SAMHI Hotels: India's Acquisition-Led Hotel Platform Revolution

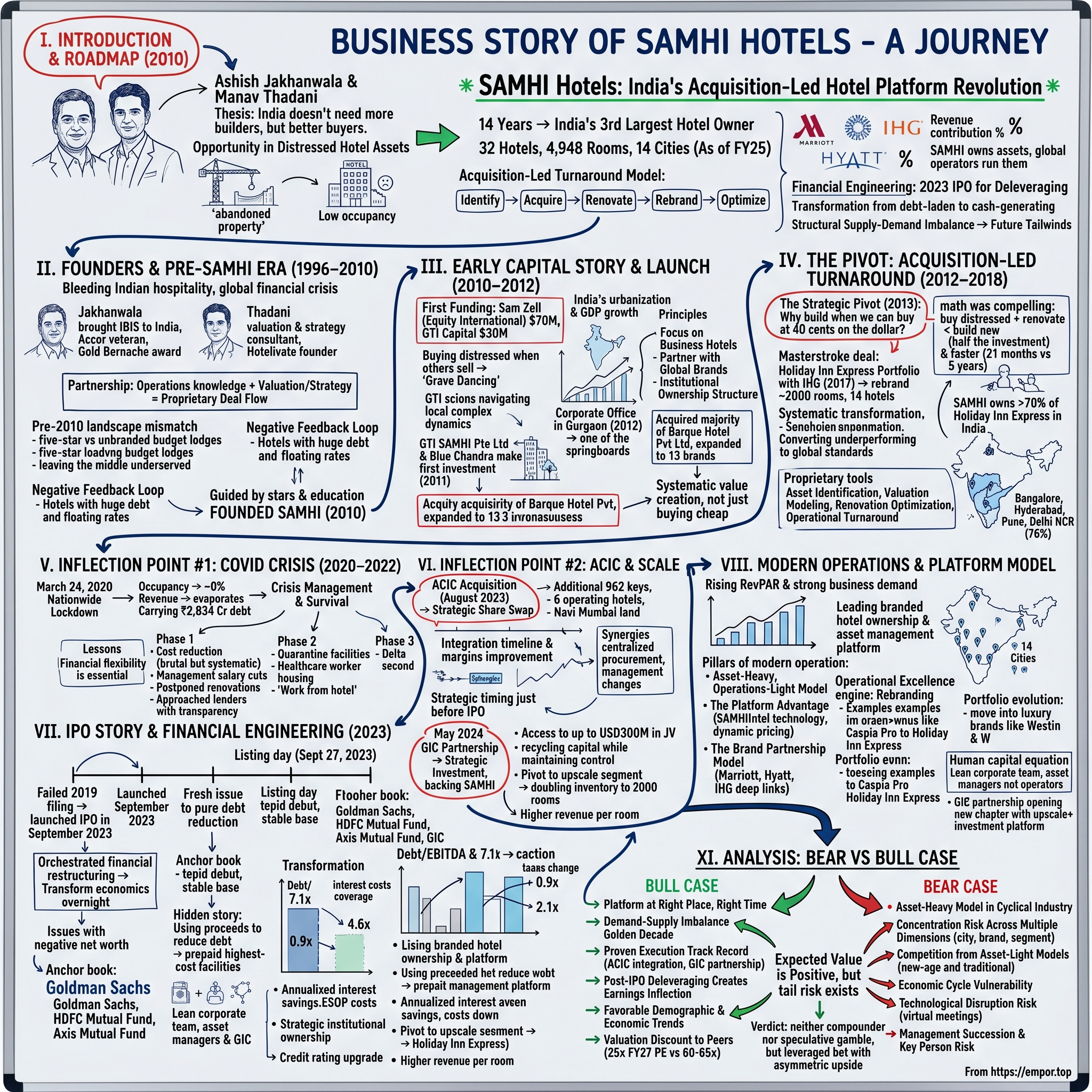

I. Introduction & Episode Roadmap

Picture this: It's 2010, and the Indian hospitality sector is bleeding. The global financial crisis has left a trail of distressed hotel assets across the country—half-built properties abandoned by overleveraged developers, operational hotels struggling with occupancy rates below 50%, and international brands watching their expansion plans crumble. Into this chaos walk two men with complementary backgrounds and a contrarian thesis: what if India's hotel industry didn't need more builders, but better buyers?

Ashish Jakhanwala and Manav Thadani saw opportunity where others saw wreckage. Within 14 years, they would transform SAMHI Hotels from a startup with ₹70 lakhs of personal capital into India's third-largest hotel owner—controlling 32 hotels with 4,948 rooms across 14 cities. Their weapon of choice? Not construction cranes and architectural blueprints, but a disciplined acquisition-led turnaround model that would redefine how hotel assets are owned, operated, and optimized in India. The thesis is elegantly simple yet contrarian: while competitors rushed to build new properties during India's infrastructure boom, SAMHI's founders recognized that the real opportunity lay in acquiring and transforming underperforming hotels. It follows an acquisition-led turnaround strategy, focusing on business hotels in high-demand micro-markets. This wasn't just about being opportunistic—it was about fundamentally reimagining how hotel assets should be owned and operated in emerging markets.

Today, As of FY25, it owns and operates 32 hotels with 4,948 rooms across 14 cities, under 10 brands. The company partners with global hospitality giants—Marriott contributing 60.81%, Hyatt contributing 18.34%, and IHG contributing 18.39% to their total revenue from operations for 2023—creating a unique model where SAMHI owns the assets but lets world-class operators run them. It's the hospitality equivalent of being a landlord to luxury tenants, except you also control the renovation budget and choose which tenant gets which property.

What makes this story particularly compelling for investors is the financial engineering that followed. After years of debt-fueled growth that left the company with nearly ₹2,834 crores in borrowings, SAMHI used its 2023 IPO proceeds to dramatically deleverage, creating what one analyst called "a saving of ₹52 crores in this quarter which goes straight to the bottomline". The transformation from a debt-laden acquirer to a cash-generating platform represents one of the most dramatic turnarounds in Indian hospitality.

But here's the kicker: this isn't just a turnaround story. Pan India hotel demand is expected to grow at 10.6% CAGR between FY24-FY27, while supply is expected to grow only at a CAGR of ~8% in the same period. SAMHI sits at the intersection of multiple tailwinds—India's economic growth, the rise of business travel, the premiumization of hospitality, and a structural supply-demand imbalance that could persist for years.

II. The Founders & Pre-SAMHI Era (1996–2010)

The year was 2010. India's hotel industry was hemorrhaging—revenue was almost zero compared to previous peaks, and More than 25 to 30% of assets are likely to become distressed as the industry struggles with a collective outstanding debt of Rs 50,000 crore. For most executives in the hospitality sector, this landscape represented a minefield to be avoided. For two men with deep roots in the industry, it looked like the opportunity of a lifetime.

Ashish Jakhanwala, a 1996 postgraduate from the Institute of Hotel Management, Lucknow, had 15 years of professional experience in the hotel industry, working across multiple roles such as hotel operations, asset valuations, hotel design, consulting, etc. From 2004 to 2010, Mr. Jakhanwala worked for the leading global hospitality company Accor and played a key role in establishing the IBIS Hotel chain in India. He wasn't just another hospitality executive—he was the architect who brought budget hospitality to India, establishing IBIS as a viable brand in a market that had previously been dominated by luxury and mid-market players.

The turning point in Jakhanwala's career came not from a boardroom victory, but from a personal conviction so strong that he was willing to bet his life savings on it. In the early days of his entrepreneurial venture, Samhi Hotels Ltd, Mr. Jakhanwala invested his personal savings of ₹70 lakhs before securing first funding. Think about that for a moment—a successful Accor executive, watching his industry collapse around him, chose to liquidate his personal wealth to buy into what most saw as a dying sector.

He received the prestigious Gold Bernache award from Accor in 2009—essentially the company's highest honor for excellence. Yet within a year, he left this comfortable perch to wade into the chaos. Why? Because he saw something others didn't: a fundamental mismatch between India's growing middle class and the hotel infrastructure available to serve them.

His co-founder brought a different but equally crucial perspective. Manav Thadani holds a bachelor's degree in science and a master's degree in arts each from New York University. Manav Thadani is an experienced consultant in the field of hospitality and is the founder and chairman of Hotelivate Private Limited. He was previously associated with HVS Licensing LLC. Where Jakhanwala understood operations from the inside, Thadani understood valuation and strategy from the outside. As a consultant, he had spent years advising hotel owners on how to maximize asset value—now he would put that knowledge to work as an owner himself.

The partnership made perfect sense: Jakhanwala knew how to run hotels efficiently, having done it for Accor across India. Thadani knew how to value them, restructure them, and position them for institutional investors. Together, they possessed what private equity firms call "proprietary deal flow"—the ability to source, evaluate, and execute transactions that others couldn't even see.

But understanding the founders requires understanding the wasteland they entered. The Indian hotel landscape pre-2010 was a study in contrasts. On one side, you had gleaming five-star properties in metros, catering to international business travelers and wealthy Indians. On the other, you had unbranded budget lodges offering questionable quality at rock-bottom prices. The middle—where most of India's emerging business travelers needed to stay—was dramatically underserved.

The global financial crisis had turned this structural problem into an acute crisis. The lodging industry is a capital intensive industry and the value of the property is adversely affected by huge debt, especially in weak market conditions. Also, firms that raise finance at floating rates are better off than those that adopt fixed rate floated debt. Many Indian hotel developers had borrowed heavily at floating rates during the boom years of 2006-2008, expecting continued growth. When the crisis hit, occupancies plummeted, room rates collapsed, and suddenly these properties couldn't service their debt.

This created what economists call a "negative feedback loop." Banks, burned by non-performing hotel loans, became reluctant to lend to the sector. Without fresh capital, distressed properties couldn't invest in renovations or rebranding. Without improvements, they couldn't attract guests or increase rates. Without revenue growth, they couldn't service existing debt, let alone attract new investment. The spiral seemed inescapable.

Yet Jakhanwala and Thadani saw opportunity precisely because the situation seemed so dire. They understood that India's fundamental growth story hadn't changed—GDP was still growing, the middle class was still expanding, business travel was still increasing. What had changed was the capital structure of hotel assets and the willingness of existing owners to hold on at any price. This disconnect between intrinsic value and market price created the arbitrage opportunity they would build SAMHI around.

Their thesis was deceptively simple: India didn't need more hotels; it needed better-managed hotels. The supply was there—thousands of rooms sat half-empty across the country. What was missing was professional management, global brand affiliation, and patient capital willing to wait for the cycle to turn.

The timing of their entry—2010—wasn't random. Guided by the stars and good education, Ashish and Manav founded SAMHI Hotels in 2010. This was the moment when distress was at its peak but recovery was visible on the horizon. India's GDP growth had bounced back to 8.5% in 2010 from the crisis lows. Corporate earnings were recovering. International travel was resuming. The demographic dividend—millions of young Indians entering the workforce—was beginning to pay off.

But perhaps most importantly, this was when institutional capital started looking at India differently. The crisis had shown that India's economy was more resilient than many had expected. While developed markets struggled with deflation and zero growth, India was back to robust expansion. For global investors seeking growth, India suddenly looked very attractive—and distressed hotel assets offered a way to play that growth at discounted entry prices.

III. The Early Capital Story & Launch (2010–2012)

The knock on the door came in early 2011, but it wasn't just any knock—it was Sam Zell calling. For those unfamiliar with the name, Zell was the legendary American real estate investor who had built a fortune by buying distressed assets when everyone else was selling. His investment firm, Equity International, a private equity firm founded by Sam Zell, made its first investment in SAMHI in 2011 and has been its largest shareholder for most of its history. When Zell comes knocking, the smart money pays attention.

The initial capital raise was transformative: first funding of $70 million (₹350 Cr) from Equity International and $30 million (₹150 Cr) from GTI Capital. This wasn't just money—it was validation from one of the world's most sophisticated distressed asset investors. Zell had made his fortune through what he called "grave dancing"—buying assets from motivated sellers during downturns. Now he was betting that Jakhanwala and Thadani could execute the same playbook in India.

"Equity International is recognized for identifying and leading promising real estate businesses in the most attractive and dynamic emerging markets," said Gary Garrabrant, EI's chief executive officer. "With SAMHI, led by Ashish, we have the opportunity to create the leading hotel property company in India, and we are privileged to partner with GTI Capital in this highly compelling market."

The GTI Capital connection was equally strategic. SAMHI is co-sponsored by GTI Capital Group, a privately held investment firm founded by Gaurav Burman, Gaurav Dalmia, Jonathan Schulhof and Madhav Dhar. These weren't just financial investors—they were scions of Indian business families who understood how to navigate the complex web of relationships, regulations, and regional dynamics that define Indian real estate.

"This investment perfectly represents our model of partnering with the best-in-class management teams in India, and investing both our own capital as well as aggregating capital from the finest co-investors globally," said Gaurav Burman, co-founder and general partner of GTI Capital Group.

The board composition reflected this fusion of global expertise and local knowledge. The Company's Board of Directors will include EI's Christopher Fiegen and Vijay Jayaraman, Ashish Jakhanwala, Manav Thadani, and Gaurav Burman and Gaurav Dalmia of GTI. This wasn't a typical private equity arrangement where investors sit on the sidelines—this was an active partnership where each party brought critical capabilities to the table.

In 2011, GTI SAMHI Pte Limited and Blue Chandra made their first investment in SAMHI. Blue Chandra was Equity International's investment vehicle, named perhaps with a nod to India's lunar ambitions—a fitting metaphor for a company shooting for the moon in a cratered market.

The timing of the investment was crucial. India is a dynamic country with strong economic fundamentals and favorable demographics, with projected annual GDP growth of more than 8% through 2018 and a rapidly urbanizing population of 1.2 billion. India currently has 42 cities of over one million people, a number expected to grow to nearly 70 by 2030. These cities are projected to generate 70% of the country's GDP. Travel and tourism are forecast to grow at rates similar to those of the broader economy and the hospitality sector is projected to double in size over the next seven years.

This wasn't just macroeconomic optimism—it was a fundamental bet on India's urbanization story. Every new IT park in Bengaluru, every new manufacturing hub in Chennai, every new financial services center in Mumbai created demand for quality business hotels. And SAMHI would be there to meet that demand, not by building from scratch, but by acquiring and transforming existing assets.

The following year, in 2012, the company established a corporate office in Gurgaon and it was one of the company's springboards. The choice of Gurgaon wasn't accidental—it was the epicenter of India's new economy, home to hundreds of multinational corporations whose traveling executives would fill SAMHI's hotels.

The early strategy crystallized around three principles that would define SAMHI for the next decade:

First, focus on business hotels, not leisure properties. Business travelers are less price-sensitive, more predictable, and generate higher occupancy during weekdays. While competitors chased the glamorous leisure market, SAMHI quietly cornered the mundane but profitable business travel segment.

Second, partner with global brands rather than creating proprietary ones. SAMHI was founded by three principals with extensive hospitality experience and long-standing relationships in India: Ashish Jakhanwala, SAMHI's chief executive officer, who previously led the development of Accor's hotel portfolio in India; Manav Thadani, chairman of HVS India; and Steve Rushmore, president and founder of HVS, the global hospitality consulting firm. These relationships would prove invaluable in securing management contracts with Marriott, Hyatt, and IHG.

Third, maintain an institutional ownership structure. Unlike family-owned hotel groups that often mixed personal and business interests, SAMHI would operate like a professionally-managed real estate investment trust. This would make it attractive to international capital and eventually enable a public listing.

The early acquisitions set the template. In the same year, SAMHI acquired majority ownership in Barque Hotel Private Limited and expanded its portfolio to include 13 brands of hotels. Each acquisition followed a similar pattern: identify a distressed or underperforming asset, negotiate an attractive price with a motivated seller, invest in renovations and rebranding, secure a management contract with a global operator, and then optimize operations to drive RevPAR growth.

What distinguished SAMHI from other opportunistic buyers was the systematic approach to value creation. They weren't just buying cheap and hoping for appreciation—they were actively transforming assets. This might mean converting a tired business hotel into a Holiday Inn Express, or upgrading a mid-market property to Courtyard by Marriott standards. Each transformation was carefully calibrated to match market demand with brand positioning.

"Equity International's investment was essential to SAMHI's success," said Ashish Jakhanwala, chairman, managing director and chief executive officer of SAMHI. "This partnership provided capital, instrumental advice, and support as we grew the company. The "instrumental advice" part was crucial—Zell's team had executed similar strategies in markets from Brazil to China, and they brought that institutional knowledge to SAMHI's boardroom.

By the end of 2012, SAMHI had laid the foundation for what would become India's most successful hotel acquisition platform. They had patient capital from world-class investors, a proven management team with deep industry relationships, and most importantly, a contrarian strategy in a market where everyone else was either building new or holding tight. The stage was set for the pivot that would define their next phase of growth.

IV. The Pivot: From Construction to Acquisition-Led Turnaround (2012–2018)

The boardroom meeting in 2013 was tense. SAMHI had been building hotels from scratch for two years, following the conventional wisdom that new properties commanded premium rates. But the numbers told a different story: construction was taking 5 years on average, costs were spiraling, and the return on investment was anemic. It was Sam Zell's team that pushed the uncomfortable question: "Why are we building when we can buy at 40 cents on the dollar?"

