Sagility India: The Story of Healthcare BPO's Quiet Giant

I. Introduction & Episode Roadmap

Picture this: It's 2024, and a company that technically didn't exist three years ago just listed on the Indian stock exchanges with a market cap exceeding ₹20,000 crores. Not a flashy tech unicorn. Not a consumer brand. But a healthcare operations company that most Indians have never heard of—yet one that touches millions of American lives every single day.

Sagility India processes over 150 million healthcare transactions annually, recovers billions of dollars for U.S. health insurers, and employs over 35,000 people across five countries. When an American patient's insurance claim gets approved, when a hospital gets reimbursed for a complex surgery, or when a billing error gets caught before it becomes a million-dollar mistake—there's a good chance someone at Sagility had a hand in it.

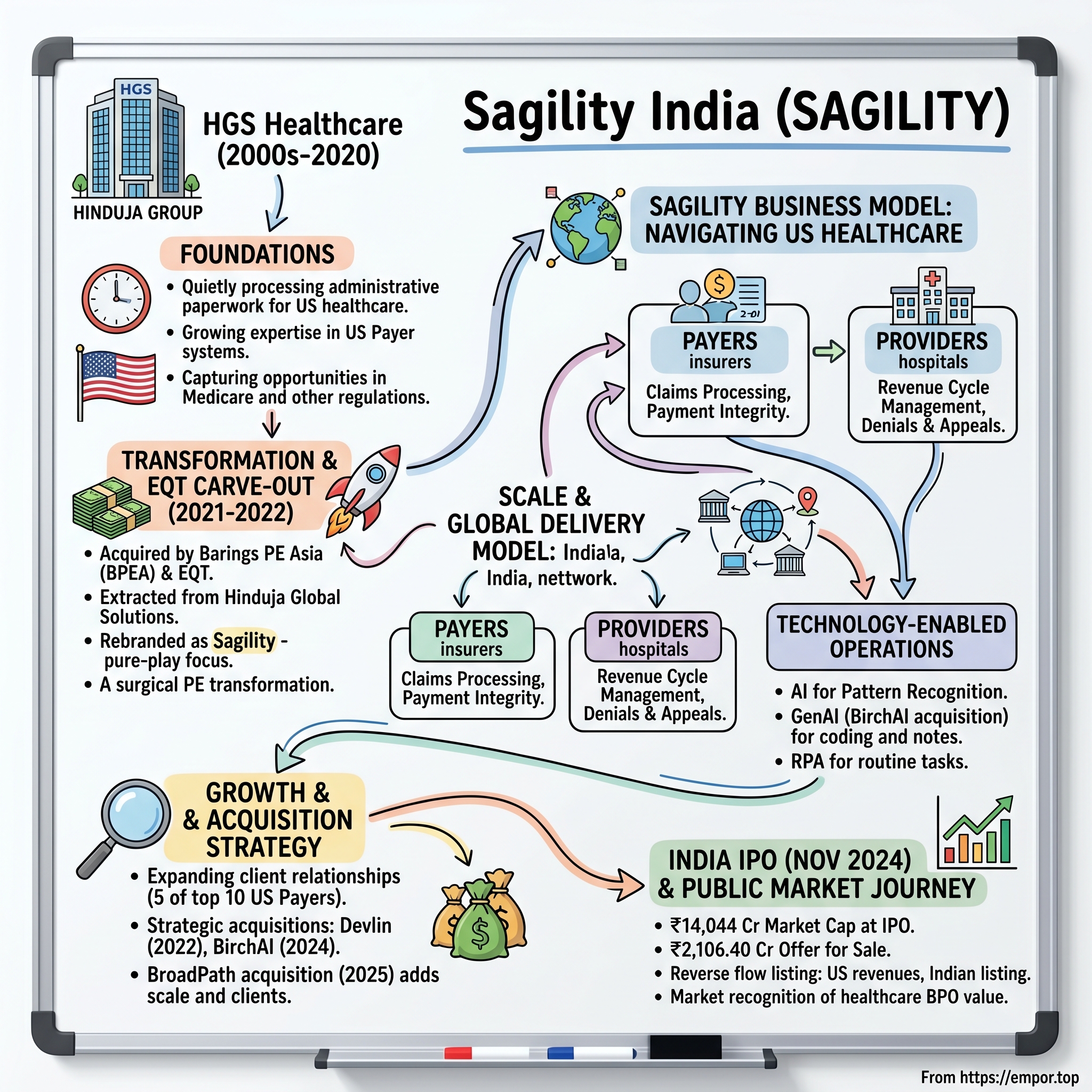

The fascinating paradox here is that this isn't really a startup story at all. The core business traces back to 2000, when it began serving U.S. healthcare payers as part of Hinduja Global Solutions. But the Sagility we see today—the focused, technology-enabled healthcare services platform—emerged from a classic private equity transformation play that began in 2021.Think about it: The market capitalization of Sagility India IPO is ₹14043.99 Cr at the IPO price, but today it trades at over ₹20,846 Cr—a testament to how the market values this unique healthcare services story. This is a company that serves five of the top ten U.S. healthcare payers, yet most of its 35,000+ employees sit in offices from Mumbai to Manila, processing the byzantine paperwork that keeps American healthcare functioning.

How did we get here? How does a company carved out of an Indian conglomerate's back-office operations become essential infrastructure for the world's most expensive healthcare system? And what does this tell us about the future of global healthcare operations?

This is a story about arbitrage—not just of labor costs, but of expertise, scale, and the ability to make sense of complexity. It's about how private equity can transform a sleepy division into a focused powerhouse. And ultimately, it's about how the most mundane parts of healthcare—the claims, the coding, the billing—became a multi-billion-dollar opportunity hiding in plain sight.

Let's dive into how this unlikely champion of healthcare operations was built, transformed, and ultimately became public market gold.

II. The Pre-History: Healthcare BPO Origins & HGS Healthcare

The year 2000 feels like ancient history in technology terms—Google was barely two years old, the iPhone wouldn't exist for seven years, and "outsourcing" was still a dirty word in many American boardrooms. But in the labyrinthine world of U.S. healthcare administration, a quiet revolution was beginning.

That's when the business that would become Sagility first started serving American healthcare payers. Not with fanfare or venture capital, but as part of Hinduja Global Solutions' growing portfolio of back-office services. The timing was no accident. Y2K had just forced American companies to realize that Indian engineers could handle mission-critical technology work. The next logical step? If India could debug your systems, maybe it could also process your paperwork.

But healthcare BPO wasn't like handling credit card disputes or tech support calls. The U.S. healthcare system is a Rube Goldberg machine of regulations, codes, and counter-incentives. Every claim involves multiple parties with conflicting interests. Every procedure has a code—actually, multiple codes. The ICD-10 system alone has over 70,000 diagnosis codes, including such gems as "V91.07XD: Burn due to water-skis on fire, subsequent encounter" (yes, that's real).

This complexity is precisely what created the opportunity. American hospitals and insurance companies were drowning in their own administrative burden. Studies showed that for every doctor, there were nearly ten administrative staff members. Healthcare administration costs were eating up 8% of total healthcare spending—hundreds of billions of dollars annually. The system had become so complex that even the people running it couldn't navigate it efficiently.

Enter the Indian BPO industry, which had a unique combination of advantages: English fluency, strong educational systems producing millions of graduates annually, and most importantly, the ability to build massive operations at a fraction of U.S. costs. But healthcare required something more—domain expertise that couldn't be learned from a manual.

Over two decades, what started as basic claims processing evolved into something far more sophisticated. The HGS Healthcare division wasn't just following scripts; it was building deep expertise in the arcane rules of American healthcare. Teams in Chennai became experts in Medicare regulations. Offices in Bangalore specialized in prior authorization workflows. Manila centers mastered the art of provider credentialing.

By 2020, this operation had grown to thousands of employees and was processing millions of transactions. But it was still just one division within HGS, competing for resources with other service lines, unable to fully capitalize on the healthcare opportunity. The company was carved out of Hinduja Global's healthcare business in Jan 2022 and enjoys a 1.23% market share of US healthcare operations outsourcing market—seemingly small, but representing billions in processed claims.

The business had proven something crucial: healthcare BPO wasn't a race to the bottom on costs. It was about building specialized expertise at scale, creating what economists call "increasing returns to scale." The more claims you processed, the better you understood the patterns. The more denials you handled, the better you got at preventing them. This wasn't commodity work—it was institutional knowledge, packaged and delivered globally.

What the Hindujas had built was valuable, but it was also constrained. Within a conglomerate structure, the healthcare division couldn't move fast enough, couldn't invest aggressively enough, couldn't attract the specialized talent it needed to truly scale. It was a classic case of a good business trapped inside the wrong corporate structure.

The stage was set for transformation. All it needed was a catalyst—and that catalyst would come in the form of private equity with a very specific playbook.

III. The EQT Acquisition & Transformation (2021–2022)

The private equity world loves a good carve-out story, but what happened to HGS Healthcare in 2021 was something special. On July 28, 2021, a new entity was quietly incorporated in India: Berkmeer India Private Limited. The name meant nothing to anyone—which was precisely the point. This was the vehicle through which one of the most ambitious healthcare services transformations would unfold.

Baring Private Equity Asia acquired HGS Healthcare in August 2021 for approximately $1.2 billion, but this wasn't just another PE deal. BPEA, which would itself soon be acquired by Swedish PE giant EQT in a €6.8 billion ($7.5 billion) mega-merger, saw something in this healthcare services business that others had missed.

The timing was exquisite. COVID-19 had just stress-tested the entire U.S. healthcare system, exposing massive operational inefficiencies. Telehealth adoption had gone from 11% to 46% of consumers in a matter of months. Healthcare payers were drowning in claims complexity as treatment patterns shifted overnight. The need for scalable, technology-enabled healthcare operations had never been clearer.

BPEA's playbook was classic private equity, but executed with surgical precision. First, extract the asset from its conglomerate parent—HGS was happy to monetize a non-core division at an attractive valuation. Second, rebrand completely. In September 2022, Berkmeer India Private Limited shed its anonymous shell and emerged as Sagility, a name suggesting both wisdom and agility.

But the real transformation went deeper than cosmetics. Under BPEA's ownership, Sagility became a pure-play healthcare services platform for the first time in its history. No more competing for capital allocation with call centers and other BPO services. No more sharing management attention with unrelated business lines. Every dollar of investment, every strategic decision, every hire would now be focused on one thing: becoming the dominant player in healthcare operations outsourcing.

The vision was ambitious: targeting $1 billion in revenue by 2026. To put that in perspective, the company posted revenue of $460 million in FY22, up from about $400 million in FY21. Achieving this target would require a CAGR of nearly 15%—aggressive but not impossible in a market growing at double digits.

BPEA brought more than just capital. As part of the broader EQT ecosystem post-merger, Sagility gained access to a global PE platform with deep expertise in healthcare and technology investments. EQT became one of the world's largest private markets firms combined with BPEA, the third largest in Asia, creating powerful synergies for portfolio companies like Sagility.

The transformation strategy had three pillars. First, accelerate organic growth by expanding relationships with existing clients and winning new logos. Second, invest heavily in technology and automation to improve margins and service quality. Third, pursue strategic acquisitions to add capabilities and scale.

Deep domain expertise in healthcare is central to its plan to grow by developing technological solutions. This wasn't about replacing humans with bots—it was about augmenting human expertise with technology to handle ever-increasing complexity. The company began building proprietary platforms for document processing, leveraging AI for pattern recognition in claims denials, and creating automated workflows for routine tasks.

The geographic expansion strategy was equally important. The company plans to open centres in tier-2 cities and small towns and plans to add 3,000 individuals to its employee base globally. About 45% of Sagility's workforce is in India. This wasn't just about cost arbitrage—tier-2 cities offered access to untapped talent pools, lower attrition rates, and better quality of life for employees.

What BPEA understood, and what would become crucial for the eventual IPO story, was that Sagility wasn't really competing with other Indian BPO companies. It was competing with the in-house operations of U.S. healthcare companies, with specialized healthcare services firms, and increasingly, with technology-first solutions. The competitive set wasn't Infosys or TCS—it was Optum, Change Healthcare, and Cognizant's healthcare division.

The rebranding to Sagility marked more than a name change—it was a declaration of independence from the commoditized BPO past and an embrace of a specialized, technology-enabled future. The stage was set for aggressive expansion, both organic and through acquisition, that would define the company's trajectory toward public markets.

IV. The Business Model: Payers, Providers & The Healthcare Maze

To understand Sagility's business model, you first need to understand the beautiful dysfunction of American healthcare. Imagine a system where the person receiving the service (patient) isn't the one paying for it (insurer), where the entity providing the service (hospital) has to negotiate prices with hundreds of different payers, and where a simple doctor's visit generates a cascade of paperwork that would make Kafka weep.

This is Sagility's playground.

The company operates in two distinct but interconnected markets. On one side are the Payers—health insurance companies that finance and reimburse healthcare services. These aren't just processing claims; they're managing risk, ensuring compliance with thousands of regulations, and trying to control costs in a system where nobody knows the real price of anything. Sagility provides them with services spanning claims processing, payment integrity (finding errors and fraud), and clinical management (determining if that MRI is really necessary).

On the other side are the Providers—hospitals, physician practices, diagnostic centers—who need to get paid for services rendered. Sounds simple? It's not. The average hospital has to deal with dozens of insurance companies, each with different rules, forms, and payment schedules. A single patient visit can generate multiple claims, require prior authorizations, face denials, go through appeals, and eventually (hopefully) result in payment months later. Sagility's revenue cycle management (RCM) services handle this entire byzantine process, from insurance verification at admission to the final collection of accounts receivable.

The numbers here are staggering. The company processes over 150 million transactions annually. Think about that—150 million individual touchpoints where something could go wrong, where money could be lost, where a patient could fall through the cracks. The company processes over 60 million claims, resulting in the recovery of over $5 billion for clients. That's $5 billion that would have been lost in the healthcare system's administrative maze without Sagility's intervention.

But here's where it gets interesting: this isn't just about moving paper from point A to point B. Each claim is a puzzle. Why was this claim denied? Is the coding correct? Does the documentation support the level of service billed? Is this provider properly credentialed with this payer? Modern healthcare billing involves over 70,000 diagnosis codes and 10,000 procedure codes. The difference between coding a "subsequent encounter" versus an "initial encounter" can mean thousands of dollars.

This complexity creates a moat. You can't just hire smart people and throw them at this problem. It takes years to build the domain expertise, to understand the nuances of Medicare Advantage versus commercial insurance, to know that certain payers require specific modifiers for certain procedures in certain states. The company has 1,687 individuals with specialized certifications, including 374 certified medical coders and 1,280 registered nurses.

The technology layer is where Sagility differentiates itself from traditional BPO players. They're not just processing claims manually—they're using machine learning to predict which claims will be denied, natural language processing to extract information from unstructured medical records, and robotic process automation to handle routine tasks. The company's platforms include document processing engines, genAI solutions for customer engagement, and specialized tools for contract management.

Consider the "prior authorization" process—a special circle of healthcare hell where providers must get permission from insurers before performing certain procedures. This single process costs the U.S. healthcare system $31 billion annually in administrative burden. Sagility's technology can predict which authorizations will be approved, automatically gather required documentation, and submit requests in the specific format each payer requires. What used to take days now takes hours.

The unit economics are compelling. Unlike pure software companies that need massive R&D investments upfront, Sagility's model scales linearly with revenue. Each new client brings predictable revenue streams—typically multi-year contracts with high switching costs. Once you're integrated into a hospital's revenue cycle or a payer's claims system, you become part of their operational DNA.

The business model also benefits from powerful network effects. The more claims they process, the better their algorithms become at predicting denials. The more payers they work with, the deeper their understanding of each payer's quirks. The more providers they serve, the more comprehensive their database of coding patterns and best practices.

But perhaps the most underappreciated aspect of Sagility's model is its counter-cyclical resilience. When the economy booms, healthcare utilization increases, driving more transactions. When the economy struggles, healthcare organizations focus on cost reduction and operational efficiency—exactly what Sagility provides. COVID-19 proved this: while elective procedures plummeted, the complexity of healthcare operations skyrocketed, and companies like Sagility became more essential than ever.

The margin structure tells the story of a business in transition. Pure labor arbitrage BPO might generate 15-20% EBITDA margins. But as Sagility layers in technology, automates routine tasks, and moves up the value chain to more complex services, margins expand. The company isn't just processing claims—it's becoming the operational intelligence layer for American healthcare.

V. Scale, Geography & Global Delivery Model

The sun never sets on Sagility's operations—literally. When Mumbai's offices close for the day, Manila is still processing claims. When Manila winds down, Jamaica picks up the slack. And underpinning it all is a 24/7 operation in the United States, ensuring real-time support for critical healthcare functions.

Sagility has more than 25,000 employees across 5 countries, with 35,044 employees as of March 31, 2024, of which 60.52% were women. This isn't just a statistic—it's a deliberate strategy. In an industry plagued by 30-40% annual attrition rates, having women comprise the majority of your workforce in countries like India and the Philippines provides stability. These employees often have deeper community roots, lower turnover intentions, and bring a different perspective to patient-centric healthcare services.

Sagility has offshore delivery centers in India, the Philippines, Jamaica, and Colombia and an onshore presence in the US serviced by 35858 employees. The geographic distribution isn't random—it's a carefully orchestrated symphony of time zones, talent pools, and risk mitigation. India provides scale and deep technical expertise. The Philippines offers excellent English proficiency and cultural alignment with American healthcare norms. Jamaica and Colombia provide nearshore advantages—same time zones as the U.S. East Coast, easier travel for training and client meetings, and backup for business continuity.

The talent story goes beyond numbers. As of March 31, 2024, 1,687 of the employees held certifications, including 374 certified medical coders, 1,280 registered nurses in the US, Philippines and India, and 33 employees with other degrees such as dentistry, surgery and pharmacy. Think about that—1,280 registered nurses who chose to work in healthcare operations rather than clinical care. These aren't call center operators reading scripts; they're healthcare professionals who understand the clinical implications of every authorization, every denial, every appeal.

The Philippines operation deserves special attention. Filipino nurses have been the backbone of American healthcare for decades—there are more Filipino nurses in California than in Manila. Sagility tapped into this diaspora knowledge, recruiting nurses who understood American healthcare but chose to stay in the Philippines. They bring clinical credibility that no amount of training can replicate. When a Sagility nurse in Manila calls a U.S. hospital about a prior authorization, they're speaking the same clinical language.

India remains the intellectual powerhouse of the operation. The Bangalore and Chennai centers don't just process transactions—they build the technology platforms, develop the algorithms, and create the process innovations that get rolled out globally. The Indian centers also handle the most complex analytical work: pattern recognition in claims data, predictive modeling for denials, and the intricate work of payment integrity where millions of dollars hang in the balance.

Its global delivery presence has helped to tap into a wider talent pool, providing timely service to clients, leading to revenue growth. But the real innovation is in how these centers work together. A claim might be initially processed in India during U.S. nighttime, flagged for clinical review by a nurse in the Philippines, have additional documentation gathered by a team in Jamaica during U.S. business hours, and finally be submitted by the U.S. onshore team who can directly interface with the payer.

This "follow the sun" model provides 24/7 productivity, but more importantly, it provides resilience. When COVID-19 hit and India went into lockdown, operations shifted seamlessly to other locations. When hurricanes threaten Caribbean operations, capacity moves to Asia. When the Philippines has connectivity issues, India scales up. This isn't just business continuity—it's business anti-fragility.

The economics of this model are compelling. Labor arbitrage remains real—a medical coder in India costs perhaps 20-30% of their U.S. counterpart. But the real advantage isn't just cost; it's the ability to scale rapidly. Need to process a surge in COVID-19 claims? Sagility can add 500 trained professionals in weeks, not months. A U.S. hospital trying to do the same would face months of recruitment, training, and onboarding.

The company is also rethinking the geography of talent. Plans to open centers in tier-2 cities and small towns reflect a deeper understanding of India's changing demographics. Tier-2 cities offer lower costs, better quality of life, and most importantly, lower attrition. An employee in Coimbatore or Mysore is less likely to job-hop than one in Bangalore or Gurgaon. These locations also tap into educated talent that might not want to relocate to metros—creating a win-win for both employer and employee.

What Sagility has built is more than a global delivery network—it's a living, breathing organism that processes the administrative lifeblood of American healthcare. Each location brings unique strengths, but together they create something more powerful: a platform that can handle any volume, any complexity, any challenge that the U.S. healthcare system can throw at it.

This geographic arbitrage story is entering a new chapter. As automation takes over routine tasks, the work moving offshore is increasingly complex, requiring higher skills and deeper domain expertise. The next frontier isn't just about cost—it's about accessing specialized talent wherever it exists, creating global centers of excellence that couldn't exist in any single geography.

VI. The Growth Story: Acquisitions & Client Expansion

The playbook for building a healthcare services platform isn't just about organic growth—it's about strategic acquisitions that add capabilities, clients, and scale. Sagility's M&A strategy reads like a masterclass in platform consolidation, each deal carefully chosen to fill a gap or accelerate a strategic priority.

The story begins in January 2022 when Sagility acquired the Indian undertaking of Hinduja Global Solutions Limited conducting the business of providing healthcare services—essentially formalizing the carve-out that created the company. But the real acquisition spree was just beginning.

Later in 2022, Sagility acquired Devlin Consulting, Inc. (DCI) to enhance its payment integrity (PI) solutions for health plans. Payment integrity is where the real money is in healthcare—finding overpayments, identifying fraud, ensuring claims are paid correctly. DCI brought sophisticated analytics capabilities and deep relationships with major payers. This wasn't just buying revenue; it was buying expertise that would take years to build organically.

Then in March 2024, Sagility made a technology play by acquiring BirchAI, a healthcare technology firm specialising in cloud-based, generative AI solutions. The timing was perfect—GenAI was having its ChatGPT moment, and every enterprise was scrambling to figure out how to leverage these capabilities. BirchAI brought real, production-ready AI solutions specifically designed for healthcare operations. Their natural language processing could extract information from unstructured medical records, their conversational AI could handle member inquiries, and their predictive models could identify high-risk claims before they became problems.

But the most transformative deal came in January 2025. Sagility acquired US-based healthcare focused services company BroadPath Healthcare Solutions for 502 crore rupees ($58 million) in cash, with the transaction completed on January 29, 2025. With BroadPath generating revenues of approximately $70 million, the acquisition was done at less than 1x EV/Revenue—a valuation that would make any CFO smile.

BroadPath wasn't just another tuck-in acquisition. The acquisition added another top 10 US payer to Sagility's client list and increased the company's footprint with two other existing top 10 payer clients. Post-acquisition, Sagility will serve six of the top 10 payers in the US. This acquisition significantly expands Sagility's market presence, adding more than 30 new clients.

What made BroadPath special was its pioneering work-from-home model. BroadPath has been a pioneer in the work-from-home model even before the COVID-19 pandemic. Their proprietary Bhive platform improves employee engagement and optimizes operating metrics in a work-from-home model ensuring superior experience for employees and clients alike. In a post-COVID world where remote work had become table stakes, BroadPath had already solved the operational challenges that others were just beginning to grapple with.

The strategic logic was compelling. BroadPath's strength in member acquisition and enrollment services in medicare and medicaid complements Sagility's strength in claims management and payment integrity. This wasn't overlap—it was complementary capabilities that would allow Sagility to offer end-to-end services to payers.

Client expansion has been equally impressive. The company has systematically grown from serving a concentrated base of large payers to a more diversified portfolio. By 2024, they had added 22 new clients since the 2021 transformation. Each new logo isn't just incremental revenue—it's validation of the platform strategy, proof that Sagility can compete and win against established players.

The client acquisition strategy follows a land-and-expand playbook. Start with a single service line—maybe claims processing for one division. Prove your value through superior accuracy rates and turnaround times. Then expand into adjacent services: payment integrity, prior authorization, member services. Before long, you're embedded across multiple functions, with switching costs so high that the relationship becomes virtually permanent.

Given Sagility's success in mining accounts in the past, the BroadPath transaction will boost its longer-term growth potential as it will be able to mine over 70 clients instead of 42 as of June 2024. This expanded client base provides a massive runway for organic growth through cross-selling and upselling.

The financial impact of this growth strategy has been dramatic. Revenue grew from about $400 million in FY21 to $460 million in FY22, then to approximately $500 million in calendar year 2023. The company is reportedly targeting $1 billion in revenue by 2026—a target that looked ambitious before the BroadPath acquisition but now seems increasingly achievable.

What's remarkable about Sagility's M&A strategy is its discipline. These aren't ego-driven deals or desperate attempts to buy growth. Each acquisition brings something specific: technology (BirchAI), capabilities (Devlin), or client relationships and delivery models (BroadPath). The valuations have been reasonable, integration risks manageable, and synergies real.

The acquisition strategy also reveals something deeper about the healthcare BPO market: it's ripe for consolidation. There are dozens of small, specialized firms serving niche segments of the market. Many lack the scale to invest in technology, the balance sheet to weather downturns, or the breadth to serve large enterprise clients. For Sagility, with its PE backing and public market currency, these firms represent a pipeline of accretive acquisitions that can accelerate both growth and capability development.

VII. The IPO Story: Going Public in 2024

The journey from private equity portfolio company to public market darling is never straightforward, but Sagility's IPO in November 2024 was a masterclass in timing, positioning, and execution. The book build issue of ₹2,106.40 crores was entirely an offer for sale of 70.22 crore shares—no fresh capital raise, just EQT's partial exit from a wildly successful investment.

The IPO opened for subscription on November 5, 2024, at a price band of ₹28-30 per share. For a company that had been carved out just three years earlier, this represented a remarkable transformation. The valuation implied a market cap of approximately ₹14,044 crores at the upper price band—a testament to how the market valued specialized healthcare services over generalist BPO operations.

The subscription story unfolded like a three-act drama. Day one saw tepid interest, with only 22% subscription—the market was cautious, perhaps wary of another PE exit dressed up as a growth story. But by day two, retail investors began to see the opportunity. The retail portion was subscribed 1.9 times, even as institutional investors remained on the sidelines.

Then came the surge. By the close on November 7, 2024, the IPO was subscribed 3.20 times overall. The retail portion ended up being subscribed 4.16 times, QIBs came in strong at 3.52 times, and even the traditionally cautious NIIs subscribed 1.93 times. The employee portion—offered at a ₹2 discount—was subscribed 3.75 times, showing internal confidence in the company's prospects.

What drove this late surge? Several factors converged. First, the valuation began to look attractive relative to peers—at the upper price band, the company was valued at roughly 24x FY24 adjusted earnings, reasonable for a business growing at double digits with improving margins. Second, anchor investors had already committed significant capital, providing validation. Third, the grey market premium, while modest, remained positive throughout the subscription period.

The listing day—November 12, 2024—brought measured optimism. Sagility India shares listed at ₹31.06 on both BSE and NSE, a 3.53% premium over the issue price of ₹30. Not a blockbuster debut, but solid enough to validate the IPO pricing and leave something on the table for investors.

The OFS structure revealed the sophistication of EQT's exit strategy. By selling only 15% of the company's equity, they maintained control while establishing public market valuation. The promoter holding post-IPO stood at 85%—enough to drive the business forward while having the optionality for future stake sales at potentially higher valuations.

The investor mix was telling. Foreign institutional investors dominated the QIB book with 55.43 crore shares bid, showing international capital's confidence in the India-to-U.S. healthcare services story. This wasn't just about Indian retail enthusiasm; global investors saw the structural opportunity.

The use of proceeds—or rather, the lack thereof—was refreshing. Since this was purely an OFS, the company didn't receive any proceeds. This meant no grand capex plans to justify, no acquisition war chest to defend, no working capital requirements to explain. The business was already profitable, cash-generative, and growing. The IPO was simply about providing liquidity to the PE investor and creating a public currency for future growth.

The pricing strategy deserves scrutiny. At ₹30 per share, the company was asking investors to value it at less than 3x FY24 revenues—aggressive for a traditional BPO but reasonable for a specialized healthcare services platform with 15%+ growth and expanding margins. The comparison set wasn't Indian IT services companies trading at 4-5x revenues, but specialized healthcare technology companies in the U.S. trading at even higher multiples.

The anchor book, while not disclosed in detail, reportedly included several marquee domestic mutual funds and global investors who understood the healthcare services space. Their participation provided crucial price discovery and confidence to retail investors who followed.

What made this IPO particularly interesting was what it represented for the broader Indian capital markets. Here was a company that derived 100% of its revenues from the U.S., employed thousands in India and other emerging markets, and was now listing in India rather than the U.S. This reverse flow of listing—operational arbitrage but capital market locality—represented a new model for global services companies.

The timing couldn't have been better. The Indian IPO market was recovering from a subdued period, investors were looking for quality stories with international revenues (providing natural currency hedging), and the healthcare sector was back in focus post-pandemic. Sagility offered all three in a package that was both familiar (BPO/services) and novel (pure-play healthcare, PE-transformed).

For EQT, the IPO represented a partial victory lap on what would likely be one of their most successful investments in Asia. Having acquired the business for $1.2 billion in 2021 and taking it public at a significantly higher valuation just three years later—while retaining majority control—exemplified the value creation possible when operational expertise meets market timing.

The post-IPO performance would be crucial. Unlike tech unicorns that could promise growth at any cost, Sagility would be judged on its ability to deliver consistent revenue growth, margin expansion, and strategic acquisitions. The public market scorecard would be less forgiving but potentially more rewarding for a business that could deliver predictable, profitable growth.

VIII. Financials & Unit Economics

The financial story of Sagility reads like a masterclass in operational leverage and margin expansion. Revenue: 5,886 Cr, Profit: 665 Cr for the trailing twelve months tells only part of the story. The real magic is in how those numbers have evolved and what drives them.

Let's start with the headline growth. Sagility India's revenue increased by 13% and profit after tax (PAT) rose by 59% between the financial year ending with March 31, 2024 and March 31, 2023. When your profits are growing 4.5x faster than revenues, you're either cutting costs dramatically or moving up the value chain. In Sagility's case, it's both.

The Q4 FY2025 results paint an even more dramatic picture. Sagility India Q4 FY25 results show a 127.7% profit surge, 22% revenue growth. The company posted Revenue: ₹1497.02 crore Net Profit: ₹216.91 crore for the quarter. This acceleration suggests the business model is hitting an inflection point where scale benefits are really kicking in.

The unit economics tell a compelling story. Healthcare BPO isn't like software—you can't have 90% gross margins. But what you can have is predictable, improving margins as you scale. The company's EBITDA margins have been steadily expanding as automation takes hold and utilization improves. Each additional client doesn't require proportional increases in infrastructure or management overhead.

Revenue per employee is a crucial metric in services businesses. With approximately 35,000 employees generating roughly ₹5,886 crores annually, that's about ₹16.8 lakhs per employee—impressive for an India-based services company. But the trajectory is more important than the absolute number. As the company adds more complex services and leverages technology, revenue per employee should continue climbing.

The working capital dynamics deserve attention. Unlike product companies that need to finance inventory, or construction companies with long receivable cycles, Sagility operates with negative working capital in many cases. Clients often pay retainers or make advance payments, while employee costs are paid monthly. This creates a natural cash float that funds growth without external capital.

Customer concentration has historically been both a strength and a risk. The five largest customer groups have an average tenure of 17 years—extraordinary loyalty in the services business. But concentration also means vulnerability. The BroadPath acquisition helps here, adding 30+ new clients and reducing dependency on any single customer.

The margin story is particularly compelling when you understand the layers. At the gross level, you have the basic labor arbitrage—Indian costs, U.S. pricing. Layer on utilization improvements (getting from 70% to 85% utilization is pure margin). Add automation (every process automated drops straight to the bottom line). Finally, mix shift to higher-value services (payment integrity commands better margins than basic claims processing).

The latest quarterly performance shows this playing out. Revenue jumped 24.13% since last year same period to ₹1,548.84Cr in the Q1 2025-2026... Net profit jumped 566.49% since last year same period to ₹148.56Cr. While some of this dramatic profit growth comes from a low base and one-time items, the underlying operational improvements are real.

Foreign exchange dynamics add another dimension. With 100% of revenues in U.S. dollars but majority costs in Indian rupees and Philippine pesos, every 1% depreciation in the rupee adds directly to margins. This natural hedge means Sagility benefits from emerging market currency weakness—a built-in tailwind for margins.

The capital efficiency metrics are where Sagility really shines compared to traditional healthcare companies. No massive hospital buildings to construct. No expensive medical equipment to purchase. No drug development costs. The primary assets walk out the door every evening—and the key is making sure they come back the next morning. This asset-light model means that growth requires minimal capital investment, allowing for high returns on invested capital.

Contract economics matter enormously. Most contracts are multi-year (typically 3-5 years) with built-in price escalations. This provides revenue visibility that most businesses would kill for. Moreover, the contracts often have volume commitments, ensuring baseline utilization, with upside for additional volume. Some contracts include gain-sharing provisions where Sagility participates in the cost savings it generates for clients.

The technology investments are starting to show returns. While the company doesn't break out technology spend separately, industry sources suggest 8-10% of revenues go toward technology and innovation. This isn't just IT infrastructure—it's building proprietary platforms, training AI models, and creating automation tools. These investments have high upfront costs but near-zero marginal costs once deployed.

Looking at peer comparisons, Sagility trades at a discount to pure-play healthcare technology companies but at a premium to traditional BPO firms—exactly where it should be as a hybrid model. The market is still figuring out how to value this unique combination of services and technology, creating potential opportunity for investors who understand the model.

The cash generation profile is robust. Though the company is reporting repeated profits, it is not paying out dividend—a sign that management sees better uses for capital, whether organic investment or acquisitions. With the PE owner still holding majority stake, the focus remains on value creation rather than dividend distribution.

The path to $1 billion in revenue by 2026 implies roughly 15% annual growth from current levels—aggressive but achievable given the market dynamics and recent acquisition. More importantly, if margins continue expanding at even half the recent rate, profit growth will substantially exceed revenue growth, creating significant shareholder value.

IX. Technology, AI & The Future of Healthcare Operations

The conference room in Sagility's Bangalore office has a wall of screens showing real-time metrics: claims processed, average handling time, accuracy rates, denial percentages. But increasingly, these screens also show something else—AI confidence scores, automation rates, and pattern recognition alerts. This is the future of healthcare operations, and it's being built in real-time.

Sagility's technology strategy isn't about replacing humans with machines—it's about making humans superhuman. When a medical coder in Chennai can process three times as many claims with AI assistance, when a nurse in Manila can review prior authorizations with predictive analytics guiding her decisions, when pattern recognition can flag potential fraud that human reviewers would miss—that's the multiplier effect of technology in healthcare operations.

The company's platforms include document processing engines, genAI solutions for customer engagement, nurse assist, provider forward, and contract central. These aren't just rebadged third-party tools—they're proprietary platforms built on deep healthcare domain expertise. The document processing engine, for instance, can extract information from unstructured medical records with accuracy rates exceeding 95%—crucial when a single missed diagnosis code can mean thousands in lost revenue.

The BirchAI acquisition brought cutting-edge GenAI capabilities in-house. Their transformer-based natural language processing doesn't just read medical records—it understands context, identifies relationships between conditions and treatments, and can even suggest appropriate codes based on clinical documentation. This isn't theoretical—it's processing millions of documents monthly, getting smarter with each one.

Consider the prior authorization challenge. Traditionally, a nurse would review each request, check criteria, gather documentation, and make a determination—a process taking hours or days. Sagility's AI can now predict with >90% accuracy which authorizations will be approved, automatically gather required documentation from electronic health records, and present a complete package for human review. The nurse still makes the final decision, but now processes 10x the volume.

The automation roadmap is ambitious but grounded in reality. Level 1: Robotic Process Automation for routine tasks—logging into systems, copying data, filling forms. Level 2: Machine learning for pattern recognition—identifying billing anomalies, predicting denials, flagging compliance risks. Level 3: Natural language processing for unstructured data—reading doctor's notes, extracting diagnoses, understanding treatment plans. Level 4: Generative AI for complex interactions—drafting appeals letters, responding to patient inquiries, creating care summaries.

But here's the counterintuitive insight: the more Sagility automates, the more valuable its human workforce becomes. When machines handle the routine, humans can focus on the exceptional—the complex appeals that require clinical judgment, the patient interactions that need empathy, the provider relationships that demand trust. This isn't about fewer jobs; it's about better jobs.

The competitive moat in healthcare AI isn't just algorithms—it's data. Sagility processes over 150 million transactions annually, each one a training example. But more importantly, they have the outcomes data. They know which claims were ultimately paid, which appeals succeeded, which prior authorizations led to good patient outcomes. This feedback loop is impossible to replicate without being in the workflow.

The platform approach is crucial. Rather than building point solutions, Sagility is creating an integrated ecosystem. The same data that powers claims processing feeds the payment integrity engine. The patterns identified in prior authorization improve denial prevention. The member interaction insights enhance provider engagement. It's a virtuous cycle where each component strengthens the others.

Healthcare's regulatory environment, often seen as a barrier to innovation, actually advantages Sagility. HIPAA compliance, data security, audit requirements—these aren't afterthoughts but built into the platform architecture. While startups struggle with healthcare's complex requirements, Sagility's solutions are enterprise-ready from day one.

The GenAI revolution presents both opportunity and threat. Large language models can now pass medical licensing exams, understand clinical guidelines, and even generate treatment recommendations. But they also hallucinate, make errors, and lack the judgment that comes from experience. Sagility's approach—AI-assisted but human-governed—provides the best of both worlds: machine efficiency with human accountability.

Looking ahead, the convergence of several trends will reshape healthcare operations. Value-based care shifts focus from volume to outcomes, requiring sophisticated analytics to manage risk. Interoperability mandates mean data will flow more freely, creating opportunities for integration. Consumer expectations, shaped by Amazon and Netflix, demand real-time, personalized experiences. Sagility is positioning itself at the intersection of these trends.

The industry recognition tells the story: Major Contender & Star Performer in RCM... Leader in Healthcare Payer Operations PEAK Matrix® Assessment in 2022 and 2023. These aren't participation trophies—they're validation from industry analysts who deeply understand the space.

The real test of Sagility's technology strategy will be its ability to maintain margins while scaling. As volumes grow, can automation keep pace? As complexity increases, can AI maintain accuracy? As regulations evolve, can platforms adapt? The early evidence is promising, but the healthcare industry has a way of humbling those who underestimate its complexity.

What's clear is that the future of healthcare operations won't be purely human or purely automated—it will be a carefully orchestrated hybrid. Sagility's investment in both technology and talent, its focus on augmentation rather than replacement, and its deep domain expertise position it well for this future. The question isn't whether AI will transform healthcare operations—it's who will lead that transformation.

X. Playbook: Business & Investing Lessons

Every great business story teaches lessons that transcend its specific industry. Sagility's journey from a division within a conglomerate to a public company valued at over ₹20,000 crores offers a masterclass in value creation, operational excellence, and strategic positioning. Here are the key lessons for operators and investors alike.

The Private Equity Value Creation Playbook

EQT's transformation of HGS Healthcare into Sagility is textbook private equity, but executed with unusual precision. First, identify an undervalued asset trapped in the wrong structure—a specialized business buried in a conglomerate. Second, carve it out and give it focus, capital, and mandate to grow. Third, professionalize operations, upgrade technology, and accelerate growth through strategic acquisitions. Finally, achieve partial liquidity through public markets while maintaining control for future value creation.

The key insight: value wasn't created through financial engineering or cost-cutting alone. It came from recognizing that a specialized healthcare services business deserved a specialized strategy, management team, and investor base. The 3-year transformation timeline—from acquisition to IPO—shows that with the right strategy and execution, value creation can be rapid without being reckless.

Building Domain Expertise as a Competitive Advantage

In an era where everyone talks about disruption, Sagility shows the power of deep, accumulated expertise. Twenty-plus years of processing healthcare claims isn't easily replicated by a Silicon Valley startup or an Indian IT giant. The 1,280 registered nurses, 374 certified medical coders, and thousands of professionals who understand the byzantine rules of American healthcare—this is intellectual capital that compounds over time.

The lesson: in complex, regulated industries, domain expertise is the ultimate moat. It's not enough to be smart or have good technology. You need to understand why Medicare Advantage claims process differently than commercial claims, why certain modifiers matter in certain states, why some payers require specific documentation formats. This knowledge, encoded in people and processes, becomes increasingly valuable as complexity grows.

Geographic Arbitrage in Knowledge Work

Sagility's model goes beyond simple labor cost arbitrage. It's about accessing talent pools that wouldn't otherwise participate in the U.S. healthcare system. The Filipino nurse who understands American healthcare but chooses to stay in Manila. The Indian engineer who can build healthcare platforms but doesn't want to relocate to Seattle. The Jamaican customer service rep who works U.S. hours but at Caribbean costs.

The sophisticated insight: geographic arbitrage in knowledge work isn't just about cost—it's about capability. Different locations offer different advantages. India for technology and analytics. Philippines for clinical expertise and customer service. Jamaica for near-shore convenience. The U.S. for client relationships and regulatory expertise. The art is orchestrating these capabilities into a seamless delivery model.

The Importance of Scale in Healthcare BPO

Healthcare BPO exhibits powerful economies of scale, but not in the traditional sense. It's not about spreading fixed costs over more volume—it's about learning curves, data network effects, and operational density. Every claim processed makes the next one easier. Every denial pattern identified prevents future denials. Every client added enriches the knowledge base for all clients.

The math is compelling: building the technology platform, training the workforce, achieving compliance certifications—these are largely fixed costs. But once you have them, the marginal cost of serving additional clients drops dramatically. This creates a winner-take-more dynamic where scaled players like Sagility have structural advantages over subscale competitors.

Platform Consolidation Strategies

Sagility's acquisition strategy reveals sophisticated thinking about platform value. Rather than buying competitors for market share (horizontal consolidation), they're buying capabilities that strengthen the platform (vertical integration). Devlin for payment integrity. BirchAI for GenAI capabilities. BroadPath for work-from-home expertise and mid-market clients.

Each acquisition makes the next one more valuable. BirchAI's technology makes BroadPath's agents more productive. BroadPath's client base provides more data for BirchAI's models. Devlin's payment integrity expertise can be cross-sold to BroadPath's clients. It's a compounding effect that accelerates with each addition to the platform.

Public Market Arbitrage Between India and U.S. Valuations

Here's the fascinating arbitrage: Sagility generates 100% of its revenues from the U.S., serves American clients, and competes with U.S. companies. Yet it's listed in India at Indian multiples. U.S. healthcare technology companies trade at 4-6x revenues; Indian IT services companies at 2-3x. Sagility, as a hybrid, trades somewhere in between—creating opportunity for investors who recognize its true nature.

The broader lesson: listing geography matters less than business quality, but market perception creates opportunities. As Indian capital markets mature and global investors increase allocation to India, companies like Sagility that straddle geographies can benefit from multiple expansion as markets better understand their business models.

The Human + AI Partnership Model

While pure-play AI companies get headlines and sky-high valuations, Sagility shows that the real value in enterprise AI comes from thoughtful human-machine partnership. Their approach—using AI to augment human expertise rather than replace it—may seem less revolutionary but is far more practical and valuable in complex domains like healthcare.

The investment insight: look for companies that use AI to make their existing operations better rather than those trying to reinvent everything with AI. The former can show immediate ROI and compound improvements; the latter often struggle with adoption, accuracy, and accountability.

Riding Secular Trends While Managing Cyclical Risks

Healthcare outsourcing benefits from powerful secular trends: aging populations, increasing complexity, cost pressures, and regulatory burden. These aren't going away regardless of economic cycles. But Sagility also has natural hedges: when economy booms, healthcare utilization increases; when it busts, cost reduction becomes paramount. This counter-cyclical characteristic provides stability that pure growth companies lack.

The Power of Boring

In a market obsessed with disruption, there's value in the boring but essential. Processing claims isn't sexy. Managing prior authorizations doesn't make headlines. But these functions are absolutely critical to the healthcare system functioning. Sagility has built a large, profitable, growing business by excel at the mundane but necessary.

The meta-lesson: the best businesses often do things that others don't want to do, can't do, or don't think are worth doing. The mundane can be magnificent if you do it better than anyone else, at scale, with technology leverage, and with deepening competitive moats.

XI. Analysis & Bear vs. Bull Case

Every investment thesis has two sides, and Sagility is no exception. The bull case is compelling, but the bear case has merit. Let's examine both with the intellectual honesty that good investing requires.

Bull Case: The Structural Growth Story

The bulls see Sagility as perfectly positioned at the intersection of several powerful trends. U.S. healthcare spending continues its inexorable climb—approaching $5 trillion annually—and administrative complexity grows even faster. Every new regulation, every new treatment modality, every new payment model adds complexity that someone needs to manage. Sagility is that someone.

The demographic tailwind is undeniable. Ten thousand Americans turn 65 every day, entering Medicare and driving massive volume growth in the exact services Sagility provides. Medicare Advantage penetration continues rising, adding layers of complexity as private insurers manage government benefits. The aging population doesn't just mean more claims—it means more complex claims, more chronic conditions, more care coordination.

Client relationships represent perhaps the strongest bull argument. When you're processing millions of claims for a major insurer, handling their payment integrity, managing their prior authorizations—you're not a vendor, you're part of their operational DNA. The 17-year average tenure of top clients isn't just a nice statistic—it's proof of switching costs so high that client relationships are essentially permanent.

The technology transformation story is just beginning. As AI and automation take hold, margins should expand dramatically. Every process automated, every pattern recognized, every error prevented drops straight to the bottom line. The company is still early in this journey—current EBITDA margins in the low-20% range could expand to 30%+ as technology leverage increases.

Platform consolidation provides a clear path to growth. The U.S. healthcare services market remains fragmented with hundreds of small, specialized firms. Sagility, with its public currency and scaled platform, can roll up these subscale players at attractive multiples, immediately benefit from cost synergies, and cross-sell services to expanded client bases.

Geographic expansion offers another growth vector. While the U.S. represents the largest opportunity, other developed markets face similar challenges. The UK's NHS, Canada's provincial systems, Australia's hybrid model—all struggle with administrative complexity and cost pressures. Sagility's model is exportable, and early expansion could capture first-mover advantages.

The valuation argument is straightforward: quality at a reasonable price. Trading at roughly 30x earnings, Sagility is priced like a mature IT services company but growing like a healthcare technology firm. As the market better understands the model—not just labor arbitrage but technology-enabled services with high switching costs—multiple expansion seems likely.

Bear Case: The Risks Are Real

The bears have legitimate concerns, starting with concentration risk. Despite recent diversification, Sagility remains heavily dependent on a handful of large U.S. payers. The loss of even one major client would be devastating. While switching costs are high, they're not infinite—a determined client could insource operations or switch to a competitor over time.

Regulatory changes represent an existential risk. What if the U.S. moves to single-payer healthcare? What if administrative simplification actually succeeds? What if new regulations favor onshore operations? The company's entire business model depends on U.S. healthcare remaining complex, fragmented, and outsourceable—a bet that has been right historically but isn't guaranteed forever.

AI disruption cuts both ways. Yes, Sagility is adopting AI, but what if breakthrough technologies make their human-heavy model obsolete? Large language models are improving exponentially. Google, Microsoft, and Amazon are all investing heavily in healthcare AI. Could a pure-technology solution eventually eliminate the need for thousands of offshore workers processing claims?

Competition from Indian IT giants looms large. Infosys, TCS, Wipro—all have healthcare practices and could decide to seriously compete in healthcare BPO. They have deeper pockets, broader client relationships, and strong technology capabilities. If they decided to buy their way into the market or undercut on price, Sagility could face margin pressure.

The wage inflation challenge is structural. As India develops, wage expectations rise. The cost arbitrage that makes the model work erodes over time. Yes, Sagility can move work to lower-cost locations, but there's a limit to this strategy. Eventually, you run out of cheaper places with sufficient talent.

Healthcare reform, while always talked about and never achieved, remains a tail risk. Both U.S. political parties agree healthcare costs are too high. Administrative waste is an obvious target. While wholesale reform seems unlikely, even marginal simplification could impact volumes and margins.

The macro sensitivity concern is real. While healthcare is relatively recession-resistant, it's not recession-proof. Elective procedures get delayed. Employers cut benefits. Unemployed people lose insurance. A severe recession could impact volumes more than bulls expect.

Quality and compliance risks can't be ignored. Sagility handles sensitive health information for millions of Americans. One major data breach, one systematic coding error, one compliance failure could damage relationships and trigger massive liability. The company's offshore operations add complexity to oversight and increase operational risk.

The Balanced View

The truth, as usual, lies somewhere between the extremes. Sagility is neither a guaranteed winner nor a disaster waiting to happen. It's a solid business with real competitive advantages, operating in a growing market, but facing genuine risks and challenges.

The key questions for investors: - Is the U.S. healthcare complexity problem solvable? (Probably not in our lifetimes) - Can Sagility maintain its competitive position against larger players? (Yes, if they continue executing) - Will AI be a friend or foe? (Friend if they adapt, foe if they don't) - Can margins expand while maintaining quality? (The early evidence says yes) - Is the valuation reasonable given the risks? (At current levels, arguably yes)

The most likely scenario is neither explosive growth nor dramatic decline, but steady expansion as Sagility benefits from structural tailwinds while navigating operational challenges. For investors with moderate risk tolerance and multi-year time horizons, the risk-reward appears favorable. For those seeking either hyper-growth or deep value, better opportunities likely exist elsewhere.

XII. Epilogue & "If We Were CEOs"

Standing at the crossroads of 2025, Sagility has achieved remarkable success but faces defining choices ahead. The path from $600 million to $1 billion in revenue by 2026 is visible but not guaranteed. If we were running this company, here's how we'd think about the road ahead.

The Path to $1 Billion: Execution is Everything

The $1 billion target isn't just a nice round number—it's a psychological threshold that separates the serious players from the also-rans. Achieving it requires roughly 15% annual growth, which breaks down to roughly 8-10% organic growth plus 5-7% from acquisitions. The BroadPath acquisition gets us partway there, but execution on integration and cross-selling will determine success.

We'd focus relentlessly on Net Revenue Retention (NRR)—the percentage of revenue retained and expanded from existing clients. Currently around 110%, we'd target 120%+ by systematically expanding services within existing accounts. Every client using claims processing should also use payment integrity. Every payer client is a potential provider RCM opportunity through their network relationships.

Expansion Beyond U.S. Markets: The Next Frontier

The U.S. will remain the core market, but geographic concentration is a strategic vulnerability. We'd establish beachheads in other English-speaking markets with complex healthcare systems. The UK, despite the NHS's public nature, increasingly outsources administrative functions. Canada's provincial systems face similar pressures. Australia's hybrid model creates opportunities.

The approach would be opportunistic acquisition rather than organic entry. Find a local player with client relationships and regulatory knowledge, acquire them, then leverage Sagility's technology and operational excellence to improve margins and expand services. Think of it as the BroadPath playbook applied internationally.

Building Proprietary Healthcare Tech Products

Services are good; products are better. We'd invest aggressively in productizing our capabilities. The prior authorization engine that processes millions of requests? Package it as a SaaS solution for mid-market payers. The payment integrity algorithms that identify billions in savings? License them to health systems wanting to self-serve.

This isn't about abandoning services—it's about climbing the value chain. Products have higher margins, create stickier relationships, and can scale without linear headcount growth. Start with hybrid models where products are bundled with services, then gradually unbundle as products mature.

M&A Strategy: Capability Aggregation Over Market Share

The next wave of acquisitions should focus on capability gaps rather than just adding revenue. We'd target:

- A clinical analytics company to deepen healthcare AI capabilities

- A patient engagement platform to extend beyond B2B into B2B2C

- A revenue cycle automation company to accelerate provider-side technology

- A specialized Medicaid processor to diversify payer mix

Each acquisition should strengthen the platform effect, where 1+1=3 through cross-selling, technology leverage, and operational synergies. We'd avoid large, transformational deals that risk integration challenges, preferring smaller, digestible acquisitions that can be quickly integrated.

The Technology Transformation: From Services to Solutions

The biggest strategic shift would be repositioning from a services company that uses technology to a technology company that provides services. This isn't just marketing—it requires fundamental changes in investment allocation, talent acquisition, and client engagement.

We'd establish a Silicon Valley innovation lab, not to be trendy but to access talent and partnerships unavailable in India. Hire engineers from Google and Microsoft who understand enterprise AI. Partner with Stanford and MIT on healthcare AI research. Build relationships with health tech startups that could become acquisition targets or partnership opportunities.

Talent Strategy: The War for Healthcare Expertise

The constraint on growth isn't capital or clients—it's talent. We'd implement radical approaches to talent acquisition and retention: - Partner with nursing schools in the Philippines to create Sagility-specific curricula - Establish coding academies in tier-2 Indian cities with guaranteed job placement - Create an internal university for continuous upskilling - Implement an employee stock ownership plan that goes deep into the organization

The goal: make Sagility the employer of choice for anyone interested in healthcare operations and technology. When the best talent consistently chooses you, competitive advantages compound.

Financial Strategy: Balancing Growth and Returns

With strong cash generation and minimal capital requirements, we'd implement a balanced capital allocation strategy: - 40% reinvested in organic growth (technology, talent, infrastructure) - 30% allocated to strategic acquisitions - 20% returned to shareholders through dividends once the business stabilizes - 10% reserved for opportunistic investments or buybacks

The key is maintaining flexibility while signaling confidence. A modest dividend would attract a different investor base while retaining capital for growth investments.

The ESG Angle: Healthcare Equity Through Operations

We'd lean into the social impact story. Sagility helps make healthcare more efficient and accessible. Every claim processed correctly means a patient gets care. Every prior authorization approved quickly means treatment isn't delayed. Every billing error caught means lower costs for everyone.

Create a Healthcare Equity Institute that publishes research on administrative burden in healthcare. Partner with nonprofits to provide free services to safety-net providers. Establish metrics around patient impact, not just financial performance. This isn't just corporate social responsibility—it's building a purpose-driven organization that attracts mission-oriented talent and clients.

The Long Game: Building a Healthcare Operating System

The ultimate vision would be to build the operating system for healthcare administration. Just as Microsoft Windows became the default platform for personal computing, Sagility could become the default platform for healthcare operations. Every payer, every provider, every patient interaction flowing through Sagility's platforms and services.

This requires thinking in decades, not quarters. It means sacrificing short-term margins for long-term positioning. It means building ecosystems, not just businesses. But the payoff—becoming truly indispensable to the healthcare system—would create value far beyond what any traditional services company could achieve.

Final Reflections

Sagility's story is still being written. From its origins in the back offices of HGS to its emergence as a public company, it has defied easy categorization. Not quite a BPO, not quite a tech company, but something uniquely positioned for the complexities of modern healthcare.

The challenges ahead are real: technological disruption, competitive threats, regulatory uncertainty. But so are the opportunities: an aging population, increasing complexity, technological leverage, and global expansion possibilities.

What makes Sagility fascinating isn't just its business model or financial performance—it's what it represents for the future of global services. In a world where AI threatens to automate everything, Sagility shows that human expertise, augmented by technology and delivered globally, remains irreplaceable in complex domains.

For India, Sagility represents the evolution from back-office outsourcing to strategic partnership, from cost arbitrage to capability arbitrage, from doing what others don't want to do to doing what others can't do.

For healthcare, Sagility embodies both the problem and the solution—the administrative complexity that drives costs but also the operational excellence that can contain them.

For investors, Sagility offers a window into a unique business model that combines the stability of healthcare, the growth of technology, and the efficiency of global delivery.

The next chapter of Sagility's story will be written by its ability to execute on these opportunities while navigating the challenges. If past is prologue, there's reason for optimism. But in business, as in healthcare, past performance doesn't guarantee future results. What matters is the quality of the diagnosis, the appropriateness of the treatment, and the diligence of the follow-up.

Sagility has diagnosed the problem correctly: healthcare administration is broken and needs fixing. Their treatment—technology-enabled global services—is showing promising results. Now comes the hard part: the long-term follow-up that determines whether this is a cure or just symptom management.

For those watching from the sidelines—investors, competitors, clients, employees—the prescription is clear: pay attention. This story is far from over, and the implications extend far beyond one company's success or failure. This is about the future of work, the globalization of expertise, and the transformation of healthcare.

The examination is complete. The charts have been reviewed. The diagnosis is cautiously optimistic with regular monitoring recommended. In healthcare, as in investing, that's often the best prognosis one can hope for.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube