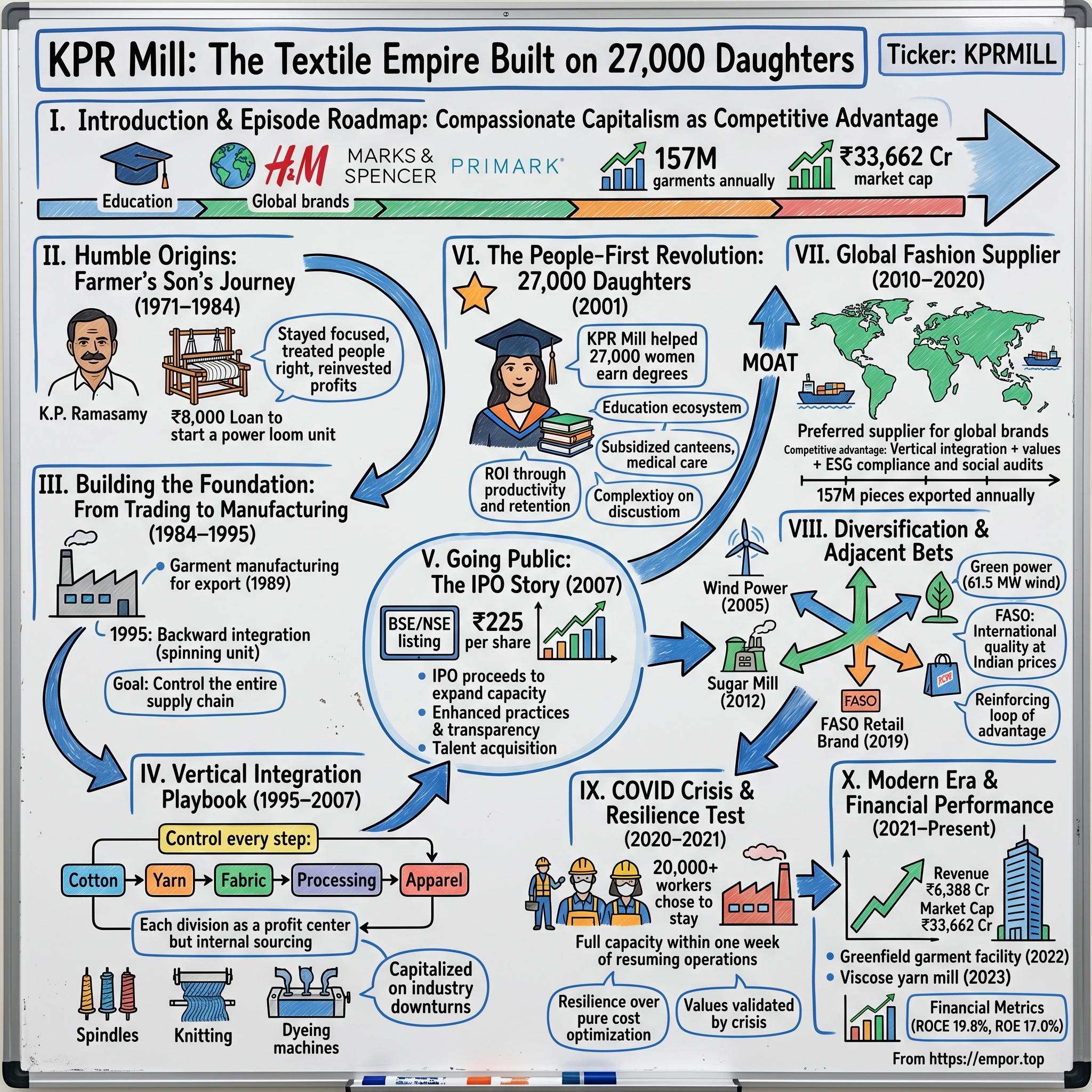

KPR Mill: The Textile Empire Built on 27,000 Daughters

I. Introduction & Episode Roadmap

Picture this: In a nondescript conference room in Coimbatore, a young mill worker approaches the chairman of her company with an unusual request. She doesn't want a raise or a promotion. She wants to complete her education—something poverty had stolen from her years ago. The chairman, K.P. Ramasamy, doesn't just approve her request. He sets up a correspondence program for 50 women workers. Today, that program has helped 27,000 women earn degrees, some even MBAs, while working full-time at what would become one of India's most valuable textile companies.

This is KPR Mill—a ₹33,662 crore market cap giant that produces 157 million garments annually for global brands like H&M, Marks & Spencer, and Primark. It's vertically integrated from cotton yarn to finished apparel, operates wind farms and sugar mills, and somehow maintains operating margins that make competitors weep. But the numbers only tell half the story.

How did a farmer's son who dropped out of school and started with an ₹8,000 loan build one of India's textile powerhouses? How did a company in a commoditized, labor-intensive industry create such a defensible moat that it trades at a P/E of 40.8—premium valuations typically reserved for tech companies? And why do 100% of its workers choose to stay during a pandemic when factories across India emptied?

The answer lies in a uniquely Indian story of what happens when you combine vertical integration, counter-cyclical thinking, and treating 27,000 female workers not as labor inputs but as daughters. It's a playbook that shouldn't work in cutthroat global fashion supply chains—yet it does, spectacularly.

Today we're diving deep into KPR Mill's five-decade journey from power looms to global fashion supplier, examining how compassionate capitalism became a competitive advantage, why vertical integration matters more than ever in volatile markets, and what modern founders can learn from a company that built wealth by empowering the poorest.

II. The Humble Origins: A Farmer's Son's Journey (1971–1984)

The India of 1971 was a different universe. Indira Gandhi had just swept to power with her "Garibi Hatao" slogan. The License Raj strangled entrepreneurship. And in rural Tamil Nadu, a young man named K.P. Ramasamy faced a choice that would define not just his life, but thousands of others.

Ramasamy came from an agricultural family with no manufacturing background, no connections, and certainly no capital. Financial hardship had forced him to drop out of school—a wound that would later drive his obsession with education for others. But he had something else: an uncle willing to lend him ₹8,000 and brothers who believed in his vision.

With that modest loan—worth perhaps ₹4 lakhs in today's money—Ramasamy didn't aim for the stars. He started a power loom cloth manufacturing unit. Not glamorous. Not innovative. Just practical. Power looms were the workhorses of India's textile industry, sitting between handlooms and modern mills. They required less capital than mills but offered better productivity than handlooms.

The pre-liberalization textile landscape was Byzantine. The government's Textile Policy divided the industry into three segments: handlooms (protected for employment), power looms (the middle child), and organized mills (heavily regulated). Each had quotas, restrictions, and bureaucratic mazes. Ramasamy navigated this by staying small, staying focused, and most importantly, staying honest in an industry rife with tax evasion and labor exploitation.

What set him apart wasn't technology or capital—it was values. While other mill owners saw workers as costs to minimize, Ramasamy saw them as extended family. While others cut corners on quality, he obsessed over every thread. These weren't business strategies; they were simply how he believed business should be done. His younger brothers joined him, bringing complementary skills—one was a chartered accountant, another had a knack for operations.

By 1984, after thirteen years of grinding it out in power looms, the brothers were ready for something bigger. They incorporated KPR Mill, naming it after the patriarch. They had no idea they were laying the foundation for what would become a ₹33,000 crore empire. But they had learned crucial lessons: treat people right, control quality obsessively, and reinvest every rupee back into growth.

The timing was fortuitous. India was slowly awakening from its socialist slumber. Export markets were opening up. And the global fashion industry was beginning its decades-long search for reliable, large-scale suppliers. KPR Mill was about to ride a wave it couldn't yet see coming.

III. Building the Foundation: From Trading to Manufacturing (1984–1995)

The late 1980s brought seismic shifts to Indian textiles. The government, desperate for foreign exchange, began incentivizing exports. Global brands started looking beyond East Asia. And in 1989, KPR Mill made a pivotal decision: instead of just making fabric, they would manufacture fashion apparel for export.

This wasn't an obvious move. Garment manufacturing required different skills, equipment, and critically, relationships with international buyers who had exacting standards. Most Indian textile companies stayed in their lanes—spinners spun, weavers wove, and garment makers stitched. But Ramasamy saw something others missed: the real value wasn't in any single process but in controlling the entire chain.

The export market of 1989 was brutal for Indian companies. Buyers demanded consistent quality, on-time delivery, and compliance with labor standards that many Indian factories couldn't meet. KPR's early approach was refreshingly simple: under-promise and over-deliver. While competitors chased volume with aggressive pricing, KPR focused on building trust with smaller orders executed flawlessly.

The company's first major breakthrough came through a European buyer who needed a reliable backup supplier. The order was small—just 50,000 pieces—but KPR delivered early, with quality that exceeded specifications. Word spread in the tight-knit community of international fashion buyers. By 1991, they were handling orders of 500,000 pieces.

But Ramasamy realized they were still at the mercy of yarn and fabric suppliers. Price fluctuations, quality inconsistencies, and delivery delays upstream cascaded into problems downstream. The solution was radical for its time: backward integration. In 1995, KPR set up its first spinning unit in Sathyamangalam with 6,000 spindles to produce cotton hosiery yarn.

The Sathyamangalam location was strategic. It sat in Tamil Nadu's cotton belt, reducing transportation costs. Land was affordable. Labor was available. But most importantly, it was far from the labor unrest that plagued urban textile centers. KPR could build its unique culture from scratch.

The economics of the spinning unit were compelling. By producing their own yarn, KPR captured margins that previously went to suppliers. Quality control started at the cotton stage. And during demand downturns, they could sell excess yarn to other manufacturers, creating a natural hedge.

This period also saw the emergence of KPR's distinctive management philosophy. While other companies hired and fired with market cycles, KPR maintained stable employment. While others squeezed suppliers and workers, KPR shared profits through bonuses and benefits. It seemed naive, even foolish, in the cutthroat textile industry. But it was building something invaluable: loyalty.

By 1995, KPR Mill had evolved from a trading company to a manufacturer with backward integration capabilities. Revenue had grown from lakhs to crores. But more importantly, they had proven a hypothesis: in a commoditized industry, the combination of vertical integration and values-based management could create differentiation. The stage was set for massive scaling.

IV. The Vertical Integration Playbook (1995–2007)

The late 1990s marked KPR's transformation from a modest textile player to a vertically integrated powerhouse. While competitors debated the merits of specialization versus integration, Ramasamy had already made his choice. The company would control every step from cotton to clothing.

The first spinning mill, established in 1996, started with 6,000 spindles. By 2007, KPR operated 111,264 spindles across multiple units. But this wasn't just about adding capacity. Each expansion was strategically timed during industry downturns when equipment was cheap and contractors desperate for work. "The right time to start a project is during the dull phase," became Ramasamy's mantra—a contrarian approach that would define KPR's capital allocation strategy.

The economics of vertical integration in textiles are compelling but complex. A typical garment goes through multiple stages: cotton to yarn (spinning), yarn to fabric (knitting/weaving), fabric processing (dyeing/printing), cutting, and finally stitching. At each stage, standalone players add their margins, typically 8-12%. By controlling all stages, KPR captured cumulative margins of 40-50% while maintaining price competitiveness.

But integration brought challenges. Each process required different expertise. Spinning was capital-intensive and technology-driven. Knitting needed precision and consistency. Processing involved chemistry and environmental compliance. Garment manufacturing was labor-intensive and detail-oriented. Most companies struggled to excel across this spectrum. KPR's solution was elegant: treat each division as a profit center with its own P&L, but mandate internal sourcing at market prices.

The company added knitting capacity in 1998, processing capabilities in 2001, and continuously expanded garment manufacturing. By 2005, they had created a fully integrated ecosystem where cotton entered one end and finished garments emerged from the other. The entire process, from fiber to fashion, happened within a 50-kilometer radius in Tamil Nadu.

This integration created unexpected advantages. When cotton prices spiked, KPR's yarn division benefited, offsetting pressure on garment margins. When international demand slowed, excess capacity could serve domestic markets. Quality issues could be traced and fixed at the source. Lead times shortened from 90 days to 45 days—crucial for fast fashion clients.