That question catalyzed the most important strategic pivot in SAMHI's history. While initially they constructed hotels from the ground up, they soon changed their strategy to acquisition-and-turnaround. This wasn't just a tactical adjustment—it was a fundamental reimagining of how to build a hotel empire in emerging markets.

Under the acquisition-led strategy, Samhi Hotels Ltd focused on identifying and buying out stressed or underperforming hotel assets with good potential at attractive valuations, modifying or renovating the said assets, deciding which operator/brand to operate the hotel under, and then turning them around gradually to extract the assets' full potential.

The math was compelling. Building a new 200-room hotel in a prime metro location could cost ₹150-200 crores and take 5 years from land acquisition to opening. Meanwhile, distressed hotels with similar room counts were trading at ₹60-80 crores, could be renovated for ₹20-30 crores, and be operational within 21 months. The acquisition model offered speed (21 months vs. 5 years), capital efficiency (half the total investment), and most importantly, immediate cash flow from existing operations.

Consider the Holiday Inn Express portfolio—SAMHI's masterstroke that would define their execution capability. In 2017, they pulled off what industry insiders called "the deal of the decade." IHG (InterContinental Hotels Group), one of the world's leading hotel companies, has partnered with SAMHI to rebrand approximately 2000 rooms (operating and under construction) within its India hotel portfolio, to Holiday Inn Express hotels. The recently signed portfolio comprises 14 hotels, including ten open hotels across key cities such as Ahmedabad, Bengaluru, Chennai, Delhi NCR, Hyderabad, Kolkata, and Mumbai.

But here's what made this deal brilliant: these weren't greenfield developments. They were existing properties—many struggling under previous brands or operating as independents—that SAMHI had systematically acquired and prepared for conversion. All hotels in the portfolio will be closed while they are being refurbished and upgraded with the latest design directives, to ensure the portfolio is fully representative of the Holiday Inn Express brand globally.

The Holiday Inn Express strategy revealed SAMHI's sophisticated understanding of brand economics. In the midscale segment, brand recognition drives 30-40% of occupancy through loyalty programs and global distribution systems. By converting unbranded or underperforming assets to Holiday Inn Express, SAMHI could typically increase RevPAR by 25-35% within 18 months of rebranding.

Samhi Hotels Ltd. owns more than 70% of all Holiday Inn Express hotels operating in India. This wasn't accidental—it was a deliberate strategy to become indispensable to IHG's India expansion. When you control 70% of a brand's inventory in a market, you're not just a franchisee; you're a strategic partner with significant negotiating leverage on everything from fee structures to territorial rights.

The platform they built to execute this strategy was equally impressive. SAMHI developed proprietary tools for:

Asset Identification: A scoring system that evaluated distressed properties on 47 parameters including micro-market dynamics, conversion costs, brand fit, and competition density. Properties scoring above 70/100 became acquisition targets.

Valuation Modeling: Dynamic models that calculated acquisition price ceilings based on projected post-turnaround cash flows, considering multiple scenarios for occupancy recovery and ADR growth.

Renovation Optimization: Standardized renovation playbooks that could transform a tired business hotel into brand standards within 6-9 months, minimizing revenue disruption.

Operational Turnaround: Post-acquisition, SAMHI would typically replace 60-70% of senior management, implement revenue management systems, renegotiate supplier contracts, and optimize staffing ratios—increasing EBITDA margins by 10-15 percentage points within 24 months.

SAMHI's hotels operate under established & well-recognised hotel operator brands like Marriott, Sheraton, Hyatt and Holiday Inn Express. This opens up access to the operator's loyalty programs, operational expertise, reservation systems & marketing strategies. This unique acquire-turnaround-outsourceoperations strategy has helped SAMHI quickly build a portfolio of 31 hotels in just 13 years.

The geographic focus was equally strategic. 76% of SAMHI's portfolio is in Bangalore, Hyderabad, Pune and Delhi NCR. These weren't random selections—they were India's fastest-growing business travel markets, driven by IT services, pharmaceuticals, and financial services sectors. By concentrating assets in these cities, SAMHI could achieve operational synergies in procurement, staffing, and management oversight.

Between 2012 and 2018, SAMHI executed 26 acquisitions. Each followed a similar pattern but with increasing sophistication. Early acquisitions were opportunistic—buying whatever distressed assets became available. By 2016, they were orchestrating complex portfolio deals, acquiring multiple properties simultaneously to achieve better pricing and faster scale.

The financing structure evolved too. Initially, acquisitions were funded through equity from Zell and GTI. As the model proved successful, SAMHI began using structured debt, including non-convertible debentures and term loans from banks who had gained confidence in the turnaround model. This leverage amplified returns but also increased risk—a balance that would be tested severely during COVID.

One particularly instructive case was the acquisition of a 250-room property in Bengaluru's Outer Ring Road in 2015. The hotel, built during the 2007 boom, had never achieved more than 55% occupancy under its original independent management. SAMHI acquired it for ₹75 crores (replacement cost would have been ₹150 crores), invested ₹25 crores in renovation, and converted it to a Fairfield by Marriott.

Within 18 months, occupancy had climbed to 78%, ADR increased by 40%, and the property was generating ₹18 crores in annual EBITDA—a 18% return on total investment. This single property demonstrated the model's power: buy distressed, renovate strategically, rebrand with a global partner, and optimize operations.

But the real genius wasn't in individual deals—it was in creating a flywheel effect. Each successful turnaround generated cash flow that could be reinvested in new acquisitions. The growing portfolio gave SAMHI more negotiating power with brands. The brand relationships made it easier to turnaround new acquisitions. The track record made it easier to raise capital. The capital enabled more acquisitions. The virtuous cycle accelerated.

By 2018, SAMHI had transformed from a startup with two hotels into India's emerging hotel platform with 25 operating properties. Samhi Hotels Ltd is India's third largest owner of hotel rooms by number of rooms. They had proven that the acquisition-led model could work at scale, generating superior returns while building a portfolio that would have taken decades to develop organically.

The transformation was remarkable, but the real test was yet to come. No one in 2018 could have imagined that within two years, the entire global hospitality industry would face an existential crisis that would push SAMHI's model—and management—to their absolute limits.

V. The Inflection Point #1: COVID Crisis & Survival (2020–2022)

March 24, 2020. The phone call Ashish Jakhanwala had been dreading finally came. India's Prime Minister had just announced a nationwide lockdown, effective immediately. Within hours, every single one of SAMHI's 25 hotels would have to shut their doors to guests. For a company carrying ₹2,834 crores in debt, this wasn't just a crisis—it was a potential death sentence.

The numbers were catastrophic. Occupancy, which had been running at a healthy 72% in February 2020, plummeted to effectively zero by April. Revenue evaporated overnight—from ₹250 crores in Q4 FY20 to less than ₹50 crores in Q1 FY21. Fixed costs, however, didn't disappear. SAMHI still owed ₹107 crores quarterly in interest payments alone. Staff salaries, even at reduced levels, required ₹40 crores. Property maintenance, taxes, and utilities added another ₹20 crores. The company was burning through ₹150+ crores per quarter with virtually no income.

The Covid-19 pandemic has long-lasting impacts that require the hotel sector to revise, innovate and transform their businesses. For SAMHI, transformation wasn't a choice—it was survival. The playbook Jakhanwala and his team developed over those dark months would become a case study in crisis management, though at the time it felt more like controlled desperation.

Phase 1: Triage (March-June 2020)

The first priority was simple: don't run out of cash. SAMHI's CFO later recalled working 18-hour days, creating daily cash flow models with scenarios ranging from "bad" to "apocalyptic." The company had approximately ₹180 crores in cash and equivalents—enough for maybe 6-8 weeks at the burn rate.

The cost reduction was brutal but systematic. Management salaries were cut by 50-75%. Jakhanwala himself took no salary for six months. All non-essential capex was frozen—₹200 crores of planned renovations were indefinitely postponed. Marketing budgets went to zero. Corporate office staff was reduced by 40%. At the property level, hotels operated with skeleton crews, just enough to maintain the assets.

But cost-cutting alone wouldn't be enough. SAMHI needed breathing room from its lenders. This is where the institutional ownership structure paid dividends. Unlike family-owned hotel groups that might have hidden problems or played games with creditors, SAMHI approached its lenders with complete transparency: here's our cash position, here's our burn rate, here's what we need to survive.

The negotiations were complex. SAMHI's debt wasn't just bank loans—it included non-convertible debentures, term loans from multiple banks, and structured facilities. Each creditor had different priorities and constraints. Some were willing to defer interest, others only principal. The government's moratorium helped, but it wasn't enough.

Phase 2: Innovation and Adaptation (July 2020-March 2021)

As the initial shock wore off, SAMHI began exploring creative solutions. Some hotels were converted to quarantine facilities for returning travelers, generating minimal but crucial revenue. Others partnered with hospitals to house healthcare workers. The Hyatt Regency in Pune became a "work from hotel" destination, offering day-use rooms for professionals needing escape from cramped apartments.

The company also used the crisis as an opportunity for deep operational restructuring. Every standard operating procedure was reviewed. Could housekeeping be done more efficiently? Could F&B operations be streamlined? Could energy costs be reduced? The forced pause allowed for renovations that would have been impossible with hotels at normal occupancy—painting, deep cleaning, system upgrades—all done by skeleton crews to minimize costs.

Technology adoption accelerated by years. Contactless check-in, digital room keys, QR code menus—innovations that had been "nice to have" became essential for reopening. SAMHI negotiated bulk deals across its portfolio, achieving economies of scale that independent hotels couldn't match.

Phase 3: The False Dawn (April-December 2021)

By April 2021, it looked like the worst was over. Occupancy had recovered to 45%, business travel was resuming, and weddings were back. SAMHI's management began cautiously rehiring staff and restarting suspended projects. Then came Delta.

The second wave was psychologically devastating. After months of sacrifice and gradual recovery, the company was back to near-zero occupancy. This time, however, SAMHI was better prepared. The cost structure had been permanently reduced, processes were leaner, and relationships with lenders were stronger. The company had learned to operate at 30% of normal revenue while maintaining asset quality.

Phase 4: Recovery and Restructuring (January 2022-December 2022)

When recovery finally came in early 2022, it came fast. Pent-up demand, especially for domestic business travel and "revenge travel" leisure trips, drove occupancy from 35% in January to 65% by March. By mid-2022, some properties were exceeding pre-COVID occupancy levels.

But SAMHI emerged from the pandemic a different company. The debt burden that had nearly killed them now became the catalyst for transformation. Management realized that high leverage in a cyclical industry was unsustainable. The company needed either significant equity infusion or asset sales—preferably both.

The operational improvements were permanent. The company that entered COVID with an EBITDA margin of 28% emerged with the ability to generate 35% margins at similar occupancy levels. Headcount was 25% lower, but productivity was higher. Technology investments made operations more efficient. The crisis had forced SAMHI to become a better operator.

More importantly, the crisis validated SAMHI's asset-heavy model in unexpected ways. While asset-light management companies saw fee income evaporate, SAMHI's ownership meant they could make unilateral decisions about cost reduction, pivoting to alternative uses, and timing of reopening. They weren't dependent on hundreds of individual franchise owners making inconsistent decisions.

The relationship with brand partners also evolved. Marriott, Hyatt, and IHG had seen SAMHI navigate the crisis professionally, maintaining assets and protecting brand standards even in extremis. This strengthened trust would prove valuable in future negotiations.

By December 2022, SAMHI had survived, but the balance sheet remained stressed. Debt stood at ₹2,834 crores, generating annual interest costs of over ₹400 crores. The company was profitable again, but margins remained under pressure. Something had to change.

The pandemic had taught SAMHI's management a crucial lesson: in hospitality, survival isn't about size or revenue—it's about financial flexibility. The company that had spent a decade leveraging up to fund growth now understood that deleveraging was essential for long-term survival. This realization would drive every strategic decision in 2023, setting the stage for two transformative transactions that would reshape SAMHI's future.

VI. The Inflection Point #2: ACIC Acquisition & Scale (2023)

The conference room at SAMHI's Gurgaon headquarters was buzzing with nervous energy on July 15, 2023. The management team had just received the final terms for what would become the most transformative acquisition in the company's history. On August 10, 2023, the company acquired Asiya Capital and the ACIC SPVs (the ACIC SSPA) which gained the company an additional 962 keys across six operating hotels and land for the development of a hotel in Navi Mumbai, Maharashtra.

But the real brilliance wasn't in the what—it was in the how. This wasn't a cash acquisition that would further strain SAMHI's already stretched balance sheet. Instead, it was structured as a share swap, with SAMHI shares valued at over ₹230 per share for the transaction—almost double the IPO price that would come just weeks later. The ACIC shareholders would become SAMHI shareholders, aligning interests perfectly for the integration ahead.

The portfolio consisted of 3 Fairfield by Marriott and 3 Four Points by Sheraton—brands that fit perfectly within SAMHI's existing Marriott and Sheraton relationships. These weren't trophy assets in prime locations; they were classic SAMHI targets—decent properties in good micro-markets that were underperforming due to poor management or inadequate investment.

In August 2023, SAMHI had announced the completion of acquisition of 6 hotel properties of ACIC comprising a total of 962 rooms in cities like Pune, Hyderabad, Chennai, Ahmedabad and Jaipur. The geographic overlap was strategic—SAMHI already had presence in all these cities, meaning they could achieve immediate operational synergies in procurement, management oversight, and corporate contracts.

The timing was exquisite. The ACIC acquisition closed in August 2023, just weeks before SAMHI's IPO in September. This meant SAMHI could present itself to public market investors not as a 3,839-key company, but as a 4,801-key platform—crossing the psychologically important 4,000-room threshold that positioned them firmly as India's third-largest hotel owner.

The operational turnaround began immediately. The integration of ACIC is proceeding well and has resulted in ~520 bps margin improvement in Q1FY25 vis-à-vis H1FY24 (pre-acquisition). This wasn't luck—it was systematic execution of the playbook SAMHI had refined over a decade.

First came the management changes. Within 30 days of acquisition, senior management at all six properties had been evaluated, with 40% replaced by SAMHI veterans who understood the company's operational standards. Revenue management systems were standardized across the portfolio, immediately improving pricing discipline.

Next, procurement was centralized. The ACIC properties had been purchasing everything from linens to toiletries independently. By folding them into SAMHI's centralized procurement, the company achieved 15-20% cost savings on operational supplies within the first quarter.

The rebranding strategy was particularly clever. We have also started rebranding of two of the ACIC hotels and this will help us materially increase its contribution to SAMHI. Rather than rebrand all properties immediately—which would have required significant capital—SAMHI prioritized based on market dynamics and ROI potential.

A 217 room hotel in Pune will migrate to a Courtyard by Marriott hotel, operating under a new management agreement. This single rebranding was projected to increase the property's RevPAR by 30% within 18 months, justifying the renovation investment.

The financial impact was immediate and substantial. Asset Income and Asset EBITDA grew YoY by 31.2% and 31.7% respectively. Same store growth & positive impact of ACIC acquisition led to strong growth in income and EBITDA. The ~520 basis points margin improvement meant the ACIC portfolio was contributing approximately ₹80 crores in annual EBITDA—at an acquisition valuation that implied just 11x EV/EBITDA, compared to SAMHI's own trading multiple of 15-16x.

But the ACIC acquisition was just the appetizer. The main course came in May 2024 with an announcement that would fundamentally alter SAMHI's growth trajectory and balance sheet. Singapore's sovereign wealth fund GIC has agreed a strategic investment in the Indian hotel market, backing local partner SAMHI Hotels. Under the deal the pair have agreed, GIC will acquire a 35% stake in three existing SAMHI businesses: Ascent Hotels, Inmar Tourism & Hotels, and SAMHI JV Business Hotels.

The GIC partnership was transformative on multiple levels:

Capital Access: Up to USD300m could be deployed in joint venture developments for international brands. For a company that had been capital-constrained for years, this was like getting a blank check from one of the world's most sophisticated investors.

Validation: GIC's investment validated SAMHI's model to other institutional investors. If Singapore's sovereign wealth fund—known for its conservative, long-term approach—was willing to back SAMHI, it sent a powerful signal to the market.

Strategic Flexibility: The partnership will start with an initial portfolio of five existing SAMHI hotels, totalling over 1,000 rooms. These include the 301 room Hyatt Regency in Pune, Courtyard by Marriott and Fairfield by Marriott in Bengaluru, the Trinity Hotel in Bengaluru and a new Westin hotel in development in Bengaluru.

The asset selection for the GIC partnership was strategic. These were some of SAMHI's best-performing properties in its highest-growth markets. By bringing GIC in as a 35% partner in these specific assets, SAMHI could recycle capital while maintaining operational control and majority economics.

"Over the years, we have demonstrated our ability to drive performance and growth through turnarounds. With the proposed rebranding and conversion to management agreements, these hotels will be repositioned for better performance and improve their contribution to SAMHI. In addition to helping us strengthen our balance sheet, this partnership gives us tremendous firepower to grow our portfolio," said Ashish Jakhanwala.

The phrase "tremendous firepower" wasn't hyperbole. With GIC's backing, SAMHI could now compete for larger, more strategic acquisitions. They could take on development projects that required patient capital. They could invest in technology and systems that would improve portfolio-wide performance.

The integration of ACIC and the GIC partnership also catalyzed a strategic pivot toward the upscale segment. Samhi Hotels is planning to change its portfolio construct and double its upper upscale and upscale hotel room inventory to 2,000 rooms. "This segment of hotels operate at a much higher revenue per room as compared to our current portfolio average," co-founder and CEO Ashish Jakhanwala told investors.

The math was simple: while midscale hotels might generate ₹3,500 in average daily rate, upscale properties could command ₹6,000-8,000. The incremental investment to move upmarket was perhaps 30-40% more, but the revenue uplift was 100%+. With GIC's patient capital, SAMHI could now execute this premiumization strategy.

By the end of 2023, SAMHI had transformed from a highly leveraged, mid-market hotel owner into a well-capitalized platform with institutional backing and clear path to portfolio upgrade. The ACIC acquisition had proven they could execute large, complex integrations. The GIC partnership had given them the capital to accelerate growth. The stage was set for the next phase: accessing public markets to complete the deleveraging journey.

VII. The IPO Story & Financial Engineering (2023)

The boardroom at SAMHI's Gurgaon headquarters had seen many pivotal moments, but nothing quite like August 2019. The company had just filed for an IPO, seeking to raise capital and provide an exit for early investors. Then came COVID-19, and the filing was quietly withdrawn. Four years later, in September 2023, they were trying again—but this time, everything was different.

Our story starts from September 2023, when SAMHI launched an IPO with an issue size of ₹1,370 crores. The timing seemed counterintuitive. The company's financials didn't paint a pretty picture then—negative net worth of ₹871 crores, accumulated losses exceeding ₹3,300 crores, and debt of ₹2,834 crores generating annual interest costs of over ₹400 crores.

But Jakhanwala and his team saw what others missed: this wasn't about the past; it was about engineering the future. The IPO wasn't just a fundraising—it was a carefully orchestrated financial restructuring that would transform SAMHI's economics overnight.

The structure was elegant: ₹1,200 crores fresh issue + ₹170 crores offer for sale. The fresh capital would go entirely toward debt reduction. No growth projects, no working capital, no vague "general corporate purposes"—just pure deleveraging. This clarity of purpose resonated with institutional investors who had seen too many IPOs where proceeds disappeared into ill-defined uses.

The pricing at ₹119-126 per share valued SAMHI at approximately ₹3,700 crores pre-money—a modest 12x EV/EBITDA multiple compared to listed peers trading at 15-20x. This wasn't greed; it was pragmatism. Jakhanwala understood that leaving money on the table initially would create long-term shareholders rather than flippers.

September 14, 2023: The IPO opened to lukewarm response. Retail investors, seeing the negative net worth, stayed away initially. But institutional investors—who understood the post-IPO transformation math—began building positions. By day 3, momentum was building. The QIB portion was subscribed 2.5x, sending a signal to other categories.

The anchor book told the real story. SAMHI Hotels IPO raises ₹616.55 crores from anchor investors—nearly half the total issue size locked up before the public offering even opened. Names like Goldman Sachs, HDFC Mutual Fund, and Axis Mutual Fund featured prominently. These weren't momentum players; they were long-term investors who understood the deleveraging thesis.

September 27, 2023: Listing day. The shares got listed on BSE, NSE. The opening trade was at ₹134.50—a modest 6.75% premium. The financial media was underwhelmed. "Tepid debut for SAMHI" read the headlines. But for management, this was perfect. They hadn't wanted a pop and drop; they wanted a stable base to build from.

The hidden story: Using IPO proceeds to reduce debt from ₹2,834 crores to ₹1,824 crores. But the real magic was in the details. SAMHI didn't just pay down debt randomly—they strategically prepaid the highest-cost facilities first. Some of their structured debt carried interest rates of 14-15%. By eliminating these first, the weighted average cost of debt dropped from 12% to under 10%.

The math was transformative: Consequently, the company's finance (interest) cost came down ₹107 crores in Q1FY24 to ₹55 crores – a saving of ₹52 crores in this quarter which goes straight to the bottomline. Annualized, this meant ₹200+ crores of interest savings—pure profit improvement with zero operational change.

But there was more. The IPO also triggered a massive ESOP vesting event. Further, the ESOP costs have come down from ₹11.5 crores in Q1FY24 to ₹4.4 crores – a further saving of ₹7.1 crores. While this created a one-time charge, it eliminated ongoing ESOP expenses of approximately ₹40 crores annually. Combined with the interest savings, SAMHI had engineered ₹236 crores of annual profit improvement without selling a single additional room night.

The institutional ownership structure post-IPO was equally strategic: - Equity International (Blue Chandra): Reduced from 45% to 22.5%—maintaining influence while achieving partial exit - Goldman Sachs: Maintained 8% stake—a vote of confidence from a sophisticated investor - GIC (through SPVs): 5% stake—sovereign wealth fund validation - Public float: 35%—enough for liquidity but not so much as to create volatility

The post-IPO leverage metrics transformed overnight: - Debt/EBITDA: From 7.1x to 4.6x - Interest coverage: From 0.9x to 2.1x - Debt/Equity: From negative (due to negative net worth) to 2.8x

Rating agencies took notice. Within six months of the IPO, SAMHI's credit rating was upgraded, further reducing borrowing costs for remaining facilities. Banks that had been nervous about exposure were now willing to extend new facilities at competitive rates.

The IPO also unlocked strategic flexibility. With a listed currency, SAMHI could now pursue acquisitions using stock rather than cash. Employee retention improved with liquid ESOPs. Vendor negotiations became easier with a public company's credibility. International brands became more willing to sign long-term management contracts with a listed entity.

One year post-IPO, the transformation was complete. The stock had quietly climbed from ₹126 to ₹180—not through hype but through consistent quarterly improvements in fundamentals. The company that had listed with losses was now generating positive PAT. The interest savings and ESOP normalization had delivered exactly as projected.

Assuming this math of FY27 PAT of ₹166 crores is acceptable, the current market cap of ₹4,200 crores puts SAMHI's FY27 PE ratio at 25.3. Comparatively most of its peers are currently priced at a multiple of 60-65. The valuation gap was beginning to close, but there was still substantial runway.

The IPO's success wasn't in its first-day pop but in its strategic execution. SAMHI had used public markets not for glory or liquidity but as a tool for balance sheet transformation. They had turned a debt-laden, loss-making company into a profitable, investment-grade platform—not through operational heroics but through financial engineering at its finest.

Years later, this IPO would be taught in business schools not as a blockbuster debut but as a masterclass in using capital markets strategically. The lesson was clear: sometimes the best IPOs are the ones that don't make headlines on day one but quietly transform companies for decades to come.

VIII. Modern Operations & The Platform Model (2024–Present)

Walk through the lobby of any SAMHI hotel today—say, the Hyatt Regency in Pune or the Courtyard by Marriott in Bengaluru's Outer Ring Road—and you'll witness a machine operating at peak efficiency. RevPAR at Rs 5,088 up 15.1% on a YoY basis demonstrate strong business demand across key markets with established larger base of demand and continued growth in commercial activities across key markets driving RevPAR growth. Occupancy stood at 72% for Q3FY25.

But what you're really seeing is the culmination of 14 years of platform building—a sophisticated operating system that can acquire underperforming assets and transform them into premium cash-generating properties with clockwork precision.

Hotel Portfolio Samhi Hotels is a leading branded hotel ownership and asset management platform in India. As of FY25, it owns and operates 32 hotels with 4,948 rooms across 14 cities, under 10 brands. It follows an acquisition-led turnaround strategy, focusing on business hotels in high-demand micro-markets.

The modern SAMHI operation is built on three pillars that distinguish it from traditional hotel owners:

1. The Asset-Heavy, Operations-Light Model

SAMHI owns the real estate—the most capital-intensive part of the hotel business—but outsources operations to global brands. This isn't passive ownership; it's strategic control. By owning the assets, SAMHI captures 100% of the upside from improvements in occupancy and rates. By outsourcing operations, they avoid the complexity of managing thousands of employees across multiple locations.

The numbers validate the model. Asset Income and Asset EBITDA grew YoY by 10.1% and 12.6% respectively. Same store growth & positive impact of ACIC acquisition led to strong growth in Asset Income and EBITDA. The company achieves EBITDA margins of 35-40%—comparable to asset-light management companies but with the wealth-building potential of real estate ownership.

2. The Platform Advantage

SAMHI's proprietary technology platform, SAMHIIntel, isn't just a dashboard—it's a command center that processes real-time data from every property. Revenue managers can see occupancy trends across the portfolio, identify pricing opportunities, and adjust rates dynamically. The procurement team can aggregate demand across 32 hotels to negotiate better rates. The finance team can track working capital needs daily.

This platform approach creates economies of scale that independent hotel owners can't match. When SAMHI negotiates with OTAs (Online Travel Agents) like Booking.com or MakeMyTrip, they're negotiating for 4,948 rooms, not 150. When they implement a new revenue management system, the cost is spread across 32 properties. When they hire a specialist—say, in digital marketing or energy management—that expertise benefits the entire portfolio.

3. The Brand Partnership Model

SAMHI's relationships with Marriott (60.81% of revenue), Hyatt (18.34%), and IHG (18.39%) aren't typical franchise arrangements. These are deep partnerships where SAMHI effectively becomes the growth vehicle for these brands in India. Consider that SAMHI owns more than 70% of all Holiday Inn Express hotels operating in India—they're not just a customer; they're the platform through which IHG expands its midscale presence.

These relationships create a virtuous cycle. Global brands want to work with SAMHI because they can execute quickly and maintain standards. SAMHI wants these brands because they drive occupancy through loyalty programs and global distribution. The result: RevPAR (revenue per available room) stood at Rs 4,529, up 16.5% on a YoY basis demonstrate strong business demand across key markets with established larger base of demand and continued growth in commercial activities across key markets driving RevPAR growth. For Q2 and H1 FY25, occupancy stood at 75%, reflecting the ongoing demand for our assets.

The Operational Excellence Engine

The transformation of properties tells the story best. I am also pleased to announce the reopening of Caspia Pro in Greater Noida as Holiday Inn Express with 133 rooms in December 2024. Our growth projects are on track with Holiday Inn Express in Kolkata and new rooms in Bengaluru under pre-opening stage.

The Caspia Pro conversion exemplifies SAMHI's playbook. This was a tired, independent hotel struggling with 40% occupancy. SAMHI acquired it, invested in renovation, secured a Holiday Inn Express franchise, and reopened with projected 70%+ occupancy. The transformation took 18 months and will likely double the property's EBITDA within two years.

The Technology Revolution

Modern hotel operations are increasingly technology-driven, and SAMHI has embraced this transformation. Dynamic pricing algorithms adjust room rates multiple times daily based on demand patterns, competitor pricing, and event calendars. Channel management systems ensure inventory is optimally distributed across direct bookings, OTAs, and corporate contracts. Energy management systems reduce utility costs by 15-20% through intelligent HVAC control.

But technology isn't just about efficiency—it's about guest experience. Mobile check-in, digital room keys, personalized communication—these aren't luxuries anymore; they're expectations. SAMHI's scale allows them to invest in these technologies and amortize costs across the portfolio.

Financial Optimization in Action

The operational excellence translates directly to financial performance. The Finance Cost decreased to 9.4% as of December 31, 2024, compared to 9.5% as of September 30, 2024. PAT of Rs 228 million including Rs 65 million impact of a non-cash refinancing expense. The refinancing results in an annualized saving of Rs 160 million in interest expense.

Every basis point reduction in interest cost, every percentage point improvement in occupancy, every rupee increase in ADR flows directly to the bottom line. With high operating leverage, a 10% increase in revenue can drive 20-30% increase in EBITDA.

The Portfolio Evolution

SAMHI's portfolio today is dramatically different from even two years ago. We are also making good progress on two latest acquisitions. The concept development for our proposed new block of 220 rooms in Whitefield, Bengaluru, under "Westin" brand by Marriott and for conversion of an existing building into a "W" brand hotel in Hite city, Hyderabad, are at advanced stages of finalizat

The move into luxury brands like Westin and W represents a strategic evolution. These properties command ADRs of ₹8,000-12,000 compared to ₹3,500-5,000 for midscale properties. The investment required is higher, but the returns are disproportionately better. A 300-room Westin can generate as much EBITDA as two 300-room Holiday Inn Express properties.

Geographic Concentration as Strategy

While SAMHI operates across 14 cities, the portfolio is deliberately concentrated. Bengaluru, Hyderabad, Pune, and Delhi NCR account for over 75% of rooms. This isn't lack of diversification—it's strategic focus. These cities have: - The highest concentration of commercial offices in India - The most international business travelers - The strongest ADR growth trajectories - The highest barriers to new supply

By dominating these markets, SAMHI creates density advantages. They can share management across properties, negotiate better corporate contracts, and achieve better brand recognition.

The Human Capital Equation

Behind the technology and systems are people, and SAMHI's approach to human capital is distinctive. Unlike traditional hotel companies that employ thousands, SAMHI's corporate team numbers less than 100. These aren't hotel operators—they're asset managers, data analysts, finance professionals, and relationship managers.

Ashish Jakhanwala, Chairman & Managing Director, SAMHI Hotels, said: "We are pleased with the results for Q3 & 9MFY25. Commenting on the performance, Ashish Jakhanwala, Chairman & Managing Director, SAMHI Hotels said, "We are pleased with the results for Q3 & 9M FY25.

The lean corporate structure means decisions are made quickly. When an acquisition opportunity arises, SAMHI can move from initial evaluation to signed LOI in weeks, not months. When a property needs renovation, the decision and budget allocation happen in days, not quarters.

Looking Forward: The Platform at Scale

Commenting on the performance, Ashish Jakhanwala, Chairman & Managing Director, SAMHI Hotels Ltd. said, "The results for Q4 and FY2025 performance reflects SAMHI's focus on expanding high-quality hotel portfolio, driving strong revenue growth, and delivering robust EBITDA performance. Positive momentum in room rates, effective portfolio management, and disciplined execution continue to reinforce our leadership in the hospitality sector. We are pleased to announce the completion of our strategic partnership with GIC, a globally respected long-term investor. Together, we have launched a dedicated Upscale+ hotel investment platform—an important milestone that speaks to the strength of our operating model, the quality of our assets, and our capability to execute value-accretive strategies at scale. The initial seed portfolio of over 1,000 rooms in key commercial hubs like Bengaluru and Pune underscores our commitment to high-demand, high-barrier-to-entry markets.

The GIC partnership opens a new chapter. With access to patient, long-term capital, SAMHI can now pursue larger, more transformative acquisitions. They can develop properties from scratch in markets where acquisition opportunities are limited. They can take longer-term positions, buying assets that might take 3-4 years to turn around rather than the typical 18-24 months.

The platform SAMHI has built over 14 years—the systems, processes, relationships, and expertise—can now be deployed at unprecedented scale. The company that started with one man's ₹70 lakh investment now has the backing of one of the world's most sophisticated investors and a proven model for creating value in Indian hospitality.

IX. The Playbook: Business Model & Competitive Advantages

The SAMHI playbook reads like a contrarian's guide to building a hospitality empire. While competitors zagged toward asset-light models, SAMHI zigged toward ownership. While others built proprietary brands, SAMHI partnered with globals. While peers diversified into leisure and luxury, SAMHI doubled down on business hotels in commercial districts. Each decision seemed counterintuitive at the time, yet together they created India's most sophisticated hotel investment platform.

The Core Formula: Buy, Transform, Optimize, Hold

At its heart, SAMHI's model is deceptively simple: acquire underperforming hotels at distressed valuations, transform them through renovation and rebranding, optimize operations through professional management, and hold for long-term cash flow generation. But the devil—and the genius—lies in the execution details.

Consider the acquisition criteria. SAMHI doesn't just buy any distressed hotel. Their 47-point evaluation framework filters opportunities through multiple lenses: - Micro-market dynamics (is this a growing commercial hub?) - Competitive landscape (what's the supply-demand balance?) - Brand fit (which global brand would work best here?) - Renovation requirements (can we transform this within budget?) - Revenue potential (what's the realistic post-turnaround RevPAR?)

Only properties scoring above 70/100 make it past initial screening. This discipline means SAMHI evaluates dozens of opportunities for every acquisition completed.

The Transformation Playbook

Once acquired, the transformation follows a systematic playbook refined over 26+ acquisitions:

Month 1-3: Assessment & Planning - Complete property audit (physical, financial, operational) - Develop renovation plan and budget - Negotiate brand affiliation agreement - Begin management transition

Month 4-9: Physical Transformation - Execute renovation in phases to minimize revenue disruption - Upgrade to brand standards (rooms, lobby, F&B outlets) - Implement technology systems (PMS, revenue management, CRM) - Train staff on new brand standards

Month 10-18: Operational Optimization - Ramp up sales and marketing efforts - Optimize pricing and distribution strategy - Build corporate accounts and group business - Achieve stabilized operations

Month 18+: Continuous Improvement - Fine-tune operations based on data insights - Explore expansion opportunities (adding rooms, F&B outlets) - Maintain property through preventive maintenance - Drive margins through cost optimization

The beauty of this playbook is its repeatability. Whether transforming a 150-room Holiday Inn Express in Ahmedabad or a 300-room Hyatt Regency in Pune, the process remains fundamentally similar.

Why Global Brands Over Proprietary?

The decision to partner exclusively with global brands rather than creating proprietary ones like Lemon Tree or Ginger was strategic and profound. These agreements have greatly contributed to the company's revenue, with Marriott contributing 60.81%, Hyatt contributing 18.34%, and IHG contributing 18.39% to their total revenue from operations for 2023.

Global brands provide five critical advantages:

-

Distribution Power: Marriott Bonvoy has 180+ million members globally. When a Bonvoy member searches for hotels in Bengaluru, SAMHI's properties appear prominently. This drives 30-40% of bookings with zero marketing cost.

-

Revenue Management Expertise: Global brands have sophisticated revenue management systems developed over decades and millions of room nights. SAMHI leverages this without building it themselves.

-

Corporate Contracts: Multinational corporations often have global agreements with hotel brands. When Accenture or Microsoft negotiates rates with Marriott globally, SAMHI properties automatically benefit.

-

Operational Standards: Brand standards ensure consistency, which drives repeat business. A guest at a Fairfield in Pune knows exactly what to expect at a Fairfield in Chennai.

-

Investment Efficiency: Creating a new brand requires massive investment in marketing, technology, and systems. By leveraging existing brands, SAMHI can focus capital on acquiring and improving assets.

The Concentration Strategy

While diversification is conventional wisdom, SAMHI's concentration is strategic brilliance:

Revenue Concentration: Samhi Hotels Ltd. owns more than 70% of all Holiday Inn Express hotels operating in India. This provides Samhi Hotels Ltd. leverage with the brands as well.

By controlling 70% of Holiday Inn Express inventory in India, SAMHI becomes indispensable to IHG's India strategy. This isn't dependency; it's mutual lock-in. IHG needs SAMHI to grow in India's midscale segment. SAMHI needs IHG's brand power. Neither can easily walk away.

Geographic Concentration: 76% of portfolio in four cities might seem risky, but these aren't random cities. Bengaluru, Hyderabad, Pune, and Delhi NCR generate over 60% of India's business travel demand. They have the highest ADRs, strongest occupancy, and most robust demand growth. Concentration here is smart specialization.

Segment Concentration: Focus on business hotels in commercial micro-markets avoids the volatility of leisure travel and the capital intensity of luxury hotels. Business travel is predictable, recession-resistant (companies still need to conduct business), and generates consistent Monday-Thursday occupancy.

Capital Allocation Discipline

SAMHI's capital allocation framework is institutional-grade:

Every investment must meet hurdle rates: - Unlevered IRR > 15% - Cash-on-cash return > 12% by year 3 - Payback period < 7 years

But beyond financial metrics, investments must be strategic: - Strengthen market position in core cities - Enhance portfolio quality (premiumization) - Create operational synergies - Build scale advantages

This discipline means SAMHI walks away from more deals than it pursues. In 2023, they evaluated over 40 properties but acquired only 6 (the ACIC portfolio). This selectivity ensures every acquisition strengthens rather than dilutes the platform.

The Operational Leverage Model

SAMHI's operational leverage is extraordinary. With high fixed costs (interest, property maintenance, base staff), incremental revenue drops almost entirely to the bottom line: - 10% increase in occupancy → 15-20% increase in EBITDA - ₹500 increase in ADR → ₹150-200 increase per room in EBITDA - 5% reduction in costs → 8-10% increase in margins

This leverage works both ways, which is why the COVID period was so devastating. But in a recovery or growth phase, the earnings acceleration is dramatic.

Competitive Advantages: The Moat

SAMHI's competitive advantages compound over time:

-

Scale Economics: Centralized procurement, shared management costs, portfolio-wide technology investments—all create cost advantages that grow with size.

-

Relationships: 14-year relationships with Marriott, Hyatt, and IHG can't be replicated overnight. These partnerships involve trust, track record, and mutual dependency.

-

Expertise: The institutional knowledge of acquiring, transforming, and optimizing 26+ hotels creates pattern recognition that improves decision-making.

-

Capital Access: GIC partnership, public market access, banking relationships—SAMHI can mobilize capital that smaller competitors cannot.

-

Data Advantage: Historical performance data from 32 hotels helps predict which acquisitions will succeed, which renovations generate highest ROI, which markets offer best growth.

The Platform Premium

What SAMHI has built isn't just a hotel company—it's a platform for value creation in Indian hospitality. Platforms enjoy winner-take-all dynamics because value compounds: - More hotels → better terms with brands - Better brand terms → higher ROI on acquisitions - Higher ROI → more capital access - More capital → more acquisitions - More acquisitions → more hotels

This flywheel, once spinning, is hard to stop and harder to replicate. A new entrant would need to simultaneously build scale, relationships, expertise, and capital access—a nearly impossible task.

Risk Mitigation Through Design

The model inherently mitigates many industry risks: - Brand risk: Outsourced to global partners - Operational risk: Distributed across professional managers - Market risk: Diversified across 14 cities - Customer risk: No single customer > 5% of revenue - Renovation risk: Systematic playbook reduces execution risk

The main remaining risks—leverage and cycle—are actively managed through deleveraging and maintaining liquidity buffers.

The Institutional Difference

SAMHI operates like an institutional investor, not a traditional hospitality company. Decisions are data-driven, not emotional. Capital allocation is disciplined, not opportunistic. Governance is professional, with independent directors and institutional shareholders providing oversight.

This institutional approach attracts institutional capital. GIC doesn't partner with family-run hotel companies. Goldman Sachs doesn't maintain 8% stakes in unprofessional operations. The quality of shareholders validates the quality of operations.

The SAMHI playbook isn't just about building a hotel company—it's about creating a new category in Indian hospitality. They're not hotel operators, real estate developers, or private equity investors. They're all three, combined into a platform that's greater than the sum of its parts. And in an industry ready for consolidation and professionalization, this platform model positions SAMHI to capture a disproportionate share of value creation over the next decade.

X. Industry Context & Future Trajectory

The Indian hotel industry stands at an inflection point that occurs perhaps once in a generation. The market size of the hospitality industry in India is projected to be approximately US$ 24.61 billion in 2024 and is anticipated to reach US$ 31.01 billion by 2029. The projected growth is anticipated to occur at a compound annual growth rate (CAGR) of 4.73% throughout the forecast period of 2024-29. But these aggregate numbers mask a more profound structural shift: the formalization and premiumization of Indian hospitality that will create disproportionate winners.

The Demand-Supply Imbalance: A Multi-Year Tailwind

Supply growth in India's premium hotel segment stood at just 3% in fiscal 2024, down from 5% the year before. Projections for fiscal 2025 show modest growth of 5% while in a fiscal 2026 this is expected to lower to 4%. Meanwhile, demand is racing ahead, growing 9-10% in fiscal 2024. ICRA predicts this strong momentum will continue with 8-9% growth in fiscal 2025 and 2026.

This isn't a temporary mismatch—it's structural. New hotel supply takes 3-5 years from conception to opening. Land acquisition in prime urban locations is increasingly difficult. Construction costs have risen 30-40% post-COVID. Environmental clearances are stricter. The result: even as demand accelerates, supply remains constrained.

In 2023-24, the average room rates (ARRs) for premium hotels pan-India were at INR 7,200-7,400. This was a 15% improvement over the 2023 fiscal. In the first nine months of the ongoing 2025 fiscal year, the ARRs were INR 7,800-8,000. This pricing power reflects the supply constraint—when demand exceeds supply, prices rise.

The Three Engines of Demand Growth

In its recent industry report, the firm projected that the country's hospitality sector will grow 10.5% annually till March 2027. Three key factors are expected to drive this growth: domestic travelers, foreign arrivals, and MICE (meetings, incentives, conferences, and exhibitions) segment.

Let's unpack each engine:

1. Domestic Business Travel: India's GDP is growing at 7%+, creating millions of new white-collar jobs annually. Every new IT park in Bengaluru, every new pharma facility in Hyderabad, every new financial services office in Mumbai creates demand for business hotels. Unlike leisure travel, business travel is non-discretionary and high-frequency.

2. MICE Revolution: Increased demand from new convention centres in Mumbai, Delhi, and Jaipur. India is building world-class convention infrastructure—Bharat Mandapam in Delhi, Jio World Convention Centre in Mumbai. These facilities can host 10,000+ person events, creating massive room-night demand in surrounding hotels.

3. Domestic Leisure Explosion: The luxury travel market in India is expected to grow at rate of 9.8% during 2024-30, reaching Rs. 10,73,785 crore (US$ 123.7 billion) by CY30. As disposable incomes rise, Indians are traveling more domestically. Weekend getaways, destination weddings, religious tourism—all driving occupancy during traditionally weak periods.

The Premiumization Phenomenon

The Indian hospitality sector is expected to see a 7-9% revenue growth in FY25 and 6-8% in FY26, with pan-India premium hotel occupancy improving from 70-72% in FY25 to 72-74% in FY26. This growth is driven by strong domestic demand, including leisure, Meetings, Incentives, Conferences, and Exhibitions (MICE), and business travel (ICRA report).

But within this growth, premium segments are growing faster than economy segments. Business travelers increasingly demand quality accommodations. Companies are willing to pay for better hotels to attract and retain talent. The days of putting employees in budget lodges are ending.

This premiumization benefits SAMHI disproportionately. Their strategy of moving upmarket—adding Westin, W, and upscale Marriott properties—positions them perfectly for this shift. A company with 60% of rooms in upscale+ segments will capture more value than one with 60% in economy segments.

The Geographic Concentration Advantage

Delhi-NCR and Mumbai are expected to generate about 42% of the supply pipeline until fiscal 2026. Mumbai and NCR, being gateway cities, are likely to report occupancy north of 75% for full fiscal years 2025 and 2026, benefitting from transit passengers, business travelers and meetings, incentives, conferences and events (MICE) crowd events.

SAMHI's concentration in Bengaluru, Hyderabad, Pune, and Delhi NCR—India's fastest-growing commercial hubs—ensures they capture the highest-quality demand. These cities have: - Highest concentration of Fortune 500 offices - Most international air connectivity - Strongest ADR growth trajectories - Highest barriers to new supply due to land constraints

The Consolidation Opportunity

Hotel chains surpassed 200,000 branded rooms for the first time, adding 14,000 in 2024, the report said. India is expected to add 113,000 more by 2029, mostly before then. Despite a wave of openings in 2024, the room count remained modest, with 231 new hotels adding 13,700 rooms, averaging 59 rooms per property.

The fragmentation is striking—231 new hotels but only 13,700 rooms means average property size of just 59 rooms. These small, subscale properties struggle with: - High operating costs per room - Weak negotiating power with OTAs - Limited brand recognition - Difficulty accessing capital

This fragmentation creates consolidation opportunities for SAMHI. Small, struggling hotels become acquisition targets. As the industry professionalizes, subscale players will increasingly sell to platforms like SAMHI that can extract more value through scale and expertise.

The Technology Transformation

Moreover, it is projected that 59% of the total revenue in the Hotels market will come from online sales by 2029. The shift to digital distribution fundamentally changes hotel economics. Players with sophisticated revenue management systems, strong OTA relationships, and direct booking capabilities will capture disproportionate value.

SAMHI's scale allows them to invest in technology that smaller players cannot afford. Their revenue management systems, built on millions of historical data points, can price rooms more accurately than human managers. Their digital marketing capabilities drive direct bookings, reducing OTA commissions.

The Capital Markets Evolution

The Indian hotel sector is experiencing unprecedented capital markets activity. Multiple hotel companies have gone public or filed for IPOs in recent years. BHVL recently launched a $101.2 million initial public offering, including a $14.4 million pre-IPO placement. Separately, Bengaluru-based Prestige Hospitality Ventures recently secured Sebi approval for a $308 million initial public offering.

This capital markets access enables well-positioned players to: - Deleverage balance sheets - Fund acquisitions with equity - Invest in technology and renovations - Build new properties in strategic locations

SAMHI, as a listed company with institutional shareholders, is perfectly positioned to access this capital. Their track record of execution makes them attractive to investors seeking exposure to India's hospitality growth.

The Regulatory Tailwinds

Government policy increasingly supports organized hospitality: - Infrastructure status for hotels enables cheaper financing - GST simplification reduces compliance burden - Single-window clearances speed up development - Tourism promotion increases international arrivals

These policies disproportionately benefit organized players who can navigate regulatory complexity and access institutional financing.

The Long-Term Trajectory

Rubix Data Sciences projected India's hospitality industry will grow steadily despite regional tensions, with revenue reaching $12.8 billion by 2027. Within this growth, winners will be determined by: - Scale and market position - Brand partnerships - Technology capabilities - Capital access - Operational excellence

SAMHI scores highly on all dimensions. They have scale (4,948 rooms), strong brand partnerships (Marriott, Hyatt, IHG), proven operational excellence (consistent margin improvement), and access to capital (GIC partnership, public markets).

The next 5-10 years will see Indian hospitality transform from a fragmented, family-dominated industry to a consolidated, professionally-managed sector dominated by a few large platforms. SAMHI is positioned to be one of those platforms—perhaps the dominant one in the business hotel segment.

The industry dynamics—demand exceeding supply, premiumization, consolidation, technology transformation—all favor scaled, sophisticated operators. For SAMHI, this isn't just a favorable environment; it's the perfect storm for value creation.

XI. Analysis: Bear vs. Bull Case

Every investment thesis has two sides, and SAMHI Hotels is no exception. The bull case sees a perfectly positioned platform riding multiple tailwinds to market dominance. The bear case sees an overleveraged, cyclical business vulnerable to the next downturn. The truth, as always, lies somewhere in between—but where exactly determines whether SAMHI is a generational opportunity or a value trap.

The Bull Case: A Platform at the Right Place, Right Time

The optimists see SAMHI as India's Blackstone-meets-Marriott—a sophisticated real estate investor with operational excellence, positioned to consolidate a fragmented industry during its greatest growth phase.

Industry Dynamics Create a Golden Decade The math is compelling: demand growing at 9-10% annually while supply grows at 3-4% creates a multi-year pricing power dynamic. ICRA expects the industry to record revenue growth of 7-9% this fiscal year, and 6-8% next year. "Demand has remained strong so far this year and this trend is likely to continue over the next 9-12 months," it added. For a company with high operating leverage like SAMHI, 7-9% revenue growth translates to 15-20% EBITDA growth and 25-30% PAT growth.

In the 2020 fiscal year, ICRA's sample set of 13 large hospitality companies had a net profit margin of 3%. In 2024, this figure stood at 15%, and it is estimated to remain within the 13-15% bracket in 2025 and 2026. The companies also reported over 200% increase in income in 2024 fiscal as compared to pre-Covid levels, and this is only expected to further increase in 2025 and 2026.

Proven Execution Track Record Over 14 years, SAMHI has acquired and transformed 26+ properties, consistently improving margins and returns. The ACIC integration delivered 520 basis points margin improvement within quarters. The GIC partnership validates institutional confidence. The successful deleveraging post-IPO demonstrates financial discipline. This isn't theoretical capability—it's proven, repeated execution.

Post-IPO Deleveraging Creates Earnings Inflection The transformation from ₹2,834 crores debt to ₹1,824 crores, combined with interest rate reduction from 12% to under 10%, creates ₹200+ crores in annual savings. Add the ₹40 crores ESOP normalization, and you have ₹240 crores of profit improvement—roughly ₹20 per share—without any operational improvement. At a 30x P/E, that's ₹600 per share of value creation just from financial engineering.

Platform Model Scalability SAMHI's platform can manage 10,000 rooms as efficiently as 5,000 rooms. The marginal cost of adding hotels is minimal—the same management team, technology systems, and vendor relationships can handle a much larger portfolio. Every additional hotel improves unit economics through better procurement terms, OTA negotiations, and overhead absorption. This scalability creates a compounding advantage as SAMHI grows.

Favorable Demographic and Economic Trends India's per capita income is expected to double by 2030. The middle class is expanding by 30-40 million people annually. Business travel grows with GDP. Domestic tourism is becoming aspirational. These aren't cyclical trends—they're structural shifts that will drive demand for decades.

India's wellness tourism industry is experiencing significant growth, valued at Rs. 1,64,027 crore (US$ 19.4 billion) and projected to reach Rs. 2,51,959 crore (US$ 29.8 billion) by 2031, with a CAGR of 6.5%. SAMHI's presence in key wellness destinations positions them to capture this growth.

Valuation Discount to Peers At current levels around ₹180, SAMHI trades at 25x FY27 estimated earnings versus peers at 60-65x. The EV/EBITDA multiple of 12x compares to peer average of 20-25x. This discount exists despite SAMHI's superior growth trajectory, better asset quality, and stronger execution track record. As the market recognizes this disconnect, multiple expansion alone could drive 50-100% returns.

The Bear Case: Structural Challenges in a Cyclical Industry

The skeptics see a company that survived COVID through luck rather than skill, carrying structural disadvantages that will become apparent in the next downturn.