GMR Power & Urban Infra: India's Infrastructure Conglomerate Rises from the Ashes

I. Introduction & Setting the Stage

Picture this: It's December 2021, and in a boardroom overlooking the sprawling Delhi skyline, executives at GMR Power & Urban Infra Limited are signing documents that would complete one of India's most ambitious corporate restructurings. The National Company Law Tribunal has just approved their scheme of amalgamation, effectively birthing a new entity from the ashes of what was once India's most debt-laden infrastructure conglomerate. This wasn't just paperwork—it was resurrection.

GMR Power and Urban Infra Limited (GPUIL), trading as GMRP&UI on the NSE, represents something unique in Indian corporate history: a subsidiary of GMR Enterprises Private Limited that holds expertise across energy, urban infrastructure, and transportation sectors. But calling it merely a "subsidiary" undersells the drama. This is a company that emerged from near-death, restructured its way out of a crushing debt crisis, and today commands a market capitalization of ₹8,213 crores.

The company's formal incorporation on May 17, 2019, might seem recent, but its roots stretch back over four decades. When the NCLT approved the Scheme of Amalgamation on December 22, 2021—retroactively effective from April 1, 2021—it wasn't creating something new so much as reorganizing something battle-tested. The restructuring separated operating assets from development assets, creating a cleaner, more focused entity that investors could actually understand and value.

Why does this story matter? Because it encapsulates the entire evolution of India's infrastructure financing model—from the exuberant leverage of the 2000s boom, through the near-collapse of the early 2010s, to today's more disciplined, asset-light approach. It's a case study in how family-controlled conglomerates adapt, survive, and sometimes thrive in emerging markets. And it's a window into India's infrastructure future, where smart meters, electric vehicle charging, and renewable energy are replacing the coal plants and highways of yesteryear.

The numbers tell part of the story: Revenue of ₹6,344 crores, profit of ₹1,552 crores, trading at 14.0 times book value. But numbers alone don't capture the human drama, the strategic pivots, or the lessons learned from building—and nearly losing—an infrastructure empire. This is that story.

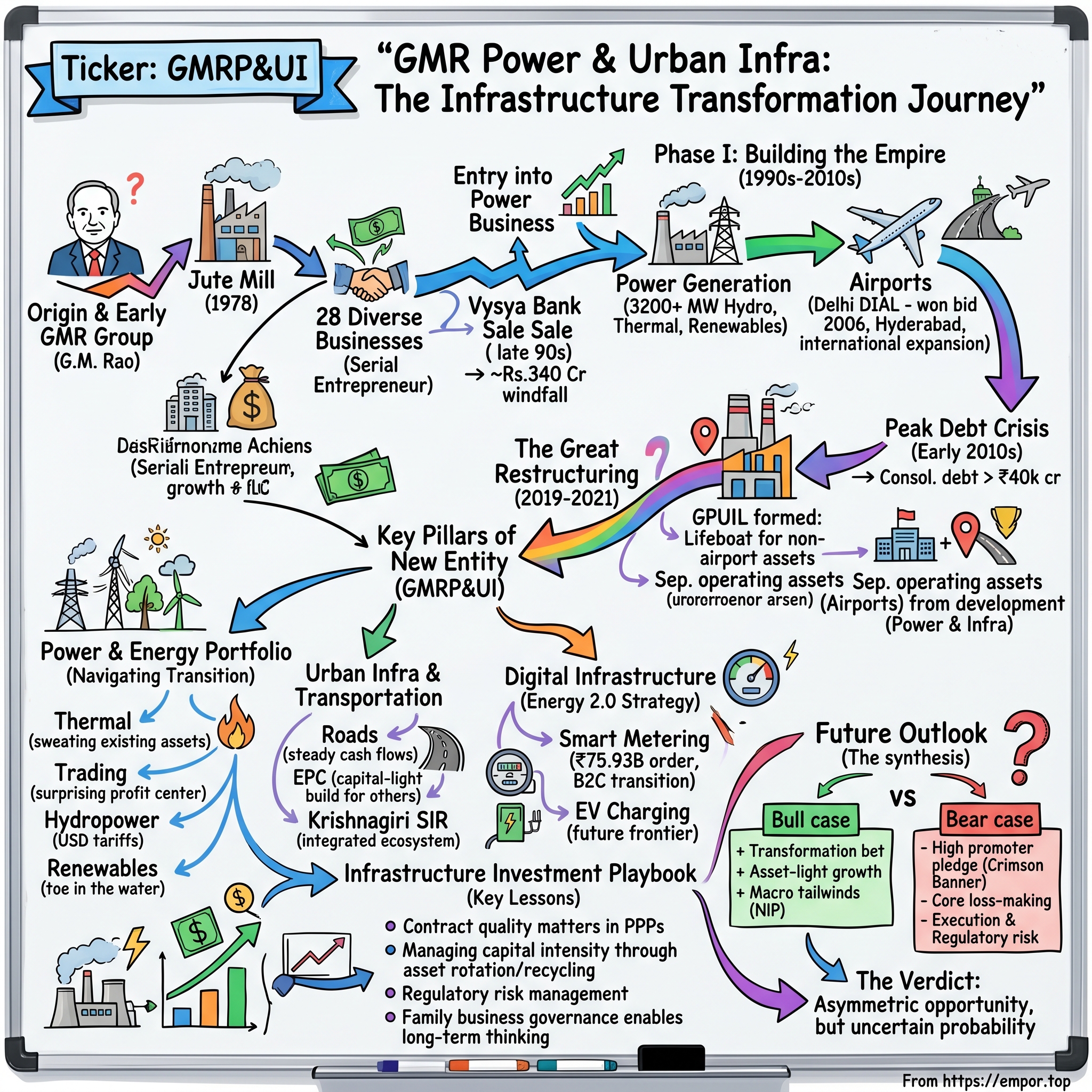

The G.M. Rao Origin Story & GMR Group Genesis

The G.M. Rao story began in 1978 when Grandhi Mallikarjuna Rao started a small jute mill in Rajam, Andhra Pradesh. From these humble beginnings, G.M. Rao went on to build GMR Group into one of India's leading infrastructure companies through vision, determination and a series of strategic business moves over four decades.

In the small town of Rajam, Srikakulam district, Andhra Pradesh, Grandhi Mallikarjuna Rao was born in 1950 into an upper-middle-class trading family. After failing his 10th class examination, his family asked him to leave his studies and join the family business—an apparent setback that would mark the beginning of the GMR Group saga.

This failure would become the founding myth of one of India's greatest infrastructure empires.

Against expectations, Rao didn't stay in the family business long. He went back, completed his education, and graduated from Andhra University and began his career as a shift engineer in a paper mill. Later, he worked as a junior engineer in the Public Works Department of the Andhra Pradesh Government. Picture him in those early days: a government engineer by day, dreaming of business opportunities by night. His mother saw something in him that even he might not have recognized. At his mother's insistence, Grandhi Mallikarjuna Rao entered commodities trading.

The year 1978 marked the inflection point. In the stifling environment of License Raj India, where getting any industrial license was nearly impossible, opportunity knocked in the most unlikely form. During the License Raj days, when it was next to impossible to get a licence, they happened to come across someone who was selling a jute mill licence in Chennai and the factory was closed. Quickly, they purchased the licence and machinery, and after a lot of hassles and struggles which required getting all the permissions from the state government and also the Jute Commissioner at Kolkata, they managed to shift the plant & set-up the factory by investing around Rs.40 lakhs from their own pocket.

This wasn't just a business acquisition—it was a masterclass in recognizing hidden value. After developing good relations with suppliers and customers in the business of commodities trading, he acquired a failing jute mill at a bargain, this venture proved to be lucrative and allowed GM Rao to use this leverage from local banks to acquire other assets. The jute mill became the springboard for everything that followed.

What emerged over the next decade was extraordinary: Starting with a single jute mill in 1978 he has ventured into 28 different businesses as a serial entrepreneur. Twenty-eight businesses! This wasn't diversification—it was exploration on an industrial scale. Sugar mills, ferro-alloys, breweries, cotton ear-buds (where he took on Johnson & Johnson), outsourcing, even a BPO that he sold to I-Gate within months for a handsome profit. Each venture was a learning laboratory, each exit a lesson in capital allocation.

But the masterstroke came with banking. Eventually, GM Rao divested his stake in a multitude of industries and started a bank named Vysya Bank in collaboration with ING. The Vysya Bank story deserves its own telling. Started in collaboration with ING, it became Rao's finishing school in high finance. When competition intensified and capital requirements soared, he eventually was forced to sell his 23.99% stake to the ING Group for about Rs.340 Cr during the late 90's.

That ₹340 crore windfall changed everything. The cash from the bank stake sale allowed his entry into the power business allowed Rao to build what would become India leading infrastructure asset developer. This wasn't just a pivot—it was a complete metamorphosis. The serial entrepreneur who had tried everything from jute to ear-buds was about to become an infrastructure titan.

The philosophical foundation of GMR Group was as important as its financial foundation. Rao believes that "Family must be run like Business and Business must be run like Family". He quotes "Strong family governance ensures strong corporate governance". This wasn't just a platitude—it was operational philosophy. In 2004, after attending a conference about the Murugappa group's family succession, Rao spent over 570 hours across four years crafting a family constitution that would govern how the business would be passed down, how conflicts would be resolved, and how new family members would be inducted.

The values weren't afterthoughts—they were architecture. It includes entrepreneurship, humility, delivering on promises, teamwork and relationships, social responsibility, respect for individuals and learning. In GMR's performance appraisals, these values carried actual weight alongside financial metrics.

By 2007, this mechanical engineer from Rajam who had failed his 10th standard exam was receiving the Economic Times Entrepreneur of the Year Award. But awards were just punctuation marks in a larger story. The group was founded in 1978 by Grandhi Mallikarjuna Rao and comprises several companies including GMR Infrastructure, GMR Energy, GMR Airports, and GMR Enterprises.

The philanthropy deserves special mention. In 2012, he donated ₹1,540 crores for charitable purposes. He mentioned in an interview that Warren Buffett is an inspiration for him to pledge his money in support of 'Giving back to society'. The GMR Varalakshmi Foundation, named after his mother who had pushed him into business, today serves the underserved sections of society in 22 locations.

What's remarkable about the GM Rao story isn't just the scale of success—it's the deliberate, almost methodical way he built not just a business but an institution designed to outlast him. The boy from Rajam had become a builder of nations' infrastructure, but he never forgot where he came from. As we'll see in the next chapter, when India opened up its infrastructure sector to private participation, GMR was perfectly positioned to seize the moment.

III. Building the Infrastructure Empire (1990s-2010s)

The monsoon of 2003 wasn't just transforming Mumbai's streets—it was about to transform India's infrastructure landscape. Employing the public-private partnership model, the Group has implemented several infrastructure projects in India. This simple statement belies the drama of what was about to unfold: a private company from Andhra Pradesh was about to take on the Indian government's monopoly on critical infrastructure.

The real action began in November 2000, when the erstwhile government and the Airports Authority of India (AAI) signed a memorandum of understanding on the greenfield airport project, establishing it as a public–private partnership. The State and AAI together would hold a 26% stake in the project, while the remaining 74% would be allotted to private companies. Through a bidding process the Shamshabad international airport with already land acquired of 5500 acres is in government possession and assigned bid to consortium consisting of Grandhi Mallikarjuna Rao (GMR Group) and Malaysia Airports Holdings Berhad was chosen as the holder of the 74% stake.

But it was 2003 that marked GMR's true entry into the big leagues. GMR Group entered the airports development space in 2003, through subsidiary GMR Airports Limited. The stakes couldn't have been higher. India's airports were a national embarrassment—dingy, overcrowded facilities that ranked among the worst in Asia. The government knew privatization was necessary but politically explosive.

Then came the moment that would define GMR's future. On 31 January 2006, the aviation minister Praful Patel announced that the empowered Group of Ministers have agreed to sell the management-rights of Delhi Airport to the DIAL consortium and the Mumbai Airport to the GVK Group. On 2 May 2006, the management of Delhi and Mumbai airports were handed over to the private consortia. GMR had won India's crown jewel—the capital's airport.

The Delhi International Airport Limited (DIAL) structure was elegant: Delhi International Airport Limited (DIAL) is a consortium of the GMR Group (54% (currently 64%)), Fraport (10%) and Malaysia Airports (10% (currently no share)), and the Airports Authority of India retains a 26% stake. This wasn't just a management contract—it was a 30-year concession, extendable by another 30 years.

Meanwhile, in Hyderabad, GMR was simultaneously building from scratch. Construction began by GMR on 16 March 2005 when Sonia Gandhi laid the foundation stone... Roughly three years after the foundation stone laying ceremony, the airport was inaugurated on 14 March 2008 amid protests. The Hyderabad project showcased GMR's ability to execute greenfield projects on schedule—a rarity in Indian infrastructure.

The transformation of Delhi airport was nothing short of miraculous. To ease the traffic congestion on the existing terminals and in preparation for the 2010 Commonwealth Games, a much larger Terminal 3 was constructed and inaugurated on 3 July 2010. The new terminal's construction took 37 months for completion and this terminal increased the airport's total passenger capacity by 34 million. Terminal 3 became a symbol of new India—gleaming, efficient, world-class.

But airports were just one piece of the infrastructure puzzle. GMR Group is a player in the Indian power sector with an installed capacity of 3200 MW. The group has 15 power generation projects across Hydro, Thermal, and Renewable energy of which 11 are operational and 4 are under various stages of development. The power portfolio was deliberately diversified—coal, gas, hydro, and increasingly, renewables.

The highways business demonstrated GMR's ability to execute at scale. In roads and highways, GMR is a leading developer with 6 operating assets adding to the total length of over 2,400 lane km. These weren't just roads—they were economic corridors connecting India's heartland to its ports and cities.

The railway projects showed ambition beyond traditional PPP models. In railways, GMR has a total order book of 4,000 Crores with projects from clients like Dedicated Freight Corridor Corporation of India (DFCCIL) and Rail Vikas Nigam Limited (RVNL). This was infrastructure building infrastructure—the meta-layer of development.

Urban infrastructure represented the future. In the Urban structure business, the GMR group is currently developing an 850-hectare large format 'Special Investment Regions' (SIR) at Krishna[giri]. These weren't just industrial parks but entire ecosystems designed for the 21st century economy.

The airports business evolved beyond mere operations. GMR Airports limited operates Delhi's Indira Gandhi International Airport, Hyderabad's Rajiv Gandhi International Airport, Goa's Manohar International Airport and Nagpur's Dr. Babasaheb Ambedkar International Airport. Each airport became a hub for economic activity, spawning aerotropolises—entire cities built around aviation.

The international expansion demonstrated global ambitions. In the International market, it operates Mactan Cebu International Airport in The Philippines and New Heraklion International Airport in Greece. GMR wasn't just an Indian infrastructure company anymore—it was a global player.

But this aggressive expansion came at a cost. By the early 2010s, GMR Infrastructure was drowning in debt. The company had borrowed heavily to fund its infrastructure projects, betting on India's growth story. When growth slowed after the 2008 financial crisis and projects got delayed due to regulatory issues, the debt became unsustainable.

The numbers were staggering. At its peak, GMR Infrastructure's consolidated debt exceeded ₹40,000 crores. Interest costs were eating up operational profits. Credit rating agencies were circling. Something had to give.

GVK and GMR, which won the Delhi airport bid around that time, had to navigate red tape, snail pace approvals, political vote banks not leading to handover of land and other hurdles... While Delhi, Mumbai, Bengaluru and Hyderabad airports are now recognised among the most developed airports in Asia, it was a hard struggle for the operators.

The infrastructure boom of the 2000s had turned into a bust by 2012. GMR's stock price collapsed. Lenders were nervous. The company that had built India's finest airports was facing an existential crisis. As we'll see in the next chapter, this crisis would force a radical restructuring that would give birth to GMR Power & Urban Infra—a phoenix rising from the ashes of overleveraging.

IV. The Great Restructuring & GMRP&UI Formation (2019-2021)

December 22, 2021, will be etched in GMR's corporate history as the moment the phoenix finally emerged from the ashes. The sanction was pronounced by the tribunal on this date, but this wasn't a sudden decision—it was the culmination of years of painstaking restructuring, delicate negotiations, and strategic sacrifices.

The crisis had been building for years. Gross debt for the company came down to Rs 19,856 crore in FY17 from Rs 37,480 crore last year whereas and net debt to EBITDA ratio for the year improved to 4.3 from 10.2 in FY16. Even after this massive deleveraging, the burden remained crushing. By 2019, GMR Infrastructure knew something radical had to be done.

GMR Infrastructure had unveiled the rejig plan on August 27 last year, to simplify the corporate holding structure and to attract sector-specific global investors. The plan was elegant in its simplicity but complex in execution: separate the crown jewel airports business from the debt-laden power and infrastructure assets.

The formal structure emerged on May 17, 2019. The Company was incorporated as a wholly owned subsidiary of GMR Infrastructure Limited. But GMR Power and Urban Infra Limited wasn't just another subsidiary—it was designed to be a lifeboat for the non-airport businesses.

The Scheme of Arrangement was aimed at demerger of Urban Infrastructure Business and EPC Business of GMR Infrastructure Limited into the Company. The Scheme was sanctioned by NCLT vide Order dated December 22, 2021 and is effective from the Appointed Date. The appointed date—April 1, 2021—meant that retroactively, GMRP&UI had been operating as a separate entity for most of the year.

The restructuring wasn't happening in isolation. GMR had been aggressively courting strategic investors for its airport business. France's Groupe ADP agreed to acquire 49 per cent stake in GMR's airport business for Rs 10,780 crore, a deal that will help the domestic entity reduce its debt burden. This wasn't just a financial transaction—it was validation that GMR's airports were world-class assets worth fighting for.

Simultaneously, another deal materialized. JSW Energy, which has signed a share-purchase agreement with the subsidiary GMR Energy to acquire entire stake in 1,050 MW thermal power plant, GMR Kamalanga. The deal is valued at Rs 5,321 crore. Asset sales became the oxygen keeping the restructuring alive.

The demerger structure was carefully calibrated to protect existing shareholders. In the demerger, existing shareholders of GMR Infrastructure will receive 1 equity share of Rs. 5 /-(Face value) each of GMR Power and Urban Infra Limited for holding 10 equity shares of Rs.1/- (Face value) share of each GMR Infrastructure Limited. No one would be left behind in the restructuring.

What exactly was being transferred to GMRP&UI? The portfolio was substantial. In aggregate, GMR Power and Urban Infra Limited (the Companys) operating power plants had a gross capacity of 1,679.35 MW as of September 30, 2021 excluding two gas-based power plants having gross capacity of 1,155.18 MW which are both currently non-operational due to non-availability of natural gas. Further, gross capacity of 1,775 MW of hydropower is under development, of which a plant with 900 MW capacity is in advanced stages of development, with a major part of its power output being tied up under a long term PPA and with USD denominated tariff.

The transportation assets were equally significant. As of September 30, 2021, the Transportation Business held a roads portfolio consisting of four operational roads located in Andhra Pradesh, Telangana, Haryana, Punjab and Tamil Nadu, with a total length of 349.48 km.

The urban infrastructure crown jewel was the Krishnagiri SIR. GMR Krishnagiri SIR currently holds 1,032 acres of land parcel and are developing the Special Investment Regions (SIR) in phased manner in Krishnagiri District of the State of Tamil Nadu owned by GMR Krishnagiri SIR Limited (KrishnagiriSIR) as a joint venture with Tamil Nadu Industrial Development Corporation.

The EPC business added another dimension. EPC business means the business undertaken by GMR Infrastructure Limited (GIL) pertaining to the E[ngineering, Procurement and Construction]. This wasn't just about owning assets—it was about building them for others, generating cash flow without capital intensity.

The market's initial reaction to the listing was brutal. Shares hit 5% lower circuit soon after listing at Rs 46.50 per equity share on the BSE and Rs 48 a share on the NSE. The newly listed entity would trade in the T-to-T (Trade-to-Trade) category for the first 10 days, meaning no intraday trading was allowed.

But the strategic rationale was sound. The vertical split demerger will go a long way in facilitating deeper understanding of the airport business independently as compared to other business verticals within the group. Investors could now choose—pure-play airports or diversified infrastructure.

The debt reduction impact was immediate and dramatic. According to the December quarter numbers, the group has a net debt of Rs 25,660 crore. It is expected to come down to at least Rs 12,000 crore, if the group uses most part of the transaction proceeds for deleveraging the balance sheet.

"GMR Infra (GMRI) is set to benefit from dual triggers of deleveraging and the demerger of its airport business, coupled with steady growth in passenger footfall (PAX - factoring preCovid levels by FY24) and real estate monetisation. We maintain our hold rating on this counter, " says brokerage JM Financial in its report.

The restructuring represented more than financial engineering. It was a philosophical shift—from empire building through leverage to value creation through focus. The promoters, led by G.M. Rao, maintained control but now held Promoters of the Company are Mr. Grandhi Mallikarjuna Rao and GMR Enterprises Private Limited, with promoter holding at 50.6%.

What emerged from this chrysalis was a cleaner, more focused entity. GMRP&UI would handle the complex, capital-intensive businesses of power generation, urban infrastructure, and EPC. Meanwhile, GMR Airports Infrastructure would soar as a pure-play aviation story. The great restructuring wasn't just about survival—it was about positioning for the next phase of growth. As we'll see in the next chapter, the power and energy portfolio would become the backbone of this new entity's ambitions.

V. The Power & Energy Portfolio Deep Dive

The morning shift at GMR's Warora power plant begins at 6 AM, when the Maharashtra sun hasn't yet begun its assault on the coal yards. Inside the control room, engineers monitor screens displaying real-time data from turbines spinning at 3,000 RPM, converting Maharashtra's coal into the electricity that powers Mumbai's dreams. This is the heart of GMRP&UI's energy empire—not glamorous like airports, but fundamental to India's economy.

GMR Group has a current installed capacity of 4436 MW which includes coal based and gas based thermal power plants across different geographies of India. But this headline number tells only part of the story. The real narrative is about transformation—from coal-heavy legacy assets to a more balanced, sustainable portfolio.

The crown jewel of the thermal portfolio had been Kamalanga in Odisha. Kamalanga power station is an operating power station of at least 1050-megawatts (MW) in Kamalanga, Odapada, Dhenkanal, Odisha, India with multiple units. This wasn't just any power plant—it represented GMR's ability to execute large-scale thermal projects. The three 350 MW units had been commissioned between 2013 and 2014, during the height of India's power deficit crisis.

But Kamalanga also embodied the challenges of thermal power in modern India. In August 2020, the Indian power utility JSW Energy announced that it had called off its deal to acquire the 1,050 MW Kamalanga power station project in Odisha after entering into exclusive talks with GMR Energy to buy it in October 201[9]. The deal that eventually went through for ₹5,321 crores was both a relief and a strategic pivot—exit the problematic assets, focus on the profitable ones.

Warora in Maharashtra represented the operational excellence side of the portfolio. GMR Warora Energy power station is an operating power station of at least 600-megawatts (MW) in Naideo, Warora, Chandrapur, Maharashtra, India... The two 300 MW units were commissioned in 2013. Located in the coal belt of Chandrapur, Warora had geographical advantages that Kamalanga lacked—proximity to coal mines and established transmission infrastructure.

The fuel security strategy was sophisticated. GWEL has tied up 58% of its overall capacity in long term PPAs and 25% of its capacity through medium term PPA. Low fuel availability risk stems owing to fuel supply agreements (FSA) for supply of coal up to 2.6 million tonnes per annum (MTPA) which covers for majority requirement. This wasn't just about having coal—it was about having guaranteed coal at predictable prices.

But thermal power was increasingly yesterday's story. The real action was in the energy transition. With an operating capacity of over 2500 MW , it has a balanced fuel mix of coal, gas, LSHS as well as renewable sources of wind and solar energy. Apart from this, plants of over 2300 MW generation capacity are under advanced stages of completion and nearly 3700 MW of projects are under various stages of development in India and Nepal.

The renewable push, though modest, signaled intent. GMR Renewable Energy Limited, Kutch India is a wind-based power plant with a gross capacity of 2.10 MW which was commissioned in July 2011. Small, yes, but it was a toe in the water of India's renewable revolution.

The stranded gas assets told another story—of bets that didn't pay off. Operating power plants had a gross capacity of 1,679.35 MW as of September 30, 2021 excluding two gas-based power plants having gross capacity of 1,155.18 MW which are both currently non-operational due to non-availability of natural gas. Over 1,100 MW of gas-based capacity sitting idle—a monument to India's failed gas economy dreams.

The hydropower pipeline offered redemption. Further, gross capacity of 1,775 MW of hydropower is under development, of which a plant with 900 MW capacity is in advanced stages of development, with a major part of its power output being tied up under a long term PPA and with USD denominated tariff. USD-denominated tariffs in a depreciating rupee environment—this was financial engineering at its finest.

Power trading emerged as the surprise profit center. GMR Energy Trading Limited (GMRETL) is a category-1 trading licensee which was incorporated on 29th January'20. In India's complex power market, with different states having surpluses and deficits at different times, trading became a high-margin, asset-light business.

The merchant power strategy was equally sophisticated. A balanced mix of power sales contracts in the short term, medium term and long term have given GMR Energy a unique strength in terms of portfolio diversity. When spot prices spiked during summer peaks or unexpected outages, GMR's merchant capacity could capture windfall profits.

Coal mining and exploration represented backward integration at scale. An operating coal property in Indonesia provides essential requirement of fuel security. It has been allotted two coal blocks through the transparent e-auction and bidding process in India, Talabira I in Sambalpur district in Odisha and Ganeshpur in Jharkhand with estimated reserves. Controlling the fuel source meant controlling destiny in a coal-dependent economy.

The transmission assets added another layer. Additionally, GMR Energy has developed and is operating 2 large 400 kV transmission lines of 366 kms. These weren't just wires—they were toll roads for electrons, generating steady returns with minimal operational risk.

But the energy portfolio's real value wasn't in megawatts—it was in optionality. Coal plants for baseload, gas plants ready if fuel became available, hydro projects for peaking power, renewables for the future, trading for opportunistic profits. This wasn't a collection of power plants—it was a platform for navigating India's complex energy transition.

As coal plants across India faced increasing environmental scrutiny and renewable energy costs plummeted, GMRP&UI's energy strategy evolved. The focus shifted from building new thermal capacity to sweating existing assets, from megawatts to margins, from generation to trading. The future wouldn't be about who had the most power plants—it would be about who could navigate the transition most profitably. As we'll see in the next chapter, this same philosophy would guide the urban infrastructure and transportation businesses.

VI. Urban Infrastructure & Transportation Assets

The bulldozers arrived at Krishnagiri at dawn, not to destroy but to build. Developing an 850-hectare large format 'Special Investment Regions' (SIR) at Krishnagiri, near Hosur in Tamil Nadu. The SIR is designed and developed by GMR as self-contained eco-systems for economic activity. This wasn't just land development—it was nation-building at the micro level.

Krishnagiri represented GMR's most ambitious urban infrastructure play. GMR Krishnagiri SIR currently holds 1,032 acres of land parcel and are developing the Special Investment Regions (SIR) in phased manner in Krishnagiri District of the State of Tamil Nadu owned by GMR Krishnagiri SIR Limited (KrishnagiriSIR) as a joint venture with Tamil Nadu Industrial Development Corporation. The location was strategic—close to Bangalore's tech corridor but in Tamil Nadu's manufacturing belt.

The SIR concept was borrowed from China's special economic zones but adapted for Indian realities. Unlike traditional industrial parks that simply provided land and basic infrastructure, SIRs were designed as integrated ecosystems. Residential complexes for workers, commercial zones for services, logistics hubs for supply chains—entire cities built from scratch.

The transportation portfolio told a different story—one of steady, predictable cash flows. As of September 30, 2021, the Transportation Business held a roads portfolio consisting of four operational roads located in Andhra Pradesh, Telangana, Haryana, Punjab and Tamil Nadu, with a total length of 349.48 km. These weren't trophy assets but workhorses—toll roads and annuity projects generating steady returns.

The highway model had evolved significantly from GMR's early days. In roads and highways, GMR is a leading developer with 6 operating assets adding to the total length of over 2,400 lane km. The shift from build-operate-transfer (BOT) toll to hybrid annuity model (HAM) reduced traffic risk while ensuring predictable returns.

Each road had its own story. The Tambaram-Tindivanam highway in Tamil Nadu connected Chennai to the industrial corridors of the south. The Ambala-Chandigarh expressway served the prosperous Punjab-Haryana belt. These weren't just strips of asphalt—they were economic arteries pumping commerce through India's heartland.

The EPC business added another dimension. EPC Business established in 2007, ISO & OHSAS certified with capability to provide turnkey EPC solutions across multiple business sectors. The division has delivered several critical projects. This wasn't about owning assets but building them for others—a capital-light way to leverage GMR's execution expertise.

Railway projects represented the frontier. GMR has a total order book of 4,000 Crores with projects from clients like Dedicated Freight Corridor Corporation of India (DFCCIL) and Rail Vikas Nigam. The Jhansi-Bhimsen project and the MMTS work in Hyderabad weren't glamorous, but they were essential—the unglamorous work of connecting India.

RVNLs Multi Modal Transport System (MMTS) project involves construction of civil works, track linking, yard arrangements, railway electrification, signaling and telecommunication works in Secunderabad and Hyderabad divisions of South Central Railway, Andhra Pradesh. RVNLs Jhansi - Bhimsen Project, Uttar Pradesh involves various works on the Jhansi to Bhimsen stretch including construction of roadbed, major and minor bridges, track inking, S&T etc. These projects showcased GMR's ability to handle complex, multi-disciplinary infrastructure work.

The urban infrastructure strategy was deliberately anti-glamorous. While competitors chased smart city projects and flashy real estate developments, GMR focused on industrial infrastructure. The Krishnagiri SIR wasn't trying to be Singapore—it was trying to be a profitable, functional space for manufacturing and logistics.

The transportation assets followed a similar philosophy. No iconic sea links or mountain tunnels—just profitable stretches of highway in high-traffic corridors. The focus was on traffic density, not engineering marvels. Every kilometer was chosen for its revenue potential, not its photo opportunities.

The integration between different businesses created synergies. The EPC division built projects for the transportation business. The transportation assets connected to the SIRs. The power plants supplied electricity to the industrial zones. This wasn't coincidence—it was design.

But challenges remained significant. Land acquisition for linear projects like highways and railways was increasingly contentious. Environmental clearances were getting tougher. The HAM model, while reducing traffic risk, also capped upside potential. The Krishnagiri SIR faced competition from other industrial zones and the general slowdown in manufacturing investment.

The financing structure for these assets was complex. BOT projects required significant upfront investment with returns spread over 15-30 years. HAM projects needed less equity but generated lower returns. The SIR required patient capital—land appreciation and development took time.

Yet the portfolio positioning was strategic. As India pushed toward a $5 trillion economy, infrastructure would be critical. The Production Linked Incentive (PLI) schemes would drive manufacturing investment, benefiting SIRs. The PM Gati Shakti program would create demand for EPC services. The focus on logistics efficiency would increase highway traffic.

The real value of the urban infrastructure and transportation portfolio wasn't in the assets themselves but in the platform they created. GMR wasn't just building roads and industrial parks—it was building the physical layer for India's economic transformation. Less glamorous than airports, less exciting than power plants, but equally essential. As we'll explore next, this platform would become the foundation for GMR's pivot toward smart infrastructure and new growth vectors.

VII. Smart Metering & New Growth Vectors

July 24, 2023 marked GMR Power & Urban Infra's strategic shift from heavy industry to digital infrastructure. GMR Smart Electricity Distribution Private Limited, a subsidiary of GMR Power and Urban Infra Limited, has been awarded an order worth Rs 75.93 billion to implement a large-scale smart metering project under the revamped distribution sector scheme (RDSS) program. This wasn't just another contract—it was a transformation.

The numbers were staggering. The order, received under the design, build, finance, own, operate, and transfer model, entails 7.57 million prepaid smart meters across two discoms – Dakshinanchal Vidyut Vitran Nigam Limited (DVVNL) and Purvanchal Vidyut Vitaran Nigam Limited (PuVVNL). Seven and a half million meters—each one a data point, a revenue stream, a connection to the future of energy management.

Emkay maintains a Buy rating with a target price of Rs 180, citing successful debt restructuring and expansion in smart metering and EV infrastructure. The market was beginning to understand what GMR was becoming—not just an infrastructure company, but a technology-enabled services provider.

The smart metering opportunity represented everything modern infrastructure should be: asset-light, technology-heavy, recurring revenue. This comprehensive approach leverages state-of-the-art technology and software solutions, offering end-to-end automated system management. Crucially, the project aligns with the objectives of the Revamped Distribution Sector Scheme (RDSS) and is expected to contribute significantly to reducing Aggregate Technical and Commercial (AT&C) losses in the designated areas.

The project geography was strategic. According to a press release by the company, the project will span 22 districts covering prominent areas such as Varanasi, Prayag Raj, Agra, Mathura and Aligarh among others. These weren't backwaters—they were the heartland of Uttar Pradesh, India's most populous state, where electricity theft and distribution losses had plagued the system for decades.

"With this mandate, GMR group make its entry into the B2C business in the power sector at a substantial scale and will create value for GPUIL shareholders," said Srinivas Bommidala, Chairman - Energy, GMR Group. "We consider this as a good beginning for our Energy 2.0 strategy of new growth business areas in the Power Sector and have plans in the offing for further initiatives in this space," Bommidala added.

Energy 2.0—the phrase captured the ambition. This wasn't about megawatts anymore; it was about data, analytics, and customer relationships. Each smart meter wasn't just measuring electricity; it was generating information about consumption patterns, payment behaviors, and grid performance.

The business model was revolutionary for GMR. The project timeline estimates an implementation period of 27 months from the contract's execution date, followed by an operating period of 93 months. With a total contract value of approximately ₹24,69.71 crore (inclusive of GST) for the Agra and Aligarh Zones, this initiative promises significant economic impact and technological advancement. Nearly eight years of recurring revenue from a single project—this was the holy grail of infrastructure investing.

The global context made the opportunity even more compelling. As of late 2023, the smart electricity meter market achieved 43% penetration of the overall global electricity meter market, according to the market tracker. Electricity grid modernization initiatives started in the late 2000s in Italy and the US and accelerated to national rollouts throughout the EU and APAC regions after 2010. Regulatory policies—supported by financial incentives from regional or national governments—have contributed to this growth, as these policies have encouraged utilities to replace mechanical electricity meters with smart meters to modernize their grid infrastructure.

India was late to the party but moving fast. South Asia, Latin America, and Africa represent a high-growth potential for smart meters, as some regional governments have become convinced of the need to update their aging grid infrastructure and are more actively engaging with smart grid industry stakeholders to develop regulatory policies to drive the adoption of smart meters.

The EV infrastructure opportunity was the next frontier. GMR Power & Urban Infra Ltd is on a strategic transformation path, focusing on asset-light operations and smart energy. While specific EV projects weren't yet announced, the strategic direction was clear—leverage the same capabilities that made smart metering successful.

The synergies were obvious. Smart meters created relationships with millions of electricity consumers. EV charging required electricity infrastructure and customer relationships. GMR's highways and urban infrastructure provided locations for charging stations. The airports under the broader GMR Group offered captive demand for electric vehicle fleets.

But execution challenges loomed. Installing millions of meters across rural and semi-urban Uttar Pradesh wasn't just a technical challenge—it was a logistical nightmare. Consumer resistance to prepaid meters, political pressure against disconnections, and the sheer scale of operations would test GMR's execution capabilities.

The technology platform was equally critical. Smart meters generated massive amounts of data—consumption patterns, voltage fluctuations, outage information. Converting this data into actionable insights required sophisticated analytics capabilities that GMR was still building.

The competitive landscape was intensifying. Adani was making similar moves. Tata Power had its own smart metering ambitions. Global players like Schneider Electric and Siemens were partnering with Indian companies. The window for establishing market leadership was narrow.

Yet the transformation was undeniable. From a company that built coal plants and highways, GMR was becoming a digital infrastructure player. The smart metering contracts weren't just projects—they were proof points of a new business model.

The financial implications were profound. Asset-light models meant lower capital requirements and higher returns on equity. Recurring revenue streams meant predictable cash flows. Technology-enabled services commanded higher multiples than traditional infrastructure assets.

The company is divesting stakes to reduce debt significantly, enhancing its balance sheet and operational focus. The proceeds from asset sales could fund the working capital needs of smart metering projects without adding debt. This was financial engineering meeting operational transformation.

As India pushed toward its net-zero ambitions and power distribution reforms accelerated, GMR's pivot to smart infrastructure looked prescient. The company that had nearly collapsed under infrastructure debt was reinventing itself as a technology-enabled services provider. The next chapter would test whether this transformation could deliver the promised returns.

VIII. Financial Performance & Market Position

The numbers tell a story of volatility masking transformation. Market Cap ₹ 8,213 Crore (up 17.8% in 1 year). Revenue: 6,344 Cr. Profit: 1,552 Cr. Stock is trading at 14.0 times its book value. On the surface, respectable metrics. But dig deeper, and the complexity emerges.

The quarterly performance painted a picture of extreme volatility. Net profit of GMR Power & Urban Infra declined 73.04% to Rs 43.72 crore in the quarter ended March 2025 as against Rs 162.18 crore during the previous quarter ended March 2024. Yet Sales rose 41.34% to Rs 6343.97 crore in the year ended March 2025 as against Rs 4488.57 crore during the previous year ended March 2024. Revenue growth alongside profit collapse—the classic infrastructure conundrum.

The most recent quarter was particularly brutal. GMR Power & Urban Infra Ltd's net profit fell -334.57% since last year same period to ₹-106.45Cr in the Q3 2024-2025. A loss of over ₹100 crores in a single quarter would typically signal distress. But in infrastructure, one-time items and project timing can distort quarterly numbers beyond recognition.

The market's reaction was surprisingly sanguine. Gmrp&Ui target price ₹182, a slight upside of 55.05% compared to current price of ₹124.24. According to 2 analysts rating. Emkay maintains a Buy rating with a target price of Rs 180, citing successful debt restructuring and expansion in smart metering and EV infrastructure. Analysts were looking through the noise to the transformation story.

The balance sheet revealed both progress and challenges. Company has reduced debt. But context mattered: Company has low interest coverage ratio. Contingent liabilities of Rs.5,484 Cr. The debt reduction was real, but the balance sheet remained stressed.

The promoter situation added another layer of complexity. Promoter Holding: 50.6% seemed healthy, but Promoters have pledged or encumbered 75.4% of their holding. Three-quarters of the promoter stake pledged—a sword of Damocles hanging over the stock.

Recent developments suggested accelerating transformation. GMR Power and Urban Infra announced plans to divest stakes in non-operating and stressed assets for ₹653 crore, aiming to deleverage its balance sheet by ₹4,400 crore. The stock surged 15% following the announcement. Asset sales of ₹4,400 crores would fundamentally transform the balance sheet.

The earnings quality remained concerning. Earnings include an other income of Rs.2,228 Cr. Other income of over ₹2,000 crores against total profit of ₹1,552 crores meant the core operations were actually loss-making. This wasn't sustainable.

Working capital deterioration added pressure. Working capital days have increased from -96.7 days to 81.1 days. From negative working capital (getting paid before paying suppliers) to 81 days of capital locked up—a dramatic shift in cash flow dynamics.

Yet the market's faith stemmed from the transformation narrative. GMR Power & Urban Infra Ltd is on a strategic transformation path, focusing on asset-light operations and smart energy... The company is divesting stakes to reduce debt significantly, enhancing its balance sheet and operational focus. The market was betting on the future, not the present.

The peer comparison was revealing. Trading at 14 times book value when infrastructure peers traded at 2-3 times suggested either extreme overvaluation or recognition of hidden value. The smart metering contracts, not yet fully reflected in earnings, might justify the premium.

Institutional interest was growing. Investment in GMR Power & Urban Infra Ltd Shares on INDmoney has grown by 20.68% over the past 30 days, indicating increased transactional activity. Search interest for GMR Power & Urban Infra Ltd Stock has increased by 57% in the last 30 days, reflecting an upward trend in search activity. Retail and institutional interest converging—often a precursor to re-rating.

The valuation disconnect was stark. A P/E ratio effectively negative due to recent losses, yet analysts maintaining buy ratings with 50%+ upside targets. This wasn't irrational—it reflected the belief that current earnings were meaningless for valuing a company in transformation.

The revenue trajectory told the real story. From ₹4,488 crores to ₹6,344 crores in a year—41% growth during a period of supposed stress. This wasn't a dying company; it was a growing one with profitability challenges.

The segment performance revealed the dichotomy. Power generation faced headwinds from coal costs and regulatory changes. Roads generated steady but unspectacular returns. But smart metering and EPC were accelerating, though not yet material to overall profits.

Cash flow, the ultimate reality check, remained challenging. Interest payments, though reduced, still consumed significant cash. Capital expenditure for smart metering projects created near-term pressure despite long-term promise. Asset sale proceeds would be critical for bridging the gap.

The market capitalization of ₹8,213 crores against revenue of ₹6,344 crores suggested modest expectations. At 1.3 times sales, GMRP&UI traded at a discount to global infrastructure comparables. If the transformation succeeded, rerating potential was substantial.

The quarterly volatility would likely continue. Infrastructure projects don't generate smooth earnings. Power plant outages, highway traffic variations, and project commissioning schedules create lumpy revenues and profits. Investors needed strong stomachs.

Yet beneath the volatility, a transformation was underway. From asset-heavy to asset-light, from construction to services, from infrastructure owner to technology provider. The financial performance was messy, but the strategic direction was clear. Whether the transformation would succeed before the balance sheet constraints became binding—that remained the ₹8,213 crore question.

IX. Playbook: Infrastructure Investment Lessons

The conference room at GMR's headquarters has witnessed four decades of infrastructure battles. The walls, if they could speak, would tell stories of boom and bust, of leveraged bets that nearly destroyed the company, and of resurrection through discipline and strategic pivots. These lessons, earned through billions in write-offs and restructurings, constitute a playbook for infrastructure investing in emerging markets.

Lesson 1: The Public-Private Partnership model in India—what works, what doesn't

The PPP model was supposed to be India's infrastructure panacea. Private efficiency meeting public purpose. The reality proved messier. GMR's experience across airports, highways, and power plants revealed a fundamental truth: PPP success depends entirely on contract design and regulatory stability.

Airports worked because the concession agreements were clear, revenue models diversified (aeronautical plus commercial), and regulatory frameworks relatively stable. Employing the public-private partnership model, the Group has implemented several infrastructure projects in India. But success wasn't automatic—it required choosing the right projects with the right terms.

Power plants struggled because fuel supply agreements fell apart, power purchase agreements got renegotiated, and environmental regulations changed mid-stream. The 1,100 MW of stranded gas assets stood as monuments to PPP agreements that didn't account for ground realities.

Highways fell somewhere in between. Toll roads worked in high-traffic corridors but failed in optimistic projections. The shift to hybrid annuity models—reducing traffic risk while ensuring returns—showed PPP evolution through painful experience.

The lesson: In PPPs, contract quality matters more than project quality. A mediocre project with an ironclad agreement beats a great project with regulatory uncertainty.

Lesson 2: Managing capital intensity and debt in infrastructure projects

Infrastructure is inherently capital-intensive, but GMR learned that capital intensity without capital discipline is fatal. The pre-2010 strategy of "build it and they will come" nearly killed the company. Gross debt for the company came down to Rs 19,856 crore in FY17 from Rs 37,480 crore last year—this deleveraging wasn't voluntary; it was survival.

The new playbook emphasized capital recycling. Build an asset, stabilize operations, sell to yield-hungry investors, redeploy capital. The Kamalanga sale to JSW for ₹5,321 crores exemplified this—crystallize value, reduce debt, move on.

Project finance structures became critical. Non-recourse debt at the project level protected the parent. When projects failed, losses were contained. When they succeeded, dividends flowed up. This compartmentalization saved GMR during the crisis years.

The smart metering pivot represented the ultimate capital efficiency play. DBFOOT models meant GMR provided expertise and management, while project finance handled capital. Returns on equity could exceed 20% with minimal capital at risk.

Lesson 3: The importance of asset rotation and recycling capital

GMR discovered that infrastructure developers and infrastructure owners are different businesses requiring different skills and capital structures. Developers need entrepreneurial energy and risk capital. Owners need operational excellence and cheap, patient capital.

The airport stake sale to Groupe ADP for ₹10,780 crores validated this model. GMR retained management control while bringing in patient capital. This wasn't retreat—it was optimization.

Asset rotation also provided market feedback. If nobody wanted to buy your operational assets, maybe they weren't as good as you thought. The discipline of regular asset sales forced operational excellence—buyers conduct ruthless due diligence.

Timing mattered enormously. Selling during infrastructure boom cycles maximized value. Holding through downturns destroyed returns. GMR learned to be countercyclical in building but procyclical in selling.

Lesson 4: Regulatory risk management in power and infrastructure

Regulatory risk nearly killed GMR, but surviving it created institutional knowledge worth billions. Every infrastructure asset in India faces regulatory risk—tariff changes, environmental norms, land acquisition laws. Managing this risk separated winners from casualties.

Diversification across states and sectors provided hedge. When Andhra Pradesh's power policies turned adverse, Maharashtra projects cushioned the blow. When environmental regulations hit coal plants, highways provided stability.

Relationship capital mattered more than financial capital. Understanding regulatory processes, maintaining transparent communication with regulators, and building trust over decades—these intangibles determined project success more than engineering excellence.

The company learned to price regulatory risk explicitly. Projects in states with poor regulatory track records required higher returns. Sometimes, the best deal was the one you didn't do.

Lesson 5: Building conglomerate value vs. pure-play focused strategy

The demerger creating GMRP&UI represented a philosophical evolution. For decades, GMR believed in conglomerate synergies—airports feeding highways feeding power plants. The market disagreed, applying a conglomerate discount that destroyed shareholder value.

Pure-play entities commanded premium valuations. The vertical split demerger will go a long way in facilitating deeper understanding of the airport business independently as compared to other business verticals within the group. Investors wanted focused stories, not complex conglomerates.

Yet some synergies were real. Corporate overhead spread across businesses reduced costs. Banking relationships built on airport success enabled highway financing. Reputation in one sector opened doors in another.

The solution was structural—maintain operational synergies while creating financial separation. Shared services for efficiency, separate listings for value realization. This hybrid model preserved benefits while eliminating discounts.

Lesson 6: The family business governance model and its impact on decision-making

Rao believes that "Family must be run like Business and Business must be run like Family". He quotes "Strong family governance ensures strong corporate governance". This wasn't just philosophy—it was operational reality.

Family control enabled long-term thinking. While listed peers chased quarterly earnings, GMR could endure years of losses to build airports. Patient capital from family sources bridged timing gaps that would break purely financial investors.

But family control also created challenges. Promoters have pledged or encumbered 75.4% of their holding. Pledged shares created overhang, limiting strategic flexibility. The need to service family debt sometimes conflicted with corporate capital allocation.

The institutionalization of family governance through written constitutions and professional boards tried to capture benefits while mitigating risks. Next-generation family members had to prove competence before receiving responsibilities. Merit mattered, even within family.

The Meta-Lessons

Beyond specific tactics, GMR's journey revealed meta-lessons about infrastructure investing:

Infrastructure is a marathon, not a sprint. Projects take decades to mature. Companies that survive long enough usually succeed. Patience isn't just a virtue—it's a requirement.

Execution beats strategy. Everyone knew India needed infrastructure. The winners were those who could actually build and operate assets. Operational excellence, boring as it sounds, created more value than financial engineering.

Cycles are everything. Infrastructure is violently cyclical. Companies that extrapolate boom times fail in busts. Those that prepare for downturns during upturns survive and thrive.

Relationships are assets. In emerging markets, relationships with regulators, financiers, and communities determine success more than spreadsheet models. These relationships, built over decades, can't be bought—only earned.

Transformation is possible but painful. GMR transformed from a jute trader to infrastructure giant to technology-enabled services provider. Each transformation nearly killed the company but ultimately created value. The ability to reimagine identity while maintaining core capabilities separated survivors from casualties.

These lessons, written in the scar tissue of GMR's corporate body, offer a roadmap for infrastructure investing in emerging markets. They're not theoretical—they're empirical, validated through billions deployed and lost and earned again. For investors considering infrastructure in India or similar markets, ignoring these lessons means repeating GMR's mistakes without capturing its ultimate successes.

X. Bear vs. Bull Case Analysis

The investment thesis for GMRP&UI splits the market into believers and skeptics, each armed with compelling arguments. The truth, as always in infrastructure investing, lies somewhere in the uncomfortable middle.

Bull Case: The Transformation Story

The bulls see GMRP&UI as a transformation story trading at distressed valuations. India's infrastructure spending is set to explode—₹143 lakh crores over the next five years according to the National Infrastructure Pipeline. GMRP&UI, with its diversified portfolio and execution track record, stands to capture a meaningful share.

The smart metering opportunity alone could transform the company. With contracts worth ₹7,593 crores already secured and India needing 250 million smart meters, GMRP&UI has first-mover advantage in a market that could exceed ₹100,000 crores. At 20% ROE, these asset-light projects could generate returns that dwarf the legacy infrastructure business.

The debt reduction trajectory validates the bull case. From crushing leverage that nearly killed the company to manageable debt levels with improving coverage ratios, the balance sheet transformation is real. The ₹4,400 crore asset sale pipeline would further strengthen finances, potentially eliminating net debt entirely.

GMR Power & Urban Infra Ltd is on a strategic transformation path, focusing on asset-light operations and smart energy. This isn't just financial engineering—it's business model transformation. Asset-light models in infrastructure can generate 20%+ ROEs versus sub-10% returns for asset-heavy models.

The parentage provides strategic advantages. While GMRP&UI operates independently, the broader GMR Group's reputation opens doors. The same relationships that built Delhi and Hyderabad airports can win smart city contracts and EV infrastructure deals.

Valuation appears compelling for bulls. Trading at 1.3 times sales versus global infrastructure comparables at 3-4 times, rerating potential is substantial. If smart metering delivers promised returns and debt continues declining, the stock could double or triple.

The macro tailwinds are undeniable. India's per capita power consumption must double to support economic growth. The energy transition requires massive investment. Infrastructure spending typically leads GDP growth. GMRP&UI plays all these themes.

Management's execution track record, despite financial stress, impressed bulls. Completing projects on time, maintaining operational excellence during restructuring, and winning competitive bids—these operational achievements matter more than quarterly earnings volatility.

Bear Case: The Leverage and Legacy Concerns

Bears see a leveraged legacy infrastructure player masquerading as a technology company. Promoters have pledged or encumbered 75.4% of their holding—this isn't a red flag; it's a crimson banner. Pledged shares create overhang, limit strategic flexibility, and signal financial stress despite restructuring claims.

The contingent liabilities worry bears. Contingent liabilities of Rs.5,484 Cr could materialize at worst possible times. In infrastructure, contingent often becomes actual when projects fail or disputes escalate.

The earnings quality is abysmal. Core operations remain unprofitable with other income masking losses. Earnings include an other income of Rs.2,228 Cr against total profits of ₹1,552 crores means the actual business loses money. How is this sustainable?

Recent quarterly performance validated bear concerns. GMR Power & Urban Infra Ltd's net profit fell -334.57% since last year same period to ₹-106.45Cr in the Q3 2024-2025. Losses of ₹100+ crores per quarter would drain cash and require additional financing, potentially diluting shareholders.

The smart metering execution risk looms large. Installing 7.5 million meters across rural Uttar Pradesh isn't just technically challenging—it's a political minefield. Consumer resistance, payment defaults, and political interference could derail projects and destroy returns.

Competition intensifies daily. Adani, Tata Power, L&T—every major infrastructure player targets smart metering. International players partner with local companies. GMRP&UI's first-mover advantage erodes as competition scales. Margins will compress; returns will normalize.

Legacy thermal assets face existential threats. Coal plants confront tightening environmental regulations, renewable competition, and stranded asset risk. The 1,100 MW of idle gas capacity may never generate returns. These legacy assets consume capital while destroying value.

The working capital deterioration signals operational stress. Working capital days have increased from -96.7 days to 81.1 days. This isn't just accounting—it's cash trapped in operations when the company desperately needs liquidity.

Regulatory risks multiply across sectors. Power tariff regulations, highway toll revisions, environmental norms, land acquisition challenges—each regulatory change could impair asset values or project returns. GMR's history is littered with regulatory casualties.

The conglomerate structure, despite demerger, creates complexity. Multiple businesses with different economics, capital needs, and risk profiles make valuation difficult. The market hates complexity and assigns discounts accordingly.

The Synthesis: A Nuanced Reality

The truth incorporates both narratives. GMRP&UI is simultaneously a transformation story and a legacy infrastructure player, a technology pivot and a traditional contractor, a deleveraging success and a stressed balance sheet.

The smart metering opportunity is real but execution remains unproven at scale. The contracts are signed but the meters aren't installed. The returns are projected but not realized. Promise and performance diverge in infrastructure.

Debt has declined but remains elevated for the business quality. Interest coverage improved but stays uncomfortably low. Asset sales are announced but not closed. Financial improvement is directionally correct but insufficiently rapid.

The transformation to asset-light models makes strategic sense but requires capabilities GMRP&UI is still building. Technology platforms, data analytics, customer service—these aren't traditional infrastructure competencies. Can a company that built coal plants become a technology services provider?

Management quality is proven in engineering but untested in new businesses. Building airports and highways demonstrates execution excellence. But smart metering and EV infrastructure require different skills—software development, consumer engagement, regulatory navigation in nascent markets.

Valuation appears cheap but reflects genuine risks. The market isn't stupid—it sees the opportunity but also the execution challenges, financial constraints, and competitive threats. Current multiples might be fair given the risk-reward balance.

The macro story supports infrastructure investment but doesn't guarantee individual company success. India needs infrastructure, but that doesn't mean GMRP&UI captures value. Execution, not opportunity, determines returns.

The Verdict: Asymmetric but Uncertain

GMRP&UI presents an asymmetric opportunity—limited downside with substantial upside if transformation succeeds. But the probability of success remains uncertain. This isn't a value play or a growth story—it's a transformation bet.

For believers in India's infrastructure story and management's execution ability, current valuations offer compelling entry. For skeptics worried about leverage, competition, and execution risk, the stock remains uninvestable despite apparent cheapness.

The next 18-24 months will prove decisive. Smart meter installation progress, asset sale completion, and debt reduction trajectory will validate either bulls or bears. Until then, GMRP&UI remains a battle between promise and performance, between transformation potential and legacy challenges.

XI. Epilogue & Strategic Outlook

Mumbai, 2030. The monsoon that once inspired Ratan Tata's vision for affordable cars now powers something different through GMR's smart grid infrastructure. Every drop measured, every watt tracked, every electron optimized through millions of smart meters spread across India's heartland. The company that nearly drowned in infrastructure debt has emerged as an unlikely leader in India's energy transition. Or has it?

The future of integrated infrastructure players in India stands at an inflection point. The old model—leverage up, build assets, pray for traffic or power demand—died in the 2010s debt crisis. The new model—asset-light, technology-enabled, service-oriented—remains unproven at scale. GMRP&UI straddles both worlds, one foot in legacy infrastructure, another stepping toward digital services.

Can GMRP&UI successfully transition to a smart infrastructure company? The question haunts every board meeting, every analyst call, every strategic decision. The smart metering contracts provide proof of concept but not proof of scale. Installing 7.5 million meters is impressive; making them profitable is transformational. The difference between the two will determine GMRP&UI's fate.

The challenges ahead are formidable. Execution risk in smart metering remains paramount—every delayed installation, every technical glitch, every payment default erodes returns and credibility. Competition intensifies as every infrastructure player recognizes the opportunity. Regulatory uncertainty persists as policies evolve with technology. Financial constraints, though reduced, still limit strategic flexibility.

Yet the opportunities are equally compelling. India's power distribution reforms create a ₹100,000 crore smart metering market. The EV revolution requires charging infrastructure that leverages GMRP&UI's highway and power assets. Urban infrastructure demand explodes as India urbanizes. The energy transition from coal to renewables creates new service opportunities. Each trend favors players who can execute complex, technology-enabled infrastructure projects.

The lessons for emerging market infrastructure investing are profound. First, survival requires adaptability—companies that can't transform die. GMR survived by reimagining itself from builder to operator to service provider. Second, leverage kills more companies than competition—financial discipline matters more than growth. Third, regulatory relationships are assets—trust built over decades enables success in regulated sectors. Fourth, family governance can provide patient capital but must be professionally managed. Fifth, conglomerate structures destroy value unless carefully managed through focused subsidiaries.

The role of family-controlled conglomerates in nation-building remains contested. Critics see inefficient capital allocation, corporate governance concerns, and market-distorting influence. Supporters see patient capital, long-term thinking, and alignment with national development goals. GMR embodies both narratives—a family conglomerate that nearly collapsed from overleverage but also built world-class airports that transformed India's image.

GMRP&UI's strategic positioning for the next decade depends on three critical factors:

Technology Capability Building: The company must transform from engineering excellence to technology leadership. This means hiring software developers, data scientists, and digital natives. It means building platforms that can manage millions of data points in real-time. It means becoming a technology company that happens to own infrastructure, not an infrastructure company trying to adopt technology.

Capital Allocation Discipline: Every rupee matters when you're transforming a business model. Legacy assets must generate cash to fund new opportunities. Failed projects must be shut down quickly. Success must be scaled rapidly. The capital allocation decisions over the next 24 months will determine whether GMRP&UI becomes a smart infrastructure leader or another leveraged infrastructure player.

Regulatory Navigation: India's infrastructure regulations are evolving rapidly—new policies for smart meters, changing norms for power distribution, emerging frameworks for EV charging. GMRP&UI must not just comply but shape these regulations. The company's four-decade relationship with regulators provides advantage, but past relationships don't guarantee future success.

The bear scenario sees GMRP&UI trapped between legacy and future—unable to escape infrastructure debt while failing to capture smart infrastructure opportunities. Execution failures in smart metering destroy credibility. Competition erodes margins. Legacy assets become stranded. The stock languishes as investors lose faith in the transformation story.

The bull scenario envisions successful transformation—smart metering delivers promised returns, creating cash flow for further investment. EV infrastructure leverages existing assets for new revenue streams. Asset sales eliminate debt, creating financial flexibility. The company rerates as a technology-enabled infrastructure player, commanding multiples similar to global smart infrastructure peers.

The most likely scenario lies between extremes. GMRP&UI will probably succeed partially—some smart metering projects will deliver strong returns while others struggle. The transformation will take longer and cost more than expected. Competition will compress margins but not eliminate profits. The company will survive and eventually thrive, but the journey will be volatile.

For long-term fundamental investors, GMRP&UI presents a complex proposition. The transformation story is real but execution risk is substantial. The valuation appears attractive but reflects genuine challenges. The opportunity is massive but competition is fierce. This isn't a simple value play or growth story—it's a bet on India's infrastructure future and management's ability to navigate transformation.

The next 18-24 months will prove decisive. Smart meter installations must accelerate. Asset sales must close. Debt must continue declining. Any material failure could unravel the transformation narrative and send the stock lower. But successful execution could catalyze a rerating that rewards patient investors.

As the monsoon clouds gather over Mumbai in 2030, GMR's smart infrastructure will either be managing India's energy transition or struggling with legacy infrastructure burdens. The difference between these futures depends on decisions being made today in boardrooms and project sites across India. The transformation from infrastructure builder to smart services provider isn't just corporate strategy—it's a bet on India's development trajectory.

The story of GMRP&UI is far from over. It's a story of resilience and transformation, of family enterprise and professional management, of infrastructure dreams and financial reality. Whether it becomes a case study in successful transformation or another cautionary tale of infrastructure overreach remains to be written. But one thing is certain: the company that emerged from near-death in 2021 will look very different by 2030, for better or worse.

The infrastructure sector's evolution from asset-heavy to asset-light, from construction to services, from analog to digital, will create winners and losers. GMRP&UI has positioned itself for this transition, but positioning and success are different things. The execution over the next few years will determine whether GMR Power & Urban Infra becomes India's smart infrastructure champion or another infrastructure company that couldn't escape its legacy.

For investors, employees, and stakeholders, the journey ahead promises to be anything but boring. In infrastructure, transformation is measured in decades, not quarters. The patience to endure volatility while maintaining strategic direction will determine success. GMR has survived 45 years of India's infrastructure evolution—the next chapter will test whether it can thrive in the digital infrastructure age.

The monsoon that inspired Ratan Tata's vision now falls on GMR's smart meters, each drop measured, each watt counted, each electron tracked. The transformation from building infrastructure to making it intelligent has begun. Whether it succeeds will shape not just GMRP&UI's future but India's infrastructure evolution. The story continues, one smart meter at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube