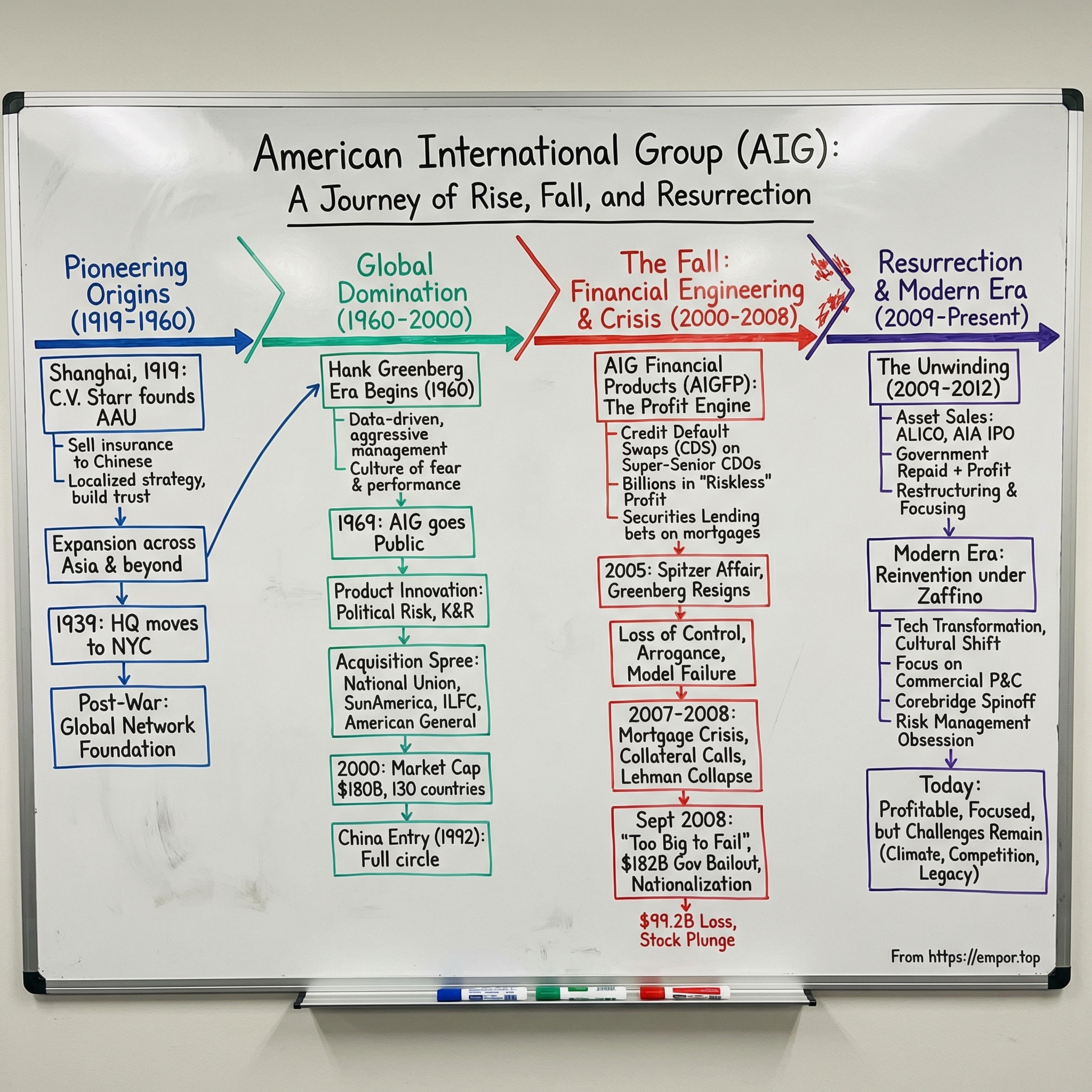

American International Group (AIG): The Rise, Fall, and Resurrection of an Insurance Empire

I. Introduction & Cold Open

The date was September 16, 2008. Inside the Federal Reserve Bank of New York, exhausted officials huddled around conference tables littered with coffee cups and financial models. Outside, the autumn air carried whispers of panic from Wall Street trading floors. American International Group—AIG—the insurance titan that had insured everything from Hollywood films to space satellites, teetered on the edge of collapse. Its stock had plummeted 95% in a year. Credit rating downgrades had triggered $32 billion in collateral calls that the company couldn't meet. Without intervention, AIG would declare bankruptcy within hours, potentially triggering a global financial apocalypse that would make Lehman Brothers' collapse the day before look like a mere tremor.

Fed Chairman Ben Bernanke, typically measured and academic, would later confess that of all the decisions during the financial crisis, the AIG bailout made him "angrier than anything else in the recession." Treasury Secretary Henry Paulson, a former Goldman Sachs CEO who understood the interconnected web of global finance, knew that AIG's failure would be catastrophic. The company had written over $440 billion in credit default swaps—essentially insurance on mortgage-backed securities—held by banks worldwide. If AIG defaulted, those banks would face immediate losses that could cascade through the entire financial system.

That evening, the Federal Reserve did something unprecedented in its 95-year history: it extended an $85 billion credit facility to a private insurance company in exchange for a 79.9% equity stake. The government had effectively nationalized one of America's largest corporations. The bailout would eventually swell to $182 billion—the largest corporate rescue in U.S. history.

How did an insurance company—a business model built on careful risk assessment and conservative management—become the epicenter of global financial catastrophe? The answer stretches back nearly a century, from a two-room office in 1919 Shanghai to boardrooms in Manhattan, from the vision of an adventurous entrepreneur named C.V. Starr to the iron-fisted leadership of Maurice "Hank" Greenberg, from selling fire insurance to Chinese merchants to trading complex derivatives that few people understood.

This is the story of American International Group: a company that rose from Asian streets to become the world's largest insurer, controlling over $1 trillion in assets and operating in 130 countries. It's a tale of audacious global expansion, brilliant innovation, spectacular hubris, and ultimately, resurrection. It's about how a company became so large and so interconnected that its failure threatened the entire global economy—the very definition of "too big to fail."

The journey from Shanghai to systemic risk spans three distinct eras: the pioneering Asian empire built by C.V. Starr, the global domination achieved under Hank Greenberg's four-decade reign, and the descent into financial engineering that nearly destroyed capitalism as we know it. Along the way, we'll explore fundamental questions about risk, regulation, leadership, and the price of unbridled ambition. Because understanding AIG's rise and fall isn't just about comprehending one company's history—it's about grasping how modern finance can transform from servant to master, from risk manager to risk creator, from protector to predator.

II. The Shanghai Origins: C.V. Starr's Asian Empire (1919–1945)

Picture Shanghai in December 1919: the "Paris of the East," where Art Deco buildings rose alongside traditional Chinese architecture, where rickshaws competed with automobiles on the Bund, where fortunes were made and lost in the international concessions. Into this cauldron of commerce and chaos stepped Cornelius Vander Starr—C.V. to his friends—a 27-year-old American with no insurance experience, no knowledge of Chinese, and just enough capital to rent two rooms and hire a handful of local staff.

Starr had arrived in Shanghai via Yokohama, where he'd briefly worked as a clerk. But Japan felt too rigid, too established for his ambitions. Shanghai, with its Wild West capitalism and minimal regulation, offered something irresistible: the chance to build something from nothing. On December 19, 1919, he founded American Asiatic Underwriters (AAU) with a simple but radical premise: sell insurance to the Chinese middle class, not just to Western expatriates and foreign firms as other insurers did.

The conventional wisdom among Western businessmen was that Chinese merchants didn't understand or trust insurance. Starr saw it differently. He hired talented Chinese employees—unusual for a Western firm at the time—and had them explain insurance using familiar concepts from Chinese mutual aid societies. He printed policies in Chinese. He paid claims quickly and fairly, building trust in a market where handshake deals still dominated. Within eighteen months, AAU was profitable.

But Starr's real genius lay in recognizing that Shanghai was merely the gateway to a vast Asian opportunity. By 1921, he'd opened offices in Hong Kong and Hankou. By 1926, he'd expanded to the Philippines, founding Philippine American Life Insurance Company—which would become one of the country's largest insurers. Indonesia and Malaysia followed. Each expansion followed a similar playbook: partner with local talent, adapt products to local needs, and reinvest profits locally rather than extracting them to a distant headquarters.

The year 1926 marked a crucial strategic pivot. Starr opened his first U.S. office, incorporating the American International Underwriters Corporation (AIU) to handle the growing business of insuring American companies operating in Asia. This wasn't just geographic expansion—it was the birth of a new business model. While other insurers operated in single countries or regions, Starr was building something unprecedented: a truly international insurance network where risks and knowledge could be shared across borders.

As the 1930s dawned, storm clouds gathered over Starr's Asian empire. Japanese aggression in China threatened his largest market. The 1931 invasion of Manchuria was just the beginning. By 1937, full-scale war had erupted. Japanese bombs fell on Shanghai. Starr watched from his office window as the city burned. Yet rather than retreat, he adapted. He moved into Latin America, opening offices in Cuba and throughout Central America. When Asia generated profits, he invested them in Latin expansion. When Latin America prospered, he strengthened Asian operations. This geographic diversification—revolutionary for its time—would become AIG's defining characteristic.

The decision that saved the company came in 1939. With war engulfing Asia and Europe, Starr made a choice that seemed like retreat but was actually strategic brilliance: he relocated AAU's headquarters from Shanghai to New York City. Not to San Francisco, the traditional American gateway to Asia, but to Manhattan, the center of global finance. Starr wasn't abandoning Asia—he was positioning his company for the post-war world he could already envision.

When Pearl Harbor brought America into the war in 1941, Starr's Asian operations were essentially frozen. Japanese occupation made normal business impossible. Employees were interned or fled. Policies couldn't be serviced. Assets were seized. A lesser entrepreneur might have written off the Asian business entirely. Starr did something extraordinary: he kept meticulous records of every policy, every claim, every employee. He promised that when the war ended, he would return and make good on every obligation.

The war years transformed Starr from entrepreneur to intelligence asset. His knowledge of Asia and network of contacts made him valuable to the Office of Strategic Services (OSS), predecessor to the CIA. He provided intelligence on Japanese positions, helped plan economic warfare, and built relationships that would prove invaluable in the post-war period. This wasn't just patriotic service—it was strategic positioning for the reconstruction that would follow.

When atomic bombs ended the war in August 1945, Starr was ready. Within months, he was back in Asia, reopening offices and honoring pre-war obligations. The gesture built enormous goodwill. But the real opportunity lay in the occupied territories of Japan and Germany. Hundreds of thousands of American servicemen needed insurance—life, auto, property. Local insurers were destroyed or discredited. Starr's companies, with their American credentials and government connections, were perfectly positioned.

By 1948, Starr's various insurance entities were operating across Asia, Europe, and the Americas. The boy from California who'd started with two rooms in Shanghai had built the foundation of what would become the world's largest insurance company. His model—think globally, act locally, diversify geographically, reinvest aggressively—would define AIG for the next six decades. But Starr knew that to truly dominate, his creation needed something he couldn't provide: a killer instinct and operational excellence that would transform his international network into a global empire.

III. The Greenberg Era Begins: Building a Global Empire (1960–1980)

In 1960, a meeting took place that would reshape the insurance industry. C.V. Starr, now 68 and searching for someone to revitalize his companies' North American operations, sat across from Maurice "Hank" Greenberg, a 35-year-old lawyer turned insurance executive. Greenberg had just been passed over for the presidency at Continental Casualty. He was angry, ambitious, and looking for a platform to prove his worth. Starr saw something in this intense, combative man that others might have found off-putting: the ruthlessness necessary to transform a successful international business into a dominant global empire.

Greenberg didn't ease into his role as head of North American holdings—he attacked it. Within months, he'd fired underperforming executives, slashed costs, and instituted performance metrics that were revolutionary for the clubby insurance industry of the early 1960s. Where other insurers relied on relationships and tradition, Greenberg demanded data. He wanted to know the profitability of every policy, every client, every line of business. Executives who couldn't answer his rapid-fire questions didn't last long.

His management style was equal parts strategic brilliance and psychological warfare. Greenberg would call subordinates at 2 AM to discuss quarterly numbers. He'd pit executives against each other, creating internal competition that drove performance but also created a culture of fear. One former executive recalled: "Working for Hank was like being in the Marines. You either thrived under the pressure or you washed out. There was no middle ground."

By 1967, Starr had seen enough. Despite having two sons, he named Greenberg his successor. The transition required restructuring the various Starr companies into a single entity. On June 27, 1967, American International Group, Inc. was incorporated in Delaware—creating the AIG acronym that would become synonymous with both spectacular success and spectacular failure. Starr died in 1968, leaving Greenberg in complete control.

Greenberg's first major strategic decision as CEO revealed his ambition: in 1969, he took AIG public. This was controversial within the company. Many old-timers believed insurance companies should be private, stable, conservative. Greenberg saw it differently. Public markets meant access to capital. Capital meant the ability to acquire competitors, enter new markets, and build scale. The initial public offering valued AIG at $300 million—a number that would seem quaint compared to what was coming.

The 1970s tested Greenberg's leadership in ways that would have broken a lesser executive. The Middle East erupted in conflict—the Yom Kippur War of 1973, the Lebanese Civil War beginning in 1975, the Iranian Revolution in 1979. AIG had significant operations across the region. Rather than retreat, Greenberg innovated. He created political risk insurance, allowing companies to invest in unstable regions knowing AIG would cover losses from expropriation, war, or currency inconvertibility.

This kind of product innovation became Greenberg's signature. When traditional insurers avoided risky coverage, AIG stepped in. Environmental liability insurance for chemical companies? AIG would write it. Directors and officers liability for corporate boards? AIG pioneered it. Kidnap and ransom insurance for executives traveling to dangerous countries? AIG became the market leader. Each product commanded premium prices because alternatives didn't exist.

The key to Greenberg's strategy was information asymmetry. AIG hired specialists—former EPA officials for environmental coverage, ex-FBI agents for kidnap and ransom, retired State Department personnel for political risk. These experts could price risks that competitors couldn't even understand. A chemical company might pay millions in annual premiums for pollution coverage, but AIG's experts knew which companies had good safety records and which were accidents waiting to happen.

By 1975, AIG's net income had surpassed $50 million, growing at a compound rate of 20% annually. But Greenberg wasn't satisfied with organic growth. He embarked on an acquisition spree that would transform AIG from a successful international insurer into a financial conglomerate. The pattern was consistent: identify an undervalued or underperforming insurance company, acquire it with AIG stock or cheap debt, slash costs ruthlessly, integrate the best assets, and discard the rest.

The acquisitions weren't random. Each filled a strategic gap or provided entry into a new market. Need presence in domestic property insurance? Acquire National Union Fire Insurance Company. Want to enter the life insurance business in a major way? Buy multiple smaller life insurers and consolidate them. Each deal was meticulously analyzed, aggressively negotiated, and brutally integrated.

Greenberg's management philosophy during this period crystallized into what he called "All Hands on Deck"—though employees had other names for it. Every Monday morning at 9 AM, senior executives would gather in the boardroom at 70 Pine Street. Greenberg would grill each executive on their division's performance, often from memory, catching any discrepancy or weakness. Executives prepared for these meetings like students for final exams. One mistake could end a career.

Yet for those who survived and thrived, the rewards were substantial. Greenberg created more insurance industry millionaires than any other CEO. He promoted from within, often elevating young, hungry executives over industry veterans. He created a culture that one former executive described as "a band of brothers who'd been through combat together." The loyalty this engendered would sustain AIG through decades of growth—and make Greenberg's eventual departure all the more devastating.

The 1984 New York Stock Exchange listing marked AIG's arrival as a blue-chip company. The boy from Shanghai's two-room office had become a NYSE-listed corporation worth billions. But this was just the beginning. Greenberg's vision extended beyond insurance. He saw AIG as a global financial services empire that happened to be built on an insurance foundation. The seeds of both spectacular growth and eventual catastrophe were being planted.

IV. The Golden Age: Global Domination (1980–2000)

The 1987 acquisition started with a phone call that Hank Greenberg almost didn't take. Howard Sosin, a former Drexel Burnham Lambert trader with a PhD in finance from Wharton, wanted to discuss a joint venture. Sosin and his team had an idea: use AIG's triple-A credit rating to enter the nascent derivatives market. They would trade interest rate swaps, currency swaps, and other complex instruments that banks needed but couldn't always access efficiently. Greenberg, never one to miss an opportunity to deploy AIG's balance sheet profitably, agreed to meet.

The resulting entity, AIG Financial Products Corp. (AIGFP), would generate billions in profits over the next two decades—and ultimately destroy the company. But in 1987, it seemed like genius. AIGFP would operate semi-independently from a London office, far from Greenberg's microscopic oversight. It would use AIG's sterling credit rating to intermediate between parties who needed to hedge various financial risks. The initial capital requirement was minimal—just $250 million—but the profit potential was enormous.

Within three years, AIGFP was generating hundreds of millions in annual profits with fewer than 100 employees. The mathematics were beautiful in their simplicity: borrow at rates available only to AAA-rated entities, lend at slightly higher rates, pocket the spread, and use sophisticated models to ensure risks cancelled out. It was "riskless" profit—or so everyone believed. Sosin and Greenberg eventually clashed over compensation, with Sosin departing in 1993, but AIGFP continued its spectacular growth under new leadership.

While AIGFP represented AIG's push into financial engineering, Greenberg hadn't forgotten the insurance business. The 1990s witnessed an acquisition spree that dwarfed anything from the previous decade. The crown jewel came in 1999: SunAmerica Inc., the retirement savings giant built by Eli Broad. The $18 billion acquisition—AIG's largest to date—gave the company massive scale in the U.S. retirement market. Middle-class Americans who'd never heard of AIG suddenly had their 401(k)s and annuities managed by the company.

The SunAmerica deal demonstrated Greenberg's evolved thinking about financial services. Insurance wasn't just about protecting against losses—it was about accumulating and managing assets. Life insurance policies built cash value. Annuities gathered retirement savings. These products generated "float"—money that AIG could invest for years or decades before paying out claims. With interest rates high in the 1980s and 1990s, this float was enormously profitable.

But the acquisition that perhaps best exemplified AIG's ambitions was International Lease Finance Corporation (ILFC), purchased in 1990 for $1.3 billion. ILFC owned and leased commercial aircraft to airlines worldwide. What did airplane leasing have to do with insurance? In Greenberg's mind, everything. Both businesses involved assessing risk, managing large assets, and generating steady cash flows. Plus, ILFC gave AIG relationships with every major airline—relationships that could be leveraged to sell insurance.

The 2001 acquisition of American General Corporation for $23 billion cemented AIG's position as one of America's largest life insurers. American General brought 12 million customers, massive distribution networks, and decades of actuarial data. The integration was brutal—thousands of employees were terminated, duplicate offices closed, systems consolidated—but the resulting entity dominated multiple insurance markets.

Throughout this expansion, Greenberg maintained an iron grip on operations. Despite AIG's size—revenues exceeding $40 billion by 2000—he insisted on personally approving any transaction over $1 million. He knew the combined ratios of obscure subsidiaries. He could recite premium volumes in remote markets. This micromanagement should have been impossible in such a large organization, but Greenberg made it work through fear, technology, and an army of internal auditors who served as his eyes and ears.

The culture Greenberg built during this period was unique in corporate America. AIG executives didn't just work for the company—they lived it. Sixteen-hour days were standard. Vacations were interrupted by conference calls. Marriages strained under the pressure. But the compensation was extraordinary. Senior executives earned millions. Stock options made hundreds of employees wealthy. The company jet ferried dealmakers around the world. It was intoxicating.

China represented the ultimate validation of AIG's global strategy. In 1992, AIG became the first foreign insurer licensed to operate in Communist China since 1949. Greenberg had been cultivating relationships with Chinese officials since the 1970s, making dozens of trips, hosting delegations, promising technology transfer and expertise. When China finally cracked open its insurance market, AIG was first through the door.

The symbolism was perfect: C.V. Starr had started in Shanghai in 1919, been forced out by revolution and war, and now his company was returning in triumph. Greenberg opened the Shanghai office himself, giving speeches about AIG's historical connections to China. Within a decade, AIG would have operations across China, selling life insurance to the emerging middle class that would eventually number in the hundreds of millions.

By 2000, AIG's market capitalization had reached $180 billion, making it one of the world's most valuable companies. It operated in 130 countries, employed 40,000 people, and generated profits that grew like clockwork every quarter for decades. Greenberg, now 75, showed no signs of slowing down. He'd built one of the great American business empires, a company that touched virtually every aspect of global commerce.

The numbers were staggering: AIG insured oil rigs in the North Sea, satellites in orbit, Hollywood films, Japanese earthquakes, European factories, American homes. It managed hundreds of billions in retirement assets. It leased billions in aircraft. It traded trillions in derivatives. The company that started in two rooms in Shanghai had become too big to fail—though nobody used that phrase yet. The very comprehensiveness of AIG's success contained the seeds of its destruction. But in 2000, as the new millennium dawned, AIG seemed invincible.

V. Seeds of Destruction: Financial Products and Risk (2000–2005)

In a nondescript office building in Wilton, Connecticut, far from AIG's Manhattan headquarters and even further from AIGFP's London trading floor, a small team of mathematicians and traders made a decision in 2002 that would eventually cost American taxpayers $182 billion. They decided to start selling credit default swaps on "super-senior" tranches of collateralized debt obligations (CDOs)—essentially insurance on bundles of mortgages that rating agencies deemed safer than U.S. Treasury bonds.

The logic seemed unassailable. These super-senior tranches were designed to withstand even catastrophic mortgage defaults. They sat at the top of complex structures where losses would hit lower tranches first. For there to be any losses on super-senior tranches, housing prices would need to collapse nationwide—something that had never happened in modern American history. The models, built by PhDs from MIT and Princeton, showed the probability of losses as effectively zero.

Joseph Cassano, who had run AIGFP since 1987, saw credit default swaps as the perfect product. Unlike traditional insurance, they didn't require regulatory approval or reserves. Unlike interest rate swaps, they generated upfront income. Banks desperately wanted them to reduce regulatory capital requirements. And the premiums, while small in percentage terms—often just 0.12% annually—added up when applied to hundreds of billions in notional value.

Between 2002 and 2005, AIGFP wrote credit default swaps on over $440 billion worth of CDOs. The income was intoxicating: hundreds of millions in essentially free money, requiring no initial capital outlay. AIGFP's profits soared, accounting for nearly 17% of AIG's total operating income despite having fewer than 400 employees. Cassano was hailed as a genius, earning $280 million in compensation over eight years.

But there was a cancer growing inside these products that no one at AIG fully understood. The CDOs weren't just packages of prime mortgages—they increasingly contained subprime loans, adjustable-rate mortgages, and even synthetic CDOs (CDOs made up of other CDOs). The rating agencies, paid by the issuers, had every incentive to rate them highly. The models assumed housing prices would always rise and that mortgage defaults would remain uncorrelated. Every assumption was wrong.

Meanwhile, AIG's securities lending division was creating its own disaster. This sleepy division had traditionally lent out AIG's vast portfolio of stocks and bonds to short sellers, earning modest fees. But in the early 2000s, with interest rates at historic lows, the division's managers made a fateful decision: invest the cash collateral from these loans in mortgage-backed securities to earn higher returns.

By 2007, the securities lending division had invested over $75 billion in mortgage-backed securities. Like AIGFP's credit default swaps, these seemed safe—they were highly rated, liquid, and generated attractive yields. Nobody considered what would happen if the mortgage market froze and counterparties demanded their cash back simultaneously. The securities lending program had essentially become a giant, unregulated bank, borrowing short and lending long, without any of a bank's safety nets.

The risk management failures during this period were systematic and profound. AIG had a chief risk officer, but the position lacked real authority. Risk reports went to Cassano at AIGFP, who had every incentive to minimize concerns. The board of directors, populated by Greenberg loyalists and later by members who didn't fully understand the complexities of structured finance, provided no meaningful oversight.

Even more fundamentally, AIG's culture—built on decades of success—bred a dangerous arrogance. The company had weathered Asian financial crises, Latin American debt defaults, and September 11th (which cost AIG $820 million in claims). Executives believed they understood risk better than anyone. When a few internal voices raised concerns about mortgage exposure, they were dismissed as overly conservative or not understanding the sophisticated models.

The compensation structure at AIGFP made matters worse. Bonuses were based on upfront income, not long-term performance. If a credit default swap generated $10 million in premiums over its life, traders booked that entire amount immediately and received bonuses accordingly. If losses emerged years later, the bonuses had already been paid. This created powerful incentives to write as much business as possible without regard for tail risk.

September 11, 2001, should have been a wake-up call about unexpected correlations and black swan events. AIG faced claims from multiple angles: property damage, business interruption, life insurance, workers' compensation, aviation liability. The attacks demonstrated how a single event could trigger losses across seemingly unrelated business lines. But instead of increasing caution, AIG used its successful navigation of 9/11 claims as evidence of its superior risk management.

The London location of AIGFP created additional problems. British regulators focused on local banks, not American insurance subsidiaries. American insurance regulators had no jurisdiction over London operations. The Federal Reserve didn't regulate insurance companies. AIGFP operated in a regulatory blind spot, able to take massive positions without meaningful oversight. This regulatory arbitrage was intentional—Cassano had explicitly stated that London's lighter touch was one reason for basing operations there.

By 2005, cracks were beginning to show. Housing prices in some markets had stopped rising. Adjustable-rate mortgages were resetting at higher rates. Mortgage delinquencies were creeping up. But these were seen as temporary adjustments, not harbingers of catastrophe. AIG's models showed that even a 20% decline in housing prices wouldn't trigger losses on super-senior tranches. The idea of a 30% or 40% decline was literally outside the models' parameters.

Internal emails from this period, later revealed in congressional investigations, show a disturbing pattern. Some risk managers were raising alarms about mortgage exposure. Some traders were questioning the models' assumptions. Some accountants were worried about valuation methods. But these concerns never cohered into action. The profits were too large, the momentum too strong, the culture too confident. AIG had become a victim of its own success, unable to imagine that the strategies that had built an empire could also destroy it.

VI. The Spitzer Affair and Greenberg's Exit (2005)

The call came on a February morning in 2005. Eliot Spitzer, New York's ambitious attorney general who'd already taken down Wall Street analysts and mutual fund companies, wanted to discuss "irregularities" in AIG's accounting. Hank Greenberg, now 79 but still running AIG with an iron fist, initially dismissed it as another Spitzer publicity stunt. He'd survived four decades of challenges. What could a grandstanding prosecutor do to him?

Spitzer's investigation centered on a reinsurance transaction with General Re, a Berkshire Hathaway subsidiary. The deal, executed in 2000, appeared to be a legitimate transfer of risk. But Spitzer alleged it was actually a sham—designed solely to inflate AIG's reserves by $500 million and deceive investors about the company's financial health. The smoking gun was a phone call where Greenberg allegedly ordered the transaction to "shore up" reserves.

The details were complex, involving non-traditional reinsurance structures and side agreements that potentially negated risk transfer. But the implications were simple: if Spitzer was right, AIG and Greenberg had committed accounting fraud. The stock market reacted violently. AIG shares dropped 20% in days. Rating agencies threatened downgrades. The SEC launched its own investigation.

Inside AIG, panic set in. The board of directors, previously docile under Greenberg's domination, suddenly grew spines. Led by Frank Zarb, they hired independent counsel to investigate. They discovered not just the General Re transaction but a pattern of aggressive accounting that pushed legal boundaries. Finite reinsurance deals that weren't quite finite. Reserve adjustments that always seemed to smooth earnings. Tax strategies that regulators might view as evasion.

Greenberg fought back with characteristic ferocity. He hired David Boies, the super-lawyer who'd represented Al Gore in Bush v. Gore. He went on television declaring innocence. He rallied loyal employees, many of whom owed their wealth to him. He portrayed Spitzer as an ambitious politician destroying an American business icon for personal gain. For a moment, it seemed like Greenberg might survive.

But on March 14, 2005, everything changed. PricewaterhouseCoopers, AIG's auditor, informed the board that Greenberg's presence was hampering their investigation. Without full cooperation, they couldn't certify AIG's financial statements. For a public company, this was a death sentence. The board delivered an ultimatum: resign or be fired.

On March 28, 2005, Maurice "Hank" Greenberg resigned as CEO of AIG after 38 years at the helm. He maintained his innocence, claiming he was victim of a witch hunt. But he also understood the reality: fighting would destroy the company he'd built. His handpicked successor, Martin Sullivan, took over—a British insurance executive who'd risen through AIG's ranks but lacked Greenberg's strategic vision and commanding presence.

The aftermath was chaotic. AIG had to restate five years of financial results, reducing net income by $3.9 billion. The SEC fined the company $1.6 billion. Dozens of executives were investigated. The company's reputation, carefully built over decades, was shattered. But the real damage was internal. Greenberg hadn't just run AIG—he was AIG. His departure created a power vacuum that would prove catastrophic.

Sullivan faced an impossible situation. He inherited a company with $850 billion in assets, operations in 130 countries, and dozens of business lines he didn't fully understand. AIGFP's derivatives portfolio, which Greenberg had personally monitored, was now essentially unsupervised. The securities lending division's mortgage bets continued growing. Risk management, always secondary to profit generation under Greenberg, became even weaker without his oversight.

The cultural impact was equally devastating. Greenberg's "band of brothers" fractured. Some executives left for competitors. Others, sensing opportunity in chaos, pursued aggressive strategies to boost their divisions' profits. The Monday morning interrogations that had terrorized but also informed executives ended. Information flow, which Greenberg had forced through fear, dried up. AIG became a collection of feudal kingdoms rather than a unified empire.

In 2017, twelve years after his resignation, Greenberg finally settled with the New York Attorney General's office. He admitted to fraudulent conduct and paid $9 million personally. For a man worth hundreds of millions, the fine was insignificant. But the admission was devastating. The executive who'd built one of America's great companies had to acknowledge breaking the law to do it.

The timing of Greenberg's departure was tragically perfect. He left just as the mortgage market was peaking, just as AIGFP's credit default swaps were becoming toxic, just as the securities lending division's bets were growing most dangerous. Had he remained, would his paranoid oversight have detected the brewing catastrophe? Would his relationships with regulators have bought more time? Would his sheer force of personality have found a solution? These questions haunt AIG to this day.

Sullivan tried to maintain normalcy, declaring that AIG remained strong, that nothing fundamental had changed. But everything had changed. The emperor was gone, and the empire was crumbling. Within three years, AIG would need the largest government bailout in history. The company Greenberg spent four decades building would be destroyed in months. The seeds of destruction had been planted during his tenure, but they flowered in his absence.

VII. The Collapse: Financial Crisis and Bailout (2007–2008)

The first margin call arrived on July 27, 2007, from Goldman Sachs. It was modest—just $1.8 billion in collateral on credit default swaps that AIGFP had written. The mortgage securities these swaps insured had declined slightly in value, triggering contractual provisions requiring AIG to post cash. Joseph Cassano, still running AIGFP from London, was furious. The securities hadn't defaulted. No actual losses had occurred. This was just Goldman being aggressive. AIG reluctantly posted the collateral, confident the demand was temporary.

But Goldman's call was like blood in the water attracting sharks. Soon, every counterparty—Merrill Lynch, Deutsche Bank, UBS, Société Générale—wanted collateral. The demands accelerated through 2007 and into 2008. By March 2008, AIG had posted $30 billion in collateral on swaps that had generated less than $500 million in premiums. The mathematics of catastrophe were becoming clear: AIGFP had sold insurance too cheaply on risks it didn't understand.

Inside AIG's Connecticut financial products office, traders watched in horror as their models disintegrated. The mortgage securities they'd deemed "money good" were trading at 60, 50, 40 cents on the dollar. The super-senior CDO tranches, supposedly safer than Treasury bonds, were being marked down 20%, 30%, even 50%. Every basis point decline triggered more collateral calls. The spiral was accelerating.

The securities lending division faced its own crisis. As mortgage markets froze, the securities it had purchased with borrowed cash became illiquid. When counterparties demanded their money back, AIG couldn't sell the securities without massive losses. By summer 2008, the securities lending program had unrealized losses exceeding $20 billion. The division designed to earn modest fees on stock loans had become a ticking time bomb.

Martin Sullivan, overwhelmed and out of his depth, was replaced as CEO in June 2008 by Robert Willumstad, an AIG board member and former Citigroup president. Willumstad immediately grasped the severity of the situation. He hired JPMorgan and Blackstone to explore options: asset sales, capital raises, even a breakup of the company. But time was running out faster than anyone realized.

September 2008 began with Hurricane Ike devastating Texas, generating billions in insurance claims that strained AIG's liquidity. Then, on September 7, the government seized Fannie Mae and Freddie Mac. On September 14, Bank of America acquired Merrill Lynch in a shotgun wedding. On September 15, Lehman Brothers filed for bankruptcy—the largest corporate bankruptcy in U.S. history.

Lehman's collapse triggered a global financial panic. Credit markets froze. Nobody would lend to anybody. For AIG, this was catastrophic. The company needed to roll over billions in commercial paper daily just to fund operations. Suddenly, that market disappeared. Rating agencies, spooked by Lehman, downgraded AIG's credit rating on September 15. The downgrades triggered $32 billion in additional collateral calls—cash AIG didn't have.

Inside the Federal Reserve Bank of New York, officials worked through the night of September 15-16. Fed President Tim Geithner, Treasury Secretary Hank Paulson, and Fed Chairman Ben Bernanke faced an impossible choice. Letting AIG fail would likely trigger a complete collapse of the global financial system. AIG had written $2.7 trillion in derivatives contracts. Its failure would cause immediate losses at every major bank. The psychological impact, coming one day after Lehman, could cause a run on the entire financial system.

But saving AIG meant crossing a line the Fed had never crossed: lending to an insurance company. It meant taxpayers bailing out a company that had made spectacularly bad bets. It meant moral hazard on an unprecedented scale. Bernanke later said the decision made him "angrier than anything else in the recession." But the alternative—potential economic collapse—was worse.

At 9 PM on September 16, 2008, the Federal Reserve announced an $85 billion secured credit facility for AIG. The terms were punitive: 14% interest rate, warrants for 79.9% of AIG's equity, and effective government control of the company. It was nationalization in all but name. The U.S. government now owned what had been one of America's most valuable corporations.

The bailout triggered public outrage that would define politics for years. How could the government bail out wealthy Wall Street executives while ordinary Americans lost homes? Why save AIG but not Lehman? The Tea Party movement, Occupy Wall Street, and the broader populist revolution in American politics all trace roots to this moment when capitalism's winners were protected from capitalism's consequences.

The initial $85 billion proved insufficient. In November 2008, the government restructured the bailout, providing another $40 billion and creating vehicles to buy toxic assets from AIG. In March 2009, another restructuring added $30 billion more. The total government commitment eventually reached $182 billion—the largest corporate rescue in history.

Then came the moment that crystallized public fury: in March 2009, news broke that AIGFP—the division that had destroyed the company—was paying $165 million in retention bonuses to executives. The same traders who'd written catastrophic credit default swaps were receiving million-dollar bonuses funded by taxpayers. Congress held emergency hearings. Death threats poured in. AIG executives needed bodyguards. The bonuses were eventually reduced, but the reputational damage was permanent.

The numbers from 2008 tell the story of corporate catastrophe: AIG lost $99.2 billion, the largest annual loss in corporate history. The stock price fell from $50 to $1.25, destroying $180 billion in market value. Over 100,000 employees lost their jobs. Millions of policyholders worried their insurance was worthless. Retirees saw their annuities threatened. An empire built over 90 years nearly collapsed in 90 days.

But perhaps the most profound loss was philosophical. AIG's collapse shattered the myth of sophisticated risk management. The company that had pioneered modern actuarial science, that had priced risks others couldn't understand, had failed to grasp its own exposure. The smartest people in finance, using the most advanced models, had been completely, catastrophically wrong. If AIG could fail, what company was truly safe?

VIII. The Unwinding: Asset Sales and Restructuring (2009–2012)

Edward Liddy had been enjoying retirement, serving on corporate boards and playing golf, when Hank Paulson called in September 2008. The government needed someone to run AIG—someone with insurance experience, unimpeachable credibility, and no connection to the disaster. Liddy, former CEO of Allstate, agreed to take the job for $1 annual salary. He thought it would take six months. It would consume four years of his life.

Liddy inherited a company that existed more on spreadsheets than in reality. AIG comprised over 4,000 legal entities across 130 countries. Many subsidiaries had their own subsidiaries, creating corporate structures so complex that no single person understood them all. The immediate priority was survival: meeting collateral calls, maintaining insurance operations, and preventing further rating downgrades. But the ultimate goal was repaying taxpayers—all $182 billion.

The asset sale program began immediately, but market conditions were brutal. In normal times, AIG's crown jewels—its Asian life insurance operations, its aircraft leasing business, its domestic insurance units—would have commanded premium prices. But in 2009, credit markets were frozen, buyers were scarce, and everyone knew AIG was desperate. It was the worst possible time to sell anything.

The first major transaction came in November 2009: the sale of Hartford Steam Boiler to Munich Re for $742 million. Hartford, which inspected and insured industrial equipment, was profitable and stable—exactly the kind of business AIG needed to keep. But the government demanded speed over value. Every month AIG remained in government hands increased political pressure and reputational damage.

The sale of American Life Insurance Company (ALICO) to MetLife for $15.5 billion in 2010 was more significant. ALICO operated in 50 countries, had 20 million customers, and generated billions in annual revenue. It was C.V. Starr's original international platform, the foundation of AIG's global empire. Selling it was like selling the company's soul. But ALICO's size and international scope made it attractive to MetLife, one of the few buyers with both appetite and capital.

The most creative solution involved American International Assurance (AIA), AIG's massive Asian life insurance operation. Rather than sell to a competitor at a discount, AIG executed a partial IPO in Hong Kong in October 2010, raising $20.5 billion. The offering was 14 times oversubscribed, with demand from both institutional investors betting on Asian growth and retail investors who'd been AIA customers for generations. AIG retained a 33% stake, allowing participation in future upside while raising immediate cash.

Each sale required excruciating negotiations. Buyers knew AIG's desperation and demanded warranties, indemnities, and price adjustments. Regulatory approvals took months. Countries worried about foreign ownership of domestic insurers. Employees feared job losses. Customers worried about policy coverage. Every transaction generated headlines reminding the public of AIG's failure.

The human cost was staggering. Each divested business meant thousands of employees either losing jobs or transferring to new companies. Career AIG executives who'd spent decades building businesses watched them sold for fractions of perceived value. The company's paternalistic culture, where employees expected lifetime employment, shattered. Suicide rates among former employees spiked. Divorces multiplied. The psychological trauma rivaled the financial destruction.

Meanwhile, the core insurance operations that remained needed complete restructuring. Expenses were slashed by $3 billion annually. Marginal business lines were discontinued. The workforce was reduced from 116,000 to 60,000. Historic offices were closed. The corporate jet fleet was sold. Executive compensation was capped by government pay czar Kenneth Feinberg, causing talent to flee to competitors. It was corporate chemotherapy—poisoning the organization to save it.

The unwinding of AIGFP was particularly complex. The division's derivatives portfolio couldn't simply be sold—most contracts ran for decades and required AIG's credit support. Instead, AIGFP had to be wound down transaction by transaction, hedging existing positions while preventing new losses. The unit that had once employed 400 people making millions was reduced to a skeleton crew managing a legacy portfolio in run-off.

By late 2011, AIG had raised over $50 billion from asset sales and was generating profits from remaining operations. The government began selling its stake through public offerings. Each sale was meticulously orchestrated to avoid depressing the stock price while maximizing taxpayer recovery. The Fed sold the last of its preferred shares in January 2011. The Treasury continued selling common stock throughout 2012.

The final Treasury sale came on December 11, 2012. The government sold its remaining 234 million shares for $7.6 billion, ending one of the most controversial chapters in American financial history. When all transactions were tallied—loan repayments, interest, dividends, and stock sales—taxpayers had recovered $205 billion on their $182 billion investment, a profit of $22.7 billion.

The profit was both vindication and complication. Critics argued it justified the bailout, proving the government made smart investments. Others countered that moral hazard remained—that bailing out AIG encouraged future recklessness. The profit also ignored opportunity cost and systemic risk. What could that $182 billion have accomplished if invested elsewhere? What long-term damage did "too big to fail" create?

Robert Benmosche, who replaced Liddy as CEO in 2009, deserves credit for the successful unwinding. A colorful, controversial figure who worked from his Croatian vineyard and compared AIG's treatment to lynch mobs, Benmosche restored employee morale and fought for better prices on asset sales. His death from cancer in 2015 marked the end of AIG's crisis era leadership.

In 2017, the Financial Stability Oversight Council removed AIG's designation as a "systemically important financial institution"—effectively declaring it no longer too big to fail. The company that had threatened global financial collapse was now just another insurer. The unwinding was complete. AIG had been saved, dismembered, and rebuilt. Whether it had been redeemed remained an open question.

IX. The Modern Era: Reinvention and Recovery (2013–Present)

Peter Zaffino didn't follow the traditional path to insurance industry leadership. He'd spent his career at Marsh & McLennan, the world's largest insurance broker, watching AIG from the outside—first as a dominant competitor, then as a cautionary tale, finally as a diminished giant trying to find its way. When he joined AIG in 2017 as chief operating officer, then became CEO in 2021, he brought an outsider's perspective to an insular culture.

Zaffino inherited a company that had survived but hadn't thrived. Post-crisis AIG was profitable but uninspiring, generating returns below its cost of capital. The stock price languished. Talented executives left for competitors or startups. The name AIG still triggered negative reactions from regulators, rating agencies, and the public. Recovery wasn't enough—AIG needed reinvention.

The strategy Zaffino articulated was deceptively simple: AIG would be a focused commercial property-casualty insurer with complementary life and retirement operations. No more financial engineering. No more derivative trading. No more ventures beyond core competencies. The company that had once done everything would now do a few things exceptionally well.

The transformation began with technology. AIG had operated on systems dating to the 1980s, with different platforms for different countries and business lines. Policy data was trapped in silos. Claims processing was manual. Underwriting relied on intuition rather than analytics. For a company that had pioneered data-driven risk assessment under Greenberg, the technological decay was embarrassing.

AIG invested billions in digital transformation, building new underwriting platforms, claims systems, and data analytics capabilities. Artificial intelligence began screening claims for fraud. Machine learning models improved risk pricing. Digital interfaces allowed customers to purchase policies and file claims online. The company that had been synonymous with bureaucracy was becoming agile.

The cultural transformation was equally dramatic. The fear-based management of the Greenberg era and crisis-mode mentality of the bailout years gave way to something new. Zaffino emphasized collaboration over competition, transparency over secrecy, innovation over tradition. Town halls replaced intimidation sessions. Employee resource groups flourished. Diversity initiatives weren't just rhetoric—by 2023, 40% of senior executives were women or minorities.

The business portfolio was systematically simplified. In 2021, AIG spun off its life and retirement business as Corebridge Financial, raising $1.7 billion while retaining majority ownership. The separation allowed each business to focus on its distinct market and regulatory requirements. Corebridge could pursue growth in retirement products without dragging down AIG's property-casualty operations. AIG could improve its commercial insurance margins without worrying about long-term annuity obligations.

The numbers showed steady improvement. Combined ratios—the key measure of insurance profitability—improved from 110% in 2017 to 95% by 2023. Return on equity rose from negative to low double digits. The stock price, which had languished around $50 for years, climbed above $70. Rating agencies upgraded AIG's credit rating. The company that couldn't borrow at any price in 2008 was again investment grade.

Risk management, the catastrophic failure that had nearly destroyed AIG, became an obsession. The company hired chief risk officers with real authority, built sophisticated monitoring systems, and created a culture where raising concerns was rewarded rather than punished. Every major transaction required multiple risk assessments. Compensation was tied to long-term performance rather than short-term profits. The cowboys who'd bet the company on mortgage securities were replaced by cautious technocrats.

The client base reflected AIG's new focus. The company served 87% of the Fortune Global 500 and 83% of the Forbes 2000. These weren't small businesses buying basic coverage—they were multinational corporations needing sophisticated solutions for complex risks. Cyber insurance for technology companies. Political risk coverage for emerging market investments. Environmental liability for energy companies. The specialized products Greenberg had pioneered remained AIG's competitive advantage.

Geographic concentration also shifted. While AIG maintained international operations, the focus moved from expansion to optimization. Unprofitable countries were exited. Marginal business lines were discontinued. The company that had once bragged about operating in 130 countries now emphasized profitability over presence. Quality replaced quantity as the metric of success.

The workforce transformation was remarkable. From 116,000 employees at its peak, AIG operated with just 25,200 by 2023. But these weren't the same jobs—modern AIG employed more data scientists, software engineers, and risk analysts than traditional insurance underwriters. The company recruited from technology firms and consulting companies rather than just insurance competitors. Average employee age dropped by a decade.

Yet challenges remained substantial. The AIG brand, while improved, still carried stigma. Talented recruits often needed convincing to join a company associated with financial crisis. Customers paid "AIG discounts" compared to competitors with cleaner histories. Regulators scrutinized AIG more carefully than peers. The bailout's shadow, while fading, hadn't disappeared.

Competition had also intensified during AIG's decade of distraction. While AIG was being rescued and restructured, competitors had expanded, consolidated, and innovated. New entrants, particularly technology-enabled "insurtech" companies, threatened traditional business models. Climate change created unprecedented catastrophe exposure. Social inflation drove claim costs higher. The insurance industry AIG rejoined was fundamentally different from the one it had dominated.

X. Playbook: Lessons from the Rise and Fall

The story of AIG offers a masterclass in both empire building and empire destruction. The strategies that created one of the world's most powerful financial institutions also contained the seeds of its near-annihilation. Understanding these paradoxes is essential for investors, executives, and regulators seeking to avoid future catastrophes.

The Genius and Danger of Regulatory Arbitrage

C.V. Starr built AIG by operating where regulations were weakest—1920s Shanghai, post-war occupied territories, emerging markets with minimal oversight. Greenberg expanded this strategy, using Bermuda subsidiaries for reinsurance, London offices for derivatives trading, and complex corporate structures to minimize taxes and regulatory scrutiny. AIGFP operated in a regulatory blind spot, neither fully regulated as a bank nor an insurer.

This arbitrage generated enormous profits but created systemic vulnerabilities. When crisis struck, no single regulator had complete oversight or authority. The Federal Reserve had to intervene despite having no experience regulating insurance companies. The lesson: regulatory arbitrage might boost short-term profits, but it creates long-term instability that can destroy companies and threaten entire systems.

Leadership Succession and Institutional Knowledge

Greenberg's 38-year tenure as CEO created both strength and weakness. His encyclopedic knowledge of AIG's operations, photographic memory for numbers, and extensive relationships were irreplaceable assets. But his domination prevented development of successor talent. When he departed suddenly in 2005, the institutional knowledge went with him.

Martin Sullivan and Robert Willumstad, his immediate successors, didn't understand AIGFP's derivatives portfolio or the securities lending program's risks. They relied on subordinates who had incentives to minimize problems. The lesson: great leaders must build institutions that can survive their departure. Concentrated knowledge is concentrated risk.

Financial Engineering Versus Core Business

AIG's destruction came not from insurance operations but from financial products that had nothing to do with traditional risk assessment. Credit default swaps were insurance in name only—they required no reserves, faced no regulation, and were priced using models rather than actuarial experience. The securities lending program turned a conservative business into a shadow bank.

The core insurance operations remained profitable throughout the crisis. Even in 2008, while losing $99 billion overall, AIG's traditional insurance units generated positive cash flow. The lesson: financial innovation that strays from core competencies often destroys more value than it creates. Complexity is not sophistication.

The Moral Hazard of "Too Big to Fail"

AIG's bailout created precedents that still shape financial markets. Creditors who should have suffered losses were made whole. Executives who made catastrophic decisions kept bonuses. Shareholders who should have been wiped out eventually recovered value. The government's $22.7 billion profit validated the rescue but obscured its costs.

The moral hazard persists. Large financial institutions know that reaching sufficient size and interconnectedness provides implicit government protection. Risk-taking is subsidized by taxpayers who bear downside while private actors capture upside. The lesson: "too big to fail" is too big to exist. Size itself becomes a source of systemic risk.

Culture and Risk Management

Greenberg built a culture of fear that paradoxically both managed and created risk. Executives were terrified of reporting bad news, so problems festered until they became catastrophes. The same culture that drove exceptional performance prevented honest assessment of dangers. When Greenberg left, the culture collapsed but wasn't replaced with effective risk management.

Modern AIG has attempted to build a culture balancing performance with prudence, but cultural transformation takes generations. The aggressive, risk-taking DNA that made AIG great also made it dangerous. The lesson: culture is destiny in financial services. Risk management must be embedded in culture, not imposed through systems.

Global Expansion Strategies

AIG's international expansion succeeded through localization—hiring local talent, adapting products to local needs, and reinvesting profits locally. This differed from competitors who exported American products globally. But international expansion also created complexity that became unmanageable. By 2008, AIG comprised 4,000 legal entities that no single person understood.

The unwinding revealed how much value had been destroyed by complexity. Simplified, focused AIG generated better returns than the sprawling empire. The lesson: global expansion must balance growth with manageability. Scale without control is vulnerability.

Understanding Actual Risk Exposure

AIG's fundamental failure was misunderstanding its own risks. The company that had pioneered modern actuarial science couldn't grasp that housing prices could decline nationally. The firm that priced political risk in emerging markets couldn't see systemic risk in American mortgages. Models replaced judgment. Mathematics replaced experience.

The correlations that destroyed AIG were hiding in plain sight. mortgage securities, credit default swaps, and securities lending were all exposed to the same underlying risk: U.S. housing prices. But organizational silos prevented integrated risk assessment. The lesson: risk management requires humility, skepticism, and constant questioning of assumptions.

When Innovation Becomes Destruction

Every financial innovation that nearly destroyed AIG began with legitimate business purpose. Credit default swaps helped banks manage regulatory capital. Securities lending generated income from idle assets. Complex reinsurance structures improved capital efficiency. But innovation evolved into speculation, prudence morphed into recklessness, and hedging became betting.

The progression from innovation to destruction followed a predictable pattern: initial success, competitive pressure to grow, model-driven expansion, ignored warning signs, and catastrophic failure. The lesson: financial innovation requires constant vigilance against mission creep. Today's hedge is tomorrow's speculation.

XI. Bull & Bear Case: AIG Today

The Bull Case: A Focused Giant Ready to Dominate

Today's AIG is fundamentally different from its pre-crisis incarnation—and that's exactly why bulls are optimistic. The company has shed the complexity that nearly destroyed it, focusing on what it does best: commercial property and casualty insurance for large corporations. This isn't the AIG that bet billions on mortgage securities; it's a disciplined underwriter with genuine expertise in complex risks.

The numbers support optimism. AIG's combined ratio has improved from 110% to 95%, meaning the company now makes underwriting profits rather than relying solely on investment income. Return on equity has reached sustainable double digits. The balance sheet is clean, with minimal debt and strong capital ratios. Rating agencies have upgraded their assessments. The stock trades at a discount to book value, suggesting significant upside potential.

The competitive position remains formidable despite the crisis. AIG still serves 87% of the Fortune Global 500—relationships built over decades that competitors can't easily replicate. These aren't price-sensitive customers buying commodity coverage; they're sophisticated corporations needing specialized solutions. Cyber insurance for technology giants. Political risk coverage for emerging market investments. Environmental liability for energy companies. Few competitors can match AIG's expertise in these complex areas.

Technology investments are beginning to pay dividends. Modern underwriting platforms allow better risk selection and pricing. Digital distribution reduces costs and improves customer experience. Data analytics identify profitable niches competitors miss. The company that was technologically backward has become genuinely innovative. This isn't cosmetic digital transformation—it's fundamental business improvement.

Leadership under Peter Zaffino represents generational change. Unlike predecessors who were AIG lifers, Zaffino brings outside perspective and broker relationships. He understands what customers want because he spent decades representing them. The cultural transformation from fear to collaboration has improved employee morale and retention. The company that couldn't attract talent now recruits successfully from technology firms and competitors.

The macro environment favors commercial insurers. Rising interest rates improve investment income—crucial for an industry that invests premiums until claims are paid. Inflation drives premium growth as coverage amounts increase. Corporate investment in technology, infrastructure, and international expansion creates demand for specialized insurance. Climate change, while creating catastrophe exposure, also drives demand for coverage and allows repricing of risk.

The Corebridge Financial spinoff unlocked value by separating distinct businesses with different capital requirements, growth profiles, and regulatory oversight. AIG retains majority ownership, participating in upside while improving its own metrics. The life and retirement business can pursue strategies appropriate for long-term liabilities without constraining property-casualty operations. Both entities are worth more separately than combined.

The Bear Case: Permanent Impairment in a Difficult Industry

Bears see AIG as a permanently impaired franchise in a structurally challenged industry. The company may have survived its near-death experience, but it emerged diminished, struggling to compete in markets it once dominated. The improvements touted by management are more recovery from crisis lows than genuine competitive advantage.

The reputational damage from 2008 persists despite management's claims otherwise. "AIG" remains synonymous with financial crisis in public consciousness. Corporate customers remember the uncertainty when AIG nearly failed. Talented employees have better options at firms without baggage. Regulators scrutinize AIG more carefully than competitors. This "AIG discount" affects everything from customer acquisition to capital costs.

The competitive landscape has fundamentally shifted during AIG's lost decade. While AIG was being rescued and restructured, competitors expanded and consolidated. Chubb, Travelers, and Zurich captured market share AIG surrendered. New entrants, particularly technology-enabled "insurtech" companies, threaten traditional business models with lower costs and better customer experience. AIG is fighting to reclaim position in markets that have moved on.

Financial metrics, while improved, remain mediocre by industry standards. Return on equity in the low double digits barely exceeds cost of capital. Combined ratios in the mid-90s are acceptable but not exceptional. Premium growth lags competitors. The company generates profits, but not the exceptional returns that justify its complexity and history. Mediocrity doesn't merit premium valuations.

Climate change poses existential threats that dwarf previous challenges. Increased frequency and severity of natural catastrophes make underwriting profits harder to achieve. Secondary perils—floods, wildfires, convective storms—create losses traditional models don't capture. Litigation over climate risks could generate liability similar to asbestos. The industry that exists to manage risk faces risks it can't fully understand or price.

The technology transformation, while necessary, is expensive and uncertain. Billions invested in digital systems must compete with insurtech startups born digital. Legacy systems can't simply be replaced—they must be maintained while new systems are built. Data trapped in silos resists integration. Cultural resistance from employees threatened by automation slows implementation. Technology might be necessary for survival but doesn't guarantee success.

Social inflation—the trend of rising jury awards and litigation costs—threatens profitability in key lines like directors and officers liability, professional liability, and general liability. Nuclear verdicts exceeding $10 million have become common. Litigation funding enables lawsuits that previously wouldn't have been pursued. Legal system abuse in certain jurisdictions makes some risks essentially uninsurable. AIG's concentration in complex commercial risks gives it disproportionate exposure to these trends.

Management's strategy of focus and simplification, while prudent, also limits growth opportunities. The company that once entered every market now retreats from many. The sprawling empire that provided diversification has been replaced by concentration risk. Innovation that drove past growth has been replaced by cautious incrementalism. AIG might be safer, but safety doesn't create value in competitive markets.

The burden of the past can't be entirely escaped. Legal settlements from crisis-era actions continue. Regulatory oversight remains heightened. Political risk exists—another financial crisis could trigger retroactive punishment for 2008 beneficiaries. The company that was "too big to fail" remains vulnerable to populist backlash. History casts a shadow that time alone can't eliminate.

XII. Reflections & What-Ifs

What if Hank Greenberg had never been forced out in 2005? This question haunts every analysis of AIG's collapse. Greenberg, despite his flaws, understood the company's complexity in ways his successors didn't. He personally reviewed AIGFP's positions, questioned assumptions, and had relationships with counterparties that might have enabled better negotiations. His paranoid management style, while toxic in many ways, might have detected brewing problems earlier.

But this counterfactual assumes Greenberg would have recognized dangers he'd helped create. The credit default swap business flourished under his watch. The securities lending program's risks accumulated during his tenure. The culture that prevented bad news from surfacing was his creation. Perhaps Greenberg's presence would have only delayed, not prevented, catastrophe. Or perhaps his political connections and force of personality could have secured private rescue without taxpayer involvement.

Could the financial crisis have been prevented if AIG hadn't existed, or hadn't entered derivatives markets? Probably not. The housing bubble had multiple causes—loose monetary policy, regulatory failure, misaligned incentives, and basic human greed. If AIG hadn't written credit default swaps, other firms would have. The demand for mortgage risk transfer was insatiable. AIG's participation amplified the crisis but didn't cause it.

Yet AIG's specific failure pattern created unique systemic risks. Unlike investment banks that could fail relatively cleanly, AIG's insurance subsidiaries were regulated by fifty state insurance commissioners with different priorities and powers. Its derivatives were governed by International Swaps and Derivatives Association agreements requiring immediate settlement. Its global presence meant failure would cascade through multiple financial systems simultaneously. AIG wasn't just too big to fail—it was too complex to fail.

The role of rating agencies deserves special scrutiny. Moody's, S&P, and Fitch maintained AIG's AA rating until days before collapse. Their models, like AIG's, couldn't conceive of nationwide housing price declines. They treated mortgage securities and credit default swaps as fundamentally different from traditional insurance, not requiring the same reserves or scrutiny. Their failure was both cause and symptom of broader analytical blindness.

Regulatory failure was comprehensive and bipartisan. The Office of Thrift Supervision, AIG's consolidated supervisor, was laughably understaffed and underqualified. State insurance regulators focused on their local subsidiaries, missing group-wide risks. The Fed didn't regulate insurance companies. The SEC had limited authority over derivatives. This regulatory balkanization was partly accidental, partly deliberate—AIG had structured itself to minimize oversight.

What if the government had let AIG fail? This remains the most contentious question. Free market advocates argue bailouts create moral hazard that ensures future crises. They contend creative destruction would have purged bad actors and practices, creating a healthier system. The $182 billion could have helped homeowners directly rather than filtering through financial institutions.

But Federal Reserve officials who lived through those September days paint an apocalyptic picture of what AIG's bankruptcy would have triggered. Every major bank would have faced immediate losses on credit default swaps. Money market funds holding AIG commercial paper would have "broken the buck," triggering runs. Insurance policyholders worldwide would have panicked, demanding withdrawals that would cascade through the industry. International commerce would have frozen as trade credit disappeared.

The true cost of "too big to fail" extends beyond the financial. It corrodes capitalism's moral foundation—the principle that profit and loss are private. It creates a class of institutions effectively backstopped by taxpayers. It encourages size for its own sake, as companies seek the implicit government guarantee that comes with systemic importance. It politicizes finance, making every major financial firm a potential political issue.

Modern parallels are uncomfortable but important. Today's financial system has new vulnerabilities—leveraged loans, private credit, cryptocurrency, and complex ETF structures. Risk has migrated from banks to shadow banking, from regulated to unregulated sectors. Financial innovation continues racing ahead of regulatory understanding. The next crisis likely won't look like 2008, but the underlying patterns—excessive leverage, model failure, and interconnected risk—persist.

The transformation of insurance from risk management to risk creation warrants reflection. Insurance should make the economy more stable by spreading risks across time and parties. But financial innovation transformed insurers into risk manufacturers, creating exposures that didn't previously exist. Credit default swaps didn't transfer risk—they multiplied it. The securities lending program didn't reduce risk—it concentrated it. When risk managers become risk creators, systemic instability follows.

Personal responsibility remains unsettled. Executives who made fortunes creating risks that destroyed AIG largely kept their wealth. Joseph Cassano, who ran AIGFP, retained hundreds of millions despite overseeing catastrophic losses. Board members who failed in oversight faced minimal consequences. Regulators who missed obvious problems advanced in their careers. The individuals who caused the crisis prospered while institutions and taxpayers bore costs.

The question of whether AIG has truly learned its lessons remains open. Current management says the right things about risk management and cultural change. But institutional memory fades. New employees don't remember the crisis. Competitive pressures encourage risk-taking. Quarterly earnings demands conflict with long-term prudence. The cycles that created one crisis continue, awaiting the right combination of circumstances to create another.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube