Sanghvi Movers: Asia's Crane Rental Giant That Lifted India's Infrastructure

I. Introduction & Episode Roadmap

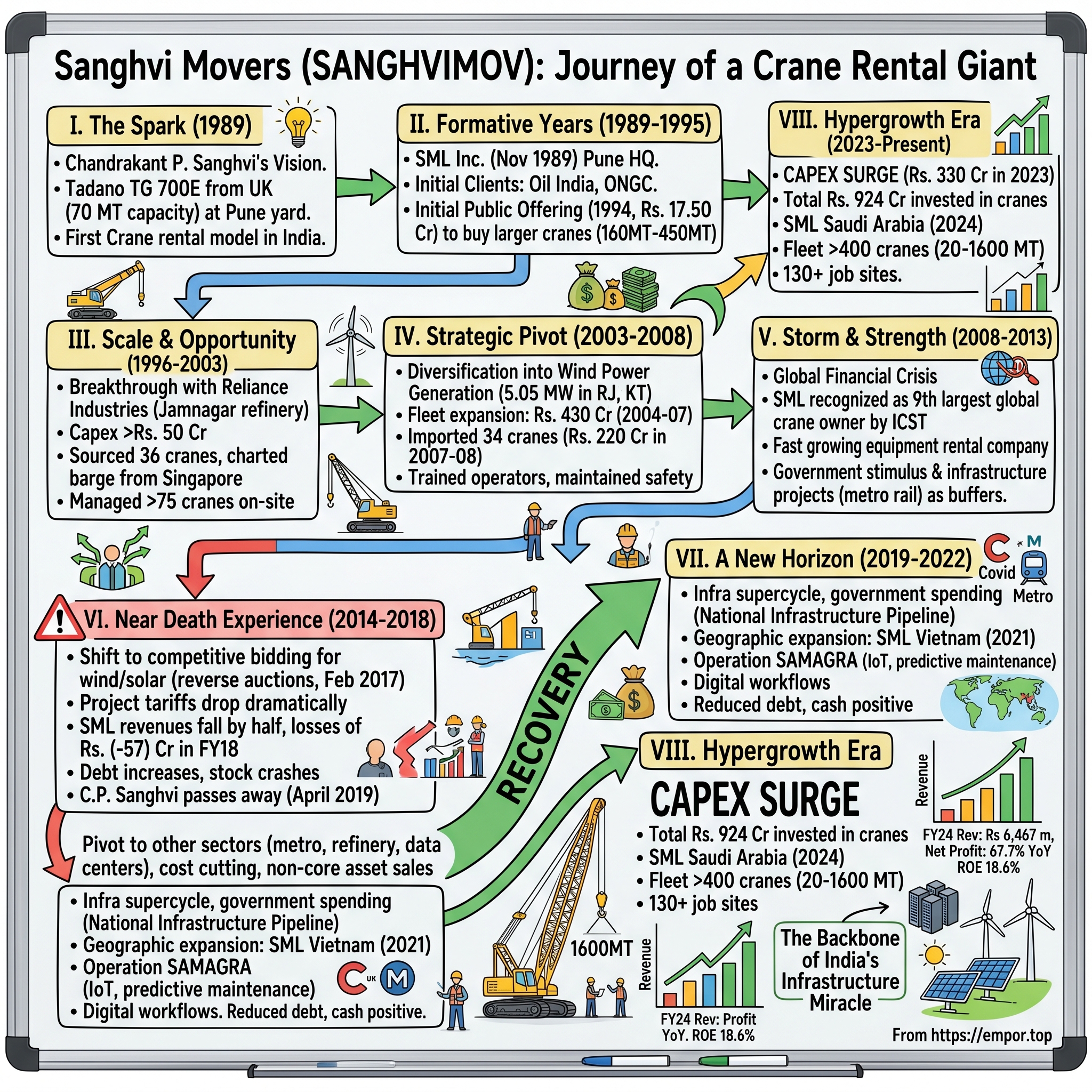

Picture this: A single crane imported from the UK in 1989, a Tadano TG 700E with 70 MT capacity, sitting in a dusty yard in Pune. Fast forward thirty-five years—that lone machine has multiplied into a fleet of over 400 cranes, some capable of lifting 1,600 metric tons, deployed across 130+ job sites from the windswept plains of Rajasthan to the coastal refineries of Gujarat. This is the story of how a small-time entrepreneur's vision built Asia's largest crane rental company and the fourth-largest in the world as ranked by International Cranes (June 2024).

The protagonist? Chandrakant P. Sanghvi—a man who saw opportunity where others saw only construction sites and industrial chaos. His company, Sanghvi Movers Limited, would become the invisible backbone of India's infrastructure miracle, lifting everything from wind turbines to petrochemical reactors, metro segments to power plant boilers. While Larsen & Toubro and Reliance Industries grabbed headlines for their mega-projects, it was Sanghvi's cranes doing the heavy lifting—literally.

What makes this story particularly fascinating for investors is the cyclical brutality of the infrastructure business. SANGHVI MOVERS' revenue has grown from Rs 3,262 m in FY20 to Rs 6,467 m in FY24. Over the past 5 years, the revenue of SANGHVI MOVERS has grown at a CAGR of 18.7%. But that glossy CAGR masks a roller coaster: near-death experiences during policy shifts, phoenix-like recoveries during infrastructure booms, and the constant dance between capital allocation and utilization rates.

Today, as India stands at the cusp of a renewable energy revolution with ambitious targets of 500 GW by 2030, and as the government pumps unprecedented capital into infrastructure development, Sanghvi Movers finds itself at an inflection point. The company that once struggled with negative profits in FY18 now boasts net profit for the year grew by 67.7% YoY. Net profit margins during the year grew from 24.6% in FY23 to 30.4% in FY24.

This episode will trace the arc from that first crane to today's empire, examining the strategic pivots, near-fatal crises, and the operational excellence that transformed a regional equipment rental business into an infrastructure powerhouse. We'll dissect how policy changes nearly destroyed the company, how management navigated through existential threats, and why this unsexy, asset-heavy business might be one of the best proxies for India's next decade of growth.

Buckle up—this is a story of steel, grit, and the unsung heroes who literally lift nations.

II. Origins & Foundation (1989-1995)

The year was 1989. India was still two years away from economic liberalization, operating under the shadow of the License Raj. Most entrepreneurs were scrambling for government permits to manufacture widgets or textiles. But in Pune, Maharashtra, a businessman named Chandrakant P. Sanghvi was thinking differently. He wasn't interested in making things—he wanted to help others build them.

In the year 1989, Mr C.P. Sanghvi imported 1st crane from the UK, Tadano TG 700E (capacity 70 MT). This wasn't just equipment acquisition; it was the birth of an entirely new business model in India. While construction companies were accustomed to either buying expensive cranes that sat idle between projects or relying on primitive lifting methods, Sanghvi introduced the radical concept of crane rentals—pay only for what you use, when you use it.

The timing seemed almost counterintuitive. India's infrastructure sector in 1989 was nascent at best. The country's GDP was around $300 billion, foreign exchange reserves were precariously low, and major infrastructure projects were few and far between. But Sanghvi saw what others didn't: India would eventually have to build, and when it did, someone would need to do the heavy lifting.

Sanghvi Movers Ltd. (SML) was incorporated on 3rd November, 1989 by Late Mr. Chandrakant P. Sanghvi, Ex-Chairman & founder of the company having its Head Quarter in Pune. The choice of Pune was strategic—close enough to Mumbai's commercial center, yet offering lower operational costs and proximity to the industrial corridors of western India.

Subsequently, he bought more cranes which were deployed with clients like Oil India Ltd., and ONGC. These weren't glamorous clients by Wall Street standards, but they were exactly what a fledgling crane rental company needed: government-backed, deep-pocketed, and engaged in continuous infrastructure development. Oil India and ONGC were laying pipelines, building refineries, and setting up drilling rigs—all activities requiring specialized heavy-lifting equipment.

The early 1990s brought economic liberalization, and with it, a surge in industrial activity. Foreign companies were entering India, domestic conglomerates were expanding, and suddenly, construction wasn't just about government projects anymore. Sanghvi's rental model began attracting attention. Why should a company building a single refinery invest crores in cranes that would become idle assets post-construction?

By 1994, the company had built enough credibility and scale to contemplate a public offering. This was audacious for a five-year-old crane rental company in a market that barely understood the business model. Headquartered in Pune, SML was incorporated in 1989 and went through an Initial Public Offering in 1994.

In the year 1995, the company went public and used the IPO proceeds (Rs. 17.50 Crores) to purchase some other cranes between 160MT to 450MTs. This wasn't just capital raising—it was a statement of intent. The IPO proceeds allowed Sanghvi to acquire heavy-duty cranes that could handle larger, more complex projects. The 450MT capacity cranes were among the largest in India at the time.

The entrepreneurial vision of C.P. Sanghvi was remarkable for its simplicity and foresight. Sanghvi, considered as a pioneer in the crane rental industry in India to date. With his farsightedness he not only identified the potential of crane business but the need of heavy duty cranes for speedy infrastructure development in India. He understood that India's infrastructure deficit would eventually translate into decades of construction activity. Rather than compete in manufacturing or construction, he chose to be the arms dealer in India's infrastructure wars.

Under His vision, leadership skills and exemplary entrepreneur qualities SML has invested over Rs.2500 Crores in crane business since its inception. But in 1995, with just Rs. 17.50 crores from the IPO, that journey of thousands of crores was just beginning.

By the mid-1990s, Sanghvi Movers had established a unique position in the Indian market. It wasn't just renting cranes; it was pioneering an entire industry. The company's early focus on government clients provided stability, while the IPO gave it the capital to scale. The foundation was set, but the real test was about to come—could a crane rental company capture the opportunity of India's impending infrastructure boom? The answer would arrive in 1997, wearing the colors of Reliance Industries.

III. The Reliance Breakthrough & Early Growth (1996-2003)

The phone call came in late 1996. Reliance Industries, India's petrochemical giant led by Dhirubhai Ambani, was planning something massive—a world-scale refinery and petrochemical complex at Jamnagar that would eventually become the world's largest oil refining hub. They needed cranes. Lots of them. More than any single project in India had ever required.

For Sanghvi Movers, this was the Olympics, World Cup, and Super Bowl rolled into one. SML has got major breakthrough with Reliance Industries Limited in FY 1997 and 1998. But the scale of Reliance's requirement was staggering—it would require Sanghvi to essentially bet the company on a single project.

C.P. Sanghvi didn't blink. SML did a capex of more than Rs. 50 crores during those 2 years and imported 36 cranes from Singapore with a charted barge for this project. To put this in perspective, the company had raised just Rs. 17.50 crores in its IPO two years earlier. This Rs. 50 crore investment represented a 3x expansion, funded through a combination of debt, internal accruals, and sheer entrepreneurial courage.

The logistics alone were mind-bending. Thirty-six cranes don't just appear—they need to be sourced, inspected, shipped, cleared through customs, transported to site, assembled, tested, and deployed. Sanghvi chartered an entire barge from Singapore, creating a floating convoy of yellow steel that sailed into Indian waters like a merchant armada. Port authorities had never processed such a shipment. Custom officials scrambled to classify and clear these machines.

More than 75 cranes were deployed for the construction of the Reliance Project during the span of 18 months. At Jamnagar, the sight was extraordinary—a forest of crane booms reaching into the Gujarat sky, lifting reactors, distillation columns, and pipe racks. Sanghvi's operators worked in shifts around the clock. The company had to rapidly train crane operators, riggers, and supervisors. They established on-site maintenance workshops, spare parts inventories, and even residential facilities for their crews.

The Reliance project wasn't just about scale—it was about complexity. Petrochemical projects require millimeter precision when positioning multi-hundred-ton vessels. A refinery column must be lifted, rotated, and placed exactly vertical. A slight tilt could cause catastrophic failure under operational pressures. Sanghvi's team had to coordinate multiple cranes working in tandem—one crane might hold a vessel steady while two others positioned it, all choreographed like a massive industrial ballet.

The financial model was transforming too. Rather than simple hourly rentals, Sanghvi began offering integrated solutions. They would survey lift requirements, plan crane deployment, manage logistics, and provide operators—essentially becoming a turnkey heavy-lifting contractor. Margins expanded from simple rental yields to value-added service premiums.

Reliance's project had a demonstration effect across Indian industry. If Sanghvi could handle Jamnagar—the largest, most complex industrial project in India—they could handle anything. Orders began flowing from other industrial houses. Essar was building refineries, L&T was constructing power plants, and Indian Oil was modernizing its facilities. Each wanted the "Reliance-proven" crane company.

Between 1998 and 2003, Sanghvi's fleet expanded from roughly 40 cranes to over 150. The company established regional depots in Gujarat, Maharashtra, and Tamil Nadu. They weren't just parking cranes anymore—each depot became a full-service center with maintenance bays, operator training facilities, and logistics hubs.

The boom in petrochemicals and oil refining wasn't accidental. India's economy was growing at 6-7% annually, driving energy demand. The government's liberalization policies allowed private players like Reliance to build massive refineries. Global oil companies were entering India. This created a perfect storm of demand for heavy lifting services.

But C.P. Sanghvi was already thinking beyond petrochemicals. He observed the cyclicality in oil and gas—projects would surge during high oil prices and collapse during downturns. The company needed diversification, a hedge against sector-specific volatility. His eyes turned to an emerging sector that promised steady, long-term growth: renewable energy, specifically wind power.

By 2003, Sanghvi Movers had established itself as India's undisputed leader in crane rentals. The Reliance project had transformed it from a promising startup to an industrial powerhouse. Revenues had grown from tens of crores to hundreds of crores. The company had proven it could execute at any scale.

Yet, the decision that would define Sanghvi's next phase had nothing to do with cranes. It was about wind turbines and a prescient bet on India's energy transition.

IV. Diversification into Wind Power (2003-2008)

The boardroom at Sanghvi Movers' Pune headquarters was divided. It was early 2003, and C.P. Sanghvi had just proposed something radical: the crane rental company should become a power producer. Not everyone was convinced. Why would a company that made money from construction invest in operations? Why wind power when India ran on coal? The answer lay in Sanghvi's unique vantage point—his cranes had been erecting wind turbines across India, and he saw what others didn't.

During the year 2003-04, the company diversified their business activities and ventured in the Business of Power Generation by commissioning 5.05 MW Wind Mills of Rs 21.90 crore in Jaisalmer, Rajasthan and Chitradurga, Karnataka. Power Generation from Wind Mills commenced on September 30, 2003.

This wasn't a random diversification. Sanghvi's cranes had been erecting wind turbines for companies like Suzlon and Vestas. The company's operators had intimate knowledge of wind sites, installation challenges, and maintenance requirements. They understood wind patterns, foundation requirements, and grid connectivity issues better than many wind farm developers. If anyone could efficiently operate wind assets, it was the company that had been installing them.

The strategic rationale was multi-layered. First, wind power provided a natural hedge against the cyclicality of crane rentals. When construction slowed, power generation would provide steady cash flows. Second, wind projects offered attractive tax benefits through accelerated depreciation, allowing Sanghvi to shelter profits from its increasingly profitable crane business. Third, and most importantly, it gave Sanghvi a foothold in what would become India's renewable energy revolution.

The locations—Jaisalmer in Rajasthan and Chitradurga in Karnataka—were carefully chosen. Both sites offered consistent wind speeds above 7 meters per second, crucial for efficient power generation. Jaisalmer's location in the Thar Desert provided vast, unobstructed terrain, while Chitradurga's position in the Deccan Plateau caught strong monsoon winds. The company wasn't just buying turbines; it was acquiring some of India's best wind real estate.

With the wind business established, Sanghvi returned to aggressive expansion in its core crane business. The company completed expansion in cranes of Rs 81 crore during the year 2004-05, Rs 170 crore during the year 2005-06 and Rs 180 crore during the year 2006-07. This represented over Rs. 430 crores in capital expenditure over three years—a staggering amount for a company that had gone public with Rs. 17.50 crores less than a decade earlier.

During the year 2007-08, the company imported 34 Nos cranes and some attachments aggregating Rs 22048.43 lakh. The timing seemed perfect. India's economy was roaring at 9% GDP growth. Infrastructure spending was at all-time highs. The government had announced ambitious plans for power generation capacity addition. Every industrial group was expanding.

Sanghvi's fleet had evolved dramatically. From basic mobile cranes, the company now operated sophisticated crawler cranes with lattice booms capable of reaching heights of over 150 meters. They had specialized attachments for different industries—heavy lift attachments for refinery modules, specialized booms for wind turbine erection, and precision equipment for metro construction.

The operational complexity had increased exponentially. The company now managed maintenance schedules for hundreds of cranes across dozens of sites. They had developed proprietary software for fleet tracking, utilization optimization, and predictive maintenance. Each crane's location, operating hours, maintenance history, and revenue generation were tracked in real-time.

Training had become a critical differentiator. Sanghvi established India's first private crane operator training institute. They recruited mechanical engineers and trained them in hydraulics, load calculations, and safety protocols. Operators underwent 500 hours of training before touching a crane. This focus on safety and skill was crucial—a single accident could destroy reputation and trigger massive liabilities.

By early 2008, Sanghvi Movers looked unstoppable. The company operated the largest crane fleet in India with over 200 cranes. They had diversified into wind power with expanding generation capacity. Clients included every major industrial house in India. Order books were full, utilization rates exceeded 80%, and profits were at record highs.

In June 2009, SML held the 9th largest global crane owning company globally by the ICST magazine. In Dec 2007 and December 2008, awarded as the fastest growing equipment rental company in the world of construction.

But storm clouds were gathering on the global horizon. In the United States, subprime mortgages were defaulting. Investment banks were collapsing. Credit markets were freezing. The global financial crisis was about to test every assumption about India's infrastructure story. For an asset-heavy, debt-funded business like Sanghvi Movers, the coming crisis would be the ultimate stress test.

Yet, in what would become a defining characteristic of the company, Sanghvi would emerge from the crisis stronger than ever, setting the stage for its next phase of growth.

V. Global Financial Crisis & Recognition (2008-2013)

September 15, 2008. Lehman Brothers collapsed, sending shockwaves through global financial markets. In Mumbai, the Sensex crashed 1,070 points in a single day. Credit markets froze overnight. For Sanghvi Movers, sitting on hundreds of crores worth of crane assets financed largely through debt, this should have been catastrophic. Infrastructure projects across India ground to a halt. Real estate developers abandoned half-built towers. Industrial expansion plans were shelved. The crane rental business, which depends entirely on construction activity, faced an existential crisis.

Yet something remarkable happened. While global crane rental companies were filing for bankruptcy and selling assets at fire-sale prices, Sanghvi Movers not only survived but thrived. The recognition that came during this period wasn't despite the crisis—it was because of how the company navigated through it.

India's response to the global financial crisis was fundamentally different from the West. India's high domestic demand and large infrastructure projects will act as a buffer reducing the impact of the global downturn on its economy. The government, led by Prime Minister Manmohan Singh and Finance Minister P. Chidambaram, launched massive fiscal stimulus packages focused on infrastructure. The National Highway Development Project accelerated. Power generation capacity addition continued. Metro rail projects in Delhi and Mumbai pushed forward.

For Sanghvi, this meant that while private sector projects dried up, government infrastructure spending actually increased. The company's early relationships with PSUs like ONGC, NTPC, and Indian Oil became lifelines. These government entities, flush with stimulus funds and mandate to spend, continued their expansion projects. Sanghvi's cranes moved from stalled private projects to bustling government sites.

The company's disciplined approach to the crisis was masterful. Instead of panic-selling assets like their global peers, management took several counter-intuitive decisions. First, they used the downturn to acquire distressed assets from smaller competitors who couldn't survive the credit crunch. Quality cranes were available at 40-50% discounts from desperate sellers. Second, they invested heavily in maintenance and refurbishment, ensuring their fleet would be ready when demand returned.

In June 2009, SML held the 9th largest global crane owning company globally by the ICST magazine. In Dec 2007 and December 2008, awarded as the fastest growing equipment rental company in the world of construction. This recognition was extraordinary—while American and European crane companies were shrinking, an Indian company was climbing global rankings.

The wind power business proved its worth as a hedge during this period. While crane rental revenues declined, the wind mills continued generating power and cash flow. The steady revenue from power sales helped service debt and maintain liquidity. This diversification strategy, questioned by many during the boom years, now looked prescient.

By 2010, as the global economy stabilized and India returned to 8%+ GDP growth, Sanghvi was perfectly positioned. They had a larger, modernized fleet acquired at attractive prices. Competitors had been weakened or eliminated. Government infrastructure spending was at record highs. The company's order book exploded as delayed projects resumed and new projects were announced.

The crisis also triggered important operational improvements. Sanghvi implemented strict working capital management, reducing debtor days and improving cash conversion cycles. They renegotiated debt terms with banks, securing lower rates and longer tenures. The company also diversified its customer base, reducing dependence on any single sector or client.

Between 2010 and 2013, India's infrastructure sector entered a golden period. The government targeted $1 trillion in infrastructure investment. Power generation capacity was to double. Thousands of kilometers of highways were planned. New airports, ports, and metro systems were approved. For a crane rental company, it was like all festivals arriving at once.

Sanghvi's fleet utilization rates exceeded 85%. Rental yields improved as demand outstripped supply. The company expanded into new segments—metro rail construction in Delhi and Mumbai, nuclear power projects, and ultra-mega power projects. They developed specialized capabilities for each sector, becoming not just crane suppliers but technical partners in complex lifting operations.

The international recognition continued. Global crane manufacturers like Liebherr, Terex, and Manitowoc began viewing Sanghvi as a key customer. The company's orders for new cranes often determined production schedules at European factories. Sanghvi executives were invited to global crane conferences, sharing insights about emerging market dynamics.

By 2013, Sanghvi Movers had transformed from a survivor of the financial crisis to a leader of the post-crisis infrastructure boom. Revenues had nearly doubled from pre-crisis levels. The company operated over 250 cranes, making it one of the largest fleets in Asia. But the biggest transformation was yet to come.

Wind energy in India was about to shift from a niche renewable sector to a mainstream power source. For Sanghvi, which had quietly built expertise in wind turbine erection over the past decade, this would open unprecedented opportunities. The company that had started with a single crane was about to become the backbone of India's renewable energy revolution.

VI. Wind Energy Pivot & The Great Slowdown (2014-2018)

By 2014, Sanghvi Movers had quietly become India's wind energy installation powerhouse. While media attention focused on turbine manufacturers like Suzlon and project developers like ReNew Power, it was Sanghvi's cranes doing the actual work—lifting 90-ton nacelles to heights of 120 meters, precisely positioning 60-meter blades in howling winds, executing installations from the deserts of Rajasthan to the coastal plains of Tamil Nadu.

SML, for over the past 17 years, has erected approx. 10GW of windmills all over India and is a preferred partner to all the leading OEM's as well as IPPs. To understand the scale: 10GW represents roughly 15,000 wind turbines, each requiring multiple crane deployments for foundation, tower, nacelle, and blade installation. Sanghvi had touched nearly every major wind farm in India.

The economics of wind installation were attractive. A typical 2MW wind turbine installation required specialized cranes for 15-20 days and generated revenues of Rs. 50-75 lakhs. With India adding 3-4 GW of wind capacity annually, this translated to thousands of installations and hundreds of crores in revenue. Better yet, wind projects were geographically concentrated in wind-rich states, allowing efficient fleet deployment.

Between 2014 and 2017, everything aligned perfectly. Approximately 80% of its business comes from installation of wind mills and thermal power plants. The government's generation-based incentives and accelerated depreciation benefits had made wind projects financially attractive. State electricity boards were mandated to buy wind power at preferential feed-in tariffs of Rs. 4-6 per unit. Developers rushed to install capacity, and Sanghvi's cranes worked round the clock.

Then came February 2017—a date that would live in infamy for India's wind sector.

The first-ever reverse auction for wind power projects was conducted by SECI for 1,000 MW of capacity in February 2017. The lowest tariff that emerged in the auction was Rs 3.46 per kWh. This wasn't just a price reduction—it was a paradigm shift. The comfortable world of fixed feed-in tariffs was dead. Competitive bidding had arrived.

Before FY18, the wind and solar energy projects used to work on cost-plus tariff mechanism... In FY2018, the government changed the rules of the game for renewable energy (Wind and Solar). The impact was immediate and brutal.

Aggressive bidding by companies led tariffs to plummet and drop to as low as Rs 2.43 per kWh in December 2017 from feed-in tariffs ranging between Rs 4.6 and Rs 6 until 2016. Developers who had built business models around Rs. 5 per unit suddenly faced Rs. 2.43 per unit. Projects became financially unviable overnight. Wind capacity additions, which had reached 5.5 GW in FY2017, collapsed.

For Sanghvi Movers, the impact was catastrophic. Revenues fell by half in FY2018 and profits reduced from Rs 109 Crs in 2017 to a loss of Rs (-57) Crs in FY2018... revival in wind energy capacity addition will have a very visible and immediate impact on the financials of Sanghvi Movers.

The numbers were staggering. A company that had reported Rs. 109 crores in profit suddenly faced Rs. 57 crores in losses—a swing of Rs. 166 crores. Crane utilization rates plummeted from over 80% to below 50%. Hundreds of cranes sat idle in depots, their yellow paint fading under the sun, their loan EMIs ticking regardless.

The crisis exposed the vulnerability of Sanghvi's business model. The company had built its entire growth strategy around wind energy expansion. They had invested hundreds of crores in specialized wind turbine erection cranes. Operators had been trained specifically for wind projects. Regional depots were located near wind sites. When wind stopped, everything stopped.

Management faced impossible choices. Should they sell cranes at distressed prices to reduce debt? Should they lay off trained operators who had been with the company for years? Should they exit wind altogether and refocus on traditional infrastructure? C.P. Sanghvi, the founder who had built this empire, had passed away in April 2019, leaving his son Rishi to navigate the worst crisis in company history.

The response was measured but decisive. First, the company sold non-core assets including some older cranes, generating cash to service debt. Second, they aggressively cut costs, reducing administrative expenses and renegotiating supplier contracts. Third, and most importantly, they didn't abandon wind—instead, they doubled down on building relationships with IPPs who would eventually return when policy stabilized.

The company also diversified frantically. Metro rail projects in Mumbai and Delhi absorbed some crane capacity. Refinery modernization projects at BPCL and HPCL provided work. The company even entered new segments like data center construction and warehouse development. But these couldn't fully compensate for the wind collapse.

The financial stress was severe. Banks classified loans as stressed assets. Stock price crashed from over Rs. 100 to below Rs. 30. Investors questioned whether the company would survive. Rating agencies downgraded debt. The company that had won global awards just years earlier was fighting for survival.

Yet, hidden in this crisis were seeds of recovery. The government, realizing that competitive bidding had gone too far, began policy corrections. Wind developers, having bid unsustainably low tariffs, started defaulting, forcing a reset in pricing. Most importantly, India's renewable energy ambitions—175 GW by 2022—remained intact, and wind had to be a major component.

By late 2018, green shoots appeared. 23.375 GW of solar, wind and hybrid capacity has been auctioned by central and state agencies during the period 2017–2018. The auctions resulted in historical low bids, due to the expectation of low price of capital goods like solar modules. While tariffs remained low, volumes were returning. Developers had adjusted business models. Financing was available again.

Sanghvi had survived its near-death experience. The company that entered 2018 with existential questions would exit it with renewed purpose. The wind sector was recovering, and Sanghvi—leaner, more diversified, but with its core capabilities intact—was ready for the next chapter. The crisis had been brutal, but it had also forced evolution. The company that emerged would be stronger, more resilient, and better positioned for India's renewable energy supercycle that was just beginning.

VII. Recovery & Strategic Repositioning (2019-2022)

The morning of March 24, 2020, should have been another disaster for Sanghvi Movers. Prime Minister Modi announced a nationwide lockdown, bringing India's $3 trillion economy to a grinding halt. Construction sites abandoned. Cranes frozen mid-lift. Workers fled to villages. For a company just recovering from the wind energy crisis, COVID-19 looked like the knockout punch. Yet by December 2020, Sanghvi's cranes were busier than they'd been in years. The recovery story that unfolded between 2019 and 2022 would redefine the company's trajectory.

The first signs of recovery had actually emerged in late 2019, before anyone had heard of coronavirus. Wind energy capacity additions, which had collapsed to barely 1.5 GW in FY2018, started recovering. Developers had figured out how to make projects work at lower tariffs through better technology and financial engineering. State governments, realizing that competitive bidding had gone too far, began offering more realistic prices.

When COVID struck, the government's response inadvertently accelerated Sanghvi's recovery. Infrastructure was declared an essential service. While restaurants and malls shut, highway construction continued. Power projects kept building. More importantly, the government launched a Rs. 111 lakh crore National Infrastructure Pipeline, essentially deciding to build its way out of the pandemic.

The pandemic also triggered a global renewable energy awakening. Climate commitments hardened. India announced ambitious targets—450 GW of renewable energy by 2030. Global investors, flush with liquidity from central bank stimulus, poured billions into Indian renewable energy. Suddenly, wind wasn't just recovering—it was booming.

But Sanghvi's management, scarred by the 2017-18 crisis, refused to put all eggs in the wind basket again. The company aggressively diversified its revenue streams. Metro construction in Mumbai, Delhi, and Bangalore absorbed crane capacity. The Dedicated Freight Corridor—India's ambitious rail infrastructure project—required hundreds of heavy lifts. Data center construction, driven by digitalization, emerged as a new segment.

During FY 2021-22, the Company incorporated its wholly owned subsidiary namely "Sanghvi Movers Vietnam Company Limited" at Vietnam on 16 September 2021. This wasn't just geographic expansion—it was a strategic hedge. Vietnam's infrastructure boom resembled India's a decade earlier. The subsidiary would provide growth optionality beyond India's borders.

Operational excellence became the mantra. The company implemented "Project SAMAGRA"—a comprehensive operational overhaul. IoT sensors were installed on cranes for real-time monitoring. Predictive maintenance algorithms reduced breakdowns. Digital workflows eliminated paperwork. Utilization tracking became granular—not just daily rates but hourly productivity. The company that had managed cranes with Excel sheets now ran on sophisticated ERP systems.

Financial discipline transformed from necessity to competitive advantage. Working capital cycles improved from 120 days to 75 days. Debt, which had peaked at dangerous levels during the crisis, was systematically reduced. The company even turned cash-positive on operations, a remarkable achievement for an asset-heavy business.

The workforce transformation was equally important. During the crisis, Sanghvi had retained its core technical team despite pressure to cut costs. Now, this loyalty paid dividends. Experienced operators who had stayed through tough times became training masters for new recruits. The company's crane operator training institute, established years earlier, became a competitive moat—producing certified operators faster than competitors could poach them.

Customer relationships deepened beyond transactional rentals. Sanghvi began offering "Crane-as-a-Service"—taking complete responsibility for lifting operations at client sites. Instead of renting cranes by the day, clients paid for outcomes—successful lifts, on-time completion, zero accidents. This shifted Sanghvi from vendor to partner, improving both margins and stickiness.

By late 2021, the transformation was evident. Utilization rates climbed back above 75%. Rental yields improved as demand exceeded supply. The order book, which had emptied during the crisis, filled with multi-year contracts. Financial results turned from losses to profits. The stock price, which had crashed below Rs. 30, started its recovery journey.

The masterstroke came in early 2022 when management made a bold decision: massive capacity expansion. While memories of the 2018 crisis remained fresh, management saw what others didn't—India was entering an infrastructure supercycle. The government's infrastructure spending was accelerating. Private capex was reviving. Renewable energy was exploding. The company that had barely survived was now preparing to attack.

The average capacity utilisation of crane fleet improved to 76% in Financial Year 2021-22. This wasn't just recovery—it was validation that demand had structurally shifted higher. The company began planning its largest-ever capex cycle.

The strategic repositioning was complete. Sanghvi Movers had evolved from a wind-dependent, operationally basic, financially stretched company to a diversified, digitally enabled, financially strong infrastructure play. The company that had started 2019 fighting for survival was ending 2022 preparing for hypergrowth.

But the real fireworks were about to begin. India's renewable energy sector was about to enter its most aggressive expansion phase. Manufacturing was booming on China-plus-one strategies. The government was spending unprecedented amounts on infrastructure. For Sanghvi Movers, perfectly positioned at the intersection of these megatrends, the next phase would be transformational.

VIII. The Capex Surge & Modern Era (2023-Present)

January 2023 marked an inflection point. In Sanghvi Movers' boardroom, management approved the largest capital expenditure in company history—over Rs. 330 crores for new cranes in a single year. This wasn't just expansion; it was a statement that the company which had nearly died in 2018 was now betting aggressively on India's infrastructure supercycle. The transformation that followed would be nothing short of spectacular.

Company invested INR924 crores in cranes over the last 4 years, including current year's INR200 crore capex. Despite this, net debt is only INR250-280 crores. This financial feat—investing nearly Rs. 1,000 crores while maintaining minimal leverage—showcased the cash-generative power of the rebuilt business model.

The numbers tell a story of explosive growth. The revenues of SANGHVI MOVERS stood at Rs 6,467 m in FY24, which was up 33.2% compared to Rs 4,856 m reported in FY23. SANGHVI MOVERS' revenue has grown from Rs 3,262 m in FY20 to Rs 6,467 m in FY24. But revenue growth only scratches the surface of the transformation.

The real story was operational leverage. As utilization rates climbed toward 85%, incremental revenue dropped straight to the bottom line. Net profit for the year grew by 67.7% YoY. Net profit margins during the year grew from 24.6% in FY23 to 30.4% in FY24. A 30% net margin in an asset-heavy, capital-intensive business is almost unheard of.

The capex wasn't random—it was surgical. Management identified specific segments with multi-year visibility. Wind energy, recovering from its nadir, needed specialized cranes for new 3MW+ turbines with hub heights exceeding 140 meters. Data centers required precision lifting in urban environments. Metro projects needed cranes that could operate in congested city centers. Each segment got purpose-built equipment.

Technology integration accelerated. Every new crane came equipped with telematics, GPS tracking, and operational sensors. The company developed a proprietary app where customers could book cranes like booking Uber—see available equipment, get instant quotes, track deployment, and receive digital invoices. This wasn't just digitization; it was reimagining the customer experience in a traditionally relationship-driven industry.

The wind energy renaissance drove much of the growth. As of October 2024, Suzlon's wind energy order book reached 5,131 MW, marking a 3.2-fold increase from 1,613 MW in September 2023. The company now holds its highest-ever domestic order book of 5.1 GW. For Sanghvi, Suzlon's order book was essentially its forward revenue pipeline—every megawatt Suzlon sold meant crane deployments for Sanghvi.

Geographic expansion accelerated beyond Vietnam. Date of Incorporation: 17 December 2024. Country of incorporation is Kingdom of Saudi Arabia. The Middle East subsidiary wasn't just about following Indian EPC companies to Gulf projects—it was about capturing the region's renewable energy boom. Saudi Arabia's Vision 2030 included massive renewable energy targets. The UAE was building the world's largest solar parks. Sanghvi's expertise in desert installations, honed in Rajasthan, translated perfectly.

The competitive landscape had fundamentally shifted in Sanghvi's favor. During the 2017-18 crisis, several competitors had exited or dramatically shrunk operations. Foreign crane rental companies found India too volatile. Local players lacked capital for expansion. Sanghvi emerged with an estimated 40-45% market share in organized crane rentals—almost monopolistic in certain specialized segments.

Financial metrics reached extraordinary levels. The ROCE for the company improved and stood at 23.6% during FY24, from 17.7% during FY23. The ROCE measures the ability of a firm to generate profits from its total capital (shareholder capital plus debt capital) employed in the company. A 23.6% ROCE meant every rupee invested generated 24 paise annually—remarkable for a capital-intensive business.

The balance sheet transformation was equally impressive. Debt to Equity ratio for FY24 stood at 0.2 as compared to 0.1 in FY23. Despite massive capex, leverage remained minimal. The company funded expansion through internal accruals—the holy grail of sustainable growth.

Human capital became a strategic differentiator. The company employed over 1,500 skilled operators, riggers, and engineers. Training programs expanded beyond technical skills to include safety certifications, customer service, and digital literacy. Sanghvi operators commanded premium salaries in the market, but their productivity justified the cost.

Customer concentration, once a risk, became diversified. While Reliance had dominated the early years and wind energy the middle years, the modern Sanghvi served hundreds of clients across dozens of sectors. No single customer exceeded 15% of revenue. No single sector exceeded 40%. This diversification provided resilience against sector-specific shocks.

The company's valuation began reflecting its transformation. From penny stock status during the crisis, market capitalization exceeded Rs. 3,000 crores. Institutional investors, who had fled during 2018, returned. Mutual funds accumulated positions. The stock that nobody wanted at Rs. 30 was now being chased at Rs. 300+.

But management remained grounded, scarred by the 2018 near-death experience. Capital allocation stayed disciplined. Instead of buying fancy corporate offices, money went into cranes. Instead of acquisitions, focus remained on organic growth. Instead of financial engineering, emphasis stayed on operational excellence.

Looking ahead, the pipeline appeared robust. The government targeted Rs. 143 lakh crores in infrastructure spending through 2030. Renewable energy capacity was to reach 500 GW. Manufacturing, boosted by production-linked incentives, would require industrial construction. Data centers, 5G infrastructure, and semiconductor fabs represented new opportunities.

The modern Sanghvi Movers was unrecognizable from even five years ago. It was now a technology-enabled, financially robust, operationally excellent infrastructure platform. The company that had started with one crane now operated over 400. The business that nearly died had become almost un-killable. The transformation was complete, but the growth journey had just begun.

IX. Wind Energy Renaissance & Order Book Explosion

The Suzlon headquarters in Pune was buzzing with unusual energy in September 2024. India's largest wind turbine manufacturer had just closed its biggest order ever—1,166 MW from NTPC Green Energy. For Suzlon's management, this validated their recovery strategy. For Sanghvi Movers, watching from just a few kilometers away in the same city, this single order represented hundreds of crores in future revenue. The wind energy renaissance wasn't coming—it had arrived with thunderous force.

The company now holds its highest-ever domestic order book of 5.1 GW, supported by a robust pipeline that offers a clear revenue outlook... As of October 2024, Suzlon's wind energy order book reached 5,131 MW, marking a 3.2-fold increase from 1,613 MW in September 2023. To understand the magnitude: 5.1 GW represents approximately 1,700 wind turbines, each requiring multiple crane deployments. For Sanghvi, this translated to thousands of lifting operations over the next 24 months.

The mathematics were compelling. Each modern wind turbine—now typically 3MW+ capacity—required larger, more sophisticated installations than earlier 2MW models. Tower sections had grown from 80 meters to 140 meters. Nacelles now weighed over 100 tons. Blade lengths exceeded 70 meters. These weren't just bigger components; they required exponentially more complex lifting operations.

But Sanghvi wasn't just riding Suzlon's coattails. The company had strategically created Sangreen Future Renewables, a subsidiary focused on complete wind project execution. Sanghvi Movers Limited announced that its material subsidiary, Sangreen Future Renewables Private Limited, has been awarded significant work orders totaling Rs 292 crore from prominent Independent Power Producers (IPPs) in India.

This wasn't just crane rental anymore—it was complete EPC (Engineering, Procurement, Construction) for wind projects. This includes the construction of wind turbine generator (WTG) civil foundations, internal roads, crane platforms, and the movement of WTGs from storage yards to their respective locations. Additionally, the scope covers the installation of WTGs, mechanical completion, internal 33kV line works, and the development of dedicated DP yards for each turbine.

The strategic evolution was brilliant. Instead of being a vendor to EPC contractors, Sanghvi became the EPC contractor. Margins expanded from 15-20% for crane rentals to 25-30% for turnkey projects. More importantly, it locked in multi-year revenues. A typical wind farm took 18-24 months from foundation to commissioning. Sanghvi now controlled the entire value chain.

The order book composition revealed the breadth of the renaissance. NTPC Green Energy, Tata Power, Adani Green Energy, ReNew Power, Greenko—every major renewable player was expanding aggressively. State utilities, mandated to meet renewable purchase obligations, were directly contracting wind capacity. Even industrial houses like JSW, Vedanta, and UltraTech were building captive wind farms to meet sustainability targets.

Government policy had finally aligned with ground reality. SECI will issue bids with a cumulative capacity of about 8 GW every calendar year from 2023 up to 2030. A detailed break-up of this capacity shall be issued by SECI. Eight gigawatts annually meant approximately 2,500-3,000 wind turbines per year—a massive pipeline providing visibility unprecedented in the sector's history.

The technology evolution favored Sanghvi's capabilities. Modern wind turbines weren't just larger; they were smarter. Installation required precise GPS positioning, real-time wind monitoring, and complex multi-crane coordination. Sanghvi's investments in technology and training over the years now provided competitive advantages. Competitors couldn't simply buy cranes and compete—they lacked the ecosystem of skills, systems, and relationships.

Market share dynamics had shifted decisively. Sanghvi Movers · Mkt Cap: 3,198 Crore (down -5.71% in 1 year) · Revenue: 905 Cr · Profit: 166 Cr · Promoter Holding: 47.2%. The company controlled an estimated 40-45% of India's organized crane rental market, but in specialized wind installation, the share was even higher—potentially exceeding 60%.

The competitive moat was widening. Wind turbine installation required specific certifications from turbine manufacturers. Vestas, Siemens Gamesa, and GE validated only select contractors. Insurance companies insisted on proven track records. Project developers preferred integrated solutions over managing multiple vendors. Every successful project strengthened Sanghvi's position for the next one.

Financial implications were staggering. If India achieved even 6 GW of annual wind installations (75% of the 8 GW target), and Sanghvi captured 50% market share, it translated to 3 GW of installations. At Rs. 75-100 crores revenue per GW, this meant Rs. 225-300 crores annually from wind alone. Add the higher-margin EPC business, and wind could contribute Rs. 400-500 crores to topline.

The growth wasn't just quantitative but qualitative. Relationships with OEMs deepened. Suzlon's new turbine designs were developed with input from Sanghvi's installation teams. Project developers consulted Sanghvi during site selection, understanding that installation feasibility affected project economics. The company had evolved from service provider to ecosystem partner.

International opportunities beckoned. Sri Lanka, Bangladesh, and Nepal were beginning their renewable journeys. African nations, particularly South Africa and Kenya, needed expertise for wind projects. Sanghvi's experience in challenging terrains—from Himalayan foothills to coastal marshlands—was globally relevant. The Vietnam subsidiary was already operational; more international expansion seemed inevitable.

Risk management had evolved too. The company no longer depended solely on policy-driven wind auctions. Corporate renewable energy procurement—where companies directly bought wind power—was growing. Hybrid projects combining wind and solar provided steady work. Energy storage projects, requiring heavy lifting for battery installations, represented future opportunity.

The renaissance felt sustainable this time. Unlike the 2014-17 boom driven by subsidies, current growth stemmed from fundamental economics. Wind power at Rs. 2.5-3 per unit competed with thermal power. Grid integration had improved. Battery costs were declining, solving intermittency issues. Climate commitments had hardened from nice-to-have to must-have.

For Sanghvi Movers, the wind energy renaissance represented vindication of a two-decade bet. The company that had suffered most during wind's collapse was now positioned to benefit most from its recovery. The order book explosion wasn't just about current revenues—it validated the strategic patience of staying invested in wind through its darkest period. The company that had erected 10 GW historically was now positioned to install another 10 GW in just the next five years.

X. Business Model & Competitive Advantages

To understand Sanghvi Movers' remarkable resilience through multiple crises and its current dominance, one must dissect its business model with surgical precision. On the surface, it appears deceptively simple: buy cranes, rent them out, maintain them, repeat. But beneath this simplicity lies a complex web of operational excellence, financial engineering, and strategic positioning that creates formidable competitive advantages.

The Company has a fleet of 400+ medium to large sized heavy duty telescopic and crawler cranes ranging from 20 to 1600 MT across 130+ operational job sites in India. This isn't just about fleet size—it's about fleet composition. Sanghvi operates a barbell strategy: smaller cranes (20-100 MT) for volume and utilization, massive cranes (500-1600 MT) for specialty lifts with premium pricing. A 1600 MT crane can command Rs. 50-75 lakhs monthly rental, but only a handful exist in India.

The asset-heavy nature of the business, often viewed as a weakness, is actually a strength when executed correctly. Cranes are productive assets with 20-25 year lifespans. Unlike technology equipment that obsoletes quickly, a well-maintained crane from 2010 remains fully functional today. Depreciation charges reduce taxable income while the assets continue generating cash—a beautiful tax shield that technology companies can't replicate.

The company's operating profit increased by 48.3% YoY during the fiscal. This operational leverage is the model's magic. Cranes have high fixed costs—depreciation, insurance, parking—but minimal variable costs. Once utilization exceeds 60%, incremental revenue has 70%+ contribution margins. At 85% utilization, the business prints money.

Network effects, typically associated with software platforms, exist in crane rentals too. SML has a PAN India presence with its Depot network spread across all over India in more than 10 states. A customer needing cranes in multiple locations prefers a single vendor for standardization, training, and commercial simplicity. Sanghvi's pan-India presence becomes a competitive moat—regional players can't match the geographic coverage.

The technical expertise moat is underappreciated. Operating a 1000 MT crawler crane isn't like driving a truck. Load calculations, ground bearing pressure, wind effect compensation, multi-crane synchronization—these require engineering expertise. ISO 45001:2018, ISO 9001:2015 & ISO 14001:2015, certified company. These certifications aren't bureaucratic checkboxes; they represent systematic safety and quality processes that prevent catastrophic accidents that could bankrupt smaller operators.

Customer switching costs are surprisingly high. Once Sanghvi cranes are deployed on a multi-year project, switching becomes impractical. Operators are trained on specific equipment. Safety certifications are equipment-specific. Insurance policies are negotiated based on operator-equipment combinations. Project delays from switching vendors can cost crores daily. Customers become locked in, providing pricing power and renewal probability.

The financial model reveals sophisticated capital allocation. Company invested INR924 crores in cranes over the last 4 years, including current year's INR200 crore capex. Despite this, net debt is only INR250-280 crores. This means the business generated over Rs. 650 crores in free cash flow while growing rapidly—a rare combination. The company funds growth from internal accruals, avoiding dilution or dangerous leverage.

Working capital management provides another advantage. Sanghvi typically receives 15-30 day advances from customers but pays crane manufacturers over 90-180 days. This negative working capital cycle means growth is partially funded by suppliers and customers—brilliant financial engineering hiding in plain sight.

The crane lifecycle economics are compelling. A new 500 MT crane costs Rs. 50 crores. At Rs. 40 lakhs monthly rental and 70% utilization, annual revenue is Rs. 3.4 crores. Assuming 40% EBITDA margins, annual cash generation is Rs. 1.35 crores. The crane pays for itself in 37 years theoretically, but accelerated depreciation and tax shields reduce this to 15-20 years effective payback, while the asset operates for 25+ years.

Human capital is the hidden differentiator. 1500+ workforces 400+ latest crane fleet and modern machinery, 18 warehouses serving 11 different segments. These aren't just employees; they're specialized technicians. Training a competent crane operator takes 500+ hours. Developing a lifting supervisor requires years of experience. This tacit knowledge can't be quickly replicated by new entrants.

The business model evolution from pure rental to integrated solutions multiplies value. EPC business revenue expected to be INR200-250 crores in FY25, a significant jump from INR30 crores in FY24. EPC projects command 25-30% margins versus 15-20% for simple rentals. More importantly, they create stickiness—customers prefer single-source responsibility for complex projects.

Risk mitigation is embedded structurally. Fleet diversification across crane types prevents dependence on specific equipment. Sector diversification across wind, refining, infrastructure, and metros prevents customer concentration. Geographic spread across states prevents regional economic impacts. Contract structures with monthly minimums and take-or-pay clauses ensure revenue visibility.

The capital intensity that scares many investors actually creates barriers to entry. A new entrant needs Rs. 500+ crores just for a basic fleet. They need another Rs. 100 crores for depots and infrastructure. Working capital requirements add Rs. 200 crores. Technical team building takes 3-5 years. Customer credibility requires a track record. By the time a new entrant becomes competitive, Sanghvi has moved further ahead.

The ROE for the company improved and stood at 18.6% during FY24, from 13.3% during FY24. An 18.6% ROE in a capital-intensive business rivals software companies' returns but with more predictability. The business model that appears industrial and boring actually generates venture capital-like returns with infrastructure-like stability.

The ultimate competitive advantage is survival. Sanghvi has operated through the 1991 economic crisis, 2008 financial crisis, 2018 wind energy collapse, and 2020 pandemic. Each crisis eliminated competitors but strengthened Sanghvi. This antifragility—getting stronger from stress—is perhaps the most valuable moat. Customers, lenders, and suppliers know Sanghvi will exist next decade. In infrastructure, a 35-year track record is the ultimate competitive advantage.

XI. Playbook: Lessons for Investors & Operators

The Sanghvi Movers saga offers a masterclass in navigating cyclical, capital-intensive businesses through multiple economic cycles. For investors evaluating industrial companies and operators running similar businesses, the lessons are profound and often counterintuitive. This isn't about financial engineering or strategic brilliance alone—it's about understanding the fundamental rhythms of infrastructure businesses and positioning accordingly.

Lesson 1: Embrace Cyclicality, Don't Fight It

Most companies try to smooth cyclicality through diversification or financial hedging. Sanghvi did something different—they accepted cyclicality as fundamental to infrastructure and built their entire strategy around it. During upturns, they invested aggressively. During downturns, they preserved capital and acquired distressed assets. Revenues fell by half in FY2018 and profits reduced from Rs 109 Crs in 2017 to a loss of Rs (-57) Crs in FY2018... revival in wind energy capacity addition will have a very visible and immediate impact on the financials of Sanghvi Movers.

The key insight: In cyclical businesses, survival through downturns matters more than optimization during upturns. Companies that maintain balance sheet strength to survive troughs inevitably thrive during peaks because weaker competitors have been eliminated.

Lesson 2: Asset-Heavy Doesn't Mean Asset-Stupid

Conventional wisdom suggests asset-light models are superior. Sanghvi proves otherwise. Company invested INR924 crores in cranes over the last 4 years, including current year's INR200 crore capex. Despite this, net debt is only INR250-280 crores. The company generated enough cash to fund massive expansion while reducing leverage—a feat most asset-light businesses can't achieve.

The playbook: Buy productive assets that generate cash over decades, not years. Maintain them meticulously. Depreciate them aggressively for tax shields. Fund expansion through internal accruals, not debt. The result is a business that compounds capital at high rates without dilution or leverage risk.

Lesson 3: Policy Risk Is Both Threat and Opportunity

The 2017-18 wind energy crisis nearly destroyed Sanghvi because of policy changes. Tariff-based competitive bidding in reverse auctions (called e-reverse auctions because these auctions are held electronically) is gradually replacing the system of fixed feed-in-tariff (FIT) in the renewable energy sector. But companies that survived the policy shift emerged stronger.

The lesson: In regulated or policy-dependent sectors, assume policies will change adversely. Build balance sheets that can survive 50% revenue drops. When policy shifts occur, weak players exit, creating opportunities for survivors to gain market share and acquire assets cheaply.

Lesson 4: Specialization Beats Diversification—Until It Doesn't

For years, Sanghvi's focus on crane rentals created competitive advantages through specialization. But excessive concentration in wind energy nearly killed them. The solution wasn't abandoning specialization but thoughtful diversification within core competencies.

The framework: Maintain deep specialization in capability (heavy lifting) but diversify across applications (wind, metros, refineries). This provides resilience without sacrificing competitive advantage. SML, for over the past 17 years, has erected approx. 10GW of windmills all over India and is a preferred partner to all the leading OEM's as well as IPPs.

Lesson 5: Balance Sheet Strength Is The Ultimate Strategy

Debt to Equity ratio for FY24 stood at 0.2 as compared to 0.1 in FY23. A 0.2 debt-to-equity ratio in a capital-intensive business is remarkable. This conservative leverage allowed Sanghvi to survive when revenues halved and invest aggressively when opportunities emerged.

The principle: In cyclical businesses, balance sheet strength determines strategic options. Companies with low leverage can acquire distressed assets, invest counter-cyclically, and survive extended downturns. Highly leveraged competitors become forced sellers, creating opportunities for strong balance sheets.

Lesson 6: Operational Excellence Compounds Quietly

The average capacity utilisation of crane fleet improved to 76% in Financial Year 2021-22. Improving utilization from 60% to 76% increased revenue by 25%+ with minimal incremental cost. These operational improvements compound over time but are invisible in financial statements until they reach inflection points.

The playbook: Focus relentlessly on utilization, turnaround time, maintenance efficiency, and operator productivity. Small improvements in operational metrics translate to large improvements in financial returns due to operational leverage.

Lesson 7: Customer Concentration Risk Can Be Managed

Early Sanghvi depended heavily on Reliance. During the wind boom, 80% of revenue came from wind installations. Both concentrations nearly destroyed the company at different times. The solution was systematic diversification without abandoning core relationships.

The approach: Accept concentration risk during growth phases but systematically diversify during mature phases. Maintain deep relationships with anchor clients while building broader customer bases. Never let a single customer or sector exceed 40% of revenue in steady state.

Lesson 8: Technical Moats Beat Financial Moats

ISO 45001:2018, ISO 9001:2015 & ISO 14001:2015, certified company. These certifications represent technical and operational capabilities that money alone can't buy. Training operators, building safety protocols, and establishing maintenance systems takes years.

The insight: In industrial businesses, technical competence creates more sustainable moats than capital access. Competitors can raise money, but they can't quickly replicate decades of operational experience and technical knowledge.

Lesson 9: Crisis Creates Opportunity—If You Survive

Every crisis in Sanghvi's history eliminated competitors and created opportunities. The 2008 financial crisis allowed asset acquisition at distressed prices. The 2018 wind crisis eliminated regional players. COVID accelerated infrastructure spending.

The framework: Build businesses that become stronger during crises. Maintain cash reserves for opportunistic acquisitions. Retain talent during downturns. Invest in capability building when others are cutting costs. The companies that survive crises inevitably dominate recoveries.

Lesson 10: Patience Pays in Infrastructure

Infrastructure moves in decade-long cycles, not quarters. Sanghvi waited through the entire 2017-2020 wind energy winter, maintaining capabilities despite losses. When wind recovered, they captured disproportionate value.

The principle: In infrastructure businesses, strategic patience beats tactical agility. Build for 10-year horizons. Maintain capabilities through downturns. Accept short-term pain for long-term positioning. The companies that can think in decades while operating in quarters inevitably win.

The Meta-Lesson

The ultimate lesson from Sanghvi Movers is that boring businesses with excellent execution beat exciting businesses with poor execution. Crane rental isn't glamorous. It won't feature in technology conferences or innovation summits. But executed well, it generates returns that rival any venture capital investment while building critical infrastructure for national development.

For investors, the playbook is clear: Find asset-heavy businesses with high returns on capital, conservative balance sheets, and exposure to structural growth trends. For operators, the message is simpler: Excellence in execution beats brilliance in strategy. The company that lifts steel beams reliably for 35 years builds more value than startups that promise to revolutionize everything but deliver nothing.

XII. Bull vs. Bear Case & Future Trajectory

Every investment thesis eventually faces the court of market opinion. For Sanghvi Movers, trading at Rs. 314 with a market capitalization exceeding Rs. 3,000 crores, the debate between bulls and bears isn't academic—it's about whether this crane rental company can sustain its remarkable transformation or whether structural challenges will reassert themselves. Let's examine both sides with the rigor they deserve.

The Bull Case: Infrastructure Supercycle Meets Execution Excellence

Bulls see Sanghvi Movers as the perfect proxy for India's infrastructure ambitions. The government has announced Rs. 143 lakh crores in infrastructure spending through 2030. Even if only 60% materializes, it represents unprecedented construction activity. Every highway, metro, refinery, and power plant needs cranes. Sanghvi, with 40-45% market share, captures value disproportionately.

The renewable energy opportunity alone justifies optimism. As of October 2024, Suzlon's wind energy order book reached 5,131 MW, marking a 3.2-fold increase from 1,613 MW in September 2023. The company now holds its highest-ever domestic order book of 5.1 GW. With India targeting 280 GW of wind capacity by 2030 from current 44 GW, annual installations must average 35-40 GW over six years. At 50% market share, Sanghvi could generate Rs. 500-600 crores annually from wind alone.

Manufacturing renaissance provides another growth vector. Production-linked incentive schemes are driving $500 billion in manufacturing investments. Semiconductor fabs, battery gigafactories, and automobile plants all require heavy lifting during construction. Each fab requires 200+ crane deployments over 24 months. The manufacturing capex cycle, just beginning, could rival infrastructure spending.

The financial metrics support aggressive optimism. The ROE for the company improved and stood at 18.6% during FY24. An 18.6% ROE with minimal leverage suggests enormous capacity for profitable growth. If management maintains these returns while deploying Rs. 300 crores annually in new cranes, earnings could compound at 20%+ annually.

International expansion multiplies opportunity. Date of Incorporation: 17 December 2024. Country of incorporation is Kingdom of Saudi Arabia. Saudi Arabia's $500 billion NEOM project alone could require hundreds of cranes. The Middle East's renewable energy ambitions—60 GW by 2030—need specialized installation expertise that Sanghvi possesses.

The competitive landscape increasingly favors incumbents. New emission norms, safety regulations, and insurance requirements create barriers for small operators. Customers prefer established players with track records. Technology requirements for modern projects exclude traditional operators. Sanghvi's scale advantages compound while competition weakens.

Valuation remains reasonable despite the rally. At 15x forward earnings, Sanghvi trades at discounts to global peers like Ashtead (20x) or United Rentals (18x), despite superior growth prospects. If India's infrastructure story plays out, multiple expansion to 20-25x seems plausible, suggesting 50%+ upside from re-rating alone.

The Bear Case: Structural Challenges and Cyclical Risks

Bears acknowledge recent success but question sustainability. The infrastructure boom depends on government spending, which depends on fiscal health. India's fiscal deficit remains elevated. State governments, primary infrastructure spenders, face stretched finances. Any fiscal consolidation could dramatically reduce infrastructure spending.

Wind energy, driving current growth, remains policy-dependent. Till 2017, wind energy capacity addition was through a feed-in tariff mechanism... There has been a transition from a relatively high tariff of Rs 4-5/unit to a more competitive tariff of Rs 2.5-3/unit. If competitive bidding drives tariffs below Rs. 2/unit, projects become unviable again, repeating the 2018 crisis.

Technology disruption poses existential risks. Modular construction reduces on-site lifting requirements. 3D printing could eliminate certain lifting needs. Automation might reduce crane operator requirements. While these changes seem distant, they could fundamentally alter the industry within a decade.

Capital intensity constrains returns. Despite operational excellence, the business requires continuous capital investment. Company invested INR924 crores in cranes over the last 4 years. This capital intensity limits free cash flow available for dividends or buybacks. Shareholders fund growth but may not receive proportional returns.

Competition from Chinese manufacturers intensifies. Chinese OEMs have successfully tapped into the Indian market by providing attractive financing options and ensuring quick delivery times. They have also streamlined their supply chains and established local manufacturing. Chinese companies could offer integrated packages—crane plus financing plus operators—at prices Sanghvi can't match.

Execution risks multiply with scale. Managing 400+ cranes across 130+ sites requires operational excellence. A single major accident could trigger liability claims, insurance issues, and reputational damage. As operations expand internationally, execution complexity compounds.

Customer concentration, while improved, remains concerning. Large infrastructure projects are typically awarded to a handful of EPC contractors—L&T, Tata Projects, Afcons. If any major EPC contractor faces difficulties, Sanghvi's revenue could suffer disproportionately.

The Balanced View: Structural Growth with Cyclical Volatility

Reality likely lies between extremes. India's infrastructure needs are real and massive—the country needs 50 new airports, 60,000 km of highways, 25 GW of annual renewable capacity, and massive urban infrastructure. This creates multi-decade demand for lifting services. Sanghvi, as the market leader with operational excellence, captures significant value.

However, the path won't be linear. Infrastructure spending fluctuates with economic cycles, political priorities, and global conditions. Wind energy will grow but face periodic policy challenges. Competition will intensify as the market expands. Margins will compress as the industry matures.

The company's response to these challenges matters more than the challenges themselves. Management has demonstrated ability to navigate crises, adapt to policy changes, and evolve business models. The conservative balance sheet provides cushion for volatility. Operational excellence creates resilience against competition.

SANGHVI MOVERS' revenue has grown from Rs 3,262 m in FY20 to Rs 6,467 m in FY24. Over the past 5 years, the revenue of SANGHVI MOVERS has grown at a CAGR of 18.7%. If the company maintains even 12-15% growth over the next five years—below historical rates—it becomes a Rs. 10,000+ crore revenue company. At current margins, this implies Rs. 2,500+ crores in market value creation.

The Verdict

Sanghvi Movers represents a classic "picks and shovels" play on India's infrastructure boom. While construction companies face execution risks and developers face financing challenges, Sanghvi simply rents cranes to whoever builds. This positioning—essential but not risky—creates an attractive risk-reward profile.

For long-term investors, the bull case appears stronger. India's infrastructure deficit is real, government commitment seems genuine, and execution capabilities are proven. Near-term volatility is certain, but structural growth seems assured. The company that survived the 2018 crisis will likely thrive through the 2020s boom.

XIII. Epilogue: Building India's Future

Chandrakant P. Sanghvi passed away on April 8, 2019, at the age of 65. He didn't live to see his company's remarkable recovery from the wind energy crisis, the pandemic resilience, or the current infrastructure boom. But perhaps that's fitting. Great builders rarely see their edifices complete—they lay foundations for others to build upon. The man who started with one imported crane in 1989 left behind an infrastructure institution that would literally lift India into its next phase of development.

In the year 1989, Mr C.P. Sanghvi imported 1st crane from the UK, Tadano TG 700E (capacity 70 MT). That single crane has multiplied into a fleet of 400+ medium to large sized heavy duty telescopic and crawler cranes ranging from 20 to 1600 MT across 130+ operational job sites in India. From lifting pipe sections for ONGC in the early 1990s to installing 140-meter wind turbines today, Sanghvi's cranes have been silent partners in India's transformation.

The numbers tell one story—revenues growing from Rs. 3,262 million to Rs. 6,467 million, market capitalization exceeding Rs. 3,000 crores, fourth-largest crane company globally. But the real story is written in steel and concrete across India's landscape. The Jamnagar refinery that processes 1.4 million barrels daily—Sanghvi cranes lifted those distillation columns. The Mumbai Metro that carries 500,000 passengers daily—Sanghvi cranes placed those segments. The wind farms generating 44 GW of clean energy—Sanghvi cranes erected those turbines.

This infrastructure enabling is profound yet invisible. Nobody drives on a highway thinking about how the bridge segments were lifted. Nobody switches on a light wondering how wind turbines were installed. Nobody fills petrol considering how refinery reactors were positioned. This invisibility is Sanghvi's burden and blessing—crucial yet unrecognized, essential yet uncelebrated.

The company today stands at an inflection point more promising than any in its 35-year history. India needs to build infrastructure worth $4.5 trillion to become a developed nation. Renewable energy capacity must increase 5x to meet climate goals. Manufacturing must double to create employment. Each represents thousands of lifting operations, millions of crane-hours, billions in revenue opportunity.

SML, for over the past 17 years, has erected approx. 10GW of windmills all over India and is a preferred partner to all the leading OEM's as well as IPPs. The next 17 years could see them erect 50 GW as India races toward energy independence. The company that struggled through policy shifts and market cycles has emerged as an indispensable partner in India's renewable transition.

But challenges remain formidable. China's infrastructure investment dwarfs India's. Technology evolution threatens traditional construction methods. Climate change makes project execution increasingly unpredictable. Financial markets remain volatile. Policy consistency isn't guaranteed. The company that survived past crises must navigate future uncertainties.

The transition from founder to second generation often destroys companies. Yet Rishi Sanghvi, taking charge during the company's darkest period, has proven worthy of his father's legacy. The aggressive capacity expansion, international ventures, and digital transformation show evolution beyond preservation. The company isn't just surviving post-founder—it's thriving with renewed ambition.

Date of Incorporation: 17 December 2024. Country of incorporation is Kingdom of Saudi Arabia. The Middle East expansion symbolizes ambition beyond India. From a Pune-based crane rental company to an international infrastructure services provider—the evolution continues. The cranes that built India's infrastructure now aim to build the world's.

What would C.P. Sanghvi make of today's company? The entrepreneur who bet everything on Reliance's Jamnagar project would likely approve of the calculated risks. The visionary who diversified into wind power would appreciate the renewable energy focus. The builder who invested Rs. 2,500 crores over decades would admire the current Rs. 300 crore annual capex program.

For investors, Sanghvi Movers represents something beyond returns—it's participation in nation-building. Every rupee invested enables infrastructure that serves millions. Every crane purchased creates employment for operators, riggers, and engineers. Every project completed advances India's development. This isn't just capital allocation—it's capital with purpose.

The story that began with one crane now encompasses 400+. The company that started with one client now serves hundreds. The business that began in Pune now operates across India and beyond. Yet fundamentally, nothing has changed. Sanghvi Movers still does what it did in 1989—lift heavy things for people building India.

Net profit for the year grew by 67.7% YoY. Net profit margins during the year grew from 24.6% in FY23 to 30.4% in FY24. These aren't just financial metrics—they're validation of a 35-year journey through India's economic evolution. From License Raj to liberalization, from industrial economy to services economy, from fossil fuels to renewable energy—Sanghvi's cranes have lifted India through each transition.

Looking ahead, the opportunity seems boundless yet grounded. India will build, and Sanghvi will lift. Wind turbines will rise, and Sanghvi will erect them. Metros will expand, and Sanghvi will place segments. Refineries will modernize, and Sanghvi will position reactors. The company doesn't need to innovate or disrupt—it needs to execute what it has done for 35 years, just at larger scale.

In the end, Sanghvi Movers' story isn't about cranes—it's about enablement. It's about the unglamorous, uncelebrated work of building nations. It's about showing up at dusty construction sites, calculating load charts, coordinating lifts, and ensuring safety. It's about turning architectural drawings into physical reality, one lift at a time.

The single crane that C.P. Sanghvi imported in 1989 has become a fleet that's lifting India's future. The next decade will determine whether this crane rental company becomes a true infrastructure institution—essential, enduring, and excellent. Based on the journey so far, betting against Sanghvi Movers seems like betting against India itself. And that's a bet few would make as India rises, one crane lift at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube