Repco Home Finance: The Untold Story of India's Government-Backed Housing Finance Company

I. Introduction & Episode Teaser

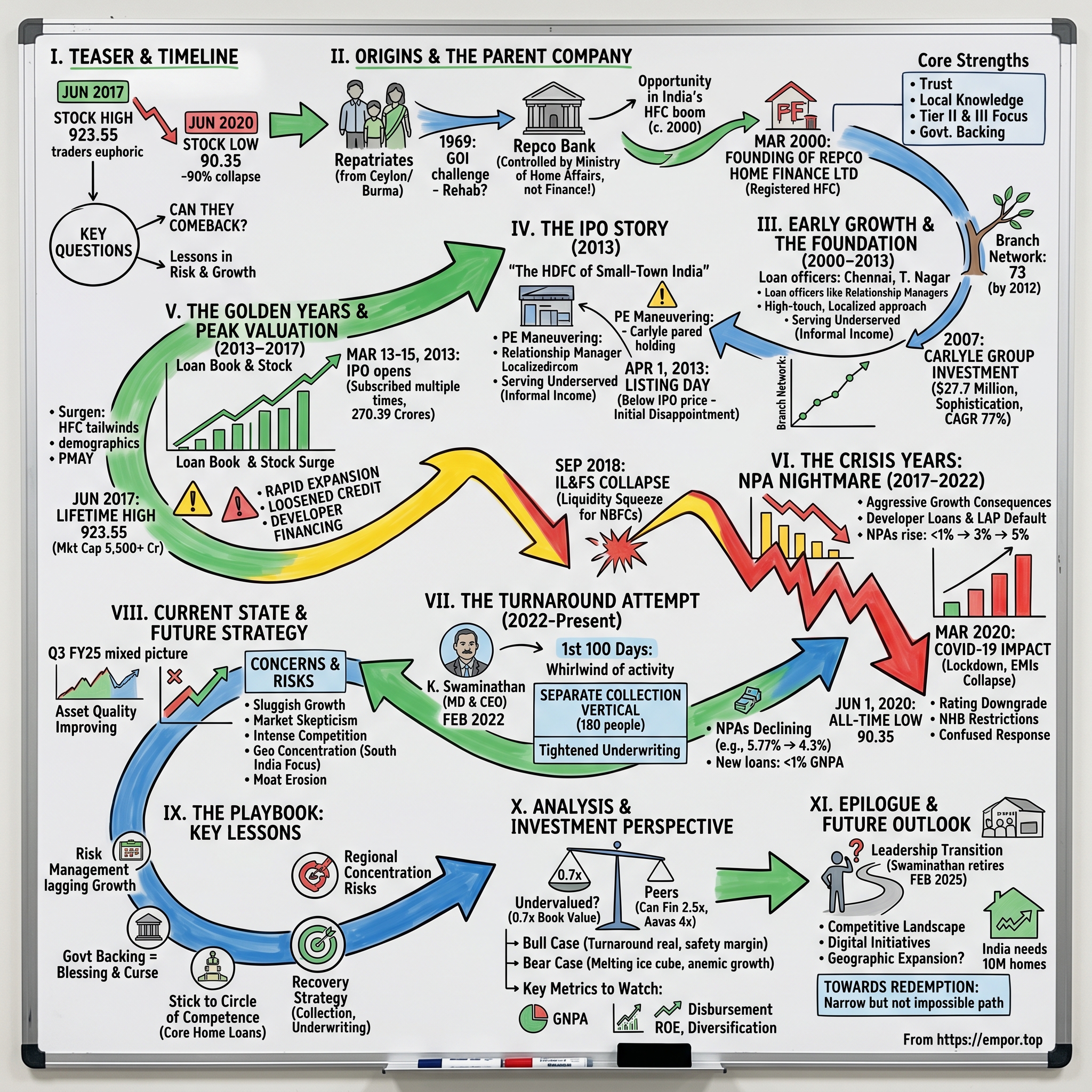

Picture this: It's a sweltering Chennai afternoon in June 2017. In the trading rooms of Mumbai's financial district, screens flash green as Repco Home Finance Ltd.'s stock reached its lifetime high, touching a price level of 923.55. Traders are euphoric. A housing finance company that started as a subsidiary of a government bank for repatriates had just crossed ₹900 per share—a stunning 5x appreciation since its IPO just four years earlier.

Fast forward three years to June 2020. Those same trading screens now show a different story. REPCOHOME's all-time low was 90.35 INR and was reached on Jun 1, 2020. A 90% collapse. What happened in those three years that transformed a market darling into a cautionary tale?

This is the story of Repco Home Finance Limited—a company whose journey mirrors the broader narrative of India's housing finance sector. From its unique origins serving repatriates to becoming a public market sensation, from a devastating NPA crisis to an ongoing turnaround attempt, Repco's arc offers profound lessons about risk management, government backing as both blessing and curse, and the perils of rapid growth without adequate guardrails.

Established in April 2000, Repco Home Finance Ltd. is a registered housing finance company. It is a subsidiary of the Repatriates Cooperative Finance and Development Bank Limited(Repco Bank). But this simple description barely scratches the surface of a company whose story encompasses private equity deals, IPO dreams, regulatory challenges, and a management overhaul that's still playing out today.

The central question we're exploring isn't just what went wrong—it's whether Repco can engineer one of Indian finance's most compelling comebacks. With Mkt Cap: 2,226 Crore (down -32.2% in 1 year) and The company has delivered a poor sales growth of 4.95% over past five years, the jury is still out.

What makes Repco's story particularly fascinating is how it sits at the intersection of multiple India stories: the affordable housing boom, the NBFC crisis that shook the financial system, the COVID-19 pandemic's devastating impact on lenders, and now, the potential resurrection under new leadership. This isn't just a company story—it's a window into how India's financial system works, breaks, and sometimes repairs itself.

II. Origins & The Parent Company Story

To understand Repco Home Finance, you first need to understand its parent—and that takes us back to 1969, to a story of displacement and redemption that most investors have never heard.

The year is 1969. Thousands of Indian-origin families are streaming back from neighboring countries—Ceylon (now Sri Lanka) and Burma (Myanmar)—forced to leave behind businesses, properties, and lives they had built over generations. These weren't economic migrants; they were refugees of political upheaval. The newly independent nations were implementing policies that effectively pushed out their Indian-origin populations. Families that had lived in these countries for decades, sometimes centuries, suddenly found themselves stateless and asset-less.

The Government of India faced a unique challenge: how to rehabilitate these repatriates who had lost everything? The answer came in the form of Repco Bank—the Repatriates Cooperative Finance and Development Bank Limited. This wasn't just another government initiative; it was a lifeline for a displaced community. Controlled by the Ministry of Home Affairs (not Finance, notably), the bank operated exclusively in South India where most repatriates had settled.

Think about the peculiarity of this setup. While most banks fall under the Finance Ministry's purview, Repco Bank answered to Home Affairs—the ministry responsible for internal security and citizenship matters. This unique reporting structure would later play a crucial role in shaping its subsidiary's destiny.

For three decades, Repco Bank operated in relative obscurity, serving its niche community with dedication. But as the new millennium approached, the bank's leadership saw an opportunity. India's housing finance market was exploding. The liberalization of the 1990s had created a new middle class hungry for home ownership. Traditional banks were slow and bureaucratic. Housing finance companies like HDFC were focusing on the urban elite. There was a gap in the market—particularly in Tier II and III cities of South India where Repco Bank had its roots.

The company went IPO on 2013-04-01, but the seeds were planted much earlier. In March 2000, the board of Repco Bank made a decision that would define the next two decades: they would create a specialized housing finance subsidiary. Repco was established in 2000 for the purpose of providing housing finance.

The timing was no accident. The year 2000 marked a turning point in India's economic story. The dot-com boom was creating new wealth. Interest rates were declining. The Nuclear family structure was replacing joint families, creating massive new demand for housing. And crucially, the National Housing Bank had just liberalized norms for housing finance companies, making it easier to enter the market.

But why would a cooperative bank for repatriates venture into mainstream housing finance? The answer lay in a strategic insight: the repatriate community Repco Bank served had largely stabilized. Their children, born in India, were indistinguishable from other Indians. They needed homes just like everyone else. Moreover, the bank's deep roots in South India's smaller cities gave it something money couldn't buy—trust and local knowledge.

When Repco Home Finance was formally incorporated in April 2000, it inherited more than just capital from its parent. It inherited a philosophy of serving the underserved, a network of relationships in South India's tier-II cities, and perhaps most importantly, the implicit backing of a government-controlled institution. This last factor—government backing—would prove to be both its greatest strength and, eventually, a dangerous crutch.

The early vision was clear: while HDFC and others fought for the lucrative metros, Repco would own the next tier. Salem, not Chennai. Belgaum, not Bangalore. This wasn't just a business strategy; it was almost a social mission wrapped in commercial clothing. The company would democratize home ownership for India's small-town middle class—teachers, small business owners, government employees—people who banks often ignored because their loan tickets were too small or their documentation too informal.

III. Early Growth & Building the Foundation (2000-2013)

The first branch opened in Chennai's T. Nagar in 2000—a deliberate choice. T. Nagar wasn't the city's financial district; it was its commercial heart, where middle-class families came to shop for silk sarees and gold jewelry. If you wanted to understand middle India's aspirations, you set up shop in T. Nagar, not Nariman Point.

In those early days, Repco's loan officers operated more like relationship managers than bankers. They would visit customers' homes, understand their informal income sources, and structure loans that traditional banks wouldn't touch. A street vendor who sold idlis but had no formal income proof? Repco would look at his daily cash flows. A private tuition teacher with seasonal income? They'd structure repayments accordingly.

This high-touch, localized approach meant growth was slow but steady. By 2005, Repco had expanded to 25 branches, all in South India. The average ticket size was just ₹5-7 lakhs—a fraction of what HDFC or LIC Housing Finance targeted. But the margins were healthy, and more importantly, the repayment culture in these smaller towns was strong.

The product portfolio evolved organically from customer needs. Beyond standard home loans, Repco introduced plot loans (crucial in smaller towns where people buy land first and build later), loans against property (LAP) for small business needs, and home improvement loans. Each product was tweaked for local preferences. In Tamil Nadu, for instance, they understood that families often built homes incrementally—first the ground floor, then adding floors as children grew. Repco's products accommodated this reality.

But the real transformation came in 2007, and it arrived in the form of a visitor from Washington DC.

Mumbai, India - Global private equity firm The Carlyle Group has committed US$27.7 million in Repco Home Finance Limited, a Chennai-based housing finance company focusing on Southern India. When Carlyle's team first looked at Repco, they saw what others missed. Here was a company with a pristine asset quality, operating in markets with low competition, backed by a government entity, and run by conservative bankers who understood risk.

The investment thesis was compelling. Repco, a subsidiary of Repatriates Co-operative Finance & Development Bank Ltd, has been in the housing finance business since 2000, and has grown at a CAGR of 77% over the last five years. That 77% CAGR number made Carlyle's partners sit up. This wasn't just growth; it was explosive expansion with minimal NPAs.

Carlyle had invested Rs. 76 crore via 2 tranches in the company since 2007. The PE giant didn't just bring capital; it brought sophistication. New risk management systems were implemented. The board was strengthened with independent directors. Hiring standards were raised—suddenly, Repco was recruiting from IIMs and NITs, not just local commerce colleges.

The Carlyle investment also changed Repco's ambitions. Mr. Shankar Narayanan, Managing Director and Head of Carlyle Growth Capital team in India, said, "Indians place a high importance on home ownership. Repco's business model is focused on fulfilling this basic need in a customer-friendly and transparent manner. Repco is a good example of a company that has built a strong business in a short time span. Carlyle's network of relationships may act as a catalyst in Repco's evolution into a top player in the housing finance market."

Under Carlyle's watch, Repco's operational metrics improved dramatically. Turnaround time for loan approvals dropped from weeks to days. The company invested in technology—not cutting-edge by global standards, but revolutionary for customers used to paper-heavy processes. By 2010, Repco had a basic loan origination system that could track applications from submission to disbursement.

The branch network expanded strategically. Chennai headquartered housing finance company promoted by GoI's The Repatriates Co-operative Finance and Development Bank (Repco Bank) in April 2000, Repco Home Finance has 73 branches and 19 satellite centres, mostly in the tier 2 and tier 3 cities of Tamil Nadu, Karnataka, Andhra Pradesh, Kerala, Maharashtra, Odisha, West Bengal, Gujarat and Puducherry, as of 31st December 2012.

Each new branch opening followed a template: identify cities with 2-5 lakh population, ensure no more than 2-3 competitors present, hire locals who understood the market, and maintain loan sizes between ₹5-15 lakhs. This wasn't sexy, but it was profitable.

The numbers told the story. Loan disbursements grew from ₹200 crores in 2007 to over ₹1,200 crores by 2012. NPAs remained below 1%—almost unheard of in Indian lending. The return on equity consistently exceeded 20%. Repco had found a sweet spot: serving customers that banks ignored, in markets where competition was minimal, with a cost structure that worked for small ticket loans.

But success creates its own pressures. By 2012, Carlyle had been invested for five years. The PE firm needed an exit, and Repco needed capital to fund its continued growth. The solution seemed obvious: tap the public markets.

IV. The IPO Story & Public Market Dreams (2013)

The roadshow began in February 2013. In the wood-paneled conference rooms of Mumbai's Nariman Point and the glass towers of Singapore's Raffles Place, Repco's management team told their story to institutional investors. The pitch was simple but powerful: "We are the HDFC of small-town India."

Repco Home Finance IPO is a main-board IPO of 15720262 equity shares of the face value of ₹10 aggregating up to ₹270.39 Crores. The issue is priced at ₹165 to ₹172 per share. The pricing was aggressive but not unreasonable—about 11 times earnings, in line with smaller housing finance peers.

But behind the scenes, the PE choreography was fascinating. While there is no offer for sale by Carlyle in the ensuring IPO, it has sold 46 lakh shares or 9.99% equity stake to Creador, a South East Asia focused Rs 700 crore PE fund, for Rs. 72.4 crore in February 2013 (i.e. just one month back). Also, Carlyle has sold 62 lakh shares or 13.33% equity in the company, to another PE firm WCP Holdings, after 30th September 2012. Thus, Carlyle has pared its holding by more than half from 49.85% to 23.75% of pre-IPO shareholding.

This pre-IPO maneuvering was classic PE financial engineering. Carlyle was taking money off the table before the IPO, de-risking their investment while still maintaining a significant stake to benefit from any post-listing pop. The buyers—Creador and WCP Holdings—were betting they could flip their stakes post-IPO for quick gains.

The Repco Home Finance IPO opens on March 13, 2013 and closes on March 15, 2013. The three-day window saw extraordinary interest. Institutional investors, starved of quality financial services IPOs, poured in. The retail portion was oversubscribed within hours of opening. By the time the bidding closed, the issue was subscribed multiple times over.

But then came listing day—April 1, 2013. The shares listed at ₹160.85, below the IPO price of ₹172. For retail investors who had bet on a listing pop, it was a cruel April Fool's joke. The weak listing reflected broader market concerns about rising interest rates and questions about whether Repco's small-town strategy could scale.

The initial disappointment, however, quickly gave way to a spectacular run. Within months, the stock had not just recovered but surged past ₹200. What changed? The market began to understand what Carlyle had seen years earlier—Repco wasn't competing with HDFC; it was creating a new market altogether.

The IPO proceeds of ₹270 crores transformed Repco's balance sheet. The company could now borrow at lower rates, expand faster, and most importantly, had the currency (public stock) to attract talent. The first post-IPO annual report read like a victory lap—loan book crossed ₹5,000 crores, NPAs remained under 1%, and ROE exceeded 22%.

V. The Golden Years & Peak Valuation (2013-2017)

If you wanted to understand India's housing finance boom in the mid-2010s, you could do worse than studying Repco's trajectory during these years. Everything that could go right, did.

Interest rates were falling—the RBI cut rates multiple times between 2013 and 2017. Property prices in Tier II and III cities were still affordable, unlike the bubble valuations in metros. The government launched Pradhan Mantri Awas Yojana in 2015, providing subsidies for affordable housing. Demographics were favorable—millions of young Indians were entering their home-buying years. And credit penetration in smaller cities was still minimal, providing enormous room for growth.

Repco rode every one of these tailwinds. The loan book grew from ₹5,000 crores in 2013 to over ₹12,000 crores by 2017. The company expanded beyond South India, entering Gujarat, West Bengal, and Odisha. The average ticket size crept up from ₹7 lakhs to ₹12 lakhs as customer affluence improved. New products were launched—loans for senior citizens, special schemes for women borrowers, green housing loans.

The stock market loved the story. From the IPO price of ₹172, the stock began a relentless climb. ₹300 by 2014. ₹500 by 2015. ₹700 by 2016. Television channels that had ignored Repco during its IPO now featured the company regularly. "The next multibagger," proclaimed one market expert on CNBC. "Small-town India's mortgage play," declared another on ET Now.

The competition landscape during these years was surprisingly benign. HDFC and LIC Housing Finance remained focused on larger tickets in metros. Can Fin Homes, Repco's closest peer, was concentrated in Karnataka. Newer players like Aavas Financiers and Home First Finance were still finding their feet. Repco had its niche largely to itself.

Management spoke confidently about reaching ₹25,000 crores in AUM by 2020. Branch expansion accelerated—from 73 at IPO to over 140 by 2017. The company hired aggressively, building specialized verticals for collections, credit assessment, and legal documentation. Everything pointed to continued success.

Repco Home Finance Ltd.'s stock reached its lifetime high in June 2017, touching a price level of 923.55. However, we are considering setting the ultimate target price at 880.05, which is the target of the Cup with Handle pattern, suggesting a potential gain of 71.20%. When the stock hit ₹923 in June 2017, the market cap crossed ₹5,500 crores. For a company that Carlyle had valued at less than ₹200 crores just a decade earlier, it was a stunning transformation.

But beneath the surface, problems were brewing. The rapid expansion had stretched the company's risk management capabilities. Branches opened hastily in new geographies didn't have the same deep local knowledge that had been Repco's strength. The pressure to grow meant credit standards were loosened—not dramatically, but enough. Competition for talent meant salary costs were ballooning. And most dangerously, the company had started lending to real estate developers for construction finance—a major departure from its retail focus.

The first warning signs appeared in early 2017. A few developer loans in Andhra Pradesh turned sticky. Some branches reported higher delinquencies in their LAP portfolio. The incremental cost of funds started rising as the bond market became nervous about NBFCs' aggressive growth. But with the stock at all-time highs and sell-side analysts still bullish, these concerns were brushed aside.

Nobody knew it then, but June 2017 would mark not just Repco's peak, but the beginning of one of the most dramatic destructions of value in Indian financial services.

VI. The Crisis Years: NPA Nightmare & Fall from Grace (2017-2022)

The unraveling began not with Repco, but 1,200 kilometers away in Mumbai's Bandra-Kurla Complex. In September 2018, It all began in September 2018, when financing behemoth Infrastructure Leasing & Financial Services (IL&FS) collapsed. CNBC-TV18 reports that the IL&FS group is saddled with a debt of Rs91,091 crore and is facing losses to the tune of Rs1,887 crore in the financial year 2018. News reports also say IL&FS has been funding long-term projects via short-term borrowing. As the cost of borrowing rises due to an increase in debt, short-term liquidity dries up and projects get delayed, and IL&FS finds it difficult to make repayments.

The IL&FS default sent shockwaves through India's financial system. Mumbai-based DSP Mutual Funds dumps Rs300 crore worth of commercial papers of another NBFC, Dewan Housing Finance Limited (DHFL), at a discounted rate in September, sparking speculation that the company is staring at a rating downgrade. These developments make investors nervous and the market cap of NBFCs is decimated. Between Sept. 21 and 24, large NBFCs like Housing Development and Finance Corporation (HDFC) and Bajaj Finance's market cap erodes by around Rs18,600 crore and Rs13,800 crore, respectively. Twelve other NBFCs including L&T Finance Holdings, DHFL, and Indiabulls Housing Finance also witness a sharp fall in market cap.

For Repco, the IL&FS crisis was like a hurricane hitting an unprepared coastal town. The company had been borrowing short-term through commercial papers and refinancing them regularly—a common practice that worked fine until it didn't. Suddenly, mutual funds stopped buying NBFC paper. Banks, already struggling with their own NPA problems, cut credit lines. The cost of borrowing spiked from 7% to over 9% within months.

But this was just the appetizer for the main crisis. Repco's aggressive expansion between 2013-2017 had planted seeds of destruction that now began sprouting. Loans given to real estate developers in Andhra Pradesh and Karnataka—a segment the company had no expertise in—started defaulting en masse. The LAP portfolio, which had grown rapidly as the company chased growth, showed stress as small businesses struggled with GST implementation and demonetization aftershocks.

The numbers told a story of rapid deterioration. NPAs, which had been below 1% for years, jumped to 3% by March 2019, then 5% by March 2020. The stock price, which had peaked at ₹923, began a sickening slide. ₹600 by December 2018. ₹400 by June 2019. ₹250 by December 2019.

Then came COVID-19.

If the NBFC crisis was a hurricane, COVID was an asteroid impact. In March 2020, India went into one of the world's strictest lockdowns. Construction sites shut down. EMI collections collapsed. Customers who had never missed a payment in their lives suddenly had no income. The RBI announced a moratorium, but for NBFCs like Repco, this meant cash inflows stopped while outflows to lenders continued.

REPCOHOME reached its all-time low on Jun 1, 2020 with the price of 90.35 INR. Think about that—from ₹923 to ₹90 in three years. It was one of the most spectacular wealth destructions in Indian capital markets. Investors who had bought at the peak had lost over 90% of their capital.

The company's response during these crisis years was confused and ineffective. Management seemed paralyzed, unable to decide whether to focus on growth or asset quality. The collection machinery, built for normal times, couldn't cope with the scale of defaults. Branches that had opened hastily during the expansion years lacked the local relationships needed to recover stressed assets. Employee morale plummeted as the stock options they'd received became worthless.

By 2021, Repco had become a case study in everything that could go wrong with a housing finance company. NPAs had crossed 7%. The company was finding it difficult to raise fresh capital. Rating agencies had downgraded its debt. The National Housing Bank, the regulator, had restricted its ability to do fresh business until asset quality improved. The stock was trading below book value, suggesting the market believed the book itself was overstated.

But it's worth noting that even during these darkest days, Repco never defaulted on its obligations. Unlike IL&FS or DHFL, which went into resolution, Repco continued to service its debt, pay its employees, and operate its branches. The government backing through Repco Bank, which had seemed like a minor detail during good times, proved crucial. It gave lenders confidence that Repco wouldn't be allowed to fail completely.

VII. The Turnaround Attempt: New Leadership & Recovery Strategy (2022-Present)

February 2022 marked a potential inflection point. The company said it has appointed K. Swaminathan as the managing director and chief executive officer for a period of three years. Swaminathan wasn't a housing finance veteran—he came from Indian Overseas Bank where he served as Executive Director from 2016 to 2018. But perhaps that's exactly what Repco needed—someone who understood NPAs, having dealt with them in the banking sector.

Swaminathan's first 100 days were a whirlwind of activity. He visited every branch, met key borrowers, and most importantly, rebuilt the collection machinery from scratch. A separate collection vertical of approximately 180 personnel was created—professionals who understood the psychology of recovery, the legal frameworks, and the art of negotiation.

The new CEO's approach was surgical. Demand notices were sent to NPA accounts under the SARFAESI Act, signaling that Repco was serious about recovery. Underwriting standards were tightened dramatically—loan approvals dropped in the short term, but quality improved. Most impressively, out of total disbursements of approximately ₹7,500 crores over 2.5 years under new management, only around ₹50 crores turned into NPAs, reflecting a GNPA ratio of less than 1%.

The asset quality improvements were tangible. Gross NPAs, which had peaked at nearly 7% in 2022, began declining. By March 2023, they were down to 5.77%. By March 2024, 4.1%. The latest numbers show them at 4.3% as of June 2024—still elevated, but trending in the right direction.

The company also appointed K. Lakshmi as the chief financial officer, bringing in fresh talent at key positions. The new team focused on basics: know your customer, understand their cash flows, maintain conservative loan-to-value ratios, and build strong local relationships.

Technology, long neglected, finally got attention. The company launched digital initiatives for customer onboarding, though it remained far behind fintech-savvy competitors. The branch network was rationalized—underperforming locations were closed while new ones opened in carefully selected markets. As of March 2024, RHFL operates through 168 branches and 44 satellite centers.

The recovery strategy also involved a conscious shift in product mix. The company decided to focus more on core home loans rather than the LAP segment that had caused problems. Developer financing was completely stopped. The average ticket size was brought back down to ₹10-15 lakhs, returning to Repco's traditional strength.

Management set ambitious targets: a ₹20,000 crore loan book by FY27 (with non-home loans capped at 25-30%), and GNPA below 2%. Whether these targets are achievable remains to be seen, but at least there was a plan, communicated clearly and pursued consistently.

VIII. Current State & Future Strategy

Today's Repco is a company in transition. The Q3 FY25 numbers present a mixed picture. Repco Home Finance Ltd. released its un-audited financial results for Q3 FY25, reporting a total income of Rs. 445 crores, a 4% increase from Q2 FY25, and net profits of Rs. 107 crores, down from Rs. 113 crores in the previous quarter.

The good news: Asset quality continues to improve, with NPAs trending down. The collection machinery is working. New disbursements are showing excellent quality. The company maintains strong capital adequacy ratios well above regulatory requirements.

The concerning aspects: Growth remains sluggish—the 4.95% five-year sales CAGR is poor by any standard. The stock trades at just 0.7x book value, suggesting deep market skepticism. Competition has intensified dramatically, with new-age players like Home First Finance and established giants like HDFC all fighting for the same customers.

Regulatory changes have added complexity. The harmonization of regulations between banks and NBFCs means Repco can no longer arbitrage regulatory gaps. Growth in Karnataka has been flat due to state-specific regulatory issues. The company has made a conscious decision to focus on home loans over the more profitable but riskier LAP segment, impacting margins.

Geographic concentration remains a critical risk. Despite years of expansion attempts, Repco remains heavily concentrated in South India, particularly Tamil Nadu. This makes it vulnerable to regional economic shocks or regulatory changes. Attempts to expand into North and East India have been half-hearted at best.

The competitive landscape has transformed beyond recognition since Repco's golden years. Affordable housing finance is no longer a niche—it's a mainstream segment everyone wants. Banks have become aggressive in small-ticket home loans. Fintech players are using technology to reduce costs and improve customer experience in ways Repco struggles to match. The moat that once protected Repco's franchise has largely eroded.

IX. Playbook: Lessons from the Rise, Fall, and Recovery

Repco's journey offers a masterclass in both how to build a successful housing finance company and how to destroy it. Let's extract the key lessons:

The Dangers of Rapid Growth Without Risk Management: Between 2013-2017, Repco grew its loan book at over 20% annually. But the risk management infrastructure didn't keep pace. New branches were opened without ensuring adequate local knowledge. Credit standards were loosened to meet growth targets. The company ventured into developer financing without the requisite expertise. The lesson is clear: growth without accompanying risk management is not growth—it's deferred destruction.

Government Backing: Both Blessing and Curse: Repco's government parentage gave it credibility and prevented complete collapse during the crisis. But it also bred complacency. Management knew they had an implicit safety net, which may have encouraged riskier behavior. The government backing also meant bureaucratic decision-making and inability to respond quickly to market changes.

The Importance of Sticking to Your Core: Repco succeeded when it focused on small-ticket home loans in Tier II and III cities. It struggled when it ventured into developer financing and grew its LAP book aggressively. The best businesses have a clear understanding of their circle of competence and the discipline to stay within it.

Regional Concentration Risks: Repco's heavy concentration in South India seemed like a strength when the region was doing well. But it became a vulnerability when faced with region-specific challenges. Diversification isn't just about products; it's about geography too.

Recovery Strategies That Work: The post-2022 turnaround shows what works in recovery: bring in fresh leadership from outside, rebuild the collection machinery, tighten underwriting standards, return to core strengths, and communicate clearly with stakeholders. It also shows what doesn't work: trying to grow your way out of an asset quality problem.

The Affordable Housing Opportunity: Despite Repco's struggles, the affordable housing opportunity in India remains massive. India needs 10 million new homes annually; only 3 million are being built. The challenge isn't demand—it's execution.

Building a Sustainable Housing Finance Business: The key elements are clear: conservative underwriting, deep local knowledge, reasonable growth targets, robust risk management, and most importantly, remembering that in lending, return of capital is more important than return on capital.

X. Analysis & Investment Perspective

Compared to the current market price of 433.3 INR, Repco Home Finance Ltd is Undervalued by 61% according to some estimates. The stock trades at approximately 0.7x book value, well below peers like Can Fin Homes (2.5x) or Aavas Financiers (4x). This valuation gap reflects both the company's challenges and potential opportunity.

The bear case is straightforward: Repco is a melting ice cube. Growth is anemic. Geographic concentration is dangerous. Competition is intense. The company lacks the technology infrastructure to compete with new-age players. NPAs, while improving, remain elevated. Management's ambitious targets seem unrealistic. The parent bank's influence prevents nimble decision-making.

The bull case requires more imagination but isn't without merit: The turnaround is real and gaining momentum. NPAs are trending down consistently. New disbursements show excellent quality. The company is trading well below book value, providing a margin of safety. Government backing ensures survival. The affordable housing segment has massive tailwinds. If management delivers even half their targets, the stock could re-rate significantly.

Comparison with peers reveals Repco's challenges and opportunities. Can Fin Homes, with its Karnataka focus and conservative approach, trades at a premium despite similar size. Aavas Financiers, focused on self-employed customers in similar markets, commands a much higher valuation due to superior execution. Home First Finance, despite being smaller, has better technology and growth rates. The message is clear: the market rewards execution, not just opportunity.

Key metrics to watch going forward: GNPA trends (needs to drop below 3% for comfort), disbursement growth (needs to accelerate beyond current levels), ROE improvement (currently sub-10%, needs to reach 15%+), and geographic diversification progress. The company's ability to grow its loan book to ₹20,000 crores by FY27 while maintaining asset quality will be the acid test.

For investors, Repco represents a classic turnaround bet. The risk-reward is skewed but not uniformly in one direction. Conservative investors should wait for clearer evidence of sustainable turnaround—perhaps GNPA below 3% and ROE above 12%. Aggressive investors might see the current valuation as offering sufficient margin of safety, especially if they believe in India's long-term affordable housing story.

XI. Epilogue & Future Outlook

Repco Home Finance's story is far from over. Tenure of Mr. K.Swaminathan (DIN: 06485385) as Chief Executive Officer of the company is ending on 20th February, 2025. Accordingly, he will retire from the directorship of the company by the close of business on 20th February, 2025. This leadership transition adds another layer of uncertainty to an already complex situation.

The broader affordable housing finance sector in India stands at an inflection point. The government's push for "Housing for All" continues. Technology is democratizing access to credit. But regulatory tightening and competitive intensity are squeezing margins. Winners will be those who can combine operational excellence with technological innovation while maintaining conservative underwriting.

For Repco, the path forward is narrow but not impossible. The company needs to complete its asset quality cleanup, accelerate growth without compromising standards, invest in technology without losing its high-touch advantage, and expand geographically while maintaining local knowledge. It's a difficult balance, but not an impossible one.

The Indian financial sector has seen remarkable turnarounds before. ICICI Bank recovered from its infrastructure and corporate lending mess. Yes Bank survived a near-death experience. Even IL&FS is being resolved in an orderly manner. Repco's challenge is less severe than any of these cases.

What needs to happen for a complete turnaround? First, NPAs need to normalize below 2%. Second, growth needs to accelerate to at least 15% annually. Third, the company needs to expand successfully beyond South India. Fourth, technology investments need to bear fruit in improved efficiency and customer experience. Finally, and perhaps most importantly, the company needs to regain the trust of institutional investors who fled during the crisis years.

The story of Repco Home Finance is ultimately a very Indian story—of ambition and overreach, of crisis and resilience, of government support and market discipline. It's a reminder that in financial services, there are no permanent winners, only permanent principles: lend carefully, grow sustainably, and never forget that in banking, the return of capital matters more than the return on capital.

Whether Repco can engineer one of Indian finance's great comebacks remains to be seen. But for students of financial history and investors seeking to understand India's complex financial ecosystem, the journey itself offers invaluable lessons. The company that began as a vehicle to serve displaced repatriates may yet find redemption serving the housing dreams of small-town India. The next chapter is still being written.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube