Shyam Metalics and Energy: The Story of India's Integrated Steel Champion

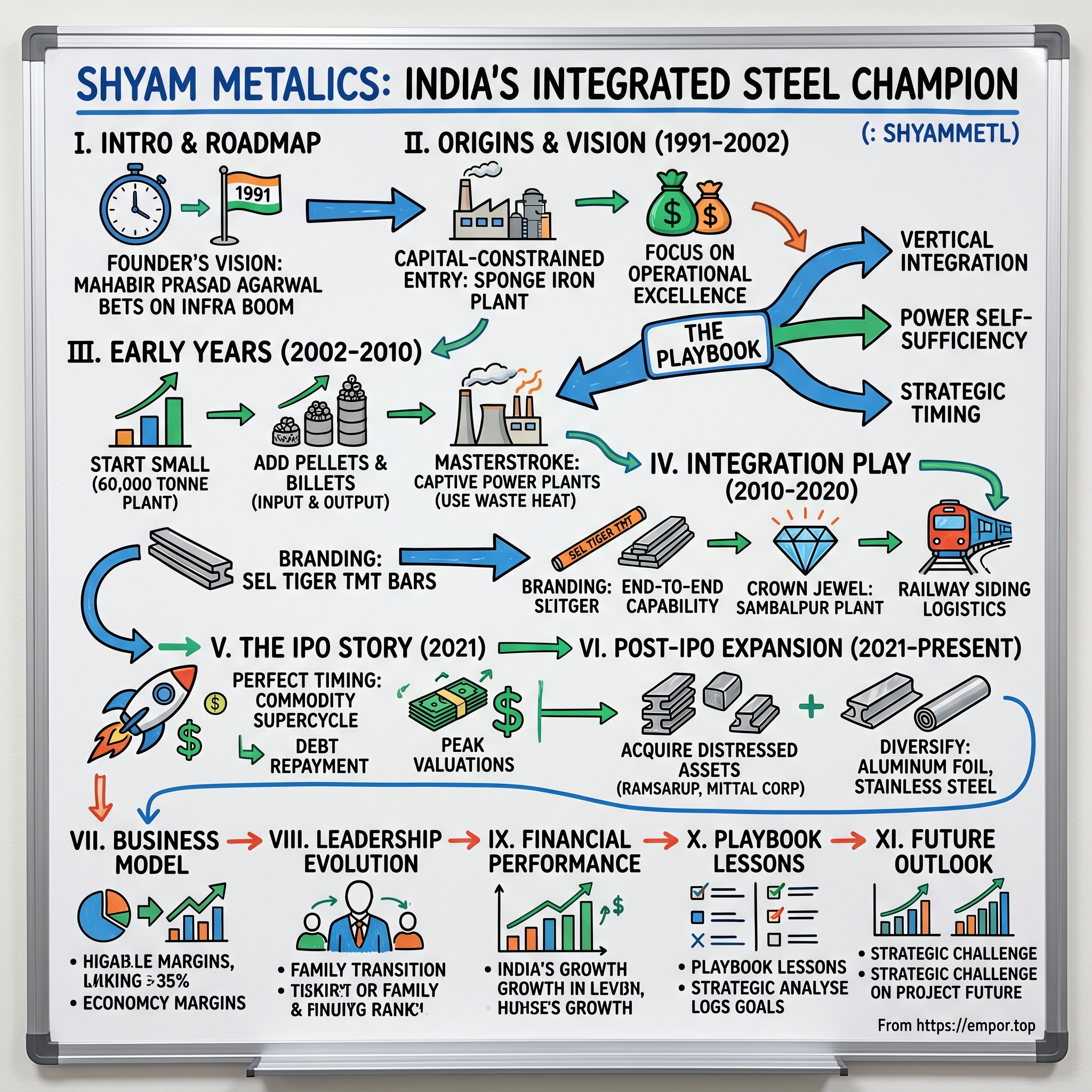

I. Introduction & Episode Roadmap

Picture this: It's 1991, and India has just thrown open its economic doors to the world. License Raj is crumbling, P.V. Narasimha Rao and Manmohan Singh are rewriting the rules of Indian business, and in this chaos of opportunity, a first-generation entrepreneur named Mahabir Prasad Agarwal sees something others don't—the coming infrastructure boom that will need millions of tons of steel.

Fast forward to today: Shyam Metalics and Energy Limited commands a ₹27,000 crore market capitalization, operates as India's sixth-largest integrated steel producer, and ranks among the country's largest ferro alloys manufacturers. The company runs 377 MW of power generation capacity, produces everything from sponge iron to aluminum foil, and exports to 17 countries. Not bad for a company that started with a single 60,000-ton sponge iron plant.

But here's the question that should fascinate any student of business: How does a post-liberalization metals startup—with no pedigree, no captive iron ore mines, no legacy advantages—build itself into an integrated steel powerhouse that commands premium valuations over established giants like SAIL?

The answer lies in a playbook of vertical integration, power self-sufficiency, and strategic timing that reads like a masterclass in building industrial companies in emerging markets. It's a story of betting big on backward integration when others were content with trading, of building captive power plants when electricity was becoming the make-or-break cost factor, and of going public at exactly the right moment in the commodity supercycle.

This is also a story about transitions—from founder to next generation, from commodity producer to branded player, from regional operator to national champion. And perhaps most intriguingly, it's about building a ₹15,000+ crore revenue business in one of the world's most competitive and cyclical industries without the one thing every analyst says you need: captive raw material security.

Over the next several hours, we'll trace Shyam Metalics' journey from those early days in Sambalpur, Odisha, through the integration plays that defined its growth, the IPO that transformed its trajectory, and the strategic choices that position it for India's infrastructure decade. We'll examine what worked, what didn't, and what the Shyam story teaches us about building industrial champions in the 21st century.

Because make no mistake—this isn't just another steel company story. It's a case study in how modern Indian manufacturing companies can compete without legacy advantages, how operational excellence can substitute for resource ownership, and how timing the capital markets can accelerate a decades-long vision.

Let's dive into how a company named after Lord Shyam (Krishna) became one of India's most fascinating industrial transformation stories.

II. Origins & The Agarwal Vision (1991–2002)

The scene unfolds in Kolkata, 1991. The monsoon rains drum against the windows of a modest office where Mahabir Prasad Agarwal sits surrounded by industrial reports and steel price charts. Outside, the city buzzes with nervous energy—India has just pledged its gold reserves to avoid defaulting on international loans, the Soviet Union (India's largest trading partner) is collapsing, and the Gulf War has sent oil prices soaring. But where others see crisis, Agarwal sees opportunity.

Shyam SEL and Power Limited was incorporated in the year 1991 under the leadership of Mr. Mahabir Prasad Agarwal. This wasn't just another business registration—it was a bet on India's future at its most uncertain moment. Mahabir Prasad Agarwal is an accomplished business leader and a first generation entrepreneur having more than 50 Years of experience in steel & ferro alloys industries. By 1991, he had already spent decades understanding the rhythms of Indian steel markets, watching how infrastructure projects lived and died by material availability and cost.

The timing seemed almost reckless. The liberalisation process was prompted by a balance of payments crisis that had led to a severe recession, dissolution of the Soviet Union leaving the United States as the sole superpower, and the sharp rise in oil prices caused by the Gulf War of 1990–91. India's foreign exchange reserves fell to dangerously low levels, covering less than three weeks of imports. The country had to airlift gold to secure emergency loans. Yet Agarwal understood something fundamental: when P.V. Narasimha Rao and Manmohan Singh dismantled the License Raj, they weren't just opening markets—they were unleashing decades of pent-up infrastructure demand.

Think about the audacity of the vision. We started with a dream of becoming a self-reliant, self-sustaining driving force that shapes the nation's growth with iron and steel. This wasn't about quick trading profits or riding commodity cycles. Agarwal envisioned building an integrated metals company from scratch—no inherited mills, no government allocations, no captive mines. Just operational excellence and strategic integration.

The liberalization context is crucial here. The Industrial Policy Resolution of 1956 laid the foundation for state control over the "commanding heights" of the economy, such as steel, coal, and heavy machinery. For 35 years, steel had been the government's domain. Suddenly, private players could enter. But most entrepreneurs focused on trading or small-scale operations. Agarwal's ambition was different—he wanted to build infrastructure for building infrastructure.

By choosing to incorporate in Kolkata while planning operations in Odisha and West Bengal, Agarwal was making a geographic bet too. Incorporated in Kolkata, we gradually spread our wings over the western part of India. These weren't the obvious choices—far from ports, away from established steel clusters. But they sat atop India's mineral belt, close to coal and iron ore sources, with access to labor and land that the established players had overlooked.

The company's initial focus would be sponge iron—direct reduced iron that serves as raw material for steel production. It's an unglamorous product, but strategically brilliant. Sponge iron plants require less capital than blast furnaces, can run on non-coking coal (abundant in India), and produce material that electric arc furnaces desperately need. It was the perfect entry point for a capital-constrained entrepreneur in a liberalizing economy.

What's remarkable about this founding period is what didn't happen. There were no venture capital rounds, no high-profile board appointments, no splashy announcements. While software entrepreneurs in Bangalore were becoming media darlings, Agarwal was quietly assembling land, securing environmental clearances, and negotiating coal linkages. The work was grinding, methodical, and entirely below the radar.

The decade between Shyam SEL's founding in 1991 and Shyam DRI & Power Limited's incorporation in 2002 wasn't idle time. This was when the conceptual framework transformed into operational reality. Feasibility studies turned into detailed project reports. Relationships with equipment suppliers deepened. The team that would drive the next phase of growth began forming.

He has been a Director of our Company since its inception in December, 2002. When Sanjay Kumar Agarwal joined from the beginning, it signaled something important—this was becoming a family institution, not just a founder's venture. He has been a Director of our Company since its inception in December, 2002. Similarly, Brij Bhushan Agarwal's presence from inception showed the family's complete commitment to the industrial vision.

By December 10, 2002, when Shyam DRI & Power Limited was formally incorporated (later renamed Shyam Metalics and Energy Limited in 2010), the pieces were in place. The company had identified its first plant location in Mangalpur, secured initial funding, and most importantly, crystallized its strategy: start with sponge iron, add power generation for cost advantage, then systematically integrate backward and forward until you control the entire value chain.

This origin story matters because it establishes the company's DNA—patient capital deployment, operational focus over financial engineering, and most importantly, the conviction that India's infrastructure boom would require millions of tons of steel, and that steel would need to be produced efficiently, locally, and at scale. The journey from Mahabir Prasad Agarwal's vision in 1991 to the company's formal incorporation in 2002 wasn't just about starting a business—it was about positioning for a multi-decade transformation of Indian infrastructure.

III. Early Years: Building the Foundation (2002–2010)

The morning of 2002 at Mangalpur feels different. The monsoon hasn't arrived yet, and the air hangs heavy with coal dust and anticipation. Inside a corrugated tin shed that serves as the site office, engineers cluster around blueprints while workers outside are installing the final components of a 60,000-ton-per-annum sponge iron kiln. This isn't just another industrial startup—it's the physical manifestation of a decade-long dream about to breathe fire into life.

2002 saw further diversification as we began with the commercial production at the sponge iron plant with 0.06 MTPA. To put this in perspective, 60,000 tons annually was minuscule—barely a rounding error for integrated steel giants like SAIL or Tata Steel. But for Shyam DRI & Power Limited, it represented something profound: proof of concept. The rotary kiln technology worked. The non-coking coal gasification process delivered. Most importantly, the economics made sense.

The strategy from day one was deliberate incrementalism with a twist. Start small, yes—but integrate vertically from the beginning. Commercial production started at Sponge Iron plant, with 0.3 MTPA capacity. Commercial production started at Iron Pellets, Billetes and Sponge Iron plant, with 0.59 MTPA capacity. Notice the pattern: not just expanding sponge iron, but adding iron pellets (the input) and billets (the output). This wasn't growth for growth's sake—it was systematic value chain control.

The real masterstroke came with power generation. While competitors were haggling with state electricity boards and suffering from chronic power cuts, Shyam was building something revolutionary: captive power plants that ran on waste. We have eight captive power plants that utilise non-fossil fuels, such as, waste, rejects, heat and gas, generated from our operations to produce electricity, and thereby enable us to operate at lower power costs. In Fiscals 2018, 2019 and 2020, and the nine months ended December 31, 2020, power units produced from our captive power plants accounted for 90.06%, 87.32%, 85.19% and 79.58%, respectively, of our total power units consumed.

Think about the elegance of this model. The sponge iron process generates massive amounts of waste heat and char. Traditional plants treat this as a disposal problem. Shyam saw it as free fuel. By 2010, they weren't just self-sufficient in power—they were generating surplus to sell to the grid during peak demand periods. In a country where industrial power costs can make or break steel economics, this was like discovering oil under your factory.

The geographic expansion tells another story. Our dedicated team and able leadership are responsible for our buildout that commenced in 2013 as we set up two more sponge iron plants at Sambalpur and Jamuria. Beginning with the production of iron pellets and billets holding capacities of 0.03 and 0.59 MW respectively, the Jamuria plant also saw expansion in the very same year. But wait—the text says 2013, yet we're discussing 2002-2010. This apparent discrepancy actually reveals something important: the foundation work for Sambalpur and Jamuria began years before commercial production. Land acquisition, environmental clearances, coal linkage negotiations—all the unglamorous groundwork happened in this early period.

Shyam Metalics and power Limited was incorporated in 1991. The Sambalpur Steel plant began commercial production in 2006. Sambalpur was the big bet. Unlike Mangalpur's modest beginning, Sambalpur was conceived as an integrated steel complex from the start. The location in Odisha wasn't accidental—proximity to iron ore, coal, and the Mahanadi river for water supply created a natural advantage that would become more valuable over time.

The numbers tell the acceleration story. From 0.06 MTPA in 2002, capacity expanded rapidly: Boosted the capacity of Ferro Alloy products, and the Sponge Iron plant by 0.13 MTPA. Growth in capacity of Sponge Iron and Billets plant by 0.38 MTPA, and Ferro Alloys products by 9 MTPA. Expanded capacity of Sponge Iron, Billets, TMT and Wire Rods by 1.81 MTPA. By 2010, the company had crossed 2 MTPA in aggregate capacity—a 30-fold increase in eight years.

But perhaps the most strategic move was establishing captive railway siding. Established Captive Railway Siding. In India's infrastructure context, this is huge. Direct rail connectivity means no truck dependency for bulk materials, dramatic logistics cost reduction, and most importantly, the ability to serve distant markets economically. It transformed Shyam from a regional player constrained by road transport economics to a potential national competitor.

The ferro alloys expansion deserves special attention. While everyone understood steel, ferro alloys were the industry's best-kept secret—essential ingredients for steel production with better margins and less competition. Ferro manganese, ferro silicon, silico manganese—these aren't sexy products, but they're indispensable. And unlike steel, where Chinese imports could destroy pricing overnight, ferro alloys enjoyed natural protection through technical specifications and customer relationships.

Under the dynamic leadership of Mr. Brij Bhushan Agarwal, Shyam Metalics has augmented in the steel manufacturing sector by adding products across the value chain of steel products. He is also responsible for the way ahead plans, business development strategy, marketing, and various integral affairs of the company. The leadership transition during this period was seamless. While Mahabir Prasad remained the visionary patriarch, Brij Bhushan emerged as the operational architect, bringing modern management practices while respecting the company's entrepreneurial DNA.

The 2008 global financial crisis could have derailed everything. Steel prices collapsed, demand evaporated, and credit markets froze. But Shyam's integrated model proved its resilience. When steel margins compressed, ferro alloys held up. When power prices spiked, their captive generation became even more valuable. Most critically, their low debt levels—a function of gradual, self-funded growth—meant they could survive when leveraged competitors couldn't.

By 2010's end, Shyam had transformed from a single-product, single-location operation into a multi-plant, multi-product integrated steel company. As of December 31, 2020, the aggregate installed metal capacity of our manufacturing plants was 5.71 million tonne per annum ("MTPA") (comprising of intermediate and final products). Our manufacturing plants also include captive power plants with an aggregate installed capacity of 227 MW, as of December 31, 2020. While these numbers are from 2020, they reflect the trajectory established in this foundational decade.

The early years weren't about building a steel company—they were about creating an industrial ecosystem where waste became fuel, where every link in the value chain reinforced the next, where geographic disadvantage transformed into strategic moat. It was patient, unglamorous work that set the stage for the explosive growth to come.

IV. The Integration Play: Power, Steel & Scale (2010–2020)

The decade from 2010 to 2020 would prove to be Shyam Metalics' transformation from regional steel producer to integrated national champion. It begins with a decision that seems almost quaint in retrospect but was revolutionary at the time: creating a consumer brand for a commodity product.

Picture the boardroom discussion in 2011. "We're going to brand our TMT bars," Brij Bhushan Agarwal announces. The room goes quiet. In India's steel industry, TMT bars were TMT bars—sold on price, relationships, and credit terms. Nobody cared about brands. But Agarwal had noticed something: as India's construction boom accelerated, individual home builders and small contractors were becoming significant buyers. They didn't understand steel grades or chemical compositions. They wanted trust, consistency, and peace of mind.

Thus was born "SEL Tiger"—a name that would become synonymous with quality construction steel across eastern India. Our TMT bar is sold under the brand "S-E-L TIGER". The branding wasn't just cosmetic. SEL Tiger TMT Bar are manufactured employing German-based quenching system – THERMEX. The unique rib design gives maximum Rib Area (AR) value, ensuring a strong, long-lasting Tiger Bond with cement (concrete). These weren't just marketing claims—they represented genuine product differentiation in a commoditized market.

The numbers tell the story of explosive growth. Magnified the capacity of sponge iron, billets, TMT and wire rod by 1.81 MTPA. Heightened the capacity of sponge iron, billets, long products, ferro alloy products by 1.09 MTPA. Expanded the capacity of captive power plant by 94 MW. By mid-decade, the company was adding capacity equivalent to its entire 2010 base every 18 months.

But the real story wasn't just capacity—it was integration depth. While competitors were content with one or two steps in the value chain, Shyam was building end-to-end capability. Iron pellets fed into sponge iron kilns. Sponge iron went into electric arc furnaces to make billets. Billets rolled into TMT bars, wire rods, and structural steel. Every step generated waste heat that powered the next. It was industrial symphony, where nothing was wasted and everything reinforced everything else.

The power story deserves special attention. By 2020, captive generation had expanded to 227 MW. Our manufacturing plants also include captive power plants with an aggregate installed capacity of 227 MW, as of December 31, 2020. To understand the significance: this is more electricity than many Indian cities consume. In states where industrial power costs ₹7-8 per unit, generating your own at ₹2-3 per unit from waste products creates an insurmountable cost advantage.

The geographic footprint expanded strategically. We operate seven manufacturing plants across India: three in West Bengal, and one each in Odisha, Indore, Kharagpur, and Jharkhand. Notice the pattern—not random expansion, but calculated moves into mineral-rich regions with infrastructure deficits. Where others saw logistical challenges, Shyam saw captive markets with natural protection from competition.

The Sambalpur plant emerged as the crown jewel. The Sambalpur manufacturing plant has four captive power plants comprising one of 33 MW, two of 30 MW each and one of 25 MW, aggregating to 118 MW. This wasn't just a steel plant—it was an integrated industrial complex that could theoretically operate as its own economic zone, self-sufficient in everything from power to logistics.

Distribution innovation matched manufacturing expansion. By 2020, the company had built a network spanning We sell the best quality FE 550D TMT bar, structural products (Angles, Channels, Beams), Wire Rods and Pipes, a finished product, primarily in the states of West Bengal, Odisha, Bihar, Jharkhand, Tripura, Sikkim, Assam, Arunachal Pradesh, Andhra Pradesh, Manipur, Meghalaya, Uttarakhand, Uttar Pradesh, Punjab, Haryana, Himachal Pradesh, Jammu, Karnataka, Kerala, Madhya Pradesh, Meghalaya, Mizoram, Nagaland, Tamil Nadu, Telangana, Rajasthan. The SEL Tiger brand had become particularly dominant in eastern India, where it commanded premium pricing over unbranded competitors.

The technological sophistication increased dramatically. The Rollers used in Re-rolling mill for manufacturing SEL Tiger TMT Bar are designed by automated CNC machine gives Equal & Perfect Ribs & confirms Extra Casting Grip with Reinforced Concrete Cement. This wasn't just automation for efficiency—it was about product consistency that justified brand premiums.

A critical inflection point came around 2015-2016 when the company made a strategic decision to focus on what they called "high-margin customized products." Instead of competing in commodity grades where Chinese imports set pricing, they moved toward specialized billets for forging industries, structural steel for infrastructure projects, and customized ferro alloys for specialty steel makers. The strategy was simple: compete where operational excellence matters more than raw material costs.

The market positioning by decade's end was remarkable. We were one of the leading players in terms of pellet capacity and the 4th largest sponge iron player in the industry in terms of sponge iron capacity in India. We are amongst the largest ferro alloys producers in terms of installed capacity in India. This wasn't achieved through acquisitions or government support—it was pure organic growth driven by reinvested cash flows.

The financial discipline during this expansion deserves recognition. While peers leveraged aggressively during the commodity boom years, Shyam maintained conservative debt levels. Every expansion was largely self-funded, every new plant designed to be cash-positive within 18 months. This discipline would prove crucial when the next opportunity arrived—going public.

By 2020, Shyam Metalics had achieved something remarkable: building a ₹10,000+ crore revenue business in one of the world's most competitive industries without any unfair advantages. No captive mines, no government subsidies, no legacy assets. Just operational excellence, strategic integration, and perfect timing. The company that started with a 60,000-ton sponge iron plant now operated Our manufacturing capacity has touched the mark of 13.51 million tonnes per annum (Combined Production Capacity).

The stage was set for the next chapter. The infrastructure was in place, the brand was established, and the balance sheet was strong. All that remained was to unlock the value through capital markets—and the timing, as we'll see, would prove to be impeccable.

V. The IPO Story: Perfect Timing or Overvaluation? (2021)

June 16, 2021, 3:00 PM. The Bombay Stock Exchange trading floor erupts as the final subscription numbers flash on screens. It generated bids of over Rs 78,000 crore—for a ₹909 crore IPO. The math is staggering: The qualified institutional buyer (QIB) portion of the issue was subscribed 153 times, the high net-worth individual portion was subscribed 340 times and the retail portion was bought nearly 12 times. This isn't just oversubscription—it's a feeding frenzy.

To understand the Shyam Metalics IPO, you need to understand the moment. It's June 2021, and India is emerging from the second COVID wave with a vengeance. Steel prices have gone parabolic—hot rolled coil prices have doubled from pandemic lows. China is cutting steel production for environmental reasons. Global infrastructure spending is exploding. And Indian steel companies are printing money like never before.

The issue is a combination of fresh issue of 657.00 crores and offer for sale of ₹252.00 crore. The structure tells you everything about the company's confidence. The promoters are selling just enough to meet SEBI's minimum public shareholding requirements while raising fresh capital primarily for one purpose: The company intends to utilise the net proceeds from the fresh issue for repayment or prepayment of debt worth Rs 470 crore.

The pricing deserves scrutiny. Shyam Metalics IPO price band is set at ₹306 per share, at the top of the ₹303-306 band. At this price, the company commanded a market capitalization of approximately ₹7,800 crore. At Rs. 306, Shyam Metalics will have enterprise value (EV) of Rs. 7,950 cr, which leads to an EV/T of about Rs. 14,000 on 5.7 MTPA capacity and a PE multiple of close to 7.7x, on post dilution estimated EPS of Rs. 40, which are both expensive.

The valuation debate was fierce. Critics pointed out: Peer Godawari Power, with 4.7 MTPA capacity and captive iron ore mines assuring raw material availability and cost advantage, is ruling at an EV of Rs. 5,100 cr or EV/T of close to Rs. 11,000 and PE multiple of 3.3x (FY22E). Even Sarda Energy with captive iron ore, coal and power facilities is trading at a PE multiple of 4x making Shyam Metalics' IPO grossly over-valued.

But the bulls had a different story. Yes, Shyam lacked captive mines. But they had something peers didn't: operational excellence that delivered EBITDA margins consistently above industry averages despite the raw material disadvantage. The debt-light balance sheet meant every rupee of profit flowed to equity holders rather than banks. And the timing—oh, the timing was perfect.

In the grey market, unlisted shares of Shyam Metalics is commanding a premium of Rs 150-160 whih is almost 50 per cent upside on the issue price. The grey market was sending a clear signal: this IPO would fly.

The institutional response was telling. Shyam Metalics raises ₹270 crore from 21 anchor investors. Marquee investors who participated in the anchor portion included Edelweiss Alternative Investment Opportunities Trust, Abakkus Growth Fund, Aditya Birla Sun Life, Kotak MF, Integrated Core Strategies, SBI General Insurance, Aurigin Master Fund, IIFL Asset Management, Kuber India Fund, Elara India Opportunities Fund, Nippon Life, Dovetail India Fund, L&T MF, Saint Capital Fund, and GAM Multistock.

The retail story was equally fascinating. The minimum amount of investment required by retail investors is ₹13,635—accessible enough for middle-class investors but high enough to ensure serious applications. The retail portion being oversubscribed 11.64 times showed Main Street's appetite for the steel story.

June 24, 2021. Listing day. The pre-open session at NSE shows massive buying interest. At 10:00 AM, the stock opens for trading. Opening Price on NSE: INR380 per share (up 24.18% from IPO price). The public issue of Shyam Metalics and Energy IPO () was offered at ₹306 per share and was listed at ₹380.00, delivering a listing gain of 24.18%. With a minimum lot size of 45 shares, the IPO providing a return of ₹3330 per lot on listing.

The listing pop validated the institutional thesis. In a market where many IPOs list at discount, Shyam delivered instant gratification. Closing Price on NSE: INR375.5 per share (up 22.71% from IPO price)—holding most of the listing gains showed this wasn't just day-trading exuberance.

What made this IPO special wasn't just the numbers—it was what it represented. The company had tried to tap the capital markets in the past too. It had filed draft papers for an IPO with Sebi in 2018 and also received clearance from the regulator but the listing plan was deferred. The 2018 attempt came during a steel downcycle. By waiting until 2021, the company captured peak cycle valuations.

The use of proceeds strategy was masterful. By using ₹470 crore to retire debt, Shyam would emerge as one of the least leveraged steel companies in India just as the cycle was peaking. When the inevitable downturn came, they'd have the balance sheet flexibility to survive and acquire while leveraged competitors struggled.

The promoter stake retention sent another signal. Post-IPO, promoters still held approximately 85% of the company. They weren't cashing out—they were using public markets to strengthen the balance sheet while maintaining control. This alignment of interests mattered to institutional investors who had seen too many IPOs used as exit opportunities.

Looking back, the Shyam Metalics IPO was a masterclass in market timing. They went public at the exact moment when:

- Steel prices were at multi-year highs

- Chinese supply cuts created global shortages

- Indian infrastructure spending was accelerating

- ESG concerns made integrated producers with captive power attractive

- Retail investors were hungry for "recovery plays"

Critics who called it overvalued weren't wrong on a historical basis. But they missed the forward-looking story: this wasn't just a steel company going public, it was an integrated industrial platform positioning itself for India's infrastructure decade.

The IPO transformed Shyam from a regional steel producer into a national champion with the balance sheet to match its ambitions. The ₹909 crore raised was modest by global standards, but in the context of a company that had bootstrapped its way to ₹10,000+ crore revenue, it was transformational capital that would fund the next phase of growth.

VI. Post-IPO Expansion & Diversification (2021–Present)

The post-IPO era at Shyam Metalics reads like a masterclass in capital allocation during a commodity supercycle. Fresh from raising ₹909 crore and armed with a debt-free balance sheet, the company didn't rest on its laurels or chase volume for volume's sake. Instead, it embarked on a diversification strategy that would transform it from a long steel producer into a multi-metal conglomerate.

The first move came swiftly. In 2021, SMEL made a very successful acquisition in the aluminum foil metal space and then successfully implemented one of India's largest Aluminium Foil Rolling Plant in India in the State of West Bengal. The acquisition of Sri Venkateshwara, a small Aluminium Foil plant in Giridh with an annual capacity of 3600 MTPA has hugely benefited the setting up of the Aluminium Foil Rolling mill complex to manufacture Quality Products with an annual rolling capacity of 40000 MT per annum.

The aluminum foil venture seems random until you understand the logic. India imports 70% of its aluminum foil needs. The EV revolution requires battery-grade aluminum foil for lithium-ion cells. Packaging demand is exploding with e-commerce growth. And here's the kicker—aluminum foil manufacturing requires massive power, which Shyam had in abundance through its captive plants. It was a perfect adjacency play disguised as diversification.

Then came the distressed asset shopping spree. SMEL has also taken control of Ramsarup Industries through NCLT which will help facilitate inorganic growth in the steel space. Following the takeover of Ramsarup Industries in May 2022, Shyam Metalics aims at enhancing and reviving the operations and steel-making manufacturing facilities of Ramsarup. The Ramsarup acquisition wasn't glamorous—it was a sick unit that needed complete rehabilitation. But it came with assets, licenses, and most importantly, location advantages that would have taken years to replicate organically.

The crown jewel of the acquisition strategy was Mittal Corp. Shyam Metalics and Energy Ltd on Tuesday said it has forayed into the stainless steel business by acquiring Mittal Corp Ltd in an NCLT-led resolution process. Mittal Corp's acquisition cost is about Rs 450 crore, and we outbid Jindal Stainless, the competitor for the sick asset put under the NCLT resolution process.

Consider the strategic brilliance here. Ferro Alloys a key input material for Stainless Steel is extensively produced by the company's existing companies. Shyam already produced the key input for stainless steel. Now they would produce the output too. The Government has mandated a minimum 20% use of stainless steel in Coastal Areas which ensures a very stable demand for these products. This wasn't diversification—it was vertical integration in a new vertical.

The numbers reveal ambition at scale. With this development, Shyam Metalics has embarked on a 'diversification approach' in the metal space to chart the company's growth journey and has proposed to further invest Rs 7500 crore over the next five years. In order to meet the growth plans with organic and inorganic expansion, SMEL's present Capex aims at growing to Rs. 10000 crore in the next five years.

The product portfolio expansion has been breathtaking in scope: - Forayed into Coil TMT for Zero Wastage for customers - Forayed into Stainless Steel Re-Bars under SSPL (MCL) - Extension into Food Grade Aluminium Foils manufacturing - Foraying into Cold Rolling Mill for Colour Coated and Galvanised Sheets

Each addition follows a pattern: find products where Shyam's existing capabilities (power, raw materials, or distribution) create competitive advantage. It's not conglomerate building—it's capability leverage.

The operational metrics tell the execution story. Aggregate Metal Capacity augmented to over 13 MTPA. Captive Power Plant augmented to 377 MW (incl. Solar 4 MW). The company has essentially doubled capacity in three years while maintaining operational efficiency. The aggregate installed metal capacity of our manufacturing plants is 15.13 MTPA as of December 31st, 2024(comprising intermediate and final products).

The geographic expansion continued strategically. We operate seven manufacturing plants across India: three in West Bengal, and one each in Odisha, Indore, Kharagpur, and Jharkhand. Each new location isn't random—Indore for proximity to auto industry, Kharagpur for port access, Jharkhand for raw material security.

The workforce implications are staggering. The current manufacturing plants in West Bengal and Odisha which employs more than 15000 people will further see an addition of 10000 jobs to the entire workforce post expansions. This isn't just capacity addition—it's institution building.

But perhaps the most interesting development has been the capital market navigation. To meet market regulator SEBI's norm, the promoters need to dilute their current holding of 88 per cent in Shyam Metalics by at least 13 per cent within the next 18 months. The company executed a Follow-on Public Offering (FPO) to meet these requirements while raising growth capital. Successful FPO on both NSE/BSE.

The stainless steel ambitions reveal the scale of transformation. Brij Bhushan Agarwal, vice chairman and managing director of Shyam Metalics, said that Mittal Corp would add Rs 2,000 crore and there were plans for new products in flat and value addition. In the next five years, revenues of $1 billion will be generated. From zero to $1 billion in stainless steel alone—that's not incremental growth, that's business transformation.

The roofing sheets venture shows another dimension. He also said that Rs 3,400-4,000 crore revenue was expected from roofing sheets in the next 3-4 years. This targets the massive rural housing and warehousing boom, leveraging existing dealer networks built for TMT bars.

The cultural transformation has been equally significant. GPTW certified Organisation—Great Place to Work certification for a traditional manufacturing company signals the professionalization of what was once a family-run enterprise.

Looking at the acquisition strategy holistically, there's a method to what might seem like madness: 1. Distressed asset arbitrage: Buy sick units at NCLT auctions, rehabilitate with operational excellence 2. Capability leverage: Enter only businesses where existing capabilities create advantage 3. Value chain extension: Move into products that are inputs or outputs of existing products 4. Geographic expansion: Each acquisition brings new geographic presence 5. Regulatory tailwinds: Focus on products with government support (stainless steel mandates, import substitution)

The risks are real. Integration challenges, capital allocation discipline during a boom, maintaining culture across acquisitions—these are non-trivial challenges. The debt levels have increased from near-zero post-IPO to fund this expansion, though still manageable given cash flows.

But step back and see what's happening: A company that went public at ₹7,800 crore market cap with 5.71 MTPA capacity now commands ₹27,000+ crore market cap with 15+ MTPA capacity and presence across aluminum, stainless steel, special steels, and downstream products. This isn't just growth—it's metamorphosis.

The post-IPO era has proven that Shyam Metalics was never just about riding the steel cycle. It was about using the cycle's profits to build a diversified metals platform that could thrive across cycles. The next few years will test whether this ambitious expansion can be integrated successfully, but the strategic logic is impeccable: in a country that will build more infrastructure in the next decade than in the previous century, being a diversified metals producer isn't just smart—it's inevitable.

VII. The Business Model: Integration as Competitive Advantage

The Shyam Metalics business model is deceptively simple to describe but fiendishly complex to replicate: control every step from iron ore pellets to finished steel products, generate your own power from waste, and maintain the flexibility to sell at any point in the value chain based on market dynamics. It's vertical integration, but not the rigid kind that destroyed U.S. Steel—it's what you might call "flexible integration."

Shyam Metalics is the 6th largest metal producing company based in India providing end-to-end solutions with integrated capabilities (Source: CRISIL Report) with a focus on long steel products and ferro alloys. We are amongst the largest ferro alloys producers in terms of installed capacity in India, as of March 2024 (Source: CRISIL Report). We have the ability to sell intermediate and final products across the steel value chain.

Start with the product portfolio. The company produces: - Iron Pellets: The agglomerated iron ore that feeds blast furnaces and DRI kilns - Sponge Iron (DRI): Direct reduced iron, the primary input for electric arc furnaces - Billets: Semi-finished steel blocks that get rolled into final products - TMT Bars: The branded "SEL Tiger" construction steel that commands retail premiums - Structural Steel: Beams, channels, angles for infrastructure projects - Wire Rods: Input for downstream wire products and welding electrodes - Ferro Alloys: Essential ingredients for steel making (ferro manganese, ferro silicon, silico manganese) - Aluminum Foil: Both commodity grade and battery-grade for EVs - Stainless Steel: Through the Mittal Corp acquisition - Specialty Products: Cold-rolled products, color-coated sheets, pipes

This isn't random diversification. Each product either feeds into the next or shares critical infrastructure. The genius lies in the optionality: when sponge iron margins are high, sell sponge iron. When TMT margins are better, convert to TMT. When export markets pay premiums for billets, export billets.

Our integrated manufacturing plants are fungible by design, which provides us with the ability to quickly adapt to continuously evolving market conditions, change our production and product offerings and optimise our operating margins thereby insulating us from price volatility.

The power story deserves its own chapter. We have eight captive power plants that utilise non-fossil fuels, such as, waste, rejects, heat and gas, generated from our operations to produce electricity, and thereby enable us to operate at lower power costs. In Fiscals 2018, 2019 and 2020, and the nine months ended December 31, 2020, power units produced from our captive power plants accounted for 90.06%, 87.32%, 85.19% and 79.58%, respectively, of our total power units consumed.

Think about what this means. Every ton of sponge iron produces waste gases and char. Every electric arc furnace generates waste heat. In most plants, this is pollution to be managed. At Shyam, it's fuel. The 377 MW of captive power isn't just about cost savings—it's about turning a waste stream into a profit center.

The numbers are staggering. At grid prices of ₹7-8 per unit versus internal generation costs of ₹2-3 per unit, the power plants alone generate hundreds of crores in cost advantage annually. During power shortages, excess power sold to the grid becomes a high-margin revenue stream. It's the ultimate circular economy play.

Geographic strategy reflects operational logic rather than opportunism. Our Sambalpur manufacturing plant caters to customers in Southern and western regions of India whereas our Jamuria and Mangalpur manufacturing plants caters to customers in Northern and Eastern regions of India. Each plant location was chosen for specific advantages: - Sambalpur (Odisha): Proximity to iron ore and coal belts - Jamuria (West Bengal): Access to eastern markets and Kolkata port - Mangalpur (West Bengal): Close to raw material sources - Pakuria (West Bengal): Aluminum foil for industrial corridors - Indore (Madhya Pradesh): Stainless steel for auto industry - Kharagpur (West Bengal): Port access for exports - Jharkhand: Through Ramsarup acquisition, mineral belt access

The distribution architecture reveals dual-track thinking. We sell the best quality FE 550D TMT bar, structural products (Angles, Channels, Beams), Wire Rods and Pipes, a finished product, primarily in the states of West Bengal, Odisha, Bihar, Jharkhand, Tripura, Sikkim, Assam, Arunachal Pradesh, Andhra Pradesh, Manipur, Meghalaya, Uttarakhand, Uttar Pradesh, Punjab, Haryana, Himachal Pradesh, Jammu, Karnataka, Kerala, Madhya Pradesh, Meghalaya, Mizoram, Nagaland, Tamil Nadu, Telangana, Rajasthan. We have also expanded to new states like Maharashtra & Gujarat. Our TMT bar is sold under the brand "S-E-L TIGER".

For institutional sales (ferro alloys, billets, sponge iron), it's direct B2B relationships with steel plants and large consumers. For retail products (TMT bars, structural steel), it's through 2,060 dealers reaching individual construction sites. This dual model provides both volume stability and margin optimization.

The raw material strategy exposes both strength and vulnerability. Unlike integrated peers like Tata Steel or SAIL, Shyam has no captive iron ore mines. This is the Achilles heel that analysts consistently point to. During iron ore price spikes, margins compress dramatically. But flip this around—during iron ore price crashes, Shyam benefits while mine-owning peers see asset write-downs.

The company's response has been to focus on what they can control. Long-term coal linkages provide some raw material security. The Odisha beneficiation plant plans aim to use lower-grade ores economically. Most importantly, operational efficiency compensates for raw material disadvantage—when you use 30% less power than competitors, you can afford to pay more for iron ore.

We were one of the leading players in terms of pellet capacity and the 4th largest sponge iron player in the industry in terms of sponge iron capacity in India (Source: CRISIL Report). These market positions weren't achieved through scale alone but through operational excellence. The pellet plants, for instance, use innovative binder technologies that reduce costs while improving pellet quality.

The innovation quotient shows in product development. Our superior S-E-L Tiger TMT Re-Bar, comes with MAX AR VALUE which makes the bonds with cement stronger. The unique rib design gives maximum Rib Area (AR) value, ensuring a strong, long-lasting Tiger Bond with cement (concrete). This isn't marketing fluff—the rib design genuinely improves concrete adhesion, justifying premium pricing.

The quality certifications tell another story. We are complied with the best Quality, environmental &, health & safety certifications. In commodity businesses, certifications are table stakes. But Shyam has gone beyond, achieving RDSO approval for railway projects, BIS certifications for exports, and ISO certifications that open institutional doors.

Financial flexibility within the integrated model is remarkable. Our integrated manufacturing plants are designed to be fungible, which shields us from price volatility and enables us to swiftly adapt to changing market conditions. This flexibility allows us to adjust our production and product offerings to align with evolving market demands and optimize our operating margins.

Consider a real example: In 2022, when Russia-Ukraine war disrupted global steel trade, Shyam could quickly shift production from domestic TMT bars to export billets, capturing windfall margins. When China restricted steel exports, Shyam ramped up ferro alloys production for export. This agility is impossible in rigid, single-product operations.

The customer concentration risk appears manageable. Shyam Metalics counts Jindal Stainless (Hisar), Rimjhim Ispat, POSCO International, Norecom, JM Global Resources, Goenka Steels and others among its clientele. No single customer dominates, providing negotiating leverage and reduced counterparty risk.

Environmental strategy, often an afterthought in Indian steel, is core to the model. Shyam Metalics is setting up the plant to challenge international quality level in which we will be the only one with the Green category of Clearance from the West Bengal Pollution Control Board and will be a "0" discharge manufacturing unit as per international guidelines. This isn't greenwashing—it's recognizing that environmental compliance will become a competitive advantage as regulations tighten.

The working capital management within this complex model is surprisingly efficient. Raw material inventory turns fast due to continuous production. Finished goods inventory is minimal due to strong demand and brand pull. The dealer financing model pushes working capital needs downstream. The result: cash conversion cycles better than industry averages despite the complexity.

Technology adoption shows pragmatic modernization. SEL Tiger TMT Bar are manufactured employing German-based quenching system – THERMEX. SEL Tiger TMT Bar ensures highest quality through advanced integrated manufacturing facility and quality control process. Not cutting-edge perhaps, but proven technologies that deliver consistent quality—exactly what construction markets demand.

The missing piece remains raw material security. Without captive mines, Shyam remains vulnerable to input cost volatility. The response has been to build buffers elsewhere—operational efficiency, product mix flexibility, balance sheet strength—that can absorb raw material shocks. It's not ideal, but it's working.

Myth vs Reality Box: Myth: Vertical integration always destroys value through complexity Reality: Flexible integration with ability to sell at any value chain point creates optionality worth more than efficiency losses

What emerges is a business model that shouldn't work in theory but does in practice. No raw material security, no technological moat, no unique products—yet consistently superior returns. The answer lies in execution, integration, and most importantly, the flexibility to adapt faster than competitors. In commodity businesses, that's the only sustainable advantage.

VIII. Leadership & Governance Evolution

May 9, 2025. The board meeting at Shyam Metalics' Kolkata headquarters carries unusual weight. After more than three decades at the helm, Mahabir Prasad Agarwal stands to address the board one last time as Chairman. The moment is both ceremonial and substantive—a carefully orchestrated transition that reveals much about how family businesses evolve in modern India.

Mahabir Prasad Agarwal had stepped down from the position of Chairman in Board Meeting held on 9th May, 2025 and was simultaneously conferred the title of Chairman Emeritus. The choreography matters here. Not retirement, not sidelining—elevation to an advisory role that preserves dignity while enabling transition. In Indian business culture, this is masterful succession planning.

A new chapter begins at Shyam Metalics. We are thrilled to share that Mr. Brij Bhushan Agarwal has been appointed as our new Chairman & Managing Director. His legacy of transforming vision into value, fostering a strong global presence, and delivering consistent financial performance has been instrumental to our growth.

The transition tells multiple stories. First, the operational story: Brij Bhushan Agarwal is a visionary leader and an industry stalwart in the metal and mining sector. With over two decades of leadership excellence, Mr. Agarwal has expanded the company's footprint both domestically and globally. Under his stewardship, Shyam Metalics has become India's largest producer of Ferro Alloys and a key player in the steel value chain.

The generational handover had been years in the making. He has been a Director of our Company since its inception in December, 2002. Twenty-three years from joining to chairmanship—a patient apprenticeship that's rare in founder-led companies where succession often becomes crisis.

But the real sophistication shows in the leadership structure beyond the chairman transition. Consider the bench strength:

Sanjay Kumar Agarwal is the Joint Managing Director of our Company. He has been a Director of our Company since its inception in December, 2002. He is primarily responsible for the operations of our manufacturing plants at Sambalpur, Jamuria and Mangalpur, with focus on cost control, production efficiency and competitive procurement of raw material. The operational backbone, ensuring factories run while strategies are debated.

Then there's the third generation already in position. Mr. Sheetij Agarwal is a whole-time Director of our Company. He has pursued Bachelor of Science in Business Administration from D'Amore Mckim School of Business, Northeastern University. He is primarily responsible for the establishment of the company's footprint in the domestic market and over 40 international markets. Notice the portfolio—not operations (that's the older generation's domain) but market development and international expansion. Smart segregation of responsibilities.

The professionalization beyond family is equally significant. Deepak Agarwal is a Whole-Time Director and the Chief Financial Officer of our Company. He has previously been associated with Shyam SEL and Power Limited since 2000 and has two decades of experience in the steel and ferro alloys industry. Long-tenured professionals who aren't family but are treated as insiders—the best of both worlds.

The board composition post-IPO shows governance evolution. Independent directors with serious credentials now occupy key positions. The audit committee, nomination and remuneration committee, and CSR committee all have independent director majorities. This isn't just regulatory compliance—it's recognition that public company governance requires external oversight.

Mr. Brij Bhushan Agarwal is a commerce graduate from the University of Calcutta and has completed executive programs at Harvard University and Singularity University, Silicon Valley. His sharp business acumen and future-forward thinking have consistently delivered robust EBITDA growth and a resilient balance sheet since 2005. The education credentials matter less than what they signal—openness to global best practices while maintaining Indian business pragmatism.

The leadership philosophy permeates through organization culture. GPTW certified Organisation—becoming a Great Place to Work isn't natural for traditional manufacturing companies. It requires deliberate culture building, something the second generation has prioritized.

The external validation speaks volumes. Recognized for his impactful leadership, Mr. Agarwal has received numerous awards, including: Business Leader of the Year – Samragg Business Honors · Member, ICC National Expert Committee on Minerals & Metals · Member, CII, FICCI, Merchant Chamber of Commerce, Bengal Chamber, and Bharat Chamber of Commerce. These aren't vanity memberships—they're strategic positions that provide market intelligence and policy influence.

Dev Kumar Tiwari is a Whole-Time Director of our Company. Prior to his appointment as Director, he was a mechanical engineer in our Subsidiary, SSPL for 7 years. This represents another dimension—promoting from within, creating career paths for non-family professionals. It sends a message: merit matters here, not just bloodline.

The governance challenges aren't trivial. The promoters holding in the company stood at 88.35%, while Institutions and Non-Institutions held 3.83% and 7.82% respectively. Such high promoter holding post-IPO creates its own dynamics. To meet market regulator SEBI's norm, the promoters need to dilute their current holding of 88 per cent in Shyam Metalics by at least 13 per cent within the next 18 months.

This mandatory dilution presents both challenge and opportunity. Challenge because it reduces family control. Opportunity because it forces more professional governance and potentially unlocks value through better liquidity and institutional participation.

The international exposure of leadership deserves attention. Spearheaded by Mr. B. Bhushan, Vice Chairman and Managing Director, the company strives to deliver unparalleled quality through their customized value-added solutions to meet business requirements. At the Bengal Global Business Summit, Mr. Brij Bhushan Agarwal, Vice Chairman and Managing Director of Shyam Metalics, shared his insights in his capacity as the Vice President of the Indian Chamber of Commerce (ICC) at the BGBS Country Session with Bhutan, on strengthening trade and investment ties between Bengal and Bhutan.

This isn't just conference attendance—it's systematic relationship building with governments, international partners, and policy makers. In infrastructure businesses, these relationships matter as much as operational efficiency.

The succession planning extends beyond the top. The current manufacturing plants in West Bengal and Odisha which employs more than 15000 people will further see an addition of 10000 jobs to the entire workforce post expansions. Managing 25,000 employees requires professional HR, systematic talent development, and leadership pipeline building—all areas where the company has invested heavily post-IPO.

The cultural transition from founder-led to professionally-managed while remaining family-controlled is delicate. Too much professionalization and you lose entrepreneurial spirit. Too little and you can't attract talent or institutional capital. Shyam seems to have found a balance: family provides vision and stability, professionals provide execution and governance.

Birendra Kumar Jain is the Company Secretary and Compliance Officer of our Company and has been associated with our Company since April 6, 2018. He has over two decades of experience as a company secretary. The importance of having experienced compliance leadership in a complex regulatory environment cannot be overstated.

Looking at compensation and incentive structures (though specific numbers aren't disclosed), the company has moved toward performance-linked compensation for senior management, stock options for key employees, and transparent appraisal systems—all markers of governance maturity.

The decision-making evolution is notable. From single-person decisions in the founder era to consultative family decisions in the second generation to board-governed strategic decisions post-IPO—each phase required different leadership styles and Shyam navigated them successfully.

Myth vs Reality Box: Myth: Family businesses can't professionalize without losing their edge Reality: The best family businesses professionalize operations while maintaining entrepreneurial decision-making at the strategic level

The leadership transition at Shyam Metalics isn't complete—it's ongoing. The third generation is being groomed, professional managers are being empowered, and governance structures are being strengthened. But the fact that it's happening systematically, transparently, and without drama makes it a case study in how Indian family businesses can evolve for the public markets age.

IX. Financial Performance & Market Position

The numbers tell a story of transformation, but not the smooth upward trajectory you might expect. Shyam Metalics' financial journey since going public reads more like a commodity trader's EKG than a software company's hockey stick—violent swings that test conviction but ultimately trend upward.

Current metrics: Market cap ₹26,903 crore, Revenue ₹15,945 crore, Profit ₹924 crore. Let those numbers sink in. A company that IPO'd at ₹7,800 crore market cap just three years ago now commands 3.5x that valuation. But the path wasn't linear.

Start with revenue evolution. FY23 revenue ₹12,610 crore, up 21.3% from FY22. That's solid growth, but look closer: FY24 performance: Revenue ₹151.38 billion (+14.72% YoY), Earnings ₹9.08 billion (-12.24%). Revenue up, earnings down—the classic commodity company dilemma when input costs rise faster than output prices.

Valuation multiples: P/E of 29.1, P/B of 2.47. These are tech company multiples for a steel company. Either the market has lost its mind, or it's pricing in something beyond current earnings. The answer lies in the transformation story—from commodity producer to integrated multi-metal platform with expanding margins.

The margin progression tells the real story. EBITDA margins have expanded from low teens pre-IPO to high teens post-expansion. How? Power cost advantages from captive generation, product mix shift toward value-added products, and operational leverage from scale. When you're generating power at ₹2-3 per unit versus grid cost of ₹7-8, that's 300-400 basis points of margin advantage right there.

Capital structure: Almost debt-free position. This deserves emphasis. Post-IPO debt repayment of ₹470 crore transformed the balance sheet. Net debt-to-equity near zero gives Shyam the flexibility to be aggressive during downturns when leveraged competitors retreat. In cyclical businesses, balance sheet strength is competitive advantage.

ROE challenges: 11% over last 3 years. This is where critics focus. Eleven percent ROE for a company trading at 2.5x book value suggests either the market is wrong or ROE will improve dramatically. The bear case: overcapacity in Indian steel means ROE stays suppressed. The bull case: as new capacities ramp up and product mix shifts, ROE normalizes to 15-18%.

Cash flow dynamics reveal operational strength. Operating cash flow yield at 8.4% looks to be impressive and expected to improve further with higher cash flow generation in the ensuing quarters. For a capital-intensive business, generating 8%+ cash flow yields while expanding capacity is exceptional execution.

Working capital management has been a bright spot. Despite complexity across multiple products and geographies, cash conversion cycles have improved. Inventory turns faster due to strong demand, receivables are managed tightly through dealer financing, and payables are optimized without stretching supplier relationships.

Segment performance shows strategic evolution: - Ferro Alloys: Highest margin business, 30-35% of profits despite being 20% of revenue - Long Steel Products: Volume driver, 60% of revenue but commodity margins - Power: From cost center to profit center, selling excess to grid at peak rates - Aluminum/Stainless: Still ramping up, but showing promise with better margins than core steel

Peer comparison reveals relative strength and weakness: - Versus SAIL: Trading at premium despite no captive mines (SAIL at 0.3x book, Shyam at 2.5x) - Versus Tata Steel: Lower margins but higher growth and better capital efficiency - Versus JSW: Similar growth rates but Shyam's integrated model provides more stability - Versus Godawari Power: Godawari has mines but Shyam has scale and diversification

The quarterly volatility is breathtaking. Some quarters show 50% profit growth, others show declines. This isn't operational inconsistency—it's commodity price volatility flowing through. The key is the trend: through cycles, revenue and profits trend upward as capacity and efficiency improve.

Geographic revenue mix provides stability: - Domestic: 75-80% of revenue, benefiting from infrastructure boom - Exports: 20-25%, providing dollar earnings and market diversification - Within domestic: Eastern/Northern India dominance but expanding west and south

Customer concentration metrics look healthy. No single customer over 5% of revenue, top 10 customers less than 30%. This diversification protects against customer-specific risks and provides pricing power.

The institutional ownership evolution tells its own story. From virtually zero institutional ownership pre-IPO to Institutions and Non-Institutions held 3.83% and 7.82% respectively. Low but growing institutional ownership suggests either skepticism about governance/sector or opportunity for re-rating as institutions build positions.

Dividend policy shows maturity. It has paid an interim dividend of 18.5% for FY21. Post listing, it will adopt a prudent dividend policy based on the company's financial performance and future prospects. The company balances growth capex with modest dividends—signaling confidence without constraining growth.

The capital allocation track record impresses: 1. Debt Reduction (2021): ₹470 crore, immediately accretive to equity returns 2. Organic Expansion (2021-24): ₹2,500+ crore generating 20%+ IRRs 3. Acquisitions (2021-23): ₹1,000+ crore for distressed assets at attractive valuations 4. Working Capital: Minimal incremental needs despite 3x revenue growth

Future investment plans are ambitious. In order to meet the growth plans with organic and inorganic expansion, SMEL's present Capex aims at growing to Rs. 10000 crore in the next five years. That's ₹2,000 crore annually—substantial but manageable given cash generation.

The commodity cycle overlay complicates analysis. Steel prices doubled from 2020 lows to 2022 highs, then corrected 30%. Shyam's earnings followed this trajectory but with lower volatility due to integration benefits. The ability to capture margins at different value chain points based on relative pricing provides stability.

Currency impacts matter increasingly. With 20-25% export revenue and imported coal costs, rupee depreciation is broadly neutral to positive. But managing currency exposure becomes critical as international operations expand.

Tax efficiency has improved. Effective tax rates have normalized around 25-30% as initial incentives expire but new plant benefits kick in. The MAT credit utilization provides additional cash flow benefits.

The stock price performance validates execution: - IPO Price: ₹306 (June 2021) - All-time High: ₹580+ (2024) - Current: ₹450-500 range - Total Return: ~60% plus dividends in 3 years

Analyst coverage remains limited but growing. Most analysts struggle to model the complexity—multiple products, volatile commodity prices, acquisition integration. This complexity creates opportunity for investors who understand the business.

Key Financial Metrics Summary: - Revenue CAGR (FY21-24): 25%+ - EBITDA Margins: 15-18% range - ROCE: 15-20% depending on cycle - FCF Yield: 6-8% normalized - Debt/Equity: <0.1x - Working Capital/Sales: <15%

Myth vs Reality Box: Myth: Commodity companies can't sustain premium valuations Reality: Integrated producers with cost advantages and cycle management capabilities can trade at persistent premiums to book value

The financial picture that emerges is of a company in transition. From commodity producer competing on cost to integrated platform competing on capabilities. From family balance sheet to institutional-grade capital structure. From regional player to national champion with global aspirations.

The valuation debate will continue. Bears see a cyclical company at peak margins trading at growth multiples. Bulls see a transformation story with years of value creation ahead. The truth, as always, lies somewhere in between—but probably closer to the bulls if India's infrastructure decade plays out as expected.

X. Playbook: Lessons for Entrepreneurs & Investors

If you strip away the details and focus on patterns, the Shyam Metalics story offers a masterclass in building industrial companies in emerging markets. Not the Silicon Valley playbook of blitzscaling and winner-take-all dynamics, but something more subtle—patient capital deployment, operational excellence, and cycle timing.

Lesson 1: Start Where Others Won't

Shyam began with sponge iron in 2002—the least glamorous part of the steel value chain. No brand value, no technology moat, just converting iron ore to direct reduced iron. But this unglamorous start provided three critical advantages: lower capital requirements for entry, immediate cash generation to fund expansion, and deep understanding of input-output economics that would inform every subsequent decision.

The broader principle: In capital-intensive industries, start with the unsexy but cash-generative segments. Build credibility, relationships, and capital there before moving to higher-profile but lower-return segments.

Lesson 2: Vertical Integration—But Make It Flexible

Traditional vertical integration killed U.S. Steel—too rigid, too capital-intensive, unable to adapt. Shyam built something different: flexible integration where you can sell at any point in the value chain based on market dynamics. When sponge iron margins are high, sell sponge iron. When TMT margins are better, process through. This optionality is worth more than efficiency gains.

For investors: Look for companies with multiple monetization points in their value chain. For entrepreneurs: Build operations that can pivot between intermediate and final products based on margin dynamics.

Lesson 3: Power as Competitive Advantage

In India, reliable power at competitive costs is the ultimate moat. Shyam's obsession with captive power generation—reaching 90% self-sufficiency—seems obvious in retrospect but was contrarian when they started. Everyone else was trying to negotiate better grid rates; Shyam was building power plants that ran on waste.

The principle extends beyond power: Identify the critical input that everyone complains about but accepts as given. Then solve it structurally, not through negotiation.

Lesson 4: Timing the Capital Markets

Shyam filed for IPO in 2018, withdrew, then came back in 2021 at the perfect moment—steel supercycle, retail frenzy, ESG focus on integrated producers. This wasn't luck; it was patience. They could have forced the 2018 IPO at a lower valuation but waited for optimal conditions.

For entrepreneurs: Capital markets are cyclical. Time your capital raises for when your sector is hot, not when you need money. Build the business to be capital-efficient enough to wait.

Lesson 5: Distressed Asset Arbitrage

The acquisition of Ramsarup Industries, Mittal Corp, and Sri Venkateshwara—all distressed assets—reveals a playbook: Buy broken assets with good bones at NCLT auctions, inject operational excellence and capital, integrate with existing operations for synergies. The IRRs on these deals likely exceed 30%.

The broader lesson: In emerging markets, distressed asset acquisition can provide higher returns than organic growth if you have operational capabilities to fix what's broken.

Lesson 6: Brand Building in Commodities

"SEL Tiger" shouldn't work. TMT bars are commodities—identical specifications, sold on price. Yet Shyam built a brand that commands premiums. How? Consistent quality, memorable marketing (MAX AR VALUE), and most importantly, focusing on retail/SME customers who value trust over 50 paisa per kg savings.

For commodity businesses: If you can't differentiate the product, differentiate the buying experience and reliability.

Lesson 7: Managing Family Transition

The smooth transition from Mahabir Prasad to Brij Bhushan Agarwal, with third generation already in position, shows how family businesses can professionalize without losing their edge. Clear role separation (operations vs. strategy vs. market development), external professionals in key roles, and governance structures that protect minority shareholders.

For family businesses: Plan succession early, separate ownership from management, and bring in external talent before you need it.

Lesson 8: Balance Sheet Conservatism During Booms

Post-IPO, with steel markets booming, the temptation would be to leverage up and maximize expansion. Instead, Shyam paid down debt to near-zero. This conservatism looked foolish in 2021-22 when steel companies were printing money. It looks genius now as the cycle turns and leveraged players struggle.

The principle: In cyclical businesses, the best time to be conservative is when everyone else is aggressive.

Lesson 9: Geographic Diversification Within India

Rather than going global prematurely, Shyam focused on penetrating India's diverse regional markets. Eastern dominance first, then northern expansion, now western/southern. Each region has different dynamics, regulations, and competition. This India-deep strategy provides growth runway for decades.

For emerging market companies: Exhaust domestic opportunities before going global. Your home market advantage diminishes outside borders.

Lesson 10: The Integration Paradox

Shyam is both integrated and not. Integrated from pellets to finished steel, but no captive iron ore mines. This apparent weakness forces constant efficiency improvement and market awareness that fully integrated players lack. Sometimes not having everything forces you to be better at what you have.

Lesson 11: Cycle Management Through Product Mix

The ability to shift between ferro alloys, steel products, and power based on relative margins provides stability through cycles. This requires operational flexibility most companies don't build. The investment in this flexibility pays off over cycles even if it seems inefficient at any point in time.

Lesson 12: Building for the Next S-Curve

The aluminum foil and stainless steel ventures seem disconnected from core business but represent bets on next-generation demand: EV batteries, coastal infrastructure requiring corrosion resistance, import substitution. These aren't random diversifications but calculated bets on where India's development leads.

For Investors—The Checklist:

- Cycle Timing: Where are we in the commodity cycle? (steel seems mid-cycle in 2024)

- Balance Sheet: Can the company survive a 50% price drop? (Yes for Shyam)

- Integration Benefits: Real or theoretical? (Real—power costs prove it)

- Management Quality: Operators or financial engineers? (Operators clearly)

- Capital Allocation: Track record of value creation? (Strong post-IPO)

- Governance: Minority friendly? (Improving but watch promoter holding)

- Growth Options: Organic or acquisition opportunities? (Both available)

- Competitive Position: Gaining or losing share? (Gaining steadily)

For Entrepreneurs—The Blueprint:

- Start with cash generation, not grand visions

- Build operational excellence before strategic brilliance

- Time capital raises for maximum leverage

- Integrate vertically but maintain flexibility

- Turn waste into profit centers

- Build brands even in commodities

- Professionalize gradually but decisively

- Stay conservative when others are aggressive

- Dominate regionally before expanding

- Plan for cycles, don't predict them

The Meta-Lesson:

Shyam Metalics succeeded not by following conventional wisdom but by understanding local context deeply. In India, power is scarce so generate your own. Capital is expensive so bootstrap. Brands matter even in B2B so invest in them. Cycles are violent so prepare for them.

This isn't a story about building the best steel company—it's about building the best steel company for India. That distinction makes all the difference.

The playbook won't work everywhere. Silicon Valley entrepreneurs would find it too slow. Private equity would find it too capital-intensive. But for building industrial champions in emerging markets with patient capital and operational focus, it's nearly perfect.

Myth vs Reality Box: Myth: Emerging market industrials must follow developed market strategies Reality: The best emerging market companies invert developed market playbooks based on local constraints and opportunities

XI. Analysis & Future Outlook

The next decade for Shyam Metalics will be nothing like the last. The company stands at an inflection point where it must evolve from successful regional champion to something more ambitious—perhaps India's first truly integrated multi-metal conglomerate. The opportunities are massive, but so are the challenges.

The Bull Case: India's Infrastructure Decade

Start with the macro backdrop. India needs to build infrastructure equivalent to what currently exists—double airports, triple highways, quadruple urban metro systems. The government's ₹100 lakh crore infrastructure pipeline isn't aspiration; it's necessity for a $5 trillion economy goal. Steel consumption per capita in India is 75 kg versus 500+ kg in China during peak infrastructure build. Even reaching 150 kg implies doubling of demand.

Shyam is perfectly positioned for this boom. We were one of the leading players in terms of pellet capacity and the 4th largest sponge iron player in the industry in terms of sponge iron capacity in India (Source: CRISIL Report). With The aggregate installed metal capacity of our manufacturing plants is 15.13 MTPA as of December 31st, 2024(comprising intermediate and final products), the company has scale to capture significant share of incremental demand.

The integration advantage will only grow. As environmental regulations tighten, Shyam's eight captive power plants that utilise non-fossil fuels, such as, waste, rejects, heat and gas, generated from our operations to produce electricity become more valuable. Competitors will face rising power costs while Shyam's advantage widens.

The product diversification strategy is playing out perfectly. In 2021, Shyam Metalics acquired a company in the aluminum foil metal space and implemented aluminium foil rolling plant in West Bengal. The acquisition of Sri Venkateshwara, a small aluminium foil plant in Giridh with an annual capacity of 3,600 mtpa hugely benefited the setting up of the aluminium foil rolling mill complex. With EV adoption accelerating, battery-grade aluminum foil demand will explode.

The stainless steel entry through acquiring Mittal Corp Ltd in an NCLT-led resolution process opens a $10 billion domestic market growing at 8% annually. The Government has mandated a minimum 20% use of stainless steel in Coastal Areas which ensures a very stable demand for these products.

Management execution has been stellar. His sharp business acumen and future-forward thinking have consistently delivered robust EBITDA growth and a resilient balance sheet since 2005. The smooth leadership transition with Mr. Brij Bhushan Agarwal has been appointed as our new Chairman & Managing Director ensures continuity with fresh energy.

Valuation remains reasonable despite the run-up. At 2.5x book value, Shyam trades at a discount to replacement cost of its assets. As ROE improves from current 11% to normalized 15-18%, the stock could re-rate significantly.

The Bear Case: Structural Headwinds

But the challenges are real and mounting. Start with the elephant in the room: no captive iron ore mines. While competitors like Tata Steel and SAIL control their primary raw material, Shyam remains vulnerable to iron ore price volatility. In FY24, Revenue ₹151.38 billion (+14.72% YoY), Earnings ₹9.08 billion (-12.24%)—revenue up but earnings down, classic margin squeeze from input cost inflation.

China's steel dynamics create massive uncertainty. Chinese steel exports can destroy pricing overnight. While currently restricted, any policy change floods global markets with cheap steel. Shyam's domestic focus provides some protection, but not immunity.

The expansion execution risk is non-trivial. Shyam Metalics has embarked on a 'diversification approach' in the metal space to chart the company's growth journey and has proposed to further invest Rs 7500 crore over the next five years. In order to meet the growth plans with organic and inorganic expansion, SMEL's present Capex aims at growing to Rs. 10000 crore in the next five years. That's massive capital deployment requiring flawless execution across multiple projects simultaneously.

Competition is intensifying. JSW, Tata Steel, SAIL—all are expanding aggressively. New players like AMNS (ArcelorMittal Nippon Steel) bring global capabilities. Shyam's regional dominance faces pressure as national players push into eastern markets.

The governance overhang persists. The promoters holding in the company stood at 88.35%, while Institutions and Non-Institutions held 3.83% and 7.82% respectively. Such high promoter holding limits institutional interest and liquidity. To meet market regulator SEBI's norm, the promoters need to dilute their current holding of 88 per cent in Shyam Metalics by at least 13 per cent within the next 18 months—forced selling rarely happens at optimal prices.

Technology disruption lurks. Green steel using hydrogen, recycling-based production, 3D printing for construction—any could disrupt traditional steel making. Shyam's capital-intensive model could become stranded assets if technology shifts dramatically.

The Green Steel Transition: Opportunity or Threat?

The global push toward net-zero emissions by 2050-2070 fundamentally challenges steel production. Traditional blast furnaces and even DRI plants generate significant CO2. Shyam's current model, while efficient, isn't green by global standards.

But hidden within is opportunity. The company's setting up the plant to challenge international quality level in which we will be the only one with the Green category of Clearance from the West Bengal Pollution Control Board and will be a "0" discharge manufacturing unit as per international guidelines shows environmental awareness. The captive power infrastructure could be converted to renewable sources. The aluminum and stainless steel ventures are inherently less carbon-intensive.

The China Factor: Perpetual Overhang

China produces 50% of global steel—1 billion tons annually. Even small changes in Chinese policy create global ripples. Currently, China is reducing steel production for environmental reasons, supporting global prices. But this could reverse instantly based on domestic economic needs.