Sanofi: From French Oil Subsidiary to Global Pharma Giant

I. Introduction & Episode Preview

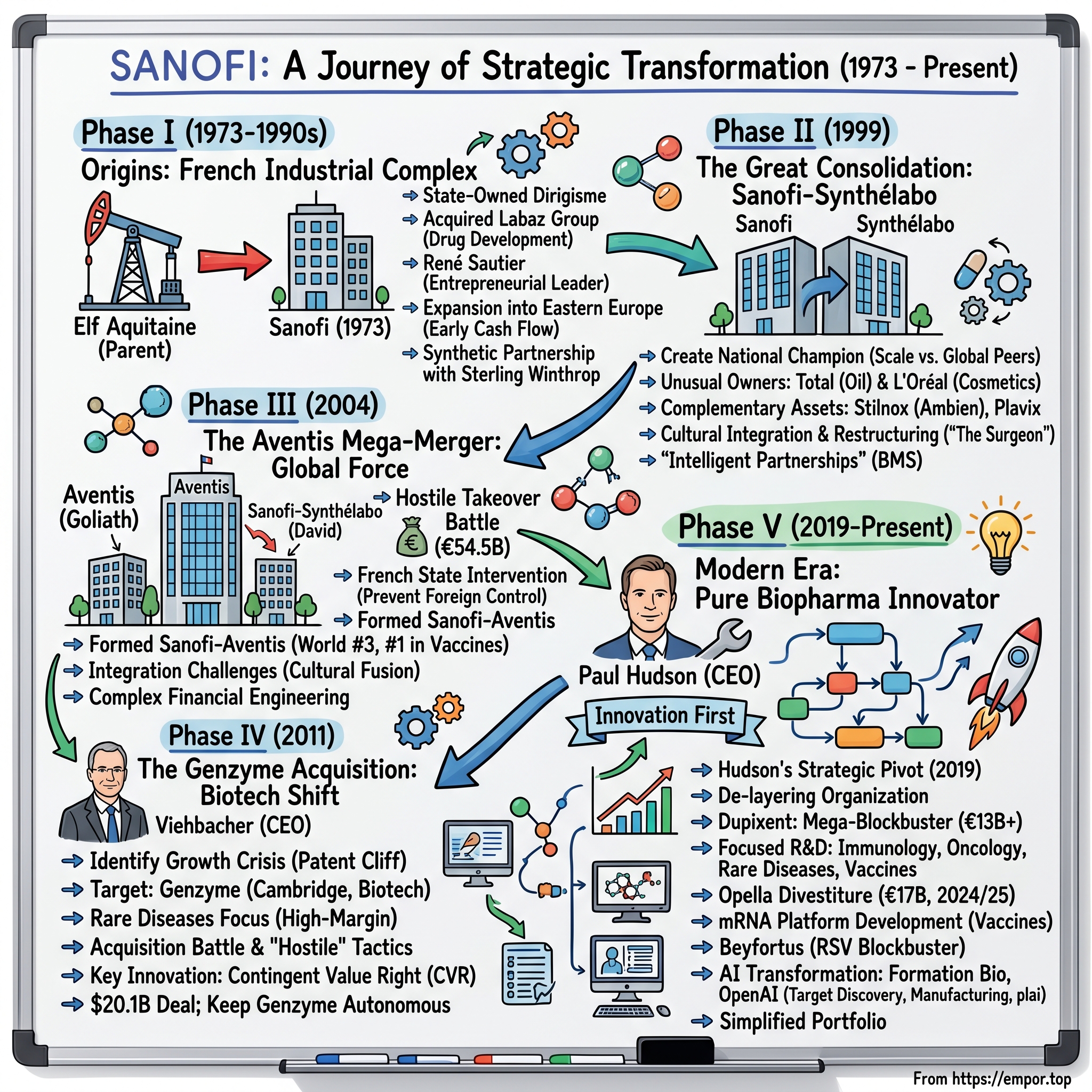

Picture this: It's 1973, and inside the headquarters of Elf Aquitaine—France's state-controlled oil giant—executives are debating an unusual proposition. Why should an oil company, riding high on petroleum profits, venture into pharmaceuticals? The answer would reshape not just French industry, but global healthcare over the next five decades.

Today, Sanofi stands as a €47 billion pharmaceutical colossus, employing over 83,000 people across 100 countries. It's the world's largest producer of vaccines by volume, the leader in rare disease treatments, and home to Dupixent—a €13 billion blockbuster that's revolutionizing immunology. Yet this empire began as a ten-person subsidiary of an oil company, a curious footnote in France's industrial ambitions.

The paradox at Sanofi's heart remains: How does a European pharmaceutical company compete against American innovation giants while navigating the complex web of state interests, national pride, and shareholder returns? It's a tension that has defined every major decision in the company's history—from hostile takeovers orchestrated with government blessing to multi-billion dollar biotech acquisitions that transformed its scientific capabilities.

This is the story of how financial engineering, political maneuvering, and scientific ambition converged to create one of pharma's most unlikely success stories. It's about leaders who played three-dimensional chess with governments, shareholders, and competitors simultaneously. And it's about a company that has reinvented itself completely at least three times—from oil subsidiary to French national champion, from European consolidator to global biotech powerhouse, and now, as it sheds its consumer healthcare division, into a pure-play biopharma innovator. The journey from those ten employees in 1973 to today's AI-powered drug discovery platform is anything but linear.

II. Origins: The French Industrial Complex (1973–1990s)

The conference room at Elf Aquitaine's Paris headquarters buzzed with skepticism in early 1973. René Sautier, a young executive with entrepreneurial ambitions, was presenting his vision for pharmaceutical expansion. "Gentlemen," he argued, "oil won't last forever. But people will always need medicine." The board members, flush with petroleum profits from the ongoing oil crisis, weren't immediately convinced. Yet by year's end, they had authorized the acquisition of Labaz group, birthing Sanofi with just ten employees and a mandate to build France's pharmaceutical future.

This wasn't merely corporate diversification—it was industrial policy wrapped in commercial ambition. Post-World War II France operated under a dirigiste economic model where the state orchestrated industrial champions. While Americans built their pharmaceutical giants through pure capitalism, France approached drug development as a matter of national sovereignty. The creation of Sanofi represented President Georges Pompidou's belief that France needed indigenous pharmaceutical capabilities, not just for commercial reasons but for strategic independence.

Sautier, who would lead Sanofi for its first two decades, embodied a uniquely French archetype: the entrepreneur within the state apparatus. Trained at École Polytechnique—France's MIT—he understood both innovation and bureaucracy. His early moves revealed shrewd strategic thinking. Rather than compete head-on with established Western pharma, Sanofi expanded eastward. By 1975, they were selling in Poland and Hungary, markets American companies couldn't touch due to Cold War restrictions. This Eastern European beachhead would generate crucial early cash flows and establish distribution networks that competitors wouldn't replicate for decades.

Parallel to Sanofi's development, another piece of the puzzle was taking shape. Synthélabo, founded in 1970 through the merger of two century-old French pharmaceutical companies, was pursuing a complementary strategy focused on central nervous system drugs and cardiovascular treatments. While Sanofi built from scratch with oil money, Synthélabo consolidated existing French pharmaceutical assets. Both companies shared a common mission: proving that French science could compete globally.

The 1980s brought Sanofi's first major international partnership. The collaboration with Sterling Winthrop, an American pharmaceutical company, gave Sanofi access to U.S. distribution networks and regulatory expertise. But more importantly, it provided legitimacy. When American partners took French pharma seriously, so did global markets. By 1989, Sanofi had grown from those original ten employees to become France's second-largest pharmaceutical company with over 10,000 staff worldwide.

Yet success bred complexity. Being owned by an oil company created strange dynamics. Elf Aquitaine's shareholders questioned pharmaceutical investments during oil downturns. Government ministers pushed for unprofitable domestic projects. Competitors whispered that Sanofi was more politique than pharmaceutique. These tensions would eventually force a reckoning, but first, the company needed to survive the wave of global consolidation that would define pharma's next decade. The stage was set for transformation—Sanofi had proven French pharma could exist, but could it truly compete?

III. The Great Consolidation: Sanofi-Synthélabo Merger (1999)

Jean-François Dehecq stood before a packed auditorium at Synthélabo's headquarters in May 1999, his normally reserved demeanor giving way to visible excitement. "Today," he announced, "we stop being French pharmaceutical companies. We become a global force." The merger creating Sanofi-Synthélabo wasn't just corporate consolidation—it was France's answer to the mega-mergers reshaping global pharma. Pfizer had just swallowed Warner-Lambert for $90 billion. GlaxoWellcome and SmithKline Beecham were in talks. France needed scale, and fast.

The ownership structure that emerged was perhaps the most unusual in pharmaceutical history. L'Oréal, the cosmetics giant, and Total (formerly Elf Aquitaine), the oil major, would each own approximately 20% of the combined entity. A beauty company and an oil company as the largest shareholders of a pharmaceutical firm—only in France could such an arrangement make sense. Yet it reflected a sophisticated logic: patient capital from non-competing industries that understood long development cycles and wouldn't demand quarterly earnings management.

The numbers told a compelling story. Combined revenues of €5.3 billion made Sanofi-Synthélabo Europe's seventh-largest pharmaceutical company. But size alone wasn't the prize. The real value lay in complementary assets: Synthélabo brought blockbusters like Stilnox (Ambien in the U.S.) and Plavix (through its partnership with Bristol-Myers Squibb), while Sanofi contributed its vaccine capabilities and emerging market presence. Together, they held critical mass in cardiovascular, central nervous system, and internal medicine—therapeutic areas large enough to support global infrastructure.

Integration, however, proved culturally explosive. Sanofi's entrepreneurial cowboys, accustomed to René Sautier's "build fast, fix later" philosophy, collided with Synthélabo's methodical scientists who prized precision over speed. In one legendary incident, teams from both companies presented competing development strategies for the same molecule to the board, each unaware the other was working on it. Dehecq, who became CEO of the merged entity, instituted "Thursday Unity Sessions"—mandatory joint meetings where duplicate projects were identified and eliminated. Within eighteen months, he had cut 3,000 positions and closed seven research sites, earning him the nickname "The Surgeon" among French unions.

The post-merger period revealed the strategic sophistication hidden beneath the cultural chaos. Rather than pursue the American model of massive R&D spending, Sanofi-Synthélabo pioneered what Dehecq called "intelligent partnerships." The Plavix arrangement with Bristol-Myers Squibb became the template: co-development and co-marketing agreements that shared both risks and rewards. By 2003, Plavix was generating €2 billion annually, validating the partnership model that would become central to European pharma strategy.

Geographic expansion accelerated dramatically. While American competitors focused on developed markets, Sanofi-Synthélabo doubled down on emerging economies. They established local manufacturing in Brazil, expanded clinical trials in India, and built governmental relationships in China years before competitors recognized these markets' potential. By 2003, emerging markets contributed 15% of revenues—double the industry average. This wasn't just opportunistic expansion; it was preparation for the next phase of transformation that Dehecq and his inner circle were secretly planning.

IV. The Aventis Mega-Merger: Creating a Global Player (2004)

The fax machine in Dehecq's office whirred to life at 6:47 AM on January 26, 2004. The message from Aventis CEO Igor Landau was brief: "Your offer is unwelcome and undervalues our company." Sanofi-Synthélabo had just launched a hostile takeover bid worth €47.8 billion for Aventis, a company twice its size. David was attempting to swallow Goliath, and the entire pharmaceutical world was watching. What followed would become a masterclass in financial engineering, political maneuvering, and strategic patience.

Aventis itself was a creature of consolidation—born from the 1999 merger of France's Rhône-Poulenc and Germany's Hoechst Marion Roussel. The Hoechst lineage traced back to IG Farben, the infamous German chemical conglomerate, adding historical weight to what was already a complex corporate story. With €19 billion in revenues, Aventis dwarfed Sanofi-Synthélabo's €8 billion. Yet Aventis was vulnerable: integration problems from its own merger persisted, its stock had underperformed, and its pipeline looked thin. Dehecq saw opportunity where others saw impossibility.

The initial €47.8 billion offer—€60.43 per share—was immediately rejected as "inadequate." But Dehecq had anticipated this. His real concern wasn't Aventis management but the Swiss pharmaceutical giant Novartis, which began circling with its own potential bid. The prospect of France's largest pharmaceutical company falling into Swiss hands triggered alarm bells in the Élysée Palace. President Jacques Chirac personally called Novartis chairman Daniel Vasella, making clear that while France welcomed foreign investment, certain assets were considered strategic. The message was unmistakable: Aventis would remain French.

This government intervention, while never officially acknowledged, fundamentally altered the negotiation dynamics. Novartis withdrew from formal bidding, though they extracted a consolation prize: Sanofi would divest certain Aventis assets post-merger, which Novartis could acquire. The path was clear for Sanofi-Synthélabo, but the price would be steep. After four months of brinksmanship, the final deal valued Aventis at €54.5 billion—€65.49 per share, a 15.7% premium to the initial offer. It was the largest European hostile takeover ever completed.

The merged entity, simply called Sanofi-Aventis, instantly became the world's third-largest pharmaceutical company by sales and number one in vaccines. But integration would prove brutal. Two proud cultures—French entrepreneurial and German systematic—had to merge while absorbing the already-fragmented Aventis organization. Chris Viehbacher, brought in as CEO in 2008, later described finding "seven different email systems, four enterprise resource planning platforms, and executives who literally hadn't spoken to counterparts in other divisions for years."

The financial engineering behind the deal deserves special attention. Sanofi-Synthélabo financed the acquisition through a combination of €12 billion in new equity, €9 billion in assumed debt, and crucially, €7 billion in asset disposals identified before the deal closed. They pre-negotiated sales of non-core businesses to companies like Procter & Gamble and Novartis, essentially using the target's own assets to fund its acquisition. The effective cost of capital, after accounting for tax shields and synergies, was under 4%—remarkable for such a massive transaction. This would become the template for future European pharmaceutical consolidation: strategic focus combined with financial creativity.

V. The Genzyme Acquisition: Biotech Ambitions (2011)

Henri Termeer slammed his fist on the mahogany conference table in Genzyme's Cambridge headquarters. "Absolutely not," he told his board in August 2010. "We're worth far more than $69 per share." Sanofi's initial $18.5 billion bid for Genzyme had just arrived, and Termeer, who'd built Genzyme from 11 employees to a rare disease powerhouse over 27 years, wasn't about to let his life's work go cheap. What followed was a six-month corporate siege that would redefine how pharmaceutical companies approach biotech acquisitions.

Genzyme represented everything Sanofi wasn't but desperately wanted to become. While Sanofi excelled at large-molecule manufacturing and global distribution, Genzyme had cracked the code on rare diseases—conditions affecting fewer than 200,000 people but commanding premium prices often exceeding $200,000 per patient annually. Genzyme's Cerezyme for Gaucher disease generated $800 million yearly from just 5,000 patients worldwide. This wasn't traditional pharmaceutical economics; this was biotech's promise of doing well by doing good.

Chris Viehbacher, now three years into his role as Sanofi CEO, understood that organic growth couldn't deliver the transformation Sanofi needed. The patent cliff looming in 2012-2013 would erase billions in revenue. He needed biotechnology capabilities, rare disease expertise, and most importantly, a foothold in Cambridge—biotech's global epicenter. Genzyme checked every box, but Termeer's resistance turned what Viehbacher hoped would be a friendly merger into a hostile takeover.

The tactical maneuvering was extraordinary. Sanofi began buying Genzyme shares on the open market, eventually accumulating a 5% stake. They launched a tender offer directly to shareholders. They even initiated a proxy fight to replace Genzyme's board. Termeer responded with poison pills, litigation threats, and a PR campaign highlighting Sanofi's "inadequate" valuation. The standoff paralyzed both companies' operations for months. Investment bankers later calculated that the distraction cost both firms a combined $500 million in lost productivity.

The breakthrough came through financial innovation. In February 2011, Sanofi proposed a novel structure: $74 per share in cash plus a Contingent Value Right (CVR) worth up to $14 per share based on future sales of Lemtrada, Genzyme's experimental multiple sclerosis drug. This wasn't just clever deal-making—it was philosophical bridge-building. The CVR acknowledged uncertainty about Lemtrada's prospects while giving Genzyme shareholders upside if the drug succeeded. It allowed both sides to claim victory: Termeer could say shareholders might receive $88 per share, while Viehbacher's CFO could model the deal at $74.

The final agreement, valued at $20.1 billion, closed in April 2011. But the real story was what happened next. Rather than integrate Genzyme into Sanofi's French bureaucracy, Viehbacher made a radical decision: Genzyme would remain in Cambridge as Sanofi's global center for rare diseases, maintaining its entrepreneurial culture and decision-making autonomy. He even kept Genzyme's iconic double-helix logo on the building. This wasn't just symbolic—it was strategic recognition that biotech innovation couldn't be managed like traditional pharma.

The CVR mechanism proved transformative for the industry. By 2014, when the rights expired, Genzyme shareholders had received an additional $4.75 per share—less than the maximum but enough to validate the structure. More importantly, CVRs became standard in biotech acquisitions, used in dozens of subsequent deals. Sanofi had not only acquired critical capabilities but had also innovated the very mechanics of how big pharma buys biotech. The Genzyme acquisition marked Sanofi's transformation from a traditional pharmaceutical company to a modern biopharmaceutical enterprise—a shift that would define its next decade.

VI. Modern Era: Innovation & Transformation (2011–Present)

Paul Hudson strode into Sanofi's Paris headquarters in September 2019 with an outsider's perspective and an insider's track record. The British executive, poached from Novartis where he'd run their pharmaceutical division, inherited a company at an inflection point. Revenue growth had stalled, the stock price had languished for five years, and investors openly questioned whether European pharma could compete in an increasingly American-dominated industry. Hudson's response would be nothing short of revolutionary: tear up the playbook and rebuild Sanofi as an innovation-first biopharma company.

The numbers told a stark story. Despite €36 billion in 2019 revenues, Sanofi's R&D productivity lagged American peers dramatically. They were spending €6 billion annually on research but hadn't launched a true blockbuster since Dupixent in 2017. Hudson's first executive decision shocked the organization: he eliminated 25 middle management layers between himself and bench scientists. "I want to hear from the people actually discovering medicines," he told his leadership team, "not from PowerPoint professionals interpreting their work. "Dupixent's trajectory vindicated Hudson's strategy spectacularly. Sales targets exceeded: Dupixent >€13 billion and Beyfortus blockbuster status (€1.7 billion) in its first full year, transforming what had been a promising drug into one of the industry's mega-blockbusters. The monoclonal antibody, developed with Regeneron, works by inhibiting interleukin-4 and interleukin-13, key drivers of type 2 inflammation. What made Dupixent revolutionary wasn't just its efficacy but its breadth—approved for atopic dermatitis, asthma, chronic rhinosinusitis, and most recently, chronic obstructive pulmonary disease (COPD). Due to Dupixent's "pipeline in a product" approach, the treatment could reach more than $22 billion in sales by the end of the decade

The COVID-19 pandemic fundamentally reshaped vaccine development priorities worldwide. Sanofi Pasteur and Translate Bio collaborated to develop a novel mRNA vaccine for COVID-19, leveraging an existing 2018 agreement between the two companies to develop mRNA vaccines for infectious diseases. This marked Sanofi's entry into the mRNA race, though later than competitors Pfizer-BioNTech and Moderna who captured early market dominance.

Sanofi set to invest €400 million ($476 million) a year in a dedicated vaccines mRNA Center of Excellence, intended to establish Sanofi as a frontrunner in the race to develop mRNA vaccines against a wide range of infectious diseases. In 2021, Sanofi launched its mRNA Center of Excellence (CoE) to accelerate the development and delivery of the next generation of mRNA vaccines. The company's approach differed from competitors—rather than rushing a COVID vaccine to market, they focused on building a sustainable mRNA platform for future vaccines.

The strategic pivot became clearer in 2024. Sanofi announced a co-exclusive licensing agreement with Novavax to co-commercialize a protein-based non-mRNA adjuvanted COVID-19 vaccine, with Novavax receiving cash and an equity investment totaling approximately $1.2 billion. This partnership represented a sophisticated hedging strategy—offering both mRNA and protein-based vaccine options to address different patient preferences and tolerability profiles.

The US Food and Drug Administration granted Fast Track designation to two Sanofi combination vaccine candidates to prevent influenza and COVID-19 infections in individuals 50 years of age and older, with both candidates combining two already licensed and authorized vaccines with proven efficacy through randomized controlled studies, and with favorable tolerability. This combination approach exemplified Hudson's strategy of leveraging existing assets to create innovative solutions rather than competing head-on in saturated markets.

The 2024 Opella divestiture marked Sanofi's most decisive strategic transformation. Sanofi and CD&R entered exclusive negotiations for the potential sale and purchase of a 50% controlling stake in Opella, with valuation based on an enterprise value of c.€16 billion, corresponding to c.14 times 2024 estimated EBITDA. The transaction, closing in April 2025, represented more than financial engineering—it was philosophical realignment. Sanofi announced the closing of the sale to CD&R of a 50.0% controlling stake of its consumer healthcare business Opella, with Sanofi retaining a significant shareholding with a 48.2% stake and receiving total net cash proceeds of around €10 billion.

The proceeds enabled aggressive capital returns. The company is divesting its Opella consumer health unit for €17 billion, with proceeds funding a €5 billion share buyback in 2025. This wasn't mere financial engineering but strategic focus—every euro returned to shareholders was a euro not invested in consumer products, reinforcing Sanofi's commitment to innovation-driven biopharma.

Hudson's most ambitious initiative might be his AI transformation. Sanofi, Formation Bio and OpenAI are collaborating to build AI-powered software to accelerate drug development, bringing together data, software and tuned models to develop custom, purpose-built solutions across the drug development lifecycle, with Sanofi leveraging this partnership to provide access to proprietary data to develop AI models. This wasn't following Silicon Valley trends—it was recognition that traditional pharmaceutical development cycles couldn't compete in a world where biotechs could design molecules in silico.

The practical applications already showed results. Sanofi's Target Discovery engines combine advanced AI, machine learning and data integration with experimental techniques for target validation, delivering seven novel drug targets in just one year. Scientists are developing mRNA-based vaccines and therapies faster than ever with CodonBERT, a large language model pre-trained on 10 million mRNA sequences, which has cut down mRNA design time by 50%. These weren't incremental improvements but step-function changes in productivity.

Manufacturing transformation paralleled R&D innovation. With SimplY, an AI-powered yield analytics platform, M&S teams learn from past and current batch performance to enable consistently higher yield, supporting improved cost efficiency and contributing to environmental objectives. The adoption of plai within Manufacturing & Supply teams demonstrated the ability to predict 80% of stock disruptions through probabilistic planning, correlating 65% of risks with a root cause.

By 2025, Sanofi had transformed from a traditional pharmaceutical conglomerate into what Hudson called "the first biopharma company powered by AI at scale." The numbers validated the strategy: Dupixent exceeded €13 billion in sales, Beyfortus achieved blockbuster status in its first year, and the pipeline contained multiple late-stage assets with multi-billion dollar potential. The Opella divestiture freed management to focus exclusively on innovation while providing capital for both R&D investment and shareholder returns.

VII. The Science & Pipeline

The transformation of Sanofi's R&D organization under Hudson represents one of pharma's most dramatic scientific pivots. Where predecessors spread resources across dozens of therapeutic areas hoping for serendipitous discoveries, Hudson concentrated firepower on seven core domains where Sanofi possessed genuine competitive advantage: immunology, oncology, rare diseases, vaccines, neurology, cardiovascular, and rare blood disorders. This wasn't retreat—it was strategic focus that would yield extraordinary returns.

Dupixent exemplifies this focused innovation philosophy. The IL-4/IL-13 inhibitor started as a narrow atopic dermatitis treatment but evolved into what analysts call a "pipeline in a product." Each new indication—asthma, chronic rhinosinusitis with nasal polyps, eosinophilic esophagitis, prurigo nodularis, and most recently COPD—expanded the addressable patient population by millions. The COPD approval alone added a $10 billion market opportunity. By 2024, Dupixent generated over €13 billion annually with potential to exceed €22 billion by decade's end.

The rare disease portfolio, anchored by the Genzyme acquisition, demonstrates how specialized expertise creates defensible moats. Pompe disease, affecting fewer than 10,000 patients globally, generates over $1 billion annually through Nexviazyme. The economics seem paradoxical—tiny patient populations supporting blockbuster revenues—but reflect the value of life-saving treatments for previously untreatable conditions. Sanofi's rare disease unit operates with biotech agility while leveraging big pharma's global infrastructure, a combination competitors struggle to replicate.

Sanofi is on track to start at least six mRNA clinical trials by 2025, with goals to develop vaccines for infectious diseases with unmet medical needs, such as chlamydia in adolescents and young adults, and respiratory diseases in older adults, while also using mRNA to develop solutions for cancer, immune-mediated diseases, and rare diseases. The mRNA platform represents Sanofi's boldest scientific bet, requiring mastery of lipid nanoparticle formulation, sequence optimization, and thermostability engineering simultaneously.

The oncology pipeline showcases sophisticated molecular engineering. Sanofi's trispecific antibodies—molecules targeting three distinct antigens simultaneously—represent technical achievements few companies can match. Sanofi is the first pharma company to have trispecific—or triple-targeting—antibodies for both HIV and cancer in the clinic, combining three different antibodies into a single molecule that can act on three targets in one or more of a disease's pathways simultaneously. These aren't incremental improvements but fundamental reimaginings of how antibodies can work.

Rilzabrutinib for immune thrombocytopenia exemplifies precision medicine evolution. This oral BTK inhibitor selectively targets B-cells while sparing other immune components, potentially offering efficacy without broad immunosuppression. Phase 3 data expected in 2025 could establish a new treatment paradigm for autoimmune conditions affecting platelet production. The program demonstrates Sanofi's ability to compete in crowded therapeutic classes through superior molecular design.

Tolebrutinib for multiple sclerosis represents another differentiated approach. Unlike existing MS therapies that primarily target peripheral immune cells, tolebrutinib crosses the blood-brain barrier to modulate inflammation within the central nervous system itself. Phase 3 trials in progressive MS—historically the graveyard of drug development—showed unprecedented slowing of disability progression. If approved, it would be the first BTK inhibitor for MS, opening a multi-billion dollar market.

The vaccine pipeline extends beyond traditional prophylaxis into therapeutic applications. RSV prevention through Beyfortus already achieved blockbuster status, but the real innovation lies in next-generation platforms. Sanofi uses a range of vaccine technologies from recombinant proteins to purified viral and bacterial components, approaches such as conjugated polysaccharides for diseases where the target is a sugar rather than a protein, and machine learning to identify the most broadly protective antigens.

R&D productivity metrics tell the transformation story. From 2019 to 2024, Sanofi increased the number of Phase 3 assets from 12 to 21 while reducing overall R&D spending as a percentage of sales. This wasn't cost-cutting but intelligent resource allocation—killing failing programs faster while doubling down on winners. The €7.4 billion R&D budget in 2024 concentrated on programs with clear differentiation rather than me-too drugs in crowded markets.

Powered by Insilico's PandaOmics AI platform, joint teams with Sanofi focused on highly novel "undruggable" targets, addressing druggability challenges through lead optimization based on novel scaffolds generated by Chemistry42, yielding an AI-facilitated lead with first-in-class potential against an undruggable transcription factor target for treating oncology diseases. These AI collaborations aren't publicity stunts but fundamental changes in how Sanofi discovers drugs.

The Regeneron partnership remains the crown jewel of external innovation. Beyond Dupixent, the collaboration yielded Kevzara for rheumatoid arthritis, Praluent for cholesterol management, and multiple oncology programs. The 20-year partnership generated over $20 billion in combined sales while sharing both risks and rewards. It's a model for how big pharma can access biotech innovation without acquisition premiums.

VIII. Playbook: Business & Strategic Lessons

The Sanofi story offers a masterclass in navigating the inherent tensions of European pharmaceutical leadership. Unlike American peers who operate in relatively unfettered capital markets, or Swiss companies shielded by canton-level governance, French pharma must balance shareholder returns with national industrial policy, union demands with restructuring needs, and global ambitions with local obligations. Sanofi's journey from state-owned oil subsidiary to global biopharma leader reveals strategies applicable far beyond pharmaceuticals.

The first lesson involves managing government as both enabler and constraint. The 2004 Aventis acquisition succeeded precisely because Sanofi understood how to weaponize national interest. When Novartis threatened to acquire Aventis, Sanofi didn't just outbid—they mobilized the French state apparatus to make foreign acquisition politically impossible. Yet this same government influence later constrained restructuring options, forcing Sanofi to maintain French employment levels even when efficiency demanded otherwise. The key insight: government partnership works best when corporate and national interests align, but companies must build financial strength to act independently when they diverge.

M&A as transformation tool represents Sanofi's most distinctive capability. Each major acquisition—Aventis, Genzyme, Bioverativ—brought not just products but capabilities Sanofi couldn't build organically. The Genzyme deal particularly stands out for its structural innovation. The CVR mechanism, now standard in biotech acquisitions, solved the fundamental valuation disconnect between buyers focused on probability-weighted outcomes and sellers believing in best-case scenarios. By making part of the payment contingent on future success, both parties could agree on a deal that might otherwise have stalled.

The complexity management challenge at Sanofi—100+ countries, 83,000+ employees, thousands of products—required organizational innovations rarely discussed in business schools. Sanofi pioneered the "franchise" model where therapeutic areas operate as quasi-independent businesses with their own P&Ls, development budgets, and commercial strategies. This structure allows entrepreneurial speed within big company infrastructure. Dupixent's success stemmed partly from immunology operating like a biotech within Sanofi, making rapid decisions without corporate committee approval.

Manufacturing excellence often gets overlooked in pharma narratives focused on R&D breakthroughs, but Sanofi's industrial capabilities represent genuine competitive advantage. Producing vaccines requires different skills than small molecules, which differ from biologics, which differ from cell therapies. Sanofi masters them all. The company's ability to manufacture COVID vaccines for three different companies simultaneously—while maintaining its own vaccine production—demonstrated industrial flexibility competitors couldn't match. This manufacturing prowess becomes increasingly valuable as drug complexity grows.

The financing architecture of Sanofi's transformations deserves study. The Aventis acquisition's pre-negotiated asset sales, Genzyme's CVR structure, and Opella's retained minority stake all show sophisticated financial engineering. These aren't just clever deal structures—they're risk management tools that allow bold strategic moves while protecting downside. The Opella transaction particularly stands out: selling control while retaining upside through minority ownership provides capital for innovation while maintaining exposure to consumer healthcare growth.

Cultural transformation proves harder than financial engineering. Sanofi navigated the integration of French entrepreneurial culture (from original Sanofi), German systematic approach (from Hoechst), American biotech innovation (from Genzyme), and Swiss precision (from acquired assets). Each culture brought strengths—French creativity, German process excellence, American risk-taking—but also created friction. Hudson's solution involved radical decentralization, letting each unit maintain its cultural identity while aligning around common performance metrics.

The partnership philosophy differentiates European from American pharma models. While U.S. companies often acquire to own innovation, Sanofi perfected the art of strategic collaboration. The Regeneron partnership generated more value than most acquisitions without integration costs. The BioNTech manufacturing agreement provided COVID vaccine exposure without development risk. The Novartis swap of animal health for consumer products optimized both companies' portfolios. These partnerships require surrendering some control but enable access to innovation across multiple fronts simultaneously.

Capital allocation discipline evolved dramatically from the conglomerate era to focused biopharma. Early Sanofi pursued diversification—from pharmaceuticals to beauty products to animal health. Modern Sanofi ruthlessly prioritizes: divesting non-core assets, concentrating R&D spending on differentiated programs, and returning excess capital to shareholders. The €5 billion 2025 buyback program signals confidence but also discipline—management won't empire-build when returns to shareholders exceed marginal investment opportunities.

The geographic balancing act remains perpetually challenging. Sanofi generates most profits from the U.S. market's premium pricing but maintains European cost structures and French headquarters. Emerging markets offer volume growth but require local manufacturing and pricing flexibility. China presents enormous opportunity shadowed by intellectual property risks. Sanofi's solution involves tailored strategies: innovation for developed markets, volume for emerging economies, and partnerships for complex markets like China where local knowledge matters more than global scale.

IX. Bull vs. Bear Case & Competitive Analysis

The investment case for Sanofi in 2025 hinges on whether Paul Hudson's transformation has fundamentally altered the company's competitive position or merely delayed inevitable decline in a rapidly evolving industry. Bulls see a focused biopharma leader with blockbuster growth drivers and underappreciated pipeline depth. Bears worry about patent cliffs, European structural disadvantages, and competition from more agile biotechs. The truth, as always, lies in the nuanced middle.

The bull case starts with Dupixent's seemingly unstoppable expansion. With €13+ billion in 2024 sales and new indications launching regularly, it could become pharma's best-selling drug by 2027. The COPD indication alone doubles the addressable population. Unlike traditional blockbusters facing immediate biosimilar competition upon patent expiry, Dupixent's complex manufacturing and broad indication portfolio create barriers beyond patent protection. Even assuming biosimilar entry in the early 2030s, the franchise could generate over €150 billion in cumulative sales—funding Sanofi's next generation of innovation.

Beyfortus validates Sanofi's vaccine innovation capabilities, achieving €1.7 billion in first-year sales for RSV prevention. This isn't just revenue—it's proof that Sanofi can still launch transformative products in competitive markets. The combination vaccine strategy with Novavax could revolutionize respiratory disease prevention, combining flu and COVID protection in single shots. With vaccine hesitancy partially driven by injection frequency, combination products could expand the total market while commanding premium pricing.

The rare disease portfolio provides ballast against patent cliffs elsewhere. These ultra-orphan drugs face minimal competition due to small patient populations and complex manufacturing. A competitor would need to invest hundreds of millions to capture markets worth tens of millions annually—economically irrational unless pursuing broader strategic goals. Sanofi's 40+ rare disease products create steady, high-margin revenue streams funding riskier innovation investments.

Geographic diversification offers resilience against single-market shocks. While U.S. pricing reforms threaten industry margins, Sanofi's 40% emerging market exposure provides growth even if developed markets stagnate. The company's early investments in China, India, and Brazil—building local manufacturing and government relationships—created advantages competitors can't quickly replicate. As these economies develop, demand for innovative medicines will explode, benefiting established players like Sanofi.

The bear case begins with looming patent expiries. Despite Dupixent's growth, other key products face generic competition. Aubagio for multiple sclerosis, generating €1.5 billion annually, loses exclusivity in 2025. Toujeo, the long-acting insulin worth €2 billion yearly, faces biosimilar competition. While Sanofi's pipeline contains promising assets, none match Dupixent's commercial potential. The company essentially runs to stand still—new launches barely offsetting losses from patent expiries.

European structural disadvantages persist despite Hudson's reforms. French labor laws make restructuring expensive and slow. Government pressure prevents closing facilities even when economically necessary. While American competitors can pivot quickly—cutting programs, laying off staff, acquiring companies—Sanofi must navigate complex stakeholder negotiations for any significant change. This institutional inertia creates permanent competitive disadvantage in fast-moving therapeutic areas.

The innovation gap versus American biotechs seems insurmountable. Despite AI investments and external partnerships, Sanofi's R&D productivity lags Vertex in genetic diseases, Moderna in mRNA, or Regeneron in antibody engineering. These focused biotechs attract top scientific talent with equity upside Sanofi can't match. While Sanofi talks about becoming "biotech-like," its 83,000-person organization inherently moves slower than 1,000-person biotechs. Size brings scale advantages but innovation disadvantages—a tradeoff increasingly unfavorable in precision medicine era.

Competition intensifies across every therapeutic area. In immunology, AbbVie's Rinvoq and Skyrizi challenge Dupixent. In vaccines, Moderna and BioNTech use mRNA platforms to develop products faster than Sanofi's traditional approaches. In rare diseases, Vertex and Biomarin focus exclusively on orphan conditions with deeper expertise than Sanofi's broader approach. In oncology, Sanofi lacks the critical mass to compete against Roche, Bristol-Myers Squibb, or Merck's immuno-oncology franchises.

Competitive positioning reveals both strengths and vulnerabilities. Against Pfizer, Sanofi shows superior commercial execution and pipeline productivity despite similar size. Versus Roche, Sanofi lacks oncology depth but exceeds in vaccines and consumer health. Compared to Novartis, Sanofi demonstrates clearer strategic focus post-Opella divestiture. Against Johnson & Johnson, Sanofi's pure-play biopharma model offers cleaner investment thesis. Yet versus focused biotechs, Sanofi appears slow and bureaucratic regardless of Hudson's reforms.

Financial metrics present mixed signals. Sanofi reported a 10.3% sales increase in Q4 2024, with Beyfortus surpassing forecasts by doubling sales to €841 million and Dupixent growing by 16% to €3.46 billion. Yet profitability faces pressure from R&D investments and currency headwinds. The forward P/E ratio around 12x suggests market skepticism about growth sustainability—significantly below biotech valuations despite superior current profitability.

X. Epilogue & Looking Forward

As Sanofi enters its sixth decade, the company stands at an inflection point that will determine whether it becomes a case study in successful transformation or gradual decline. The post-Opella era beginning in 2025 strips away the safety net of consumer healthcare's steady cash flows, forcing Sanofi to succeed purely as an innovation-driven biopharma company. This isn't just strategic evolution—it's existential metamorphosis that will test every assumption about European pharma's ability to compete globally.

The AI integration represents more than technological adoption; it's a fundamental reimagining of pharmaceutical development. AI enables R&D teams to scale and accelerate research processes from weeks to just hours and improve potential target identification in therapeutic areas like immunology, oncology or neurology by 20 to 30%, while also accelerating mRNA research by increasing the speed of the lipid nanoparticle prediction process from months to days. If successful, Sanofi could leapfrog competitors still relying on traditional development approaches. If not, the billions invested in digital transformation become an expensive distraction from core challenges.

The French model's future remains uncertain. Can a company headquartered in Paris, subject to European regulations, and influenced by government stakeholders truly compete against American biotechs operating with complete strategic freedom? Sanofi's answer involves selective adaptation—maintaining European stability and stakeholder capitalism benefits while adopting American innovation practices and return expectations. It's a delicate balance that no company has perfectly achieved.

For founders and executives, Sanofi offers crucial lessons about building within constraints. Every company faces limitations—regulatory, financial, cultural, or competitive. Sanofi's journey demonstrates that constraints can catalyze creativity. The CVR structure emerged because Sanofi couldn't match competitors' cash offers. The partnership model developed because Sanofi couldn't acquire every innovation. The AI transformation accelerated because traditional R&D couldn't compete. Necessity mothered invention repeatedly.

Alternative ownership structures might have yielded different outcomes. Had Sanofi remained state-owned, it likely would have remained a subscale French player, protected domestically but irrelevant globally. Private equity ownership might have driven faster restructuring but sacrificed long-term research for short-term returns. The public company model, despite its quarterly earnings pressures, provided the right balance of accountability and patience for pharmaceutical timescales.

The next decade will reveal whether Hudson's transformation secured Sanofi's future or merely delayed reckoning with structural challenges. Success requires threading multiple needles simultaneously: maintaining Dupixent growth while launching new blockbusters, improving R&D productivity while controlling costs, expanding in emerging markets while protecting developed market margins, and embracing AI while maintaining human scientific judgment. It's a complex optimization problem with no clear solution.

Yet Sanofi's history suggests resilience. The company survived being an oil subsidiary, thrived through hostile takeovers, integrated incompatible cultures, and emerged stronger from each crisis. This adaptability—more than any single drug or technology—might be Sanofi's greatest asset. In an industry where today's blockbuster becomes tomorrow's generic, corporate evolution capabilities matter more than current portfolio strength.

The ultimate judgment on Sanofi's transformation won't come from quarterly earnings or stock price movements but from patient outcomes. If the AI platforms accelerate drug discovery, if the rare disease treatments save lives, if the vaccines prevent pandemics, then financial returns follow naturally. Sanofi's bet is that by focusing relentlessly on innovation and patient benefit, commercial success becomes inevitable rather than engineered.

Looking forward, three scenarios seem plausible. In the optimistic case, AI transformation succeeds, the pipeline delivers multiple blockbusters, and Sanofi emerges as the leading global biopharma company by 2030. In the pessimistic scenario, patent cliffs overwhelm new product launches, AI investments fail to yield returns, and Sanofi becomes an acquisition target for American giants. The most likely outcome lies between—Sanofi remains a solid if unspectacular pharma major, generating steady returns without revolutionary breakthroughs.

What would different leadership have meant? Had Sanofi recruited an American CEO instead of Hudson, the company might have pursued more aggressive restructuring but lost European stakeholder support. A French CEO might have maintained better government relations but moved too slowly on transformation. Hudson's British background—European enough to understand stakeholder capitalism, Anglo enough to drive performance—proved ideal for this particular moment. Leadership fit matters as much as leadership quality.

The Sanofi story ultimately transcends pharmaceutical industry dynamics to illuminate broader questions about industrial policy, corporate governance, and innovation systems. Can Europe maintain strategic industries while competing globally? How should companies balance stakeholder interests in multipolar worlds? What role should governments play in corporate strategy? Sanofi doesn't answer these questions definitively but provides rich empirical evidence for the debates.

As this analysis concludes, Sanofi stands transformed but not yet triumphant. The company has successfully shed non-core assets, focused on innovation, and embraced digital transformation. Yet the hardest work lies ahead—proving that a European pharmaceutical company can lead in precision medicine, that AI can revolutionize drug discovery, and that patient focus drives sustainable returns. The next chapter of Sanofi's story remains unwritten, its ending uncertain. But after fifty years of reinvention, betting against Sanofi's adaptability seems premature. The company that began as an oil subsidiary may yet become the model for 21st-century biopharma—combining European stability with American innovation, AI efficiency with human insight, and commercial success with patient benefit. Time, as always in pharmaceuticals, will tell.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube