Sharda Cropchem: The Asset-Light Agrochemical Maverick

I. Introduction & Episode Roadmap

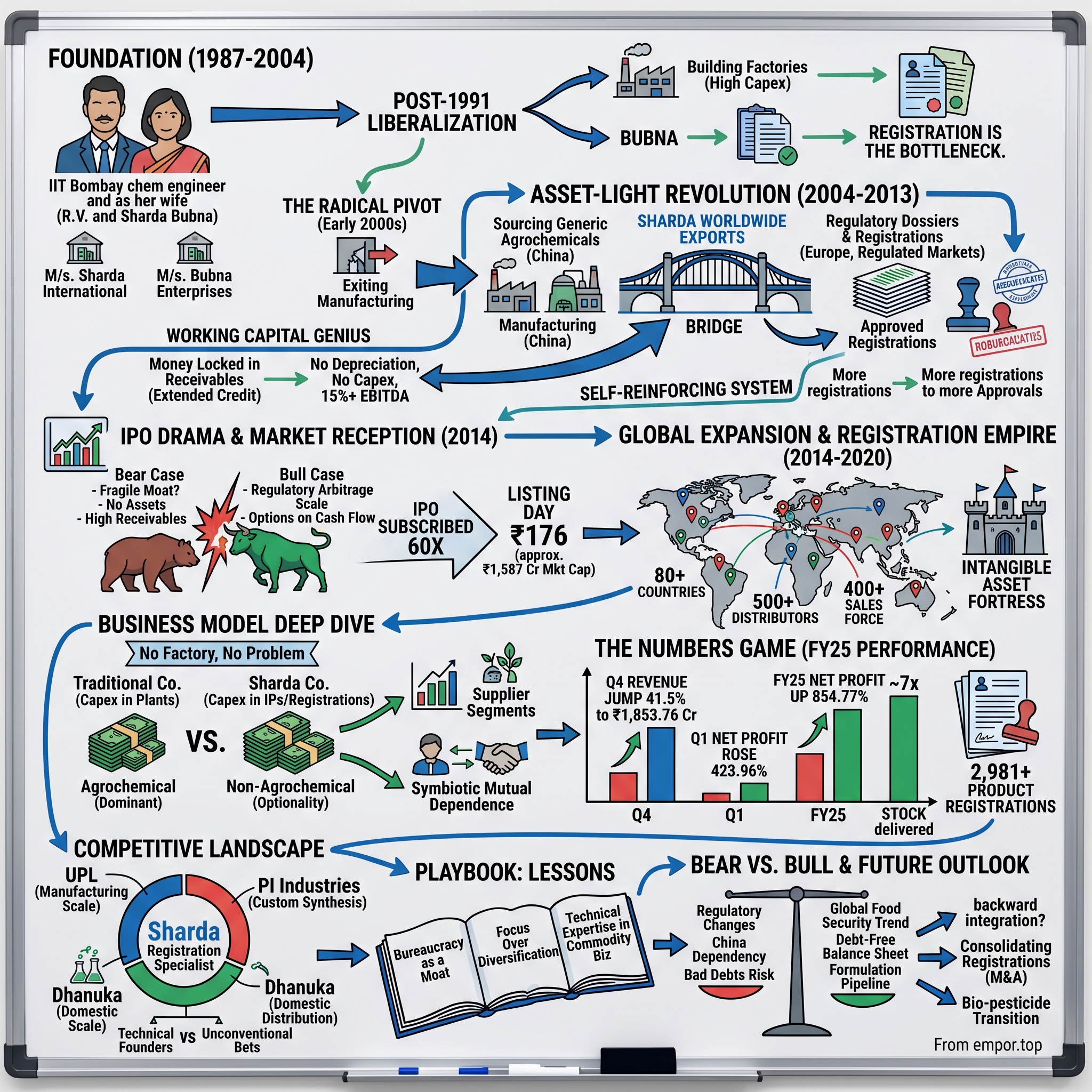

Picture this: A chemical engineer from IIT Bombay and his wife, starting with a small trading operation in 1987, building what would become an ₹8,945 crore agrochemical empire—all without owning a single manufacturing facility. While competitors poured billions into factories, reactors, and production lines, R.V. Bubna and Sharda Bubna chose a radically different path: they would conquer the global agrochemical market armed with nothing but regulatory dossiers, relationships, and an iron grip on working capital management. Today, Sharda Cropchem stands as an ₹8,945 crore market capitalization giant with revenue jumping 41.5% year-over-year to ₹1,853.76 crore in Q4 FY25. But the numbers only tell part of the story. This is a tale of regulatory arbitrage at its finest—where understanding European Union dossier requirements better than European companies themselves became a multi-billion rupee business model. It's about recognizing that in agrochemicals, as in pharmaceuticals, the real value often lies not in the molecule but in the right to sell it.

The asset-light model of Sharda Cropchem challenges everything we think we know about manufacturing businesses. While UPL invests thousands of crores in production facilities and PI Industries builds sophisticated chemistry plants, Sharda has proven that in the modern economy, intellectual property in the form of regulatory approvals can be more valuable than physical assets. Think of it as the Uber of agrochemicals—except instead of disrupting taxi medallions, they're arbitraging pesticide registrations.

What makes this story particularly fascinating for investors is the paradox at its core: a company with a low return on equity of 9.89% over the last 3 years and high debtors of 165 days, yet one that has delivered spectacular returns since its 2014 IPO. How does a business with negligible tangible assets and six months of sales locked in receivables create sustainable competitive advantages? The answer lies in understanding that in regulated markets, bureaucracy itself can become a moat.

II. The Bubna Story & Foundation (1987–2004)

The Mumbai of 1987 was a city on the cusp of transformation. License Raj still gripped the economy, but whispers of liberalization were beginning to circulate in business circles. In this environment, R.V. Bubna, a chemical engineer from IIT Bombay with the technical precision that comes from India's premier engineering institute, saw an opportunity that others missed. Together with his wife Sharda, they didn't just start a business—they began what would become a masterclass in spotting inefficiencies in global supply chains.

The initial ventures—M/s. Sharda International in 1987 and M/s. Bubna Enterprises in 1989—were humble sole proprietorships. But the Bubnas weren't thinking small. They began manufacturing and exporting dyes, dye intermediates, pesticides, agrochemicals, and even V-Belts. It was a scattered portfolio by design, allowing them to learn the nuances of international trade while building relationships across multiple product categories. Each shipment taught them something new about documentation, quality requirements, and most importantly, the regulatory maze that governed chemical exports.

The post-1991 liberalization changed everything. Suddenly, Indian chemicals could compete globally, and the Bubnas found themselves perfectly positioned. But here's where the story takes its first unexpected turn. While competitors rushed to build bigger factories and increase production capacity, R.V. Bubna noticed something peculiar: the real bottleneck in international agrochemical trade wasn't manufacturing—it was registration.

Consider the European market in the late 1990s. A generic pesticide molecule might cost $50,000 to manufacture in bulk, but obtaining the registration to sell it could cost millions and take years. Most Indian manufacturers viewed this as a barrier. Bubna saw it as an opportunity. Why compete on manufacturing efficiency when you could compete on regulatory expertise?

The early 2000s brought a series of pivotal decisions. The Bubnas began systematically reducing their manufacturing footprint while increasing their investment in understanding global registration processes. They hired regulatory experts, not chemical engineers. They studied dossier requirements, not reactor designs. By 2003, they had made the radical decision to exit manufacturing entirely.

This wasn't just a business pivot—it was heresy in Indian chemical circles. Manufacturing was seen as the source of value creation. Trading was for those who couldn't manufacture. But the Bubnas understood something their peers didn't: in a world where China was becoming the workshop of the world, competing on manufacturing costs was a race to the bottom. Competing on regulatory intelligence, however, was a race few were even running.

In 2004, Sharda Worldwide Exports Private Limited was formally incorporated, marking the official beginning of what would become one of India's most unconventional business success stories. The company started with a simple premise: source generic agrochemicals from the most cost-effective manufacturers (primarily in China), handle the complex registration process in regulated markets (primarily in Europe), and distribute through established channels. No factories, no R&D labs, no massive capital investments—just deep expertise in navigating bureaucracy.

The early years weren't without challenges. Building trust with Chinese suppliers who were used to large volume commitments was difficult. Convincing European distributors that an Indian company without manufacturing facilities could be a reliable partner required patience and persistence. There were months when working capital was stretched thin, when a single delayed payment could have derailed everything.

But the Bubnas had one advantage that proved invaluable: they understood both sides of the equation. R.V. Bubna's technical background meant he could speak the language of manufacturers and regulators alike. Sharda Bubna's business acumen ensured that relationships were nurtured and contracts were structured intelligently. Together, they were building something that looked like a trading company but functioned like a regulatory arbitrage machine.

By 2004, the foundation was set. The company had established relationships with key suppliers in China, understood the registration processes in multiple European countries, and most importantly, had begun accumulating the most valuable currency in the agrochemical world: approved registrations. What started as a husband-wife duo's trading operation was about to transform into something far more sophisticated—and far more valuable.

III. The Asset-Light Revolution (2004–2013)

The conference room in Sharda's modest Mumbai office in 2005 would have seemed unremarkable to any visitor. No impressive manufacturing photographs on the walls, no scale models of chemical plants, no awards for production excellence. Just files—thousands upon thousands of regulatory files. To the untrained eye, it looked like a law firm, not an agrochemical company. But those files represented something revolutionary: a new way of creating value in the chemical industry without owning a single reactor.

The asset-light model that Sharda pioneered wasn't born from strategy consultants or MBA case studies. It emerged from a fundamental insight about how value flows through the agrochemical supply chain. In 2005, producing a ton of generic Glyphosate in China cost roughly $2,000. Selling that same ton in Europe could fetch $6,000. The difference wasn't just markup—it was the value of market access, and market access came through registration.

Here's where the story becomes fascinating. Obtaining a registration for a generic agrochemical in the European Union required preparing a dossier that could run thousands of pages. It meant conducting studies on environmental impact, toxicology, efficacy, and residue levels. It meant understanding the specific requirements of each country's regulatory body. It meant investing millions of euros and waiting years for approval. Most manufacturers saw this as a necessary evil. Sharda saw it as their core business.

The company's core competence lies in developing product dossiers and seeking product registrations in different countries. By 2008, they had developed a systematic approach to registration that was almost industrial in its efficiency. They would identify molecules coming off patent, assess market demand in various countries, calculate the cost and time for registration, and then make strategic bets on which products to pursue.

The numbers tell a remarkable story. By 2014, just before their IPO, the company had over 180 Good Laboratory Practices certified dossiers and owned over 1,040 registrations for formulations and over 155 registrations for generic active ingredients. Each registration represented not just a permit to sell, but a barrier to entry for competitors. In regulated markets, these registrations were as valuable as any manufacturing facility—perhaps more so, because they couldn't be easily replicated.

The China-India arbitrage story added another layer to their model. Chinese manufacturers excelled at producing chemicals cheaply but struggled with the soft skills needed for European registration—language barriers, regulatory complexity, and cultural differences in documentation standards. Indian companies had the English advantage and bureaucratic expertise but lacked China's manufacturing scale. Sharda positioned itself as the bridge, sourcing from China while managing the registration and distribution in Europe.

But the real genius was in the working capital management. Traditional chemical companies tied up capital in inventory, manufacturing facilities, and raw materials. Sharda's capital was tied up in registrations and receivables. Yes, this meant extended payment terms—money locked up for months—but it also meant no depreciation, no maintenance capex, no risk of plant accidents, and no environmental liabilities.

Consider the economics: A traditional agrochemical company might generate 15% EBITDA margins with massive capital employed in fixed assets. Sharda could generate similar margins with virtually no fixed assets. Every rupee of profit was truly free cash flow, not accounting profit that needed to be reinvested in maintaining aging infrastructure.

The 2008 financial crisis actually accelerated their growth. While manufacturers struggled with capacity utilization and credit crunches, Sharda's asset-light model proved remarkably resilient. They could scale up or down simply by adjusting purchase orders. When demand fell, they weren't stuck with idle factories. When it recovered, they could immediately capitalize without waiting for capacity expansion.

By 2010, the company had refined its model to an art form. They would identify a molecule, invest ₹3-5 crore in registration over 2-3 years, and then generate ₹15-20 crore in annual revenue from that single registration for the next decade. The return on investment was extraordinary, but it required patience—something public markets aren't always known for.

The transformation from trader to registration powerhouse was complete by 2013. That year, the company changed its name to Sharda Cropchem Limited, and on September 18, 2013, converted to a public limited company. The stage was set for one of the most interesting IPOs in India's agrochemical sector—a company seeking to raise hundreds of crores despite owning almost no tangible assets.

The registration portfolio they had built was valued at ₹196 crore on their books, but the replacement cost would be multiples of that figure. More importantly, the time required to replicate their portfolio—even with unlimited capital—would be at least a decade. In the fast-moving world of generic agrochemicals, time was the ultimate moat.

IV. The IPO Drama & Market Reception (2014)

September 5, 2014. The investment banking teams at the book-running lead managers were nervous. They were about to take public a company that defied every conventional metric investors used to value chemical companies. No significant fixed assets. Six months of sales locked in receivables. No manufacturing facilities. How do you pitch this to institutional investors who are used to evaluating companies based on capacity utilization and replacement cost?

The IPO prospectus read like a thought experiment in modern capitalism. Sharda Cropchem was seeking to raise ₹351.86 crore through an offer of 22,555,124 equity shares, priced between ₹145 to ₹156 per share. But here's the twist that made analysts scratch their heads: this was entirely an offer for sale by existing shareholders. The company itself wouldn't receive a single rupee from the IPO. The Bubna family was partially cashing out, and they were asking public markets to value their intangible-asset fortress.

The roadshow presentations must have been fascinating. Imagine explaining to a room full of fund managers that your competitive advantage was bureaucracy navigation. That your assets were PDF files and registration certificates. That your business model was essentially regulatory arbitrage at scale. The skepticism was palpable. One fund manager reportedly asked, "So you're asking us to pay ₹156 per share for a company that could theoretically be replicated with a laptop and a credit card?"

The bear case was compelling and seemingly obvious. With negligible tangible assets and ₹400 crore locked in receivables as of March 31, 2014—representing 177 days of sales—the company looked more like a financing operation than an industrial enterprise. What if China suppliers decided to forward integrate? What if European regulations changed? What if those receivables turned bad? The company was essentially asking investors to pay a premium for operational leverage without any asset backing.

But the bulls saw something different. They saw a company that had cracked the code on one of the most regulated industries in the world. They understood that in agrochemicals, as in pharmaceuticals, the ability to sell was often more valuable than the ability to produce. They recognized that Sharda's 1,040+ registrations weren't just permits—they were options on future cash flows that would be extremely expensive and time-consuming for competitors to replicate.

The quality of the order book told the real story. Despite the unconventional business model, or perhaps because of it, the IPO was subscribed 59.97 times. Institutional investors bid for 91.67 times their allocated portion. The retail portion was subscribed 19.22 times. For a company with no factories, this was a stunning vote of confidence.

What the smart money understood was the operating leverage inherent in Sharda's model. Every additional dollar of revenue flowed almost directly to the bottom line. No additional factory workers, no increased depreciation, no rising maintenance costs. Just marginal working capital requirements and distribution expenses. In a world where asset-light models were disrupting everything from hotels to taxis, here was the agrochemical industry's answer to the platform economy.

The listing day—September 23, 2014—provided the first verdict from public markets. The stock opened at ₹165, a 5.8% premium to the IPO price, and touched ₹189 intraday before closing at ₹176. Not the spectacular pop that some IPOs see, but solid enough to validate the model. The market capitalization on listing day was approximately ₹1,587 crore, valuing those intangible registration assets at nearly 8 times their book value.

The immediate post-IPO period revealed an interesting dynamic. Sell-side analysts struggled to initiate coverage. How do you model capacity expansion for a company with no capacity? How do you forecast capex for a business whose primary investments are in regulatory filings? The traditional templates didn't work. Some analysts tried to value Sharda like a distribution company, others like a specialty chemical player, but neither framework quite fit.

The IPO proceeds usage by the selling shareholders was itself a statement. The Bubna family retained 74.82% of the company post-IPO, signaling their confidence in the long-term prospects. They had monetized just enough to provide liquidity while maintaining firm control. This wasn't an exit; it was a validation.

Media coverage of the IPO ranged from skeptical to bewildered. "Asset-light or asset-less?" asked one business daily. Another questioned whether Sharda was really a chemical company or just a "regulatory arbitrage play dressed up as one." But perhaps the most insightful comment came from a veteran fund manager who noted, "In a world where Uber owns no cars and Airbnb owns no hotels, why shouldn't an agrochemical company own no factories?"

The successful IPO marked a crucial transition. Sharda now had the currency of listed equity to pursue acquisitions of registration portfolios. They had the credibility that comes with public market scrutiny. Most importantly, they had proven that Indian capital markets were sophisticated enough to value intangible assets and asset-light business models. The registration empire was ready for its next phase of growth.

V. Global Expansion & Registration Empire (2014–2020)

The post-IPO era began with a map spread across the boardroom table—not of India, but of the world. Colored pins marked existing registrations: a cluster in Western Europe, scattered presence in Latin America, early footholds in other markets. By 2020, that map would be transformed into a constellation of 80+ countries, with a sales force of 400+ and 500+ distributors. But the journey from IPO proceeds to global empire would require navigating regulatory frameworks as diverse as the cultures they emerged from.

Europe remained the cornerstone, and for good reason. The continent accounted for 60% of revenues—a concentration that made some investors nervous but made perfect strategic sense to anyone who understood the regulatory arbitrage game. European Union's harmonized but complex registration system created exactly the kind of barriers that Sharda had learned to traverse. Each successful registration in an EU member state could be leveraged for mutual recognition in others, creating a multiplier effect on their investment.

In 2015, Sharda made a strategic decision that would define the next half-decade: they would double down on registrations rather than diversify into manufacturing. While competitors like UPL were acquiring production facilities globally, Sharda was acquiring something less tangible but equally valuable—registration portfolios from companies exiting the agrochemical business. These acquisitions rarely made headlines, but each one added irreplaceable assets to their portfolio.

The biocides expansion deserves special attention. The company recently entered into the biocide segment and has acquired several registrations from existing registration holders, primarily in Europe. Biocides—chemicals used to control harmful organisms outside agriculture—represented a natural adjacency. The regulatory expertise required was similar, but the market dynamics were different. Less competitive, more specialized, higher margins. It was like a chess player who mastered classical chess suddenly discovering they could apply the same strategic thinking to three-dimensional chess.

The numbers from this period tell a story of methodical execution. By 2018, Sharda had built a portfolio that would take a new entrant at least a decade and hundreds of crores to replicate. But more importantly, they had created a self-reinforcing system. Each new registration made the next one easier to obtain—regulators began to recognize Sharda as a serious player, not just an opportunistic trader.

The regulatory arbitrage playbook they perfected was elegant in its simplicity but fiendishly difficult to execute. Step one: identify molecules where the innovator's patent was expiring or had expired. Step two: assess the competitive landscape—how many generic players were likely to enter? Step three: calculate the total addressable market and likely price erosion. Step four: invest in registration only if the NPV was compelling. Step five: leverage relationships with Chinese manufacturers to secure supply at the lowest possible cost. Step six: use the registration as a barrier to prevent those same suppliers from competing directly.

What made this model particularly powerful was its scalability without capital intensity. Adding a new country didn't require building a new factory—just understanding new regulations. Adding a new product didn't mean installing new production lines—just preparing new dossiers. The main constraint was human capital: regulatory experts who could navigate the Byzantine requirements of different jurisdictions.

By 2019, Sharda had become a case study in building barriers through bureaucracy. They had turned regulatory compliance—usually seen as a cost center—into their primary competitive advantage. Every page of every dossier, every successful registration, every relationship with regulatory bodies added another brick to their moat. Competitors could copy their strategy but couldn't copy their decade of accumulated expertise and relationships.

The geographic expansion strategy was particularly clever. Rather than trying to be everywhere at once, they focused on markets with three characteristics: complex regulatory requirements (creating barriers to entry), large agricultural sectors (ensuring demand), and fragmented distribution (allowing them to add value). This led them to prioritize Europe and Latin America while being selective about Asian markets where local manufacturers had natural advantages.

The company also began experimenting with forward integration—selectively. In certain markets, they established their own sales forces rather than relying entirely on distributors. This wasn't about capturing more margin; it was about understanding end-user needs better and identifying new product opportunities faster. The sales force became their market intelligence network, feeding insights back to the registration team about which molecules to pursue next. The COVID-19 pandemic, rather than disrupting their model, actually validated it. While manufacturers struggled with lockdowns and supply chain disruptions, Sharda's distributed network of suppliers meant they could pivot quickly. If one supplier shut down, they had alternatives. Their lack of fixed costs meant they could weather demand volatility better than asset-heavy competitors. The pandemic became an unexpected proof point for the resilience of asset-light models in chemical distribution.

By the end of 2020, Sharda had transformed from a scrappy startup into a sophisticated registration machine. They owned rights to sell products that would cost competitors hundreds of crores and a decade to replicate. The registration empire wasn't just built—it was fortified with layers of regulatory complexity that made assault nearly impossible.

VI. Business Model Deep Dive: No Factory, No Problem

Walk into any traditional agrochemical company's headquarters, and you'll find scale models of reactors, photos of sprawling manufacturing facilities, awards for production excellence. Walk into Sharda Cropchem's office, and you'll find something radically different: lawyers, scientists, and regulatory experts hunched over computers, preparing dossiers that represent the company's true manufacturing capability—the manufacture of market access.

The Company operates through an asset-light business model, and its core competency lies in developing product dossiers and obtaining product registrations in different countries. This isn't just corporate speak—it's a fundamental reimagining of what creates value in the chemical industry. While competitors measure success in tons produced, Sharda measures it in registrations obtained.

The financial engineering behind this model is elegant. Company remain focus on increasing its product registrations in FY26, with planned Capex of around Rs. 400-450 crores—but this isn't capex in the traditional sense. There are no steel and concrete structures that will depreciate over 20 years. These are investments in intellectual property that, if successful, will generate cash flows for decades with minimal additional investment.

Consider the unit economics of a single registration. Preparing a comprehensive dossier for a generic agrochemical in the European Union might cost ₹5-10 crore over 2-3 years. This includes toxicology studies, environmental impact assessments, efficacy trials, and the endless documentation required by regulators. Once approved, that registration allows Sharda to import and sell that product in that market indefinitely (subject to periodic renewals). A successful product might generate ₹20-30 crore in annual revenue with 15-20% EBITDA margins. The payback period is typically 3-4 years, after which it's pure profit.

But here's where it gets interesting. The Company operates through two segments: Agrochemicals and Non-agrochemicals. Agrochemicals segment is engaged in Insecticides, Herbicides, Fungicides and Biocides. Non-agrochemicals segment is engaged in Conveyor Belts, V Belts and Timing Belts. The non-agrochemical business, contributing about 16% of revenues, isn't just diversification—it's strategic optionality. These industrial products use the same distribution networks and relationships but face different demand cycles, providing natural hedging.

The supplier management strategy deserves special attention. Sharda doesn't sign long-term supply contracts with Chinese manufacturers. This might seem risky—what if suppliers cut them off?—but it's actually a source of competitive advantage. Without contracts, Sharda can switch suppliers instantly if quality issues arise or better prices become available. The suppliers, in turn, need Sharda more than Sharda needs any individual supplier. Sharda provides them access to regulated markets they couldn't enter on their own. It's a symbiotic relationship built on mutual dependence rather than legal contracts.

The working capital puzzle is perhaps the most misunderstood aspect of their model. Yes, Company has high debtors of 165 days. To conventional analysts, this looks like a weakness—money locked up, collection risk, potential bad debts. But in the agrochemical distribution business, extended credit terms are a competitive weapon. Distributors prefer working with suppliers who offer favorable payment terms. Sharda's ability to finance this working capital—essentially providing trade finance to their customers—becomes a barrier to entry for smaller competitors who can't afford to wait six months for payment.

The intangible asset fortress continues to grow. Product Registrations stand at 2,981 with 1,021 applications pending at various stages as on 30th June 2025. Each registration is a call option on future cash flows. Not all will be successful, but the ones that are can generate returns for decades. It's a portfolio approach to value creation—diversified across molecules, geographies, and crop types.

The company remains debt free with cash, bank and liquid investments of Rs. 791 crores. This financial strength isn't just a buffer—it's a strategic weapon. In an industry where many players are leveraged, Sharda can move quickly on acquisition opportunities, invest countercyclically during downturns, and most importantly, never be forced to compromise on working capital terms due to financial pressure.

The model's true genius lies in its scalability without complexity. Adding a new product doesn't require building a new production line, hiring specialized operators, or worrying about capacity utilization. It requires identifying the opportunity, investing in registration, and leveraging existing relationships. The marginal cost of adding the 1000th product is not much different from adding the 100th. This is the kind of operating leverage that software companies enjoy, but in the supposedly capital-intensive chemical industry.

Critics point to the low return on equity—Company has a low return on equity of 9.89% over last 3 years. But this misses the point. In an asset-light model, ROE becomes less relevant than return on invested capital (ROIC) and cash flow generation. The company isn't trying to maximize ROE through leverage; they're building a sustainable, defensible business that can compound value over decades.

VII. The Numbers Game: Financial Performance Analysis

The transformation of Sharda Cropchem's financial profile from 2014 to 2025 reads like a case study in operational leverage. The raw numbers are impressive—revenue exploding from under ₹1,500 crore at IPO to ₹1,853.76Cr in the Q4 2024-2025, representing a 41.5% jump since last year same period. But the real story lies in understanding how an asset-light model translates abstract registrations into concrete cash flows.

The quarterly progression through FY25 tells a story of momentum building. Net profit of Sharda Cropchem rose 423.96% to Rs 142.78 crore in the quarter ended June 2025 as against Rs 27.25 crore during the previous quarter ended June 2024. Sales rose 25.44% to Rs 984.81 crore in the quarter ended June 2025 as against Rs 785.11 crore during the previous quarter ended June 2024. This isn't just recovery from a low base—it's the registration engine firing on all cylinders.

For the full year, the numbers become even more remarkable. For the full year, net profit rose 854.77% to Rs 304.38 crore in the year ended March 2025 as against Rs 31.88 crore during the previous year ended March 2024. Sales rose 36.57% to Rs 4319.85 crore in the year ended March 2025 as against Rs 3163.02 crore during the previous year ended March 2024. An 854% increase in net profit on a 36% increase in sales—this is the kind of operational leverage that makes asset-light models so compelling when they work.

The segment-wise performance reveals strategic focus. Agrochemical Segment contributes 86% whereas Non-Agrochemical Segment contributes 14%. The agrochemical dominance isn't accidental—it's where the registration moat is strongest. But the non-agrochemical segment, growing at 71% year-over-year in FY22, provides diversification without diluting the core competency.

Volume growth tells another story. Overall Volumes have increased by 13.2% Y-o-Y in Q1 FY26. Agrochemical volumes grew by 11.4% & Non-Agrochemical volumes grew by 59%. In a commoditized market, consistent double-digit volume growth suggests that Sharda's registrations are opening doors that remain closed to competitors.

The margin dynamics deserve careful analysis. Sharda Cropchem Ltd's net profit margin jumped 0.27% since last year same period to 10.98% in the Q4 2024-2025. On a quarterly growth basis, Sharda Cropchem Ltd has generated 227.84% jumped in its net profit margins since last 3-months. In an asset-light model, margin expansion flows almost directly to the bottom line. There's no additional depreciation, minimal incremental fixed costs—just pure operational leverage.

The balance sheet strength provides the foundation for growth. Being debt-free isn't just conservative financial management—it's strategic positioning. In a business where working capital needs can spike suddenly (if a large order comes in or payment terms need to be extended to win a contract), having a clean balance sheet means never having to pass up an opportunity due to financial constraints.

The stock price performance reflects market recognition of the model's potential. From the IPO price of ₹156 in 2014 to trading around ₹1,088 in July 2025, the stock has delivered a roughly 7x return in 11 years—a compound annual growth rate of approximately 19%. This outperformance hasn't been smooth—there have been periods of significant volatility—but the long-term trajectory validates the business model.

As of Jul 25, 2025 01:37 PM, the market cap of Sharda Cropchem Ltd stood at Rs. 9,112.22 Cr. For a company with minimal tangible assets, this valuation represents the market's assessment of the value of their registration portfolio and execution capability. It's a bet that bureaucratic complexity will continue to be a source of competitive advantage.

The cash flow characteristics are particularly attractive for long-term investors. Unlike manufacturing companies that must constantly reinvest to maintain competitiveness, Sharda's maintenance capex is minimal. The majority of their capital allocation goes toward growth—new registrations that will generate returns for years to come. This creates a compounding effect: more registrations lead to more cash flow, which funds more registrations, which generates more cash flow.

The working capital intensity remains the one contentious point. Critics correctly point out that 165 days of receivables is high by any standard. But in the context of the industry and business model, it's a necessary evil—perhaps even a competitive advantage. European distributors are used to extended payment terms. By providing this credit, Sharda essentially becomes their financing partner, creating switching costs that go beyond just product quality and price.

The recent quarterly momentum suggests the model is hitting its stride. On a quarterly growth basis, Sharda Cropchem Ltd has generated 553.52% jump in its net profits since last 3-months. While some of this is base effect, it also reflects the cumulative impact of years of registration investments beginning to pay off simultaneously.

VIII. Competitive Landscape & Market Position

In the grand theatre of Indian agrochemicals, Sharda Cropchem plays a role that others either can't or won't. While UPL builds global manufacturing footprints through multi-billion dollar acquisitions, while PI Industries invests in complex chemistry and custom synthesis, while Dhanuka Agritech focuses on domestic distribution, Sharda has carved out a unique position: the registration arbitrageur who wins by not playing the traditional game.

The competitive landscape in Indian agrochemicals traditionally rewarded scale, manufacturing excellence, and R&D capabilities. UPL, with revenues exceeding ₹50,000 crore, represents the conventional path to greatness—acquire, integrate, manufacture, dominate. PI Industries, with its focus on custom synthesis and partnerships with innovators, shows another path—technical excellence and moving up the value chain. Against these giants, Sharda's ₹4,320 crore revenue might seem modest. But comparing revenues misses the point entirely. Sharda isn't trying to be the biggest; they're trying to be the most efficient converter of regulatory complexity into shareholder value.

The real competition for Sharda isn't other Indian companies—it's time and regulatory change. Every day that passes without a competitor replicating their registration portfolio is another day their moat deepens. Every new registration requirement added by regulators is another brick in their wall. They're not competing on who can produce chemicals cheapest (that game is won by China) or who can innovate fastest (that game is won by multinationals with billion-dollar R&D budgets). They're competing on who can navigate bureaucracy most efficiently—a game where few even know they're playing.

The China Plus One strategy that everyone talks about has different implications for different players. For manufacturers, it means opportunity to build capacity as global companies diversify supply chains. For Sharda, it means something else entirely: as Chinese companies lose direct access to global markets due to geopolitical tensions, the value of Sharda's registration bridge increases. They become more essential, not less, as the world fragments.

Consider the market dynamics in Europe, Sharda's primary market. The EU's regulatory framework for pesticides is perhaps the world's most stringent. Getting a new active ingredient approved can cost €100 million and take a decade. Even generic registrations require millions of euros and years of effort. This regulatory burden has caused many smaller players to exit, concentrating the market among those with the resources and expertise to navigate the system. Sharda, paradoxically, benefits from increased regulatory complexity—it raises barriers to entry for new competitors while making their existing registration portfolio more valuable.

The sustainability transition presents both opportunity and threat. As older, more toxic pesticides are banned, new registrations are required for replacement products. Sharda's expertise in registration positions them well to capitalize on this transition. But the push toward biological pesticides and precision agriculture could eventually disrupt the entire generic pesticide model. The company has begun moving into biocides and bio-pesticides, but it remains to be seen whether their registration expertise translates to these new categories.

India's agrochemical export opportunity is massive and growing. With global agrochemical markets worth over $60 billion and India's share still under 5%, there's substantial headroom for growth. But not all Indian companies are positioned equally to capture this opportunity. Manufacturing-focused companies face competition from China on cost and from multinationals on technology. Sharda's positioning as a registration specialist gives them a differentiated angle of attack.

The competitive dynamics with suppliers add another layer of complexity. Chinese manufacturers, Sharda's primary suppliers, are both partners and potential competitors. They need Sharda for market access but would prefer to sell directly if they could navigate the regulatory maze. Sharda's value proposition to suppliers is clear: focus on what you do best (manufacturing), and let us handle what we do best (registration and distribution). It's a delicate balance that requires constant relationship management.

Looking at comparable companies globally, there are few true peers. Some Japanese trading houses like Sumitomo Chemical have similar registration-focused models in certain markets, but they're part of larger conglomerates. Some European distributors like Nufarm have extensive registration portfolios, but they also own manufacturing assets. Sharda's pure-play asset-light model remains relatively unique, which makes both valuation and competitive analysis challenging.

The barriers to replicating Sharda's model are more subtle than they appear. It's not just about having money to invest in registrations—it's about knowing which products to register, in which markets, at what time. It's about having relationships with suppliers who trust you with their products and customers who trust you with their supply. It's about having the working capital to finance the long cash conversion cycles. And most importantly, it's about having the patience to invest millions today for returns that might not materialize for years.

IX. Playbook: Business & Investing Lessons

The Sharda Cropchem story offers a masterclass in contrarian business building that challenges everything they teach in business schools. While MBAs debate optimal capital structure and manufacturing efficiency, the Bubnas built a billion-dollar business by refusing to manufacture anything. The lessons from their journey read like a playbook for building competitive advantages in unexpected places.

Lesson 1: Asset-light doesn't mean risk-light. The absence of manufacturing facilities doesn't eliminate operational risk—it transforms it. Instead of worrying about plant accidents or equipment failures, Sharda faces regulatory risk across multiple jurisdictions, supplier concentration risk, and massive working capital risk. The lesson isn't that asset-light is inherently superior, but that choosing your risks deliberately is better than accepting default risks.

Lesson 2: Bureaucracy as a moat. In most industries, regulatory compliance is a cost center. Sharda turned it into their core competency. They understood that in a world of increasing regulation, the ability to navigate complex approval processes could be more valuable than the ability to manufacture. For investors, this suggests looking for companies that thrive on complexity rather than despite it.

Lesson 3: The power of focus. Sharda could have diversified into manufacturing, could have entered domestic markets, could have backward integrated. They didn't. They stuck to their core competency—registration and distribution—and became world-class at it. In an era of conglomerates and diversification, their single-minded focus stands out. They do one thing exceptionally well rather than many things adequately.

Lesson 4: Working capital as competitive advantage. Conventional wisdom says high receivables are bad. Sharda shows that in certain contexts, the ability to extend credit can be a powerful competitive weapon. By financing their customers' purchases, they create switching costs and deepen relationships. The lesson: sometimes what looks like a weakness in the numbers is actually a strategic choice.

Lesson 5: Family businesses and unconventional bets. The Bubna family's continued 74.82% ownership isn't just about control—it's about having the freedom to pursue strategies that public markets might not initially understand. Quarter-to-quarter earnings matter less when you're playing a decade-long game. Family ownership allowed them to invest in registrations that wouldn't pay off for years, something that might be difficult for a widely-held public company with quarterly earnings pressure.

Lesson 6: Technical founders in commodity businesses. R.V. Bubna's IIT Bombay chemical engineering background wasn't used to design reactors—it was used to understand products deeply enough to navigate regulatory requirements. Technical expertise applied to business model innovation can be more powerful than technical expertise applied to technical problems. The lesson: domain expertise matters, but how you apply it matters more.

Lesson 7: Geographic concentration versus diversification. Conventional wisdom suggests geographic diversification reduces risk. Sharda's 60% revenue concentration in Europe suggests otherwise. By focusing on markets with the highest regulatory barriers, they built deeper moats than they could have by spreading themselves thin across many markets. Sometimes concentration is a feature, not a bug.

Lesson 8: The platform dynamics in traditional industries. Sharda essentially built a platform business in the chemical industry. They connect Chinese manufacturers with global markets, taking a toll on transactions that pass through their regulatory gateway. This platform thinking—creating value by connecting others rather than by producing yourself—can be applied to many traditional industries.

Lesson 9: Capital allocation in asset-light models. Without the need for maintenance capex, every rupee of profit is truly free cash flow. This creates unusual capital allocation dynamics. Sharda can afford to be patient with new registration investments because they're not racing against depreciation. For investors, this suggests that return on incremental invested capital might be a better metric than ROE for such businesses.

Lesson 10: Timing and market evolution. Sharda's model worked because they executed it at the right time—when China was becoming the world's chemical factory, when regulations were tightening globally, when generic agrochemicals were coming off patent in waves. The lesson isn't to copy their model, but to understand how structural changes create new business model opportunities.

For investors evaluating similar asset-light models, Sharda offers both a template and a warning. The template: look for businesses that create value through expertise and relationships rather than physical assets. The warning: ensure that the intangible assets are truly defensible and that the working capital requirements don't become a trap.

The ultimate lesson from Sharda might be this: in a world obsessed with disruption and innovation, sometimes the biggest opportunities lie in mundane activities like filing paperwork and managing compliance. They found treasure not in gold mines or oil fields, but in file cabinets full of regulatory dossiers. It's a reminder that value creation doesn't always look like value creation—sometimes it looks like bureaucracy.

X. Bear vs. Bull Case & Future Outlook

The investment case for Sharda Cropchem splits the room like few others. Bears see a house of cards built on regulatory arbitrage that could collapse with a single policy change. Bulls see a fortress of intangible assets that becomes more valuable every year. Both sides have compelling arguments, and understanding them is crucial for any investor considering this unique business model.

The Bear Case: Fragility Masquerading as a Moat

The bears start with a simple question: What exactly does Sharda own that can't be replicated? Yes, they have 2,981 registrations, but registrations can be obtained by anyone with money and patience. There's no proprietary technology, no manufacturing excellence, no brand value with end consumers. In a world where Chinese suppliers are increasingly sophisticated and European regulations are harmonizing, the arbitrage opportunity that Sharda exploits could evaporate.

The working capital stress is a ticking time bomb in the bears' view. With 165 days of receivables, a few bad debts could trigger a crisis. Unlike manufacturing companies that can slow production if customers don't pay, Sharda must keep buying and selling to maintain relationships. They're essentially a finance company masquerading as a chemical company, and finance companies blow up when credit cycles turn.

The China dependency is another critical vulnerability. Despite all the talk of supplier diversification, the reality is that most generic agrochemicals are produced in China. If China decides to forward integrate, if geopolitical tensions escalate, if supply chains get disrupted again, Sharda has no Plan B. They don't control their supply, which means they don't really control their destiny.

The low return on equity of 9.89% over three years is particularly damning. In a business with minimal capital requirements, why are returns so poor? The bears argue it's because the business isn't as good as it appears. The registration moat isn't generating excess returns because it's not really a moat—it's just a temporary regulatory inefficiency that markets will eventually arbitrage away.

Regulatory risk looms large. Sharda operates across 80+ countries, each with its own regulatory framework. A single change in EU pesticide regulations could wipe out hundreds of crores in registration value overnight. They're not masters of regulation; they're slaves to it. And regulators worldwide are becoming increasingly skeptical of synthetic pesticides, potentially making Sharda's entire portfolio obsolete.

The Bull Case: Compounding Machine Hidden in Plain Sight

The bulls see the same facts but draw opposite conclusions. Those 2,981 registrations? Try replicating them. It would cost hundreds of crores and take a decade, by which time Sharda would have moved further ahead. The registration portfolio isn't just a collection of permits—it's a network effect where each registration makes the next one easier to obtain and more valuable to own.

The working capital requirements, rather than being a weakness, are a barrier to entry. Most chemical traders can't afford to wait 165 days for payment. Sharda can because they've built the balance sheet strength to support it. It's not financial stress—it's financial strategy. They're using their balance sheet as a competitive weapon in a way that capital-constrained competitors cannot match.

The asset-light model provides optionality that manufacturing-heavy competitors lack. When demand shifts, Sharda can pivot immediately. When new molecules become available, they can register them without worrying about existing capacity. When margins compress, they don't have fixed costs to cover. This flexibility is worth more than any physical asset in a rapidly changing world.

The bulls point to the strong pipeline of formulation filings that can provide 15-20% annual revenue growth for years to come. With 1,021 applications pending, the growth is already in the pipeline—it just needs time to materialize. Each approval drops almost directly to the bottom line, creating a step-function increase in profitability that's already visible in recent quarters.

The global food security megatrend provides a multi-decade tailwind. With population growing and arable land shrinking—from half an acre per person today to less than one-third by 2050—agricultural productivity must increase dramatically. Generic agrochemicals remain the most cost-effective way to boost yields, and Sharda is perfectly positioned to distribute these products globally.

The debt-free balance sheet with ₹791 crore in cash provides both safety and opportunity. They can weather any storm and pounce on any opportunity. In a cyclical industry, this financial strength allows them to invest countercyclically, acquiring registrations when others are retrenching.

The Future Outlook: Transformation or Steady State?

Looking forward, Sharda faces strategic choices that will define the next decade. Should they backward integrate into manufacturing? The temptation is obvious—capture more margin, control supply, reduce dependency. But manufacturing would fundamentally change the business model, adding fixed costs and reducing flexibility. The Bubnas have resisted this temptation so far, but pressure from investors might eventually force their hand.

The M&A opportunity in consolidating registrations is compelling. As smaller players exit due to regulatory burden, their registration portfolios become available. Sharda, with its expertise and balance sheet strength, is a natural consolidator. Each acquisition adds immediately to their moat and creates synergies with existing registrations.

Digital transformation of distribution presents another opportunity. While registrations remain analog and bureaucratic, the actual distribution of products could be digitized. Direct-to-farmer platforms, precision agriculture integration, supply chain transparency—all represent opportunities to add value beyond just regulatory arbitrage.

The ESG pressures and bio-pesticide transition can't be ignored. The world is moving away from synthetic pesticides, slowly but inevitably. Sharda must evolve or risk obsolescence. Their early moves into biocides suggest they understand this, but the transition from chemical to biological products isn't just a regulatory challenge—it's a fundamental business model change.

XI. Epilogue & "If We Were CEOs"

If we were sitting in R.V. Bubna's chair today, looking at the empire built on registrations and relationships, what strategic decisions would define the next chapter? The temptation to tamper with a successful formula would be strong, but perhaps the greatest wisdom would be recognizing what not to change.

The backward integration question would dominate board discussions. With ₹791 crore in cash and consistent cash generation, acquiring or building manufacturing facilities is financially feasible. The strategic logic seems compelling—control your supply, capture more margin, reduce dependency. But this would be fighting the last war. The future of agrochemicals isn't about who can manufacture cheapest—that game is already won by China. It's about who can navigate the increasing complexity of global regulations, manage the transition to sustainable agriculture, and build trusted distribution networks. Manufacturing assets would be a distraction from these core challenges.

Instead, we'd double down on what Sharda does best—regulatory intelligence. We'd establish Sharda Regulatory Services, a subsidiary that offers registration services to other companies for a fee. Why let competitors slowly build their own expertise when we could monetize our knowledge? This would transform a cost center into a profit center while reinforcing our position as the regulatory experts in the industry.

The geographic expansion strategy would shift from breadth to depth. Rather than trying to enter every market, we'd identify 10-15 key countries where regulatory barriers are highest and market opportunity is greatest, then dominate them completely. Own every important registration, control every major distribution channel, become indispensable to both suppliers and customers. Market share in chosen markets matters more than presence in many markets.

The digital transformation wouldn't be about e-commerce or farmer apps—everyone's doing that. It would be about using artificial intelligence to optimize the registration process. Imagine an AI system that can predict which molecules to register, in which markets, at what time, based on patent expiries, competitive dynamics, and demand patterns. Turn registration from an art into a science, creating an even wider moat between Sharda and would-be competitors.

On the sustainability front, we wouldn't abandon synthetic pesticides—they'll remain necessary for decades—but we'd build a parallel track in biological products. Not through manufacturing, but through the same asset-light model: identify promising biological products, handle registration, manage distribution. The expertise in navigating regulatory frameworks translates directly, even if the products are different.

The working capital challenge would be addressed not by reducing receivable days—that's a competitive advantage—but by innovative financing. Why not securitize the receivables, creating a new asset class for investors while freeing up capital for growth? Or partner with banks to offer supply chain financing, where we guarantee the receivables and banks provide the funding? Transform a balance sheet constraint into a fee-generating business.

The human capital strategy would recognize that in an asset-light model, people are everything. We'd establish Sharda University—not a real university, but an internal training program that turns smart graduates into regulatory experts. Create the talent pipeline that doesn't exist elsewhere, making it even harder for competitors to replicate our capabilities.

Perhaps most importantly, we'd resist the siren call of diversification. No entry into domestic markets where we have no advantage. No expansion into other chemicals where regulations are different. No acquisition of manufacturing assets just because we can afford them. Stay focused on the one thing we do better than anyone else: turning bureaucratic complexity into shareholder value.

The capital allocation framework would be simple: every rupee should either strengthen our registration moat or be returned to shareholders. No empire building, no ego projects, no strategic investments in adjacent areas. The discipline that got Sharda here—focusing on registrations while others built factories—should continue to guide them forward.

Looking at the next decade, the biggest risk isn't competition or regulation or technology—it's success. When a unconventional strategy works, the temptation is to become conventional. To start thinking like everyone else. To build factories because that's what chemical companies do. To diversify because that's what large companies do. To optimize metrics that analysts care about rather than building value that customers pay for.

The Sharda story isn't finished. At ₹8,945 crore market cap, they're still a mid-cap in Indian terms, tiny in global terms. The opportunity ahead—helping feed 10 billion people by 2050 while navigating increasing regulatory complexity—is orders of magnitude larger than what they've captured so far. The question isn't whether the opportunity exists, but whether they can maintain the discipline and focus that brought them this far.

The ultimate lesson from Sharda Cropchem might be this: in business, as in life, you don't have to do everything—you just have to do something better than everyone else. For Sharda, that something is navigating the byzantine world of agrochemical regulations. It's not glamorous, it's not cutting-edge, but it's valuable. And in the end, value creation doesn't care about glamour—it only cares about solving real problems for real customers in ways that others can't or won't replicate.

The registration empire built by a husband-wife team from Mumbai stands as testimony to a simple truth: competitive advantages can be found in the most unexpected places. Sometimes, the best business to be in isn't the one making products, but the one making it possible for products to be sold. Sometimes, the most valuable factory is no factory at all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube