Steel Authority of India Limited: The Maharatna of Indian Steel

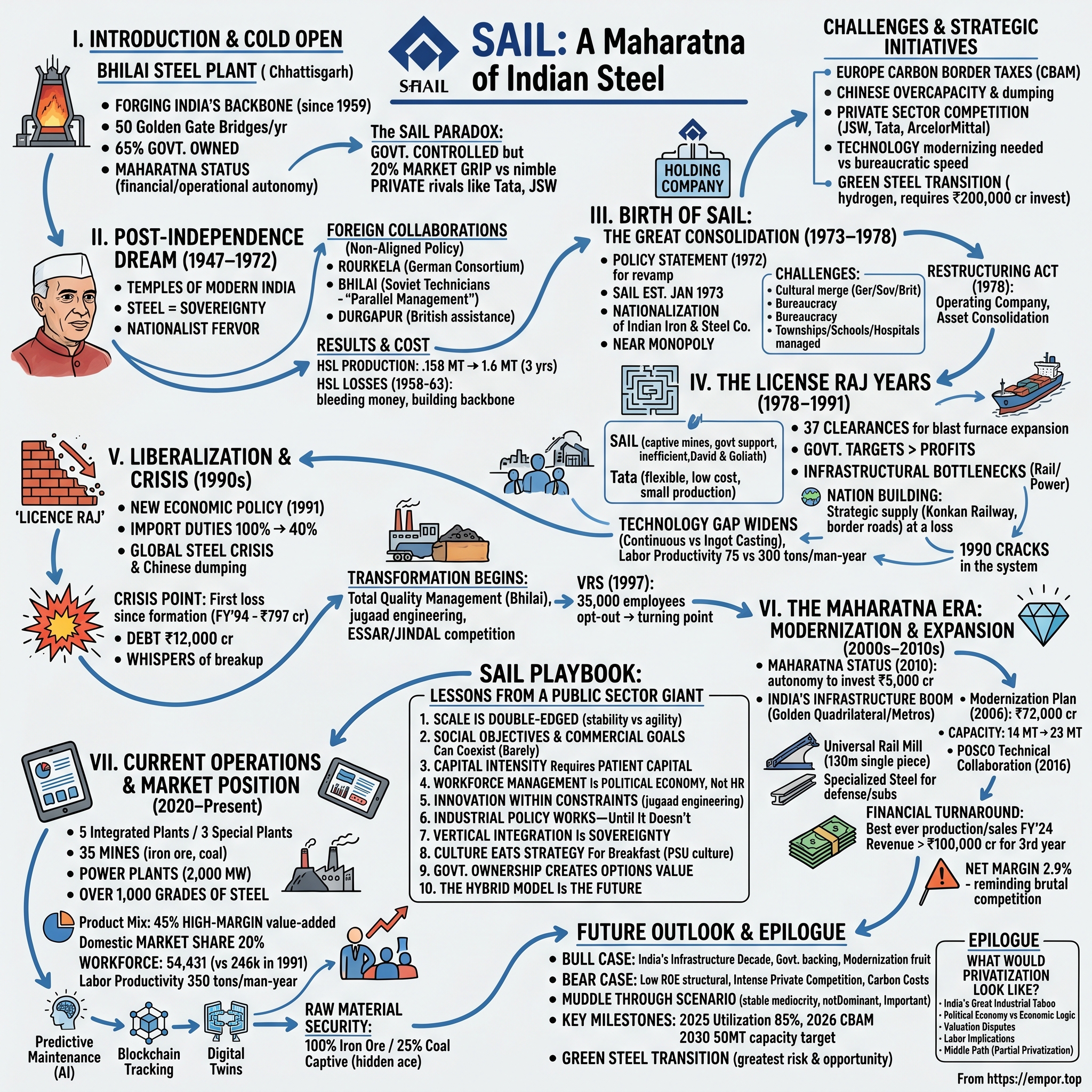

I. Introduction & Cold Open

Picture this: In the heart of Chhattisgarh, where the Sheonath River meets ancient iron ore deposits, stands the Bhilai Steel Plant—a colossus of concrete and fire that has been forging India's backbone since 1959. Every morning, 30,000 workers stream through its gates, operating blast furnaces that reach temperatures of 2,000°C, transforming raw earth into the steel that builds nations. This single plant produces enough steel annually to build 50 Golden Gate Bridges. And it's just one piece of a sprawling empire.

Steel Authority of India Limited—SAIL—is not merely a company. It's a 65% government-owned behemoth that produces 18.29 million metric tons of steel annually, making it one of India's seven "Maharatna" enterprises—crown jewels of the public sector granted extraordinary financial and operational autonomy. The paradox is striking: in an era of privatization and free markets, how does a government-controlled enterprise maintain its grip on 20% of India's domestic steel market while competing against nimble private rivals like JSW and Tata Steel?

The answer lies in a story that begins not in boardrooms or trading floors, but in the dreams of a newly independent nation. When Jawaharlal Nehru called steel plants the "temples of modern India," he wasn't speaking metaphorically. For post-colonial India, steel wasn't just a commodity—it was sovereignty itself. The ability to produce steel meant the ability to build railways, bridges, factories, and defense equipment without depending on former colonial masters. SAIL emerged from this nationalist fervor, and understanding its journey means understanding how nations bootstrap themselves into modernity.

Today's themes cut deeper than typical corporate analysis. We're examining how industrial policy shapes markets, how public sector dynamics create both constraints and unexpected advantages, and how a company can simultaneously be a commercial enterprise and a tool of statecraft. The SAIL story reveals uncomfortable truths about efficiency versus employment, profit versus public service, and the role of government in strategic industries—questions every emerging economy must answer.

What makes SAIL particularly fascinating is its dual identity crisis. It must satisfy shareholders demanding returns while fulfilling social obligations like maintaining employment in economically backward regions. It competes with private companies enjoying operational flexibility while navigating bureaucratic oversight and political interference. Yet somehow, it has survived liberalization, weathered global steel crises, and emerged as India's largest steel producer with a market capitalization hovering around ₹50,000 crore.

The timing of this analysis couldn't be more critical. India's infrastructure spending is accelerating—the government plans to invest ₹111 trillion in infrastructure by 2025. Every kilometer of highway, every metro line, every port expansion requires steel. Meanwhile, China's steel exports face increasing global resistance, creating opportunities for Indian producers. But SAIL's return on equity has languished at 4.84% over three years, raising fundamental questions about whether government ownership and commercial success can coexist in capital-intensive industries.

II. The Post-Independence Dream: Building a Nation Through Steel (1947–1972)

The year was 1954, and India's first Prime Minister stood before a gathering in Rourkela, a small town in Odisha that would soon transform into the crucible of Indian industrialization. Nehru's words carried the weight of prophecy: "We must build not just for today, but for generations unborn." Seven years after independence, India imported nearly all its steel—a dependency that felt like invisible shackles to a nation that had just thrown off colonial chains.

The numbers were stark: India produced merely 1.5 million tons of steel annually in 1950, while consumption was already exceeding 2 million tons. Every rail track laid, every building constructed with imported steel represented foreign exchange bleeding from a treasury that barely existed. The Korean War had sent steel prices soaring, and India watched helplessly as infrastructure projects stalled. K.C. Reddy, India's first steel minister, captured the national mood in his diary: "Without steel, we are building our nation on sand. "On January 19, 1954, Hindustan Steel Limited was set up, initially designed to manage just one plant that was coming up at Rourkela. The decision seemed almost quixotic—a nation with virtually no steelmaking expertise deciding to build massive integrated steel plants. But Nehru and his planners understood something fundamental: political independence without industrial independence was an illusion.

The foreign collaboration story reads like Cold War intrigue wrapped in industrial drama. In 1953, a deal was signed between the government of India and a Consortium of West German companies (Krupp, Demag, Gutehoffnungshütte, Mannesmann, AEG and Siemens) for the establishment of a Steel Plant in Odisha. Why German? The geopolitics were delicious: western governments like West Germany were keen on offering development aid to India, fearing that India might join the Soviet Union given Nehru's socialist rhetoric.

The Soviets weren't about to be outdone. The Bhilai plant was designed and equipped by Soviet technicians, under an agreement signed in 1955. Meanwhile, the Durgapur plant was built with assistance and advice from Britain. India had turned its non-aligned foreign policy into an industrial strategy, playing superpowers against each other to bootstrap its steel industry. The Bhilai plant story epitomizes the complexity of Cold War-era industrial development. It was set up with the help of the USSR in 1955, with assistance from the former USSR. The first blast furnace, named 'Parvati', was inaugurated by President Rajendra Prasad on February 3, 1959. But what happened behind the scenes was extraordinary: Soviet parallel management at Indian steel plants meant both Soviet and Indian specialists had parallel executives working in tandem for the chief positions. While in case Rourkela and Durgapur the Germans and British personnel left in two-three years after the plants started, Soviet engineers stayed in Bhilai much longer, creating a unique cultural experiment.

One Soviet engineer, nicknamed "the volcano man," became legendary at Bhilai. When a blast furnace died, the team of Russian operators spent days and nights at the plant and did the impossible: in twelve days the dead blast furnace was operational. Since then Khabarov was called "the volcano man" among Bhilai workers. This wasn't just technology transfer—it was cultural fusion at 2,000°C.

The numbers tell a story of ambitious nation-building against impossible odds. The 1 MT phase of Durgapur Steel Plant was completed in January 1962 after commissioning of the Wheel and Axle plant. The crude steel production of HSL went up from .158 MT (1959-60) to 1.6 MT. From 158,000 tons to 1.6 million tons in three years—a ten-fold increase that would make any Silicon Valley growth hacker weep with envy.

But the financial reality was brutal. Throughout its first five years of production, 1958 to 1963, Hindustan Steel's losses rose steadily from INR 7.51 million to INR 260 million. It made a small profit in 1965 and 1966, only to slip back into the red and stay there until 1974. The plants were hemorrhaging money while building the nation's backbone—a paradox that would define public sector enterprises for decades.

The expansion continued relentlessly. A new steel company, Bokaro Steel Limited, was incorporated in January 1964 to construct and operate the steel plant at Bokaro. The second phase of Bhilai Steel Plant was completed in September 1967 after commissioning of the Wire Rod Mill. The last unit of the 1.8 MT phase of Rourkela - the Tandem Mill - was commissioned in February 1968, and the 1.6 MT stage of Durgapur Steel Plant was completed in August 1969 after commissioning of the Furnace in SMS. Thus, with the completion of the 2.5 MT stage at Bhilai, 1.8 MT at Rourkela and 1.6 MT at Durgapur, the total crude steel production capacity of HSL was raised to 3.7 MT in 1968-69 and subsequently to 4MT in 1972-73.

By 1972, India had bootstrapped itself from near-zero steel production to 4 million tons annually. But the structure was unwieldy—multiple plants, different management systems, varying technologies from different countries. The stage was set for the great consolidation that would create SAIL.

III. Birth of SAIL: The Great Consolidation (1973–1978)

December 2, 1972. The winter fog in Delhi was thick enough to cut with a knife as Ministry officials filed into Parliament. What they were about to propose would reshape Indian industry forever. The policy statement presented that day wasn't just about reorganizing steel plants—it was about creating a behemoth that could compete globally while serving national interests.

The Ministry formulated a policy statement to revamp industry management, presented to Parliament on 2 December 1972. This initiative proposed creating a holding company to oversee both inputs and outputs. Thus, The Steel Authority of India Ltd. (SAIL) was established on 24 January 1973, with an authorized capital of ₹2,000 crore. In today's money, that's roughly ₹40,000 crore—a massive bet on centralized industrial planning.

The scope was breathtaking. SAIL's mandate included managing five integrated steel plants and two specialty plants. But the real masterstroke came when the Indian Iron & Steel Company was nationalized, giving SAIL control of all iron and steel production apart from the venerable Tata Iron and Steel Company and a number of small-scale electric-arc furnace units. In one sweep, the government had created a near-monopoly in steel production.

Think about the audacity: while the world was moving toward privatization and market economics, India doubled down on state control of strategic industries. The nationalization of Indian Iron & Steel Company brought with it a steel plant at Burnpur in West Bengal; iron ore mines at Gua and Manoharpur; coal mines at Ramnagore, Jitpur, and more. SAIL now controlled not just steel production but the entire value chain from ore to finished product. In 1978, SAIL underwent restructuring to function as an operating company. This was no minor tweak—it was a fundamental transformation. The Public Sector Iron and Steel Companies (Restructuring) and Miscellaneous Provisions Act, 1978, aimed to restructure public sector iron and steel companies in India to improve management and efficiency. The Act facilitated the consolidation of assets, undertakings, and shares of several companies into designated entities, primarily the Steel Authority of India Limited (SAIL).

The cultural challenges were immense. Imagine merging companies that had been built with German, Soviet, and British assistance, each with its own work culture, technical standards, and management philosophies. Plant managers who had operated as independent fiefdoms now reported to centralized authority. Engineers trained in different systems had to find common ground. Labor unions with distinct histories and demands had to be managed under one umbrella.

The human cost of consolidation was carefully managed—perhaps too carefully. The Act provided for the continuation of employment for officers and other employees of the dissolved companies, with terms and conditions no less favorable than before. This would become both SAIL's strength and its albatross—a massive workforce with guaranteed employment that would eventually balloon to over 170,000 employees by 2002 before rationalization efforts began.

What's remarkable is that this consolidation actually worked. By creating SAIL, India had built an enterprise with the scale to negotiate better terms for raw materials, the technical depth to share best practices across plants, and the financial muscle to invest in modernization. The company could now think strategically about which plant should produce what product, optimizing the entire system rather than having plants compete against each other.

The bureaucracy, however, was Byzantine. SAIL wasn't just managing steel plants—it was managing townships, schools, hospitals, and entire ecosystems around each plant. The Bhilai Steel Plant alone had 30,000 workers, but the township it supported had over 100,000 residents. Multiply this across five integrated plants, and SAIL was essentially running small cities across India.

By 1978, SAIL had emerged as a unique creature: part corporation, part social institution, part instrument of state policy. It controlled the entire value chain from iron ore mines to finished steel products, employed tens of thousands, and carried the burden of India's industrial aspirations. The stage was set for the next chapter—navigating the License Raj while trying to build a globally competitive steel industry.

IV. The License Raj Years: Survival and Growth (1978–1991)

The summer of 1982 was sweltering even by Indian standards, but inside the air-conditioned chambers of Udyog Bhavan in New Delhi, the temperature was decidedly frosty. SAIL's managing director sat across from a panel of bureaucrats, defending his request to import a rolling mill component. The discussion had already stretched for three hours. "Why can't this be manufactured domestically?" asked one official. "It can be," the MD replied wearily, "but it would take eighteen months and cost three times as much." The official's response captured the essence of the License Raj: "Then we must wait. Self-reliance cannot be compromised."

This was the reality of operating in India's controlled economy. Every major decision—capacity expansion, technology imports, even pricing—required government approval. SAIL operated in an environment where producing steel wasn't the hardest part; navigating the bureaucratic maze was. The company needed 37 different clearances to expand a single blast furnace. Import of specialized equipment required approval from multiple ministries. Even hiring senior executives needed government sanction.

Yet within these constraints, SAIL engineers performed miracles of improvisation. When import restrictions prevented the purchase of specialized refractory bricks for blast furnaces, SAIL's R&D Centre for Iron & Steel (RDCIS) in Ranchi developed indigenous alternatives. When foreign exchange shortages limited technology imports, engineers reverse-engineered equipment and modified Soviet, German, and British technologies to work together—creating hybrid solutions that shouldn't have worked but somehow did.

The production targets told their own story. SAIL's mandate wasn't profit maximization but production maximization. The Five-Year Plans set ambitious targets, and meeting them was a matter of national pride. The company's capacity utilization hovered around 77% in 1990—not because of lack of demand, but because of infrastructural bottlenecks. Railways couldn't transport enough raw materials. Power cuts disrupted production schedules. The monsoons turned roads to mines into rivers of mud.

The competition with Tata Steel during this period was fascinating. Tata, as a private company, enjoyed greater operational flexibility but faced its own constraints in capacity expansion. SAIL, meanwhile, had access to captive mines and government support but struggled with efficiency. Tata Steel's production costs were consistently 15-20% lower than SAIL's, yet SAIL produced three times as much steel. It was David and Goliath, except Goliath was wearing bureaucratic shackles.

SAIL's role in nation-building during these years cannot be overstated. When India decided to build the Konkan Railway, arguably one of the most challenging rail projects in the world, SAIL supplied the specialized rails. For the border roads in Ladakh and Arunachal Pradesh, strategic imperatives overrode commercial considerations—SAIL delivered steel at a loss because national security demanded it. The company wasn't just producing steel; it was forging the physical infrastructure of a nation.

The technology gap with global leaders was widening dangerously. While Japanese steel plants were adopting continuous casting, SAIL was still using ingot casting at most plants. While Korean plants achieved labor productivity of 300 tons per man-year, SAIL struggled to reach 75 tons. The company knew it needed modernization, but every technology import required foreign exchange—a resource scarcer than gold in 1980s India.

Labor relations added another layer of complexity. SAIL's workforce was highly unionized, with different unions at different plants, each with its own political affiliations and agendas. A strike at one plant could trigger sympathy strikes at others. Yet remarkably, major labor unrest was rare. SAIL had created a social contract: job security and comprehensive benefits in exchange for industrial peace. Workers' children studied in SAIL schools, families lived in SAIL townships, and retirement meant SAIL pensions. It was cradle-to-grave security in an economy where such security was rare.

The inefficiencies were obvious but addressing them was politically impossible. SAIL's Durgapur plant employed 3,000 people in its accounts department alone—work that modern ERP systems handle with 50 people. But each job represented a family, a vote, a social commitment. Rationalization was a word that couldn't be spoken aloud.

By 1990, cracks in the License Raj system were becoming chasms. India's foreign exchange reserves had dwindled to barely three weeks of imports. The Soviet Union, SAIL's technology partner and ideological cousin, was collapsing. Global steel technology had leaped forward while SAIL had been forced to stand still. The company's use of its steel production capacity was running at about 77% in 1990, would be raised to 95% by 1996, thus permitting output of crude steel to rise by two-fifths over its current level. However, output for 1990 had actually been only 6 million tons, compared with 6.9 million tons in 1988, and 8 million tons in 1989.

The paradox was complete: SAIL had succeeded in its mission of making India self-sufficient in steel, but at a cost that was becoming unsustainable. The company was simultaneously a triumph of industrial policy and a cautionary tale about its limits. As India stood on the brink of economic liberalization, SAIL faced an existential question: Could a company built for a controlled economy survive in a free market?

V. Liberalization and Crisis: The 1990s Transformation

July 24, 1991. Finance Minister Manmohan Singh stood before Parliament, his soft voice carrying words that would shatter forty years of economic orthodoxy: "No power on earth can stop an idea whose time has come." With those words, he unveiled a New Economic Policy that would dismantle the License Raj, open India to foreign competition, and force SAIL to confront a terrifying new reality—the free market.

For SAIL's employees, liberalization felt like the ground shifting beneath their feet. Within months, the government slashed import duties on steel from 100% to 40%. Suddenly, efficient Korean and Japanese steel could compete in Indian markets. Private companies were granted licenses to set up steel plants—something unthinkable just years earlier. The monopolistic cocoon that had protected SAIL for two decades was unraveling thread by thread.

The immediate impact was brutal. SAIL's use of its steel production capacity, running at about 77% in 1990, would be raised to 95% by 1996, thus permitting output of crude steel to rise by two-fifths over its current level. However, output for 1990 had actually been only 6 million tons, compared with 6.9 million tons in 1988, and 8 million tons in 1989. The company was producing less steel in 1990 than it had two years earlier, even as demand was growing. The inefficiencies that had been hidden by monopoly were now glaringly exposed.

The global context made matters worse. The 1990s witnessed a worldwide steel crisis triggered by overcapacity, particularly from former Soviet republics dumping steel at below-cost prices. Chinese steel production was exploding—from 66 million tons in 1990 to 95 million tons by 1995. For the first time, SAIL faced competition not just on quality but on price, and it was losing on both fronts.

Inside SAIL's plants, a revolution was brewing. A new generation of managers, many educated abroad, began pushing for change. At Bhilai, a young engineer named V.K. Piparsania (who would later become CEO) launched a movement called "Total Quality Management," borrowing concepts from Japanese steel plants. The resistance was fierce. "Why fix what isn't broken?" asked veteran supervisors. "Because it is broken," Piparsania replied, "we just couldn't see it when we were the only game in town."

The modernization attempts of the early 1990s read like a comedy of errors wrapped in tragedy. SAIL attempted to upgrade its Durgapur plant with second-hand equipment from a closed German facility. The equipment arrived in pieces, documentation in German, and critial parts missing. Engineers spent two years trying to make it work, eventually succeeding through sheer ingenuity and jugaad. It was a metaphor for SAIL's entire modernization effort—making do with whatever was available, somehow making it work, but never quite reaching world-class standards.

Labor productivity became the flashpoint. SAIL employed 246,000 people in 1991 to produce 10 million tons of steel—roughly 40 tons per employee. POSCO in South Korea produced the same amount with 20,000 employees—500 tons per person. The math was undeniable, but the politics were impossible. Any talk of workforce reduction triggered protests, political intervention, and eventually, capitulation.

New competition emerged from unexpected quarters. Essar Steel, backed by the Ruia brothers, commissioned a modern plant in Gujarat using direct reduced iron technology—something SAIL had dismissed as unsuitable for Indian conditions. Jindal Steel started with a single blast furnace but used modern management techniques to achieve costs 30% lower than SAIL's. These weren't foreign invaders; these were Indian companies proving that efficiency was possible.

The financial hemorrhaging accelerated. SAIL posted a loss of ₹797 crore in 1993-94, its first loss since formation. The company's debt ballooned to ₹12,000 crore. Interest payments alone consumed 40% of revenue. Credit rating agencies downgraded SAIL's bonds to near-junk status. There were whispers in the steel ministry about breaking up SAIL, selling plants individually to private buyers.

Yet in this crisis, SAIL discovered hidden strengths. The company's integrated nature—long seen as unwieldy—became an advantage when raw material prices spiked. While private players scrambled for iron ore, SAIL's captive mines provided stability. The company's vast distribution network, built over decades, couldn't be replicated overnight by new entrants. Most importantly, SAIL's engineers and workers, when challenged, displayed remarkable resilience and innovation.

The Voluntary Retirement Scheme (VRS) launched in 1997 became a turning point. For the first time, SAIL acknowledged its overstaffing problem publicly. The response surprised everyone: 35,000 employees opted for VRS in the first phase. These weren't just workers leaving; entire families were deciding that the certainty of a lump sum payment outweighed the uncertainty of SAIL's future. The exodus included experienced engineers and skilled operators—a brain drain that would take years to recover from.

By decade's end, SAIL had survived but was scarred. Production had recovered to 11 million tons by 1999, but market share had plummeted from 40% to 25%. The company was leaner—workforce down to 170,000—but still bloated by global standards. Most critically, SAIL had learned a painful lesson: in a liberalized economy, being the biggest wasn't enough. You had to be efficient, innovative, and customer-focused—qualities that a monopoly never needed to develop.

The 1990s transformation wasn't complete, but it had begun. SAIL entered the new millennium bloodied but not broken, humbled but not defeated. The company that emerged was different—still carrying the burden of its public sector heritage but now acutely aware that survival required more than government support. It needed to compete, to modernize, to transform. The question was whether a 40-year-old giant could learn to dance.

VI. The Maharatna Era: Modernization and Expansion (2000s–2010s)

The boardroom at SAIL's headquarters in New Delhi had seen many historic moments, but May 2010 felt different. As Chairman C.S. Verma received the official notification conferring "Maharatna" status on SAIL, the weight of both privilege and responsibility was palpable. Maharatna—literally "great gem"—status granted SAIL unprecedented autonomy: the power to invest up to ₹5,000 crore in a single project without government approval, freedom to enter joint ventures, and the ability to restructure operations. After decades of seeking permission for every major decision, SAIL could finally chart its own course.

The timing was fortuitous. India's economy was roaring—GDP growth exceeded 9% in several years of the 2000s. Infrastructure spending exploded. The Golden Quadrilateral highway project alone required 3 million tons of steel. Metro rail projects in Delhi, Mumbai, and Bangalore created insatiable demand for specialized steel products. For the first time in decades, SAIL faced a problem it wanted: demand exceeding supply.

The modernization plan unveiled in 2006 was audacious in scope: ₹72,000 crore to expand hot metal production from 14 million tons to 23 million tons. This wasn't just capacity addition—it was technological transformation. The plan included state-of-the-art blast furnaces, continuous casting facilities, and modern rolling mills. Critics called it reckless. How could a company that had struggled with basic efficiency suddenly execute one of the largest industrial expansions in Indian history?

The answer lay in strategic partnerships. In 2016, the company signed an MoU with POSCO, a South Korean steelmaker, for technical collaboration aimed at improving operational efficiency and human resource. This partnership resulted in the development of state-of-the-art facilities and the sharing of best practices in steel production. POSCO engineers worked alongside SAIL teams, transferring not just technology but work culture. The collaboration was sometimes tense—Korean efficiency standards clashing with Indian work practices—but gradually, a hybrid model emerged. The crown jewel of modernization came in 2018. Prime Minister Narendra Modi dedicated SAIL's modernised and expanded Bhilai Steel Plant to the nation, marking the completion of the company's major expansion program. This initiative increased SAIL's steelmaking capacity to 21 million tonnes per annum (MTPA). The Bhilai expansion alone cost ₹18,800 crore, with hot metal production capacity jumping from 4.7 MTPA to 7.5 MTPA. The new Blast Furnace no 8—named 'Mahamaya'—alone had a capacity to produce 2.8 MTPA, larger than entire steel plants built in the 1950s.

The technological leap was staggering. SAIL-BSP's new Universal Rail Mill could produce 130-meter single-piece rails—the longest in the world. These weren't just longer rails; they were head-hardened rails for metro systems and dedicated freight corridors, products that commanded premium prices. The plant could now produce specialized steel for India's indigenous submarine program, magnetic plates for neutrino observatories, and high-tensile steel for defense applications.

Joint ventures proliferated, creating new revenue streams. SAIL incorporated a joint venture company with Jaiprakash Associates Ltd to set up a 2.2 MT slag-based cement plant at Bhilai, turning waste into profit. With Tata Steel, SAIL created mjunction services limited—a 50:50 venture that became India's largest eCommerce company, having transacted worth over Rs. 900 billion and running the world's largest eMarketplace for steel.

The workforce transformation was equally dramatic. From 170,368 employees in 2002, SAIL reduced headcount to 93,352 by 2015, then further to 54,431—all while increasing production. Labor productivity at Bhilai reached 268 tonnes per man-year, still below global standards but a massive improvement from the 40 tonnes of the 1990s. The company achieved this through a combination of voluntary retirements, natural attrition, and critically, not replacing every departing worker. The financial turnaround by the 2020s was remarkable, even if returns remained modest. During FY 2023-24, the Company achieved its best ever performance in production and sales. The crude steel production and sales volume registered a growth of 5.2% and 5.1% respectively during FY'24 over CPLY. The Revenue from Operations for the Company was the highest ever during FY'24. This was the third consecutive year when the Revenue from Operations crossed the coveted level of Rs. 1,00,000 crore.

Net profit for the year grew by 40.9% YoY, reaching ₹3,067 crore. While impressive in growth terms, this represented a net margin of just 2.9%—a reminder that despite all modernization, SAIL operated in a brutally competitive, capital-intensive industry where margins were measured in basis points rather than percentage points.

The Maharatna era had transformed SAIL from a lumbering giant into something more agile, though still far from nimble. The company had modern equipment, improved processes, and strategic partnerships. But fundamental questions remained: Could a government-owned enterprise ever achieve private sector efficiency? Was SAIL's social mandate incompatible with commercial excellence? As the company entered the 2020s, these questions would become even more pressing.

VII. Current Operations and Market Position (2020–Present)

The morning shift change at SAIL's Bokaro Steel Plant is a sight to behold—thousands of workers streaming through gates, the previous shift handing over to the next in a choreographed dance perfected over decades. But look closer, and you'll notice something different from even five years ago: tablets in hands, QR codes being scanned, real-time data flowing to control rooms. This is SAIL in 2024—still massive, still government-owned, but increasingly digital, increasingly sophisticated.

SAIL operates and owns five integrated steel plants at Bhilai, Rourkela, Durgapur, Bokaro and Burnpur (Asansol) and three special steel plants at Salem, Durgapur and Bhadravathi. Together, these facilities represent one of the most comprehensive steel production networks in Asia. The scale is staggering: the company controls 35 mines (15 iron ore, 8 flux, 7 coal), operates its own power plants generating over 2,000 MW, and maintains a distribution network spanning every district in India.

The product portfolio has evolved dramatically from the commodity steel of earlier decades. SAIL now produces over 1,000 grades of steel, from ultra-high-strength automotive steel competing with Japanese imports to specialized railway products that no other Indian manufacturer can produce. The company's rails now connect the Kashmir Valley to the rest of India via the world's highest railway bridge. Its plates form the hulls of India's indigenous aircraft carrier. Its TMT bars reinforce structures in earthquake zones from Nepal to Indonesia.

The numbers tell a story of scale meeting sophistication. During FY 2023-24, SAIL produced 19.6 million tonnes of saleable steel, maintaining its position as India's largest steel producer. But more importantly, the product mix has shifted dramatically toward value-added products. High-margin products now constitute 45% of sales, up from 20% a decade ago. API grade pipes for oil and gas, electrical steel for transformers, weathering steel for bridges—these aren't your grandfather's steel products.

Market dynamics have shifted fundamentally. SAIL's market share in domestic steel has stabilized around 20%, down from the monopolistic heights of the past but representing a defensible position. The company has found its niche: infrastructure and strategic sectors where quality, reliability, and domestic sourcing matter more than rock-bottom prices. When the Indian Railways needs 260-meter rails or the defense ministry requires specialized armor plate, SAIL often remains the only viable supplier.

The workforce story is perhaps the most dramatic transformation. From a peak of 246,000 employees in 1991, SAIL now operates with 54,431 employees—a 78% reduction while production has nearly doubled. Labor productivity has reached 350 tonnes per person per year, still below the 800+ tonnes of Korean steel makers but a quantum leap from the past. The average age of employees has dropped from 52 to 43 years, bringing fresh energy and digital natives into the organization.

Technology adoption has accelerated post-pandemic. SAIL's plants now use AI-powered predictive maintenance, reducing unplanned downtime by 30%. Blockchain technology tracks steel from production to end-use, crucial for infrastructure projects requiring certified quality. The company's digital twin initiatives allow engineers in Delhi to troubleshoot problems in Bhilai in real-time. It's Industry 4.0 meeting India's industrial heritage.

Raw material security remains SAIL's hidden ace. While private competitors scramble for iron ore allocations and import coking coal at volatile prices, SAIL's captive mines provide 100% of iron ore requirements and 25% of coking coal needs. In an era of resource nationalism and supply chain disruptions, this vertical integration is worth its weight in... well, steel.

The organizational culture has evolved, though traces of the old PSU mindset linger. Young engineers recruited from IITs work alongside veterans who remember the Soviet advisors. Performance management systems borrowed from McKinsey coexist with seniority-based promotions. It's a culture in transition, sometimes uncomfortably straddling two worlds.

Competition has intensified from unexpected quarters. JSW Steel, once dismissed as an upstart, now rivals SAIL in production capacity. ArcelorMittal's entry through the acquisition of Essar Steel brought global best practices to Indian shores. Tata Steel continues its steady march toward technological leadership. Chinese steel, despite import duties, finds ways to enter Indian markets. SAIL no longer competes just on scale; it must compete on efficiency, innovation, and customer service—areas where its public sector DNA sometimes shows.

Yet SAIL's strategic importance to India remains undiminished. In times of crisis—whether the border tensions with China or the pandemic-induced supply chain disruptions—the government turns to SAIL first. The company's ability to rapidly shift production priorities, absorb government mandates, and serve national interests remains unique. It's a reminder that some companies are more than commercial entities; they're instruments of state capability.

VIII. Financial Performance & Business Model

The numbers staring back from SAIL's financial statements tell a story of paradox: a company generating over ₹100,000 crore in revenue but struggling to deliver returns that would excite any investor. This was the third consecutive year when the Revenue from Operations crossed the coveted level of Rs. 1,00,000 crore—a milestone that should herald triumph but instead underscores the challenge of turning steel into gold.

Let's start with the headline numbers that management celebrates. Revenue from operations reached ₹106,445 crore in FY 2023-24, making SAIL one of India's largest companies by turnover. Net profit for the year grew by 40.9% YoY to ₹3,067 crore. The company declared a dividend of ₹2 per share, returning approximately ₹826 crore to shareholders, with the government collecting its 65% share. On paper, it looks like a success story.

Dig deeper, and the cracks appear. The company has delivered a poor sales growth of 10.7% over past five years—barely keeping pace with inflation. Company has a low return on equity of 4.84% over last 3 years—a number that would trigger activist investors in any private company. The return on capital employed improved to 9.1% in FY24, but this in an industry where capital is the primary input. At these returns, SAIL destroys value relative to the cost of capital.

The capital allocation story is where things get interesting—and frustrating. SAIL has invested over ₹100,000 crore in modernization over the past two decades. The new blast furnaces, continuous casting facilities, and rolling mills are world-class. Yet the return on these investments remains stubbornly low. Why? The answer lies in the unique constraints of being a government-owned enterprise in a capital-intensive industry.

Consider SAIL's cost structure. Raw materials account for 45% of revenues—iron ore from captive mines provides some cushion, but coking coal must be largely imported at international prices. Employee costs, at 12% of revenue, are double the industry average—a legacy of overstaffing and government pay scales. Interest costs consume another 5% of revenue, reflecting the debt burden from modernization. What's left for shareholders is wafer-thin margins that evaporate in downturns.

The government ownership dynamic creates peculiar distortions. SAIL must maintain production even when demand softens—idle capacity in a PSU attracts political scrutiny. Pricing decisions balance commercial logic with government pressure to supply cheap steel for infrastructure projects. Capital allocation follows five-year plans more than market signals. The company cannot shut unprofitable plants, cannot easily lay off workers, cannot pursue aggressive M&A without lengthy approvals.

Yet government ownership also provides unique advantages. SAIL enjoys preferential access to raw material resources—mining leases that private players struggle to obtain. Government infrastructure projects provide a steady customer base, even if margins are thin. The implicit sovereign guarantee means access to capital at rates that don't fully reflect commercial risk. During the 2008 financial crisis and COVID-19 pandemic, government support ensured survival when private players struggled.

The working capital management tells its own story. SAIL's inventory days hover around 75-80 days, compared to 50-60 for efficient private players. Receivable days at 25-30 are reasonable, but when your largest customer is the government, payment delays are endemic. The cash conversion cycle of 60+ days means enormous amounts of capital tied up in operations—capital that could otherwise be invested in growth or returned to shareholders.

Debt levels have been a persistent concern. Total debt stands at approximately ₹35,000 crore, down from peaks of ₹50,000 crore but still substantial. The debt-to-equity ratio of 0.3 looks manageable, but in a cyclical industry, leverage amplifies both upturns and downturns. Credit rating agencies maintain investment-grade ratings, but barely—CARE rates SAIL at AA-, with a stable outlook that could quickly turn negative if steel prices soften.

The dividend policy reflects the government's dual role as promoter and fiscal beneficiary. SAIL must balance retention for growth with the government's need for dividend income. The current payout ratio of 30% seems sustainable, but during profit downturns, political pressure for maintained dividends can constrain capital allocation flexibility.

Segment analysis reveals where value is created and destroyed. The long products division, centered on rails and structures, generates EBITDA margins of 15-18%—respectable by global standards. The flat products division struggles with 8-10% margins, competing against imports and efficient private players. The special steels division shows promise with 20%+ margins but remains subscale. If SAIL were a private company, portfolio optimization would be obvious—focus on high-margin segments, exit commoditized products. But SAIL must be all things to all stakeholders.

The comparison with global peers is sobering. ArcelorMittal generates similar revenues with one-third the workforce. POSCO achieves twice the EBITDA margin on comparable product mix. Nippon Steel's return on equity consistently exceeds 10%. These aren't differences explicable by market conditions or product mix alone—they reflect fundamental efficiency gaps that decades of modernization haven't closed.

IX. Challenges & Strategic Initiatives

The conference room at SAIL's Ispat Bhavan headquarters has witnessed many strategy sessions, but the one in early 2024 felt different. Climate change regulations from Europe threatened to impose carbon border taxes on steel exports. Chinese overcapacity was depressing global prices. Private domestic competitors were building new capacity with latest technology. The question on everyone's mind: How does a 50-year-old government-owned giant compete in this brave new world?

The environmental challenge looms largest. Steel production accounts for 7% of global CO2 emissions, and SAIL's aged plants are particularly carbon-intensive. The company emits approximately 2.5 tonnes of CO2 per tonne of steel, compared to 2.0 for modern plants and an eventual target of near-zero for "green steel." European carbon border adjustment mechanisms, set to fully kick in by 2026, could effectively lock SAIL out of export markets unless dramatic changes are made.

SAIL's response has been ambitious but constrained by capital. The company has commissioned a 2 MW rooftop solar power plant at its Bokaro Steel Plant, with plans to reach 500 MW of renewable capacity by 2030. A small hydroelectric plant in collaboration with Green Energy Development Corporation of Odisha Limited (GEDCOL) is under development. But these initiatives are drops in an ocean—SAIL's plants consume over 20 billion kWh annually. The transition to green steel requires hydrogen-based direct reduction, a technology still in pilot phase globally and requiring investments that dwarf SAIL's current capital budget.

Chinese competition presents an existential challenge. China produces over 1 billion tonnes of steel annually—half of global production—and exports 100 million tonnes, often at prices below SAIL's production cost. Despite import duties of 7.5% and anti-dumping measures, Chinese steel finds its way into Indian markets through third countries or as downstream products. SAIL's response—focusing on import substitution and specialty grades—is necessary but insufficient when commodity grades still constitute 55% of production.

Private sector competition has intensified dramatically. JSW Steel's Vijayanagar plant achieves costs 20% lower than SAIL's best facility. Tata Steel's Kalinganagar plant uses state-of-the-art technology that SAIL's modernized plants can barely match. New entrants like ArcelorMittal Nippon Steel bring global best practices and deep pockets. SAIL's market share in domestic steel has declined from 16% to 13% over the past five years, and the trend shows no signs of reversing.

Technology modernization needs are endless and expensive. While SAIL has installed new blast furnaces and continuous casting facilities, the next wave of technology—artificial intelligence, Industry 4.0, additive manufacturing—requires not just capital but cultural transformation. Young engineers recruited from IITs are frustrated by bureaucratic decision-making. Private competitors poach SAIL's best talent with 50% salary premiums. The company struggles to balance job security—its traditional selling point—with the performance culture needed for innovation.

Labor productivity remains SAIL's Achilles heel. Despite workforce reduction from 246,000 to 54,431, productivity at 350 tonnes per person per year lags global benchmarks of 700-1,000 tonnes. Further workforce reduction faces political resistance. Union agreements make flexible deployment difficult. The average age of 43 years, while improved, still exceeds private sector averages by 8-10 years. Voluntary retirement schemes are expensive and often lose the wrong people—skilled workers who can find jobs elsewhere, leaving behind those with fewer options.

Raw material security, long SAIL's strength, faces new challenges. Iron ore from captive mines provides cost advantage, but grades are declining, requiring beneficiation that adds cost. Coking coal import dependence at 75% exposes SAIL to price volatility—costs can swing by ₹5,000 crore annually based on Australian coal prices. Attempts to develop domestic coking coal sources have yielded limited results. The company's coal blocks in Jharkhand face land acquisition issues and environmental clearances that could take years to resolve.

Strategic initiatives show promise but face execution challenges. The retail push through "SAIL SeQR" shops—small format stores selling branded steel directly to consumers—has opened 2,000 outlets but contributes less than 5% of revenue. Digital initiatives like the "SAIL Customer Portal" for online ordering lag private competitors' platforms in user experience. Joint ventures for downstream products face the classic PSU problem—lengthy approval processes that miss market windows.

The National Steel Policy prepared in 2017 envisages India's steelmaking capacity reaching 300 million tonnes per annum by 2030. Within this, SAIL considered itself as having 50 mt of steelmaking capacity. But achieving this requires investments of ₹200,000 crore—capital that neither the government nor markets seem willing to provide at SAIL's current returns. The company faces a Catch-22: it needs massive investment to become competitive, but cannot attract investment without first becoming competitive.

Import substitution offers tactical wins but not strategic transformation. SAIL has successfully developed head-hardened rails for metros, replacing European imports worth ₹1,000 crore annually. Special grades for defense applications provide high margins and strategic value. But these niche victories don't address the fundamental challenge of competing in commodity steel markets that constitute 70% of demand.

The sustainability push creates both opportunity and burden. SAIL's commitment to reduce carbon intensity by 30% by 2030 requires ₹50,000 crore in green investments. The company's sustainability report showcases water recycling, waste utilization, and energy efficiency improvements. But global steel is moving toward net-zero emissions by 2050—a target that may require replacing blast furnaces entirely with hydrogen-based technologies SAIL cannot currently afford.

X. Playbook: Lessons from a Public Sector Giant

After examining SAIL's seven-decade journey, certain patterns emerge—lessons that transcend steel and speak to fundamental questions about state ownership, industrial policy, and competing in capital-intensive industries. This isn't just SAIL's playbook; it's a manual for understanding how public sector enterprises navigate the intersection of commercial pressures and social mandates.

Lesson 1: Scale Is a Double-Edged Sword

SAIL's massive scale—five integrated plants, 54,000 employees, 20 million tonnes capacity—provides tremendous advantages in raw material sourcing, market presence, and political importance. But scale also brings inertia. Decisions that private companies make in weeks take SAIL months. A blast furnace relining that should be a technical decision becomes a political event. The lesson: in government frameworks, scale provides stability but impedes agility. Success requires accepting this trade-off and optimizing within constraints rather than fighting them.

Lesson 2: Social Objectives and Commercial Goals Can Coexist—Barely

SAIL employs thousands in backward regions where alternative employment doesn't exist. It supplies steel for strategic projects at non-remunerative prices. It maintains production during downturns to preserve jobs. These social objectives directly conflict with profit maximization, yet SAIL has survived and occasionally thrived. The key is transparency about the social cost and explicit recognition through government support, whether subsidies, preferential resource allocation, or protected markets. Pretending PSUs can match private efficiency while carrying social burdens is delusional.

Lesson 3: Capital Intensity Requires Patient Capital

Steel plants have 30-50 year lifecycles. Modernization investments take 7-10 years to pay back. Market cycles can destroy returns for years. SAIL's government ownership provides patient capital that private markets wouldn't tolerate—no activist investor would accept 4.84% ROE for three years. But patient capital can become complacent capital. SAIL's playbook shows the need for intermediate metrics and milestones that maintain pressure for improvement while acknowledging long-term horizons.

Lesson 4: Workforce Management in PSUs Is Political Economy, Not HR

SAIL cannot hire and fire based on business cycles. Compensation follows government pay commissions, not market rates. Unions have political connections that reach the Prime Minister's office. Traditional HR strategies fail in this environment. SAIL's approach—gradual workforce reduction through VRS, investment in training and cultural change, separate performance incentives within government constraints—shows what's possible. The transformation from 246,000 to 54,000 employees over 30 years is remarkable, even if productivity still lags.

Lesson 5: Innovation Within Constraints Requires Different Muscles

SAIL's engineers have developed indigenous technologies for Indian raw materials, created products for extreme conditions, and kept 50-year-old plants running efficiently. This isn't Silicon Valley innovation—it's jugaad engineering at industrial scale. The constraint-based innovation muscle, once developed, becomes a competitive advantage. SAIL's ability to produce 130-meter rails with Soviet-era equipment upgraded with Indian modifications exemplifies this capability.

Lesson 6: Industrial Policy Works—Until It Doesn't

SAIL's creation made India self-sufficient in steel, built industrial ecosystems, and developed technical capabilities. Clear industrial policy success. But protection bred inefficiency, government ownership created rigidities, and social mandates undermined commercial viability. The playbook lesson: industrial policy can build industries but struggles to make them globally competitive. The transition from protection to competition requires deliberate, painful restructuring that political systems resist.

Lesson 7: Vertical Integration Is Sovereignty

SAIL's control from mines to market provides resilience that purely commercial analysis misses. During COVID-19, when global supply chains collapsed, SAIL maintained production. During border tensions with China, SAIL could rapidly shift to defense priorities. The captive mines that analysts criticize as capital-intensive provide supply security worth more than NPV calculations capture. For strategic industries, vertical integration is about capability, not just efficiency.

Lesson 8: Culture Eats Strategy for Breakfast—Especially in PSUs

SAIL has announced numerous strategies—modernization, digitalization, customer focus. Implementation varies dramatically across plants and departments. Bhilai's entrepreneurial culture delivers results; Durgapur's bureaucratic mindset creates delays. The 50-year-old PSU culture—risk aversion, process orientation, hierarchy—cannot be strategized away. It must be gradually evolved through personnel changes, incentive alignment, and sustained leadership focus. Cultural transformation in PSUs is generational, not quarterly.

Lesson 9: Government Ownership Creates Options Value

Markets value SAIL based on current returns, missing the options value of government ownership. The ability to access resources, influence policy, survive downturns, and serve strategic needs has value not captured in DCF models. During crises, this options value crystallizes—government support, preferential treatment, assured demand. The playbook lesson: PSUs should be valued not just on commercial metrics but on their role in national capability and resilience.

Lesson 10: The Hybrid Model Is the Future

SAIL's journey suggests neither full government ownership nor complete privatization is optimal. The emerging hybrid model—majority government ownership with private sector participation, commercial orientation with strategic flexibility, professional management with political oversight—may be the sustainable path. This requires sophisticated governance mechanisms, clear performance contracts, and political maturity to respect operational autonomy while maintaining strategic control.

XI. Bear vs. Bull Case & Future Outlook

The investment committee meeting at a major mutual fund is debating SAIL. The analyst presenting is conflicted—the numbers suggest caution, but the strategic positioning intrigues. "At ₹122 per share, SAIL trades at 0.6x book value," she begins. "That's either a value trap or the opportunity of the decade." This debate plays out across trading floors and boardrooms—what is SAIL really worth?

The Bull Case: India's Infrastructure Decade

The bulls start with a simple premise: India will invest ₹111 trillion in infrastructure by 2030, and every project needs steel. The National Infrastructure Pipeline includes 9,000 projects across sectors—highways, railways, urban infrastructure, energy. SAIL, as India's largest steel producer with unique capabilities in long products, is perfectly positioned. The math is compelling: even maintaining 15% market share of incremental demand adds 10 million tonnes to SAIL's volumes by 2030.

Government backing provides unmatched advantages. While private players struggle with land acquisition and environmental clearances, SAIL's PSU status opens doors. The company's mining leases, secured decades ago, would be impossible to replicate today. As resource nationalism intensifies globally, SAIL's captive raw materials become increasingly valuable. Iron ore that costs SAIL ₹2,000 per tonne to mine trades at ₹8,000 in open markets—a ₹100 billion annual advantage.

The modernization is finally bearing fruit. The ₹100,000 crore invested over two decades has created assets that would cost ₹200,000 crore to build today. Blast furnaces with 30-year lives, rolling mills with cutting-edge technology, logistics infrastructure spanning the nation—these aren't reflected in book value based on historical cost. The replacement value of SAIL's assets far exceeds market capitalization.

Domestic market protection is strengthening, not weakening. India's quality control orders mandate BIS standards that Chinese steel struggles to meet. Anti-dumping duties and safeguard measures provide breathing room. The "Atmanirbhar Bharat" push prioritizes domestic steel for government projects. Trade wars and supply chain resilience post-COVID favor local producers. SAIL benefits from every protectionist measure.

The financial turnaround is gaining momentum. Net profit grew 40.9% YoY in FY24. Working capital optimization could release ₹10,000 crore. Cost reduction through operational efficiency could improve EBITDA margins by 300 basis points. At normalized margins of 15% and 8x EV/EBITDA multiple, SAIL's enterprise value should be ₹150,000 crore—triple current levels.

The Bear Case: Structural Challenges Trump Cyclical Recovery

The bears counter with harsh realities. Low returns and efficiency gaps aren't temporary—they're structural. SAIL's 4.84% ROE over three years isn't a cyclical trough; it's the new normal. Labor productivity at 350 tonnes per person cannot compete with private players achieving 700+ tonnes. The company has destroyed value for a decade—why would the next decade be different?

Private sector competition is intensifying, not abating. JSW, Tata Steel, and ArcelorMittal Nippon Steel are adding 50 million tonnes of capacity by 2030. These modern plants will have 30% lower costs than SAIL's upgraded facilities. Market share loss is inevitable. SAIL's 15% market share could shrink to 10% even as absolute volumes grow—a recipe for margin compression.

Global oversupply pressures are structural. China's 1 billion tonne capacity facing slowing domestic demand means persistent export pressure. Even with duties, Chinese steel influences Indian pricing. Green steel transition in developed markets will create stranded assets—older, carbon-intensive plants like SAIL's become uncompetitive. Carbon border taxes will eliminate export opportunities. SAIL lacks capital for the ₹200,000 crore green transition.

Environmental compliance costs are astronomical and rising. Each tonne of CO2 emitted will eventually carry a cost—at $50 per tonne, SAIL faces ₹10,000 crore annual carbon costs. Water scarcity in plant locations threatens production. Air quality regulations require continuous investment with no return. The environmental liability on SAIL's balance sheet is understated by ₹50,000 crore.

Legacy issues and bureaucracy prevent transformation. The average employee age of 43 means 15-20 years of salary escalations without commensurate productivity gains. Political interference in commercial decisions—from pricing to plant locations—destroys value. The cultural transformation needed for competitiveness will take a generation SAIL doesn't have.

Future Outlook: The Muddle Through Scenario

Reality will likely fall between extremes. SAIL will neither collapse nor achieve private sector returns. The company will muddle through—generating enough cash to invest, returning modest dividends, serving strategic purposes, but never exciting investors. This "stable mediocrity" could persist for decades.

Key milestones to watch:

- 2025: Capacity utilization reaching 85% would signal operational improvement

- 2026: Carbon border adjustment mechanism implementation will test export viability

- 2027: Next pay commission will impact cost structure

- 2028: Major blast furnace relining decisions will indicate capital allocation priorities

- 2030: 50 MT capacity target will measure execution capability

The green steel transition represents both the greatest risk and opportunity. If SAIL can access green financing and government support for hydrogen-based steel, it could leapfrog private competitors. But if the transition is unfunded and delayed, SAIL's plants become stranded assets. The next five years will determine whether SAIL transforms or merely survives.

India's National Steel Policy envisions 300 million tonnes capacity by 2030, with SAIL targeting 50 mt. Achieving this requires ₹200,000 crore investment—impossible at current returns. More likely, SAIL reaches 30-35 mt through debottlenecking and selective expansion. The company will remain relevant but not dominant, important but not impressive.

Consolidation possibilities intrigue but face political hurdles. Merging with RINL (Vizag Steel) would create synergies worth ₹20,000 crore. Acquiring stressed private assets could add modern capacity cheaply. Joint ventures with global leaders could bring technology and capital. But government decision-making timelines make opportunistic M&A impossible.

The investment case ultimately depends on time horizon and risk appetite. For traders, SAIL offers volatility around steel cycles and government announcements. For value investors, the discount to replacement value and hidden assets provide margin of safety. For growth investors, the structural challenges outweigh cyclical opportunities. For the government, SAIL remains a strategic asset worth preserving regardless of returns.

XII. Epilogue: What Would Privatization Look Like?

The question hangs in the air at every SAIL board meeting, every investor call, every policy discussion, though rarely spoken aloud: Should SAIL be privatized? It's India's great industrial taboo—questioning whether the crown jewel of public sector industry should remain in government hands. Yet understanding what privatization would mean illuminates SAIL's true value and constraints.

The privatization debate isn't new. In 1999, the Vajpayee government proposed selling 10% of SAIL—unions threatened nationwide strikes, opposition parties called it selling the family silver, and the proposal died. In 2006, the UPA government considered strategic sale but retreated after political pushback. In 2020, the Modi government's privatization push explicitly excluded SAIL, designating steel as a strategic sector requiring government presence. The pattern is clear: economic logic collides with political reality.

Valuation considerations are fascinating and contentious. SAIL's market capitalization hovers around ₹50,000 crore, but what's the true value? Book value exceeds ₹80,000 crore. Replacement cost of assets approaches ₹200,000 crore. The value of mining leases—impossible to replicate—could be ₹100,000 crore alone. Add real estate in prime urban locations, strategic importance, and market position, and valuations range from ₹150,000 to ₹300,000 crore. No price would satisfy both sellers and buyers.

The strategic asset argument cuts both ways. Proponents argue steel is too strategic for private control—national security requires government oversight of critical infrastructure. Can India trust private owners to prioritize defense needs over commercial interests? To maintain capacity for crisis response? To develop indigenous technology rather than importing? The counter-argument is equally compelling: strategic importance requires efficiency and innovation that government ownership inhibits. Private Tata Steel served India's strategic needs for a century without government control.

Global comparisons provide limited guidance. South Korea's POSCO was privatized successfully, becoming globally competitive. China's Baosteel remains state-owned but operates with commercial autonomy. ArcelorMittal emerged from privatized European state steel companies. Brazil's CSN thrived post-privatization. But each had unique contexts—different labor laws, political systems, and market structures. India's democracy, with its coalition politics and powerful unions, creates constraints others didn't face.

The mechanics of privatization would be extraordinarily complex. Would the government sell SAIL as a whole or break it into plant-specific companies? The latter might maximize value—Bhilai could attract premium valuations while Durgapur might struggle to find buyers. But breaking SAIL would lose synergies in raw materials, marketing, and technology. Would captive mines be included or retained by government? Mining leases are SAIL's crown jewels, but selling them raises sovereignty concerns.

Labor implications dominate political calculations. SAIL's 54,431 employees represent 200,000+ family members and dependents. Each plant supports entire townships—schools, hospitals, markets. Privatization fears center on job losses, benefit cuts, and community abandonment. The VRS cost alone could exceed ₹30,000 crore. Political parties calculating electoral math see more votes lost than economic gains won.

The Vizag Steel precedent looms large. Rashtriya Ispat Nigam Limited (RINL), which operates Vizag Steel Plant, has been slated for privatization since 2021. Two years later, it remains unsold despite multiple attempts. Employee protests, political opposition, and valuation disputes have stalled the process. If the government cannot privatize a single plant, how could it privatize SAIL's entire network?

Lessons from other PSU privatizations are sobering. Bharat Aluminium Company (BALCO) was privatized to Sterlite in 2001—efficiency improved dramatically, but thousands lost jobs and communities suffered. Hindustan Zinc's privatization succeeded commercially but faced persistent criticism about resource giveaways. Air India's recent privatization to Tata took two decades and multiple attempts. Each case reinforces that PSU privatization in India is a marathon, not a sprint.

The middle path—partial privatization—offers political cover but limited benefits. Selling 10-15% through public offers raises capital without losing control. But minority private shareholders cannot drive transformation when government retains majority ownership and control. SAIL already has 35% public shareholding, yet operates like a PSU. Meaningful privatization requires control transfer, not just equity dilution.

Strategic alternatives to outright privatization deserve consideration. Professional management with operational autonomy—the Singaporean model—could improve efficiency without ownership change. Performance contracts with clear targets and consequences could drive accountability. Public-private partnerships for new projects could bring private efficiency to specific initiatives. These alternatives offer improvement without political confrontation.

The ultimate question isn't whether SAIL should be privatized, but what India wants from its steel industry. If the goal is maximizing efficiency and returns, privatization makes sense. If the goal is maintaining strategic capability and social stability, government ownership has logic. India seems to want both—world-class efficiency with public sector control. This contradiction defines SAIL's challenge.

The privatization debate reveals a deeper truth about SAIL and India's economic model. The company embodies the tension between market economics and democratic politics, between efficiency and equity, between global integration and strategic autonomy. SAIL isn't just a steel company—it's a 50-year experiment in managed capitalism, industrial democracy, and nation-building through enterprise.

As India charts its future, SAIL's fate will signal broader choices about the role of state in the economy. Will India embrace full market economics, accepting inequality and disruption for efficiency and growth? Will it maintain strategic state presence, accepting lower returns for greater control? Or will it continue muddling through, keeping SAIL in perpetual transition between public purpose and private efficiency?

The answer matters beyond steel. In SAIL's blast furnaces, India forges not just metal but its economic identity. The company that Nehru called a temple of modern India remains a pilgrimage site—not for the faithful seeking blessing, but for a nation seeking balance between its socialist past and capitalist future. Whether SAIL remains a public trust or becomes private enterprise, its story will continue to illuminate fundamental questions about development, democracy, and the proper role of state in shaping economic destiny.

For investors, SAIL represents a bet not just on steel or infrastructure but on India's political economy itself. Those who believe India will maintain its mixed economy model, balancing state presence with market forces, might find SAIL's current valuation attractive. Those who believe India must choose—either full socialism or unfettered capitalism—should look elsewhere. SAIL thrives in ambiguity, struggles with clarity, and embodies India's refusal to choose between competing visions of progress.

The steel will continue flowing from SAIL's furnaces regardless of ownership. Trains will run on SAIL rails, buildings will rise with SAIL steel, and bridges will span rivers with SAIL girders. But whether this steel carries the weight of public purpose or the efficiency of private profit remains India's great unresolved question. In that irresolution lies both SAIL's burden and its opportunity—forever caught between what India was and what it might become.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube