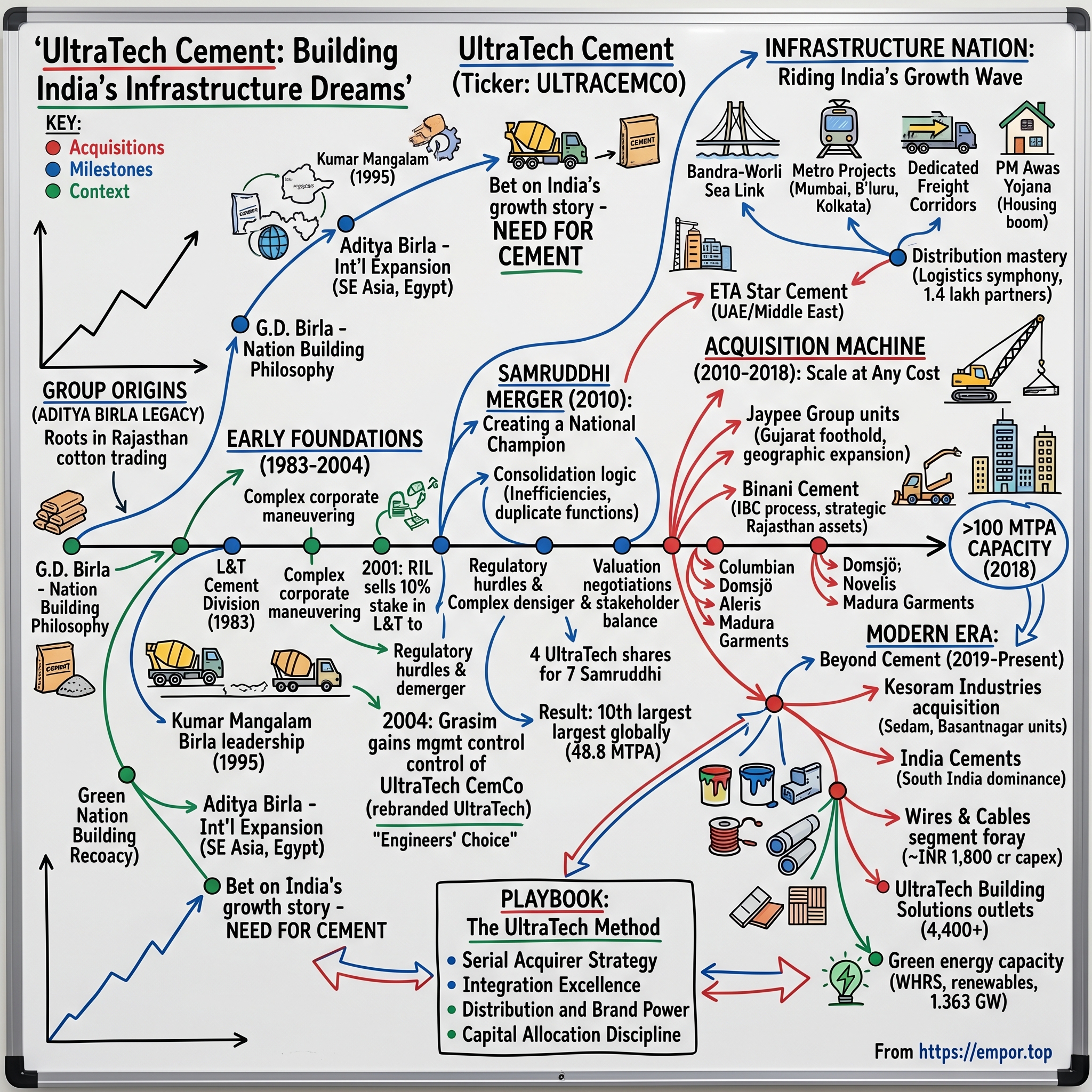

UltraTech Cement: Building India's Infrastructure Dreams

I. Introduction & Episode Hook

What if we told you a cement company became India's largest by acquisition after acquisition—and nobody saw it coming? While tech unicorns grab headlines and consumer brands capture imaginations, a cement manufacturer quietly assembled one of the most dominant market positions in modern Indian business history. This is the story of UltraTech Cement—a USD 8.9 billion behemoth that stands as the third-largest cement company in the world, excluding China.

The numbers alone command attention: over 140 million tonnes per annum of grey cement capacity, operations spanning India, UAE, Bahrain, and Sri Lanka, and a distribution network so vast it reaches 80% of India's geography through 1.4 lakh channel partners. But numbers tell only part of the story. The real narrative is how a cement division of an engineering conglomerate transformed into India's infrastructure backbone through relentless acquisition, integration excellence, and an almost prophetic bet on India's growth story.

This isn't just a tale of industrial consolidation. It's about timing markets perfectly, outmaneuvering global giants, and building a commodity business with brand power. It's about how Kumar Mangalam Birla took what could have been a sleepy industrial division and turned it into a strategic weapon for nation-building. Most importantly, it's about recognizing that in a country adding cities the size of Chicago every year, whoever controls cement controls the future.

II. The Aditya Birla Legacy & Group Origins

The Birla family's journey into India's industrial aristocracy begins not with cement or infrastructure, but with cotton trading in the dusty towns of Rajasthan. It's a saga spanning four generations, marked by calculated risks, nation-building ambitions, and an almost religious devotion to growth through acquisition. To understand UltraTech Cement, you must first understand the family philosophy that birthed it—a philosophy where business expansion wasn't just about profit, but about participating in India's transformation from a colonial economy to an industrial powerhouse.

The story truly accelerates with Ghanshyam Das Birla, the patriarch who transformed a modest trading operation into an industrial empire. G.D. Birla wasn't just building businesses; he was funding India's independence movement, establishing universities, and creating institutions that would outlive him by decades. His advice to his grandson Aditya, studying at MIT, encapsulated the family ethos: "eat only vegetarian food, never drink alcohol or smoke, keep early hours, marry young, switch-off lights when leaving the room, cultivate regular habits, go for a walk everyday, keep in touch with the family, and above all, don't be extravagant." This wasn't merely personal guidance—it was a business philosophy of restraint, discipline, and long-term thinking that would define how the Birlas approached empire-building.

At the age of 24, Aditya Birla assumed control of the group in 1969. He set up 19 companies outside India, in Thailand, Malaysia, Indonesia, the Philippines, and Egypt. This international expansion wasn't just ambitious—it was revolutionary for an Indian business house at that time. While other Indian conglomerates were content with protected domestic markets, Aditya Birla was planting flags across Southeast Asia, understanding that true scale required thinking beyond national boundaries. His vision wasn't just to build factories; it was to create an industrial network that could leverage opportunities across emerging markets.

The real transformation, however, came with Kumar Mangalam Birla's unexpected ascension to leadership. Kumar Mangalam Birla became the chairman of the Aditya Birla Group in 1995, succeeding his late father Aditya Vikram Birla when he was just 28 years old. Under his leadership, the group's annual turnover grew from $2 billion in 1995 to $60 billion in 2022. This thirty-fold growth wasn't achieved through organic expansion alone—it was orchestrated through a series of bold acquisitions, strategic pivots, and an uncanny ability to identify undervalued assets.

What Kumar Mangalam understood, perhaps better than his peers, was that India's infrastructure story was just beginning. The country needed everything—roads, bridges, airports, metros, housing for hundreds of millions. And all of it required cement. Lots of cement. The group's philosophy evolved from industrial diversification to strategic dominance in sectors critical to India's growth. This wasn't just business strategy; it was nation-building through capitalism.

The cement story within the Aditya Birla empire began modestly. Grasim Industries, the group's flagship company, had established cement operations in the mid-1980s through Vikram Cement, while Indian Rayon operated Rajashree Cement. These were respectable operations, but hardly dominant. The real opportunity emerged when Kumar Mangalam recognized that the Indian cement industry was ripe for consolidation. Fragmented, capital-intensive, and cyclical, it was an industry where scale provided insurmountable advantages—in procurement, distribution, and pricing power.

Some of the key acquisitions led by Mr. Kumar Mangalam Birla include Aleris Corporation, Novelis, the second largest acquisition ever by an Indian company, Columbian Chemicals, Domsjö Fabriker, CTP — Chemicals & Technologies, Jaypee Cement, Binani Cement, Larsen & Toubro's cement division, Indal from Alcan, Madura Garments, the Chlor Alkali division of Kanoria Chemicals and Solaris Chemtech Industries. This acquisition machine wasn't random—each deal was carefully orchestrated to either eliminate competition, gain strategic assets, or expand geographical reach. The cement acquisitions, in particular, followed a pattern: identify distressed or undervalued assets, leverage the group's financial strength to acquire them, and then integrate them into a larger, more efficient operation.

The group's approach to cement wasn't just about manufacturing capacity. It was about creating an ecosystem—from limestone mining to distribution networks, from research facilities to customer relationships. They understood that in a commodity business, differentiation came not from the product itself but from the ability to deliver it reliably, efficiently, and at scale. This philosophy would guide every major decision in UltraTech's journey from a division of an engineering company to India's cement champion.

III. Early Foundations: From L&T to UltraTech (1983–2004)

The story of UltraTech's birth is a masterclass in strategic corporate maneuvering, regulatory navigation, and the art of the complex deal. UltraTech Cement traces its origins to 1983 when it began as the cement division of Larsen & Toubro (L&T), being sold under the "L&T Cement" brand. What started as a division within one of India's most respected engineering conglomerates would eventually become the foundation of India's cement empire—but the journey from L&T Cement to UltraTech was neither simple nor straightforward.

Larsen & Toubro had built a formidable cement business over two decades. By the late 1990s, L&T Cement had become synonymous with quality in the Indian construction industry. Engineers trusted it, contractors specified it, and the brand carried the weight of L&T's engineering heritage. At the time, L&T was the largest cement manufacturer in India, while Grasim was the third-largest. But the engineering giant was facing its own strategic crossroads. The cement business, while profitable, was capital-intensive and cyclical—characteristics that didn't align perfectly with L&T's vision of becoming a focused engineering and construction powerhouse.

Meanwhile, Kumar Mangalam Birla was orchestrating his own vision. Having already established cement operations through Grasim Industries and Indian Rayon, he understood that the path to dominance in the Indian cement industry required scale—massive scale. The fragmented nature of the industry presented an opportunity: while dozens of players competed regionally, no single entity had achieved true national dominance. Birla saw in L&T's cement division not just production capacity, but distribution networks, brand equity, and strategic plant locations that would take decades to replicate organically.

The dance between L&T and Grasim began in earnest in 2001. In 2001, Reliance Industries sold its entire 10% stake in L&T to Grasim Industries. This wasn't just a financial investment—it was a strategic foothold. Kumar Mangalam Birla now had a seat at L&T's table, and more importantly, a voice in discussions about the future of its cement business. In 2002, Grasim would increase its stake in L&T to 15% and its attempt to launch an open offer to acquire an additional 20% stake was stayed by the SEBI over a possible violation of takeover rules.

The regulatory challenge from SEBI could have derailed the entire strategy. But rather than retreat, Birla and his team engineered one of the most complex corporate restructurings in Indian business history. The solution was elegant in its complexity: rather than acquire L&T outright (which would have been prohibitively expensive and strategically unnecessary), they would surgically extract the cement business through a demerger.

In 2003, L&T announced that it would demerge the cement business into a company called UltraTech CemCo. As part of the demerger plan, Grasim agreed to acquire an 8.5% stake in UltraTech CemCo from L&T, make an open offer to acquire another 30%, and transfer its 15% stake in L&T (residual engineering company) to L&T Employees Welfare Foundation. This wasn't just a transaction—it was corporate chess at its finest. L&T got to exit a non-core business while rewarding its employees, Grasim got the cement assets it coveted without having to buy all of L&T, and shareholders on all sides saw value creation.

The deal was executed in 2004, with Grasim obtaining management control of UltraTech CemCo (later renamed as UltraTech Cement) with its 51% stake, while L&T retained 11.5% shareholding. The structure was crucial—Grasim had control, but L&T maintained a stake, ensuring continued cooperation and smooth transition of relationships, contracts, and operational knowledge.

The rebranding from L&T Cement to UltraTech was more than cosmetic. Talking to reporters on the transition from the L&T Cement to Ultratech Cement, he unveiled a new tag-line — The Engineers' Choice — and announced that the brand makeover will be completed by the end of this year. The tagline was brilliant—it maintained continuity with L&T's engineering heritage while establishing UltraTech's own identity. Birla expressed the optimism that UltraTech Cement will resonate with buyers in just the way L&T Cement did. "Nothing has changed except the name. What was L&T Cement becomes UltraTech Cement," he added.

But behind the seamless branding transition was a massive operational integration challenge. UltraTech inherited 17 million tonnes of annual capacity, multiple manufacturing plants, thousands of employees, and complex supplier and customer relationships. The integration had to be flawless—any disruption in supply or quality would have given competitors an opening to capture market share.

Kumar Mangalam Birla's approach was methodical. Kumar Mangalam Birla, who sits at the head of the company culled out of L&T, has decided to shovel Rs 200 crore into plans that will maximise efficiencies and tap assets. This wasn't just about maintaining operations—it was about optimization. Every plant was evaluated for expansion potential, every distribution route was analyzed for efficiency, and every customer relationship was strengthened.

The financial engineering was equally sophisticated. UltraTech and Grasim have given the Birlas a cement capacity of over 31Mt, of which 17Mt comes from the former. This makes the group the eighth-largest cement player in the world. Overnight, the Aditya Birla Group had transformed from a significant player to a global force in cement. The combined entity wasn't just larger—it was strategically superior, with plants located near limestone reserves, integrated operations reducing costs, and a distribution network that covered the length and breadth of India.

They made it clear that Grasim's cement brand, Birla Plus, and UltraTech Cement would complement — rather than compete against — each other across the country. This dual-brand strategy was unconventional but shrewd. Rather than consolidate under a single brand (which would have meant writing off significant brand equity), the group maintained both, targeting different market segments and geographies. UltraTech would focus on premium institutional sales and large projects, while Birla Plus would cater to other segments.

The L&T-UltraTech transformation also established a template that Kumar Mangalam Birla would use repeatedly in subsequent acquisitions: identify strategic assets in companies looking to exit non-core businesses, structure complex deals that create value for all parties, execute flawless operational integration, and maintain brand equity while building new identities. This wasn't just M&A—it was corporate architecture at its finest.

Looking back, the period from 1983 to 2004 represents the gestation phase of what would become India's cement giant. The foundation was L&T's operational excellence and market presence, but the vision and execution came from Kumar Mangalam Birla's understanding that in a rapidly growing economy, the winners would be those who could consolidate fragmented industries. The successful integration of L&T's cement business didn't just create UltraTech—it proved that the Aditya Birla Group had the capability to execute complex acquisitions and integrate large operations. This capability would become their primary competitive advantage in the acquisition spree that followed.

IV. The Samruddhi Merger: Creating a National Champion (2010)

The year 2010 marked a pivotal moment in Indian cement history. While the world was recovering from the financial crisis and Indian infrastructure spending was accelerating, Kumar Mangalam Birla orchestrated what would become a template for industry consolidation. The Samruddhi merger wasn't just about adding capacity—it was about creating an entity with the scale to dominate an industry entering hypergrowth.

The strategic logic was compelling. Grasim Industries, the Aditya Birla Group's flagship company, had built a substantial cement business over decades, operating separately from UltraTech. This dual-structure made sense historically but was becoming increasingly inefficient. Two separate management teams, duplicate corporate functions, competing capital allocation decisions, and market confusion about which entity represented the group's cement ambitions. In an industry where scale determines everything from procurement costs to pricing power, this fragmentation was a luxury the group could no longer afford.

The cement business of Grasim is currently under demerger to Samruddhi Cement, and the proposed merger scheme will take effect only upon completion of the demerger and the issuance of shares by Samruddhi to shareholders of Grasim pursuant to the demerger. The structure was complex by necessity—Indian corporate law and tax regulations made direct mergers challenging. The solution was elegant: first, demerge Grasim's cement business into a new entity called Samruddhi Cement Limited, then merge Samruddhi with UltraTech.

The valuation negotiations were intense. Independent valuers had to balance the interests of multiple stakeholder groups: Grasim shareholders who owned the cement assets being transferred, UltraTech's minority shareholders who would see their stakes diluted, and the Aditya Birla Group which needed to maintain control while being fair to all parties. The exchange ratio recommended by the valuers and approved by both boards is 4 (four) equity shares of UltraTech of face value Rs. 10/- each for every 7 (seven) equity shares of Samruddhi of face value Rs. 5/- each.

The numbers told a compelling story. The merger will result in UltraTech emerging as the largest cement company in India and 10th largest in the world. The merged entity will have the following capacities: = 48.8 million tpa of grey cement across 22 plants = 504 MW of captive thermal power plants = 11.7 million cubic metres of ready-mix concrete capacity. This wasn't just growth—it was transformation.

Kumar Mangalam Birla's statement captured the strategic intent perfectly: "The merger will achieve the group's objective of consolidating its cement business into a single entity, thereby creating a platform that will help in pursuing aggressive growth going forward." This platform concept was crucial. The merged entity wouldn't just be larger; it would have the financial strength, operational efficiency, and market presence to pursue opportunities that neither entity could capture alone.

The financial engineering was sophisticated. Upon effectiveness of the Scheme, UltraTech's expanded equity capital will be 60.3 per cent held by Grasim and 39.7 per cent will be held directly by the other shareholders of UltraTech and Samruddhi. This structure gave Grasim clear control while providing enough public float to ensure liquidity and institutional investor interest. "Upon effectiveness of the merger, Grasim will retain a strategic and controlling interest in UltraTech while providing UltraTech flexibility for future fund raising."

The operational synergies were immediate and substantial. The combined entity could optimize plant utilization across a larger network, leverage combined purchasing power for raw materials and energy, eliminate duplicate corporate costs, and present a unified face to customers. With the merger UltraTech will add White cement and wallcare putty to its portfolio. These specialty products commanded higher margins and opened new market segments.

Mr. K.C. Birla Chief Financial Officer, UltraTech, said "The merger represents an inflexion point for UltraTech. The combined profitability and cash flows of the resultant entity will provide an impetus to our growth and will act as a force multiplier to our efforts of increasing market share. This wasn't corporate speak—it was a declaration of intent. The merged entity would have the financial firepower to pursue aggressive expansion, whether through organic growth or further acquisitions.

The timing was perfect. India's infrastructure spending was accelerating, driven by government programs and private investment. The cement industry was fragmented, with regional players struggling to compete with emerging national champions. Capital was becoming more important as environmental regulations required investments in cleaner technologies. The merged UltraTech would have advantages in all these areas.

The integration process was meticulously planned. Unlike many mergers that struggle with cultural integration, this was essentially a family reunion. Both organizations shared the Aditya Birla DNA, similar management philosophies, and complementary capabilities. Grasim's plants were primarily in central and western India, while UltraTech (through its L&T heritage) had strong positions in southern and northern markets. The combined network provided true pan-India coverage.

The market response was overwhelmingly positive. "The financial indicators post merger will support UltraTech to maintain its credit rating. We expect UltraTech's stock to be re-rated on completion of the merger process." Investors recognized that the merged entity would have better growth prospects, stronger cash flows, and enhanced competitive positioning. The stock price reflected this optimism, providing currency for future acquisitions.

The Samruddhi merger also established Kumar Mangalam Birla's reputation as a dealmaker who could execute complex transactions while maintaining stakeholder trust. Samruddhi Cement will be listed separately on the stock exchanges for a short period to provide an avenue for investors who are not convinced about the swap ratio. This provision showed respect for dissenting shareholders while maintaining deal momentum.

Looking back, the Samruddhi merger was more than a corporate transaction—it was the creation of a national champion. The combined entity had the scale to compete globally, the financial strength to invest in technology and sustainability, and the market presence to shape industry dynamics. It set the stage for the aggressive acquisition spree that would follow, as UltraTech leveraged its enhanced capabilities to consolidate the Indian cement industry.

The merger also demonstrated the power of patient capital and long-term thinking. Rather than rushing to integrate operations or cut costs, the focus was on building capabilities and market position. This approach would prove prescient as India entered a decade of unprecedented infrastructure development, and UltraTech was perfectly positioned to capture the opportunity. The creation of India's largest cement company wasn't just about size—it was about building an institution capable of supporting India's transformation from a developing economy to a global powerhouse.

V. The Acquisition Machine: Scale at Any Cost (2010–2018)

The period from 2010 to 2018 represents UltraTech's most aggressive phase of expansion—a relentless acquisition machine that would fundamentally reshape India's cement industry. Having created a national champion through the Samruddhi merger, Kumar Mangalam Birla now had the platform, the capital, and the credibility to pursue a consolidation strategy that would have seemed impossible just years earlier.

The opening salvo came almost immediately after the Samruddhi merger with international expansion. India's Ultratech Cement has acquired an 80 per cent stake of the UAE's ETA Star Cement Company (Star Cement) for $380m. This wasn't just another acquisition—it was a statement of intent. Mr. Kumar Mangalam Birla, Chairman, Aditya Birla Group, "The acquisition of ETA Star Cement marks the entry of the Aditya Birla Group Cement Business into the Middle East. It is in line with our long-term strategy of expanding our global presence across businesses and is consistent with our vision of taking India to the world."

The ETA Star acquisition was strategically brilliant for multiple reasons. Star Cement has a capacity of around 7 million tonnes-a-year (t/y) and has manufacturing plants in the UAE, Bahrain and Bangladesh. This gave UltraTech not just production capacity but access to high-margin export markets and a hedge against Indian market cycles. Mr. O. P. Puranmalka, Whole-time Director of the company, said, "The acquisition of ETA Star Cement will give us immediate scale and a footprint in the Indian Ocean Rim without disturbing the market matrix. This acquisition together with the amalgamation of Samruddhi Cement with UltraTech will enhance UltraTech's capacity to around 52mtpa."

But the real action was happening back home. The Indian cement industry in the early 2010s was facing a perfect storm: oversupply from aggressive capacity additions, infrastructure projects delayed by regulatory issues, and heavily leveraged players struggling with debt. For UltraTech, with its strong balance sheet and access to capital, this crisis was an opportunity.

The first major domestic acquisition came in 2013. UltraTech acquired Jaypee Group's Gujarat cement unit for ₹3,800 crores. This wasn't just about adding capacity—it was about gaining a strategic foothold in Gujarat, one of India's fastest-growing states with massive infrastructure ambitions. The plant came with limestone reserves, power generation capacity, and crucially, a captive jetty that reduced logistics costs significantly.

But the real game-changer came in 2017. The Scheme Implementation Committee of the Board of Directors of UltraTech Cement Limited, an Aditya Birla Group company, at its meeting held today, have made effective the Scheme of Arrangement between UltraTech, Jaiprakash Associates Limited (JAL), Jaypee Cement Corporation Limited (JCCL) and their respective shareholders and creditors, ("Scheme") for the acquisition of their six integrated cement plants and five grinding units, spread across the states of Himachal Pradesh, Uttar Pradesh, Uttarakhand, Madhya Pradesh, and Andhra Pradesh, with a capacity of 21.2 million tons.

The Jaypee acquisition was massive—₹16,189 crores for assets that would have cost multiples of that to build from scratch. It is horizontal merger, Ultratech cement is a one of the largest cement manufacture in the country but it has been limited to few areas and it doesn't concentred on the areas where the demand is more in the country, to expand it business geographically, Ultratech plan to acquire big cement plants in the country which was hold by Jaypee Associations, so they made a deal with Jaypee cement to acquire its biggest cement plants in the area's like Gujarat, Madhya Pradesh, Andhra Pradesh, Uttar Pradesh, Uttarakhand, Himachal Pradesh, to Acquire those plants, they offered 16,189 crores to Jaypee cements groups, Jaypee cement showed positive response to the deal because Jaypee associations facing debt burden form it lenders banks ICICI, YES Bank, to clear those debts Jaypee cements accepted the deal with Ultratech.

The strategic logic was impeccable. Says Mr. Kumar Mangalam Birla, Chairman, UltraTech – "This move is essentially for geographic market expansion, enabling UltraTech's entry into the high growth markets of India where it needed greater reinforcemen The acquisition transformed UltraTech's geographic footprint, giving it dominant positions in northern states that were expected to see massive infrastructure spending.

After the acquisition, UltraTech has 18 Integrated Plants, 1 clinkerisation unit, 25 Grinding Units and 7 bulk terminals, augmenting its Grey Cement manufacturing capacity to 93 mtpa. With this UltraTech becomes the 4th largest cement player globally (excluding the Chinese players) and the largest player in India by an even larger margin.

The Binani Cement acquisition in 2018 was different—it was UltraTech's first major play through India's new Insolvency and Bankruptcy Code (IBC). The battle for Binani was fierce, with Dalmia Bharat initially winning the bid. But UltraTech's persistence and superior offer eventually prevailed. The National Company Law Appellate Tribunal had on November 14, 2018 approved the Rs 79.5 billion offer of UltraTech for the Rajasthan-based firm.

The Binani acquisition showcased UltraTech's evolving acquisition strategy. As per Ultratech's resolution plan, financial as well as operational creditors are getting 100% of their claims amount. This wasn't a distressed asset grab—it was a strategic acquisition where UltraTech paid full value to ensure smooth integration and maintain relationships with stakeholders.

UltraTech Nathdwara Cement has an installed capacity to produce 6.25 million tonnes per annum (MTPA) cement and 4.59 MTPA clinker in Rajasthan. UltraTech's capacity in the North region will get enhanced to 24 MTPA and it would "become one of the strongest player in North market", it added. The Rajasthan location was crucial—rich limestone reserves, proximity to high-growth markets, and synergies with existing operations.

What made this acquisition spree successful wasn't just financial firepower—it was operational excellence in integration. In 2017, Ultratech acquired plants of Jaiprakash Associates having 21.2 million tonne per annum capacity. Each acquisition followed a playbook: immediate focus on operational efficiency, integration of procurement and logistics, leveraging UltraTech's brand and distribution network, and crucially, retaining key talent while eliminating redundancies.

The numbers tell the story of transformation. Starting the decade with around 50 MTPA capacity, UltraTech ended 2018 with over 100 MTPA—becoming the first cement company globally outside China to achieve this milestone in a single country. The company had gone from being one of several large players to being larger than its next two competitors combined.

But this growth came at a cost. Ultratech's acquisition spree has also led to an increase in debt for the company The company's debt levels rose significantly, though still manageable given its cash generation capabilities. More challenging was the operational complexity of managing such a vast, geographically dispersed operation with plants acquired from different companies with different cultures and systems.

The acquisition machine also changed the competitive dynamics of the Indian cement industry. Regional players found it increasingly difficult to compete with UltraTech's scale advantages in procurement, logistics, and pricing. This triggered a wave of consolidation as other large players like Dalmia Bharat and Shree Cement also went on acquisition sprees to maintain competitive scale.

Looking back, the 2010-2018 period represents one of the most successful industrial consolidation stories in Indian corporate history. Kumar Mangalam Birla had recognized that in a capital-intensive, commodity business like cement, scale wasn't just an advantage—it was the only sustainable competitive advantage. By moving aggressively when others were constrained by debt or uncertainty, UltraTech built a position that would be nearly impossible for competitors to challenge. The acquisition machine hadn't just added capacity—it had created a structural advantage that would define the Indian cement industry for decades to come.

VI. Infrastructure Nation: Riding India's Growth Wave

If cement is the foundation of modern civilization, then UltraTech has become the foundation of modern India. The transformation of India from a developing nation into an infrastructure powerhouse has created one of the greatest demand stories in industrial history—and UltraTech positioned itself perfectly at the center of this narrative.

Bandra - Worli Sea Link, Mumbai Metro, Bengaluru Metro and Kolkata Metro are all built on the robustness and high quality standards of UltraTech Cement. These aren't just construction projects—they're symbols of India's ambition, and UltraTech's cement forms their backbone. It's 120 concrete pillars built with UltraTech is what makes this bridge stand tall and mighty that can hold up to 128 metres of concrete pylon towers that beautify the bridge. The Bandra-Worli Sea Link, in particular, represents something profound about UltraTech's evolution—from being a cement supplier to becoming an infrastructure partner.

The quality of cement had to be superlative as the pillars would have to withstand the fury of the ocean's waves. Therefore, the choice, not surprisingly was 'UltraTech Cement'. This wasn't just about providing bags of cement. UltraTech had to develop specialized marine-grade concrete that could withstand saltwater corrosion, create custom mixes for different structural elements, and provide real-time technical support during critical pours. Realising the criticality and linkage of these projects to nation building, UltraTech has set up dedicated plants at project sites to cater to the projects' concrete and cement requirements, customizing the product as per required quality standards and providing it in real time.

The scale of India's infrastructure ambitions is staggering. The NIP encompasses capital outlay of INR100 trillion (US$1.2 trillion) in infrastructure over 2020-2025, a doubling of the sum spent in 2014-2019. Projects will span roads, housing, urban infrastructure, railways, power, and irrigation. Such works account for most of the cement consumption in India. This isn't incremental growth—it's a fundamental reimagining of what India could be.

We expect India's cement demand to grow at a 7% CAGR over the next four years, higher than the likely pace of capacity additions during the period. As such, capacity utilization levels will remain above 70%, in our view. This structural demand-supply imbalance is exactly what UltraTech had positioned itself to capture through its aggressive acquisition strategy. While competitors scrambled to add capacity, UltraTech already had it.

The numbers paint a picture of explosive growth. Indian cement consumption expanded 6.2 per cent YoY in 2024, amounting to 444.2Mt, up from 418.1Mt in 2023. But this is just the beginning. India is the second-largest cement maker in the world after China, with total installed capacity of 635 million tons in fiscal year 2024. However, at 280 kilograms (kg) per person, the country's per capita consumption is well below the world average of 500 kg-550 kg. This presents a significant growth opportunity for the cement companies as India continues to urbanize and invest in infrastructure.

In October 2021, Prime Minister, Mr. Narendra Modi, launched the 'PM Gati Shakti - National Master Plan (NMP)' for multimodal connectivity. Gati Shakti will bring synergy to create a world-class, seamless multimodal transport network in India. This will boost the demand for cement in the future. Gati Shakti isn't just another government program—it's a coordinated effort to break infrastructure bottlenecks that have constrained India's growth for decades.

UltraTech's involvement goes beyond just supplying materials. Today, UltraTech has consolidated its position as a Preferred supplier to large, prestigious infrastructure projects across the country like the Bandra-Worli Sea Link, the Monorail Project and the T2 airport terminal in Mumbai, all the Metro projects in the country, the refinery in Jamnagar, Golden Quadrilateral Road Project and many major nuclear, thermal and hydel projects. Each of these projects required different specifications, delivery schedules, and technical support—complexity that only a company of UltraTech's scale could handle.

UltraTech has contributed as a reliable partner for the more than 1400 km long Western dedicated freight corridor developed by Indian Railways, power plant in Korba (Chhattisgarh), Tata Thermal Power Plant in Kutch, and Reliance's Jamnagar Refinery. These aren't just construction projects—they're the arteries of India's economic transformation. The Western Dedicated Freight Corridor alone will revolutionize logistics in India, reducing transportation costs and making Indian manufacturing globally competitive.

The housing boom represents another massive opportunity. The PM Awas Yojana for rural India has 34.9 million registered beneficiaries as of November 2024 with 26.6 million houses already being completed. For Urban India, the same scheme is being implemented with an investment of USD95.9 billion and has completed 8.7 million houses, out of 11.8 million sanctioned. Each house requires approximately 10-15 tonnes of cement—multiply that by millions, and you understand the scale of demand.

UltraTech's distribution mastery becomes crucial here. Through a robust logistics network of 30 plants, 500 plus warehouses and 150 plus railheads, UltraTech serves 14000 orders per day by using a mix of various logistics modes including rail, road and sea. These orders originate from 50000 plus dealers, retailers and institutional customers with lot size varying from of 1 MT to 40 MT. This isn't just logistics—it's a symphony of coordination that ensures cement reaches every corner of India, from mega-projects to individual home builders.

The company's investment in technology and capacity is preparing for even greater growth. UltraTech Cement, for instance, revealed that the firm will be commissioning two new greenfield projects in India. Over the next three years, the firm is planning to invest INR 324 billion towards its capital expenditure. This isn't defensive investment—it's aggressive positioning for a future where India's infrastructure spending accelerates further.

We estimate they will spend about US$14.3 billion on additional capacity over the next four years, enough to make an extra 160-170 million tons of cement annually. S&P Global Ratings believes this expansion will be well supported by demand--the Indian government plans to spend US$1.7 trillion on infrastructure projects through to 2030, according to Crisil. This will vastly raise cement consumption in the country.

The competitive dynamics are shifting in UltraTech's favor. We believe the operating cash flows of the top-three cement companies by volume--Ultratech Cement Ltd., Ambuja Cement Ltd. and Shree Cement Ltd.--will adequately cover their capex needs through to end-fiscal 2027. The three firms will account for more than 70% of the country's total cement capacity increase over the next four years. Scale is becoming destiny in Indian cement, and UltraTech has the most scale.

The growth of the ready-mix concrete (RMC) market is another significant trend in the India cement industry. RMC is concrete that is manufactured in a batching plant according to a set recipe and then delivered to a construction site in a ready-to-use form. The increasing preference for RMC over traditional site-mixed concrete is driven by its superior quality, consistency, and convenience. The use of RMC reduces construction time, minimizes material wastage, and enhances project efficiency. This trend is particularly prominent in urban areas where space constraints and the need for faster construction timelines make RMC a more viable option. UltraTech, with its extensive RMC network, is perfectly positioned to capture this shift.

The urbanization story is perhaps the most compelling long-term driver. Increase in core infrastructure also accelerates urbanization. Between 2014 and 2050, an additional 404 million Indians are expected to move to the country's urban areas, according to the United Nations. This is equivalent to the entire population of the United States and United Kingdom combined moving to cities—and they'll all need housing, offices, roads, and infrastructure.

The expected cement production capacity in 2028 will be nearly 720 MT. In addition, India's cement production in 2024 is expected to grow by 7-8 per cent driven by infrastructure-led investment and mass residential projects. The industry is preparing for sustained high growth, and UltraTech, with its dominant market position, will capture a disproportionate share.

What makes UltraTech's position particularly strong is the alignment between its geographic footprint and India's growth corridors. In 2024, mega construction projects such as the GIFT City in Gujarat, the Surat DREAM City, and the Dholera SIR are expected to aid the cement demand in India. Furthermore, projects like the Bengaluru-Mumbai economic corridor and the Delhi-Mumbai industrial corridor will drive cement consumption over the medium term. UltraTech has strategic presence in all these high-growth regions.

The company isn't just riding India's infrastructure wave—it's helping create it. Being 'The Engineer's Choice' has made UltraTech the preferred brand for large infrastructural projects of repute that contribute to India's growth story. This brand positioning is crucial. In a commodity business, being specified by engineers and architects creates a moat that's difficult for competitors to breach.

Looking ahead, the infrastructure story is far from over. As per Morgan Stanley, India's infrastructure as a percentage of GDP stood at 5.3% in FY24 and will increase to 6.5% by FY29. This will result in the burgeoning growth in the cement consumption of India with the heightened infrastructure spending thereby boosting India's Cement Industry over the foreseeable future. For UltraTech, this isn't just about selling more cement—it's about being the backbone of India's transformation from a $3.7 trillion economy to a $10 trillion economy by 2030.

The symbiotic relationship between UltraTech and India's growth is perhaps unique in global business. As India builds its future—smart cities, industrial corridors, mass transit systems, affordable housing—UltraTech provides the fundamental building material. And as UltraTech grows stronger, it gains the capacity to support even more ambitious projects. It's a virtuous cycle where corporate success and national development are perfectly aligned. In many ways, UltraTech isn't just participating in India's growth story—it's writing it, one infrastructure project at a time.

VII. Modern Era: Beyond Cement (2019–Present)

The years from 2019 to the present represent UltraTech's evolution from a cement giant to something more ambitious—a comprehensive building solutions provider. This transformation isn't just about diversification; it's about recognizing that India's construction boom requires more than just cement, and whoever controls the broader ecosystem will dominate the future.

The pace of acquisitions hasn't slowed. The Composite Scheme of Arrangement between Kesoram Industries Limited ("Kesoram") and the Company became effective from 1st March, 2025. The cement business of KIL consists of 2 integrated cement units at Sedam (Karnataka) and Basantnagar (Telangana) with a total cement production capacity of 10.75 mtpa. Out of this total capacity, 8.50 mtpa is clinker backed and 2.25 mtpa is surplus grinding capacity. The cement business also has a 0.66 mtpa packing plant in Solapur, Maharashtra.

The Kesoram acquisition showcased UltraTech's continued ability to execute complex transactions. Under the demerger scheme, UltraTech will issue 1 equity share of the face value of Rs.10/- each for every 52 equity shares of Kesoram of face value Rs. 10/- each as recommended by the valuers and accepted by the Board. The valuation reflected the distressed nature of Kesoram's business, but UltraTech saw opportunity where others saw problems.

UltraTech's acquisition of Kesoram Cement will raise its share of capacity in the Southern Indian cement market to 21% from 11%, according to BusinessLine Online News. Market researcher Emkay Global said that it expects the acquisition and UltraTech Cement's current expansion plans to raise the group's total share of cement capacity in Southern India and Western India by 7 – 8%. The geographic logic was compelling—Southern India had been UltraTech's relative weakness, and this acquisition addressed that gap decisively.

But the real game-changer came with India Cements. Upon receipt of unconditional approval from the Competition Commission of India, UltraTech acquired the equity stake of the erstwhile promoters and members of the promoter group of The India Cements Limited ("ICEM"), resulting in ICEM becoming a subsidiary company with effect from 24th December, 2024. Consequently, UltraTech's total shareholding in ICEM stands at 25,25,29,160 equity shares of Rs.10/- each, representing 81.49% of ICEM's equity share capital.

The India Cements acquisition was particularly strategic. India Cement is one of the oldest cement companies in South India. India Cements has a total capacity of 14.45 mtpa of grey cement. This wasn't just about adding capacity—it was about acquiring a storied brand with deep relationships in Southern markets. Pursuant to the same, Ultratech entered into a share purchase agreement to purchase 32.72% equity stake held by promoters & promoter group at INR 390 per share aggregating to INR 3954 crores.

With the addition of 10.75 MTPA of grey cement capacity of KIL, UltraTech has now reached a total capacity of 183.06 MTPA. The company is now within striking distance of its stated goal of 200 MTPA—a target that would have seemed fantastical just a decade ago.

But the most surprising move came in February 2025. Mumbai, 25th February, 2025: UltraTech Cement Limited, an Aditya Birla Group company (the Company), proposes to extend its footprint in the construction value chain, through wires and cables segment with a nominal capital expenditure of ~ INR 1,800 crore over the next 2 years. This wasn't just diversification—it was a fundamental reimagining of what UltraTech could be.

Mr. Kumar Mangalam Birla, Chairman, Aditya Birla Group, stated, "We intend to expand our presence in the construction value chain through our foray in the cables and wires segment, which aligns with our vision of providing comprehensive solutions to our end customers in the construction sector. This statement revealed the strategic thinking—UltraTech wasn't just selling cement; it was positioning itself as the one-stop solution for India's construction needs.

The wires and cables industry has witnessed revenue compound annual growth rate (CAGR) of around 13 per cent between FY19 and FY24. The market was growing rapidly, driven by the same infrastructure and housing boom that was driving cement demand. UltraTech's entry into this segment with a planned capex of ₹1,800 crore sent shockwaves through the industry.

KEI Industries and Polycab India stocks fell 10 per cent each and RR Kabel shares dropped 9.8 per cent. Havells India and Finolex Cables also witnessed downturns, of 7.4% and 3.3%, respectively. The market's reaction was telling—investors recognized that UltraTech's entry could fundamentally disrupt the industry dynamics.

The strategic logic was compelling. UltraTech proposes to leverage its extensive manufacturing expertise coupled with its connect with end-customers to deliver high-quality wires and cables. Through UltraTech's cement, Hindalco Industries' aluminium and copper, and Grasim's entry into paints last year, the group already covers a larger part of the construction value chain. Hindalco's metal production is also a key raw material in the making of wires and cables.

Strategically, the new plant will be located 100 km from Hindalco's Dahej copper plant, ensuring a steady supply of copper, which constitutes ~75% of raw material costs. This proximity will optimise working capital management. This will be the most important advantage to UltraTech since other listed players don't have a dedicated copper facility for backward integration. The synergies within the Aditya Birla Group were creating competitive advantages that standalone players couldn't match.

UltraTech's foray into Cables & Wires (W&C) aligns with its strategy to increase its share of wallet from individual homeowners in the construction value chain. This was crucial—rather than just selling cement for the foundation, UltraTech wanted to participate in every aspect of construction. He noted that there were more than 4,400 outlets of UltraTech Building Solutions as of December 2024, already selling some non-cement products such as construction chemicals, dry mortars and waterproofing.

The financial targets were ambitious. The expected internal rate of return for the investment is 25 per cent, with a ROCE of 20 per cent. The capacity of this division would be 35-40 lakh KM. These weren't speculative projections—they were based on UltraTech's proven ability to leverage its distribution network and brand strength.

UltraTech's chief financial officer said during the analysts call, that pricing won't be impacted with another player. The executive also reiterated cement remains the core business, which is expected to have ₹1 trillion capital employment soon, with the company operating 214 million tonnes per annum. This reassurance was important—UltraTech wasn't abandoning cement; it was building around it.

The sustainability initiatives have also accelerated. Continuing its stated commitment towards enhancing environment conservation measures, UltraTech added 269 MW of renewable power during the quarter. Combined with its 342 MW in Waste Heat Recovery Systems (WHRS), UltraTech's total green energy capacity has now reached 1.363 GW, which will cover about 46% of UltraTech's current power needs. This wasn't just about regulatory compliance—it was about future-proofing the business as carbon costs become increasingly important.

The financial performance reflects the strength of the strategy. Consolidated Net Sales for the year reached Rs. 74,936 crores, up from Rs. 69,810 crores last year. Despite increased competition and input cost pressures, UltraTech maintained profitability through operational excellence and market leadership. The Board of Directors at their meeting held today have recommended a dividend of 775% at the rate of Rs.77.50/- per equity share of face value of Rs.10/- per share, aggregating Rs.2,283.75 crores.

The company also recognized the need for adjacent acquisitions. In a separate development, UltraTech's Board approved acquisition of 6,42,40,000 equity shares of Rs. 10/- each of Wonder WallCare Private Limited ("Wonder WallCare"), engaged in the manufacture of wall putty and related products for an Enterprise Value not exceeding Rs. 235 crores. These smaller, strategic acquisitions complemented the mega-deals, filling product gaps and strengthening the building solutions portfolio.

Looking ahead, the outlook remains robust. Given the government's focus on infrastructure and housing projects, alongwith increased rural and urban demand, a sustainable volume growth of 7- 8% is expected, going forward. While the sector may face short-term challenges, the long-term outlook is indicating signs of improvement with stable demand likely to support growth.

UltraTech achieved the distinction of recording 100 million tonnes of grey cement sales in a single financial year. This achievement comes within 5 years of the company achieving 100 MTPA production capacity. The acceleration is remarkable—what took decades to build initially is now being replicated in years.

The transformation from cement manufacturer to building solutions provider represents a fundamental shift in strategy. This year UltraTech reached a new milestone of crossing 175 mtpa of cement capacity in India and is likely to emerge as the largest cement company globally (by sales volume ex-China). But size alone isn't the goal—it's about creating an ecosystem where UltraTech becomes indispensable to India's construction industry.

The modern era of UltraTech is characterized by three key themes: relentless capacity expansion through acquisitions, diversification into adjacent building materials, and sustainability initiatives that future-proof the business. The company is no longer just riding India's infrastructure wave—it's helping to create it. As India transforms from a $3.7 trillion economy to its ambition of becoming a $10 trillion economy, UltraTech is positioning itself not just as a supplier, but as an essential partner in that transformation.

The journey from a cement division of L&T to potentially the world's largest cement company outside China, with growing presence in paints, wires, cables, and building solutions, represents one of the most successful corporate transformations in Indian business history. And if Kumar Mangalam Birla's track record is any indication, this is just the beginning of UltraTech's ambitions to dominate India's construction ecosystem.

VIII. Playbook: The UltraTech Method

The UltraTech story isn't just about size or market share—it's about developing a replicable playbook for dominating a commodity business. After two decades of relentless execution, the UltraTech method has emerged as a masterclass in industrial strategy, combining financial engineering, operational excellence, and strategic patience in ways that competitors struggle to replicate.

Serial Acquirer Strategy: The Art of Buying Competitors

UltraTech's acquisition strategy isn't opportunistic—it's systematic. The company has developed a sophisticated framework for identifying, valuing, and integrating targets. The pattern is clear: focus on distressed or subscale assets where the seller has compelling reasons to exit, whether it's debt pressure (Jaypee, Binani), strategic realignment (L&T, Century), or generational transition (India Cements).

The valuation discipline is remarkable. Recently, Ultratech bought Kesoram having a total capacity of 10.75 MTPA at enterprise value per ton of INR 7070 & Century Textiles cement business at enterprise value per ton of INR 6073. These valuations, substantially below replacement cost, create immediate value. The company doesn't chase growth at any price—it waits for the right asset at the right price.

Timing is crucial. UltraTech typically strikes when the broader industry is stressed, using its strong balance sheet as a competitive weapon. The 2017-2018 period, when many players were struggling with debt and overcapacity, saw UltraTech's most aggressive moves. This countercyclical approach requires courage and capital—both of which UltraTech has in abundance.

The funding strategy is equally sophisticated. For strategic acquisitions within the group (like Kesoram and Century), share swaps preserve cash and align interests. For external acquisitions, a mix of internal accruals and debt maintains financial flexibility. Ultratech will finance the Binani acquisition of Rs 7900 crores with 60% debts and 40% from equity. This balanced approach ensures acquisitions are accretive without compromising the balance sheet.

Integration Excellence: From Acquisition to Value Creation

Acquisition is just the beginning—integration is where value is created. UltraTech has developed a systematic integration playbook that transforms underperforming assets into profit centers. The approach is methodical: first, stabilize operations and ensure safety compliance; second, optimize production through debottlenecking and efficiency improvements; third, integrate procurement and logistics; finally, leverage UltraTech's brand and distribution network.

Ready to use assets which are currently operating at 50% capacity utilization · Location benefit since Binani cement unit is in Rajasthan which will help Ultratech realignment of its existing market for Rajasthan and Gujarat. This exemplifies the approach—UltraTech sees opportunity where others see problems. Within 18-24 months, most acquired assets reach optimal utilization levels.

The cultural integration is equally important. Rather than imposing a top-down culture, UltraTech selectively retains key talent from acquired companies while introducing Aditya Birla Group's management systems and values. This balanced approach preserves institutional knowledge while driving performance improvement.

Synergy realization is systematic. The operations will be bolstered by economies of scale resulting from synergies in procurement, logistics and fixed costs. These aren't just paper synergies—they're real cost reductions achieved through combined purchasing power, optimized logistics networks, and elimination of duplicate functions.

Capital Allocation: The Discipline of Growth

UltraTech's capital allocation framework balances growth, returns, and financial flexibility. The company maintains clear hurdles for investment: The expected internal rate of return for the investment is 25 per cent, with a ROCE of 20 per cent. These aren't aspirational—they're minimum requirements that ensure capital discipline even during aggressive expansion phases.

The company's approach to organic versus inorganic growth is pragmatic. UltraTech Cement, for instance, revealed that the firm will be commissioning two new greenfield projects in India. Over the next three years, the firm is planning to invest INR 324 billion towards its capital expenditure. This dual approach—buying existing capacity when valuations are attractive while building new capacity in high-growth markets—optimizes capital efficiency.

Dividend policy reflects confidence. The Board of Directors at their meeting held today have recommended a dividend of 775% at the rate of Rs.77.50/- per equity share of face value of Rs.10/- per share, aggregating Rs.2,283.75 crores. This generous payout, despite aggressive expansion, signals management's confidence in cash generation capabilities.

Distribution and Brand Power in a Commodity Business

In a commodity business, distribution is destiny. UltraTech has built India's most extensive cement distribution network—not through organic growth alone, but by integrating and optimizing acquired networks. Through a robust logistics network of 30 plants, 500 plus warehouses and 150 plus railheads, UltraTech serves 14000 orders per day by using a mix of various logistics modes including rail, road and sea. These orders originate from 50000 plus dealers, retailers and institutional customers with lot size varying from of 1 MT to 40 MT.

The brand strategy is sophisticated. While cement is fundamentally a commodity, UltraTech has created differentiation through consistent quality, technical support, and reliability. Being 'The Engineer's Choice' has made UltraTech the preferred brand for large infrastructural projects of repute that contribute to India's growth story. This positioning—targeting engineers and architects who specify cement—creates pull-through demand that commands premium pricing.

The company's approach to customer segmentation is nuanced. For large infrastructure projects, dedicated plants and customized products create switching costs. For retail customers, the extensive dealer network ensures availability. For institutional customers, technical support and reliability matter more than price. This multi-pronged approach captures value across segments.

Managing Cyclicality and Input Costs

Cement is inherently cyclical, but UltraTech has developed strategies to dampen volatility. Geographic diversification across India's regions smooths regional demand variations. Product diversification into ready-mix concrete, white cement, and now building solutions reduces dependence on grey cement cycles.

Input cost management is sophisticated. Energy costs were lower by 14% YoY, mainly on account of decrease in fuel cost which was Rs.881/t in Q4FY25 compared to Rs.1025/t in Q4FY24. This isn't luck—it's the result of strategic investments in captive power, waste heat recovery, and renewable energy. Combined with its 342 MW in Waste Heat Recovery Systems (WHRS), UltraTech's total green energy capacity has now reached 1.363 GW, which will cover about 46% of UltraTech's current power needs.

The company's approach to capacity utilization is strategic. Effective capacity utilization was 89% during the quarter and 78% for the full year. Rather than chasing maximum utilization, UltraTech maintains strategic spare capacity to capture demand surges and maintain pricing discipline.

Competing with Regional Players and MNCs

UltraTech faces competition from multiple angles—regional players with local advantages, MNCs with global resources, and new entrants like Adani with deep pockets. The strategy is differentiated by competitor type.

Against regional players, UltraTech leverages scale advantages in procurement and the ability to supply large projects that require multi-location delivery. Against MNCs, local knowledge and relationships matter more than global best practices. Against new entrants, the company uses its installed base and customer relationships as defensive moats.

The competitive response is calibrated. Rather than engaging in price wars, UltraTech focuses on service, quality, and availability. Today, UltraTech has consolidated its position as a Preferred supplier to large, prestigious infrastructure projects across the country like the Bandra-Worli Sea Link, the Monorail Project and the T2 airport terminal in Mumbai, all the Metro projects in the country, the refinery in Jamnagar, Golden Quadrilateral Road Project and many major nuclear, thermal and hydel projects. These marquee projects create demonstration effects that influence smaller customers.

The Aditya Birla Umbrella Advantage

Being part of the Aditya Birla Group provides advantages beyond capital access. The group's reputation opens doors with governments and large customers. Shared services reduce costs. Most importantly, sister companies provide strategic synergies.

On raw material sourcing, he said the proposed factory at Jhagadia in Gujarat is in close proximity to the copper-producing facilities in Gujarat. Group entity Hindalco Industries also operates a copper smelting unit near Dahej in the same state. These intra-group synergies create competitive advantages that standalone players cannot replicate.

The group's management development programs create a pipeline of talent. The ability to move executives between group companies brings fresh perspectives while maintaining cultural alignment. This human capital advantage is often underappreciated but crucial for managing a complex, multi-plant operation.

The Learning Organization

Perhaps UltraTech's most underrated capability is its ability to learn and adapt. Each acquisition teaches lessons that improve the next. Each market cycle provides insights that inform strategy. Each competitive threat triggers innovation.

The company's entry into new businesses shows this learning in action. As part of extending our offering from Building Products Division (BPD), we have examined multiple other adjacencies – pipes, tiles, wood adhesives, sanitary fitting, furniture, lights, and so on, and dropped all these product categories because they were not as good as expected. This disciplined evaluation process—testing hypotheses and pivoting based on data—prevents costly mistakes.

Execution Excellence

Ultimately, the UltraTech method comes down to execution excellence. The company doesn't just have a strategy—it executes it relentlessly. Acquisitions close on schedule. Plants get integrated ahead of plan. Capacity additions come online on time and under budget.

This execution capability creates a virtuous cycle. Success in execution builds credibility with stakeholders. Credibility provides access to opportunities. Opportunities, well-executed, create value. Value creation provides resources for the next opportunity.

The UltraTech method isn't revolutionary—it's evolutionary. It takes established business principles—scale economies, operational excellence, financial discipline—and applies them consistently over time. What makes it powerful is the combination of strategic vision and operational execution, financial strength and market insight, aggressive expansion and prudent risk management.

For competitors, the UltraTech method presents a formidable challenge. It's not enough to match one element—the entire system must be replicated. And by the time competitors catch up, UltraTech has moved further ahead. This is the essence of sustainable competitive advantage in a commodity business—not a single moat, but a system of reinforcing advantages that compounds over time.

IX. Analysis & Investment Case

The investment case for UltraTech Cement represents a fascinating study in how a commodity business can create enduring value. At current valuations, investors face a classic dilemma: paying a premium for quality in a cyclical industry. Yet, the analysis reveals why UltraTech commands—and likely deserves—its valuation premium.

Financial Performance Deep-Dive

Consolidated Net Sales for the year reached Rs. 74,936 crores, up from Rs. 69,810 crores last year. This 7.3% growth during a challenging year demonstrates pricing power even in competitive markets. More impressive is the maintenance of margins despite input cost pressures—a testament to operational excellence and scale advantages.

The company's return metrics tell the story of value creation. With ROE consistently above 12% and ROCE targets of 20% for new investments, UltraTech generates returns well above its cost of capital. The cash generation is robust— The Board of Directors at their meeting held today have recommended a dividend of 775% at the rate of Rs.77.50/- per equity share of face value of Rs.10/- per share, aggregating Rs.2,283.75 crores. This massive dividend, representing a 7.75% yield on face value, signals confidence in sustained cash generation.

The balance sheet strength enables strategic flexibility. Despite aggressive acquisitions, debt levels remain manageable with debt-to-EBITDA ratios below 2x. This financial strength becomes a competitive weapon during downturns, enabling countercyclical acquisitions when weaker players face distress.

Competitive Positioning vs. ACC, Ambuja, Shree Cement

The Indian cement industry has evolved into a three-way race between UltraTech, the Adani Group (through ACC and Ambuja), and Shree Cement, with regional players increasingly marginalized. UltraTech's competitive position is formidable but not unassailable.

UltraTech is the third largest cement producer in the world, outside of China, with a total Grey Cement capacity of 154.86 MTPA. This scale advantage translates into procurement benefits, logistics optimization, and the ability to serve pan-India projects that smaller players cannot handle.

Against Adani's aggressive expansion, UltraTech's advantage lies in operational expertise and market knowledge accumulated over decades. While Adani brings financial firepower, UltraTech brings institutional knowledge—understanding of local markets, relationships with contractors, and technical expertise that takes years to develop.

Shree Cement represents a different challenge—a focused, efficient operator with industry-leading margins. UltraTech's response has been to match efficiency while leveraging superior scale and distribution reach. The acquisition strategy effectively prevents Shree from achieving comparable scale through inorganic growth.

UltraTech Cement's acquisition of Kesoram Cement will raise its share of capacity in the Southern Indian cement market to 21% from 11%, according to BusinessLine Online News. Market researcher Emkay Global said that it expects the acquisition and UltraTech Cement's current expansion plans to raise the group's total share of cement capacity in Southern India and Western India by 7 – 8%. This geographic expansion addresses UltraTech's historical weakness in South India while strengthening dominance in core markets.

Industry Structure and Consolidation Trends

In CY24, the cement sector in India witnessed a significant increase in mergers and acquisitions, with more than ten deals announced, representing the highest level of activity since CY14. This consolidation wave is transforming industry structure from fragmented to oligopolistic, with the top three players likely to control 60%+ of capacity within five years.

Consolidation benefits UltraTech disproportionately. As the largest player, it has the financial capacity to acquire, operational expertise to integrate, and market position to extract synergies. Each acquisition strengthens UltraTech's position while reducing competitive intensity.

We believe the operating cash flows of the top-three cement companies by volume--Ultratech Cement Ltd., Ambuja Cement Ltd. and Shree Cement Ltd.--will adequately cover their capex needs through to end-fiscal 2027. The three firms will account for more than 70% of the country's total cement capacity increase over the next four years. This concentration of expansion among the top three players will likely lead to more rational pricing and better industry returns.

The regulatory environment remains supportive of consolidation. Competition authorities have generally approved cement mergers, recognizing that regional competition remains intense even as national concentration increases. This regulatory stance enables continued consolidation.

Bear Case: Challenges and Risks

The bear case for UltraTech centers on several structural challenges. Overcapacity remains a persistent threat— The Indian cement sector's capacity is expected to expand at a Compound Annual Growth Rate (CAGR) of 4-5% over the four-year period up to the end of FY27. It would thus begin the 2028 financial year at 715-725 MT/ year in installed capacity. If demand growth disappoints, utilization rates could fall, pressuring pricing and margins.

Environmental regulations pose increasing challenges. The cement industry contributes approximately 8% of global CO2 emissions, making it a target for climate regulations. Carbon taxes or emission trading schemes could significantly impact cost structures, particularly for older, less efficient plants.

Technology disruption, while distant, remains a long-term threat. Alternative construction materials, 3D printing technologies, or breakthrough innovations in low-carbon cement could disrupt traditional business models. UltraTech's scale, while an advantage today, could become a liability if technology shifts rapidly.

The diversification into wires and cables introduces execution risk. If the strategy of diversification does not succeed, then it could lead to capital misallocation. The consolidated margins for the company may see a dip considering wires and cables are low margins business. While cement has been a negative working cycle business for - UltraTech as mentioned by them in conference calls, foray into new business will require higher working capital and will change the dynamics.

Competition from new entrants, particularly the Adani Group, threatens market share and pricing discipline. This acquisition raises the Adani Group's overall cement capacity to 77.40 MTPA, with plans to expand to 106 MTPA by FY26. Adani's aggressive expansion could trigger market share battles that compress industry margins.

Bull Case: Infrastructure Supercycle and Market Leadership

The bull case rests on India's infrastructure supercycle. S&P Global Ratings believes this expansion will be well supported by demand--the Indian government plans to spend US$1.7 trillion on infrastructure projects through to 2030, according to Crisil. This will vastly raise cement consumption in the country. This unprecedented infrastructure spending provides multi-year demand visibility.

However, at 280 kilograms (kg) per person, the country's per capita consumption is well below the world average of 500 kg-550 kg. This presents a significant growth opportunity for the cement companies as India continues to urbanize and invest in infrastructure. The convergence toward global averages implies decades of growth potential.

Housing demand adds another growth layer. The PM Awas Yojana for rural India has 34.9 million registered beneficiaries as of November 2024 with 26.6 million houses already being completed. For Urban India, the same scheme is being implemented with an investment of USD95.9 billion and has completed 8.7 million houses, out of 11.8 million sanctioned. Each house drives cement demand, creating a multi-year demand pipeline.

UltraTech's market leadership position provides pricing power. As the largest player with the best distribution network, UltraTech can maintain price premiums while gaining market share. The ability to supply large projects end-to-end creates competitive advantages that translate into superior returns.

The sustainability initiatives position UltraTech for a carbon-constrained future. Combined with its 342 MW in Waste Heat Recovery Systems (WHRS), UltraTech's total green energy capacity has now reached 1.363 GW, which will cover about 46% of UltraTech's current power needs. These investments, while costly today, will become competitive advantages as carbon costs rise.

Valuation and Multiples Analysis

At current valuations, UltraTech trades at approximately 25x P/E and 15x EV/EBITDA—premiums to both historical averages and peer valuations. The premium reflects market leadership, superior execution, and growth optionality through diversification.

The valuation must be contextualized against growth prospects. However, ICRA projects a 7-8% growth for FY25, driven by strong demand in infrastructure and housing. With capacity expansion and market share gains, UltraTech's volume growth should exceed industry averages, justifying premium valuations.

The sum-of-parts valuation reveals hidden value. The cement business alone justifies current valuations, meaning the building solutions and wires/cables ventures represent free optionality. If these diversifications succeed, significant value creation is possible.

Comparison with global peers suggests upside potential. International cement majors trade at higher multiples despite lower growth prospects, suggesting UltraTech's valuation could re-rate as India's growth story gains global recognition.

The Investment Decision

UltraTech represents a classic quality growth story in a cyclical industry. The investment case hinges on belief in India's infrastructure story, confidence in management execution, and willingness to pay for market leadership.

For long-term investors, UltraTech offers exposure to India's infrastructure transformation with the safety of market leadership and proven execution. The diversification initiatives provide optionality while the core cement business generates steady cash flows.

For value investors, the premium valuation may be concerning, but the quality of assets, strength of market position, and duration of growth opportunity arguably justify the premium. The ability to compound capital at mid-teen returns over decades is rare in commodity businesses.

The key risk is that market leadership attracts regulatory scrutiny or competitive response that erodes advantages. However, the track record suggests management can navigate these challenges while continuing to create value.

Ultimately, UltraTech isn't just a cement investment—it's a bet on India's transformation from emerging to developed economy. As India builds its future—literally—UltraTech will provide the foundation. For investors who share this vision, UltraTech offers a compelling way to participate in one of the world's great growth stories.

X. Future Scenarios & Strategic Questions

The future of UltraTech Cement hinges on several critical uncertainties that will shape not just the company but India's entire infrastructure landscape. As we look toward 2030 and beyond, the strategic questions facing UltraTech reveal broader tensions about growth, sustainability, competition, and technological change.

Can UltraTech Maintain Dominance as Industry Consolidates?

The cement industry's evolution toward oligopoly seems inevitable, but UltraTech's ability to maintain leadership is not guaranteed. India's Cement Industry is poised for consolidation. In the recent past, we have seen multiple large & small acquisitions in the cement segment for consolidating positions. Moving towards the world trend, India will have dominant 3-4 companies controlling substantial cement capacity.

The Adani Group's aggressive entry has fundamentally altered competitive dynamics. With deep pockets and infrastructure synergies through ports and power assets, Adani could potentially outbid UltraTech for future acquisitions. The question becomes whether UltraTech can maintain its acquisition-led growth strategy when facing an equally capitalized competitor.

Market share caps could emerge as a regulatory constraint. If UltraTech approaches 30-35% market share nationally, competition authorities might block further acquisitions. This would force a shift from inorganic to organic growth, fundamentally altering the company's expansion playbook.

Regional dynamics add complexity. While UltraTech dominates nationally, regional players maintain strong positions in specific geographies. The future might see a barbell structure—national giants like UltraTech and Adani controlling 60% of capacity, with resilient regional champions holding the remainder. UltraTech's challenge is preventing regional players from consolidating into national competitors.

Green Cement and Carbon Neutrality Challenges

The sustainability transition represents both UltraTech's greatest challenge and biggest opportunity. Cement production inherently involves limestone calcination, which releases CO2 regardless of energy source. This process emissions problem has no easy solution, making cement one of the hardest industries to decarbonize.

A prominent trend in the India cement market is the growing adoption of green cement and sustainable construction practices. As environmental awareness increases and regulatory pressures intensify, cement manufacturers are investing heavily in developing eco-friendly products. Green cement, which incorporates alternative materials like fly ash, slag, and silica fume, significantly reduces carbon dioxide emissions compared to traditional Portland cement.

UltraTech's response has been multi-pronged but incremental. The investments in renewable energy address scope 2 emissions but don't solve the fundamental process emissions challenge. The company needs breakthrough innovation—whether carbon capture and storage, alternative binders, or revolutionary new materials—to achieve true carbon neutrality.

The economic implications are staggering. Carbon capture could add $50-100 per tonne to production costs, fundamentally altering industry economics. The question is whether customers will pay green premiums or whether regulations will level the playing field by penalizing high-carbon alternatives.

International carbon border adjustments could reshape trade flows. If developed countries impose carbon tariffs, India's cement exports could become uncompetitive. Conversely, if India moves faster on decarbonization than peers, it could create export opportunities. UltraTech's strategic choice—whether to lead or follow on sustainability—will define its global competitiveness.

International Expansion Possibilities

UltraTech's international presence remains limited despite being the third-largest global player outside China. The strategic question is whether to remain India-focused or pursue meaningful international expansion.

Africa presents the most obvious opportunity. With demographics similar to India's but 20 years behind in development, Africa offers decades of growth potential. UltraTech's experience building in challenging environments and managing complex logistics could provide competitive advantages. However, political risk, currency volatility, and local competition present significant challenges.

Southeast Asia offers geographic proximity and cultural familiarity. Markets like Bangladesh, Vietnam, and Indonesia are growing rapidly but already have established players. The question is whether UltraTech can replicate its India consolidation strategy in these markets or whether local champions will prove too entrenched.

Developed markets seem unlikely targets given low growth and high valuations. However, technology or sustainability leadership could create niche opportunities. If UltraTech develops breakthrough green cement technology, it could license or export to developed markets facing stringent regulations.