The numbers tell the story. Between 1995 and 2007, revenue grew at a CAGR of over 30%. EBITDA margins expanded from single digits to over 20%. Return on capital employed consistently exceeded 25%. But perhaps most remarkably, this growth was largely self-funded. While competitors leveraged aggressively, KPR maintained conservative debt levels, funding expansion through internal accruals.

The vertical integration strategy also shaped KPR's workforce approach. With operations spanning multiple processes, workers could be cross-trained and redeployed based on demand. Career paths emerged from shop floor to management. The company's unique education programs made more sense when workers could aspire to roles across the value chain.

By 2007, KPR Mill had become a textbook case of successful vertical integration. But Ramasamy knew that to scale further, they needed external capital and institutional credibility. The company was ready for its next chapter: going public.

V. Going Public: The IPO Story (2007)

The conversation that changed KPR Mill's trajectory happened almost by accident. In 2003, K.P. Ramasamy's brother Nataraj, the family's chartered accountant, was discussing business with a friend. The friend asked a simple question: "What's your vision for this business beyond your generation?" That question haunted Nataraj. The family had built something special, but it remained a closely-held private company. Going public wasn't just about raising capital—it was about institutional permanence.

The path to IPO took four years of preparation. KPR had to transform from a family-run enterprise to a professionally managed corporation. This meant implementing robust financial controls, establishing independent board oversight, and most challengingly, opening their books to scrutiny. For a company that had operated on handshakes and trust, the compliance requirements were cultural shock therapy.

The IPO, launched on August 2, 2007, was priced at ₹225 per share, aggregating ₹133.02 crores. The timing seemed terrible. Global markets were jittery with early signs of the subprime crisis. Indian markets had corrected 15% from their peaks. Investment bankers suggested waiting. But Ramasamy, true to his contrarian philosophy, saw opportunity in others' fear.

The IPO roadshow revealed something interesting. While institutional investors grilled them about working capital cycles and capital allocation, they kept returning to one theme: how did KPR maintain such high employee retention in an industry notorious for 30-40% annual attrition? The answer—treating workers like family—seemed too simple to be true. Several investors visited the factories, expecting to find creative accounting. Instead, they found workers pursuing correspondence degrees during breaks and speaking about five-year career plans.

The issue was subscribed 1.8 times—modest by Indian IPO standards but respectable given market conditions. On August 28, 2007, KPR Mill listed on both BSE and NSE. The stock opened at ₹241, a 7% premium to the issue price. Within weeks, it would be tested by the global financial crisis.

Post-IPO, KPR's capital allocation remained remarkably disciplined. While newly-listed companies often splurge on acquisitions or unrelated diversification, KPR stuck to its knitting—literally. The IPO proceeds went toward expanding spinning capacity and upgrading technology. The company also did something unusual: it maintained its high dividend payout ratios, signaling confidence in cash generation.

The institutional scrutiny that came with being public actually strengthened KPR's practices. Quarterly earnings calls forced management to articulate strategy clearly. Analyst coverage brought visibility to their unique model. Corporate governance requirements formalized what had been informal family values. The company discovered that transparency, rather than threatening their competitive advantage, actually enhanced it.

One unexpected benefit of going public was talent acquisition. The ESOP program could now offer real liquidity. Professional managers who might have hesitated to join a family-run company saw the institutional framework. The company could benchmark compensation to market rates. This professionalization would prove crucial for the next phase of growth.

By 2008, as the financial crisis devastated global markets, KPR Mill's stock had fallen 60% from its listing price. But the company's fundamentals remained strong. Order books were full. Margins held steady. And Ramasamy, remembering his principle about dull phases being the best time to invest, began planning the company's most ambitious expansion yet. The IPO hadn't just brought capital—it had brought the discipline and credibility needed to execute at scale.

VI. The People-First Revolution: 27,000 Daughters

The moment that would define KPR Mill's soul happened in 2001. A young mill worker, barely 18, approached Chairman K.P. Ramasamy during a factory visit. She didn't ask for a raise or better working conditions. She asked if he could help her complete her education—something poverty had forced her to abandon. Ramasamy didn't just say yes. He asked how many others wanted the same opportunity.

Within weeks, KPR had arranged a correspondence program for 50 women workers. The company partnered with Alagappa University to conduct classes on-site. Teachers came to the factory. Study materials were provided free. Work schedules were adjusted to accommodate exam preparation. The initial results stunned everyone: these women, many of whom had been out of school for years, passed their +2 examinations with distinction.

But Ramasamy saw something beyond academic success. These educated workers made fewer errors, suggested process improvements, and most remarkably, stayed with the company. In an industry where annual attrition of 30-40% was normal, KPR's educated workers showed attrition rates below 5%. The ROI was undeniable, but for Ramasamy, it was never about ROI.

The program scaled rapidly. By 2010, over 5,000 women had completed their basic education. Some went further, pursuing bachelor's degrees in commerce and arts. A few even completed MBAs while working full-time on the shop floor. The company established libraries, computer centers, and study halls within factory premises. What started as correspondence courses evolved into a full-fledged education ecosystem.

The numbers are staggering: 27,000 women have now completed their education through KPR's programs. But the real impact goes beyond diplomas. These women send their children to English-medium schools. They make financial decisions for their families. They've broken generational cycles of poverty. And 194 of them have leveraged their education to land jobs at companies like Tata Electronics, Tech Mahindra, and Titan—which Ramasamy celebrates rather than laments.

"We treat these women like we would treat our own daughters," Ramasamy often says. This isn't corporate PR speak. The company provides free transportation from 200 villages. It runs subsidized canteens serving nutritious meals. It offers free medical care including annual health checkups. During festivals, workers receive bonuses equal to several months' salary. The company even maintains marriage halls that workers can use free for family functions.

The economic impact of this approach is counterintuitive but powerful. KPR's labor cost as a percentage of revenue is actually lower than industry averages, despite higher per-worker spending. The reason? Productivity. Educated workers produce 20-30% more output per shift. Quality defect rates are 50% lower. The need for supervision is minimal. Workers train each other, creating a self-reinforcing culture of excellence.

During the COVID-19 lockdown in 2020, this people-first approach faced its ultimate test. While factories across India sent workers home, KPR gave its 20,000+ workers a choice: stay with full salary, food, shelter, and even entertainment, or leave. The result? "100 percent of the people said we will stay here only," recalls the management. When operations resumed, KPR ramped to full capacity within a week while competitors struggled for months to rebuild their workforce.

The model has created an unusual competitive moat. Fashion brands increasingly demand ESG compliance and social audits. While competitors scramble to meet minimum standards, KPR exceeds them naturally. Buyers visit expecting to find sweatshops; they find workers discussing production optimization while pursuing distance education degrees. This has become KPR's most powerful marketing tool.

The 27,000 daughters program has also transformed KPR's innovation capacity. Workers who understand both production realities and theoretical principles suggest improvements that outside consultants might miss. The company holds monthly innovation meetings where workers present ideas. The best ones are implemented with the suggesting worker leading the rollout. It's bottom-up innovation at scale.

Critics argue this model isn't replicable—that it requires patient capital and long-term thinking incompatible with quarterly earnings pressure. They're probably right. But that's exactly the point. KPR's people-first approach isn't easily copied, making it a sustainable competitive advantage. In an industry racing to the bottom on costs, KPR has won by racing to the top on human capital.

VII. Global Fashion Supplier: Breaking Into International Markets (2010–2020)

By 2010, KPR Mill had evolved from a yarn-and-fabric maker into a serious garment exporter, producing 50 million pieces annually. But the real transformation was about to begin. The global fashion industry was undergoing its own revolution—fast fashion was accelerating, supply chains were consolidating, and buyers were desperately seeking suppliers who could deliver quality, scale, and compliance. KPR was perfectly positioned.

The numbers tell only part of the story: 157 million knit garments exported annually, generating 40% of revenue, supplied to marquee brands like Marks & Spencer, H&M, and Primark. But how does a company from Coimbatore compete with Bangladesh on price, Vietnam on trade preferences, and China on scale? The answer lay in KPR's unique value proposition: vertical integration plus values.

Breaking into global fashion wasn't about cold-calling buyers. It started with relationships. KPR's first major breakthrough came through a British buyer who visited the factory in 2008 during the financial crisis. While competitors were cutting corners to maintain margins, KPR had maintained quality standards and worker benefits. The buyer placed a small trial order. Six months later, after flawless execution, that order had grown 10x.

The fashion industry's dirty secret is that most suppliers can't actually supply. They take orders, then scramble to source fabric, book capacity, and hire workers. Delays are endemic. Quality varies by batch. Social compliance is often theatrical. KPR offered something radical: genuine vertical integration where cotton entered one gate and finished garments left another, all within their control.

This integration advantage became crucial as fast fashion accelerated. H&M wanted styles to go from design to store shelf in 21 days. Most suppliers needed 90 days just for procurement. KPR could commit to 45-day delivery because they controlled every step. When cotton prices spiked 50% in 2011, competitors faced margin compression or contract violations. KPR absorbed the shock through their spinning division's windfall profits.

But the real differentiation came from compliance and sustainability. By 2015, fashion brands faced mounting pressure over supply chain ethics. The Rana Plaza disaster had awakened consumers to sweatshop realities. Brands needed suppliers who could pass increasingly stringent social audits. KPR didn't need to prepare for audits—their everyday operations exceeded standards.

The company's pitch to global brands was compelling: "We're not the cheapest, but we're the most reliable." While Bangladesh offered 20% lower prices, hidden costs emerged through delays, quality issues, and compliance failures. KPR's total cost of ownership was actually lower. Brands could visit anytime without notice. Workers were genuinely empowered, not coached for audits. The 27,000 educated women became KPR's best advertisement.

Scaling from 50 million to 157 million garments required massive capital investment. But true to form, KPR expanded counter-cyclically. The 2011-2013 Indian economic slowdown saw textile valuations crash. KPR acquired equipment at distressed prices. They hired talented managers from struggling competitors. By 2014, when demand recovered, KPR had capacity while competitors scrambled to expand.

The client concentration strategy was deliberate. Rather than chasing hundreds of small buyers, KPR focused on 20-30 strategic relationships. They embedded themselves in clients' supply chains, understanding design preferences, quality requirements, and commercial pressures. Some clients contributed over ₹500 crores in annual revenue. This concentration risk was mitigated by multi-year contracts and deep operational integration.

Technology adoption accelerated during this period. KPR implemented SAP for real-time inventory tracking. RFID tags traced garments through production. Digital pattern-making reduced sampling time. Video analytics optimized production lines. But technology augmented rather than replaced human judgment. The educated workforce could actually utilize these tools effectively, unlike competitors struggling with basic computer literacy.

By 2020, KPR had become a preferred supplier for global fashion's biggest names. The company's garment exports showed a 25% CAGR over the decade. Margins remained stable despite pricing pressure. But most importantly, KPR had proven that Indian textile companies could compete globally not just on cost but on capability. The next frontier would be capturing even more value through retail and brand building.

VIII. Diversification & Adjacent Bets (2005–Present)

While KPR Mill's core story centers on textiles, the company's diversification strategy reveals sophisticated thinking about capital allocation, risk management, and sustainability. These weren't random bets—each adjacency leveraged existing capabilities or created strategic synergies.

The wind power venture, initiated in 2005, seemed puzzling initially. Why would a textile company invest in windmills? The answer was brilliantly practical. Tamil Nadu suffered from chronic power shortages that disrupted manufacturing. The state's wind corridor offered excellent generation potential. And government incentives made the economics attractive. KPR installed windmills with 61.5 MW capacity, ensuring uninterrupted power for operations while selling excess to the grid.

But Ramasamy's environmental drive went deeper. The textile industry is notoriously polluting—consuming vast quantities of water and energy while generating chemical waste. KPR's green power initiatives weren't just about cost savings or compliance. They reflected genuine environmental consciousness. The company established co-generation plants, solar installations, and achieved zero liquid discharge years before regulations mandated it.

The sugar mill venture in 2012 followed similar logic. Coimbatore district had abundant sugarcane cultivation. The mill could generate ethanol for industrial use and molasses for distilleries. Bagasse, the fibrous residue, fueled co-generation plants. Every byproduct found purpose. The integration was elegant: power from windmills and co-gen plants powered textile operations, which generated profits to fund more green investments.

The 2019 launch of FASO, KPR's retail brand, marked a pivotal strategic shift. For decades, KPR had manufactured garments that sold for $20-50 in Western stores while receiving $3-5 per piece. The value capture opportunity was obvious. But private label retail is littered with manufacturing companies that failed to build brands. KPR's approach was characteristically patient—starting with company-owned stores in Tamil Nadu before expanding gradually.

FASO leveraged KPR's manufacturing prowess to offer premium quality at competitive prices. The vertical integration that served B2B clients now served consumers directly. Design-to-shelf time was weeks, not months. Inventory risk was minimal since unsold items could be redirected to export clients. The brand positioned itself as "international quality at Indian prices"—a compelling proposition for India's aspirational middle class.

The education venture deserves special mention. In 2009, KPR established the K.P.R. Institute of Engineering and Technology. This wasn't vanity project or CSR obligation. The institute focused on technical education relevant to modern manufacturing—textile technology, mechanical engineering, computer applications. Graduates often joined KPR, bringing fresh perspectives. The institute also conducted research on sustainable textiles and process optimization.

KPR's automobile component subsidiary, K.P.R. Industries, manufactured precision components for commercial vehicles. While seemingly unrelated to textiles, it leveraged similar capabilities: precision manufacturing, quality control, and supply chain management. The subsidiary remained small relative to textiles but provided portfolio diversification and learning opportunities.

Each diversification followed patterns. First, identify adjacencies with strategic logic. Second, start small and prove the concept. Third, scale gradually using internal resources. Fourth, maintain focus on the core business. Textiles still contributed 85% of revenue. The adjacent bets were options on future growth, not distractions from present operations.

The financial discipline across ventures was remarkable. Each business had to meet hurdle rates for return on capital. Cross-subsidization was forbidden—every unit stood on its own merits. This prevented the empire-building that destroyed many Indian conglomerates. It also created internal competition that drove efficiency.

By 2020, KPR's diversification strategy had created a resilient portfolio. When textile demand slumped, power generation provided stable cash flows. When cotton prices spiked, the sugar business hedged agricultural exposure. The retail brand captured downstream value. The education institute built human capital. Each piece reinforced the whole, creating what strategists call a "reinforcing loop" of competitive advantage.

IX. COVID Crisis & Resilience Test (2020–2021)

March 24, 2020. India announces the world's strictest lockdown. Factories must shut immediately. Workers have four hours to reach home before transportation stops. Across the country, biblical scenes unfold—millions of migrant workers walking hundreds of kilometers to their villages. The textile industry, dependent on daily-wage laborers, faces existential crisis.

At KPR Mill's facilities in Coimbatore, something different happens. Management gathers 20,000+ workers and makes an unprecedented offer: "If you stay, we will provide food, shelter, full salary, and entertainment. If you leave, we'll arrange transportation and welcome you back whenever you return." The choice is yours.

The response stunned even Ramasamy: "100 percent of the people said we will stay here only."

Think about that. While workers across India fled industrial centers, fearing starvation and abandonment, every single KPR worker chose to stay. This wasn't compliance or coercion. This was trust, accumulated over decades, paying its ultimate dividend.

The logistics of housing and feeding 20,000 people during indefinite lockdown were staggering. KPR converted training centers into dormitories. The company kitchens, designed for regular meals, now operated round-the-clock. Medical teams conducted daily health monitoring. But beyond basic needs, KPR understood the psychological challenge. They organized movie screenings, sports tournaments, and skill development programs. Workers used the time to complete online courses. Some learned new trades. The factory became a self-contained township.

The financial implications were severe. Revenue dropped to zero overnight. Fixed costs—salaries, interest, maintenance—continued burning cash. Many companies would have invoked force majeure, furloughed workers, and preserved capital. KPR did the opposite. They paid full salaries, maintained benefits, and even distributed additional support for workers' families in villages.

"What would have happened if the lockdown had extended to 6 months?" management later reflected. "Revenue was zero. Expenses were running into crores." The company had sufficient reserves to survive a year without revenue—a testament to conservative financial management. But Ramasamy wasn't thinking about survival. He was thinking about competitive advantage.

When Tamil Nadu permitted textile operations to resume in May 2020, KPR faced none of the challenges plaguing competitors. No need to recall workers from villages. No need to quarantine returning migrants. No need to rebuild team dynamics. Within one week—seven days—KPR reached 100% capacity utilization. Competitors took months to reach 50%.

The operational advantage translated into commercial advantage. International buyers, desperate for reliable suppliers as global supply chains fragmented, shifted orders to whoever could deliver. KPR could commit to schedules while competitors couldn't guarantee workforce availability. Orders that might have taken years to win through competitive bidding landed in weeks through sheer execution capability.

The pandemic accelerated existing trends favorable to KPR. Brands wanted supply chain resilience over pure cost optimization. Social compliance became non-negotiable as COVID highlighted worker vulnerability. The China-plus-one strategy gained urgency. India's production-linked incentive schemes favored integrated manufacturers. Every trend pointed toward KPR's model.

Financial performance during this period defied logic. While FY2020-21 saw industry-wide carnage, KPR's revenue declined only 8%. EBITDA margins actually expanded as raw material costs dropped faster than selling prices. The company generated positive cash flow throughout the crisis. The stock, which had crashed 40% in March 2020, recovered to all-time highs by year-end.

But the real victory wasn't financial. It was cultural. The crisis validated everything KPR stood for. Workers who experienced the company's support became evangelists. Their stories spread through villages, attracting quality talent. Clients who witnessed KPR's resilience deepened relationships. Even competitors acknowledged grudging respect.

The pandemic also revealed hidden strengths. The educated workforce adapted quickly to COVID protocols. Digital literacy enabled remote coordination. The vertical integration that seemed capital-heavy provided supply chain control. The conservative balance sheet that looked inefficient provided crisis flexibility. Every supposed weakness became a strength when stress-tested.

X. Modern Era & Financial Performance (2021–Present)

The post-pandemic era has been KPR Mill's golden period. In 2024, revenue reached ₹6,388 crores, up 5.42% year-over-year. Earnings touched ₹815 crores. The stock trades at ₹690, giving it a market capitalization of ₹33,662 crores. These numbers would be impressive for any company. For a textile manufacturer in a commoditized industry, they're extraordinary.

The garment division has been the standout performer, achieving 25% CAGR over the past decade. From 50 million pieces in 2010 to 157 million pieces today, the scale expansion has been methodical. The March 2022 greenfield facility added 42 million pieces capacity at precisely the moment when global brands were diversifying away from China. Timing, as always with KPR, was impeccable.

The ₹100-crore viscose yarn spinning mill commissioned in 2023 represents KPR's evolution beyond cotton. Viscose, derived from wood pulp, offers different properties—softness, breathability, moisture absorption. Fashion trends increasingly favor cotton-viscose blends. By backward integrating into viscose yarn, KPR can now offer complete solutions for blended fabrics, further differentiating from cotton-focused competitors.

The financial metrics tell a story of exceptional capital efficiency. Return on capital employed (ROCE) stands at 19.8%, remarkable for a capital-intensive industry. Return on equity (ROE) at 17.0% reflects conservative leverage—the company could juice returns through debt but chooses stability. The dividend yield of 0.51% seems low, but this reflects reinvestment for growth rather than capital starvation.

What's driving this performance? First, pricing power from integration. When cotton prices fluctuate, KPR adjusts transfer pricing between divisions to optimize taxes and margins. Second, operational leverage from scale. Fixed costs spread across growing volumes drive margin expansion. Third, premium realization from ESG compliance. Brands pay 5-10% premiums for suppliers who exceed social standards.

The company's capacity expansion continues aggressively. Current plans include adding 30 million garment pieces annually for the next three years. New spinning capacity of 50,000 spindles is under implementation. The retail division targets 100 FASO stores by 2027. Each expansion is self-funded, maintaining the zero-debt philosophy that has served KPR well.

Working capital management deserves special mention. In an industry notorious for stretched receivables and inventory buildup, KPR maintains negative working capital cycles. How? Suppliers trust KPR's payment record, offering favorable terms. Customers pay advances for capacity allocation. Inventory turns rapidly through vertical integration. This capital efficiency funds growth without external borrowing.

The market's premium valuation—P/E of 40.8 versus industry average of 15-20—reflects several factors. First, earnings quality and consistency. Second, ESG credentials increasingly important to institutional investors. Third, operating leverage potential as capacity expands. Fourth, optionality from retail and new ventures. The market is betting that KPR's model will continue outperforming in an industry facing structural challenges.

Technology investments are accelerating. KPR is implementing AI-driven demand forecasting, automated quality inspection, and predictive maintenance. But unlike peers chasing full automation, KPR sees technology as augmenting human capability. The educated workforce can leverage sophisticated tools that would be wasted in traditional factories.

International expansion beyond exports is under consideration. KPR evaluates manufacturing facilities in Africa, leveraging trade preferences and lower labor costs. Joint ventures in Bangladesh could access duty benefits. But true to character, expansion will be gradual, self-funded, and culturally aligned. No transformative acquisitions or debt-funded empire building.

The sustainability initiatives go beyond compliance. KPR targets carbon neutrality by 2030 through renewable energy and process optimization. Water consumption per garment has dropped 40% through recycling and efficient dyeing. These aren't just ESG checkboxes—they're cost advantages as resource prices rise and regulations tighten.

XI. Playbook: Business & Leadership Lessons

The KPR story offers a masterclass in building competitive advantage in commoditized industries. While business schools teach differentiation through innovation or branding, KPR achieved it through integration and values. The playbook is deceptively simple but extraordinarily difficult to execute.

Vertical Integration as Strategy, Not Tactics: Most companies integrate to reduce costs or ensure supply. KPR integrated to capture value and control quality. The difference is strategic. Cost reduction is temporary—competitors can match it. Value capture is structural—it changes industry economics. By controlling cotton to garment, KPR captures 40-50% margins versus 8-12% for specialized players.

Counter-Cyclical Capital Allocation: "The right time to start a project is during the dull phase" isn't just contrarian wisdom—it's mathematical logic. Equipment costs drop 30-40% during downturns. Construction contractors offer discounts. Talented managers become available. When demand recovers, new capacity meets rising prices. KPR's major expansions—1996, 2008, 2013, 2020—all came during crisis periods.

People as Moat, Not Cost: The 27,000 daughters program seems like expensive corporate social responsibility. It's actually brilliant strategy. Educated workers are 20-30% more productive. Attrition below 5% versus industry average of 30-40% saves recruitment and training costs. Premium realization from ESG compliance adds 5-10% to margins. The math works, but only with decades-long time horizons.

Trust-Based Relationships: In an industry of transactional relationships, KPR builds partnerships. Suppliers get consistent orders and prompt payments. Workers get education and dignity. Customers get reliability and transparency. These relationships become switching costs. A competitor offering 5% lower prices can't overcome decades of trust.

Financial Conservatism: KPR's debt-to-equity ratio rarely exceeds 0.5 versus industry average of 1.5-2.0. This seems inefficient—leverage could boost returns. But it provides crisis resilience. During downturns, leveraged competitors face distress while KPR expands. The tortoise beats the hare through economic cycles.

Cultural Coherence: Every decision reflects core values. Treat workers like family. Maintain quality regardless of cost. Honor commitments despite market conditions. These aren't policies that can be copied. They're beliefs that must be lived. This coherence creates predictability that stakeholders value.

Gradual Scaling: KPR never bet the company on transformation. Each expansion was incremental, proven, then scaled. This seems slow versus moon-shot strategies. But it compounds. Steady 20% annual growth for 30 years creates more value than sporadic 50% growth with occasional zeros.

The Compassionate Capitalism Paradox: Setting up a for-profit business with compassionate capitalism mindset helped transform KPR into a formidable force. This seems contradictory—capitalism is supposedly cutthroat. But compassion created loyalty, loyalty drove productivity, productivity enabled competitiveness. The paradox resolves when you extend time horizons.

For modern founders, the lessons are profound. In the age of blitzscaling and growth-at-all-costs, KPR proves that patient capital and values-based management can build enduring value. In industries dismissed as sunset or commoditized, integration and execution can create differentiation. In the war for talent, treating people with dignity becomes competitive advantage.

The playbook won't work everywhere. It requires patient capital that public markets rarely provide. It needs leadership committed to values despite quarterly pressures. It demands operational excellence that most companies can't sustain. But for those who can execute it, the rewards are exceptional.

XII. Analysis & Investment Case

The investment case for KPR Mill presents a fascinating study in contrasts. The stock trades at premium valuations—P/E of 40.8, P/B of 4.7—typically reserved for technology or consumer companies. Yet this is a textile manufacturer in a cyclical, commoditized industry. Understanding this disconnect requires examining both the bull and bear cases.

The Bull Case: KPR is not a textile company but an execution machine that happens to make textiles. The 19.8% ROCE and 17% ROE are sustainable through the cycle. Vertical integration provides margin resilience. The educated workforce creates productivity advantages. ESG compliance attracts premium customers. India's rising manufacturing competitiveness, potential UK-India FTA, and production-linked incentives provide multi-year tailwinds. The retail venture offers optionality for value capture. Management's track record of capital allocation deserves premium valuation.

The Bear Case: Textile remains a cyclical commodity business subject to cotton price volatility and fashion demand swings. The premium valuation leaves no room for error. Succession planning remains unclear despite next-generation involvement. Labor-intensive manufacturing faces long-term automation threats. Bangladesh and Vietnam offer structural cost advantages. Client concentration creates vulnerability. The compassionate capitalism model depends on founder-leadership and may not survive generational transition.

Competitive Positioning: Versus Vardhman Textiles (similar integration, lower margins), KPR shows superior execution. Against Arvind Limited (denim focus, brand portfolio), KPR has better capital efficiency. Compared to Page Industries (outsourced manufacturing, brand licensing), KPR lacks pricing power but controls production. Each peer represents different strategic choices, but none match KPR's unique combination of integration, values, and execution.

Growth Drivers: Export opportunities remain robust as fashion brands diversify supply chains. India's textile exports could double from $40 billion to $80 billion by 2030. KPR's capacity expansions position it to capture disproportionate share. The UK-India FTA could reduce duties by 9.6%, improving competitiveness. Domestic consumption growth as India's per-capita income rises offers additional runway. The FASO retail brand, though nascent, could become material if execution matches ambition.

Key Risks: Cotton price volatility remains perpetual threat, though vertical integration provides hedging. Global recession would hurt discretionary apparel spending. ESG requirements could intensify, raising compliance costs. Succession planning needs clarity—will next generation maintain founder values? Technology disruption through automation or 3D printing could undermine labor-based advantages. Trade wars or protectionism could disrupt export markets.

Valuation Framework: The market values KPR using multiple lenses. As a manufacturing company, 20x P/E seems full. As an ESG leader, 30x seems reasonable. As a play on India's manufacturing renaissance, 40x might be justified. The truth likely lies between these extremes. The company's consistent 20%+ ROE justifies premium to book value. The question is whether current valuations already discount perfect execution.

Financial Health: The balance sheet remains fortress-like. Debt-to-equity at 0.3x provides downturn protection. Cash generation funds all expansion without external capital. Working capital efficiency creates natural hedge. The only concern is whether excessive conservatism limits growth potential. Could judicious leverage accelerate expansion without compromising stability?

Management Quality: The founder-led management shows exceptional execution over decades. Capital allocation has been stellar. Governance standards exceed requirements. The commitment to values seems genuine, not performative. However, key-man risk is real. The transition to professional management while maintaining culture will be critical.

ESG Considerations: KPR's social initiatives go beyond compliance to create competitive advantage. The 27,000 daughters program is both morally admirable and economically smart. Environmental initiatives reduce costs while meeting standards. Governance structures balance family control with institutional oversight. ESG is embedded in operations, not bolted on for optics.

For investors, KPR Mill presents a philosophical question: Should quality companies in mediocre industries trade at premium valuations? The market says yes, but history shows such premiums can evaporate quickly if execution falters. The investment case ultimately depends on time horizon. Short-term traders might find better opportunities. Long-term investors betting on India's manufacturing story, ESG importance, and execution excellence might find KPR's premium justified.

XIII. Future Outlook & Strategic Questions

As KPR Mill enters its sixth decade, the company faces strategic crossroads that will determine whether it remains a successful family enterprise or evolves into an institutional giant. The challenges ahead are different from those conquered—less about survival, more about succession; less about growth, more about governance.

Succession Planning: The most critical question facing KPR is leadership transition. K.P. Ramasamy, now in his 70s, has built an institution around his personal values. His children are involved in operations but haven't yet demonstrated independent leadership. Can compassionate capitalism survive the founder? Will the second generation maintain worker-first philosophy when faced with quarterly pressures? The company needs transparent succession planning that preserves culture while enabling evolution.

Scale vs. Soul: KPR's magic came from treating 27,000 workers like daughters. Can this intimacy scale to 50,000 or 100,000 workers? At what point does family feeling become corporate policy? The company must find ways to institutionalize values without bureaucratizing them. This might mean smaller autonomous units rather than massive factories, even if it sacrifices some economies of scale.

Digital Transformation: The textile industry stands at the cusp of digital revolution. AI-driven demand prediction, automated quality control, blockchain supply chain tracking, and virtual sampling are becoming table stakes. KPR's educated workforce provides advantage in adopting these technologies. But will management embrace digital transformation or see it as threatening their people-first model? The balance between automation and employment will test leadership wisdom.

Sustainability Leadership: Climate change and resource scarcity will reshape textiles over the next decade. Circular economy principles, biodegradable materials, and carbon neutrality will move from nice-to-have to must-have. KPR's early investments in renewable energy and water conservation provide foundation. But can they lead industry transformation or merely comply with evolving standards? The company that defines sustainable textiles will capture premium valuations.

International Expansion: KPR's production remains India-centric while competitors build global footprints. Africa offers labor cost advantages and trade preferences. Bangladesh provides duty benefits. Vietnam has established ecosystem. Should KPR remain focused on Indian manufacturing excellence or diversify geographic risk? The answer depends on whether competitive advantage comes from integration or values—integration travels, values might not.

Retail Ambitions: The FASO brand represents KPR's attempt to capture downstream value. But building brands requires different capabilities than manufacturing excellence. Marketing, merchandising, and consumer insight are alien to KPR's DNA. Should they partner with brand builders or develop capabilities internally? The retail venture could be transformative or a costly distraction.

Capital Allocation Evolution: KPR's conservative balance sheet served well during growth phase. But at current scale, should capital allocation evolve? Share buybacks at reasonable valuations? Dividend policy reflecting maturity? Strategic acquisitions to accelerate capability building? The company must balance financial flexibility with shareholder returns.

Next-Generation Workforce: The women who joined KPR in the 1990s are approaching retirement. Their children, educated and ambitious, have different expectations. They want careers, not just jobs. They seek meaning beyond wages. Can KPR evolve its people model for a workforce that has options? The answer will determine whether KPR remains an employer of choice.

Technology and Tradition: KPR succeeded by combining modern management with traditional values. As technology accelerates change, can this balance hold? Will AI-driven efficiency clash with human-centric culture? Can the company use technology to amplify rather than replace human potential? These aren't just operational questions but existential ones.

The strategic questions facing KPR don't have easy answers. They require choosing between equally valid paths. Focus or diversification? Automation or employment? Family or professional management? The choices made in the next five years will determine whether KPR Mill remains a remarkable Indian success story or becomes a global textile leader.

XIV. Epilogue & Reflections

Nothing about K.P. Ramasamy reveals that he is one of India's 100 richest people, with a staggering net worth of ₹19,000 crore. He still lives simply in Coimbatore, drives modest cars, and spends his days on factory floors rather than boardrooms. When asked about wealth, he seems genuinely puzzled by the question. For him, the 27,000 educated women, the 30,000 employed families, and the institutions built are the real wealth.

This presents a fascinating paradox: Ramasamy built extraordinary wealth precisely by not pursuing it. By focusing on worker welfare, he created productivity advantages. By maintaining quality regardless of cost, he attracted premium customers. By reinvesting profits rather than extracting them, he built compounding machines. The wealth was outcome, not objective.

This paradox challenges modern capitalism's assumptions. The dominant narrative suggests profit maximization drives value creation. KPR's story suggests the opposite—that value creation drives profit maximization. The distinction isn't semantic. It fundamentally changes decision-making. When faced with choices, KPR asks "what's right?" not "what's profitable?" Paradoxically, this often proves most profitable long-term.

The lessons for modern founders are profound but difficult. In an era of growth hacking and blitzscaling, KPR's patient building seems anachronistic. While unicorns chase valuations, KPR chased values. While startups pivot rapidly, KPR stayed consistent for decades. While technology companies pursue disruption, KPR pursued execution. Yet KPR's ₹33,000 crore market cap exceeds many unicorns' valuations.

What makes KPR Mill uniquely Indian yet globally competitive? It's the synthesis of seemingly contradictory elements. Traditional values with modern management. Social consciousness with commercial success. Family ownership with professional governance. Local roots with global reach. This synthesis couldn't have happened in Silicon Valley's move-fast-break-things culture or Wall Street's quarterly capitalism. It required India's unique combination of family business tradition, social hierarchy consciousness, and emerging market pragmatism.

The company also challenges ESG investing's superficiality. While funds screen for metrics and rankings, KPR shows that genuine social and environmental commitment creates competitive advantage. The 27,000 daughters program wasn't designed for ESG scores—it predated the acronym. The renewable energy investments weren't for carbon credits—they ensured production stability. Authentic purpose beats performative compliance.

Looking ahead, KPR Mill's greatest contribution might be proving an alternative model for industrial development. While automation threatens employment, KPR shows technology can augment human potential. While globalization creates race-to-bottom dynamics, KPR demonstrates that values-based differentiation commands premiums. While financialization prioritizes shareholders, KPR proves that stakeholder capitalism generates superior returns.

The story also raises uncomfortable questions. Is KPR's model replicable or does it require exceptional leadership? Can compassionate capitalism survive market pressures or does it need patient capital? Will second-generation leadership maintain founder values or succumb to conventional wisdom? These aren't just questions about KPR but about capitalism's evolution.

Perhaps the deepest lesson from KPR Mill is about time horizons. In a world accelerating toward quarterly earnings, KPR thinks in decades. In industries chasing cost reduction, KPR invests in human development. In markets demanding growth at any cost, KPR grows at sustainable pace. This temporal arbitrage—being long-term in short-term world—might be the ultimate competitive advantage.

The final reflection is personal. In researching KPR Mill, one encounters not just business success but human transformation. The stories of women completing education while working, of families escaping poverty, of dignity restored through employment—these transcend financial metrics. They remind us that business, at its best, is about human flourishing, not just wealth creation.

K.P. Ramasamy often says he's building for generations, not quarters. The 27,000 educated women, their educated children, and the communities transformed suggest he's succeeding. Whether KPR Mill becomes a global giant or remains an Indian champion matters less than the model it has proven: that compassion and capitalism need not be contradictory, that values create value, and that the best businesses, like the best lives, are built by lifting others.

KPR Mill's story continues to evolve. From humble beginnings with an ₹8,000 loan to a ₹33,000 crore enterprise, from power looms to global supply chains, from family business to institutional force—the journey demonstrates that extraordinary success can emerge from ordinary values extraordinarily executed. In an era searching for sustainable and inclusive growth models, KPR Mill offers not just inspiration but a proven playbook. The question isn't whether the model works—five decades of evidence confirms it does. The question is whether modern capitalism has the patience and purpose to implement it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube