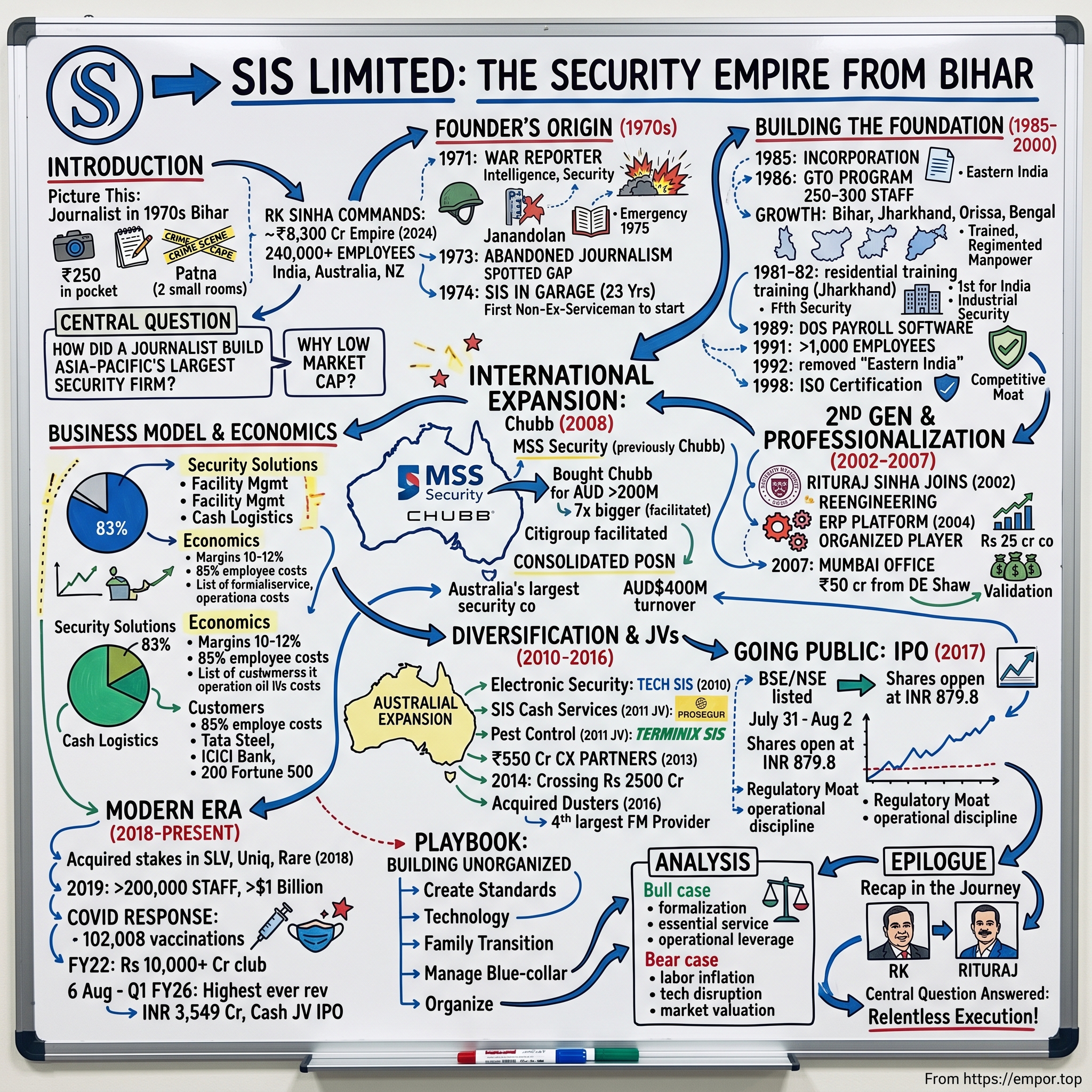

SIS Limited: The Security Empire from Bihar

I. Introduction & Episode Roadmap

Picture this: A young journalist in 1970s Bihar, covering crime beats and political upheavals, carries just ₹250 in his pocket and rents two small rooms in Patna. Fast forward to 2024, and that same man—Ravindra Kishore Sinha—commands a security empire worth over ₹8,300 crore, employing more than 240,000 people across India, Australia, and New Zealand. This is the story of SIS Limited, India's largest private security firm, and perhaps the most unlikely multinational to emerge from eastern India. The company just posted its highest ever revenue of INR 3,549 Cr in Q1 FY26, a testament to the durability of a business model that many dismiss as unglamorous—providing security guards, managing facilities, and transporting cash. Yet beneath this apparent simplicity lies one of India's most fascinating entrepreneurship stories: how a crime reporter built a multinational corporation by professionalizing an industry that barely existed when he started.

The central question driving our exploration today: How did a journalist from Bihar—a state more associated with political upheaval than corporate success stories—build one of Asia-Pacific's largest security services empires? And perhaps more intriguingly, why does a company with 240,000 employees and operations across four countries trade at just ₹5,154 crore market cap, while software companies with a fraction of the revenue command multiples of that valuation?

This is a story that touches on several profound themes in Indian business history. First, the formalization of India's vast informal economy—SIS essentially created an organized sector where none existed. Second, the challenge of building a services multinational from India, particularly one that succeeded in acquiring and integrating the largest security company in Australia during the 2008 financial crisis. Third, the unique dynamics of managing a blue-collar workforce at massive scale in an era obsessed with technology and automation.

We'll trace this journey from those two rooms in Patna through the company's transformation under second-generation leadership, its audacious international expansion, and its evolution into a three-pillar conglomerate spanning security services, facility management, and cash logistics. Along the way, we'll examine how SIS navigated the peculiar challenges of being a manpower-intensive business in capital markets that prefer asset-light models, and what this tells us about value creation in emerging markets.

II. The Founder's Origin Story: From Journalism to Security

The monsoon of 1971 had turned the Indo-Pak border into a muddy battlefield. Among the journalists covering the war was a young reporter named Ravindra Kishore Sinha, dodging artillery fire to file dispatches about one of South Asia's most consequential conflicts. His reporting earned him high commendations—rare recognition for a journalist barely out of college. But as RK Sinha would later reflect, those months covering the war taught him something more valuable than journalism: the critical importance of intelligence, security, and systematic information gathering in a chaotic world. Sinha, who had graduated in Political Science and Law from Anugrah Narayan College in Patna, wasn't just any reporter. By 1973, he had become deeply embedded in Bihar's tumultuous political landscape. He authored "Janandolan" that has been widely recognized as the first authentic research book on the student movement in India led by Jai Prakash Narayan between 1970 and 1975, documenting one of India's most significant political upheavals—the movement that would eventually lead to the Emergency of 1975.

But here's where the story takes an unexpected turn. In 1973, at the peak of his journalistic career, Sinha abruptly ended his work as a trainee reporter. The reason? He had spotted something others hadn't—an enormous gap in India's security infrastructure. Crime reporting had given him unique insights into how poorly protected Indian businesses and institutions were. Law enforcement was stretched thin, private security was virtually non-existent beyond chowkidars (watchmen), and the concept of professional security services was alien to most Indian companies. In 1974, with just ₹250 in his pocket, RK Sinha set up Security and Intelligence Services in a small garage in Patna at 23 years old. The garage was provided by an acquaintance who promised to charge rent only if Sinha made a profit—a kindness that would prove pivotal. After a lot of efforts, RK finally got a garage as office space in Patna from an acquaintance, who gave it to him with a promise that he would take rent only if Sinha made any profit.

The Bihar context made this venture both audacious and logical. In the 1970s, Bihar was undergoing massive political and social upheaval. The state had seen the JP movement, rising crime rates, and the emergence of private militias. Industrial development was bringing new factories and infrastructure projects that needed protection. Yet the security services available were either government forces stretched beyond capacity or traditional chowkidars with no training or accountability.

Sinha's vision was revolutionary for its time: create a professional, organized security service that would bridge the gap between unreliable watchmen and expensive police protection. What was interesting about SIS was that it was the first security service providing company which was started by a person who was not an Ex-serviceman and at the same time was a first generation entrepreneur, during a time when venture capital was not even ideated. This outsider perspective would prove to be SIS's greatest strength—Sinha approached security not as a military problem but as a service industry challenge.

III. Building the Foundation: The Early Years (1985–2000)

The transformation from a garage startup to a corporate entity began on January 2, 1985, when the company was formally incorporated as 'Security and Intelligence Services (Eastern India) Private Limited.' In its foundation year, 1986, SIS India launched its Graduate Trainee Officer (GTO) program initiated to build a cadre of security officers and managers. The company also employed a workforce between 250-300 people with a turnover of ₹1 Lakh.

The early years were marked by a systematic approach to building credibility in an industry that barely existed. Between 1985 and 1990, the company experienced massive growth in states like Bihar, Jharkhand, Orissa and West Bengal, majorly because they were the only security service company who offered trained, regimented and disciplined manpower.

What set SIS apart wasn't just the uniforms or the discipline—it was the infrastructure. In 1981-82, recognizing that corporate clients demanded specialized training, RK established India's first fully residential training facility, which was setup on the lines of Police Training Academies and was located at Palamu District, Jharkhand. This wasn't just about teaching guards to stand at gates; it was about creating a professional cadre that understood industrial security, loss prevention, and emergency response.

The company's growth trajectory accelerated through technological adoption unusual for a manpower business. In 1989, SIS India developed a DOS-based software program for payroll & its management on 486 computers—a remarkably early adoption of IT for managing what was essentially a blue-collar workforce. By 1991, SIS India completed the milestone of crossing its employee count beyond 1000.

The pivotal moment of this era came in 1992 when the words 'Eastern India' were removed from the company name, signaling ambitions beyond regional boundaries. The company was no longer content being Bihar's security provider—it wanted to be India's.

The late 1990s brought validation of SIS's professionalization efforts. In 1998, SIS India obtained ISO Certification, becoming the first Indian Security company to acquire it. This certification wasn't just a piece of paper; in an industry plagued by fly-by-night operators, it was a competitive moat. Multinational clients, particularly those in manufacturing and IT, began insisting on ISO-certified vendors, and SIS was the only game in town.

By 2000, SIS had established operations across eastern and northern India, with a workforce approaching 10,000. The company had successfully transformed from a Bihar-based startup into a regional powerhouse. But the real transformation was yet to come—and it would arrive in the form of the founder's son returning from England with ideas that would reshape the company's destiny.

IV. The Second Generation & Professionalization (2002–2007)

The year 2002 marked a generational shift that would define SIS's trajectory for the next two decades. Rituraj Kishore Sinha, alumnus of Leeds University Business School, joined the family business when SIS was an INR 25 crore company but very well regarded brand in industry. The contrast between father and son was striking—where RK Sinha was the journalist-turned-entrepreneur who built through relationships and intuition, Rituraj brought the toolkit of modern management: process optimization, financial engineering, and strategic planning.

The younger Sinha's first major initiative was a complete business process reengineering. He recognized that SIS's growth was being constrained not by market demand but by operational inefficiencies. Managing thousands of security guards across multiple states with paper-based systems was becoming impossible. In 2004, SIS India developed and launched first integrated end-to-end ERP platform—a remarkable achievement for a company in the manpower services sector, where most competitors still operated with ledgers and manual attendance registers. The real acceleration came in 2007, when the company commenced West India operations by opening a regional office in Mumbai. More significantly, SIS received approximately ₹50 crores investment from DE Shaw, Hedge Funds Firm. This wasn't just capital—it was validation. DE Shaw, one of the world's most sophisticated quantitative hedge funds, had seen something in this Bihar-born security company that most investors missed.

The DE Shaw investment marked a turning point in how SIS thought about itself. As Rituraj would later reflect, this was when they stopped thinking of themselves as a security guard company and started seeing themselves as an organized player in a massively unorganized market. The opportunity wasn't just to provide guards; it was to formalize an entire sector of the Indian economy.

By 2007, SIS had grown from the INR 25 crore company Rituraj had joined to a business approaching INR 500 crore in revenue. The company had successfully expanded beyond its eastern India stronghold, establishing operations in all major metros. The Graduate Trainee Officer program had created a pipeline of professional managers, solving one of the industry's biggest challenges—finding educated people willing to work in security services.

But the younger Sinha had bigger ambitions. He had seen how global security companies operated during his time in the UK. He understood that true scale in the services business came not just from organic growth but from consolidation. And in 2008, he would get the chance to execute on that vision—though the timing would prove to be either brilliantly contrarian or dangerously reckless.

V. The International Expansion: Chubb Acquisition (2008)

The call came in late 2007. United Technologies Corporation, the American industrial conglomerate, was looking to divest its Australian security operations—Chubb Security Personnel. For most Indian companies, especially one from Bihar, this would have been an impossible dream. Chubb was Australia's largest security company, with operations across the continent and New Zealand. The asking price was rumored to be north of AUD 200 million. And the global financial system was beginning to show cracks that would soon become the 2008 crisis. Rituraj Sinha had been tracking Chubb for months. Now in 2008, his son wanted the Rs 150-crore company to buy an Australian security firm Chubb that was over seven times bigger in revenues. The audacity of the proposal stunned even SIS's board. Not surprisingly, none of the senior officials at SIS were enthusiastic. Rituraj was beset with questions: "Who would give us money to make the acquisition?

But Rituraj saw what others didn't. The global financial crisis was creating once-in-a-lifetime opportunities. United Technologies needed to raise cash quickly. Australian banks were in no position to finance local buyouts. And most importantly, SIS acquired Australia's largest security company, Chubb Security, becoming the first Indian multinational in security services. The acquisition of the Australian guarding and mobile patrol business unit of US industrial conglomerate United Technologies was handled by Citigroup on their behalf.

The fact that Citigroup—one of the world's premier investment banks—was willing to handle the transaction for a relatively unknown Indian company from Bihar spoke volumes about how far SIS had come. The DE Shaw investment had opened doors, but it was the company's track record and Rituraj's vision that sealed the deal.

SIS has been active in the Australian market since 2008, when it purchased MSS Security, previously known as Chubb Security Personnel. The renamed MSS Security brought with it a 112-year heritage—MSS Security's history dates back to 1896, when Chubb, as we were previously known, opened its first Australian office.

The integration challenges were immense. How do you merge a company from Patna with operations in Sydney and Melbourne? The cultural differences were stark—Australian labor laws, wage structures, and client expectations were worlds apart from Indian operations. SIS had to prove that an Indian company could maintain, even improve, service standards in a developed market.

The genius of the acquisition wasn't just the timing—buying at the bottom of the market—but the strategic rationale. Australia's security market was consolidated, professional, and commanded premium pricing. Labor costs were high, but so were margins. Most importantly, it gave SIS instant credibility as a true multinational, not just an Indian company with overseas ambitions.

Since then, MSS has consolidated its position as Australia's largest security company with in excess of 5,000 employees and a turnover of nearlyAUD$400 million. The acquisition transformed SIS from a regional Indian player into an Asia-Pacific powerhouse, validating the vision of a journalist's son who dared to think beyond Bihar's borders.

VI. Diversification & Joint Ventures (2010–2016)

The post-Chubb years saw SIS executing a carefully orchestrated diversification strategy. Having proven it could acquire and integrate international operations, the company now turned to building adjacent businesses through strategic partnerships. In 2010, SIS India launched its Electronic Security arm under the name of TECH SIS. This wasn't just adding cameras to guard services—it was recognition that security was evolving from manpower to technology.

In 2011, SIS India formed a joint venture with Prosegur called SIS Prosegur for providing SIS Cash Services. Prosegur, Spain's largest security company, brought global expertise in cash logistics—a business that required different skills from guarding but leveraged the same trust and operational excellence. The timing was perfect: India's retail boom and ATM expansion created massive demand for secure cash transportation.

The same year brought another unexpected diversification. On 24 August 2011, SIS announced that it is entering into a joint venture with Terminix, to perform pest and termite control in India. The venture incorporated Pest Control Segment into its Facilities Management Segment and is called TerminiXSIS. To outsiders, pest control seemed unrelated to security. But SIS saw the connection: both were essential services that businesses outsourced, both required trained manpower and systematic processes, and both benefited from scale and professionalization. The momentum accelerated in 2013 when SIS India received ₹550 crores investment from CX Partners, a private equity firm, affirming history's largest PE investment in the Security Sector. In 2013, SIS India received ₹550 crores investment from CX Partners, a private equity firm, affirming history's largest PE investment in the Security Sector. The valuation had jumped dramatically—CX Partners picked up a 20% stake in the firm for Rs 500 crore in 2012, valuing it at Rs 2,500 crore.

This wasn't just capital raising; it was validation of the three-pillar strategy. PE firms like CX Partners saw what public markets would take years to recognize: SIS wasn't a security guard company anymore. It was an essential services platform with natural synergies across verticals.

The year 2014 marked a significant milestone: In 2014, SIS India celebrated its 40th anniversary, with its consolidated revenue crossing Rs 2500 crore. The company that started in a garage with ₹250 had grown 10,000-fold. But perhaps more importantly, The company also acquires the ISS cash business and rebrands it as SISCO. This acquisition from the Danish facilities management giant ISS further strengthened SIS's position in cash logistics.

By 2016, the transformation was complete. In 2016, SIS India made over Rs 4000 crore in revenue, besides acquiring Dusters, becoming India's 4th largest Facility Management Provider. The company now operated across the entire spectrum of business support services. From guarding factories to managing facilities to transporting cash—SIS had become indispensable to corporate India.

VII. Going Public: The IPO Story (2017)

The road show for SIS's IPO in July 2017 was unlike any other. Investment bankers had to explain to skeptical fund managers why a "security guard company" deserved a premium valuation. The pushback was immediate and harsh: low margins, high employee costs, minimal technology differentiation. How was this different from any other labor contractor?

In 2017, the SIS Group IPO was launched, making the company the first in the nation to become listed. The IPO opened July 31, 2017 and closed August 2, 2017, with shares listing on BSE and NSE on August 10, 2017. The pricing reflected the market's ambivalence—an IPO price of ₹815 per share, aggregating up to ₹779.58 Crores.

The first day of trading brought modest relief. SIS listed at INR 879.8 per share on NSE, up 7.9% from the IPO price. Not the blockbuster debut many had hoped for, but respectable given the sector's perception issues. CX Partners sold about a 5% stake in Security and Intelligence Services (India) Ltd, or SIS, through its IPO in August. CX had bought a 15.5% stake in SIS in 2013.

The decision to go public was driven by multiple factors. The PE investors needed an exit path after holding for several years. The company needed currency for future acquisitions. But most importantly, Rituraj Sinha believed that being a listed company would force operational discipline and transparency that would ultimately benefit the business.

The post-IPO journey has been mixed. The stock has struggled to gain traction, often trading below comparable multiples of other business services companies. The market's fixation on technology and asset-light models has worked against SIS, despite its strong cash flows and market leadership.

Yet the IPO achieved something crucial: it established SIS as the only NSE/BSE-listed security service company in India with PSARA license. This regulatory moat, combined with public company governance standards, became a powerful differentiator when approaching large corporate clients and government contracts.

VIII. Modern Era: Scale, Technology & Consolidation (2018–Present)

The post-IPO years have been defined by relentless execution and strategic consolidation. In 2018, SIS India consolidated its leadership position in India Security & FM by acquiring stakes in SLV, Bengaluru-based Uniq Detective and Security Services & Rare Hospitality and Services Pvt. Ltd. Each acquisition wasn't just about adding revenue—it was about acquiring capabilities, geographic presence, or client relationships that would have taken years to build organically.

In 2019, SIS India crossed a workforce of more than 200,000 with over $1 Billion in revenues. The psychological barrier of $1 billion in revenue was important—it placed SIS among a select group of Indian services companies that had achieved global scale.

Then came COVID-19—a crisis that could have devastated a company dependent on deploying hundreds of thousands of workers daily. Instead, SIS's response became a case study in crisis management. SIS Group, has completed inoculating 102,008 employees of its 2,30,000 workforce. This was done through Humare Heroes Vaccination Drive (HHVD) launched on May 1, 2021, within a record timeframe of 30 days.

The pandemic accelerated certain trends that benefited SIS. Companies realized the critical importance of professional facility management and hygiene services. E-commerce growth drove demand for cash logistics and last-mile security. Most importantly, the formalization of the economy accelerated as informal players couldn't survive the lockdowns.

January 2021 marked a subtle but significant change: the company changed its name from Security and Intelligence Services (India) Limited to SIS Limited. Dropping "India" from the name reflected the company's evolution into a truly international player with significant overseas revenue.

The growth trajectory continued to accelerate. In FY22, SIS entered into the Rs10,000-crore revenue club by clocking Rs10,059.1 crore, a growth of over 10.2 percent over the last fiscal. What's remarkable is the pace: What is most interesting is that the security services, facility management and cash logistics major took just five years to double its revenue.

Rituraj Sinha's perspective on this growth is telling: "From Rs25 crore in 2002 to Rs10,000 crore in 2022. That's our story," he says. He quickly qualifies his statement. "It's a profitable and sustainable story,"

The latest milestone came in Q1 FY26: 6 Aug - SIS Q1 FY26: Highest ever revenue INR 3,549 Cr, 13.4% YoY growth, net debt down to INR 540 Cr, Cash JV IPO approved. This performance, achieved in a challenging macro environment, validates the durability of the business model. The consolidation continues. Recent news shows: 2d - SIS to acquire 51% of A P Securitas for INR73.40 Cr now; remaining shares by 2029; FY25 revenue INR1,119 Cr. This acquisition strategy—buying controlling stakes with options for full ownership—allows SIS to integrate operations gradually while managing capital efficiently.

IX. Business Model & Competitive Dynamics

Understanding SIS requires grasping a fundamental paradox: it's simultaneously a commodity business and a differentiated service provider. At its core, Security Solutions comprises 83% of business. The remaining comes from facility management and cash logistics, but all three segments share common characteristics.

The economics are brutal yet beautiful. Gross margins hover around 10-12%, with EBITDA margins in the 4-6% range. For every ₹100 of revenue, roughly ₹85 goes to employee costs. This isn't a business where you can dramatically improve margins through automation or efficiency gains. Yet within these constraints, SIS has built sustainable competitive advantages.

First, scale matters enormously. Managing 240,000 employees requires sophisticated systems for recruitment, training, deployment, and payroll. Smaller competitors simply can't match this infrastructure. The company has over 10,000 customers which include major industry players such as Tata Steel, Tata Motors, ICICI Bank, Idea Cellular and Future Group.

Second, trust is everything. Catering to 200 of top Fortune 500 companies of India, SIS has become the default choice for corporations that cannot afford security breaches or service disruptions. The PSARA license and public company status create additional trust markers that matter in enterprise sales.

Third, the market structure favors consolidation. The Indian security services market remains massively fragmented, with thousands of small, informal operators. GST implementation and increased regulatory compliance are forcing formalization, creating acquisition opportunities for organized players like SIS.

The competitive landscape is evolving. Global players like G4S and Securitas have Indian operations but lack SIS's local market understanding and relationships. Regional players are strong in specific geographies but can't match SIS's pan-India presence. Technology startups are trying to disrupt with AI-powered surveillance and robotics, but the human element remains irreplaceable for most security needs.

What's often misunderstood is that SIS isn't really selling security guards—it's selling peace of mind, operational continuity, and risk management. When a bank needs cash transported, when a factory needs round-the-clock security, when an office building needs comprehensive facility management, the cost of failure far exceeds the service fee. This creates switching costs that aren't visible in the financials but are very real in client relationships.

X. Playbook: Building in Unorganized Sectors

The SIS story offers a masterclass in formalizing unorganized sectors in emerging markets. The playbook, refined over four decades, contains lessons that extend far beyond security services.

Start with the insight: massive inefficiencies exist when essential services are delivered through informal channels. In 1970s India, security meant hiring local strongmen or retired servicemen through contractors who provided no training, no accountability, and no recourse if things went wrong. RK Sinha saw that businesses would pay a premium for professionalization.

The first step was creating standards where none existed. The training academy in Jharkhand wasn't just about teaching guards to salute properly—it was about creating a visible differentiator. When clients visited the academy, they saw infrastructure, process, and investment. This tangible commitment to quality justified premium pricing.

Technology adoption, counterintuitively, matters more in labor-intensive businesses than in many tech companies. The DOS-based payroll system in 1989, the ERP in 2004—these weren't nice-to-haves but essential for managing complexity at scale. When you're deploying thousands of workers across hundreds of sites daily, manual processes simply don't work.

The family-to-professional transition deserves special attention. Many Indian family businesses struggle when the next generation joins—ego clashes, resistance to change, inability to let go. The Sinha family navigated this by clearly delineating roles. RK Sinha remained the visionary and relationship builder; Rituraj became the operator and strategist. Neither stepped on the other's toes.

Geographic expansion followed a hub-and-spoke model. Start with a stronghold (Eastern India), achieve dominance, then expand to adjacent regions. But here's the crucial insight: SIS didn't try to replicate the same model everywhere. Mumbai operations looked different from Patna operations, reflecting local labor markets, client needs, and competitive dynamics.

The acquisition strategy was equally sophisticated. Never buy just for revenue—buy for capabilities (Chubb's international operations), client relationships (ISS's cash business), or market access (regional players). And always integrate slowly, preserving what works while imposing financial discipline and operational standards.

Managing blue-collar workers at scale requires a different playbook from managing white-collar professionals. SIS's innovation was treating security guards not as contractors but as employees, providing benefits, career paths, and dignity. The COVID vaccination drive wasn't charity—it was recognizing that employee welfare directly impacts service quality and client retention.

Perhaps the most important lesson: in unorganized sectors, the opportunity isn't to disrupt but to organize. SIS never tried to reinvent security services. Instead, it took an existing need and delivered it professionally, systematically, and at scale. The ₹250 in RK Sinha's pocket grew to ₹8,300 crore not through radical innovation but through relentless execution.

XI. Analysis & Investment Case

The investment case for SIS is a study in contradictions. The company has delivered a poor sales growth of 9.22% over past five years and low return on equity of 7.75% over last 3 years. With Promoter Holding: 72.1%, there's limited free float, contributing to low liquidity and institutional interest.

Yet these headline numbers obscure a more nuanced reality. The 9% growth rate, while uninspiring compared to tech companies, represents steady market share gains in a sector growing with GDP. The low ROE reflects the capital intensity of acquisitions and the working capital requirements of a services business, not operational inefficiency.

The bull case rests on several pillars. First, formalization of the economy is irreversible. GST, digital payments, and increased compliance requirements are squeezing out informal players. SIS, as the only listed player with national scale, is the natural consolidator.

Second, the essential services nature provides resilience. Security, facility management, and cash logistics aren't discretionary spends—they're operational necessities. Even during COVID, while revenues dipped, they didn't collapse like in many other sectors.

Third, operational leverage is finally showing. 6 Aug - SIS Q1 FY26: Highest ever revenue INR 3,549 Cr, 13.4% YoY growth, net debt down to INR 540 Cr. As the company reaches scale, incremental revenues flow through at higher margins.

The bear case is equally compelling. Labor cost inflation is structural in India, with minimum wages rising faster than service price increases. Technology disruption—AI-powered surveillance, drone security, automated cash handling—threatens the core business model. Most concerningly, the market simply doesn't value manpower-intensive businesses, regardless of execution quality.

The valuation reflects this ambivalence. At Mkt Cap: 5,154 Crore, SIS trades at less than 0.5x revenues, a discount to global security services peers and a fraction of Indian IT services multiples. The market is essentially saying: we don't believe this business can generate meaningful returns on capital.

But this might be missing the forest for the trees. SIS isn't trying to be a high-ROE, asset-light marvel. It's building an essential services platform in one of the world's fastest-growing major economies. The question isn't whether SIS can match software company metrics—it can't and won't. The question is whether steady, single-digit growth with strong cash generation in an essential service deserves such a dramatic discount.

The Cash JV IPO approved could be a catalyst, unlocking value by separately listing the cash logistics business. But the fundamental re-rating likely requires a broader shift in how markets value essential services businesses in emerging markets.

XII. Epilogue & Lessons

The journey from ₹250 to billions is remarkable enough, but the numbers vary depending on the source. Today, Ravindra Kishore Sinha's net worth is estimated at Rs 5000 crore, while another source states As of 2018, Ravindra Kishore Sinha's net worth was $1.00 billion. Regardless of the exact figure, RK Sinha has joined the ranks of India's billionaire entrepreneurs, a testament to what's possible when vision meets execution in emerging markets.

But the real legacy isn't the wealth—it's the transformation of an entire industry. When SIS started, private security in India meant hiring local strongmen. Today, it's a professional services sector employing millions, with standards, training, and accountability. SIS didn't just build a company; it created a template for formalizing unorganized sectors.

The generational transition offers another crucial lesson. Now led by son Rituraj Sinha as Group Managing Director, SIS represents a successful handover from founder to next generation—rare in Indian family businesses. Rituraj's comment captures the essence: "From Rs25 crore in 2002 to Rs10,000 crore in 2022. That's our story... It's a profitable and sustainable story."

For investors, SIS presents a philosophical question: How do you value essential services in emerging markets? The company's poor sales growth of 9.22% over past five years and low ROE might disappoint growth investors. But for those who understand the power of steady compounding in essential services, the story might be different.

The broader implications extend beyond finance. SIS's 240,000 employees represent 240,000 families lifted into formal employment. The COVID vaccination drive, the training programs, the career paths created—these aren't just CSR initiatives but fundamental to the business model. In a country where job creation is the paramount challenge, SIS has quietly become one of India's largest employers.

Perhaps most importantly, SIS proves that you don't need to be in Bangalore or Mumbai, you don't need venture capital, and you don't need to build software to create a valuable business. A journalist from Bihar with ₹250 built a multinational corporation by solving a basic problem—providing reliable security services—and executing relentlessly for four decades.

The market may never fully appreciate manpower-intensive businesses. Technology may eventually disrupt parts of the model. Competition will intensify as the sector formalizes. But SIS has already achieved something remarkable: it transformed an unorganized sector into a professional industry, created massive employment, and built enduring value for stakeholders.

XIII. Recent News

The momentum continues into 2025. The Q3 FY25 results show the operational improvements bearing fruit: Net profit of SIS rose 176.52% to Rs 102.12 crore in the quarter ended December 2024 as against Rs 36.93 crore during the previous quarter ended December 2023. Sales rose 9.41% to Rs 3362.51 crore in the quarter ended December 2024 as against Rs 3073.44 crore during the previous quarter ended December 2023.

The acquisition strategy remains active with SIS to acquire 51% of A P Securitas for INR73.40 Cr now; remaining shares by 2029; FY25 revenue INR1,119 Cr. This structured deal—majority stake now, full ownership later—shows sophisticated capital allocation.

Management commentary from recent earnings calls reflects confidence in the trajectory, though challenges remain in the Australian operations due to labor cost pressures. The approved Cash JV IPO could unlock significant value, potentially re-rating the entire company if executed well.

XIV. Links & Resources

For those interested in diving deeper into the SIS story, the company's investor relations section provides comprehensive financial reports and presentations. Industry reports on India's security services sector from FICCI and ASSOCHAM offer context on market dynamics. The PSARA regulations governing private security agencies in India are essential reading for understanding the regulatory framework.

Academic studies on the formalization of India's economy post-GST help contextualize SIS's growth opportunity. Books on family business transitions in India provide frameworks for understanding the Sinha family's successful generational handover. And for those interested in the broader narrative of entrepreneurship in India's smaller cities, SIS represents a compelling case study in building from the periphery rather than the center.

The SIS story isn't finished. At current valuations, the market clearly doesn't believe in the model. But for those who understand that emerging markets need more than just software and e-commerce—that someone needs to guard the factories, manage the facilities, and transport the cash—SIS represents something profound: the unglamorous businesses that make modern economies actually function. From a garage in Patna to the NSE, from ₹250 to billions, from journalist to billionaire—it's a distinctly Indian story of transformation through determination.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube