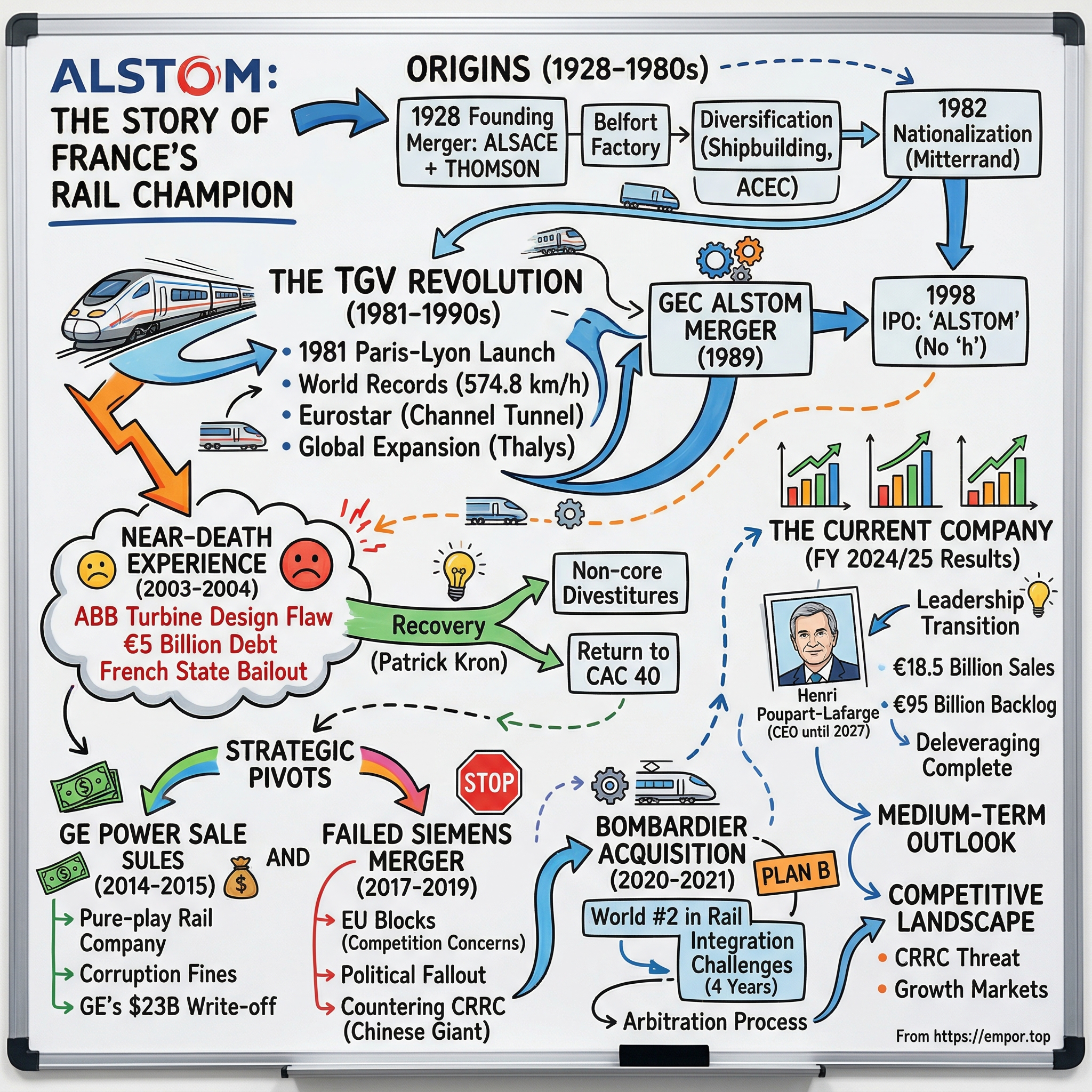

Alstom: The Story of France's Rail Champion

I. Introduction & Episode Roadmap

Picture this: It's February 2019, and the corridors of power in Brussels are humming with tension. European Competition Commissioner Margrethe Vestager is about to block what the French and German governments consider a matter of European industrial sovereignty—the merger of Alstom and Siemens Mobility. The logic seemed bulletproof: combine Europe's two largest rail manufacturers to counter the Chinese juggernaut CRRC, which produces more high-speed trains in a year than Alstom and Siemens combined produce in a decade. But Vestager says no, citing harm to competition in signalling systems and very high-speed trains.

How did a 1920s electrical engineering merger become the builder of the iconic TGV, nearly collapse under the weight of a disastrous turbine acquisition, sell its entire energy business to General Electric (and watch GE write off $23 billion from that deal), have its Siemens merger blocked by Brussels, and then pull off a transformational acquisition of Bombardier—all in the span of a decade?

Today, the combined company has proforma revenue of around €15.7 billion and a €71.1 billion combined backlog. It employs 75,000 people worldwide in 70 countries, has unparalleled R&D capabilities and a complete portfolio of products and solutions. But those headline numbers obscure a far more turbulent journey—one defined by French industrial policy, near-bankruptcy, strategic reinvention, and the existential question of how European companies can compete in a world where state-backed Chinese giants dominate their home markets while eyeing expansion abroad.

For fiscal year 2024/25, Alstom's sales amounted to €18.5 billion, representing a growth of 4.9% on a reported basis and a strong 6.6% on an organic basis. As of 31 March 2025, the backlog stood at €95 billion, providing the Group with strong visibility over future sales. The Bombardier integration, which consumed management attention and capital for four painful years, is finally complete. CEO Henri Poupart-Lafarge announced in May 2025 that he would not seek a fourth term, having shepherded the company through its most transformational decade.

This is the story of a French national champion that has survived nationalization, privatization, near-bankruptcy, massive M&A deals both successful and blocked, corruption scandals, and now faces the defining challenge of an industry in transition: how to build the sustainable mobility systems of the future while competing against competitors that operate by different rules.

II. Origins & Early History (1928–1980s)

The Founding Merger

In 1928, in the industrial heartland of Alsace, two French engineering giants decided their futures lay together. The company and its name were formed by a merger between the electric engineering division of Société Alsacienne de Constructions Mécaniques and Compagnie Française Thomson-Houston in 1928. The name itself tells the story of French industrial geography and ambition: "Alsthom" is a portmanteau of "ALSace" (referencing the Société Alsacienne de Constructions Mécaniques, or SACM) and "THOMson" (from Compagnie Française Thomson-Houston).

The company's first factory was established in Belfort, a city in eastern France that would become synonymous with French heavy industry. This wasn't just another merger of convenience—it was a deliberate consolidation of France's electrical engineering capabilities at a time when electrification was transforming every aspect of industry and society. The new Alsthom would build everything from electrical equipment to locomotives, positioning itself at the intersection of power generation and transportation.

Early Industrial Diversification

Significant acquisitions later included the Constructions Électriques de France, shipbuilder Chantiers de l'Atlantique, and parts of ACEC. The acquisition of Constructions Électriques de France came in 1932, expanding the company's manufacturing footprint. In 1969, Compagnie Générale d'Electricité (CGE) became the majority shareholder of Alsthom, bringing the company under the umbrella of one of France's most powerful industrial conglomerates.

The 1976 merger with Chantiers de l'Atlantique marked a major diversification into shipbuilding. The combined entity was renamed Alsthom Atlantique, and the company now straddled three major industrial sectors: electrical engineering, rail transportation, and marine construction. This was the era of the French industrial conglomerate—vertically integrated, nationally focused, and often tied to state priorities.

Then came 1982, and everything changed. Under President François Mitterrand's socialist government, both CGE and Alsthom were nationalized. For many companies, nationalization would have meant stagnation. For Alsthom, it would prove to be a period of remarkable technological advancement.

The Dawn of Power Generation

Alsthom's power generation business was becoming increasingly sophisticated. In 1977, the company set a world record by constructing the first 1300 MW generator set for the Paluel Nuclear Power Plant—a milestone that cemented Alsthom's position as a global leader in power generation equipment. France was embarking on an ambitious nuclear program in response to the 1973 oil crisis, and Alsthom would be a key supplier of turbines and generators for the country's fleet of nuclear reactors.

By the late 1980s, Alsthom was a sprawling French industrial conglomerate: trains, ships, power plants, and electrical equipment. It was exactly the kind of company that French industrial policy was designed to create—a national champion with capabilities across multiple strategic sectors. But the seeds of both its greatest triumph and its near-destruction were being planted simultaneously: the development of high-speed rail, and the acquisition of turbine technology that would later prove catastrophically flawed.

The question for any investor studying Alsthom's early history is whether conglomerate diversification created value or merely obscured risk. The answer, as the next decades would reveal, was both.

III. The TGV Revolution: Creating France's Crown Jewel (1981–1990s)

The Genesis of High-Speed Rail

In 1966, when top rail speeds were 200 km/h, an ambitious plan was hatched to create a high-speed train. Code-named Project C03, it led to the futuristic train's original design, inspired by the Murène Porsche, which was sketched by Jacques Cooper. Beyond notching up remarkable speeds, the prototype introduced a key innovation: the "articulated" trainset, featuring a non-deformable structure with two carriages sharing a single bogie.

The timing of the TGV's development coincided with one of the most consequential energy crises in modern history. SNCF presented the project to President Georges Pompidou in 1974 who approved it. Originally designed as turbotrains to be powered by gas turbines, TGV prototypes evolved into electric trains with the 1973 oil crisis. This pivot from gas turbines to electric traction would prove prescient—France's nuclear program meant abundant, cheap electricity, while oil prices remained volatile.

In 1976 the SNCF ordered 87 high-speed trains from Alstom. This order represented more than just a commercial contract; it was a bet on a new vision of transportation that would reshape France's geography of economic activity.

1981: A National Triumph

On 27 September 1981, to great fanfare, the first TGV with paying passengers left Paris, after the inauguration by French president François Mitterrand five days earlier. Thus began the long tradition of high speed ground transportation in France.

The TGV (1981) was the world's second commercial and the fastest standard gauge high-speed train service, after Japan's Shinkansen, which connected Tokyo and Osaka from 1 October 1964. It was a commercial success.

The marketing strategy was as innovative as the technology. Contrary to its earlier fast services, SNCF intended TGV service for all types of passengers, with the same initial ticket price as trains on the parallel conventional line. To counteract the popular misconception that the TGV would be a premium service for business travellers, SNCF started a major publicity campaign focusing on the speed, frequency, reservation policy, normal price, and broad accessibility of the service. This commitment to a democratised TGV service was enhanced in the Mitterrand era with the promotional slogan "Progress means nothing unless it is shared by all".

Speed Records & Global Expansion

The TGV didn't just succeed commercially—it dominated. Alstom has gained unrivalled experience since the TGV was introduced in 1981: TGVs have clocked up in excess of 2 billion kilometers traveled (50,000 times around the world), carried over 1.2 billion passengers, seen in-service operating speeds rise from 260 kph to 320 kph.

A TGV test train holds the world speed record for conventional trains. On 3 April 2007 a modified TGV POS train reached 574.8 km/h (357.2 mph) under test conditions on the LGV Est between Paris and Strasbourg. That record still stands today for conventional rail.

European Integration: Eurostar & Beyond

During the early-1990s, GEC Alsthom was the principal manufacturer of the British Rail Class 373, a variant of their TGV family specially designed for traversing the Channel Tunnel between the UK and France. The Eurostar trains represented something unprecedented: a French-built train carrying passengers under the English Channel to London.

The Eurostar service began operation in 1994, connecting continental Europe to London via the Channel Tunnel. The success of Eurostar and Thalys (connecting Paris to Brussels and Amsterdam) demonstrated that high-speed rail could transcend national boundaries, creating an integrated European rail network.

The TGV transformed Alstom from a diversified industrial conglomerate into something more valuable: the company that defined high-speed rail. The technology, the brand recognition, and the operational expertise accumulated over two decades positioned Alstom as one of the few companies globally capable of delivering complete high-speed rail systems. This crown jewel would prove to be the company's salvation when everything else fell apart.

IV. The GEC Merger & IPO Era (1989–2000)

Creating GEC Alsthom

In early 1989, GEC Alsthom was formed from a 50–50 merger of Alsthom and the Power Systems Division of the British General Electric Company. For Alsthom, this move was intended to aid the company in selling its products outside the French market—a recognition that even national champions eventually need to compete globally.

The merger created a genuinely European industrial company at a time when "European champions" was still a concept more discussed than realized. Within months, GEC Alsthom acquired the British rail vehicle manufacturer Metro-Cammell, giving the combined company manufacturing capabilities in the UK market.

Going Public & Becoming "Alstom"

Alstom was listed on the London, New York and Paris Stock Exchanges when it was floated on 22 June 1998. Following the financial reconstruction in 2003, the company remained listed on the Paris Stock Exchange, but was delisted from the London Stock Exchange on 17 November 2003 and the New York Stock Exchange in August 2004.

At listing, 52% of the company's capital was made available to the public by parent companies GEC and Alcatel. The flotation represented the biggest European stock exchange operation of the year, and it came with a subtle but significant change: the company dropped its "h" and became simply Alstom.

The timing seemed propitious. Alstom was riding high on TGV success, had a diversified portfolio across power generation and transportation, and was positioned to benefit from both European rail investment and the global buildout of power infrastructure. The company that went public in 1998 appeared to be a well-positioned industrial champion entering a new era of growth.

But hidden within the balance sheet were the seeds of disaster. In 2000, Alstom acquired ABB's gas turbine business—a deal that would prove to be one of the most destructive acquisitions in European industrial history.

V. Near-Death Experience: The 2003-2004 Crisis

The ABB Turbine Disaster

These heavy debts were largely due to a $4 billion charge over a design flaw in a turbine developed by ABB, acquired by Alstom in 2000, as well as the collapse of customer Renaissance Cruises amid a general downturn in the marine market.

The downward spiral in which Alstom finds itself in 2003 dates back to the turn of the 21st century, when serious design flaws affecting the gas turbines recently acquired from ABB led to considerable commercial and financial difficulties. Problems in contract execution, notably in rail transport, and the bankruptcy of a major customer of the company's shipyards worsen the financial drain. This is compounded by a lack of confidence among customers, suppliers and bankers, and even among employees, as to the company's ability to stay the course — a disastrous situation for a long-term business like Alstom's.

In 2003/2004, the Group's order book shrinks to one year of sales, far below the usual backlog of two to three years. Net losses total over €1 billion in FY 2002/03, followed by a loss of €1.8 billion in 2003/04. Debt reaches €5 billion and the losses wipe out the company's capital.

Alstom's share price had dropped by 90% over two years. A company that had been valued at billions was now worth pennies on the euro.

EU Conditions & French Politics

The French government wanted to save Alstom, but European competition law placed severe constraints on state aid. This was obtained, but required Alstom to sell several of its subsidiaries, including its shipbuilding and electrical transmission assets. In 2004, the French state took a 21% stake in Alstom for €772 million and Alstom received an EU-approved bailout worth in total €2.5 billion.

The conditions were brutal. Alstom had to divest its electrical transmission and distribution activities to Areva, its diesel locomotive manufacturer to Vossloh, and other non-core assets. The company that emerged from the crisis was smaller, more focused, but still wounded.

However, Patrick Kron and the fully renewed management team he put in place stand firm in a "never give up" policy and, disappointing the expectations of many observers, turn things around in under three years. Alstom cuts its workforce from 110,000 in 2003 to 65,000 in 2006. Many assets are divested, such as the industrial turbine business in 2003, the transmission & distribution division in 2004, the electric motors and converters activity (Power Conversion) in 2005 and the shipbuilding sector (Alstom Marine) in 2006.

In 2005/06, the Group announces net gains of €178 million after four successive years of losses. Order backlog once again tops €30 billion the following year. On 26 April 2006, the French government sells its 21% stake in Alstom to Bouygues, with a capital gain of €1 billion. Alstom shares — demoted to penny stock on the Paris stock exchange at the core of the crisis — return to the CAC 40 three months later.

Lessons from Near-Bankruptcy

The 2003-2004 crisis revealed several enduring truths about Alstom and its industry. First, acquisition integration in complex engineering businesses is extraordinarily dangerous. The ABB turbine business looked attractive on paper, but the design flaws embedded in that acquisition nearly destroyed the acquirer.

Second, French industrial policy operates within a tension between national interest and EU competition rules. The state will step in to save strategic companies, but Brussels will extract its pound of flesh in required divestitures.

Third—and this would become apparent only later—the near-bankruptcy planted the seeds for the eventual GE sale. A company that had nearly died once develops a different relationship with risk, and Patrick Kron, who rescued Alstom, would prove willing to make radical strategic moves to avoid ever facing that abyss again.

VI. The GE Power Sale: Becoming a Pure-Play Rail Company (2014-2015)

The Bidding War

On April 30, 2014, GE and Alstom announced that GE had submitted a binding offer to acquire the Thermal, Renewables ("Power") and Grid businesses of Alstom consisting of $13.5 billion enterprise value and $3.4 billion of net cash, totaling $16.9 billion (€12.35 billion). The Alstom board of directors has positively received GE's offer and appointed a committee of independent directors to review the transaction. Bouygues S.A., a 29% non-controlling shareholder of Alstom, supports the transaction.

GE originally reached an agreement to purchase Alstom's power and grid businesses back in April 2014 after a bidding war with Siemens.

The Deal Structure & French Politics

The French government was furious. Arnaud Montebourg, the Minister of Economy, elicited a counter-offer from Siemens. The transaction was heavily criticized in France, as many in the French government considered the assets that were sold as strategic. France had initially blocked General Electric's acquisition of Alstom. But after Arnaud Montebourg's resignation as Minister of the Economy and Finance, he was replaced by Emmanuel Macron, who relented and approved the sale.

On November 2, 2015, GE announced that it had completed the acquisition of Alstom's power and grid businesses. The completion of the transaction follows the regulatory approval of the deal in over 20 countries and regions including the EU, U.S., China, India, Japan and Brazil. It is GE's largest-ever industrial acquisition.

Alstom closes the sale of its Energy activities (Power generation and Grid) to General Electric for an amount of approximately €12.4 billion. Consequently the Group is today entirely refocused on rail transport. Proceeds of the transaction are used to acquire GE signalling activities for an amount of approximately €700 million and to reinvest in 3 Joint Ventures with General Electric.

Alstom recorded sales of €6.2 billion and booked €10 billion of orders in the 2014/15 fiscal year. The pure-play rail company was dramatically smaller than the diversified conglomerate, but arguably more focused and strategically coherent.

Corruption Scandal Backdrop

The timing of the GE sale coincided with a major corruption investigation that cast a shadow over the entire transaction. In late 2014, Alstom was fined $772 million by the DOJ, and admitted guilt under the Foreign Corrupt Practices Act in relation to bribes paid to obtain contracts in various countries.

The widespread scheme uncovered through an extensive FBI investigation involved tens of millions of dollars in bribes that took place over a decade in countries including Saudi Arabia, Indonesia, Egypt, Taiwan and the Bahamas. In total, the DOJ says Alstom paid more than $US 75m to secure $US 4bn in projects around the world, with a profit to the company of approximately $US 300m.

"The record dollar amount of the fine is a clear deterrent to companies who would engage in foreign bribery, but an even better deterrent is that we are sending executives who commit these crimes to prison." Alstom pleaded guilty to a two-count criminal information charging the company with violating the Foreign Corrupt Practices Act (FCPA) by falsifying its books and records and failing to implement adequate internal controls.

Some observers have drawn connections between the corruption investigation and the willingness of Alstom's management to sell to GE. While under Kron's leadership, Alstom was investigated by the United States Department of Justice and ultimately agreed to pay a $772 million fine. Some mid-level Alstom executives were arrested in the United States, and then either enrolled as FBI informants in the company, or jailed.

The Irony: GE's Disaster

What happened next was one of the most spectacular value destructions in modern industrial history. By the time GE finalized its purchase price allocation and acquisition accounting for the deal a year later, the amount of goodwill that was recognized in GE's business combination accounting exercise was $17.3 billion.

The result is the almost $23 billion writedown GE announced in October, the majority of which is tied to the Alstom deal.

The acquisition was completed in November 2015, just one month before hundreds of people gathered in Paris to ratify the landmark climate agreement in December of 2015. "It was kind of like Bayer buying Monsanto just as the bulk of the class action suits were coming through," said Ion Yadigaroglu, Managing Partner at Capricorn Investment Group. GE's purchase of Alstom also coincided with a global downturn in the price of renewables, lessening demand for the gas turbines right after GE had made its costly pick.

In 2018, GE was forced to write down $23 billion in goodwill for its power segment, more than it had paid for the Alstom business just three years earlier. New CEO Larry Culp even overhauled the power segment and brought in new leadership.

Did Patrick Kron time the exit perfectly? From Alstom's perspective, the sale looks like an act of strategic genius—divesting a cyclical, capital-intensive business at the top of the market to a buyer desperate to acquire scale. GE paid a full price for a business that would prove to be worth far less. Alstom kept its crown jewel—the rail business—and used the proceeds to transform itself.

VII. The Failed Siemens Merger (2017-2019)

The "European Champion" Vision

In September 2017, Siemens and Alstom signed a memorandum of understanding to merge their mobility and railway businesses. That was followed by a business combination agreement in March 2018. The merger would have led to a listing in France, with the group headquarters based in Paris. The term 'European champion' was used in the joint press release of Siemens and Alstom, entailing that this was indeed a key consideration for the merger.

The combined rail business would have had $18 billion in revenue and employed 62,300 people in more than 60 countries. The deal structure reflected careful political calibration: Siemens would have majority economic ownership, but the headquarters would be in Paris and the company would be named Siemens Alstom.

The CRRC Threat

The strategic rationale centered on China. The merger was to take place on the backdrop of the rise of CRRC, a Chinese behemoth of the sector – and the result of a merger itself - that is buoyed by the rapid growth of a largely closed Chinese market. As Elie Cohen writes, where Alstom and Siemens fight over the production of 35 high-speed trains a year, the CRRC makes 230.

Siemens and Alstom were willing to merge in order to tackle increasing competition from the Chinese competitor CRRC Corp. and in order to seize an opportunity to better innovate. In 2017, CRRC Railway amassed $20.7 billion of revenue, whereas Siemens Mobility counted for $8.6 billion and Alstom for $8 billion.

With $35 billion in total revenue in 2021, CRRC, the Chinese state-owned railroad rolling stock manufacturer, is the largest player in the $71 billion global railroad rolling stock industry. The scale disparity was staggering.

EU Competition Blocks the Deal

On 6 February 2019 the European Commission blocked that move, as the "merger would have harmed competition in markets for railway signalling systems and very high-speed trains". This decision attracted attention for two reasons.

Competition Commissioner Margrethe Vestager's reasoning was straightforward but controversial. "CRRC has more than 90% of activities in China. No Chinese supplier has ever participated in a signalling tender in Europe, or delivered a single very high-speed train outside China. There's no prospect of Chinese entry into the European market in the foreseeable future."

On the other hand, the market investigation confirmed that China's insurmountable barriers made the entry of any European player into the Chinese markets impossible because of the rules under which only national undertakings were allowed to bid for rolling stock contracts, the requirement that companies be licensed to bid – under no predefined criteria, and public procurement rules requiring local production.

Political Fallout

The European Commission's decision to block the Siemens-Alstom mega-merger in February 2019 provoked the anger of the French and German governments that had backed the deal. They accused the Commission of playing against the interests of the European economy by preventing the emergence of a European champion capable of competing with major foreign rivals in the global economy, particularly state-subsidised Chinese companies.

Le Maire said that China's CRRC was likely to arrive in Europe "in a very short while." The Commission would be serving Chinese interests "because they will prevent Alstom and Siemens, the two champions of signalling and rail, from merging to have the same weight as the great Chinese industrial champion," he argued.

On January 22nd, 2024, strikingly on the fifth anniversary of the merger decision, the contracting authority concerning the Bulgarian procurement procedure for the project 'Bulgaria-Sofia: Railway and tramway locomotives and rolling stock and associated parts' forwarded a notification under Article 29(1) FSR from Chinese CRRC. The (back then) unlikely possibility of CRRC submitting credible bids became a reality, and the parties' arguments came back to life.

The blocked Siemens merger forced Alstom to find another path to scale. Within a year, that path would become clear: Bombardier Transportation.

VIII. The Bombardier Acquisition: Plan B Succeeds (2020-2021)

The Deal Announcement

Alstom announced a Memorandum of Understanding with Bombardier Inc. and Caisse de dépôt et placement du Québec ("CDPQ") in view of the acquisition of Bombardier Transportation. Post-transaction, Alstom will have a backlog of around €75bn and revenues around €15.5bn. The price for the acquisition of 100% of Bombardier Transportation shares will be €5.8bn to €6.2bn.

The contrast with the Siemens merger was instructive. Where Siemens-Alstom would have combined two strong companies, Bombardier was struggling. During the past years, Bombardier Transportation's financial problems became bigger and bigger – the company was bleeding money as the result of several large problematic rail projects – plus it was tied to Bombardier's aerospace division which was facing bankruptcy after it tried to grow into the market for larger commercial passenger planes (C-series).

Closing the Transaction

On 29 January 2021 Alstom announced the completion of the acquisition of Bombardier Transportation. Leveraging on its clear Alstom in Motion strategy and its strong operational fundamentals and financial trajectory, Alstom, integrating Bombardier Transportation, will strengthen its leadership in the growing sustainable mobility market by reaching a critical size in all geographies.

The reference price was established at €5.5 billion, at the bottom of the range of €5.5 billion to €5.9 billion communicated on September 16th, 2020. The proceeds for the acquisition were established at €4.4 billion, which include the impact of the minimum cash adjustment mechanism based on a negative net cash position of Bombardier Transportation as of December 31st, 2020 and other further contractual adjustments for an amount of €1.1 billion.

By incorporating Bombardier Transportation, Alstom says it will now have an unparalleled commercial reach in all geographies, because the two companies had been complementary in this respect. Alstom's established base was France, Italy, Spain, India, South East Asia, Northern Africa and Brazil, while Bombardier Transportation had a focus on the United Kingdom, Germany, the Nordics, China, and North America.

Creating a Global Rail Giant

From now on, Alstom is the world N°2 in the sector behind the Chinese giant CRRC.

With a fleet of 150,000 vehicles, Alstom will have the largest installed base worldwide, a unique springboard to further expand its leadership in Services. Its Signalling product line gains significant scale, becoming No. 2 worldwide in terms of revenue, acquiring technological capabilities and commercial capacities in strategic markets, complementary to Alstom's.

Alstom confirms its objective to generate €400 million cost synergies on annual run rate basis by the fourth to fifth year and to restore Bombardier Transportation's margin to a standard level in the medium term.

Integration Challenges

The Bombardier integration proved far more difficult than anticipated. French rail-equipment maker Alstom SA remains under pressure more than a year after the acquisition of a Canadian rival that rapidly soured. The stock whipsawed after Alstom reported full-year earnings. The company swung to a loss after burning through 992 million euros ($1 billion) for the fiscal year to the end of March and writing down the value of its stake in a key Russian supplier. "We still have a lot of work in terms of execution," Chief Executive Officer Henri Poupart-Lafarge said on a call with analysts, referring to challenging contracts it took over after acquiring the train operations from Bombardier Inc last year.

All the positivity of the basic design could not disguise the serious problems that Alstom had to deal with when it took over at the start of 2021. The supply chain was suffering serious cash flow issues, due mainly to Bombardier's well publicised issues arising from its aircraft manufacturing business. There were shortages of critical materials, yet anyone walking around the factory would see a huge amount of material in stock. Moreover, hundreds of part-completed cars were stored at Derby and other sites, each of which required an individual rectification plan to bring it up to the correct configuration. The first action was to inject finance into the supply chain to stabilise the position.

The former fierce competitors are now in an arbitration process over the accord, with the Alstom CEO blaming mismanagement of contracts by Bombardier for delivery delays and the heavy spending needed to complete them. "Since the beginning we have said that there are clauses in the contract that protect us from a certain number of things," Poupart-Lafarge said. "We decided to go into arbitration to defend our rights."

IX. The Current Company: Leadership, Strategy, and Financial Position

Leadership: Henri Poupart-Lafarge

Henri Poupart-Lafarge (born 10 April 1969) is a French business executive and the current CEO of Alstom, a post which he has occupied since February 2016. After acquiring degrees from École polytechnique in 1988, École des ponts ParisTech, and MIT, Poupart-Lafarge went to work for the World Bank. In 1994, he joined the French Ministry for the Economy and Finance. By 1998, Poupart-Lafarge became Alstom's Head of Investor Relations.

Then, he became the Vice President of Distribution Finance. Before occupying the position of Alstom's CEO, Poupart-Lafarge was successively Chief Financial Officer of Alstom and President of two sectors of the Alstom Group, Alstom Grid for one year, then Alstom Transport for five years.

Warm, straight to the point, Poupart-Lafarge displays a certain skepticism toward disruptive projects of magnetic levitation trains like Hyperloop. "A key lesson I got is that resilience is extremely important. No matter the ups and downs, you should not change direction each time the wind blows. Of course, you should manage people and projects in a pragmatic manner. But never compromise with your values. Stick to them."

Alstom announced on 16 May 2025 that Henri Poupart-Lafarge is not seeking a fourth term as CEO of Alstom at the end of his current term, which expires at the general meeting called to approve the financial statements for the financial year ending 31 March 2027. At the recommendation of the company's Nominations and Remuneration Committee, the Board of Directors have decided to launch the process of identifying his successor.

Financial Recovery: FY 2024/25 Results

Alstom recorded 19.8 billion EUR in orders and 18.5 billion EUR in sales over the year, resulting in a book-to-bill ratio of 1.1. The backlog reached 95 billion EUR, offering continued visibility on future revenue.

FY 2024/25 results: Book-to-bill ratio at 1.1 and organic sales up 6.6%. Adjusted EBIT of €1,177 million, up 18%, with a margin of 6.4%. Net profit at €498 million.

During the fiscal year 2024/25, Alstom's non-operating expenses decreased from €(510) million in the fiscal year 2023/2024 to €(198) million in the fiscal year 2024/2025. They notably relate to the last year of integration costs of Bombardier Transportation - for an amount of €(97) million.

"With a strengthened balance sheet and the successful completion of Bombardier Transportation integration, Alstom is embarking on a new phase. We will leverage our market-leading position to accelerate Services and enhance the digitalisation of our solutions," said Henri Poupart-Lafarge, Chief Executive Officer of Alstom.

Deleveraging Complete

On 23 May 2024, Alstom successfully placed an issuance of €750 million in principal amount of subordinated perpetual securities. The bonds bear a fixed rate coupon of 5.868% per annum for the first 5.25 years. In June 2024, Alstom completed a share capital increase with shareholder's preferential subscription rights in an amount of €1 billion.

The deleveraging plan was painful but successful. Alstom sold its North American signalling business to Knorr-Bremse, raised capital, and issued subordinated securities. At 31 March 2025, the Group recorded a net debt position of €(434) million, compared to the €(2,994) million net debt balance that was reported on 31 March 2024. The €2,558 million reduction is driven by the execution in Q1 of deleveraging plan for €2,315 million.

Medium-Term Outlook

Alstom confirmed its financial outlook for FY 2025/26, targeting organic sales growth of 3%–5%, an adjusted EBIT margin of around 7%, and free cash flow of 200–400 million EUR. Over the medium term, Alstom reiterated its target of at least €1.5 billion cumulative free cash flow over the three fiscal years from 2024/25 to 2026/27.

On the back of supportive Rail market dynamics, the Group expects its backlog to exceed €100 billion in the coming two years. The Group's ambition is to deliver around 5% average sales growth over the medium term. Rolling stock is expected to grow above market rate, Services and Signalling at mid- to high-single digit rates and Systems at high-single digit rates. On profitability, Alstom's ambition is to consistently deliver an adjusted EBIT margin between 8% and 10% over the medium term.

The Board of Directors, in its meeting of 13 May 2025, proposed that no dividend will be paid with regards to the fiscal year 2024/25.

X. Competitive Landscape and Industry Dynamics

The CRRC Question

The rolling stock market is consolidated, with five leading players such as CRRC Corporation Limited (China), Siemens AG (Germany), Alstom SA (France), Stadler Rail AG (Switzerland), and Wabtec Corporation (US) collectively holding 71–81% of the total market share.

CRRC Corporation Limited holds a substantial market position in China and other Asian regions, making it one of the biggest rolling stock manufacturers worldwide. The reason behind CRRC's market domination is its wide range of products, which includes metro cars and high-speed trains, as well as its strong presence in both local and international markets.

CRRC alone covers two thirds of all current deliveries, but most other manufacturers were not able to maintain their market share. This concentration took place in a dynamically growing market which today stands at EUR 9.9 billion.

Between 2015 and 2020, CRRC won seven passenger rail projects in North America worth over $4.3 billion. It undercut the next lowest bidder on these projects by an average of 21%.

However, geopolitical factors have constrained CRRC's expansion. Despite the goals of the BRI, there is not clear evidence of a clear upward trend in CRRC's penetration of rolling stock markets outside mainland China. The reason for CRRC's failure, thus far, to significantly expand its share of these foreign markets is not certain, but likely reflects the long lead time of rail projects, as well as the success of investment restrictions by other countries against Chinese rail imports.

Market Dynamics

The rolling stock market is projected to grow from USD 30.94 billion in 2025 to USD 41.79 billion by 2032, at a CAGR of 4.4%.

The global railroad market size was estimated at USD 314.84 billion in 2024 and is projected to reach USD 436.35 billion by 2030, growing at a CAGR of 5.5% from 2025 to 2030. The market is likely to be driven by continued investments in railway line projects and the expansion of railroad networks around the world.

China accounts for about 45% of the global train market. This concentration creates a structural challenge: the largest market is effectively closed to non-Chinese competitors, while Chinese competitors are increasingly seeking to expand abroad.

XI. Bull Case, Bear Case, and Key Metrics

The Bull Case

Porter's Five Forces Analysis:

-

Barriers to Entry (High): Rail manufacturing requires massive capital investment, decades of engineering expertise, established safety certifications, and reference projects. The certification process alone can take years. New entrants face an almost impossible task.

-

Supplier Power (Moderate): Alstom has a diversified supply chain across 70 countries. The Bombardier integration brought additional manufacturing capacity and supplier relationships. Supply chain is a competitive advantage, not a weakness.

-

Buyer Power (Moderate): Customers are typically governments and state-owned enterprises with procurement cycles measured in decades. Relationships matter enormously. Once a rail operator has standardized on Alstom equipment, switching costs are substantial.

-

Substitutes (Low): For urban and intercity passenger transport, rail has no substitute that matches its capacity, speed, and environmental profile. The energy transition is a tailwind, not a threat.

-

Competitive Rivalry (Moderate): Outside China, the market is an oligopoly of Alstom, Siemens, Stadler, Hitachi, and CAF. Competition is fierce for individual contracts but pricing discipline generally prevails.

Hamilton Helmer's 7 Powers:

-

Scale Economies: Alstom now operates at sufficient scale to amortize R&D across a global order book. The €95 billion backlog provides visibility that smaller competitors cannot match.

-

Network Effects (Limited): Rail systems are becoming more integrated with digital signalling and traffic management, creating some lock-in effects.

-

Counter-Positioning: Against CRRC, Alstom can position on quality, safety certification, service capabilities, and political acceptability in Western markets.

-

Switching Costs: Once a rail operator has invested in Alstom systems, switching to a competitor requires massive reinvestment in training, spare parts, and integration.

-

Branding: The TGV is one of the most recognized brands in transportation globally. This heritage creates trust with procurement officials.

-

Cornered Resource: Alstom's engineering talent, particularly in high-speed rail and signalling, is a cornered resource developed over decades.

-

Process Power: The operational improvements post-Bombardier have rebuilt execution capability. If margins continue to improve, this represents genuine process power.

The Bear Case

-

Execution Risk: The Bombardier integration took four painful years. Future acquisitions may carry similar integration challenges. Complex engineering businesses are notoriously difficult to merge.

-

CRRC Threat: The Commission's assessment that CRRC would not enter Europe within five years was proven wrong in January 2024 when CRRC bid on Bulgarian projects. If CRRC gains a foothold in Europe through aggressive pricing, Alstom's margins could compress.

-

Government Dependence: Rail is fundamentally a government-driven market. Budget pressures, political changes, or austerity measures could slow order intake.

-

Capital Intensity: The business requires continuous capital investment in R&D and manufacturing. Free cash flow generation has been volatile and remains a question mark.

-

Currency Exposure: With operations in 70 countries, Alstom faces significant currency risk that can mask or amplify underlying performance.

-

Leadership Transition: Poupart-Lafarge's departure creates uncertainty. His successor will inherit a transformed company but also the responsibility for delivering on ambitious margin targets.

Key Metrics to Track

Book-to-Bill Ratio: This single metric tells the story of whether Alstom is building or depleting its backlog. A ratio consistently above 1.0 indicates growing future visibility. The 1.1 ratio in FY 2024/25 is healthy.

Adjusted EBIT Margin: The company targets 8-10% over the medium term, up from 6.4% in FY 2024/25. Progress toward this target will determine whether the Bombardier synergies materialize and whether Alstom can achieve premium margins consistent with its market position.

Free Cash Flow: After years of cash burn during the Bombardier integration and deleveraging, Alstom must demonstrate consistent positive free cash flow generation. The target of €1.5 billion cumulative free cash flow over three years (FY 2024/25 to 2026/27) is the key commitment.

XII. What It Means for Investors

Alstom today is a dramatically different company than the conglomerate that nearly collapsed in 2003 or the diversified industrial that sold its energy business to GE in 2015. The transformation is complete: this is now a pure-play global rail transportation company, the #2 player worldwide outside China, with a €95 billion backlog providing multi-year visibility.

The strategic logic of sustainable mobility is compelling. Rail is the lowest-carbon mode of motorized transportation. Government stimulus programs globally prioritize green infrastructure. Urbanization drives demand for metros and light rail. Freight rail offers efficiency advantages over trucking as logistics networks evolve.

Yet the investment case ultimately rests on execution. The €400 million in annual synergies from Bombardier took four painful years to achieve. The margin trajectory from 6.4% toward 8-10% requires continued operational improvement. Free cash flow generation remains the key proof point.

The CRRC threat is real but perhaps overstated in the near term. Regulatory barriers, certification requirements, and political resistance to Chinese infrastructure in Western markets provide some protection. However, a company that produces 230 high-speed trains annually while Alstom and Siemens fight over 35 represents a structural competitive challenge that scale alone cannot address.

Leadership transition creates both risk and opportunity. Poupart-Lafarge successfully navigated the Bombardier integration, the deleveraging, and the transformation to a pure-play rail company. His successor inherits a stronger balance sheet and completed integration but must deliver on the medium-term margin and cash flow targets.

The century of history matters. From the 1928 merger that created Alsthom, through the TGV revolution, the near-bankruptcy, the GE sale, the blocked Siemens merger, and the Bombardier acquisition—Alstom has repeatedly demonstrated the resilience that Poupart-Lafarge cites as essential. The question for the next decade is whether that resilience can translate into consistent value creation in a world where the largest rail market remains closed to Western competition and the largest rail company enjoys structural advantages that no amount of European consolidation can match.

The rails are laid. The destination remains uncertain.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube