Rustomjee: Building Mumbai's Skyline

I. Introduction & Episode Roadmap

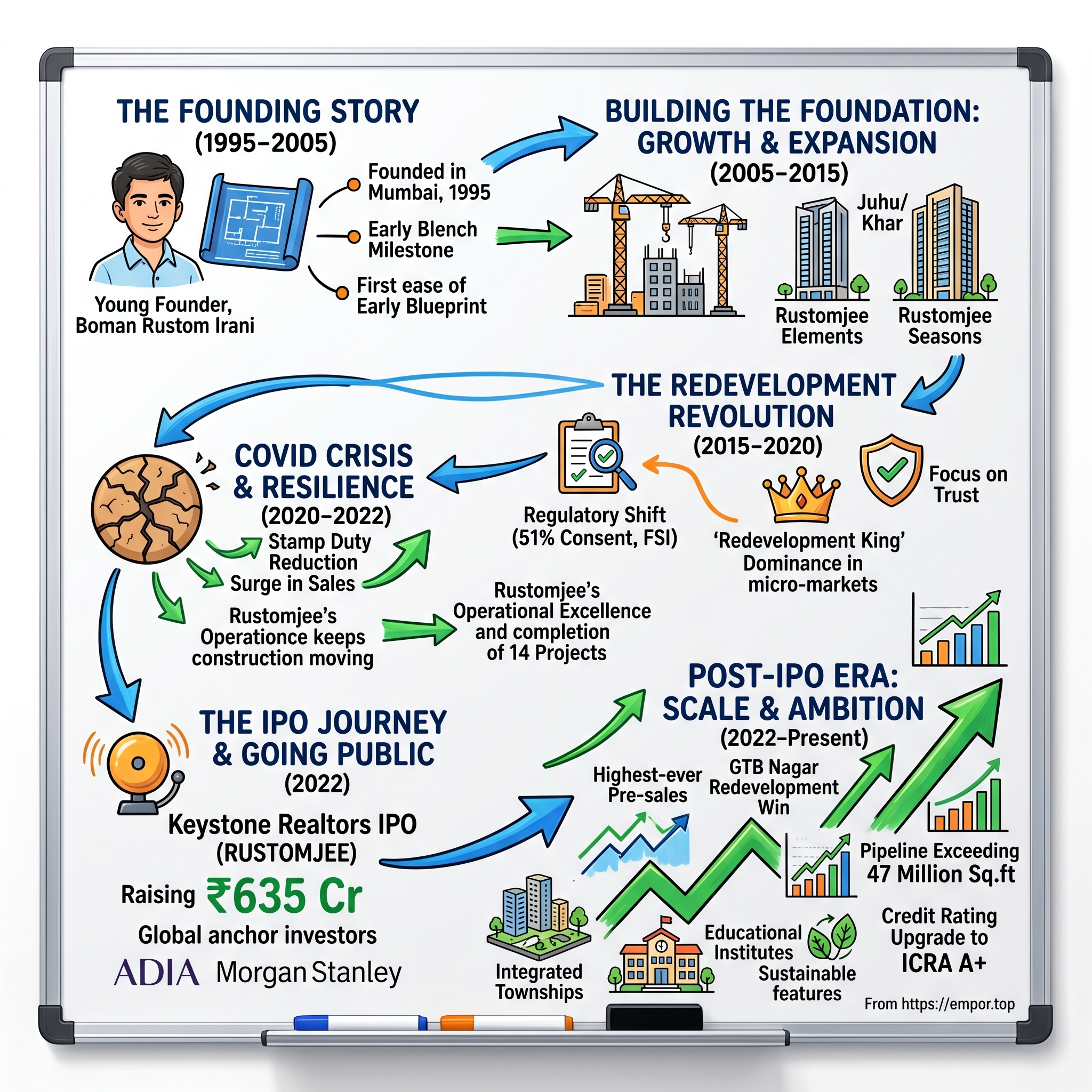

Picture this: It's a sweltering Mumbai afternoon in 1995. The city's skyline is transforming—cranes pierce the horizon, the liberalization wave has just unleashed entrepreneurial energy, and everyone wants a piece of India's commercial capital. In a modest office in suburban Mumbai, Boman Rustom Irani is sketching blueprints, not just for buildings, but for what would become one of Mumbai's most trusted real estate brands. He doesn't know it yet, but he's about to build a company that will house over 14,000 families and fundamentally reshape how Mumbai thinks about redevelopment.

Welcome to the story of Keystone Realtors Limited—better known by its brand name, Rustomjee. This isn't just another real estate developer's tale. It's the story of how a Mumbai-focused company became the undisputed redevelopment king of India's financial capital, commanding 28% market share in Khar, 23% in Juhu, and turning the complex art of society redevelopment into a scalable business model.

The November 2022 IPO marked a pivotal moment—not just for Rustomjee, but for understanding how regional real estate champions can thrive in India's fragmented property market. The company raised ₹635 crores through its IPO, but the real story isn't about the capital raise. It's about how a company built on the philosophy that "ideas form the cornerstones of buildings. Bricks and mortar are merely the blocks that help in realizing them" navigated Mumbai's labyrinthine real estate market for nearly three decades.

Today, we'll dissect how Rustomjee cracked the code on Mumbai's most challenging real estate opportunity: redevelopment. We'll explore their journey from a single-project developer to completing 37 projects and constructing 16 more, with a pipeline that reads like a who's who of Mumbai's premium neighborhoods. This is a masterclass in focus, trust-building, and understanding that in Mumbai real estate, location isn't just important—it's everything.

II. The Founding Story & Early Vision (1995–2005)

The Mumbai of 1995 was a city in transition. The economic liberalization of 1991 had unleashed entrepreneurial energy across India, but nowhere was it more palpable than in the Maximum City. Construction cranes dotted the horizon, land prices were climbing, and a new generation of developers was emerging. Into this milieu stepped Boman Rustom Irani, who founded the Rustomjee Group in 1995.

An engineer by profession who had attended the Harvard Leadership Program, Boman wasn't your typical real estate developer. He was adopted at birth, and his father—who ran one of the three large companies in the two-wheeler automobile space—passed away when Boman was just 19. The company was Ideal Jawa India Private Limited, and young Boman had dreams of becoming a motorcycle racer. Life, however, had other plans.

His humble family owned farms in Dahisar and Dahanu, and his father, interested in motorbikes, had set up a motorcycle factory in Mysore with his brothers. This background—straddling industry and land—would prove crucial in shaping Boman's approach to real estate. He understood both the discipline of manufacturing and the value of land, a rare combination in Mumbai's property market.

The philosophy that would define Rustomjee was crystallized early: "Ideas form the cornerstones of buildings. Bricks and mortar are merely the blocks that help in realizing them." This wasn't just marketing speak—it was a fundamental belief that real estate wasn't just about construction, but about creating living experiences. In a market dominated by builders focused on maximizing FSI (Floor Space Index) and cramming units, this was revolutionary thinking.

Mumbai's real estate context in the 1990s presented both enormous opportunity and significant challenges. The city was experiencing unprecedented urban growth—millions were pouring in from across India seeking opportunity. The old textile mills were shutting down, creating vast redevelopment opportunities. The emerging IT and financial services sectors were creating a new middle class with disposable income. Yet the market was fragmented, unorganized, and plagued by trust issues.

As a first-generation real estate developer with over 16 years of experience by 2012, Boman faced the classic entrepreneur's challenge: how to build credibility in an industry where established names dominated and customers were inherently skeptical. His solution was to focus obsessively on quality and customer satisfaction from day one.

The early projects were modest—single buildings in suburban Mumbai. But each one was executed with meticulous attention to detail. Rustomjee became one of the first real estate firms to receive an ISO 9001 certification in 2001—a signal to the market that this wasn't just another fly-by-night operator. This was a company building for the long term.

The business model that emerged was innovative for its time: partnering with landowners rather than purchasing land outright, with 30 partners to date by 2021. Remarkably, there had been no litigation or problems between Rustomjee and any of their partners—an almost unheard-of track record in Mumbai's contentious real estate market.

Building relationships with early customers required a different approach. Boman instituted an open-door policy at Rustomjee, sitting in the same-sized cabin as everyone else with a glass door that remained open. He was happy to interact on all levels and walk around construction sites personally. This accessibility was unusual in an industry known for its hierarchical, often inaccessible leadership.

The philosophy extended beyond business. Boman founded the Rustom Irani Foundation, which manages institutes in all spheres of education from pre-school to post-graduation, with capacity for more than 12,000 students. This commitment to education and community building would become a cornerstone of the Rustomjee brand—you weren't just buying an apartment; you were buying into a vision of community development.

By 2005, Rustomjee had established itself as a credible player in Mumbai's suburban real estate market. The company had developed a reputation for quality construction, timely delivery, and fair dealing with partners and customers. But this was just the foundation. The real transformation was about to begin, as Mumbai's real estate market entered a period of explosive growth that would test every developer's ability to scale while maintaining quality.

III. Building the Foundation: Growth & Expansion (2005–2015)

The year 2005 marked an inflection point. Mumbai's real estate market was entering a golden age—GDP growth was robust, the IT boom had created a new affluent class, and infrastructure projects like the Sea Link were transforming connectivity. For Rustomjee, this was the moment to scale from boutique developer to major player. They had the credibility, the relationships, and most importantly, the vision to ride this wave.

Boman Rustom Irani, who founded the Rustomjee Group in 1995, was an Engineer by profession and had attended the Harvard Leadership Program. This combination of technical expertise and global business exposure would prove critical as the company navigated its expansion phase. The strategy was clear: focus on premium micro-markets where quality commanded a premium and where the Rustomjee brand could become synonymous with trust.

The company heralded the rise of insightful design and eco-friendly construction technologies during this period. Rustomjee had significantly contributed to changing the Mumbai Skyline over 24 years. By June 30, 2022, they would have developed over 280 buildings and homes for over 14,000 families—but the journey to reach these numbers began in earnest during the 2005-2015 decade.

The flagship project that announced Rustomjee's arrival as a premium developer was Rustomjee Elements in Upper Juhu. Juhu is arguably Mumbai's most affluent suburb and home to some of the biggest names in Bollywood, boasting more celebrities per square kilometre than any other corner of the city. Rustomjee Elements, one of the most luxurious properties in Juhu is surrounded by high street retail destinations, popular nightclubs, fine-dining restaurants, bistros, lounges and pubs. It is located within a short drive of the Western Express Highway and the domestic and international airports, with a number of renowned educational institutions and world-class healthcare facilities in the vicinity.

This prime property in Juhu is conceptualised by renowned Hong Kong based architect James Law Cybertecture. These bespoke flats in Juhu boast of a 40,000 sq. ft. landscaped podium garden, an infinity rooftop swimming pool, sky lounge and other lavish amenities. With spacious limited edition 3, 4 and 5 bedroom luxury apartments in Juhu, this is a landmark so lavish, it deserves its own pincode.

The Elements project wasn't just about luxury—it was a statement of intent. By bringing in international architects and focusing on design elements typically reserved for ultra-luxury projects globally, Rustomjee was redefining what Mumbai real estate could be. The project attracted Bollywood celebrities, industrialists, and the city's elite, establishing Rustomjee as a brand that understood sophisticated living.

But Elements was just one piece of a larger puzzle. During this period, Rustomjee executed a series of strategic projects that would establish its dominance in specific micro-markets. Rustomjee Paramount emerged as a signature complex in Khar, while Rustomjee Seasons—a 3.82-acre gated community in Bandra Annexe—showcased the company's ability to create community living spaces in dense urban environments.

The numbers tell a compelling story of market domination through focused execution. The company commands a market share of 28% in Khar, 23% in Juhu, 11% in Bandra East, 14% in Virar, 3% in Thane, and 5% in Bhandup. These aren't random achievements—they represent a deliberate strategy of becoming the dominant player in specific high-value micro-markets rather than spreading thin across the entire city.

Since its inception in 1996, Rustomjee has heralded the rise of insightful design and eco-friendly construction technologies. This wasn't just marketing—the company was among the first to integrate sustainable building practices when "green building" was still a nascent concept in Indian real estate. Solar panels, rainwater harvesting, and waste management systems became standard features, not premium add-ons.

The period also saw Rustomjee perfect its partnership model. Rather than the traditional approach of purchasing land outright—which tied up capital and increased risk—the company pioneered joint development agreements with landowners. This asset-light approach allowed rapid expansion without the massive capital requirements that constrained many competitors. By 2021, the company had partnered with 30 landowners without a single litigation—a testament to their fair dealing and transparent approach.

What made this expansion remarkable wasn't just the scale but the consistency of execution. In an industry notorious for delays, cost overruns, and quality compromises, Rustomjee delivered project after project on time and to specification. Rustomjee has definitely carved a niche for itself in the ever-growing real estate sector and thus is a name synonymous with innovation, transparency and customer satisfaction.

The company's approach to community building extended beyond bricks and mortar. Boman Rustom Irani is also the founder and chief benefactor of the 'Rustom Irani Foundation' which manages and runs institutes in all spheres of education from pre-school to post-graduation, with the capacity of more than 12000 students. His vision aligned with his mission to 'Make Education a Priority' has led the Rustomjee Institutes to achieve an enviable reputation in a short span of time. This investment in education wasn't just corporate social responsibility—it was building the ecosystem that would support Rustomjee's communities for generations.

The leadership team that emerged during this period would prove crucial for the next phase of growth. Chandresh Dinesh Mehta is an Executive Director of our Company. He is the face behind the Group's operational excellence. He is an Engineer from IIT BHU and holds an MBA from Xavier's Institute of Management, Bhubaneshwar. Percy Sorabji Chowdhry is an Executive Director of our Company. He holds a bachelor's degree in commerce from the University of Bombay. He has 23 years of experience in real estate industry. He has been associated with our Company since 1999.

This wasn't a one-man show—it was a professional team building an institution. The combination of Boman's vision, Chandresh's operational excellence, and Percy's deep industry experience created a leadership troika that could handle both strategy and execution.

By 2015, Rustomjee had transformed from a single-building developer to a force reshaping Mumbai's skyline. Our portfolio includes 16.6 million sq.ft in completed development, 10.9 million sq ft in ongoing construction currently and a projected 22 million sq.ft in planned development spanning the best locations of Mumbai Metropolitan Region. The portfolio currently includes 2 very large townships, commercial spaces, retail developments, residential, spaces for healthcare and education spread across Prabhadevi, BKC Annexe, Khar, Off Juhu Circle, Kandivali, Borivali, Virar and Thane.

But the real transformation was yet to come. The company had built the foundation, established the brand, and assembled the team. Now it was time to tackle Mumbai's biggest real estate opportunity—and challenge—redevelopment.

IV. The Redevelopment Revolution (2015–2020)

Mumbai in 2015 presented a unique paradox. The city had some of the most expensive real estate in the world, yet thousands of buildings—many constructed in the 1960s and 70s—were crumbling. Housing societies were trapped: repair costs were astronomical, individual members couldn't afford reconstruction, and the regulatory maze made redevelopment seem impossible. This was the opportunity Rustomjee had been preparing for.

The State Government had approved Development Plan (DP) 2014-2034. The new DP 2034 had curtailed the rights of tenants residing in old residential buildings, reducing the minimum consent required from 70% to 51% to undertake redevelopment work. The reason given behind the move was to speed up the redevelopment projects in Mumbai city.

This regulatory shift was seismic. Suddenly, projects that had been stuck for years because a minority of residents held them hostage could move forward. But the opportunity came with enormous complexity. With real estate prices touching a new high, residents in old buildings discovered they had an opportunity to unlock immense value from their property by offering it to a Builder/Developer for redevelopment. Redevelopment is the process of demolishing existing old society building and reconstructing it by appointing a good Builder who can construct and handover new flats to the Society members free of cost with some additional benefits.

For Rustomjee, becoming "a leader in the redevelopment space" wasn't just about seizing an opportunity—it was about fundamentally reimagining their business model. The traditional approach of purchasing land and developing it required massive capital, carried significant risk, and limited growth potential. Redevelopment offered an alternative: partner with housing societies, provide them new homes at no cost, and profit from the additional saleable area created through increased FSI (Floor Space Index).

The mechanics were elegant but execution was brutal. In Mumbai, the permitted FSI varies in various locations depending upon the land and type of existing residence. In case of redevelopment, the builder gets incentive FSI of 50% or 60% of FSI over and above the FSI consumed to re-house the existing tenants. This meant a building that originally had 20 apartments could be rebuilt with 40 or more units—the original residents get new homes, and the developer sells the additional units for profit.

But here's where Rustomjee's approach diverged from competitors. While others saw redevelopment as a transactional opportunity, Rustomjee understood it was fundamentally about trust. A Redevelopment arrangement begins with the conception of an idea to redevelop the old building and it ends with the handing over of the agreed constructed area in new building and the corpus money or other monetary consideration to the Society by the Builder. Builders on their part are also on the lookout for properties with unused development rights where they can build a new structure of a few storeys higher and sell those additional flats for a tidy profit.

The company developed what can only be described as a "redevelopment playbook." First, identify buildings with the right profile: 30-50 years old, good location, cooperative society willing to engage. Second, spend months—sometimes years—building relationships with society members. Third, present a proposal that addresses not just the economics but the emotional concerns: Where will residents live during construction? How will elderly members cope with displacement? What guarantees exist for timely completion?

This patient approach paid dividends. Entering into joint development agreements, redevelopment agreements with landowners or developers or societies, and slum rehabilitation projects became Rustomjee's specialty. Each successful project became a reference point for the next. Society members would visit completed Rustomjee redevelopments, see the quality of construction, talk to residents about their experience, and return convinced.

The regulatory landscape during this period was evolving rapidly. Real Estate Regulation and Development Act (RERA) was introduced in 2016 in India to ensure transparency and accountability in the real estate sector. The act governs various aspects of real estate development, including redevelopment of properties. RERA rules for redevelopment are designed to provide transparency, accountability, and protection to property owners and buyers.

RERA's introduction could have been a challenge, but Rustomjee turned it into a competitive advantage. While many developers struggled with compliance, Rustomjee's existing systems—remember, they were ISO 9001 certified since 2001—meant they were already operating at standards RERA required. This gave societies additional confidence: here was a developer who welcomed regulation rather than feared it.

The complexities of managing multiple stakeholders in redevelopment projects cannot be overstated. Disputes between society members, the Managing Committee (Landowner) and the Developer were common. A dispute between society members and the society has to be resolved under Co-operative Society Act while a dispute between the society and builder is a civil dispute. Rustomjee developed specialized teams to manage these relationships—legal experts who understood cooperative society laws, community managers who could handle resident concerns, and project managers who ensured construction didn't disrupt neighboring buildings.

One innovation that set Rustomjee apart was their approach to temporary accommodation. While most developers offered a standard rent allowance during construction, Rustomjee went further—helping societies find suitable temporary housing, sometimes even developing rental properties specifically for this purpose. This attention to the human side of redevelopment built enormous goodwill.

The business model evolution during this period was remarkable. From land acquisition to joint development agreements represented a fundamental shift in how value was created and risk was managed. Builders/Developers, who opt to purchase land and develop the same, incur huge stamp duty cost on transfer of land. However, when it comes to redevelopment of old buildings, the stamp duty is reduced by a significant extent and this acts as a major benefit for developers.

By 2020, Rustomjee had become synonymous with redevelopment in Mumbai. They weren't just participating in the redevelopment boom—they were leading it, setting standards that others followed. The trust they built with housing societies became a moat that competitors found difficult to cross. When a society decided to redevelop, Rustomjee was invariably on the shortlist, often the preferred choice despite not always offering the highest commercial terms.

This period also saw Rustomjee expand beyond pure residential redevelopment. Commercial properties, mixed-use developments, and even slum rehabilitation projects entered their portfolio. Each brought unique challenges but also leveraged the core competency they had built: managing complexity, building trust, and delivering on promises in India's most challenging real estate market.

The redevelopment revolution had transformed Rustomjee from a premium developer into something more—a company that understood how to unlock value from Mumbai's aging building stock while navigating the city's complex social and regulatory landscape. This expertise would prove invaluable when COVID-19 struck, threatening to derail not just individual projects but the entire real estate sector.

V. COVID Crisis & Resilience (2020–2022)

March 2020. The city that never sleeps came to a grinding halt. Construction sites fell silent, migrant workers fled the city, and Mumbai's real estate market—which had been riding high on years of growth—faced an existential crisis. For 15 days, Boman Rustom Irani went into a shell when COVID hit in March 2020. Factories were shut, everything was over, the world had ended. His real estate business also—he was scared. "Boss, what's gonna happen? No one's gonna buy homes, no one's gonna buy offices. We're in trouble."

The numbers were catastrophic. The unprecedented scale of the impact of COVID-19 on Indian real estate can be gauged from the fact that the sector has incurred a loss of over Rs 1 lakh crore since the pandemic broke out. The sentiment scores of the real estate partners had arrived at an unequalled low score of 31. The crash of the real estate put many companies and brokers into bankruptcy. For a capital-intensive, long-cycle business like real estate, this wasn't just a temporary setback—it was potentially fatal.

But here's where Rustomjee's story diverges from the industry narrative. After the initial shock, a builder always has this blood group, always facing adversity. He always says something better will come out of this, so he's got to be positive no matter what. During the COVID period between April 2019 and March 2021, they completed fourteen projects with an aggregated saleable area of 1.73 million square feet. While competitors froze, Rustomjee kept building.

The Maharashtra government's response proved pivotal. Maharashtra Government took a well-thought and highly-appreciated decision by reducing the stamp duty from 5 percent to 2 percent until December 31, 2020. Following the trend, NAREDCO decided to give a Zero Stamp Duty booster to homebuyers from September 3, 2020, to October 31, 2020, which was later extended till December 31, 2020. This wasn't just a minor adjustment—it was a game-changer that would reshape Mumbai's property market.

What happened next defied all predictions. Home sales volume in Mumbai was recorded to be of 9,301 units in November 2020. Mumbai witnessed a record high volume of home sales at 9,301 units in the month of November 2020 which is a whopping 67 percent rise over November 2019. After the pandemic, real estate sales in Mumbai soared due to a combination of low-interest rates on loans and pent-up demand.

For Rustomjee, the pandemic became an opportunity to demonstrate operational excellence. While others struggled with labor shortages and supply chain disruptions, the company's integrated model—where they controlled everything from design to construction—proved its worth. They could pivot quickly, redeploy resources, and most critically, maintain construction momentum when others couldn't.

The company made several strategic decisions during this period that would pay dividends. First, they doubled down on redevelopment projects, which had lower capital requirements and were less affected by financing constraints. Second, they accelerated digital adoption—virtual site visits, online bookings, and digital documentation became standard. Third, and perhaps most importantly, they maintained communication with all stakeholders—housing societies waiting for redevelopment, customers in ongoing projects, and potential buyers sitting on the fence.

The demand for real estate in Mumbai is strong, especially now that all travel restrictions have been lifted and the economy is gradually returning to its previous pace. Registrations have nearly tripled in the last 60 days, with sales increasing from 7,635 in the third quarter of 2020 to 22,407 in the fourth quarter, a stunning 147 percent rise.

The psychology behind this surge was fascinating. According to a survey performed by ANAROCK Property Consultants and the Confederation of Indian Industry (CII), about 62 percent of Indians believe that the period following the coronavirus outbreak is the best time to invest in real estate. The coronavirus outbreak and its consequences have persuaded them that owning a home is essential. The demand for homes is increasing at a dizzying pace as new cultures such as work-from-home and online education pervade practically every household, sparking the desire for additional space.

Rustomjee read this shift perfectly. They repositioned their marketing to emphasize space, community amenities, and the security of owning versus renting. Projects were reconfigured where possible to add home offices and study areas. The messaging shifted from luxury and location to safety and stability—exactly what pandemic-shocked buyers wanted to hear.

The financial management during this period deserves special mention. While many developers faced severe liquidity crunches, Rustomjee's asset-light model and strong pre-sales meant they had better cash flow visibility. They could afford to offer attractive payment plans to buyers without compromising their own financial stability. This wasn't luck—it was the result of years of conservative financial management paying off when it mattered most.

By late 2021, a remarkable transformation had occurred. In December 2020, when the pandemic lockdown restrictions were lifted in Maharashtra, there was a surge in property registrations in Mumbai with 19,581 agreements translating into Rs680.49 crore of revenue. Such a high number was also on account of the Government rolling out a partial stamp duty waiver, dropping the rate to 2% between September and December 2020 and 3% between January and March 2021.

The company's decision to continue construction during the pandemic also built enormous goodwill. Housing societies saw that Rustomjee didn't abandon projects when times got tough. Customers appreciated that delivery timelines were largely maintained despite unprecedented challenges. This reputation for reliability in crisis became a powerful differentiator as the market recovered.

Internally, the pandemic forced operational innovations that made the company stronger. Site safety protocols improved dramatically. Digital project management tools that were nice-to-have became mission-critical. The ability to manage projects remotely meant senior management could be more involved in multiple projects simultaneously. These efficiencies didn't disappear when the pandemic ended—they became part of Rustomjee's operational DNA.

The human dimension of Rustomjee's pandemic response set them apart. Even today, Boman Irani maintains an open-door policy at Rustomjee, allowing most people to come and talk to him. If you come to his office, you'll be surprised—he sits in the same-sized cabin as everybody else with a glass door. "I'm very happy to interact on all levels. When I go to my sites, I'm happy to walk around." This accessibility and hands-on approach during crisis built loyalty that money couldn't buy.

By early 2022, Rustomjee had not just survived the pandemic—they had thrived. Data from the Inspector General of Registrations show that 1,22,033 properties were registered in Mumbai in 2022, drawing Rs8,900.52 crore into Maharashtra's coffers. Property registration and revenue collection surpassed pre-pandemic numbers for the second year running. In calendar year 2019, 67,863 properties were registered in the city, just about half the 2022 number.

The stage was set for the next chapter. The company had proven its resilience, the Mumbai market was booming again, and investor confidence in real estate was returning. It was time to tap the capital markets and fund the next phase of growth. The IPO journey was about to begin.

VI. The IPO Journey & Going Public (2022)

The boardroom at Rustomjee's headquarters was unusually quiet on a November morning in 2022. After 27 years of building Mumbai's skyline, the company was about to take its most public step yet. The decision to go public wasn't made lightly—it represented a fundamental shift from private entrepreneurship to public accountability, from family control to market scrutiny.

Incorporated in 1995, Keystone Realtors Limited is one of the prominent real estate developer. The company is engaged primarily in the business of real estate construction, development and other related activities in India. As of June 30, 2022, the company had 32 Completed Projects, 12 Ongoing Projects and 21 Forthcoming Projects across the Mumbai Metropolitan Region ("MMR") that includes a comprehensive range of projects under the affordable, mid and mass, aspirational, premium and super premium categories, all under the Rustomjee brand.

The timing seemed counterintuitive. Global markets were jittery, interest rates were rising, and the post-pandemic euphoria in real estate was showing signs of cooling. Yet Boman and his team saw opportunity where others saw risk. The Mumbai real estate market had proven its resilience, Rustomjee had a robust pipeline, and most importantly, they needed capital to fund their ambitious expansion plans.

Keystone Realtors IPO is a main-board IPO of 1,17,37,523 equity shares of the face value of ₹10 aggregating up to ₹635.00 Crores. The issue is priced at ₹541 per share. The structure was carefully designed: Keystone Realtors IPO had a fresh issue of up to ₹560 crore and an offer for sale of up to ₹75 crore.

The use of proceeds revealed the company's strategic priorities. The company intends to utilise the net proceeds towards funding the repayment/prepayment of borrowings to the tune of ₹341.6 crore as well as towards funding the acquisition of future real estate projects and general corporate purposes. This wasn't about financial engineering—it was about creating a stronger balance sheet to pursue bigger opportunities.

The roadshow preceding the IPO was a masterclass in storytelling. The Rustomjee team didn't just present financial metrics; they sold a vision of Mumbai's future. It commands a market share of 28% in Khar, 23% market in Juhu, 11% in Bandra East, 14% in Virar, 3% in Thane and 5% in Bhandup in terms of absorption (in units) from 2017 to 2021. These weren't just numbers—they represented market dominance in Mumbai's most coveted neighborhoods.

The anchor investor round proved pivotal. On Friday, Keystone Realtors said it has collected a little over ₹190 crore from anchor investors. The company decided to allot 35.21 lakh equity shares to 16 anchor investors at ₹541 apiece. Abu Dhabi Investment Authority, Morgan Stanley and Saint Capital accounted for nearly 35% of the anchor investor portion. Domestic mutual funds Aditya Birla Mutual Fund, IDFC Mutual Fund, Tata Mutual Fund and Quant Mutual Fund also participated in the anchor investor portion.

This mix of global and domestic institutional investors sent a powerful signal to the market. Here was a Mumbai-focused developer attracting capital from Abu Dhabi to Morgan Stanley—validation that the Rustomjee story resonated beyond local markets.

When the IPO opened on November 14, 2022, the response was measured but positive. The initial public offering (IPO) of Keystone Realtors, which sells properties under the brand 'Rustomjee', received 2 times subscription on the last day of offer on Wednesday, November 16, 2022. The issue got bids for 1,73,72,367 shares against 86,47,858 shares on offer.

In today's frothy IPO markets, a 2x subscription might seem modest. But for a real estate company in uncertain times, it represented solid investor confidence. The retail portion was oversubscribed, institutional investors participated meaningfully, and the grey market premium, while not spectacular, remained positive.

Axis Capital Limited, Credit Suisse Securities (India) Private Limited are the book running lead managers of the Keystone Realtors IPO, while MUFG Intime India Private Limited ((Link Intime) is the registrar for the issue. The choice of bankers—combining global expertise with local knowledge—reflected the company's positioning: rooted in Mumbai but ready for institutional capital.

The listing day, November 24, 2022, brought its own drama. Keystone Realtors IPO (Rustomjee) had a marginally positive listing on 24th November 2022, listing at a slight premium of 2.6%, and closing the day flat, almost very close to the listing price itself. While the stock did show some bouts of volatility during the day it closed the day at around the listing price with marginal gains. Keystone Realtors IPO (Rustomjee) closed nearly 3% above the issue price on the first day of trading on the NSE.

The muted listing might have disappointed day traders, but for long-term investors and the company's management, it was actually positive. A stable debut meant real investors, not speculators, had bought the stock. The company wouldn't have to deal with the volatility that often plagues IPOs with excessive listing gains.

What made the Keystone Realtors IPO particularly interesting was what it revealed about the company's business model and competitive advantages. Keystone Realtors Limited has an asset-light and scalable model resulting in profitability and stable financial performance. As part of its business model, the company focuses on entering into joint development agreements and re-development agreements with landowners or developers, or societies, which requires lower upfront capital expenditure compared to the direct acquisition of land parcels.

This asset-light approach was revolutionary in Indian real estate, where developers traditionally tied up massive capital in land banks. Rustomjee had figured out how to grow without the capital intensity that constrained competitors—and now they were taking this model public.

The IPO documents also revealed impressive operational metrics that hadn't been public before. June 30, 2022, Keystone Realtors have developed 20.22 million square feet of high-value and affordable residential buildings, premium gated estates, townships, corporate parks, retail spaces, schools, iconic landmarks and various other real estate projects.

The company's leadership in redevelopment was particularly striking. Keystone Realtors Limited is amongst the leading residential real estate development companies in MMR with a well-diversified portfolio and strong pipeline, the company commands a market share of 39% in Khar, 14% in Bandra East, and 14% in Juhu from the overall redevelopment supply between 2017 and 2021.

The IPO also marked a generational transition. While Boman Rustom Irani remained firmly in control as Chairman and Managing Director, going public meant instituting professional governance structures. Independent directors joined the board, quarterly reporting became mandatory, and the company's decisions would now be scrutinized by analysts and investors.

As part of the OFS, promoter Boman Rustom Irani will sell shares worth up to Rs 37.5 crore. This partial exit wasn't about cashing out—it was about creating liquidity while maintaining control. With promoter holding still at 78.4% post-IPO, the founding family retained firm control while welcoming public shareholders.

The market's initial assessment was pragmatic. Stock is trading at 2.95 times its book value. Company has a low return on equity of 6.81% over last 3 years. These metrics reflected the reality of real estate development—a capital-intensive, long-cycle business where returns come in spurts rather than steady streams.

But the IPO wasn't just about raising capital—it was about institutionalizing excellence. Public market discipline would force the company to maintain higher standards of disclosure, governance, and performance. For a company that had always prided itself on transparency with housing societies and customers, this was a natural evolution.

The timing, in retrospect, was shrewd. By going public when markets were cautious, Rustomjee avoided the hype and overvaluation that often accompany bull market IPOs. They attracted serious, long-term investors who understood real estate cycles and appreciated the company's focus on Mumbai's redevelopment opportunity.

As the closing bell rang on November 24, 2022, marking Rustomjee's first day as a public company, it marked not an end but a beginning. The company now had the capital, credibility, and currency (in the form of listed shares) to pursue larger opportunities. The real test would come in the quarters ahead—could they deliver on the promises made during the IPO? Could they maintain their culture and values as a public company? The post-IPO era was about to begin.

VII. Post-IPO Era: Scale & Ambition (2022–Present)

The post-IPO era has been nothing short of transformative for Keystone Realtors. Mumbai-based Keystone Realtors achieved the highest-ever quarterly pre-sales of ₹1,068 crore in April-June period of 2025-26 fiscal, a rise of 75% from the same quarter last year. This wasn't just growth—it was acceleration at a scale that few real estate companies achieve post-listing.

In 2024, it reported revenue of ₹1,149.13 Cr and a net worth of ₹1,653.11 Cr. The transformation from a private company to a public powerhouse was complete. Q1 FY26 pre-sales up 75%, launched 3 projects worth INR 40bn, credit rating upgraded to ICRA A+. The credit rating upgrade was particularly significant—it validated the company's financial management and opened doors to cheaper capital.

The numbers tell only part of the story. So far, it has delivered 26 million square feet of real estate across 37 completed projects. Currently, the company has 18 projects under execution and a future development pipeline exceeding 47 million square feet. This pipeline represents nearly double what the company had delivered in its entire history—a testament to the scale of ambition post-IPO.

Keystone Realtors Ltd bagged three Mumbai redevelopment projects in Q1 FY26 worth a combined ₹7,727 crore GDV. The company posted record pre-sales of ₹1,068 crore in April–June, up 75% YoY, and launched projects worth ₹4,000 crore. Keystone is actively scouting more land in the Mumbai Metropolitan Region to expand its residential real estate portfolio under the Rustomjee brand.

The business development momentum has been remarkable. Selected for redevelopment of 8 housing societies in Andheri West, gaining development rights and additional FSI. Keystone Realtors received LOA for GTB Nagar redevelopment project with MHADA, enabling additional FSI benefits. Company Has Been Selected By 8 Housing Societies As The Developer For The Large-Scale Cluster Redevelopment Project In The Highly Sought After Residential Neighborhood Of Andheri West, Mumbai.

These aren't just projects—they're transformative urban interventions. The GTB Nagar project alone has a GDV of Rs 4,521 crore and will benefit over 1,400 families. The scale and complexity of these projects would have been impossible without the credibility and capital access that came with being a listed company.

The strategic partnerships announced post-IPO have been game-changing. Joint venture between Ajmera Realty & Infra India Limited and Keystone Realtors Limited (Rustomjee), will execute a redevelopment project in Bandra West. Both companies will hold a 50% stake in the project, which is expected to generate a Gross Development Value (GDV) of INR 760 crores. This willingness to partner with competitors shows a maturity and confidence that comes from market leadership.

"In line with our proactive approach to business development, we added three new projects in Q1 FY26 (including two cluster redevelopment projects) with a combined GDV of ₹77.27 billion, which exceeds our entire FY26 business development guidance by more than 1.25x. This reinforces the success of our asset-light, capital-efficient model with a sharp focus on redevelopment within Mumbai MMR. With a healthy balance sheet and strong capitalisation, we remain well-equipped to pursue emerging opportunities and create sustainable value for all stakeholders," Irani said.

The financial discipline post-IPO has been exemplary. The company's gross debt stands at ₹304 crore, with a gross debt-to-equity ratio of 0.11 as of Q1 FY26. Rustomjee remains a net debt-free company. In an industry notorious for leverage, this conservative approach provides enormous flexibility to pursue opportunities without financial stress.

The company's approach to financial reporting is also evolving. To better align revenue with actual project progress, Keystone Realtors plans to shift to the percentage of completion method for its new launches going forward. This change, while potentially creating short-term volatility in reported numbers, will provide investors with better visibility into the company's actual performance.

The operational excellence continues to improve. Debtor days have improved from 21.7 to 15.2 days. This improvement in working capital management is crucial in real estate, where cash flow timing can make or break projects.

Boman Irani's leadership vision remains clear: "Q1FY26 has laid a strong foundation for the year, marking a pivotal moment for our company as we build on the solid momentum carried over from FY25. We recorded pre-sales of Rs 10.68 billion, reflecting a robust 75% year-on-year growth. During the quarter, we launched three projects with an estimated Gross Development Value (GDV) of Rs 40 billion, representing nearly 57% of our full-year FY26 guidance achieved in just the first quarter. On the business development front, we secured three new projects in Q1FY26, adding a GDV of Rs 77.27 billion. With this, we have already surpassed our full-year FY26 guidance for new additions. Mumbai's redevelopment opportunities continue to be a key strategic focus, and our leadership in this segment positions us well to harness the potential it offers."

The market's assessment has been nuanced but positive. While the stock hasn't been a multibagger post-listing, it has provided steady returns with lower volatility than many real estate stocks. Rustomjee target price ₹866.67, a slight upside of 33.52% compared to current price of ₹653.5. According to 3 analysts rating.

The company's expansion into new segments within real estate is noteworthy. While residential remains the core, there's increasing focus on mixed-use developments, commercial spaces within residential projects, and social infrastructure. The vision is to create integrated communities, not just buildings.

The post-IPO era has also seen significant organizational development. Professional managers have been inducted, systems have been strengthened, and the company is investing heavily in technology and talent. The family-run business is transforming into a professionally managed institution while retaining its entrepreneurial DNA.

"Our asset-light model, with a focus on redevelopment opportunities, particularly in Mumbai MMR, continues to be a key driver of growth." This statement encapsulates the strategic clarity that has emerged post-IPO. Rather than diversifying geographically or into new asset classes, Rustomjee is doubling down on what it does best—redevelopment in Mumbai.

Looking at the pipeline and momentum, the next few years promise to be transformative. Keystone Realtors aims for ₹4,000 crore in pre-sales by FY26, driven by strong demand in Mumbai's mid-market and aspirational housing segments. The company has a robust launch pipeline and is well-positioned in the redevelopment market, despite rising competition. Current market cap stands at ₹7,140 crore, with shares trading at ₹568.55, down 16% over the past year.

The journey from IPO to today has validated the decision to go public. Access to capital, enhanced credibility, and the discipline of quarterly reporting have made Rustomjee a stronger company. As Mumbai continues its transformation into a global city, Rustomjee is positioned to play a central role in shaping its skyline and communities.

VIII. The Business Model Deep Dive

The genius of Rustomjee's business model lies not in what it does—develop real estate—but in how it does it. While competitors tie up billions in land banks and struggle with capital efficiency, Rustomjee has crafted an approach that generates superior returns with minimal capital deployment.

The Company provides various residential buildings, premium gated estates, townships, corporate parks, retail spaces, schools, iconic landmarks and various other real estate projects. It offers one bedroom, hall, and kitchen (BHK), two BHK, three BHK, four BHK, and five BHK. But this product range is just the surface. The real innovation is in the execution model.

The asset-light approach is the cornerstone. Focus on redevelopment vs. land acquisition fundamentally changes the economics. In traditional development, a developer might spend ₹100 crores acquiring land, then need another ₹200 crores for construction. In Rustomjee's redevelopment model, that ₹100 crore land cost disappears—replaced by an agreement to give existing residents new homes. The capital efficiency is transformative.

Consider the math: In a typical redevelopment project, Rustomjee might rebuild a society of 50 units into a tower of 150 units. The original 50 owners get new, larger homes. Rustomjee sells the additional 100 units. The land cost? Zero. The only capital required is for construction and temporary accommodation for residents. This model can generate IRRs of 25-30%, compared to 15-18% for traditional development.

The integrated real estate development model for every stage of the property development life cycle, commencing from business development, which involves the identification of land parcels and the conceptualization of the development, to execution, comprising planning, designing and overseeing the construction activities, marketing and sales—this isn't just vertical integration, it's complete control over the value chain.

This integration provides multiple advantages. Quality control is absolute—from design to handover, every element meets Rustomjee standards. Timeline management improves dramatically when you don't depend on third-party contractors for critical path activities. Cost management becomes predictable when you control procurement and execution. Most importantly, the customer experience remains consistent across touchpoints.

Revenue recognition and cash flow dynamics in real estate are notoriously complex, and Rustomjee has mastered this complexity. The shift to percentage completion method for new projects provides better matching of revenue with actual work done. But the real sophistication is in cash flow management—structuring payment plans that fund construction while maintaining healthy margins.

The company's approach to managing project portfolio is surgical in its precision: 32 completed projects, 12 ongoing projects and 19 forthcoming projects across the Mumbai Metropolitan Region (MMR). Each project is at a different stage of the development cycle, ensuring steady cash flow and risk diversification. If one project faces delays, others compensate. This portfolio approach smooths out the inherent lumpiness of real estate development.

The redevelopment model itself deserves deeper analysis. When Rustomjee approaches a housing society, they're not just offering to rebuild—they're offering a complete solution. Temporary accommodation is arranged and often subsidized beyond the standard rent allowance. Legal complexities are handled by Rustomjee's in-house team. Society members get larger homes with modern amenities at zero cost. The entire risk of development, approvals, and construction is borne by Rustomjee.

This model creates powerful network effects. Every successful redevelopment becomes a reference project. Society members become ambassadors, recommending Rustomjee to other societies. The trust compounds over time. This is why Rustomjee commands dominant market share in specific micro-markets—once they establish trust in an area, it becomes nearly impossible for competitors to dislodge them.

The financial structuring of projects showcases sophisticated capital management. Rather than funding entire projects through debt, Rustomjee uses customer advances effectively. Pre-sales often fund 40-50% of project cost, reducing both capital requirements and risk. Construction finance covers the balance, but with pre-sales in place, banks offer better terms. This cascading capital structure minimizes equity requirements while maintaining healthy returns.

Risk management is embedded in the model. By focusing on redevelopment in established areas of Mumbai, location risk is minimal—these areas already have infrastructure, connectivity, and demand. Construction risk is managed through in-house execution and long-term vendor relationships. Market risk is mitigated by pre-sales and focus on mid-market segments with steady demand. Regulatory risk, while always present in Indian real estate, is managed through compliance systems and relationships built over decades.

The technology integration, while not visible to customers, drives operational efficiency. Building Information Modeling (BIM) reduces design errors and construction waste. Project management software ensures real-time tracking across multiple sites. Customer relationship management systems track every interaction from inquiry to handover. This tech stack, built over years, provides competitive advantages that are hard to replicate.

The model's scalability is perhaps its most impressive feature. Adding a new project doesn't require proportional increases in overhead. The same design team can handle multiple projects. Construction teams move from one project to another. The brand and trust built in one micro-market accelerate entry into adjacent areas. This operational leverage means margins improve with scale—a rarity in real estate.

Sustainability isn't just CSR—it's embedded in the business model. Redevelopment is inherently more sustainable than greenfield development. Demolition waste is recycled. New buildings are more energy-efficient than the structures they replace. Solar panels, rainwater harvesting, and waste management systems aren't add-ons but standard features. This sustainability focus resonates with modern buyers and provides regulatory advantages.

The sales and marketing approach reflects deep market understanding. Rather than carpet-bombing advertising, Rustomjee focuses on targeted marketing in specific micro-markets. The sales process emphasizes experience over hard selling—site visits, interaction with existing customers, and detailed walkthroughs of completed projects. The conversion rate from site visit to booking is among the highest in the industry.

Customer financing facilitation has become a crucial differentiator. Rustomjee doesn't just sell homes; they help customers buy them. Relationships with multiple banks ensure competitive mortgage rates. Documentation support simplifies the complex loan process. For redevelopment projects, they even assist original owners with paperwork for their new homes. This end-to-end support builds tremendous goodwill.

The model's resilience was proven during COVID. When construction stopped, the asset-light model meant lower fixed costs to manage. When demand returned, the ability to quickly restart projects provided first-mover advantage. The focus on redevelopment meant dealing with committed stakeholders (existing societies) rather than speculative buyers who might withdraw.

Looking forward, the business model positions Rustomjee perfectly for Mumbai's future. As the city densifies, redevelopment will only accelerate. As land becomes scarcer, the ability to unlock value from existing properties becomes more valuable. As customers become more sophisticated, the trust and track record Rustomjee has built become stronger moats.

This isn't just a business model—it's a system perfectly adapted to Mumbai's unique real estate market. Every element reinforces others, creating competitive advantages that compound over time. While competitors can copy individual elements, replicating the entire system—with its relationships, trust, capabilities, and track record—is virtually impossible. This is why Rustomjee's business model isn't just successful; it's sustainable for the long term.

IX. Competition & Market Position

Mumbai's real estate landscape reads like a who's who of Indian business dynasties: Lodha, Oberoi, Godrej, Hiranandani. Each name carries weight, commands respect, and has shaped Mumbai's skyline in distinctive ways. Yet in this constellation of established stars, Rustomjee has carved out a unique position—not by competing head-to-head, but by defining its own game.

The Mumbai real estate market is paradoxical. It's simultaneously the most expensive in India and the most undersupplied. It's where a 300-square-foot apartment can cost more than a villa in other cities, yet where millions still live in substandard housing. It's a market where location isn't just important—it's everything. A project in Khar commands 3x the price of an identical project in Kandivali, just 15 kilometers away.

In this complex landscape, A prominent MMR-based real estate developer and a leader in the redevelopment space, Rustomjee has chosen focus over diversification. While Lodha spans from London to Mumbai, while Godrej develops across India, Rustomjee remains laser-focused on Mumbai. This isn't limitation—it's strategic clarity.

The competitive advantages start with brand trust. In an industry where buyer-developer disputes are common, where project delays are routine, where quality compromises are expected, Rustomjee's track record stands out. Zero litigation with joint development partners over 30 partnerships. Consistent on-time delivery. Quality that matches promises. These aren't marketing claims—they're verifiable facts that matter in a trust-deficit industry.

The execution track record creates a powerful moat. When a housing society evaluates developers for redevelopment, they don't just look at proposals—they visit completed projects, talk to residents, check track records. Rustomjee's ability to point to successful redevelopments in the same neighborhood, to introduce society members to satisfied residents just blocks away, is invaluable. Competitors might match commercial terms, but they can't instantly create a 27-year track record.

Micro-market dominance is perhaps Rustomjee's most underappreciated advantage. Market share analysis in key locations reveals the strategy's success. In Khar, controlling 28% market share means Rustomjee isn't just a player—they're the market maker. They influence pricing, set quality standards, and shape buyer expectations. New entrants must position themselves relative to Rustomjee. This local dominance creates pricing power that translates directly to margins.

The pricing power and premium positioning deserve closer analysis. Rustomjee commands 5-10% premiums over comparable projects from other developers. This isn't because of luxury amenities or prime locations—competitors offer those too. The premium comes from trust, track record, and the confidence that buying Rustomjee means predictable execution and quality. In a market where a home purchase might represent 20 years of savings, that confidence is worth paying for.

The challenge from new entrants and national players is real but manageable. When DLF or Prestige enter Mumbai, they bring capital and brand recognition. But they lack local knowledge, relationships with housing societies, understanding of Mumbai's byzantine approval processes, and most importantly, trust built over decades. Rustomjee's embedded position in Mumbai's real estate ecosystem—relationships with contractors, architects, approval consultants, and local authorities—creates switching costs that money alone can't overcome.

Competition takes different forms across segments. In the luxury segment (₹5 crores+), Rustomjee competes with Lodha, Oberoi, and Raheja. Here, product differentiation and location matter more than price. In the mid-market segment (₹1-3 crores), competition includes Kalpataru, Kanakia, and dozens of smaller developers. Here, Rustomjee's execution reliability becomes the key differentiator. In affordable housing (under ₹1 crore), competition is fragmented but intense. Rustomjee's ability to deliver quality at these price points, leveraging their redevelopment model, provides an edge.

The competitive dynamics in redevelopment are particularly interesting. While every developer now claims to focus on redevelopment, few have Rustomjee's capabilities. Redevelopment requires patient capital (projects can take 5-7 years), stakeholder management skills (handling 100+ society members), and most importantly, trust. Rustomjee's leadership in redevelopment isn't just about market share—it's about capabilities that take years to build.

Lodha (now Macrotech) represents the most direct competition. They're larger, more diversified, and have deeper pockets. But their focus on scale and geographic expansion means less attention to specific Mumbai micro-markets. Their approach—large townships, massive marketing budgets, volume over margins—differs fundamentally from Rustomjee's focused, relationship-driven model. Both can coexist because they're essentially serving different customer needs.

Oberoi Realty operates at the ultra-luxury end, where Rustomjee selectively competes. Oberoi's model—few projects, ultra-premium positioning, long development cycles—means they're more complementary than competitive. A customer choosing between Oberoi and Rustomjee is really choosing between different philosophies of luxury living.

Godrej Properties brings the strength of the Godrej brand and access to patient capital. Their professional management and national presence are advantages. But in Mumbai, they're still building local credibility and relationships that Rustomjee has cultivated over decades. Their focus on large township developments also differs from Rustomjee's redevelopment-led model.

Hiranandani, with its focus on integrated townships and commercial development, operates in a different niche. Their Powai success created a template they're replicating elsewhere. But this model requires large land parcels—increasingly scarce in Mumbai—making it less competitive with Rustomjee's redevelopment focus.

The competitive advantage extends beyond direct competition to ecosystem relationships. Rustomjee's relationships with architects, contractors, and approval consultants create an informal barrier to entry. These professionals prefer working with Rustomjee because of consistent work, timely payments, and professional dealings. New entrants must not only compete for customers but also for these crucial ecosystem partners.

Financial strength has become increasingly important post-RERA. Many smaller developers couldn't adapt to RERA's compliance requirements and capital needs. This consolidation benefits established players like Rustomjee. Every competitor that exits increases Rustomjee's market share and pricing power. The regulatory environment that was supposed to level the playing field has actually strengthened established players' positions.

Technology adoption is emerging as a new competitive frontier. While not traditionally tech-focused, Rustomjee has quietly built capabilities in digital marketing, virtual reality for project visualization, and construction technology. They're not trying to be PropTech pioneers but fast followers, adopting proven technologies that enhance their core model.

Brand perception studies reveal Rustomjee's unique position. While not the largest or most luxurious, Rustomjee consistently ranks high on trust, value for money, and execution reliability. These aren't the most glamorous attributes, but they're what matter when making India's largest personal financial decision.

The competitive strategy going forward is clear: defend and deepen position in core Mumbai markets while selectively expanding in adjacent areas. Rather than geographic diversification, Rustomjee is pursuing depth—more projects in the same micro-markets, strengthening relationships, building switching costs. This focus strategy has proven more profitable than the diversification strategies pursued by competitors.

Looking ahead, competition will intensify as Mumbai's real estate market matures. International capital will enter through REITs and foreign developers. Technology will enable new models like co-living and fractional ownership. Customer expectations will continue rising. But Rustomjee's positioning—trusted, local, execution-focused—remains defensible. In a market where relationships and trust matter as much as capital and capability, Rustomjee's 27-year investment in Mumbai's real estate ecosystem provides competitive advantages that are nearly impossible to replicate.

X. Playbook: Real Estate Development Lessons

After nearly three decades of navigating Mumbai's real estate market, Rustomjee has developed a playbook that reads like a masterclass in building a sustainable real estate business in India's most complex market. These aren't theoretical frameworks but battle-tested principles forged in the crucible of Mumbai's unforgiving property market.

Building trust in a trust-deficit industry isn't a mission statement—it's an operational imperative. Every interaction, from the first sales call to the handover ceremony, is an opportunity to build or break trust. Rustomjee's approach is radical transparency. Construction progress is shared monthly with buyers. Financial statements are available to housing society members. Problems are communicated proactively, not hidden until they explode. This transparency is expensive and time-consuming but creates a moat competitors can't cross with capital alone.

The trust-building extends to small details that matter disproportionately. When a society visits a completed project, they meet actual residents, not paid actors. Sales teams are trained to under-promise and over-deliver, the opposite of industry norms. Legal documents are written in plain language, not deliberate obfuscation. These practices seem obvious but are revolutionary in Indian real estate.

The importance of location and micro-market focus cannot be overstated. Rustomjee doesn't just develop in Mumbai—they develop in specific neighborhoods where they understand every lane, every shop, every dynamic. They know that Khar West is different from Khar East, that 14th Road is more valuable than 13th Road, that proximity to the station matters more than sea view in certain pockets. This granular knowledge, accumulated over decades, informs every acquisition and development decision.

The micro-market focus extends to community understanding. Rustomjee knows which buildings have active societies, which have litigation histories, which have influential members who can swing decisions. This intelligence, gathered through years of presence and relationships, provides an information advantage that no amount of market research can replicate.

Managing regulatory complexity in Indian real estate requires a specific competency that Rustomjee has mastered. Mumbai's approval process involves multiple authorities—BMC, MHADA, Environment Department, Aviation Authority, Coastal Zone Management, Fire Department, and more. Each has its own requirements, timelines, and quirks. Rustomjee maintains a specialized team that does nothing but manage approvals. They know which documents each authority prioritizes, which officers are sticklers for detail, which applications get fast-tracked.

But regulatory management isn't just about navigation—it's about anticipation. Rustomjee studies proposed regulation changes, participates in industry consultations, and adapts proactively. When RERA was announced, they were ready on day one. When environmental norms tightened, they had already begun adapting designs. This proactive approach turns regulatory changes from disruptions into competitive advantages.

Cash flow management and project financing separate successful developers from failures. Real estate's long cycles and lumpy cash flows have killed more developers than market downturns. Rustomjee's approach is conservative but sophisticated. Projects are financially structured to be self-funding after initial investment. Customer advances are collected based on construction milestones, ensuring cash comes in as costs go out. Multiple projects at different stages ensure steady cash flow even if individual projects face delays.

The financing strategy extends beyond project level. Corporate debt is kept minimal, used for working capital rather than land acquisition. Banking relationships are cultivated carefully—Rustomjee works with multiple banks but maintains deep relationships with a core few. This ensures capital availability even during credit crunches that periodically hit Indian real estate.

The power of brand in residential real estate is often underestimated. Unlike commercial real estate where location dominates, residential purchases are emotional decisions where brand matters enormously. Rustomjee has built their brand not through massive advertising but through consistent delivery. Every project that delivers on time, every promise kept, every satisfied customer becomes a brand ambassador.

The brand strategy is deliberately focused. Rather than trying to be everything to everyone, Rustomjee stands for specific values: reliability, quality, and community living. They don't chase the ultra-luxury segment where they can't compete with Oberoi, nor the rock-bottom affordable segment where margins don't justify their overhead. They own the middle and upper-middle segment—the heart of Mumbai's housing market.

Redevelopment as a sustainable growth strategy is Rustomjee's most important strategic insight. As Mumbai runs out of developable land, redevelopment isn't just an option—it's the only option. But successful redevelopment requires capabilities beyond traditional development. You need to manage hundreds of stakeholders with different interests. You need patient capital for projects that can take 5-7 years. You need execution capability to deliver quality while managing costs.

Rustomjee's redevelopment playbook has been refined over dozens of projects. Start with smaller societies to build credibility. Offer terms slightly better than competition but focus on non-monetary benefits like quality and timeline certainty. Assign dedicated relationship managers who handle society concerns throughout the project. Create template agreements that are fair and transparent. Most importantly, deliver early projects flawlessly—they become your calling card for future opportunities.

Building for the long term vs. quick profits distinguishes Rustomjee from opportunistic developers who enter during booms and exit during busts. Every decision is evaluated not just for immediate returns but for long-term impact. This means passing on lucrative projects that might compromise reputation. It means investing in quality even when customers might not immediately notice. It means maintaining teams during downturns when competitors are firing.

This long-term orientation manifests in stakeholder relationships. Contractors are partners, not vendors to be squeezed. Employees are developed over years, not hired and fired based on project needs. Housing societies are relationships to be nurtured even after project completion. This ecosystem approach creates resilience that purely transactional approaches can't match.

The talent strategy reflects long-term thinking. Rustomjee invests heavily in training, sending employees to learn best practices globally. They promote internally, creating career paths that retain talent. They maintain teams during slow periods, ensuring capability is available when opportunities arise. This approach is expensive but creates organizational capability that becomes a competitive advantage.

Quality systems and process orientation might seem boring but are crucial for scaling while maintaining standards. Rustomjee has documented processes for everything—from site selection to customer handover. These aren't bureaucratic exercises but living documents updated based on learnings. New employees can quickly understand the "Rustomjee way." Mistakes in one project become learnings preventing repetition elsewhere.

Technology adoption supports process orientation. Digital project management ensures nothing falls through cracks. Quality checklists are digitized and mandatory. Customer feedback is systematically collected and analyzed. This systematic approach ensures that scale doesn't compromise quality—a common failure point for growing developers.

The importance of patient capital cannot be overstated in real estate. Rustomjee's capital structure—minimal debt, strong promoter commitment, and now public market access—provides the patience to wait for the right opportunities. They can hold land through downturns. They can invest in quality without immediate returns. They can pursue complex redevelopments that others avoid. This patient capital, combined with operational excellence, creates a powerful competitive advantage.

Risk management through diversification —not geographic but across project types, customer segments, and development stages—provides resilience. When luxury slows, mid-market continues. When new sales slow, construction of pre-sold projects generates cash. When one micro-market faces issues, others compensate. This portfolio approach smooths volatility inherent in real estate.

The playbook's final lesson is perhaps most important: culture and values matter. In an industry known for sharp practices, Rustomjee's commitment to ethics and transparency isn't just nice to have—it's a business advantage. It attracts quality talent who might otherwise avoid real estate. It enables partnerships that purely commercial relationships can't achieve. It builds a reputation that becomes the ultimate competitive advantage.

These lessons aren't just applicable to real estate—they're principles for building any business in a complex, relationship-driven market. Focus beats diversification. Trust beats advertising. Long-term thinking beats short-term optimization. Process beats genius. Patient capital beats leveraged returns. Together, these lessons form a playbook for building not just a successful business, but a sustainable institution.

XI. Analysis & Investment Case

The investment case for Keystone Realtors rests on a fundamental truth: Mumbai's housing shortage isn't getting solved anytime soon. With Current valuation: Market Cap ₹ 8,181 Crore, the company trades at interesting multiples relative to both its growth potential and the broader Mumbai real estate opportunity.

Let's start with the macro picture. A Reuters survey conducted in November 2024 among 12 property market experts projects that average home prices - broadly referring to housing in major cities - will rise by 6.5% in 2025 and 7.5% in 2026, largely supported by strong demand for high-end properties. India's economic expansion has remained robust, with the annual growth level estimated at 7%. The IMF currently projects further moderation to a 6.5% growth in 2025 and 2026.

Mumbai specifically presents an even more compelling picture. Mumbai accounted for the largest share of new residential launches at 26%, followed by NCR and Pune, each at 16%. Pune registered the highest year-on-year growth at 40%, while Hyderabad (-6%), Ahmedabad (-2%), and NCR (-3%) recorded declines in new supply. This concentration of activity in Mumbai validates Rustomjee's geographic focus.

The financial metrics tell a nuanced story. Financial metrics: Revenue: 2,004 Cr, Profit: 188 Cr. Company has a low return on equity of 6.81% over last 3 years. Stock is trading at 2.95 times its book value. These numbers might seem modest compared to tech companies, but in real estate context, they're solid. The low ROE reflects the capital intensity of real estate, while the price-to-book multiple suggests the market values Rustomjee's execution capability and land bank pipeline above its stated book value.

The Bull Case centers on several powerful drivers:

Mumbai's perpetual housing shortage is structural, not cyclical. Mumbai Metropolitan Region (MMR) led India's housing inventory with around 1.9 lakh units. It marked a 1% increase from the previous quarter. The MMR also witnessed the launch of approximately 44,120 new units, showcasing a 31% rise from Q1 2024. Despite this supply, demand continues to outstrip availability, particularly in established neighborhoods where Rustomjee operates.

The redevelopment opportunity is massive and accelerating. The majority of Mumbai's residential property sales involve redevelopment, especially in zones such as Dadar, Chembur, and Bandra. With thousands of buildings constructed in the 1960s-80s reaching end of life, the redevelopment pipeline could sustain decades of growth. Rustomjee's established position as redevelopment leader provides first-mover advantages in capturing this opportunity.

The execution track record differentiates Rustomjee from competitors. In an industry where delays are standard and quality compromises common, Rustomjee's consistent delivery builds compound value over time. Each successful project makes the next one easier to win, creating a virtuous cycle of growth.

Rising incomes and urbanization provide secular tailwinds. Rising incomes and growing consumer confidence. India is witnessing a surge in high-net-worth individuals, supported by a fast-growing economy and rising incomes. Additionally, non-resident Indians are increasingly viewing Indian real estate as an attractive investment opportunity. This wealth creation directly benefits Mumbai's premium and mid-market segments where Rustomjee operates.

Infrastructure investments are unlocking value. Mumbai's infrastructure transformation—metro expansion, coastal road, trans-harbor link—is improving connectivity and opening new micro-markets. Rustomjee's presence across Mumbai positions them to benefit regardless of which areas see maximum appreciation.

The Bear Case presents real risks that investors must consider:

Interest rate sensitivity remains a concern. While The anticipated interest rate reduction, combined with moderate price growth and sustained income increases, is expected to create a conducive environment for home purchases over the next 12-18 months, any unexpected rate increases could dampen demand. Real estate is inherently leveraged, both at developer and buyer levels, making the sector vulnerable to rate cycles.

Regulatory risks are ever-present in Indian real estate. While Rustomjee has navigated regulations successfully, sudden policy changes—FSI modifications, approval process changes, tax adjustments—can impact profitability. The complexity of Mumbai's regulatory environment adds layers of execution risk.

Concentration risk in Mumbai is both strength and weakness. While focus has driven Rustomjee's success, it also means exposure to Mumbai-specific shocks. A major economic disruption affecting Mumbai disproportionately—whether natural disaster, political instability, or economic downturn—would impact Rustomjee more than diversified competitors.

Competition is intensifying. As Mumbai's real estate market matures, national players and international capital are entering. While Rustomjee has defensive moats, margin pressure from competition is a real possibility, particularly in commodity segments of the market.

Execution risks scale with ambition. Managing multiple large redevelopment projects simultaneously strains organizational capacity. Any major project failure could damage the carefully built reputation, with cascading effects on future project wins.

Future growth drivers paint an optimistic picture:

The asset-light model provides scalability without proportional capital requirements. This means Rustomjee can grow faster than traditional developers while maintaining return metrics. The model becomes more valuable as land prices increase and capital becomes more expensive.

Expansion plans remain focused but ambitious. Rather than geographic diversification, Rustomjee is deepening presence in existing markets and selectively entering adjacent micro-markets. This focused expansion leverages existing capabilities while minimizing execution risk.

Demographic trends favor sustained demand. Mumbai's population has been steadily going up, and it's expected to keep rising. Because of this, more and more people will need places to live in the city. The working-age population growth, combined with urbanization trends, suggests decades of housing demand ahead.

The institutionalization post-IPO strengthens the investment case. Professional management, improved governance, and access to capital markets position Rustomjee for the next phase of growth. The company can now pursue larger projects and weather downturns better than private competitors.

Valuation Perspective:

At current levels, Rustomjee trades at reasonable multiples considering its growth trajectory. The market cap of ₹8,181 crores against a revenue of ₹2,004 crores gives a P/S ratio of about 4x—not expensive for a growing real estate company with strong competitive positions. The Enterprise Value/EBITDA multiples appear reasonable compared to listed peers.